Attached files

| file | filename |

|---|---|

| EX-99.2 - EX-99.2 - POTASH CORP OF SASKATCHEWAN INC | d489097dex992.htm |

| 8-K - 8-K - POTASH CORP OF SASKATCHEWAN INC | d489097d8k.htm |

Exhibit 99.1

THIS LETTER OF TRANSMITTAL AND ELECTION FORM IS FOR USE ONLY IN CONNECTION WITH THE PLAN OF ARRANGEMENT UNDER SECTION 192 OF THE CANADA BUSINESS CORPORATIONS ACT INVOLVING, AMONG OTHERS, AGRIUM INC., SHAREHOLDERS OF AGRIUM INC., POTASH CORPORATION OF SASKATCHEWAN INC., SHAREHOLDERS OF POTASH CORPORATION OF SASKATCHEWAN INC. AND NUTRIEN LTD., A NEWLY-INCORPORATED ENTITY FORMED TO MANAGE AND HOLD THE COMBINED BUSINESSES OF AGRIUM INC. AND POTASH CORPORATION OF SASKATCHEWAN INC.

IT IS IMPORTANT THAT YOU VALIDLY COMPLETE, DULY EXECUTE AND RETURN THIS LETTER OF TRANSMITTAL AND ELECTION FORM IN A TIMELY MANNER TO THE DEPOSITARY, AST TRUST COMPANY (CANADA), IN ACCORDANCE WITH THE INSTRUCTIONS CONTAINED HEREIN. THE DEPOSITARY OR YOUR FINANCIAL ADVISOR CAN ASSIST YOU IN COMPLETING THIS LETTER OF TRANSMITTAL.

The instructions accompanying this Letter of Transmittal and Election Form should be read carefully before this Letter of Transmittal and Election Form is completed or submitted to the Depositary. If you have any questions or require more information with regard to the procedures for completing this Letter of Transmittal and Election Form, please contact the Depositary Toll Free (North America) at 1-800-387-0825 or Outside of North America at 1-416-682-3860. You can email the Depositary at inquiries@astfinancial.com.

LETTER OF TRANSMITTAL AND ELECTION FORM

FOR COMMON SHARES OF

POTASH CORPORATION OF SASKATCHEWAN INC.

| TO: |

AST TRUST COMPANY (CANADA) (the “Depositary”) | |

| AND TO: |

POTASH CORPORATION OF SASKATCHEWAN INC. (“PotashCorp”) | |

| AND TO: |

AGRIUM INC. (“Agrium”) | |

This Letter of Transmittal and Election Form (“Letter of Transmittal”) is for use by registered holders (“Registered Shareholders”) of common shares in the capital of PotashCorp (“PotashCorp Shares”), including participants (“DRIP Participants”) in PotashCorp’s Dividend Reinvestment Plan (the “DRIP”), in connection with the plan of arrangement (the “Arrangement”) involving, among others, Agrium, holders of common shares of Agrium, PotashCorp, holders of PotashCorp Shares (“PotashCorp Shareholders”) and Nutrien Ltd. (“New Parent”), a newly-incorporated entity formed to manage and hold the combined businesses of Agrium and PotashCorp. Pursuant to the Arrangement, New Parent will, directly and indirectly, acquire all of the issued and outstanding PotashCorp Shares and all of the issued and outstanding common shares in the capital of Agrium. PotashCorp Shareholders will receive 0.40 common shares in the capital of New Parent (each one share, a “New Parent Share”) for each PotashCorp Share held pursuant to the Arrangement all as set forth in further detail in the previously delivered joint information circular (the “Information Circular”) of Agrium and PotashCorp dated October 3, 2016.

Copies of the Information Circular, arrangement agreement and plan of arrangement may be accessed through PotashCorp’s profile on the SEDAR website at www.sedar.com or through the EDGAR website at www.sec.gov. Capitalized terms used but not defined in this Letter of Transmittal have the meaning set out in the Information Circular.

IN THIS LETTER OF TRANSMITTAL, “ELECTION DEADLINE” MEANS 5:00 P.M. (CENTRAL STANDARD TIME) ON THE DATE TO BE SPECIFIED BY POTASHCORP IN A PRESS RELEASE TO BE DISSEMINATED THROUGH NATIONALLY RECOGNIZED WIRE SERVICES IN CANADA AND THE UNITED STATES AT LEAST SIX (6) BUSINESS DAYS PRIOR TO THE ELECTION DEADLINE.

PRIOR TO THE ELECTION DEADLINE, CERTAIN HOLDERS OF POTASHCORP SHARES WILL BE ELIGIBLE TO MAKE AN ELECTION THAT MAY PERMIT THE DISPOSITION OF SUCH POTASHCORP SHARES TO OCCUR ON A TAX-DEFERRED BASIS FOR CANADIAN INCOME TAX PURPOSES. SUCH ELECTION IS DESCRIBED IN BOX D OF THIS LETTER OF TRANSMITTAL AND IN THE INFORMATION CIRCULAR AND HOLDERS OF POTASHCORP SHARES SHOULD CAREFULLY REVIEW SUCH

INFORMATION AND CONSIDER SEEKING PROFESSIONAL ADVICE REGARDING THE AVAILABILITY AND EFFECT OF MAKING SUCH ELECTION.

All Registered Shareholders must complete Box E. Each U.S. Person (as defined below) should complete and submit IRS Form W-9. See Instruction 6. Each Registered Shareholder who provides an address in Box A or Box B that is located within the United States or any territory or possession thereof and is not a U.S. Person should complete and submit the appropriate IRS Form W-8. See Instruction 6. If you require a Form W-8, please contact the Depositary.

Completion of the Arrangement is subject to the satisfaction or waiver of certain conditions. No New Parent Shares or any Fractional Share Cash Consideration (as defined below), if any, will be issued to PotashCorp Shareholders or holders of shares of Agrium prior to the effective time of the Arrangement, as set forth in the Plan of Arrangement (the “Effective Time”).

This Letter of Transmittal is for use by Registered Shareholders only and is not to be used by beneficial holders of PotashCorp Shares (the “Beneficial Shareholders”). A Beneficial Shareholder does not have PotashCorp Shares registered in its name; rather, such PotashCorp Shares are registered in the name of a broker, investment dealer, bank, trust company, nominee or other intermediary (each, an “Intermediary”) through which it purchased the shares or in the name of a clearing agency (such as CDS Clearing and Depository Services Inc.) of which the Intermediary is a participant. If you are a Beneficial Shareholder, you should contact your Intermediary for instructions and assistance in receiving the New Parent Shares and any Fractional Share Cash Consideration for such PotashCorp Shares, as well as any Dividends (as defined below), and providing instructions regarding the election described herein.

If you are a DRIP Participant, please note that, in connection with the Arrangement, the DRIP will be terminated prior to the Effective Time (including prior to the record date for any dividend that is expected to have a payment date after the Effective Time). As a result of such termination of the DRIP, (i) each whole PotashCorp Share held in the DRIP (“DRIP Shares”) will participate in, and be exchanged for New Parent Shares and Fractional Share Cash Consideration (as defined below) pursuant to, the Arrangement, and (ii) DRIP Participants will be mailed a cheque for the market value of any fraction of a DRIP Share calculated by PotashCorp in accordance with the terms of the DRIP. All DRIP Shares are held in book entry form and no certificates have been, or will be, issued to DRIP Participants upon termination of the DRIP in connection with the Arrangement and prior to the Effective Time, however, DRIP Participants are nonetheless required to submit this Letter of Transmittal, which will apply in respect of any DRIP Shares held by such DRIP Participant. In order to submit this Letter of Transmittal in respect of DRIP Shares, a DRIP Participant must validly complete and duly execute this Letter of Transmittal, including indicating a deposit of DRIP Shares in the appropriate box on page 3 hereof. See “Note Regarding Dividends Declared But Not Yet Paid on PotashCorp Shares” below for additional information regarding PotashCorp dividends and the DRIP.

No certificates representing fractional New Parent Shares shall be issued upon the surrender for exchange of certificates by PotashCorp Shareholders pursuant to the Arrangement and no dividend, stock split or other change in the capital structure of New Parent shall relate to any such fractional security and such fractional interests shall not entitle the owner thereof to exercise any rights as a holder of New Parent Shares. In lieu of any fractional New Parent Shares, a PotashCorp Shareholder otherwise entitled to a fractional interest in a New Parent Share shall receive a cash amount (less any applicable withholding taxes) determined by reference to the volume weighted average trading price of New Parent Shares on the TSX on the first five trading days on which such shares trade on such exchange following (but not including) the Effective Date (the “Fractional Share Cash Consideration”). Former PotashCorp Shareholders will also be entitled to receive, at the time of such surrender for exchange of certificates, without interest, all dividends or other distributions made after the Effective Time in respect of the New Parent Shares to which such holder is entitled, less any applicable withholdings (collectively, “Dividends”).

In order to receive the New Parent Shares and Fractional Share Cash Consideration, if any, that a holder of PotashCorp Shares is entitled to receive pursuant to the Arrangement, as well as any Dividends, Registered Shareholders are required to deposit the certificate(s) representing their PotashCorp Shares with the Depositary. This Letter of Transmittal, properly completed and duly executed, together with all other required documents, must accompany the certificate(s) for PotashCorp Shares deposited for receipt of New Parent Shares and any Fractional Share Cash Consideration pursuant to the Arrangement, as well as any Dividends.

