Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DFC GLOBAL CORP. | d735910d8k.htm |

|

|

CONFIDENTIAL

|

|

Forward-Looking Statements

This presentation contains forward-looking statements, including, among other things, statements regarding the following: the Company’s future results, growth, guidance and operating strategy; the global economy; the effects of currency exchange rates and fluctuations in the price of gold on reported operating results; the regulatory environment in Canada, the United Kingdom, the United States, Scandinavia and other countries; the impact of future development strategy, new stores and acquisitions; litigation matters; financing initiatives; and the performance of new products and services. These forward-looking statements involve risks and uncertainties, including risks related to: approval of the transaction by the Company’s stockholders (or the failure to obtain such approval), the ability to obtain regulatory approvals for the transaction, the Company’s ability to maintain relationships with customers and employees following the announcement of the transaction, the ability of third parties to fulfill their commitments relating to the transaction, including providing financing, the ability of the parties to satisfy the closing conditions, and the risk that the transaction may not be completed in the anticipated time frame or at all; the regulatory environments of the jurisdictions in which we do business, including reviews of our operations principally by the CFPB in the United States and the Financial Conduct Authority in the United Kingdom, and other changes in laws affecting how we do business and the regulatory bodies which govern us; current and potential future litigation; the identification of acquisition targets; the integration and performance of acquired stores and businesses; the performance of new stores and internet businesses; the impact of debt and equity financing transactions; the results of certain ongoing income tax appeals; the effects of new products and services, or changes to our existing products and services, on the Company’s business, results of operations, financial condition, prospects and guidance; and uncertainties related to the effects of changes in the value of the U.S. Dollar compared to foreign currencies. There can be no assurance that the Company will attain its expected results, successfully integrate and achieve anticipated synergies from any of its acquisitions, obtain acceptable financing, or attain its published guidance metrics, or that ongoing and potential future litigation or the various U.S. Federal or state, U.K., or other foreign legislative or regulatory activities affecting the Company or the banks with which the Company does business will not negatively impact the Company’s operations. A more complete description of these and other risks, uncertainties and assumptions is included in the Company’s filings with the Securities and Exchange Commission, including those described under the heading “Risk Factors” in the Company’s Annual Report on Form 10-K for the Company’s fiscal year ended June 30, 2013, as amended in its Form 10-Q for the quarter ended December 31, 2013 and in its Form 10-Q for the quarter ended March 31, 2014. You should not place any undue reliance on any forward-looking statements. The Company disclaims any obligation to update any such factors or to publicly announce results of any revisions to any of the forward-looking statements contained herein to reflect future events or developments.

