Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - SYNOPSYS INC | a103118exhibit321.htm |

| EX-31.3 - EXHIBIT 31.3 - SYNOPSYS INC | a103118exhibit313.htm |

| EX-31.2 - EXHIBIT 31.2 - SYNOPSYS INC | a103118exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - SYNOPSYS INC | a103118exhibit311.htm |

| EX-23.1 - EXHIBIT 23.1 - SYNOPSYS INC | a103118exhibit231.htm |

| EX-21.1 - EXHIBIT 21.1 - SYNOPSYS INC | a103118exhibit211.htm |

| EX-3.2 - EXHIBIT 3.2 - SYNOPSYS INC | a103118exhibit32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended October 31, 2018

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 0-19807

SYNOPSYS, INC.

(Exact name of registrant as specified in its charter)

Delaware | 56-1546236 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

690 East Middlefield Road, Mountain View, California 94043

(Address of principal executive offices, including zip code)

(650) 584-5000

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.01 par value | Nasdaq Global Select Market | |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller Reporting Company ¨ | |||

Emerging growth company ¨ | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $10.5 billion. Aggregate market value excludes an aggregate of approximately 29.2 million shares of common stock held by the registrant’s executive officers and directors and by each person known by the registrant to own 5% or more of the outstanding common stock on such date. Exclusion of shares held by any of these persons should not be construed to indicate that such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the registrant, or that such person is controlled by or under common control with the registrant.

On December 12, 2018, 149,515,012 shares of the registrant’s Common Stock, $0.01 par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement relating to the registrant’s 2019 Annual Meeting of Stockholders, scheduled to be held on April 8, 2019, are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. Except as expressly incorporated by reference, the registrant’s Proxy Statement shall not be deemed to be part of this report.

SYNOPSYS, INC.

ANNUAL REPORT ON FORM 10-K

Fiscal year ended October 31, 2018

TABLE OF CONTENTS

Page No. | ||||

Item 1. | ||||

Item 1A. | ||||

Item 1B. | ||||

Item 2. | ||||

Item 3. | ||||

Item 4. | ||||

Item 5. | ||||

Item 6. | ||||

Item 7. | ||||

Item 7A. | ||||

Item 8. | ||||

Item 9. | ||||

Item 9A. | ||||

Item 9B. | ||||

Item 10. | ||||

Item 11. | ||||

Item 12. | ||||

Item 13. | ||||

Item 14. | ||||

Item 15. | ||||

i

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K (this Form 10-K or Annual Report) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the Securities Act), Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act), and the Private Securities Litigation Reform Act of 1995. Any statements herein that are not statements of historical fact are forward-looking statements. Words such as “may,” “will,” “could,” “would,” “can,” “should,” “anticipate,” “expect,” “intend,” “believe,” “estimate,” “project,” “continue,” “forecast,” “likely,” “potential,” “seek,” or the negatives of such terms, and similar expressions are intended to identify forward-looking statements. This Form 10-K includes, among others, forward-looking statements regarding:

• | our business, product and platform strategies; |

• | our business outlook; |

• | the continuation of current industry trends towards customer and vendor consolidation, and the impact of such consolidation; |

• | prior and future acquisitions, including the expected benefits and risks of completed acquisitions; |

• | the impact of macroeconomic conditions on our business and our customers’ businesses; |

• | demand for our products and our customers’ products; |

• | the expected realization of our backlog; |

• | customer license renewals; |

• | the completion of development of our unfinished products, or further development or integration of our existing products; |

• | technological trends in integrated circuit design; |

• | our ability to successfully compete in the markets in which we serve; |

• | our license mix, our business model, and variability in our revenue; |

• | litigation; |

• | our ability to protect our intellectual property; |

• | our cash, cash equivalents and cash generated from operations; |

• | our available-for-sale securities; and |

• | our future liquidity requirements. |

These statements are based on our current expectations about future events and involve certain known and unknown risks, uncertainties and other factors that could cause our actual results, time frames or achievements to differ materially from those expressed or implied in our forward-looking statements. Accordingly, we caution readers not to place undue reliance on these statements. Such risks and uncertainties include, among others, those listed in Part I, Item 1A, Risk Factors of this Form 10-K. The information included herein represents our estimates and assumptions as of the date of this filing. Unless required by law, we undertake no obligation to update publicly any forward-looking statements, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. All subsequent written or oral forward-looking statements attributable to Synopsys, Inc. or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Readers are urged to carefully review and consider the various disclosures made in this report and in other documents we file from time to time with the Securities and Exchange Commission (SEC) that attempt to advise interested parties of the risks and factors that may affect our business.

1

Fiscal Year End

Our fiscal year ends on the Saturday nearest to October 31 and consists of 52 weeks, with the exception that approximately every five years, we have a 53-week year. Fiscal 2018 was a 53-week year and ended on November 3, 2018. Fiscal 2017 and 2016 were 52-week years and ended on October 28, 2017 and October 29, 2016, respectively. Fiscal 2019 will be a 52-week year.

For presentation purposes, this Form 10-K refers to the closest calendar month end.

2

PART I

Item 1. Business |

Company Overview

Synopsys, Inc. provides products and services used by designers across the entire silicon to

software spectrum, from engineers creating advanced semiconductors to software developers seeking to ensure

the security and quality of their code. We are a global leader in supplying the electronic design automation

(EDA) software that engineers use to design and test integrated circuits (ICs), also known as chips. We also offer semiconductor intellectual property (IP) products, which are pre-designed circuits that engineers use as components of larger chip designs rather than designing those circuits themselves. We provide software and hardware used to validate the electronic systems that incorporate chips and the software that runs on them. To complement these offerings, we provide technical services and support to help our customers develop advanced chips and electronic systems. We are also a leading provider of software tools and services that improve the security and quality of software code in a wide variety of industries, including electronics, financial services, media, automotive, medicine, energy and industrials.

Corporate Information

We incorporated in 1986 in North Carolina and reincorporated in 1987 in Delaware. Our headquarters are located at 690 East Middlefield Road, Mountain View, California 94043, and our headquarters’ telephone number is (650) 584-5000. We have approximately 120 offices worldwide.

Our annual and quarterly reports on Forms 10-K and 10-Q (including related filings in XBRL format), current reports on Form 8-K, and Proxy Statements relating to our annual meetings of stockholders (including any amendments to these reports, as well as filings made by our executive officers and directors) are available through the Investor Relations page of our website (www.synopsys.com) free of charge as soon as practicable after we file them with, or furnish them to, the SEC (www.sec.gov). We use our Investor Relations page as a routine channel for distribution of important information, including news releases, investor presentations, and financial information. The contents of our website are not part of this Form 10-K.

Background

Recent years have seen a remarkable proliferation of consumer and wireless electronic products, particularly mobile devices. The growth of the Internet and cloud computing has provided people with new ways to create, store and share information. At the same time, the increasing use of electronics in cars, buildings, appliances and other consumer products is creating a connected landscape of “smart” devices. Numerous software applications (apps) have been developed to expand the potential of these connected devices. The increasing viability of artificial intelligence and machine learning is driving an increase in the activity of new and existing chip design companies around the world.

