Attached files

| file | filename |

|---|---|

| EX-24 - EXHIBIT 24 - GCP Applied Technologies Inc. | exh24gcp.htm |

| EX-31.1 - EXHIBIT 31.1 GCP 2015 10-K - GCP Applied Technologies Inc. | exh311ceocert.htm |

| EX-31.2 - EXHIBIT 31.2 GCP 2015 10-K - GCP Applied Technologies Inc. | exh312cfocert.htm |

| EX-23 - EXHIBIT 23 GCP 2015 10-K - GCP Applied Technologies Inc. | exh23audconsent.htm |

| EX-32.1 - EXHIBIT 32.1 GCP 2015 10-K - GCP Applied Technologies Inc. | exh321ceocfosoxcert.htm |

| EX-21 - EXHIBIT 21 - GCP Applied Technologies Inc. | exh21gcpsubsidiarylist.htm |

| EX-10.11 - EXHIBIT 10.11 - GCP Applied Technologies Inc. | exh1011gcpexecutiveannuali.htm |

| EX-10.18 - EXHIBIT 10.18 - GCP Applied Technologies Inc. | exh1018gcp2016stockoptiong.htm |

| EX-10.17 - EXHIBIT 10.17 - GCP Applied Technologies Inc. | exh1017gcp2016rsuagreement.htm |

| EX-10.19 - EXHIBIT 10.19 - GCP Applied Technologies Inc. | exh1019gcp2016pbuagreement.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________________________________________________________

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015 |

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____ |

Commission file number 1-37533

GCP Applied Technologies Inc.

Delaware | 47-3936076 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

62 Whittemore Avenue, Cambridge, Massachusetts 02140-1623

(Address of principal executive offices) (Zip code)

(617) 876-1400

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act: | ||

Title of each class | Name of each exchange on which registered | |

Common Stock, $.01 par value | New York Stock Exchange, Inc. | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulations S-K is not contained herein and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

As of June 30, 2015, the registrant's common stock was not publicly traded.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ý No o

At February 29, 2016, 70,625,404 shares of GCP Applied Technologies Common Stock, $.01 par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

Presentation of Information

Unless the context requires otherwise, references to "GCP Applied Technologies Inc.," "GCP," "we," "us," "our" and "the Company" refer to GCP Applied Technologies Inc. and its consolidated subsidiaries for periods subsequent to its separation from W. R. Grace & Co. on February 3, 2016. For periods prior to February 3, 2016, these terms refer to the combined historical business and operations of W. R. Grace & Co.’s construction products and packaging technologies businesses as they were historically managed as part of W. R. Grace & Co. Unless the context requires otherwise, references to "Grace" refer to W. R. Grace & Co. and its consolidated subsidiaries, which is the Company’s former parent company. References in this Annual Report on Form 10-K to the "Separation" refer to the legal separation and transfer of Grace’s construction products and packaging technologies businesses to the Company through a dividend distribution to Grace shareholders on February 3, 2016.

Forward-Looking Statements

The Company has made forward-looking statements in this Annual Report on Form 10-K that are based on management's beliefs and assumptions and on information currently available to management. Forward-looking statements include, but are not limited to, information concerning the Company's possible or assumed future results of operations, financial position, business strategies, financing plans, capital or other expenditures, competitive position, potential growth opportunities, potential operating performance improvements, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and can be identified by the use of forward-looking terminology such as the words "believe," "expect," "plan," "intend," "project," "target," "suggest," "outlook," "anticipate," "estimate," "predict," "potential," "continue," "may," "will," "should" or the negative of these terms or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in these forward-looking statements. You should not place undue reliance on any forward-looking statements.

The risk factors included in Item 1A of this Annual Report on Form 10-K could cause the Company's results to differ materially from those expressed in forward-looking statements. Additionally, there may be other risks and uncertainties that the Company is unable to predict at this time or that the Company currently does not expect to have a material adverse effect on its business that may cause the Company's results to differ materially from those expressed in forward-looking statements.

These forward-looking statements are made as of the filing date of this Annual Report on Form 10-K. The Company expressly disclaims any obligation to update these forward-looking statements other than as required by law.

Trademarks and Trade Names

We own or have rights to trademarks, service marks, copyrights and trade names that we use in conjunction with the operation of our business, including, except as otherwise indicated, the trademarks, service marks or trade names used in this report. This report may include trademarks, service marks and trade names of other companies. Each trademark, service mark or trade name of any other company appearing in this Annual Report on Form 10-K belongs to its holder. Unless otherwise indicated, use or display by us of other parties’ trademarks, service marks or trade names is not intended to and does not imply a relationship with the trade name owner, or endorsement or sponsorship by us of the trademark, service mark or trade name owner.

PART I

Item 1. BUSINESS

BUSINESS OVERVIEW

We are engaged in the production and sale of specialty construction chemicals, specialty building materials and packaging sealants and coatings through three global operating segments in which we have achieved leadership positions. Specialty Construction Chemicals manufactures and markets products to improve the performance of Portland cement, the most widely used construction material in the world, and materials based on Portland cement such as concrete admixtures and cement additives, as well as, concrete production management systems. Specialty Building Materials manufactures and markets building envelope products, residential building products and specialty construction products. Darex Packaging Technologies manufactures and markets sealants and coatings for use in beverage and food containers and other consumer and industrial applications.

GCP Applied Technologies Inc. was incorporated on May 1, 2015 for the purpose of holding the construction products and packaging technologies businesses of W. R. Grace & Co. On February 3, 2016, Grace shareholders of record received one common share of GCP for every one common share of Grace held as of the record date, January 27, 2016, and the construction products and packaging technologies businesses of Grace were transferred to GCP, thereby completing our legal separation from Grace ("the Separation"). On February 4, 2016, we began "regular way" trading on the New York Stock Exchange under the ticker symbol "GCP."

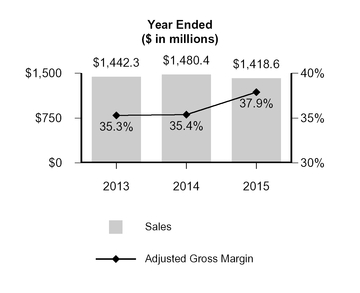

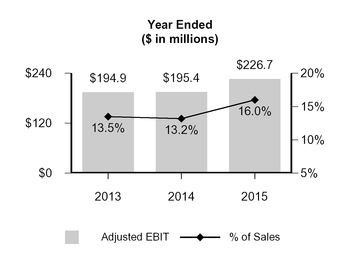

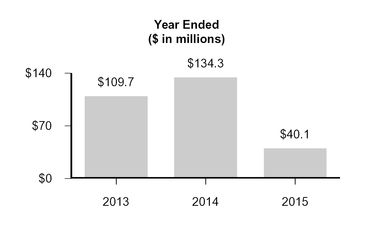

For the years ended December 31, 2015 and 2014, while we were still a part of Grace, we had net sales of $1.4 billion and $1.5 billion, income before income taxes of $125.2 million and $191.1 million and net income of $40.1 million and $134.3 million, respectively. Approximately 64% of our 2015 sales are generated outside the United States and we operate in over 40 countries.

Strategy Overview

Our objective is to deliver value to shareholders by growing our earnings, cash flow and returns on invested capital through the implementation of our business strategies. The Specialty Construction Chemicals, Specialty Building Materials and Darex Packaging Technologies segments are comprised of a portfolio of high-performance products. These products must satisfy well-defined performance requirements and specifications providing high-value to our customers, although they typically represent a low percentage of the total cost of customers’ end-products.