- 2 -

Whether or not the undersigned delivers the required documentation to the Depositary, as of the Effective Time, the undersigned will cease to be a holder of PotashCorp Shares and, subject to the ultimate expiry deadline identified below, will only be entitled to receive the New Parent Shares and the Fractional Share Cash Consideration, if any, to which the undersigned is entitled under the Arrangement, as well as any Dividends. REGISTERED SHAREHOLDERS WHO DO NOT DELIVER CERTIFICATES REPRESENTING THEIR POTASHCORP SHARES AND ALL OTHER REQUIRED DOCUMENTS TO THE DEPOSITARY ON OR BEFORE THE DAY THAT IS THREE YEARS LESS ONE DAY FROM THE EFFECTIVE DATE WILL LOSE THEIR RIGHT TO RECEIVE ANY CONSIDERATION FOR THEIR POTASHCORP SHARES AND ANY CLAIM OR INTEREST OF ANY KIND OR NATURE AGAINST NEW PARENT, AGRIUM OR POTASHCORP OR THE DEPOSITARY, INCLUDING WITH RESPECT TO ANY DIVIDENDS.

Delivery of this Letter of Transmittal to an address other than as set forth on the last page of this Letter of Transmittal will not constitute a valid delivery. If PotashCorp Shares are registered in different names, a separate Letter of Transmittal must be submitted for each different Registered Shareholder. See Instruction 2.

The undersigned hereby deposits with the Depositary the enclosed certificate(s) representing PotashCorp Shares, details of which are as follows:

| Name of Registered Shareholder

|

Certificate Number(s)

|

Number of PotashCorp Shares

| ||

| TOTAL: |

| ☐ | Check here if you hold PotashCorp Shares in the DRIP. By checking here the undersigned hereby deposits the undersigned’s DRIP Shares, if any, with the Depositary. |

| ☐ | Check here if some or all of your PotashCorp Share certificates have been lost, stolen or destroyed. Please review Instruction 7 for the procedure to replace lost, stolen or destroyed certificates. |

(Please print or type. If space is insufficient, please attach a list to this Letter of Transmittal in the above form. See Instruction 9)

It is understood that, upon receipt of this duly completed and signed Letter of Transmittal and of the certificate(s) representing the PotashCorp Shares deposited herewith, as well as any DRIP Shares (collectively, the “Deposited PotashCorp Shares”) and following the Effective Time of the Arrangement, the Depositary will deliver to the undersigned, in accordance with the issuance and delivery instructions provided in Box A and Box B below, share certificates (“New Parent Share Certificates”) or Direct Registration System advices (“DRS Advices”) representing the New Parent Shares and a cheque representing the Fractional Share Cash Consideration that the undersigned is entitled to receive under the Arrangement, as well as a cheque representing any Dividends, or hold such New Parent Share Certificates or DRS Advices and cheque(s) for pick-up in accordance with the instructions set out in Box C below, and the certificate representing the Deposited PotashCorp Shares will forthwith be cancelled. If no selection is made in Box A between receiving New Parent Share Certificates and DRS Advices, then DRS Advices will be issued. If neither Box A nor Box B is completed, DRS Advices representing New Parent Shares issued in exchange for the Deposited PotashCorp Shares will be issued in the name of the registered holder of the Deposited PotashCorp Shares and it, along with the cheque representing the Fractional Share Cash Consideration, as well as a cheque representing any Dividends, will be mailed to the address of the registered holder of the Deposited PotashCorp Shares as it appears on the register of PotashCorp.

The undersigned holder of PotashCorp Shares represents and warrants in favour of PotashCorp and New Parent that: (i) the undersigned is the registered and legal owner of the Deposited PotashCorp Shares, has good right and title to the rights represented by the Deposited PotashCorp Shares and that such Deposited PotashCorp Shares represent all of the PotashCorp Shares owned, directly or indirectly, by the undersigned; (ii) such Deposited PotashCorp Shares are owned by the undersigned free and clear of all mortgages, liens, charges, encumbrances, security interests and adverse claims; (iii) the undersigned has full power and authority to execute and deliver this Letter of Transmittal and to deposit, assign, transfer and deliver the Deposited PotashCorp Shares and that, when the New Parent Shares and any cheque(s) representing the Fractional Share Cash Consideration or Dividends are delivered, none of Agrium, PotashCorp or New Parent, or any affiliate thereof or

- 3 -

successor thereto will be subject to any adverse claim in respect of such Deposited PotashCorp Shares; (iv) the Deposited PotashCorp Shares have not been sold, assigned or transferred, nor has any agreement been entered into to sell, assign or transfer any such Deposited PotashCorp Shares, to any other person; (v) the transfer of the Deposited PotashCorp Shares complies with all applicable laws; (vi) all information inserted by the undersigned into this Letter of Transmittal is complete, true and accurate; (vii) the delivery of the applicable number of New Parent Shares and a cheque representing the applicable Fractional Share Cash Consideration, as well as a cheque representing any Dividends, will discharge any and all obligations of Agrium, PotashCorp, New Parent and the Depositary with respect to the matters contemplated by this Letter of Transmittal and the Arrangement; and (viii) if the undersigned has elected in Box D to have its Deposited PotashCorp Shares be treated as Elected PotashCorp Shares (as defined below), the undersigned is not, and will not be as of the Effective Time, (a) a person who holds the PotashCorp Shares other than as capital property for purposes of the Tax Act, (b) a non-resident person for the purposes of the Tax Act, unless that Registered Shareholder holds the Deposited PotashCorp Shares as part of a business carried on by the person in Canada, as determined for the purposes of the Tax Act, (c) a partnership that is not a Canadian partnership for the purposes of the Tax Act, or (d) a person exempt from tax under section 149 of the Tax Act, which for greater certainty, includes a trust governed by a registered retirement savings plan, registered retirement income fund, registered disability savings plan, deferred profit sharing plan, registered education savings plan or a tax-free savings account, each as defined in the Tax Act. These representations and warranties shall survive the completion of the Arrangement. The undersigned further acknowledges receipt of the Information Circular.

The undersigned revokes any and all authority, other than as granted in this Letter of Transmittal, whether as agent, attorney-in-fact, proxy or otherwise, previously conferred or agreed to be conferred by the undersigned at any time with respect to the Deposited PotashCorp Shares and no subsequent authority, whether as agent, attorney-in-fact, proxy or otherwise, will be granted with respect to the Deposited PotashCorp Shares.

The undersigned hereby agrees to transfer, effective at the Effective Time and pursuant to the Arrangement, all right, title and interest in the Deposited PotashCorp Shares and irrevocably appoints and constitutes the Depositary, each officer of New Parent and PotashCorp and any other person designated by New Parent or PotashCorp in writing, the lawful attorney of the undersigned, with full power of substitution (such powers of attorney, being coupled with an interest, being irrevocable) to deliver the Deposited PotashCorp Shares pursuant to the Arrangement and to effect the transfer of the Deposited PotashCorp Shares on the books of PotashCorp to the extent and in the manner provided under the Arrangement.

The undersigned will, upon request, execute any signature guarantees or additional documents deemed by the Depositary to be reasonably necessary or desirable to complete the transfer of the Deposited PotashCorp Shares contemplated by this Letter of Transmittal.

The undersigned agrees that all questions as to validity, form, eligibility (including timely receipt) and acceptance of any PotashCorp Shares transferred in connection with the Arrangement shall be determined by New Parent and PotashCorp in their sole discretion and that such determination shall be final and binding and acknowledges that there is no duty or obligation upon PotashCorp, New Parent, the Depositary or any other person to give notice of any defect or irregularity in any such surrender of PotashCorp Shares and no liability will be incurred by any of them for failure to give any such notice.

The undersigned hereby acknowledges that the delivery of the Deposited PotashCorp Shares shall be effected and the risk of loss to such Deposited PotashCorp Shares shall pass only upon proper receipt thereof by the Depositary.

The undersigned acknowledges that all authority conferred, or agreed to be conferred, by the undersigned herein may be exercised during any subsequent legal incapacity of the undersigned and shall survive the death, incapacity, bankruptcy or insolvency of the undersigned and all obligations of the undersigned herein shall be binding upon the heirs, personal or legal representatives, successors and assigns of the undersigned.

The undersigned acknowledges that New Parent, Agrium and/or PotashCorp may be required to disclose personal information in respect of the undersigned and consents to disclosure of personal information in respect of the undersigned to (i) stock exchanges or securities regulatory authorities, (ii) the Depositary, (iii) any of the parties to the Arrangement, (iv) legal counsel to any of the parties to the Arrangement, and (v) as otherwise required by any applicable law.

The undersigned instructs the Depositary to mail the New Parent Share Certificates or DRS Advices representing the New Parent Shares and the cheque representing the Fractional Share Cash Consideration that the undersigned is entitled to pursuant to the Arrangement in exchange for the Deposited PotashCorp Shares, as well as a cheque representing any

- 4 -

Dividends, promptly after the Effective Time, by first-class insured mail, postage prepaid, to the undersigned, or to hold such New Parent Share Certificates or DRS Advices representing the New Parent Shares and the cheque(s) representing the Fractional Share Cash Consideration for the Deposited PotashCorp Shares and Dividends, if any, for pick-up, in accordance with the instructions given in Box C below.