These developments have been fueled by innovation in the semiconductor and software industries. It is common for a single chip to combine many components (processor, communications, memory, custom logic, input/output) and embedded software into a single system-on-chip (SoC), necessitating highly complex chip designs. The most complex chips today contain more than a billion transistors. Transistors are the basic building blocks for ICs, each of which may have features that are less than 1/1,000th the diameter of a human hair. At such small dimensions, the wavelength of light itself can become an obstacle to production, proving too big to create such dense features and requiring creative and complicated new approaches from designers. Designers have turned to new manufacturing techniques to solve these problems, such as multiple-patterning lithography and FinFET transistors, which in turn have introduced new challenges to design and production.

The popularity of mobile devices and other electronic products has increased demand for chips and systems with greater functionality and performance, reduced size, and lower power consumption. Our customers are the designers of those products and are facing intense pressure to deliver innovative products in shorter timeframes and at lower prices. In other words, innovation in chip and system design often hinges on providing products “better,” “sooner,” and “cheaper” than competitors. The designs of these chips and systems are extremely complex and necessitate state-of-the-art design solutions.

3

A similar dynamic is at work in the software arena, where the pace of innovation often requires developers—also our customers—to deliver more secure, high-quality software, which can include millions of lines of code, in increasingly frequent release cycles. Bugs, defects, and security vulnerabilities in code can be difficult to detect and expensive to fix. But, at a time when software is prevalent in many industries across a growing array of smart devices, it is crucial to have high-quality, secure code to ensure consumers’ privacy and safety.

Our Role—The Silicon to Software™ Partner

Synopsys' products and services enable innovators across a variety of markets—from mobile electronics and finance to media, medical, energy, industrial, and automotive—to develop smart and secure products and applications. Across all industries, our customers face tremendous pressure to build differentiated chips and develop robust code more quickly and cost-effectively than ever before. With the increasing amount of embedded software in today’s devices, security and quality are top concerns. Synopsys technologies and services are designed to help our customers—both hardware designers and software developers—to speed time to market, achieve the highest quality of results, mitigate risk, and maximize profitability. Our offerings span from silicon to software.

The task of the chip and system designer is to determine how best to design, locate, and connect the building blocks of chips, and to verify that the resulting design behaves as intended and can be manufactured efficiently and cost-effectively. This task is a complex, multi-step process that is both expensive and time-consuming. We offer a wide range of products that help designers at different steps in the overall design process, both for the design of individual ICs and for the design of larger systems. Our products can increase designer productivity and efficiency by automating tasks, keeping track of large amounts of design data, adding intelligence to the design process, facilitating reuse of past designs and reducing errors. Our IP products offer proven, high-quality pre-configured circuits that are ready-to-use in a chip design, saving customers time and enabling them to direct resources to features that differentiate their products. Our global service and support engineers also provide expert technical support and design assistance to our customers.

The task of the software developer is to write code that not only accomplishes the developer's goal as efficiently as possible, but also runs securely and is free of defects. We offer products that can help developers write higher quality, more secure code by analyzing their code for quality defects and known security vulnerabilities, adding intelligence and automation to the software testing process, and helping to eliminate defects in a systematic manner. To the extent that developers make use of open source software in their code, our products can help developers better manage the composition and security of the code. Our products enable software developers to catch flaws earlier in the development cycle, when they are less costly to fix.

Products and Services

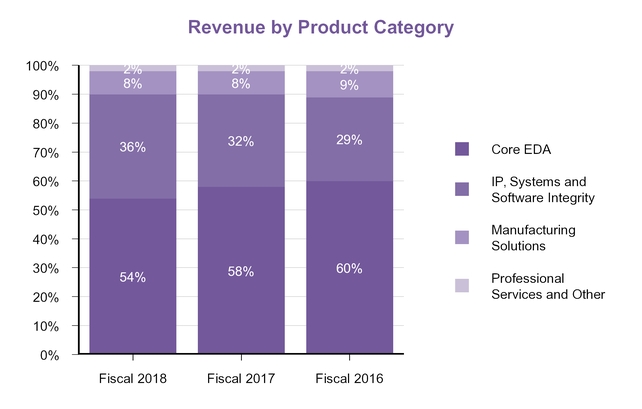

Revenue from our products and services is categorized into four groups:

• | Core EDA, which includes digital, custom and Field Programmable Gate Array (FPGA) IC design and verification products; |

• | IP, Systems and Software Integrity, which includes our DesignWare® IP portfolio, system-level products, and software security and quality testing solutions; |

• | Manufacturing Solutions; and |

• | Professional Services and Other. |

Core EDA

The process of designing ICs contains many complex steps: architecture definition, register transfer level (RTL) design, functional/RTL verification, logic design or synthesis, gate-level verification, floorplanning, and place and route, to name just a few. Designers use our Core EDA products to automate the IC design process and to reduce errors. We offer a platform that features a large number of Core EDA products intended to address the process comprehensively. Our Core EDA products generally fall into the following categories:

• | Digital, custom and FPGA IC design, which includes software tools to design an IC; and |

• | Verification, which includes technology to verify that an IC design behaves as intended. |

4

Digital and Custom IC Design

Our Fusion Design Platform™ provides customers with a comprehensive digital design implementation solution that includes industry-leading products and incorporates common libraries and consistent timing, delay calculation, UPF power intent descriptions, and constraints throughout the design process. The Fusion Design Platform, which was launched in the fall of 2018, redefines conventional design tool boundaries to deliver a more integrated flow than ever before, with better quality of results and time to results. The platform gives designers the flexibility to integrate internally developed and third-party tools. With innovative technologies, a common foundation, and flexibility, our Fusion Design Platform helps reduce design times, decrease uncertainties in the design steps, and minimize the risks inherent in advanced, complex IC design. The platform supports multiple technology nodes, including most advanced technology nodes such as 16/14nm, 12nm, 10nm, and 7/8nm, with technology collaborations at 5nm and below.

Key design products, available as part of the Fusion Design Platform, include Design Compiler® logic synthesis, IC Compiler™ II physical design, Fusion Compiler™ RTL to GDSII design implementation, PrimeTime® static timing analysis, StarRC™ parasitic extraction, Ansys RedHawk fusion rail analysis, and IC Validator physical verification.

Our Custom Design Platform™ is a unified suite of design and verification tools that accelerates the development of robust custom and AMS designs. Anchored by the Custom Compiler custom design environment, the platform features industry-leading circuit simulation performance, a fast, easy-to-use custom layout editor complemented with best-in-class technologies for parasitic extraction, reliability analysis, and physical verification. Key features of the Custom Design Platform include reliability-aware verification, visually-assisted layout automation, extraction fusion, and DRC fusion technologies. The platform supports multiple technology nodes, including most advanced technology nodes such as 16/14nm, 12nm, 10nm, and 7/8nm.

Our Custom Design Platform is based on the OpenAccess database and includes open APIs for third-party tool integration. Platform tools include HSPICE® and FineSim® SPICE circuit simulators, CustomSim™ FastSPICE, Custom Compiler layout and schematic editor, StarRC parasitic extraction, and IC Validator physical verification.

FPGA Design

FPGAs are complex chips that can be customized or programmed to perform a specific function after they are manufactured. For FPGA design, we offer Synplify® (Pro® and Premier) implementation and Identify® debug software tools.

Verification

Our Verification Continuum™ platform is built from our industry-leading and fastest verification technologies, providing virtual prototyping, static and formal verification, simulation, emulation, FPGA-based prototyping, and debug in a unified environment with verification IP and planning and coverage technology. By providing a consistent model and debug environment across the flow of verification tasks and by enabling seamless transitions between simulation, emulation, and prototyping, the platform helps our customers accelerate hardware verification, bring up software earlier, and get to market sooner with advanced SoCs.

The individual products included in the Verification Continuum platform are reported in our Core EDA and IP, Systems & Software Integrity revenue categories. The solutions reported in our Core EDA revenue include the following:

• | SpyGlass® family of static verification technologies including lint, CDC (clock domain crossing), RDC (reset domain crossing), DFT (design for test), and low-power analysis and verification; |

• | VCS® functional verification solution, our comprehensive RTL and gate-level simulation technology, including Fine-Grained Parallelism (FGP); |

• | Verdi® debug technology, the industry’s most compressive SoC debug; |

• | VC Formal, our next-generation formal verification product; |

• | Verdi Coverage, our verification planning and coverage technology; |

5

• | ZeBu® emulation systems, which use high-performance hardware to emulate SoC designs so that designers can accelerate verification of large complex SoCs and perform earlier verification of the SoC together with software; and |

• | Other principal individual verification solutions, including CustomSim™ FastSPICE and FineSim® SPICE/FastSPICE circuit simulation and analysis products, HSPICE® circuit simulator, and CustomExplorer™ Ultra mixed-signal regression and analysis environment. |

The verification IP, virtual prototyping and FPGA-based prototyping solutions that are part of our Verification Continuum platform are included in our IP, Systems & Software Integrity category and further described below.

IP, Systems and Software Integrity

IP Products

As more functionality converges into a single device or even a single chip, and as chip designs grow more complex, the number of third-party IP blocks incorporated into designs is rapidly increasing. We are a leading provider of high-quality, silicon-proven IP solutions for SoCs. Our broad DesignWare IP portfolio includes:

• | High-quality solutions for widely used wired and wireless interfaces such as USB, PCI Express, DDR, Ethernet, SATA, MIPI, HDMI, and Bluetooth Low Energy; |

• | Logic libraries and embedded memories, including memory compilers, non-volatile memory, standard cells, and integrated test and repair; |

• | Processor solutions, including configurable ARC® processor cores, software, Embedded Vision processor cores and application-specific instruction-set processor (ASIP) tools for embedded applications; |

• | IP subsystems for audio, sensor, and data fusion functionality that combine IP blocks, an efficient processor, and software into an integrated, pre-verified subsystem; |

• | Security IP solutions, including cryptographic cores and software, security subsystems, platform security and content protection IP; |

• | Analog IP including data converters and audio codecs; and |

• | SoC infrastructure IP, datapath and building block IP, mathematical and floating point components, ARM® AMBA® interconnect fabric and peripherals, and verification IP. |

Our IP Accelerated initiative augments our established, broad portfolio of silicon-proven DesignWare IP with IP Prototyping Kits and customized IP subsystems to accelerate prototyping, software development, and integration of IP into SoCs.

We also offer a broad portfolio of IP that has been optimized to address specific application requirements for the mobile, automotive, digital home, internet of things, and cloud computing markets, enabling designers to quickly develop SoCs in these areas.

Our Verification IP portfolio, part of our Verification Continuum platform, is also part of the IP Products category.

System-Level Solutions

Our System-Level verification solutions include the following elements of our Verification Continuum platform:

• | HAPS® FPGA-based prototyping systems, which provide design and verification teams with an integrated and scalable hardware-software solution for early software development and to improve their SoC schedules; |

• | Virtualizer™ virtual prototyping solutions, which address the increasing development challenges associated with software-rich semiconductor and electronic products by accelerating both the development and deployment of virtual prototypes; and |

6

• | Platform Architect solution, which provides architects and system designers with tools and efficient methods for early analysis and optimization of multi-core SoC architectures for performance and power. |

We also provide a series of tools used in the design of optical systems and photonic devices. Our CODE V® solution enables engineers to model, analyze and optimize designs for optical imaging and communication systems. Our LightTools® design and analysis software allows designers to simulate and improve the performance of a broad range of illumination systems, from vehicle lighting to projector systems.

Software Integrity Solutions

Our Software Integrity platform is a comprehensive solution for building integrity—security and quality—into our customers’ software development lifecycle and supply chain. These testing tools, services and programs enable our customers to manage open source license compliance and detect and remediate security vulnerabilities and defects across their entire software development lifecycle. Our offerings include security testing, managed services, programs and professional services, and training.

Key products in the security, quality and compliance testing space include:

• | Coverity® static analysis tools (including regular critical updates), which analyze software code to find crash-causing bugs, incorrect program behavior, the latest security vulnerabilities, memory leaks and other performance-degrading flaws; |

• | Defensics® fuzz testing tools, which examine security vulnerabilities in software binaries and libraries, particularly network protocols and file formats, by systematically sending invalid or unexpected inputs to the system under test; |

• | Black Duck™ software composition analysis tools, which scan binary and source code for license issues and other known security vulnerabilities stemming from incorporated third-party and open source code; and |

• | Seeker® IAST tool, which identifies exploitable security vulnerabilities while web applications are running, thereby verifying results and eliminating false positives. |

Managed Services allow developers to test code across many dimensions, and to rapidly respond to changing testing requirements and evolving threats. This includes Mobile AST services to find vulnerabilities in mobile applications as well as DAST services which identify security vulnerabilities while web applications are running, without the need for source code.

Programs and Professional Services address unique security and quality needs with specialized consulting by skilled experts, including the Building Security in Maturity Mode (BSIMM), which measures the effectiveness of software security initiatives by assessing the current state as compared to industry benchmarks.

Finally, training includes eLearning and instructor-led training that prepares developers and security professionals to build security and quality into their software development process and remediate found vulnerabilities and defects.

Manufacturing Solutions

Our Manufacturing Solutions software products and technologies enable semiconductor manufacturers to more quickly develop new fabrication processes that produce production-level yields. These products are used in the early research and development phase, as well as in the production phase, where designers use these products to help convert IC design layouts into the masks used to manufacture the devices.

Our Manufacturing Solutions include Sentaurus™ technology computer-aided design (TCAD) device and process simulation products, Proteus™ mask synthesis tools, CATS® mask data preparation software, Yield Explorer® Odyssey, and Yield-Manager® yield management solutions.

