Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-14760

RAIT FINANCIAL TRUST

(Exact name of registrant as specified in its charter)

| Maryland | 23-2919819 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 2929 Arch Street, 17th Floor Philadelphia, PA |

19104 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (215) 243-9000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Shares of Beneficial Interest | New York Stock Exchange | |

| 7.75% Series A Cumulative Redeemable | ||

| Preferred Shares of Beneficial Interest | New York Stock Exchange | |

| 8.375% Series B Cumulative Redeemable | ||

| Preferred Shares of Beneficial Interest | New York Stock Exchange | |

| 8.875% Series C Cumulative Redeemable | ||

| Preferred Shares of Beneficial Interest | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | þ | |||||

| Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the common shares of the registrant held by non-affiliates of the registrant, based upon the closing price of such shares on June 30, 2009 of $1.37, was approximately $84,000,000.

As of February 26, 2010, 74,423,075 common shares of beneficial interest, par value $0.01 per share, of the registrant were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for registrant’s 2010 Annual Meeting of Shareholders are incorporated by reference in Part III of this Form 10-K.

TABLE OF CONTENTS

| Page No. | ||||

| 1 | ||||

| 2 | ||||

| Item 1. |

2 | |||

| Item 1A. |

11 | |||

| Item 1B. |

39 | |||

| Item 2. |

39 | |||

| Item 3. |

39 | |||

| Item 4. |

40 | |||

| 41 | ||||

| Item 5. |

Market for Our Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

41 | ||

| Item 6. |

44 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

45 | ||

| Item 7A. |

75 | |||

| Item 8. |

77 | |||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

144 | ||

| Item 9A. |

144 | |||

| Item 9B. |

144 | |||

| 145 | ||||

| Item 10. |

145 | |||

| Item 11. |

145 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

145 | ||

| Item 13. |

Certain Relationships and Related Transactions and Trustee Independence |

145 | ||

| Item 14. |

145 | |||

| 146 | ||||

| Item 15. |

146 | |||

| 147 | ||||

| 148 | ||||

The Securities and Exchange Commission, or SEC, encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This report contains or incorporates by reference such “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act.

Words such as “anticipates,” “estimates,” “expects,” “projects,” “intends,” “plans,” “believes” and words and terms of similar substance used in connection with any discussion of future operating or financial performance identify forward-looking statements. Unless we have indicated otherwise, or the context otherwise requires, references in this report to “RAIT,” “we,” “us,” and “our” or similar terms, are to RAIT Financial Trust and its subsidiaries.

We claim the protection of the safe harbor for forward-looking statements provided in the Private Securities Litigation Reform Act of 1995. These statements may be made directly in this report and they may also be incorporated by reference in this report to other documents filed with the SEC, and include, but are not limited to, statements about future financial and operating results and performance, statements about our plans, objectives, expectations and intentions with respect to future operations, products and services, and other statements that are not historical facts. These forward-looking statements are based upon the current beliefs and expectations of our management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are difficult to predict and generally beyond our control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. Actual results may differ materially from the anticipated results discussed in these forward-looking statements.

The risk factors discussed and identified in item 1A of this report and in other of our public filings with the SEC, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed in the forward-looking statements. We caution you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable law or regulation, we undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this filing or to reflect the occurrence of unanticipated events.

1

| Item 1. | Business |

Our Company

RAIT Financial Trust uses its vertically integrated platform to invest in, manage and service real estate-related assets with a focus on commercial real estate. We offer a comprehensive set of debt financing options to the commercial real estate industry along with fixed income trading and advisory services. We also own and manage a portfolio of commercial real estate properties and manage real estate-related assets for third parties. We are a self-managed and self-advised Maryland real estate investment trust, or REIT, formed in August 1997, that commenced operations in January 1998.

Our investments consist primarily of the following asset classes:

| • | commercial mortgages, mezzanine loans, other loans and preferred equity interests; |

| • | investments in real estate or in entities that own commercial real estate; and |

| • | investments in debt securities issued by real estate companies, including trust preferred securities, or TruPS, and subordinated debentures, mortgage-backed securities, including commercial mortgage-backed securities, or CMBS, unsecured REIT notes and other real estate-related debt. |

Our revenue is generated primarily from:

| • | interest income from our investments, net of any financing costs, or net interest margin; |

| • | rental income from our direct investments in real estate assets; and |

| • | fee income generated from: |

| • | originating, servicing and managing assets, |

| • | fixed income trading services, |

| • | advisory services, and |

| • | other brokerage-related services. |

2009 was part of an ongoing transition period for RAIT as we continue to adapt our business to current economic conditions. We engaged in a series of transactions intended to focus RAIT on opportunities in financing and owning commercial real estate by removing non-core assets from our balance sheet. These transactions included selling our equity in securitizations holding our residential mortgage portfolio and a substantial amount of our investments in debt securities issued by real estate companies. For further discussion of these transactions, see Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Business Strategy

Our objective is to provide our shareholders with total returns over time while managing the risks associated with our investment strategy. The core components of our business strategy are described in more detail below.

Provide commercial real estate financing. We provide a comprehensive set of debt financing options to the commercial real estate industry, including commercial mortgages, mezzanine loans, other loans and preferred equity interests. We have primarily financed this portfolio through securitizations, in which we have a retained interests, or through lines of credit.

2

Own commercial real estate. Our ownership of commercial real estate has grown recently as we have restructured loans in response to credit events to take control of properties where we believe we can continue to generate or enhance our risk-adjusted returns. To support our increased ownership of properties and to further vertically integrate our platform, we expanded our property management capabilities by purchasing a majority interest in Jupiter Communities, LLC, or Jupiter Communities, in May 2009. Jupiter Communities is an established property management firm specializing in managing multifamily commercial real estate properties. We have financed this portfolio through secured mortgages held by either third party lenders or our commercial real estate securitizations. See “Financing Strategy” below.

Manage our portfolio of debt securities issued by real estate companies. Included in our assets are debt securities issued by real estate companies. As noted above, we have been reducing the amount of these investments reflected on our balance sheet to focus on commercial real estate loans and properties. We have financed this portfolio through securitizations in which we have retained interests in the subordinated notes and equity. Our retained interests in these securitizations no longer generate cash flow for us; however, we continue to act as collateral manager and receive collateral management fees. See “Generate Fee Income” and “Financing Strategy” below.

Generate fee income. We manage a portfolio of real estate related assets. As of December 31, 2009, we had $10.1 billion of assets under management. Assets under management are comprised of our consolidated assets and assets we manage but do not consolidate. At December 31, 2009, we served as the collateral manager on thirteen securitizations that are collateralized by U.S. commercial real estate investments, TruPS and European real estate investments. As collateral manager, we seek to maintain and enhance the performance of the investments collateralizing, and the cash flows of, these securitizations. We also service our U.S. commercial real estate investments. We have been added to Standard & Poor’s select servicer list as a commercial mortgage primary servicer. We generate fee income from our asset management efforts, primarily from serving as collateral manager. During the years ended December 31, 2009, 2008 and 2007, we received asset management fee income of $16.1 million, $23.2 million and $26.1 million, respectively, of which we eliminated $7.0 million, $12.2 million and $19.1 million, respectively, upon consolidation of securitizations in our consolidated financial statements.