We implement our growth strategies using a number of key levers to accelerate our progress:

Leverage Strong Segment Leadership Positions for Sales Growth — We utilize our global manufacturing and technical service footprint, our research and development and sales organizations, to increase geographic and customer penetration across our global footprint. We intend to make targeted investments to expand our capabilities in geographies and segments where trends and economic cycles present the best opportunities.

Strengthen and Enhance Our Segment Positions with Product Innovation — We will seek to further advance our position as an industry innovator by investing in research development focused on commercializing differentiated products and services. To drive this innovation, we intend to employ our business model of introducing and supporting new technologies through our centralized research and development center in Cambridge, Massachusetts as well as our regional global applications labs. We may invest in additional regional application labs and field technical support resources as we expand our customer base and geographic penetration.

Maintain Strong Customer Focus — A key aspect of our strategy is to continue to deliver product and technology solutions to our customers that help improve their product performance and productivity in their manufacturing operations. We believe that maintaining a close partnership with our customers allows us to effectively focus our innovation efforts and respond to their changing demands at a global, regional and local level.

4

Increase Productivity by Optimizing Global Supply Chain Opportunities — Given the relatively low conversion costs of our products, GCP’s productivity strategies focus on the supply chain. We have established procurement and product formulation expertise to manage our product costs and production efficiencies. Product formulations are optimized at our regional development labs around the world. These formulations are designed to meet specific customer needs while also considering the costs of the various raw material options available to meet those needs. Our global supply chain organization balances local raw material supply with global contracts that improve our buying power. Our manufacturing network also maximizes production and delivery efficiencies.

Grow Through Strategic Acquisitions — When consistent with our business strategies, we will continue to consider seeking strategic, bolt-on acquisitions and alliances to accelerate our customer and geographic penetration, broaden our technology and product portfolios and bolster our manufacturing capacity and capability. Darex Packaging Technologies has provided stable and predictable cash flows and we plan to operate Darex in a manner which allows us to capture growth opportunities across our portfolio.

Drive Cash Flow Conversion and Adjusted EBIT Return on Invested Capital to Deliver Long-Term Value to Our Shareholders — We believe the above strategies will allow us to accelerate our cash flow conversion to invest in research and development activities, manufacturing operations, technical service and sales organizations, strategic acquisitions and to return excess capital to shareholders.

PRODUCTS AND SEGMENTS

Specialty Construction Chemicals Operating Segment (SCC)

We supply concrete admixtures, polymer fibers and in transit monitoring systems to concrete producers that are used to improve the rheology, workability, quality, durability and other engineering properties of concrete, mortar, masonry and other cementitious construction materials. We also supply cement additives to cement manufacturers that are used to improve energy efficiency in cement processing, enhance the characteristics of finished cement and improve ease of use.

Our products reduce our customers' environmental footprints by lowering the energy use and CO2 emissions of our customers' processes. Portland cement-based concrete is the most widely used construction material in the world, with global production of approximately 4 billion tons of Portland cement and more than 10 billion cubic yards of concrete. We compete with several large international suppliers and regionally with smaller competitors. Competition for our products is based on product performance, technical support, the breadth of our manufacturing and distribution infrastructure and our ability to bring value to our customers in the construction industry. Our major global competitors are BASF and Sika.

The following table sets forth SCC sales of similar products as a percentage of GCP total revenue.

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of GCP Revenue | Sales | % of GCP Revenue | Sales | % of GCP Revenue | ||||||||||||||

Concrete Admixtures | $ | 532.7 | 37.5 | % | $ | 541.9 | 36.6 | % | $ | 513.5 | 35.6 | % | ||||||||

Cement Additives | 161.6 | 11.4 | % | 184.4 | 12.5 | % | 174.6 | 12.1 | % | |||||||||||

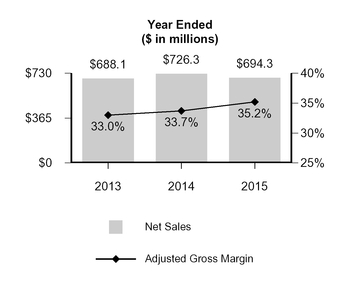

Total SCC Revenue | $ | 694.3 | 48.9 | % | $ | 726.3 | 49.1 | % | $ | 688.1 | 47.7 | % | ||||||||

The following table sets forth SCC sales by geographic region as a percentage of SCC total revenue.

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of SCC Revenue | Sales | % of SCC Revenue | Sales | % of SCC Revenue | ||||||||||||||

North America | $ | 242.0 | 34.9 | % | $ | 235.0 | 32.4 | % | $ | 219.1 | 31.8 | % | ||||||||

Europe Middle East Africa (EMEA) | 141.2 | 20.3 | % | 170.3 | 23.4 | % | 164.6 | 23.9 | % | |||||||||||

Asia Pacific | 181.9 | 26.2 | % | 185.5 | 25.5 | % | 170.6 | 24.8 | % | |||||||||||

Latin America | 129.2 | 18.6 | % | 135.5 | 18.7 | % | 133.8 | 19.5 | % | |||||||||||

Total SCC Revenue | $ | 694.3 | 100.0 | % | $ | 726.3 | 100.0 | % | $ | 688.1 | 100.0 | % | ||||||||

5

SCC consists of two product groups: concrete admixtures and cement additives.

Concrete admixtures

The concrete admixtures product group includes concrete admixtures, admixtures for decorative concrete and concrete production management systems.

Concrete admixtures allow concrete producers to use a limited selection of locally-sourced raw materials (cement and aggregates) to produce concrete to meet a wide variety of performance specifications. Our products are based on a set of core platform technologies formulated regionally into admixtures tailored to local end-use requirements. For example, our MIRA® admixtures allow concrete to be produced with a lower amount of water, which improves the compressive strength and the long-term durability of the concrete. ADVA® admixtures are used to make flowable "self-compacting concrete" which is popular in precast concrete manufacturing where the rapid filling of large molds is a major driver of economics. ECLIPSE® admixtures are used to minimize the formation of shrinkage cracks in critical applications, such as bridge decks. STRUX® polymeric fibers are designed to improve the ductility of concrete which is a naturally brittle material. In some cases, STRUX® polymeric fibers may be used to replace steel reinforcement near the surface of concrete that will be exposed to corrosive de-icing salts.

Admixtures for decorative concrete are used to create decorative/architectural concrete. PIERI® surface retarders are used to obtain exposed aggregate finishes in precast and cast-in-place concrete, achieving the desired surface appearance. PIERI® release agents allow for the efficient removal of mold forms with a resultant blemish-free concrete surface.

Concrete production management systems provide sophisticated process monitoring and control while concrete is in transit to the jobsite. Our patented concrete production management system, VERIFI®, measures, monitors and manages critical concrete properties and systematically adds water or admixtures to maintain optimum concrete flow properties. The result is increased product quality and consistency of concrete, fewer rejected loads, increased jobsite efficiency and minimized costly project delays.

Cement additives

Portland cement is the binding agent for concrete. National standards usually dictate the compressive strength and other properties that must be met by cement. Cement additives are used to reduce the energy required to mill cement to the desired fineness and to improve the handling characteristics of the powdered material. These products are also used to adjust the performance of Portland cement, permitting our customers to optimize production economics. Examples include HEA2®, which is used around the world to improve the energy efficiency of cement grinding operations and CBA®, which is used to produce higher cement strength, providing a high level of process flexibility to the cement manufacturer. Increasingly, cement manufacturers seek to reduce the environmental impact of their manufacturing processes; our additives provide greater flexibility in raw materials, enabling customers to achieve improvements such as reductions in energy use and CO2 emissions.