CONFIDENTIAL 1

|

|

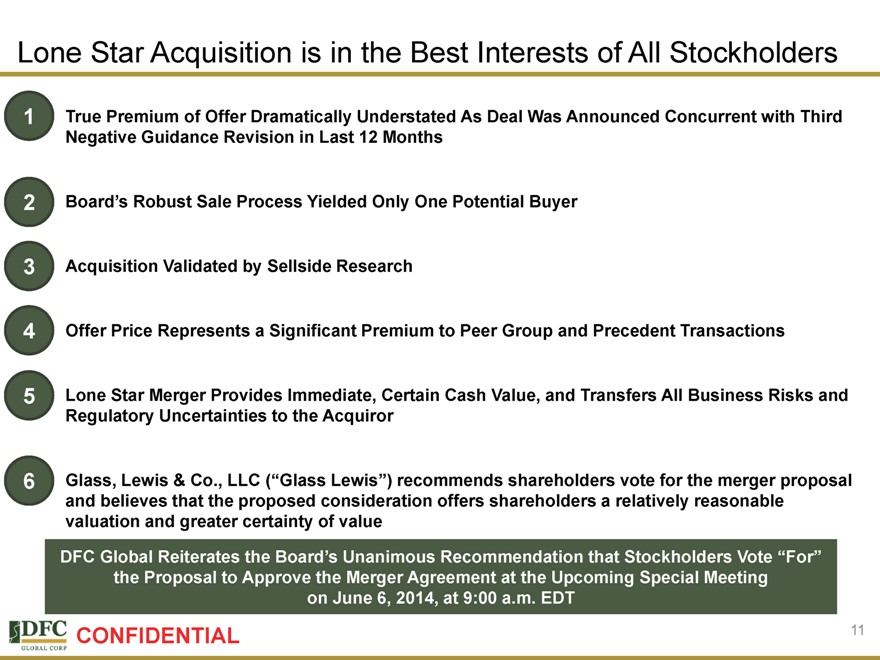

Lone Star Acquisition is in the Best Interests of All Stockholders

1 True Premium of Offer Dramatically Understated As Deal Was Announced Concurrent with Third

Negative Guidance Revision in Last 12 Months

2 Board’s Robust Sale Process Yielded Only One Potential Buyer

3 Acquisition Validated by Sellside Research

4 Offer Price Represents a Significant Premium to Peer Group and Precedent Transactions

5 Lone Star Merger Provides Immediate, Certain Cash Value, and Transfers All Business Risks and

Regulatory Uncertainties to the Acquiror

6 Glass, Lewis & Co., LLC (“Glass Lewis”) recommends shareholders vote for the merger proposal

and believes that the proposed consideration offers shareholders a relatively reasonable

valuation and greater certainty of value

DFC Global Reiterates the Board’s Unanimous Recommendation that Stockholders Vote “For” the Proposal to Approve the Merger Agreement at the Upcoming Special Meeting on June 6, 2014, at 9:00 a.m. EDT

CONFIDENTIAL 2

|

|

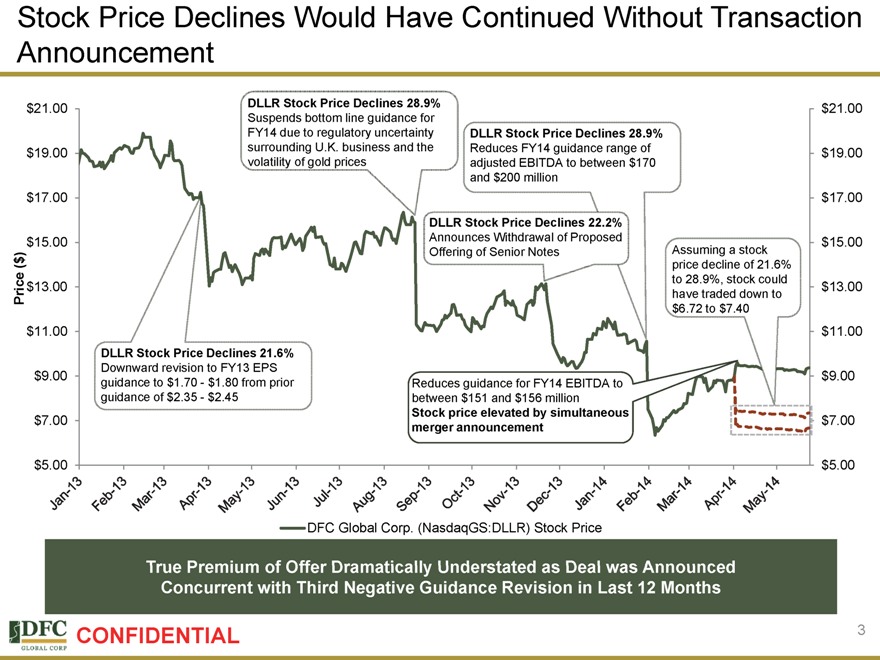

Stock Price Declines Would Have Continued Without Transaction Announcement

$21.00 DLLR Stock Price Declines 28.9% $21.00

Suspends bottom line guidance for

FY14 due to regulatory uncertainty DLLR Stock Price Declines 28.9%

$19.00 surrounding U.K. business and the Reduces FY14 guidance range of $19.00

volatility of gold prices adjusted EBITDA to between $170

and $200 million

$17.00 $17.00

DLLR Stock Price Declines 22.2%

$15.00 Announces Withdrawal of Proposed $15.00

Offering of Senior Notes Assuming a stock

($)

price decline of 21.6%

e to 28.9%, stock could

$13.00 $13.00

Pric have traded down to

$6.72 to $7.40

$11.00 $11.00

DLLR Stock Price Declines 21.6%

Downward revision to FY13 EPS

$9.00 $9.00

guidance to $ 1.70 - $1.80 from prior Reduces guidance for FY14 EBITDA to

guidance of $ 2.35 - $2.45 between $151 and $156 million

Stock price elevated by simultaneous

$7.00 $7.00

merger announcement

$5.00 $5.00

DFC Global Corp. (NasdaqGS:DLLR) Stock Price

True Premium of Offer Dramatically Understated as Deal was Announced Concurrent with Third Negative Guidance Revision in Last 12 Months

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14

CONFIDENTIAL 3

|

|

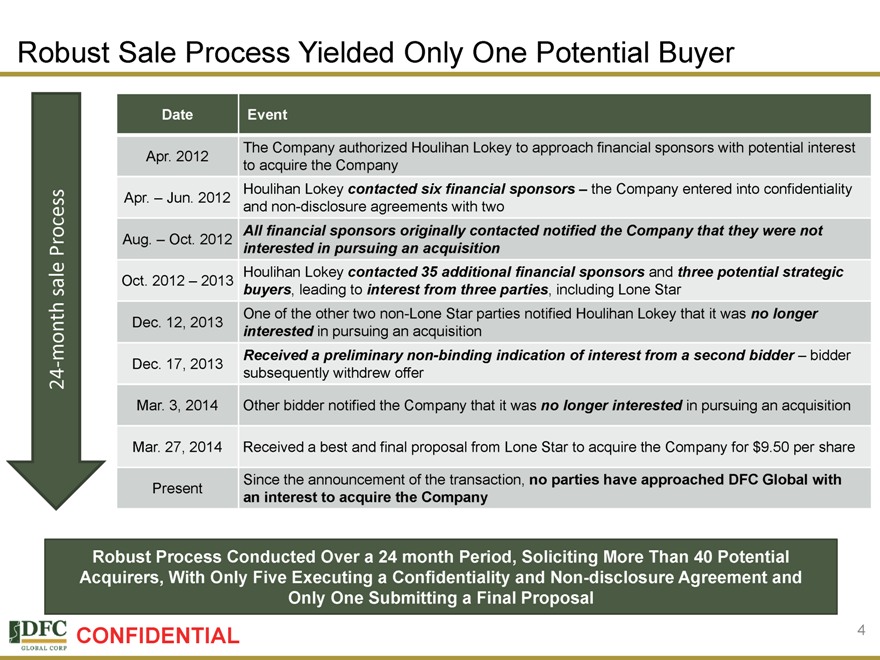

Robust Sale Process Yielded Only One Potential Buyer

Date Event

Apr. 2012 The Company authorized Houlihan Lokey to approach financial sponsors with potential interest

to acquire the Company

Apr. – Jun. 2012 Houlihan Lokey contacted six financial sponsors the Company entered into confidentiality

and non-disclosure agreements with two

Aug. – Oct. 2012 All financial sponsors originally contacted notified the Company that they were not

interested in pursuing an acquisition

Oct. 2012 – 2013 Houlihan Lokey contacted 35 additional financial sponsors and three potential strategic

buyers, leading to interest from three parties, including Lone Star

One of the other two non-Lone Star parties notified Houlihan Lokey that it was no longer

Dec. 12, 2013 interested in pursuing an acquisition

24 month sale process

Received a preliminary non-binding indication of interest from a second bidder – bidder

Dec. 17, 2013 subsequently withdrew offer

Mar. 3, 2014 Other bidder notified the Company that it was no longer interested in pursuing an acquisition

Mar. 27, 2014 Received a best and final proposal from Lone Star to acquire the Company for $9.50 per share

Present Since the announcement of the transaction, no parties have approached DFC Global with

an interest to acquire the Company

Robust Process Conducted Over a 24 month Period, Soliciting More Than 40 Potential Acquirers, With Only Five Executing a Confidentiality and Non-disclosure Agreement and Only One Submitting a Final Proposal

CONFIDENTIAL 4

|

|

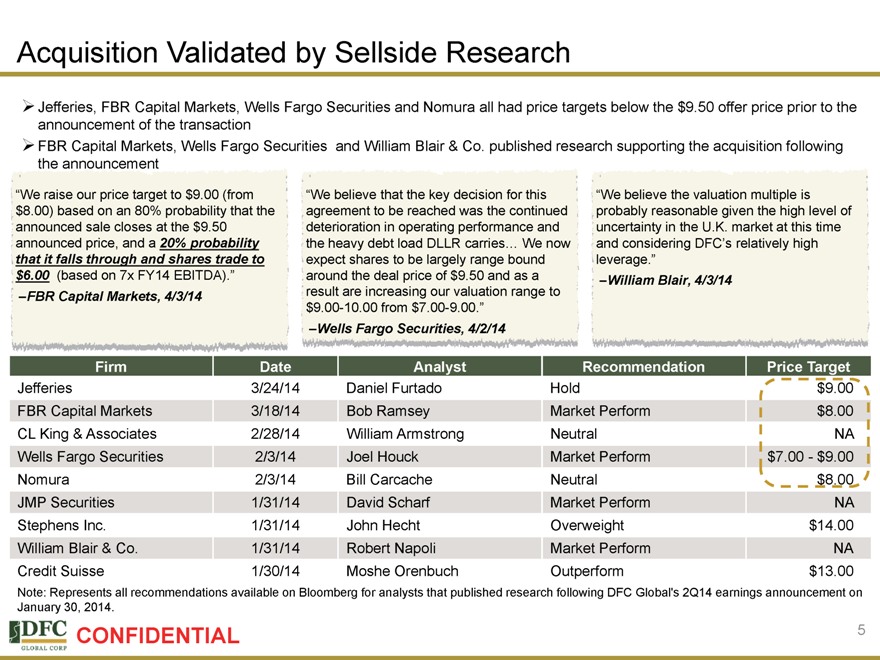

Acquisition Validated by Sellside Research

Jefferies, FBR Capital Markets, Wells Fargo Securities and Nomura all had price targets below the $9.50 offer price prior to the announcement of the transaction FBR Capital Markets, Wells Fargo Securities and William Blair & Co. published research supporting the acquisition following the announcement

“We raise our price target to $9.00 (from $8.00) based on an 80% probability that the announced sale closes at the $9.50 announced price, and a 20% probability that it falls through and shares trade to $6.00 (based on 7x FY14 EBITDA).”

–FBR Capital Markets, 4/3/14

“We believe that the key decision for this agreement to be reached was the continued deterioration in operating performance and the heavy debt load DLLR carries… We now expect shares to be largely range bound around the deal price of $9.50 and as a result are increasing our valuation range to $9.00-10.00 from $7.00-9.00.”

–Wells Fargo Securities, 4/2/14

“We believe the valuation multiple is probably reasonable given the high level of uncertainty in the U.K. market at this time and considering DFC’s relatively high leverage.”

–William Blair, 4/3/14

Firm Date Analyst Recommendation Price Target

Jefferies 3/24/14 Daniel Furtado Hold $9.00 FBR Capital Markets 3/18/14 Bob Ramsey Market Perform $8.00 CL King & Associates 2/28/14 William Armstrong Neutral NA Wells Fargo Securities 2/3/14 Joel Houck Market Perform $7.00-$9.00 Nomura 2/3/14 Bill Carcache Neutral $8.00 JMP Securities 1/31/14 David Scharf Market Perform NA Stephens Inc. 1/31/14 John Hecht Overweight $14.00 William Blair & Co. 1/31/14 Robert Napoli Market Perform NA Credit Suisse 1/30/14 Moshe Orenbuch Outperform $13.00

Note: Represents all recommendations available on Bloomberg for analysts that published research following DFC Global’s 2Q14 earnings announcement on January 30, 2014.

CONFIDENTIAL 5

|

|

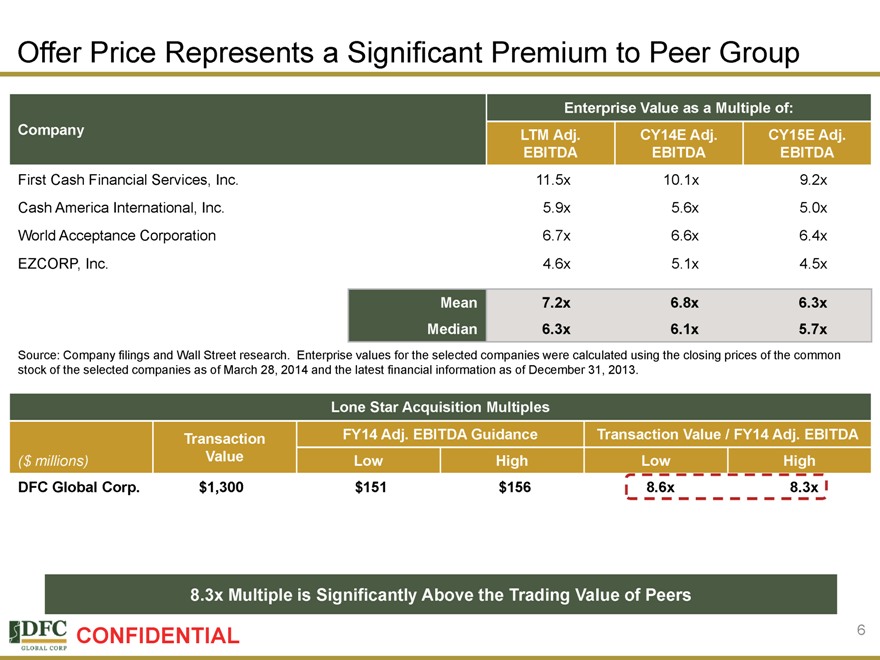

Offer Price Represents a Significant Premium to Peer Group

Enterprise Value as a Multiple of:

Company LTM Adj. CY14E Adj. CY15E Adj.

EBITDA EBITDA EBITDA

First Cash Financial Services, Inc. 11.5x 10.1x 9.2x

Cash America International, Inc. 5.9x 5.6x 5.0x

World Acceptance Corporation 6.7x 6.6x 6.4x

EZCORP, Inc. 4.6x 5.1x 4.5x

Mean 7.2x 6.8x 6.3x

Median 6.3x 6.1x 5.7x

Source: Company filings and Wall Street research. Enterprise values for the selected companies were calculated using the closing prices of the common stock of the selected companies as of March 28, 2014 and the latest financial information as of December 31, 2013.

Lone Star Acquisition Multiples

Transaction FY14 Adj. EBITDA Guidance Transaction Value / FY14 Adj. EBITDA

($ millions) Value Low High Low High

DFC Global Corp. $1,300 $151 $156 8.6x 8.3x

8.3x Multiple is Significantly Above the Trading Value of Peers

CONFIDENTIAL 6

|

|

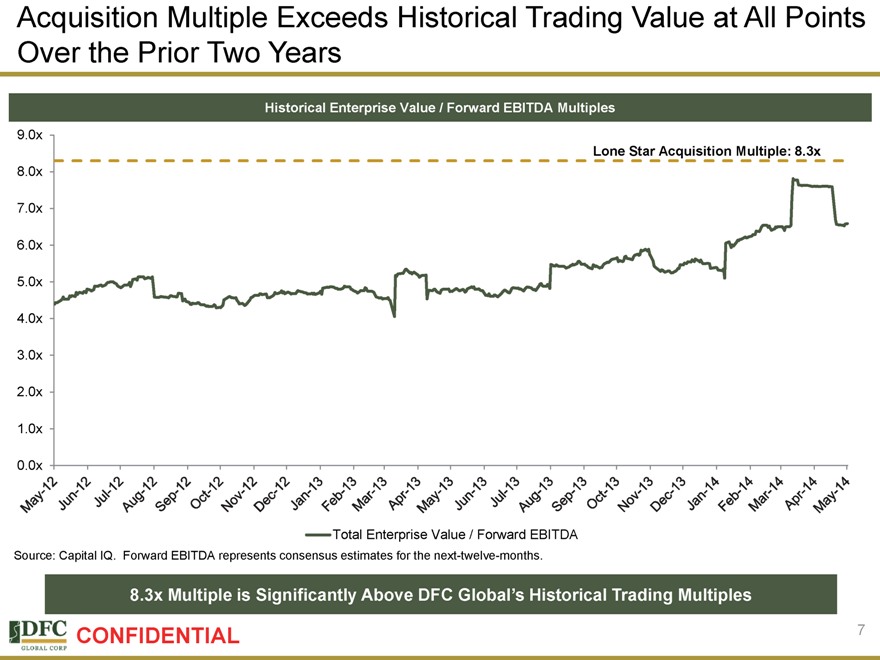

Acquisition Multiple Exceeds Historical Trading Value at All Points Over the Prior Two Years

Historical Enterprise Value / Forward EBITDA Multiples

9.0x

Lone Star Acquisition Multiple: 8.3x

8.0x

7.0x

6.0x

5.0x

4.0x

3.0x

2.0x

1.0x

0.0x

Total Enterprise Value / Forward EBITDA

Source: Capital IQ. Forward EBITDA represents consensus estimates for the next-twelve-months.

8.3x Multiple is Significantly Above DFC Global’s Historical Trading Multiples

May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14

CONFIDENTIAL 7

|

|

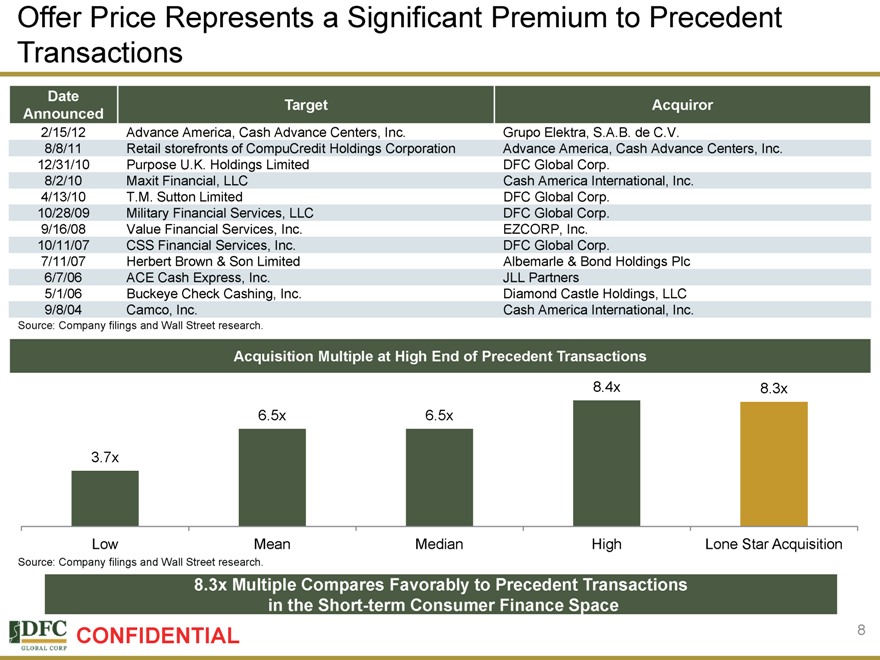

Offer Price Represents a Significant Premium to Precedent Transactions

Date Target Acquiror

Announced

2/15/12 Advance America, Cash Advance Centers, Inc. Grupo Elektra, S.A.B. de C.V.

8/8/11 Retail storefronts of CompuCredit Holdings Corporation Advance America, Cash Advance Centers, Inc.

12/31/10 Purpose U.K. Holdings Limited DFC Global Corp.

8/2/10 Maxit Financial, LLC Cash America International, Inc.

4/13/10 T.M. Sutton Limited DFC Global Corp.

10/28/09 Military Financial Services, LLC DFC Global Corp.

9/16/08 Value Financial Services, Inc. EZCORP, Inc.

10/11/07 CSS Financial Services, Inc. DFC Global Corp.

7/11/07 Herbert Brown & Son Limited Albemarle & Bond Holdings Plc

6/7/06 ACE Cash Express, Inc. JLL Partners

5/1/06 Buckeye Check Cashing, Inc. Diamond Castle Holdings, LLC

9/8/04 Camco, Inc. Cash America International, Inc.

Source: Company filings and Wall Street research.

Acquisition Multiple at High End of Precedent Transactions

8.4x 8.3x

6.5x 6.5x

3.7x

Low Mean Median High Lone Star Acquisition

Source: Company filings and Wall Street research.

8.3x Multiple Compares Favorably to Precedent Transactions in the Short-term Consumer Finance Space

CONFIDENTIAL 8

|

|

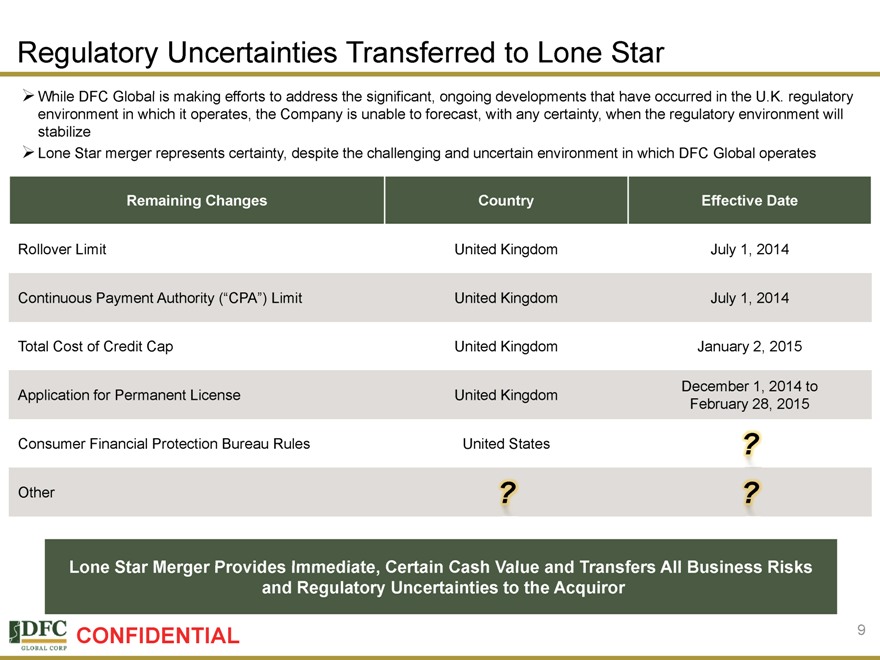

Regulatory Uncertainties Transferred to Lone Star

While DFC Global is making efforts to address the significant, ongoing developments that have occurred in the U.K. regulatory environment in which it operates, the Company is unable to forecast, with any certainty, when the regulatory environment will stabilize Lone Star merger represents certainty, despite the challenging and uncertain environment in which DFC Global operates

Remaining Changes Country Effective Date

Rollover Limit United Kingdom July 1, 2014

Continuous Payment Authority (“CPA”) Limit United Kingdom July 1, 2014

Total Cost of Credit Cap United Kingdom January 2, 2015

Application for Permanent License United Kingdom December 1, 2014 to

February 28, 2015

Consumer Financial Protection Bureau Rules United States ?

Other ? ?

Lone Star Merger Provides Immediate, Certain Cash Value and Transfers All Business Risks and Regulatory Uncertainties to the Acquiror

CONFIDENTIAL 9

|

|

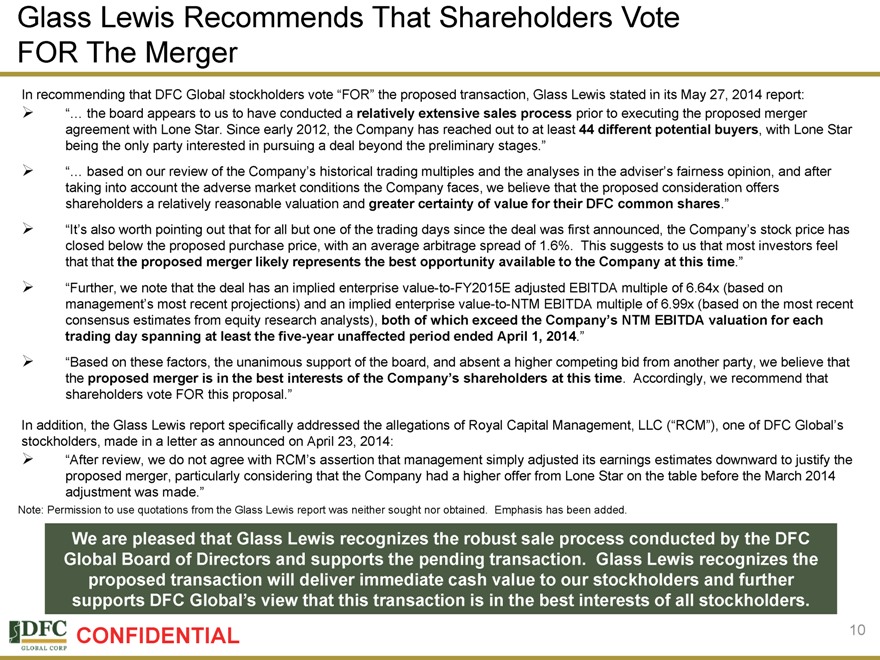

Glass Lewis Recommends That Shareholders Vote FOR The Merger

In recommending that DFC Global stockholders vote “FOR” the proposed transaction, Glass Lewis stated in its May 27, 2014 report: “… the board appears to us to have conducted a relatively extensive sales process prior to executing the proposed merger agreement with Lone Star. Since early 2012, the Company has reached out to at least 44 different potential buyers, with Lone Star being the only party interested in pursuing a deal beyond the preliminary stages.” “… based on our review of the Company’s historical trading multiples and the analyses in the adviser’s fairness opinion, and after taking into account the adverse market conditions the Company faces, we believe that the proposed consideration offers shareholders a relatively reasonable valuation and greater certainty of value for their DFC common shares.”

“It’s also worth pointing out that for all but one of the trading days since the deal was first announced, the Company’s stock price has closed below the proposed purchase price, with an average arbitrage spread of 1.6%. This suggests to us that most investors feel that that the proposed merger likely represents the best opportunity available to the Company at this time.”

“Further, we note that the deal has an implied enterprise value-to-FY2015E adjusted EBITDA multiple of 6.64x (based on management’s most recent projections) and an implied enterprise value-to-NTM EBITDA multiple of 6.99x (based on the most recent consensus estimates from equity research analysts), both of which exceed the Company’s NTM EBITDA valuation for each trading day spanning at least the five-year unaffected period ended April 1, 2014.”

“Based on these factors, the unanimous support of the board, and absent a higher competing bid from another party, we believe that the proposed merger is in the best interests of the Company’s shareholders at this time. Accordingly, we recommend that shareholders vote FOR this proposal.”

In addition, the Glass Lewis report specifically addressed the allegations of Royal Capital Management, LLC (“RCM”), one of DFC Global’s stockholders, made in a letter as announced on April 23, 2014: “After review, we do not agree with RCM’s assertion that management simply adjusted its earnings estimates downward to justify the proposed merger, particularly considering that the Company had a higher offer from Lone Star on the table before the March 2014 adjustment was made.”

Note: Permission to use quotations from the Glass Lewis report was neither sought nor obtained. Emphasis has been added.

We are pleased that Glass Lewis recognizes the robust sale process conducted by the DFC Global Board of Directors and supports the pending transaction. Glass Lewis recognizes the proposed transaction will deliver immediate cash value to our stockholders and further supports DFC Global’s view that this transaction is in the best interests of all stockholders.

CONFIDENTIAL 10

|

|

Lone Star Acquisition is in the Best Interests of All Stockholders

1 True Premium of Offer Dramatically Understated As Deal Was Announced Concurrent with Third

Negative Guidance Revision in Last 12 Months

2 Board’s Robust Sale Process Yielded Only One Potential Buyer

3 Acquisition Validated by Sellside Research

4 Offer Price Represents a Significant Premium to Peer Group and Precedent Transactions

5 Lone Star Merger Provides Immediate, Certain Cash Value, and Transfers All Business Risks and

Regulatory Uncertainties to the Acquiror

6 Glass, Lewis & Co., LLC (“Glass Lewis”) recommends shareholders vote for the merger proposal

and believes that the proposed consideration offers shareholders a relatively reasonable

valuation and greater certainty of value

DFC Global Reiterates the Board’s Unanimous Recommendation that Stockholders Vote “For” the Proposal to Approve the Merger Agreement at the Upcoming Special Meeting on June 6, 2014, at 9:00 a.m. EDT

CONFIDENTIAL 11

|

|

Additional Information and Where to Find It

In connection with the proposed transaction, DFC Global has filed a proxy statement with the SEC. The definitive proxy statement and a form of proxy has been mailed to the stockholders of DFC Global. BEFORE MAKING A VOTING DECISION, DFC GLOBAL’S SECURITY HOLDERS ARE URGED TO READ THE PROXY STATEMENT BECAUSE IT CONTAINS IMPORTANT INFORMATION. DFC Global’s stockholders and other interested parties may obtain, without charge, a copy of the proxy statement and other relevant documents filed with the SEC from the SEC’s website at www.sec.gov. DFC Global’s stockholders and other interested parties may also obtain, without charge, a copy of the proxy statement and other relevant documents by going to the Investors section of DFC Global’s corporate website, www.dfcglobalcorp.com, or directing a request by mail or telephone to DFC Global Corp., 1436 Lancaster Avenue, Berwyn, Pennsylvania 19312.

DFC Global and its directors and officers may be deemed to be participants in the solicitation of proxies from DFC Global’s stockholders with respect to the special meeting of stockholders that will be held to consider the proposed transaction. Information about DFC Global’s directors and executive officers and their ownership of DFC Global’s common stock is set forth in the proxy statement for the Company’s 2013 annual meeting of stockholders, which was filed with the SEC on October 7, 2013 and the Company’s Annual Report on Form 10-K for 2013 filed with the SEC on August 29, 2013. Stockholders may obtain additional information regarding the interests of DFC Global and its directors and executive officers in the proposed merger, which may be different than those of the Company’s stockholders generally, by reading the proxy statement and other relevant documents regarding the proposed merger, when filed with the SEC.

CONFIDENTIAL 12