In 2009, we expanded our fixed income trading services primarily in riskless principal transactions and we initiated an advisory services platform to investors in commercial real estate assets.

Financing Strategy. We have financed a substantial portion of our portfolio investments through borrowing and securitization strategies that seek to match the payment terms, interest rate and maturity dates of our financings with the payment terms, interest rate and maturity dates of those investments. We seek to mitigate interest rate risk through derivative instruments. We own junior debt tranches and equity of a number of the securitizations which we structured to finance a substantial portion of our investment portfolio.

We financed a majority of our commercial real estate loan portfolio through two non-recourse loan securitizations which aggregate $1.85 billion of loan capacity. These financing structures have built-in revolver features that permit us to replace maturing loan collateral with new loans up through the fifth year anniversary of each financing in 2011 and 2012. We retained all of the most junior debt tranche (BB rated) and all of the preferred equity issued by these securitizations.

We finance our acquisitions of real estate through a combination of secured mortgage financing provided by third party financial institutions and existing financing provided by our two CRE loan securitizations. During 2009, we acquired $416.7 million of direct real estate investments upon conversion of $515.5 million of commercial real estate loans, retaining the existing financing provided by our two CRE loan securitizations.

We financed most of our debt securities portfolio in a series of non-recourse collateralized debt obligations, or CDOs, which provided long-dated, interest-only, match funded financing to the TruPS and subordinated

3

debenture investments. As of December 31, 2009, we retained a controlling interest in two securitizations—Taberna Preferred Funding VIII, Ltd., or Taberna VIII and Taberna Preferred Funding IX, Ltd., or Taberna IX, which are consolidated entities. All of the debt securities collateral assets and the related non-recourse CDO financing obligations are presented at fair value in our reported results. During 2009, due to the non-recourse nature of these entities and the recent credit performance of the underlying collateral, we received only our senior collateral management fees from these two CDOs.

See Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations-Securitization Summary” for further discussion of our securitizations.

Our Investment Portfolio

Our consolidated investment portfolio is currently comprised of the following asset classes:

Commercial mortgages, mezzanine loans, other loans and preferred equity interests. We have originated senior long-term mortgage loans, short-term bridge loans, subordinated, or “mezzanine,” financing and preferred equity interests. Our financing is usually “non-recourse.” Non-recourse financing means we look primarily to the assets securing the payment of the loan, subject to certain standard exceptions. We may also engage in recourse financing by requiring personal guarantees from controlling persons of our borrowers. We also acquire existing commercial real estate loans held by banks, other institutional lenders or third-party investors. Where possible, we seek to maintain direct lending relationships with borrowers, as opposed to investing in loans controlled by third party lenders.

The tables below describe certain characteristics of our commercial mortgages, mezzanine loans, other loans and preferred equity interests as of December 31, 2009 (dollars in thousands):

| Book Value | Weighted- Average Coupon |

Range of Maturities |

Number of Loans | |||||||

| Commercial mortgages |

$ | 825,044 | 6.9 | % | Mar. 2010 to Mar. 2016 | 55 | ||||

| Mezzanine loans |

421,805 | 9.8 | % | Mar. 2010 to Aug. 2021 | 129 | |||||

| Other loans |

123,889 | 5.2 | % | Apr. 2010 to Oct. 2016 | 9 | |||||

| Preferred equity interests |

98,584 | 10.9 | % | Mar. 2010 to Sep. 2021 | 25 | |||||

| Total |

$ | 1,469,322 | 7.9 | % | 218 | |||||

Due to current economic conditions referred to above, we currently have limited capacity to originate new investments. However, we expect to focus on this asset class when economic conditions improve.

4

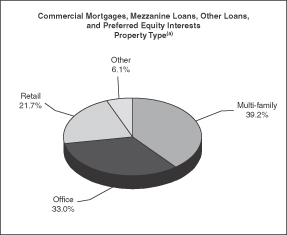

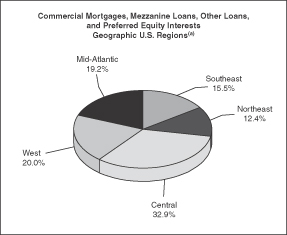

The charts below describe the property types and the geographic breakdown of our commercial mortgages, mezzanine loans, other loans, and preferred equity interests as of December 31, 2009:

|

|

| (a) | Based on book value. |

Investments in real estate. We generate a return on our real estate investments through rental income and other sources of income from the operations of the real estate underlying our investment. We also participate in any increase in the value of the real estate in addition to current income. We finance our acquisitions of real estate through a combination of secured mortgage financing provided by financial institutions and existing financing provided by our two CRE loan securitizations. During 2009, we acquired $416.7 million of real estate investments upon conversion of $515.5 million of commercial real estate loans, usually subject to retaining the existing financing provided by our two CRE loan securitizations.

The table below describes certain characteristics of our investments in real estate as of December 31, 2009 (dollars in thousands):

| Book Value | % of Total Portfolio |

Units / Square Feet / Acres |

Number of Properties | |||||||

| Multi-family real estate properties |

$ | 497,578 | 67.4 | % | 6,967 | 27 | ||||

| Office real estate properties |

178,750 | 24.2 | % | 1,324,368 | 6 | |||||

| Retail real estate properties |

35,437 | 4.8 | % | 1,095,452 | 3 | |||||

| Parcels of land |

26,470 | 3.6 | % | 7.3 | 3 | |||||

| Total |

$ | 738,235 | 100.0 | % | 39 | |||||

We expect this asset category to increase in size as we may find it desirable to protect or enhance our risk-adjusted returns by taking control of properties underlying our commercial real estate loans when restructuring or otherwise exercising our remedies regarding loans that become subject to increased credit risks.

5

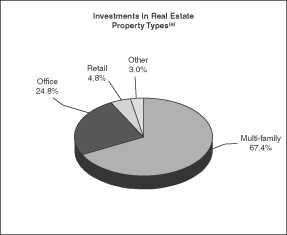

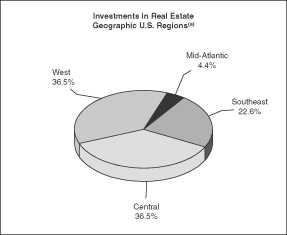

The charts below describe the property types and the geographic breakdown of our investments in real estate as of December 31, 2009:

|

|

| (a) | Based on book value. |

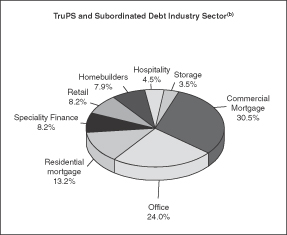

Investment in debt securities. We have provided REITs and real estate operating companies the ability to raise subordinated debt capital through TruPS and subordinated debentures. TruPS are long-term instruments, with maturities ranging from 5 to 30 years, which are priced based on short-term variable rates, such as the three-month London Inter-Bank Offered Rate, or LIBOR. TruPS are unsecured and generally contain minimal financial and operating covenants. We financed most of our debt securities portfolio in a series of non-recourse securitizations which provided long-dated, interest-only, match funded financing to the TruPS and subordinated debenture investments. As of December 31, 2009, we retained a controlling interest in two securitizations—Taberna VIII and Taberna IX, which are consolidated entities. All of the collateral assets for the debt securities and the related non-recourse CDO financing obligations are presented at fair value in our reported results. During 2009, due to the non-recourse nature of these entities and the recent credit performance of the underlying collateral, we received only our senior collateral management fees from these two CDOs.

The table below describes our investment in TruPS and subordinated debentures as included in our consolidated financial statements as of December 31, 2009 (dollars in thousands):

| Issuer Statistics | |||||||||||||||

| Industry Sector |

Estimated Fair Value |

% of Total |

Weighted- Average Coupon |

Weighted Average Ratio of Debt to Total Capitalization |

Weighted Average Interest Coverage Ratio |

||||||||||

| Commercial Mortgage |

$ | 165,625 | 30.5 | % | 3.7 | % | 79.1 | % | 0.9x | ||||||

| Office |

130,799 | 24.0 | % | 7.8 | % | 63.9 | % | 1.9x | |||||||

| Residential Mortgage |

71,635 | 13.2 | % | 2.5 | % | 99.2 | % | (1.4 | )x | ||||||

| Specialty Finance |

44,821 | 8.2 | % | 5.3 | % | 118.9 | % | 1.0x | |||||||

| Homebuilders |

43,198 | 7.9 | % | 7.8 | % | 4.1 | % | (0.2 | )x | ||||||

| Retail |

44,609 | 8.2 | % | 4.3 | % | 185.4 | % | 2.2x | |||||||

| Hospitality |

24,777 | 4.5 | % | 5.8 | % | 111.6 | % | (1.4 | )x | ||||||

| Storage |

19,291 | 3.5 | % | 8.0 | % | 62.4 | % | 3.6x | |||||||

| Total |

$ | 544,755 | 100.0 | % | 5.3 | % | 76.2 | % | 1.2x | ||||||

6

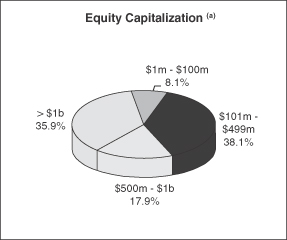

The chart below describes the equity capitalization of our investment in TruPS and subordinated debentures as included in our consolidated financial statements as of December 31, 2009:

|

|

| (a) | Based on the most recent information available to management as provided by our TruPS issuers or through public filings. |

| (b) | Based on estimated fair value. |

We have invested, and expect to continue to invest, in CMBS, unsecured REIT notes and other real estate-related debt securities.

Unsecured REIT notes are publicly traded debentures issued by large public reporting REITs and other real estate companies. These debentures generally pay interest semi-annually. These companies are generally rated investment grade by one or more nationally recognized rating agencies.

CMBS generally are multi-class debt or pass-through certificates secured or backed by single loans or pools of mortgage loans on commercial real estate properties. Our CMBS investments may include loans and securities that are rated investment grade by one or more nationally-recognized rating agencies, as well as both unrated and non-investment grade loans and securities.

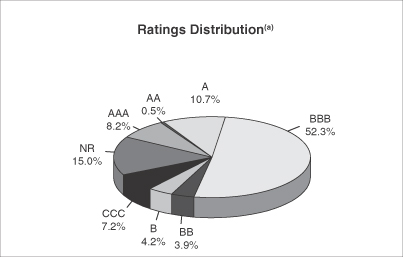

The table and the chart below describe certain characteristics of our real estate-related debt securities as of December 31, 2009 (dollars in thousands):

| Investment Description |

Estimated Fair Value |

Weighted- Average Coupon |

Weighted- Average Years to Maturity |

Book Value | |||||||

| Unsecured REIT note receivables |

$ | 65,393 | 6.6 | % | 7.8 | $ | 68,049 | ||||

| CMBS receivables |

58,894 | 6.0 | % | 34.3 | 158,368 | ||||||

| Other securities |

25,465 | 3.2 | % | 30.1 | 93,419 | ||||||

| Total |

$ | 149,752 | 5.1 | % | 27.9 | $ | 319,836 | ||||

7

| (a) | S&P Ratings as of December 31, 2009. |

Certain REIT and Investment Company Act Limits On Our Strategies

REIT Limits

We conduct our operations so as to qualify as a REIT. Our subsidiary, Taberna Realty Finance Trust, or Taberna, is also a REIT and we cause Taberna to conduct its operations to qualify as a REIT. For a discussion of the tax implications of our and Taberna’s REIT status to us and our shareholders, see “Material U.S. Federal Income Tax Considerations” contained in Exhibit 99.1 to this Annual Report on Form 10-K. To qualify as a REIT, we and Taberna must continually satisfy various tests regarding sources of income, nature and diversification of assets, amounts distributed to shareholders and the ownership of common shares. In order to satisfy these tests, we and Taberna may be required to forgo investments that might otherwise be made. Accordingly, compliance with the REIT requirements may hinder our or Taberna’s investment performance. These requirements include the following:

| • | At least 75% of each of our and Taberna’s total assets and 75% of gross income must be derived from qualifying real estate assets, whether or not such assets would otherwise represent our or Taberna’s best investment alternative. For example, since neither TruPS nor investments in the debt or equity of CDOs are qualifying real estate assets, to the extent that we have historically invested in such assets, or may do so in the future, Taberna (and we, to the extent that we invest in such assets) must hold substantial investments in qualifying real estate assets, including mortgage loans and CMBS, which may have lower yields than such investments. Also, at least 95% of each of our and Taberna’s gross income in each taxable year, excluding gross income from prohibited transactions, must be derived from some combination of income that qualifies under the 75% gross income test described above, as well as other dividends, interest, and gain from the sale or disposition of shares or securities, which need not have any relation to real property. |

| • | A REIT’s net income from prohibited transactions is subject to a 100% penalty tax. In general, prohibited transactions are sales or other dispositions of property, other than foreclosure property, but including any mortgage loans, held in inventory or primarily for sale to customers in the ordinary course of business. The prohibited transaction tax may apply to any sale of assets to a CDO and to any sale of CDO securities, and therefore may limit our and Taberna’s ability to sell assets to or equity in CDOs and other assets. |

| • | Overall, no more than 25% of the value of a REIT’s assets may consist of securities of one or more taxable REIT subsidiaries, or TRSs. Taberna Capital LLC, or Taberna Capital, RAIT Securities LLC, or RAIT Securities, Jupiter Communities, RAIT Securities (U.K.) Ltd., or RAIT Securities UK, RAIT Capital Ltd., Taberna |

8

| Funding LLC, or Taberna Funding, Taberna Equity Funding, Ltd., or Taberna Equity Funding, and Taberna’s non-U.S. corporate subsidiaries are TRSs. Taberna’s ability to invest in CDOs that are structured as TRSs and to grow or expand the fee-generating businesses of Taberna Capital and RAIT Securities, as well as the business of Taberna Funding, RAIT Securities UK, RAIT Capital Ltd. and future TRSs Taberna may form, will be limited by Taberna’s need to meet this 25% test, which may adversely affect distributions Taberna pays to us. |

| • | The REIT provisions of the Internal Revenue Code limit our and Taberna’s ability to hedge mortgage-backed securities, preferred securities and related borrowings. Except to the extent provided by the regulations promulgated by the U.S. Treasury Department, or the Treasury regulations, any income from a hedging transaction we or Taberna enter into in the normal course of business primarily to manage risk of interest rate or price changes or currency fluctuations with respect to borrowings made or to be made, or ordinary obligations incurred or to be incurred, to acquire or carry real estate assets, which is clearly identified as specified in the Treasury regulations before the close of the day on which it was acquired, originated, or entered into, including gain from the sale or disposition of such a transaction, will not constitute gross income for purposes of the 95% gross income test (and will generally constitute non-qualifying income for purposes of the 75% gross income test). To the extent that we or Taberna enter into other types of hedging transactions, the income from those transactions is likely to be treated as non- qualifying income for purposes of both of the gross income tests. As a result, we or Taberna might have to limit use of advantageous hedging techniques or implement those hedges through TRSs. This could increase the cost of our or Taberna’s hedging activities or expose it or us to greater risks associated with changes in interest rates than we or it would otherwise want to bear. |

There are other risks arising out of our and Taberna’s need to comply with REIT requirements. See Item 1A—“Risk Factors-Tax Risks” below.

Investment Company Act Limits

We seek to conduct our operations so that we are not required to register as an investment company. Under Section 3(a)(1) of the Investment Company Act, a company is not deemed to be an “investment company” if:

| • | it neither is, nor holds itself out as being, engaged primarily, nor proposes to engage primarily, in the business of investing, reinvesting or trading in securities; and |

| • | it neither is engaged nor proposes to engage in the business of investing, reinvesting, owning, holding or trading in securities and does not own or propose to acquire “investment securities” having a value exceeding 40% of the value of its total assets on an unconsolidated basis, which we refer to as the 40% test. “Investment securities” excludes U.S. government securities and securities of majority-owned subsidiaries that are not themselves investment companies and are not relying on the exception from the definition of investment company under Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act. |

We rely on the 40% test. Because we are a holding company that conducts our businesses through wholly-owned or majority-owned subsidiaries, the securities issued by our subsidiaries that are excepted from the definition of “investment company” under Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act, together with any other investment securities we may own, may not have a combined value in excess of 40% of the value of our total assets on an unconsolidated basis. In fact, based on the relative value of our investment in Taberna, on the one hand, and our investment in RAIT Partnership, on the other hand, we can comply with the 40% test only if Taberna satisfies the 40% test on which it relies (or another exemption other than Section 3(c)(1) or 3(c)(7)) and RAIT Partnership complies with Section 3(c)(5)(c) or 3(c)(6), the exemptions upon which it relies (or another exemption other than Section 3(c)(1) or 3(c)(7)). This requirement limits the types of businesses in which we may engage through our subsidiaries.

9

None of RAIT, RAIT Partnership or Taberna has received a no-action letter from the SEC regarding whether it complies with the Investment Company Act or how its investment or financing strategies fit within the exclusions from regulation under the Investment Company Act that it is using. To the extent that the SEC provides more specific or different guidance regarding, for example, the treatment of assets as qualifying real estate assets or real estate-related assets, we may be required to adjust these investment and financing strategies accordingly. See Item 1A—“Risk Factors- Other Regulatory and Legal Risks of Our Business- Loss of our Investment Company Act exemption would affect us adversely.”

Competition

We are subject to significant competition in all aspects of our business. Existing industry participants and potential new entrants compete with us for the available supply of investments suitable for origination or acquisition, as well as for debt and equity capital. We compete with many third parties engaged in real estate finance and investment activities, including other REITs, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, lenders, governmental bodies and other entities. Competition, particularly in our commercial mortgage and mezzanine loan business, may increase, and other companies and funds with investment objectives similar to ours may be organized in the future. Some of these competitors have, or in the future may have, substantially greater financial resources than we do and generally may be able to accept more risk. They may also enjoy significant competitive advantages that result from, among other things, a lower cost of capital and enhanced operating efficiencies. In addition, competition may lead us to pay a greater portion of the origination fees that we expect to collect in our future origination activities to third-party investment banks and brokers that introduce borrowers to us in order to continue to generate new business from these sources.

Employees

As of February 26, 2010, we had 329 employees and believe our relationships with our employees to be good. None of our employees is covered by a collective bargaining agreement.

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the SEC. The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The internet address of the SEC site is http://www.sec.gov. Our internet address is http://www.raitft.com. We make our SEC filings available free of charge on or through our internet website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. We are not incorporating by reference in this report any material from our website.

10

| Item 1A. | Risk Factors |

This section describes material risks affecting our business. In addition, in connection with the forward-looking statements that appear in this annual report, we urge you to review carefully not only the factors discussed below but also the cautionary statements referred to in “Forward-Looking Statements.”

Risks Related to Our Business

Global recessionary economic conditions and adverse developments in the credit markets have had, and we expect will continue to have, an adverse effect on our investments and our operating results, including causing significant reduction in the availability of financing to us and for refinancing to our borrowers, increases in payment defaults and other credit risks in our investments, decreases in the fair value of our assets and decreases in the cash flow we receive from our investments.

Global recessionary economic conditions and adverse developments in the credit markets have substantially reduced or eliminated the availability of financing for most real estate sectors in which we and the companies we finance operate. This has reduced, and may continue to reduce, the amount of capital we have available to make new investments, contributing to the reduction of our assets under management, and the reduction of income and fees derived from our investments. These conditions and developments have adversely affected many real estate sectors in which the companies we finance operate, resulting in increasing credit risk relating to, and payment defaults in, our investments. This has reduced, and may continue to reduce, the revenue and cash flow we receive from our investments and the fair value of our investments and has resulted in, and may continue to cause, material asset impairment of these investments. Our response to current economic conditions may require us to change our business strategy, including the types of investments we make, how we finance them and our dividend policies, from our historical approaches.

Our ability to generate operating cash flow and access capital has been, and may continue to be, adversely affected by the global recessionary economic conditions and adverse developments in the capital markets.

Our business requires a substantial amount of liquidity to fund investments, to pay expenses and to acquire and hold assets. As REITs, we must distribute at least 90% of REIT taxable income to our respective shareholders, determined without regard to the deduction for dividends paid and excluding net capital gain, which substantially limits our ability to accumulate cash from our operations. Developments in the capital markets have substantially reduced the debt capital and equity capital available to us and adversely affected our ability to execute successfully our business plan.

With respect to debt capital, we believe many of the types of financing arrangements we used historically will not be available for investments of the type we have originated historically for the foreseeable future, including repurchase agreements for short term financing and securitizations for long term financing of our investments. Our continued use of secured bank financing will depend on our ability to negotiate renewals of our current lines of credit as they mature and to obtain new secured bank financing on acceptable terms. We have historically issued debt securities to one or more institutional investors from time to time as market conditions permitted, particularly our TruPS and our convertible senior notes. We expect that our opportunities to issue additional debt will be limited for the foreseeable future.

