Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Corvus Gold Inc. | exh_322.htm |

| EX-32.1 - EXHIBIT 32.1 - Corvus Gold Inc. | exh_321.htm |

| EX-31.2 - EXHIBIT 31.2 - Corvus Gold Inc. | exh_312.htm |

| EX-31.1 - EXHIBIT 31.1 - Corvus Gold Inc. | exh_311.htm |

| EX-23.4 - EXHIBIT 23.4 - Corvus Gold Inc. | exh_234.htm |

| EX-23.3 - EXHIBIT 23.3 - Corvus Gold Inc. | exh_233.htm |

| EX-23.2 - EXHIBIT 23.2 - Corvus Gold Inc. | exh_232.htm |

| EX-23.1 - EXHIBIT 23.1 - Corvus Gold Inc. | exh_231.htm |

| EX-21.1 - EXHIBIT 21.1 - Corvus Gold Inc. | exh_211.htm |

| EX-4.1 - EXHIBIT 4.1 - Corvus Gold Inc. | exh_41.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended May 31, 2020 | ||

| OR | ||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

| Commission file number: 000-55447 |

![]()

CORVUS GOLD INC.

(Exact Name of Registrant as Specified in its Charter)

| British Columbia, Canada | 98-0668473 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

1750 -700 West Pender Street (Address of Principal Executive Offices) |

V6C 1G8 (Zip code) |

|

Registrant’s telephone number, including area code: (604) 638-3246 | |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Trading Symbol | Name of each exchange on which registered: | ||

| Common Shares, no par value | KOR | Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☒ | |

| Non-Accelerated Filer ☐ | Small Reporting Company ☒ | |

| Emerging Growth Company ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $80,521,510

As of August 13, 2020, the registrant had 123,987,845 Common Shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

To the extent specifically referenced in Part III, portions of the registrant’s definitive Proxy Statement on Schedule 14A to be filed with the Securities and Exchange Commission in connection with the registrant’s 2020 Annual Meeting of Shareholders are incorporated by reference into this report. See Part III.

Table of Contents

CAUTIONARY NOTE TO U.S. INVESTORS REGARDING ESTIMATES OF MEASURED, INDICATED AND INFERRED RESOURCES AND PROVEN AND PROBABLE RESERVES

The mineral estimates in this Annual Report on Form 10-K have been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. As used in this Annual Report on Form 10-K, the terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101 “Standards of Disclosure for Mineral Projects” (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) CIM Definition Standards on mineral resources and mineral reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in the United States Securities and Exchange Commission (“SEC”) Industry Guide 7 (“SEC Industry Guide 7”). Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves, and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that all or any part of a mineral deposit in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all, or any part, of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this report and the documents incorporated by reference herein contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

The term “mineralized material” as used in this Annual Report on Form 10-K, although permissible under SEC Industry Guide 7, does not indicate “reserves” by SEC Industry Guide 7 standards. We cannot be certain that any part of the mineralized material will ever be confirmed or converted into SEC Industry Guide 7 compliant “reserves”. Investors are cautioned not to assume that all or any part of the mineralized material will ever be confirmed or converted into reserves or that mineralized material can be economically or legally extracted.

The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC. These amendments became effective February 25, 2019 (the “SEC Modernization Rules”) and, following a two-year transition period, the SEC Modernization Rules will replace the historical property disclosure requirements for mining registrants that are included in SEC Industry Guide 7. The Company is not required to provide disclosure on its mineral properties under the SEC Modernization Rules until its fiscal year beginning May 31, 2021. Under the SEC Modernization Rules, the definitions of “proven mineral reserves” and “probable mineral reserves” have been amended to be substantially similar to the corresponding CIM Definition Standards and the SEC has added definitions to recognize “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” which are also substantially similar to the corresponding CIM Definition Standards; however there are differences in the definitions under the SEC Modernization Rules and the CIM Definition Standards and therefore once the Company begins reporting under the SEC Modernization Rules there is no assurance that the Company’s mineral reserve and mineral resource estimates will be the same as those reported under CIM Definition Standards as contained in this in the prospectus supplement and the accompanying base prospectus and the documents incorporated by reference herein and therein.

| 3 |

CAUTIONARY NOTE TO ALL INVESTORS CONCERNING ECONOMIC ASSESSMENTS THAT INCLUDE INFERRED RESOURCES

The Company currently holds or has the right to acquire interests in an advanced stage exploration project in Nye County, Nevada referred to as the North Bullfrog Project (the “NBP”) and exploration project referred to as the Mother Lode Project (“MLP”). Mineral resources that are not mineral reserves have no demonstrated economic viability. The preliminary economic assessment on the NBP and the MLP is preliminary in nature and includes “inferred mineral resources” that have a great amount of uncertainty as to their existence and are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. It cannot be assumed that all, or any part, of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies. There is no certainty that such inferred mineral resources at the NBP will ever be realized. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable.

| 4 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the exhibits attached hereto contain “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995, as amended, and “forward-looking information” within the meaning of applicable Canadian securities legislation, collectively “forward-looking statements”. Such forward-looking statements concern our anticipated results and developments in the operations of the Company in future periods, planned exploration activities, the adequacy of the Company’s financial resources and other events or conditions that may occur in the future. Forward-looking statements are frequently, but not always, identified by words such as “expects,” “anticipates,” “believes,” “intends,” “estimates,” “potential,” “possible” and similar expressions, or statements that events, conditions or results “will,” “may,” “could” or “should” (or the negative and grammatical variations of any of these terms) occur or be achieved. These forward looking statements may include, but are not limited to, statements concerning:

| • | the Company’s strategies and objectives, both generally and in respect of its specific mineral properties; |

| • | the results of the preliminary economic assessment; |

| • | the timing of decisions regarding the timing and costs of exploration programs with respect to, and the issuance of the necessary permits and authorizations required for, the Company’s exploration programs, including for the NBP and for the MLP; |

| • | the Company’s estimates of the quality and quantity of the mineral resources at its mineral properties; |

| • | the future price of minerals; |

| • | estimates of future operating and financial performance; |

| • | potential funding requirements and sources of capital, including near-term sources of additional cash; |

| • | the Company’s expectation that we will continue to raise capital through the sale of non-core assets, equity and/or debt financings and through the exercise of stock options and warrants; |

| • | the Company’s expectation that the Company will continue to incur losses and will not pay dividends for the foreseeable future; |

| • | the Company’s estimates of its future cash position; |

| • | the Company’s intention to identify and execute cost cutting initiatives; |

| • | the Company’s expectation that raising capital for mining companies without producing assets will continue to be difficult for the foreseeable future, and the potential impact of this on the Company’s ability to raise capital in sufficient amounts on reasonable terms; |

| • | the Company’s potential ability to generate proceeds from operations or the dispositions of its assets; |

| • | the timing, performance and results of feasibility studies; |

| • | the Company’s potential entry into agreements to find, lease, purchase, option or sell mineral interests; |

| • | plans and estimates concerning potential project development, including matters such as schedules, estimated completion dates and estimated capital and operating costs; |

| • | costs and timing of the exploration and development of new deposits; |

| • | success of exploration activities; |

| • | permitting and certification time lines; |

| • | government regulation of mining exploration, development and operations; |

| • | environmental risks; |

| • | timing and possible outcome of pending litigation, title disputes or claims; |

| • | the timing and cost of planned exploration programs of the Company and its joint venture partners (as applicable), and the timing of the receipt of results therefrom; |

| • | the Company’s future cash requirements and use of proceeds of sales of none-core assets; |

| • | general business and economic conditions; |

| • | the Company’s ability to meet its financial obligations as they come due, and to be able to raise the necessary funds to continue operations; |

| • | the Company’s expectation that it will be able to add additional mineral projects of merit to its assets; |

| • | the potential for the existence or location of additional high-grade veins, or high-grade mineralization; |

| • | the potential for any delineation of higher grade mineralization; |

| • | the potential for there to be one or more additional vein zone(s); |

| • | the potential discovery and delineation of mineral deposits/resources/reserves and any expansion thereof beyond the current estimate; |

| • | the Company’s expectation that it will be able to build itself into a non-operator gold producer with significant carried interests and royalty exposure |

| • | that the Company will operate at a loss; |

| • | that the Company will need to scale back anticipated costs and activities or raise additional funds; |

| • | that the Company will have to raise substantial additional capital to accomplish its business plan over the next couple of years; |

| 5 |

| • | the estimated reclamation and asset retirement costs; |

| • | the plans related to the potential development of the MLP and the NBP; and |

| • | the NBP and MLP work plans and mine development plan/programs. |

Such forward-looking statements reflect the Company’s current views with respect to future events and are subject to certain known and unknown risks, uncertainties and assumptions. Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements, including, among others, risks related to:

| • | risks related to the evolving novel coronavirus (“COVID-19”) pandemic and health crisis and the governmental and regulatory actions taken in response thereto; |

| • | our requirement of significant additional capital and our ability to raise such additional capital on favourable terms; |

| • | our ability to raise funds in new share offerings due to future sales of Common Shares in the public or private market and our ability to raise funds from the exercise of stock options and warrants; |

| • | whether our acquisition, exploration and potential development activities, as well as the realization of the market value of our assets, will be commercially successful and whether any transaction we enter will maximize the realization of the market value of our assets; |

| • | our limited operating history; |

| • | our history of losses; |

| • | a shortage of skilled labour, equipment and supplies; |

| • | our reliance on third parties to fulfill their obligations under our agreements; |

| • | cost increases for our exploration and, if warranted, development projects; |

| • | our Properties (as defined herein) being in the exploration stage; |

| • | mineral exploration, development and production activities; |

| • | our lack of mineral production from our Properties; |

| • | estimates of mineral resources, the accuracy of such estimates and the accuracy of sampling and subsequent assays and geologic interpretations on which they are based; |

| • | preliminary assessment results and the accuracy of estimates and assumptions on which they are based; |

| • | changes in project parameters; |

| • | failure of equipment and processes to operate as anticipated; |

| • | accidents, labour disputes and other risks of the mining industry; |

| • | changes in mineral resource estimates; |

| • | the accuracy of calculations of mineral resources and mineralized material fluctuations therein based on metal prices, inherent vulnerability of the ore and recoverability of metal in the mining process; |

| • | actual results of current exploration activities; |

| • | risks associated with restructuring and cost-efficiency initiatives; |

| • | differences in United States and Canadian mineral reserve and mineral resource reporting; |

| • | our exploration activities being unsuccessful; |

| • | the success of future joint ventures, partnership and other arrangements relating to our properties; |

| • | technical and operational feasibility and the economic viability of deposits; |

| • | fluctuations in gold, silver and other metal prices; |

| • | our ability to obtain permits and licenses for production; |

| • | government and environmental regulations that may increase our costs of doing business or restrict our operations; |

| • | proposed legislation that may significantly affect the mining industry; |

| • | changes in corporate governance and public disclosure regulations; |

| • | inherent hazards of mining exploration, development and operating activities; |

| • | future water supply issues; |

| • | land reclamation requirements; |

| • | competition in the mining industry; |

| • | equipment and supply shortages; |

| • | tax issues; |

| • | current and future joint ventures and partnerships; |

| • | our ability to attract qualified management and other key personnel; |

| • | the ability to enforce judgment against certain of our Directors (as defined herein); |

| • | conflicts of interest of some of our Directors as a result of their involvement with other natural resource companies; |

| • | currency fluctuations; |

| • | claims on the title to our Properties; |

| • | surface access on our Properties; |

| 6 |

| • | potential future litigation; |

| • | our lack of insurance covering all our operations; |

| • | risks related to current global financial conditions; |

| • | our status as a “passive foreign investment company” under US federal tax code; |

| • | the Common Shares (as defined herein); and |

| • | events such as war, terrorism, natural disaster or outbreaks of disease (including COVID-19). |

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein. This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including without limitation those discussed in Part I, Item 1A, Risk Factors, of this Annual Report on Form 10-K, which are incorporated herein by reference, as well as other factors described elsewhere in this report and the Company’s other reports filed with the SEC.

The Company’s forward-looking statements contained in this Annual Report on Form 10-K are based on the beliefs, expectations and opinions of management as of the date of this Annual Report. The Company does not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by law. For the reasons set forth above, investors should not attribute undue certainty to or place undue reliance on forward-looking statements.

| 7 |

GLOSSARY OF TERMS

| “Ag” | Silver |

| “alteration” | Changes in the chemical or mineralogical composition of a rock, generally produced by weathering or hydrothermal solutions |

| “Arrangement” | The corporate spin-out of Corvus from ITH by way of a plan of arrangement among ITH, the shareholders of ITH and Corvus under the BCBCA, effective August 26, 2010 |

| “Au” | Gold |

| “Board” | The board of directors of Corvus |

| “BCBCA” | Business Corporations Act (British Columbia), Corvus’ governing statute |

| “Corvus Nevada” | Corvus Gold Nevada Inc., a wholly owned subsidiary of Corvus USA subsisting under the laws of Nevada |

| “Corvus USA” | Corvus Gold (USA) Inc., a wholly owned subsidiary of Corvus subsisting under the laws of Nevada |

| “Common Shares” | The Common Shares without par value in the capital stock of Corvus as the same are constituted on the date hereof |

| “Corvus” | Corvus Gold Inc., a company organized under the laws of British Columbia |

| “cut-off grade” | The lowest grade of mineralized material that qualifies as ore in a given deposit, that is, material of the lowest assay value that is included in a resource/reserve estimate |

| “deposit” | A mineralized body which has been physically delineated by sufficient drilling, trenching, and/or underground work, and found to contain a sufficient average grade of metal or metals to warrant further exploration and/or development expenditures. Such a deposit does not qualify as a commercially mineable ore body or as containing reserves or ore, unless final legal, technical and economic factors are resolved |

| “Director” | A member of the Board |

| “disseminated” | Fine particles of mineral dispersed throughout the enclosing rock |

| “epigenetic” | Said of a mineral deposit of origin later than that of the enclosing rocks |

| “Exchange Act” | The United States Securities Exchange Act of 1934, as amended |

| “executive officer” |

When used in relation to any issuer (including the Company) means an individual who is:

(a) a chair, vice chair or president;

(b) a vice-president in charge of a principal business unit, division or function, including sales, finance or production; or

(c) performing a policy-making function in respect of the issuer

|

| “g/t” | Grams per metric tonne |

| “grade” | To contain a particular quantity of ore or mineral, relative to other constituents, in a specified quantity of rock |

| “heap leaching” | A method of recovering minerals from ore whereby crushed rock is stacked on a non-porous liner and an appropriate chemical solution is sprayed on the top of the pile (the “heap”) and allowed to percolate down through the crushed rock, dissolving the desired minerals(s) as it does so. The chemical solution is then collected from the base of the heap and is treated to remove the dissolved mineral(s) |

| “host” | A rock or mineral that is older than rocks or minerals introduced into it or formed within it |

| 8 |

| “host rock” | A body of rock serving as a host for other rocks or for mineral deposits, or any rock in which ore deposits occur |

| “hydrothermal” | A term pertaining to hot aqueous solutions of magmatic origin which may transport metals and minerals in solution |

| “ITH” | International Tower Hill Mines Ltd., a company subsisting under the laws of British Columbia |

| “massive” | Said of a mineral deposit, especially of sulphides, characterized by a great concentration of ore in one place, as opposed to a disseminated or veinlike deposit |

| “Moz” | Million ounces |

| “mineral reserve” | The economically mineable part of a measured and/or indicated mineral resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at pre-feasibility or feasibility level as appropriate that include application of modifying factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The reference point at which mineral reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. Under NI 43-101 standards, the public disclosure of a mineral reserve must be demonstrated by a pre-feasibility study or feasibility study. See Cautionary Note to U.S. Investors Regarding Estimates of Measured, Indicated, and Inferred Resources and Proven and Probable Reserves above. |

| “mineral resource” | A mineral resource is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. Material of economic interest refers to diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals. Mineral resources are sub-divided, in order of increasing geological confidence, into inferred, indicated and measured categories. The term mineral resource covers mineralization and natural material of intrinsic economic interest which has been identified and estimated through exploration and sampling and within which mineral reserves may subsequently be defined by the consideration and application of modifying factors. See Cautionary Note to U.S. Investors Regarding Estimates of Measured, Indicated, and Inferred Resources and Proven and Probable Reserves above. |

| “mineralization” | The concentration of metals and their chemical compounds within a body of rock |

| “modifying factors” | Considerations used to convert mineral resources to mineral reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors |

| “MLP” | The Mother Lode Project in Nevada held by Corvus Nevada, as more particularly described under “Properties” |

| “National Instrument 43-101”/ “NI 43-101” | National Instrument 43-101 of the Canadian Securities Administrators entitled “Standards of Disclosure for Mineral Projects” |

| “NBP” | The North Bullfrog Project in Nevada held by Corvus Nevada, as more particularly described under “Properties” |

| “NSR” | Net smelter return |

| “Properties” | The NBP in Nevada and the MLP in Nevada |

| “Raven Gold” | Raven Gold Alaska Inc., a wholly owned subsidiary of Corvus USA subsisting under the laws of Alaska |

| “SEC” | United States Securities and Exchange Commission |

| 9 |

| “SoN” | SoN Land and Water, LLC, a limited liability company subsisting under the laws of Nevada, of which Corvus Nevada is the sole member |

| “tabular” | Said of a feature having two dimensions that are much larger or longer than the third, or of a geomorphic feature having a flat surface, such as a plateau |

| “TSX” | Toronto Stock Exchange |

| “vein” | An epigenetic mineral filling of a fault or other fracture, in tabular or sheetlike form, often with the associated replacement of the host rock; also, a mineral deposit of this form and origin |

| SEC Industry Guide 7 Definitions: | |

| exploration stage | An “exploration stage” prospect is one which is not in either the development or production stage |

| development stage | A “development stage” project is one which is undergoing preparation of an established commercially mineable deposit for its extraction but which is not yet in production. This stage occurs after completion of a feasibility study |

| mineralized material | The term “mineralized material” refers to material that is not included in the reserve as it does not meet all of the criteria for adequate demonstration for economic or legal extraction |

| probable reserve | The term “probable reserve” refers to reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation |

| production stage | A “production stage” project is actively engaged in the process of extraction and beneficiation of mineral reserves to produce a marketable metal or mineral product |

| proven reserve | The term “proven reserve” refers to reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established |

| reserve | The term “reserve” refers to that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. Reserves must be supported by a feasibility study done to bankable standards that demonstrates the economic extraction. “Bankable standards” implies that the confidence attached to the costs and achievements developed in the study is sufficient for the project to be eligible for external debt financing. A reserve includes adjustments to the in-situ tonnes and grade to include diluting materials and allowances for losses that might occur when the material is mined |

1 For SEC Industry Guide 7 purposes this study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified.

2 SEC Industry Guide 7 does not require designation of a qualified person.

USE OF NAMES

In this Annual Report on Form 10-K, unless the context otherwise requires, the terms "we", "us", "our", "Corvus", "Corvus Gold Inc." or the "Company" refer to Corvus Gold Inc. and its subsidiaries.

Metric Equivalents

For ease of reference, the following factors for converting Imperial measurements into metric equivalents are provided:

| 10 |

| To convert from Imperial | To metric | Multiply by |

| Acres | Hectares | 0.404686 |

| Feet | Metres | 0.30480 |

| Miles | Kilometres | 1.609344 |

| Tons | Tonnes | 0.907185 |

| Ounces (troy)/ton | Grams/Tonne | 34.2857 |

| 1 mile = 1.609 kilometres 1 acre = 0.405 hectares 2,204.62 pounds = 1 metric ton = 1 tonne |

2000 pounds (1 short ton) = 0.907 tonnes 1 ounce (troy) = 31.103 grams 1 ounce (troy)/ton = 34.2857 grams/tonne | |

| 11 |

General Corporate Information

We were incorporated under the BCBCA with the name “Corvus Gold Inc.” on April 13, 2010 as a wholly-owned subsidiary of ITH, with an authorized capital consisting of an unlimited number of Common Shares. Pursuant to the corporate spin-out of Corvus from ITH by way of a plan of arrangement among ITH, the shareholders of ITH and Corvus under the BCBCA, effective August 26, 2010, Corvus was spun out as a separate and independent public company, and each shareholder of ITH received one-half of a Common Share.

We are a reporting issuer in the Canadian Provinces of British Columbia, Alberta and Ontario and the Common Shares are listed for trading on the TSX and the Nasdaq Capital Market in each case under the trading symbol “KOR”.

Our head office is located at Suite 1750 – 700 West Pender Street, Vancouver, British Columbia, Canada V6C 1G8, and our registered and records office is located at Suite 2200, HSBC Building, 885 West Georgia Street, Vancouver, British Columbia V6C 3E8.

We are a mineral exploration company engaged in the acquisition, exploration and development of mineral properties. We currently hold or have the right to acquire interests in the NBP and the MLP in Nevada. We are in the exploration stage as our Properties have not yet reached commercial production and our Properties are not beyond the preliminary exploration stage. All work presently planned by us is directed at defining mineralization and increasing understanding of the characteristics of, and economics of, that mineralization.

Emerging Growth Company Status

We lost our status as an emerging growth company on May 31, 2020, the last day of our fiscal year following the fifth anniversary of the date of the first sale of common equity securities pursuant to an effective registration statement.

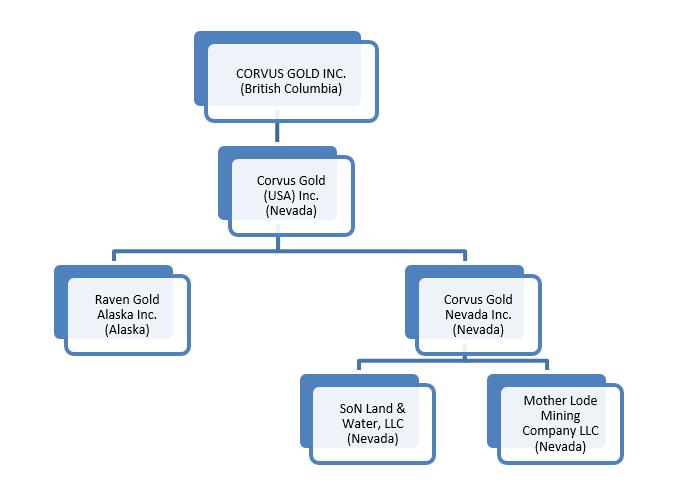

Intercorporate Relationships

We have five material subsidiaries:

| (a) | Corvus Nevada, a corporation incorporated in Nevada on April 9, 2007, which holds all of our properties in Nevada and is 100% owned by Corvus USA; |

| (b) | Raven Gold, a corporation incorporated in Alaska on July 2, 2009, which held all of our properties in Alaska and will hold any future properties in Alaska and is 100% owned by Corvus USA; |

| (c) | SoN Land & Water, LLC, a limited liability company incorporated in Nevada on July 25, 2013, of which Corvus Nevada is the sole member; |

| (d) | Corvus USA, a corporation incorporated in Nevada on February 25, 2013, which holds all of the shares of Corvus Nevada and Raven Gold and is 100% owned by Corvus; and |

| (e) | Mother Lode Mining Company LLC, a limited liability company incorporated in Nevada on March 14, 2014 of which Corvus Nevada is the sole member. |

The following corporate chart sets forth all of our material subsidiaries:

| 12 |

Recent Corporate History

In May 2010, the board of directors of ITH approved a proposal to undertake a spin-out transaction to segregate its then existing assets into two separate and highly focused companies.

The spin-out transaction pursuant to the Arrangement was approved by the shareholders of ITH on August 12, 2010, and the final order of the Supreme Court of British Columbia approving the plan of arrangement necessary to implement the transaction was received on August 20, 2010. The effective date of the Arrangement was August 26, 2010 and the Common Shares commenced trading on the TSX on August 30, 2010. Under the terms of the Arrangement, ITH retained all assets relating to the Livengood gold project in Alaska, together with approximately $33 million in working capital, while Corvus received all of ITH’s other existing Alaska and Nevada assets (including the shares of Corvus Nevada), together with approximately $3.3 million in working capital.

Following the completion of the Arrangement, Corvus held four advanced to early stage exploration projects in Alaska (Chisna, Terra, LMS and West Pogo) and the advanced exploration stage NBP in Nevada. Our primary focus is to leverage our exploration expertise to discover major new gold deposits. Furthermore, we intend to try and build ourselves into a non-operator gold producer with significant carried interests and royalty exposure. To meet this objective, all of the Alaskan projects received by us in the Arrangement have been sold.

We also received from ITH a 100% interest in the NBP, which is Corvus’ sole material mineral property and the primary focus of our exploration activities. Since the acquisition of the NBP from ITH, we have expanded the NBP by entering into additional leases of patented lode mining claims and staking additional unpatented lode mining claims.

In June 2017, Corvus acquired 100% of the MLP from Goldcorp USA, Inc. and staked two additional claim blocks adjacent to the MLP. The MLP is in close proximity to Corvus Gold’s NBP with potential for integration into a single operation.

Business Operations

Summary

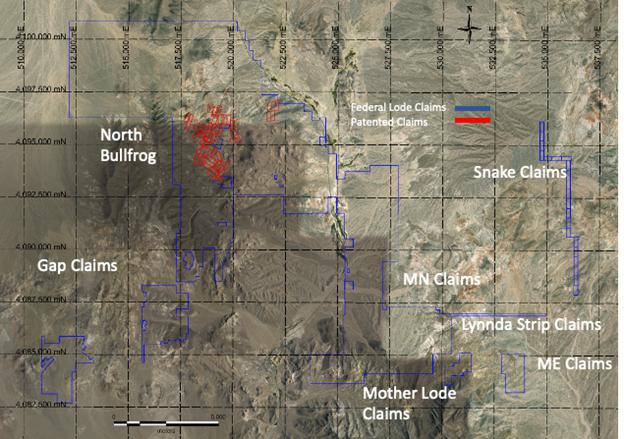

We currently hold, or have rights to acquire, interests in two mineral properties in Nevada, USA, the NBP and the MLP. The Company’s objectives with respect to these Properties are to evaluate the potential of the Properties and to determine if spending additional funds is warranted (in which case, an appropriate program to advance the Properties to the next decision point will be formulated and, depending upon available funds, implemented by us) or not (in which case the Properties may be returned by us to the optionor/lessor or, in respect of properties in which we are earning an interest, be returned to the optionor thereof). Our present focus is on the exploration and, if warranted, development of the NBP, located 15 kilometres north of Beatty, Nevada, and the MLP, located in the Bare Mountain District, approximately 10 kilometres from the NBP. Corvus also staked additional claim blocks, the MN claim group, to the northwest of the Mother Lode claims, the ME claim group, to the east of the Mother Lode claims, and the GAP claim group, immediately to the south of NBP. During the fiscal year, the Company extended its claim holdings in an unstaked areas lying between Coeur Mining Inc. and AngloGold Ashanti Limited (“AngloGold Ashanti”) called the Lynnda Strip and an unstaked area, the Snake Claims between AngloGold Ashanti claims on the east boundary of the Silicon Block (see Figure 1). The progress on, and results of, the work programs on our material mineral property is set out under Part I, Item 2, Properties in this Annual Report. We continue to assess additional mineral property acquisitions but do not presently contemplate entering into any such agreements, other than in connection with the NBP and the MLP.

