Attached files

| file | filename |

|---|---|

| EX-11 - EXHIBIT 11 - POTASH CORP OF SASKATCHEWAN INC | d336595dex11.htm |

| EX-95 - EXHIBIT 95 - POTASH CORP OF SASKATCHEWAN INC | d336595dex95.htm |

| EX-32 - EXHIBIT 32 - POTASH CORP OF SASKATCHEWAN INC | d336595dex32.htm |

| EX-31.B - EXHIBIT 31(B) - POTASH CORP OF SASKATCHEWAN INC | d336595dex31b.htm |

| EX-31.A - EXHIBIT 31(A) - POTASH CORP OF SASKATCHEWAN INC | d336595dex31a.htm |

| EX-10.LL - EXHIBIT 10(LL) - POTASH CORP OF SASKATCHEWAN INC | d336595dex10ll.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended March 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-10351

Potash Corporation of Saskatchewan Inc.

(Exact name of registrant as specified in its charter)

| Canada | N/A | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 122 — 1st Avenue South Saskatoon, Saskatchewan, Canada |

S7K 7G3 (Zip Code) | |

| (Address of principal executive offices) | ||

306-933-8500

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2).

Yes ¨ No þ

As at April 30, 2012, Potash Corporation of Saskatchewan Inc. had 858,930,147 Common Shares outstanding.

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Financial Position

(in millions of US dollars)

(unaudited)

| As at | March 31, 2012 |

December 31, 2011 |

||||||

| Assets |

||||||||

| Current assets |

||||||||

| Cash and cash equivalents |

$ | 417 | $ | 430 | ||||

| Receivables |

1,218 | 1,195 | ||||||

| Inventories (Note 2) |

728 | 731 | ||||||

| Prepaid expenses and other current assets |

62 | 52 | ||||||

| 2,425 | 2,408 | |||||||

| Non-current assets |

||||||||

| Property, plant and equipment |

10,150 | 9,922 | ||||||

| Investments in equity-accounted investees |

1,259 | 1,187 | ||||||

| Available-for-sale investments (Note 3) |

2,387 | 2,265 | ||||||

| Other assets |

303 | 360 | ||||||

| Intangible assets |

118 | 115 | ||||||

| Total Assets |

$ | 16,642 | $ | 16,257 | ||||

| Liabilities |

||||||||

| Current liabilities |

||||||||

| Short-term debt and current portion of long-term debt (Note 4) |

$ | 1,250 | $ | 832 | ||||

| Payables and accrued charges |

978 | 1,295 | ||||||

| Current portion of derivative instrument liabilities |

75 | 67 | ||||||

| 2,303 | 2,194 | |||||||

| Non-current liabilities |

||||||||

| Long-term debt (Note 4) |

3,457 | 3,705 | ||||||

| Derivative instrument liabilities |

198 | 204 | ||||||

| Deferred income tax liabilities |

1,094 | 1,052 | ||||||

| Pension and other post-retirement benefit liabilities |

576 | 552 | ||||||

| Asset retirement obligations and accrued environmental costs |

560 | 615 | ||||||

| Other non-current liabilities and deferred credits |

94 | 88 | ||||||

| Total Liabilities |

8,282 | 8,410 | ||||||

| Shareholders’ Equity |

||||||||

| Share capital (Note 5) |

1,486 | 1,483 | ||||||

| Contributed surplus |

320 | 291 | ||||||

| Accumulated other comprehensive income |

937 | 816 | ||||||

| Retained earnings |

5,617 | 5,257 | ||||||

| Total Shareholders’ Equity |

8,360 | 7,847 | ||||||

| Total Liabilities and Shareholders’ Equity |

$ | 16,642 | $ | 16,257 | ||||

| Contingencies and Other Matters (Note 10) |

||||||||

(See Notes to the Condensed Consolidated Financial Statements)

| 1 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Income

(in millions of US dollars except per-share amounts)

(unaudited)

| Three Months Ended March 31 |

||||||||

| 2012 | 2011 | |||||||

| Sales (Note 6) |

$ | 1,746 | $ | 2,204 | ||||

| Freight, transportation and distribution |

(104 | ) | (149 | ) | ||||

| Cost of goods sold |

(944 | ) | (959 | ) | ||||

| Gross Margin |

698 | 1,096 | ||||||

| Selling and administrative expenses |

(57 | ) | (75 | ) | ||||

| Provincial mining and other taxes |

(28 | ) | (34 | ) | ||||

| Share of earnings of equity-accounted investees |

75 | 51 | ||||||

| Other expenses |

(3 | ) | (13 | ) | ||||

| Operating Income |

685 | 1,025 | ||||||

| Finance Costs |

(34 | ) | (50 | ) | ||||

| Income Before Income Taxes |

651 | 975 | ||||||

| Income Taxes (Note 7) |

(160 | ) | (243 | ) | ||||

| Net Income |

$ | 491 | $ | 732 | ||||

| Net Income per Share (Note 8) |

||||||||

| Basic |

$ | 0.57 | $ | 0.86 | ||||

| Diluted |

$ | 0.56 | $ | 0.84 | ||||

| Dividends Declared per Share |

$ | 0.14 | $ | 0.07 | ||||

(See Notes to the Condensed Consolidated Financial Statements)

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 2 |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Comprehensive Income

(in millions of US dollars)

(unaudited)

| Three Months Ended March 31 |

||||||||

| (Net of related income taxes) | 2012 | 2011 | ||||||

| Net Income |

$ | 491 | $ | 732 | ||||

| Other comprehensive income (loss) |

||||||||

| Net increase (decrease) in net unrealized gain on available-for-sale investments(1) (Note 3) |

122 | (271 | ) | |||||

| Net actuarial loss on defined benefit plans(2) |

(11 | ) | — | |||||

| Net (loss) gain on derivatives designated as cash flow hedges(3) |

(13 | ) | 13 | |||||

| Reclassification to income of net loss on cash flow hedges(4) |

12 | 14 | ||||||

| Other |

— | (2 | ) | |||||

| Other Comprehensive Income (Loss) |

110 | (246 | ) | |||||

| Comprehensive Income |

$ | 601 | $ | 486 | ||||

| (1) | Available-for-sale investments are comprised of shares in Israel Chemicals Ltd. and Sinofert Holdings Limited. |

| (2) | Net of income taxes of $4 (2011 — $NIL). |

| (3) | Cash flow hedges are comprised of natural gas derivative instruments, and are net of income taxes of $8 (2011 — $(8)). |

| (4) | Net of income taxes of $(8) (2011 — $(8)). |

(See Notes to the Condensed Consolidated Financial Statements)

| 3 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Cash Flow

(in millions of US dollars)

(unaudited)

| Three Months Ended March 31 |

||||||||

| 2012 | 2011 | |||||||

| Operating Activities |

||||||||

| Net income |

$ | 491 | $ | 732 | ||||

| Adjustments to reconcile net income to cash provided by operating activities |

||||||||

| Depreciation and amortization |

128 | 124 | ||||||

| Share-based compensation |

16 | 14 | ||||||

| Realized excess tax benefit related to share-based compensation |

2 | 12 | ||||||

| Provision for deferred income tax |

52 | 75 | ||||||

| Undistributed earnings of equity-accounted investees |

(73 | ) | (51 | ) | ||||

| Other long-term liabilities and miscellaneous |

9 | (7 | ) | |||||

| Subtotal of adjustments |

134 | 167 | ||||||

| Changes in non-cash operating working capital |

||||||||

| Receivables |

49 | (213 | ) | |||||

| Inventories |

26 | (27 | ) | |||||

| Prepaid expenses and other current assets |

(14 | ) | — | |||||

| Payables and accrued charges |

(314 | ) | 31 | |||||

| Subtotal of changes in non-cash operating working capital |

(253 | ) | (209 | ) | ||||

| Cash provided by operating activities |

372 | 690 | ||||||

| Investing Activities |

||||||||

| Additions to property, plant and equipment |

(476 | ) | (441 | ) | ||||

| Purchase of non-current investments |

(1 | ) | — | |||||

| Other assets and intangible assets |

(19 | ) | — | |||||

| Cash used in investing activities |

(496 | ) | (441 | ) | ||||

| Financing Activities |

||||||||

| Proceeds from (repayments of) short-term debt obligations |

168 | (253 | ) | |||||

| Dividends |

(59 | ) | (28 | ) | ||||

| Issuance of common shares |

2 | 18 | ||||||

| Cash provided by (used in) financing activities |

111 | (263 | ) | |||||

| Decrease in Cash Position |

(13 | ) | (14 | ) | ||||

| Cash Position, Beginning of Period |

430 | 412 | ||||||

| Cash Position, End of Period |

$ | 417 | $ | 398 | ||||

| Cash position comprised of: |

||||||||

| Cash |

$ | 37 | $ | 82 | ||||

| Short-term investments |

380 | 391 | ||||||

| Cash and cash equivalents |

417 | 473 | ||||||

| Bank overdraft (included in short-term debt) |

— | (75 | ) | |||||

| $ | 417 | $ | 398 | |||||

| Supplemental cash flow disclosure |

||||||||

| Interest paid |

$ | 38 | $ | 41 | ||||

| Income taxes paid |

$ | 316 | $ | 175 | ||||

(See Notes to the Condensed Consolidated Financial Statements)

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 4 |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Changes in Equity

(in millions of US dollars)

(unaudited)

| Equity Attributable to Common Shareholders(1) | ||||||||||||||||||||||||||||||||||||

| Accumulated Other Comprehensive Income | ||||||||||||||||||||||||||||||||||||

| Share Capital |

Contributed Surplus |

Net unrealized gain on available-for- sale investments |

Net loss on derivatives designated as cash flow hedges |

Net actuarial loss on defined benefit plans |

Other | Total Accumulated Other Comprehensive Income |

Retained Earnings |

Total Equity |

||||||||||||||||||||||||||||

| Balance — December 31, 2011 |

$ | 1,483 | $ | 291 | $ | 982 | $ | (168 | ) | $ | — | (2) | $ | 2 | $ | 816 | $ | 5,257 | $ | 7,847 | ||||||||||||||||

| Net income |

— | — | — | — | — | — | — | 491 | 491 | |||||||||||||||||||||||||||

| Other comprehensive income (loss) |

— | — | 122 | (1 | ) | (11 | ) | — | 110 | — | 110 | |||||||||||||||||||||||||

| Effect of share-based compensation |

— | 30 | — | — | — | — | — | — | 30 | |||||||||||||||||||||||||||

| Dividends declared |

— | — | — | — | — | — | — | (120 | ) | (120 | ) | |||||||||||||||||||||||||

| Issuance of common shares |

3 | (1 | ) | — | — | — | — | — | — | 2 | ||||||||||||||||||||||||||

| Transfer of actuarial losses on defined benefit plans |

— | — | — | — | 11 | — | 11 | (11 | ) | — | ||||||||||||||||||||||||||

| Balance — March 31, 2012 |

$ | 1,486 | $ | 320 | $ | 1,104 | $ | (169 | ) | $ | — | (2) | $ | 2 | $ | 937 | $ | 5,617 | $ | 8,360 | ||||||||||||||||

| (1) | All equity transactions are attributable to common shareholders. |

| (2) | Any amounts incurred during a period are closed out to retained earnings at each period-end. Therefore, no balance exists in the reserve at beginning or end of period. |

| Equity Attributable to Common Shareholders(1) | ||||||||||||||||||||||||||||||||||||

| Accumulated Other Comprehensive Income | ||||||||||||||||||||||||||||||||||||

| Share Capital |

Contributed Surplus |

Net unrealized gain on available-for- sale investments |

Net loss on derivatives designated as cash flow hedges |

Net actuarial loss on defined benefit plans |

Other | Total Accumulated Other Comprehensive Income |

Retained Earnings |

Total Equity |

||||||||||||||||||||||||||||

| Balance — December 31, 2010 |

$ | 1,431 | $ | 308 | $ | 2,563 | $ | (177 | ) | $ | — | (2) | $ | 8 | $ | 2,394 | $ | 2,552 | $ | 6,685 | ||||||||||||||||

| Net income |

— | — | — | — | — | — | — | 732 | 732 | |||||||||||||||||||||||||||

| Other comprehensive (loss) income |

— | — | (271 | ) | 27 | — | (2 | ) | (246 | ) | — | (246 | ) | |||||||||||||||||||||||

| Effect of share-based compensation |

— | 51 | — | — | — | — | — | — | 51 | |||||||||||||||||||||||||||

| Dividends declared |

— | — | — | — | — | — | — | (60 | ) | (60 | ) | |||||||||||||||||||||||||

| Issuance of common shares |

18 | — | — | — | — | — | — | — | 18 | |||||||||||||||||||||||||||

| Balance — March 31, 2011 |

$ | 1,449 | $ | 359 | $ | 2,292 | $ | (150 | ) | $ | — | (2) | $ | 6 | $ | 2,148 | $ | 3,224 | $ | 7,180 | ||||||||||||||||

| (1) | All equity transactions are attributable to common shareholders. |

| (2) | Any amounts incurred during a period are closed out to retained earnings at each period-end. Therefore, no balance exists in the reserve at beginning or end of period. |

| (See | Notes to the Condensed Consolidated Financial Statements) |

| 5 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Notes to the Condensed Consolidated Financial Statements

For the Three Months Ended March 31, 2012

(in millions of US dollars except share amounts)

(unaudited)

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 6 |

| 7 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| 6. | Segment Information |

The company’s operating segments have been determined based on reports reviewed by the Chief Executive Officer, its chief operating decision maker, that are used to make strategic decisions. The company has three reportable operating segments: potash, phosphate and nitrogen. These operating segments are differentiated by the chemical nutrient contained in the product that each produces. Inter-segment sales are made under terms that approximate market value. The accounting policies of the segments are the same as those described in Note 1.

| Three Months Ended March 31, 2012 | ||||||||||||||||||||

| Potash | Phosphate | Nitrogen | All Others | Consolidated | ||||||||||||||||

| Sales |

$ | 583 | $ | 613 | $ | 550 | $ | — | $ | 1,746 | ||||||||||

| Freight, transportation and distribution |

(34 | ) | (41 | ) | (29 | ) | — | (104 | ) | |||||||||||

| Net sales — third party |

549 | 572 | 521 | — | ||||||||||||||||

| Cost of goods sold |

(222 | ) | (420 | ) | (302 | ) | — | (944 | ) | |||||||||||

| Gross margin |

327 | 152 | 219 | — | 698 | |||||||||||||||

| Depreciation and amortization |

(30 | ) | (60 | ) | (35 | ) | (3 | ) | (128 | ) | ||||||||||

| Inter-segment sales |

— | — | 42 | — | — | |||||||||||||||

| Three Months Ended March 31, 2011 | ||||||||||||||||||||

| Potash | Phosphate | Nitrogen | All Others | Consolidated | ||||||||||||||||

| Sales |

$ | 1,109 | $ | 549 | $ | 546 | $ | — | $ | 2,204 | ||||||||||

| Freight, transportation and distribution |

(83 | ) | (43 | ) | (23 | ) | — | (149 | ) | |||||||||||

| Net sales — third party |

1,026 | 506 | 523 | — | ||||||||||||||||

| Cost of goods sold |

(283 | ) | (356 | ) | (320 | ) | — | (959 | ) | |||||||||||

| Gross margin |

743 | 150 | 203 | — | 1,096 | |||||||||||||||

| Depreciation and amortization |

(42 | ) | (47 | ) | (33 | ) | (2 | ) | (124 | ) | ||||||||||

| Inter-segment sales |

— | — | 38 | — | — | |||||||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 8 |

| 7. | Income Taxes |

A separate estimated average annual effective tax rate is determined for each taxing jurisdiction and applied individually to the interim period pre-tax income of each jurisdiction.

For the three months ended March 31, 2012, the company’s income tax expense was $160 (2011 — $243). The actual effective tax rate including discrete items for the three months ended March 31, 2012 was 25 percent (2011 — 25 percent). Total discrete tax adjustments that impacted the rate in the three months ended March 31, 2012 resulted in an income tax recovery of $2 compared to an income tax recovery of $23 in the same period last year. The significant item recorded in first-quarter 2011 was a current tax recovery of $21 for previously paid withholding taxes.

Income tax balances within the consolidated statements of financial position were comprised of the following:

| Income Tax Assets (Liabilities) | Statements of Financial Position Location | March 31, 2012 |

December 31, 2011 |

|||||||

| Current income tax assets: |

||||||||||

| Current |

Receivables |

$ | 104 | $ | 21 | |||||

| Non-current |

Other assets |

122 | 117 | |||||||

| Deferred income tax assets |

Other assets |

28 | 19 | |||||||

| Total income tax assets |

$ | 254 | $ | 157 | ||||||

| Current income tax liabilities: |

||||||||||

| Current |

Payables and accrued charges |

$ | (64 | ) | $ | (271 | ) | |||

| Non-current |

Other non-current liabilities and deferred credits |

(92 | ) | (85 | ) | |||||

| Deferred income tax liabilities |

Deferred income tax liabilities |

(1,094 | ) | (1,052 | ) | |||||

| Total income tax liabilities |

$ | (1,250 | ) | $ | (1,408 | ) | ||||

| 9 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 10 |

| 11 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 12 |

| 13 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Key Performance Drivers — Performance Compared to Goals

In all areas of our business, we set goals and design strategies that focus on delivering sustainable value while appropriately balancing stakeholder interests. We demonstrate our accountability by tracking and reporting our progress against targets related to each goal. Our long-term goals and 2012 targets are set out on pages 31 to 42 of our 2011 Annual Report. A summary of our progress against selected goals and representative annual targets is set out below.

| Goal | Representative 2012 Annual Target |

Performance to March 31, 2012 | ||

| Create superior long-term shareholder value. | Exceed total shareholder return performance for our sector and the DAXglobal Agribusiness Index. | PotashCorp’s total shareholder return was 11 percent in the first three months of 2012 compared to our sector’s weighted average return (based on market capitalization) of 13 percent and the DAXglobal Agribusiness Index weighted average return (based on market capitalization) of 12 percent. | ||

| Be the supplier of choice to the markets we serve. | Reduce the number of product tonnes involved in customer complaints below the prior three-year average. | First-quarter product tonnes involved in customer complaints fell 68 percent compared to the prior first-quarter three-year average. | ||

| Attract and retain talented, motivated and productive employees who are committed to our long-term goals. | Maintain an annual employee turnover rate (excluding retirements) of 5 percent or less. | Employee turnover rate (excluding retirements) on an annualized basis for the first three months of 2012 was 4 percent. | ||

| Achieve no harm to people. | Reduce total site severity injury rate by 35 percent from 2008 levels by the end of 2012.

Reduce total site recordable injury rate to 1.30 (per 200,000 hours worked) or lower. |

Total site severity injury rate was 52 percent below the 2008 annual level for the first three months of 2012. It was 32 percent below the 2008 annual level for the first three months of 2011 and 44 percent below the 2008 annual level by the end of 2011.

During the first quarter of 2012, total site recordable injury rate was 1.17. | ||

| Achieve no damage to the environment. | Reduce total reportable incidents (releases, permit excursions and spills) by 10 percent from 2011 levels. | Annualized total reportable incidents were up 100 percent during the first three months of 2012 compared to 2011 annual levels. Compared to the first three months of 2011, total reportable incidents were up 133 percent. |

Financial Overview

This discussion and analysis are based on the company’s unaudited interim condensed consolidated financial statements included in Item 1 of this Quarterly Report on Form 10-Q (financial statements in this Form 10-Q) reported under International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB), unless otherwise stated. All references to per-share amounts pertain to diluted net income per share.

For an understanding of trends, events, uncertainties and the effect of critical accounting estimates on our results and financial condition, the entire document should be read carefully, together with our 2011 Annual Report.

Earnings Guidance — First Quarter 2012

| Company Guidance | Actual Results | |||||||

| Earnings per share |

$ | 0.55 – $0.75 | $ | 0.56 | ||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 14 |

Overview of Actual Results

| Three Months Ended March 31 | ||||||||||||||||

| Dollars (millions) — except per-share amounts | 2012 | 2011 | Change | % Change |

||||||||||||

| Sales |

$ | 1,746 | $ | 2,204 | $ | (458 | ) | (21 | ) | |||||||

| Gross Margin |

698 | 1,096 | (398 | ) | (36 | ) | ||||||||||

| Operating Income |

685 | 1,025 | (340 | ) | (33 | ) | ||||||||||

| Net Income |

491 | 732 | (241 | ) | (33 | ) | ||||||||||

| Net Income per Share — Diluted |

0.56 | 0.84 | (0.28 | ) | (33 | ) | ||||||||||

| Other Comprehensive Income (Loss) |

110 | (246 | ) | 356 | n/m | |||||||||||

| n/m | = not meaningful |

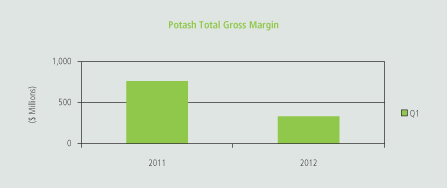

Net income in the first quarter of 2012 was down compared to the first quarter of 2011 due primarily to lower potash sales volumes. First-quarter potash gross margin represented 47 percent of total gross margin (68 percent in the first quarter of 2011). Lower potash sales volumes offset the positive impact of higher prices and resulted in potash gross margin of $327 million for first-quarter 2012, well below the first-quarter record of $743 million generated in 2011. The strength of our diversified phosphate product offering offset general weakness in solid phosphate fertilizer. Nitrogen gross margin climbed to a first-quarter record of $219 million, exceeding the $203 million earned in the same period last year.

Buyers in all major potash markets were slow to commit to new purchases through most of the first quarter. Shipments from North American producers reflected this pause, declining 48 percent from the record level of last year’s first quarter. While underlying consumption at the farm level was expected to be strong globally, most dealers chose to defer major purchasing decisions rather than build inventory. In North America, distributors felt little pressure to act quickly in light of elevated producer inventories and greater availability of offshore product. Offshore buyers slowed purchasing in the absence of new Chinese potash supply contracts and the deferral of shipments to India for previously contracted volumes with global suppliers. Although potash prices avoided the pricing volatility of solid phosphate fertilizer and nitrogen products in previous months, they pulled back slightly on limited demand and increased competitive pressures. In this environment, many buyers focused on consuming inventory and awaited greater certainty before committing to new purchases.

By quarter-end, the global potash market strengthened. China settled new supply contracts late in March – including a contract between Canpotex Limited (Canpotex), the offshore marketing organization for Saskatchewan potash producers, and Sinofert Holdings Limited (Sinofert). After this development and the gathering momentum of the North American planting season, customers in most major markets were actively securing new supply to satisfy pent-up demand for potash.

The North American solid phosphate market was impacted by similar caution among dealers, as domestic shipments of solid fertilizers declined from first-quarter 2011 levels. Shipments to offshore markets more than offset weak North American demand, largely as a result of strong movement to India, which had been limited in the first quarter of last year due to the early completion of contract deliveries. The slower demand environment that carried over from late 2011 resulted in solid phosphate fertilizer prices lower than in the first quarter of last year.

In nitrogen, purchasing patterns were markedly better than those of the other nutrients. After the general slowdown in fertilizer markets late in 2011, nitrogen buyers moved quickly to place new orders – buoyed by the prospect of large US corn plantings and concerned about product availability given a reduction in North American import volumes and certain unplanned domestic plant outages. These tight supply/demand fundamentals were most pronounced in urea, which pushed prices higher during the quarter.

Other significant factors that affected earnings in the first quarter of 2012 compared to the same period in 2011 were lower income taxes due to decreased earnings before taxes and higher earnings from equity-accounted investees. Other comprehensive income for the first quarter of 2012 was due to a rise in the fair value of our investment in Israel Chemicals Ltd. (ICL) and was partially offset by a decline in the fair value of our investment in Sinofert. In 2011, other comprehensive loss for the first quarter was the result of declines in the fair values of our investments in both ICL and Sinofert.

| 15 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

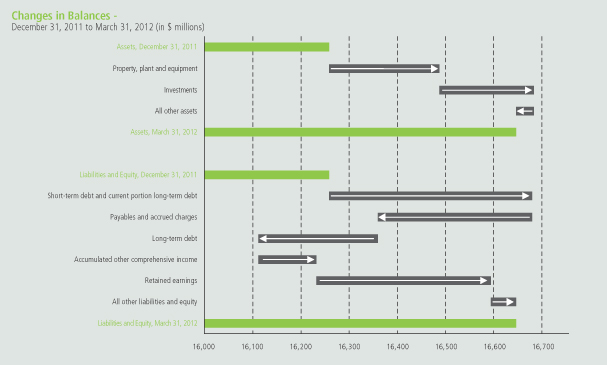

Balance Sheet

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 16 |

Potash

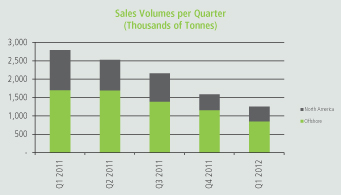

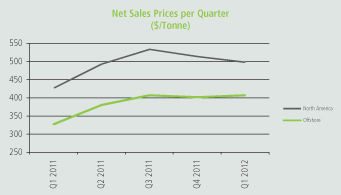

| Three Months Ended March 31 | ||||||||||||||||||||||||||||||||||||

| Dollars (millions) | Tonnes (thousands) | Average per Tonne(1) | ||||||||||||||||||||||||||||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | 2012 | 2011 | % Change | ||||||||||||||||||||||||||||

| Manufactured product |

||||||||||||||||||||||||||||||||||||

| Net sales |

||||||||||||||||||||||||||||||||||||

| North America |

$ | 199 | $ | 466 | (57 | ) | 400 | 1,092 | (63 | ) | $ | 497 | $ | 427 | 16 | |||||||||||||||||||||

| Offshore |

344 | 555 | (38 | ) | 849 | 1,696 | (50 | ) | $ | 406 | $ | 327 | 24 | |||||||||||||||||||||||

| 543 | 1,021 | (47 | ) | 1,249 | 2,788 | (55 | ) | $ | 435 | $ | 366 | 19 | ||||||||||||||||||||||||

| Cost of goods sold |

(218 | ) | (280 | ) | (22 | ) | $ | (175 | ) | $ | (100 | ) | 75 | |||||||||||||||||||||||

| Gross margin |

325 | 741 | (56 | ) | $ | 260 | $ | 266 | (2 | ) | ||||||||||||||||||||||||||

| Other miscellaneous and purchased product gross margin(2) |

2 | 2 | — | |||||||||||||||||||||||||||||||||

| Gross Margin |

$ | 327 | $ | 743 | (56 | ) | $ | 262 | $ | 266 | (2 | ) | ||||||||||||||||||||||||

| (1) | Rounding differences may occur due to the use of whole dollars in per-tonne calculations. |

| (2) | Comprised of net sales of $6 million (2011 — $5 million) less cost of goods sold of $4 million (2011 — $3 million). |

| Three Months Ended March 31 | ||||||||||||||||||

| 2012 | 2011 | % Change | ||||||||||||||||

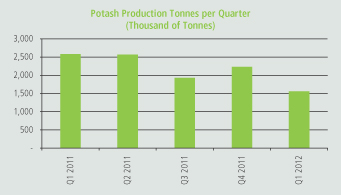

| KCl tonnes produced (thousands) |

1,575 | 2,592 | (39 | ) | ||||||||||||||

| Total site severity injury rate |

0.67 | 0.78 | (14 | ) | ||||||||||||||

| Environmental incidents |

2 | 2 | — | |||||||||||||||

Potash gross margin variance attributable to:

| Three Months Ended March 31 2012 vs. 2011 |

||||||||||||||||

| Change in Prices/Costs |

||||||||||||||||

| Dollars (millions) | Change in Sales Volumes |

Net Sales |

Cost of Goods Sold |

Total | ||||||||||||

| Manufactured product |

||||||||||||||||

| North America |

$ | (251 | ) | $ | 28 | $ | (14 | ) | $ | (237 | ) | |||||

| Offshore |

(215 | ) | 67 | (31 | ) | (179 | ) | |||||||||

| Change in market mix |

10 | (9 | ) | (1 | ) | — | ||||||||||

| Total manufactured product |

$ | (456 | ) | $ | 86 | $ | (46 | ) | $ | (416 | ) | |||||

| Other miscellaneous and purchased product |

— | |||||||||||||||

| Total |

$ | (416 | ) | |||||||||||||

| 17 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Canpotex Limited (Canpotex) sales to major markets, by percentage of sales volumes, were as follows:

| Three Months Ended March 31 | ||||||||||||||||

| 2012 | 2011 | Change | % Change | |||||||||||||

| Asia (excluding China and India) |

70 | 45 | 25 | 56 | ||||||||||||

| Latin America |

12 | 27 | (15 | ) | (56 | ) | ||||||||||

| China |

7 | 16 | (9 | ) | (56 | ) | ||||||||||

| India |

4 | 7 | (3 | ) | (43 | ) | ||||||||||

| Oceania, Europe and Other |

7 | 5 | 2 | 40 | ||||||||||||

| 100 | 100 | |||||||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 18 |

The most significant contributors to the change in total gross margin quarter over quarter were as follows(1):

| (1) | Direction of arrows refers to impact on gross margin. |

| Net Sales Prices | Sales Volumes | Cost of Goods Sold | ||||||||

| h | Our average realized potash price was up, reflecting price gains in spot and contract markets achieved throughout 2011. Although prices in most major spot markets declined slightly from fourth-quarter 2011, our average realized price moved higher and reflected a lower percentage of sales shipped to offshore contract markets. | i | Volumes fell as a result of slower movement to all major markets, including China, which did not settle its new contract with Canpotex until late March, and India, which delayed shipments of most remaining tonnage on existing contracts until the second quarter of 2012. While demand in other Asian markets slowed compared to the record first quarter of 2011, it remained a region of relative strength, taking 70 percent of Canpotex shipments. Buyers in Latin America worked through inventories to meet continued strong consumption. | i |

29 shutdown weeks incurred in 2012 (at our Lanigan, Rocanville, and Allan facilities) to match supply to demand (no shutdown weeks taken in 2011 as facilities operated at or near their full capabilities). During this downtime, we opted to allocate resources to non-production activities rather than lay off employees, which resulted in higher shutdown costs. | |||||

| i | In North America, where distributors deferred major purchasing ahead of the spring planting season, our sales volumes were well below the seasonally strong first-quarter 2011. | |||||||||

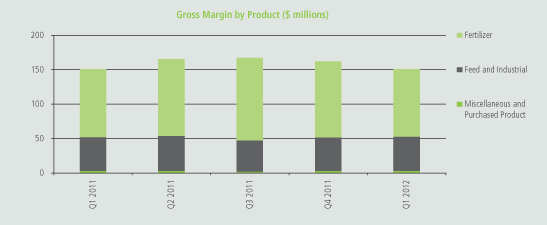

Phosphate

| Three Months Ended March 31 | ||||||||||||||||||||||||||||||||||||

| Dollars (millions) | Tonnes (thousands) | Average per Tonne(1) | ||||||||||||||||||||||||||||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | 2012 | 2011 | % Change | ||||||||||||||||||||||||||||

| Manufactured product |

||||||||||||||||||||||||||||||||||||

| Net sales |

||||||||||||||||||||||||||||||||||||

| Fertilizer |

$ | 363 | $ | 327 | 11 | 637 | 604 | 5 | $ | 570 | $ | 542 | 5 | |||||||||||||||||||||||

| Feed and Industrial |

201 | 172 | 17 | 293 | 289 | 1 | $ | 686 | $ | 594 | 15 | |||||||||||||||||||||||||

| 564 | 499 | 13 | 930 | 893 | 4 | $ | 607 | $ | 559 | 9 | ||||||||||||||||||||||||||

| Cost of goods sold |

(416 | ) | (353 | ) | 18 | $ | (447 | ) | $ | (395 | ) | 13 | ||||||||||||||||||||||||

| Gross margin |

148 | 146 | 1 | $ | 160 | $ | 164 | (2 | ) | |||||||||||||||||||||||||||

| Other miscellaneous and purchased product gross margin(2) |

4 | 4 | — | |||||||||||||||||||||||||||||||||

| Gross Margin |

$ | 152 | $ | 150 | 1 | $ | 163 | $ | 168 | (3 | ) | |||||||||||||||||||||||||

| (1) | Rounding differences may occur due to the use of whole dollars in per-tonne calculations. |

| (2) | Comprised of net sales of $8 million (2011 — $7 million) less cost of goods sold of $4 million (2011 — $3 million). |

| Three Months Ended March 31 | ||||||||||||||||||

| 2012 | 2011 | % Change | ||||||||||||||||

|

P2O5 tonnes produced (thousands) |

486 | 532 | (9 | ) | ||||||||||||||

|

P2O5 operating rate percentage |

82 | 90 | (9 | ) | ||||||||||||||

| Total site severity injury rate |

0.56 | 1.15 | (51 | ) | ||||||||||||||

| Environmental incidents |

3 | — | n/m | |||||||||||||||

| n/m | = not meaningful |

| 19 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Phosphate gross margin variance attributable to:

| Three Months Ended March 31 2012 vs. 2011 |

||||||||||||||||

| Change in Prices/Costs |

||||||||||||||||

| Dollars (millions) | Change in Sales Volumes |

Net Sales |

Cost of Goods Sold |

Total | ||||||||||||

| Manufactured product |

||||||||||||||||

| Fertilizer |

$ | 12 | $ | 14 | $ | (26 | ) | $ | — | |||||||

| Feed and Industrial |

1 | 27 | (26 | ) | 2 | |||||||||||

| Change in market mix |

(4 | ) | 3 | 1 | — | |||||||||||

| Total manufactured product |

$ | 9 | $ | 44 | $ | (51 | ) | $ | 2 | |||||||

| Other miscellaneous and purchased product |

— | |||||||||||||||

| Total |

$ | 2 | ||||||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 20 |

The most significant contributors to the change in total gross margin quarter over quarter were as follows(1):

| (1) | Direction of arrows refers to impact on gross margin. |

| Net Sales Prices | Sales Volumes | Cost of Goods Sold | ||||||||

| h | Results were supported by the typically more stable pricing environment in feed and industrial products, combined with the ability of liquid fertilizer products to attract a premium relative to solid fertilizers and the benefit of a time lag on quarterly contract sales. | h | A larger percentage of sales allocated to meet offshore fertilizer demand, combined with strong feed and industrial volumes, helped offset weakness in North American fertilizer markets. | i | Costs were impacted by higher sulfur costs (up 19 percent). |

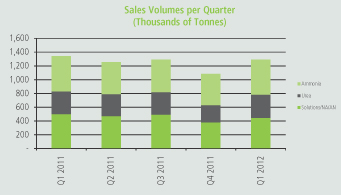

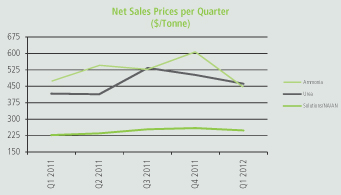

Nitrogen

| Three Months Ended March 31 | ||||||||||||||||||||||||||||||||||||

| Dollars (millions) | Tonnes (thousands) | Average per Tonne(1) | ||||||||||||||||||||||||||||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | 2012 | 2011 | % Change | ||||||||||||||||||||||||||||

| Manufactured product |

||||||||||||||||||||||||||||||||||||

| Net sales |

||||||||||||||||||||||||||||||||||||

| Ammonia |

$ | 230 | $ | 244 | (6 | ) | 516 | 514 | — | $ | 447 | $ | 474 | (6 | ) | |||||||||||||||||||||

| Urea |

154 | 138 | 12 | 334 | 331 | 1 | $ | 462 | $ | 416 | 11 | |||||||||||||||||||||||||

| Nitrogen solutions/Nitric acid/Ammonium nitrate |

110 | 112 | (2 | ) | 440 | 495 | (11 | ) | $ | 249 | $ | 226 | 10 | |||||||||||||||||||||||

| 494 | 494 | — | 1,290 | 1,340 | (4 | ) | $ | 383 | $ | 368 | 4 | |||||||||||||||||||||||||

| Cost of goods sold |

(288 | ) | (299 | ) | (4 | ) | $ | (223 | ) | $ | (223 | ) | — | |||||||||||||||||||||||

| Gross margin |

206 | 195 | 6 | $ | 160 | $ | 145 | 10 | ||||||||||||||||||||||||||||

| Other miscellaneous and purchased product gross margin(2) |

13 | 8 | 63 | |||||||||||||||||||||||||||||||||

| Gross Margin |

$ | 219 | $ | 203 | 8 | $ | 170 | $ | 151 | 13 | ||||||||||||||||||||||||||

| (1) | Rounding differences may occur due to the use of whole dollars in per-tonne calculations. |

| (2) | Comprised of net sales of $27 million (2011 — $29 million) less cost of goods sold of $14 million (2011 — $21 million). |

| Three Months Ended March 31 | ||||||||||||||

| 2012 | 2011 | % Change | ||||||||||||

| N tonnes produced (thousands) |

681 | 686 | (1 | ) | ||||||||||

| Total site severity injury rate |

0.11 | 0.29 | (62 | ) | ||||||||||

| Environmental incidents |

2 | 1 | 100 | |||||||||||

| 21 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Nitrogen gross margin variance attributable to:

| Three Months Ended March 31 2012 vs. 2011 |

||||||||||||||||

| Change in Prices/Costs |

||||||||||||||||

| Dollars (millions) | Change in Sales Volumes |

Net Sales |

Cost of Goods Sold |

Total | ||||||||||||

| Manufactured product |

||||||||||||||||

| Ammonia |

$ | 1 | $ | (14 | ) | $ | 4 | $ | (9 | ) | ||||||

| Urea |

— | 15 | — | 15 | ||||||||||||

| Solutions, NA, AN |

(9 | ) | 10 | — | 1 | |||||||||||

| US natural gas hedge |

— | — | 4 | 4 | ||||||||||||

| Change in market mix |

(7 | ) | 8 | (1 | ) | — | ||||||||||

| Total manufactured product |

$ | (15 | ) | $ | 19 | $ | 7 | $ | 11 | |||||||

| Other miscellaneous and purchased product |

5 | |||||||||||||||

| Total |

$ | 16 | ||||||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 22 |

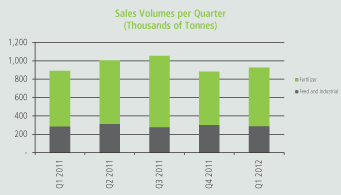

| Three Months Ended March 31 | ||||||||||||||||

| Sales Tonnes (thousands) |

Price per Tonne | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Fertilizer |

375 | 388 | $ | 413 | $ | 371 | ||||||||||

| Industrial and Feed |

915 | 952 | $ | 371 | $ | 367 | ||||||||||

| 1,290 | 1,340 | $ | 383 | $ | 368 | |||||||||||

The most significant contributors to the change in total gross margin quarter over quarter were as follows(1):

| (1) | Direction of arrows refers to impact on gross margin, while the • symbol signifies a neutral impact. |

| Net Sales Prices | Sales Volumes | Cost of Goods Sold | ||||||||

| h | Strong demand for urea, nitrogen solutions, nitric acid and ammonium nitrate, combined with limited supply, pushed prices for these products higher. | i | Sales volumes were slightly below the same period last year, largely as a result of reduced production at Geismar. |

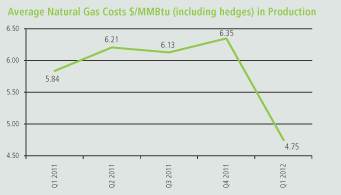

h | Average natural gas costs in production, including hedge, decreased 19 percent. Natural gas costs in Trinidad production fell 12 percent (contract price indexed, in part, to Tampa ammonia prices) while our US spot costs for natural gas used in production decreased 30 percent. Including losses on our hedge position, US gas prices declined 28 percent. | |||||

| i | While ammonia prices strengthened towards the end of the quarter, key benchmark prices were below that of the same period last year due to tight global supplies in the first quarter of 2011. |

Other Expenses and Income

| Three Months Ended March 31 | ||||||||||||||||

| Dollars (millions) | 2012 | 2011 | Change | % Change | ||||||||||||

| Selling and administrative expenses |

$ | (57 | ) | $ | (75 | ) | $ | 18 | (24 | ) | ||||||

| Provincial mining and other taxes |

(28 | ) | (34 | ) | 6 | (18 | ) | |||||||||

| Share of earnings of equity-accounted investees |

75 | 51 | 24 | 47 | ||||||||||||

| Other expenses |

(3 | ) | (13 | ) | 10 | (77 | ) | |||||||||

| Finance costs |

(34 | ) | (50 | ) | 16 | (32 | ) | |||||||||

| Income taxes |

(160 | ) | (243 | ) | 83 | (34 | ) | |||||||||

Selling and administrative expenses were lower due primarily to decreased accruals for our short-term incentive plan and our medium-term incentive plan.

Provincial mining and other taxes are comprised mainly of the Saskatchewan Potash Production Tax (PPT) and a resource surcharge. The PPT is comprised of a base tax per tonne of product sold and an additional tax based on mine profit, which is reduced by an amount based on potash capital expenditures. The resource surcharge is a percentage (3 percent) of the value of the company’s Saskatchewan resource sales. The PPT expense in the first quarter of 2012 was higher than in the first quarter of 2011 as a result of loss carry-forwards utilized in the prior year. The resource surcharge decreased as a result of lower potash sales revenues in the first quarter of 2012.

Share of earnings of equity-accounted investees, primarily Arab Potash Company Ltd. and Sociedad Quimica y Minera de Chile S.A., was higher than last year due to increased earnings by these companies.

| 23 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

Finance costs were affected by the repayment of 10-year senior notes during the second quarter of 2011 and lower average commercial paper balances quarter over quarter. Weighted average debt obligations outstanding and the associated interest rates were as follows:

| Three Months Ended March 31 | ||||||||||||||||

| Dollars (millions) — except percentage amounts | 2012 | 2011 | Change | % Change | ||||||||||||

| Long-term debt obligations, including current portion |

||||||||||||||||

| Weighted average outstanding |

$ | 3,757 | $ | 4,358 | $ | (601 | ) | (14 | ) | |||||||

| Weighted average effective interest rate |

5.2% | 5.5% | (0.3)% | (5 | ) | |||||||||||

| Short-term debt obligations |

||||||||||||||||

| Weighted average outstanding |

$ | 837 | $ | 1,106 | $ | (269 | ) | (24 | ) | |||||||

| Weighted average effective interest rate |

0.4% | 0.4% | — | — | ||||||||||||

Income taxes decreased due to lower income before taxes. The effective tax rate including discrete items remained at 25 percent, unchanged quarter over quarter. The income tax expense for the first three months of 2012 was impacted by a reduction in the Canadian statutory tax rate. The income tax expense for the first three months of 2011 was impacted by a current tax recovery of $21 million for previously paid withholding taxes. For the first three months of 2012, 74 percent of the effective tax rate on the current year’s ordinary earnings pertained to current income taxes and 26 percent related to deferred income taxes.

Liquidity and Capital Resources

Cash Requirements

Contractual Obligations and Other Commitments

Our contractual obligations and other commitments detailed on pages 68 and 69 of our 2011 Annual Report summarize our short- and long-term liquidity and capital resource requirements, excluding obligations with original maturities of less than one year and planned (but not legally committed) capital expenditures.

Capital Expenditures

Page 47 of our 2011 Annual Report outlines key potash construction projects and their expected total cost, as well as the impact of these projects on capacity expansion/debottlenecking and any expected remaining spending on each project still in progress. During 2012, we expect to incur capital expenditures, including capitalized interest, of approximately $1,770 million for opportunity capital, approximately $410 million to sustain operations at existing levels, approximately $181 million for major repairs and maintenance (including plant turnarounds) and approximately $40 million for site improvements.