6

The SCC product portfolio includes:

Products | Uses | Customers | Key Brands | |||

Concrete admixtures | Chemicals and polymeric fibers used to reduce the production and in-place costs of concrete, increase the performance of concrete and improve the life cycle cost of structures | Ready-mix and precast concrete producers, engineers and specifiers | ADVA®, STRUX®, MIRA®, POLARSET®, ECLIPSE®, DARACEM®, DARASET®, DCI®, RECOVER®, WRDA®, ZYLA® | |||

Admixtures for decorative concrete | Products for architectural concrete include surface retarders, coatings, pigments and release agents used by concrete producers and contractors to enhance the surface appearance and aesthetics of concrete | Precast concrete producers and architects | PIERI® | |||

Concrete production management systems | Proprietary sensors, algorithms and control systems which monitor and adjust the flow properties while in transit to construction sites, providing concrete producers quality control and operational efficiencies | Ready-mix concrete manufacturers | VERIFI® | |||

Cement additives | Formulated chemicals added to the milling stage of the cement manufacturing process to improve plant energy efficiency, enhance the performance of the finished cement and help our customers meet environmental regulations and reduce their CO2 footprints | Cement manufacturers | CBA®, SYNCHRO®, HEA2®, TDA®, ESE® | |||

Specialty Building Materials Operating Segment (SBM)

We supply building materials used in both new construction and renovation/repair projects. We manufacture and sell products that protect structures from water, vapor transmission and air penetration as well as fire damage. Our products also reduce energy usage and improve the long-term durability of structures. They include waterproofing membranes and roofing underlayments for use in commercial and residential buildings, polymeric grouts for use in waterproofing and soil stabilization applications, air and vapor barriers, cementitious grouts and passive fire protection.

Our products are specified and installed on commercial, residential and infrastructure projects around the world. Our technology platforms, project selling competencies and international reach are the foundation for our industry leadership. We are dedicated to understanding local codes and construction practices to ensure that our technology solutions address the regional needs of our customers. Our global specification sales organization emphasizes its technical expertise and has established relationships with key influencers and decision makers across the entire project selling value chain including architects, engineers, general contractors, specialty contractors and other channel partners. We continue to expand our international presence in targeted regions with our core product lines and by adding new technologies.

Our specialty building materials product sales are global. We engage with global architectural and contracting firms as well as local specifiers, engineers, contractors and building material distributors that influence the buying decisions for our products. We compete globally with several large international construction materials suppliers, also regionally and locally with numerous smaller competitors. Competition for our products is based on product performance, technical support and service, brand name recognition and price. Our major competitors are Sika, RPM and Carlisle.

The following table sets forth SBM sales of similar products as a percentage of GCP total revenue.

7

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of GCP Revenue | Sales | % of GCP Revenue | Sales | % of GCP Revenue | ||||||||||||||

Building Envelope | $ | 234.7 | 16.6 | % | $ | 236.3 | 16.0 | % | $ | 219.1 | 15.2 | % | ||||||||

Residential Building Products | 79.3 | 5.6 | % | 59.2 | 4.0 | % | 69.3 | 4.8 | % | |||||||||||

Specialty Construction Products | 84.1 | 5.9 | % | $ | 83.8 | 5.6 | % | 81.7 | 5.7 | % | ||||||||||

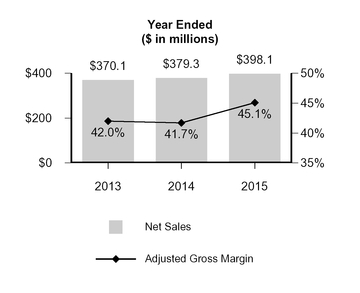

Total SBM Revenue | $ | 398.1 | 28.1 | % | $ | 379.3 | 25.6 | % | $ | 370.1 | 25.7 | % | ||||||||

The following table sets forth SBM sales by geographic region as a percentage of SBM total revenue.

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of SBM Revenue | Sales | % of SBM Revenue | Sales | % of SBM Revenue | ||||||||||||||

North America | $ | 229.6 | 57.7 | % | $ | 201.0 | 53.0 | % | $ | 204.2 | 55.2 | % | ||||||||

Europe Middle East Africa (EMEA) | 94.7 | 23.8 | % | 100.4 | 26.4 | % | 96.3 | 26.0 | % | |||||||||||

Asia Pacific | 69.4 | 17.4 | % | 72.0 | 19.0 | % | 63.0 | 17.0 | % | |||||||||||

Latin America | 4.4 | 1.1 | % | 5.9 | 1.6 | % | 6.6 | 1.8 | % | |||||||||||

Total SBM Revenue | $ | 398.1 | 100.0 | % | $ | 379.3 | 100.0 | % | $ | 370.1 | 100.0 | % | ||||||||

SBM consists of three product groups: building envelope, residential building products and specialty construction products.

Building envelope products

Building envelope products protect structures from water and help manage air and vapor transmission through building walls. The majority of sales in this product group are waterproofing products that protect commercial structures, residential structures and infrastructure. Our waterproofing products are used in both above-grade and below-grade applications. Above grade, our products protect the material to which they are applied and allow architects to design occupied spaces free from water infiltration, and below grade, our products enable the construction of structures in challenging sites, including portions below the existing water table. Examples of these products include our self-adhesive rubberized asphalt membrane, BITUTHENE® and our innovative pre-applied sheet membrane, PREPRUFE®.

Our BITUTHENE® product line is manufactured globally and has a long track record of providing waterproofing in the most challenging conditions. Designers and contractors have relied on BITUTHENE® for over 40 years and continue to specify it by name. We pioneered the pre-applied waterproofing category with our Advanced Bond Technology™ found in PREPRUFE®. Our unique technology allows a waterproofing membrane to be installed on the ground or on walls before concrete is placed for a foundation. This technology also allows waterproofing of walls normally inaccessible during the construction of a building, such as foundations in densely populated cities. Major projects around the world have successfully implemented our PREPRUFE® system and it continues to gain recognition for its waterproofing performance.

Residential building products

Residential building products consist of roofing underlayments, flashing and weather barriers. Roofing underlayments are placed below the outermost roof covering, such as shingles, to protect sloped roofs from water damage caused by wind-driven rain and ice dams. ICE & WATER SHIELD® roofing underlayments are known throughout the industry and are sold in North America through a network of distributors. The VYCOR® flashing portfolio consists of high performance self-adhered flashing products that provide premium protection against water infiltration in critical areas such as windows and doors. VYCOR® flashing reduces the risk of mold and rot development and contributes to energy efficiency by sealing air leakages from the building.

Specialty construction products

Specialty construction products include fire protection, chemical grouts and cementitious grouts and mortars. Passive fire protection products are marketed under the MONOKOTE® brand. Chemical grouts are sold under the DE NEEF® brand and are used to repair cracks in concrete, seal water leaks in commercial buildings and infrastructure in addition to soil stabilization. BETEC® cementitious grouts and mortars are used in applications

8

where specific strength and/or flow are required. Examples of these applications include assembly of concrete precast elements for wind turbines, filling under rails for railroads and providing a high-strength surface for heavy machinery in industrial settings.

