Attached files

| file | filename |

|---|---|

| EX-10.1 - EXHIBIT 10.1 - GCP Applied Technologies Inc. | a2017q110-qexhibit101.htm |

| EX-32 - EXHIBIT 32 - GCP Applied Technologies Inc. | a2017q110-qexhibit32.htm |

| EX-31.2 - EXHIBIT 31.2 - GCP Applied Technologies Inc. | a2017q110-qexhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - GCP Applied Technologies Inc. | a2017q110-qexhibit311.htm |

| EX-10.3 - EXHIBIT 10.3 - GCP Applied Technologies Inc. | a2017q110-qexhibit103.htm |

| EX-10.2 - EXHIBIT 10.2 - GCP Applied Technologies Inc. | a2017q110-qexhibit102.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Quarterly Period Ended March 31, 2017 | ||

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number 1-137533 | ||

GCP Applied Technologies Inc.

Delaware (State of Incorporation) | 47-3936076 (I.R.S. Employer Identification No.) | |

62 Whittemore Avenue, Cambridge, Massachusetts 02140-1623

(617) 876-1400

(Address and phone number of principal executive offices)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o | Emerging growth company o | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class | Outstanding at May 2, 2017 | |

Common Stock, $0.01 par value per share | 71,465,608 shares | |

TABLE OF CONTENTS | ||||

_______________________________________________________________________________

2

Presentation of Information

Unless the context requires otherwise, references to "GCP Applied Technologies Inc.", "GCP", "we", "us", "our" and "the Company" refer to GCP Applied Technologies Inc., and its consolidated subsidiaries for periods subsequent to its separation from W.R. Grace & Co. on February 3, 2016. For periods prior to February 3, 2016, these terms refer to the combined historical business and operations of W.R. Grace & Co.’s construction products and packaging technologies businesses as they were historically managed as part of W.R. Grace & Co. Unless the context requires otherwise, references to "Grace" refer to W.R. Grace & Co., and its consolidated subsidiaries, which is the Company’s former parent company. References in this Quarterly Report on Form 10-Q to the "Separation" refer to the legal separation and transfer of Grace’s construction products and packaging technologies businesses to the Company through a dividend distribution of all of the then-outstanding common stock of GCP to Grace shareholders on February 3, 2016.

Forward-Looking Statements

This document contains, and our other public communications may contain, forward-looking statements, that is, information related to future, not past, events. Such statements generally include the words "believes," "plans," "intends," "targets," "will," "expects," "suggests," "anticipates," "outlook," "continues" or similar expressions. Forward-looking statements include, without limitation, expected financial positions; results of operations; cash flows; financing plans; business strategy; operating plans; capital and other expenditures; competitive positions; growth opportunities for existing products; benefits from new technology and cost reduction initiatives, plans and objectives; and markets for securities. Like other businesses, we are subject to risks and uncertainties that could cause our actual results to differ materially from our projections or that could cause other forward-looking statements to prove incorrect. Factors that could cause actual events to materially differ from those contained in the forward-looking statements include, without limitation: risks related to foreign operations, especially in emerging regions; the cost and availability of raw materials and energy; the effectiveness of GCP's research and development and growth investments; acquisitions and divestitures of assets and gains and losses from dispositions; developments affecting GCP’s outstanding indebtedness; developments affecting GCP's funded and unfunded pension obligations; GCP's legal and environmental proceedings; uncertainties related to the Company’s ability to realize the anticipated benefits of the separation transaction; the inability to establish or maintain certain business relationships and relationships with customers and suppliers or the inability to retain key personnel; costs of compliance with environmental regulation, and those factors set forth in our most recent Annual Report on Form 10-K, this Quarterly Report on Form 10-Q and Current Reports on Form 8-K, which have been filed with the Securities and Exchange Commission ("SEC") and are available on the Internet at www.sec.gov. Our reported results should not be considered as an indication of our future performance. Readers are cautioned not to place undue reliance on our projections and forward-looking statements, which speak only as of the date thereof. We undertake no obligation to publicly release any revisions to the projections and forward-looking statements contained in this document, or to update them to reflect events or circumstances occurring after the date of this document.

3

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

GCP Applied Technologies Inc.

Consolidated Statements of Operations (unaudited)

Three Months Ended March 31, | |||||||

(In millions, except per share amounts) | 2017 | 2016 | |||||

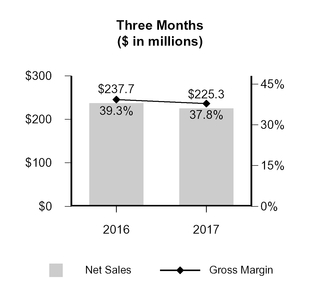

Net sales | $ | 225.3 | $ | 237.7 | |||

Cost of goods sold | 140.0 | 144.5 | |||||

Gross profit | 85.3 | 93.2 | |||||

Selling, general and administrative expenses | 72.8 | 63.4 | |||||

Research and development expenses | 4.8 | 4.1 | |||||

Interest expense and related financing costs | 17.0 | 12.5 | |||||

Repositioning expenses | 2.0 | 4.3 | |||||

Restructuring expenses | 1.1 | 0.9 | |||||

Other income (expense), net | 1.0 | (0.1 | ) | ||||

Total costs and expenses | 98.7 | 85.1 | |||||

(Loss) income from continuing operations before income taxes | (13.4 | ) | 8.1 | ||||

Provision for income taxes | (11.6 | ) | (1.7 | ) | |||

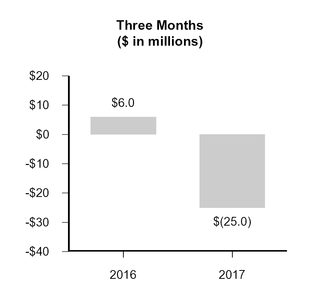

(Loss) income from continuing operations | (25.0 | ) | 6.4 | ||||

Income from discontinued operations, net of income taxes | 8.1 | 11.8 | |||||

Net (loss) income | (16.9 | ) | 18.2 | ||||

Less: Net income attributable to noncontrolling interests | — | (0.4 | ) | ||||

Net (loss) income attributable to GCP shareholders | $ | (16.9 | ) | $ | 17.8 | ||

Amounts Attributable to GCP Shareholders: | |||||||

(Loss) income from continuing operations attributable to GCP shareholders | (25.0 | ) | 6.0 | ||||

Income from discontinued operations, net of income taxes | 8.1 | 11.8 | |||||

Net (loss) income attributable to GCP shareholders | $ | (16.9 | ) | $ | 17.8 | ||

Earnings Per Share Attributable to GCP Shareholders | |||||||

Basic earnings per share: | |||||||

(Loss) income from continuing operations attributable to GCP shareholders | $ | (0.35 | ) | $ | 0.08 | ||

Income from discontinued operations, net of income taxes | $ | 0.11 | $ | 0.17 | |||

Net (loss) income attributable to GCP shareholders | $ | (0.24 | ) | $ | 0.25 | ||

Weighted average number of basic shares | 71.2 | 70.6 | |||||

Diluted earnings per share: | |||||||

(Loss) income from continuing operations attributable to GCP shareholders | $ | (0.35 | ) | $ | 0.08 | ||

Income from discontinued operations, net of income taxes | $ | 0.11 | $ | 0.17 | |||

Net (loss) income attributable to GCP shareholders | $ | (0.24 | ) | $ | 0.25 | ||

Weighted average number of diluted shares | 71.2 | 70.9 | |||||

The Notes to Consolidated Financial Statements are an integral part of these statements.

4

GCP Applied Technologies Inc.

Consolidated Balance Sheets (unaudited)

(In millions, except par value and shares) | March 31, 2017 | December 31, 2016 | |||||

ASSETS | |||||||

Current Assets | |||||||

Cash and cash equivalents | $ | 109.5 | $ | 146.1 | |||

Trade accounts receivable, less allowance of $4.6 (2016—$4.5) | 169.4 | 166.6 | |||||

Inventories | 101.3 | 89.3 | |||||

Other current assets | 53.1 | 42.9 | |||||

Current assets held for sale | 120.3 | 108.9 | |||||

Total Current Assets | 553.6 | 553.8 | |||||

Properties and equipment, net | 191.5 | 192.2 | |||||

Goodwill | 115.1 | 114.9 | |||||

Technology and other intangible assets, net | 51.0 | 52.6 | |||||

Deferred income taxes | 59.0 | 76.9 | |||||

Overfunded defined benefit pension plans | 22.0 | 21.2 | |||||

Other assets | 23.7 | 22.4 | |||||

Noncurrent assets held for sale | 61.8 | 55.8 | |||||

Total Assets | $ | 1,077.7 | $ | 1,089.8 | |||

LIABILITIES AND STOCKHOLDERS' (DEFICIT) EQUITY | |||||||

Current Liabilities | |||||||

Debt payable within one year | $ | 37.9 | $ | 47.9 | |||

Accounts payable | 104.7 | 95.4 | |||||

Other current liabilities | 96.9 | 119.5 | |||||

Current liabilities held for sale | 54.8 | 48.7 | |||||

Total Current Liabilities | 294.3 | 311.5 | |||||

Debt payable after one year | 782.7 | 783.0 | |||||

Deferred income taxes | 5.9 | 6.6 | |||||

Unrecognized tax benefits | 10.9 | 9.7 | |||||

Underfunded and unfunded defined benefit pension plans | 86.2 | 83.2 | |||||

Other liabilities | 13.8 | 13.9 | |||||

Noncurrent liabilities held for sale | 21.6 | 20.9 | |||||

Total Liabilities | 1,215.4 | 1,228.8 | |||||

Commitments and Contingencies - Note 7 | |||||||

Stockholders' (Deficit) Equity | |||||||

Common stock issued, par value $0.01; 300,000,000 shares authorized; outstanding: 71,450,751 | 0.7 | 0.7 | |||||

Paid-in capital | 17.2 | 11.0 | |||||

Accumulated deficit | (21.6 | ) | (4.7 | ) | |||

Accumulated other comprehensive loss | (135.0 | ) | (147.6 | ) | |||

Treasury stock | (3.0 | ) | (2.1 | ) | |||

Total GCP's Shareholders' (Deficit) Equity | (141.7 | ) | (142.7 | ) | |||

Noncontrolling interests | 4.0 | 3.7 | |||||

Total Stockholders' (Deficit) Equity | (137.7 | ) | (139.0 | ) | |||

Total Liabilities and Stockholders' (Deficit) Equity | $ | 1,077.7 | $ | 1,089.8 | |||

The Notes to Consolidated Financial Statements are an integral part of these statements.

5

GCP Applied Technologies Inc.

Consolidated Statements of Comprehensive Income (Loss) (unaudited)

Three Months Ended March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Net (loss) income | $ | (16.9 | ) | $ | 18.2 | ||

Other comprehensive income (loss): | |||||||

Currency translation adjustments | 12.6 | 3.9 | |||||

Loss from hedging activities, net of income taxes | — | (0.2 | ) | ||||

Total other comprehensive income attributable to noncontrolling interests | — | 0.2 | |||||

Total other comprehensive income | 12.6 | 3.9 | |||||

Comprehensive (loss) income | (4.3 | ) | 22.1 | ||||

Less: Comprehensive income attributable to noncontrolling interests | — | (0.6 | ) | ||||

Comprehensive (loss) income attributable to GCP shareholders | $ | (4.3 | ) | $ | 21.5 | ||

The Notes to Consolidated Financial Statements are an integral part of these statements.

6

GCP Applied Technologies Inc.

Consolidated Statements of Stockholders' Equity (Deficit) (unaudited)

Common Stock | Treasury Stock | ||||||||||||||||||||||||||||||||||||

(In millions) | Number of Shares | Par Value | Number of Shares | Cost | Additional Paid-in Capital | Accumulated Deficit | Net Parent Investment | Accumulated Other Comprehensive Loss | Noncontrolling Interests | Total Stockholders' Equity (Deficit) | |||||||||||||||||||||||||||

Balance, December 31, 2015 | — | $ | — | — | $ | — | $ | — | $ | — | $ | 598.3 | $ | (127.7 | ) | $ | 3.5 | $ | 474.1 | ||||||||||||||||||

Net income | — | — | — | — | — | 10.6 | 7.2 | — | 0.4 | 18.2 | |||||||||||||||||||||||||||

Net transfer to parent | — | — | — | — | — | — | (677.9 | ) | — | — | (677.9 | ) | |||||||||||||||||||||||||

Issuance of common stock and reclassification of net parent investment in connection with Separation | 70.5 | 0.7 | — | — | — | (73.1 | ) | 72.4 | — | — | — | ||||||||||||||||||||||||||

Issuance of common stock in connection with stock plans | 0.1 | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Share-based compensation | — | — | — | — | 0.7 | — | — | — | — | 0.7 | |||||||||||||||||||||||||||

Exercise of stock options | 0.2 | — | — | — | 0.6 | — | — | — | — | 0.6 | |||||||||||||||||||||||||||

Treasury stock purchased under GCP 2016 Stock Incentive Plan | — | — | 0.1 | (1.7 | ) | — | — | — | — | — | (1.7 | ) | |||||||||||||||||||||||||

Other comprehensive income | — | — | — | — | — | — | — | 3.7 | 0.2 | 3.9 | |||||||||||||||||||||||||||

Balance, March 31, 2016 | 70.8 | $ | 0.7 | 0.1 | $ | (1.7 | ) | $ | 1.3 | $ | (62.5 | ) | $ | — | $ | (124.0 | ) | $ | 4.1 | $ | (182.1 | ) | |||||||||||||||

Balance, December 31, 2016 | 71.2 | $ | 0.7 | 0.1 | $ | (2.1 | ) | $ | 11.0 | $ | (4.7 | ) | $ | — | $ | (147.6 | ) | $ | 3.7 | $ | (139.0 | ) | |||||||||||||||

Net loss | — | — | — | — | — | (16.9 | ) | — | — | — | (16.9 | ) | |||||||||||||||||||||||||

Issuance of common stock in connection with stock plans | 0.1 | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Share-based compensation | — | — | — | — | 2.1 | — | — | — | — | 2.1 | |||||||||||||||||||||||||||

Exercise of stock options | 0.3 | — | — | — | 4.1 | — | — | — | — | 4.1 | |||||||||||||||||||||||||||

Treasury stock purchased under GCP 2016 Stock Incentive Plan | — | — | — | (0.9 | ) | — | — | — | — | — | (0.9 | ) | |||||||||||||||||||||||||

Other comprehensive income | — | — | — | — | — | — | — | 12.6 | — | 12.6 | |||||||||||||||||||||||||||

Dividends and other changes in noncontrolling interest | — | — | — | — | — | — | — | — | 0.3 | 0.3 | |||||||||||||||||||||||||||

Balance, March 31, 2017 | 71.6 | $ | 0.7 | 0.1 | $ | (3.0 | ) | $ | 17.2 | $ | (21.6 | ) | $ | — | $ | (135.0 | ) | $ | 4.0 | $ | (137.7 | ) | |||||||||||||||

The Notes to Consolidated Financial Statements are an integral part of these statements.

7

GCP Applied Technologies Inc.

Consolidated Statements of Cash Flows (unaudited)

Three Months Ended March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

OPERATING ACTIVITIES | |||||||

Net (loss) income | $ | (16.9 | ) | $ | 18.2 | ||

Less: Income from discontinued operations | 8.1 | 11.8 | |||||

(Loss) income from continuing operations | (25.0 | ) | 6.4 | ||||

Reconciliation to net cash (used in) provided by operating activities: | |||||||

Depreciation and amortization | 8.4 | 7.4 | |||||

Amortization of debt discount and financing costs | 0.8 | 0.5 | |||||

Stock-based compensation expense | 2.1 | 1.1 | |||||

Currency and other losses in Venezuela | 0.1 | 0.1 | |||||

Deferred income taxes | 8.5 | (7.4 | ) | ||||

(Gain) loss on disposal of property and equipment | (0.8 | ) | 0.7 | ||||

Changes in assets and liabilities, excluding effect of currency translation: | |||||||

Trade accounts receivable | (0.4 | ) | (5.5 | ) | |||

Inventories | (12.7 | ) | (1.0 | ) | |||

Accounts payable | 16.7 | 7.3 | |||||

Pension assets and liabilities, net | 1.9 | 1.1 | |||||

Other assets and liabilities, net | (27.6 | ) | (2.5 | ) | |||

Net cash (used in) provided by operating activities from continuing operations | (28.0 | ) | 8.2 | ||||

Net cash provided by operating activities from discontinued operations | 14.3 | 16.3 | |||||

Net cash (used in) provided by operating activities | (13.7 | ) | 24.5 | ||||

INVESTING ACTIVITIES | |||||||

Capital expenditures | (12.7 | ) | (12.7 | ) | |||

Other investing activities | 2.9 | 0.1 | |||||

Net cash used in investing activities from continuing operations | (9.8 | ) | (12.6 | ) | |||

