Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - InPoint Commercial Real Estate Income, Inc. | ck0001690012-ex322_7.htm |

| EX-32.1 - EX-32.1 - InPoint Commercial Real Estate Income, Inc. | ck0001690012-ex321_8.htm |

| EX-31.2 - EX-31.2 - InPoint Commercial Real Estate Income, Inc. | ck0001690012-ex312_6.htm |

| EX-31.1 - EX-31.1 - InPoint Commercial Real Estate Income, Inc. | ck0001690012-ex311_9.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2020

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-55782

INPOINT COMMERCIAL REAL ESTATE INCOME, INC.

(Exact name of registrant as specified in its charter)

|

Maryland |

32-0506267 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

2901 Butterfield Road Oak Brook, Illinois |

60523 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (800) 826-8228

Securities registered pursuant to Section 12(b) of the Act:

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

|

|

|

|

|

|

Non-accelerated filer |

☒ |

Smaller Reporting Company |

☒ |

|

|

|

|

|

|

Emerging Growth Company |

☒ |

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of May 10, 2020, the Registrant had the following shares outstanding: 10,151,787 shares of Class P common stock, 397,251 shares of Class T common stock, 378,302 shares of Class I common stock, 653,566 shares of Class A common stock, 50,081 shares of Class D common stock and no shares of Class S common stock.

|

PART I FINANCIAL INFORMATION |

|

||

|

Item 1. |

Financial Statements |

|

|

|

|

|

|

|

|

|

Consolidated Balance Sheets as of March 31, 2020 (unaudited) and December 31, 2019 |

2 |

|

|

|

|

|

|

|

|

Unaudited Consolidated Statements of Operations for the three-months ended March 31, 2020 and 2019 |

3 |

|

|

|

|

|

|

|

|

4 |

||

|

|

|

|

|

|

|

Unaudited Consolidated Statements of Cash Flows for the three-months ended March 31, 2020 and 2019 |

5 |

|

|

|

|

|

|

|

|

6 |

||

|

|

|

|

|

|

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

18 |

|

|

|

|

|

|

|

Item 3. |

32 |

||

|

|

|

|

|

|

Item 4. |

33 |

||

|

|

|

|

|

|

PART II OTHER INFORMATION |

|

||

|

|

|

|

|

|

Item 1. |

33 |

||

|

|

|

|

|

|

Item 1A. |

33 |

||

|

|

|

|

|

|

Item 2. |

35 |

||

|

|

|

|

|

|

Item 3. |

36 |

||

|

|

|

|

|

|

Item 4. |

36 |

||

|

|

|

|

|

|

Item 5. |

36 |

||

|

|

|

|

|

|

Item 6. |

37 |

||

|

|

|

||

|

38 |

|||

1

INPOINT COMMERCIAL REAL ESTATE INCOME, INC.

(Dollar amounts in thousands, except share data)

|

|

|

March 31, 2020 (unaudited) |

|

|

December 31, 2019 |

|

||

|

ASSETS |

|

|

|

|

|

|||

|

Cash and cash equivalents |

|

$ |

27,642 |

|

|

$ |

37,210 |

|

|

Restricted cash |

|

|

19,033 |

|

|

|

429 |

|

|

Real estate securities at fair value |

|

|

117,814 |

|

|

|

157,869 |

|

|

Commercial mortgage loans at cost, net of allowance for loan loss of $4,500 and $0, respectively |

|

|

551,336 |

|

|

|

504,702 |

|

|

Deferred debt finance costs |

|

|

2,089 |

|

|

|

1,133 |

|

|

Accrued interest receivable |

|

|

1,880 |

|

|

|

1,822 |

|

|

Prepaid expenses and other assets |

|

|

141 |

|

|

|

154 |

|

|

Total assets |

|

$ |

719,935 |

|

|

$ |

703,319 |

|

|

LIABILITIES AND EQUITY |

|

|

|

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

|

|

|

Repurchase agreements—real estate securities |

|

$ |

103,307 |

|

|

$ |

107,489 |

|

|

Repurchase agreements—commercial mortgage loans |

|

|

375,447 |

|

|

|

335,805 |

|

|

Loan fees payable |

|

|

485 |

|

|

|

55 |

|

|

Due to related parties |

|

|

1,914 |

|

|

|

698 |

|

|

Interest payable |

|

|

514 |

|

|

|

652 |

|

|

Distributions payable |

|

|

— |

|

|

|

1,699 |

|

|

Accrued expenses |

|

|

1,417 |

|

|

|

755 |

|

|

Total liabilities |

|

|

483,084 |

|

|

|

447,153 |

|

|

Stockholders’ Equity: |

|

|

|

|

|

|

|

|

|

Class P common stock, $0.001 par value, 500,000,000 shares authorized, 10,151,787 and 10,182,305 shares issued and outstanding at March 31, 2020 and December 31, 2019, respectively |

|

|

10 |

|

|

|

10 |

|

|

Class A common stock, $0.001 par value, 500,000,000 shares authorized, 653,566 and 272,006 shares issued and outstanding as of March 31, 2020 and December 31, 2019, respectively |

|

|

1 |

|

|

|

— |

|

|

Class T common stock, $0.001 par value, 500,000,000 shares authorized, 397,251 and 121,718 shares issued and outstanding as of March 31, 2020 and December 31, 2019, respectively |

|

— |

|

|

|

— |

|

|

|

Class S common stock, $0.001 par value, 500,000,000 shares authorized, 0 shares issued and outstanding as of March 31, 2020 and December 31, 2019, respectively |

|

— |

|

|

|

— |

|

|

|

Class D common stock, $0.001 par value, 500,000,000 shares authorized, 50,081 and 41,538 shares issued and outstanding as of March 31, 2020 and December 31, 2019, respectively |

|

— |

|

|

|

— |

|

|

|

Class I common stock, $0.001 par value, 500,000,000 shares authorized, 378,302 and 100,743 shares issued and outstanding as of March 31, 2020 and December 31, 2019, respectively |

|

— |

|

|

|

— |

|

|

|

Additional paid in capital (net of offering costs of $24,283 and $22,718 at March 31, 2020 and December 31, 2019, respectively) |

|

|

288,030 |

|

|

|

265,963 |

|

|

Accumulated deficit |

|

|

(51,190 |

) |

|

|

(9,807 |

) |

|

Total stockholders’ equity |

|

|

236,851 |

|

|

|

256,166 |

|

|

Total liabilities and stockholders’ equity |

|

$ |

719,935 |

|

|

$ |

703,319 |

|

The accompanying notes are an integral part of these consolidated financial statements