The undersigned acknowledges that if the Arrangement is completed, the delivery of Deposited PotashCorp Shares pursuant to this Letter of Transmittal is irrevocable. If the Arrangement is not completed or proceeded with, the enclosed certificate(s) and all other ancillary documents will be returned as soon as possible to the undersigned at the address set out below in Box A or Box B, as applicable, or, failing such address being specified, to the undersigned at the last address of the undersigned as it appears on the securities register of PotashCorp.

It is understood that the undersigned will not receive the New Parent Shares, the cheque representing the Fractional Share Cash Consideration under the Arrangement, or the cheque representing any Dividends, in respect of the Deposited PotashCorp Shares until following the Effective Time and after certificate(s) representing the Deposited PotashCorp Shares owned by the undersigned are received by the Depositary at the address set forth on the back of this Letter of Transmittal, together with a duly completed Letter of Transmittal and such additional documents as the Depositary may require, and until the same are processed by the Depositary. It is understood that under no circumstances will interest accrue or be paid in respect of the Deposited PotashCorp Shares in connection with the Arrangement, including on any Dividends.

The undersigned acknowledges that New Parent and the Depositary shall be entitled to deduct and withhold from any consideration otherwise payable to any former PotashCorp Shareholder under the Arrangement and from all Dividends or other distributions otherwise payable to any former PotashCorp Shareholder such amounts as New Parent or the Depositary is required or permitted to deduct and withhold with respect to such payment under the Tax Act or any provision of any applicable federal, provincial, state, local or foreign tax law or treaty (including the United States Internal Revenue Code of 1986 and the rules and regulations promulgated thereunder), in each case, as amended. To the extent that amounts are so withheld, such withheld amounts shall be treated for all purposes hereof as having been paid to the former PotashCorp Shareholder in respect of which such deduction and withholding was made, provided that such withheld amounts are actually remitted to the appropriate taxing authority. The undersigned acknowledges that it has consulted or has had the opportunity to consult its own tax advisor with respect to the potential income tax consequences to it of the Arrangement, including any elections to be made in respect thereof.

The undersigned understands and acknowledges that the New Parent Shares to be received by it pursuant to the Arrangement have not been registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and are being issued in reliance on the exemption from the registration requirements thereof provided by Section 3(a)(10) of the Securities Act. Upon issuance, the New Parent Shares will be transferable without restriction under the Securities Act, except by persons who are “affiliates” (as such term is defined under the Securities Act) of New Parent as of such time, or were “affiliates” of Agrium or PotashCorp within 90 days prior to such time. Persons who may be deemed to be “affiliates” of an issuer include individuals or entities that, directly or indirectly, control, are controlled by, or are under common control with, the issuer, whether through the ownership of voting securities, by contract, or otherwise, and generally include executive officers and directors of the issuer as well as principal shareholders of the issuer. Any resale of such New Parent Shares by such an affiliate (or former affiliate) may be subject to the registration requirements of the Securities Act, absent an exemption therefrom as more fully described in the Information Circular.

Following the Arrangement, New Parent will be deemed to be a “successor issuer” to Agrium and PotashCorp under the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), and consequently the New Parent Shares will be deemed to be registered under Section 12(b) of the Exchange Act.

The foregoing discussion is only a general overview of certain requirements of United States federal securities laws applicable to the New Parent Shares received upon completion of the Arrangement. All holders of such securities are urged to consult with counsel to ensure that any action taken with respect to their securities complies with applicable securities legislation, including any resale of such securities.

By reason of the use by the undersigned of an English language Letter of Transmittal, the undersigned shall be deemed to have required that any contract in connection with the delivery of the PotashCorp Shares pursuant to the Arrangement through this Letter of Transmittal, as well as all documents related thereto, be drawn exclusively in the English language. En raison de l’utilisation d’une lettre d’envoi en langue anglaise par le soussigné, le soussigné et les destinataires sont présumés

- 5 -

avoir requis que tout contrat relié à l’envoi d’actions ordinaires de PotashCorp en vertue de l’arrangement au moyen de la présente lettre d’envoi, de même que tous les documents qui s’y rapportent, soient rédigés exclusivement en langue anglaise.

This letter will be governed by and construed in accordance with the laws of the Province of Ontario and the federal laws of Canada applicable therein. Any Fractional Share Cash Consideration payable under the Arrangement will be paid in Canadian dollars.

Note Regarding Dividends Declared But Not Yet Paid on PotashCorp Shares

Where the Effective Date occurs before the payment date, but after the record date, of any dividend declared by the PotashCorp Board in respect of PotashCorp Shares, such dividend will be paid in cash in accordance with ordinary procedures established by PotashCorp and its registrar and transfer agent. As a result of the termination of the DRIP in connection with the Arrangement and prior to the Effective Date (including prior to the record date for any dividend that is expected to have a payment date after the Effective Time), any such dividend will not be subject to the DRIP and will be paid in cash as described in the preceding sentence.

- 6 -

PLEASE COMPLETE THE FOLLOWING BOXES, AS APPROPRIATE.

| BOX A REGISTRATION INSTRUCTIONS

Issue New Parent Shares and any cheque in the name of:

Issue in the Name of (please print) Address:

(include postal or zip code)

Social Insurance Number (or Taxpayer Identification Number)

Evidence issuance of New Parent Shares in the form of (see

☐ New Parent Share Certificate ☐ DRS Advice

|

BOX B SPECIAL ISSUANCE INSTRUCTIONS

To be completed ONLY if the New Parent Shares and any

Send to (please print)

Address:

(include postal or zip code) |

BOX C

SPECIAL PICK-UP INSTRUCTIONS

| ☐ | Mark here if the New Parent Share Certificate or DRS Advice representing the New Parent Shares and any cheque representing the Fractional Share Cash Consideration issuable in exchange for the PotashCorp Shares (in accordance with the issuance instructions provided in Box A above), as well as any cheque representing Dividends, is to be held for pick-up at the office of the Depositary where the Letter of Transmittal is deposited. |

- 7 -

BOX D

ELECTION

This Box D applies only to Registered Shareholders that meet specific eligibility criteria (as set out below) and that choose to elect to have their PotashCorp Shares be Elected PotashCorp Shares. An election made by a Registered Shareholder that does not meet the eligibility criteria described herein will not be valid and such Registered Shareholder will be treated in the manner the Registered Shareholder would have been treated if an election had not been made.

A summary of the principal Canadian federal income tax considerations in respect of the Arrangement including in respect of an eligible Registered Shareholder that elects to have Elected PotashCorp Shares, is included in the Information Circular under “Part I – The Arrangement—Certain Canadian Federal Income Tax Considerations”.

Under the Arrangement, Registered Shareholders that hold Elected PotashCorp Shares will dispose of their PotashCorp Shares to New Parent in exchange for New Parent Shares in accordance with the terms of the Arrangement. Registered Shareholders that hold PotashCorp Shares that are not Elected PotashCorp Shares will dispose of their Shares to PotashCorp AcquisitionCo in exchange for New Parent Shares in accordance with the terms of the Arrangement.

An “Elected PotashCorp Share” means any PotashCorp Share that a Registered Shareholder (other than New Parent) shall have validly elected (by marking the appropriate box below and depositing this Letter of Transmittal with the Depositary prior to the Election Deadline) to transfer directly to New Parent under the Arrangement as provided for in the Plan of Arrangement, provided that at the Effective Time such electing Registered Shareholder is not (a) a person who holds the PotashCorp Share other than as capital property for purposes of the Tax Act, (b) a non-resident person for the purposes of the Tax Act, unless that Registered Shareholder holds the PotashCorp Share as part of a business carried on by the person in Canada, as determined for the purposes of the Tax Act, (c) a partnership that is not a Canadian partnership for the purposes of the Tax Act, or (d) a person exempt from tax under section 149 of the Tax Act, which, for greater certainty, includes a trust governed by a registered retirement savings plan, registered retirement income fund, registered disability savings plan, deferred profit sharing plan, registered education savings plan or a tax-free savings account, each as defined in the Tax Act.

A Registered Shareholder that is eligible to elect and so elects to have its PotashCorp Shares be Elected PotashCorp Shares will dispose of its Elected PotashCorp Shares to New Parent under the Arrangement in a tax-deferred transaction, provided the Registered Shareholder does not include any portion of the capital gain (or capital loss) otherwise determined in respect of the exchange in computing its income in its tax return for the year in which the exchange occurs. For more information refer to the summary of the principal Canadian federal income tax considerations in respect of the Arrangement included in the Information Circular under “Part I – The Arrangement—Certain Canadian Federal Income Tax Considerations”.

A Registered Shareholder that is not eligible to or does not elect to have its PotashCorp Shares be Elected PotashCorp Shares will dispose of its PotashCorp Shares to PotashCorp AcquisitionCo under the Arrangement in a potentially taxable transaction. The Canadian federal income tax consequences may be materially different for Registered Shareholders that hold Elected PotashCorp Shares and Registered Shareholders that do not hold Elected PotashCorp Shares. Registered Shareholders should consult their own tax advisors for advice in respect of the consequences to them of the Arrangement having regard to their particular circumstances.

All eligible Registered Shareholders that wish to elect must place an “X” in the box below.

| ☐ | Mark here if you are a Registered Shareholder that is eligible, and hereby elects, to have its PotashCorp Shares be treated as Elected PotashCorp Shares. NOTWITHSTANDING THIS ELECTION, IF THE ADDRESS PROVIDED IN BOX A OR BOX B IS LOCATED OUTSIDE OF CANADA, A REGISTERED SHAREHOLDER WILL NOT BE CONSIDERED TO BE ELIGIBLE TO MAKE THIS ELECTION AND HAVE ITS POTASHCORP SHARES BE TREATED AS ELECTED POTASHCORP SHARES. |

- 8 -

BOX E

U.S. STATUS

All Registered Shareholders must place an “X” in the applicable box below. See Instruction 6.

| ☐ | The Registered Shareholder is not a U.S. Shareholder, a person in the United States, or a person acting for the account or benefit of a U.S. Person or a person in the United States. |

| ☐ | The Registered Shareholder is a U.S. Shareholder, a person in the United States, or a person acting for the account or benefit of a U.S. Person or a person in the United States. |

A “U.S. Shareholder” is any Registered Shareholder that is either (a) providing an address in Box A or Box B that is located within the United States or any territory or possession thereof, or (b) a U.S. Person as described in Instruction 6. If you are a U.S. Shareholder or are acting on behalf of a U.S. Shareholder, then in order to avoid possible U.S. backup withholding you must complete the Form W-9 in Box H included below or otherwise provide certification that you are exempt from backup withholding, or provide the appropriate IRS Form W-8. If you require a copy of Form W-8, please contact the Depositary.

| BOX F SIGNATURE GUARANTEE

Signature guaranteed by (if required under Instruction 3)

Authorized Signature

Name of Guarantor (please print)

Address (please print)

Area Code and Telephone Number

|

BOX G SIGNATURE (as required under Instruction 2)

Dated

(Signature of Shareholder or Authorized Representative)

(Signature of any Joint Holder)

(Name of Shareholder)

(Name of Authorized Representative)

(Social Insurance Number or Taxpayer Identification Number)

(Daytime Telephone Number of Shareholder or Authorized Representative)

(Daytime Facsimile Number of Shareholder or Authorized Representative)

|

- 9 -

BOX H – FORM W-9

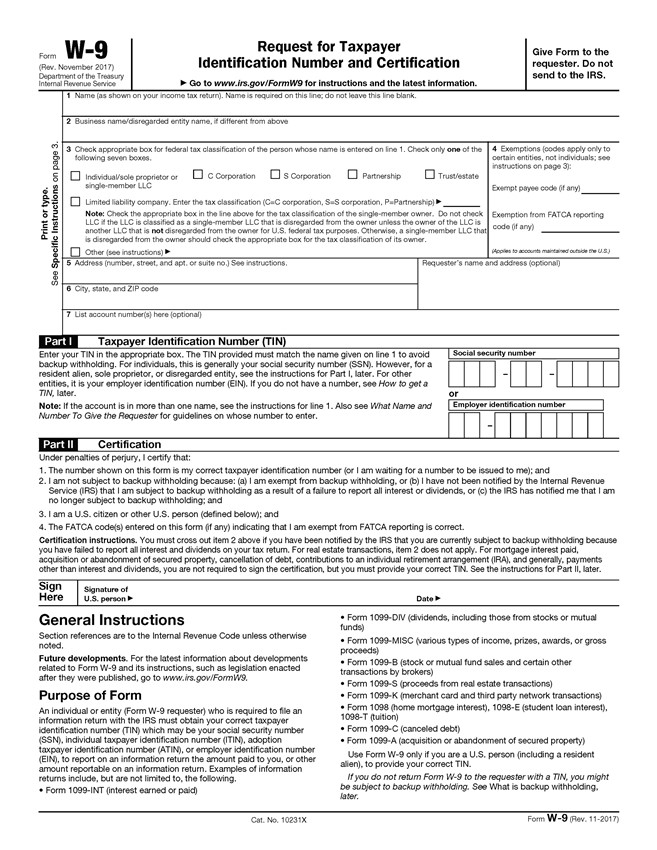

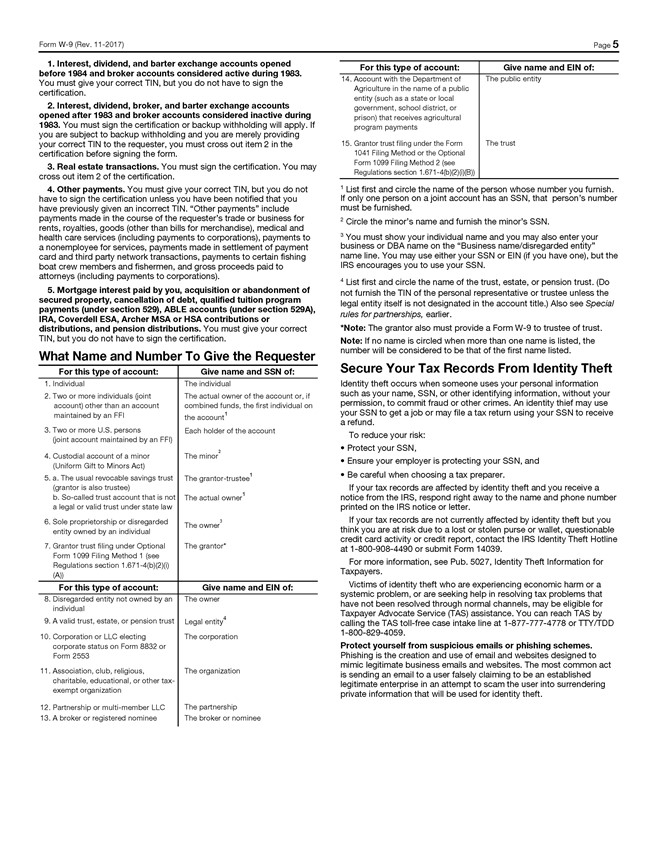

Request for Taxpayer W-9 Give Form to the Form (Rev. November 2017) Identification Number and Certification requester. Do not Department of the Treasury send to the IRS. Internal Revenue Service a Go to www.irs.gov/FormW9 for instructions and the latest information. 1Name (as shown on your income tax return). Name is required on this line; do not leave this line blank. 2Business name/disregarded entity name, if different from above 3.3 Check appropriate box for federal tax classification of the person whose name is entered on line 1. Check only one of the 4 Exemptions (codes apply only to following seven boxes. certain entities, not individuals; see page instructions on page 3): on Individual/sole proprietor or C Corporation S Corporation Partnership Trust/estate single-member LLC Exempt payee code (if any) type. Limited liability company. Enter the tax classification (C=C corporation, S=S corporation, P=Partnership) a or Note: Check the appropriate box in the line above for the tax classification of the single-member owner. Do not check Exemption from FATCA reporting LLC if the LLC is classified as a single-member LLC that is disregarded from the owner unless the owner of the LLC is code (if any) Print Instructions another LLC that is not disregarded from the owner for U.S. federal tax purposes. Otherwise, a single-member LLC that is disregarded from the owner should check the appropriate box for the tax classification of its owner. Other (see instructions) a (Applies to accounts maintained outside the U.S.) Specific5 Address (number, street, and apt. or suite no.) See instructions. Requester’s name and address (optional) See 6City, state, and ZIP code 7List account number(s) here (optional) Part I Taxpayer Identification Number (TIN) Enter your TIN in the appropriate box. The TIN provided must match the name given on line 1 to avoid Social security number backup withholding. For individuals, this is generally your social security number (SSN). However, for a resident alien, sole proprietor, or disregarded entity, see the instructions for Part I, later. For other ––entities, it is your employer identification number (EIN). If you do not have a number, see How to get a TIN, later. or Note: If the account is in more than one name, see the instructions for line 1. Also see What Name and Employer identification number Number To Give the Requester for guidelines on whose number to enter. – Part II Certification Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number (or I am waiting for a number to be issued to me); and 2. I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or (c) the IRS has notified me that I am no longer subject to backup withholding; and 3. I am a U.S. citizen or other U.S. person (defined below); and 4. The FATCA code(s) entered on this form (if any) indicating that I am exempt from FATCA reporting is correct. Certification instructions. You must cross out item 2 above if you have been notified by the IRS that you are currently subject to backup withholding because you have failed to report all interest and dividends on your tax return. For real estate transactions, item 2 does not apply. For mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirement arrangement (IRA), and generally, payments other than interest and dividends, you are not required to sign the certification, but you must provide your correct TIN. See the instructions for Part II, later. Sign Signature of Here U.S. person a General Instructions Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For the latest information about developments related to Form W-9 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/FormW9. Purpose of Form An individual or entity (Form W-9 requester) who is required to file an information return with the IRS must obtain your correct taxpayer identification number (TIN) which may be your social security number (SSN), individual taxpayer identification number (ITIN), adoption taxpayer identification number (ATIN), or employer identification number (EIN), to report on an information return the amount paid to you, or other amount reportable on an information return. Examples of information returns include, but are not limited to, the following. • Form 1099-INT (interest earned or paid) Date a • Form 1099-DIV (dividends, including those from stocks or mutual funds) • Form 1099-MISC (various types of income, prizes, awards, or gross proceeds) • Form 1099-B (stock or mutual fund sales and certain other transactions by brokers) • Form 1099-S (proceeds from real estate transactions) • Form 1099-K (merchant card and third party network transactions) • Form 1098 (home mortgage interest), 1098-E (student loan interest), 1098-T (tuition) • Form 1099-C (canceled debt) • Form 1099-A (acquisition or abandonment of secured property) Use Form W-9 only if you are a U.S. person (including a resident alien), to provide your correct TIN. If you do not return Form W-9 to the requester with a TIN, you might be subject to backup withholding. See What is backup withholding, later. Cat. No. 10231X Form W-9 (Rev. 11-2017)

- 10 -

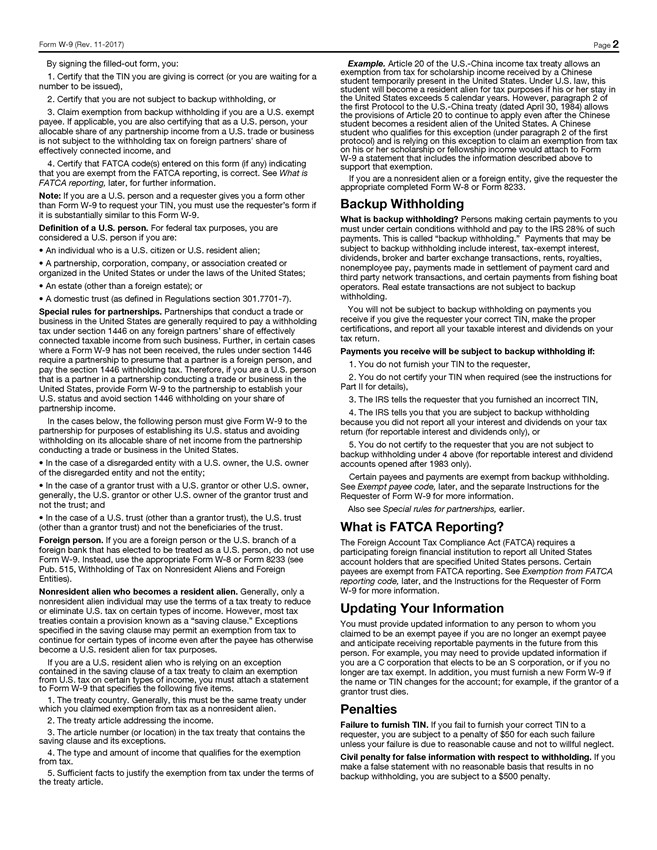

By signing the filled-out form, you: 1. Certify that the TIN you are giving is correct (or you are waiting for a number to be issued), 2. Certify that you are not subject to backup withholding, or 3. Claim exemption from backup withholding if you are a U.S. exempt payee. If applicable, you are also certifying that as a U.S. person, your allocable share of any partnership income from a U.S. trade or business is not subject to the withholding tax on foreign partners’ share of effectively connected income, and 4. Certify that FATCA code(s) entered on this form (if any) indicating that you are exempt from the FATCA reporting, is correct. See What is FATCA reporting, later, for further information. Note: If you are a U.S. person and a requester gives you a form other than Form W-9 to request your TIN, you must use the requester’s form if it is substantially similar to this Form W-9. Definition of a U.S. person. For federal tax purposes, you are considered a U.S. person if you are: • An individual who is a U.S. citizen or U.S. resident alien; • A partnership, corporation, company, or association created or organized in the United States or under the laws of the United States; • An estate (other than a foreign estate); or • A domestic trust (as defined in Regulations section 301.7701-7). Special rules for partnerships. Partnerships that conduct a trade or business in the United States are generally required to pay a withholding tax under section 1446 on any foreign partners’ share of effectively connected taxable income from such business. Further, in certain cases where a Form W-9 has not been received, the rules under section 1446 require a partnership to presume that a partner is a foreign person, and pay the section 1446 withholding tax. Therefore, if you are a U.S. person that is a partner in a partnership conducting a trade or business in the United States, provide Form W-9 to the partnership to establish your U.S. status and avoid section 1446 withholding on your share of partnership income. In the cases below, the following person must give Form W-9 to the partnership for purposes of establishing its U.S. status and avoiding withholding on its allocable share of net income from the partnership conducting a trade or business in the United States. • In the case of a disregarded entity with a U.S. owner, the U.S. owner of the disregarded entity and not the entity; • In the case of a grantor trust with a U.S. grantor or other U.S. owner, generally, the U.S. grantor or other U.S. owner of the grantor trust and not the trust; and • In the case of a U.S. trust (other than a grantor trust), the U.S. trust (other than a grantor trust) and not the beneficiaries of the trust. Foreign person. If you are a foreign person or the U.S. branch of a foreign bank that has elected to be treated as a U.S. person, do not use Form W-9. Instead, use the appropriate Form W-8 or Form 8233 (see Pub. 515, Withholding of Tax on Nonresident Aliens and Foreign Entities). Nonresident alien who becomes a resident alien. Generally, only a nonresident alien individual may use the terms of a tax treaty to reduce or eliminate U.S. tax on certain types of income. However, most tax treaties contain a provision known as a “saving clause.” Exceptions specified in the saving clause may permit an exemption from tax to continue for certain types of income even after the payee has otherwise become a U.S. resident alien for tax purposes. If you are a U.S. resident alien who is relying on an exception contained in the saving clause of a tax treaty to claim an exemption from U.S. tax on certain types of income, you must attach a statement to Form W-9 that specifies the following five items. 1. The treaty country. Generally, this must be the same treaty under which you claimed exemption from tax as a nonresident alien. 2. The treaty article addressing the income. 3. The article number (or location) in the tax treaty that contains the saving clause and its exceptions. 4. The type and amount of income that qualifies for the exemption from tax. 5. Sufficient facts to justify the exemption from tax under the terms of the treaty article. Example. Article 20 of the U.S.-China income tax treaty allows an exemption from tax for scholarship income received by a Chinese student temporarily present in the United States. Under U.S. law, this student will become a resident alien for tax purposes if his or her stay in the United States exceeds 5 calendar years. However, paragraph 2 of the first Protocol to the U.S.-China treaty (dated April 30, 1984) allows the provisions of Article 20 to continue to apply even after the Chinese student becomes a resident alien of the United States. A Chinese student who qualifies for this exception (under paragraph 2 of the first protocol) and is relying on this exception to claim an exemption from tax on his or her scholarship or fellowship income would attach to Form W-9 a statement that includes the information described above to support that exemption. If you are a nonresident alien or a foreign entity, give the requester the appropriate completed Form W-8 or Form 8233. Backup Withholding What is backup withholding? Persons making certain payments to you must under certain conditions withhold and pay to the IRS 28% of such payments. This is called “backup withholding.” Payments that may be subject to backup withholding include interest, tax-exempt interest, dividends, broker and barter exchange transactions, rents, royalties, nonemployee pay, payments made in settlement of payment card and third party network transactions, and certain payments from fishing boat operators. Real estate transactions are not subject to backup withholding. You will not be subject to backup withholding on payments you receive if you give the requester your correct TIN, make the proper certifications, and report all your taxable interest and dividends on your tax return. Payments you receive will be subject to backup withholding if: 1. You do not furnish your TIN to the requester, 2. You do not certify your TIN when required (see the instructions for Part II for details), 3. The IRS tells the requester that you furnished an incorrect TIN, 4. The IRS tells you that you are subject to backup withholding because you did not report all your interest and dividends on your tax return (for reportable interest and dividends only), or 5. You do not certify to the requester that you are not subject to backup withholding under 4 above (for reportable interest and dividend accounts opened after 1983 only). Certain payees and payments are exempt from backup withholding. See Exempt payee code, later, and the separate Instructions for the Requester of Form W-9 for more information. Also see Special rules for partnerships, earlier. What is FATCA Reporting? The Foreign Account Tax Compliance Act (FATCA) requires a participating foreign financial institution to report all United States account holders that are specified United States persons. Certain payees are exempt from FATCA reporting. See Exemption from FATCA reporting code, later, and the Instructions for the Requester of Form W-9 for more information. Updating Your Information You must provide updated information to any person to whom you claimed to be an exempt payee if you are no longer an exempt payee and anticipate receiving reportable payments in the future from this person. For example, you may need to provide updated information if you are a C corporation that elects to be an S corporation, or if you no longer are tax exempt. In addition, you must furnish a new Form W-9 if the name or TIN changes for the account; for example, if the grantor of a grantor trust dies. Penalties Failure to furnish TIN. If you fail to furnish your correct TIN to a requester, you are subject to a penalty of $50 for each such failure unless your failure is due to reasonable cause and not to willful neglect. Civil penalty for false information with respect to withholding. If you make a false statement with no reasonable basis that results in no backup withholding, you are subject to a $500 penalty.

- 11 -

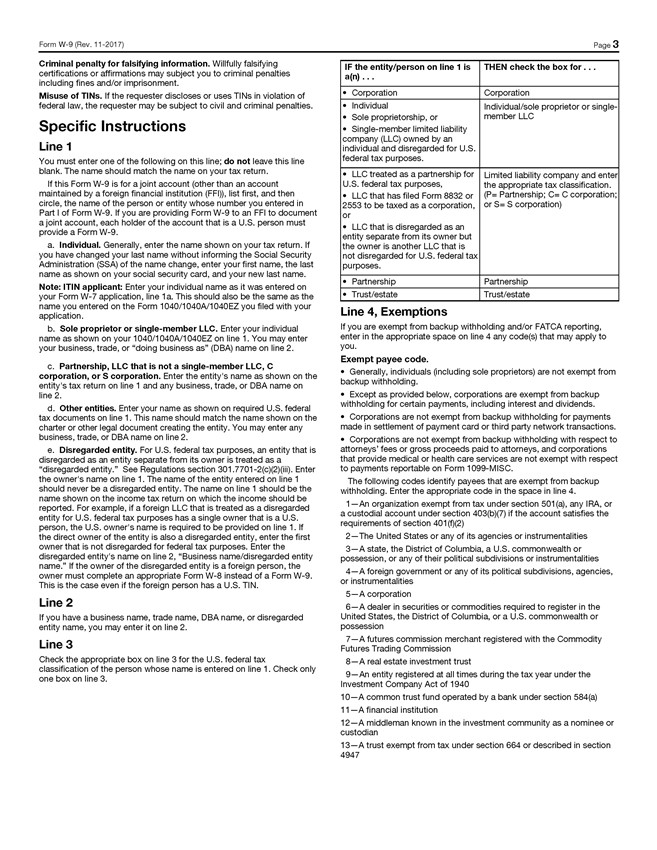

Criminal penalty for falsifying information. Willfully falsifying certifications or affirmations may subject you to criminal penalties including fines and/or imprisonment. Misuse of TINs. If the requester discloses or uses TINs in violation of federal law, the requester may be subject to civil and criminal penalties. Specific Instructions Line 1 You must enter one of the following on this line; do not leave this line blank. The name should match the name on your tax return. If this Form W-9 is for a joint account (other than an account maintained by a foreign financial institution (FFI)), list first, and then circle, the name of the person or entity whose number you entered in Part I of Form W-9. If you are providing Form W-9 to an FFI to document a joint account, each holder of the account that is a U.S. person must provide a Form W-9. a. Individual. Generally, enter the name shown on your tax return. If you have changed your last name without informing the Social Security Administration (SSA) of the name change, enter your first name, the last name as shown on your social security card, and your new last name. Note: ITIN applicant: Enter your individual name as it was entered on your Form W-7 application, line 1a. This should also be the same as the name you entered on the Form 1040/1040A/1040EZ you filed with your application. b. Sole proprietor or single-member LLC. Enter your individual name as shown on your 1040/1040A/1040EZ on line 1. You may enter your business, trade, or “doing business as” (DBA) name on line 2. c. Partnership, LLC that is not a single-member LLC, C corporation, or S corporation. Enter the entity’s name as shown on the entity’s tax return on line 1 and any business, trade, or DBA name on line 2. d. Other entities. Enter your name as shown on required U.S. federal tax documents on line 1. This name should match the name shown on the charter or other legal document creating the entity. You may enter any business, trade, or DBA name on line 2. e. Disregarded entity. For U.S. federal tax purposes, an entity that is disregarded as an entity separate from its owner is treated as a “disregarded entity.” See Regulations section 301.7701-2(c)(2)(iii). Enter the owner’s name on line 1. The name of the entity entered on line 1 should never be a disregarded entity. The name on line 1 should be the name shown on the income tax return on which the income should be reported. For example, if a foreign LLC that is treated as a disregarded entity for U.S. federal tax purposes has a single owner that is a U.S. person, the U.S. owner’s name is required to be provided on line 1. If the direct owner of the entity is also a disregarded entity, enter the first owner that is not disregarded for federal tax purposes. Enter the disregarded entity’s name on line 2, “Business name/disregarded entity name.” If the owner of the disregarded entity is a foreign person, the owner must complete an appropriate Form W-8 instead of a Form W-9. This is the case even if the foreign person has a U.S. TIN. Line 2 If you have a business name, trade name, DBA name, or disregarded entity name, you may enter it on line 2. Line 3 Check the appropriate box on line 3 for the U.S. federal tax classification of the person whose name is entered on line 1. Check only one box on line 3. IF the entity/person on line 1 is THEN check the box for a(n) • Corporation Corporation • Individual Individual/sole proprietor or single- • Sole proprietorship, or member LLC • Single-member limited liability company (LLC) owned by an individual and disregarded for U.S. federal tax purposes. • LLC treated as a partnership for Limited liability company and enter U.S. federal tax purposes, the appropriate tax classification. • LLC that has filed Form 8832 or (P= Partnership; C= C corporation; 2553 to be taxed as a corporation, or S= S corporation) or • LLC that is disregarded as an entity separate from its owner but the owner is another LLC that is not disregarded for U.S. federal tax purposes. • Partnership Partnership • Trust/estate Trust/estate Line 4, Exemptions If you are exempt from backup withholding and/or FATCA reporting, enter in the appropriate space on line 4 any code(s) that may apply to you. Exempt payee code. • Generally, individuals (including sole proprietors) are not exempt from backup withholding. • Except as provided below, corporations are exempt from backup withholding for certain payments, including interest and dividends. • Corporations are not exempt from backup withholding for payments made in settlement of payment card or third party network transactions. • Corporations are not exempt from backup withholding with respect to attorneys’ fees or gross proceeds paid to attorneys, and corporations that provide medical or health care services are not exempt with respect to payments reportable on Form 1099-MISC. The following codes identify payees that are exempt from backup withholding. Enter the appropriate code in the space in line 4. 1—An organization exempt from tax under section 501(a), any IRA, or a custodial account under section 403(b)(7) if the account satisfies the requirements of section 401(f)(2) 2—The United States or any of its agencies or instrumentalities 3—A state, the District of Columbia, a U.S. commonwealth or possession, or any of their political subdivisions or instrumentalities 4—A foreign government or any of its political subdivisions, agencies, or instrumentalities 5—A corporation 6—A dealer in securities or commodities required to register in the United States, the District of Columbia, or a U.S. commonwealth or possession 7—A futures commission merchant registered with the Commodity Futures Trading Commission 8—A real estate investment trust 9—An entity registered at all times during the tax year under the Investment Company Act of 1940 10—A common trust fund operated by a bank under section 584(a) 11—A financial institution 12—A middleman known in the investment community as a nominee or custodian 13—A trust exempt from tax under section 664 or described in section 4947