7

Professional Services and Other

We provide consulting and design services that address all phases of the SoC development process. These services assist our customers with new tool and methodology adoption, chip architecture and specification development, functional and low-power design and verification, and physical implementation and signoff. We also provide a broad range of expert training and workshops on our latest tools and methodologies. Professional services related to the security and quality of the software embedded on the chip or elsewhere are included in the Software Integrity Solutions category and further described above.

Customer Service and Technical Support

A high level of customer service and support is critical to the adoption and successful use of our products. We provide technical support for our products through both field-based and corporate-based application engineering teams. Customers that purchase Technology Subscription Licenses (TSLs) receive post-contract customer support bundled with their license fee. Customers that purchase perpetual licenses may purchase these services separately, as further described in Product Sales and Licensing Agreements below.

Post-contract customer support includes providing frequent updates and upgrades to maintain the utility of the software due to rapid changes in technology. Post-contract customer support for our EDA and IP products also includes access to the SolvNet® portal, where customers can explore our complete design knowledge database. Updated daily, the SolvNet portal includes technical documentation, design tips, and answers to user questions. Customers can also engage, for additional charges, with our worldwide network of applications consultants for additional support needs.

In addition, we offer training workshops designed to increase customer design proficiency and productivity with our products. Workshops cover our EDA products and methodologies used in our design and verification flows, as well as specialized modules addressing system design, logic design, physical design, simulation and testing. We offer regularly scheduled public and private courses in a variety of locations worldwide, as well as online training (live or on-demand) through our Virtual Classrooms.

Product Warranties

We generally warrant our products to be free from defects in media and to substantially conform to material specifications for a period of 90 days for our software products and for up to 6 months for our hardware products. In many cases, we also provide our customers with limited indemnification with respect to claims that their use of our software products infringes on United States patents, copyrights, trademarks or trade secrets. We have not experienced material warranty or indemnity claims to date.

Support for Industry Standards

We actively create and support standards that help our EDA and IP customers increase productivity, facilitate efficient design flows, improve interoperability of tools from different vendors, and ensure connectivity, functionality and interoperability of IP building blocks. Standards in the electronic design industry can be established by formal accredited organizations, industry consortia, company licensing made available to all, de facto usage, or through open source licensing.

Synopsys’ EDA products support many standards, including the most commonly used hardware description languages: SystemVerilog, Verilog, VHDL, and SystemC®. Our products utilize numerous industry-standard data formats, APIs, and databases for the exchange of design data among our tools, other EDA vendors’ products, and applications that customers develop internally. We also comply with a wide range of industry standards within our IP product family to ensure usability and interconnectivity.

Our Software Integrity solutions support several existing and emerging industry standards for software coding and security, such as the Motor Industry Software Reliability Association (MISRA) coding standards for the automotive industry. In addition, our products support multiple major programming languages, including C/C++, Objective C, C#, JavaScript (including many commonly used frameworks), and others. In addition, we support many common compilers, development environments, frameworks, and data and file formats.

8

Sales, Distribution and Backlog

Our EDA and IP customers are primarily semiconductor and electronics systems companies. The customers for our Software Integrity solutions include many of these companies as well as companies from a wider array of industries, including electronics, financial services, media, automotive, medicine, energy and industrials. We market our products and services principally through direct sales in the United States and our principal foreign markets. We typically distribute our software products and documentation to customers electronically, but provide physical media (e.g., DVD-ROMs) when requested by the customer.

We maintain sales and support centers throughout the United States. Outside the United States, we maintain sales, support or service offices in Canada, multiple countries in Europe, Israel and multiple countries in Asia, including Japan, China, Korea, and Taiwan. Our international headquarters are located in Dublin, Ireland. Our offices are further described under Part I, Item 2, Properties.

Information relating to domestic and foreign operations, including revenue and long-lived assets by geographic area, is contained in Note 13 of Notes to Consolidated Financial Statements in Part II, Item 8, Financial Statements and Supplementary Data. Risks related to our foreign operations are described in Part I, Item 1A, Risk Factors.

Our backlog was approximately $4.0 billion on October 31, 2018, an increase from backlog of $3.7 billion on October 31, 2017, resulting primarily from the timing of large multi-year contract renewals. Backlog represents committed orders that are expected to be recognized as revenue over the following three years. We currently expect that $1.7 billion of our backlog will be recognized after fiscal 2019. Backlog may not be a reliable predictor of our future sales as business conditions may change and technologies may evolve, and customers may seek to renegotiate their arrangements or may default on their payment obligations. For this and other reasons, we may not be able to recognize expected revenue from backlog when anticipated.

9

Revenue attributable to each of our four product categories is shown below as a percentage of total revenue for the last three fiscal years.

Aggregate revenue derived from Intel Corporation and its subsidiaries through multiple agreements accounted for 15.4%, 17.9% and 15.9% of our total revenue in fiscal 2018, 2017 and 2016, respectively. No other customer accounted for more than 10% of our revenue during such periods.

Product Sales and Licensing Agreements

We typically license our software to customers under non-exclusive license agreements that restrict use of our software to specified purposes within specified geographical areas. The majority of our licenses are network licenses that allow a number of individual users to access the software on a defined network, including, in some cases, regional or global networks. License fees depend on the type of license, product mix and number of copies of each product licensed.

In a number of cases, we provide our customers the right to “re-mix” a portion of the software they initially licensed for other specified Synopsys products. For example, a customer may use our front-end design products for a portion of the license term and then exchange such products for back-end place-and-route software for the remainder of the term in order to complete the customer’s IC design. This practice helps ensure the customer’s access to the complete design flow needed to design their product. Offering remix rights to customers gives us an advantage over competitors who offer a narrower range of products because customers can obtain more of their design flow from a single vendor. At the same time—because in such cases the customer does not need to obtain a new license and pay an additional license fee for the use of the additional products—the use of these arrangements could result in reduced revenue compared to licensing the individual products separately without re-mix rights.

We currently offer our software products under, primarily, two license types: TSLs and perpetual licenses. For a full discussion of these types of licenses, see Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates and Results of Operations—Revenue Background.

We typically license our DesignWare IP products under nonexclusive license agreements that provide usage rights for specific applications. Fees under these licenses are typically charged on a per design basis plus, in some cases, royalties. Royalty arrangements are not material to our total revenue.

10

Our hardware products, which principally consist of our prototyping and emulation systems, are either sold or leased to our customers. Our professional services team typically provides design consulting services to our customers under consulting agreements with statements of work specific to each project.

Competition

The EDA industry is highly competitive. We compete against other EDA vendors and against our customers’ own design tools and internal design capabilities. In general, we compete principally on technology leadership, product quality and features (including ease-of-use), license terms, price and payment terms, post-contract customer support, flexibility of tool use, and interoperability with our own and other vendors’ products. We also deliver a significant amount of engineering and design consulting for our products. No single factor drives an EDA customer’s buying decision, and we compete on all fronts to capture a higher portion of our customers’ budgets. Our competitors include EDA vendors that offer varying ranges of products and services, such as Cadence Design Systems, Inc. and Mentor Graphics Corporation (now part of Siemens AG). We also compete with other EDA vendors, including new entrants to the marketplace, that offer products focused on one or more discrete phases of the IC design process, as well as with customers’ internally developed design tools and capabilities.

In the area of IP products, we compete against numerous other IP providers, including Cadence Design Systems, Inc., and our customers' internally developed IP. We generally compete on the basis of product quality, reliability and features, ease of integration with customer designs, compatibility with design tools, license terms, price and payment terms, and customer support.

In the area of Software Integrity solutions, we compete with numerous other solution providers, many of which focus on specific aspects of software security or quality analysis. We also compete with frequent new entrants, which include start-up companies and more established software companies. For example, competitors named in the Gartner Magic Quadrant for Application Security Testing include Checkmarx Ltd., International Business Machines Corporation, Micro Focus International plc, and Veracode (acquired by Thoma Bravo, LLC).

Proprietary Rights

We primarily rely upon a combination of copyright, patent, trademark, and trade secret laws and license and non-disclosure agreements to establish and protect our proprietary rights. We have a diversified portfolio of more than 3,100 United States and foreign patents issued, and we will continue to pursue additional patents in the future. Our issued patents have expiration dates through 2037. Our patents primarily relate to our products and the technology used in connection with our products. Our source code is protected both as a trade secret and as an unpublished copyrighted work. However, third parties may independently develop similar technology. In addition, effective copyright and trade secret protection may be unavailable or limited in some foreign countries. While protecting our proprietary technology is important to our success, our business as a whole is not significantly dependent upon any single patent, copyright, trademark, or license.

In many cases, under our customer agreements and other license agreements, we offer to indemnify our customers if the licensed products infringe on a third party’s intellectual property rights. As a result, we may from time to time need to defend claims that our customers’ use of our products infringes on these third-party rights. We license software and other intellectual property from third parties, including, in several instances, for inclusion in our products. Risks related to our use of third-party technology are described in Part I, Item 1A, Risk Factors.

Employees

As of October 31, 2018, Synopsys had 13,245 employees, of which 4,679 were based in the United States.

11

Executive Officers of the Registrant

The executive officers of Synopsys and their ages as of December 14, 2018 were as follows:

Name | Age | Position | ||

Aart J. de Geus | 64 | Co-Chief Executive Officer and Chairman of the Board of Directors | ||

Chi-Foon Chan | 69 | Co-Chief Executive Officer and President | ||

Trac Pham | 49 | Chief Financial Officer | ||

Joseph W. Logan | 59 | Sales and Corporate Marketing Officer | ||

John F. Runkel, Jr. | 63 | General Counsel and Corporate Secretary | ||

Aart J. de Geus co-founded Synopsys and has served as Chairman of our Board of Directors since February 1998 and Chief Executive Officer since January 1994. He has served as Co-Chief Executive Officer with Dr. Chi-Foon Chan since May 2012. Since the inception of Synopsys in December 1986, Dr. de Geus has held a variety of positions, including President, Senior Vice President of Engineering and Senior Vice President of Marketing. He has served as a member of Synopsys’ Board of Directors since 1986, and served as Chairman of our Board from 1986 to 1992 and again from 1998 until present. Dr. de Geus has also served on the board of directors of Applied Materials, Inc. since July 2007. Dr. de Geus holds an M.S.E.E. from the Swiss Federal Institute of Technology in Lausanne, Switzerland and a Ph.D. in Electrical Engineering from Southern Methodist University.

Chi-Foon Chan has served as our Co-Chief Executive Officer since May 2012 and as our President and a member of our Board of Directors since February 1998. Prior to his appointment as our Co-Chief Executive Officer in May 2012, he had served as our Chief Operating Officer since April 1997. Dr. Chan joined Synopsys in May 1990 and has held various senior management positions, including Executive Vice President, Office of the President from September 1996 to February 1998 and Senior Vice President, Design Tools Group from February 1994 to April 1997. Dr. Chan has also held senior management and engineering positions at NEC Electronics and Intel Corporation. Dr. Chan holds a B.S. in Electrical Engineering from Rutgers University, and an M.S. and a Ph.D. in Computer Engineering from Case Western Reserve University.

Trac Pham is our Chief Financial Officer. Mr. Pham joined Synopsys in November 2006 as Vice President, Financial Planning and Strategy. He became our Vice President, Corporate Finance, in August 2012, assuming additional responsibility for our tax and treasury functions, before being appointed Chief Financial Officer in December 2014. Mr. Pham holds a Bachelor of Arts in Economics from the University of California, Berkeley and an MPIA (Master of Pacific International Affairs) from the University of California, San Diego. He is an active status California CPA.

Joseph W. Logan serves as our Sales and Corporate Marketing Officer. He became Senior Vice President of Worldwide Sales in September 2006, and assumed responsibility for our Corporate Marketing organization in August 2013. Previously, Mr. Logan was head of sales for Synopsys’ North America East region from September 2001 to September 2006. Prior to Synopsys, Mr. Logan was head of North American Sales and Support at Avant! Corporation. Mr. Logan holds a B.S.E.E. from the University of Massachusetts, Amherst.

John F. Runkel, Jr. has served as our General Counsel and Corporate Secretary since May 2014. From October 2008 to March 2013, he was Executive Vice President, General Counsel, and Corporate Secretary of Affymetrix, Inc. He served as Senior Vice President, General Counsel and Corporate Secretary of Intuitive Surgical, Inc. from 2006 to 2007. Mr. Runkel served in several roles at VISX, Inc. from 2001 to 2005, most recently as Senior Vice President of Business Development and General Counsel. Mr. Runkel was also a partner at the law firm of Sheppard, Mullin, Richter & Hampton LLP for 11 years. He holds a Bachelor of Arts and a Juris Doctorate from the University of California, Los Angeles.

There are no family relationships among any Synopsys executive officers or directors.

12

Item 1A. Risk Factors |

A description of the risk factors associated with our business is set forth below. Investors should carefully consider these risks and uncertainties before investing in our common stock.

The growth of our business depends primarily on the semiconductor and electronics industries.

The growth of the electronic design automation (EDA) industry as a whole, our EDA and intellectual property (IP) product sales, and to some extent our Software Integrity Solutions sales, is dependent on the semiconductor and electronics industries. A substantial portion of our business and revenue depends upon the commencement of new design projects by semiconductor manufacturers and their customers. The increasing complexity of designs of systems-on-chips and integrated circuits, and customers’ concerns about managing costs, have previously led and in the future could lead to a decrease in design starts and design activity in general, with some customers focusing more on one discrete phase of the design process or opting for less advanced, but less risky, manufacturing processes that may not require the most advanced EDA products. Demand for our products and services could decrease and our financial condition and results of operations could be adversely affected if growth in the semiconductor and electronics industries slows or stalls. Additionally, as the EDA industry matures, consolidation may result in stronger competition from companies better able to compete as sole source vendors. This increased competition may cause our revenue growth rate to decline and exert downward pressure on our operating margins, which may have an adverse effect on our business and financial condition.

Furthermore, the semiconductor and electronics industries have become increasingly complex ecosystems. Many of our customers outsource the manufacture of their semiconductor designs to foundries. Our customers also frequently incorporate third-party IP, whether provided by us or other vendors, into their designs to improve the efficiency of their design process. We work closely with major foundries to ensure that our EDA, IP, and manufacturing solutions are compatible with their manufacturing processes. Similarly, we work closely with other major providers of semiconductor IP, particularly microprocessor IP, to optimize our EDA tools for use with their IP designs and to assure that their IP and our own IP products, which may each provide for the design of separate components on the same chip, work effectively together. If we fail to optimize our EDA and IP solutions for use with major foundries’ manufacturing processes or major IP providers’ products, or if our access to such foundry processes or third-party IP products is hampered, then our solutions may become less desirable to our customers, resulting in an adverse effect on our business and financial condition.

Consolidation among our customers and within the industries in which we operate, as well as our dependence on a relatively small number of large customers, may negatively impact our operating results.

A number of business combinations, including mergers, asset acquisitions and strategic partnerships, among our customers in the semiconductor and electronics industries have occurred over the last several years, and more could occur in the future. Consolidation among our customers could lead to fewer customers or the loss of customers, increased customer bargaining power, or reduced customer spending on software and services. Furthermore, we depend on a relatively small number of large customers, and on such customers continuing to renew licenses and purchase additional products from us, for a large portion of our revenue. Reduced customer spending or the loss of a small number of customers, particularly our large customers, could adversely affect our business and financial condition. In addition, we and our competitors from time to time acquire businesses and technologies to complement and expand our respective product offerings. If any of our competitors consolidate or acquire businesses and technologies which we do not offer, they may be able to offer a larger technology portfolio, additional support and service capability, or lower prices, which could negatively impact our business and operating results.

Uncertainty in the global economy, and its potential impact on the semiconductor and electronics industries in particular, may negatively affect our business, operating results and financial condition.

While the global economy has shown improvement in recent years, there are still uncertainties surrounding the strength of the recovery in many regions. Uncertainty caused by challenging global economic conditions could lead some of our customers to postpone their decision-making, decrease their spending and/or delay their payments to us. Such caution by customers could, among other things, limit our ability to maintain or increase our sales or recognize revenue from committed contracts.

We cannot predict the stability of the economy as a whole or the industries in which we operate. Further economic instability could adversely affect the banking and financial services industry and result in credit downgrades of the

13

banks we rely on for foreign currency forward contracts, credit and banking transactions, and deposit services, or cause them to default on their obligations. There is uncertainty regarding how proposed, contemplated or future changes to the complex laws and regulations governing our industry, the banking and financial services industry, and the economy could affect our business. In addition, economic conditions could deteriorate in the future, and, in particular, the semiconductor and electronics industries could fail to grow, including as the result of any disruption of international trade relationships. In the event of future improvements in economic conditions for our customers, the positive impact on our revenues and financial results may be deferred due to our business model. Any of the foregoing could cause adverse effects on our business, operating results and financial condition, and could cause our stock price to decline.

Our operating results may fluctuate in the future, which may adversely affect our stock price.

Our operating results are subject to quarterly and annual fluctuations, which may adversely affect our stock price. Our historical results should not be viewed as indicative of our future performance due to these periodic fluctuations.

Many factors may cause our revenue or earnings to fluctuate, including:

• | Changes in demand for our products—especially products, such as hardware, generating upfront revenue—due to fluctuations in demand for our customers’ products and due to constraints in our customers’ budgets for research and development and EDA products and services; |

• | Product competition in the EDA industry, which can change rapidly due to industry or customer consolidation and technological innovation; |

• | Our ability to innovate and introduce new products and services or effectively integrate products and technologies that we acquire; |

• | Failures or delays in completing sales due to our lengthy sales cycle, which often includes a substantial customer evaluation and approval process because of the complexity of our products and services; |

• | Our ability to implement effective cost control measures; |

• | Our dependence on a relatively small number of large customers, and on such customers continuing to renew licenses and purchase additional products from us, for a large portion of our revenue; |

• | Changes to the amount, composition and valuation of, and any impairments to or write-offs of, our inventory; |

• | Changes in the mix of our products sold, as increased sales of our products with lower gross margins, such as our hardware products, may reduce our overall margins; |

• | Expenses related to our acquisition and integration of businesses and technology; |

• | Changes in tax rules, as well as changes to our effective tax rate, including the tax effects of infrequent or unusual transactions and tax audit settlements; |

• | Delays, increased costs or quality issues resulting from our reliance on third parties to manufacture our hardware products, which includes a sole supplier for certain hardware components; |

• | General economic and political conditions that affect the semiconductor and electronics industries, such as disruptions to international trade relationships, including tariffs, export licenses, or other trade barriers affecting our or our suppliers' products; and |

• | Changes in accounting standards, such as Topic 606, as discussed in Note 14 of Notes to Consolidated Financial Statements, which, for example, could impact the expected realization of our backlog. |

The timing of revenue recognition may also cause our revenue and earnings to fluctuate. The timing of revenue recognition is affected by factors that include:

• | Cancellations or changes in levels of orders or the mix between upfront products revenue and time-based products revenue; |

• | Delay of one or more orders for a particular period, particularly orders generating upfront products revenue, such as hardware; |

• | Delay in the completion of professional services projects that require significant modification or customization and are accounted for using the percentage of completion method; |

• | Delay in the completion and delivery of IP products in development as to which customers have paid for early access; |

14

• | Customer contract amendments or renewals that provide discounts or defer revenue to later periods; |

• | The levels of our hardware revenues, which are recognized upfront and are primarily dependent upon our ability to provide the latest technology and meet customer requirements, and which may also impact our levels of excess and obsolete inventory expenses; |

• | Changes in accounting standards, such as Topic 606, as discussed in Note 14 of Notes to Consolidated Financial Statements; and |

• | Changes in our revenue recognition model. |

These factors, or any other factors or risks discussed herein, could negatively impact our revenue or earnings and cause our stock price to decline. Additionally, our results may fail to meet or exceed the expectations of securities analysts and investors, or such analysts may change their recommendation regarding our stock, which could cause our stock price to decline. Our stock price has been, and may continue to be, volatile, which may make it more difficult for our stockholders to sell their shares at a time or a price that is favorable to them.

We operate in highly competitive industries, and if we do not continue to meet our customers’ demand for innovative technology at lower costs, our products may become uncompetitive and obsolete, and our business and financial condition may be harmed.

We compete against EDA vendors that offer a variety of products and services, such as Cadence Design Systems, Inc. and Mentor Graphics Corporation (now part of Siemens AG). We also compete with other EDA vendors, including new entrants to the marketplace, that offer products focused on one or more discrete phases of the IC design process. Moreover, our customers internally develop design tools and capabilities that compete with our products, including internal designs that compete with our IP products.

In the area of IP products, we compete against numerous other IP providers as well as our customers' internally developed IP. In the area of software integrity solutions, we compete with numerous other solution providers, many of which focus on specific aspects of software security or quality analysis. We also compete with frequent new entrants, which include start-up companies and more established software companies.

The industries in which we operate are highly competitive and the demand for our products and services is dynamic and depends on a number of factors, including demand for our customers’ products, design starts and our customers’ budgetary constraints. Technology in these industries evolves rapidly and is characterized by frequent product introductions and improvements as well as changes in industry standards and customer requirements. Semiconductor device functionality requirements continually increase while feature widths decrease, substantially increasing the complexity, cost and risk of chip design and manufacturing. At the same time, our customers and potential customers continue to demand an overall lower total cost of design, which can lead to the consolidation of their purchases with one vendor. In order to succeed in this environment, we must successfully meet our customers’ technology requirements and increase the value of our products, while also striving to reduce their overall costs and our own operating costs.

We compete principally on the basis of technology, product quality and features (including ease-of-use), license or usage terms, post-contract customer support, interoperability among products, and price and payment terms. Specifically, we believe the following competitive factors affect our success:

• | Our ability to anticipate and lead critical development cycles and technological shifts, innovate rapidly and efficiently, improve our existing products, and successfully develop or acquire new products; |

• | Our ability to offer products that provide both a high level of integration into a comprehensive platform and a high level of individual product performance; |

• | Our ability to enhance the value of our offerings through more favorable terms such as expanded license usage, future purchase rights, price discounts and other differentiating rights, such as multiple tool copies, post-contract customer support, “re-mix” rights that allow customers to exchange the software they initially licensed for other Synopsys products, and the ability to purchase pools of technology; |

• | Our ability to compete on the basis of payment terms; and |

• | Our ability to provide engineering and design consulting for our products. |

If we fail to successfully manage these competitive factors, fail to successfully balance the conflicting demands for innovative technology and lower overall costs, or fail to address new competitive forces, our business and financial condition will be adversely affected.

15

The global nature of our operations exposes us to increased risks and compliance obligations that may adversely affect our business.

We derive roughly half of our revenue from sales outside the United States, and we expect our orders and revenue to continue to depend on sales to customers outside the U.S. In addition, we have continually expanded our non-U.S. operations in the past several years. This strategy requires us to recruit and retain qualified technical and managerial employees, manage multiple remote locations performing complex software development projects and ensure intellectual property protection outside of the U.S. Our international operations and sales subject us to a number of increased risks, including:

• | Ineffective or weaker legal protection of intellectual property rights; |

• | Uncertain economic and political conditions in countries where we do business; |

• | Difficulties in adapting to cultural differences in the conduct of business, which may include business practices in which we are prohibited from engaging by the Foreign Corrupt Practices Act or other anti-corruption laws; |

• | Financial risks such as longer payment cycles and difficulty in collecting accounts receivable; |

• | Inadequate local infrastructure that could result in business disruptions; |

• | Government trade restrictions, including tariffs, export licenses, or other trade barriers, and changes to existing trade arrangements between various countries; |

• | Additional taxes, interest, and potential penalties, and uncertainty around changes in tax laws of various countries; and |

• | Other factors beyond our control such as natural disasters, terrorism, civil unrest, war and infectious diseases. |

As our business volume increases in the Asia Pacific region, there is inherent risk, based on the complex relationships between certain Asian countries and the United States, that political, diplomatic, or military events could result in trade disruptions, including tariffs, trade embargoes, and other trade barriers. A significant trade disruption or the establishment or increase of any trade barrier in any area where we do business could increase the cost of our products, which could adversely impact the margin that we earn on sales; make our products more expensive for customers, which could make our products less competitive and reduce consumer demand; adversely restrict or delay our suppliers of hardware components and products, which could adversely impact our future revenues and financial results; or otherwise have a materially adverse impact on our future revenue and profits, our and our customers’ and suppliers’ businesses, and our results of operations. Furthermore, if any of the foreign economies in which we do business deteriorate or if we fail to effectively manage our global operations, our business and results of operations will be harmed.

In response to U.S. tariffs, other countries may adopt tariffs and other trade barriers that could limit our ability to offer our products and services. Additionally, political uncertainty surrounding international trade disputes could have a negative impact on consumer confidence and spending, which could adversely impact our business operations.

In addition to tariffs and other trade barriers, our global operations are subject to numerous U.S. and foreign laws and regulations, including those related to anti-corruption, tax, corporate governance, imports and exports, financial and other disclosures, privacy and labor relations. These laws and regulations are complex and may have differing or conflicting legal standards, making compliance difficult and costly. In addition, there is uncertainty regarding how proposed, contemplated or future changes to these complex laws and regulations could affect our business. We may incur substantial expense in complying with the new obligations to be imposed by these laws and regulations, and we may be required to make significant changes in our business operations, all of which may adversely affect our revenues and our business overall. If we violate these laws and regulations we could be subject to fines, penalties or criminal sanctions, and may be prohibited from conducting business in one or more countries. Although we have implemented policies and procedures to help ensure compliance with these laws and regulations, there can be no assurance that our employees, contractors, agents or partners will not violate such laws and regulations. Any violation individually or in the aggregate could have a material adverse effect on our operations and financial condition.

Our financial results are also affected by fluctuations in foreign currency exchange rates. A weakening U.S. dollar relative to other currencies increases expenses of our foreign subsidiaries when they are translated into U.S. dollars in our consolidated statement of operations. Likewise, a strengthening U.S. dollar relative to other currencies, especially the Japanese Yen, reduces revenue of our foreign subsidiaries upon translation and consolidation.

16

Exchange rates are subject to significant and rapid fluctuations, and therefore we cannot predict the prospective impact of exchange rate fluctuations. Although we engage in foreign currency hedging activity, we may be unable to hedge all of our foreign currency risk, which could have a negative impact on our results of operations.

Cybersecurity threats or other security breaches could compromise sensitive information belonging to us or our customers and could harm our business and our reputation, particularly that of our security testing solutions.

We store sensitive data, including intellectual property, our proprietary business information and that of our customers, and confidential employee information, in our data centers and on our networks. Despite our security measures, our information technology and infrastructure may be vulnerable to attacks by hackers or breached due to employee error, malfeasance or other disruptions that could result in unauthorized disclosure or loss of sensitive information.

For example, in October 2015, we discovered unauthorized third-party access, which had begun in July 2015, to our products and product license files hosted on our SolvNet customer license and product delivery system. We determined that no customer project or design data had been accessed. No personally identifiable information or payment card information is stored on the system. While we identified and closed the method used to gain access, it is possible that our security measures may be circumvented again in the future, and such a breach could harm our business and reputation. The techniques used to obtain unauthorized access to networks, or to sabotage systems, change frequently and generally are not recognized until launched against a target. We may be unable to anticipate these techniques or to implement adequate preventative measures. Furthermore, in the operation of our business we also use third-party vendors that store certain sensitive data, including confidential information about our employees, and these third parties are subject to their own cybersecurity threats. While our standard vendor terms and conditions include provisions requiring the use of appropriate security measures to prevent unauthorized use or disclosure of our data, as well as other safeguards, a breach may still occur. Any security breach of our own or a third-party vendor’s systems could cause us to be non-compliant with applicable laws or regulations, subject us to legal claims or proceedings, disrupt our operations, damage our reputation, and cause a loss of confidence in our products and services, any of which could adversely affect our business.

Our software products, including our hosted solutions as well as our software security and quality testing solutions, may also be vulnerable to cyber attack. An attack could disrupt the proper functioning of our software, cause errors in the output of our customers’ work, allow unauthorized access to our or our customers’ proprietary information, and other destructive outcomes. As a result, our reputation could suffer, customers could stop buying our products, we could face lawsuits and potential liability, and our financial performance could be negatively impacted.

We offer software security and quality testing solutions. If we fail to identify new and increasingly sophisticated methods of cyber attack, or fail to invest sufficient resources in research and development regarding new threat vectors, our security testing products and services may fail to detect vulnerabilities in our customers’ software code. An actual or perceived failure to identify security flaws may harm the perceived reliability of our security testing products and services, and could result in a loss of customers or sales, or an increased cost to remedy a problem. Furthermore, our growth and recent acquisitions in the software security and quality testing space may increase our visibility as a security-focused company and may make us a more attractive target for attacks on our own information technology infrastructure. Successful attacks could damage our reputation as a security-focused company.

If we fail to protect our proprietary technology, our business will be harmed.

Our success depends in part upon protecting our proprietary technology. Our efforts to protect our technology may be costly and unsuccessful. We rely on agreements with customers, employees and other third-parties as well as intellectual property laws worldwide to protect our proprietary technology. These agreements may be breached, and we may not have adequate remedies for any breach. Additionally, despite our measures to prevent piracy, other parties may attempt to illegally copy or use our products, which could result in lost revenue. Some foreign countries do not currently provide effective legal protection for intellectual property and our ability to prevent the unauthorized use of our products in those countries is therefore limited. Our trade secrets may also be stolen, otherwise become known, or be independently developed by competitors.

We may need to commence litigation or other legal proceedings in order to:

• | Assert claims of infringement of our intellectual property; |

• | Defend our products from piracy; |

17

• | Protect our trade secrets or know-how; or |

• | Determine the enforceability, scope and validity of the propriety rights of others. |

If we do not obtain or maintain appropriate patent, copyright or trade secret protection, for any reason, or cannot fully defend our intellectual property rights in certain jurisdictions, our business and operating results would be harmed. In addition, intellectual property litigation is lengthy, expensive and uncertain. Legal fees related to such litigation will increase our operating expenses and may reduce our net income.

We may not be able to realize the potential financial or strategic benefits of the acquisitions we complete, or find suitable target businesses and technology to acquire, which could hurt our ability to grow our business, develop new products or sell our products.

Acquisitions are an important part of our growth strategy. We have completed a significant number of acquisitions in recent years. We expect to make additional acquisitions in the future, but we may not find suitable acquisition targets or we may not be able to consummate desired acquisitions due to unfavorable credit markets, commercially unacceptable terms, or other risks, which could harm our operating results. Acquisitions are difficult, time-consuming, and pose a number of risks, including:

• | Potential negative impact on our earnings per share; |

• | Failure of acquired products to achieve projected sales; |

• | Problems in integrating the acquired products with our products; |

• | Difficulties entering into new markets in which we are not experienced or where competitors may have stronger positions; |

• | Potential downward pressure on operating margins due to lower operating margins of acquired businesses, increased headcount costs and other expenses associated with adding and supporting new products; |

• | Difficulties in retaining and integrating key employees; |

• | Substantial reductions of our cash resources and/or the incurrence of debt; |

• | Failure to realize expected synergies or cost savings; |

• | Difficulties in integrating or expanding sales, marketing and distribution functions and administrative systems, including information technology and human resources systems; |

• | Dilution of our current stockholders through the issuance of common stock as part of the merger consideration; |

• | Assumption of unknown liabilities, including tax and litigation, and the related expenses and diversion of resources; |

• | Disruption of ongoing business operations, including diversion of management’s attention and uncertainty for employees and customers, particularly during the post-acquisition integration process; |

• | Potential negative impacts on our relationships with customers, distributors and business partners; |

• | Exposure to new operational risks, regulations, and business customs to the extent acquired businesses are located in regions where we are not currently conducting business; |

• | The need to implement controls, processes and policies appropriate for a public company at acquired companies that may have lacked such controls, processes and policies; |

• | Negative impact on our net income resulting from acquisition-related costs; and |

• | Requirements imposed by government regulators in connection with their review of an acquisition, including required divestitures or restrictions on the conduct of our business or the acquired business. |

If we do not manage the foregoing risks, the acquisitions that we complete may have an adverse effect on our business and financial condition.

We pursue new product and technology initiatives from time to time, and if we fail to successfully carry out these initiatives, our business, financial condition, or results of operations could be adversely impacted.

As part of the evolution of our business, we have made substantial investments to develop new products and enhancements to existing products through our acquisitions and research and development efforts. If we are unable to anticipate technological changes in our industry by introducing new or enhanced products in a timely and cost-effective manner, or if we fail to introduce products that meet market demand, we may lose our competitive position, our products may become obsolete, and our business, financial condition or results of operations could be adversely affected.

18

Additionally, from time to time, we invest in expansion into adjacent markets, including software security and quality solutions. Although we believe these solutions are complementary to our EDA tools, we have less experience and a more limited operating history in offering software quality, testing, and security products and services, and our efforts in this area may not be successful. Our success in these new markets depends on a variety of factors, including the following:

• | Our ability to attract a new customer base, including in industries in which we have less experience; |

• | Our successful development of new sales and marketing strategies to meet customer requirements; |

• | Our ability to accurately predict, prepare for, and promptly respond to technological developments in new fields, including, in the case of our software quality, testing, and security tools and services, identifying new security vulnerabilities in software code and ensuring support for a growing number of programming languages; |

• | Our ability to compete with new and existing competitors in these new industries, many of which may have more financial resources, industry experience, brand recognition, relevant intellectual property rights, or established customer relationships than we currently do, and could include free and open source solutions that provide similar software quality, testing, and security tools without fees; |

• | Our ability to skillfully balance our investment in adjacent markets with investment in our existing products and services; |

• | Our ability to attract and retain employees with expertise in new fields; |

• | Our ability to sell and support consulting services at profitable margins; and |

• | Our ability to manage our revenue model in connection with hybrid sales of licensed products and consulting services. |

Difficulties in any of our new product development efforts or our efforts to enter adjacent markets could adversely affect our operating results and financial condition.

We may have to invest more resources in research and development than anticipated, which could increase our operating expenses and negatively affect our operating results.