Net cash used in investing activities from discontinued operations | (2.4 | ) | (1.0 | ) | |||

Net cash used in investing activities | (12.2 | ) | (13.6 | ) | |||

FINANCING ACTIVITIES | |||||||

Borrowings under credit arrangements | 1.6 | 283.1 | |||||

Repayments under credit arrangements | (13.0 | ) | (9.1 | ) | |||

Proceeds from issuance of notes | — | 525.0 | |||||

Cash paid for debt financing costs | — | (18.2 | ) | ||||

Share repurchase under GCP 2016 Stock Incentive Plan | (0.9 | ) | (1.7 | ) | |||

Proceeds from exercise of stock options | 3.5 | 0.2 | |||||

Transfers to parent, net | — | (758.7 | ) | ||||

Net cash (used in) provided by financing activities from continuing operations | (8.8 | ) | 20.6 | ||||

Net cash provided by (used in) financing activities from discontinued operations | 0.4 | (5.8 | ) | ||||

Net cash (used in) provided by financing activities | (8.4 | ) | 14.8 | ||||

Effect of currency exchange rate changes on cash and cash equivalents | 2.8 | 2.4 | |||||

(Decrease) increase in cash and cash equivalents | (31.5 | ) | 28.1 | ||||

Cash and cash equivalents, beginning of period | 163.3 | 98.6 | |||||

Cash and cash equivalents, end of period | 131.8 | 126.7 | |||||

Less: Cash and cash equivalents of discontinued operations | 22.3 | 15.9 | |||||

Cash and cash equivalents of continuing operations, end of period | $ | 109.5 | $ | 110.8 | |||

The Notes to Consolidated Financial Statements are an integral part of these statements.

8

Notes to Consolidated Financial Statements

1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies

On January 27, 2016, GCP entered into a separation and distribution agreement pursuant to which W.R. Grace & Co. ("Grace") agreed to transfer its Grace Construction Products operating segment and the packaging technologies business, operated under the “Darex” name, of its Grace Materials Technologies operating segment to GCP (the "Separation"). The Separation occurred on February 3, 2016, by means of a pro rata distribution to Grace stockholders of all of the then-outstanding shares of Company common stock, at which time GCP became an independent public company and its common stock listed and began trading under the symbol "GCP" on the New York Stock Exchange.

GCP is engaged in the production and sale of specialty construction chemicals and specialty building materials through two operating segments. Specialty Construction Chemicals ("SCC") manufactures and markets concrete admixtures and cement additives. Specialty Building Materials ("SBM") manufactures and markets sheet and liquid membrane systems that protect structures from water, air and vapor penetration, fireproofing and other products designed to protect the building envelope.

On March 2, 2017, GCP announced the sale of its Darex Packaging Technologies ("Darex") business to Henkel AG & Co. KgaA (“Henkel”). As discussed further below under "Discontinued Operations," the results of operations for Darex have been excluded from continuing operations and segment results for all periods presented.

Basis of Presentation

The accompanying Consolidated Financial Statements are presented on a consolidated basis and include all of the accounts and operations of GCP and its majority-owned subsidiaries. The financial statements reflect the financial position, results of operations and cash flows of GCP in accordance with generally accepted accounting principles in the United States of America ("GAAP") and with the instructions to Form 10-Q and Article 10 of SEC Regulation S-X for interim financial information.

The interim financial statements presented herein are unaudited and should be read in conjunction with the Consolidated Financial Statements presented in the Company's 2016 Annual Report on Form 10-K. Such financial statements reflect all adjustments that, in the opinion of management, are necessary for a fair statement of the results of the interim periods presented; all such adjustments are of a normal recurring nature except for the impacts of adopting new accounting standards as discussed below. All significant intercompany accounts and transactions have been eliminated. The results of operations for the three-month period ended March 31, 2017 are not necessarily indicative of the results of operations for the year ending December 31, 2017.

Discontinued Operations As noted above, on March 2, 2017, the Company entered into a final, binding and irrevocable offer letter (the "Offer Letter") with Henkel, pursuant to which Henkel made a binding offer to acquire Darex for approximately $1.05 billion (the "Acquisition"). Pursuant to the terms of the Offer Letter, following the conclusion of statutory employee consultation processes in connection with the Acquisition by the relevant works councils in France, the Company accepted Henkel’s offer and countersigned the Stock and Asset Purchase Agreement (the “Purchase Agreement”) with respect to the Acquisition on April 28, 2017. The Purchase Agreement was previously executed by Henkel. Completion of the Acquisition remains subject to the satisfaction or waiver of customary closing conditions, including regulatory approvals.

In conjunction with this transaction and applicable GAAP, the assets and liabilities related to Darex have been reclassified and reflected as "held for sale" on the Consolidated Balance Sheets for all periods presented. Additionally, Darex has been reclassified and reflected as "discontinued operations" on the Consolidated Statements of Operations and Consolidated Statements of Cash Flows for all periods presented. Unless otherwise noted, the information throughout the Notes to the Consolidated Financial Statements pertains only to the continuing operations of GCP. Refer to Note 14 for further discussion of the Acquisition.

9

Use of Estimates The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the Consolidated Financial Statements, and the reported amounts of revenues and expenses for the periods presented. Actual amounts could differ from those estimates, and the differences could be material. Changes in estimates are recorded in the period identified. GCP's accounting measurements that are most affected by management's estimates of future events are:

•Contingent liabilities, which depend on an assessment of the probability of loss and an estimate of ultimate resolution cost, that may arise from circumstances such as legal disputes, environmental remediation, product liability claims, material commitments (refer to Note 7 to the Consolidated Financial Statements) and income taxes (refer to Note 4 to the Consolidated Financial Statements);

•Pension and postretirement liabilities that depend on assumptions regarding participant life spans, future inflation, discount rates and total returns on invested funds (refer to Note 5 to the Consolidated Financial Statements); and

•Realization values of net deferred tax assets, which depend on projections of future taxable income (refer to Note 4 to the Consolidated Financial Statements).

Reclassifications Certain amounts in prior period financial statements have been reclassified to conform to the current period presentation. Such reclassifications have not materially affected previously reported amounts.

Income Tax As a global enterprise, GCP is subject to a complex array of tax regulations and must make assessments of applicable tax law and judgments in estimating its ultimate income tax liability. Refer to Note 4 for details regarding estimates used in accounting for income tax matters including unrecognized tax benefits.

Stock-Based Compensation Expense Prior to the Separation, GCP was allocated stock-based compensation expense from Grace related to GCP employees receiving awards denominated in Grace equity instruments. In accordance with an employee matters agreement entered into between Grace and GCP on January 27, 2016 in connection with the Separation (the "Employee Matters Agreement"), previously outstanding stock-based compensation awards granted under Grace's equity compensation programs prior to the Separation and held by certain executives and employees of GCP and Grace were adjusted to reflect the impact of the Separation on these awards. To preserve the aggregate intrinsic value of these stock-based compensation awards, as measured immediately before and immediately after the Separation, each holder of Grace stock-based compensation awards generally received an adjusted award consisting of either (i) both a stock-based compensation award denominated in Grace equity as it existed subsequent to the Separation and a stock-based compensation award denominated in GCP equity or (ii) solely a stock-based compensation award denominated in the equity of the company at which the person was employed following the Separation. In the Separation, the determination as to which type of adjustment applied to a holder’s previously outstanding Grace award was based upon the type of stock-based compensation award that was to be adjusted and the date on which the award was originally granted under the Grace equity compensation programs prior to the Separation. Under the Employee Matters Agreement, GCP retains certain obligations related to all stock- and cash-settled stock-based compensation awards denominated in GCP equity, regardless of whether the holder is a GCP or Grace employee. Following the Separation, the Company records stock-based compensation expense for equity awards in accordance with authoritative accounting guidance.

Currency Translation Assets and liabilities of foreign subsidiaries (other than those located in countries with highly inflationary economies) are translated into U.S. dollars at current exchange rates, while revenues, costs and expenses are translated at average exchange rates during each reporting period. The resulting currency translation adjustments are included in accumulated other comprehensive loss in the Consolidated Balance Sheets. The financial statements of any subsidiaries located in countries with highly inflationary economies are remeasured as if the functional currency were the U.S. dollar; the remeasurement creates translation adjustments that are reflected in net income in the Consolidated Statements of Operations.

10

Effective January 1, 2010, GCP began to treat Venezuela as a highly inflationary economy. As a result, the functional currency of its Venezuelan subsidiary became the U.S. dollar; therefore, all translation adjustments are reflected in net income in the accompanying Consolidated Statements of Operations. Effective September 30, 2015, the Company began accounting for its results in Venezuela at the SIMADI rate. In mid-February 2016, changes to the currency exchange systems were announced that eliminated the SICAD exchange rate and replaced the name SIMADI rate with DICOM. The DICOM rate was 708 bolivars to one U.S. dollar at March 31, 2017, an increase of approximately 4.9% from the rate at December 31, 2016, resulting in an immaterial impact on income from continuing operations.

In March 2017, the Venezuelan government announced that a new exchange rate would be introduced to replace the DICOM rate, although further details have not been publicly announced. Management believes the new exchange rate would result in a further devaluation of the local currency and additional currency remeasurement losses in net income. At March 31, 2017, monetary net assets denominated in local currency within the Company's Venezuela subsidiary were $8.7 million, of which $5.0 million has been reflected as "held for sale" on the Consolidated Balance Sheet.

During the quarter ended March 31, 2017, except as discussed above, there were no material changes to the Company's significant accounting and financial reporting policies from those reflected in the Annual Report on Form 10-K for the year ended December 31, 2016.

Recently Issued Accounting Standards

Business Combinations

In January 2017, the FASB issued Accounting Standards Update ("ASU") 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business, which clarifies the definition of a business when evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The update provides that when substantially all the fair value of the assets acquired is concentrated in a single identifiable asset or a group of similar identifiable assets, the transaction does not involve a business. The standard is effective for the Company on January 1, 2018, with early application permitted for certain transactions. GCP will consider the provisions of this update in conjunction with qualifying transactions in periods subsequent to March 31, 2017, as applicable.

Goodwill

In January 2017, the FASB issued ASU 2017-04, Intangibles—Goodwill and Other (Topic 350). This ASU modifies the concept of impairment from the condition that exists when the carrying amount of goodwill exceeds its implied fair value to the condition that exists when the carrying amount of a reporting unit exceeds its fair value, which eliminates Step 2 from the goodwill impairment test. The standard is effective for the Company for annual or any interim goodwill impairment tests beginning on or after January 1, 2020. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017.

Revenue from Contracts with Customers

In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606). This update is intended to remove inconsistencies and weaknesses in revenue requirements; provide a more robust framework for addressing revenue issues; improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets; provide more useful information to users of financial statements through improved disclosure requirements; and simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer. The new requirements were to be effective for fiscal years beginning after December 15, 2016, and for interim periods within those fiscal years, with early adoption not permitted. In August 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers-Deferral of the Effective Date, deferring the effective date by one year but permitting adoption as of the original effective date. The revised standard allows for two methods of adoption: (a) full retrospective adoption, meaning the standard is applied to all periods presented, or (b) modified retrospective adoption, meaning the cumulative effect of applying the new standard is recognized as an adjustment to the opening retained earnings balance. The standard will be effective for the Company on January 1, 2018.

11

In addition to the expanded disclosures regarding revenue, this guidance may impact timing of revenue recognition in some arrangements with variable consideration or contracts for the sale of goods and services. GCP is currently evaluating the available transition methods and the potential impact of the standard on its Consolidated Financial Statements and related disclosures. Specifically, management has established a mutli-disciplinary project team to evaluate and implement Topic 606, and the project team is currently collecting information from key organizational stakeholders to identify revenue streams for focused individual contract analysis.

Leases

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which is intended to increase transparency and comparability among organizations by recognizing lease assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. The core principle of Topic 842 is that a lessee should recognize the assets and liabilities that arise from leases. A lessee should recognize in the statement of financial position a liability to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset for the lease term, including optional payments where they are reasonably certain to occur. The amendments in this update are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years, with early adoption permitted. GCP is currently evaluating the potential impact on its Consolidated Financial Statements and related disclosures.

Other new pronouncements issued but not effective until after March 31, 2017 are not expected to have a material impact on the Company's financial position, results of operations or liquidity.

Recently Adopted Accounting Standards

Pension and Other Postretirement Benefit Costs

In March 2017, the FASB issued ASU 2017-07, Compensation—Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, which changes certain presentation and disclosure requirements for employers that sponsor defined benefit pension and other postretirement benefit plans. The amendments in this ASU require entities to (1) report the service cost component of net periodic pension/postretirement benefit cost in the same line item or items as other compensation costs arising from services rendered by the pertinent employees during the period; (2) capitalize only the service cost component of net periodic pension/postretirement benefit cost (when applicable); and (3) present other components of net periodic pension/postretirement benefit cost separately from the service cost component and outside a subtotal of income from operations (if applicable). The standard is effective for the Company on January 1, 2018, with early adoption permitted as of January 1, 2017.

GCP elected to early adopt this standard in the first quarter of 2017 and has reflected only the service cost component of net periodic pension/postretirement benefit cost in "Cost of goods sold" and presented the other components of net periodic pension/postretirement benefit cost in "Other (income) expense, net," within the Consolidated Statements of Operations. In accordance with the standard, GCP utilized prior period footnote disclosures as a practical expedient to apply these retrospective presentation requirements and will prospectively apply the capitalization requirements. GCP's adoption of this standard did not have a material effect on the accompanying Consolidated Financial Statements.

Inventory

In July 2015, the FASB issued ASU 2015-11, Simplifying the Measurement of Inventory. The update requires that inventory be measured at the lower of cost or net realizable value for entities using first-in, first-out ("FIFO") or average cost methods. The new requirements are effective for fiscal years beginning after December 15, 2016, and for interim periods within those fiscal years, with early adoption permitted. GCP adopted this standard for the 2017 first quarter and there were no material effects on the accompanying Consolidated Financial Statements.

12

2. Inventories

Inventories are stated at the lower of cost or net realizable value. GCP determines cost using the FIFO methodology. Inventories presented on GCP's Consolidated Balance Sheets consisted of the following:

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Raw materials | $ | 35.9 | $ | 35.7 | |||

In process | 3.4 | 3.6 | |||||

Finished products and other | 62.0 | 50.0 | |||||

Total inventories | $ | 101.3 | $ | 89.3 | |||

Included above as "other" within "Finished products and other" are finished products purchased rather than produced by GCP of $12.7 million and $10.9 million as of March 31, 2017 and December 31, 2016, respectively.

3. Debt and Other Financial Instruments

Components of Debt

__________________________

(In millions) | March 31, 2017 | December 31, 2016 | |||||

9.5% Senior Notes due 2023, net of unamortized debt issuance costs of $7.1 at March 31, 2017 (2016—$7.3) | $ | 517.9 | $ | 517.7 | |||

Term Loan due 2022, net of unamortized discount of $2.3 and unamortized debt issuance costs of $4.1 at March 31, 2017 (1) (2016—$2.4, $4.3) | 265.9 | 266.2 | |||||

Revolving credit facility due 2021(2) | 15.0 | 25.0 | |||||

Other borrowings(3) | 21.8 | 22.0 | |||||

Total debt | 820.6 | 830.9 | |||||

Less debt payable within one year | 37.9 | 47.9 | |||||

Debt payable after one year | $ | 782.7 | $ | 783.0 | |||

Weighted average interest rates on total debt | 7.7 | % | 7.5 | % | |||

(1) | Interest at LIBOR +325 bps with a 75 bps LIBOR floor at March 31, 2017. |

(2) | Interest at LIBOR +200 bps at March 31, 2017. |

(3) | Represents borrowings under various lines of credit and other borrowings, primarily by non-U.S. subsidiaries. |

The principal maturities of debt outstanding (net of unamortized discounts and debt issuance costs) at March 31, 2017, were as follows:

(In millions) | |||

2017 | $ | 37.1 | |

2018 | 3.4 | ||

2019 | 3.4 | ||

2020 | 3.4 | ||

2021 | 2.8 | ||

Thereafter | 770.5 | ||

Total debt | $ | 820.6 | |

13

Credit Agreement

On February 3, 2016, GCP entered into a credit agreement (the “Credit Agreement”) that provides for senior secured credit facilities (the “Credit Facilities”) in an aggregate principal amount of $525.0 million, consisting of:

(a) | term loan (the “Term Loan”) in an aggregate principal amount of $275.0 million maturing in 2022; and |

(b) | $250.0 million revolving credit facility (the "Revolving Loan") due in 2021. |

The Term Loan principal balance is scheduled to be repaid in equal quarterly installments in aggregate annual amounts equal to 1.0% of the original principal amount, with the balance due upon the maturity date.

The Credit Agreement contains customary affirmative covenants, including, but not limited to (i) maintenance of legal existence and compliance with laws and regulations; (ii) delivery of consolidated financial statements and other information; (iii) payment of taxes; (iv) delivery of notices of defaults and certain other material events; and (v) maintenance of adequate insurance. The Credit Agreement also contains customary negative covenants, including but not limited to restrictions on (i) dividends on, and redemptions of, equity interests and other restricted payments; (ii) liens; (iii) loans and investments; (iv) the sale, transfer or disposition of assets and businesses; (vi) transactions with affiliates; and (vii) a maximum total leverage ratio. Certain debt covenants may restrict the entity's ability as it relates to dividends, acquisitions and other borrowings. The Credit Agreement contains conditions that would require mandatory principal payments in advance of the maturity date of the Term Loan and Revolving Credit Facility; the Company was in compliance with all terms as of March 31, 2017.

Events of default under the Credit Agreement include, but are not limited to: (i) failure to pay principal, interest, fees or other amounts under the Credit Agreement when due, taking into account any applicable grace period; (ii) any representation or warranty proving to have been incorrect in any material respect when made; (iii) failure to perform or observe covenants or other terms of the Credit Agreement subject to certain grace periods; (iv) a cross-default and cross-acceleration with certain other material debt; (v) bankruptcy events; (vi) certain defaults under ERISA; and (vii) the invalidity or impairment of security interests. There are no events of default as of March 31, 2017.

The Credit Facilities are secured on a first priority basis by a perfected security interest in, and mortgages on, substantially all tangible and intangible personal property and material fee-owned real property (specifically properties in Chicago, Illinois and Mount Pleasant, Tennessee) of the Company, a pledge of 100% of the equity of each material U.S. subsidiary of the Company and 65% of the equity of the United Kingdom holding company.

During 2016, GCP refinanced the existing Credit Agreement with a syndicate of banks (the “Amended Credit Agreement”). The Amended Credit Agreement reduced the interest rate margins applicable to the Term Loan from base rate plus a margin of 3.5% or LIBOR plus a margin of 4.5% to a base rate plus a margin of 2.25% or LIBOR plus a margin of 3.25% at GCP’s option. The outstanding principal balance was replaced by a like aggregate principal balance with substantially similar terms to the Credit Agreement.

The interest rate per annum applicable to the Revolving Loan is equal to, at GCP’s option, either a base rate plus a margin ranging from 0.5% to 1.0% or LIBOR plus a margin ranging from 1.5% to 2.0%, in either case based upon the total leverage ratio of GCP and its restricted subsidiaries. During 2016, GCP borrowed $25.0 million on its Revolving Loan and used the funds, together with cash on hand, to acquire Halex Corporation. Of the $25.0 million draw, $15.0 million was outstanding as of March 31, 2017 alongside approximately $9 million in outstanding letters of credit, which reduced available credit under that facility to $226.0 million.

The summary above of the Credit Agreement and Amended Credit Agreement does not purport to be complete and is qualified in its entirety by reference to the full text of such agreements, copies of which have been filed with the SEC.

Senior Notes

On January 27, 2016, GCP issued $525.0 million aggregate principal amount of 9.5% Senior Notes due 2023 (the “Notes”). Interest is payable semi-annually in arrears on February 1 and August 1 of each year.

14

The Notes were issued subject to covenants that limit the Company's and certain of its subsidiaries’ ability, subject to certain exceptions and qualifications, to (i) create or incur liens on assets, (ii) incur additional debt (iii) sell certain assets (iv) make certain investments and acquisitions, merge or sell or otherwise dispose of all or substantially all assets.

Divestiture of Darex

As discussed in Note 1, on March 2, 2017, the Company entered into the Offer Letter with Henkel, pursuant to which Henkel made a binding offer to acquire Darex for approximately $1.05 billion, subject to working capital and certain other adjustments. The proposed sale of Darex is a permitted transaction under the Company's Credit Agreement and the Indenture governing the Notes. Under the Credit Agreement and Indenture, the Company would be required to use any net cash proceeds from the proposed sale of Darex to prepay debt or make investments in its business over a period of approximately 18 months. Refer to Note 14 for further discussion of the proposed sale of Darex.

During 2016, GCP incurred debt issuance costs relating to issuance of the Notes, Term Loan, and Revolving Loan of $8.0 million, $5.0 million and $5.2 million, respectively. GCP deducted the debt issuance costs relating to the Notes and the Term Loan from the carrying amounts presented on its Consolidated Balance Sheet and is amortizing those costs over the terms of the underlying obligations.

GCP classified debt issuance costs relating to the Revolving Loan in "Other assets" on its Consolidated Balance Sheet and is amortizing those costs over the term of the Revolving Loan. The unamortized portion of these costs was $4.0 million as of March 31, 2017 and $4.2 million as of December 31, 2016.

During the first quarter of 2016, GCP used certain proceeds from the Notes and Credit Facilities to fund a distribution to Grace in an amount of $750.0 million related to the Separation. Approximately $50 million was retained to meet operating requirements and to pay fees associated with the debt financing and other costs of the Separation that may be incurred subsequent to the Separation. Related party debt of approximately $42 million and related interest was transferred from Grace to GCP in connection with the Separation.

Debt Fair Value

At March 31, 2017, the carrying amounts and fair values of GCP's debt were as follows:

March 31, 2017 | December 31, 2016 | ||||||||||||||

(In millions) | Carrying Amount | Fair Value | Carrying Amount | Fair Value | |||||||||||

9.5% Senior Notes due 2023 | $ | 517.9 | $ | 595.7 | $ | 517.7 | $ | 603.1 | |||||||

Term Loan due 2022 | 265.9 | 268.9 | 266.2 | 274.6 | |||||||||||

Revolving credit facility due 2021 | 15.0 | 15.0 | 25.0 | 25.0 | |||||||||||

Other borrowings | 21.8 | 21.8 | 22.0 | 22.0 | |||||||||||

Total debt | $ | 820.6 | $ | 901.4 | $ | 830.9 | $ | 924.7 | |||||||

Fair value is determined based on Level 2 inputs, including expected future cash flows (discounted at market interest rates), estimated current market prices and quotes from financial institutions. The decrease in fair value as of March 31, 2017 was due primarily to the Federal Reserve raising the federal funds target rate during the first quarter of 2017.

15

4. Income Taxes

The income tax provision on continuing operations for the three months ended March 31, 2017 and 2016 was $11.6 million and $1.7 million, respectively, representing effective tax rates of (86.6%) and 21.0%, respectively. The increase in the effective tax rate for the three month period of 107.6 percentage points compared to the same period in 2016 was primarily due to the recording of valuation allowances against certain U.S., Brazil, and Turkey deferred tax assets and a change in the Company’s assertion that it is indefinitely reinvested in Mexico, as further discussed below. The difference between the provision for income taxes at the U.S. federal income tax rate of 35% and GCP’s overall income tax rate is summarized below.

Three Months Ended March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Tax provision at U.S. federal income tax rate | $ | (4.7 | ) | $ | 2.8 | ||

Change in provision resulting from: | |||||||

Valuation allowance | 13.8 | — | |||||

Tax on undistributed foreign earnings | 1.9 | — | |||||

Effect of tax rates in foreign jurisdictions | 0.7 | (0.6 | ) | ||||

Permanent items and other | (0.1 | ) | (0.5 | ) | |||

Provision for income taxes | $ | 11.6 | $ | 1.7 | |||

For the three months ended March 31, 2017 and 2016, GCP recorded income tax expense on discontinued operations of $1.8 million and $5.9 million, respectively. Refer to Note 14 for further details.

As of December 31, 2016, GCP had the intent and ability to indefinitely reinvest undistributed earnings of its foreign subsidiaries outside the United States. During the first quarter of 2017, GCP determined it could no longer assert it is indefinitely reinvested in Mexico because that entity is anticipated to be sold as part of the Darex transaction. The tax associated with its outside book and tax basis difference in Mexico was recorded during the quarter as a discrete item resulting in a tax expense of $1.9 million. GCP believes that the anticipated sale of Darex is a one-time, non-recurring event and that recognition of deferred taxes of undistributed earnings during 2017 would not have occurred if not for the anticipated sale. As of March 31, 2017, GCP has the intent and ability to indefinitely reinvest undistributed earnings of all its other foreign subsidiaries outside the United States. Subsequent to the anticipated sale of Darex, GCP expects undistributed prior-year earnings of its foreign subsidiaries to remain indefinitely reinvested except in certain instances where repatriation of such earnings would result in minimal or no tax. GCP bases this assertion on:

(1) | the expectation that it will satisfy its U.S. cash obligations in the foreseeable future without requiring the repatriation of prior-year foreign earnings; |

(2) | plans for significant and continued reinvestment of foreign earnings in organic and inorganic growth initiatives outside the U.S.; and |

(3) | remittance restrictions imposed by local governments. |

GCP will continually analyze and evaluate its cash needs to determine the appropriateness of its indefinite reinvestment assertion.

16

In evaluating GCP's ability to realize its deferred tax assets, GCP considers all reasonably available positive and negative evidence, including recent earnings experience, expectations of future taxable income and the tax character of that income, the period of time over which the temporary differences become deductible and the carryforward and/or carryback periods available to GCP for tax reporting purposes in the related jurisdiction. In estimating future taxable income, GCP relies upon assumptions and estimates about future activities, including the amount of future federal, state and foreign pretax operating income that GCP will generate; the reversal of temporary differences; and the implementation of feasible and prudent tax planning strategies. GCP records a valuation allowance to reduce deferred tax assets to the amount that it believes is more likely than not to be realized. During the first quarter of 2017, GCP determined it is more likely than not a portion of its deferred tax assets will not be realized. As a result, GCP recorded valuation allowances on those deferred tax assets during the quarter as discrete items, as they are significant, unusual and infrequent in nature. The allowances recorded relate to $4.3 million of U.S. foreign tax credit carryovers and $9.1 million and $0.4 million of Brazil and Turkey deferred tax assets, respectively, relating primarily to net operating loss carryovers. The determination to record the valuation allowances in the first quarter was made predominantly due to the anticipated sale of Darex and its impact on future taxable income and the ability to utilize those tax assets.

As also discussed in Note 1, on February 3, 2016 the Separation of Grace and GCP was completed. In conjunction with the Separation, GCP increased its deferred tax assets and prepaid taxes in the U.S. by approximately $74 million, which primarily relates to the step up in tax basis and transfer of a net pension liability.

In connection with the Separation, GCP and Grace entered into various agreements that govern the relationship between the parties going forward, including a tax matters agreement (the "Tax Sharing Agreement"). Under the Tax Sharing Agreement, which was entered into on the distribution date, GCP and Grace will indemnify and hold each other harmless in accordance with the principles outlined therein.

During the first quarter of 2017, GCP reached a proposed favorable settlement with the Canada Revenue Agency for tax years 2007-2015. As a result of the proposed settlement, a tax benefit of $1.5 million, primarily for an anticipated refund of previously paid tax, was recorded during the quarter. GCP is required to pay Grace for the amount of the expected tax refund pursuant to the Tax Sharing Agreement in effect. GCP also recorded a charge to its U.S. deferred tax assets of $1.6 million related to the settlement due to the reduction of its step-up in tax basis. Both adjustments were recorded as discrete tax items.

5. Pension Plans and Other Postretirement Benefit Plans

Postretirement Benefits Other Than Pensions Prior to the Separation, Grace provided postretirement life insurance benefits for retired employees of certain U.S. business units and certain divested business units. GCP’s allocated income for these postretirement life insurance benefits plan was $1.2 million for the three months ended March 31, 2016. The postretirement life insurance benefits plan liability related to GCP employees who were participants in this plan at the time of Separation was legally transferred to GCP.

During the second half of 2016, GCP eliminated retiree life insurance benefits at the remaining bargaining locations and, as a result, did not recognize any related amounts in its Consolidated Statement of Operations for the three months ended March 31, 2017.

Pension Plans GCP sponsors certain defined benefit pension plans, primarily in the U.S. and the U. K. in which GCP employees participate. GCP records an asset or liability to recognize the funded status of these pension plans in its Consolidated Balance Sheets.

17

The following table presents the funded status of GCP's overfunded, underfunded and unfunded defined pension plans from continuing operations:

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Overfunded defined benefit pension plans | $ | 22.0 | $ | 21.2 | |||

Underfunded defined benefit pension plans | (57.7 | ) | (55.6 | ) | |||

Unfunded defined benefit pension plans | (28.5 | ) | (27.6 | ) | |||

Total underfunded and unfunded defined benefit pension plans | (86.2 | ) | (83.2 | ) | |||

Pension liabilities included in other current liabilities | (0.5 | ) | (0.4 | ) | |||

Net funded status | $ | (64.7 | ) | $ | (62.4 | ) | |

Overfunded plans include several advance-funded plans for which the fair value of the plan assets exceeds the projected benefit obligation ("PBO"). This group of plans was overfunded by $22.0 million as of March 31, 2017, and the overfunded status is reflected as assets in "Overfunded defined benefit pension plans" in the Consolidated Balance Sheets. Underfunded plans include a group of advance-funded plans that are underfunded on a PBO basis. Unfunded plans include several plans that are funded on a pay-as-you-go basis, and therefore, the entire PBO is unfunded. As of March 31, 2017, the combined balance of $86.7 million for the underfunded and unfunded plans included as liabilities in the Consolidated Balance Sheets is comprised of current and non-current components of $0.5 million in "Other current liabilities" and $86.2 million in "Underfunded and unfunded defined benefit pension plans," respectively.

Components of Net Periodic Benefit Cost (Income)

Three Months Ended March 31, | |||||||||||||||||||||||

2017 | 2016 | ||||||||||||||||||||||

Pension | Other Post Retirement | Pension | Other Post Retirement | ||||||||||||||||||||

(In millions) | U.S. | Non-U.S. | U.S. | Non-U.S. | |||||||||||||||||||

Service cost | $ | 1.9 | $ | 1.0 | $ | — | $ | 1.5 | $ | 0.9 | $ | — | |||||||||||

Interest cost | 1.5 | 1.5 | — | 1.2 | 2.1 | — | |||||||||||||||||

Expected return on plan assets | (1.4 | ) | (1.7 | ) | — | (1.2 | ) | (2.3 | ) | — | |||||||||||||

Amortization of prior service credit | — | — | — | — | — | (0.1 | ) | ||||||||||||||||

Net periodic benefit cost (income)(1) | $ | 2.0 | $ | 0.8 | $ | — | $ | 1.5 | $ | 0.7 | $ | (0.1 | ) | ||||||||||

Less: Discontinued operations | — | 0.2 | — | — | 0.3 | — | |||||||||||||||||

Net periodic benefit cost (income) from continuing operations | $ | 2.0 | $ | 0.6 | $ | — | $ | 1.5 | $ | 0.4 | $ | (0.1 | ) | ||||||||||

(1) | Includes expense that was allocated to Grace of $0.1 million for the three months ended March 31, 2016. |

Plan Contributions and Funding GCP intends to satisfy its funding obligations under the U.S. qualified pension plans and to comply with all of the requirements of the Employee Retirement Income Security Act of 1974, as amended ("ERISA"). For ERISA purposes, funded status is calculated on a different basis than under GAAP.

GCP intends to fund non-U.S. pension plans based on applicable legal requirements as well as actuarial and trustee recommendations.

Defined Contribution Retirement Plan As part of the Separation, GCP established a defined contribution retirement plan for its employees in the U.S. This plan is qualified under section 401(k) of the U.S. tax code. Currently, GCP contributes an amount equal to 100% of employee contributions, up to 6% of an individual employee's salary or wages. GCP's costs included in selling, general and administrative expenses related to this benefit plan for the three months ended March 31, 2017 were $1.4 million, compared with GCP's allocation of the total cost related to this benefit plan for the three months ended March 31, 2016 of $1.0 million.

18

6. Other Balance Sheet Accounts

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Other Current Assets: | |||||||

Non-trade receivables | $ | 19.0 | $ | 19.9 | |||

Income tax receivable | 18.0 | 10.6 | |||||

Prepaid and other | 16.1 | 12.4 | |||||

Total other current assets | $ | 53.1 | $ | 42.9 | |||

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Other Current Liabilities | |||||||

Customer volume rebates | $ | 21.7 | $ | 30.5 | |||

Accrued compensation(1) | 20.0 | 28.0 | |||||

Income tax payable | 5.3 | 6.7 | |||||

Accrued interest | 8.3 | 20.8 | |||||

Pension liabilities | 0.5 | 0.4 | |||||

Other accrued liabilities | 41.1 | 33.1 | |||||

Total other current liabilities | $ | 96.9 | $ | 119.5 | |||

(1) | Accrued compensation in the table above includes salaries and wages as well as estimated current amounts due under the annual and long-term incentive programs. |

7. Commitments and Contingent Liabilities

Purchase Commitments GCP uses purchase commitments to ensure supply and to minimize the volatility of certain key raw materials including lignins, polycarboxylates, amines and other materials. Such commitments are for quantities that GCP fully expects to use in its normal operations.