| 13 |

We are in the exploration stage and do not mine, produce or sell any mineral products at this time. With respect to the NBP and MLP, our present preliminary studies indicate that any production would be through a combination of heap leaching some of the mineralization (and treatment of the leaching solution to recover gold and silver) and processing higher grade mineralization through a plant incorporating both a gravity concentration-cyanide leach circuit and a concentration circuit followed by pressure oxidation of the concentrate and then leaching of the oxidized filtrate.

Exploration drilling has been distributed between the two properties throughout the year, with both core drilling rigs and an RC drilling rig being transferred between the properties at various time of the year. The RC rig was used to conduct infill and step out drilling as well as drill pre-collars for core-tail holes to allow the drilling to reach greater depths. Corvus expects to continue with drilling activities at both North Bullfrog, Mother Lode and other targets through much of the next fiscal year.

Availability of Raw Materials

All of the raw materials we require to carry on our business are readily available through normal supply or business contracting channels in Canada and the United States. Since commencing current operations in August 2010, we have been able to secure the appropriate personnel, equipment and supplies required to conduct our contemplated programs. As a result, we do not believe that we will experience any shortages of required personnel, equipment or supplies in the foreseeable future.

Dependence on a Few Contracts

Our business is not substantially dependent on any contract such as a contract to sell the major part of the Company’s products or services or to purchase the major part of its requirements for goods, services or raw materials, or on any franchise or license or other agreement to use a patent, formula, trade secret, process or trade name upon which its business depends. Rather, our ability to continue making the holding, assessment, lease and option payments necessary to maintain our interest in our mineral projects is of primary concern. We do not presently anticipate any difficulties in this regard in the current financial year.

Competitive Conditions

There is aggressive competition within the minerals industry to discover and acquire mineral properties considered to have commercial potential. We compete with other entities for the opportunity to participate in exploration projects which we believe are promising. In addition, we compete with others in efforts to obtain financing to acquire and explore mineral properties, acquire and utilize mineral exploration equipment and hire qualified mineral exploration personnel. We may compete with other junior mining companies for mining claims in regions adjacent to our existing claims, or in other parts of the world should we dedicate resources to doing so in the future. These companies may be better capitalized than us and we may have difficulty in expanding our holdings through the staking or acquisition of additional mining claims or other mineral tenures.

In competing for qualified mineral exploration personnel, we may be required to pay compensation or benefits relatively higher than those paid in the past, and the availability of qualified personnel may be limited in high-demand mining periods, such as was in past years when the price of gold was higher than it is now.

Government Regulation

The exploration and development of a mining prospect is subject to regulation by a number of federal and state government authorities. These include the United States Environmental Protection Agency (“EPA”) and the United States Bureau of Land Management (“BLM”) as well as the various state environmental protection agencies. The regulations address many environmental issues relating to air, soil and water contamination and apply to many mining related activities including exploration, mine construction, mineral extraction, ore milling, water use, waste disposal and use of toxic substances. In addition, we are subject to regulations relating to labor standards, occupational health and safety, mine safety, general land use, export of minerals and taxation. Many of the regulations require permits or licenses to be obtained and the filing of Notices of Intent and Plans of Operations, the absence of which or inability to obtain will adversely affect the ability for us to conduct our exploration, development and operation activities. The failure to comply with the regulations and terms of permits and licenses may result in fines or other penalties or in revocation of a permit or license or loss of a prospect.

| 14 |

Federal

On lands owned by the United States, mining rights are governed by the General Mining Law of 1872, as amended, which allows the location of mining claims on certain federal lands upon the discovery of a valuable mineral deposit and compliance with location requirements. The exploration of mining properties and development and operation of mines is governed by both federal and state laws. Federal laws that govern mining claim location and maintenance and mining operations on federal lands are generally administered by the BLM. Additional federal laws, governing mine safety and health, also apply. State laws also require various permits and approvals before exploration, development or production operations can begin. Among other things, a reclamation plan must typically be prepared and approved, with bonding in the amount of projected reclamation costs. The bond is used to ensure that proper reclamation takes place, and the bond will not be released until that time. Local jurisdictions may also impose permitting requirements (such as conditional use permits or zoning approvals).

Nevada

In Nevada, initial stage surface exploration activities that do not disturb the surface, do not require any permits. Notice-level exploration permits (“NOI”) are required (through the BLM) for the NBP and MLP to perform drilling or other surface disturbing activities with less than five acres extent. More extensive disturbance requires submittal and approval of a “Plan of Operations” and “Environmental Assessment” from the BLM. In May 2013, Corvus obtained an amended Plan of Operations allowing 100 acres of surface disturbance in the public lands portion of the NBP, which is considered sufficient by us for our currently planned drilling and characterization program. Reclamation costs have been re-estimated on a 3-year basis, with the most recent submitted June 19, 2019. We also applied for, and received in August 2013, a NOI for disturbance of an additional 1.3 acres outside the currently defined NBP area in order to allow us to drill water monitor wells and perform geotechnical soil investigations outside the NBP area. This NOI has been reviewed and extended until May 9, 2021 by BLM. In June of 2015, the Company applied for, and received a NOI which allowed an additional 2.1 acres of disturbance for exploration of the Eastern Steam-heated Alteration zone, outside of the NBP permit area. On December 7, 2015, a decision allowing the increase in disturbance area to 4.8 acres in the Eastern Steam-heated Alteration zone was received from BLM. This Notice has been extended to 2021. In August of 2017, the Company received an NOI from BLM which allowed 4.8 acres of surface disturbance for drilling exploration at the MLP. In June 2018, Corvus received approval of an NOI for 4.4 acres of disturbance at the Company’s Willy’s Exploration Project near the MLP. In September 2018, Corvus received approval of an NOI for 0.7 acres of disturbance at the Company’s Sawtooth Project site near the MLP. On June 23, 2020, the Company received approval of a Plan of Operations at the Mother Lode site allowing up to 145 acres of disturbance for future exploration. As of July 2, 2020, the Company had posted with the BLM, as security for the reclamation obligations at North Bullfrog and at Mother Lode, a Surety Bond of USD 588,056. In addition, as part of the approval of the Mother Lode Plan of Operations, BLM has granted the company two Right-of-Ways (“ROWs”), (1) for road access to the Mother Lode site and further to the east to the location of the Company’s three installed water wells, and (2) for the water well sites. Additional reclamation bonds were required for the individual ROWs in the amounts USD 113,000 and USD 188,200, for the access road and water wells, respectively. In general, exploration activities in Nevada can be carried out on a year-round basis. Mining is conducted in Nevada on a year round basis, both open pit and underground.