The SBM product portfolio includes:

Products | Uses | Customers | Key Brands | |||

Building envelope products | Structural barrier systems to prevent above and below ground water, vapor and air infiltration of the building envelope of commercial structures, including self-adhered sheet and liquid membranes, joint sealing materials, drainage composites and waterstops | Architects, consultants and structural engineers; specialty waterproofing, masons, dry wall contractors and general contractors; specialty distributors | BITUTHENE®, PREPRUFE®, ADPRUFE®, HYDRODUCT®, ADCOR®, SILCOR®, PERM-A-BARRIER® | |||

Residential building products | Specialty roofing membranes and flexible flashings for windows, doors, decks and detail areas, including fully adhered roofing underlayments, synthetic underlayments and self-adhered flashing | Roofing contractors, home builders and remodelers; building material distributors, lumberyards and home centers; architects and specifiers | ICE & WATER SHIELD®, TRI-FLEX®, VYCOR® | |||

Fire protection materials | Fire protection products spray-applied to the structural steel frame, encasing and insulating the steel and protecting the building in the event of fire and enhancing the heat resistance during a fire | Local contractors and specialty subcontractors and applicators; building materials distributors; industrial manufacturers; architects and structural engineers | MONOKOTE® | |||

Chemical grouts | Products for repair and remediation in waterproofing applications and soil stabilization | Contractors; specialty distributors; municipalities; and other owners of large infrastructure facilities | DE NEEF®, HYDRO ACTIVE®, SWELLSEAL®, DE NEEF® PURe™ | |||

Cementitious grouts and mortars | Cementitious grouts and mortars used for under filling and gap filling | Specialty contractors engaged in the repair of concrete, installation of new precast concrete elements and infrastructure repair | BETEC® | |||

Darex Packaging Technologies Operating Segment (Darex)

We supply sealants and coatings to global manufacturers of beverage, food and consumer metal containers and closures and industrial packaging applications. These products, designed with our significant regulatory and application knowledge, protect the packaging materials and preserve their contents. We are the global leader in can sealants.

Our growth is driven by innovation of higher performing products, continuous development of new applications, increasing demand for sustainability, rising disposable income in emerging regions, general economic growth and increasing demand for canned and bottled packaged products. Our customers trust and rely on our global technical service as well as our expertise in global regulatory compliance (including food laws) to address industry challenges and enhance their productivity. We believe we are well positioned to capture industry growth, especially in emerging regions with our global infrastructure. We seek to develop and introduce new products that add additional value to the current and future needs of our customers, such as our introduction of new BPA-NI coatings and products with oxygen scavenging functionality.

Our Darex business is global. We compete with several large international suppliers, and regionally, with many smaller competitors. Our primary global competitors are Altana, Akzo Nobel, PPG and Valspar. Competition for our products is generally based on product performance and reliability, technical service, price and additional value-added features to address the needs of our customers, end-users and brand owners.

9

The following table sets forth Darex sales of similar products as a percentage of GCP total revenue:

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of GCP Revenue | Sales | % of GCP Revenue | Sales | % of GCP Revenue | ||||||||||||||

Sealants and Closures | $ | 221.2 | 15.6 | % | $ | 254.8 | 17.2 | % | $ | 262.2 | 18.2 | % | ||||||||

Coatings | 105.0 | 7.4 | % | 120.0 | 8.1 | % | 121.9 | 8.4 | % | |||||||||||

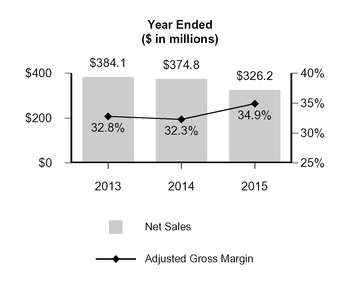

Total Darex Revenue | $ | 326.2 | 23.0 | % | $ | 374.8 | 25.3 | % | $ | 384.1 | 26.6 | % | ||||||||

The following table sets forth Darex sales by geographic region as a percentage of Darex total revenue.

2015 | 2014 | 2013 | ||||||||||||||||||

(In millions) | Sales | % of Darex Revenue | Sales | % of Darex Revenue | Sales | % of Darex Revenue | ||||||||||||||

North America | $ | 66.6 | 20.4 | % | $ | 67.9 | 18.1 | % | $ | 64.9 | 16.9 | % | ||||||||

Europe Middle East Africa (EMEA) | 105.2 | 32.3 | % | 125.3 | 33.4 | % | 124.3 | 32.3 | % | |||||||||||

Asia Pacific | 78.3 | 24.0 | % | 92.2 | 24.6 | % | 102.0 | 26.6 | % | |||||||||||

Latin America | 76.1 | 23.3 | % | 89.4 | 23.9 | % | 92.9 | 24.2 | % | |||||||||||

Total Darex Revenue | $ | 326.2 | 100.0 | % | $ | 374.8 | 100.0 | % | $ | 384.1 | 100.0 | % | ||||||||

Darex consists of two product groups: sealants and closures and coatings.

Sealants and closures

Our sealants and closures product group includes two product lines: can sealants and closures.

Can sealants provide a hermetic seal between the lid and the body of the metal can used in beverage, food, aerosol and industrial packaging. We offer our customers a complete portfolio of both water-base and solvent-base technologies to address current industry trends of thinner gauge metals and high-speed production processes.

Closures provide the seal for pry-off crowns, twist-off crowns and roll-on pilfer-proof (ROPP) and plastic caps. Our CELOX® oxygen scavenging technology protects sensitive beverages from oxygen ingress into the packaging to extend product shelf life and prevent flavor deterioration, color changes and nutrient depletion. Our SINCERA® lubricants are specifically designed for taste sensitive applications.

Coatings

Coatings protect both the interior and exterior surfaces of metal packaging containers and closures. Our coatings are engineered to prevent metal corrosion, ensure proper adhesion of sealing compounds and enhance graphic decorations on the exterior of containers and closures. We introduced our APPERTA® coatings to address increasing industry demands for non-BPA technology. We specifically formulated our SISTIAGA® coatings for technically demanding monobloc beverage and aerosol containers.

10

The Darex product portfolio includes:

Products | Uses | Customers | Key Brands | |||

Sealants | Solvent and water-based compounds for rigid metal containers that ensure a hermetic seal between the lid and the body of beverage, food, aerosol and other cans | Packaging manufacturers and food and beverage companies | DAREX® | |||

Closures | PVC and PVC-free compounds for metal and plastic bottle closures that are used on pry-off and twist-off metal crowns, as well as roll-on pilfer-proof and plastic closures to seal and enhance the shelf life of food and beverages in glass and plastic bottles and jars | Manufacturers of closures for food and beverages | DAREX®, DARAFORM®, DARASEAL®, DARABLEND®, SINCERA®, CELOX® | |||

Coatings | Products for coating metal cans, crowns and closure packaging that protect the metal against corrosion, protect the contents against the influences of metal, ensure proper adhesion of sealing compounds to metal surfaces and provide base coats for inks and for decorative purposes | Packaging manufacturers and food and beverage companies | DAREX®, APPERTA®, SISTIAGA® | |||

SALES AND MARKETING

Our three operating segments maintain direct sales and technical teams made up of approximately 700 employees supporting customers in over 100 countries worldwide. Our global team sells products under annual and multi-year global, regional and local agreements and has developed deep segment and product application knowledge key to our customers' success. We believe our deep rooted understanding of our customers' needs, challenges and operations and our ability to service at high standards throughout the world, give all three segments a competitive advantage. The majority of our products require local, regional, country and international code approvals related to use, storage and performance. Our commercial organization supports and consults on committees and technical associations in order to ensure codes and product standards are consistently applied.