The most significant potash projects(1) on which funds are expected to be spent in 2012, excluding capitalized interest, are outlined in the table below:

| CDN Dollars (millions) | 2012 Forecast | Total Forecast | Started | Expected Completion(2) (Description) |

Forecasted Remaining Spending (after 2012) |

|||||||||||||

| Allan, Saskatchewan |

$ | 200 | $ | 770 | 2008 | 2012 (general expansion) | $ | 50 | ||||||||||

| Cory, Saskatchewan |

$ | 30 | $ | 1,640 | 2007 | 2012 (general expansion) | $ | — | ||||||||||

| Picadilly, New Brunswick |

$ | 300 | $ | 1,660 | 2007 | 2013 (mine shaft and mill) | $ | 40 | ||||||||||

| Rocanville, Saskatchewan |

$ | 800 | $ | 2,800 | 2008 | 2014 (mine shaft and mill) | $ | 540 | ||||||||||

| (1) | The expansion at each of these projects is discussed in the technical report for such project filed on SEDAR in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects. |

| (2) | Excludes ramp-up time. We expect these projects will be fully ramped up by the end of 2015, provided market conditions warrant. |

We anticipate that all capital spending will be financed by internally generated cash flows supplemented, if and as necessary, by borrowing from existing financing sources.

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 24 |

Sources and Uses of Cash

Cash flows from operating, investing and financing activities, as reflected in the unaudited interim Condensed Consolidated Statements of Cash Flow, are summarized in the following table:

| Three Months Ended March 31 | ||||||||||||||||

| Dollars (millions) | 2012 | 2011 | Change | % Change | ||||||||||||

| Cash provided by operating activities |

$ | 372 | $ | 690 | $ | (318 | ) | (46 | ) | |||||||

| Cash used in investing activities |

(496 | ) | (441 | ) | (55 | ) | 12 | |||||||||

| Cash provided by (used in) financing activities |

111 | (263 | ) | 374 | n/m | |||||||||||

| n/m | = not meaningful |

The following table presents summarized working capital information as at March 31, 2012 compared to December 31, 2011:

| Dollars (millions) — except ratio amounts | March 31, 2012 | December 31, 2011 | Change | % Change | ||||||||||||

| Current assets |

$ | 2,425 | $ | 2,408 | $ | 17 | 1 | |||||||||

| Current liabilities |

$ | (2,303 | ) | $ | (2,194 | ) | $ | (109 | ) | 5 | ||||||

| Working capital |

$ | 122 | $ | 214 | $ | (92 | ) | (43 | ) | |||||||

| Current ratio |

1.05 | 1.10 | (0.05 | ) | (5 | ) | ||||||||||

| 25 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

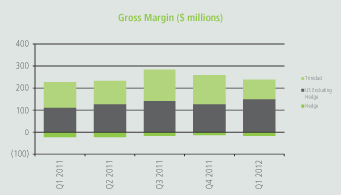

Quarterly Financial Highlights

| Dollars (millions) — except per-share amounts |

March 31, 2012 |

December 31, 2011 |

September 30, 2011 |

June 30, 2011 |

March 31, 2011 |

December 31, 2010 |

September 30, 2010 |

June 30, 2010 |

||||||||||||||||||||||||

| Sales |

$1,746 | $ | 1,865 | $ | 2,321 | $ | 2,325 | $ | 2,204 | $ | 1,813 | $ | 1,575 | $ | 1,437 | |||||||||||||||||

| Gross margin |

698 | 890 | 1,132 | 1,168 | 1,096 | 826 | 550 | 585 | ||||||||||||||||||||||||

| Net income |

491 | 683 | 826 | 840 | 732 | 508 | 343 | 480 | ||||||||||||||||||||||||

| Net income per share — basic |

0.57 | 0.80 | 0.96 | 0.98 | 0.86 | 0.58 | 0.39 | 0.54 | ||||||||||||||||||||||||

| Net income per share — diluted |

0.56 | 0.78 | 0.94 | 0.96 | 0.84 | 0.56 | 0.38 | 0.53 | ||||||||||||||||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 26 |

| 27 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 28 |

| 29 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 30 |

Part II. Other Information

For a description of certain other legal and environmental proceedings, see Note 10 to the unaudited interim condensed consolidated financial statements included in Part I of this Quarterly Report on Form 10-Q.

Mine Safety Disclosures

Safety is the company’s top priority and we are committed to providing a healthy and safe work environment for our employees, contractors and all others at our sites to help meet our company-wide goal of achieving no harm to people.

The operations at the company’s Aurora, Weeping Water and White Springs facilities are subject to the Federal Mine Safety and Health Act of 1977, as amended by the Mine Improvement and New Emergency Response Act of 2006, and the implementing regulations, which impose stringent health and safety standards on numerous aspects of mineral extraction and processing operations, including the training of personnel, operating procedures, operating equipment and other matters. Our Senior Safety Leadership Team is responsible for managing compliance with applicable government regulations, as well as implementing and overseeing the elements of our safety program as outlined in our Safety, Health and Environment Manual.

Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Section 1503(a)) requires us to include certain safety information in the periodic reports we file with the United States Securities and Exchange Commission. The information concerning mine safety violations and other regulatory matters required by Section 1503(a) and Item 104 of Regulation S-K is included in Exhibit 95 to this Quarterly Report on Form 10-Q.

| (a) | Exhibits |

| Incorporated by Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 3(a) | Articles of Continuance of the registrant dated May 15, 2002. | 10-Q | 6/30/2002 | |||||||||

| 3(b) | Bylaws of the registrant effective May 15, 2002. | 10-Q | 6/30/2002 | |||||||||

| 4(a) | Term Credit Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated September 25, 2001. | 10-Q | 9/30/2001 | |||||||||

| 4(b) | Syndicated Term Credit Facility Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 23, 2003. | 10-Q | 9/30/2003 | |||||||||

| 4(c) | Syndicated Term Credit Facility Second Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 21, 2004. | 8-K | 9/24/2004 | |||||||||

| 4(d) | Syndicated Term Credit Facility Third Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 20, 2005. | 8-K | 9/22/2005 | 4(a) | ||||||||

| 4(e) | Syndicated Term Credit Facility Fourth Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 27, 2006. | 10-Q | 9/30/2006 | |||||||||

| 4(f) | Syndicated Term Credit Facility Fifth Amending Agreement between the Bank of Nova Scotia and other financial institutions and the registrant dated as of October 19, 2007. | 8-K | 10/22/2007 | 4(a) | ||||||||

| 4(g) | Indenture dated as of February 27, 2003, between the registrant and The Bank of Nova Scotia Trust Company of New York. | 10-K | 12/31/2002 | 4(c) | ||||||||

| 4(h) | Form of Note relating to the registrant’s offering of $250,000,000 principal amount of 4.875% Notes due March 1, 2013. | 8-K | 2/28/2003 | 4 | ||||||||

| 31 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| Incorporated by Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 4(i) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.875% Notes due December 1, 2036. | 8-K | 11/30/2006 | 4(a) | ||||||||

| 4(j) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.25% Notes due May 15, 2014. | 8-K | 5/1/2009 | 4(a) | ||||||||

| 4(k) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 6.50% Notes due May 15, 2019. | 8-K | 5/1/2009 | 4(b) | ||||||||

| 4(l) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 3.75% Notes due September 30, 2015. | 8-K | 9/25/2009 | 4(a) | ||||||||

| 4(m) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 4.875% Notes due March 30, 2020. | 8-K | 9/25/2009 | 4(b) | ||||||||

| 4(n) | Revolving Term Credit Facility Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated December 11, 2009. | 8-K | 12/15/2009 | 4(a) | ||||||||

| 4(o) | Revolving Term Credit Facility First Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 23, 2011. | 8-K | 9/26/2011 | 4(a) | ||||||||

| 4(p) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 3.25% Notes due December 1, 2017. | 8-K | 11/29/2010 | 4(a) | ||||||||

| 4(q) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.625% Notes due December 1, 2040. | 8-K | 11/29/2010 | 4(b) | ||||||||

The registrant hereby undertakes to file with the Securities and Exchange Commission, upon request, copies of any constituent instruments defining the rights of holders of long-term debt of the registrant or its subsidiaries that have not been filed herewith because the amounts represented thereby are less than 10% of the total assets of the registrant and its subsidiaries on a consolidated basis.

| Incorporated By Reference | ||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||

| 10(a) | Sixth Voting Agreement dated April 22, 1978, between Central Canada Potash, Division of Noranda, Inc., Cominco Ltd., International Minerals and Chemical Corporation (Canada) Limited, PCS Sales and Texasgulf Inc. | F-1 (File No. |

9/28/1989 | 10(f) | ||||||

| 10(b) | Canpotex Limited Shareholders Seventh Memorandum of Agreement effective April 21, 1978, between Central Canada Potash, Division of Noranda Inc., Cominco Ltd., International Minerals and Chemical Corporation (Canada) Limited, PCS Sales, Texasgulf Inc. and Canpotex Limited as amended by Canpotex S&P amending agreement dated November 4, 1987. | F-1 (File No. |

9/28/1989 | 10(g) | ||||||

| 10(c) | Producer Agreement dated April 21, 1978, between Canpotex Limited and PCS Sales. | F-1 (File No. |