In Nevada, we are also required to post bonds with the State of Nevada to secure our environmental and reclamation obligations on private land, with amount of such bonds reflecting the level of rehabilitation anticipated by the then proposed activities. Currently, the Company has posted with Nevada Division of Minerals BMRR in the State of Nevada, as security for these reclamation obligations, a Surety Bond of USD 209,070.

In June 2013, formal meetings were held with officials of both the Nevada Department of Environmental Protection (“NDEP”) and the BLM to discuss the design criteria for the environmental baseline studies that will be required to support the development of a Plan of Operation and other permit applications necessary to enable any mining at or production from the NBP. In January 2014, Corvus Nevada executed a Memorandum of Understanding (“MOU”) with the Tonopah Office of the BLM for definition of baseline characterization requirements and development of a mining plan of operations at the NBP. Characterization plans for hydro-geologic modeling studies, rock geochemical studies and biologic/wildlife studies have been developed and have been reviewed by BLM specialists. We are in the process of responding to comments and additional requirements received from the BLM with respect to such plans.

If we are successful in the future at discovering a commercially viable mineral deposit on our property interests, then if and when we commence any mineral production, we will also need to comply with laws that regulate or propose to regulate our mining activities, including the management and handling of raw materials, disposal, storage and management of hazardous and solid waste, the safety of our employees and post-mining land reclamation.

We cannot predict the impact of new or changed laws, regulations or permitting requirements, or changes in the ways that such laws, regulations or permitting requirements are enforced, interpreted or administered. Health, safety and environmental laws and regulations are complex, are subject to change and have become more stringent over time. It is possible that greater than anticipated health, safety and environmental capital expenditures or reclamation and closure expenditures will be required in the future. We expect continued government and public emphasis on environmental issues will result in increased future investments for environmental controls at our operations.

| 15 |

Environmental Regulation

Our mineral projects are subject to various federal, state and local laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. The development, operation, closure, and reclamation of mining projects in the United States requires numerous notifications, permits, authorizations, and public agency decisions. Compliance with environmental and related laws and regulations requires us to obtain permits issued by regulatory agencies, and to file various reports and keep records of our operations. Certain of these permits require periodic renewal or review of their conditions and may be subject to a public review process during which opposition to our proposed operations may be encountered. We are currently operating under various permits for activities connected to mineral exploration, reclamation, and environmental considerations. Our policy is to conduct business in a way that safeguards public health and the environment. We believe that our operations are conducted in material compliance with applicable laws and regulations.

Changes to current local, state or federal laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could impact the economics of our projects.

U.S. Federal Laws

The Comprehensive Environmental, Response, Compensation, and Liability Act (“CERCLA”), and comparable state statutes, impose strict, joint and several liability on current and former owners and operators of sites and on persons who disposed of or arranged for the disposal of hazardous substances found at such sites. It is not uncommon for the government to file claims requiring cleanup actions, demands for reimbursement for government-incurred cleanup costs, or natural resource damages, or for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the environment. The Federal Resource Conservation and Recovery Act (“RCRA”), and comparable state statutes, govern the disposal of solid waste and hazardous waste and authorize the imposition of substantial fines and penalties for noncompliance, as well as requirements for corrective actions. CERCLA, RCRA and comparable state statutes can impose liability for clean-up of sites and disposal of substances found on exploration, mining and processing sites long after activities on such sites have been completed.

The Clean Air Act (“CAA”), as amended, restricts the emission of air pollutants from many sources, including mining and processing activities. Any future mining operations by the Company may produce air emissions, including fugitive dust and other air pollutants from stationary equipment, storage facilities and the use of mobile sources such as trucks and heavy construction equipment, which are subject to review, monitoring and/or control requirements under the CAA and state air quality laws. New facilities may be required to obtain permits before work can begin, and existing facilities may be required to incur capital costs in order to remain in compliance. In addition, permitting rules may impose limitations on our production levels or result in additional capital expenditures in order to comply with the rules.

The National Environmental Policy Act (“NEPA”) requires federal agencies to integrate environmental considerations into their decision-making processes by evaluating the environmental impacts of their proposed actions, including issuance of permits to mining facilities, and assessing alternatives to those actions. If a proposed action could significantly affect the environment, the agency must prepare a detailed statement known as an Environmental Impact Statement (“EIS”). The EPA, other federal agencies, and any interested third parties will review and comment on the scoping of the EIS and the adequacy of and findings set forth in the draft and final EIS. This process can cause delays in issuance of required permits or result in changes to a project to mitigate its potential environmental impacts, which can in turn impact the economic feasibility of a proposed project.

The Clean Water Act (“CWA”), and comparable state statutes, impose restrictions and controls on the discharge of pollutants into waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or an analogous state agency. The CWA regulates storm water mining facilities and requires a storm water discharge permit for certain activities. Such a permit requires the regulated facility to monitor and sample storm water run-off from its operations. The CWA and regulations implemented thereunder also prohibit discharges of dredged and fill material in wetlands and other waters of the United States unless authorized by an appropriately issued permit. The CWA and comparable state statutes provide for civil, criminal and administrative penalties for unauthorized discharges of pollutants and impose liability on parties responsible for those discharges for the costs of cleaning up any environmental damage caused by the release and for natural resource damages resulting from the release.

| 16 |

The Safe Drinking Water Act (“SDWA”) and the Underground Injection Control (“UIC”) program promulgated thereunder, regulate the drilling and operation of subsurface injection wells. The EPA directly administers the UIC program in some states and in others the responsibility for the program has been delegated to the state. The program requires that a permit be obtained before drilling a disposal or injection well. Violation of these regulations and/or contamination of groundwater by mining related activities may result in fines, penalties, and remediation costs, among other sanctions and liabilities under the SWDA and state laws. In addition, third party claims may be filed by landowners and other parties claiming damages for alternative water supplies, property damages, and bodily injury.

Nevada

Other Nevada regulations govern operating and design standards for the construction and operation of any source of air contamination and landfill operations. Any changes to these laws and regulations could have an adverse impact on our financial performance and results of operations by, for example, requiring changes to operating constraints, technical criteria, fees or surety requirements.