Our SCC and SBM sales professionals work with leading architects, engineers and contractors across the globe seeking to ensure that our products are specified for use in thousands of projects annually. Our products are designed for use in some of the world's most demanding environments including the Getty Center in Los Angeles, the London Underground, Hong Kong’s Bank of China Tower, the Guggenheim Museum Bilbao in Spain and many other landmarks. As part of our "go to market" strategy, the SCC team provides technical services to over 10,000 concrete and cement production facilities worldwide. In many cases, we also provide product dispensing equipment to our customers as an integral part of the concrete and cement production process.

Our Darex business employs a dedicated sales and technical service team to market our line of sealants and coatings in over 75 countries. Darex provides a high level of technical service at the customer facility to ensure proper use of our products, as well as ongoing consultation with our customers to drive productivity and value for the customer throughout the value chain.

MANUFACTURING, RAW MATERIALS AND SUPPLY CHAIN

Our three operating segments share global supply chain processes, manufacturing facilities, as well as technical service and sales centers around the world, which provides cost efficiency.

Specialty Construction Chemicals and Specialty Building Materials

We utilize internal and third party manufacturing to produce our products to our specifications. Our low capital intensive plants along with third-party manufacturers provide us with flexibility in servicing our customers. Several of our plants ship internationally but most of our facilities are positioned to serve local market demand. We have the ability to respond quickly to changes in local demand by establishing or expanding manufacturing capacity with low capital investment. With both vendors and customers, we have numerous multi-year supply and purchasing agreements which help to minimize volume disruption. Construction demand is seasonal resulting in demand variations requiring effective management of our manufacturing and distribution assets. For many of our

11

SCC customers, we install and maintain a chemical dispensing and storage system for our products at their production facilities. We periodically replenish the on-site systems to give our customers instant access to our SCC products in the amounts they require twenty-four hours a day. These dispensing and storage systems have accounted for approximately 32% of our annual capital spend.

The raw materials we use in our products are obtained from a variety of suppliers, including basic chemical and petrochemical producers. Many of our raw materials are organic chemicals derived from olefins, including specialty films and fibers. We also make significant purchases of inorganic materials such as gypsum and specialty materials, including papers, rubber and asphalt. We have multiple raw material sources and balance our purchasing requirements between local and global sources seeking to maximize performance and profitability. Global supply and demand factors, changes in currency exchange rates and petroleum prices can significantly impact the price and availability of our key raw materials.

Our global supply chain team is constantly monitoring the global market to identify cost and productivity opportunities. We seek to leverage our overall volumes for all regions. Since we manufacture a portion of our products in emerging regions using raw materials from suppliers in the U.S., Europe and other advanced economies, changes in the values of the currencies of these emerging regions versus the U.S. dollar and the euro may adversely affect our raw material costs. This effect is partially mitigated by our reliance on local sourcing for some raw materials.

The construction business is cyclical, in response to economic conditions, as well as seasonal, driven by weather conditions. Demand for our products is primarily driven by global non-residential construction activity and U.S. residential construction activity. We seek to increase profitability and minimize the impact of cyclical downturns in regional economies by introducing technically advanced high-performance products and expanding geographically.

Darex Packaging Technologies

Our packaging products are manufactured by a network of globally integrated plants that are positioned to service our customers regionally. Our packaging products are manufactured in both large facilities to permit economies of scale and a network of smaller operations that enable customization to local conditions.

The principal raw materials for Darex products include resins, solvents, latexes (including certain food-grade raw materials), polyolefins, pigments and rubber. Multiple suppliers are generally available for each of these materials; however, some of our raw materials may be provided by single sources of supply. We seek to mitigate the risk of using single source suppliers by identifying and qualifying alternative suppliers or, for unique materials, by using alternative formulations from other suppliers. In some instances, we produce our own raw materials and intermediates.

Prices for many of our raw materials, including specialty and commodity materials such as latex, rubbers, pigments, resins and solvents, have been volatile in recent years. In response to increases in raw material costs, we generally take actions to mitigate the effect of higher costs including increasing our product prices, developing alternative formulations for our products, increasing productivity and fixing purchase costs for certain raw materials.

Since we manufacture a substantial portion of our packaging products in emerging regions using raw materials from suppliers in the U.S., Europe and other advanced economies, changes in the values of the currencies of these emerging regions versus the U.S. dollar and the euro may adversely affect our raw material costs. This effect is partially mitigated by our reliance on local sourcing for many of our raw materials.

FINANCIAL INFORMATION ABOUT INDUSTRY SEGMENTS AND GEOGRAPHIC AREAS

Disclosure of financial information about industry segments and geographic areas for 2015, 2014 and 2013 is provided in this Annual Report on Form 10-K in Item 8 (Financial Statements and Supplementary Data) under Note 14 (Operating Segment Information) to the Combined Financial Statements, which disclosure is incorporated herein by reference. Disclosure of risks attendant to our foreign operations is provided in this Report in Item 1A (Risk Factors).

12

BACKLOG OF ORDERS

While at any given time there may be some backlog of orders, backlog is not material in respect to our total annual sales, nor are the changes, from time to time, significant.

RESEARCH ACTIVITIES; INTELLECTUAL PROPERTY

We believe success in our industries is driven by technology and innovation. Growing our businesses and maintaining our margins depends on our ability to introduce new products based on innovative technology, as well as our ability to obtain patent or other intellectual property protection. Our research and development programs emphasize development of new products and processes, improvement of existing products and processes and application of existing products and processes to new industries and uses. The programs with the highest risk-adjusted impacts garner the necessary resources for success.

Our world-class Global Technology Center in Cambridge, Massachusetts houses the product research activities of all three of our operating segments. The global marketing resources that we believe are essential to a successful product development process are also located with our research and development group in Cambridge. Overall, we have approximately 65 research and development employees based in Cambridge, Massachusetts.

Technologies developed by our Global Technology Center are customized for the regions and supported in the field by a network of Regional Technical Centers. This includes facilities in Sorocaba, Brazil; Singapore; Beijing, China; Atsugi, Japan; Epernon, France; Lügde, Germany; Norderstedt, Germany; and Heist, Belgium. Across all three segments, there are over 300 research and development and technical service employees in our Regional Technical Centers. Globally we have close to 11% of our workforce focused on technology. We believe the collective technical expertise, industry knowledge and professionalism of this team is a significant differentiator for us.

We file and patent applications internationally on a routine basis and obtain grants in numerous countries around the world in support of our products, formulations, manufacturing processes, equipment and improvements. We also benefit from technological and commercial advantages protected under trade secret laws, including know-how and other proprietary information relating to many of our products, technologies and internal quality control and testing methodologies. Entering 2016, we have over 800 active patents and patent applications in a number of countries around the world, including approximately 150 in the U.S. During the past five years, we have averaged approximately 5-10 U.S. patent issuances per year, with similar results in other countries in which we have filed counterpart patent applications. The average number of patents filed and granted could go up or down from year to year, depending on various factors, some of which may not be within our control. It is our intent to continue to file for patents to protect our proprietary innovations and investments in research.

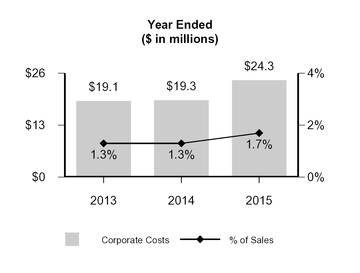

Research and development expenses were approximately $22.3 million in 2015, $27.9 million in 2014 and $24.3 million in 2013. These amounts include depreciation and amortization expenses related to research and development and expenses incurred in funding external research projects. The amount of research and development expenses relating to government -and customer- sponsored projects (rather than projects that we sponsor) was not material during these periods.

ENVIRONMENT, HEALTH AND SAFETY MATTERS

We are subject, along with other manufacturers of specialty chemicals, to stringent regulations under numerous U.S. federal, state and local and foreign environmental, health and safety laws and regulations relating to the generation, storage, handling, discharge, disposition and stewardship of hazardous wastes and other materials. Environmental laws require that certain responsible parties, as defined in the relevant statute, fund remediation actions regardless of legality of original disposal or ownership of a disposal site. We are involved in remediation actions to address hazardous wastes or other materials as required by U.S. federal, state and local and foreign laws.

We continuously seek to improve our environment, health and safety performance. We have expended funds to comply with environmental laws and regulations and expect to continue to do so in the future. The following table sets forth our expenditures in the past three years and our estimated expenditures in 2016 and 2017, for (i) environmental, health and safety (EH&S) operating costs and waste disposal; (ii) capital expenditures for EH&S related investments; and (iii) site remediation:

13

Year (In millions) | EH&S Operating Costs and Waste Disposal | Capital Expenditures | Site Remediation | ||||||||||

2013 | $ | 4.8 | $ | 1.9 | $ | 1.0 | |||||||

2014 | 4.8 | 2.4 | 0.6 | ||||||||||

2015 | 4.7 | 4.4 | 0.4 | ||||||||||

2016 | 4.9 | 4.6 | 0.2 | * | |||||||||

2017 | 5.2 | 5.0 | 0.1 | * | |||||||||

___________________________________________________________________________________________________________________

* | Amounts are based on site remediation matters for which sufficient information is available to estimate remediation costs. We do not have sufficient information to estimate all of our possible future remediation costs. As we receive new information, our estimate of remediation costs may change materially. |

EMPLOYEE RELATIONS

As of December 31, 2015, we had approximately 2,900 employees, of which approximately 680 were employed in the United States. Of our total employees, approximately 2,400 were salaried and 500 were hourly.

Approximately 85 of our manufacturing employees in the United States are represented for collective bargaining purposes by five different local collective bargaining groups. We have operated without a labor work stoppage for more than 10 years.

We have works councils representing the majority of our European sites serving approximately 150 employees.

AVAILABLE INFORMATION

We maintain an Internet website at www.gcpat.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, on our website as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the Securities and Exchange Commission, or "SEC." Further, the SEC's website, www.sec.gov, contains reports and other information regarding our filings or you may read and copy any materials that we file with the SEC at its Public Reference Room, located at 100 F Street, NE, Washington, DC 02549. These reports may be accessed through our website's investor relations page.

In addition, the charters for the Audit, Compensation, Nominating and Governance, and Corporate Responsibility Committees of our Board of Directors, our corporate governance guidelines and code of ethics are available, free of charge, on our website at http://investor.gcpat.com/corporate-governance/governance-documents. Printed copies of the charters, governance guidelines and code of ethics may be obtained free of charge by contacting GCP Shareholder Services at (617) 876-1400.The information on our website is not, and shall not be deemed to be, a part of this report or incorporated into any other filings we make with the SEC.

14

Item 1A. RISK FACTORS

Our operations are subject to a number of risks, including those listed below. When considering investments in our company, you should carefully consider each of the following risk factors and all of the other information set forth in this Annual Report on Form 10-K. The risk factors generally have been separated into three groups: (1) risks relating to our business, (2) risks relating to the Separation and (3) risks relating to the ownership of company common stock. Based on the information currently known to us, we believe that the following information identifies the most significant risk factors affecting the Company and our business in each of these categories of risks. However, the risks and uncertainties the Company faces are not limited to those set forth in the risk factors described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business. In addition, past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods.

If any of the following risks and uncertainties develops into actual events, these events could have a material adverse effect on our business, financial condition or results of operations. In such case or in the case that an additional risk or uncertainty not presently known to us or that we currently believe to be immaterial develops into actual events, the trading price of our common stock could decline.

Risks Relating to Our Business

We face significant competition and, if we are not able to respond to competition, our revenues may decrease.

We face significant competition from a variety of competitors in each of our markets. Some of our competitors have substantially greater financial, marketing, personnel and other resources than we do. New competitors also could enter our markets and certain of our customers could decide to self-manufacture or otherwise enter our markets. We consider product quality, performance, customer service, on-time delivery, price, distribution capabilities and breadth of product offerings to be the primary competitive factors in our markets. Our competitors may be able to offer more attractive pricing, duplicate our strategies, or develop enhancements to products that could offer performance features that are superior to our products. Competitive pressures, including those described above, could adversely affect our competitive position, leading to a loss of market share or decreases in prices, either of which could have a material adverse effect on our business, financial condition or results of operations.

The length and depth of product and industry business cycles in our segments may result in periods of reduced sales, earnings and cash flows, and portions of our business are subject to seasonality and weather-related effects.

Our operating segments are sensitive to the cyclical nature of the industries they serve. Our construction business is cyclical in response to economic conditions and construction demand and is also seasonal and dependent on favorable weather conditions, with a decrease in construction activity during the winter months. Our packaging products are affected by seasonal and weather-related factors including the consumption of beverages and the size and quality of food crops.

If we are not able to continue our technological innovation and successful introduction of new products, our customers may turn to other suppliers to meet their requirements.

The specialty chemicals industry and the end-use applications into which we sell our products experience ongoing technological change and product improvements. A key element of our business strategy is to invest in research and development activities with the goal of introducing new high-performance, technically differentiated products. We may not be successful in developing new technology and products that successfully compete with products introduced by our competitors, and our customers may not accept or may have lower demand for, our new products. If we fail to keep pace with evolving technological innovations or fail to improve our products in response to our customers’ needs, then our business, financial condition and results of operations could be adversely affected as a result of reduced sales of our products.

15

Prices for certain raw materials are volatile and can have a significant effect on our manufacturing and supply chain strategies as we seek to maximize our profitability. If we are unable to successfully adjust our strategies in response to volatile raw materials prices, such volatility could have a negative effect on our earnings in future periods.

We use petroleum-based materials, natural gas derivatives and other materials in the manufacture of our products. Prices for these materials are volatile and can have a significant effect on our pricing, sales, manufacturing and supply chain strategies as we seek to maximize our profitability. Our ability to successfully adjust strategies in response to volatile raw material prices by increasing prices, reducing costs or taking other actions is a significant factor in maintaining or improving our profitability. If we are unable to successfully adjust our strategies in response to volatile prices, such volatility could have a negative effect on our sales and earnings in future periods.

A substantial portion of our raw materials are commodities whose prices fluctuate as market supply and demand fundamentals change. We attempt to manage exposure to price volatility of major commodities through:

• | long-term supply contracts; |

• | customer contracts that permit adjustments for changes in prices of commodity-based materials and energy; and |

• | forward buying programs that layer in our expected requirements systematically over time; |

Although we regularly assess our exposure to raw material price volatility, we cannot always predict the prospects of volatility and we cannot always cover the risk in a cost-effective manner.

We have a policy of maintaining, when available, multiple sources of supply for raw materials. However, certain of our raw materials may be provided by single sources of supply. We may not be able to obtain sufficient raw materials due to unforeseen developments that would cause an interruption in supply. Even if we have multiple sources of supply for raw materials, these sources may not make up for the loss of a major supplier.

The global scope of our operations subjects us to the risks of doing business in foreign countries, which could adversely affect our business, financial condition and results of operations.

We operate our business on a global scale with approximately 64% of our 2015 sales outside the United States. We operate in over 40 countries and in over 30 currencies. We currently have many production facilities, technical centers and administrative and sales offices located outside North America, including facilities and offices in Europe, the Middle East, Africa, Asia Pacific and Latin America. We expect non-U.S. sales to continue to represent a substantial majority of our revenue. Accordingly, our business is subject to risks related to the differing legal, political, social and economic conditions as well as regulatory requirements of many jurisdictions. Risks inherent in non-U.S. operations include the following:

• | commercial agreements may be more difficult to enforce and receivables more difficult to collect; |

• | intellectual property rights may be more difficult to enforce; |

• | we may experience increased shipping costs, disruptions in shipping or reduced availability of freight transportation; |

• | we may have difficulty transferring our profits or capital from foreign operations to other countries where such funds could be more profitably deployed; |

• | we may experience unexpected adverse changes in export duties, quotas and tariffs and difficulties in obtaining export licenses; |

• | some foreign countries have adopted, and others may impose, additional withholding taxes or other restrictions on foreign trade or investment, including currency exchange and capital controls; |

• | foreign governments may nationalize private enterprises; |

16

• | our business and profitability in a particular country could be affected by political or economic repercussions on a domestic, country specific or global level from terrorist activities and the response to such activities; |

• | we may be affected by unexpected adverse changes in foreign laws or regulatory requirements; and |

• | unanticipated events, such as geopolitical changes, could adversely affect our foreign operations. |

Our success as a global business will depend, in part, upon our ability to succeed in differing legal, regulatory, economic, social and political conditions by developing, implementing and maintaining policies and strategies that are effective in each location where we do business.

In particular, our ability to manage our Venezuelan operations has been and will continue to be negatively affected by difficult conditions in Venezuela, including continuing high inflation and the significant devaluation of the Venezuelan bolivar. Government regulations regarding price increases limit our ability to offset the effects of high inflation and the currency devaluations. Import authorization controls and the limited availability of foreign exchange limit our ability to import raw materials needed for the production of our products. In addition, labor laws limit our ability to manage overhead costs and, at times, production has been negatively impacted by local labor issues. Additional government actions, including in the form of further currency devaluations or effective devaluations or continued or worsening import authorization controls, foreign exchange or price or profit controls could have further adverse impacts on our business, results of operations, cash flows and financial condition, as could further deterioration in the Venezuelan economy resulting from the decline in the price of oil or from other factors.

We have no assurance that we will be able to sustain operations in Venezuela. Economic factors as well as further government actions affecting our ability to do business (including the possibility of nationalization, expropriation of assets or other similar actions) could affect both our results of operations as well as our accounting presentation for the Venezuelan business. Specialty Construction Chemicals and Darex Packaging Technologies have operated in Venezuela for several decades with sales in that country representing approximately 8% of each segment’s sales in 2015. The future sales of our Venezuelan subsidiary are expected to be immaterial after September 30, 2015 due to Venezuela's currency devaluation.

For additional information regarding these and other risks associated with our operations in Venezuela, refer to the “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Certain of our customer relationships outside of the United States are with governmental entities and we could be materially and adversely affected by violations of the U.S. Foreign Corrupt Practices Act ("FCPA") and similar worldwide anti-bribery laws in non-U.S. jurisdictions.

The FCPA and similar worldwide anti-bribery laws in non-U.S. jurisdictions generally prohibit companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. Because certain of our customer relationships outside of the United States are with governmental entities, we are subject to such anti-bribery laws. Our policies mandate compliance with these anti-bribery laws. We operate in many parts of the world that have experienced governmental corruption to some degree, and in certain circumstances strict compliance with anti-bribery laws may conflict with local customs and practices. Despite our training and compliance programs our internal control policies and procedures may not always protect us from reckless or criminal acts committed by our employees or agents. Violations of anti-bribery laws or allegations of such violations, could disrupt our business and result in a material adverse effect on our results of operations, financial condition and cash flows.

17

We are exposed to currency exchange rate changes that impact our profitability.

We are exposed to currency exchange rate risk through our U.S. and non-U.S. operations. Changes in currency exchange rates may materially affect our operating results. For example, changes in currency exchange rates may affect the relative prices at which we and our competitors sell products in the same region and the cost of materials used in our operations. A substantial portion of our net sales and assets are denominated in currencies other than the U.S. dollar. When the U.S. dollar strengthens against other currencies, at a constant level of business, our reported sales, earnings, assets and liabilities are reduced because the non-U.S. currencies translate into fewer U.S. dollars. In addition, since we manufacture a portion of our construction products and packaging products in emerging regions using raw materials from suppliers in the U.S., Europe and other advanced economies, changes in the values of the currencies of these emerging regions versus the U.S. dollar, the euro and the currencies of other advanced economies in which we purchase raw materials, may adversely affect our raw material costs.

We incur a currency transaction risk whenever one of our operating subsidiaries enters into either a purchase or a sales transaction using a currency different from the operating subsidiary's functional currency. Given the volatility of exchange rates, we may not be able to manage our currency transaction risks effectively or volatility in currency exchange rates may expose our financial condition or results of operations to significant additional risk.

Following the Separation, we will have debt obligations that could restrict our business, adversely impact our financial condition, results of operations or cash flows or restrict our ability to return cash to shareholders.

As of December 31, 2015, we had $68.0 million of unsecured indebtedness outstanding. Immediately following the Separation, we had a total combined indebtedness for borrowed money of approximately $826 million, including approximately $750 million borrowed, in part, to pay a distribution to Grace prior to the Separation. The amount of and terms governing the Company's indebtedness may have material effects on our business, including to:

• | require us to dedicate a substantial portion of our cash flow to debt payments, thereby reducing funds available for working capital, capital expenditures, acquisitions, research and development, distributions to holders of company common stock and other purposes; |

• | restrict us from making strategic acquisitions or taking advantage of favorable business opportunities; |

• | limit our flexibility in planning for or reacting to, changes in our business and the industries in which we operate; |

• | increase our vulnerability to adverse economic, credit and industry conditions, including recessions; |

• | make it more difficult for us to satisfy our debt service and other obligations; |

• | place us at a competitive disadvantage compared to our competitors that have relatively less debt; and |

• | limit our ability to borrow additional funds or to dispose of assets to raise funds, if needed, for working capital, capital expenditures, acquisitions, research and development and other purposes. |

We may also incur substantial additional indebtedness in the future. If we incur additional debt, the risks related to our indebtedness may intensify.

18

We require liquidity to service the Company's debt and to fund operations, capital expenditures, research and development efforts, acquisitions and other corporate expenses.

Our ability to fund operations, capital expenditures, research and development efforts, acquisitions and other corporate expenses, including repayment of our debt, depends on our ability to generate cash through future operating performance, which is subject to economic, financial, competitive, legislative, regulatory and other factors. Many of these factors are beyond our control. We cannot be certain that our businesses will generate sufficient cash or that future borrowings will be available to us in amounts sufficient to fund all of our requirements. If we are unable to generate sufficient cash to fund all of our requirements, we may need to pursue one or more alternatives, such as to:

• | reduce or delay planned capital expenditures, research and development spending or acquisitions; |

• | obtain additional financing or restructure or refinance all or a portion of our debt on or before maturity; |

• | sell assets or businesses; and |

• | sell additional equity. |

Any reduction or delay in planned capital expenditures, research and development spending or acquisitions or sale of assets or businesses may materially and adversely affect our future revenue prospects. In addition, we cannot be certain that we will be able to raise additional equity capital, restructure or refinance any of our debt or obtain additional financing on commercially reasonable terms or at all.

Restrictions imposed by agreements governing our indebtedness may limit our ability to operate our business, finance our future operations or capital needs or engage in other business activities. If we fail to comply with certain restrictions under these agreements, our debt could be accelerated and the Company may not have sufficient cash to pay the accelerated debt.

The agreements governing our indebtedness may contain various covenants that we expect may limit, among other things, our ability, and the ability of certain of our subsidiaries, to:

• | incur certain liens; |

• | enter into sale and leaseback transactions; and |

• | consolidate, merge or sell all or substantially all of our assets or the assets of our guarantors. |

As a result of these covenants, we will be limited in the manner in which we can conduct our business, and may be unable to engage in favorable business activities or finance future operations or capital needs. Accordingly, these restrictions may limit our flexibility to operate our business. A failure to comply with the restrictions contained in these agreements, including maintaining the financial ratios that we expect to be required by our credit facilities, could lead to an event of default which could result in an acceleration of the indebtedness. We cannot assure you that our future operating results will be sufficient to enable us to comply with the covenants contained in the agreements that we expect to govern our indebtedness or to remedy any such default. In addition, in the event that repayment of our debt is accelerated pursuant to the terms of these agreements, we may not have or be able to obtain sufficient funds to make such accelerated payments.

Our indebtedness exposes us to interest expense increases if interest rates increase.

As of the Separation, we had approximately $301 million, or 36%, of our borrowings, at a variable interest rates and exposed us to interest rate risk. If interest rates increase, our debt service obligations on the variable rate indebtedness would increase even though the amount borrowed would remain the same, and our net income would decrease. An increase of 1% in the interest rates payable on the variable rate indebtedness at the time of the Separation and distribution would increase our annual estimated debt-service requirements by approximately $3 million, assuming our consolidated variable interest rate indebtedness outstanding as of the time of the Separation and distribution remains the same.

19

We have unfunded and underfunded pension plan liabilities. We will require future operating cash flow to fund these liabilities. We have no assurance that we will generate sufficient cash to satisfy these obligations.

We maintain U.S. and non-U.S. defined benefit pension plans covering current and former employees who meet or met age and service requirements. Our net pension liability and cost is materially affected by the discount rate used to measure pension obligations, the longevity and actuarial profile of our workforce, the level of plan assets available to fund those obligations and the actual and expected long-term rate of return on plan assets. Significant changes in investment performance or a change in the portfolio mix of invested assets can result in corresponding increases and decreases in the valuation of plan assets or in a change in the expected rate of return on plan assets. In addition, any changes in the discount rate could result in a significant increase or decrease in the valuation of pension obligations, affecting the reported funded status of our pension plans as well as the net periodic pension cost in the following years. Similarly, changes in the expected return on plan assets can result in significant changes in the net periodic pension cost in the following years.

When consistent with our business strategies, we intend to pursue acquisitions, joint ventures and other transactions that complement or expand our businesses. We may not be able to complete proposed transactions and even if completed, the transactions may not achieve the earnings, cash flow or returns on investment that we had contemplated.

We have recently completed a number of acquisitions that we believe will contribute to our future success. We intend to continue to pursue opportunities to buy other businesses or technologies that could complement, enhance or expand our current businesses or product lines or that might otherwise offer us growth opportunities. We may have difficulty identifying appropriate opportunities or, if we do identify opportunities, we may not be successful in completing transactions for a number of reasons. Any transactions that we are able to identify and complete may involve a number of risks, including:

• | the diversion of management's attention from our existing businesses to integrate the operations and personnel of the acquired or combined business or joint venture; |

• | possible adverse effects on our operating results during the integration process; |

• | failure of the acquired business to achieve expected operational objectives; and |

• | our possible inability to achieve the intended objectives of the transaction. |

In addition, we may not be able to successfully or profitably integrate, operate, maintain and manage our newly acquired operations or their employees. We may not be able to maintain uniform standards, controls, procedures and policies, which may lead to operational inefficiencies.

Our results of operations could be adversely affected by warranty claims and product liability.

We provide standard warranties that our products perform according to their specifications and do not have material defects. In particular, for a limited number of high value construction projects we warrant the performance of some products for periods of 10 to 20 years. Our products are generally sold to the commercial construction, residential construction and food packaging industries and they often constitute an integral part of our customers’ products. If our products do not meet specifications, are otherwise defective, or are used contrary to our instructions or in applications for which they are not designed, they may contribute to damage to our customers’ products, the end users of our customers’ products and buildings and other installations that contain our products. Although we take measures to avoid product defects and instruct our customers on the proper use of our products, if a substantial warranty claim or product liability lawsuit is brought against us, the cost of defending the claim or lawsuit could be significant and any adverse determination could have a material adverse effect on our results of operations.

We manufacture and sell products into many global jurisdictions where our efforts to contractually limit our liability (e.g. by defining a maximum liability, disclaiming implied or other statutory forms of liability or by waiving certain types of damages, including consequential, indirect and non-proximately caused damages) may not be enforceable or may be found by a court to not apply in a particular situation.

20

We work with dangerous materials that can injure our employees, damage our facilities and disrupt our operations.

Some of our operations involve the handling of hazardous materials that may pose the risk of fire, explosion or the release of hazardous substances. Such events could result from terrorist attacks, natural disasters or operational failures, and might cause injury or loss of life to our employees and others, environmental contamination, and property damage. These events might cause a temporary shutdown of an affected plant or portion thereof, and we could be subject to penalties or claims as a result. A disruption of our operations caused by these or other events could have a material adverse effect on our results of operations.

We may be required to spend large amounts of money for environmental compliance.

As a manufacturer of specialty chemicals and specialty materials, we are subject to stringent regulations under numerous U.S. federal, state, local and foreign environmental, health and safety laws and regulations relating to the generation, storage, handling, discharge, disposition and stewardship of hazardous wastes and other materials. We expend funds to comply with such laws and regulations and have established a policy to minimize our emissions to the environment. Nevertheless, legislative, regulatory and economic uncertainties (including existing and potential laws and regulations pertaining to climate change) make it difficult for us to project future spending for these purposes and if there is an acceleration in new regulatory requirements, we may be required to expend additional funds to remain in compliance.

Some of our employees are unionized, represented by works councils or employed subject to local laws that are less favorable to employers than the laws in the United States.

As of December 31, 2015, we had approximately 2,900 total employees, of which 680 were employed in the United States. Of our total U.S. employees, approximately 85 are unionized. In addition, a large number of our employees are employed in countries in which employment laws provide greater bargaining or other rights to employees than the laws in the United States. Such employment rights require us to work collaboratively with the legal representatives of the employees to effect any changes to labor arrangements. For example, most of our employees in Europe are represented by works councils that have co-determination rights on any changes in conditions of employment, including salaries and benefits and staff changes, and may impede efforts to restructure our workforce. A strike, work stoppage or slowdown by our employees or significant dispute with our employees, whether or not related to these negotiations, could result in a significant disruption of our operations or higher ongoing labor costs.

We may be subject to claims of infringement of the intellectual property rights of others, which could hurt our business or financial performance.