9/28/1989 | 10(h) | ||||||

| 10(d) | Canpotex/PCS Amending Agreement, dated as of October 1, 1992. | 10-K | 12/31/1995 | 10(f) | ||||||

| 10(e) | Canpotex PCA Collateral Withdrawing/PCS Amending Agreement, dated as of October 7, 1993. | 10-K | 12/31/1995 | 10(g) | ||||||

| 10(f) | Canpotex Producer Agreement amending agreement dated as of July 1, 2002. | 10-Q | 6/30/2004 | 10(g) | ||||||

| 10(g) | Esterhazy Restated Mining and Processing Agreement dated January 31, 1978, between International Minerals & Chemical Corporation (Canada) Limited and the registrant’s predecessor. | F-1 (File No. |

9/28/1989 | 10(e) | ||||||

| 10(h) | Agreement dated December 21, 1990, between International Minerals & Chemical Corporation (Canada) Limited and the registrant, amending the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978. | 10-K | 12/31/1990 | 10(p) | ||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 32 |

| Incorporated By Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 10(i) | Agreement effective August 27, 1998, between International Minerals & Chemical (Canada) Global Limited and the registrant, amending the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978 (as amended). | 10-K | 12/31/1998 | 10(l) | ||||||||

| 10(j) | Agreement effective August 31, 1998, among International Minerals & Chemical (Canada) Global Limited, International Minerals & Chemical (Canada) Limited Partnership and the registrant assigning the interest in the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978 (as amended) held by International Minerals & Chemical (Canada) Global Limited to International Minerals & Chemical (Canada) Limited Partnership. | 10-K | 12/31/1998 | 10(m) | ||||||||

| 10(k) | Potash Corporation of Saskatchewan Inc. Stock Option Plan — Directors, as amended. | 10-K | 12/31/2006 | 10(l) | ||||||||

| 10(l) | Potash Corporation of Saskatchewan Inc. Stock Option Plan — Officers and Employees, as amended. | 10-K | 12/31/2006 | 10(m) | ||||||||

| 10(m) | Short-Term Incentive Plan of the registrant effective January 1, 2000, as amended. | 8-K | 3/13/2012 | 10(a) | ||||||||

| 10(n) | Resolution and Forms of Agreement for Supplemental Executive Retirement Income Plan, for officers and key employees of the registrant. | 10-K | 12/31/1995 | 10(o) | ||||||||

| 10(o) | Amending Resolution and revised forms of agreement regarding Supplemental Retirement Income Plan of the registrant. | 10-Q | 6/30/1996 | 10(x) | ||||||||

| 10(p) | Amended and restated Supplemental Executive Retirement Income Plan of the registrant and text of amendment to existing supplemental income plan agreements. | 10-Q | 9/30/2000 | 10(mm) | ||||||||

| 10(q) | Amendment, dated February 23, 2009, to the amended and restated Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | 10(r) | ||||||||

| 10(r) | Amendment, dated December 29, 2010, to the amended and restated Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(s) | Form of Letter of amendment to existing supplemental income plan agreements of the registrant. | 10-K | 12/31/2002 | 10(cc) | ||||||||

| 10(t) | Amended and restated agreement dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2006 | 10(s) | ||||||||

| 10(u) | Amendment, dated December 24, 2008, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(v) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(w) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated August 2, 1996, between the registrant and Wayne R. Brownlee concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(x) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated August 2, 1996, between the registrant and Garth W. Moore concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(y) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(z) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated August 2, 1996, between the registrant and Wayne R. Brownlee concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 33 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

| Incorporated By Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 10(aa) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated August 2, 1996, between the registrant and Garth W. Moore concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(bb) | Supplemental Retirement Agreement dated December 24, 2008, between the registrant and Stephen F. Dowdle. | 10-K | 12/31/2011 | |||||||||

| 10(cc) | Supplemental Retirement Benefits Plan for U.S. Executives dated effective January 1, 1999. | 10-Q | 6/30/2002 | 10(aa) | ||||||||

| 10(dd) | Amendment No. 1, dated December 24, 2008, to the Supplemental Retirement Plan for U.S. Executives. | 10-K | 12/31/2008 | 10(z) | ||||||||

| 10(ee) | Amendment No. 2, dated February 23, 2009, to the Supplemental Retirement Plan for U.S. Executives. | 10-K | 12/31/2008 | 10(aa) | ||||||||

| 10(ff) | Forms of Agreement dated December 30, 1994, between the registrant and certain officers of the registrant. | 10-K | 12/31/1995 | 10(p) | ||||||||

| 10(gg) | Amendment, dated December 31, 2010, to the Agreement, dated December 30, 1994 between the registrant and William J. Doyle. | 10-K | 12/31/2010 | 10(ee) | ||||||||

| 10(hh) | Form of Agreement of Indemnification dated August 8, 1995, between the registrant and certain officers and directors of the registrant. | 10-K | 12/31/1995 | 10(q) | ||||||||

| 10(ii) | Resolution and Form of Agreement of Indemnification dated January 24, 2001. | 10-K | 12/31/2000 | |||||||||

| 10(jj) | Resolution and Form of Agreement of Indemnification — July 21, 2004. | 10-Q | 6/30/2004 | 10(ii) | ||||||||

| 10(kk) | Chief Executive Officer Medical and Dental Benefits. | 10-K | 12/31/2010 | 10(jj) | ||||||||

| 10(ll) | Deferred Share Unit Plan for Non-Employee Directors, as amended. | |||||||||||

| 10(mm) | U.S. Participant Addendum No. 1 to the Deferred Share Unit Plan for Non-Employee Directors. | 10-K | 12/31/2008 | 10(jj) | ||||||||

| 10(nn) | Potash Corporation of Saskatchewan Inc. 2005 Performance Option Plan and Form of Option Agreement, as amended. | 10-K | 12/31/2006 | 10(cc) | ||||||||

| 10(oo) | Potash Corporation of Saskatchewan Inc. 2006 Performance Option Plan and Form of Option Agreement, as amended. | 10-K | 12/31/2006 | 10(dd) | ||||||||

| 10(pp) | Potash Corporation of Saskatchewan Inc. 2007 Performance Option Plan and Form of Option Agreement. | 10-Q | 3/31/2007 | 10(ee) | ||||||||

| 10(qq) | Potash Corporation of Saskatchewan Inc. 2008 Performance Option Plan and Form of Option Agreement. | 10-Q | 3/31/2008 | 10(ff) | ||||||||

| 10(rr) | Potash Corporation of Saskatchewan Inc. 2009 Performance Option Plan and Form of Option Agreement. | 10-Q | 3/31/2009 | 10(mm) | ||||||||

| 10(ss) | Potash Corporation of Saskatchewan Inc. 2010 Performance Option Plan and Form of Option Agreement. | 8-K | 5/7/2010 | 10.1 | ||||||||

| 10(tt) | Potash Corporation of Saskatchewan Inc. 2011 Performance Option Plan and Form of Option Agreement. | 8-K | 5/13/2011 | 10(a) | ||||||||

| 10(uu) | Medium-Term Incentive Plan of the registrant effective January 1, 2012. | 10-K | 12/31/2011 | |||||||||

| 11 | Statement re Computation of Per Share Earnings. | |||||||||||

| 31(a) | Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. | |||||||||||

| 31(b) | Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. | |||||||||||

| 32 | Certification pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. | |||||||||||

| 95 | Information concerning mine safety violations or other regulatory matters required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act. | |||||||||||

| PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q | 34 |

Signatures

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| POTASH CORPORATION OF SASKATCHEWAN INC. | ||||||

| May 2, 2012 | By: | /s/ JOSEPH PODWIKA | ||||

| Joseph Podwika | ||||||

| Senior Vice President, General Counsel and Secretary | ||||||

| May 2, 2012 | By: | /s/ WAYNE R. BROWNLEE | ||||

| Wayne R. Brownlee | ||||||

| Executive Vice President, Treasurer and Chief Financial Officer (Principal Financial and Accounting Officer) | ||||||

| 35 | PotashCorp 2012 First Quarter Quarterly Report on Form 10-Q |

EXHIBIT INDEX

| Incorporated by Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 3(a) | Articles of Continuance of the registrant dated May 15, 2002. | 10-Q | 6/30/2002 | |||||||||

| 3(b) | Bylaws of the registrant effective May 15, 2002. | 10-Q | 6/30/2002 | |||||||||

| 4(a) | Term Credit Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated September 25, 2001. | 10-Q | 9/30/2001 | |||||||||

| 4(b) | Syndicated Term Credit Facility Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 23, 2003. | 10-Q | 9/30/2003 | |||||||||

| 4(c) | Syndicated Term Credit Facility Second Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 21, 2004. | 8-K | 9/24/2004 | |||||||||

| 4(d) | Syndicated Term Credit Facility Third Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 20, 2005. | 8-K | 9/22/2005 | 4(a) | ||||||||

| 4(e) | Syndicated Term Credit Facility Fourth Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 27, 2006. | 10-Q | 9/30/2006 | |||||||||

| 4(f) | Syndicated Term Credit Facility Fifth Amending Agreement between the Bank of Nova Scotia and other financial institutions and the registrant dated as of October 19, 2007. | 8-K | 10/22/2007 | 4(a) | ||||||||

| 4(g) | Indenture dated as of February 27, 2003, between the registrant and The Bank of Nova Scotia Trust Company of New York. | 10-K | 12/31/2002 | 4(c) | ||||||||

| 4(h) | Form of Note relating to the registrant’s offering of $250,000,000 principal amount of 4.875% Notes due March 1, 2013. | 8-K | 2/28/2003 | 4 | ||||||||

| 4(i) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.875% Notes due December 1, 2036. | 8-K | 11/30/2006 | 4(a) | ||||||||

| 4(j) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.25% Notes due May 15, 2014. | 8-K | 5/1/2009 | 4(a) | ||||||||

| 4(k) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 6.50% Notes due May 15, 2019. | 8-K | 5/1/2009 | 4(b) | ||||||||

| 4(l) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 3.75% Notes due September 30, 2015. | 8-K | 9/25/2009 | 4(a) | ||||||||

| 4(m) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 4.875% Notes due March 30, 2020. | 8-K | 9/25/2009 | 4(b) | ||||||||

| 4(n) | Revolving Term Credit Facility Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated December 11, 2009. | 8-K | 12/15/2009 | 4(a) | ||||||||

| 4(o) | Revolving Term Credit Facility First Amending Agreement between The Bank of Nova Scotia and other financial institutions and the registrant dated as of September 23, 2011. | 8-K | 9/26/2011 | 4(a) | ||||||||

| 4(p) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 3.25% Notes due December 1, 2017. | 8-K | 11/29/2010 | 4(a) | ||||||||

| 4(q) | Form of Note relating to the registrant’s offering of $500,000,000 principal amount of 5.625% Notes due December 1, 2040. | 8-K | 11/29/2010 | 4(b) | ||||||||

The registrant hereby undertakes to file with the Securities and Exchange Commission, upon request, copies of any constituent instruments defining the rights of holders of long-term debt of the registrant or its subsidiaries that have not been filed herewith because the amounts represented thereby are less than 10% of the total assets of the registrant and its subsidiaries on a consolidated basis.

| Incorporated By Reference | ||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||

| 10(a) | Sixth Voting Agreement dated April 22, 1978, between Central Canada Potash, Division of Noranda, Inc., Cominco Ltd., International Minerals and Chemical Corporation (Canada) Limited, PCS Sales and Texasgulf Inc. | F-1 (File No. |

9/28/1989 | 10(f) | ||||||

| 10(b) | Canpotex Limited Shareholders Seventh Memorandum of Agreement effective April 21, 1978, between Central Canada Potash, Division of Noranda Inc., Cominco Ltd., International Minerals and Chemical Corporation (Canada) Limited, PCS Sales, Texasgulf Inc. and Canpotex Limited as amended by Canpotex S&P amending agreement dated November 4, 1987. | F-1 (File No. |

9/28/1989 | 10(g) | ||||||

| 10(c) | Producer Agreement dated April 21, 1978, between Canpotex Limited and PCS Sales. | F-1 (File No. |

9/28/1989 | 10(h) | ||||||

| 10(d) | Canpotex/PCS Amending Agreement, dated as of October 1, 1992. | 10-K | 12/31/1995 | 10(f) | ||||||

| 10(e) | Canpotex PCA Collateral Withdrawing/PCS Amending Agreement, dated as of October 7, 1993. | 10-K | 12/31/1995 | 10(g) | ||||||

| 10(f) | Canpotex Producer Agreement amending agreement dated as of July 1, 2002. | 10-Q | 6/30/2004 | 10(g) | ||||||

| 10(g) | Esterhazy Restated Mining and Processing Agreement dated January 31, 1978, between International Minerals & Chemical Corporation (Canada) Limited and the registrant’s predecessor. | F-1 (File No. |

9/28/1989 | 10(e) | ||||||

| 10(h) | Agreement dated December 21, 1990, between International Minerals & Chemical Corporation (Canada) Limited and the registrant, amending the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978. | 10-K | 12/31/1990 | 10(p) | ||||||

| 10(i) | Agreement effective August 27, 1998, between International Minerals & Chemical (Canada) Global Limited and the registrant, amending the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978 (as amended). | 10-K | 12/31/1998 | 10(l) | ||||||

| 10(j) | Agreement effective August 31, 1998, among International Minerals & Chemical (Canada) Global Limited, International Minerals & Chemical (Canada) Limited Partnership and the registrant assigning the interest in the Esterhazy Restated Mining and Processing Agreement dated January 31, 1978 (as amended) held by International Minerals & Chemical (Canada) Global Limited to International Minerals & Chemical (Canada) Limited Partnership. | 10-K | 12/31/1998 | 10(m) | ||||||

| 10(k) | Potash Corporation of Saskatchewan Inc. Stock Option Plan — Directors, as amended. | 10-K | 12/31/2006 | 10(l) | ||||||

| 10(l) | Potash Corporation of Saskatchewan Inc. Stock Option Plan — Officers and Employees, as amended. | 10-K | 12/31/2006 | 10(m) | ||||||

| 10(m) | Short-Term Incentive Plan of the registrant effective January 1, 2000, as amended. | 8-K | 3/13/2012 | 10(a) | ||||||

| 10(n) | Resolution and Forms of Agreement for Supplemental Executive Retirement Income Plan, for officers and key employees of the registrant. | 10-K | 12/31/1995 | 10(o) | ||||||

| 10(o) | Amending Resolution and revised forms of agreement regarding Supplemental Retirement Income Plan of the registrant. | 10-Q | 6/30/1996 | 10(x) | ||||||

| 10(p) | Amended and restated Supplemental Executive Retirement Income Plan of the registrant and text of amendment to existing supplemental income plan agreements. | 10-Q | 9/30/2000 | 10(mm) | ||||||

| 10(q) | Amendment, dated February 23, 2009, to the amended and restated Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | 10(r) | ||||||

| Incorporated By Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||

| 10(r) | Amendment, dated December 29, 2010, to the amended and restated Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(s) | Form of Letter of amendment to existing supplemental income plan agreements of the registrant. | 10-K | 12/31/2002 | 10(cc) | ||||||||

| 10(t) | Amended and restated agreement dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2006 | 10(s) | ||||||||

| 10(u) | Amendment, dated December 24, 2008, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(v) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(w) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated August 2, 1996, between the registrant and Wayne R. Brownlee concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(x) | Amendment, dated February 23, 2009, to the amended and restated agreement, dated August 2, 1996, between the registrant and Garth W. Moore concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2008 | |||||||||

| 10(y) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated February 20, 2007, between the registrant and William J. Doyle concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(z) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated August 2, 1996, between the registrant and Wayne R. Brownlee concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(aa) | Amendment, dated December 29, 2010, to the amended and restated agreement, dated August 2, 1996, between the registrant and Garth W. Moore concerning the Supplemental Executive Retirement Income Plan. | 10-K | 12/31/2010 | |||||||||

| 10(bb) | Supplemental Retirement Agreement dated December 24, 2008, between the registrant and Stephen F. Dowdle. | 10-K | 12/31/2011 | |||||||||

| 10(cc) | Supplemental Retirement Benefits Plan for U.S. Executives dated effective January 1, 1999. | 10-Q | 6/30/2002 | 10(aa) | ||||||||

| 10(dd) | Amendment No. 1, dated December 24, 2008, to the Supplemental Retirement Plan for U.S. Executives. | 10-K | 12/31/2008 | 10(z) | ||||||||

| 10(ee) | Amendment No. 2, dated February 23, 2009, to the Supplemental Retirement Plan for U.S. Executives. | 10-K | 12/31/2008 | 10(aa) | ||||||||

| 10(ff) | Forms of Agreement dated December 30, 1994, between the registrant and certain officers of the registrant. | 10-K | 12/31/1995 | 10(p) | ||||||||

| 10(gg) | Amendment, dated December 31, 2010, to the Agreement, dated December 30, 1994 between the registrant and William J. Doyle. | 10-K | 12/31/2010 | 10(ee) | ||||||||

| 10(hh) | Form of Agreement of Indemnification dated August 8, 1995, between the registrant and certain officers and directors of the registrant. | 10-K | 12/31/1995 | 10(q) | ||||||||

| 10(ii) | Resolution and Form of Agreement of Indemnification dated January 24, 2001. | 10-K | 12/31/2000 | |||||||||

| 10(jj) | Resolution and Form of Agreement of Indemnification — July 21, 2004. | 10-Q | 6/30/2004 | 10(ii) | ||||||||

| 10(kk) | Chief Executive Officer Medical and Dental Benefits. | 10-K | 12/31/2010 | 10(jj) | ||||||||

| 10(ll) | Deferred Share Unit Plan for Non-Employee Directors, as amended. | |||||||||||

| 10(mm) | U.S. Participant Addendum No. 1 to the Deferred Share Unit Plan for Non-Employee Directors. | 10-K | 12/31/2008 | 10(jj) | ||||||||

| Incorporated By Reference | ||||||||||||

| Exhibit Number |

Description of Document | Form | Filing Date/Period End Date |

Exhibit Number (if different) | ||||||||