- 12 -

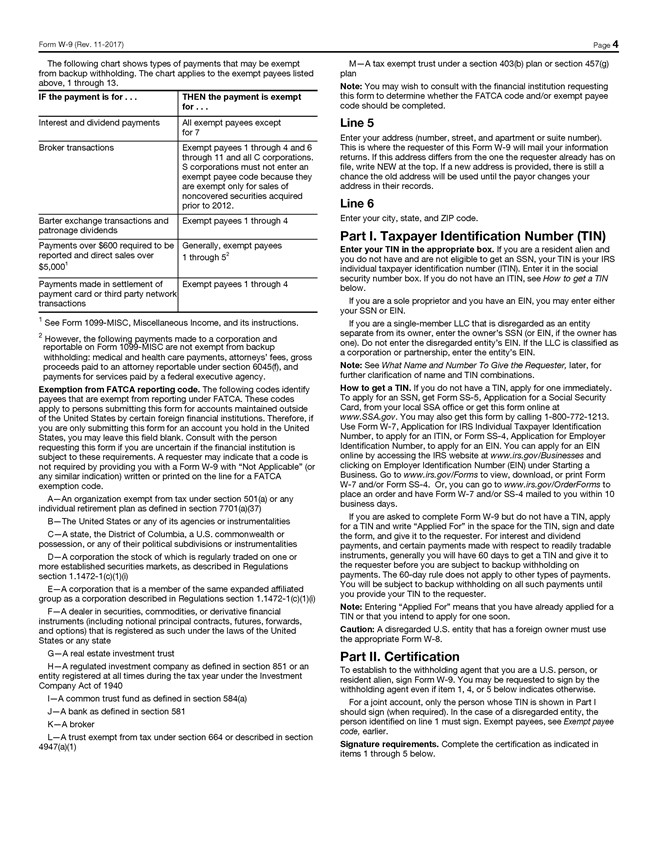

The following chart shows types of payments that may be exempt from backup withholding. The chart applies to the exempt payees listed above, 1 through 13. IF the payment is for THEN the payment is exempt for Interest and dividend payments All exempt payees except for 7 Broker transactions Exempt payees 1 through 4 and 6 through 11 and all C corporations. S corporations must not enter an exempt payee code because they are exempt only for sales of noncovered securities acquired prior to 2012. Barter exchange transactions and Exempt payees 1 through 4 patronage dividends Payments over $600 required to be Generally, exempt payees reported and direct sales over 1 through 52 $5,0001 Payments made in settlement of Exempt payees 1 through 4 payment card or third party network transactions 1 See Form 1099-MISC, Miscellaneous Income, and its instructions. 2 However, the following payments made to a corporation andreportable on Form 1099-MISC are not exempt from backupwithholding: medical and health care payments, attorneys’ fees, gross proceeds paid to an attorney reportable under section 6045(f), and payments for services paid by a federal executive agency. Exemption from FATCA reporting code. The following codes identify payees that are exempt from reporting under FATCA. These codes apply to persons submitting this form for accounts maintained outside of the United States by certain foreign financial institutions. Therefore, if you are only submitting this form for an account you hold in the United States, you may leave this field blank. Consult with the person requesting this form if you are uncertain if the financial institution is subject to these requirements. A requester may indicate that a code is not required by providing you with a Form W-9 with “Not Applicable” (or any similar indication) written or printed on the line for a FATCA exemption code. A—An organization exempt from tax under section 501(a) or any individual retirement plan as defined in section 7701(a)(37) B—The United States or any of its agencies or instrumentalities C—A state, the District of Columbia, a U.S. commonwealth or possession, or any of their political subdivisions or instrumentalities D—A corporation the stock of which is regularly traded on one or more established securities markets, as described in Regulations section 1.1472-1(c)(1)(i) E—A corporation that is a member of the same expanded affiliated group as a corporation described in Regulations section 1.1472-1(c)(1)(i) F—A dealer in securities, commodities, or derivative financial instruments (including notional principal contracts, futures, forwards, and options) that is registered as such under the laws of the United States or any state G—A real estate investment trust H—A regulated investment company as defined in section 851 or an entity registered at all times during the tax year under the Investment Company Act of 1940 I—A common trust fund as defined in section 584(a) J—A bank as defined in section 581 K—A broker L—A trust exempt from tax under section 664 or described in section 4947(a)(1) M—A tax exempt trust under a section 403(b) plan or section 457(g) plan Note: You may wish to consult with the financial institution requesting this form to determine whether the FATCA code and/or exempt payee code should be completed. Line 5 Enter your address (number, street, and apartment or suite number). This is where the requester of this Form W-9 will mail your information returns. If this address differs from the one the requester already has on file, write NEW at the top. If a new address is provided, there is still a chance the old address will be used until the payor changes your address in their records. Line 6 Enter your city, state, and ZIP code. Part I. Taxpayer Identification Number (TIN) Enter your TIN in the appropriate box. If you are a resident alien and you do not have and are not eligible to get an SSN, your TIN is your IRS individual taxpayer identification number (ITIN). Enter it in the social security number box. If you do not have an ITIN, see How to get a TIN below. If you are a sole proprietor and you have an EIN, you may enter either your SSN or EIN. If you are a single-member LLC that is disregarded as an entity separate from its owner, enter the owner’s SSN (or EIN, if the owner has one). Do not enter the disregarded entity’s EIN. If the LLC is classified as a corporation or partnership, enter the entity’s EIN. Note: See What Name and Number To Give the Requester, later, for further clarification of name and TIN combinations. How to get a TIN. If you do not have a TIN, apply for one immediately. To apply for an SSN, get Form SS-5, Application for a Social Security Card, from your local SSA office or get this form online at www.SSA.gov. You may also get this form by calling 1-800-772-1213. Use Form W-7, Application for IRS Individual Taxpayer Identification Number, to apply for an ITIN, or Form SS-4, Application for Employer Identification Number, to apply for an EIN. You can apply for an EIN online by accessing the IRS website at www.irs.gov/Businesses and clicking on Employer Identification Number (EIN) under Starting a Business. Go to www.irs.gov/Forms to view, download, or print Form W-7 and/or Form SS-4. Or, you can go to www.irs.gov/OrderForms to place an order and have Form W-7 and/or SS-4 mailed to you within 10 business days. If you are asked to complete Form W-9 but do not have a TIN, apply for a TIN and write “Applied For” in the space for the TIN, sign and date the form, and give it to the requester. For interest and dividend payments, and certain payments made with respect to readily tradable instruments, generally you will have 60 days to get a TIN and give it to the requester before you are subject to backup withholding on payments. The 60-day rule does not apply to other types of payments. You will be subject to backup withholding on all such payments until you provide your TIN to the requester. Note: Entering “Applied For” means that you have already applied for a TIN or that you intend to apply for one soon. Caution: A disregarded U.S. entity that has a foreign owner must use the appropriate Form W-8. Part II. Certification To establish to the withholding agent that you are a U.S. person, or resident alien, sign Form W-9. You may be requested to sign by the withholding agent even if item 1, 4, or 5 below indicates otherwise. For a joint account, only the person whose TIN is shown in Part I should sign (when required). In the case of a disregarded entity, the person identified on line 1 must sign. Exempt payees, see Exempt payee code, earlier. Signature requirements. Complete the certification as indicated in items 1 through 5 below.

- 13 -

1. Interest, dividend, and barter exchange accounts opened before 1984 and broker accounts considered active during 1983. You must give your correct TIN, but you do not have to sign the certification. 2. Interest, dividend, broker, and barter exchange accounts opened after 1983 and broker accounts considered inactive during 1983. You must sign the certification or backup withholding will apply. If you are subject to backup withholding and you are merely providing your correct TIN to the requester, you must cross out item 2 in the certification before signing the form. 3. Real estate transactions. You must sign the certification. You may cross out item 2 of the certification. 4. Other payments. You must give your correct TIN, but you do not have to sign the certification unless you have been notified that you have previously given an incorrect TIN. “Other payments” include payments made in the course of the requester’s trade or business for rents, royalties, goods (other than bills for merchandise), medical and health care services (including payments to corporations), payments to a nonemployee for services, payments made in settlement of payment card and third party network transactions, payments to certain fishing boat crew members and fishermen, and gross proceeds paid to attorneys (including payments to corporations). 5. Mortgage interest paid by you, acquisition or abandonment of secured property, cancellation of debt, qualified tuition program payments (under section 529), ABLE accounts (under section 529A), IRA, Coverdell ESA, Archer MSA or HSA contributions or distributions, and pension distributions. You must give your correct TIN, but you do not have to sign the certification. What Name and Number To Give the Requester For this type of account: Give name and SSN of: 1. Individual The individual 2. Two or more individuals (joint The actual owner of the account or, if account) other than an account combined funds, the first individual on maintained by an FFI the account1 3. Two or more U.S. persons Each holder of the account (joint account maintained by an FFI) 4. Custodial account of a minor The minor ² (Uniform Gift to Minors Act) 5. a. The usual revocable savings trust The grantor-trustee1 (grantor is also trustee) b. So-called trust account that is not The actual owner1 a legal or valid trust under state law 6. Sole proprietorship or disregarded The owner ³ entity owned by an individual 7. Grantor trust filing under Optional The grantor* Form 1099 Filing Method 1 (see Regulations section 1.671-4(b)(2)(i) (A)) For this type of account: Give name and EIN of: 8. Disregarded entity not owned by an The owner individual 9. A valid trust, estate, or pension trust Legal entity4 10. Corporation or LLC electing The corporation corporate status on Form 8832 or Form 2553 11. Association, club, religious, The organization charitable, educational, or other tax-exempt organization 12. Partnership or multi-member LLC The partnership 13. A broker or registered nominee The broker or nominee For this type of account: Give name and EIN of: 14. Account with the Department of The public entity Agriculture in the name of a public entity (such as a state or local government, school district, or prison) that receives agricultural program payments 15. Grantor trust filing under the Form The trust 1041 Filing Method or the Optional Form 1099 Filing Method 2 (see Regulations section 1.671-4(b)(2)(i)(B)) 1 List first and circle the name of the person whose number you furnish. If only one person on a joint account has an SSN, that person’s number must be furnished. 2 Circle the minor’s name and furnish the minor’s SSN. 3 You must show your individual name and you may also enter your business or DBA name on the “Business name/disregarded entity” name line. You may use either your SSN or EIN (if you have one), but the IRS encourages you to use your SSN. 4 List first and circle the name of the trust, estate, or pension trust. (Do not furnish the TIN of the personal representative or trustee unless the legal entity itself is not designated in the account title.) Also see Special rules for partnerships, earlier. *Note: The grantor also must provide a Form W-9 to trustee of trust. Note: If no name is circled when more than one name is listed, the number will be considered to be that of the first name listed. Secure Your Tax Records From Identity Theft Identity theft occurs when someone uses your personal information such as your name, SSN, or other identifying information, without your permission, to commit fraud or other crimes. An identity thief may use your SSN to get a job or may file a tax return using your SSN to receive a refund. To reduce your risk: Protect your SSN, Ensure your employer is protecting your SSN, and Be careful when choosing a tax preparer. If your tax records are affected by identity theft and you receive a notice from the IRS, respond right away to the name and phone number printed on the IRS notice or letter. If your tax records are not currently affected by identity theft but you think you are at risk due to a lost or stolen purse or wallet, questionable credit card activity or credit report, contact the IRS Identity Theft Hotline at 1-800-908-4490 or submit Form 14039. For more information, see Pub. 5027, Identity Theft Information for Taxpayers. Victims of identity theft who are experiencing economic harm or a systemic problem, or are seeking help in resolving tax problems that have not been resolved through normal channels, may be eligible for Taxpayer Advocate Service (TAS) assistance. You can reach TAS by calling the TAS toll-free case intake line at 1-877-777-4778 or TTY/TDD 1-800-829-4059. Protect yourself from suspicious emails or phishing schemes. Phishing is the creation and use of email and websites designed to mimic legitimate business emails and websites. The most common act is sending an email to a user falsely claiming to be an established legitimate enterprise in an attempt to scam the user into surrendering private information that will be used for identity theft.

- 14 -

The IRS does not initiate contacts with taxpayers via emails. Also, the IRS does not request personal detailed information through email or ask taxpayers for the PIN numbers, passwords, or similar secret access information for their credit card, bank, or other financial accounts. If you receive an unsolicited email claiming to be from the IRS, forward this message to phishing@irs.gov. You may also report misuse of the IRS name, logo, or other IRS property to the Treasury Inspector General for Tax Administration (TIGTA) at 1-800-366-4484. You can forward suspicious emails to the Federal Trade Commission at spam@uce.gov or report them at www.ftc.gov/complaint. You can contact the FTC at www.ftc.gov/idtheft or 877-IDTHEFT (877-438-4338). If you have been the victim of identity theft, see www.IdentityTheft.gov and Pub. 5027. Visit www.irs.gov/IdentityTheft to learn more about identity theft and how to reduce your risk. Privacy Act Notice Section 6109 of the Internal Revenue Code requires you to provide your correct TIN to persons (including federal agencies) who are required to file information returns with the IRS to report interest, dividends, or certain other income paid to you; mortgage interest you paid; the acquisition or abandonment of secured property; the cancellation of debt; or contributions you made to an IRA, Archer MSA, or HSA. The person collecting this form uses the information on the form to file information returns with the IRS, reporting the above information. Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their laws. The information also may be disclosed to other countries under a treaty, to federal and state agencies to enforce civil and criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism. You must provide your TIN whether or not you are required to file a tax return. Under section 3406, payers must generally withhold a percentage of taxable interest, dividend, and certain other payments to a payee who does not give a TIN to the payer. Certain penalties may also apply for providing false or fraudulent information.