Guarantees and Indemnification Obligations GCP is a party to many contracts containing guarantees and indemnification obligations. These contracts primarily consist of:

• | Product warranties with respect to certain products sold to customers in the ordinary course of business. These warranties typically provide that products will conform to specifications. GCP accrues a general warranty liability at the time of sale based on historical experience and on a transaction-specific basis according to individual facts and circumstances. Both the liability and annual expense related to product warranties are immaterial to the Consolidated Financial Statements. |

• | Performance guarantees offered to customers. GCP has not established a liability for these arrangements based on past performance. |

• | Contracts providing for the sale of a former business unit or product line in which GCP has agreed to indemnify the buyer against liabilities arising prior to the closing of the transaction, including environmental liabilities. |

• | The Tax Sharing Agreement, which may require GCP, in certain circumstances, to indemnify Grace if the Separation, together with certain related transactions, does not qualify under Section 355 and certain other relevant provisions of the Internal Revenue Code (the "Code"). If GCP is required to indemnify Grace under the Tax Sharing Agreement, it could be subject to significant tax liabilities. |

19

Environmental Matters GCP is subject to loss contingencies resulting from extensive and evolving federal, state, local and foreign environmental laws and regulations relating to the generation, storage, handling, discharge, disposition and stewardship of hazardous wastes and other materials. GCP accrues for anticipated costs associated with response efforts where an assessment has indicated that a probable liability has been incurred and the cost can be reasonably estimated. As of March 31, 2017, GCP did not have any material environmental liabilities.

GCP's environmental liabilities are reassessed whenever circumstances become better defined or response efforts and their costs can be better estimated. These liabilities are evaluated based on currently available information, including the progress of remedial investigations at each site, the current status of discussions with regulatory authorities regarding the method and extent of remediation at each site, existing technology, prior experience in contaminated site remediation and the apportionment of costs among potentially responsible parties.

Financial Assurances Financial assurances have been established for a variety of purposes, including insurance and environmental matters and other matters. At March 31, 2017, GCP had gross financial assurances issued and outstanding of approximately $9 million, composed of standby letters of credit.

Lawsuits and Investigations In Re: Library Gardens Balcony Litigation, Lead Case Beary v. Blackrock, Inc. Case No. RG15793054 was filed on November 12, 2015 in Alameda County Superior Court in California. It is the lead case in a consolidated lawsuit filed on behalf of six individuals who died and an additional seven individuals who were injured in a balcony collapse, which occurred on June 16, 2015 in Berkeley, California. The consolidated complaint names the Company as the sole party in the category of suppliers of materials and names twenty additional defendants in other categories, including categories for property owners, property managers, construction defendants, and development and design defendants. The consolidated complaint alleges product liability against the Company concerning one of its products. The plaintiffs seek unspecified monetary damages against all defendants and punitive damages only against the building owners, building manager and two construction company defendants. Discovery is ongoing and the trial date has been set for February 5, 2018. The Company intends to defend this action vigorously. At this time, based on available information regarding this litigation, the Company is unable to reasonably assess the ultimate outcome of this matter or determine an estimate, or a range of estimates, of potential losses, if any, that might result from an adverse resolution of this matter.

In addition to the above, from time to time, GCP and its subsidiaries are parties to, or targets of, lawsuits, claims, investigations and proceedings which are managed and defended in the ordinary course of business. While GCP is unable to predict the outcome of these matters, it does not believe, based upon currently available facts, that the ultimate resolution of any of such pending matters will have a material adverse effect on its overall financial condition, results of operations or cash flows.

Accounting for Contingencies Although the outcome of each of the matters discussed above cannot be predicted with certainty, GCP has assessed its risk and has made accounting estimates and disclosures as required under GAAP.

8. Restructuring and Repositioning Expenses

Restructuring Expenses

GCP's Board of Directors approves all major restructuring programs that may involve the discontinuance of significant product lines or the shutdown of significant facilities. From time to time, GCP takes additional restructuring actions, including involuntary terminations that are not part of a major program. GCP accounts for these costs, which are reflected in "Restructuring expenses" in its Consolidated Statements of Operations, in the period that the related liabilities are incurred. Restructuring expenses are excluded from segment operating income.

For the first quarter of 2017, GCP incurred $1.1 million ($0.8 million in SCC and $0.3 million in SBM) of restructuring expenses, which were comprised primarily of severance-related costs associated with the Separation, as well as costs related to plant closures. For the prior-year quarter, GCP incurred $0.9 million ($0.5 million in SCC and $0.4 million in SBM) of restructuring expenses related to the Separation.

20

GCP had restructuring liabilities of $1.6 million as of March 31, 2017 and $1.1 million as of December 31, 2016 primarily related to severance actions taken during the periods. GCP expects to pay substantially all costs related to its current restructuring programs by December 31, 2017.

Restructuring Liability (In millions) | Total | ||

Balance, December 31, 2016 | $ | 1.1 | |

Accruals for severance | 0.8 | ||

Payments | (0.3 | ) | |

Balance, March 31, 2017 | $ | 1.6 | |

Repositioning Expenses

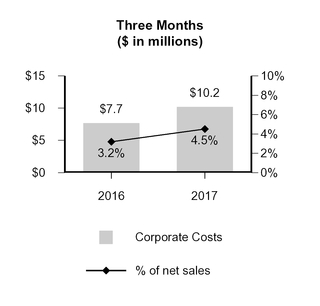

Post-Separation, GCP has incurred expenses related to its transition to a stand-alone public company. The Company expects to incur these repositioning expenses, ranging from $18.0 million to $20.0 million, by the end of the second quarter of 2017. Repositioning expenses primarily relate to the following:

• | accounting, tax, legal and other professional costs pertaining to the Separation and establishment as a stand-alone public company; |

• | costs relating to information technology systems and marketing expense for repackaging and re-branding; |

• | employee-related costs that would not be incurred absent the Separation primarily relating to compensation, benefits, retention bonuses related to new or transitioning employees; and |

• | recruitment and relocation costs associated with hiring and relocating employees. |

Due to the scope and complexity of these activities, the range of estimated repositioning expenses could increase or decrease and the timing of incurrence could change.

For the three months ended March 31, 2017, GCP incurred repositioning expenses as follows:

Three Months Ended March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Professional fees | $ | 1.4 | $ | 2.1 | |||

Software and IT implementation fees | 0.3 | — | |||||

Employee-related costs | 0.3 | 2.2 | |||||

Total | $ | 2.0 | $ | 4.3 | |||

GCP accounts for these costs, which are reflected in "Repositioning expenses" in the accompanying Consolidated Statements of Operations, in the period incurred. Substantially all of these costs have been or are expected to be settled in cash. Total cash payments for the three months ended March 31, 2017 were $1.1 million for repositioning expenses and $0.8 million for related capital expenditures.

