Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - LendingClub Corp | lc-12312015xex311.htm |

| EX-32.1 - EXHIBIT 32.1 - LendingClub Corp | lc-12312015xex321.htm |

| EX-21.1 - EXHIBIT 21.1 - LendingClub Corp | lc-12312015xex211.htm |

| EX-10.1 - EXHIBIT 10.1 - LendingClub Corp | lc-12312015xex101.htm |

| EX-23.1 - EXHIBIT 23.1 - LendingClub Corp | lc-12312015xex231.htm |

| EX-10.28 - EXHIBIT 10.28 - LendingClub Corp | lc-12312015xex1028.htm |

| EX-10.27 - EXHIBIT 10.27 - LendingClub Corp | lc-12312015xex1027.htm |

| EX-31.2 - EXHIBIT 31.2 - LendingClub Corp | lc-12312015xex312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

Commission File Number: 001-36771

LendingClub Corporation (Exact name of registrant as specified in its charter) |

Delaware | 51-0605731 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

71 Stevenson Street, Suite 300 | ||

San Francisco, California | 94105 | |

(Address of principal executive offices) | (Zip Code) | |

(415) 632-5600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class: | Name of each exchange on which registered: | |

Common Stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | ¨ | ||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter, was $4,097,335,594 based on the closing price reported for such date on the New York Stock Exchange. Shares of the registrant’s common stock held by each executive officer, director and holder of 10% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This calculation does not reflect a determination that certain persons are affiliates of the registrant for any other purpose.

As of February 18, 2016, there were 381,429,127 shares of the registrant’s common stock outstanding.

Documents Incorporated by Reference

Portions of the registrant’s Definitive Proxy Statement for the Registrant’s 2016 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K to the extent stated herein. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2015.

LENDINGCLUB CORPORATION

Annual Report On Form 10-K

For Fiscal Year Ended December 31, 2015

TABLE OF CONTENTS

LENDINGCLUB CORPORATION

Except as the context requires otherwise, as used herein, “Lending Club,” “Company,” “we,” “us,” and “our,” refer to LendingClub Corporation, a Delaware corporation, and, where appropriate, its two wholly owned subsidiaries:

• | LC Advisors, LLC (LCA), a registered investment advisor with the Securities and Exchange Commission (SEC) that acts as the general partner for certain private funds and as advisor to separately managed accounts. |

• | Springstone Financial, LLC (Springstone), a company that facilitates education and patient finance loans. |

LC Trust I (Trust) is an independent Delaware business trust that acquires loans from the Company and holds them for the sole benefit of certain investors that have purchased a trust certificate (Certificate) issued by the Trust and that are related to specific underlying loans for the benefit of the investor.

Forward-Looking Statements

This report contains forward-looking statements within the meaning of Section 29A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical facts, included in this Annual Report on Form 10-K (Report) regarding borrowers, credit scoring, Fair Isaac Corporation (FICO) or other credit scores, our strategy, future operations, expected losses, future financial position, future revenue, projected costs, prospects, plans, objectives of management and expected market growth are forward-looking statements. The words “anticipate,” “appear,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “target,” “will,” or similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

These forward-looking statements include, among other things, statements about:

• | the status of borrowers, the ability of borrowers to repay loans and the plans of borrowers; |

• | interest rates and origination fees on loans charged by issuing banks; |

• | expected rates of return for investors; |

• | the effectiveness of our platform’s credit scoring models; |

• | commitments or investments in loans to support: contractual obligations, such as to Springstone’s issuing bank for Pool B loans, regulatory commitments, such as direct mail, the testing of pilot loan programs, or customer accommodations; |

• | transaction fee or other revenue we expect to recognize after loans are issued by our issuing bank partners; |

• | our financial condition and performance, including the impact that management’s estimates have on our financial performance and the relationship between the interim period and full year results; |

• | investor, borrower, platform and loan performance-related factors that may affect our revenue; |

• | our ability to retain and hire employees and appropriately staff our operations; |

• | our ability to prevent security breaches, disruptions in service or comparable events that could compromise the personally identifiable or confidential information held in our data systems, reduce the attractiveness of the marketplace or adversely impact our ability to service loans; |

• | our ability to prevent and detect identity theft; |

• | our ability to develop and maintain effective internal controls; |

• | our compliance with applicable local, state and Federal laws; |

• | our compliance with applicable regulations and regulatory developments or court decisions affecting our marketplace; and |

• | other risk factors listed from time to time in reports we file with the SEC. |

1

LENDINGCLUB CORPORATION

We caution you that the foregoing list may not contain all of the forward-looking statements in this Report. We may not actually achieve the plans, intentions or expectations disclosed in forward-looking statements, and you should not place undue reliance on forward-looking statements. We have included important factors in the cautionary statements included in this Report, particularly in the “Risk Factors” section, that could, among other things, cause actual results or events to differ materially from forward-looking statements contained in this Report. Forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

You should read this Report carefully and completely and with the understanding that actual future results may be materially different from what we expect. We do not assume any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, other than as required by law.

2

LENDINGCLUB CORPORATION

PART I

Item 1. Business

Our Mission

Transforming the banking system to make credit more affordable and investing more rewarding.

Overview

Lending Club is the world’s largest online marketplace connecting borrowers and investors. We believe a technology-powered marketplace is a more efficient mechanism to allocate capital between borrowers and investors than the traditional banking system. Our marketplace substantially reduces the need for physical infrastructure and improves convenience and automation, which increases efficiency, reduces manual processes, and improves the overall borrower and investor experience.

Qualified consumers and small business owners borrow through Lending Club to lower the cost of their credit and enjoy a better experience than traditional bank lending. We believe the range of loan products we facilitate are simple, fair and responsible credit products that make it easier for consumers to budget for monthly repayment and meet their financial goals.

Investors use Lending Club to earn attractive risk-adjusted returns from an asset class that has generally been closed to many investors and only available on a limited basis to large institutional investors. The capital to invest in the loans enabled through our marketplace comes directly from a wide range of investors, including retail investors, high-net-worth individuals and family offices, banks and finance companies, insurance companies, hedge funds, foundations, pension plans and university endowments, and through a variety of investment channels.

We have developed our proprietary technology platform to support our marketplace and offer a variety of our issuing banks’ loan products to interested investors. Our proprietary technology automates key aspects of our operations, including the borrower application process, data gathering, credit decisioning and scoring, loan funding, investing and servicing, regulatory compliance and fraud detection. Our platform offers sophisticated analytical tools and data to enable investors to make informed decisions and assess their portfolios. Our extensible technology platform has allowed us to expand our offerings from personal loans to include small business loans, and to expand investor classes from individuals to institutions and create various investment vehicles.

We generate revenue from transaction fees from our marketplace’s role in accepting and decisioning applications for our bank partners to enable loan originations, servicing fees from investors for matching available loan assets with capital, and management fees from investment funds and other managed accounts. Our business model is not dependent on using our balance sheet and assuming credit risk for loans facilitated by our marketplace. In order to support contractual obligations (Pool B loans), regulatory commitments (direct mail), the testing of pilot loan programs, or customer accommodations, we may use our capital on the marketplace from time to time and on terms that are substantially similar to other investors.

As of December 31, 2015, our marketplace facilitated approximately $16.0 billion in loans since it first launched in 2007, of which approximately $3.3 billion were invested in through notes issued pursuant to a shelf registration statement (the Note Registration Statement), $5.5 billion were invested in through Certificates issued by the Trust, and $7.2 billion were invested in through whole loan sales.

3

LENDINGCLUB CORPORATION

Industry Background and Trends

We believe a transparent and open marketplace where borrowers and investors have access to information, complemented by technology and tools, can make credit more affordable, redirect existing pools of capital trapped inside the banking system, and attract new sources of capital to a new asset class. We believe that online marketplaces have the power to transform the traditional banking system, facilitate more efficient deployment of capital, and improve the global economy.

Personal and Small Business Lending Is Essential to the Economy

We believe the ability of individuals and small businesses to access affordable credit is essential to stimulating and sustaining a healthy, diverse and innovative economy. Lending to consumers provides financial flexibility and gives households better control over when and how to purchase goods and services. While borrower appetite for consumer and small business credit has typically remained strong in most economic environments, general economic factors and conditions, including the general interest rate environment and unemployment rates, may affect borrower willingness to seek loans and investor ability or desire to invest in loans.

Borrowers Are Inadequately Served by the Current Banking System

We believe the traditional banking system generally is burdened by its high fixed cost of underwriting and services, in part due to its physical infrastructure and labor- and paper-intensive business processes, compounded by an increasingly complex regulatory environment. As a result, we believe the traditional banking system is ill-suited to meet personal and small business demand for small balance loans and has instead relied heavily on issuing credit cards, which require less personalized underwriting and have higher interest rates. While credit cards are convenient as a payment mechanism, they are an expensive long-term financing solution. Borrowers who carry a balance on their cards are often subject to high, variable interest rates and the possibility of incurring additional fees and penalties. Additionally, many borrowers are charged the same high interest rates on their balances, regardless of an individual’s specific risk profile, so low-risk borrowers often subsidize high-risk borrowers. In the limited instances when traditional banks make personal loans available, the loan application process is often opaque, frustrating and time consuming.

Investors Have Had Limited Options to Participate in Personal and Small Business Credit

Historically, access to most personal and small business loans as an investment product was limited to the banks that hold loans on their balance sheet or to structured securitized products that were syndicated to large institutional investors. Depositors effectively fund the loans made by the banking system, but they share little in the direct returns of these loans as evidenced by the low yields on various fixed income investment or deposit products offered by banks. We believe many investors generally lack the size and access to invest in structured products directly and are unable to invest in personal and small business credit in a meaningful way. While institutional investors have had some access to this market, most have lacked the tools to customize portfolios to their specific risk tolerance, which is a feature of our marketplace and products. As a result, we believe additional capital that could be invested in personal and small business loans has largely been locked out of the market and may be available for use on our marketplace as an alternative to other similarly performing fixed asset investments.

Online Marketplaces Have Proliferated Throughout the Economy

Online marketplaces have emerged to connect buyers and sellers across many industries to increase choice, improve quality, accelerate the speed of decision making and lower costs. We believe a successful online marketplace must act as a trusted intermediary providing transparency, security, supply and demand balance, and ease of use to give marketplace participants an incentive to interact and the confidence to do business together. Initial online marketplaces connected buyers and sellers of goods and services – primarily moving demand from offline to online and making the transaction process more efficient. Online marketplaces have more recently evolved to unlock supply and demand that could not previously be matched in an efficient manner offline. The “sharing economy,” a

4

LENDINGCLUB CORPORATION

term that describes this new marketplace trend, enables a better use of resources by allowing owners of underutilized assets to offer them to people who want them while capturing an economic benefit.

Our Solution

We believe that our marketplace provides the following benefits to borrowers:

• | Access to Affordable Credit. Our innovative marketplace model, online delivery and process automation enable us to offer borrowers interest rates that are generally lower on average than the rates charged by traditional banks, credit cards or installment loans. |

• | Superior Borrower Experience. We offer a fast and easy-to-use online application process and provide borrowers with access to live support and online tools throughout the process and over the life of the loan. |

• | Transparency and Fairness. The installment loans offered through our marketplace feature a fixed rate that is clearly disclosed to the borrower during the application process, with fixed monthly payments, no hidden fees and the ability to prepay the balance at any time without penalty. Small business lines of credit have rates based upon the prime rate and allow borrowers to draw in increments, reducing their interest cost. Our platform utilizes an automated, rules-based engine for credit decisioning, which removes the human bias associated with reviewing applications. |

• | Fast and Efficient Decisioning. We leverage online data and technology to quickly assess risk, detect fraud, determine a credit rating and assign appropriate interest rates quickly. |

We believe that our marketplace provides the following benefits to investors:

• | Access to a New Asset Class. All investors can invest in personal loans facilitated through our standard loan program. Additionally, qualified investors can invest in loans facilitated through our custom program loan program in private transactions. These asset classes have historically been funded and held by financial institutions or large institutional investors on a limited basis. |

• | Attractive Risk-Adjusted Returns. We offer investors attractive risk-adjusted returns on loans offered through our marketplace. |

• | Transparency. We provide investors with transparency and choice in building their loan portfolios. |

• | Easy-to-Use Tools. We provide investors with tools to easily build and modify customized and diversified portfolios by selecting loans tailored to their investment objectives and to assess the returns on their portfolios. Investors can also enroll in automated investing, a free service that automatically invests any available cash in loans according to investor-specified criteria. |

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors and provide us with competitive advantages in realizing the potential of our market opportunity:

• | Leading Online Marketplace. We are the world’s largest online marketplace connecting borrowers and investors, based on approximately $16.0 billion in loan originations through December 31, 2015, of which approximately $3.3 billion were invested in through notes issued pursuant to the Note Registration Statement, $5.5 billion were invested in through certificates issued by the Trust and $7.2 billion were invested in through whole loan sales. |

5

LENDINGCLUB CORPORATION

• | Robust Network Effects. Our online marketplace exhibits network effects that are driven by the number of participants and investments enabled through our marketplace. More participation leads to greater potential to match borrowers with investors. Additionally, increased participation also results in the generation of substantial data that is used to improve the effectiveness of our credit decisioning and scoring models, enhancing our performance record and generating increasing trust in our marketplace. As trust increases, we believe investors will continue to demonstrate a willingness to accept lower risk premiums (all else being equal), which will allow us to offer lower interest rates and attract additional high-quality borrowers, thereby reinforcing our track record and fueling a virtuous cycle for our business. We believe that these network effects reinforce our market leadership position. |

• | High Borrower and Investor Satisfaction. Borrowers have validated our approach with an aggregate Net Promoter Score(1) in the 70s since we began surveying borrowers in January 2013, which places us at the upper end of customer satisfaction ratings for traditional financial service companies. Additionally, investors are confident transacting on our marketplace, as evidenced by high reinvestment rates. |

• | Technology Platform. Our technology platform powers our online marketplace and enables us to deliver innovative solutions to borrowers and investors. Our technology platform automates our operations and, we believe, provides a significant time and cost advantage over traditional banks that run on legacy systems that are inflexible and slow to evolve. |

• | Sophisticated Risk Assessment. We use proprietary algorithms that leverage behavioral data, transactional data and employment information to supplement traditional risk assessment tools, such as FICO scores. We have built our technology platform to automate the application of these proprietary algorithms to each individual borrower’s application profile at scale. This approach allows us to evaluate and segment each potential borrower’s risk profile and price the loan accordingly. In contrast, traditional lenders aggregate borrowers into large pools of risk profiles, which for some borrowers results in higher interest rates despite a more favorable credit profile. |

(1) | Net Promoter Score is a commonly used measure of customer loyalty and satisfaction, ranging from negative 100 to positive 100, based on direct questions to borrowers. |

Products

Borrowers

Our marketplace facilitates several types of loan products for consumers and small businesses.

Personal Loans. Our marketplace facilitates unsecured personal loans that can be used to make major purchases, refinance credit card balances or for other purposes, at generally lower rates than other alternatives. Personal loans are offered through both our standard and custom loan programs. Personal loans approved through our standard loan program include amounts from $1,000 to $35,000, maturities of three or five years, fixed interest rates, and no prepayment penalties or fees. These loans must meet certain minimum credit requirements, including a FICO score of at least 660, satisfactory debt-to-income ratios, 36 months of credit history and a limited number of credit inquiries in the previous six months. Personal loans that are approved through the standard loan program are offered to all investors on our marketplace. Personal loans that fall outside of the credit criteria for the standard program might qualify under our custom program and include amounts from $1,000 to $50,000, maturities of two, three, five or seven years, fixed interest rates and no prepayment penalties or fees.

Education and Patient Finance Loans. We facilitate unsecured education and patient installment loans and true no-interest loans through Springstone and its issuing bank partners. Installment loan terms include amounts from $2,000 to $50,000, maturities from 24 to 84 months, fixed interest rates and no prepayment penalties. The true no-interest loan terms include amounts ranging from $499 to $32,000 and no required interest payment if the balance is paid in full during the promotional period, which can be six, 12, 18 or 24 months. There is no prepayment penalty

6

LENDINGCLUB CORPORATION

and borrowers have the flexibility to pay as much or as little, subject to applicable minimums, of the outstanding balance during the promotional period as they choose. Education and Patient Finance loans are offered to private investors only and are not made publicly available on the marketplace.

Small Business Loans and Lines of Credit. In March 2014, we began facilitating unsecured small business loans, and in October 2015 we began facilitating small business lines of credit. Both of these loan products are offered through our marketplace in private transactions with qualified investors. These loan products enable small business owners to expand their business, purchase equipment or inventory, or meet other obligations at an affordable rate. Small business loans and lines of credit are fixed- or variable-rate loans in amounts ranging from $5,000 to $300,000, with maturities of 3 months to 5 years, and contain no prepayment penalties or fees. The small business lines of credit allow borrowers to draw funds in amounts they need, thus reducing their interest cost. Small Business loans are offered to private investors only and are not made publicly available on the marketplace.

Investors

Investors have the opportunity to invest in a wide range of loans based on term and credit characteristics. Personal loans that are approved through the standard loan program are offered to all investors on our marketplace, while custom program loans, which include small business, super prime, education and patient finance, new offerings, and loans that fall outside of the credit criteria of the standard program, are offered to private investors only and are not made publicly available on the marketplace. Investors receive monthly cash flow and attractive risk-adjusted returns. Investors are provided with a borrower’s proprietary credit grade and access to credit profile data on each approved loan as well as access to data on each listed loan and all of the historical performance data for nearly every loan ever invested in through our marketplace. The marketplace enables broad diversification by allowing distribution of investments in loans in increments as small as $25.

We attract a wide range of investors, including retail investors, high-net-worth individuals and family offices, banks and finance companies, insurance companies, hedge funds, foundations, pension plans and university endowments. We provide these investors with access to a variety of tools and products that seek to address their level of sophistication and desired level of interaction, which can range from low-touch self-directed accounts to high-touch funds and managed accounts. Investors can invest in loans through one or all of the following channels:

Notes: We issue notes pursuant to an effective Note Registration Statement. Investors who meet the applicable financial suitability requirements and have completed our investor account opening process may purchase unsecured, borrower payment dependent notes that correspond to payments received on an underlying standard program loan selected by the investor. When an investor registers with us, the investor enters into an investor agreement with us that governs the investor’s purchases of notes. Our note channel is supported by our website and our investor services group, which provides basic customer support to these investors.

Certificates and Investment Funds: Accredited investors and qualified purchasers may establish a relationship with LCA or another third-party advisor in order to indirectly invest in certificates, or they may directly purchase a certificate or a limited partnership interest in one of six private funds that purchase certificates. The certificates are issued by the Trust and are unsecured and settled with cash flows from underlying loans selected by the investor. Neither certificates nor limited partnership interests can be purchased through our website. Certificate investors typically seek to invest larger amounts as compared to the average note investors and often desire a more “hands off” approach to investing. Investors in certificates generally pay an asset-based management fee instead of cash flow-based servicing fee paid by note investors.

Whole Loan Purchases: Certain institutional investors, such as banks, seek to hold the actual loan on their balance sheet. To meet this need, we sell entire standard or custom program loans to these investors through purchase agreements. Upon the sale of the loan, the investor owns all right, title and interest in the loan. We establish the investors’ accounts and the procedures for the purchase of loans, including any purchase amount limitations, which we control in our discretion. We and the investor also make limited representations and warranties and agree to

7

LENDINGCLUB CORPORATION

indemnify each other for breaches of the purchase agreement. The investor also agrees to simultaneously enter into a servicing agreement with us which designates us as the loan servicer for the sold loan. We continue to service these loans after they are sold and can only be removed as the servicer in limited circumstances. For regulatory purposes, the investor also has access to the underlying borrower information, but is prohibited from contacting or marketing to the borrower in any manner and agrees to hold such borrower information in compliance with all applicable privacy laws. Whole loan purchases are attractive for some investors as it enables them to account for the loan as an asset, which can offer favorable financial reporting and capital reserve treatment.

We believe our strategy of pursuing a diverse investor base will continue to support the growth of our marketplace and our ability to facilitate a wide variety of loans through a range of business and economic conditions. For all investment channels, we agree to repurchase the loans in cases of confirmed identity theft. While our business model is not dependent on using our balance sheet and assuming credit risk, we use our capital on the marketplace from time to time to support contractual obligations (Pool B loans), regulatory commitments (direct mail), the testing of pilot loan programs, or customer accommodations.

Credit Decisioning and Scoring Process

Our marketplace provides an integrated and automated loan application and credit decisioning and scoring process that is extensible to a variety of loan products. Borrowers come to our platform to apply online for a loan. During the simple application process, our platform uses proprietary risk algorithms that leverage behavioral data, transactional data and employment information to supplement traditional risk assessment tools, such as FICO scores, to assess a borrower’s risk profile. The platform then presents an approved borrower with various loan options, including term, rate and amount, for which they qualify. Once the borrower selects the desired loan terms, the rest of the application is completed. Our verification processes and teams then verify the borrower’s identity, income or employment by connecting to various data sources, directly or through third-party service providers, or by contacting the human resources department of the borrower’s stated employer to determine whether to approve the loan request.

Technology

Key elements of our technology include:

• | Highly Automated. Our borrower and investor acquisition process, registration, credit decisioning and scoring, servicing and payment systems are highly automated using our internally developed software. We developed our own cash management software to process electronic cash movements, record book entries and calculate cash balances in our borrower and investor fund accounts. In nearly all payment transactions, an Automated Clearing House (ACH) electronic payment network is used to disburse loan proceeds, collect borrower loan payments on outstanding loans, receive funds from investors and disburse payments to investors. |

• | Scalable Platform. Our scalable infrastructure utilizes standard techniques, such as virtualization, load-balancing and high-availability platforms. Our application and database tiers are designed to be scaled horizontally by adding additional servers as needed. |

• | Proprietary Fraud Detection. We use a combination of third-party data, sophisticated analytical tools and current and historical data obtained during the loan application process to help determine fraud risk. High-risk loan applications are subject to further investigation. In cases of confirmed fraud, the application is cancelled, and we identify and flag characteristics of the loan application to help refine our fraud detection efforts. |

• | Data Integrity and Security. We maintain an effective information security program based on well-established security standards and best practices, including ISO2700x and NIST 800 series. The program establishes policies and procedures to safeguard the confidentiality, integrity and availability of borrower |

8

LENDINGCLUB CORPORATION

and investor information. The program also addresses risk assessment, training, access control, encryption, service provider oversight, an incident response program and continuous monitoring and review.

• | Application Programming Interface. Our application programming interface, referred to as our API, provides investors and partners access to publicly available loan attributes and allows them to analyze the data and place orders meeting their criteria without visiting our website. Investors and partners may create their own software that uses our API or they may use a variety of third-party services that invest via our API. |

• | Lending Club Open Integration. In August 2015, we launched Lending Club Open Integration (LCOI). LCOI allows online advisors and broker-dealers to offer Lending Club investments quickly and easily to their client bases, using a suite of API services that integrate directly into their websites. This allows these advisors and broker-dealers to provide the same functionality that currently exists on our website, including money movement, investing, reinvesting, real-time reporting of cash and holdings, and tax reporting. |

Relationships with Issuing Bank Partners

Loans facilitated through our marketplace are originated by our issuing bank partners. Our primary issuing bank is WebBank, a Utah-chartered industrial bank that handles a variety of consumer and commercial financing programs. Additionally, we rely on NBT Bank and Comenity Capital Bank as issuing banks for our education and patient finance loans. We also have an agreement with Cross River Bank, a New Jersey chartered bank, to operate as our back-up issuing bank in the event WebBank can no longer be an issuing bank.

We have entered into a loan account program agreement with WebBank that governs the terms and conditions between us and WebBank with respect to loans facilitated through our marketplace and originated by WebBank, including our obligations for servicing the loans during the period of time that the loans are owned by WebBank. Under the terms of the loan account program agreement, we pay WebBank a monthly program fee based on the amount of loans issued by WebBank and purchased by us or our partners in a given month, subject to a minimum monthly fee. Effective in October 2014 WebBank retains ownership of all loans for two business days and earns interest on the loans during that time. WebBank pays us a transaction fee for our role in processing loan applications through our marketplace on WebBank’s behalf. Under a loan sale agreement, WebBank sells us the loan without recourse two business days after WebBank originates the loan. The loan sale agreement prohibits us from securitizing the loans without prior written consent of WebBank. The loan account program agreement and the loan sale agreement terminate in November 2018, with two automatic, one-year renewal terms, subject to certain early termination provisions as set forth in the agreements.

Our issuing banks for education and patient finance loans originate, retain and service each education and patient finance loan issued. For our role in loan facilitation, we earn transaction fees paid by the issuing bank and education and patient service providers at the time of origination by the issuing bank. Currently, we do not earn any servicing fees, as loans are originated, retained and serviced by the issuing bank. We currently intend to continue to have these loans funded and serviced through these existing issuing banks while we develop plans to integrate qualifying loans into our standard loan program over time.

9

LENDINGCLUB CORPORATION

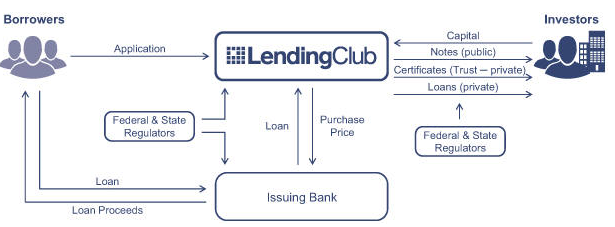

Loan Issuance Mechanism

We have developed an extensible, automated platform that allows us to work with issuing banks to originate and issue a variety of loan products to an array of borrowers. Our service is provided in a seamless fashion to the borrowers. A borrower comes to our website and completes a simple application for a loan product. We then use proprietary risk algorithms to analyze an applicant’s risk profile based upon the issuing bank’s underwriting guidelines. Once a loan application is approved, we present the borrower with various loan options. After the applicant selects their personalized financing option and completes the application process, the loan is listed on our marketplace to attract investor commitments, while we simultaneously perform additional verifications on the borrower. Once the verifications are completed and sufficient investor commitments are received, the issuing bank originates and issues the loan to the borrower, net of the origination fee charged and retained by the issuing bank. After the loan is issued, we use the proceeds from these investors to purchase the loan. Investor cash balances (excluding payments in process) are held in a segregated bank or custodial accounts and are not commingled with our monies. We receive a transaction fee from the issuing bank for our marketplace’s role in originating the loan. We also earn a recurring servicing fee from investors and management fees from investment funds and other managed accounts.

Loan Servicing

We service all loans facilitated through our marketplace, except for patient and education finance loans. Servicing is comprised of account maintenance, collections, processing payments from borrowers and distributions to investors. We have made arrangements for limited backup servicing with Portfolio Financial Servicing Company.

For the month of December 2015, approximately 99% of loan payments for loans that we service were made through an ACH withdrawal from the borrower’s bank account. Principal and interest payments on loans are remitted utilizing ACH. We also maintain segregated bank accounts for the benefit of investors, custodial or other accounts designated by our investors. This automated process allows us to avoid the time and expense of processing a significant volume of mailed payments and provides a higher degree of certainty for timely payments. This process also provides us with prompt notice in the event of a missed payment, which allows us to respond quickly to resolve the delinquency with the borrower. Generally, in the first 30 days that a loan is delinquent, our in-house collections team works to bring the account current. Once the loan becomes more than 30 days delinquent, we will typically outsource subsequent servicing efforts to third-party collection agencies.

The servicing fee paid by investors is designed to cover the day-to-day processing costs of loans. If a loan needs more intensive collection focus, whether internal or external, we may charge investors a collection fee to compensate us for the costs of this collection activity. This fee varies, with a maximum of up to 35% of the amount recovered. There is no fee charged if there are no loan payments recovered, and the fee cannot exceed any proceeds collected. We sell loans that have been charged-off to certain third parties. All proceeds received on these sales are subject to a collection fee, and the net proceeds are distributed to investors.

10

LENDINGCLUB CORPORATION

Springstone Acquisition

In April 2014, we acquired all of the outstanding limited liability company interests of Springstone, which offers education and patient finance loans. We utilize two issuing banks and a network of providers to facilitate the issuance of education and patient finance installment loans and true no-interest loans, as described above.

Competition

We compete with financial products and companies that attract borrowers, investors or both. With respect to borrowers, we primarily compete with traditional financial institutions, such as banks, credit unions, credit card issuers and other consumer finance companies. We believe our innovative marketplace model, online delivery and process automation enable us to operate more efficiently and with more competitive rates and higher borrower satisfaction than these competitors.

With respect to investors, we primarily compete with other investment vehicles and asset classes, such as equities, bonds and short-term fixed income securities. We believe that our diverse and customizable investment options give us the flexibility to offer attractive risk-adjusted returns that are generally uncorrelated with other asset classes.

We compete with other online credit marketplaces, such as Prosper Marketplace, Inc., as well as with other online lenders. We are the world’s largest online marketplace connecting borrowers to investors, which we believe provides us with a major competitive advantage. We believe that our network effects and marketplace dynamics at play make us more attractive and efficient to both borrowers and investors. We anticipate that more established internet, technology and financial services companies that possess large, existing customer bases, substantial financial resources and established distribution channels may enter the market in the future. We believe that our brand, scale, network effect, historical data and performance record provide us with significant competitive advantages over current and future competitors.

Sales and Marketing

Our marketing efforts are designed to attract and retain borrowers and investors and build brand awareness and reputation. Currently, we believe reputation, word of mouth and our direct marketing via mail drives continued organic growth in our investor and borrower base. We believe most of our marketplace investors are satisfied with their experience, often adding funds to their account and referring their friends and colleagues to us.

Regulatory and Compliance Framework

Our marketplace provides a compliance framework that allows investors to participate in consumer and commercial credit as an asset class. We believe that our relationship with issuing banks is a key component of our compliance framework.

As part of our ongoing compliance program, we have customer identification processes in place to enable us to identify user identification fraud and compare user identity against applicable governmental lists, such as the Office of Foreign Assets Control (OFAC) and the Financial Crimes Enforcement Network. We compare all users’ identities against these lists at least twice a month for continued compliance and oversight. If a user were to appear on a list, we would take appropriate action to resolve the issue. In addition to our continued identification compliance program, we use our proprietary technology to assist us in complying with applicable federal anti-money laundering laws.

Regulations and Licensing

The lending and securities industries are highly regulated. We are regulated differently than a bank as banks are exposed to capital risk from both credit and interest rate risks, whereas for loans issued through our marketplace loan balances, interest rates and maturities are matched and offset by an equal balance of notes and certificates.

11

LENDINGCLUB CORPORATION

Additionally, we do not take deposits and are therefore not regulated by the FDIC in that respect. Our current issuing banks originate all of the loans offered through our marketplace and are subject to regulation by the FDIC or other relevant federal and state regulators.

The Company and the loans made through our marketplace are subject to extensive and complex rules and regulations, licensing and examination by various federal, state and local government authorities. Our primary issuing bank, WebBank, is subject to oversight by the FDIC and the State of Utah. These authorities impose obligations and restrictions on our activities and the loans facilitated through our marketplace. For example, these rules limit the fees that may be assessed on the loans, require extensive disclosure to, and consents from, the borrowers and lenders, prohibit discrimination and unfair and deceptive acts or practices and may impose multiple qualification and licensing obligations on our activities. Failure to comply with any of these requirements may result in, among other things, revocation of required licenses or registration, loss of approved status, voiding of the loan contracts, class action lawsuits, administrative enforcement actions and civil and criminal liability. While compliance with such requirements is at times complicated by our novel business model, we believe we are in substantial compliance with these rules and regulations.

State Licensing Requirements

In most states we believe that the applicable issuing bank, as originator of loans facilitated through our marketplace, satisfies any relevant licensing requirements with respect to the origination of loans applicable to our operations. As needed, we seek authorizations to conduct activities on a uniform basis in all other states and the District of Columbia, with the exception of Iowa. State licensing statutes impose a variety of requirements and restrictions on us, including:

• | record-keeping requirements; |

• | restrictions on servicing practices, including limits on finance charges and fees; |

• | disclosure requirements; |

• | examination requirements; |

• | surety bond and minimum net worth requirements; |

• | financial reporting requirements; |

• | notification requirements for changes in principal officers, stock ownership or corporate control; |

• | restrictions on advertising; and |

• | review requirements for loan forms. |

The statutes also subject us to the supervisory and examination authority of state regulators in certain cases.

Consumer Protection Laws

State Usury Limitations. Section 521 of the Depository Institution Deregulation and Monetary Control Act of 1980 (DIDA) and Section 85 of the National Bank Act (NBA), federal case law interpreting the NBA such as Tiffany v. National Bank of Missouri and Marquette National Bank of Minneapolis v. First Omaha Service Corporation and FDIC advisory opinion 92-47 permit FDIC-insured depository institutions, such as WebBank, to “export” the interest rate permitted under the laws of the state or U.S. territory where the bank is located, regardless of the usury limitations imposed by the state law of the borrower’s residence unless the state has chosen to opt out of the exportation regime. WebBank is located in Utah, and Title 70C of the Utah Code does not limit the amount of fees or interest that may be charged by WebBank on loans of the type offered through our marketplace. Only Iowa and Puerto Rico have opted out of the exportation regime under Section 525 of DIDA and we do not operate in either jurisdiction. We believe, however, if a state or U.S. territory in which we operate opted out of rate exportation, judicial interpretations support the view that such opt outs would apply only to loans “made” in those states. We believe that the “opt-out” of any state would not affect the ability of our marketplace to benefit from the exportation of rates. If a loan made through our marketplace were deemed to be subject to the usury laws of a state or U.S. territory that had opted-out of the exportation regime, we could become subject to fines, penalties and possible

12

LENDINGCLUB CORPORATION

forfeiture of amounts charged to borrowers, and we could decide not to originate loans in that jurisdiction, which could adversely impact our growth.

State Disclosure Requirements and Other Substantive Lending Regulations. We are subject to state laws and regulations that impose requirements related to loan disclosures and terms, credit discrimination, credit reporting, debt collection and unfair or deceptive business practices. Our ongoing compliance program seeks to comply with these requirements.

Truth in Lending Act. The Truth in Lending Act (TILA), and Regulation Z, which implements it, require lenders to provide consumers with uniform, understandable information concerning certain terms and conditions of their loan and credit transactions. These rules apply to WebBank as the creditor for loans facilitated through our marketplace, but because the transactions are carried out on our hosted website, we facilitate compliance. For closed-end credit transactions of the type provided through our marketplace, these disclosures include, among others, providing the annual percentage rate, the finance charge, the amount financed, the number of payments and the amount of the monthly payment. The creditor must provide the disclosures before the loan is closed. TILA also regulates the advertising of credit and gives borrowers, among other things, certain rights regarding updated disclosures and the treatment of credit balances. Our marketplace provides borrowers with a TILA disclosure at the time a borrower posts a loan request on the marketplace. If the borrower’s request is not fully funded and the borrower chooses to accept a lesser amount offered, we provide an updated TILA disclosure. We also seek to comply with TILA’s disclosure requirements related to credit advertising.

Equal Credit Opportunity Act. The federal Equal Credit Opportunity Act (ECOA) prohibits creditors from discriminating against credit applicants on the basis of race, color, sex, age, religion, national origin, marital status, the fact that all or part of the applicant’s income derives from any public assistance program or the fact that the applicant has in good faith exercised any right under the federal Consumer Credit Protection Act or any applicable state law. Regulation B, which implements ECOA, restricts creditors from requesting certain types of information from loan applicants and from using advertising or making statements that would discourage on a prohibited basis a reasonable person from making or pursuing an application. These requirements apply both to a lender such as WebBank as the creditor for loans facilitated through our marketplace as well as to a party such as ourselves that regularly participates in a credit decision. Investors may also be subject to the ECOA in their capacity as purchasers of notes if they are deemed to regularly participate in credit decisions. In the underwriting of loans offered through our marketplace, and in all aspects of operations, both WebBank and we seek to comply with ECOA’s provisions prohibiting discouragement and discrimination. ECOA also requires creditors to provide consumers and certain small businesses with timely notices of adverse action taken on credit applications. WebBank and we provide prospective borrowers who apply for a loan through our marketplace but are denied credit with an adverse action notice in compliance with applicable requirements.

Fair Credit Reporting Act. The federal Fair Credit Reporting Act (FCRA), as amended by the Fair and Accurate Credit Transactions Act, administered by the Consumer Financial Protection Bureau (CFPB), promotes the accuracy, fairness and privacy of information in the files of consumer reporting agencies. FCRA requires a permissible purpose to obtain a consumer credit report and requires persons to report loan payment information to credit bureaus accurately. FCRA also imposes disclosure requirements on creditors who take adverse action on credit applications based on information contained in a credit report. WebBank and we have a permissible purpose for obtaining credit reports on potential borrowers, and we also obtain explicit consent from borrowers to obtain such reports. As the servicer for the loan, we accurately report loan payment and delinquency information to appropriate consumer reporting agencies. We provide an adverse action notice to a rejected borrower on WebBank’s behalf at the time the borrower is rejected that includes all the required disclosures. We also have processes in place to ensure that consumers are given “opt-out” opportunities, as required by the FCRA, regarding the sharing of their personal information. We have implemented an identity theft prevention program.

Fair Debt Collection Practices Act. The federal Fair Debt Collection Practices Act (FDCPA) provides guidelines and limitations on the conduct of third-party debt collectors in connection with the collection of consumer debts. The FDCPA limits certain communications with third parties, imposes notice and debt validation requirements, and

13

LENDINGCLUB CORPORATION

prohibits threatening, harassing or abusive conduct in the course of debt collection. While the FDCPA applies to third-party debt collectors, debt collection laws of certain states impose similar requirements on creditors who collect their own debts. In addition, the CFPB prohibits unfair, deceptive or abusive acts or practices in debt collection, including first-party debt collection. Our agreement with investors prohibits investors from attempting to collect directly on the loan. Actual collection efforts in violation of this agreement are unlikely given that investors do not learn the identity of borrowers. We use our internal collection team and a professional third-party debt collection agent to collect delinquent accounts. They are required to comply with the FDCPA and all other applicable laws in collecting delinquent accounts of our borrowers.

Privacy and Data Security Laws. The federal Gramm-Leach-Bliley Act (GLBA) includes limitations on financial institutions’ disclosure of nonpublic personal information about a consumer to nonaffiliated third parties, in certain circumstances requires financial institutions to limit the use and further disclosure of nonpublic personal information by nonaffiliated third parties to whom they disclose such information and requires financial institutions to disclose certain privacy policies and practices with respect to information sharing with affiliated and nonaffiliated entities as well as to safeguard personal customer information. We have a detailed privacy policy, which complies with GLBA and is accessible from every page of our website. We maintain consumers’ personal information securely, and we do not sell, rent or share such information with third parties for marketing purposes unless previously agreed to by the consumer. In addition, we take measures to safeguard the personal information of our borrowers and investors and protect against unauthorized access to this information.

Servicemembers Civil Relief Act. The federal Servicemembers Civil Relief Act (SCRA) allows military members to suspend or postpone certain civil obligations so that the military member can devote his or her full attention to military duties. The SCRA requires us to adjust the interest rate of borrowers who qualify for and request relief. If a borrower with an outstanding loan qualifies for SCRA protection, we will reduce the interest rate on the loan to 6% for the duration of the borrower’s active duty. During this period, the investors who have invested in such a loan will not receive the difference between 6% and the loan’s original interest rate. For a borrower to obtain an interest rate reduction on a loan due to military service, we require the borrower to send us a written request and a copy of the borrower’s mobilization orders. We do not take military service into account in assigning loan grades to borrower loan requests and we do not disclose the military status of borrowers to investors.

The Dodd-Frank Wall Street Reform and Consumer Protection Act. In July 2010, the Dodd-Frank Act was signed into law. The Dodd-Frank Act is extensive and significant legislation that includes consumer protection provisions. Among other things, the Dodd-Frank Act created the CFPB, which commenced operations in July 2011 and has authority to write regulations under federal consumer financial protection laws, such as the Truth in Lending Act and the Equal Credit Opportunity Act, and to enforce those laws against and examine large financial institutions, such as our issuing banks, for compliance. The CFPB is authorized to prevent “unfair, deceptive or abusive acts or practices” through its regulatory, supervisory and enforcement authority. We are subject to the CFPB’s jurisdiction, including its enforcement authority, as a servicer and acquirer of consumer credit. The CFPB may request reports concerning our organization, business conduct, markets and activities. The CFPB may also conduct on-site examinations of our business on a periodic basis if the CFPB were to determine, through its complaint system, that we were engaging in activities that pose risks to consumers.

Other Regulations

Electronic Fund Transfer Act and NACHA Rules. The federal Electronic Fund Transfer Act (EFTA) and Regulation E that implements it provide guidelines and restrictions on the electronic transfer of funds from consumers’ bank accounts. In addition transfers performed by ACH electronic transfers are subject to detailed timing and notification rules and guidelines administered by the National Automated Clearinghouse Association (NACHA). Most transfers of funds in connection with the origination and repayment of loans are performed by ACH. We obtain necessary electronic authorization from borrowers and investors for such transfers in compliance with such rules. We also comply with the requirement that a loan cannot be conditioned on the borrower’s agreement to repay the loan through automatic fund transfers. Transfers of funds through our platform are executed by Wells Fargo and conform to the EFTA, its regulations and NACHA guidelines.

14

LENDINGCLUB CORPORATION

Electronic Signatures in Global and National Commerce Act/Uniform Electronic Transactions Act. The federal Electronic Signatures in Global and National Commerce Act (ESIGN), and similar state laws, particularly the Uniform Electronic Transactions Act (UETA), authorize the creation of legally binding and enforceable agreements utilizing electronic records and signatures. ESIGN and UETA require businesses that want to use electronic records or signatures in consumer transactions and provide disclosures to consumers, to obtain the consumer’s consent to receive information electronically. When a borrower or investor registers on our platform, we obtain his or her consent to transact business electronically, receive electronic disclosures and maintain electronic records in compliance with ESIGN and UETA requirements.

Bank Secrecy Act. In cooperation with WebBank, we have implemented various anti-money laundering policy and procedures to comply with applicable federal law. With respect to new borrowers, we apply the customer identification and verification program rules and screen names against the list of specially designated nationals maintained by the U.S. Department of the Treasury and OFAC pursuant to the USA PATRIOT Act amendments to the Bank Secrecy Act and its implementing regulation.

New Laws and Regulations. From time to time, various types of federal and state legislation are proposed and new regulations are introduced that could result in additional regulation of, and restrictions on, the business of consumer lending. We cannot predict whether any such legislation or regulations will be adopted or how this would affect our business or our important relationships with third parties. In addition, the interpretation of existing legislation may change or may prove different than anticipated when applied to our novel business model. Compliance with such requirements could involve additional costs, which could have a material adverse effect on our business. As a consequence of the extensive regulation of commercial lending in the United States, our business is particularly susceptible to being affected by federal and state legislation and regulations that may increase the cost of doing business.

In addition, see “Item 1A – Risk Factors – Risks Related to Our Business and Regulation.”

Foreign Laws and Regulations. We do not permit non-U.S. based individuals to register as borrowers on the platform and the lending platform does not operate outside the United States. Therefore, we do not believe that we are subject to foreign laws or regulations for borrowers.

Intellectual Property

To establish and protect our technology and intellectual property rights, we rely on a combination of copyright, trade secret and other rights, as well as confidentiality procedures, non-disclosure agreements with third parties, employee disclosure and invention assignment agreements, and other contractual rights. Despite our efforts to protect our proprietary rights, third parties may, in an authorized or unauthorized manner, attempt to use, copy or otherwise obtain and market or distribute our intellectual property rights or technology or otherwise develop a product with the same functionality as our solution. In addition, our competitors may develop products that are similar to our technology. Policing all unauthorized use of our intellectual property rights is nearly impossible, and we cannot be certain that the steps we have taken or will take in the future will prevent misappropriations of our technology or intellectual property rights.

Employees

At December 31, 2015, we had 1,382 employees and contract employees. None of our employees are represented by a labor union. We have not experienced any work stoppages, and we consider our employee relations to be good.

Available Information

Our website address is www.lendingclub.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed pursuant to Section 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act), are filed with the U.S. Securities and Exchange Commission

15

LENDINGCLUB CORPORATION

(SEC). We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements and other information with the SEC. Such reports and other information filed by the Company with the SEC are available free of charge on our website at ir.lendingclub.com when such reports are available on the SEC’s website. We use our investor relations website as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD.

The public may read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

The contents of the websites referred to above are not incorporated into this filing. Further, our references to the URLs for these websites are intended to be inactive textual references only.

16

LENDINGCLUB CORPORATION

Item 1A. Risk Factors

You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report on Form 10-K, including the section titled “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes. While we believe the risks and uncertainties described below include all material risks currently known by us, it is possible that these may not be the only ones we face. If any of the risks actually occur, our business, financial condition, operating results and prospects could be materially and adversely affected.

RISKS RELATED TO OUR BUSINESS AND REGULATION

If we are unable to maintain our relationships with issuing banks, our business will suffer.

We rely on issuing banks to originate all loans and to comply with various federal, state and other laws. Our primary issuing bank is WebBank, a Utah-chartered industrial bank that handles a variety of consumer and commercial financing programs. Springstone Financial, LLC (Springstone), our wholly-owned subsidiary, relies on NBT Bank and Comenity Capital Bank as issuing banks for its education and patient finance loans.

Our agreements with WebBank are non-exclusive and do not prohibit WebBank from working with our competitors or from offering competing services. Our current agreements with WebBank have initial terms ending in November 2018, with two automatic, one-year renewal terms, subject to certain early termination provisions as set forth in the agreements. WebBank currently offers loan programs through another online marketplace. WebBank could decide that working with us is not in its interest, could make working with it cost prohibitive or could decide to enter into exclusive or more favorable relationships with our competitors. In addition, WebBank may not perform as expected under our agreements including potentially being unable to accommodate our projected growth in loan volume. We could in the future have disagreements or disputes with WebBank, which could negatively impact or threaten our relationship.

WebBank is subject to oversight by the FDIC and the State of Utah and must comply with complex rules and regulations, licensing and examination requirements, including requirements to maintain a certain amount of regulatory capital relative to its outstanding loans. We are a service provider to WebBank, and as such, we are subject to audit by WebBank in accordance with FDIC guidance related to management of third-party vendors. We may also be subject to the examination and enforcement authority of the FDIC as a bank service company covered by the Bank Service Company Act. If WebBank were to suspend, limit or cease its operations or our relationship with WebBank were to otherwise terminate, we would need to implement a substantially similar arrangement with another issuing bank, obtain additional state licenses or curtail our operations. Although we currently have a non-exclusive arrangement with Cross River Bank, another issuing bank, to date Cross River Bank has not originated any loans through our platform. If we need to enter into alternative arrangements with a different issuing bank to replace our existing arrangements, we may not be able to negotiate a comparable alternative arrangement. Transitioning loan originations to a new issuing bank is untested and may result in delays in the issuance of loans or, if our platform becomes inoperable, may result in our inability to facilitate loans through our platform. If we were unable to enter in an alternative arrangement with a different issuing bank, we would need to obtain a state license in each state in which we operate to enable us to originate loans, as well as comply with other state and federal laws, which would be costly and time-consuming. If we are unsuccessful in maintaining our relationships with WebBank or other issuing banks, our ability to provide loan products could be materially impaired and our operating results would suffer.

17

LENDINGCLUB CORPORATION

The regulatory framework for our business is evolving and uncertain as federal and state governments consider new laws to regulate online marketplaces such as ours. New laws and regulations, including taxes on services provided by us, as well as continued uncertainty regarding potential new laws or regulations, may negatively affect our business.

The regulatory framework for online marketplaces such as ours is evolving and uncertain. It is possible that new laws and regulations will be adopted in the United States and internationally, or existing laws and regulations may be interpreted in new ways, that would affect the operation of our marketplace and the way in which we interact with borrowers and investors.

Recognizing the growth in online marketplaces such as ours, in July 2015 the U.S. Treasury Department issued a request for information (RFI) to study the various business models and products offered by online marketplace lenders, the potential for online marketplace lending to expand access to credit to historically underserved borrowers and how the financial regulatory framework should evolve to support the safe growth of the industry. The RFI sought information about a number of topics, including how credit marketplaces manage the risk of fraud and security breaches, how they protect consumers against scams or default, how much investors in the loans rely on borrowed money, and whether the lenders should have to retain some risk relating to the loans they originate or underwrite. We, along with many other interested groups, submitted responses to the Treasury’s RFI by the September 30, 2015 deadline. In December 2015, the California Department of Business Oversight sent an online survey to fourteen marketplace lenders, including us, requesting information about our business model, online platform, loan performance and investor funding process.

Although the Treasury Department and California Department of Business Oversight are in the information-gathering stage and no interpretive guidance has been released, there is a possibility that our business may become subject to additional or different regulations in the future. The cost and complexity to comply with new laws or regulations could be significant and result in the need to modify our operations and increase our operating expenses, and we may be unable to pass any such costs on to borrowers and investors.

A decline in economic conditions may adversely affect our customers, which may negatively impact our business and results of operations.

As a credit marketplace, we believe our customers are more highly susceptible to uncertainties and negative trends, real or perceived, in the markets driven by, among other factors, general economic conditions in the United States and abroad. These external economic conditions and resulting trends or uncertainties could adversely impact our customer's ability or desire to participate on our marketplace as borrowers or investors, and consequently could negatively affect our business and results of operations.

There continues to be uncertainty as to how the CFPB’s actions or the actions of any other new agency could impact our business or that of our issuing banks.

The CFPB, which commenced operations in July 2011, has broad authority over the businesses in which we engage. This includes authority to write regulations under federal consumer financial protection laws, such as the Truth in Lending Act and the Equal Credit Opportunity Act, and to enforce those laws against and examine large financial institutions, such as our issuing banks, for compliance. The CFPB is authorized to prevent “unfair, deceptive or abusive acts or practices” through its regulatory, supervisory and enforcement authority. To assist in its enforcement, the CFPB maintains an online complaint system that allows consumers to log complaints with respect to various consumer finance products, including the loan products we facilitate. This system could inform future CFPB decisions with respect to its regulatory, enforcement or examination focus.

We are subject to the CFPB’s jurisdiction, including its enforcement authority, as a servicer and acquirer of consumer credit. The CFPB may request reports concerning our organization, business conduct, markets and activities. The CFPB may also conduct on-site examinations of our business on a periodic basis if the CFPB were to determine, through its complaint system that we were engaging in activities that pose risks to consumers.

18

LENDINGCLUB CORPORATION

There continues to be uncertainty as to how the CFPB’s strategies and priorities, including in both its examination and enforcement processes, will impact our businesses and our results of operations going forward. Actions by the CFPB could result in requirements to alter or cease offering affected loan products and services, making them less attractive and restricting our ability to offer them.

Although we have committed resources to enhancing our compliance programs, actions by the CFPB or other regulators against us, our issuing banks or our competitors that discourage the use of the marketplace model or suggest to consumers the desirability of other loan products or services could result in reputational harm and a loss of borrowers or investors. Our compliance costs and litigation exposure could increase materially if the CFPB or other regulators enact new regulations, change regulations that were previously adopted, modify, through supervision or enforcement, past regulatory guidance, or interpret existing regulations in a manner different or stricter than have been previously interpreted.

If the loans originated through our marketplace were found to violate a state’s usury laws, we may have to alter our business model and our business could be harmed.

The interest rates that are charged to borrowers and that form the basis of payments to investors through our marketplace are enabled by legal principles including (i) the application of federal law to enable an issuing bank that originates the loan to export the interest rates of the jurisdiction where it is located, or (ii) the application of common law “choice of law” principles based upon factors such as the loan document’s terms and where the loan transaction is completed to provide uniform rates to borrowers, or (iii) the application of principles that allow the transferee of a loan to continue to collect interest as provided in the loan document. WebBank, the primary issuing bank of the loans originated through our marketplace, is chartered in, and operates out of, Utah, which allows parties to generally agree by contract to any interest rate. The annual percentage rates offered by WebBank through our marketplace for personal loans as of December 31, 2015 range from 5.99% to 32.99%, which equate to interest rates for investors that range from 5.32% to 28.99%. Certain states, including Utah, have no statutory interest rate limitations on personal loans, while other jurisdictions have a maximum rate. In some jurisdictions, the maximum rate is less than the current maximum rate offered by WebBank through our platform. If the laws of such jurisdictions were found to apply to the loans originated through our marketplace, those loans could be in violation of such laws.

In May 2015, based on the facts of that case in which the national bank no longer had any interest in the loan,

the U.S. Court of Appeals for the Second Circuit issued its decision in Madden v. Midland Funding, LLC that interpreted the scope of federal preemption under the National Bank Act (“NBA”) and held that a nonbank assignee of a loan originated by a national bank was not entitled to the benefits of federal preemption of claims of usury. The Second Circuit denied the defendant’s motion to reconsider the decision and remanded the case to address choice of law matters. The Second Circuit’s decision is binding on federal courts located in Connecticut, New York, and Vermont, but the decision could also be adopted by other courts. The defendant’s petition to the U.S. Supreme Court to review the decision is currently pending. We are unable to predict whether the U.S. Supreme Court will review the decision and, if it does, what the outcome will be. If applied to any of the loans originated through our marketplace, the Second Circuit’s decision could adversely impact our business.