Key Personnel

As at August 13, 2020, we have two full time employees and ten part-time consultants. Our operations are managed by our officers with oversight by the Directors. We engage geological, metallurgical, and engineering consultants from time to time as required to assist in evaluating our property interests and recommending and conducting work programs.

Gold Price History

The price of gold is volatile and is affected by numerous factors all of which are beyond our control, such as the sale or purchase of gold by various central banks and financial institutions, inflation, recession, fluctuation in the relative values of the U.S. dollar and foreign currencies, changes in global and regional gold demand and the political and economic conditions.

The following table presents the high, low and average afternoon fixed prices in U.S. dollars for an ounce of gold on the London Bullion Market over the past five calendar years and the current calendar year to date:

| Year | High | Low | Average | |||

| USD | USD | USD | ||||

| 2014 | 1,385 | 1,142 | 1,267 | |||

| 2015 | 1,296 | 1,049 | 1,160 | |||

| 2016 | 1,366 | 1,077 | 1,251 | |||

| 2017 | 1,346 | 1,151 | 1,257 | |||

| 2018 | 1,355 | 1,178 | 1,268 | |||

| 2019 | 1,546 | 1,270 | 1,393 | |||

| 2020 (through August 12, 2020) | 2,067 | 1,474 | 1,691 |

Data Source: www.kitco.com

Seasonality

The NBP and the MLP are not subject to material restrictions on our operations due to seasonality.

| 17 |

Sustainability

The Company has created a Sustainable Development Committee (“SDC”) which will primarily monitor, review and provide oversight with respect to its policies, standards, accountabilities and programs relative to health, safety, community relations and environmental-related matters. Further, the SDC will advise the Board and make recommendations for the Board’s consideration regarding health, safety, community relations and environmental-related issues. In particular, the SDC will consider and advise the Board with respect to current standards of sustainable development for projects and activities such as those of the Company, particularly with a view to ensuring that the Company’s business is run in a manner, and its projects are operated and developed, so as to achieve the ideals and reflect the following principles of sustainable development:

| 1. | living within environmental limits; |

| 2. | ensuring a strong, healthy and just society; |

| 3. | achieving a sustainable economy; |

| 4. | using sound science responsibly; and |

| 5. | promoting good governance. |

Available Information

We make available, free of charge, on or through our Internet website, at www.corvusgold.com, our Annual Report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. Our Internet website and the information contained therein or connected thereto are not intended to be, and are not incorporated into this Annual Report on Form 10-K.

| 18 |

You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K. Each of these risk factors could materially and adversely affect our business, operating results and financial condition, as well as materially and adversely affect the value of an investment in our Common Shares. The risks described below are not the only ones facing the Company. Additional risks that we are not presently aware of, or that we currently believe are immaterial, may also adversely affect our business, operating results and financial condition. We cannot assure you that we will successfully address these risks or that other unknown risks exist that may affect our business.

Risks Related To Our Company

The outbreak of the coronavirus pandemic may impact the Company’s plans and activities

The Company’s exploration and development activities may be affected by existing or threatened medical pandemics, such as the novel coronavirus (COVID-19). A government may impose strict emergency measures in response to the threat or existence of an infectious disease, such as the emergency measures imposed by governments of many countries and states in response to the COVID-19 virus pandemic. As such, there are potentially significant economic and social impacts of infectious diseases, including but not limited to the inability of the Company to develop and operate as intended, shortage of skilled employees or labour unrest, inability to access sufficient healthcare, significant social upheavals or unrest, disruption to operations, supply chain shortages or delays, travel and trade restrictions, government or regulatory actions or inactions (including but not limited to, changes in taxation or policies, or delays in permitting or approvals, or mandated shut downs), declines in the price of precious metals, capital markets volatility, availability of credit, loss of investor confidence and impact on economic activity in affected countries or regions. In addition, such pandemics or diseases represent a serious threat to maintaining a skilled workforce in the mining industry and could be a major health-care challenge for the Company. There can be no assurance that the Company or the Company’s personnel will not be impacted by these pandemic diseases and the Company may ultimately see its workforce productivity reduced or incur increased medical costs/insurance premiums as a result of these health risks. COVID-19 is rapidly evolving and the effects on the mining industry and the Company are uncertain. The Company may not be able to accurately predict the impact of infectious disease, including COVID-19, or the quantum of such risks. There can be no assurance that the Company will not be impacted by adverse consequences that may be brought about by pandemics on global financial markets, which may reduce resources, share prices and financial liquidity and may severely limit the financing capital available to the Company.

We will require significant additional capital to fund our business plan.

We will be required to expend significant funds to determine if proven and probable mineral reserves exist at our Properties, to continue exploration and if warranted, develop our existing Properties and to identify and acquire additional properties to diversify our Properties portfolio. We have spent and will be required to continue to expend significant amounts of capital for drilling, geological and geochemical analysis, assaying and feasibility studies with regard to the results of our exploration. We may not benefit from some of these investments if we are unable to identify commercially exploitable mineralized material.

Our ability to obtain necessary funding for these purposes, in turn, depends upon a number of factors, including the status of the national and worldwide economy and the price of gold and silver. We may not be successful in obtaining the required financing or, if we can obtain such financing, such financing may not be on terms that are favorable to us. Failure to obtain such additional financing could result in delay or indefinite postponement of further mining operations or exploration and development and the possible partial or total loss of our potential interest in our Properties.

We have a limited operating history on which to base an evaluation of our business and prospects.

Since our inception we have had no revenue from operations. We have no history of producing metals from any of our properties. Our Properties are exploration stage properties. Advancing properties from exploration into the development stage requires significant capital and time, and successful commercial production from a property, if any, will be subject to completing feasibility studies, permitting and construction of the mine, processing plants, roads, and other related works and infrastructure. As a result, we are subject to all of the risks associated with developing and establishing new mining operations and business enterprises including:

| · | completion of feasibility studies to verify reserves and commercial viability, including the ability to find sufficient gold/silver mineral reserves to support a commercial mining operation; |

| · | the timing and cost, which can be considerable, of further exploration, preparing feasibility studies, permitting and construction of infrastructure, mining and processing facilities; |

| 19 |

| · | the availability and costs of drill equipment, exploration personnel, skilled labor and mining and processing equipment, if required; |

| · | the availability and cost of appropriate smelting and/or refining arrangements, if required; |

| · | compliance with environmental and other governmental approval and permit requirements; |

| · | the availability of funds to finance exploration, development and construction activities, as warranted; |

| · | potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants which may delay or prevent development activities; |

| · | potential increases in exploration, construction and operating costs due to changes in the cost of fuel, power, materials and supplies; and |

| · | potential shortages of mineral processing, construction and other facilities related supplies. |

The costs, timing and complexities of exploration, development and construction activities may be increased by the location of our Properties and demand by other mineral exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if commenced, development, construction and mine start-up. Accordingly, our activities may not result in profitable mining operations and we may not succeed in establishing mining operations or profitably producing metals at any of our properties.

We have a history of losses and expect to continue to incur losses in the future.

We have incurred losses since inception, have negative cash flow from operating activities and expect to continue to incur losses in the future. We incurred the following losses from operations during each of the following periods:

| · | $(16,879,394) for the year ended May 31, 2020; and |

| · | $(11,020,098) for the year ended May 31, 2019. |

We expect to continue to incur losses unless and until such time as one of our Properties enters into commercial production and generate sufficient revenues to fund continuing operations. We recognize that if we are unable to generate significant revenues from mining operations and dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition.

Negative Operating Cash Flow

The Company is an exploration stage company and has not generated cash flow from operations. The Company is devoting significant resources to the development of the Properties and to actively pursue exploration and development opportunities, however, there can be no assurance that it will generate positive cash flow from operations in the future. The Company expects to continue to incur negative consolidated operating cash flow and losses until such time as it achieves commercial production at a particular project. The Company currently has negative cash flow from operating activities.

Increased costs could affect our financial condition.

We anticipate that costs at our projects and Properties that we may explore or develop, will frequently be subject to variation from one year to the next due to a number of factors, such as changing grade, metallurgy and revisions to mine plans, if any, in response to the physical shape and location of the body. In addition, costs are affected by the price of commodities such as fuel, steel, rubber, and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any significant location could have a significant effect on our profitability.

Risks Related to Mining and Exploration

Our Properties are in the exploration stage.

The NBP and the MLP have estimated mineral resources identified, but there has not been a mineral reserve estimation in accordance with NI 43-101 or SEC Industry Guide 7. There is no assurance that we can establish the existence of any mineral reserves on the NBP or the MLP in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from the Properties and if we do not do so, we will lose all of the funds that we expend on exploration. If we do not discover any mineral reserves in a commercially exploitable quantity, the exploration component of our business could fail.

| 20 |

We have not established that our NBP or MLP contains any mineral reserve according to recognized reserve guidelines, nor can there be any assurance that we will be able to do so. A mineral reserve is defined by the SEC in its Industry Guide 7 as that part of a mineral deposit, which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a “reserve” that meets the requirements of the SEC’s Industry Guide 7 is extremely remote; in all probability our mineral Properties do not contain any “reserves” and any funds that we spend on exploration could be lost. Even if we do eventually discover a mineral reserve on our Properties, there can be no assurance that they can be developed into producing mines and extract those minerals. Both mineral exploration and development involve a high degree of risk and few mineral properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the mineral deposit to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral deposit unprofitable.

The nature of mineral exploration and production activities involves a high degree of risk and the possibility of uninsured losses.

Exploration for and the production of minerals is highly speculative and involves much greater risk than many other businesses. Most exploration programs do not result in the discovery of mineralization, and any mineralization discovered may not be of sufficient quantity or quality to be profitably mined. Our operations are, and any future development or mining operations we may conduct will be, subject to all of the operating hazards and risks normally incident to exploring for and development of mineral properties, such as, but not limited to:

| · | economically insufficient mineralized material; |

| · | the ability to find sufficient gold, silver or other metal reserves to support a profitable mining operation; |

| · | fluctuation in production costs that make mining uneconomical; |

| · | labor disputes; |

| · | unanticipated variations in grade and other geologic problems; |

| · | environmental hazards; |

| · | water conditions; |

| · | difficult surface or underground conditions; |

| · | industrial accidents; |

| · | metallurgic and other processing problems; |

| · | mechanical and equipment performance problems; |

| · | failure of pit walls or dams; |

| · | unusual or unexpected rock formations; |

| · | personal injury, fire, flooding, cave-ins and landslides; and |

| · | decrease in the value of mineralized material due to lower gold and/or silver prices. |

Any of these risks can materially and adversely affect, among other things, the development of properties, production quantities and rates, costs and expenditures, potential revenues and production dates. We currently have very limited insurance to guard against some of these risks. If we determine that capitalized costs associated with any of our mineral interests are not likely to be recovered, we would incur a write-down of our investment in these interests. All of these factors may result in losses in relation to amounts spent which are not recoverable, or result in additional expenses.

| 21 |

We have no history of producing metals from our current mineral properties and there can be no assurance that we will successfully establish mining operations or profitably produce precious metals.

We have no history of producing metals from our current mineral Properties. We do not produce gold or silver and do not currently generate operating earnings. While we seek to move our Properties into production, such efforts will be subject to all of the risks associated with establishing new mining operations and business enterprises, including:

| · | the timing and cost, which are considerable, of the construction of mining and processing facilities; |

| · | the ability to find sufficient gold/silver reserves to support a profitable mining operation; |

| · | the availability and costs of skilled labor and mining equipment; |

| · | compliance with environmental and other governmental approval and permit requirements; |

| · | the availability of funds to finance construction and development activities; |

| · | potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants that may delay or prevent development activities; and |

| · | potential increases in construction and operating costs due to changes in the cost of labor, fuel, power, materials and supplies. |

It is common in new mining operations to experience unexpected problems and delays during construction, development and mine start-up. In addition, our management will need to be expanded. This could result in delays in the commencement of mineral production and increased costs of production. Accordingly, we cannot assure you that our activities will result in profitable mining operations or that we will successfully establish mining operations.

Estimates of mineral resources are subject to evaluation uncertainties that could result in project failure.

Unless otherwise indicated, mineralization figures presented in this Annual Report and in our filings with securities regulatory authorities, press releases and other public statements that may be made from time to time are based upon estimates made by independent geologists and mining engineers. When making determinations about whether to advance any of our projects to development, we must rely upon such estimated calculations as to the mineral resources, mineral reserves and grades of mineralization on our properties. Until ore is actually mined and processed, mineral resources, mineral reserves and grades of mineralization must be considered as estimates only.

Our exploration and future mining operations, if any, are and would be faced with risks associated with being able to accurately predict the quantity and quality of mineral resources/reserves within the earth using statistical sampling techniques. Estimates of mineral resource/reserve on our Properties would be made using samples obtained from appropriately placed trenches, test pits and underground workings and intelligently designed drilling. There is an inherent variability of assays between check and duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. Additionally, there also may be unknown geologic details that have not been identified or correctly appreciated at the current level of accumulated knowledge about our Properties. This could result in uncertainties that cannot be reasonably eliminated from the process of estimating mineral resources/reserves. If these estimates were to prove to be unreliable, we could implement an exploitation plan that may not lead to commercially viable operations in the future.

Any material changes in mineral resource/reserve estimates and grades of mineralization will affect the economic viability of placing a property into production and a property’s return on capital.