Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - RAIT Financial Trust | d948739dex312.htm |

| EX-32.1 - EX-32.1 - RAIT Financial Trust | d948739dex321.htm |

| EX-12.1 - EX-12.1 - RAIT Financial Trust | d948739dex121.htm |

| EX-32.2 - EX-32.2 - RAIT Financial Trust | d948739dex322.htm |

| EX-31.1 - EX-31.1 - RAIT Financial Trust | d948739dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| x | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended June 30, 2015

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 1-14760

RAIT FINANCIAL TRUST

(Exact name of registrant as specified in its charter)

| Maryland | 23-2919819 | |

| (State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.) | |

| 2929 Arch Street, 17th Floor, Philadelphia, PA | 19104 | |

| (Address of principal executive offices) | (Zip Code) |

(215) 243-9000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

A total of 90,895,723 common shares of beneficial interest, par value $0.03 per share, of the registrant were outstanding as of August 7, 2015.

Table of Contents

RAIT FINANCIAL TRUST

| Page | ||||||

| PART I—FINANCIAL INFORMATION | 1 | |||||

| Item 1. |

1 | |||||

| Consolidated Balance Sheets as of June 30, 2015 and December 31, 2014 |

1 | |||||

| 2 | ||||||

| 3 | ||||||

| Consolidated Statement of Changes in Equity for the Six-Month Period Ended June 30, 2015 |

4 | |||||

| Consolidated Statements of Cash Flows for the Six-Month Periods Ended June 30, 2015 and 2014 |

5 | |||||

| 6 | ||||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

40 | ||||

| Item 3. |

55 | |||||

| Item 4. |

55 | |||||

| PART II—OTHER INFORMATION | 56 | |||||

| Item 1. |

56 | |||||

| Item 1A. |

56 | |||||

| Item 6. |

57 | |||||

| 58 | ||||||

Table of Contents

| Item 1. | Financial Statements |

RAIT Financial Trust

(Unaudited and dollars in thousands, except share and per share information)

| As of June 30, 2015 |

As of December 31, 2014 |

|||||||

| Assets |

||||||||

| Investment in mortgages, loans and preferred equity interests, at amortized cost: |

||||||||

| Commercial mortgages, mezzanine loans, and preferred equity interests |

$ | 1,506,542 | $ | 1,392,436 | ||||

| Allowance for loan losses |

(12,796 | ) | (9,218 | ) | ||||

|

|

|

|

|

|||||

| Total investment in mortgages, loans and preferred equity interests |

1,493,746 | 1,383,218 | ||||||

| Investments in real estate, net of accumulated depreciation of $178,572 and $168,480, respectively |

1,605,316 | 1,671,971 | ||||||

| Investments in securities and security-related receivables, at fair value |

— | 31,412 | ||||||

| Cash and cash equivalents |

104,772 | 121,726 | ||||||

| Restricted cash |

179,878 | 124,220 | ||||||

| Accrued interest receivable |

56,844 | 51,640 | ||||||

| Other assets |

77,708 | 72,023 | ||||||

| Deferred financing costs, net of accumulated amortization of $30,896 and $26,056, respectively |

25,117 | 27,802 | ||||||

| Intangible assets, net of accumulated amortization of $20,935 and $13,911, respectively |

32,195 | 29,463 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 3,575,576 | $ | 3,513,475 | ||||

|

|

|

|

|

|||||

| Liabilities and Equity |

||||||||

| Indebtedness |

$ | 2,661,528 | $ | 2,615,666 | ||||

| Accrued interest payable |

11,042 | 10,269 | ||||||

| Accounts payable and accrued expenses |

52,728 | 54,962 | ||||||

| Derivative liabilities |

12,154 | 20,695 | ||||||

| Deferred taxes, borrowers’ escrows and other liabilities |

172,621 | 144,733 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

2,910,073 | 2,846,325 | ||||||

| Series D cumulative redeemable preferred shares, $0.01 par value per share, 4,000,000 shares authorized, 4,000,000 and 4,000,000 shares issued and outstanding, respectively |

82,513 | 79,308 | ||||||

| Equity: |

||||||||

| Shareholders’ equity: |

||||||||

| Preferred shares, $0.01 par value per share, 25,000,000 shares authorized; |

||||||||

| 7.75% Series A cumulative redeemable preferred shares, liquidation preference $25.00 per share, 8,069,288 shares authorized, respectively, 5,303,591 and 4,775,569 shares issued and outstanding, respectively |

53 | 48 | ||||||

| 8.375% Series B cumulative redeemable preferred shares, liquidation preference $25.00 per share, 4,300,000 shares authorized, 2,325,626 and 2,288,465 shares issued and outstanding, respectively |

23 | 23 | ||||||

| 8.875% Series C cumulative redeemable preferred shares, liquidation preference $25.00 per share, 3,600,000 shares authorized, 1,640,100 shares issued and outstanding |

17 | 17 | ||||||

| Series E cumulative redeemable preferred shares, $0.01 par value per share, 4,000,000 shares authorized |

— | — | ||||||

| Common shares, $0.03 par value per share, 200,000,000 shares authorized, 82,895,723 and 82,506,606 issued and outstanding, respectively, including 743,014 and 541,575 unvested restricted common share awards, respectively |

2,487 | 2,473 | ||||||

| Additional paid in capital |

2,039,594 | 2,025,683 | ||||||

| Accumulated other comprehensive income (loss) |

(11,605 | ) | (20,788 | ) | ||||

| Retained earnings (deficit) |

(1,651,613 | ) | (1,633,911 | ) | ||||

|

|

|

|

|

|||||

| Total shareholders’ equity |

378,956 | 373,545 | ||||||

| Noncontrolling interests |

204,034 | 214,297 | ||||||

|

|

|

|

|

|||||

| Total equity |

582,990 | 587,842 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 3,575,576 | $ | 3,513,475 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these consolidated financial statements.

1

Table of Contents

RAIT Financial Trust

Consolidated Statements of Operations

(Unaudited and dollars in thousands, except share and per share information)

| For the Three-Month Periods Ended June 30 |

For the Six-Month Periods Ended June 30 |

|||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Revenue: |

||||||||||||||||

| Investment interest income |

$ | 24,107 | $ | 34,646 | $ | 47,355 | $ | 69,609 | ||||||||

| Investment interest expense |

(7,582 | ) | (7,523 | ) | (14,496 | ) | (14,706 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest margin |

16,525 | 27,123 | 32,859 | 54,903 | ||||||||||||

| Rental income |

55,473 | 39,214 | 109,442 | 74,390 | ||||||||||||

| Fee and other income |

7,415 | 6,919 | 13,009 | 11,271 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenue |

79,413 | 73,256 | 155,310 | 140,564 | ||||||||||||

| Expenses: |

||||||||||||||||

| Interest expense |

19,673 | 13,241 | 39,356 | 24,846 | ||||||||||||

| Real estate operating expense |

26,357 | 19,690 | 52,336 | 37,773 | ||||||||||||

| Compensation expense |

6,568 | 7,376 | 12,676 | 15,931 | ||||||||||||

| General and administrative expense |

5,065 | 4,655 | 10,465 | 8,483 | ||||||||||||

| Acquisition expense |

985 | 219 | 1,942 | 592 | ||||||||||||

| Provision for loan losses |

2,000 | 1,000 | 4,000 | 2,000 | ||||||||||||

| Depreciation and amortization expense |

17,005 | 13,441 | 36,022 | 25,483 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

77,653 | 59,622 | 156,797 | 115,108 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income |

1,760 | 13,634 | (1,487 | ) | 25,456 | |||||||||||

| Other (expense) income |

(241 | ) | 5 | (636 | ) | 15 | ||||||||||

| Gain (losses) on assets |

17,281 | (7,599 | ) | 17,281 | (5,375 | ) | ||||||||||

| Gain (losses) on extinguishment of debt |

— | — | — | 2,421 | ||||||||||||

| Change in fair value of financial instruments |

8,356 | (25,071 | ) | 12,846 | (49,210 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before taxes |

27,156 | (19,031 | ) | 28,004 | (26,693 | ) | ||||||||||

| Income tax (provision) benefit |

(715 | ) | 21 | (1,297 | ) | 260 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

26,441 | (19,010 | ) | 26,707 | (26,433 | ) | ||||||||||

| (Income) loss allocated to preferred shares |

(8,221 | ) | (7,415 | ) | (16,080 | ) | (13,221 | ) | ||||||||

| (Income) loss allocated to noncontrolling interests |

736 | 775 | 1,232 | (583 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) allocable to common shares |

$ | 18,956 | $ | (25,650 | ) | $ | 11,859 | $ | (40,237 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share-Basic: |

||||||||||||||||

| Earnings (loss) per share-Basic |

$ | 0.23 | $ | (0.31 | ) | $ | 0.14 | $ | (0.50 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted-average shares outstanding-Basic |

82,150,475 | 81,778,947 | 82,115,941 | 80,636,895 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share-Diluted: |

||||||||||||||||

| Earnings (loss) per share-Diluted |

$ | 0.22 | $ | (0.31 | ) | $ | 0.14 | $ | (0.50 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares outstanding-Diluted |

89,268,462 | 81,778,947 | 84,134,040 | 80,636,895 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of these consolidated financial statements.

2

Table of Contents

RAIT Financial Trust

Consolidated Statements of Comprehensive Income (Loss)

(Unaudited and dollars in thousands)

| For the Three-Month | For the Six-Month | |||||||||||||||

| Periods Ended June 30 | Periods Ended June 30 | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Net income (loss) |

$ | 26,441 | $ | (19,010 | ) | $ | 26,707 | $ | (26,433 | ) | ||||||

| Other comprehensive income (loss): |

||||||||||||||||

| Change in fair value of interest rate hedges |

(225 | ) | (644 | ) | (182 | ) | (1,196 | ) | ||||||||

| Realized (gains) losses on interest rate hedges reclassified to earnings |

4,398 | 7,243 | 9,365 | 14,780 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total other comprehensive income (loss) |

4,173 | 6,599 | 9,183 | 13,584 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income (loss) before allocation to noncontrolling interests |

30,614 | (12,411 | ) | 35,890 | (12,849 | ) | ||||||||||

| Allocation to noncontrolling interests |

736 | 775 | 1,232 | (583 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income (loss) |

$ | 31,350 | $ | (11,636 | ) | $ | 37,122 | $ | (13,432 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

Table of Contents

RAIT Financial Trust

Consolidated Statement of Changes in Equity

(Unaudited and dollars in thousands, except share information)

| Preferred Shares— Series A |

Par Value Preferred Shares— Series A |

Preferred Shares— Series B |

Par Value Preferred Shares— Series B |

Preferred Shares— Series C |

Par Value Preferred Shares— Series C |

Common Shares |

Par Value Common Shares |

Additional Paid In Capital |

Accumulated Other Comprehensive Income (Loss) |

Retained Earnings (Deficit) |

Total Shareholders’ Equity |

Noncontrolling Interests |

Total Equity |

|||||||||||||||||||||||||||||||||||||||||||

| Balance, December 31, 2014 |

4,775,569 | $ | 48 | 2,288,465 | $ | 23 | 1,640,100 | $ | 17 | 82,506,606 | $ | 2,473 | $ | 2,025,683 | $ | (20,788 | ) | $ | (1,633,911 | ) | $ | 373,545 | $ | 214,297 | $ | 587,842 | ||||||||||||||||||||||||||||||

| Net income (loss) |

— | — | — | — | — | — | — | — | — | — | 27,939 | 27,939 | (1,232 | ) | 26,707 | |||||||||||||||||||||||||||||||||||||||||

| Preferred dividends |

— | — | — | — | — | — | — | — | — | — | (16,080 | ) | (16,080 | ) | — | (16,080 | ) | |||||||||||||||||||||||||||||||||||||||

| Common dividends declared |

— | — | — | — | — | — | — | — | — | — | (29,561 | ) | (29,561 | ) | — | (29,561 | ) | |||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net |

— | — | — | — | — | — | — | — | — | 9,183 | — | 9,183 | — | 9,183 | ||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation |

— | — | — | — | — | — | — | — | (3,205 | ) | — | — | (3,205 | ) | — | (3,205 | ) | |||||||||||||||||||||||||||||||||||||||

| Issuance of noncontrolling interests |

— | — | — | — | — | — | — | — | — | — | — | — | (367 | ) | (367 | ) | ||||||||||||||||||||||||||||||||||||||||

| Distribution to noncontrolling interests |

— | — | — | — | — | — | — | — | — | — | — | — | (9,327 | ) | (9,327 | ) | ||||||||||||||||||||||||||||||||||||||||

| Deconsolidation of real estate owned property |

— | — | — | — | — | — | — | — | — | — | — | — | 663 | 663 | ||||||||||||||||||||||||||||||||||||||||||

| Preferred shares issued, net |

528,022 | 5 | 37,161 | — | — | — | — | — | 12,671 | — | — | 12,676 | — | 12,676 | ||||||||||||||||||||||||||||||||||||||||||

| Common shares issued for equity compensation |

— | — | — | — | — | — | 385,428 | 14 | 5,019 | — | — | 5,033 | — | 5,033 | ||||||||||||||||||||||||||||||||||||||||||

| Common shares issued, net |

— | — | — | — | — | — | 3,689 | — | (574 | ) | — | — | (574 | ) | — | (574 | ) | |||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

| Balance, June 30, 2015 |

5,303,591 | $ | 53 | 2,325,626 | $ | 23 | 1,640,100 | $ | 17 | 82,895,723 | $ | 2,487 | $ | 2,039,594 | $ | (11,605 | ) | $ | (1,651,613 | ) | $ | 378,956 | $ | 204,034 | $ | 582,990 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

Table of Contents

RAIT Financial Trust

Consolidated Statements of Cash Flows

(Unaudited and dollars in thousands)

| For the Six-Month | ||||||||

| Periods Ended June 30 | ||||||||

| 2015 | 2014 | |||||||

| Operating activities: |

||||||||

| Net income (loss) |

$ | 26,707 | $ | (26,433 | ) | |||

| Adjustments to reconcile net income (loss) to cash flow from operating activities: |

||||||||

| Provision for losses |

4,000 | 2,000 | ||||||

| Share-based compensation expense |

2,394 | 2,629 | ||||||

| Depreciation and amortization |

36,022 | 25,483 | ||||||

| Amortization of deferred financing costs and debt discounts |

9,458 | 4,646 | ||||||

| Accretion of discounts on investments |

(1,682 | ) | (1,986 | ) | ||||

| Amortization of above/below market leases |

(317 | ) | — | |||||

| (Gains) losses on assets |

(17,281 | ) | 5,375 | |||||

| (Gains) losses on extinguishment of debt |

— | (2,421 | ) | |||||

| Change in fair value of financial instruments |

(12,846 | ) | 49,210 | |||||

| Provision (benefit) for deferred taxes |

(897 | ) | (288 | ) | ||||

| Changes in assets and liabilities: |

||||||||

| (Decrease) in accrued interest receivable |

(2,956 | ) | (7,196 | ) | ||||

| (Decrease) in other assets |

(2,640 | ) | (9,246 | ) | ||||

| Increase (decrease) in accrued interest payable |

2,459 | (10,298 | ) | |||||

| (Decrease) in accounts payable and accrued expenses |

(1,609 | ) | (6,824 | ) | ||||

| Increase in borrowers’ escrows and other liabilities |

70,203 | 12,578 | ||||||

| Origination of conduit loans |

(251,959 | ) | (165,577 | ) | ||||

| Sales of conduit loans |

223,298 | 119,356 | ||||||

|

|

|

|

|

|||||

| Net conduit loans (originated) sold |

(28,661 | ) | (46,221 | ) | ||||

|

|

|

|

|

|||||

| Cash flow from operating activities |

82,354 | (8,992 | ) | |||||

| Investing activities: |

||||||||

| Proceeds from sales or repayments of other securities |

31,241 | 1,971 | ||||||

| Purchase and origination of loans for investment |

(191,892 | ) | (297,414 | ) | ||||

| Principal repayments on loans |

130,504 | 88,322 | ||||||

| Investments in real estate |

(37,500 | ) | (133,596 | ) | ||||

| Proceeds from the disposition of real estate |

20,596 | 3,820 | ||||||

| (Increase) decrease in restricted cash |

(90,590 | ) | 34,739 | |||||

|

|

|

|

|

|||||

| Cash flow from investing activities |

(137,641 | ) | (302,158 | ) | ||||

| Financing activities: |

||||||||

| Repayments on secured credit facilities and loans payable on real estate |

(20,640 | ) | (12,596 | ) | ||||

| Proceeds from secured credit facilities and loans payable on real estate |

58,275 | 46,313 | ||||||

| Repayments and repurchase of CDO notes payable |

(120,194 | ) | (131,200 | ) | ||||

| Proceeds from issuance of senior notes from floating rate CMBS transactions |

181,215 | 155,001 | ||||||

| Proceeds from issuance of 4.0% convertible senior notes |

— | 16,750 | ||||||

| Proceeds from issuance of 7.625% convertible senior notes |

— | 60,000 | ||||||

| Repayments of senior secured notes |

(4,000 | ) | — | |||||

| Net proceeds (repayments) related to conduit loan repurchase agreements |

7,277 | 576 | ||||||

| Net proceeds (repayments) related to floating rate loan repurchase agreements |

(14,587 | ) | 38,566 | |||||

| Distribution to noncontrolling interests |

(9,694 | ) | 49,428 | |||||

| Payments for deferred costs and convertible senior note hedges |

(4,466 | ) | (7,528 | ) | ||||

| Financing commitment fee |

(4,000 | ) | — | |||||

| Preferred share issuance, net of costs incurred |

12,676 | 33,552 | ||||||

| Common share issuance, net of costs incurred |

(1,140 | ) | 85,051 | |||||

| Distributions paid to preferred shareholders |

(12,872 | ) | (11,291 | ) | ||||

| Distributions paid to common shareholders |

(29,517 | ) | (25,240 | ) | ||||

|

|

|

|

|

|||||

| Cash flow from financing activities |

38,333 | 297,382 | ||||||

|

|

|

|

|

|||||

| Net change in cash and cash equivalents |

(16,954 | ) | (13,768 | ) | ||||

| Cash and cash equivalents at the beginning of the period |

121,726 | 88,847 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at the end of the period |

$ | 104,772 | $ | 75,079 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these consolidated financial statements.

5

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

NOTE 1: THE COMPANY

RAIT Financial Trust invests in and manages a portfolio of real-estate related assets, including direct ownership of real estate properties, and provides a comprehensive set of debt financing options to the real estate industry. References to “RAIT”, “we”, “us”, and “our” refer to RAIT Financial Trust and its subsidiaries, unless the context otherwise requires. RAIT is a self-managed and self-advised Maryland real estate investment trust, or REIT.

We finance a substantial portion of our investments through borrowing and securitization strategies seeking to match the maturities and terms of our financings with the maturities and terms of those investments, and to mitigate interest rate risk through derivative instruments.

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a. Basis of Presentation

The accompanying unaudited interim consolidated financial statements have been prepared by management in accordance with U.S. generally accepted accounting principles, or GAAP. Certain information and footnote disclosures normally included in annual consolidated financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to such rules and regulations, although we believe that the included disclosures are adequate to make the information presented not misleading. The unaudited interim consolidated financial statements should be read in conjunction with our audited financial statements as of and for the year ended December 31, 2014 included in our Annual Report on Form 10-K, or the 2014 annual report. In the opinion of management, all adjustments, consisting only of normal recurring adjustments, necessary to present fairly our consolidated financial position and consolidated results of operations and cash flows are included. The results of operations for the interim periods presented are not necessarily indicative of the results for the full year.

Certain prior period amounts have been reclassified to conform with the current period presentation.

During the six-month period ended June 30, 2015, we recorded the following adjustments in the accompanying consolidated statement of operations that related to transactions completed in a prior period: (a) investment interest income includes the write-off of accrued interest receivable of $842 that was associated with investments in loans that was determined to be not collectible and (b) depreciation and amortization expense includes $708 associated with capital additions associated with our investment in real estate which were not properly eliminated previously. We also recorded an adjustment to correct the deferred tax liability balance with an offset to goodwill for $2,257 related to our acquisition of Urban Retail Properties, LLC.

During the six-month period ended June 30, 2015, we revised the Consolidated Statements of Cash Flows for the six-month period ended June 30, 2014. The revision consisted of classifying the origination of conduit loans and the sale of conduit loans from cash flows from investing activities to cash flows from operating activities. The impact of this revision was a decrease to cash flows from operating activities and an increase to cash flows from investing activities of $46,221 for the period ended June 30, 2014. The revision had no impact to cash and cash equivalents as of June 30, 2014. In addition, the revision did not impact any other consolidated financial statement as of June 30, 2014 or for the six-month or three-month periods ended June 30, 2014.

We evaluated these revisions and reclassifications and determined, based on quantitative and qualitative factors, the changes were not material to the consolidated financial statements taken as a whole for any previously filed consolidated financial statements.

b. Principles of Consolidation

The consolidated financial statements reflect our accounts and the accounts of our majority-owned and/or controlled subsidiaries. We also consolidate entities that are variable interest entities, or VIEs, where we have determined that we are the primary beneficiary of such entities. The portions of these entities that we do not own are presented as noncontrolling interests as of the dates and for the periods presented in the consolidated financial statements. All intercompany accounts and transactions have been eliminated in consolidation.

Under Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 810, “Consolidation”, the determination of whether to consolidate a VIE is based on the power to direct the activities of the VIE that most significantly impact the VIE’s economic performance together with either the obligation to absorb losses or the right to receive benefits that could

6

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

be significant to the VIE. We define the power to direct the activities that most significantly impact the VIE’s economic performance as the ability to buy, sell, refinance, or recapitalize assets or entities, and solely control other material operating events or items of the respective entity. For our commercial mortgages, mezzanine loans, and preferred equity investments, certain rights we hold are protective in nature and would preclude us from having the power to direct the activities that most significantly impact the VIE’s economic performance. Assuming both criteria are met, we would be considered the primary beneficiary and would consolidate the VIE. We will continually assess our involvement with VIEs and consolidate the VIEs when we are the primary beneficiary. See Note 9 for additional disclosures pertaining to VIEs.

c. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods. The items that include significant estimates are fair value of financial instruments and allowance for losses. Actual results could differ from those estimates.

d. Investments in Loans

We invest in commercial mortgages, mezzanine loans, and preferred equity interests. We account for our investments in commercial mortgages, mezzanine loans and other loans at amortized cost. The carrying value of these investments is adjusted for origination discounts/premiums, nonrefundable fees and direct costs for originating loans which are amortized into income on a level yield basis over the terms of the loans.

e. Allowance for Losses, Impaired Loans and Non-accrual Status

We maintain an allowance for losses on our investments in commercial mortgages, mezzanine loans and preferred equity interests. Management’s periodic evaluation of the adequacy of the allowance is based upon expected and inherent risks in the portfolio, the estimated value of underlying collateral, and current economic conditions. Management reviews loans for impairment and establishes specific reserves when a loss is probable under the provisions of FASB ASC Topic 310, “Receivables.” A loan is impaired when it is probable that we may not collect all principal and interest payments according to the contractual terms. As part of the detailed loan review, we consider many factors about the specific loan, including payment history, asset performance, borrower’s financial capability and other characteristics. If any trends or characteristics indicate that it is probable that other loans, with similar characteristics to those of impaired loans, have incurred a loss, we consider whether an allowance for loss is needed pursuant to FASB ASC Topic 450, “Contingencies.” Management evaluates loans for non-accrual status each reporting period. A loan is placed on non-accrual status when the loan payment deficiencies exceed 90 days. Payments received for non-accrual or impaired loans are applied to principal until the loan is removed from non-accrual status or no longer impaired. Past due interest is recognized on non-accrual loans when they are removed from non-accrual status and are making current interest payments. The allowance for losses is increased by charges to operations and decreased by charge-offs (net of recoveries). Management charges off loans when the investment is no longer realizable and legally discharged.

f. Investments in Real Estate

Investments in real estate are shown net of accumulated depreciation. We capitalize those costs that have been evaluated to improve the real property and depreciate those costs on a straight-line basis over the useful life of the asset. We depreciate real property using the following useful lives: buildings and improvements—30 to 40 years; furniture, fixtures, and equipment—5 to 10 years; and tenant improvements—shorter of the lease term or the life of the asset. Costs for ordinary maintenance and repairs are charged to expense as incurred.

7

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

Acquisitions of real estate assets and any related intangible assets are recorded initially at fair value under FASB ASC Topic 805, “Business Combinations.” Fair value is determined by management based on market conditions and inputs at the time the asset is acquired. The fair value of the real estate acquired is allocated to the acquired tangible assets, consisting of land, building and tenant improvements, and identified intangible assets and liabilities, consisting of the value of above-market and below-market leases for acquired in-place leases and the value of tenant relationships, based in each case on their fair values. Purchase accounting is applied to assets and liabilities associated with the real estate acquired. Transaction costs and fees incurred related to acquisitions are expensed as incurred.

Upon the acquisition of properties, we estimate the fair value of acquired tangible assets (consisting of land, building and improvements) and identified intangible assets and liabilities (consisting of above and below-market leases, in-place leases and tenant relationships), and assumed debt at the date of acquisition, based on the evaluation of information and estimates available at that date. In determining the fair value of the identified intangible assets and liabilities of an acquired property, above-market and below-market in-place lease values are recorded based on the present value (using an interest rate which reflects the risks associated with the leases acquired) of the differences between (i) the contractual amounts to be paid pursuant to the in-place leases and (ii) management’s estimate of fair market lease rates for the corresponding in-place leases, measured over a period equal to the remaining term of the lease. The capitalized above-market lease values and the capitalized below-market lease values are amortized as an adjustment to rental income over the lease term.

The aggregate value of in-place leases is determined by evaluating various factors, including an estimate of carrying costs during the expected lease-up periods, current market conditions and similar leases. In estimating carrying costs, management includes real estate taxes, insurance and other operating expenses, and estimates of lost rental revenue during the expected lease-up periods based on current market demand. Management also estimates costs to execute similar leases including leasing commissions, legal and other related costs. The value assigned to this intangible asset is amortized over the assumed lease up period.

Management reviews our investments in real estate for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. The review of recoverability is based on an estimate of the future undiscounted cash flows (excluding interest charges) expected to result from the long-lived asset’s use and eventual disposition. These cash flows consider factors such as expected future operating income, trends and prospects, as well as the effects of leasing demand, competition and other factors. If impairment exists due to the inability to recover the carrying value of a long-lived asset, an impairment loss is recorded to the extent that the carrying value exceeds the estimated fair value of the property.

g. Revenue Recognition

| 1) | Interest income—We recognize interest income from investments in commercial mortgages, mezzanine loans, and preferred equity interests on a yield to maturity basis. Many of our commercial mortgages and mezzanine loans provide for the accrual of interest at specified rates which differ from current payment terms. Interest income is recognized on such loans at the accrual rate subject to management’s determination that accrued interest and outstanding principal are ultimately collectible. Management will cease accruing interest on these loans when it determines that the interest income is not collectible based on the ultimate value of the underlying collateral using discounted cash flow models and market based assumptions. Management will recognize interest on these loans on a cash basis. |

For investments that we did not elect to record at fair value under FASB ASC Topic 825, “Financial Instruments”, origination fees and direct loan origination costs are deferred and amortized to net investment income, using the effective interest method, over the contractual life of the underlying loan security or loan, in accordance with FASB ASC Topic 310, “Receivables.”

For investments that we elected to record at fair value under FASB ASC Topic 825, origination fees and direct loan costs are recorded in income and are not deferred.

We recognize interest income from interests in certain securitized financial assets on an estimated effective yield to maturity basis. Management estimates the current yield on the amortized cost of the investment based on estimated cash flows after considering prepayment and credit loss experience.

| 2) | Rental income—We generate rental income from tenant rent and other tenant-related activities at our consolidated real estate properties. For multi-family real estate properties, rental income is recorded when due from residents and recognized monthly as it is earned and realizable, under lease terms which are generally for periods of one year or less. For retail and office real estate properties, rental income is recognized on a straight-line basis from the later of the date of |

8

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

| the commencement of the lease or the date of acquisition of the property subject to existing leases, which averages minimum rents over the terms of the leases. Leases also typically provide for tenant reimbursement of a portion of common area maintenance and other operating expenses to the extent that a tenant’s pro rata share of expenses exceeds a base year level set in the lease. |

| 3) | Fee and other income—We generate fee and other income through our various subsidiaries by (a) funding conduit loans for sale into unaffiliated commercial mortgage-backed securities, or CMBS, securitizations, (b) providing or arranging to provide financing to our borrowers, (c) providing ongoing asset management services to investment portfolios under cancelable management agreements, and (d) providing property management services to third parties. We recognize revenue for these activities when the fees are fixed or determinable, are evidenced by an arrangement, collection is reasonably assured and the services under the arrangement have been provided. While we may receive asset management fees when they are earned, we eliminate earned asset management fee income from securitizations while such securitizations are consolidated. |

h. Fair Value of Financial Instruments

In accordance with FASB ASC Topic 820, “Fair Value Measurements and Disclosures”, fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Where available, fair value is based on observable market prices or parameters or derived from such prices or parameters. Where observable prices or inputs are not available, valuation models are applied. These valuation techniques involve management estimation and judgment, the degree of which is dependent on the price transparency for the instruments or market and the instruments’ complexity for disclosure purposes. Assets and liabilities recorded at fair value in the consolidated balance sheets are categorized based upon the level of judgment associated with the inputs used to measure their value. Hierarchical levels, as defined in FASB ASC Topic 820, “Fair Value Measurements and Disclosures” and directly related to the amount of subjectivity associated with the inputs to fair valuations of these assets and liabilities, are as follows:

| • | Level 1: Valuations are based on unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date. The types of assets carried at level 1 fair value generally are equity securities listed in active markets. As such, valuations of these investments do not entail a significant degree of judgment. |

| • | Level 2: Valuations are based on quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in markets that are not active or for which all significant inputs are observable, either directly or indirectly. |

Fair value assets and liabilities that are generally included in this category are unsecured REIT note receivables, commercial mortgage-backed securities, or CMBS, receivables and certain financial instruments classified as derivatives where the fair value is based primarily on observable market inputs.

| • | Level 3: Inputs are unobservable inputs for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement in its entirety. Our assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the asset. Generally, assets and liabilities carried at fair value and included in this category were TruPS and subordinated debentures, trust preferred obligations and CDO notes payable where significant observable market inputs do not exist. |

The availability of observable inputs can vary depending on the financial asset or liability and is affected by a wide variety of factors, including, for example, the type of investment, whether the investment is new, whether the investment is traded on an active exchange or in the secondary market, and the current market condition. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by us in determining fair value is greatest for instruments categorized in level 3.

Fair value is a market-based measure considered from the perspective of a market participant who holds the asset or owes the liability rather than an entity-specific measure. Therefore, even when market assumptions are not readily available, our own assumptions are set to reflect those that management believes market participants would use in pricing the asset or liability at the measurement date. We use prices and inputs that management believes are current as of the measurement

9

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

date, including during periods of market dislocation. In periods of market dislocation, the observability of prices and inputs may be reduced for many instruments. This condition could cause an instrument to be transferred from Level 1 to Level 2 or Level 2 to Level 3.

Many financial instruments have bid and ask prices that can be observed in the marketplace. Bid prices reflect the highest price that buyers in the market are willing to pay for an asset. Ask prices represent the lowest price that sellers in the market are willing to accept for an asset. For financial instruments whose inputs are based on bid-ask prices, we do not require that fair value always be a predetermined point in the bid-ask range. Our policy is to allow for mid-market pricing and adjusting to the point within the bid-ask range that results in our best estimate of fair value.

Fair value for certain of our Level 3 financial instruments is derived using internal valuation models. These internal valuation models include discounted cash flow analyses developed by management using current interest rates, estimates of the term of the particular instrument, specific issuer information and other market data for securities without an active market. In accordance with FASB ASC Topic 820, “Fair Value Measurements and Disclosures”, the impact of our own credit spreads is also considered when measuring the fair value of financial assets or liabilities, including derivative contracts. Where appropriate, valuation adjustments are made to account for various factors, including bid-ask spreads, credit quality and market liquidity. These adjustments are applied on a consistent basis and are based on observable inputs where available. Management’s estimate of fair value requires significant management judgment and is subject to a high degree of variability based upon market conditions, the availability of specific issuer information and management’s assumptions.

i. Deferred Financing Costs and Intangible Assets

Costs incurred in connection with debt financing are capitalized as deferred financing costs and charged to interest expense over the terms of the related debt agreements, under the effective interest method. Intangible assets on our consolidated balance sheets represent identifiable intangible assets acquired in business acquisitions. We amortize identified intangible assets to expense over their estimated lives using the straight-line method. We evaluate intangible assets for impairment as events and circumstances change, in accordance with FASB ASC Topic 360, “Property, Plant, and Equipment.” The gross carrying amount for our customer relationships was $19,149 as of June 30, 2015 and December 31, 2014. The gross carrying amount for our in-place leases, above market leases, and ground lease was $32,481 and $22,725 as of June 30, 2015 and December 31, 2014, respectively. The gross carrying amount for our trade name was $1,500 as of June 30, 2015 and December 31, 2014. The accumulated amortization for our intangible assets was $20,935 and $13,911 as of June 30, 2015 and December 31, 2014, respectively. We recorded amortization expense of $3,108 and $2,449 for the three-month periods ended June 30, 2015 and 2014, respectively, and $7,039 and $4,396 for the six-month periods ended June 30, 2015 and 2014, respectively. Based on the intangible assets identified above, we expect to record amortization expense of intangible assets of $3,133 for the remainder of 2015, $5,289 for 2016, $3,848 for 2017, $3,172 for 2018, $2,997 for 2019 and $13,756 thereafter. As of June 30, 2015, we have determined that no impairment exists on our intangible assets.

j. Goodwill

Goodwill on our consolidated balance sheet represented the amounts paid in excess of the fair value of the net assets acquired from business acquisitions accounted for under FASB ASC Topic 805, “Business Combinations.” Pursuant to FASB ASC Topic 350, “Intangibles-Goodwill and Other”, goodwill is not amortized to expense but rather is analyzed for impairment. We evaluate goodwill for impairment on an annual basis and as events and circumstances change, in accordance with FASB ASC Topic 350. As of June 30, 2015 and December 31, 2014, we have $8,757 and $11,014 of goodwill, respectively, that is included in Other Assets in the accompanying consolidated balance sheets. The change in goodwill is attributable to the correction discussed in the Basis of Presentation section within this Note above. As of June 30, 2015, we have determined that no triggering events occurred that would indicate an impairment on our goodwill.

k. Recent Accounting Pronouncements

On January 1, 2015, we adopted the accounting standard classified under FASB ASC Topic 205, “Presentation of Financial Statements”. This accounting standard amends existing guidance to change reporting requirements for discontinued operations by requiring the disposal of an entity to be reported in discontinued operations if the disposal represents a strategic shift that has or will have a major effect on an entity’s operations and financial results. This standard is effective for interim and annual reporting periods beginning on or after December 15, 2014. The adoption of this standard did not have a material effect on our consolidated financial statements.

10

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

In May 2014, the FASB issued an accounting standard classified under FASB ASC Topic 606, “Revenue from Contracts with Customers”. This accounting standard generally replaces existing guidance by requiring an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. This standard is currently effective for annual reporting periods beginning after December 15, 2016. On July 9, 2015, the FASB affirmed its proposal to defer the effective date of this accounting standard by one year. Management is currently evaluating the impact that this standard may have on our consolidated financial statements.

In February 2015, the FASB issued an accounting standard classified under FASB ASC Topic 810, “Consolidation”. This accounting standard amends the consolidation analysis required under GAAP and requires management to reevaluate all previous consolidation conclusions. This standard considers limited partnerships as VIEs, unless the limited partners have either substantive kick-out or participating rights. The presumption that a general partner should consolidate a limited partnership has also been eliminated. The standard amends the effect that fees paid to a decision maker or service provider have on the consolidation analysis, as well as amends how variable interests held by a reporting entity’s related parties affect the consolidation conclusion. This standard also clarifies how to determine whether equity holders as a group have power over an entity. This standard is effective for interim and annual reporting periods beginning on or after December 15, 2015, with early adoption permitted. Management is currently evaluating the impact that this standard may have on our consolidated financial statements.

In April 2015, the FASB issued an accounting standard classified under FASB ASC Topic 835, “Interest”. This accounting standard amends existing guidance to change reporting requirements for debt issuance costs by requiring debt issuance costs to be presented on the balance sheet as a direct deduction from the debt liability. This standard is effective for interim and annual reporting periods beginning on or after December 15, 2015, with an early adoption permitted. Retrospective application to prior periods is required. Management does not expect that this accounting standard will have a significant impact on our consolidated financial statements.

11

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

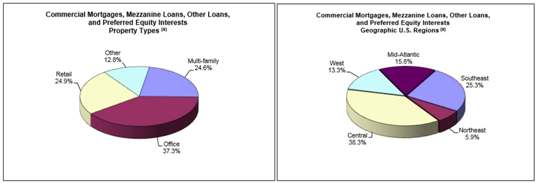

NOTE 3: INVESTMENTS IN LOANS

Investments in Commercial Mortgages, Mezzanine Loans, and Preferred Equity Interests

The following table summarizes our investments in commercial mortgages, mezzanine loans, and preferred equity interests as of June 30, 2015:

| Unpaid Principal Balance |

Unamortized (Discounts) Premiums |

Carrying Amount |

Number of Loans |

Weighted- Average Coupon (1) |

Range of Maturity Dates | |||||||||||||||||

| Commercial Real Estate (CRE) |

||||||||||||||||||||||

| Commercial mortgages (2) |

$ | 1,282,154 | $ | (14,428 | ) | $ | 1,267,726 | 108 | 5.3 | % | Sep. 2015 to Jan. 2029 | |||||||||||

| Mezzanine loans |

202,694 | (1,024 | ) | 201,670 | 62 | 9.8 | % | Jul. 2015 to May 2025 | ||||||||||||||

| Preferred equity interests |

39,311 | (2,335 | ) | 36,976 | 9 | 7.3 | % | Feb. 2016 to Aug. 2033 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total CRE |

1,524,159 | (17,787 | ) | 1,506,372 | 179 | 6.0 | % | |||||||||||||||

| Deferred fees, net |

170 | — | 170 | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

| Total |

$ | 1,524,329 | $ | (17,787 | ) | $ | 1,506,542 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

| (1) | Weighted-average coupon is calculated on the unpaid principal balance, which does not necessarily correspond to the carrying amount. |

| (2) | Commercial mortgages includes eleven conduit loans with an unpaid principal balance and carrying amount of $114,048 a weighted-average coupon of 4.3% and maturity dates ranging from November 2022 through July 2025. These commercial mortgages are accounted for as loans held for sale. |

The following table summarizes our investments in commercial mortgages, mezzanine loans, other loans and preferred equity interests as of December 31, 2014:

| Unpaid Principal Balance |

Unamortized (Discounts) Premiums |

Carrying Amount |

Number of Loans |

Weighted- Average Coupon (1) |

Range of Maturity Dates | |||||||||||||||||

| Commercial Real Estate (CRE) |

||||||||||||||||||||||

| Commercial mortgages (2) |

$ | 1,148,290 | $ | (14,519 | ) | $ | 1,133,771 | 95 | 5.9 | % | Jan. 2015 to Jan. 2025 | |||||||||||

| Mezzanine loans |

226,105 | (1,602 | ) | 224,503 | 74 | 9.8 | % | Mar. 2015 to Jan. 2029 | ||||||||||||||

| Preferred equity interests |

34,859 | (1 | ) | 34,858 | 9 | 7.1 | % | Feb. 2016 to Aug. 2025 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total CRE |

1,409,254 | (16,122 | ) | 1,393,132 | 178 | 6.5 | % | |||||||||||||||

| Deferred fees, net |

(696 | ) | — | (696 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

| Total |

$ | 1,408,558 | $ | (16,122 | ) | $ | 1,392,436 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

| (1) | Weighted-average coupon is calculated on the unpaid principal amount of the underlying instruments, which does not necessarily correspond to the carrying amount. |

| (2) | Commercial mortgages includes 11 conduit loans with an unpaid principal balance and carrying amount of $93,925, a weighted-average coupon of 4.6% and maturity dates ranging from November 2019 through January 2025. These commercial mortgages are accounted for as loans held for sale. |

12

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

During the six-month period ended June 30, 2015, we did not convert any commercial real estate loans to owned real estate property. During the six-month period ended June 30, 2014, we completed the conversion of one commercial real estate loan with a carrying value of $28,588 to real estate owned property and we recorded a gain on asset of $112 as the value of the real estate exceeded the carrying amount of the converted loan.

The following table summarizes the delinquency statistics of our commercial real estate loans as of June 30, 2015 and December 31, 2014:

| As of June 30, 2015 | ||||||||||||||||

| Delinquency Status |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Current |

$ | 1,282,154 | $ | 181,493 | $ | 35,661 | $ | 1,499,308 | ||||||||

| 30 to 59 days |

— | — | — | — | ||||||||||||

| 60 to 89 days |

— | — | — | — | ||||||||||||

| 90 days or more |

— | 19,953 | 3,650 | 23,603 | ||||||||||||

| In foreclosure or bankruptcy proceedings |

— | 1,248 | — | 1,248 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 1,282,154 | $ | 202,694 | $ | 39,311 | $ | 1,524,159 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| As of December 31, 2014 | ||||||||||||||||

| Delinquency Status |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Current |

$ | 1,148,290 | $ | 202,919 | $ | 31,209 | $ | 1,382,418 | ||||||||

| 30 to 59 days |

— | — | — | — | ||||||||||||

| 60 to 89 days |

— | 1,555 | — | 1,555 | ||||||||||||

| 90 days or more |

— | 19,953 | 3,650 | 23,603 | ||||||||||||

| In foreclosure or bankruptcy proceedings |

— | 1,678 | — | 1,678 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 1,148,290 | $ | 226,105 | $ | 34,859 | $ | 1,409,254 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

As of June 30, 2015 and December 31, 2014, all $24,851 and $25,281, respectively, of our commercial real estate loans that were 90 days or more past due or in foreclosure or bankruptcy were on non-accrual status and had a weighted-average interest rate of 5.7% and 5.8%, respectively. Also, as of June 30, 2015, two loans, with a recorded investment of $68,155 and a weighted average interest rate of 9.2%, were recognizing interest on the cash basis. Additionally, as of June 30, 2015, one loan, with an unpaid principal balance of $18,500, which had previously been restructured in a troubled debt restructuring, does not accrue interest in accordance with its restructured terms as it may be prepaid at par.

13

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

Allowance For Loan Losses And Impaired Loans

We closely monitor our loans which require evaluation for loan loss in two categories: satisfactory and watchlist/impaired. Loans classified as impaired are generally loans which have credit weaknesses or whose credit quality has temporarily deteriorated or have been restructured in troubled debt restructuring. As of June 30, 2015 and December 31, 2015, we have classified our investment in loans by credit risk category as follows:

| As of June 30, 2015 | ||||||||||||||||

| Credit Status |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Satisfactory |

$ | 1,247,234 | $ | 154,493 | $ | 31,365 | $ | 1,433,092 | ||||||||

| Watchlist/Impaired |

34,920 | 48,201 | 7,946 | 91,067 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 1,282,154 | $ | 202,694 | $ | 39,311 | $ | 1,524,159 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| As of December 31, 2014 | ||||||||||||||||

| Credit Status |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Satisfactory |

$ | 1,125,370 | $ | 175,915 | $ | 26,849 | $ | 1,328,134 | ||||||||

| Watchlist/Impaired |

22,920 | 50,190 | 8,010 | 81,120 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 1,148,290 | $ | 226,105 | $ | 34,859 | $ | 1,409,254 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The following tables provide roll-forwards of our allowance for loan losses for our commercial mortgages, mezzanine loans and preferred equity interests for the three-month periods ended June 30, 2015 and 2014:

| For the Three-Month Period Ended June 30, 2015 |

||||||||||||||||

| Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | |||||||||||||

| Beginning balance |

$ | — | $ | 9,471 | $ | 1,326 | $ | 10,797 | ||||||||

| Provision for loan losses |

— | 2,000 | — | $ | 2,000 | |||||||||||

| Charge-offs, net of recoveries |

— | (1 | ) | — | $ | (1 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Ending balance |

$ | — | $ | 11,470 | $ | 1,326 | $ | 12,796 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| For the Three-Month Period Ended June 30, 2014 |

||||||||||||||||

| Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | |||||||||||||

| Beginning balance |

$ | — | $ | 12,960 | $ | 1,319 | $ | 14,279 | ||||||||

| Provision for loan losses |

— | 1,000 | — | 1,000 | ||||||||||||

| Charge-offs, net of recoveries |

— | 57 | — | 57 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Ending balance |

$ | — | $ | 14,017 | $ | 1,319 | $ | 15,336 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

14

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

The following tables provide roll-forwards of our allowance for loan losses for our commercial mortgages, mezzanine loans and preferred equity interests for the six-month periods ended June 30, 2015 and 2014:

| For the Six-Month Period Ended June 30, 2015 |

||||||||||||||||

| Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | |||||||||||||

| Beginning balance |

$ | — | $ | 7,892 | $ | 1,326 | $ | 9,218 | ||||||||

| Provision for loan losses |

— | 4,000 | — | $ | 4,000 | |||||||||||

| Charge-offs, net of recoveries |

— | (422 | ) | — | $ | (422 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Ending balance |

$ | — | $ | 11,470 | $ | 1,326 | $ | 12,796 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| For the Six-Month Period Ended June 30, 2014 |

||||||||||||||||

| Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | |||||||||||||

| Beginning balance |

$ | — | $ | 21,636 | $ | 1,319 | $ | 22,955 | ||||||||

| Provision for loan losses |

— | 2,000 | — | 2,000 | ||||||||||||

| Charge-offs, net of recoveries |

— | (9,619 | ) | — | (9,619 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Ending balance |

$ | — | $ | 14,017 | $ | 1,319 | $ | 15,336 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Information related to those loans on our watchlist or considered to be impaired was as follows:

| As of June 30, 2015 | ||||||||||||||||

| Watchlist/Impaired Loans |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Watchlist/Impaired loans expecting full recovery |

$ | 34,920 | $ | 8,500 | $ | 4,296 | $ | 47,716 | ||||||||

| Watchlist/Impaired loans with reserves |

— | 39,701 | 3,650 | 43,351 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Watchlist/Impaired Loans(1) |

$ | 34,920 | $ | 48,201 | $ | 7,946 | $ | 91,067 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Allowance for losses |

$ | — | $ | 11,470 | $ | 1,326 | $ | 12,796 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | As of June 30, 2015, this includes $5,500 of unpaid principal relating to previously identified troubled debt restructurings (TDRs) that are on accrual status. |

| As of December 31, 2014 | ||||||||||||||||

| Watchlist/Impaired Loans |

Commercial Mortgages |

Mezzanine Loans |

Preferred Equity |

Total | ||||||||||||

| Watchlist/Impaired loans expecting full recovery |

$ | 22,920 | $ | 40,559 | $ | 4,360 | $ | 67,839 | ||||||||

| Watchlist/Impaired loans with reserves |

— | 9,631 | 3,650 | 13,281 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Watchlist/Impaired Loans(1) |

$ | 22,920 | $ | 50,190 | $ | 8,010 | $ | 81,120 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Allowance for losses |

$ | — | $ | 7,892 | $ | 1,326 | $ | 9,218 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

15

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

| (1) | As of December 31, 2014, this includes $5,500 of unpaid principal relating to previously identified TDRs that are on accrual status. |

The average unpaid principal balance and recorded investment of total impaired loans was $53,179 and $60,230 during the three-month periods ended June 30, 2015 and 2014, respectively, and $53,333 and $60,378 during the six-month periods ended June 30, 2015 and 2014, respectively. We recorded interest income of $634 and $882 on loans that were impaired for the three-month periods ended June 30, 2015 and 2014, respectively. We recorded interest income of $685 and $882 on loans that were impaired for the six-month periods ended June 30, 2015 and 2014, respectively.

We have evaluated restructurings of our commercial real estate loans to determine if the restructuring constitutes a troubled debt restructuring (TDR) under FASB ASC Topic 310, “Receivables”. During the six-month period ended June 30, 2015, there were no restructurings of our commercial real estate loans that constituted a TDR. As of June 30, 2015, there were no TDRs that subsequently defaulted for restructurings that occurred within the previous 12 months.

NOTE 4: INVESTMENTS IN SECURITIES

Our investments in securities and security-related receivables are accounted for at fair value. On December 19, 2014, our subsidiary assigned or delegated its rights and responsibilities as collateral manager for the T8 and T9 securitizations, as referenced in our 2014 annual report. As a result of the assignment and delegation, we determined that we are no longer the primary beneficiary of T8 and T9 and deconsolidated the two securitizations. During the first quarter of 2015, we sold all of our remaining securities with an aggregate fair value of $31,412 and we had no investments in securities as of June 30, 2015.

The following table summarizes our investments in securities as of December 31, 2014:

| Investment Description |

Amortized Cost |

Gross Unrealized Gains |

Gross Unrealized Losses |

Estimated Fair Value |

Weighted Average Coupon (1) |

Weighted Average Years to Maturity |

||||||||||||||||||

| Available-for-sale securities (2) |

$ | 210,600 | $ | 2,053 | $ | (193,486 | ) | $ | 19,167 | 3.5 | % | 23.1 | ||||||||||||

| Security-related receivables |

||||||||||||||||||||||||

| Unsecured REIT note receivables |

10,000 | 995 | — | 10,995 | 6.7 | % | 3.0 | |||||||||||||||||

| CMBS receivables (3) |

5,000 | — | (3,750 | ) | 1,250 | 5.7 | % | 34.5 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total security-related receivables |

15,000 | 995 | (3,750 | ) | 12,245 | 6.3 | % | 13.5 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total investments in securities |

$ | 225,600 | $ | 3,048 | $ | (197,236 | ) | $ | 31,412 | 3.6 | % | 22.7 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) | Weighted-average coupon is calculated on the unpaid principal amount of the underlying instruments, which does not necessarily correspond to the carrying amount. |

| (2) | As of December 31, 2014, this includes available-for-sale securities that are accounted for under the fair value option other than an available-for-sale security that has an amortized cost of $3,600 and a carrying value of $3,606. |

| (3) | CMBS receivables include securities with a fair value totaling $1,250 that are rated “D” by Standard & Poor’s. |

The following table summarizes the non-accrual status of our investments in securities:

| As of December 31, 2014 | ||||||||||||

| Principal /Par Amount on Non- Accrual |

Weighted Average Coupon |

Fair Value | ||||||||||

| Other securities |

$ | 210,600 | 3.5 | % | $ | 17,120 | ||||||

| CMBS receivables |

5,000 | 5.7 | % | 1,250 | ||||||||

The assets of our consolidated CDOs collateralize the debt of such entities and are not available to our creditors. As of December 31, 2014, investment in securities of $0 in principal amount of TruPS and subordinated debentures, and $10,000 in principal amount of unsecured REIT note receivables and CMBS receivables, collateralized the consolidated CDO notes payable of such entities.

16

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

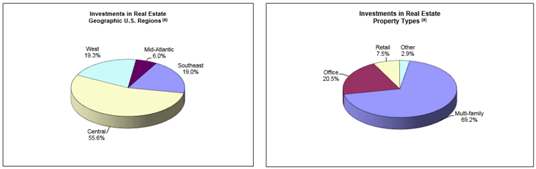

NOTE 5: INVESTMENTS IN REAL ESTATE

The table below summarizes our investments in real estate:

| Book Value | ||||||||

| As of June 30, 2015 |

As of December 31, 2014 |

|||||||

| Multi-family real estate properties (a) |

$ | 1,234,056 | $ | 1,286,898 | ||||

| Office real estate properties |

364,077 | 370,114 | ||||||

| Retail real estate properties |

133,471 | 132,117 | ||||||

| Parcels of land |

52,284 | 51,322 | ||||||

|

|

|

|

|

|||||

| Subtotal |

1,783,888 | 1,840,451 | ||||||

| Less: Accumulated depreciation and amortization (a) |

(178,572 | ) | (168,480 | ) | ||||

|

|

|

|

|

|||||

| Investments in real estate (b) |

$ | 1,605,316 | $ | 1,671,971 | ||||

|

|

|

|

|

|||||

| (a) | As of June 30, 2015, includes properties owned by Independence Realty Trust, Inc., or IRT, with a book value of $716,581 and accumulated depreciation of $31,188. As of December 31, 2014, includes properties owned by IRT, with a book value of $689,112 and accumulated depreciation of $23,376. |

| (b) | Investments in real estate includes one real estate asset held for sale as of June 30, 2015. This asset had a carrying amount of $1,196 and a fair value of $3,000. |

As of June 30, 2015 and December 31, 2014, our investments in real estate were comprised of land of $324,595 and $338,057, respectively, and investments in real estate and improvements of $1,459,293 and $1,502,394, respectively.

As of June 30, 2015, our investments in real estate of $1,605,316 are financed through $639,493 of mortgages held by third parties and $845,620 of mortgages held by our RAIT I and RAIT II CDO securitizations. As of December 31, 2014, our investments in real estate of $1,671,971 are financed through $641,874 of mortgages held by third parties and $878,856 of mortgages held by our RAIT I and RAIT II CDO securitizations. Together, along with commercial real estate loans held by RAIT I and RAIT II, these mortgages serve as collateral for the CDO notes payable issued by the RAIT I and RAIT II CDO securitizations. All intercompany balances and interest charges are eliminated in consolidation.

Acquisitions:

During the six-month period ended June 30, 2015, Independence Realty Trust, Inc., or IRT, whom we consolidate, acquired one multi-family property with a purchase price of $25,250. Upon acquisition, we recorded the investment in real estate, including any related working capital and intangible assets, at fair value of $25,250.

17

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

The following table summarizes the aggregate estimated fair value of the assets and liabilities associated with the one property acquired during the six-month period ended June 30, 2015 on the date of acquisition, which is accounted for under FASB ASC Topic 805.

| Description |

Estimated Fair Value |

|||

| Assets acquired: |

||||

| Investments in real estate |

$ | 25,031 | ||

| Other assets |

87 | |||

| Intangible assets |

219 | |||

|

|

|

|||

| Total assets acquired |

25,337 | |||

| Liabilities assumed: |

||||

| Loans payable on real estate |

— | |||

| Accounts payable and accrued expenses |

488 | |||

| Other liabilities |

103 | |||

|

|

|

|||

| Total liabilities assumed |

591 | |||

|

|

|

|||

| Estimated fair value of net assets acquired |

$ | 24,746 | ||

|

|

|

|||

The following table summarizes the consideration transferred to acquire the real estate properties and the amounts of identified assets acquired and liabilities assumed at the respective conversion date:

| Description |

Estimated Fair Value |

|||

| Fair value of consideration transferred: |

||||

| Cash |

$ | 24,808 | ||

| Other considerations |

(62 | ) | ||

|

|

|

|||

| Total fair value of consideration transferred |

$ | 24,746 | ||

|

|

|

|||

During the six-month period ended June 30, 2015, this investment contributed revenue of $597 and a net income allocable to common shares of $240. During the six-month period ended June 30, 2015, we incurred $88 of third-party acquisition-related costs, which is included in general and administrative expense in the accompanying consolidated statements of operations.

18

Table of Contents

RAIT Financial Trust

Notes to Consolidated Financial Statements

As of June 30, 2015

(Unaudited and dollars in thousands, except share and per share amounts)

The table below presents the revenue, net income and earnings per share effect of the acquired property, as reported in our consolidated financial statements and on a pro forma basis as if the acquisition occurred on January 1, 2014. These pro forma results are not necessarily indicative of the results which actually would have occurred if the acquisition had occurred on the first day of the periods presented, nor does the pro forma financial information purport to represent the results of operations for future periods.

| Description |

For the Six-Month Period Ended June 30, 2015 |

For the Six-Month Period Ended June 30, 2014 |

||||||

| Total revenue of real estate property acquired, as reported |

$ | 597 | $ | — | ||||

| Net income (loss) allocable to common shares of real estate property acquired, as reported |

240 | — | ||||||

| Earnings (loss) per share attributable to common shareholders of real estate property acquired |

||||||||

| Basic and diluted—as reported |

0.00 | 0.00 | ||||||

| Pro forma revenue of real estate property acquired (unaudited) |

1,469 | 1,257 | ||||||

| Pro forma net income (loss) allocable to common shares of real estate property acquired (unaudited) |

562 | 424 | ||||||

| Earnings (loss) per share attributable to common shareholders of real estate property acquired |

||||||||

| Basic and diluted—as pro forma (unaudited) |

0.01 | 0.01 | ||||||

During the six-month period ended June 30, 2015, we updated our allocation for a real estate acquisition from a prior period. This resulted in $4,374 being allocated between buildings (decrease) and intangible assets (increase). The cumulative catch up effect of the allocation (based on the different useful lives) was an increase to net income of $56.

Dispositions: