Attached files

| file | filename |

|---|---|

| 8-K - 8-K - RAIT Financial Trust | d794742d8k.htm |

Investor Presentation

September 2014

Cira

Centre,

2929

Arch

Street,

17

th

Floor,

Philadelphia,

PA

19104

|

215.243.9000

|

rait.com

Exhibit 99.1 |

Forward

Looking

Statements,

Non-

GAAP

Financial

Measures

&

Securities

Offering

Disclaimers

2

This

document

and

the

related

presentation

may

contain

forward-looking

statements

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

These

forward-looking

statements

include,

but

are

not

limited

to,

statements

about

RAIT

Financial

Trust’s

(“RAIT”)

plans,

objectives,

expectations

and

intentions

with

respect

to

future

operations,

projected

dividends,

projected

cash

available

for

distribution

(“CAD”),

projected

net

income

,

the

agreement

in

principle

with

the

staff

of

the

Securities

and

Exchange

Commission

(the

“SEC”)

to

resolve

an

investigation

concerning

Taberna

Capital

Management,

LLC

(the

“SEC

Settlement”),

the

possible

effects

of

exiting

the

Taberna

business

and

other

statements

that

are

not

historical

facts.

Forward-looking

statements

are

sometimes

identified

by

the

words

“may”,

“will”,

“should”,

“potential”,

“predict”,

“continue”,

“project”,

“guide”,

or

other

similar

words

or

expressions.

These

forward-looking

statements

are

based

upon

the

current

beliefs

and

expectations

of

RAIT's

management

and

are

inherently

subject

to

significant

business,

economic

and

competitive

uncertainties

and

contingencies,

many

of

which

are

difficult

to

predict

and

generally

not

within

RAIT’s

control.

In

addition,

these

forward-looking

statements

are

subject

to

assumptions

with

respect

to

future

business

strategies

and

decisions

that

are

subject

to

change.

RAIT

does

not

guarantee

that

the

assumptions

underlying

such

forward

looking

statements

are

free

from

errors.

Actual

results

may

differ

materially

from

the

anticipated

results

discussed

in

these

forward-looking

statements.

The

following

factors,

among

others,

could

cause

actual

results

to

differ

materially

from

the

anticipated

results

or

other

expectations

expressed

in

the

forward-looking

statements:

whether

RAIT’s

actual

business

performance,

developments

related

to

its

business,

ability

to

access

the

capital

markets

and

economic

conditions

affecting

commercial

real

estate

will

adversely

effect

RAIT’s

ability

to

realize

the

projections

related

to

our

future

CAD

and

net

income

and

the

underlying

assumptions

or

to

pay

declared

or

expected

future

dividends,

the

risk

that

the

SEC

Settlement

will

not

be

finalized

and/or

approved

or

that

any

final

settlement

will

have

different

or

additional

material

terms

or

have

a

different

impact

on

earnings,

CAD

or

adjusted

book

value;

the

risk

that

RAIT

will

not

be

able

to

commit

to

or

complete

exiting

the

Taberna

business

or

that

the

actual

impact

on

RAIT’s

future

financial

results,

CAD

or

adjusted

book

value

of

any

such

exit

may

differ

materially

from

the

adjustments

reflected

in

the

pro

forma

financial

data

included

in

this

presentation;

and

the

risk

factors

and

other

disclosure

contained

in

filings

by

RAIT

with

the

Securities

and

Exchange

Commission

(“SEC”),

including,

without

limitation,

RAIT’s

most

recent

annual

and

quarterly

reports

filed

with

SEC.

RAIT’s

SEC

filings

are

available

on

RAIT’s

website

at

www.rait.com.

You

are

cautioned

not

to

place

undue

reliance

on

these

forward-looking

statements,

which

speak

only

as

of

the

date

of

this

presentation.

All

subsequent

written

and

oral

forward-looking

statements

attributable

to

RAIT

or

any

person

acting

on

its

behalf

are

expressly

qualified

in

their

entirety

by

the

cautionary

statements

contained

or

referred

to

in

this

document

and

the

related

presentation.

Except

to

the

extent

required

by

applicable

law

or

regulation,

RAIT

undertakes

no

obligation

to

update

these

forward-looking

statements

to

reflect

events

or

circumstances

after

the

date

of

this

presentation

or

to

reflect

the

occurrence

of

unanticipated

events.

This

document

and

the

related

presentation

may

contain

non-U.S.

generally

accepted

accounting

principles

(“GAAP”)

financial

measures.

A

reconciliation

of

these

non-GAAP

financial

measures

to

the

most

directly

comparable

GAAP

financial

measure

is

included

in

this

document

and/or

RAIT’s

most

recent

annual

and

quarterly

reports.

This

presentation

is

for

informational

purposes

only

and

does

not

constitute

an

offer

to

sell

or

a

solicitation

of

an

offer

to

buy

any

securities

of

RAIT

or

Independence

Realty

Trust,

Inc.

(“IRT”)

,

a

RAIT

consolidated

and

managed

multifamily

equity

REIT. |

About RAIT

3

RAIT Financial Trust (“RAIT”) (NYSE: RAS), is a multi-strategy

commercial real estate company with a vertically integrated platform

focused on lending, owning and managing commercial real estate related

assets nationwide. RAIT is organized as an internally-managed

REIT with $5.3 billion of assets under management

RAIT’s IPO -

January 1998

Focus on delivering strong-risk adjusted returns

Scalable, “in-house”, commercial real estate platform with

approximately 700 employees (includes property management)

Offices

-

Philadelphia,

New

York,

Chicago,

Charlotte

RAIT originated $470.8 million of loans during the six-months ended June 30,

2014 consisting of

$288.4

million

bridge

loans,

$165.6

million

conduit

loans

and

$16.8

million

mezzanine

loans

No corporate, unsecured, recourse debt maturities until April 2016

Quarterly

common

dividend

of

$0.18

for

the

third

quarter

2014

-

a

20%

increase

over

the

third

quarter

2013.

Fourth

quarter

2014

dividend

guidance

of

at

least

$0.18

per

share

Seasoned executive team with strong real estate equity and debt experience

|

Multi-Strategy Business Approach

4

COMMERCIAL REAL ESTATE

OWNER & OPERATOR

-

Maximize value over time

-

Opportunistic acquisitions

-

Hedges against inflation

-

Adds stability to the asset mix

COMMERCIAL REAL ESTATE

LENDER

-

One-source financing option to

middle market: originate,

underwrite, close & service

commercial real estate loans

ASSET & PROPERTY MANAGER

-

Full service property manager

-

Asset Manager: S&P &

Morningstar rated primary and

special loan servicer

-

External advisor to

Independence Realty Trust, Inc.

(NYSE MKT: IRT)

Commercial

Real Estate Platform

$5.3 Billion

Assets Under Management

As of June 30, 2014 |

Commercial Real Estate Lender

5

The lending opportunity

Improved

lending

environment

-

economy,

liquid

market,

stronger

borrowers

Over

$1.5

trillion

of

CRE

debt

is

expected

to

mature

through

2019

(1)

Equity gap drives bridge and mezzanine lending opportunities

RAIT’s goal

Capitalize on lending opportunity utilizing existing, scalable platform and

internal expertise to originate and underwrite bridge, mezzanine and

conduit loans of $5 million to $30 million on multi-family, office,

retail and light industrial properties RAIT’s

competitive

advantage:

uniquely

positioned

to

deliver

a

one-source

financing

option

to

our

borrowers

-

short

term,

floating

rate

financing

for

properties

in

transition

to

long

term,

fixed

rate

financing

for

stabilized

properties

Active credit and risk management

(1)

Trepp , LLC |

Commercial Real Estate Lender

6

Loan Types

Bridge

loans

-

balance

sheet

loans:

transitional

properties,

3

to

5

year,

floating

rate

over

LIBOR,

origination

&

exit

fee,

approximate

floor

rates

4.75%

-

7.0%

Conduit

loans

-

for

sale

loans:

stable

properties,

5

to

10

year,

fixed

rate,

approximate

coupon

range

4.50%

-

5.50%

Mezzanine

loans

-

balance

sheet

loans:

stable

properties,

floating

rate,

origination

fees,

approximate

coupon:

10.00%

-12.00%

Funding Sources

Warehouse providers

Bridge loans: Citibank, Column Financial (Credit Suisse AG affiliate), UBS Real

Estate Securities, Inc.

Conduit

loans:

Barclays,

Citibank

-

sell

loans

into

third-party

securitizations

RAIT’s balance sheet

Securitizations

-

RAIT

2013-FL1

-

$135

million

floating

rate

securitization;

RAIT

2014-FL2

-

$196

million

floating

rate

securitization

Capital markets |

Commercial Real Estate Lender

7

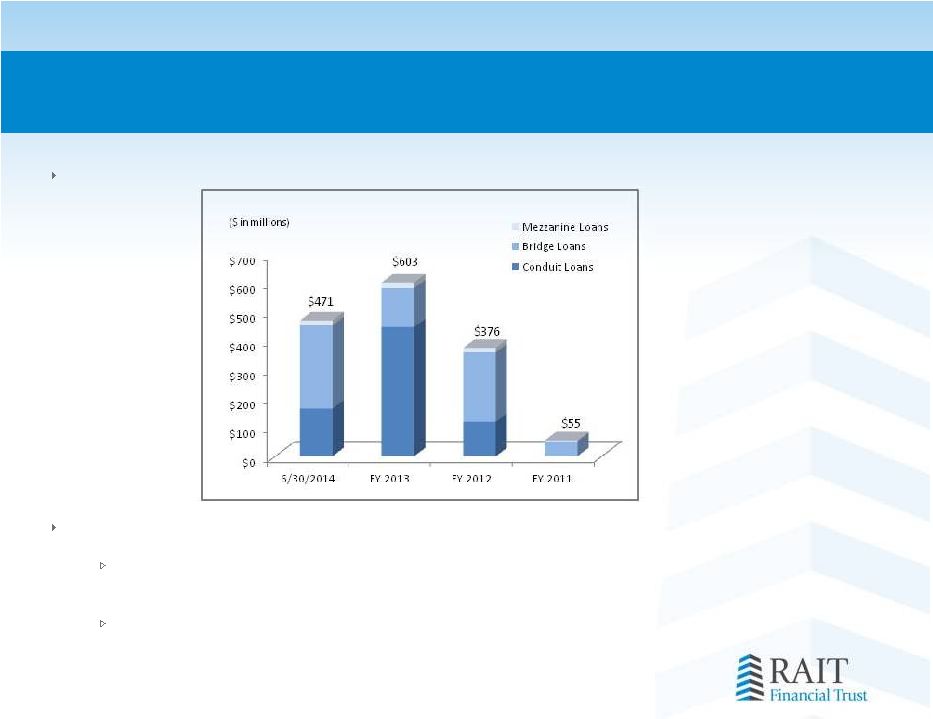

Growth in loan originations

Loan repayments and sales

Average quarterly commercial loan (bridge and mezzanine) repayments of $42.8

million for the six-months ended June 30, 2014

Average quarterly conduit loan sales of $59.7 million for the six-months ended

June 30, 2014

As of June 30, 2014 |

CRE Loan Portfolio Statistics

8

Loan Portfolio Statistics

As of June 30, 2014 unless otherwise Indicated ($ in 000s)

(1) Based on book value at 6/30/2014.

Book Value

Weighted-

Average

Coupon

Range of Maturities

Number of

Loans

Key Statistics

Q2 2014

Q4 2013

Commercial Real Estate (CRE) Loans

CRE Non-accrual loans

$30,269

$37,073

Commercial mortgages

$1,003,051

6.0%

Aug. 2014 to Jul. 2044

85

% change

(18) %

Mezzanine loans

260,320

9.5%

Sep. 2014 to Jan. 2029

80

Reserve for losses

15,336

22,955

Preferred equity interests

41,721

7.7%

May 2015 to Aug. 2025

10

% change

(33) %

Total CRE Loans

$1,305,092

6.8%

175

Provision for losses

1,000

1,500

Other loans

20,204

2.8%

Oct. 2016

1

% change

(33) %

Total investments in loans

$1,325,296

6.7%

176

|

Commercial Real Estate Owner

9

Directly owned real estate portfolio

Strategy to maximize value over time through professional management, increasing

occupancy and higher rental rates

Opportunistic acquisitions

Provides stability to asset mix and hedges against inflation

$1.3 billion of CRE properties at June 30, 2014

Portfolio is internally managed

Acquire well located apartment buildings in secondary markets via Independence

Realty Trust, Inc. (“IRT”) (NYSE MKT: IRT)

IRT owned 19 properties totaling $343.5 million at June 30, 2014

Consolidated by RAIT and externally managed by RAIT subsidiary

RAIT owns approximately 7.3 million shares of IRT common stock

(approximately 28.2% of the outstanding common stock)

IRT utilizes RAIT’s relationships, broker-network & relationships;

off-market transactions

(1)

Includes

nineteen

apartment

buildings

totaling

$343.5

million

owned

by

IRT

as

of

June

30,

2014.

At

July

21,

2014,

RAIT

owned

28.2%

of

IRT’s

outstanding

common

stock.

.

1 |

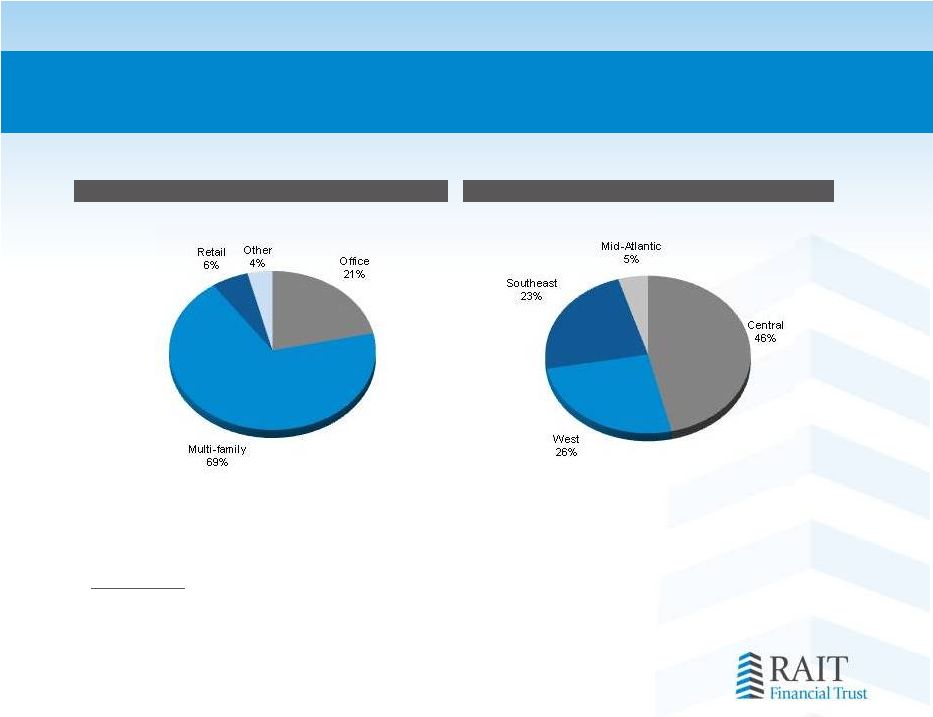

Directly Owned Commercial Real Estate Portfolio

Statistics

10

(a)

Based

on

book

value

of

properties

owned

as

of

June

30,

2014.

.

Investments

in

Real

Estate

Property

Types

(a)

Investments

in

Real

Estate

Geographic

U.S.

Regions

(a

) |

Directly Owned Commercial Real Estate Portfolio

Statistics

11

Net Real Estate Operating Income

(a)

Includes

nineteen

apartment

buildings

owned

by

IRT

with

5,342

units

and

a

book

value

of

$343.5

million

as

of

June

30,

2014.

At

August

5,

2014,

RAIT

owned

28.2%

of

IRT’s

outstanding

common

stock.

(b)

Average

monthly

effective

rent

represents

the

average

monthly

rent

collected

for

all

occupied

units

after

giving

effect

to

tenant

concessions.

We

do

not

report

average

effective

rent

per

unit

in

the

month

of

acquisition

as

it

is

not

representative

of

a

full

month

of

operations.

Based

on

properties

owned

as

of

June

30,

2014.

(c)

Average

effective

rent

is

rent

per

unit

per

month.

(d)

Average

effective

rent

is

rent

per

square

foot

per

year.

Improved Occupancy and Net Operating Income

As of June 30, 2014 unless otherwise Indicated ($ in 000s)

Average

Effective

Rent

(b)

Investments

in Real

Estate

Quantity

Number of

Properties

Average Physical Occupancy

6/30/2014

6/30/2013

Multi-family real estate properties

(a)

$957,858

12,388 units

47

92.8%

92.6%

Office real estate properties

322,477

2,248,321 sq. ft.

13

74.3%

74.3%

Retail real estate properties

84,088

1,420,909 sq. ft.

4

67.5%

68.7%

Parcels of land

50,097

21.9 acres

10

Total

$1,414,520

74

Q2 2014

Q2 2013

Rental income

$39,214

$27,858

Real estate operating expenses

19,690

14,911

Net Real Estate Operating Income

$19,524

$12,947

NOI growth

51%

Property Type

Q2 2014

Q2 2013

% Increase

Multi-family

(c)

$799

$743

8%

Office

(d)

20.10

18.77

7%

Retail

(d)

12.5

11.78

6% |

Asset and Property Manager

12

Asset & Property Management

$5.3 billion of AUM

Management fees

Manage approximately $2.6 billion of commercial real estate assets, $1.5 billion

of U.S. real estate debt securities and property manage $1.2 billion of

commercial real estate for third parties

S&P & Morningstar rated primary and special CRE loan servicer

Property

management

fees

-

RAIT,

IRT

and

3

rd

party

opportunities

Multi-family focused

–

54 properties -

12,683 units

–

17 states

Office focused

Retail focused

–

3.0 million square feet

–

13 states

–

63 properties –

18.2 million square feet

–

25 states |

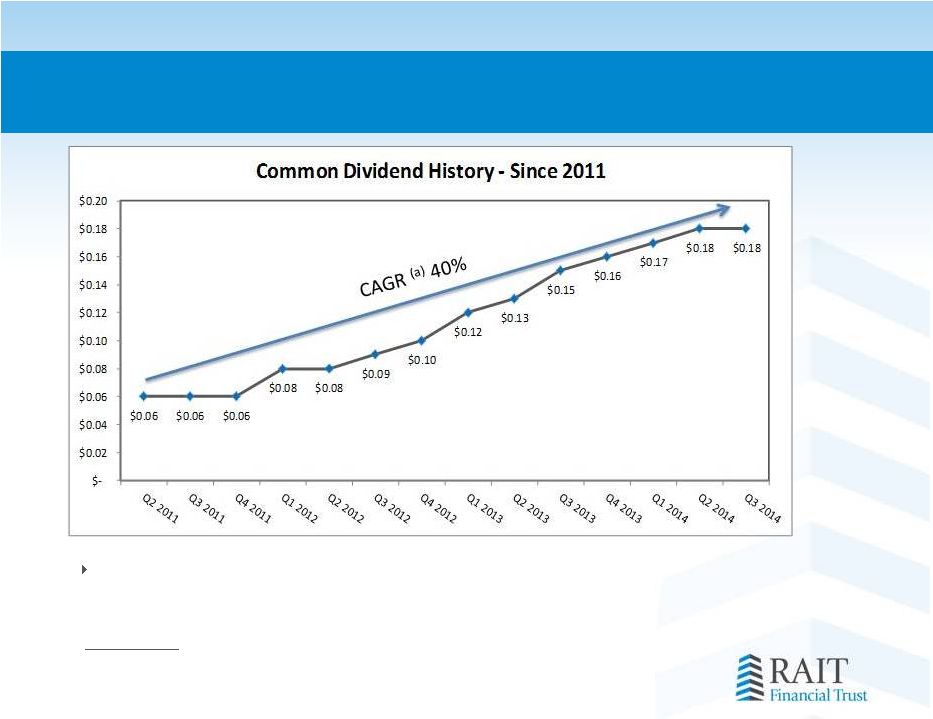

RAS Dividend History –

Since 2011

13

(a)

Compound

Annual

Growth

Rate

.

Stable and steady dividend |

2014 Projected Cash Available for Distribution

(1)

14

(1)

Please

see

slide

17

for

CAD

definition.

(2)

Constitutes

forward-looking

information.

Actual

full

2014

projected

net

income,

cash

available

for

distribution

and

each

individual

line

item

presented

herein

could

vary

significantly

from

the

projections

presented.

Net

income,

CAD

and

each

such

item

may

fluctuate

based

upon

a

variety

of

factors,

including,

but

not

limited

to,

the

timing

and

amount

of

investments,

repayments

and

asset

sales,

capital

raised,

use

of

leverage,

changes

in

the

expected

yield

of

investments

and

the

overall

conditions

in

commercial

real

estate

and

the

economy

generally.

CAD

per

share

does

not

take

into

account

any

potential

dilution

from

our

outstanding

convertible

senior

notes

or

warrants

or

equity

compensation.

The

above

projections

assume

for

2014:

gross

loan

originations

of

$900

million

to

$1.25

billion;

Investment

portfolios

do

not

experience

significant

loan

repayments;

RAIT’s

property

portfolio

performs

at

historical

levels;

RAIT

continues

to

receive

its

securitization

collateral

management

and

property

management

fees

and

RAIT

will

take

a

one-time,

$21.5

million

settlement

charge

to

GAAP

earnings

and

cash

available

for

distribution

(“CAD”)

in

the

quarter

ended

September

30,

2014.

(3)

Represents

projected

net

income

(loss)

allocable

to

common

shares

for

2014

excluding

the

changes

in

fair

value

of

financial

instruments.

For

the

six-months

ended

June

30,

2014,

changes

in

fair

value

of

financial

instruments

was

a

loss

of

$63.5

million

and

net

income

allocable

to

common

shares

was

a

loss

of

$40.2

million.

Includes

the

one-time

$21.5

million

settlement

charge

RAIT

will

take

in

the

quarter

ended

September

30,

2014.

(4)

Based

on

80,636,895

weighted-average

shares

outstanding-diluted

for

the

six-month

period

ended

June

30,

2014.

Reconciliation of RAIT Annualized Projected Cash Available for Distribution ("CAD")

(dollars in millions, except per share data)

2014 Annualized Projected CAD

(2)

Net Income (loss) allocable to common shares

(3)

$ 1.2

-

$ 7.2

Adjustments:

Depreciation, amortization expense and other items

78.6

-

78.6

Taberna VIII and Taberna IX securitizations, net effect

(28.2)

-

(28.2)

Loan origination fees

5.6

-

7.6

CAD

$ 57.2

-

$ 65.2

CAD per share

(4)

$ 0.71

-

$ 0.81

|

RAIT Highlights & Goals

15

Growth & stability through a multi-strategy approach

Utilizing RAIT’s core, integrated, real estate platform and management

expertise to generate appropriate risk-adjusted returns by originating,

underwriting and managing commercial real estate loans

Creating value in RAIT’s portfolio of owned real estate through increasing

rental and occupancy rates while managing operating costs through

RAIT’s property managers Expanding and maintaining our sources of

liquidity Maintaining a strong pipeline of investment opportunities

Delivering stable and growing dividends

Growing revenue through accretive capital deployment

Focus on bridge and conduit loans

Growing IRT’s portfolio of apartment properties

|

16

Appendix |

Cash Available for Distribution

(1)

17

(1)

Cash

available

for

distribution,

or

CAD,

is

a

non-GAAP

financial

measure.

We

believe

that

CAD

provides

investors

and

management

with

a

meaningful

indicator

of

operating

performance.

Management

also

uses

CAD,

among

other

measures,

to

evaluate

profitability

and

our

board

of

trustees

considers

CAD

in

determining

our

quarterly

cash

distributions.

We

also

believe

that

CAD

is

useful

because

it

adjusts

for

a

variety

of

noncash

items

(such

as

depreciation

and

amortization,

equity-based

compensation,

realized

gain

(loss)

on

assets,

provision

for

loan

losses

and

non-cash

interest

income

and

expense

items).

Furthermore,

CAD

removes

the

effect

from

our

consolidation

of

the

legacy

Taberna

securitizations.

We

calculate

CAD

by

subtracting

from

or

adding

to

net

income

(loss)

attributable

to

common

shareholders

the

following

items:

depreciation

and

amortization

items

including,

depreciation

and

amortization,

straight-line

rental

income

or

expense,

amortization

of

in

place

leases,

amortization

of

deferred

financing

costs,

amortization

of

discount

on

financings

and

equity-based

compensation;

changes

in

the

fair

value

of

our

financial

instruments,

including

such

changes

reflected

in

our

consolidated

Taberna

securitizations;

net

interest

income

from

consolidated

Taberna

securitizations;

realized

gain

(loss)

on

assets

and

other;

provision

for

loan

losses;

impairment

on

depreciable

property;

acquisition

gains

or

losses

and

transaction

costs;

certain

fee

income

eliminated

in

consolidation

that

is

attributable

to

third

parties;

and

one-time

events

pursuant

to

changes

in

U.S.

GAAP

and

certain

other

non-recurring

items.

CAD

should

not

be

considered

as

an

alternative

to

net

income

(loss),

determined

in

accordance

with

U.S.

GAAP,

as

an

indicator

of

operating

performance.

In

addition,

our

methodology

for

calculating

CAD

may

differ

from

the

methodologies

used

by

other

comparable

companies,

including

other

REITs,

when

calculating

the

same

or

similar

supplemental

financial

measures

and

may

not

be

comparable

with

these

companies.

(2)

Based

on

81,778,947

and

80,636,895

weighted-average

shares

outstanding-diluted

for

the

three-month

period

and

six-month

period

ended

June

30,

2014.

(3)

Based

on

69,757,807and

65,086,432

weighted-average

shares

outstanding-diluted

for

the

three-month

period

and

six-month

period

ended

June

30,

2013.

(All $ in 000s except per share numbers)

For the Three-Month Period Ended

June 30,

For the Six-Month Period Ended

June 30,

2014

2013

2014

2013

Amount

Per Share

(2)

Amount

Per Share

(3)

Amount

Per Share

(2)

Amount

Per Share

(3)

Cash Available for Distribution:

Net income (loss) allocable to common shares ..........................

$(25,650)

$ (0.31)

$(65,877)

$(0.94)

$(40,237)

$ (0.50)

$(156,409)

$(2.40)

Adjustments:

Depreciation and amortization expense .........................

13,441

0.16

8,618

0.12

25,483

0.32

17,188

0.26

Change in fair value of financial instruments ..................

25,071

0.32

76,020

1.09

49,210

0.61

175,777

2.69

(Gains) losses on assets

.................................................

7,599

0.09

(224)

0.00

5,375

0.07

(221)

0.00

(Gains) losses on extinguishment of debt .......................

-

-

-

-

(2,421)

(0.03)

-

-

Taberna VIII and Taberna IX securitizations, net effect .

(7,028)

(0.09)

(9,526)

(0.14)

(14,088)

(0.18)

(18,002)

(0.28)

Straight-line rental adjustments ......................................

24

0.00

(678)

(0.01)

(91)

0.00

(966)

(0.01)

Share-based compensation ............................................

1,180

0.01

743

0.01

2,629

0.03

1,466

0.02

Origination fees and other deferred items ......................

5,181

0.06

2,300

0.03

9,732

0.12

2,978

0.05

Provision for losses .........................................................

1,000

0.01

500

0.01

2,000

0.03

1,000

0.02

Noncontrolling interest effect from certain adjustments..

(1,095)

(0.01)

(9)

0.00

(635)

(0.01)

(9)

0.00

Cash Available for Distribution ....................................................

$19,723

$0.24

$11,867

$0.17

$36,957

$0.46

$22,802

$0.35

|

$-

$-

$34,066

$-

$141,750

$70,000

$-

$-

$-

$-

$60,000

$43,771

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

2014 (1)

2015 (1)

2016 (2)

2017 (3)

2018 (2) (3)

2019 (3)

2020

2021

2022

2023

2024 (4)

Thereafter

Unsecured Recourse Debt Maturities and Redemption Dates

(in 000s)

Unsecured Recourse Debt Summary

18

No corporate, unsecured, recourse debt maturities until April 2016

(1)

Excludes

$76.9

million

of

secured

debt

outstanding

under

RAIT’s

CMBS

and

commercial

mortgage

facilities

with

contractual

maturities

in

2015

&

2016.

(2)

Assumes

full

exercise

of

holders’

7.0%

&

4.0%

convertible

senior

notes

redemption

right

in

April

2016

and

October

2018,

respectively,

and

excludes

$12.1

million

outstanding

under

secured

credit

facilities

with

contractual

maturities

in

2016

related

to

Independence

Realty

Trust,

Inc.

(3)

Includes

$70.0

million

of

senior

unsecured

notes

issued

in

August

2014.

Excludes

$82.0

million

of

outstanding

senior

secured

notes

issued

by

us

which

are

eliminated

in

consolidation

with

contractual

maturities

ranging

from

2017

to

2019.

(4)

Includes

$60.0

million

of

senior

unsecured

notes

issued

in

April

2014.

As of June 30, 2014 |

Key Statistics –

6.30.2014

19

(All $ in 000s except per share numbers)

(a)

CRE Loan Portfolio includes commercial mortgages, mezzanine loans, and preferred equity

interests only and does not include other loans. (b)

Includes 19 apartment properties owned by IRT with 5,342 units and a book value of $343.5

million as of June 30, 2014. (c)

Based on properties owned as of June 30, 2014.

(d)

Average effective rent is rent per unit per month.

(e)

Average effective rent is rent per square foot per year.

As of or For the Three-Month Periods Ended June 30,

2014

March 31,

2014

December 31,

2013

September 30,

2013

June 30,

2013

Financial Statistics:

Total revenue .............................................................

$

73,256

$

67,308

$

67,607

$

62,395

$

58,622

Earnings (loss) per share, diluted ...............................

$

(0.31)

$

(0.18)

$

(1.90)

$

(0.24)

$

(0.94)

Cash available for distribution per share, diluted ......

$

0.24

$

0.22

$

0.27

$

0.23

$

0.17

Common dividend declared per share .......................

$

0.18

$

0.17

$

0.16

$

0.15

$

0.13

Assets under management

.........................................

$

5,266,296

$

5,119,805

$

3,595,530

$

3,567,675

$

3,616,009

Funds from operations per share, diluted ..................

$

(0.20)

$

(0.07)

$

(1.74)

$

(0.12)

$

(0.81)

Commercial Real Estate (“CRE”) Loan Portfolio (a):

Reported CRE Loans—unpaid principal ......................

$

1,325,748

$

1,228,452

$

1,115,949

$

1,103,272

$

1,154,306

Non-accrual loans—unpaid principal .........................

$

30,269

$

28,019

$

37,073

$

45,337

$

65,597

Non-accrual loans as a % of reported loans ...............

2.3%

2.3%

3.3%

4.1%

5.7%

Reserve for losses .......................................................

$

15,336

$

14,279

$

22,955

$

23,317

$

24,222

Reserves as a % of non-accrual loans .........................

50.7%

51.0%

61.9%

51.4%

36.9%

Provision for losses

.....................................................

$

1,000

$

1,000

$

1,500

$

500

$

500

CRE Property Portfolio:

Reported investments in real estate, net (b)

..............

$

1,268,769

$

1,205,995

$

1,004,186

$

986,296

$

949,649

Net operating income.................................................

$

19,524

$

17,093

$

13,919

$

13,712

$

12,947

Number of properties owned (b) ...............................

74

71

62

61

60

Multifamily units owned (b) .......................................

12,388

12,014

9,372

8,940

8,535

Office square feet owned ...........................................

2,248,321

2,097,022

2,009,852

2,015,524

2,015,576

Retail square feet owned ...........................................

1,420,909

1,420,909

1,421,059

1,421,059

1,421,059

Acres of land owned ...................................................

21.92

21.92

21.92

21.92

21.92

Average physical occupancy data:

..............................

Multifamily properties .....................................

92.8%

93.3%

92.2%

92.5%

92.6%

Office properties

..............................................

74.3%

74.8%

75.6%

74.1%

74.3%

Retail properties ..............................................

67.5%

66.6%

69.0%

68.9%

68.7%

Average effective rent per unit/square foot (c) .........

Multifamily (d) .................................................

$

799

$

767

$

763

$

761

$

743

Office (e) ..........................................................

$

20.10

$

18.70

$

18.40

$

19.45

$

18.77

Retail (e)

...........................................................

$

12.50

$

12.44

$

12.11

$

12.05

$

11.78

|

RAIT Income Statement

20

(All $ in 000s except per share numbers)

For the Three-Month

Periods Ended June 30

For the Six-Month

Periods Ended June 30

2014 2013 2014 2013 Revenue:

Investment interest income ......................................

$

34,646

$

31,256

$

69,609

$

62,536

Investment interest expense ....................................

(7,523)

(7,278)

(14,706)

(14,761)

Net interest margin .............................................................

27,123

23,978

54,903

47,775

Rental income ...........................................................

39,214

27,858

74,390

55,027

Fee and other income ...............................................

6,919

6,786

11,271

14,071

Total revenue ......................................................................

73,256

58,622

140,564

116,873

Expenses:

Interest expense .......................................................

13,241

9,978

24,846

19,644

Real estate operating expense

..................................

19,690

14,911

37,773

29,321

Compensation expense

.............................................

7,376

6,337

15,931

13,284

General and administrative expense ........................

4,874

3,562

9,075

7,338

Provision for losses ...................................................

1,000

500

2,000

1,000

Depreciation and amortization expense

...................

13,441

8,618

25,483

17,188

Total expenses

.....................................................................

59,622

43,906

115,108

87,775

Operating Income ............................................................

13,634

14,716

25,456

29,098

Other income (expense) ...........................................

5

69

15

145

Gains (losses) on assets

.............................................

(7,599)

224

(5,375)

221

Gains (losses) on extinguishment of debt .................

0

—

2,421

—

Change in fair value of financial instruments ............

(25,071)

(76,020)

(49,210)

(175,777)

Income (loss) before taxes ...............................................

(19,031)

(61,011)

(26,693)

(146,313)

Income tax benefit (provision)

..................................

21

673

260

634

Net income (loss) .............................................................

(19,010)

(60,338)

(26,433)

(145,679)

(Income) loss allocated to preferred shares ........................

(7,415)

(5,589)

(13,221)

(10,807)

(Income) loss allocated to noncontrolling interests ............

775

50

(583)

77

Net income (loss) allocable to common shares .................

$

(25,650)

$

(65,877)

$

(40,237)

$

(156,409)

Earnings (loss) per share—Basic:

Earnings (loss) per share—Basic ...............................

$

(0.31)

$

(0.94)

$

(0.50)

$

(2.40)

Weighted-average shares outstanding—Basic ....................

81,778,947

69,757,807

80,636,895

65,086,432

Earnings (loss) per share—Diluted:

Earnings (loss) per share—Diluted....................

$

(0.31)

$

(0.94)

$

(0.50)

$

(2.40)

Weighted-average shares outstanding—Diluted ................

81,778,947

69,757,807

80,636,895

65,086,432

ib

|

RAIT Balance Sheet

21

(All $ in 000s except per share numbers)

As of

June 30,

2014 As of

December 31,

2013 Assets

Investments in mortgages and loans, at amortized cost:

Commercial mortgages, mezzanine loans, other loans and preferred equity

interests………………………… $

1,323,677

$

1,122,377

Allowance for

losses……………………………………………………………………………………………………………………………

(15,336)

(22,955)

Total investments in mortgages and

loans…………………………………………………………………………………………..

1,308,341

1,099,422

Investments in real estate, net of accumulated depreciation of $145,751 and $127,745,

respectively . 1,268,769

1,004,186

Investments in securities and security-related receivables, at fair

value………………………………………………

574,178

567,302

Cash and cash

equivalents……………………………………………………………………………………………………………………

75,079

88,847

Restricted

cash…………………………………………………………………………………………………………………………………….

102,189

121,589

Accrued interest

receivable…………………………………………………………………………………………………………………

52,857

48,324

Other

assets………………………………………………………………………………………………………………………………………..

72,165

57,081

Deferred financing costs, net of accumulated amortization of $21,484 and $17,768,

respectively……... 22,469

18,932

Intangible assets, net of accumulated amortization of $8,960 and $4,564,

respectively………………………. 23,100

21,554

Total

assets…………………………………………………………………………………………………………………………..

$

3,499,147

$

3,027,237

Liabilities and Equity

Indebtedness ($425,927 and $389,146 at fair value,

respectively)………………………………………………………

$

2,417,170

$

2,086,401

Accrued interest

payable…………………………………………………………………………………………………………………….

31,177

26,936

Accounts payable and accrued

expenses…………………………………………………………………………………………….

28,683

32,447

Derivative

liabilities……………………………………………………………………………………………………………………………..

95,974

113,331

Deferred taxes, borrowers’ escrows and other

liabilities……………………………………………………………………..

128,665

79,462

Total

liabilities………………………………………………………………………………………………………………………..

2,701,669

2,338,577

Series D cumulative redeemable preferred shares, $0.01 par value per share, 4,000,000 shares

authorized, 4,000,000 and 2,600,000 shares issued and outstanding,

respectively…………………………………………...

74,723

52,970

Equity:

Shareholders’ equity:

Preferred shares, $0.01 par value per share, 25,000,000 shares authorized;

7.75% Series A cumulative redeemable preferred shares, liquidation preference $25.00 per

share, 8,069,288 and 4,760,000 shares authorized, respectively, 4,069,288 shares issued

and outstanding……………………. 41

41

8.375% Series B cumulative redeemable preferred shares, liquidation preference $25.00 per

share, 4,300,000 shares authorized, 2,288,465 shares issued and

outstanding…………………………………………………………

23

23

8.875% Series C cumulative redeemable preferred shares, liquidation preference $25.00 per

share, 3,600,000 shares authorized, 1,640,100 shares issued and

outstanding…………………………………………………………

17

17

Series E cumulative redeemable preferred shares, $0.01 par value per share, 4,000,000 shares

authorized 0

0

Common shares, $0.03 par value per share, 200,000,000 shares authorized, 82,507,410 and

71,447,437 issued and outstanding, respectively, including 541,825 and 369,500 unvested

restricted common share awards,

respectively…………………………………………………………………………………………………………………………………..

2,474

2,143

Additional paid in

capital…………………………………………………………………………………………………………………….

2,007,593

1,920,455

Accumulated other comprehensive income

(loss)……………………………………………………………………………….

(50,226)

(63,810)

Retained earnings

(deficit)…………………………………………………………………………………………………………………..

(1,326,186)

(1,257,306)

Total shareholders’

equity…………………………………………………………………………………………………………………..

633,736

601,563

Noncontrolling

interests………………………………………………………………………………………………………………………

89,019

34,127

Total

equity…………………………………………………………………………………………………………………………..

722,755

635,690

Total liabilities and

equity…………………………………………………………………………………………………….. $

3,499,147

$

3,027,237

|

Adjusted Book Value

(1)

22

(1)

Management

views

adjusted

book

value

as

a

useful

and

appropriate

supplement

to

shareholders’

equity

and

book

value

per

share.

The

measure

serves

as

an

additional

measure

of

our

value

because

it

facilitates

evaluation

of

us

without

the

effects

of

various

items

that

we

are

required

to

record

in

accordance

with

GAAP

but

which

have

limited

economic

impact

on

our

business.

Those

adjustments

primarily

reflect

the

effect

of

consolidated

securitizations

where

we

do

not

currently

receive

cash

flows

on

our

retained

interests,

accumulated

depreciation

and

amortization,

the

valuation

of

long-

term derivative instruments and a valuation of our recurring collateral and property management

fees. Adjusted book value is a non-GAAP financial measurement, and does not purport to be an

alternative

to

reported

shareholders’

equity,

determined

in

accordance

with

GAAP,

as

a

measure

of

book

value.

Adjusted

book

value

should

be

reviewed

in

connection

with

shareholders’

equity

as

set

forth in our consolidated balance sheets, to help analyze our value to investors. Adjusted book

value may be defined in various ways throughout the REIT industry. Investors should consider these

differences when comparing our adjusted book value to that of other REITs.

(2)

Based on 82,507,410 common shares outstanding as of June 30, 2014.

(3)

Based

on

4,069,288

Series

A

preferred

shares,

2,288,465

Series

B

preferred

shares,

and

1,640,100

Series

C

preferred

shares

outstanding

as

of

June

30,

2014,

all

of

which

have

a

liquidation

preference

o

f $25.00 per share.

(All $ in 000s except per share numbers)

As of June 30, 2014

Amount Per Share (2)

Total shareholders’ equity ................................................

$

633,736

$

7.68

Liquidation value of preferred shares characterized as equity(3)

(199,946)

(2.42)

Book value ........................................................................

433,790

5.26

Adjustments:

Taberna VIII and Taberna IX securitizations, net effect

(187,864)

(2.29)

RAIT I and RAIT II derivative liabilities .....................

31,102

0.38

Change in fair value for warrants and investor SARs

18,820

0.23

Accumulated depreciation and amortization .........

183,932

2.23

Valuation of recurring collateral and property management fees

57,479

0.70

Total adjustments .............................................................

103,469

1.25

Adjusted book value .........................................................

$

537,259

$

6.51

|

23

Pro-forma Financial Data: Assuming Taberna

Deconsolidation

Primary assumptions:

(1)The removal of the previously consolidated assets, liabilities and impact on

shareholders’

equity of the Taberna securitizations.

(2)The reflection of collateral management fees for the consolidated Taberna

securitizations previously eliminated in consolidation.

(3)See footnotes to each chart for additional assumptions. |

Pro-Forma RAIT Income Statement –

June 30, 2014

24

(All $ in 000s except per share numbers)

(a)

RAIT

is

undertaking

to

exit

the

Taberna

business.

RAIT

expects

that

any

such

exit

will

require

RAIT

to

deconsolidate

the

assets,

liabilities

and

impact

on

shareholders’

equity

of

RAIT’s

consolidated

Taberna

securitizations:

Taberna

VIII

and

IX.

These

adjustments

reflect

the

removal

of

the

revenue,

expenses,

gains

and

losses

and

changes

in

fair

value

derived

from

these

items

from

our

results

of

operations

for

the

six-months

ended

June

30,2014.

These

adjustments

reflect

the

collateral

management

fees

for

the

consolidated

Taberna

securitizations

previously

eliminated

inconsolidation

and

do

notassume

thesale

or

other

transfer

of

the

collateral

management

agreements

associated

withany

Taberna

securitizations.

For the Six-Month Period Ended June 30, 2014

Historical

Adjustments (a)

Pro Forma

Revenue:

Investment interest income

.................................................... $

69,609

$

(15,344)

$

54,265

Investment interest expense.

.................................................. (14,706)

4,458

(10,248)

Net interest margin

......................................................................

54,903

(10,886)

44,017

Rental income

........................................................................

74,390

-

74,390

Fee and other income

.............................................................

11,271

635

11,906

Total revenue

...............................................................................

140,564

(10,251)

130,313

Expenses:

Interest expense

.....................................................................

24,846

6,381

31,227

Real estate operating expense

................................................ 37,773

-

37,773

Compensation expense

..........................................................

15,931

-

15,931

General and administrative expense

...................................... 9,075

(387)

8,688

Provision for losses

................................................................

2,000

-

2,000

Depreciation and amortization expense

................................. 25,483

-

25,483

Total expenses

.............................................................................

115,108

5,994

121,102

Operating income (loss)

............................................................

25,456

(16,245)

9,211

Other income (expense)

......................................................... 15

-

15

Gains (losses) on assets

......................................................... (5,375)

7,712

2,337

Gains (losses) on extinguishment of debt

.............................. 2,421

-

2,421

Change in fair value of financial instruments

........................ (49,210)

52,357

3,147

Income (loss) before taxes

......................................................... (26,693)

43,824

17,131

Income tax benefit (provision)

...............................................

260

-

260

Net income (loss)

........................................................................

(26,433)

43,824

17,391

(Income) loss allocated to preferred shares

........................... (13,221)

-

(13,221)

(Income) loss allocated to noncontrolling interests

............... (583)

-

(583)

Net income (loss) allocable to common shares

........................ $

(40,237)

$

43,824

$

3,587

Earnings (loss) per share - Basic:

Earnings (loss) per share – Basic

........................................... $

(0.50)

$

0.54

$

0.04

Weighted-average shares outstanding – Basic

............................ 80,636,895

80,636,895

80,636,895

Earnings (loss) per share - Diluted:

Earnings (loss) per share – Diluted

........................................ $

(0.50)

$

0.54

$

0.04

Weighted-average shares outstanding – Diluted

......................... 80,636,895

80,636,895

80,636,895

|

Pro-Forma RAIT Income Statement –

Fiscal Year

2013

25

(All $ in 000s except per share numbers)

(a)

RAIT

is

undertaking

to

exit

the

Taberna

business.

RAIT

expects

that

any

such

exit

will

require

RAIT

to

deconsolidate

the

assets,

liabilities

and

impact

on

shareholders’

equity

of

RAIT’s

consolidated

Taberna

securitizations:

Taberna

VIIIand

IX.

These

adjustments

reflect

the

removal of the revenue, expenses, gains and losses and changes in fair value derived

from these items from our results of operations for the six-months ended June 30,

2014. These adjustments reflect the collateral management fees for the consolidated Taberna

securitizations

previously

eliminated

in

consolidation

and

do

not

assume

the

sale

or

other

transfer

of

the

collateral

management

agreements associated with any Taberna securitizations.

For the Year Ended December 31, 2013

Historical

Adjustments (a)

Pro Forma

Revenue:

Investment interest income

............................................................................................

$

134,447

$

(34,399)

$

100,048

Investment interest expense

...........................................................................................

(30,595)

9,579

(21,016)

Net interest margin

..............................................................................................................

103,852

(24,820)

79,032

Rental income

................................................................................................................

114,224

-

114,224

Fee and other income

.....................................................................................................

28,799

1,200

29,999

Total revenue

.................................................................................................................

246,875

(23,620)

223,255

Expenses:

Interest expense

.............................................................................................................

40,297

13,712

54,009

Real estate operating expense.

.......................................................................................

60,887

-

60,887

Compensation expense

..................................................................................................

26,802

-

26,802

General and administrative expense..

............................................................................

14,893

(737)

14,156

Provision for losses.

.......................................................................................................

3,000

-

3,000

Depreciation and amortization expense..

.......................................................................

36,093

-

36,093

Total expenses.

....................................................................................................................

181,972

12,975

194,947

Operating income (loss).

...................................................................................................

64,903

(36,595)

28,308

Other income (expense)

.................................................................................................

(5,233)

-

(5,233)

Gains (losses) on

assets..................................................................................................

(2,266)

90

(2,176)

Gains (losses) on extinguishment of debt.

.....................................................................

(1,275)

-

(1,275)

Change in fair value of financial instruments..

..............................................................

(344,426)

323,938

(20,488)

Income (loss) before taxes.

................................................................................................

(288,297)

287,433

(864)

Income tax benefit (provision)

.......................................................................................

2,933

-

2,933

Net income (loss)

................................................................................................................

(285,364)

287,433

2,069

(Income) loss allocated to preferred shares

...................................................................

(22,616)

-

(22,616)

(Income) loss allocated to noncontrolling interests

......................................................

(28)

-

(28)

Net income (loss) allocable to common shares.

...............................................................

$

(308,008)

$

287,433

$

(20,575)

Earnings (loss) per share - Basic:

Earnings (loss) per share - Basic

....................................................................................

$

(4.54)

$

4.24

$

(0.30)

Weighted-average shares outstanding - Basic.

....................................................................

67,814,316

67,814,316

67,814,316

Earnings (loss) per share - Diluted:

Earnings (loss) per share – Diluted

............................................................................... .

$

(4.54)

$

4.24

$

(0.30)

Weighted-average shares outstanding – Diluted

.................................................................

67,814,316

67,814,316

67,814,316

|

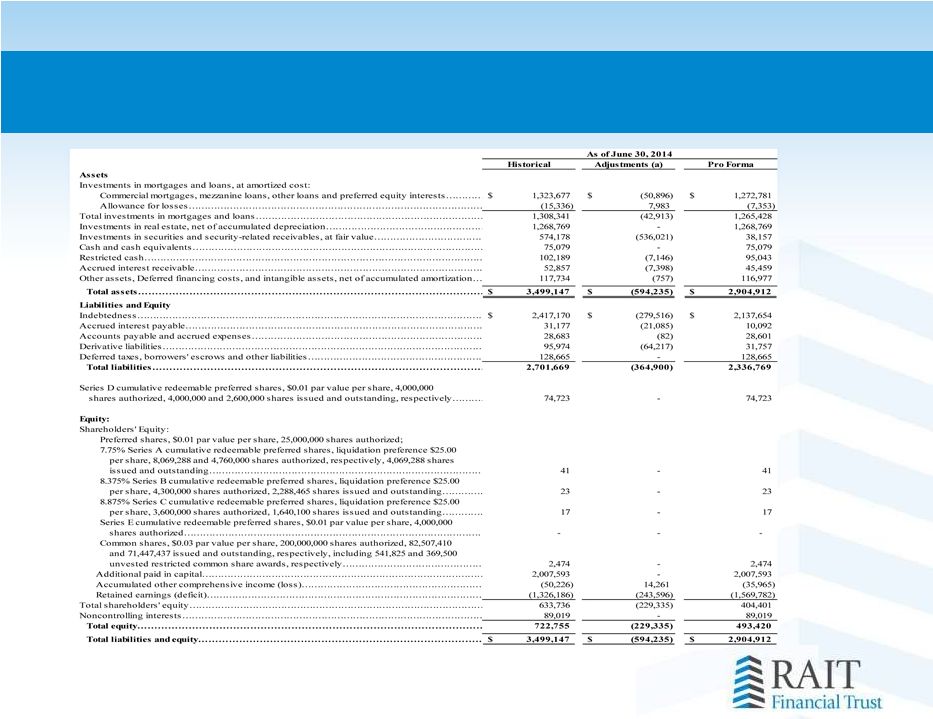

Pro-Forma RAIT Balance Sheet

26

(All $ in 000s except per share numbers)

(a)

RAIT

is

undertaking

to

exit

the

Taberna

business.

RAIT

expects

that

any

such

exit

will

require

RAIT

to

deconsolidate

the

assets,

liabilities

and

impact

on

shareholders’

equity

of

RAIT’s

consolidated

Taberna

securitizations:

Taberna

VIII

and

IX.

These

adjustments

reflect

the

removal

of

these

items

from

our

consolidated

balance

sheet

as

of

June

30,

2014.

These

adjustments

do

not

assume

the

sale

or

other

transfer

of

the

collateral

management agreements

associated with any Taberna securitizations. |

Updated Pro-Forma RAIT Adjusted Book Value

(1)

27

(1)

Management

views

adjusted

book

value

as

a

useful

and

appropriate

supplement

to

shareholders’

equity

and

book

value

per

share.

The

measure

serves

as

an

additional

measure

of

our

value

because

it

facilitates

evaluation

of

us

without

the

effects

of

various

items

that

we

are

required

to

record

in

accordance

with

GAAP

but

which

have

limited

economic

impact

on

our

business.

Those

adjustments

primarily

reflect

the

effect

of

consolidated

securitizations

where

we

do

not

currently

receive

cash

flows

on

our

retained

interests,

accumulated

depreciation

and

amortization,

the

valuation

of

long-

term derivative instruments and a valuation of our recurring collateral and property management

fees. Adjusted book value is a non-GAAP financial measurement, and does not purport to be an

alternative

to

reported

shareholders’

equity,

determined

in

accordance

with

GAAP,

as

a

measure

of

book

value.

Adjusted

book

value

should

be

reviewed

in

connection

with

shareholders’

equity

as

set

forth in our consolidated balance sheets, to help analyze our value to investors. Adjusted book

value may be defined in various ways throughout the REIT industry. Investors should consider these

differences when comparing our adjusted book value to that of other REITs.

(2)

Includes

adjustments

at

June

30,

2014

and

footnotes

(6)

and

(7)

describe

the

pro-forma

effect

of

certain

events

subsequent

to

June

30,

2014.

(3)

Based on 82,507,410 common shares outstanding as of June 30, 2014.

(4)

RAIT

is

undertaking

to

exit

the

Taberna

business.

RAIT

expects

that

any

such

exit

will

require

RAIT

to

deconsolidate

the

assets,

liabilities

and

impact

on

shareholders’

equity

of

RAIT’s

consolidated

Taberna

securitizations:

Taberna

VIII

and

IX.

See

slide

#26

for

pro-forma

balance

sheet.

The

$21.5

million

charge

RAIT

recorded

during

the

third

quarter

of

2014

for

the

SEC

Settlement

is

not

reflected

in

pro-forma

total

shareholders’

equity

but

is

reflected

as

an

adjustment

(see

footnote

7).

Does

not

assume

the

sale

or

other

transfer

of

the

collateral

management

agreements

associated

with

any

Taberna securitizations.

(5)

Based

on

4,069,288

Series

A

preferred

shares,

2,288,465

Series

B

preferred

shares,

and

1,640,100

Series

C

preferred

shares

outstanding

as

of

June

30,

2014,

all

of

which

have

a

liquidation

preference

of

$25.00 per share.

(6)

Includes

the

estimated

value

of

the

(1)

property

management

and

collateral

management

fees

to

be

received

by

RAIT

as

of

June

30,

2014

from

RAIT

Residential

and

Urban

Retail,

and

the

Taberna

I,

Taberna

VIII,

Taberna

IX,

RAIT

I

and

RAIT

II

securitizations

and

(2)

advisory

fees

to

be

received

by

RAIT

from

IRT

as

of

September

23,

2014

assuming

the

full

deployment

of

IRT’s

July

2014

common

stock

offering.

The

other

item

included

is

the

incremental

market

value

of

RAIT’s

ownership

of

7.3

million

shares

of

IRT

common

stock

over

RAIT’s

book

value

for

these

shares

at

September

16,

2014.

(7)

Includes

the

announced

$21.5

million

SEC

Settlement

charge

taken

in

the

third

quarter

of

2014.

(All $ in 000s except per share numbers)

As of June 30, 2014

(2)

Amount Per Share (3)

Pro forma total shareholders’ equity (4)

........................................................ $

404,401

$

4.90

Liquidation value of preferred shares characterized as equity (5) ........

(199,946)

(2.42)

Book value

.......................................................................................................

204,455

2.48

Adjustments (2):

RAIT I and RAIT II derivative liabilities

................................................... 31,102

0.38

Change in fair value for warrants and investor SARs ............................

18,820

0.23

Accumulated depreciation and amortization ........................................

183,932

2.23

Valuation of recurring collateral, property management fees & other

items (6)

............................................................................................

96,808

1.17

SEC settlement charge (7)

..................................................................... (21,500)

(0.26)

Total adjustments

...........................................................................................

309,162

3.75

Adjusted book value

.......................................................................................

$

513,617

$

6.23

|

Pro-Forma Cash Available for Distribution

(1)

28

(1)

Cash

available

for

distribution,

or

CAD,

is

a

non-GAAP

financial

measure.

We

believe

that

CAD

provides

investors

and

management

with

a

meaningful

indicator

of

operating

performance.

Management

also

uses

CAD,

among

other

measures,

to

evaluate

profitability

and

our

board

of

trustees

considers

CAD

in

determining

our

quarterly

cash

distributions.

We

also

believe

that

CAD

is

useful

because

it

adjusts

for

a

variety

of

noncash

items

(such

as

depreciation

and

amortization,

equity-based

compensation,

realized

gain

(loss)

on

assets,

provision

for

loan

losses

and

non-cash

interest

income

and

expense

items).

Furthermore,

CAD

removes

the

effect

from

our

consolidation

of

the

legacy

Taberna

securitizations.

We

calculate

CAD

by

subtracting

from

or

adding

to

net

income

(loss)

attributable

to

common

shareholders

the

following

items:

depreciation

and

amortization

items

including,

depreciation

and

amortization,

straight-line

rental

income

or

expense,

amortization

of

in

place

leases,

amortization

of

deferred

financing

costs,

amortization

of

discount

on

financings

and

equity-based

compensation;

changes

in

the

fair

value

of

our

financial

instruments,

including

such

changes

reflected

in

our

consolidated

Taberna

securitizations;

net

interest

income

from

consolidated

Taberna

securitizations;

realized

gain

(loss)

on

assets

and

other;

provision

for

loan

losses;

impairment

on

depreciable

property;

acquisition

gains

or

losses

and

transaction

costs;

certain

fee

income

eliminated

in

consolidation

that

is

attributable

to

third

parties;

and

one-time

events

pursuant

to

changes

in

U.S.

GAAP

and

certain

other

non-recurring

items.

CAD

should

not

be

considered

as

an

alternative

to

net

income

(loss),

determined

in

accordance

with

U.S.

GAAP,

as

an

indicator

of

operating

performance.

In

addition,

our

methodology

for

calculating

CAD

may

differ

from

the

methodologies

used

by

other

comparable

companies,

including

other

REITs,

when

calculating

the

same

or

similar

supplemental

financial

measures

and

may

not

be

comparable

with

these

companies.

(2)

RAIT

is

undertaking

to

exit

the

Taberna

business.

These

pro-forma

adjustments

remove

the

effect

of

the

assets,

liabilities

and

impact

on

sharheolders’

equity

of

RAIT’s

consolidated

securitizations;

Taberna VIII and IX. See slide #25 for the calculation of the pro-forma net income

(loss) allocable to common shares. This pro-forma CAD does not assume the sale or other transfer of the collateral

management contracts for RAIT’s managed Taberna securitizations: Taberna I, VIII

and IX. The collateral management fees for Taberna I, VIII and IX totaled $1.1 million for the six-months ended June

30, 2014 or approximately $0.01 per common share.

(3)

Based 80,636,895 weighted-average shares outstanding-diluted for the six-month

period ended June 30, 2014. (4)

Cash

available

for

distribution

for

the

six-months

ended

June

30,

2014,

as

reported

and

pro

forma,

does

not

reflect

the

impact

of

the

$21.5

million

charge

recorded