21

9. Other Comprehensive Income

The following tables present the pre-tax, tax and after-tax components of GCP's other comprehensive income for the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, 2017 (In millions) | Pre-Tax Amount | Tax (Expense)/ Benefit | After-Tax Amount | ||||||||

Currency translation adjustments | $ | 12.6 | — | $ | 12.6 | ||||||

Other comprehensive income attributable to GCP shareholders | $ | 12.6 | $ | — | $ | 12.6 | |||||

Three Months Ended March 31, 2016 (In millions) | Pre-Tax Amount | Tax (Expense)/ Benefit | After-Tax Amount | ||||||||

Defined benefit pension and other postretirement plans: | |||||||||||

Amortization of net prior service cost included in net periodic benefit cost | $ | (0.1 | ) | $ | — | $ | (0.1 | ) | |||

Assumption of net prior service credit | 1.2 | (0.4 | ) | 0.8 | |||||||

Assumption of net actuarial loss | (1.1 | ) | 0.4 | (0.7 | ) | ||||||

Benefit plans, net | — | — | — | ||||||||

Currency translation adjustments | 3.9 | — | 3.9 | ||||||||

Loss from hedging activities | (0.2 | ) | — | (0.2 | ) | ||||||

Other comprehensive income attributable to GCP shareholders | $ | 3.7 | $ | — | $ | 3.7 | |||||

The following tables present the changes in accumulated other comprehensive income (loss), net of tax, for the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, 2017 (In millions) | Defined Benefit Pension and Other Postretirement Plans | Currency Translation Adjustments | Gains (Losses) from Hedging Activities | Total | |||||||||||

Beginning balance | $ | 0.1 | $ | (147.7 | ) | $ | — | $ | (147.6 | ) | |||||

Other comprehensive income before reclassifications | — | 12.6 | 0.1 | 12.7 | |||||||||||

Amounts reclassified from accumulated other comprehensive income | — | — | (0.1 | ) | (0.1 | ) | |||||||||

Net current-period other comprehensive income | — | 12.6 | — | 12.6 | |||||||||||

Ending balance | $ | 0.1 | $ | (135.1 | ) | $ | — | $ | (135.0 | ) | |||||

Three Months Ended March 31, 2016 (In millions) | Defined Benefit Pension and Other Postretirement Plans | Currency Translation Adjustments | Gains (Losses) from Hedging Activities | Total | |||||||||||

Beginning balance | $ | 0.1 | $ | (127.8 | ) | $ | — | $ | (127.7 | ) | |||||

Other comprehensive income (loss) before reclassifications | 0.1 | 3.9 | (0.5 | ) | 3.5 | ||||||||||

Amounts reclassified from accumulated other comprehensive income (loss) | (0.1 | ) | — | 0.3 | 0.2 | ||||||||||

Net current-period other comprehensive income (loss) | — | 3.9 | (0.2 | ) | 3.7 | ||||||||||

Ending balance | $ | 0.1 | $ | (123.9 | ) | $ | (0.2 | ) | $ | (124.0 | ) | ||||

22

GCP is a global enterprise operating in over 35 countries with local currency generally deemed to be the functional currency for accounting purposes. The currency translation adjustments reflect translation of the balance sheets valued in local currencies to the U.S. dollar as of the end of each period presented, and translation of revenues and expenses at average exchange rates for each period presented.

10. Stock Incentive Plans

GCP has provided certain key employees equity awards in the form of stock options, performance-based units (“PBUs”) and restricted share units (“RSUs”) under the GCP 2016 Stock Incentive Plan, which was adopted at Separation. Certain employees and members of the Board of Directors are eligible to receive stock-based compensation, including stock, stock options, RSUs and PBUs.

Total cash and non-cash stock-based compensation cost included in "(Loss) income from continuing operations before income taxes" on the Consolidated Statements of Operations is $2.7 million and $1.1 million for the three months ended March 31, 2017 and 2016, respectively.

During 2016, previously outstanding stock-based compensation awards granted under Grace’s equity compensation programs prior to the Separation were adjusted to reflect the impact of the Separation. To preserve the aggregate intrinsic value of those Grace awards, as measured immediately before and immediately after the Separation, each holder of Grace stock-based compensation awards generally received an adjusted award consisting of either (i) both a stock-based compensation award denominated in Grace equity as it existed subsequent to the Separation and a stock-based compensation award denominated in GCP equity or (ii) solely a stock-based compensation award denominated in the equity of the company at which the person was employed following the Separation. Adjusted awards consisting of stock-based compensation awards denominated in GCP equity are considered issued under the GCP 2016 Stock Incentive Plan. These adjusted awards generally will be subject to the same vesting conditions and other terms that applied to the original Grace awards before the Separation.

Under the Employee Matters Agreement, GCP is obligated to settle all of the stock-based compensation awards denominated in GCP equity, regardless of whether the holders are employees of GCP or Grace. Likewise, Grace is obligated to settle all of the stock-based compensation awards denominated in Grace shares, regardless of whether the holders are employees of GCP or Grace. As a result, GCP has recorded a liability for cash-settled awards held by Grace employees. The adjustment of the original Grace awards that resulted in the issuance of GCP stock-based compensation awards resulted in an immaterial charge in the first quarter of 2016.

In accordance with certain provisions of the GCP 2016 Stock Incentive Plan, GCP repurchases shares issued to certain holders of GCP awards in order to fulfill statutory tax withholding requirements for the employee. In the three months ended March 31, 2017 and 2016, GCP repurchased approximately 33,000 and 84,000 shares respectively, under these provisions. These purchases are reflected as "Treasury stock purchased under 2016 Stock Incentive Plan" in the Consolidated Statements of Equity (Deficit).

As of March 31, 2017, 656,205 shares of common stock were available for issuance under the GCP 2016 Stock Incentive Plan.

Stock Options

Stock options are non-qualified and are set at exercise prices not less than 100% of the market value on the date of grant (market value is the average of the high price and low price from that trading day). Stock option awards that relate to Grace stock options originally granted prior to the Separation have a contractual term of five years from the original date of grant. Stock option awards granted post-Separation have a contractual term of seven or ten years from the original date of grant. Generally, stock options vest in substantially equal amounts each year over three years from the date of grant.

23

GCP values stock options using the Black-Scholes option pricing model, which was developed for use in estimating the fair value of traded options. The risk-free rate is based on the U.S. Treasury yield curve published as of the grant date, with maturities approximating the expected term of the options. GCP estimates the expected term of the options according to the simplified method as allowed by FASB Accounting Standards Codification ("ASC") Topic No. 718-20, Awards Classified as Equity, whereby the average between the vesting period and contractual term is used. GCP estimated the expected volatility using an industry peer group.

The following summarizes GCP's assumptions for estimating the fair value of stock options granted during 2017:

Assumptions used to calculate expense for stock option | Three Months Ended March 31, 2017 |

Risk-free interest rate | 1.95 - 2.10% |

Average life of options (years) | 5.5 - 6.5 |

Volatility | 31.42 - 31.96% |

Dividend yield | — |

Average fair value per stock option | $9.13 |

The following table summarizes GCP stock option activity for the three months ended March 31, 2017:

Stock Option Activity | Number Of Shares (in thousands) | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term (years) | Aggregated Intrinsic Value (in thousands) | ||||||||

Outstanding, December 31, 2016 | 2,122 | $ | 16.92 | 3.57 | $ | 20,748 | ||||||

Options exercised | 325 | 12.73 | ||||||||||

Options forfeited/expired/canceled | 4 | 18.79 | ||||||||||

Options granted | 235 | 26.40 | ||||||||||

Outstanding, March 31, 2017 | 2,028 | 18.69 | 4.07 | 28,863 | ||||||||

Exercisable March 31, 2017 | 814 | $ | 17.05 | 2.89 | $ | 5,776 | ||||||

The aggregate intrinsic values in the table above represent the total pre-tax intrinsic value (the difference between GCP's closing stock price on the last trading day of March 31, 2017 and the exercise price, multiplied by the number of in-the-money options) that would have been received by the option holders had all option holders exercised their in-the-money options at period end. The amount changes based on the fair market value of GCP's stock. The intrinsic value of all options exercised in the three-month period ended March 31, 2017 was $12.9 million.

Total unrecognized stock-based compensation expense for stock options outstanding at March 31, 2017, was $3.0 million and the weighted-average period over which this expense will be recognized is approximately 1.2 years.

Restricted Stock Units and Performance Based Units

Upon Separation, certain previously outstanding RSUs and PBUs granted under Grace's equity compensation programs prior to the Separation were adjusted, in accordance with the Employee Matters Agreement, such that holders of these original Grace RSUs and PBUs received RSUs denominated in GCP equity.

RSUs generally vest over a three year period, with vesting in substantially equal amounts each year over three years and some vesting 100% after the third year from the date of grant. A smaller number of RSUs were designated as sign-on awards and used for purposes of attracting key employees and to cover outstanding awards from a prior employer and vest 100% after two years.

24

GCP’s RSU activity for the three months ended March 31, 2017 is as follows:

RSU Activity | Number Of Shares (in thousands) | Weighted Average Grant Date Fair Value | ||||

Outstanding, December 31, 2016 | 538 | $ | 17.22 | |||

RSUs settled | 112 | 17.17 | ||||

RSUs forfeited | 1 | 16.90 | ||||

RSUs granted | 93 | 26.34 | ||||

RSUs outstanding, March 31, 2017 | 518 | $ | 18.86 | |||

During the three months ended March 31, 2017, GCP distributed 79,134 shares and $0.9 million of cash to settle RSUs. GCP's expectations of future RSU vesting and settlement are as follows: