Attached files

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-32924

GREEN PLAINS RENEWABLE ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Iowa | 84-1652107 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 9420 Underwood Avenue, Suite 100 Omaha, NE 68114 | (402) 884-8700 | |

| (Address of principal executive offices, including zip code) | (Registrant’s telephone number, including area code) | |

Securities registered pursuant to Section 12(b) of the Act: Common Stock, $.001 par value

Name of exchanges on which registered: NASDAQ Stock Market

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the Company’s voting common stock held by non-affiliates of the registrant as of June 30, 2010 (the last business day of the second quarter), based on the last sale price of the common stock on that date of $10.22, was approximately $165.7 million. For purposes of this calculation, executive officers, directors and holders of 10% or more of the registrant’s common stock are deemed to be affiliates of the registrant.

As of March 1, 2011, there were 36,101,888 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2011 Annual Meeting of Shareholders are incorporated by reference in Part III herein. The Company intends to file such Proxy Statement with the Securities and Exchange Commission no later than 120 days after the end of the period covered by this report on Form 10-K.

Table of Contents

Table of Contents

Cautionary Information Regarding Forward-Looking Statements

The SEC encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This report contains such “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be made directly in this report, and they may also be made a part of this report by reference to other documents filed with the SEC, which is known as “incorporation by reference.”

This report contains forward-looking statements based on current expectations that involve a number of risks and uncertainties. Forward-looking statements generally do not relate strictly to historical or current facts, but rather to plans and objectives for future operations based upon management’s reasonable estimates of future results or trends, and include statements preceded by, followed by, or that include words such as “anticipates,” “believes,” “continue,” “estimates,” “expects,” “intends,” “outlook,” “plans,” “predicts,” “may,” “could,” “should,” “will,” and words and phrases of similar impact, and include, but are not limited to, statements regarding future operating or financial performance, business strategy, business environment, key trends, and benefits of actual or planned acquisitions. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Although we believe that our expectations regarding future events are based on reasonable assumptions, any or all forward-looking statements in this report may turn out to be incorrect. They may be based on inaccurate assumptions or may not account for known or unknown risks and uncertainties. Consequently, no forward-looking statement is guaranteed, and actual future results may vary materially from the results expressed or implied in our forward-looking statements. The cautionary statements in this report expressly qualify all of our forward-looking statements. In addition, we are not obligated, and do not intend, to update any of our forward-looking statements at any time unless an update is required by applicable securities laws. Factors that could cause actual results to differ from those expressed or implied in the forward-looking statements include, but are not limited to, those discussed in the section entitled “Risk Factors” in this report or in any document incorporated by reference. Specifically, we may experience significant fluctuations in future operating results due to a number of economic conditions, including, but not limited to, competition in the ethanol and other industries in which we compete, commodity market risks, financial market risks, counter-party risks, risks associated with changes to federal policy or regulation, risks related to closing and achieving anticipated results from acquisitions, and other risk factors detailed in our reports filed with the SEC. Actual results may differ from projected results due, but not limited, to unforeseen developments.

In light of these assumptions, risks and uncertainties, the results and events discussed in the forward-looking statements contained in this report or in any document incorporated by reference might not occur. Investors are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this report or the date of the document incorporated by reference in this report. We are not under any obligation, and we expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise.

PART I

| ITEM 1. | BUSINESS. |

Overview

References to “we,” “us,” “our,” “Green Plains,” or the “Company” in this report refer to Green Plains Renewable Energy, Inc., an Iowa corporation founded in June 2004, and its subsidiaries.

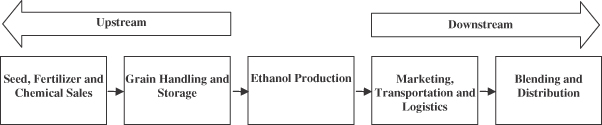

We are a leading, vertically-integrated producer, marketer and distributer of ethanol. We have grown rapidly, primarily through acquisitions, and today we have operations throughout the ethanol value chain. Our operations begin upstream with our agronomy and grain handling operations, continue through our

2

Table of Contents

approximately 680 million gallons per year, or mmgy, of ethanol production capacity and end downstream with our ethanol marketing, distribution and blending facilities. We focus on generating stable operating margins through our diversified business segments and our risk management strategy. We believe that owning and operating assets throughout the ethanol value chain enables us to mitigate the effects of changes in commodity prices on our profitability and differentiates us from companies focused only on ethanol production. Following is our visual presentation of the ethanol value chain:

Our disciplined risk management strategy is designed to lock in operating margins by forward contracting the four primary commodities involved in ethanol production: corn, natural gas, ethanol and distillers grains. We also seek to maintain an environment of continuous operational improvement to increase our efficiency and effectiveness as a low-cost producer of ethanol.

Currently, we operate within the three segments outlined below:

| • | Ethanol Production. We operated a total of eight ethanol plants in Indiana, Iowa, Michigan, Nebraska and Tennessee, with approximately 680 mmgy of total ethanol production capacity at December 31, 2010. At capacity, these plants collectively will consume approximately 245 million bushels of corn and produce approximately 2.0 million tons of distillers grains annually. In February 2011, our bid to acquire an ethanol plant in Minnesota with approximately 55 mmgy of total ethanol production capacity was accepted by the bankruptcy court overseeing the auction process. We expect to close this acquisition in March 2011. We are focused on maximizing the operational efficiency at each of our plants in order to achieve the lowest cost per gallon of ethanol produced. |

| • | Agribusiness. We operate three lines of business within our agribusiness segment: bulk grain, agronomy and petroleum. In our bulk grain business, we have 13 grain elevators with approximately 31.4 million bushels of total storage capacity. We sell fertilizer and other agricultural inputs and provide application services to area producers through our agronomy business. Additionally, we sell petroleum products including diesel, soydiesel, blended gasoline and propane, primarily to agricultural producers and consumers. We believe our bulk grain business provides synergies with our ethanol production segment as it supplies a portion of the feedstock for our ethanol plants. |

| • | Marketing and Distribution. Our in-house, fee-based marketing business is responsible for the sales, marketing and distribution of all ethanol, distillers grains and corn oil produced at our eight ethanol plants. We also market and distribute ethanol for third-party ethanol producers with expected production totaling approximately 360 mmgy. Additionally, we hold a majority interest in Blendstar, LLC, which operates nine blending or terminaling facilities with approximately 495 mmgy of total throughput capacity in seven states in the south central United States. |

Our Competitive Strengths

We believe we have created a platform that diversifies our revenues and income stream. Fundamentally, we focus on managing commodity price risks, improving operating efficiencies and controlling costs. We believe our competitive strengths include:

Disciplined Risk Management. We believe risk management is a core competency of ours. Our primary focus is to lock in favorable operating margins whenever possible. We do not speculate on general price

3

Table of Contents

movements by taking unhedged positions on commodity products such as corn, ethanol or natural gas. Our comprehensive risk management platform allows us to monitor real-time commodity price risk exposure at each of our plants, and to respond quickly to lock in acceptable margins. By using a variety of risk management tools and hedging strategies, including our internally-developed real-time operating margin management system, we believe we are able to maintain a disciplined approach to risk management.

Demonstrated Asset Acquisition and Integration Capabilities. We have demonstrated the ability to make strategic acquisitions that we believe create synergies with our vertically-integrated platform. Our belief is that acquiring and developing complementary businesses enhances our ability to mitigate risks. Our balance sheet allows us to be selective in that process. Since our inception, we have acquired or developed eight ethanol plants in addition to upstream grain elevators and agronomy businesses and downstream blending and distribution businesses. We believe these acquisitions have been successfully integrated into our business and have enhanced our overall returns.

Focus on Operational Excellence. All of our plants are staffed by experienced industry personnel. We focus on incremental operational improvements to enhance overall production efficiencies and we share operational knowledge across our plants. Using real-time production data and control systems, we continually monitor our plants in an effort to optimize performance. We believe our ability to improve operating efficiencies provides an operating cost advantage over most of our competitors. In turn, we believe we are well positioned to increase operating margins for any facilities that we may acquire in the future.

Leading Vertically-Integrated Ethanol Producer. We believe our operations throughout the ethanol value chain reduce our commodity and operating risks, and increase our pricing visibility and influence in key markets. Combined, we believe our agribusiness, ethanol production, and marketing and distribution businesses provide efficiencies across the ethanol value chain, from grain procurement to blending fuel. Our agribusiness operations help to reduce our supply risk by providing grain handling and storage capabilities for approximately 31.4 million bushels. Assuming full production capacity at each of our plants and those of our third-party ethanol producers, we would market and distribute more than one billion gallons of ethanol from twelve plants. Our majority interest in Blendstar allows us to source, store, blend and distribute ethanol and biodiesel across multiple states.

Proven Management Team. Our senior management team brings an average of 21 years of commodity risk management and related industry experience. We have specific expertise across all aspects of the ethanol supply, production, and distribution chain – from agribusiness, to plant operations and management, to commodity markets and risk management, to ethanol marketing.

Our Growth Strategy

We intend to continue to focus on strengthening and diversifying our vertically-integrated platform by implementing the following growth strategies:

Develop or Acquire Strategically-Located Grain Elevators. We intend to pursue opportunities to develop or acquire additional grain elevators within the agribusiness segment, specifically those located near our ethanol plants. We believe that owning additional grain elevators in close proximity to our ethanol plants enables us to strengthen relationships with local corn producers, allowing us to source corn more effectively and at a lower average cost. Since all of our plants are located within or near the corn belt where a number of competitors also have ethanol facilities, we believe that owning grain elevators provides us with a competitive advantage in the origination of corn.

Pursue Consolidation Opportunities within the Ethanol Industry. We continue to focus on the potential acquisition of additional ethanol plants. Throughout 2010, we were approached with opportunities to acquire existing ethanol plants. We believe those plants were available for a number of reasons including financial distress of a particular facility, a lack of operational expertise or a desire by existing owners to exit their original

4

Table of Contents

investment. We will continue to take a disciplined approach in evaluating new opportunities by considering whether the plants fit within the design, engineering and geographic criteria we have developed. We believe that our integrated platform, plant operations experience and disciplined risk management approach give us the ability to generate favorable returns from our acquisitions.

Improve Operational Efficiency. We seek to enhance profitability at each of our plants by increasing our production volumes through operational improvements. We continually research operational processes that may increase our efficiency by increasing yields, lowering our processing cost per gallon and increasing our production volumes. Additionally, we employ an extensive cost control system at each of our plants to continuously monitor our plants’ performance. We are able to use performance data from our plants to develop strategies for cost reduction and efficiency that can be applied across our platform.

Expand Our Third-Party Marketing Volumes. We plan to continue to grow our downstream access to customers and are actively looking at new marketing opportunities with other ethanol producers. We maintain active dialogues with prospective ethanol producers whose location, production and risk management practices are consistent with our vertically-integrated platform. We believe that further expansion of our third-party marketing volumes will enable us to continue to meet major ethanol customers’ needs by providing us with a broader market presence and allowing us to further leverage our marketing expertise and distribution systems.

Invest in Next Generation Biofuel Opportunities. We plan to continue our investment in the BioProcess Algae joint venture, which is focused on developing technology to grow and harvest algae, which consume carbon dioxide, in commercially viable quantities. We believe this technology has specific applications with facilities, including ethanol plants, that emit carbon dioxide. The algae produced has the potential to be used for advanced biofuel production, high quality animal feed or as biomass for energy production.

Ethanol Industry Overview

The ethanol industry has grown significantly over the past several years, with production increasing from 1.4 billion gallons in 1998 to 13.2 billion gallons in 2010, according to the U.S. Energy Information Administration. While the market prices for our feedstock commodities are volatile and at times result in unprofitable ethanol operations, during the past three years, there have been few occasions where the simple crush spread, which we define as the market value of 2.8 gallons of ethanol less the cost of one bushel of corn (which represents the typical industry yield), has dropped to below $0.10 per gallon. We believe that ethanol will continue to experience increased demand in the United States as there remains a focus on reducing reliance on petroleum-based transportation fuels due to high and volatile oil prices, heightened environmental concerns, and energy independence and national security concerns. Also according to the U.S. Energy Information Administration, ethanol blends accounted for approximately 9.1% of the U.S. gasoline supply for the twelve months ended December 31, 2010. We believe ethanol’s environmental benefits, ability to improve gasoline performance, fuel supply extender capabilities, attractive production economics and favorable government incentives could enable ethanol to comprise an increasingly larger portion of the U.S. fuel supply as more fully described below:

| • | Emissions Reduction. Ethanol demand increased substantially in the 1990’s, when federal law began requiring the use of oxygenates in reformulated gasoline in cities with unhealthy levels of air pollution on a seasonal or year-round basis. These oxygenates included ethanol and MTBE which, when blended with gasoline, reduces vehicle emissions. Although the federal oxygenate requirement was eliminated in 2006, oxygenated gasoline continues to be used in order to help meet separate federal and state air emission standards. The refining industry has all but abandoned the use of MTBE making ethanol the primary clean air oxygenate currently used. |

| • | Octane Enhancer. Ethanol, with an octane rating of 113, is used to increase the octane value of gasoline with which it is blended, thereby improving engine performance. It is used as an octane enhancer both for producing regular grade gasoline from lower octane blending stocks and for upgrading regular gasoline to premium grades. |

5

Table of Contents

| • | Fuel Stock Extender. Ethanol is a valuable blend component that is used by refiners in the United States to extend fuel supplies. According to the Energy Information Administration, from 2000 to 2010, ethanol as a component of the United States gasoline supply has grown from 1.3% to 9.0%. In 2010 alone, ethanol replaced the need for approximately 297 million barrels of oil in the United States. |

| • | E15 Blending Waiver. In March 2009, Growth Energy, an ethanol industry trade association, and 54 ethanol producers requested that the U.S. Environmental Protection Agency, or EPA, approve the use of up to 15% ethanol blended with gasoline, or E15. In October 2010, the EPA approved the use of E15 in model year 2007 and newer passenger vehicles, including cars, SUVs and light pickup trucks. In January 2011, the EPA approved the use of E15 in model year 2001 to 2006 passenger vehicles. With these approvals, over 129 million vehicles or 60% of the passenger vehicles in service are eligible to use E15. We believe that ethanol blended in the U.S. gasoline supply is an important step towards the long-term introduction of more renewable fuels into the transportation sector. We also believe that increasing the ethanol blended in the domestic gasoline supply could have a positive impact on the demand for ethanol. |

| • | Economics of Ethanol Blending. We believe that the costs ethanol producers incur in producing a gallon of ethanol currently are lower than the costs refiners incur in producing a gallon of petroleum-based gasoline. Ethanol’s favorable production economics are further enhanced in the United States by the Volumetric Ethanol Excise Tax Credit, or VEETC (commonly referred to as the “blender’s credit”), which can be captured by refiners or passed on to consumers for a benefit of $0.45 per gallon of ethanol. The blender’s credit was renewed in 2010 and is set to expire on December 31, 2011. |

| • | Mandated Use of Renewable Fuels. In addition to the blender’s tax credit, the growth in ethanol usage has also been supported by legislative requirements dictating the use of renewable fuels, including ethanol. The Energy Independence and Security Act of 2007, confirmed by the EPA regulations on the Renewable Fuel Standard, or RFS 2, issued in February 2010 mandated a minimum usage of corn-derived renewable fuels of 12.0 billion gallons in 2010, increasing annually by 0.6 million gallons to 15.0 billion gallons in 2015. |

Our Operating Segments

Ethanol Production Segment

Our ethanol production segment had the capacity to produce approximately 680 mmgy of ethanol as of December 31, 2010. Our ethanol plants also produce co-products such as wet, modified wet or dried distillers grains. Processing at full capacity, our plants will consume approximately 245 million bushels of corn and produce approximately 2.0 million tons of distillers grains annually. Our plants use a dry mill process to produce ethanol and co-products. We operate all of our ethanol plants through wholly-owned operating subsidiaries. A summary of these plants is outlined below:

| Plant | Plant Production Capacity (mmgy) |

Start Date | Technology | Land Owned (acres) |

On Site Corn Storage Capacity (bushels) | |||||

| Bluffton, Indiana |

120 | Sept. 2008 | ICM | 419 | 1,040,000 | |||||

| Central City, Nebraska(1) |

100 | July 2009 | ICM | 40 | 1,200,000 | |||||

| Lakota, Iowa(1) |

100 | Oct. 2010 | ICM/Lurgi | 230 | 1,410,000 | |||||

| Obion, Tennessee(2) |

120 | Nov. 2008 | ICM | 230 | 2,100,000 | |||||

| Ord, Nebraska(1) |

55 | July 2009 | ICM | 170 | 400,000 | |||||

| Riga, Michigan(1) |

60 | Oct. 2010 | Delta-T | 132 | 525,000 | |||||

| Shenandoah, Iowa |

65 | Aug. 2007 | ICM | 108 | 500,000 | |||||

| Superior, Iowa |

60 | July 2008 | Delta-T | 264 | 525,000 |

| (1) | These plants operated under different ownership prior to the stated start date. |

| (2) | We lease an additional 129 acres of land near the Obion, Tennessee plant. |

6

Table of Contents

Corn Feedstock and Ethanol Production

Ethanol is a chemical produced by the fermentation of carbohydrates found in grains and other biomass. Ethanol can be produced from a number of different types of grains, such as corn, wheat and sorghum, as well as from agricultural waste products such as rice hulls, cheese whey, potato waste, brewery and beverage wastes and forestry and paper wastes. At present, the majority of ethanol in the United States is produced from corn because corn contains large quantities of carbohydrates, can be handled efficiently and is in greater supply than other grains. Such carbohydrates convert into glucose more easily than most other kinds of biomass. Outside the United States, sugarcane is the primary feedstock used in ethanol production.

Our plants use corn as feedstock in the dry mill ethanol production process. Each of our plants requires, depending on their production capacity, approximately 20 million to 40 million bushels of corn annually. The price and availability of corn are subject to significant fluctuations depending upon a number of factors that affect commodity prices in general, including crop conditions, weather, governmental programs and foreign purchases. Because the market price of ethanol is not directly related to corn prices, ethanol producers are generally not able to compensate for increases in the cost of corn feedstock through adjustments to prices charged for their ethanol.

Our corn supply is obtained primarily from local markets. We utilize cash and forward fixed-price contracts with grain producers and elevators for the physical delivery of corn to our plants. At our Nebraska, Tennessee and Iowa plants, we maintain relationships with local farmers, grain elevators and cooperatives which serve as our primary sources of grain feedstock. Most farmers in the areas where our plants are located have stored their corn in their own dry storage facilities, which allows us to purchase much of the corn needed to supply our plants directly from farmers throughout the year. At our Bluffton, Lakota and Riga plants, we have contracted with a third-party grain originator to supply all of our corn requirements for ethanol production. These contracts terminate between November 2012 and September 2015. Each of our plants is also situated on rail lines that we can use to receive corn from other regions of the country, if local corn supplies are insufficient.

Corn is received at the plant by truck or rail, which is then weighed and unloaded in a receiving building. Storage bins are utilized to inventory grain, which is passed through a scalper to remove rocks and debris prior to processing. Thereafter, the corn is transported to a hammer mill where it is ground into coarse flour and conveyed into a slurry tank for enzymatic processing. Water, heat and enzymes are added to convert the complex starch molecules into simpler carbohydrates. The slurry is heated to reduce the potential of microbial contamination and pumped to a liquefaction tank where additional enzymes are added. Next, the grain slurry is pumped into fermenters, where yeast, enzymes, and nutrients are added, to begin a batch fermentation process. A beer column, within the distillation system, separates the alcohol from the spent grain mash. Alcohol is then transported through a rectifier column, a side stripper and a molecular sieve system where it is dehydrated to 200 proof. The 200 proof alcohol is then pumped to a holding tank and then blended with approximately two percent denaturant (usually natural gasoline) as it is pumped into finished product storage tanks.

Distillers Grains

The spent grain mash from the beer column is pumped into one of several decanter type centrifuges for dewatering. The water, or thin stillage, is pumped from the centrifuges and then to an evaporator where it is dried into a thick syrup. The solids, or wet cake, that exits the centrifuge are conveyed to the dryer system. The wet cake is dried at varying degrees, resulting in the production of distillers grains. Syrup might be reapplied to the wet cake prior to drying, providing nutrients if the distillers grains are to be used as animal feed. Distillers grains, the principal co-product of the ethanol production process, are principally used as high-protein, high-energy animal fodder and feed supplements marketed to the dairy, beef, swine and poultry industries. Distillers grains have alternative uses as burning fuel, fertilizer and weed inhibitors.

7

Table of Contents

Dry mill ethanol processing potentially creates three forms of distillers grains, depending on the number of times the solids are passed through the dryer system; wet, modified wet and dried distillers grains. Wet distillers grains are processed wet cake that contains approximately 65% to 70% moisture. Wet distillers grains have a shelf life of approximately three days and can be sold only to dairies or feedlots within the immediate vicinity of an ethanol plant. Modified wet distillers grains, which have been dried further to approximately 50% to 55% moisture, have a slightly longer shelf life of approximately three weeks and are marketed to regional dairies and feedlots. Dried distillers grains, which have been dried more extensively to approximately 10% to 12% moisture, have an almost indefinite shelf life and may be stored, sold and shipped to any market regardless of its proximity to an ethanol plant.

Utilities

The production of ethanol requires significant amounts of natural gas, electricity and water.

Natural Gas. Ethanol plants produce process steam from their own boiler systems and dry the distillers grains co-product via a direct gas-fired dryer. Depending on certain production parameters, our ethanol plants are expected to use approximately 22,000 to 32,000 British Thermal Units of natural gas per gallon of production. The price of natural gas can be volatile; therefore, we use hedging strategies to mitigate increases in gas prices. We have entered into certain service agreements for the natural gas required by our ethanol plants and pay tariff fees to these providers for transporting the gas through their pipelines to our plants.

Electricity. Our plants require between 0.5 and 1.0 kilowatt hours of electricity per gallon of production. Local utilities supply necessary electricity to all of our ethanol plants at market-based rates.

Water. Although some of our plants expect to satisfy the majority of their water requirements from wells located on their respective properties, each anticipates that it will obtain potable water for certain processes from local municipal water sources at prevailing rates. Each facility operates a filtration system to purify the well water that is utilized for its operations. Local municipalities supply all of the necessary water for our plants that do not have onsite wells. Water quality is very important. Much of the water used in an ethanol plant is recycled back into the process. The plants require boiler makeup water and cooling tower water. Boiler makeup water is treated on-site to minimize minerals and substances that would harm the boiler. Recycled process water cannot be used for this purpose. Cooling tower water is deemed non-contact water (it does not come in contact with the mash) and, therefore, can be regenerated back into the cooling tower process.

Agribusiness Segment

We operate our agribusiness segment primarily through our wholly-owned subsidiary, Green Plains Grain Company LLC, which is a grain and farm supply business with three primary operating lines of business: bulk grain, agronomy and petroleum. We believe our agribusiness operations increase our operational efficiency, reduce commodity price and supply risks, and diversify our revenue streams.

Bulk Grain. We buy bulk grain, primarily corn and soybeans, from area producers and provide grain drying and storage services to those producers. The grain is then sold to grain processing companies and area livestock producers. We have grain storage capacity of approximately 31.4 million bushels, not including the on-site storage capacity at each of our ethanol plants. This capacity supports the grain merchandising activities and our Lakota, Obion, Shenandoah and Superior ethanol plant operations. These bulk grain commodities are readily traded on commodity exchanges and inventory values are affected by market changes and spreads. To attempt to reduce risk due to market fluctuations from purchase and sale commitments, we enter into exchange-traded futures and options contracts designed to serve as economic hedges.

Agronomy. We have agronomists on staff who consult and provide services to our customers. The agronomy division also sells dry and liquid fertilizer and agricultural inputs, such as chemicals, seed and supplies that we buy wholesale, and provides application services to area producers. Having these experts on staff,

8

Table of Contents

coupled with the wide variety of agricultural products we offer, allows us to provide customized attention and build long-term relationships with our customers.

Petroleum. A portion of our business consists of selling diesel, soydiesel, blended gasoline and propane that we buy wholesale, primarily to agricultural producers and consumers. We believe this business line demonstrates our ability to provide a range of fuel products that support the local communities in which we are located.

We own approximately 134 acres of land in seven locations in Northwest Iowa, near our Superior ethanol plant, for our agribusiness operations with licensed grain storage capacity of approximately 16.9 million bushels, 3.6 million gallons of liquid fertilizer storage and 12,000 tons of dry fertilizer storage. We own approximately 38 acres of land in five locations in western Tennessee, in the general region of our Obion ethanol plant, for our agribusiness operations with licensed grain storage capacity of approximately 11.7 million bushels. We also own approximately 11 additional acres of land at our grain elevator in Essex, Iowa, near our Shenandoah ethanol plant, with licensed grain storage capacity of approximately 2.8 million bushels.

Seasonality is present within our agribusiness operations. The spring planting and fall harvest periods have the largest seasonal impact, directly impacting the quarterly operating results of our agribusiness segment. This seasonality generally results in higher revenues and stronger financial results for this segment during the second and fourth quarters while the financial results of the first and third quarters generally will reflect periods of lower activity with low to negative margins.

Marketing and Distribution Segment

We have an in-house, fee-based marketing business which is responsible for sales of Company-produced corn oil, along with marketing and distribution of all ethanol and distillers grains produced at our eight ethanol plants. We also market and distribute ethanol for third-party ethanol producers. Assuming full production capacity at each of our plants and those of our third-party ethanol producers, we would market and distribute more than one billion gallons of ethanol. Our majority interest in Blendstar allows us to source, store, blend and distribute biodiesel and ethanol, including our production and that of other producers, across multiple states.

Marketing

We market our ethanol and that of our third-party producers to many different customers on a local, regional and national basis. In addition, during 2010 we began purchasing ethanol from other independent producers to realize price arbitrages that may exist. These transactions are expected to increase in volume in 2011. Local markets are the easiest to service because of their close proximity to the related production facility. To achieve the best prices for the ethanol that we market, we sell into local, regional and national markets under sales agreements with integrated energy companies, jobbers, retailers, traders and resellers. Under these agreements, ethanol is priced under fixed and indexed pricing arrangements. Deliveries to the majority of the local markets, within 150 miles of the plants, are generally transported by truck, and deliveries to more distant markets are shipped by rail using major U.S. rail carriers.

The market for distillers grains generally consists of local markets for wet, modified wet and dried distillers grains, and national markets for dried distillers grains. If all of our distillers grains were marketed in the form of dried distillers grains, we expect that our ethanol plants would produce approximately 2.0 million tons of distillers grains annually. In addition, the market can be segmented by geographic region and livestock industry. The bulk of the current demand is for dried distillers grains delivered to geographic regions without significant local corn or ethanol production. Our market strategy includes shipping a substantial amount of distillers grains as dried distillers grains to regional and national markets by rail.

Most of our modified wet distillers grains are sold to midwestern feedlot markets. Our dried distillers grains are generally shipped to feedlot and poultry markets, as well as to Texas and west coast rail markets. Some of our

9

Table of Contents

distillers grains are shipped by truck to dairy, beef, and poultry operations in the eastern United States. Also, at certain times of the year, we transport product to the Mississippi River to be loaded on barges destined for export markets. We also ship by railcars into Eastern and Southeastern feed mill, poultry and dairy operations, as well as to domestic trade companies. Access to these markets allows us to move product into markets that are offering the highest net price.

Corn Oil

Recently, we began implementing corn oil extraction technology at our six legacy ethanol plants. We expect the implementation of corn oil extraction at our plants will be completed by the end of the second quarter of 2011. As of December 31, 2010, we were operating corn oil extraction systems at our Lakota, Obion, Ord and Riga plants. The corn oil systems are designed to extract non-edible corn oil from the thin stillage evaporation process immediately prior to production of distillers grains. Corn oil is produced by processing syrup and evaporated thin stillage, through a decanter style centrifuge or a disk stack style centrifuge. Corn oil has a lower density than water or solids which make up the syrup. The centrifuges separate the relatively light oil from the heavier components of the syrup, eliminating the need for significant retention time. De-oiled syrup is returned to the process for blending into wet, modified, or dry distillers grains. The corn oil product is primarily marketed as a livestock feed supplement or to the biodiesel market.

Industrial uses for corn oil include feedstock for biodiesel, livestock feed additives, rubber substitutes, rust preventatives, inks, textiles, soaps and insecticides. Our corn oil is primarily sold to biodiesel manufactures and, to a lesser extent, feed lot and poultry markets. We generally transport our corn oil by truck to locations in a close proximity to our ethanol plants, primarily in the southeastern and midwestern regions of the U.S.

Transportation and Delivery

Four of our plants are designed with unit-train load out capabilities and all have access to railroad mainlines. To meet the challenge of marketing ethanol and distillers grains to diverse market segments, five of our plants have extensive rail siding capable of handling more than 150 railcars at their production facilities while the three other plants have rail siding that can accommodate approximately 90 railcars at their respective locations. At certain of our locations, we have large loop tracks which enable loading of unit trains of both ethanol and dried distillers grains, as well as spurs connecting the site’s rail loop to the railroad mainline or spurs that allow movement and storage of railcars on-site. These rail lines allow us to sell our products to various regional and national markets. The rail providers for our ethanol plants can switch cars to most of the other major railroads, allowing the plants to easily ship ethanol and distillers grains throughout the United States.

10

Table of Contents

Ethanol Blending and Distribution

We hold a majority interest in Blendstar, a biofuels terminal operator that owns and operates biofuel holding tanks and terminals, and provides terminaling, splash blending and logistics solutions to markets that currently do not have efficient access to renewable fuels. Blendstar operates blending and terminaling facilities at one owned and eight leased locations on approximately 19 acres in seven states with a combined total storage capacity of approximately 700,000 gallons and throughput capacity of approximately 495 mmgy. These facilities are summarized below:

| Facility Location |

Storage Capacity (gallons) |

Throughput Capacity (mmgy) | ||

|

Birmingham, Alabama |

120,000 | 96 | ||

| Little Rock, Arkansas |

30,000 | 36 | ||

|

Louisville, Kentucky |

60,000 | 30 | ||

| Bossier City, Louisiana(1) |

- | 60 | ||

| Collins, Mississippi |

120,000 | 84 | ||

| Oklahoma City, Oklahoma |

150,000 | 84 | ||

| Tulsa, Oklahoma |

- | 24 | ||

|

Knoxville, Tennessee |

60,000 | 21 | ||

|

Nashville, Tennessee |

160,000 | 60 |

(1) Five acre facility is owned by Blendstar.

Risk Management and Hedging Activities

The profitability of our operations and our industry are highly dependent on commodity prices, especially prices for corn, ethanol, distillers grains and natural gas. Because the market prices among these commodities are not always correlated at times ethanol production may be unprofitable. We believe that ineffective commodity price risk management was a primary reason for the distressed conditions the ethanol industry faced in late 2008 and through the first 6 months of 2009 as ethanol producers had entered into fixed-price corn contracts, or built large inventory positions, in order to ensure corn supply. When corn and ethanol prices declined, these producers were unable to profitably produce ethanol given their higher feedstock costs. We believe the ethanol industry as a whole has and continues to demonstrate more discipline on utilizing risk management tools to avoid the issues experienced in late 2008 and early 2009.

We enter into forward contracts to supply a portion of our respective ethanol and distillers grains production or to purchase a portion of our respective corn or natural gas requirements in an attempt to partially offset the effects of volatility of ethanol, distillers grains, corn and natural gas prices. To a much lesser extent, we also engage in other hedging transactions involving exchange-traded futures contracts for corn, natural gas and ethanol from time to time. The financial statement impact of these activities is dependent upon, among other things, the prices involved and our ability to physically receive or deliver the commodities involved. Hedging arrangements also expose us to the risk of financial loss in situations where the counterparty to the hedging contract defaults on its contract or, in the case of exchange-traded contracts, where there is a change in the expected differential between the price of the commodity underlying the hedging agreement and the actual prices paid or received by us for the physical commodity bought or sold. Hedging activities can themselves result in losses when a position is purchased in a declining market or a position is sold in a rising market. A hedge position is often settled in the same time frame as the physical commodity is either purchased (corn and natural gas) or sold (ethanol, distillers grains and corn oil). Hedging losses may be offset by a decreased cash price for corn and natural gas and an increased cash price for ethanol, distillers grains and corn oil. We also vary the amount of hedging or other risk mitigation strategies we undertake, and we may choose not to engage in hedging

11

Table of Contents

transactions at all. By using a variety of risk management tools and hedging strategies, including our internally-developed real-time operating margin management system, we believe our approach to risk management allows us to monitor real-time operating price risk exposure at each of our plants and to respond quickly to lock in acceptable margins. In addition, our multiple business lines and revenue streams help diversify our operations and profitability.

Merger and Acquisition Activity

In October 2008, we completed a merger with VBV, LLC that resulted in our ownership of the Bluffton and Obion plants. Simultaneously with the closing of the merger, NTR plc, a leading international developer and operator in renewable energy and sustainable waste management and the majority equity holder of VBV prior to the merger, through its wholly-owned subsidiaries, invested $60 million in us by purchasing newly-issued shares of our common stock.

In January 2009, we acquired a majority interest in biofuel terminal operator Blendstar, LLC for $8.9 million. The acquisition of Blendstar was a strategic investment within the ethanol value chain whose operations are included in our marketing and distribution segment.

In July 2009, we acquired the membership interests in two limited liability companies that owned ethanol plants in Central City and Ord, Nebraska for approximately $121 million. These plants, which are a part of our ethanol production segment, were acquired to add to our overall ethanol and distillers grains production. The Central City and Ord plants added expected operating capacity totaling 150 mmgy. Following implementation of process improvements, they are now operating at approximately 155 mmgy.

In April 2010, we acquired agribusiness operations in western Tennessee which include five grain elevators with federally licensed grain storage capacity of 11.7 million bushels for $25.7 million. The five grain elevators and other assets acquired are included in our agribusiness segment.

In October 2010, we acquired Global Ethanol, LLC, which owned two operating ethanol plants with a combined production capacity of approximately 157 mmgy for approximately $174.2 million. These plants, which currently are operating at approximately 160 mmgy and are part of our ethanol production segment, were acquired to add to our overall ethanol, distillers grains and corn oil production.

In February 2011, we announced that our bid to purchase certain assets of Otter Tail Ag Enterprises, LLC was accepted by the bankruptcy court overseeing the auction process. The 55 mmgy dry-mill ethanol plant being acquired is located near Fergus Falls, Minnesota. The asset purchase is expected to close in March 2011. We will finance the $55 million acquisition with cash and financing from a group of nine lenders, led by AgStar Financial Services. The expected impact of this transaction on our production capacity and operations has not been included throughout this report as the transaction had not closed as of the date of this filing.

Algae Joint Venture

In November 2008, we formed a joint venture to commercialize algae production as part of our commitment to next-generation biofuels. BioProcess Algae LLC is a joint venture between us, Clarcor Inc., BioProcessH2O LLC and NTR. Using advanced photobioreactor technology developed from base technology licensed from BioProcessH2O, BioProcess Algae currently is producing algae at a pilot plant located at our Shenandoah ethanol plant, sustained by the plant’s recycled heat, water and carbon dioxide. We believe algae production fits well into our business model since we already engage in the business of marketing biofuel and feed products. The algae produced have the potential to be used for advanced bio-fuel production, high quality animal feed, or as biomass for energy production, but our current primary focus is on efficiently capturing carbon dioxide to grow and harvest algae.

12

Table of Contents

Construction of Phase II, which began during the third quarter of 2010, was completed and the Grower Harvester bioreactors were successfully started up in January 2011. Phase II allows for verification of growth rates, energy balances and operating expenses, which are considered to be some of the key steps to commercialization. The Iowa Power Fund awarded BioProcess Algae an additional grant to continue the research and development of the Grower Harvester technology, and the remaining cost of the Phase II project was shared by the joint venture partners. As part of the Phase II funding, we increased our ownership in BioProcess Algae to 35%.

Our Competition

Domestic Ethanol Competitors

We compete with numerous other ethanol producers located throughout the United States, several of which have much greater resources, in the sales of ethanol and distillers grains. In 2010, the three largest ethanol producers in North America were Archer-Daniels-Midland Company, POET, LLC and Valero Energy Corporation. We believe that our principal competitors’ expected managed production capacity and ethanol marketed ranges between approximately 200 mmgy and approximately 1,800 mmgy. Based on production capacity as reported by Ethanol Producer Magazine, we believe we are the fourth largest ethanol producer in North America. According to Ethanol Producer Magazine, as of December 31, 2010, there were 214 ethanol-producing plants within the United States, capable of producing 14.1 billion gallons of ethanol annually, as well as several new plants that were under construction or expanding their capacity. The industry typically does not operate at 100% of capacity with historical rates of annual production to available plant capacity averaging in the high 80 percent to the low 90 percent range. We believe that by the end of 2011, annual U.S. ethanol production capacity could reach 14.5 billion gallons.

Competition for corn supply from other ethanol plants and other corn consumers exists in all areas and regions in which our plants operate. According to Ethanol Producer Magazine, as of December 31, 2010, there were 42 operational ethanol plants in Iowa. The plants are concentrated, for the most part, in the northern and central regions of the state where a majority of the corn is produced. As of December 31, 2010, the state of Nebraska had 25 operating ethanol plants and one under construction. The state of Indiana had 13 operating ethanol plants with one under construction. The state of Tennessee had only two operational ethanol production facilities. The state of Michigan had 5 operational ethanol plants.

Foreign Ethanol Competitors

We also face competition from foreign producers of ethanol and such competition may increase significantly in the future. Large international companies with much greater resources than ours have developed, or are developing, increased foreign ethanol production capacities. Brazil is the world’s second largest ethanol producer. Brazil makes ethanol primarily from sugarcane. Several large companies produce ethanol in Brazil. For example, in August 2010, Royal Dutch Shell formed a joint venture with Cosan, which produces approximately 450 mmgy of sugar-based ethanol per year.

Ethanol produced in foreign countries, from sugarcane or other feed stocks imported into the United States, is subject to an import tariff of $0.54 per gallon. Production imported from the Caribbean region is eligible for tariff reduction or elimination under a program known as the Caribbean Basin Initiative. Large multinational companies have expressed interest in building dehydration plants in participating Caribbean Basin countries, such as El Salvador, which would convert ethanol into fuel-grade ethanol for shipment to the United States. Depending on feed stock prices, ethanol imported from Caribbean Basin countries may be less expensive than domestically-produced ethanol though transportation and infrastructure constraints may temper the market impact on the United States.

13

Table of Contents

Other Competition

Alternative fuels, gasoline oxygenates and ethanol production methods are continually under development by ethanol and oil companies. Ethanol production technologies continue to evolve, and changes are expected to occur primarily in the area of ethanol made from cellulose obtained from other sources of biomass such as switchgrass or fast growing poplar trees. Because our plants are designed as single-feedstock facilities, we have limited ability to adapt the plants to a different feedstock or process system without additional capital investment and retooling.

Regulatory Matters

Government Ethanol Programs, Policies and Subsidies

In an effort to reduce this country’s dependence on foreign oil, federal and state governments have enacted numerous policies, incentives and subsidies to encourage the usage of domestically-produced alternative fuel solutions. The U.S. ethanol industry has benefited significantly as a direct result of these policies. While historically the ethanol industry has been dependent on economic incentives, the need for such incentives may diminish as the acceptance of ethanol as a primary fuel and as a fuel extender continues to increase.

Passed in 2007 as part of the Energy Independence and Security Act, a federal Renewable Fuels Standard, or RFS, has been and will continue to be a driving factor in the growth of ethanol usage. As mandated by the RFS, 12.6 billion gallons of conventional biofuels, which corn-based ethanol falls under, must be blended into the U.S. fuel supply in 2011. This requirement progressively increases up to 15.0 billion gallons by 2015.

To further drive growth in the increased adoption of ethanol, Growth Energy, an ethanol industry trade association, and a number of ethanol producers requested a waiver from the EPA to increase the amount of ethanol blended into gasoline from the current 10% level, or E10, to a 15% level, or E15. In October 2010, the EPA approved E15 for use in model year 2007 and newer model passenger vehicles, including cars, SUVs and light pickup trucks. In January 2011, the EPA ruled that E15 was also approved for use in model year 2001 through 2006 passenger vehicles. The Department of Energy is funding research by two Kettering University mechanical engineering professors on how cars from the 1990s react to E15. The Kettering study is among several that may help the EPA determine whether E15 is safe in older cars. We believe this increased blend rate will have a positive impact on demand for ethanol.

Another major benefit to the industry is the Volumetric Ethanol Excise Tax Credit, or VEETC (often commonly referred to as the “blender’s credit”) created by the American Jobs Creation Act of 2004. This credit allows gasoline distributors who blend ethanol with gasoline to receive a federal excise tax credit of $0.45 per gallon of pure ethanol used, or $0.045 per gallon for E10 and $0.3825 per gallon for E85. Currently, the blender’s credit is set to expire in December 31, 2011. There can be no assurances that the blenders’ credit will be extended at the end of 2011.

In July 2010, Growth Energy called for the redirection and eventual phasing out of government support for ethanol in return for a level playing field in fuel distribution. The “Fueling Freedom” plan calls for the phasing out of the blenders credit and import tariff over time, by redirecting a portion of those funds to build out the infrastructure for the distribution and use of ethanol, and shifting the remaining portion away from oil companies. The primary elements of the plan include:

| • | VEETC credits currently going to the oil industry as an incentive for blending ethanol into gasoline would be redirected to provide incentive for the build-out of distribution infrastructure for ethanol, possibly in the form of tax credits for retailers to install 200,000 blender pumps and federal backing of ethanol pipelines. This would provide Americans the access to choose ethanol in an open and free market, and would allow for the elimination of the tax supports over time. |

14

Table of Contents

| • | Requiring that all automobiles sold in the United States be flex-fuel vehicles. Assuming that consumers purchase an average of 14 to 15 million vehicles annually, it would take an estimated nine years to replace the 120 million vehicles in the United States. This would require no additional cost to taxpayers and a minimal cost of approximately $120 per vehicle to vehicle manufacturers. |

Changes in corporate average fuel economy, or CAFE, standards have also benefited the ethanol industry by encouraging use of E85 fuel products. CAFE provides an effective 54% efficiency bonus to flexible-fuel vehicles running on E85. Though E85 is not in widespread use today, auto manufacturers may find it attractive to build more flexible-fuel trucks and sport utility vehicles that are otherwise unlikely to meet CAFE standards.

In addition to these federal standards, many states have taken other steps to encourage ethanol consumption including tax credits, mandated blend rates and subsidies.

Environmental and Other Regulation

Our ethanol production and agribusiness activities are subject to environmental and other regulations. We obtain environmental permits to construct and operate our ethanol plants.

Ethanol production involves the emission of various airborne pollutants, including particulate, carbon dioxide, oxides of nitrogen, hazardous air pollutants and volatile organic compounds. In 2007, the U.S. Supreme Court classified carbon dioxide as an air pollutant under the Clean Air Act in a case seeking to require the EPA to regulate carbon dioxide in vehicle emissions. In February 2010, the EPA released its final regulations on the Renewable Fuels Standard, or RFS 2. We believe these final regulations grandfather our plants at their current operating capacity, though expansion of our plants will need to meet a threshold of a 20% reduction in greenhouse gas, or GHG emissions from a 2005 baseline measurement to produce ethanol eligible for the RFS 2 mandate. In order to expand capacity at our plants, we may be required to obtain additional permits, install advanced technology, or reduce drying of certain amounts of distillers grains.

Separately, the California Air Resources Board has adopted a Low Carbon Fuel Standard requiring a 10% reduction in GHG emissions from transportation fuels by 2020. An Indirect Land Use Change component is included in this lifecycle GHG emissions calculation, though this standard is being challenged by numerous lawsuits.

Part of our business is regulated by environmental laws and regulations governing the labeling, use, storage, discharge and disposal of hazardous materials. Our agribusiness operations are subject to government regulation and regulation by certain private sector associations. Production levels, markets and prices of the grains we merchandise are affected by federal government programs, which include acreage control and price support programs of the U.S. Department of Agriculture, or USDA. In addition, grain that we sell must conform to official grade standards imposed by the USDA. Other examples of government policies that can have an impact on our business include tariffs, duties, subsidies, import and export restrictions and outright embargos.

We also employ maintenance and operations personnel at each of our ethanol plants. In addition to the attention that we place on the health and safety of our employees, the operations at our facilities are governed by the regulations of the Occupational Safety and Health Administration, or OSHA.

Employees

As of December 31, 2010, we had 605 full-time, part-time and temporary or seasonal employees. At that date, we employed 72 people, including 35 employees of Green Plains Trade, at our corporate office in Omaha, 111 employees at our Iowa agribusiness operations, 43 employees at our Tennessee agribusiness operations, 10 employees at Blendstar and the remainder at our eight ethanol plants.

15

Table of Contents

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act) are available free of charge on our website at www.gpreinc.com as soon as reasonably practicable after we file or furnish such information electronically with the SEC. Also available on our website in our corporate governance section are the charters of our audit, compensation, and nominating committees, and a copy of our code of conduct and ethics that applies to our directors, officers and other employees, including our Chief Executive Officer and all senior financial officers. The information found on our website is not part of this or any other report we file with or furnish to the SEC.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov.

| ITEM 1A. | RISK FACTORS. |

We operate in an evolving industry that presents numerous risks. Many of these risks are beyond our control and are driven by factors that often cannot be predicted. Investors should carefully consider the risk factors set forth below, as well as the other information appearing in this report, before making any investment in our securities. If any of the risks described below or in the documents incorporated by reference in this report actually occur, our financial results, financial condition or stock price could be materially adversely affected. These risk factors should be considered in conjunction with the other information included in this report.

Risks relating to our business and industry

Our results of operations and ability to operate at a profit is largely dependent on managing the spread among the prices of corn, natural gas, ethanol and distillers grains, the prices of which are subject to significant volatility and uncertainty.

The results of our ethanol production business are highly impacted by commodity prices, including the spread between the cost of corn and natural gas that we must purchase, and the price of ethanol and distillers grains that we sell. Prices and supplies are subject to and determined by market forces over which we have no control, such as weather, domestic and global demand, shortages, export prices, and various governmental policies in the United States and around the world. As a result of price volatility for these commodities, our operating results may fluctuate substantially. Increases in corn or natural gas prices or decreases in ethanol or distillers grains prices may make it unprofitable to operate our plants. No assurance can be given that we will be able to purchase corn and natural gas at, or near, current prices and that we will be able to sell ethanol or distillers grains at, or near, current prices. Consequently, our results of operations and financial position may be adversely affected by increases in the price of corn or natural gas or decreases in the price of ethanol or distillers grains.

In early 2006, the spread between ethanol and corn prices was at historically high levels, driven in large part by oil companies removing a competitive product, methyl tertiary butyl ether, or MTBE, from the fuel stream and replacing it with ethanol in a relatively short time period. However, since that time, this spread has fluctuated widely and narrowed significantly. Fluctuations are likely to continue to occur. A sustained narrow spread or any further reduction in the spread between ethanol and corn prices, whether as a result of sustained high or increased corn prices or sustained low or decreased ethanol prices, would adversely affect our results of operations and financial position. Further, combined revenues from sales of ethanol and distillers grains could decline below our marginal cost of production, which could cause us to suspend production at some or all of our plants.

16

Table of Contents

Our risk management strategies, including hedging transactions, may be ineffective and may expose us to decreased liquidity.

In an attempt to partially offset the effects of volatility of ethanol, distillers grains, corn oil, corn and natural gas prices, we enter into forward contracts to sell a portion of our respective ethanol, distillers grains and corn oil production or to purchase a portion of our respective corn or natural gas requirements. To a much lesser extent, we also engage in other hedging transactions involving exchange-traded futures contracts for corn, natural gas, ethanol and unleaded gasoline from time to time. The financial statement impact of these activities is dependent upon, among other things, the prices involved and our ability to physically receive or deliver the commodities involved. Hedging arrangements also expose us to the risk of financial loss in situations where the counterparty to the hedging contract defaults on its contract or, in the case of exchange-traded contracts, where there is a change in the expected differential between the price of the commodity underlying the hedging agreement and the actual prices paid or received by us for the physical commodity bought or sold. Hedging activities can themselves result in losses when a position is purchased in a declining market or a position is sold in a rising market. A hedge position is often settled in the same time frame as the physical commodity is either purchased (corn and natural gas) or sold (ethanol, distillers grains and corn oil). Hedging losses may be offset by a decreased cash price for corn and natural gas and an increased cash price for ethanol, distillers grains and corn oil. We also vary the amount of hedging or other risk mitigation strategies we undertake, and we may choose not to engage in hedging transactions at all. We cannot assure you that our risk management and hedging activities will be effective in offsetting the effects of volatility. If we fail to offset such volatility, our results of operations and financial position may be adversely affected.

We also attempt to reduce the market risk associated with fluctuations in commodity prices through the use of derivative financial instruments. Sudden changes in commodity prices may require cash deposits with brokers, or margin calls. Depending on our open derivative positions, we may require additional liquidity with little advance notice to meet margin calls. As part of our risk management strategy, we have routinely had to, and in the future will likely be required to, cover margin calls. While we continuously monitor our exposure to margin calls, we cannot guarantee you that we will be able to maintain adequate liquidity to cover margin calls in the future.

Price volatility of each commodity that we buy and sell could each adversely affect our results of operations and our ability to operate at a profit.

Corn. Because ethanol competes with non-corn derived fuels, we generally are unable to pass along increased corn costs to our customers. At certain levels, corn prices may make ethanol uneconomical to produce. There is significant price pressure on local corn markets caused by nearby ethanol plants, livestock industries and other corn consuming enterprises. Additionally, local corn supplies and prices could be adversely affected by rising prices for alternative crops, increasing input costs, changes in government policies, shifts in global markets, or damaging growing conditions such as plant disease or adverse weather.

Natural Gas. The prices for and availability of natural gas are subject to volatile market conditions. These market conditions often are affected by factors beyond our control, such as weather conditions, overall economic conditions, and foreign and domestic governmental regulation and relations. Significant disruptions in the supply of natural gas could impair our ability to manufacture ethanol for our customers. Furthermore, increases in natural gas prices or changes in our natural gas costs relative to natural gas costs paid by competitors may adversely affect our results of operations and financial position.

Ethanol. Our revenues are dependent on market prices for ethanol. These market prices can be volatile as a result of a number of factors, including, but not limited to, the availability and price of competing fuels, the overall supply and demand for ethanol and corn, the price of gasoline and corn, and the level of government support.

17

Table of Contents

Ethanol is marketed as a fuel additive to reduce vehicle emissions from gasoline, as an octane enhancer to improve the octane rating of the gasoline with which it is blended and, to a lesser extent, as a gasoline substitute. As a result, ethanol prices are influenced by the supply of and demand for gasoline. Our results of operations may be materially harmed if the demand for, or the price of, gasoline decreases. Conversely, a prolonged increase in the price of, or demand for, gasoline could lead the U.S. government to relax import restrictions on foreign ethanol that currently benefit us.

Distillers Grains. Distillers grains compete with other protein-based animal feed products. The price of distillers grains may decrease when the prices of competing feed products decrease. The prices of competing animal feed products are based in part on the prices of the commodities from which these products are derived. Downward pressure on commodity prices, such as soybeans, will generally cause the price of competing animal feed products to decline, resulting in downward pressure on the price of distillers grains.

Historically, sales prices for distillers grains has tracked along with the price of corn. However, there have been occasions when the price increase for this co-product has lagged behind increases in corn prices. In addition, our distillers grains co-product competes with products made from other feedstocks, the cost of which may not have risen as corn prices have risen. Consequently, the price we may receive for distillers grains may not rise as corn prices rise, thereby lowering our cost recovery percentage relative to corn.

Due to industry increases in U.S. dry mill ethanol production, the production of distillers grains in the United States has increased dramatically, and this trend may continue. This may cause distillers grains prices to fall in the United States, unless demand increases or other market sources are found. To date, demand for distillers grains in the United States has increased roughly in proportion to supply. We believe this is because U.S. farmers use distillers grains as a feedstock, and distillers grains are slightly less expensive than corn, for which it is a substitute. However, if prices for distillers grains in the United States fall, it may have a material adverse effect on our business.

Corn Oil. Corn oil is marketed as a feedstock for biodiesel and, therefore, the price of corn oil is affected by demand for biodiesel. In general, corn oil prices follow the same price trends as heating oil and soybean oil. Corn oil revenues historically have not been significant to our business; however, our business may be materially affected by price volatility of corn oil in the future as we expand our corn oil production.

Our existing debt arrangements require us to abide by certain restrictive loan covenants that may hinder our ability to operate and reduce our profitability.

The loan agreements governing secured debt financing at our subsidiaries and the convertible debt issued in November 2010 contain a number of restrictive affirmative and negative covenants. These covenants limit the ability of our subsidiaries to, among other things, incur additional indebtedness, make capital expenditures above certain limits, pay dividends or distributions, merge or consolidate, or dispose of substantially all of their assets.

We are also required to maintain specified financial ratios, including minimum cash flow coverage, minimum working capital and minimum net worth. Some of our loan agreements require us to utilize a portion of any excess cash flow generated by operations to prepay the respective term debt. A breach of any of these covenants or requirements could result in a default under our loan agreements. If any of our subsidiaries default, and if such default is not cured or waived, our lenders could, among other remedies, accelerate their debt and declare that debt immediately due and payable. If this occurs, we may not be able to repay such debt or borrow sufficient funds to refinance. Even if new financing is available, it may not be on terms that are acceptable. No assurance can be given that the future operating results of our subsidiaries will be sufficient to achieve compliance with such covenants and requirements, or in the event of a default, to remedy such default.

In the past, we have received waivers from our lenders for failure to meet certain financial covenants and have amended our subsidiary loan agreements to change these covenants if they have not been met. For example, during 2010, loan agreements for Bluffton and Central City were amended to reduce certain financial covenants

18

Table of Contents

related to the fixed coverage ratio. No assurance can be given that, if we are unable to comply with these covenants in the future, we will be able to obtain the necessary waivers or amend our subsidiary loan agreements to prevent a default. Default by us or any of our subsidiaries with respect to any loan in excess of $10.0 million constitutes an event of default under our convertible senior notes, which could result in the convertible senior notes being declared due and payable.

Additionally, in October 2010 we acquired Global Ethanol, LLC, which we renamed Green Plains Holdings II LLC, or Holdings II. Global Ethanol’s lenders had agreed, during a specified forbearance period, to not exercise any right or remedy under its credit agreement for specified defaults related to certain loan covenants that it had been unable to satisfy. Upon closing of the Global Ethanol acquisition, Holdings II entered into an amendment to the existing credit agreement which modifies existing covenants and extends the forbearance period to April 30, 2013. If any future defaults under Holdings II’s credit agreement occur, the lenders are permitted to accelerate the maturity date on the outstanding balance. In connection with the closing of our acquisition of Global Ethanol, we contributed $10 million of cash to Holdings II, of which $6.0 million was utilized to reduce outstanding debt. Notwithstanding these actions, we cannot assure you that Holdings II will be able to comply with the new covenants going forward or obtain additional waivers for non-compliance.

We may fail to realize all of the anticipated benefits of mergers and acquisitions that we have undertaken or may undertake because of integration challenges.

We have increased the size of our operations significantly through mergers and acquisitions and intend to continue to explore potential merger or acquisition opportunities. For example, in April 2010 we acquired additional agribusiness operations in western Tennessee that included five grain elevators with federally licensed storage capacity of 11.7 million bushels. In October 2010, we acquired Global Ethanol, which owns two operating ethanol plants with a combined annual production capacity of approximately 157 million gallons of ethanol. The anticipated benefits and cost savings of such mergers and acquisitions may not be realized fully, or at all, or may take longer to realize than expected. Acquisitions involve numerous risks, any of which could harm our business, including:

| • | difficulties in integrating the operations, technologies, products, existing contracts, accounting processes and personnel of the target and realizing the anticipated synergies of the combined businesses; |

| • | risks relating to environmental hazards on purchased sites; |

| • | risks relating to acquiring or developing the infrastructure needed for facilities or acquired sites, including access to rail networks; |

| • | difficulties in supporting and transitioning customers, if any, of the target company; |

| • | diversion of financial and management resources from existing operations; |

| • | the purchase price or other devoted resources may exceed the value realized, or the value we could have realized if the purchase price or other resources had been allocated to another opportunity; |

| • | risks of entering new markets or areas in which we have limited or no experience, or are outside our core competencies; |

| • | potential loss of key employees, customers and strategic alliances from either our current business or the business of the target; |

| • | assumption of unanticipated problems or latent liabilities, such as problems with the quality of the target company’s products; and |