2

INPOINT COMMERCIAL REAL ESTATE INCOME, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, dollar amounts in thousands, except share data)

|

|

|

Three-months ended March 31, |

|

|||||

|

|

|

2020 |

|

|

2019 |

|

||

|

Interest income: |

|

|

|

|

|

|

|

|

|

Interest income |

|

$ |

10,356 |

|

|

$ |

6,591 |

|

|

Less: Interest expense |

|

|

(3,962 |

) |

|

|

(2,755 |

) |

|

Net interest income |

|

|

6,394 |

|

|

|

3,836 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

Advisory fee |

|

|

844 |

|

|

|

1,531 |

|

|

Debt finance costs |

|

|

254 |

|

|

|

195 |

|

|

Directors compensation |

|

|

24 |

|

|

|

21 |

|

|

Professional service fees |

|

|

218 |

|

|

|

150 |

|

|

Other expenses |

|

|

225 |

|

|

|

84 |

|

|

Total operating expenses |

|

|

1,565 |

|

|

|

1,981 |

|

|

Other (loss) income: |

|

|

|

|

|

|

|

|

|

Provision for loan losses |

|

|

(4,500 |

) |

|

|

— |

|

|

Unrealized (loss) gain in value of real estate securities |

|

|

(38,187 |

) |

|

|

1,808 |

|

|

Realized loss on the sale of real estate securities |

|

|

— |

|

|

|

(43 |

) |

|

Total other (loss) income |

|

|

(42,687 |

) |

|

|

1,765 |

|

|

Net (loss) income |

|

$ |

(37,858 |

) |

|

$ |

3,620 |

|

|

Net (loss) income per share basic and diluted |

|

$ |

(3.34 |

) |

|

$ |

0.54 |

|

|

Weighted average number of shares |

|

|

|

|

|

|

|

|

|

Basic |

|

|

11,349,448 |

|

|

|

6,676,846 |

|

|

Diluted |

|

|

11,349,581 |

|

|

|

6,677,279 |

|

The accompanying notes are an integral part of these consolidated financial statements

3

INPOINT COMMERCIAL REAL ESTATE INCOME, INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(Unaudited, dollar amounts in thousands)

|

For the three-months ended March 31, 2020 |

Par Value Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

Class P |

|

|

Class A |

|

|

Class T |

|

|

Class S |

|

|

Class D |

|

|

Class I |

|

|

Additional Paid in Capital |

|

|

Accumulated Deficit |

|

|

Total Stockholders’ Equity |

|

|||||||||

|

Balance as of December 31, 2019 |

$ |

10 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

265,963 |

|

|

$ |

(9,807 |

) |

|

$ |

256,166 |

|

|

Proceeds from issuance of common stock |

|

— |

|

|

|

1 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

24,260 |

|

|

|

— |

|

|

|

24,261 |

|

|

Offering costs |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,565 |

) |

|

|

— |

|

|

|

(1,565 |

) |

|

Net loss |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(37,858 |

) |

|

|

(37,858 |

) |

|

Distributions declared |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(3,525 |

) |

|

|

(3,525 |

) |

|

Distribution reinvestment |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

127 |

|

|

|

— |

|

|

|

127 |

|

|

Redemptions |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(763 |

) |

|

|

— |

|

|

|

(763 |

) |

|

Equity-based compensation |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

8 |

|

|

|

— |

|

|

|

8 |

|

|

Balance as of March 31, 2020 |

$ |

10 |

|

|

$ |

1 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

288,030 |

|

|

$ |

(51,190 |

) |

|

$ |

236,851 |

|

|

For the three-months ended March 31, 2019 |

Par Value Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

Class P |

|

|

Class A |

|

|

Class T |

|

|

Class S |

|

|

Class D |

|

|

Class I |

|

|

Additional Paid in Capital |

|

|

Accumulated Deficit |

|

|

Total Stockholders’ Equity |

|

|||||||||

|

Balance as of December 31, 2018 |

$ |

6 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

148,650 |

|

|

$ |

(6,384 |

) |

|

$ |

142,272 |

|

|

Proceeds from issuance of common stock |

|

2 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

42,678 |

|

|

|

— |

|

|

|

42,680 |

|

|

Offering costs |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(3,024 |

) |

|

|

— |

|

|

|

(3,024 |

) |

|

Net income |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

3,620 |

|

|

|

3,620 |

|

|

Distributions declared |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(3,170 |

) |

|

|

(3,170 |

) |

|

Equity-based compensation |

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

5 |

|

|

|

— |

|

|

|

5 |

|

|

Balance as of March 31, 2019 |

$ |

8 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

188,309 |

|

|

$ |

(5,934 |

) |

|

$ |

182,383 |

|

The accompanying notes are an integral part of these consolidated financial statements

4

INPOINT COMMERCIAL REAL ESTATE INCOME, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, dollar amounts in thousands)

|

|

|

For the three-months ended March 31, |

|

|||||

|

|

|

2020 |

|

|

2019 |

|

||

|

Cash flows from operating activities: |

|

|

|

|

|

|

|

|

|

Net (loss) income |

|

$ |

(37,858 |

) |

|

$ |

3,620 |

|

|

Adjustments to reconcile net income to cash provided by operations: |

|

|

|

|

|

|

|

|

|

Net realized loss on real estate securities |

|

|

— |

|

|

|

43 |

|

|

Net unrealized loss (gain) on real estate securities |

|

|

38,187 |

|

|

|

(1,808 |

) |

|

Provision for loan losses |

|

|

4,500 |

|

|

|

— |

|

|

Amortization of equity-based compensation |

|

|

8 |

|

|

|

5 |

|

|

Amortization of debt finance costs to operating expense |

|

|

254 |

|

|

|

195 |

|

|

Amortization of debt finance costs to interest expense |

|

|

19 |

|

|

|

22 |

|

|

Amortization of bond discount |

|

|

(221 |

) |

|

|

(177 |

) |

|

Amortization of origination fees |

|

|

(360 |

) |

|

|

(268 |

) |

|

Amortization of deferred exit fees |

|

|

(231 |

) |

|

|

(131 |

) |

|

Changes in assets and liabilities: |

|

|

|

|

|

|

|

|

|

Accrued interest receivable |

|

|

(58 |

) |

|

|

(159 |

) |

|

Accrued expenses |

|

|

(381 |

) |

|

|

(91 |

) |

|

Loan fees payable |

|

|

430 |

|

|

|

50 |

|

|

Accrued interest payable |

|

|

(138 |

) |

|

|

17 |

|

|

Due to related parties |

|

|

784 |

|

|

|

350 |

|

|

Prepaid expenses and other assets |

|

|

47 |

|

|

|

(7 |

) |

|

Net cash provided by operating activities |

|

|

4,982 |

|

|

|

1,661 |

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

|

Origination of commercial loans |

|

|

(50,543 |

) |

|

|

(72,868 |

) |

|

Origination fees received on commercial loans |

|

|

— |

|

|

|

618 |

|

|

Purchase of real estate securities |

|

|

— |

|

|

|

(14,884 |

) |

|

Real estate securities sold |

|

|

— |

|

|

|

9,211 |

|

|

Real estate securities principal pay-down |

|

|

2,054 |

|

|

|

710 |

|

|

Net cash used in investing activities |

|

|

(48,489 |

) |

|

|

(77,213 |

) |

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

|

Proceeds from issuance of common stock |

|

|

24,261 |

|

|

|

42,680 |

|

|

Redemptions of common stock |

|

|

(763 |

) |

|

|

— |

|

|

Payment of offering costs |

|

|

(1,132 |

) |

|

|

(3,024 |

) |

|

Proceeds from repurchase agreements |

|

|

402,767 |

|

|

|

269,791 |

|

|

Principal repayments of repurchase agreements |

|

|

(367,307 |

) |

|

|

(229,099 |

) |

|

Debt finance costs |

|

|

(185 |

) |

|

|

(381 |

) |

|

Distributions paid |

|

|

(5,098 |

) |

|

|

(2,922 |

) |

|

Net cash provided by financing activities |

|

|

52,543 |

|

|

|

77,045 |

|

|

Net change in cash, cash equivalents and restricted cash |

|

|

9,036 |

|

|

|

1,493 |

|

|

Cash, cash equivalents and restricted cash at beginning of period |

|

|

37,639 |

|

|

|

28,497 |

|

|

Cash, cash equivalents and restricted cash at end of period |

|

$ |

46,675 |

|

|

$ |

29,990 |

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

|

Change in deferred offering costs and accrued offering expenses, included in due to related parties |

|

$ |

— |

|

|

$ |

(422 |

) |

|

Interest paid |

|

$ |

4,100 |

|

|

$ |

2,739 |

|

|

Distributions payable |

|

$ |

— |

|

|

$ |

1,189 |

|

|

Receivable for real estate securities paydown |

|

$ |

(34 |

) |

|

$ |

— |

|

|

Accrued stockholder servicing fee due to related party |

|

$ |

433 |

|

|

$ |

— |

|

|

Distribution reinvestment |

|

$ |

127 |

|

|

$ |

— |

|

The accompanying notes are an integral part of these consolidated financial statements

5

Note 1 – Organization and Business Operations

InPoint Commercial Real Estate Income, Inc. (the “Company”) was incorporated in Maryland on September 13, 2016 to originate, acquire and manage a diversified portfolio of commercial real estate (“CRE”) investments primarily comprised of (i) CRE debt, including floating rate first mortgage loans, subordinate mortgage and mezzanine loans, and participations in such loans and (ii) floating rate CRE securities, such as commercial mortgage-backed securities (“CMBS”), and senior unsecured debt of publicly traded real estate investment trusts (“REITs”). The Company may also invest in select equity investments in single-tenant, net leased properties. Substantially all of the Company’s business is conducted through InPoint REIT Operating Partnership, LP (the “Operating Partnership”), a Delaware limited partnership. The Company is the sole general partner and directly or indirectly holds all of the limited partner interests in the Operating Partnership. The Company has elected to be taxed as a REIT for U.S. federal income tax purposes.

The Company is externally managed by Inland InPoint Advisor, LLC (the “Advisor”), a Delaware limited liability company formed in August 2016 that is a wholly owned indirect subsidiary of Inland Real Estate Investment Corporation, a member of The Inland Real Estate Group of Companies, Inc. The Advisor is responsible for coordinating the management of the day-to-day operations and originating, acquiring and managing the Company’s CRE investment portfolio, subject to the supervision of the Company’s board of directors (the “Board”). The Advisor performs its duties and responsibilities as the Company’s fiduciary pursuant to an amended and restated advisory agreement dated April 29, 2019 among the Company, the Advisor and the Operating Partnership (the “Advisory Agreement”), which supersedes and replaces the advisory agreement dated October 25, 2016 (the “Prior Advisory Agreement”).

The Advisor has delegated certain of its duties to SPCRE InPoint Advisors, LLC (the “Sub-Advisor”), a Delaware limited liability company formed in September 2016 that is a wholly owned subsidiary of Sound Point CRE Management, LP, pursuant to an amended and restated sub-advisory agreement between the Advisor and the Sub-Advisor dated April 29, 2019, which supersedes and replaces the sub-advisory agreement dated October 25, 2016. Among other duties, the Sub-Advisor has the authority to identify, negotiate, acquire and originate the Company’s investments and provide portfolio management, disposition, property management and leasing services to the Company. Notwithstanding such delegation to the Sub-Advisor, the Advisor retains ultimate responsibility for the performance of all the matters entrusted to it under the Advisory Agreement, including those duties which the Advisor has not delegated to the Sub-Advisor such as (i) valuation of the Company’s assets and calculation of the Company’s net asset value (“NAV”); (ii) management of the Company’s day-to-day operations; (iii) preparation of stockholder reports and communications and arrangement of the Company’s annual stockholder meeting; and (iv) advising the Company regarding its initial qualification as a REIT for U.S. federal income tax purposes and monitoring its ongoing compliance with the REIT qualification requirements thereafter.

On October 25, 2016, the Company commenced a private offering (the “Private Offering”) of up to $500,000 in shares of Class P common stock (“Class P Shares”). Inland Securities Corporation, an affiliate of the Advisor (the “Dealer Manager”), was the dealer manager for the Private Offering. On June 28, 2019, the Company terminated the Private Offering in anticipation of selling shares in the IPO (described below). The Company continued to accept Private Offering subscription proceeds through July 16, 2019 from subscription agreements executed no later than June 28, 2019. As of July 16, 2019, the Company had received and accepted investors’ subscriptions for and issued 10,258,094 Class P Shares in the Private Offering, resulting in gross proceeds of $276,681.

On March 22, 2019, the Company filed a Registration Statement on Form S-11 (File No. 333-230465) (the “Registration Statement”) to register up to $2,350,000 in shares of common stock (the “IPO”).

On April 29, 2019, the Company filed articles of amendment with the State Department of Assessments and Taxation of the State of Maryland (the “SDAT”) (i) to modify the number of shares of capital stock the Company has authority to issue under its charter from 500,000,000 to 3,050,000,000, consisting of 3,000,000,000 Class P Shares and 50,000,000 shares of preferred stock, and (ii) to modify the aggregate par value of all authorized shares of stock from $500 to $3,050.

On April 29, 2019, the Company also filed articles supplementary with SDAT to reclassify and designate: (i) 500,000,000 authorized but unissued Class P Shares as Class A common shares; (ii) 500,000,000 authorized but unissued Class P Shares as Class D common shares; (iii) 500,000,000 authorized but unissued Class P Shares as Class I common shares; (iv) 500,000,000 authorized but unissued Class P Shares as Class S common shares; and (v) 500,000,000 authorized but unissued Class P Shares as Class T common shares.

On May 3, 2019, the Securities and Exchange Commission (the “SEC”) declared effective the Registration Statement and the Company commenced the IPO. Prior to July 17, 2019 (the “NAV Pricing Date”), the purchase price for each class of its common stock in its primary offering was $25.00 per share, plus applicable upfront selling commissions and dealer manager fees. Following the NAV Pricing Date, the purchase price per share for each class of common stock in the IPO varies and generally equals the prior

6

month’s NAV per share, as determined monthly, plus applicable upfront selling commissions and dealer manager fees. The Dealer Manager serves as the Company’s exclusive dealer manager for the IPO on a best efforts basis.

On March 24, 2020, the Board unanimously approved the suspension of (i) the sale of shares in the IPO, effective immediately, (ii) the operation of the share repurchase program (the “SRP”), effective immediately, (iii) the payment of distributions to the Company’s stockholders, effective immediately, and (iv) the operation of the distribution reinvestment plan (the “DRP”), effective as of April 6, 2020. The IPO, the SRP, the payment of distributions and the DRP will each remain suspended until such time as the Board approves their resumption.

In determining to suspend the IPO, the SRP, the payment of distributions and the DRP, the Board considered various factors, including the impact of the global COVID-19 pandemic on the economy, the inability to accurately calculate the Company’s NAV per share due to uncertainty, volatility and lack of liquidity in the market, the Company’s need for liquidity due to financing challenges related to additional collateral required by the banks that regularly finance the Company’s assets and these uncertain and rapidly changing economic conditions. While it is extremely difficult to predict when market conditions will enable an accurate calculation of the Company’s NAV, the Board believes that this is a temporary market disruption. The Company will continue to closely monitor this situation in order to determine an appropriate time to resume the IPO, the SRP, the payment of distributions and the DRP. Please refer to “Note 13 – Subsequent Events” and Part II, “Item 1A – Risk Factors” for updates on the business after March 31, 2020 and discussion of risk factors related to the COVID-19 pandemic, respectively.

Note 2 – Summary of Significant Accounting Policies

Disclosures discussing all significant accounting policies are set forth in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019 (the “Annual Report”), as filed with the SEC on March 11, 2020, under the heading Note 2 – Summary of Significant Accounting Policies. There have been no changes to the Company’s significant accounting policies for the three-months ended March 31, 2020.

Basis of Accounting

The accompanying consolidated financial statements and related footnotes have been prepared in conformity with U.S. generally accepted accounting principles (“GAAP”) and require management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reported periods. Actual results could differ from such estimates.

In the opinion of management, the accompanying unaudited consolidated financial statements reflect all adjustments, which are normal and recurring in nature, necessary for fair financial statement presentation.

Cash, Cash Equivalents and Restricted Cash

Cash and cash equivalents include funds on deposit with financial institutions, including demand deposits with financial institutions with original maturities of three months or less. The account balance may exceed the Federal Deposit Insurance Corporation (“FDIC”) insurance coverage limits and, as a result, there could be a concentration of credit risk related to amounts on deposit in excess of FDIC insurance coverage limits. The Company believes that the risk will not be significant, as the Company does not anticipate the financial institutions’ non-performance.

Restricted cash represents cash the Company is required to hold in a segregated account. As of March 31, 2020 and December 31, 2019, the restricted cash was held as additional collateral on real estate securities repurchase agreements.

The following table provides a reconciliation of cash, cash equivalents and restricted cash in the Company’s consolidated balance sheets to the total amount shown in the Company’s consolidated statements of cash flows:

|

|

|

March 31, |

|

|

December 31, |

|

||

|

|

|

2020 |

|

|

2019 |

|

||

|

Cash and cash equivalents |

|

$ |

27,642 |

|

|

$ |

37,210 |

|

|

Restricted cash |

|

|

19,033 |

|

|

|

429 |

|

|

Total cash, cash equivalents, and restricted cash |

|

$ |

46,675 |

|

|

$ |

37,639 |

|

7

Accounting Pronouncements Recently Issued but Not Yet Effective

In June 2016, the Financial Accounting Standards Board (“FASB”) issued ASU 2016-13, “Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments” (“ASU 2016-13”), which changes how entities measure credit losses for financial assets carried at amortized cost. ASU 2016-13 eliminates the requirement that a credit loss must be probable before it can be recognized and instead requires an entity to recognize the current estimate of all expected credit losses. ASU 2016-13 is effective for SEC filers for reporting periods beginning after December 15, 2019. In November 2019, the FASB issued ASU 2019-10, “Financial Instruments – Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates”, which grants smaller reporting companies (as defined by the SEC) until reporting periods commencing after December 15, 2022 to implement ASU 2016-13. The Company has elected to use this extension and is continuing to evaluate the impact ASU 2016-13 will have on its allowance for loan losses estimate.

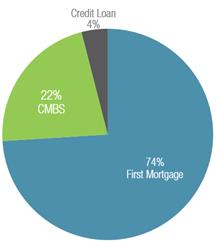

Note 3 – Commercial Mortgage Loans Held for Investment

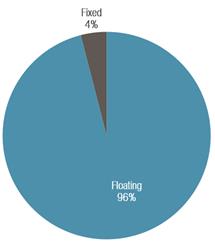

The tables below show the Company’s commercial mortgage loans held for investment as of March 31, 2020 and December 31, 2019:

March 31, 2020

|

|

|

Number of Loans |

|

|

Principal Balance |

|

|

Unamortized (fees)/costs, net |

|

|

Allowance for loan losses(1) |

|

|

Carrying Value |

|

|

Weighted Average Interest Rate |

|

|

Weighted Average Years to Maturity |

|

|||||||

|

First mortgage loans |

|

|

32 |

|

|

$ |

530,445 |

|

|

$ |

(1,109 |

) |

|

$ |

(3,000 |

) |

|

$ |

526,336 |

|

|

|

5.5 |

% |

|

|

1.9 |

|

|

Credit loans |

|

|

4 |

|

|

|

26,500 |

|

|

|

— |

|

|

|

(1,500 |

) |

|

|

25,000 |

|

|

|

9.7 |

% |

|

|

7.2 |

|

|

Total and average |

|

|

36 |

|

|

$ |

556,945 |

|

|

$ |

(1,109 |

) |

|

$ |

(4,500 |

) |

|

$ |

551,336 |

|

|

|

5.7 |

% |

|

|

2.1 |

|

December 31, 2019

|

|

|

Number of Loans |

|

|

Principal Balance |

|

|

Unamortized (fees)/costs, net |

|

|

Allowance for loan losses |

|

|

Carrying Value |

|

|

Weighted Average Interest Rate |

|

|

Weighted Average Years to Maturity |

|

|||||||

|

First mortgage loans |

|

|

29 |

|

|

$ |

489,902 |

|

|

$ |

(1,700 |

) |

|

$ |

— |

|

|

$ |

488,202 |

|

|

|

5.6 |

% |

|

|

2.0 |

|

|

Credit loans |

|

|

3 |

|

|

|

16,500 |

|

|

|

— |

|

|

|

— |

|

|

|

16,500 |

|

|

|

9.5 |

% |

|

|

5.9 |

|

|

Total and average |

|

|

32 |

|

|

$ |

506,402 |

|

|

$ |

(1,700 |

) |

|

$ |

— |

|

|

$ |

504,702 |

|

|

|

5.7 |

% |

|

|

2.2 |

|

|

____________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) |

Includes a reserve on one first mortgage loan and one credit loan at March 31, 2020. There is no general reserve for loan losses. |

Allowance for loan losses

The following table presents the activity in the Company’s allowance for loan losses:

|

|

|

Three Months Ended March 31, 2020 |

|

|

Three Months Ended March 31, 2019 |

|

||

|

Beginning of period |

|

$ |

— |

|

|

$ |

— |

|

|

Provision for loan losses |

|

|

4,500 |

|

|

|

— |

|

|

Charge-offs |

|

|

— |

|

|

|

— |

|

|

Ending allowance for loan losses |

|

$ |

4,500 |

|

|

$ |

— |

|

In accordance with the Company’s allowance for loan loss policy, during the three month period ended March 31, 2020, we recorded impairment charges of $3,000 on one first mortgage loan secured by a hotel property in Illinois and $1,500 on a credit loan secured by a hotel property located in Florida. The impairment charges were based on the estimated fair value of the underlying collateral. As of March 31, 2020, our recorded investment in the loans were $21,500 ($24,500, net of a $3,000 allowance for loan loss) and $1,500 ($3,000, net of a $1,500 allowance for loan loss), respectively. For the three months ended March 31, 2020, interest income for the impaired loans was $546. The two impaired loans were current on monthly payments, however, the economic impact of the COVID-19 pandemic on the hospitality industry was the key factor in the determination that the loans were impaired. For further information on the Company’s allowance for loan losses policy, see “Note 2 – Summary of Significant Accounting Policies” in its Annual Report.

8

As part of the Company’s process for monitoring the credit quality of its investments, it performs a quarterly asset review of the investment portfolio and assigns risk ratings to each of its loans and CMBS. Risk factors include payment status, lien position, borrower financial resources and investment in collateral, collateral type, project economics and geographic location, as well as national and regional economic factors. To determine the likelihood of loss, the loans are rated on a 5-point scale as follows:

|

Investment Grade |

Investment Grade Definition |

|

1 |

Investment exceeding fundamental performance expectations and/or capital gain expected. Trends and risk factors since time of investment are favorable. |

|

2 |

Performing consistent with expectations and a full return of principal and interest expected. Trends and risk factors are neutral to favorable. |

|

3 |

Performing investment requiring closer monitoring. Trends and risk factors show some deterioration. Collection of principal and interest is still expected. |

|

4 |

Underperforming investment with the potential of some interest loss but still expecting a positive return on investment. Trends and risk factors are negative. |

|

5 |

Underperforming investment with expected loss of interest and some principal. |

All investments are assigned an initial risk rating of 2 at origination or acquisition.

As of March 31, 2020, 28 loans had a risk rating of 2, five had a risk rating of 3, one had a risk rating of 4 and two had a risk rating of 5. As of December 31, 2019, 30 loans had a risk rating of 2 and two had a risk rating of 3.

Note 4 – Real Estate Securities

The Company classified its real estate securities as available-for-sale. These investments are reported at fair value in the consolidated balance sheets with changes in fair value recorded in other income or loss in the consolidated statements of operations.

The tables below show the Company’s real estate securities as of March 31, 2020 and December 31, 2019:

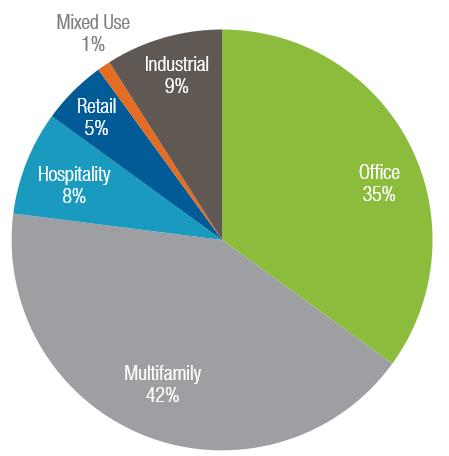

March 31, 2020

|

Number of Positions |

|

|

External Credit Rating |

|

Collateral |

|

Weighted Average Interest Rate |

|

|

Weighted Average Years to Maturity |

|

Par Value |

|

|

Amortized Cost |

|

|

Unrealized Gains |

|

|

Unrealized Losses |

|

|

Fair Value |

|

|||||||

|

3 |

|

|

AAA |

|

Hospitality, Office |

|

|

1.5 |

% |

|

0.8 |

|

$ |

17,126 |

|

|

$ |

17,117 |

|

|

$ |

— |

|

|

$ |

(1,399 |

) |

|

$ |

15,718 |

|

|

|

1 |

|

|

AA- |

|

Hospitality |

|

|

1.7 |

% |

|

0.1 |

|

|

2,000 |

|

|

|

2,000 |

|

|

|

— |

|

|

|

(263 |

) |

|

|

1,737 |

|

|

|

9 |

|

|

BB- |

|

Retail, Hospitality, Mixed Use, Office |

|

|

3.4 |

% |

|

1.1 |

|

|

71,951 |

|

|

|

71,945 |

|

|

|

— |

|

|

|

(17,132 |

) |

|

|

54,813 |

|

|

|

1 |

|

|

BBB- |

|

Multifamily |

|

|

2.4 |

% |

|

1.3 |

|

|

10,000 |

|

|

|

10,000 |

|

|

|

— |

|

|

|

(1,931 |

) |

|

|

8,069 |

|

|

|

3 |

|

|

Unrated |

|

Hospitality |

|

|

5.9 |

% |

|

0.4 |

|

|

55,275 |

|

|

|

55,150 |

|

|

|

— |

|

|

|

(17,673 |

) |

|

|

37,477 |

|

|

|

|

17 |

|

|

|

|

|

|

|

4.0 |

% |

|

0.9 |

|

$ |

156,352 |

|

|

$ |

156,212 |

|

|

$ |

— |

|

|

$ |

(38,398 |

) |

|

$ |

117,814 |

|

9

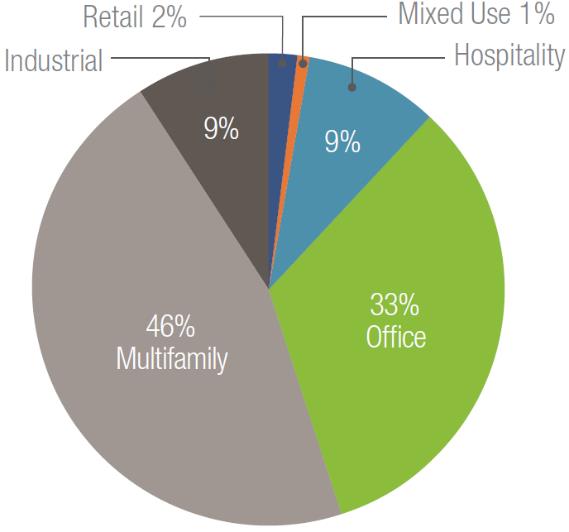

December 31, 2019

|

Number of Positions |

|

|

External Credit Rating |

|

Collateral |

|

Weighted Average Interest Rate |

|

|

Weighted Average Years to Maturity |

|

Par Value |

|

|

Amortized Cost |

|

|

Unrealized Gains |

|

|

Unrealized Losses |

|

|

Fair Value |

|

|||||||

|

3 |

|

|

AAA |

|

Hospitality, Office |

|

|

2.6 |

% |

|

0.5 |

|

$ |

19,113 |

|

|

$ |

19,081 |

|

|

$ |

— |

|

|

$ |

(43 |

) |

|

$ |

19,038 |

|

|

|

1 |

|

|

AA- |

|

Hospitality |

|

|

2.8 |

% |

|

0.4 |

|

|

2,000 |

|

|

|

1,999 |

|

|

|

— |

|

|

|

(11 |

) |

|

|

1,988 |

|

|

|

9 |

|

|

BB- |

|

Retail, Hospitality, Mixed Use, Office |

|

|

4.4 |

% |

|

1.3 |

|

|

72,052 |

|

|

|

72,033 |

|

|

|

104 |

|

|

|

(81 |

) |

|

|

72,056 |

|

|

|

1 |

|

|

BBB- |

|

Multifamily |

|

|

3.4 |

% |

|

1.5 |

|

|

10,000 |

|

|

|

10,000 |

|

|

|

— |

|

|

|

— |

|

|

|

10,000 |

|

|

|

3 |

|

|

Unrated |

|

Hospitality |

|

|

7.0 |

% |

|

0.7 |

|

|

55,275 |

|

|

|

54,967 |

|

|

|

— |

|

|

|

(180 |

) |

|

|

54,787 |

|

|

|

|

17 |

|

|

|

|

|

|

|

5.0 |

% |

|

1.0 |

|

$ |

158,440 |

|

|

$ |

158,080 |

|

|

$ |

104 |

|

|

$ |

(315 |

) |

|

$ |

157,869 |

|

At March 31, 2020, the Company held 17 CMBS with a total carrying value of $117,814 and a total net unrealized loss of $38,398. At December 31, 2019, the Company held 17 CMBS with a total carrying value of $157,869 and a total net unrealized loss of $211. The increase in the unrealized loss was primarily attributed to the significant economic impact of the COVID-19 pandemic on the economy. In particular, CMBS secured by hospitality properties were severely impacted due to concerns over a decline in hotel stays throughout the country. The Company did not have any realized gains or losses during the three months ended March 31, 2020. During the three months ended March 31, 2019, the Company sold real estate securities for $9,211 that resulted in realized losses of $43.

As of March 31, 2020, four of the CMBS had an internal risk rating of 2 and 13 of the CMBS had an internal risk rating of 3. As of December 31, 2019, each CMBS had an internal risk rating of 2.

Note 5 – Repurchase Agreements

Commercial Mortgage Loans

On February 15, 2018, the Company, through a wholly owned subsidiary, entered into a master repurchase agreement (the “CF Repo Facility”) with Column Financial, Inc. as administrative agent for certain of its affiliates. The CF Repo Facility had an initial advance amount of $100,000 subject to a maximum advance amount of $250,000. The Company increased the advance amount in August 2018 to $175,000, and in January 2019 to the maximum of $250,000. In March 2020, the Company temporarily increased the maximum advance amount to $300,000, with this increase as amended set to expire on June 30, 2020. The initial term of the CF Repo Facility was 12 months and the Company extended the maturity date in March 2020 to February 2021. Advances under the CF Repo Facility accrue interest at a per annum rate equal to the London Interbank Offered Rate (“LIBOR”) plus 2.0%. The CF Repo Facility is subject to certain financial covenants. The Company was in compliance with all financial covenant requirements as of March 31, 2020 and December 31, 2019.

On May 6, 2019, the Company, through a wholly owned subsidiary, entered into an uncommitted master repurchase agreement (the “JPM Repo Facility”) with JPMorgan Chase Bank, National Association. The JPM Repo Facility provides up to $150,000 in advances that the Company expects to use to finance the acquisition or origination of eligible loans and participation interests therein. Advances under the JPM Repo Facility accrue interest at per annum rates equal to the sum of (i) the applicable LIBOR index rate plus (ii) a margin of between 1.75% to 2.50%, depending on the attributes of the purchased assets. The initial maturity date of the JPM Repo Facility is May 6, 2021, with two successive one-year extensions at the Company’s option, which may be exercised upon the satisfaction of certain conditions. The JPM Repo Facility is subject to certain financial covenants. The Company was in compliance with all financial covenant requirements as of March 31, 2020 and December 31, 2019.

The JPM Repo Facility and CF Repo Facility (collectively, the “Repo Facilities”) are used to finance eligible loans and each act in the manner of a revolving credit facility that can be repaid as the Company’s assets are paid off and re-drawn as advances against new assets.

10

The tables below show the Repo Facilities as of March 31, 2020 and December 31, 2019:

|

March 31, 2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average |

|

|||||

|

|

Committed Financing |

|

|

Amount Outstanding(1) |

|

|

Accrued Interest Payable |

|

|

Collateral Pledged |

|

|

Interest Rate |

|

|

Days to Maturity |

|

||||||

|

CF Repo Facility |

$ |

300,000 |

|

|

$ |

236,632 |

|

|

$ |

248 |

|

|

$ |

327,010 |

|

|

|

2.70 |

% |

|

|

318 |

|

|

JPM Repo Facility |

|

150,000 |

|

|

|

138,895 |

|

|

|

140 |

|

|

|

194,115 |

|

|

|

2.60 |

% |

|

|

401 |

|

|

|

$ |

450,000 |

|

|

$ |

375,527 |

|

|

$ |

388 |

|

|

$ |

521,125 |

|

|

|

2.67 |

% |

|

|

349 |

|

|

December 31, 2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average |

|

|||||

|

|

Committed Financing |

|

|

Amount Outstanding(1) |

|

|

Accrued Interest Payable |

|

|

Collateral Pledged |

|

|

Interest Rate |

|

|

Days to Maturity |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CF Repo Facility |