- 15 -

| BOX I CERTIFICATION OF AWAITING TAXPAYER IDENTIFICATION NUMBER

|

||

| YOU MUST COMPLETE THE FOLLOWING CERTIFICATE IF YOU WROTE “APPLIED FOR” IN PART I OF THE ATTACHED IRS FORM W-9.

I certify under penalties of perjury that a taxpayer identification number has not been issued to me, and either (a) I have mailed or delivered an application to receive a taxpayer identification number to the appropriate IRS Center or Social Security Administration Office, or (b) I intend to mail or deliver an application in the near future (as described in the instructions to IRS Form W-9). I understand that if I do not provide a TIN by the time of payment, 28% of the gross cash proceeds of such payment made to me may be withheld and such withheld amounts will be treated as having been paid to the persons with respect to whom such amounts were withheld.

Signature of U.S. Shareholder: Date: |

- 16 -

INSTRUCTIONS

| 1. | Use of Letter of Transmittal |

| (a) | Registered Shareholders should review the previously distributed Information Circular prior to completing this Letter of Transmittal. |

| (b) | This Letter of Transmittal, duly completed and signed, together with any accompanying certificates representing the PotashCorp Shares and all other required documents must be sent or delivered to the Depositary at the addresses set out on the back of this Letter of Transmittal. In order to receive the New Parent Shares and any Fractional Share Cash Consideration under the Arrangement for the Deposited PotashCorp Shares, as well as any Dividends, it is recommended that the foregoing documents be received by the Depositary at the address set out on the back of this Letter of Transmittal as soon as possible. |

| (c) | The method used to deliver this Letter of Transmittal and any accompanying certificates representing PotashCorp Shares and all other required documents is at the option and risk of the Registered Shareholder and delivery will be deemed effective only when such documents are actually received by the Depositary. PotashCorp recommends that the necessary documentation be hand delivered to the Depositary at the address set out on the back of this Letter of Transmittal, and a receipt obtained; otherwise the use of registered mail with return receipt requested, properly insured, is recommended. Beneficial Shareholders whose PotashCorp Shares are registered in the name of a broker, investment dealer, bank, trust company, nominee or other intermediary should contact that intermediary for assistance in depositing those PotashCorp Shares. Delivery to an office other than to the specified office does not constitute delivery for this purpose. |

| (d) | Each of New Parent and PotashCorp reserve the right, if they so elect, in their absolute discretion, to instruct the Depositary to waive any defect or irregularity contained in any Letter of Transmittal and/or accompanying documents received by it. |

| (e) | If the New Parent Share Certificate or DRS Advice representing the New Parent Shares and the cheques representing the Fractional Share Cash Consideration or any Dividends are to be issued in the name of a person other than the person(s) signing this Letter of Transmittal under Box G or if the New Parent Share Certificate or DRS Advice representing the New Parent Shares and the cheques representing the Fractional Share Cash Consideration or any Dividends is to be mailed to someone other than the person(s) signing this Letter of Transmittal under Box G or to the person(s) signing this Letter of Transmittal under Box G at an address other than that which appears on the register of PotashCorp, the appropriate boxes on this Letter of Transmittal should be completed (Box A and Box B). |

| 2. | Signatures |

This Letter of Transmittal must be completed and signed by the Registered Shareholder under Box G or by such Registered Shareholder’s duly authorized representative (in accordance with Instruction 4).

| (a) | If this Letter of Transmittal is signed by the Registered Shareholder of any accompanying certificate(s), such signature(s) on this Letter of Transmittal must correspond with the name(s) as registered or as written on the face of such certificate(s), without any change whatsoever, and the certificate(s) need not be endorsed. If such deposited certificate(s) are owned of record by two or more joint owners, all such owners must sign this Letter of Transmittal (Box G). |

| (b) | Subject to Instruction 4, if this Letter of Transmittal is signed on behalf of a Registered Shareholder by a person other than the registered holder(s) of the accompanying certificate(s), or if New Parent Share Certificate(s) or DRS Advice(s) representing New Parent Shares or the cheque representing the Fractional Share Cash Consideration or any Dividends are to be issued to a person other than the Registered Shareholder: |

- 17 -

| (i) | any such deposited certificate(s) must be endorsed or be accompanied by appropriate share transfer power(s) of attorney duly and properly completed by the Registered Shareholder; and |

| (ii) | the signature on such endorsement or share transfer power(s) of attorney must correspond exactly to the name of the Registered Shareholder as registered or as appearing on the certificate(s) and must be guaranteed as noted in paragraph 3 below of these Instructions. |

| (c) | If any of the Deposited PotashCorp Shares are registered in different names on several certificates, it will be necessary to complete, sign and submit as many separate Letters of Transmittal as there are different registrations of such Deposited PotashCorp Shares. |

| 3. | Guarantee of Signatures |

No signature guarantee is required on this Letter of Transmittal if this Letter of Transmittal is signed by the registered holder(s) of the PotashCorp Shares surrendered herewith. Subject to Instruction 4, if this Letter of Transmittal is signed on behalf of a Registered Shareholder by a person other than the registered holder(s) of the PotashCorp Shares or if the payment is to be issued in a name other than the registered holder(s) of the PotashCorp Shares or if the payment is to be sent to an address other than the address of the registered holder(s) as shown on the register of PotashCorp maintained by PotashCorp’s transfer agent, such signature must be guaranteed by an Eligible Institution (as defined below), or in some other manner satisfactory to the Depositary (except that no guarantee is required if the signature is that of an Eligible Institution). An “Eligible Institution” means a Canadian Schedule I chartered bank, a member of the Securities Transfer Agents Medallion Program (STAMP), a member of the Stock Exchanges Medallion Program, (SEMP) or a member of the New York Stock Exchange, Inc. Medallion Signature Program (MSP). Members of these programs are usually members of a recognized stock exchange in Canada or the United States, members of the Investment Industry Regulatory Organization of Canada, members of the Financial Industry Regulatory Authority or banks and trust companies in the United States.

| 4. | Fiduciaries, Representatives and Authorizations |

Where this Letter of Transmittal or any share transfer power(s) of attorney is executed by a person as an executor, administrator, trustee or guardian, or on behalf of a corporation, partnership or association or is executed by any other person acting in a representative capacity, such person should so indicate when signing and this Letter of Transmittal must be accompanied by satisfactory evidence of the authority to act. Any of New Parent, PotashCorp or the Depositary, at their discretion, may require additional evidence of authority or additional documentation.

| 5. | Payment and Delivery Instructions |

If no selection is made in Box A between receiving New Parent Share Certificates and DRS Advices, then DRS Advices will be issued as evidence of New Parent Shares received under the Arrangement. If neither Box A nor Box B is completed, DRS Advices representing New Parent Shares and any cheque(s) representing the Fractional Share Cash Consideration issued in exchange for the Deposited PotashCorp Shares, as well as cheque(s) representing any Dividends, will be issued in the name of the registered holder of the Deposited PotashCorp Shares and will be mailed to the address of the registered holder of the Deposited PotashCorp Shares as it appears on the register of PotashCorp. Otherwise, the New Parent Share Certificates or DRS Advices representing New Parent Shares and any cheque(s) representing the Fractional Share Cash Consideration to be issued in exchange for the Deposited PotashCorp Shares, as well as cheque(s) representing any Dividends, will be issued in the name of the person indicated in Box A and delivered to the address indicated in Box A (unless another address has been provided in Box B). If any New Parent Share Certificates or DRS Advices representing New Parent Shares and any cheque(s) representing the Fractional Share Cash Consideration, as well as cheque(s) representing any Dividends, are to be held for pick-up at the offices of the Depositary, complete Box C. Any New Parent Share Certificates or DRS Advices, any cheque(s) representing the Fractional Share Cash Consideration and cheque(s) representing any Dividends, mailed in accordance with this Letter of Transmittal will be deemed to be delivered at the time of mailing.

| 6. | Tax Instructions for U.S. Shareholders |

For purposes of this Letter of Transmittal, a “U.S. Person” is a beneficial owner of PotashCorp Shares that, for U.S. federal income tax purposes, is (a) an individual who is a citizen or resident of the U.S. (including a U.S. resident alien), (b) a

- 18 -

corporation, partnership, other entity classified as a corporation or partnership for U.S. federal income tax purposes, or association that is created or organized in or under the laws of the United States, or any political subdivision thereof or therein, (c) an estate if the income of such estate is subject to U.S. federal income tax regardless of the source of such income, or (d) a trust if (i) such trust has validly elected to be treated as a U.S. person for U.S. federal income tax purposes, or (ii) a U.S. court is able to exercise primary supervision over the administration of such trust and one or more U.S. persons have the authority to control all substantial decisions of such trust.