Attached files

| file | filename |

|---|---|

| 8-K - 8-K - LendingClub Corp | form8-kasfiledon62520b.htm |

EXHIBIT 99.1

Investor Update

As the macroeconomy transitions from deep freeze into thaw, we are currently seeing signs of unemployment and market recovery (equity markets, ABS) balanced by uncertainty around a vaccine and the rate of infection.

Though the world has turned upside down, our mission to provide Americans a path to financial success hasn’t. We remain committed to helping both sides of our marketplace navigate the current environment: providing flexibility for our members and protecting returns for our investors.

To that end, we have continued to innovate and offer new solutions to borrowers looking for help: we launched interest-only hardship plans on June 11, 2020 and are planning to launch additional plans during the second half of the year. We also extended the waiving of late fees for borrowers to provide immediate relief. To help protect investor returns, since March we have taken swift and sustained action across the platform. We tightened underwriting on new loans, increased interest rates on new loans, added capacity to help borrowers over the phone, and launched self-service options online for borrowers looking for help.

Because of these actions and more, we are observing resilience on the platform:

• | Total Prime performance is strong: approximately 90% of borrowers are not enrolled in hardship plans, repayment rates remain high, roll rates (the percentage of borrowers who progress into later delinquency stages) are low, and newer vintages are displaying higher credit quality and lower enrollment rates into our Skip-a-Pay program. In fact, roll rates for the non-Skip-a-Pay portion of the prime portfolio are currently lower than historical rates. |

• | The initial set of members who enrolled in our 2-month Skip-a-Pay program is beginning to graduate, and a higher percentage than forecasted (over 90%) have either made payments (nearly 60%) or have enrolled in a second round of Skip-a-Pay, with recent graduation vintages performing better than older graduation vintages. |

• | Since its launch on June 11th, the majority of members are now opting into interest-only hardship plans; we see this as an encouraging sign for both members (as they are taking proactive steps to stay on track) and investors (who will receive any partial payments). |

Given how unique the current environment is, we’ll be watching performance closely in the next several months.

Taking a step back, and looking across grade and term, we are currently estimating approximately a 3% internal rate of return (IRR) for vintages most exposed to the impacts of COVID-19 (loans facilitated from Q1 2018 to Q1 2020). We used a bottom-up approach to estimate losses and IRRs for these vintages: we considered actual performance to date for non-Skip-a-Pay loans, and performance from prior crises (hurricanes) to estimate future cash flows for loans currently in hardship. Our model expects losses to peak in Q4 2020 and Q1 2021 based on the structure and timing of hardship plans (which enable some portion of borrowers to return to current status, but also moves the period when investors will observe peak losses into the future as borrowers have more time to digest the impact on their finances).

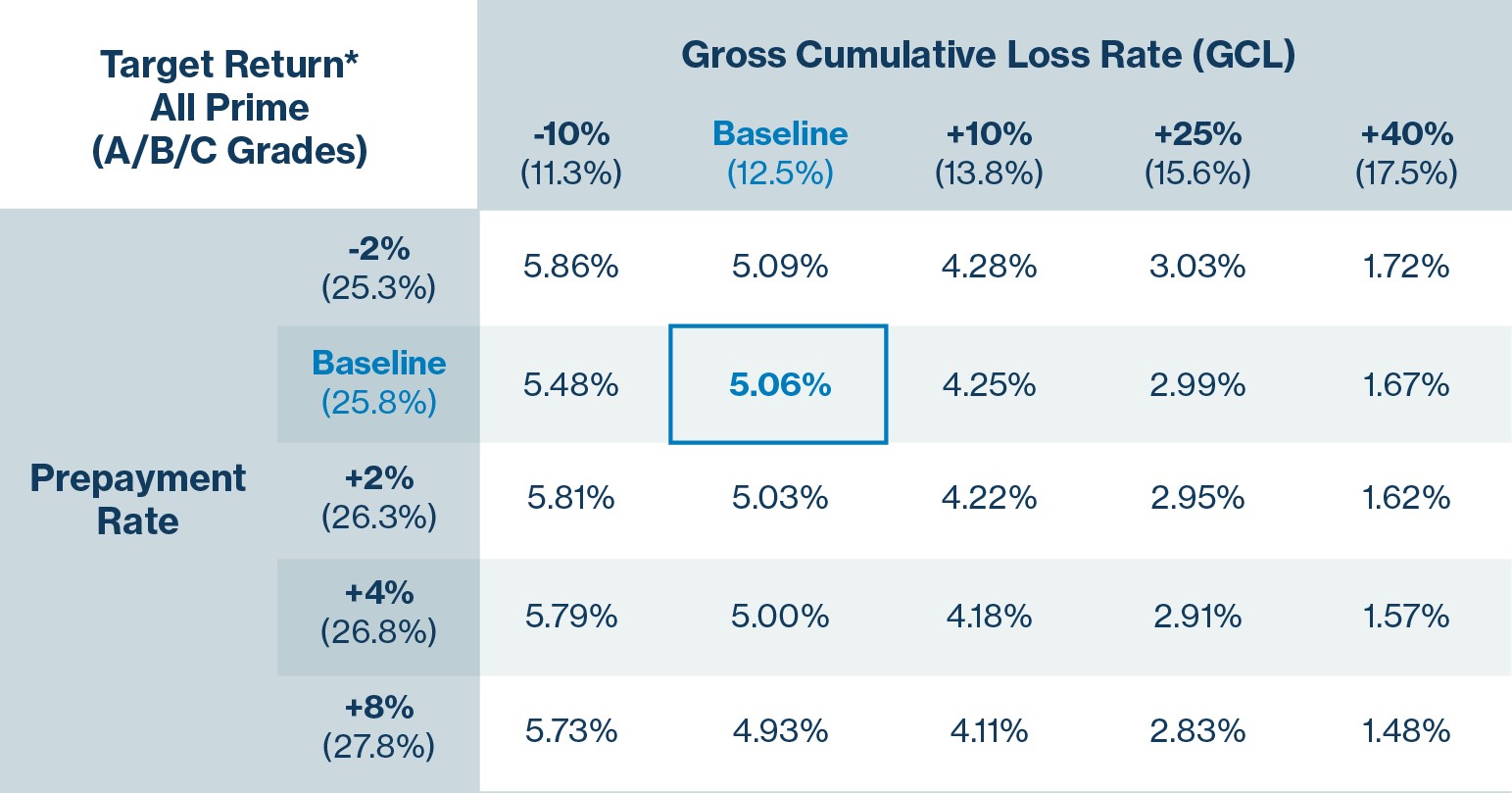

Looking ahead to potential performance for new loans being issued today, we are currently targeting an approximately 5% return for the total Prime portfolio. We believe this positions the portfolio competitively in a historically low yield environment.

This target also factors in the dramatic changes on the platform since the emergence of coronavirus (substantial credit cuts, interest rate increases, verification enhancements and more) as well as anticipated effects of the current macroeconomic outlook. We continue to utilize Moody’s economic scenarios to inform our models; their latest baseline scenario (as of June 2020) points to 9%+ unemployment until the second half of 2021. As a point of historical reference, we are reminded that following the 2008 recession, losses on consumer loans and credit cards came down faster than the unemployment rate, but only time will tell how this recession unfolds. It’s important to note that actual returns will be influenced by a variety of factors.

We’ve outlined the target return below (approximately 5% for the total Prime portfolio), plus two factors that could impact returns (prepayments and losses) to illustrate the sensitivities of returns to these key variables and provide an illustration of potential adverse impacts on returns.

*Target return is the return that LendingClub takes reasonable steps to achieve. Target return is not a promise of future results and may not accurately reflect actual returns. Target returns shown are generated utilizing an internal rate of return (IRR) methodology and reflect a number of assumptions. Actual returns experienced by any individual portfolio may be impacted by, among other things, the size and diversity of the portfolio, the exposure to any single Member Payment Dependent Note (Note) or loan, borrower or group of Notes, loans or borrowers, as well as macroeconomic conditions. Individual results may vary, and targets are subject to change. Target returns are based primarily on historical variance of previous targets to loss and prepayment rates in place at the time of facilitation since Q1 2015.

Conclusion

The environment is unprecedented and changes daily. Given the pace of change, we encourage all of our investors to reach out to us with any questions; we’re here to help and will navigate this together.

Safe Harbor Statement

Some of the statements above, including statements regarding the impact of credit and underwriting initiatives, loan performance, platform returns, borrower attributes (including the number and behavior of those enrolled in hardship plans), our ability to add and the timing of servicing and payment plan capabilities, our ability to successfully navigate the current economic climate the performance of the company and the impact of the coronavirus are “forward-looking statements.” The words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “outlook,” “plan,” “predict,” “project,” “will,” “would” and similar expressions may identify forward-looking statements, although not all forward-looking statements contain these identifying words. Factors that could cause actual results to differ materially from those contemplated by these forward-looking statements include the impact of global economic, political, market, health and social events or conditions, including the impact of the coronavirus, and those factors set forth in the section titled “Risk Factors” in our most recent Annual Report on Form 10-K, as filed with the Securities and Exchange Commission, as well as our subsequent reports on Form 10-Q each as filed with the Securities and Exchange Commission. We may not actually achieve the plans, intentions or expectations disclosed in forward-looking statements, and you should not place undue reliance on forward-looking statements. Actual results or events could differ materially from the plans, intentions and

expectations disclosed in forward-looking statements. We do not assume any obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Information in this blog post is not an offer to sell securities or the solicitation of an offer to buy securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction.