Attached files

| file | filename |

|---|---|

| 8-K - 8-K - RAIT Financial Trust | ras-8k_20160225.htm |

| EX-99.1 - EX-99.1 - RAIT Financial Trust | ras-ex991_25.htm |

Exhibit 99.2

Fourth Quarter 2015

Supplemental Information

TABLE OF CONTENTS

|

Company Information

|

3 |

|

Forward-Looking Statements

|

5 |

|

Earnings Release Text

|

6 |

|

Financial Highlights

|

10 |

|

Balance Sheets |

|

|

Consolidated by quarter |

11 |

|

Consolidating, by segment

|

12 |

|

Statements of Operations, FFO & CORE FFO |

|

|

Consolidated |

13 |

|

Consolidated – Trailing 5 Quarters |

15 |

|

Consolidating, by segment

|

17 |

|

Fee and Other Income

|

19 |

|

EBITDA and Coverage Ratios

|

20 |

|

Portfolio Data: |

|

|

Lending |

22 |

|

Real Estate Summary |

24 |

|

Real Estate Properties, Changes in the portfolio |

26 |

|

Real Estate Properties at December 31, 2015

|

27 |

|

Debt Overview

|

29 |

|

Definitions |

31 |

2

RAIT Financial Trust

December 31, 2015

Company Information:

RAIT Financial Trust is an internally-managed real estate investment trust that provides debt financing options to owners of commercial real estate and invests directly into commercial real estate properties located throughout the United States. In addition, RAIT is an asset and property manager of real estate-related assets.

|

Corporate Headquarters |

2929 Arch Street 17th Floor, Cira Centre Philadelphia, Pa 19104 215.243.9000 |

|

Trading Symbol |

NYSE: “RAS” |

|

Investor Relations Contact |

Andres Viroslav 2929 Arch Street 17th Floor, Cira Centre Philadelphia, Pa 19104 215.243.9000 |

3

Common and Preferred Stock Information:

|

|

|

For the Three-Months Ended |

|

|||||||||||||||||

|

|

|

December 31, 2015 |

|

|

September 30, 2015 |

|

|

June 30, 2015 |

|

|

March 31, 2015 |

|

|

December 31, 2014 |

|

|||||

|

Common: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Price, period end |

|

$ |

2.70 |

|

|

$ |

4.96 |

|

|

$ |

6.11 |

|

|

$ |

6.86 |

|

|

$ |

7.67 |

|

|

Share Price, high |

|

$ |

5.45 |

|

|

$ |

6.24 |

|

|

$ |

7.08 |

|

|

$ |

7.85 |

|

|

$ |

7.94 |

|

|

Share Price, low |

|

$ |

2.25 |

|

|

$ |

4.77 |

|

|

$ |

6.04 |

|

|

$ |

6.62 |

|

|

$ |

6.86 |

|

|

Dividends declared |

|

$ |

0.09 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

Dividend yield, period end |

|

|

13.3 |

% |

|

|

14.5 |

% |

|

|

11.8 |

% |

|

|

10.5 |

% |

|

|

9.4 |

% |

|

Common shares outstanding |

|

|

91,586,767 |

|

|

|

90,898,034 |

|

|

|

82,895,723 |

|

|

|

82,885,444 |

|

|

|

82,506,606 |

|

|

Weighted Average common shares, basic |

|

|

90,642,318 |

|

|

|

87,110,958 |

|

|

|

82,150,475 |

|

|

|

82,081,024 |

|

|

|

81,970,075 |

|

|

Weighted Average common shares, diluted |

|

|

90,842,752 |

|

|

|

87,110,958 |

|

|

|

89,268,462 |

|

|

|

82,081,024 |

|

|

|

81,970,075 |

|

|

Preferred: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Series A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares outstanding |

|

|

5,306,084 |

|

|

|

5,306,084 |

|

|

|

5,303,591 |

|

|

|

4,775,569 |

|

|

|

4,775,569 |

|

|

Share price, period end |

|

$ |

18.15 |

|

|

$ |

18.19 |

|

|

22.34 |

|

|

23.35 |

|

|

23.32 |

|

|||

|

Par, per share |

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

Dividend |

|

$ |

0.484375 |

|

|

$ |

0.484375 |

|

|

$ |

0.484375 |

|

|

$ |

0.484375 |

|

|

$ |

0.484375 |

|

|

Yield |

|

|

10.7 |

% |

|

|

10.7 |

% |

|

|

8.7 |

% |

|

|

8.3 |

% |

|

|

8.3 |

% |

|

Series B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares outstanding |

|

|

2,340,969 |

|

|

|

2,340,969 |

|

|

|

2,325,626 |

|

|

|

2,288,465 |

|

|

|

2,288,465 |

|

|

Share price, period end |

|

$ |

18.98 |

|

|

$ |

19.06 |

|

|

$ |

22.92 |

|

|

$ |

24.50 |

|

|

$ |

24.90 |

|

|

Par, per share |

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

Dividend |

|

$ |

0.5234375 |

|

|

$ |

0.5234375 |

|

|

$ |

0.5234375 |

|

|

$ |

0.5234375 |

|

|

$ |

0.5234375 |

|

|

Yield |

|

|

11.0 |

% |

|

|

11.0 |

% |

|

|

9.1 |

% |

|

|

8.5 |

% |

|

|

8.4 |

% |

|

Series C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares outstanding |

|

|

1,640,425 |

|

|

|

1,640,425 |

|

|

|

1,640,100 |

|

|

|

1,640,100 |

|

|

|

1,640,100 |

|

|

Share price, period end |

|

$ |

19.70 |

|

|

$ |

20.14 |

|

|

$ |

24.15 |

|

|

$ |

24.84 |

|

|

$ |

25.06 |

|

|

Par, per share |

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

Dividend |

|

$ |

0.5546875 |

|

|

$ |

0.5546875 |

|

|

$ |

0.5546875 |

|

|

$ |

0.5546875 |

|

|

$ |

0.5546875 |

|

|

Yield |

|

|

11.3 |

% |

|

|

11.0 |

% |

|

|

9.2 |

% |

|

|

8.9 |

% |

|

|

8.9 |

% |

|

Series D (not publicly traded) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares outstanding |

|

|

4,000,000 |

|

|

|

4,000,000 |

|

|

|

4,000,000 |

|

|

|

4,000,000 |

|

|

|

4,000,000 |

|

|

Par, per share |

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

$ |

25.00 |

|

|

Coupon |

|

|

8.50 |

% |

|

|

7.50 |

% |

|

|

7.50 |

% |

|

|

7.50 |

% |

|

|

7.50 |

% |

4

This press release may contain certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “guidance,” "may," “plan”, "will," "should," "expect," "intend," "anticipate," "estimate," "believe," “seek,” “opportunities” or other similar words or terms. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to: overall conditions in commercial real estate and the economy generally; whether the timing and amount of investments, repayments, any capital raised and our use of leverage will vary from those underlying our assumptions; changes in the expected yield of our investments; changes in financial markets and interest rates, or to the business or financial condition of RAIT or its business; whether RAIT will be able to originate loans in the amounts and generating the returns assumed; the availability of financing and capital, including through the capital and securitization markets; whether RAIT will be able to complete sales of RAIT owned properties, whether identified for sale or under contract, in the amounts and generating the gains assumed; and those disclosed in RAIT’s filings with the Securities and Exchange Commission. RAIT undertakes no obligation to update these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as may be required by law.

5

RAIT Financial Trust Announces Fourth Quarter and Fiscal 2015 Financial Results

PHILADELPHIA, PA — February 25, 2016 — RAIT Financial Trust (“RAIT”) (NYSE: RAS) today announced fourth quarter and fiscal 2015 financial results. All per share results are reported on a diluted basis.

Highlights

|

|

- |

Cash Available for Distribution (“CAD”) per share of $0.28 for the quarter ended December 31, 2015 and $1.11 for the year ended December 31, 2015. CAD per share, without real estate gains, of $0.19 for the quarter ended December 31, 2015 and $0.78 for the year ended December 31, 2015. |

|

|

- |

Earnings per share of $0.02 for the quarter ended December 31, 2015 and $0.08 for the year ended December 31, 2015. |

|

|

- |

Investments in mortgages and loans, at cost, increased 16.5% to $1.62 billion at December 31, 2015 from $1.39 billion at December 31, 2014. |

|

|

- |

RAIT originated $321.8 million of loans during the quarter ended December 31, 2015 and $996.9 million of loans for the year ended December 31, 2015. |

|

|

- |

RAIT paid a fourth quarter dividend of $0.09 per common share on January 29, 2016. |

Scott Schaeffer, RAIT’s Chairman and CEO, said, “Our platform generated just under $1 billion of loan originations in 2015 including more than $600 million of bridge loans. We completed two floating-rate securitizations and sold $425 million of fixed-rate conduit loans during the year. We continue to execute on our capital recycling strategy through property sales given the volatile state of the capital and securitization markets.”

Commercial Real Estate (“CRE”) Business

|

|

- |

RAIT originated $321.8 million of loans during the quarter ended December 31, 2015 consisting of $71.9 million of fixed-rate conduit loans and $249.9 million of floating-rate bridge loans. RAIT originated $996.9 million of loans during the year ended December 31, 2015 consisting of $384.1 million of fixed-rate conduit loans, $607.8 million of floating-rate bridge loans and a $5.0 million mezzanine loan. |

|

|

- |

RAIT sold $85.4 million of conduit loans during the quarter ended December 31, 2015 which generated fee income of $1.1 million. RAIT sold $425.0 million of conduit loans during the year ended December 31, 2015 which generated fee income of $7.2 million. |

|

|

- |

In December, RAIT closed its fifth non-recourse, floating-rate CMBS transaction totaling $347.4 million collateralized by floating rate commercial real estate first lien mortgage loans and pari passu participation interests in such mortgage loans. The transaction involved the sale by a RAIT subsidiary of investment grade notes totaling approximately $263.6 million with a weighted average cost of LIBOR plus 2.62%. RAIT affiliates retained certain investment grade notes and all of the below investment grade and un-rated subordinated interests totaling approximately $83.8 million. |

|

|

- |

CRE loan repayments were $121.6 million for the quarter ended December 31, 2015 and $291.2 million during the year ended December 31, 2015 |

6

CRE Property Portfolio & Property Sales

|

|

- |

As of December 31, 2015, RAIT’s investments in real estate were $2.5 billion which includes $1.4 billion of multi-family properties owned by Independence Realty Trust, Inc. (“IRT”) (NYSE MKT: IRT). IRT is externally advised by RAIT and is a consolidated RAIT entity. IRT is a REIT focused on owning multifamily properties. At December 31, 2015, RAIT owned 15.5% of IRT’s outstanding common stock. |

|

|

- |

During the quarter ended December 31, 2015, RAIT sold three properties, consisting of two apartment communities and an office property, for $52.9 million and generated net proceeds of approximately $8.4 million after costs and full repayment of the underlying debt. IRT sold one apartment community for $33.6 million and generated net proceeds of approximately $14.2 million after costs and full repayment of the underlying debt. During the year ended December 31, 2015, RAIT sold eight properties, six apartment communities and one office property, and one parcel of land for $141.4 million and generated net proceeds of approximately $27.5 million after costs and full repayment of the underlying debt. |

|

|

- |

During the three-months ended December 31, 2015, RAIT converted two loans secured by ten industrial properties and by one office property, respectively, into ownership of those properties. Those properties had an aggregate carrying value of $73.1 million. |

|

|

- |

RAIT reported a $0.9 million asset impairment for the quarter ended December 31, 2015 on an office property in Denver, Colorado and a parcel of land in Daytona Beach, FL. Both of these properties are currently under contract to be sold. |

|

|

- |

On September 17, 2015, IRT completed the acquisition of Trade Street Residential, Inc. adding nineteen high-quality properties with 4,989 units to its portfolio. RAIT expects the acquisition to benefit RAIT through RAIT’s ownership of IRT common stock and increased fees paid to RAIT by IRT. |

Asset & Property Management

|

|

- |

Total assets under management increased 33.3% to $6.0 billion at December 31, 2015 from $4.5 billion at December 31, 2014. |

|

|

- |

RAIT’s property management companies managed 19,639 apartment units and 22.8 million square feet of office and retail space at December 31, 2015. |

|

|

- |

RAIT generated $9.3 million in asset and property management fees and incentive fees through its external management of IRT during the year ended December 31, 2015. |

|

|

- |

RAIT generated $12.8 million of property management and leasing fees primarily through its retail property manager subsidiary and through services provided by its multi-family property manager subsidiary to unaffiliated properties during the year ended December 31, 2015. |

Dividends

|

|

- |

On December 7, 2015, RAIT’s Board of Trustees (the “Board”) declared a fourth quarter 2015 cash dividend on RAIT’s common shares of $0.09 per common share. The dividend was paid on January 29, 2016 to holders of record on January 8, 2016. |

|

|

- |

On November 4, 2015, the Board declared a fourth quarter 2015 cash dividend of $0.484375 per share on RAIT’s 7.75% Series A Cumulative Redeemable Preferred Shares, $0.5234375 per share on RAIT’s 8.375% Series B Cumulative Redeemable Preferred Shares and $0.5546875 per share on RAIT’s 8.875% Series C Cumulative Redeemable Preferred Shares. The dividends were paid on December 31, 2015 to holders of record on December 1, 2015. |

7

RAIT estimates that its 2016 full year CAD per diluted share will be in a range of $0.85-$0.95 per common share. 2016 full year CAD guidance includes $0.35 per share of gains on property sales. A reconciliation of RAIT's projected net income (loss) allocable to common shares to its projected CAD, a non-GAAP financial measure, is included below. The assumptions underlying this estimate are also included below.

|

|

2016 Annualized Projected CAD(1) |

|||||

|

Net income (loss) allocable to common shares |

|

$22,792 |

- |

$31,892 |

|

|

|

Adjustments: |

|

|

|

|

|

|

|

Gains on property sales |

(5,766) |

- |

(5,766) |

|

||

|

Depreciation, amortization expense and other items |

60,324 |

- |

60,324 |

|

||

|

CAD |

|

$77,350 |

- |

$86,450 |

|

|

|

CAD per share |

|

$0.85 |

- |

$0.95 |

|

|

|

CAD per share, without real estate gains |

|

$0.50 |

- |

$0.60 |

|

|

|

|

(1) |

Constitutes forward-looking information. Actual full 2016 CAD could vary significantly from the projections presented. CAD may fluctuate based upon a variety of factors, including those described in “Forward Looking Statements” below. Our estimate is based on the following key operating assumptions during 2016: |

|

|

- |

Gross loan originations of $200 million to $500 million. |

|

|

- |

No CMBS gain on sale profits. |

|

|

- |

RAIT property sale gains of $32 million. |

|

|

- |

Loan repayments totaling $200 million. |

|

|

- |

No capital issuances in 2016. |

Selected Financial Information

See Schedule I to this Release for selected financial information for RAIT.

Non-GAAP Financial Measures and Definitions

RAIT discloses the following non-GAAP financial measures in this release: funds from operations (“FFO”), CAD and net operating income (“NOI”). A reconciliation of RAIT’s reported net income (loss) allocable to common shares to its FFO and CAD is included as Schedule IV to this release. A reconciliation of RAIT’s NOI to its reported net income (loss) is included as Schedule V to this release. See Schedule VI to this release for management’s respective definitions and rationales for the usefulness of each of these non-GAAP financial measures and other definitions used in this release.

Supplemental Information

RAIT produces supplemental information that includes details regarding the performance of the portfolio, financial information, non-GAAP financial measures and other useful information for investors. The supplemental also contains deconsolidating financial information. The supplemental information is available via the Company's website, www.rait.com, through the "Investor Relations" section.

Conference Call

All interested parties can listen to the live conference call webcast at 9:00 AM ET on Thursday, February 25, 2016 from the home page of the RAIT Financial Trust website at www.rait.com or by dialing 877.787.4169, access code 38442508. For those who are not available to listen to the live call, the replay will be available shortly following the live call on RAIT’s website and telephonically until Thursday, March 3, 2016, by dialing 855.859.2056, access code 38442508.

About RAIT Financial Trust

RAIT Financial Trust is an internally-managed real estate investment trust that provides debt financing options to owners of commercial real estate and invests directly into commercial real estate properties located throughout the United States. In addition,

8

RAIT is an asset and property manager of real estate-related assets. For more information, please visit www.rait.com or call Investor Relations at 215.243.9000.

Forward-Looking Statements

This press release may contain certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “guidance,” "may," “plan”, "will," "should," "expect," "intend," "anticipate," "estimate," "believe," “seek,” “opportunities” or other similar words or terms. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to: overall conditions in commercial real estate and the economy generally; whether the timing and amount of investments, repayments, any capital raised and our use of leverage will vary from those underlying our assumptions; changes in the expected yield of our investments; changes in financial markets and interest rates, or to the business or financial condition of RAIT or its business; whether RAIT will be able to originate loans in the amounts and generating the returns assumed; the availability of financing and capital, including through the capital and securitization markets; whether RAIT will be able to complete sales of RAIT owned properties, whether identified for sale or under contract, in the amounts and generating the gains assumed; and those disclosed in RAIT’s filings with the Securities and Exchange Commission. RAIT undertakes no obligation to update these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as may be required by law.

RAIT Financial Trust Contact

Andres Viroslav

215-243-9000

aviroslav@rait.com

9

|

($'s in 000's) |

|

For the Three-Months Ended |

|

|||||||||||||||||

|

|

|

December 31, 2015 |

|

|

September 30, 2015 |

|

|

June 30, 2015 |

|

|

March 31, 2015 |

|

|

December 31, 2014 |

|

|||||

|

OPERATING DATA: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lending: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in loans |

|

$ |

1,623,583 |

|

|

$ |

1,588,097 |

|

|

$ |

1,506,542 |

|

|

$ |

1,504,456 |

|

|

$ |

1,392,436 |

|

|

Gross loan production |

|

$ |

321,837 |

|

|

$ |

237,674 |

|

|

$ |

218,613 |

|

|

$ |

218,770 |

|

|

$ |

255,335 |

|

|

CMBS gain on sales (included in fee income) |

|

$ |

1,135 |

|

|

$ |

434 |

|

|

$ |

3,681 |

|

|

$ |

1,996 |

|

|

$ |

2,986 |

|

|

CMBS loans sold |

|

$ |

85,430 |

|

|

$ |

116,251 |

|

|

$ |

130,401 |

|

|

$ |

92,897 |

|

|

$ |

170,679 |

|

|

Average CMBS Gain on Sale (points) |

|

|

1.3 |

|

|

|

0.4 |

|

|

|

2.8 |

|

|

|

2.1 |

|

|

|

1.7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Real estate portfolio: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross real estate investments (a) |

|

$ |

2,517,645 |

|

|

$ |

2,448,331 |

|

|

$ |

1,783,888 |

|

|

$ |

1,833,978 |

|

|

$ |

1,840,451 |

|

|

Property income (a) |

|

$ |

69,464 |

|

|

$ |

55,459 |

|

|

$ |

55,534 |

|

|

$ |

53,274 |

|

|

$ |

46,096 |

|

|

Operating expenses (a) |

|

$ |

31,476 |

|

|

$ |

25,832 |

|

|

$ |

26,416 |

|

|

$ |

25,277 |

|

|

$ |

22,948 |

|

|

Net operating income (a) |

|

$ |

37,988 |

|

|

$ |

29,627 |

|

|

$ |

29,118 |

|

|

$ |

27,997 |

|

|

$ |

23,148 |

|

|

NOI margin (a) |

|

|

54.7 |

% |

|

|

53.4 |

% |

|

|

52.4 |

% |

|

|

52.6 |

% |

|

|

50.2 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EARNINGS & DIVIDENDS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per Share -- diluted |

|

$ |

0.02 |

|

|

$ |

(0.07 |

) |

|

$ |

0.22 |

|

|

$ |

(0.09 |

) |

|

$ |

(3.11 |

) |

|

FFO per share |

|

$ |

(0.08 |

) |

|

$ |

(0.05 |

) |

|

$ |

0.15 |

|

|

$ |

0.05 |

|

|

$ |

(2.97 |

) |

|

CAD per share |

|

$ |

0.28 |

|

|

$ |

0.27 |

|

|

$ |

0.37 |

|

|

$ |

0.19 |

|

|

$ |

0.26 |

|

|

CAD per share, without real estate gains |

|

$ |

0.19 |

|

|

$ |

0.20 |

|

|

$ |

0.21 |

|

|

$ |

0.18 |

|

|

$ |

0.26 |

|

|

Dividends per share |

|

$ |

0.09 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

$ |

0.18 |

|

|

CAD payout ratio |

|

|

31.8 |

% |

|

|

66.0 |

% |

|

|

48.8 |

% |

|

|

96.7 |

% |

|

|

70.4 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CAPITALIZATION AND COVERAGE RATIOS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Debt: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

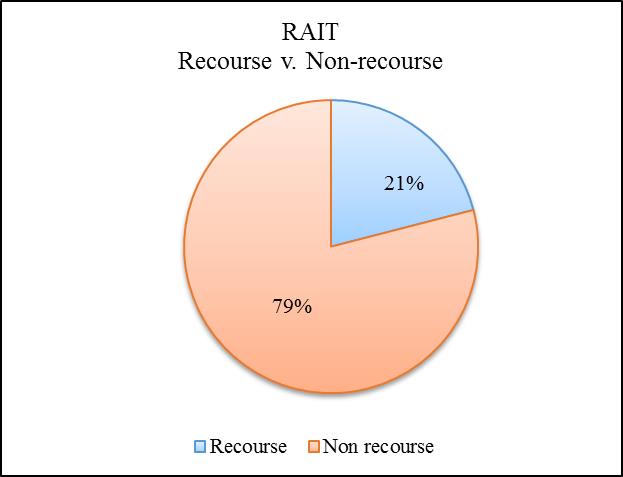

Recourse |

|

$ |

494,697 |

|

|

$ |

586,952 |

|

|

$ |

497,430 |

|

|

$ |

579,258 |

|

|

$ |

509,701 |

|

|

Non-recourse |

|

|

2,864,753 |

|

|

|

2,613,029 |

|

|

|

2,164,098 |

|

|

|

2,107,499 |

|

|

|

2,105,965 |

|

|

Total debt |

|

|

3,359,450 |

|

|

|

3,199,981 |

|

|

|

2,661,528 |

|

|

|

2,686,757 |

|

|

|

2,615,666 |

|

|

Preferred shares (par) |

|

|

332,187 |

|

|

|

332,187 |

|

|

|

331,733 |

|

|

|

317,603 |

|

|

|

317,603 |

|

|

Common shares (market capitalization) |

|

|

247,284 |

|

|

|

450,854 |

|

|

|

506,493 |

|

|

|

568,594 |

|

|

|

632,826 |

|

|

Noncontrolling interests, at carrying value |

|

|

340,213 |

|

|

|

346,063 |

|

|

|

204,034 |

|

|

|

208,894 |

|

|

|

214,297 |

|

|

Total market capitalization |

|

$ |

4,279,134 |

|

|

$ |

4,329,085 |

|

|

$ |

3,703,788 |

|

|

$ |

3,781,848 |

|

|

$ |

3,780,392 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Liabilities/Total Gross Assets |

|

|

77.9 |

% |

|

|

77.2 |

% |

|

|

77.5 |

% |

|

|

78.0 |

% |

|

|

77.3 |

% |

|

Total Liabilities + Preferred/Total Gross Assets |

|

|

85.0 |

% |

|

|

84.6 |

% |

|

|

86.4 |

% |

|

|

86.5 |

% |

|

|

85.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Coverage |

|

|

1.94 |

x |

|

|

1.81 |

x |

|

|

2.12 |

x |

|

|

1.93 |

x |

|

|

2.20 |

x |

|

Interest + Preferred Coverage |

|

|

1.55 |

x |

|

|

1.42 |

x |

|

|

1.63 |

x |

|

|

1.50 |

x |

|

|

1.70 |

x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OTHER KEY BENCHMARKS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets Under Management (AUM) |

|

$ |

6,026,341 |

|

|

$ |

5,820,702 |

|

|

$ |

4,764,259 |

|

|

$ |

4,607,413 |

|

|

$ |

4,485,525 |

|

|

Total Gross Assets |

|

$ |

4,645,622 |

|

|

$ |

4,475,217 |

|

|

$ |

3,754,148 |

|

|

$ |

3,741,103 |

|

|

$ |

3,681,955 |

|

|

|

(a) |

Includes Independence Realty Trust. |

10

CONSOLIDATED, by quarter

|

($'s in 000's) |

|

As of |

|

|

|||||||||||||||||

|

|

|

December 31, 2015 |

|

|

September 30, 2015 |

|

|

June 30, 2015 |

|

|

March 31, 2015 |

|

|

December 31, 2014 |

|

|

|||||

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in loans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment in loans |

|

$ |

1,623,583 |

|

|

$ |

1,588,097 |

|

|

$ |

1,506,542 |

|

|

$ |

1,504,456 |

|

|

$ |

1,392,436 |

|

|

|

Allowance for loan losses |

|

|

(17,097 |

) |

|

|

(14,646 |

) |

|

|

(12,796 |

) |

|

|

(10,797 |

) |

|

|

(9,218 |

) |

|

|

Investments in loans, net |

|

|

1,606,486 |

|

|

|

1,573,451 |

|

|

|

1,493,746 |

|

|

|

1,493,659 |

|

|

|

1,383,218 |

|

|

|

Investments in real estate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in real estate at cost |

|

|

2,517,645 |

|

|

|

2,448,331 |

|

|

|

1,783,888 |

|

|

|

1,833,978 |

|

|

|

1,840,451 |

|

|

|

Accumulated depreciation |

|

|

(198,326 |

) |

|

|

(188,581 |

) |

|

|

(178,572 |

) |

|

|

(175,319 |

) |

|

|

(168,480 |

) |

|

|

Investments in real estate, net |

|

|

2,319,319 |

|

|

|

2,259,750 |

|

|

|

1,605,316 |

|

|

|

1,658,659 |

|

|

|

1,671,971 |

|

|

|

Investments in securities, at fair value |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

31,412 |

|

|

|

Cash and cash equivalents |

|

|

125,886 |

|

|

|

92,652 |

|

|

|

104,772 |

|

|

|

92,657 |

|

|

|

121,726 |

|

|

|

Restricted cash |

|

|

213,012 |

|

|

|

159,200 |

|

|

|

179,878 |

|

|

|

126,850 |

|

|

|

124,220 |

|

|

|

Accrued interest receivable |

|

|

47,343 |

|

|

|

56,249 |

|

|

|

56,844 |

|

|

|

53,586 |

|

|

|

51,640 |

|

|

|

Other assets |

|

|

71,207 |

|

|

|

76,222 |

|

|

|

77,708 |

|

|

|

84,629 |

|

|

|

72,023 |

|

|

|

Deferred costs, net |

|

|

31,368 |

|

|

|

29,806 |

|

|

|

25,117 |

|

|

|

25,034 |

|

|

|

27,802 |

|

|

|

Intangible assets, net |

|

|

32,675 |

|

|

|

39,306 |

|

|

|

32,195 |

|

|

|

30,710 |

|

|

|

29,463 |

|

|

|

Total assets |

|

$ |

4,447,296 |

|

|

$ |

4,286,636 |

|

|

$ |

3,575,576 |

|

|

$ |

3,565,784 |

|

|

$ |

3,513,475 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indebtedness: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indebtedness: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recourse |

|

$ |

494,697 |

|

|

$ |

586,952 |

|

|

$ |

497,430 |

|

|

$ |

579,258 |

|

|

$ |

509,701 |

|

|

|

Nonrecourse |

|

|

2,864,753 |

|

|

|

2,613,029 |

|

|

|

2,164,098 |

|

|

|

2,107,499 |

|

|

|

2,105,965 |

|

|

|

Indebtedness, total |

|

|

3,359,450 |

|

|

|

3,199,981 |

|

|

|

2,661,528 |

|

|

|

2,686,757 |

|

|

|

2,615,666 |

|

|

|

Accrued interest payable |

|

|

9,834 |

|

|

|

13,748 |

|

|

|

11,042 |

|

|

|

12,889 |

|

|

|

10,269 |

|

|

|

Accounts payable and accrued expenses |

|

|

39,672 |

|

|

|

42,219 |

|

|

|

52,728 |

|

|

|

48,489 |

|

|

|

54,962 |

|

|

|

Derivative liabilities |

|

|

4,727 |

|

|

|

8,960 |

|

|

|

12,154 |

|

|

|

17,767 |

|

|

|

20,695 |

|

|

|

Borrowers escrows, dividends payable and other liabilities |

|

|

203,477 |

|

|

|

188,797 |

|

|

|

172,621 |

|

|

|

152,757 |

|

|

|

144,733 |

|

|

|

Total liabilities |

|

|

3,617,160 |

|

|

|

3,453,705 |

|

|

|

2,910,073 |

|

|

|

2,918,659 |

|

|

|

2,846,325 |

|

|

|

Series D preferred stock |

|

|

85,395 |

|

|

|

83,787 |

|

|

|

82,513 |

|

|

|

80,871 |

|

|

|

79,308 |

|

|

|

Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred shares: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shareholders' Equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7.75% Series A Preferred shares |

|

|

53 |

|

|

|

53 |

|

|

|

53 |

|

|

|

48 |

|

|

|

48 |

|

|

|

8.375% Series B Preferred shares |

|

|

23 |

|

|

|

23 |

|

|

|

23 |

|

|

|

23 |

|

|

|

23 |

|

|

|

8.875% Series C Preferred shares |

|

|

17 |

|

|

|

17 |

|

|

|

17 |

|

|

|

17 |

|

|

|

17 |

|

|

|

Common shares, $0.01 par value per share |

|

|

2,748 |

|

|

|

2,727 |

|

|

|

2,487 |

|

|

|

2,484 |

|

|

|

2,473 |

|

|

|

Additional paid in capital |

|

|

2,087,137 |

|

|

|

2,082,695 |

|

|

|

2,039,594 |

|

|

|

2,026,347 |

|

|

|

2,025,683 |

|

|

|

Accumulated other comprehensive income (loss) |

|

|

(4,699 |

) |

|

|

(8,022 |

) |

|

|

(11,605 |

) |

|

|

(15,778 |

) |

|

|

(20,788 |

) |

|

|

Retained earnings (deficit) |

|

|

(1,680,751 |

) |

|

|

(1,674,412 |

) |

|

|

(1,651,613 |

) |

|

|

(1,655,781 |

) |

|

|

(1,633,911 |

) |

|

|

Total shareholders' equity |

|

|

404,528 |

|

|

|

403,081 |

|

|

|

378,956 |

|

|

|

357,360 |

|

|

|

373,545 |

|

|

|

Noncontrolling Interests |

|

|

340,213 |

|

|

|

346,063 |

|

|

|

204,034 |

|

|

|

208,894 |

|

|

|

214,297 |

|

|

|

Total equity |

|

|

744,741 |

|

|

|

749,144 |

|

|

|

582,990 |

|

|

|

566,254 |

|

|

|

587,842 |

|

|

|

Total liabilities and equity |

|

$ |

4,447,296 |

|

|

$ |

4,286,636 |

|

|

$ |

3,575,576 |

|

|

$ |

3,565,784 |

|

|

$ |

3,513,475 |

|

|

11

CONSOLIDATING – AS OF DECEMBER 31, 2015

|

($'s in 000's) |

|

As of December 31, 2015 |

|

|||||||||||||

|

|

|

RAIT |

|

|

IRT |

|

|

Corporate / Eliminations |

|

|

Consolidated |

|

||||

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in loans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment in loans |

|

$ |

1,661,658 |

|

|

$ |

- |

|

|

$ |

(38,075 |

) |

|

$ |

1,623,583 |

|

|

Allowance for loan losses |

|

|

(17,097 |

) |

|

|

- |

|

|

|

- |

|

|

|

(17,097 |

) |

|

Investments in loans, net |

|

|

1,644,561 |

|

|

|

- |

|

|

|

(38,075 |

) |

|

|

1,606,486 |

|

|

Investments in real estate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in real estate at cost |

|

|

1,145,630 |

|

|

|

1,372,015 |

|

|

|

- |

|

|

|

2,517,645 |

|

|

Accumulated depreciation |

|

|

(158,688 |

) |

|

|

(39,638 |

) |

|

|

- |

|

|

|

(198,326 |

) |

|

Investments in real estate, net |

|

|

986,942 |

|

|

|

1,332,377 |

|

|

|

- |

|

|

|

2,319,319 |

|

|

Investment in IRT |

|

|

53,947 |

|

|

|

- |

|

|

|

(53,947 |

) |

|

|

- |

|

|

Cash and cash equivalents |

|

|

87,585 |

|

|

|

38,301 |

|

|

|

- |

|

|

|

125,886 |

|

|

Restricted cash |

|

|

207,599 |

|

|

|

5,413 |

|

|

|

- |

|

|

|

213,012 |

|

|

Accrued interest receivable |

|

|

47,343 |

|

|

|

- |

|

|

|

- |

|

|

|

47,343 |

|

|

Other assets |

|

|

68,281 |

|

|

|

3,362 |

|

|

|

(436 |

) |

|

|

71,207 |

|

|

Deferred costs, net |

|

|

22,142 |

|

|

|

9,226 |

|

|

|

- |

|

|

|

31,368 |

|

|

Intangible assets, net |

|

|

28,940 |

|

|

|

3,735 |

|

|

|

- |

|

|

|

32,675 |

|

|

Total assets |

|

$ |

3,147,340 |

|

|

$ |

1,392,414 |

|

|

$ |

(92,458 |

) |

|

$ |

4,447,296 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indebtedness: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recourse |

|

$ |

494,697 |

|

|

$ |

391,500 |

|

|

$ |

(391,500 |

) |

|

$ |

494,697 |

|

|

Nonrecourse |

|

|

1,926,991 |

|

|

|

584,337 |

|

|

|

353,425 |

|

|

|

2,864,753 |

|

|

Indebtedness, total |

|

|

2,421,688 |

|

|

|

975,837 |

|

|

|

(38,075 |

) |

|

|

3,359,450 |

|

|

Accrued interest payable |

|

|

8,595 |

|

|

|

1,239 |

|

|

|

- |

|

|

|

9,834 |

|

|

Accounts payable and accrued expenses |

|

|

20,368 |

|

|

|

19,304 |

|

|

|

- |

|

|

|

39,672 |

|

|

Derivative liabilities |

|

|

4,727 |

|

|

|

- |

|

|

|

- |

|

|

|

4,727 |

|

|

Borrowers escrows, dividends payable and other liabilities |

|

|

197,909 |

|

|

|

6,004 |

|

|

|

(436 |

) |

|

|

203,477 |

|

|

Total liabilities |

|

|

2,653,287 |

|

|

|

1,002,384 |

|

|

|

(38,511 |

) |

|

|

3,617,160 |

|

|

Series D preferred stock |

|

|

85,395 |

|

|

|

- |

|

|

|

- |

|

|

|

85,395 |

|

|

Equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shareholders' Equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7.75% Series A Preferred shares |

|

|

53 |

|

|

|

- |

|

|

|

- |

|

|

|

53 |

|

|

8.375% Series B Preferred shares |

|

|

23 |

|

|

|

- |

|

|

|

- |

|

|

|

23 |

|

|

8.875% Series C Preferred shares |

|

|

17 |

|

|

|

- |

|

|

|

- |

|

|

|

17 |

|

|

Common shares, $0.01 par value per share |

|

|

2,748 |

|

|

|

471 |

|

|

|

(471 |

) |

|

|

2,748 |

|

|

Additional paid in capital |

|

|

2,087,137 |

|

|

|

378,187 |

|

|

|

(378,187 |

) |

|

|

2,087,137 |

|

|

Accumulated other comprehensive income (loss) |

|

|

(4,691 |

) |

|

|

(8 |

) |

|

|

- |

|

|

|

(4,699 |

) |

|

Retained earnings (deficit) |

|

|

(1,680,751 |

) |

|

|

(14,500 |

) |

|

|

14,500 |

|

|

|

(1,680,751 |

) |

|

Total shareholders' equity |

|

|

404,536 |

|

|

|

364,150 |

|

|

|

(364,158 |

) |

|

|

404,528 |

|

|

Noncontrolling Interests |

|

|

4,122 |

|

|

|

25,880 |

|

|

|

310,211 |

|

|

|

340,213 |

|

|

Total equity |

|

|

408,658 |

|

|

|

390,030 |

|

|

|

(53,947 |

) |

|

|

744,741 |

|

|

Total liabilities and equity |

|

$ |

3,147,340 |

|

|

$ |

1,392,414 |

|

|

$ |

(92,458 |

) |

|

$ |

4,447,296 |

|

12

STATEMENTS OF OPERATIONS, FFO & CAD

CONSOLIDATED – THREE MONTHS AND YEAR ENDED DECEMBER 31, 2015

|

($'s in 000's, except per share amounts) |

|

Three-Months Ended December 31 |

|

|

Year Ended December 31 |

|

||||||||||

|

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

||||

|

Revenue: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest margin |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment interest income |

|

$ |

26,609 |

|

|

$ |

30,537 |

|

|

$ |

98,432 |

|

|

$ |

133,419 |

|

|

Investment interest expense |

|

|

(6,733 |

) |

|

|

(7,968 |

) |

|

|

(29,250 |

) |

|

|

(30,310 |

) |

|

Net interest margin |

|

|

19,876 |

|

|

|

22,569 |

|

|

|

69,182 |

|

|

|

103,109 |

|

|

Property income |

|

|

69,464 |

|

|

|

46,096 |

|

|

|

233,731 |

|

|

|

162,281 |

|

|

Fee and other income |

|

|

5,004 |

|

|

|

5,167 |

|

|

|

21,069 |

|

|

|

24,280 |

|

|

Total revenue |

|

|

94,344 |

|

|

|

73,832 |

|

|

|

323,982 |

|

|

|

289,670 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense |

|

|

25,408 |

|

|

|

16,635 |

|

|

|

84,338 |

|

|

|

55,391 |

|

|

Real estate operating expenses |

|

|

31,476 |

|

|

|

22,948 |

|

|

|

109,001 |

|

|

|

81,584 |

|

|

Compensation expenses |

|

|

8,416 |

|

|

|

5,050 |

|

|

|

28,229 |

|

|

|

28,168 |

|

|

General and administrative expenses |

|

|

5,825 |

|

|

|

4,414 |

|

|

|

20,779 |

|

|

|

17,653 |

|

|

Acquisition and integration expenses |

|

|

1,684 |

|

|

|

950 |

|

|

|

16,527 |

|

|

|

2,358 |

|

|

Provision for loan losses |

|

|

2,450 |

|

|

|

2,000 |

|

|

|

8,300 |

|

|

|

5,500 |

|

|

Depreciation and amortization expense |

|

|

22,583 |

|

|

|

18,065 |

|

|

|

73,868 |

|

|

|

56,784 |

|

|

Total expenses |

|

|

97,842 |

|

|

|

70,062 |

|

|

|

341,042 |

|

|

|

247,438 |

|

|

Operating Income |

|

|

(3,498 |

) |

|

|

3,770 |

|

|

|

(17,060 |

) |

|

|

42,232 |

|

|

Other income (expense) |

|

|

7 |

|

|

|

51 |

|

|

|

(1,009 |

) |

|

|

(21,398 |

) |

|

Gains (loss) on assets |

|

|

19,094 |

|

|

|

(20 |

) |

|

|

43,805 |

|

|

|

(5,370 |

) |

|

Asset impairment |

|

|

(929 |

) |

|

|

— |

|

|

|

(8,179 |

) |

|

|

— |

|

|

TSRE financing extinguishment and employee separation expenses |

|

|

— |

|

|

|

— |

|

|

|

(27,508 |

) |

|

|

— |

|

|

Gains (losses) on IRT merger with TSRE |

|

|

592 |

|

|

|

— |

|

|

|

64,604 |

|

|

|

— |

|

|

Gains (loss) on deconsolidation of VIEs |

|

|

— |

|

|

|

(215,804 |

) |

|

|

— |

|

|

|

(215,804 |

) |

|

Gain (loss) on sale of collateral management contracts |

|

|

— |

|

|

|

4,549 |

|

|

|

— |

|

|

|

4,549 |

|

|

Gain (loss) on debt extinguishment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

2,421 |

|

|

Change in fair value of financial instruments |

|

|

(1,828 |

) |

|

|

(39,319 |

) |

|

|

11,638 |

|

|

|

(98,752 |

) |

|

Income (loss) before taxes |

|

|

13,438 |

|

|

|

(246,773 |

) |

|

|

66,291 |

|

|

|

(292,122 |

) |

|

Income tax benefit (provision) |

|

|

(1,478 |

) |

|

|

(307 |

) |

|

|

(2,798 |

) |

|

|

2,147 |

|

|

Net income (loss) |

|

|

11,960 |

|

|

|

(247,080 |

) |

|

|

63,493 |

|

|

|

(289,975 |

) |

|

Income allocated to preferred shares |

|

|

(8,447 |

) |

|

|

(8,365 |

) |

|

|

(32,830 |

) |

|

|

(28,993 |

) |

|

(Income) loss allocated to noncontrolling interests |

|

|

(1,682 |

) |

|

|

444 |

|

|

|

(23,505 |

) |

|

|

464 |

|

|

Net income (loss) available to common shares |

|

$ |

1,831 |

|

|

$ |

(255,001 |

) |

|

$ |

7,158 |

|

|

$ |

(318,504 |

) |

|

EPS - BASIC |

|

$ |

0.02 |

|

|

$ |

(3.11 |

) |

|

$ |

0.08 |

|

|

$ |

(3.92 |

) |

|

EPS - DILUTED |

|

$ |

0.02 |

|

|

$ |

(3.11 |

) |

|

$ |

0.08 |

|

|

$ |

(3.92 |

) |

|

Weighted-average shares outstanding - Basic |

|

|

90,642,318 |

|

|

|

81,970,075 |

|

|

|

85,524,073 |

|

|

|

81,328,129 |

|

|

Weighted-average shares outstanding - Diluted |

|

|

90,842,752 |

|

|

|

81,970,075 |

|

|

|

86,457,871 |

|

|

|

81,328,129 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FUNDS FROM OPERATIONS (FFO): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (loss) available to common shares |

|

$ |

1,831 |

|

|

$ |

(255,001 |

) |

|

$ |

7,158 |

|

|

$ |

(318,504 |

) |

|

Add-Back (Deduct): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation |

|

|

10,022 |

|

|

|

11,370 |

|

|

|

41,096 |

|

|

|

38,620 |

|

|

(Gains) Losses on the sale of real estate |

|

|

(18,803 |

) |

|

|

— |

|

|

|

(43,514 |

) |

|

|

319 |

|

|

FFO |

|

$ |

(6,950 |

) |

|

$ |

(243,631 |

) |

|

$ |

4,740 |

|

|

$ |

(279,565 |

) |

|

FFO per share--basic |

|

$ |

(0.08 |

) |

|

$ |

(2.97 |

) |

|

$ |

0.06 |

|

|

$ |

(3.44 |

) |

|

Weighted-average shares outstanding |

|

|

90,642,318 |

|

|

|

81,970,075 |

|

|

|

85,524,073 |

|

|

|

81,328,129 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (loss) available to common shares |

|

$ |

1,831 |

|

|

$ |

(255,001 |

) |

|

$ |

7,158 |

|

|

$ |

(318,504 |

) |

|

Add-Back (Deduct): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization expense |

|

|

22,583 |

|

|

|

18,065 |

|

|

|

73,868 |

|

|

|

56,784 |

|

|

Change in fair value of financial instruments |

|

|

1,828 |

|

|

|

39,319 |

|

|

|

(11,638 |

) |

|

|

98,752 |

|

|

(Gains) losses on assets |

|

|

(7,803 |

) |

|

|

20 |

|

|

|

(12,204 |

) |

|

|

5,370 |

|

|

TSRE financing extinguishment and employee separation expenses |

|

|

— |

|

|

|

— |

|

|

|

27,508 |

|

|

|

— |

|

|

Gains (losses) on IRT merger with TSRE |

|

|

(592 |

) |

|

|

— |

|

|

|

(64,604 |

) |

|

|

— |

|

|

(Gains) losses on deconsolidation of VIEs |

|

|

— |

|

|

|

215,804 |

|

|

|

— |

|

|

|

215,804 |

|

|

(Gains) losses on debt extinguishment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(2,421 |

) |

|

Taberna VIII and Taberna IX securitizations, net effect |

|

|

— |

|

|

|

(5,868 |

) |

|

|

— |

|

|

|

(26,931 |

) |

|

Straight-line rental adjustments |

|

|

148 |

|

|

|

1,440 |

|

|

|

95 |

|

|

|

1,111 |

|

|

Equity based compensation |

|

|

913 |

|

|

|

630 |

|

|

|

4,466 |

|

|

|

4,407 |

|

|

Acquisition and integration expenses |

|

|

1,684 |

|

|

|

950 |

|

|

|

16,527 |

|

|

|

2,358 |

|

|

Origination fees and other deferred items |

|

|

10,768 |

|

|

|

5,554 |

|

|

|

35,659 |

|

|

|

19,596 |

|

|

Provision for losses |

|

|

2,450 |

|

|

|

2,000 |

|

|

|

8,300 |

|

|

|

5,500 |

|

|

Asset impairment |

|

|

929 |

|

|

|

— |

|

|

|

8,179 |

|

|

|

— |

|

|

Noncontrolling interest effect of certain adjustments |

|

|

(9,055 |

) |

|

|

(1,951 |

) |

|

|

1,750 |

|

|

|

(4,302 |

) |

|

CAD |

|

$ |

25,684 |

|

|

$ |

20,962 |

|

|

$ |

95,064 |

|

|

$ |

57,524 |

|

|

CAD per share |

|

$ |

0.28 |

|

|

$ |

0.26 |

|

|

$ |

1.11 |

|

|

$ |

0.71 |

|

|

CAD per share, without real estate gains |

|

$ |

0.19 |

|

|

$ |

0.26 |

|

|

$ |

0.78 |

|

|

$ |

0.71 |

|

|

Weighted-average shares outstanding |

|

|

90,642,318 |

|

|

|

81,970,075 |

|

|

|

85,524,073 |

|

|

|

81,328,129 |

|

14

STATEMENT OF OPERATIONS, FFO & CAD

CONSOLIDATED – by quarter

|

($'s in 000's, except per share amounts) |

|

For the Three-Months Ended |

|

|||||||||||||||||

|

|

|

December 31, 2015 |

|

|

September 30, 2015 |

|

|

June 30, 2015 |

|

|

March 31, 2015 |

|

|

December 31, 2014 |

|

|||||

|

Revenue: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest margin |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment interest income |

|

$ |

26,609 |

|

|

$ |

24,468 |

|

|

$ |

24,107 |

|

|

$ |

23,248 |

|

|

$ |

30,537 |

|

|

Investment interest expense |

|

|

(6,733 |

) |

|

|

(8,021 |

) |

|

|

(7,582 |

) |

|

|

(6,914 |

) |

|

|

(7,968 |

) |

|

Net interest margin |

|

|

19,876 |

|

|

|

16,447 |

|

|

|

16,525 |

|

|

|

16,334 |

|

|

|

22,569 |

|

|

Property income |

|

|

69,464 |

|

|

|

55,459 |

|

|

|

55,534 |

|

|

|

53,274 |

|

|

|

46,096 |

|

|

Fee and other income |

|

|

5,004 |

|

|

|

3,056 |

|

|

|

7,415 |

|

|

|

5,594 |

|

|

|

5,167 |

|

|

Total revenue |

|

|

94,344 |

|

|

|

74,962 |

|

|

|

79,474 |

|

|

|

75,202 |

|

|

|

73,832 |

|

|

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense |

|

|

25,408 |

|

|

|

19,574 |

|

|

|

19,673 |

|

|

|

19,683 |

|

|

|

16,635 |

|

|

Real estate operating expenses |

|

|

31,476 |

|

|

|

25,832 |

|

|

|

26,416 |

|

|

|

25,277 |

|

|

|

22,948 |

|

|

Compensation expenses |

|

|

8,416 |

|

|

|

7,137 |

|

|

|

6,568 |

|

|

|

6,108 |

|

|

|

5,050 |

|

|

General and administrative expenses |

|

|

5,825 |

|

|

|

4,489 |

|

|

|

5,065 |

|

|

|

5,400 |

|

|

|

4,414 |

|

|

Acquisition and integration expenses |

|

|

1,684 |

|

|

|

12,901 |

|

|

|

985 |

|

|

|

957 |

|

|

|

950 |

|

|

Provision for loan losses |

|

|

2,450 |

|

|

|

1,850 |

|

|

|

2,000 |

|

|

|

2,000 |

|

|

|

2,000 |

|

|

Depreciation and amortization expense |

|

|

22,583 |

|

|

|

15,254 |

|

|

|

17,007 |

|

|

|

19,024 |

|

|

|

18,065 |

|

|

Total expenses |

|

|

97,842 |

|

|

|

87,037 |

|

|

|

77,714 |

|

|

|

78,449 |

|

|

|

70,062 |

|

|

Operating Income |

|

|

(3,498 |

) |

|

|

(12,075 |

) |

|

|

1,760 |

|

|

|

(3,247 |

) |

|

|

3,770 |

|

|

Other income (expense) |

|

|

7 |

|

|

|

(380 |

) |

|

|

(241 |

) |

|

|

(395 |

) |

|

|

51 |

|

|

Gains (loss) on assets |

|

|

19,094 |

|

|

|

7,430 |

|

|

|

17,281 |

|

|

|

— |

|

|

|

(20 |

) |

|

Asset impairment |

|

|

(929 |

) |

|

|

(7,250 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

TSRE financing extinguishment and employee separation expenses |

|

|

— |

|

|

|

(27,508 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Gains (losses) on IRT merger with TSRE |

|

|

592 |

|

|

|

64,012 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Gain (loss) on deconsolidation of VIEs |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(215,804 |

) |

|

Net gain from collateral management sale |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,549 |

|

|

Change in fair value of financial instruments |

|

|

(1,828 |

) |

|

|

620 |

|

|

|

8,356 |

|

|

|

4,490 |

|

|

|

(39,319 |

) |

|

Income (loss) before taxes |

|

|

13,438 |

|

|

|

24,849 |

|

|

|

27,156 |

|

|

|

848 |

|

|

|

(246,773 |

) |

|

Income tax benefit (provision) |

|

|

(1,478 |

) |

|

|

(23 |

) |

|

|

(715 |

) |

|

|

(582 |

) |

|

|

(307 |

) |

|