With respect to equity capital, we believe the market for our common shares and preferred shares has contracted as the global recessionary economic conditions and adverse developments in the capital markets have developed from 2007. We may not be able to obtain the amounts of capital on the terms we seek through issuances of our equity securities.

We are seeking, and expect we will continue to seek, alternative financing arrangements in response to current market conditions, including joint venture and co-investment opportunities. We cannot assure you that we will be able to develop these financing sources on acceptable terms, or at all. We may need to identify capital in

11

smaller increments to attempt to match fund the investment to the financing source to the extent economically feasible. Our rate of originating new assets may decline under alternative financing arrangements which may result in lower fee income and cash flow for distribution and a reduction in our assets under management.

The failure to secure financing on acceptable terms or in sufficient amounts has reduced, and may continue to reduce, our taxable income by limiting our ability to originate loans and other investments and reducing our fee income and increasing our financing expense. A reduction in our net taxable income could impair our liquidity and our ability to pay distributions to our shareholders. We cannot assure you that any, or sufficient, funding or capital will be available to us in the future on terms that are acceptable to us.

The failure of most of our Taberna securitization financings to meet their performance tests, including over-collateralization requirements, has reduced, and may continue to reduce, our net income and cash flow generated by these securitizations, may trigger certain termination provisions in the related collateral management agreements under which we manage these securitizations and has caused an event of default under most of these securitizations and may cause an event of default under the remaining securitizations.

The terms of the securitizations we have structured generally provide that the principal amount of assets must exceed the principal balance of the related securities issued by them by a certain amount, commonly referred to as “over-collateralization.” The securitization terms provide that, if delinquencies and/or losses exceed specified levels based on the analysis by the rating agencies (or any financial guaranty insurer) of the characteristics of the assets collateralizing the securities issued in the securitization, the required level of over-collateralization may be increased or may be prevented from decreasing as would otherwise be permitted if losses or delinquencies did not exceed those levels. In addition, a failure by a securitization to satisfy an over-collateralization test typically results in accelerated distributions to the holders of the senior debt securities issued by the securitization entity. Our equity holdings and, when we acquire debt interests in securitizations, our debt interests, and our subordinated management fees, if any, are subordinate in right of payment to the other classes of debt securities issued by the securitization entity. Many of our securitizations have not passed some of their overcollateralization tests and have accelerated distributions to senior debt resulting in the cessation of distributions on the subordinated debt and equity we hold in these securitizations and our subordinated management fees from these securitizations. This has resulted in a substantial reduction in the cash flow we receive from these securitizations. Other tests (based on delinquency levels or other criteria) may restrict our ability to receive cash distributions from assets collateralizing the securities issued by the securitization entity. We cannot assure you that the performance tests will be satisfied.

In addition, collateral management agreements typically provide that if certain over-collateralization tests are failed, the collateral management agreement may be terminated by a vote of the security holders resulting in our loss of management fees from these securitizations. If the assets held by securitizations fail to perform as anticipated, our earnings may be adversely affected, and over-collateralization or other credit enhancement expenses associated with our securitization financings will increase.

The overcollateralization tests and other tests of those of our securitizations still making distributions on some or all of the subordinated debt and equity we hold in these securitizations and our subordinated management fees from these securitizations have been, and may continue to, deteriorate. If these securitizations fail to satisfy their performance tests, we may be adversely affected in a manner similar to the effects described above.

If any of our securitizations fail to meet overcollateralization tests relevant to the most senior debt issued and outstanding by the securitization, an event of default may occur under that securitization. If that occurs, our ability to manage the securitization may be terminated and our ability to attempt to cure any defaults in the securitization would be limited, which would increase the likelihood of a reduction or elimination of cash flow and returns to us in those securitizations for an indefinite time. Events of default have occurred under most of our securitizations and may occur under our remaining securitizations.

12

If our securitizations secured primarily by commercial real estate loans, RAIT CRE CDO I, Ltd., or RAIT I and RAIT Preferred Funding II, Ltd., or RAIT II, were to fail to meet their performance tests, including over-collateralization requirements, our net income and cash flow would be materially reduced.

We currently receive a substantial portion of our net income and cash flow from RAIT I and RAIT II through our consolidation of the commercial real estate loans collateralizing these securitizations, and through cash flow received through our retained interests in these securitizations and senior and subordinated management fees paid to us for managing these securitizations. If either or both of these securitizations were to fail to meet their respective overcollateralization or other tests, our net income and cash flow would be materially reduced.

We receive collateral management fees pursuant to collateral management agreements for services provided by our subsidiaries for acting as the collateral manager of securitizations sponsored by us. If a collateral management agreement is terminated or if the securities serving as collateral for a securitization are prepaid or go into default, the collateral management fees will be reduced or eliminated.

Our subsidiaries receive collateral management fees pursuant to collateral management agreements for acting as the collateral manager of securitizations sponsored by us. If all the notes issued by a securitization for which one of our subsidiaries acts as collateral manager are redeemed, or if the collateral management agreement is otherwise terminated, we will no longer receive collateral management fees from that subsidiary with respect to that securitization. In general, a collateral management agreement may be terminated both with and without cause at the direction of holders of a specified supermajority in principal amount of the notes issued by the securitization. Furthermore, such fees are based on the total amount of collateral held by the securitizations. If the securities serving as collateral for a securitization are prepaid or go into default, we will receive lower collateral management fees than expected or the collateral management fees may be eliminated.

Our investments in securitizations are exposed to greater uncertainty and risk of loss than investments in higher grade securities in these securitizations.

When we securitize assets such as commercial mortgage loans, mezzanine loans and TruPS, the various tranches of investment grade and non-investment grade debt obligations and equity securities have differing priorities and rights to the cash flows of the underlying assets being securitized. We structured our securitization transactions to enable us to place debt and equity securities with investors in the capital markets at various pricing levels based on the credit position created for each tranche of debt and equity securities. The higher rated debt tranches have priority over the lower rated debt securities and the equity securities issued by the particular securitization entity with respect to payments of interest and principal using the cash flows from the collateral assets. The relative cost of capital increases as each tranche of capital becomes further subordinated, as does the associated risk of loss if cash flows from the assets are insufficient to repay fully interest and principal or pay dividends.

Since we own in many cases the “BBB,” “BB,” “B” and unrated debt and equity classes of securitizations, we are in a “first loss” position because the rights of the securities that we hold are subordinate in right of payment and in liquidation to the rights of higher rated debt securities issued by the securitization entities. Accordingly, we have incurred and may in the future incur significant losses when investing in these securities. In the event of default, we may not be able to recover all of our respective investments in these securities. In addition, we may experience significant losses if the underlying portfolio has been overvalued or if the values subsequently decline and, as a result, less collateral is available to satisfy interest, principal and dividend payments due on the related securities. The prices of lower credit quality securities are generally less sensitive to interest rate changes than higher rated investments, but are more sensitive to economic downturns or developments specific to a particular issuer. An economic downturn, for example, could cause a decline in the price of lower credit quality securities because the ability of obligors on the underlying assets to make principal, interest and dividend payments may be impaired. In such an event, existing credit support in the securitization

13

structure may be insufficient to protect us against loss of our investments in these securities. A number of the securitizations in which we have invested have suffered events of default or other events resulting in the termination for the foreseeable future of any distributions on the subordinated securities we hold.

Adverse market trends relating to the loans and real estate securities collateralizing our securitizations have reduced, and are expected to continue to reduce, the value of our retained interests in these securitizations.

The securitizations we sponsored where we retained debt or equity issued by the securitization entity have been backed by mortgage loans, mezzanine loans, TruPS, other senior and subordinated real estate company securities, other preferred securities, CMBS or other real estate-related securities. Adverse market trends since then have reduced, and we expect them to continue to reduce, the value of these types of assets and the value of our interests in securitizations.

Representations and warranties made by us in loan sales and securitizations may subject us to liability that could result in loan losses and could harm our operating results and, therefore distributions we make to our shareholders.

In connection with securitizations, we make representations and warranties regarding the assets transferred into securitization trusts. The trustee in the securitizations has recourse to us with respect to the breach of these representations and warranties. While we generally have recourse to loan originators for any such breaches, there can be no assurance that the originators will be able to honor their obligations. We generally attempt to limit the potential remedies of the trustee to the potential remedies we have against the originators from whom we acquired the assets. However, in some cases, the remedies available to the trustee may be broader than those available to us against the originators of the assets and, in the event the trustee enforces its remedies against us, we may not always be able to enforce whatever remedies are available to us against the originators of the loans. Furthermore, if we discover, prior to the securitization of an asset, that there is any fraud or misrepresentation with respect to it and the originator fails to repurchase the asset, then we may not be able to sell the asset or may have to sell it at a discount.

Our financing arrangements contain covenants that restrict our operations, and any default under these arrangements would inhibit our ability to grow our business, increase revenue and pay distributions to our shareholders.

Our financing arrangements contain restrictions, covenants and events of default. Failure to meet or satisfy any of these covenants could result in an event of default under these agreements. Any event of default may materially adversely affect us. These agreements may contain cross- default provisions so that an event of default under any agreement will trigger an event of default under other agreements, giving our lenders the right to declare all amounts outstanding under their particular credit agreement to be immediately due and payable, and enforce their rights by foreclosing on or otherwise liquidating collateral pledged under these agreements.

These restrictions may interfere with our ability to obtain financing or to engage in other business activities. Furthermore, our default under any of our financing arrangements could have a material adverse effect on our business, financial condition, liquidity and results of operations and our ability to make distributions to our shareholders.

Our reliance on significant amounts of debt to finance investments may subject us to an increased risk of loss, reduce our return on investments, reduce our ability to pay distributions to our shareholders and possibly result in the foreclosure of any assets subject to secured financing.

We have historically incurred a significant amount of debt to finance operations, which could compound losses and reduce our ability to pay distributions to our shareholders. Changes in market conditions have caused, and may continue to cause, availability of financing to decrease and the cost of financing to increase relative to

14

the income that we can derive from investments, which has impaired, and may continue to impair, the returns we can achieve and our ability to pay distributions to our shareholders. Our debt service payments reduce the net income available for distributions to our shareholders. Most of our assets are pledged as collateral for borrowings. In addition, the assets of the securitizations that we consolidate collateralize the debt obligations of the securitizations and are not available to satisfy other creditors. To the extent that we fail to meet debt service obligations, we risk the loss of some or all of our respective assets to foreclosure or sale to satisfy these debt obligations. Currently, our declaration of trust and bylaws do not impose any limitations on the extent to which we may leverage our respective assets.

We are subject to the risks normally associated with debt financing, including the risk that our cash flows will be insufficient to meet required principal and interest payments and the risk that we will be unable to refinance our existing indebtedness when it becomes due, or that the terms of such refinancing will not be as favorable as the terms of our existing indebtedness. Included in our debt instruments are provisions providing for the lump sum payment of significant amounts of principal, whether upon maturity, upon the exercise of any applicable put rights or otherwise, which we refer to as balloon payments. Most of our debt provides for balloon payments that are payable at maturity. If collateral underlying our secured credit facilities defaults or otherwise fails to meet specified conditions, we may have to repay that facility to the extent it was secured by that collateral. Holders of our senior convertible notes may require us to repurchase all or a portion of the senior convertible notes at a purchase price equal to the principal amount plus accrued and unpaid interest (including additional interest), if any, on the senior notes on April 15, 2012 and successive put dates. Our ability to make these payments will depend upon our ability to refinance the related debt, and/or sell assets or any related collateral. Our ability to accomplish these goals will be affected by various factors existing at the relevant time, such as the state of the national and regional economies, local real estate conditions, available interest rate levels, the lease terms for and equity in any related collateral, our financial condition and the operating history of the collateral. If we are unable to pay, refinance or extend any of our debt, this could have a material adverse effect on our financial condition.

Quarterly results may fluctuate and may not be indicative of future quarterly performance.

Our quarterly operating results could fluctuate; therefore, you should not rely on past quarterly results to be indicative of our performance in future quarters. Factors that could cause quarterly operating results to fluctuate include, among others, variations in our investment origination volume, variations in the timing of repayments of debt financing, variations in the amount of time between our receipt of the proceeds of a securities offering and our investment of those proceeds in loans or real estate, market conditions that result in increased cost of funds, the degree to which we encounter competition in our markets, general economic conditions and other factors referred to elsewhere in this section.

We may seek to acquire, redeem, restructure, refinance or otherwise enter into transactions to satisfy our debt which may include issuances of our debt and/or equity securities, sales or exchanges of our assets or other methods.

We are aware that our convertible senior notes, CDO notes payable and other indebtedness are currently trading at substantial discounts to their respective face amounts. In order to reduce future cash interest payments, as well as future principal amounts due at maturity or upon redemption, or to otherwise benefit RAIT, we may, from time to time, purchase such convertible senior notes, CDO notes payable or other indebtedness for cash, in exchange for our equity securities, or for a combination of cash and equity securities, in each case in open market purchases, privately negotiated transactions, exchange offers and consent solicitations or otherwise. We will evaluate any such transactions in light of then-existing market conditions, contractual restrictions and other factors, taking into account our current liquidity and prospects for future access to capital. The amounts involved in any such transactions, individually or in the aggregate, may be material.

15

The lack of liquidity in our investments may make it difficult for us to sell such investments if the need arises and any sales may be at a loss to us.

We make and hold investments in securities issued by private companies and other illiquid investments. A portion of these investments may be subject to legal and other restrictions on resale or will otherwise be less liquid than publicly traded securities. The illiquidity of these investments may make it difficult for us to sell such investments if the need arises and may impair the value of these investments. Any sales of investments we make may result in our recognizing a loss on the sale.

We operate in a highly competitive market which may harm our business, financial condition, liquidity and results of operations.

Historically, we have been subject to significant competition in all of our business lines. We compete with many third parties engaged in finance and real estate investment activities, including other REITs, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms and broker-dealers, property managers, investment advisors, lenders, governmental bodies and other entities. Some of these competitors have, or in the future may have, substantially greater financial resources than we do and generally may be able to accept more risk. As such, they have the ability to make larger loans and to reduce the risk of loss from any one loan by having a more diversified loan portfolio. They may also enjoy significant competitive advantages that result from, among other things, a lower cost of, and greater access to, capital and enhanced operating efficiencies. An increase in the general availability of funds to lenders, or a decrease in the amount of borrowing activity, may increase competition for making loans and may reduce obtainable yields or increase the credit risk inherent in the available loans.

In addition, competition may lead us to pay a greater portion of the origination fees that we expect to collect in our future origination activities to third-party investment banks and brokers that introduce their clients to us in order to continue to generate new business from these sources or otherwise may reduce the fees we are able to earn in connection with our business lines.

Competition may limit the number of suitable investment opportunities offered to us. It may also result in higher prices, lower yields and a narrower spread of yields over our borrowing costs, making it more difficult for us to acquire new investments on attractive terms and reducing the fee income we realize from the origination, structuring and management of securitizations. It may also make it more difficult to obtain appreciation interests and increase the price, and thus reduce potential yields, on discounted loans we acquire.

Loss of our management team or the ability to attract and retain key employees could harm our business.

The real estate finance business is very labor-intensive. We depend on our management team to manage our investments and attract customers for financing by, among other things, developing relationships with issuers, financial institutions and others. The market for skilled personnel is highly competitive and has historically experienced a high rate of turnover. Due to the nature of our business, we compete for qualified personnel not only with companies in our business, but also in other sectors of the financial services industry. Competition for qualified personnel may lead to increased hiring and retention costs. We cannot guarantee that we will be able to attract or retain qualified personnel at reasonable costs or at all. If we are unable to attract or retain a sufficient number of skilled personnel at manageable costs, it could impair our ability to manage our investments and execute our investment strategies successfully, thereby reducing our earnings.

Our subsidiary Taberna Capital Management, LLC, or TCM, is named as a defendant in a lawsuit and the adverse resolution of this matter could have a material adverse effect on our financial condition and results of operations.

RAIT subsidiary TCM is named as one of eighteen defendants in a lawsuit filed by Riverside National Bank of Florida titled Riverside National Bank of Florida v. Taberna Capital Management, LLC, Trapeza Capital

16

Management, LLC, Cohen & Company Financial Management, LLC f/k/a Cohen Bros. Financial Management LLC, FTN Financial Capital Markets, Keefe, Bruyette & Woods, Inc., Merrill Lynch, Pierce, Fenner & Smith, Inc., Bank of America Corporation, as successor in interest to Merrill Lynch & Co., JP Morgan Chase, Inc, JP Morgan Securities, Citigroup Global Markets, Credit Suisse (USA) LLC, ABN AMRO, Cohen & Company, Morgan Keegan & Co., Inc., SunTrust Robinson Humphrey, Inc., The McGraw-Hill Companies, Inc., Moody’s Investors Services, Inc. and Fitch Ratings, Ltd. The plaintiff’s complaint asserts claims in connection with Riverside’s purchase of certain CDO securities, including securities from the Taberna Preferred Funding II, IV, and V CDOs. An adverse resolution of the litigation could have a material adverse effect on our financial condition and results of operations. For further information, see “Legal Proceedings.”

Our board of trustees may change our policies without shareholder consent.

Our board of trustees determines our policies and, in particular, our investment policies. Our board of trustees may amend our policies or approve transactions that deviate from these policies without a vote of or notice to our shareholders. Policy changes could adversely affect the market price of our shares and our ability to make distributions. Our board of trustees cannot take any action to disqualify us as a REIT or to otherwise revoke our election to be taxed as a REIT without the approval of a majority of our outstanding voting shares.

Our organizational documents do not limit our ability to enter into new lines of businesses, and we may enter into new businesses, make future strategic investments or acquisitions or enter into joint ventures, each of which may result in additional risks and uncertainties in our business.

Our organizational documents do not limit us to our current business lines. Accordingly, we may pursue growth through strategic investments, acquisitions or joint ventures, which may include entering into new lines of business. In addition, we expect opportunities will arise to acquire other companies, including REITs, managers of investment products or originators of real estate debt. To the extent we make strategic investments or acquisitions, enter into joint ventures, or enter into a new line of business, we will face numerous risks and uncertainties, including risks associated with:

| • | the required investment of capital and other resources, |

| • | the possibility that we have insufficient expertise to engage in such activities profitably or without incurring inappropriate amounts of risk, and |

| • | combining or integrating operational and management systems and controls and |

| • | compliance with applicable regulatory requirements including those required under the Internal Revenue Code and the Investment Company Act. |

Entry into certain lines of business may subject us to new laws and regulations with which we are not familiar, or from which we are currently exempt, and may lead to increased litigation and regulatory risk. If a new business generates insufficient revenue or if we are unable to efficiently manage our expanded operations, our results of operations will be adversely affected. In the case of joint ventures, we are subject to additional risks and uncertainties in that we may be dependent upon, and subject to liability, losses or reputation damage relating to, systems, controls and personnel that are not under our control.

We engage in transactions with related parties and our policies and procedures regarding these transactions may be insufficient to address any conflicts of interest that may arise.

Under our code of business conduct, we have established procedures regarding the review, approval and ratification of transactions which may give rise to a conflict of interest between us and any employee, officer, trustee, their immediate family members, other businesses under their control and other related persons. In the ordinary course of our business operations, we have ongoing relationships and have engaged in transactions with several related entities. These procedures may not be sufficient to address any conflicts of interest that may arise.

17

Risks Related to Our Investments

Payment defaults and other credit risks in our investment portfolio have arisen, and may continue to increase, which has caused, and may continue to cause, adverse effects on our cash flow, net income and ability to make distributions.

Global recessionary economic conditions and adverse developments in the credit markets have led to business contraction, liquidity issues and other problems for many of the companies we finance. As a result, payment defaults and other credit risks in our investment portfolio have increased, and may continue to increase, which has caused, and may continue to cause, adverse effects on our cash flow, net income and ability to make distributions.

Our portfolio of TruPS has been adversely affected by, and may continue to be adversely affected by, adverse economic developments affecting the business sectors in which our borrowers operate, including homebuilders, residential mortgage providers, commercial mortgage providers, office, specialty finance, retail, hospitality and storage resulting in a substantial reduction in their fair value which adversely affects our financial performance and a substantial decrease in the cash flow we receive from the securitizations holding TruPS. We cannot assure you that the fair value we reflect for any asset or liability in any particular reporting period will not change adversely in a subsequent reporting period.

We have increased, and may continue to increase, our loan loss reserves against our portfolios of commercial real estate investments due to general business and economic conditions and increased credit and liquidity risks which have had, and may continue to have, an adverse effect on our financial performance. Our portfolio of commercial real estate investments has been adversely affected by, and may continue to be adversely affected by, adverse economic developments affecting the business sectors in which our borrowers operate, including multi-family, office, and retail, reductions in the value of commercial real estate generally and the reduced availability of refinancing for commercial real estate investments as they mature. We cannot assure you that the loan loss reserves we adopt in any particular reporting period will be sufficient or will not increase in a subsequent reporting period.

If we are unable to improve the performance of commercial real estate properties we take control of in connection with restructurings, workouts and foreclosures of investments, our financial performance may be adversely affected.

We have taken control of an increasing number of the properties underlying our commercial real estate investments in connection with restructurings, workouts and foreclosures of these investments. If we are unable to improve the performance of these properties from their performance under their prior owners, our financial performance may be adversely affected. Any properties we consolidate may be required to be reflected at lower values on our financial statements.

We may not realize gains or income from investments and have realized, and may continue to realize, losses from some of our investments.

We seek to generate both current income and capital appreciation. However, our investments may not appreciate in value and, in fact, a substantial portion of our investments have declined, and may continue to decline, in value. In addition, some of the financings that we originated and the loans and securities in which we invest have, and may continue to, default on interest and/or principal payments. Accordingly, we may not be able to realize gains or income from investments and may realize losses. Any gains that we do realize may not be sufficient to offset any other losses we experience. Any income that we realize may not be sufficient to offset our respective expenses.

18

Longer term, subordinate and non-traditional loans and our consolidated real estate may be illiquid.

Our commercial real estate loans and our consolidated real estate are relatively illiquid investments and we may be unable to vary our portfolio promptly in response to changing economic, financial and investment conditions or dispose of these assets quickly or at all in the event we need additional liquidity.

Our subordinated real estate investments such as mezzanine loans and preferred equity interests in entities owning real estate involve increased risk of loss.

We invest in mezzanine loans and other forms of subordinated financing, such as investments consisting of preferred equity interests in entities owning real estate. Because of their subordinate position, these subordinated investments carry a greater credit risk than senior lien financing, including a substantially greater risk of non-payment. If a borrower defaults on our subordinated investment or on debt senior to us, our subordinated investment will be satisfied only after the senior debt is paid off, which may result in our being unable to recover the full amount, or any, of our investment. A decline in the real estate market could adversely affect the value of the property so that the aggregate outstanding balances of senior liens may exceed the value of the underlying property.

Where debt senior to our investment exists, the presence of inter-creditor arrangements may limit our ability to amend our loan documents, assign our loans, accept prepayments, exercise our remedies (through “standstill” periods) and control decisions made in bankruptcy proceedings relating to borrowers. Bankruptcy and borrower litigation can significantly increase the time needed for us to acquire underlying collateral in the event of a default, during which time the collateral may decline in value. In addition, there are significant costs and delays associated with the foreclosure process. In the event of a default on a senior loan, we may elect to make payments, if we have the right to do so, in order to prevent foreclosure on the senior loans. When we originate or acquire a subordinated investment, we may not have the right to service senior loans. The servicers of the senior loans are responsible to the holders of those loans, whose interests will likely not coincide with ours, particularly in the event of a default. Accordingly, the senior loans may not be serviced in a manner advantageous to us. It is also possible that, in some cases, a “due on sale” clause included in a senior mortgage, which accelerates the amount due under the senior mortgage in case of the sale of the property, may apply to the sale of the property if we foreclose, increasing our risk of loss.

We have loans that are not collateralized by recorded or perfected liens on the real estate underlying our loans. Some of the loans not collateralized by liens are secured instead by deeds-in-lieu of foreclosure, also known as “pocket deeds.” A deed-in-lieu of foreclosure is a deed executed in blank that the holder is entitled to record immediately upon a default in the loan. Loans that are not collateralized by recorded or perfected liens are subordinate not only to existing liens encumbering the underlying property, but also to future judgments or other liens that may arise as well as to the claims of general creditors of the borrower. Moreover, filing a deed-in-lieu of foreclosure with respect to these loans will usually constitute an event of default under any related senior debt. Any such default would require us to assume or pay off the senior debt in order to protect our investment. Furthermore, in a borrower’s bankruptcy, we will have materially fewer rights than secured creditors and, if our loan is secured by equity interests in the borrower, fewer rights than the borrower’s general creditors. Our rights also will be subordinate to the lien-like rights of the bankruptcy trustee. Moreover, enforcement of our loans against the underlying properties will involve a longer, more complex, and likely, more expensive legal process than enforcement of a mortgage loan. In addition, we may lose lien priority in many jurisdictions, to persons who supply labor and materials to a property. For these and other reasons, the total amount that we may recover from one of our investments may be less than the total amount of that investment or our cost of an acquisition of an investment.

Acquisitions of loans may involve increased risk of loss.

When we acquire existing loans, they are subject to general risks described in this section. When we acquire loans at a discount from both the outstanding balances of the loans and the appraised value of the properties underlying the loans; the loans typically are in default under the original loan terms or other requirements and are

19

subject to forbearance agreements. A forbearance agreement typically requires a borrower to pay to the lender all revenue from a property after payment of the property’s operating expenses in return for the lender’s agreement to withhold exercising its rights under the loan documents. Acquiring loans at a discount involves a substantially higher degree of risk of non-collection than loans that conform to institutional underwriting criteria. We do not acquire a loan unless material steps have been taken toward resolving problems with the loan, or its underlying property.

Financing with high loan-to-value ratios may involve increased risk of loss.

A loan-to-value ratio is the ratio of the amount of our financing, plus the amount of any senior indebtedness, to the appraised value of the property underlying the loan. Most of our financings have loan-to-value ratios in excess of 80% and many have loan-to-value ratios in excess of 90%. We expect to continue to hold loans with high loan-to-value ratios. By reducing the margin available to cover fluctuations in property value, a high loan-to-value ratio increases the risk that, upon default, the amount obtainable from the sale of the underlying property may be insufficient to repay the financing.

Lease expirations, lease defaults and lease terminations may adversely affect our revenue.

Lease expirations, lease defaults and lease terminations may result in reduced revenue from our real estate if the lease payments received from replacement tenants are less than the lease payments received from the expiring, defaulting or terminating tenants. In addition, lease defaults by one or more significant tenants, lease terminations by tenants following events causing significant damage to the property or takings by eminent domain, or the failure of tenants under expiring leases to elect to renew their leases, could cause us to experience long periods with reduced or no revenue from a property and to incur substantial capital expenditures in order to obtain replacement tenants.

We may need to make significant capital improvements to our properties in order to remain competitive.

The properties underlying our consolidated real estate may face competition from newer, more updated properties. In order to remain competitive, we may need to make significant capital improvements to these properties. In addition, in the event we need to re-lease a property, we may need to make significant tenant improvements.

Uninsured and underinsured losses may affect the value of, or our return from, our real estate.

Our properties, and the properties underlying our loans, have comprehensive insurance in amounts we believe are sufficient to permit the replacement of the properties in the event of a total loss, subject to applicable deductibles. There are, however, certain types of losses, such as earthquakes, floods, hurricanes and terrorism that may be uninsurable or not economically insurable. Also, inflation, changes in building codes and ordinances, environmental considerations and other factors might make it impractical to use insurance proceeds to replace a damaged or destroyed property. If any of these or similar events occurs, it may reduce our return from an affected property and the value of our investment.

Real estate with environmental problems may create liability for us.