$ |

250,000 |

|

|

$ |

224,590 |

|

|

$ |

327 |

|

|

$ |

304,708 |

|

|

|

3.74 |

% |

|

|

318 |

|

|

JPM Repo Facility |

|

150,000 |

|

|

|

111,295 |

|

|

|

157 |

|

|

|

153,194 |

|

|

|

3.63 |

% |

|

|

492 |

|

|

|

$ |

400,000 |

|

|

$ |

335,885 |

|

|

$ |

484 |

|

|

$ |

457,902 |

|

|

|

3.70 |

% |

|

|

376 |

|

|

(1) |

Excludes $80 of unamortized debt issuance costs at both March 31, 2020 and December 31, 2019. |

Real Estate Securities

The Company entered into two master repurchase agreements for real estate securities with separate counterparties and had the following balances outstanding as described in the table below:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average |

|

|||||

|

|

|

Amount Outstanding |

|

|

Accrued Interest Payable |

|

|

Collateral Pledged |

|

|

Interest Rate |

|

|

Days to Maturity |

|

|||||

|

As of March 31, 2020 |

|

$ |

103,307 |

|

|

$ |

126 |

|

|

$ |

160,664 |

|

|

|

3.20 |

% |

|

|

25 |

|

|

As of December 31, 2019 |

|

$ |

107,489 |

|

|

$ |

168 |

|

|

$ |

149,164 |

|

|

|

3.14 |

% |

|

|

11 |

|

The total amount outstanding as of March 31, 2020 and December 31, 2019 was with JP Morgan Securities LLC. The master repurchase agreements are subject to certain financial covenants. The Company was in compliance with all financial covenant requirements as of March 31, 2020 and December 31, 2019.

11

The following tables detail the change in the Company’s outstanding shares of all classes of common stock, including restricted common stock:

|

|

|

Common Stock |

|

|||||||||||||||||||||

|

Three-months ended March 31, 2020 |

|

Class P |

|

|

Class A |

|

|

Class T |

|

|

Class S |

|

|

Class D |

|

|

Class I |

|

||||||

|

Beginning balance |

|

|

10,182,305 |

|

|

|

272,006 |

|

|

|

121,718 |

|

|

|

— |

|

|

|

41,538 |

|

|

|

100,743 |

|

|

Issuance of shares |

|

|

— |

|

|

|

379,250 |

|

|

|

274,570 |

|

|

|

— |

|

|

|

8,066 |

|

|

|

276,250 |

|

|

Distribution reinvestment |

|

|

— |

|

|

|

2,310 |

|

|

|

963 |

|

|

|

— |

|

|

|

477 |

|

|

|

1,309 |

|

|

Issuance of restricted shares |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Redemptions |

|

|

(30,518 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Ending balance |

|

|

10,151,787 |

|

|

|

653,566 |

|

|

|

397,251 |

|

|

|

— |

|

|

|

50,081 |

|

|

|

378,302 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Stock |

|

|||||||||||||||||||||

|

Three-months ended March 31, 2019 |

|

Class P |

|

|

Class A |

|

|

Class T |

|

|

Class S |

|

|

Class D |

|

|

Class I |

|

||||||

|

Beginning balance |

|

|

5,940,744 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of shares |

|

|

1,583,864 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of restricted shares |

|

|

400 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Redemptions |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Ending balance |

|

|

7,525,008 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

Distributions

From January 1, 2019 to July 31, 2019, the Company paid distributions on Class P Shares based on daily record dates, payable in arrears the following month, equal to a daily amount of 1/365th of $1.92 per share. Distributions declared on or after August 1, 2019 on Class P Shares are based on monthly record dates, payable in arrears the following month equal to a monthly amount of 1/12th of $1.92 per share. Distributions on shares of Class A, Class T, Class D and Class I common stock are based on monthly record dates, payable in arrears the following month equal to a monthly amount of 1/12th of $1.62 per share. The table below presents the aggregate distributions declared for each applicable class of common stock during the three-months ended March 31, 2020. The table excludes from dividend declaration any month when there were no outstanding shares for a class of stock.

|

|

|

Common Stock |

|

|||||||||||||||||||||

|

|

|

Class P |

|

|

Class A |

|

|

Class T |

|

|

Class S |

|

|

Class D |

|

|

Class I |

|

||||||

|

Aggregate gross distributions declared per share |

|

$ |

0.3200 |

|

|

$ |

0.2700 |

|

|

$ |

0.2700 |

|

|

$ |

— |

|

|

$ |

0.2700 |

|

|

$ |

0.2700 |

|

|

Stockholder servicing fee per share |

|

N/A |

|

|

N/A |

|

|

|

0.0349 |

|

|

|

— |

|

|

|

0.0103 |

|

|

N/A |

|

|||

|

Net distributions declared per share |

|

$ |

0.3200 |

|

|

$ |

0.2700 |

|

|

$ |

0.2351 |

|

|

$ |

— |

|

|

$ |

0.2597 |

|

|

$ |

0.2700 |

|

As of December 31, 2019, distributions declared but not yet paid amounted to $1,699. No distributions were declared beginning in March 2020, as discussed below. During the three-months ended March 31, 2019, the Company had no shares of Class A, Class T, Class S, Class D or Class I common stock outstanding.

On March 24, 2020, the Board unanimously approved the suspension of the payment of distributions to the Company’s stockholders, effective immediately. The payment of distributions will remain suspended until such time as the Board approves its resumption.

In determining to suspend the payment of distributions, the Board considered various factors, including the impact of the global COVID-19 pandemic on the economy, the inability to accurately calculate the Company’s NAV per share due to uncertainty, volatility and lack of liquidity in the market, the Company’s need for liquidity due to financing challenges related to additional collateral required by the banks that regularly finance the Company’s assets and these uncertain and rapidly changing economic conditions. While it is extremely difficult to predict when market conditions will enable an accurate calculation of the Company’s NAV, the Board believes that this is a temporary market disruption. The Company will continue to closely monitor this situation in order to determine an appropriate time to resume the payment of distributions. Please refer to “Note 13 – Subsequent Events” and Part II, “Item 1A – Risk Factors” for updates on the business after March 31, 2020 and discussion of risk factors related to the COVID-19 pandemic, respectively.

12

Note 7 – Net (Loss) Income Per Share

Basic earnings per share (“EPS”) are computed by dividing net income by the weighted average number of common shares outstanding for the period. Diluted EPS is computed by dividing net income by the common shares plus common share equivalents. The Company’s common share equivalents are unvested restricted shares. For the three months ended March 31, 2020 and 2019, 133 and 433 additional shares related to restricted shares were included in the computations of diluted earnings per share, respectively, because the effect of those common share equivalents were dilutive. The Company excludes antidilutive restricted shares from the calculation of weighted-average shares for diluted earnings per share. There were 17 antidilutive restricted shares for the three months ended March 31, 2020. There were no antidilutive restricted shares for the three months ended March 31, 2019. For further information about the Company’s restricted shares, see “Note 11 – Equity Based Compensation.”

The following table is a summary of the basic and diluted net (loss) income per share computation for the three months ended March 31, 2020 and 2019:

|

|

|

Three-months ended March 31, |

|

|||||

|

|

|

2020 |

|

|

2019 |

|

||

|

Net (loss) income |

|

$ |

(37,858 |

) |

|

$ |

3,620 |

|

|

Weighted average shares outstanding, basic |

|

|

11,349,448 |

|

|

|

6,676,846 |

|

|

Weighted average shares outstanding, diluted |

|

|

11,349,581 |

|

|

|

6,677,279 |

|

|

Net (loss) income per share, basic and diluted |

|

$ |

(3.34 |

) |

|

$ |

0.54 |

|

Note 8 – Commitments and Contingencies

In the ordinary course of business, the Company may become subject to litigation, claims and regulatory matters. The Company has no knowledge of material legal or regulatory proceedings pending or known to be contemplated against the Company at this time.

The Company has made a commitment to advance additional funds under certain of its CRE loans if the borrower meets certain conditions. As of March 31, 2020 and December 31, 2019, the Company had 24 and 22 of such loans, respectively, with a total remaining future funding commitment of $65,527 and $54,620, respectively. The Company advances future funds if the borrower meets certain requirements as specified in the individual loan agreements.

Note 9 – Segment Reporting

The Company has one reportable segment as defined by GAAP for the three months ended March 31, 2020 and 2019.

Note 10 – Transactions with Related Parties

As of March 31, 2020, the Advisor had invested $1,000 in the Company through the purchase of 40,040 Class P Shares. The purchase price per Class P Share for the Advisor’s investment was equal to $25.00 (the “Transaction Price”), with no payment of selling commissions, dealer manager fees or organization and offering expenses. The Advisor has agreed pursuant to its subscription agreement that, for so long as it or its affiliate is serving as the Company’s advisor, (i) it will not sell or transfer at least 8,000 of the Class P Shares that it has purchased, accounting for $200 of its investment, to an unaffiliated third party; (ii) it will not be eligible to submit a request for these 40,040 Class P Shares pursuant to the SRP prior to the fifth anniversary of the date on which such Class P Shares were purchased (November 2021); and (iii) repurchase requests made for these Class P Shares will only be accepted (a) on the last business day of a calendar quarter, (b) after all repurchase requests from all other stockholders for such quarter have been accepted and (c) to the extent that such repurchases do not cause total repurchases in the quarter in which they are being repurchased to exceed that quarter’s repurchase cap.

As of March 31, 2020, Sound Point Capital Management, LP (“Sound Point”), an affiliate of the Sub-Advisor, had invested $3,000 in the Company through the purchase of 120,000 Class P Shares. The purchase price per Class P Share for this investment was the Transaction Price, with no payment of selling commissions, dealer manager fees or organization and offering expenses. Sound Point has agreed pursuant to its subscription agreement that, for so long as the Sub-Advisor or its affiliate is serving as the Company’s sub-advisor, (i) it will not be eligible to submit a request for the repurchase of these 120,000 Class P Shares pursuant to the SRP prior to the fifth anniversary of the date on which such Class P Shares were purchased (November 2021); and (ii) repurchase requests made for these Class P Shares will only be accepted (a) on the last business day of a calendar quarter, (b) after all repurchase requests from all other stockholders for such quarter have been accepted and (c) to the extent that such repurchases do not cause total repurchases in the quarter in which they are being repurchased to exceed that quarter’s repurchase cap.

13

The following table summarizes the Company’s related party transactions for the three months ended March 31, 2020 and 2019 and the amount due to related parties at March 31, 2020 and December 31, 2019:

|

|

|

Three-months ended March 31, |

|

|

Payable as of March 31, |

|

|

Payable as of December 31, |

|

|||||||

|

|

|

2020 |

|

|

2019 |

|

|

2020 |

|

|

2019 |

|

||||

|

Organization and offering expense reimbursement(1) |

|

$ |

60 |

|

|

$ |

112 |

|

|

$ |

9 |

|

|

$ |

17 |

|

|

Selling commissions and dealer manager fee(2) |

|

|

758 |

|

|

|

2,485 |

|

|

|

— |

|

|

|

— |

|

|

Advisory fee(3) |

|

|

844 |

|

|

|

1,531 |

|

|

|

558 |

|

|

|

— |

|

|

Loan fees(4) |

|

|

794 |

|

|

|

— |

|

|

|

641 |

|

|

|

408 |

|

|

Accrued stockholder servicing fee(5) |

|

|

446 |

|

|

|

— |

|

|

|

706 |

|

|

|

273 |

|

|

Operating expense reimbursement to advisor (6) |

|

|

— |

|

|

|

2 |

|

|

|

— |

|

|

|

— |

|

|

Total |

|

$ |

2,902 |

|

|

$ |

4,130 |

|

|

$ |

1,914 |

|

|

$ |

698 |

|

|

(1) |

The Company reimburses the Advisor, the Sub-Advisor and their respective affiliates for costs and other expenses related to the Private Offering, provided that aggregate reimbursements of such costs and expenses shall not exceed the organization and offering expenses paid by investors in connection with the sale of Class P Shares in the Private Offering. The Company also reimburses the Advisor, the Sub-Advisor and their respective affiliates for costs and other expenses related to the IPO, provided the Advisor has agreed to reimburse the Company to the extent that the organization and offering expenses that the Company incurs exceeds 15% of its gross proceeds from the IPO. For the Private Offering, offering costs were offset against stockholders’ equity when paid. Offering costs are offset against stockholders’ equity when incurred. |

|

(2) |

The Dealer Manager received selling commissions up to 5%, and a dealer manager fee up to 3%, of the transaction price for each Class P Share sold in the Private Offering, the majority of which was paid to third-party broker-dealers. For the IPO, the Dealer Manager is entitled to receive (a) upfront selling commissions of up to 6.0%, and upfront dealer manager fees of up to 1.25%, of the transaction price of each Class A share sold in the primary offering, however such amounts may vary at certain participating broker-dealers provided that the sum will not exceed 7.25% of the transaction price; (b) upfront selling commissions of up to 3.0%, and upfront dealer manager fees of 0.5%, of the transaction price of each Class T share sold in the primary offering, however such amounts may vary at certain participating broker-dealers provided that the sum will not exceed 3.5% of the transaction price; and (c) upfront selling commissions of up to 3.5% of the transaction price of each Class S share sold in the primary offering. No upfront selling commissions or dealer manager fees are paid with respect to purchases of Class D shares, Class I shares or shares of any class sold pursuant to the DRP. |

|

(3) |