Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - JOHNSON OUTDOORS INC | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - JOHNSON OUTDOORS INC | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - JOHNSON OUTDOORS INC | ex31_1.htm |

| EX-23 - EXHIBIT 23 - JOHNSON OUTDOORS INC | ex23.htm |

| EX-21 - EXHIBIT 21 - JOHNSON OUTDOORS INC | ex21.htm |

| EX-10.14 - EXHIBIT 10.14 - JOHNSON OUTDOORS INC | ex10_14.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended September 28, 2018

OR

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ______ to ______

Commission file number 0-16255

JOHNSON OUTDOORS INC.

(Exact name of registrant as specified in its charter)

|

Wisconsin

|

39-1536083

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

555 Main Street, Racine, Wisconsin 53403

(Address of principal executive offices, including zip code)

(262) 631-6600

(Registrant’s telephone number, including area code)

|

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

Title of Each Class

|

Name of Exchange on Which Registered

|

|

Class A Common Stock, $.05 par value per share

|

NASDAQ Global Select Market SM

|

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act

of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405

of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained,

to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10‑K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

|

Large Accelerated Filer

|

☐ | ||

|

Accelerated Filer

|

☒

|

||

|

Non-Accelerated Filer

|

☐

|

||

|

Smaller Reporting Company

|

☐ | ||

|

Emerging Growth Company

|

☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any

new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 23, 2018, 8,787,360 shares of Class A and 1,211,686 shares of Class B common stock of the registrant were outstanding. The aggregate

market value of voting and non-voting common stock of the registrant held by non-affiliates of the registrant was approximately $307,000,000 on March 30, 2018 (the last business day of the registrant’s most recently completed fiscal second quarter)

based on approximately 4,955,000 shares of Class A common stock held by non-affiliates as of such date. For purposes of this calculation only, shares of all voting stock are deemed to have a market value of $62.00 per share, the closing price of

the Class A common stock as reported on the NASDAQ Global Select MarketSM on March 29, 2018 (the last trading day of the registrant’s most recently completed fiscal second quarter). Shares of common stock held by any executive officer or

director of the registrant (including all shares beneficially owned by the Johnson Family, as defined herein) have been excluded from this computation because such persons may be deemed to be affiliates. This determination of affiliate status is

not a conclusive determination for other purposes.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2019 Annual Meeting of the Shareholders of the Registrant are incorporated by reference into Part III of

this report.

As used in this report, the terms “we,” “us,” “our,” “Johnson Outdoors” and the “Company” mean Johnson Outdoors Inc. and its subsidiaries

collectively, unless the context indicates another meaning.

|

Page

|

|

|

4

|

|

| 9 | |

| 16 | |

|

16

|

|

| 17 | |

| 17 | |

| 17 | |

| 19 | |

| 20 | |

| 30 | |

| 30 | |

| 30 | |

| 31 | |

| 31 | |

| 32 | |

| 32 | |

| 32 | |

| 33 | |

| 33 | |

| 33 | |

| 34 | |

| 34 | |

| 35 | |

|

F-1

|

Forward Looking Statements

Certain matters discussed in this Form 10-K are “forward-looking statements,” and the Company intends these forward-looking statements to be covered

by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and is including this statement for purposes of those safe harbor provisions. These statements may be identified by the

use of forward-looking words or phrases such as “anticipate,” “believe,” “confident,” “could,” “expect,” “intend,” “may,” “planned,” “potential,” “should,” “will,” “would” or the negative of those terms or other words of similar meaning.

Similarly, statements that describe the Company’s future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to

differ materially from those currently anticipated.

Factors that could affect actual results or outcomes include the matters described under the caption “Risk Factors” in Item 1A of this report and

the following: changes in economic conditions, consumer confidence levels and discretionary spending patterns in key markets; uncertainties stemming from changes in US trade policies, tariffs, and the reaction of other countries to such changes;

the Company’s success in implementing its strategic plan, including its targeted sales growth platforms, innovation focus and its increasing digital presence; litigation costs related to actions of and disputes with third parties, including

competitors; the Company’s continued success in working capital management and cost-structure reductions; the Company’s success in integrating strategic acquisitions; the risk of future writedowns of goodwill or other long-lived assets; the ability

of the Company's customers to meet payment obligations; movements in foreign currencies, interest rates or commodity costs; fluctuations in the prices of raw materials or the availability of raw materials or components used by the Company; any

disruptions in the Company's supply chain as a result of material fluctuations in the Company's order volumes and requirements for raw materials and other components necessary to manufacture and produce the Company's products; the success of the

Company’s suppliers and customers and the impact of any consolidation in the industries of the Company's suppliers and customers; the ability of the Company to deploy its capital successfully; unanticipated outcomes related to outsourcing certain

manufacturing processes; unanticipated outcomes related to litigation matters; and adverse weather conditions. Shareholders, potential investors and other readers are urged to consider these factors in evaluating the forward-looking statements and

are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included herein are only made as of the date of this filing. The Company assumes no obligation, and disclaims any obligation, to update

such forward-looking statements to reflect subsequent events or circumstances.

Trademarks

We have registered the following trademarks, which may be used in this report: Minn Kota®, Cannon®, Humminbird®, Eureka!®, Jetboil®, Old Town®, Ocean KayakTM,

Carlisle® and SCUBAPRO®.

PART I

Johnson Outdoors is a leading global manufacturer and marketer of branded seasonal, outdoor recreation products used primarily for fishing from a

boat, diving, paddling, hiking and camping. The Company’s portfolio of well-known consumer brands has attained leading market positions due to continuous innovation, marketing excellence, product performance and quality. Company values and culture

support innovation in all areas, promoting and leveraging best practices and synergies within and across its subsidiaries to advance the Company’s strategic vision set by executive management and approved by the Board of Directors. The Company is

controlled by Helen P. Johnson-Leipold (Chairman and Chief Executive Officer), members of her family and related entities.

The Company was incorporated in Wisconsin in 1987 as successor to various businesses.

Fishing

The Company’s Fishing segment key brands are: Minn Kota

electric motors for quiet trolling or primary propulsion, marine battery chargers and shallow water anchors; Humminbird sonar and GPS equipment for

fishfinding, navigation and marine cartography; and Cannon downriggers for controlled-depth fishing. Minn Kota trolling motors and shallow water

anchors and Cannon downriggers are designed and manufactured primarily at the Company's Mankato, Minnesota facility. Humminbird sonar and GPS equipment are designed and manufactured in Eufaula, Alabama and Alpharetta, Georgia.

Fishing brands and related accessories are sold across the globe, with the majority of sales coming from North America through large outdoor

specialty retailers, such as Bass Pro Shops and Cabela’s; large retail store chains; marine products distributors; original equipment manufacturers (OEM) of boat brands such as Tracker, Skeeter and Ranger; and internet retailers and distributors.

The Company also sells direct to consumers via its Minn Kota and Humminbird websites. Markets outside of North America are accessed through a network of international distributors.

Fishing has achieved market share gains by focusing on product innovation, quality products and effective marketing. Such consumer marketing and

promotion activities include: product placements on fishing-related television shows; print advertising and editorial coverage in outdoor, general interest and sport magazines; professional angler and tournament sponsorships; packaging and

point-of-purchase materials and offers to increase consumer appeal and sales; the Minn Kota, Humminbird and Cannon brand websites; social media networks; and online promotions.

Camping

The Company’s Camping segment key brands are: Eureka! consumer,

commercial and military tents and accessories, sleeping bags, camping furniture and stoves and other recreational camping products; and Jetboil portable

outdoor cooking systems.

Eureka! consumer tents, sleeping bags, camping furniture, camping stoves and other recreational camping products are mid- to high-price range products sold in

the U.S. and Canada through independent sales representatives, primarily to camping and backpacking specialty stores, sporting goods stores, internet retailers and direct to consumer via the Eureka! brand website. Marketing of the Company’s tents,

sleeping bags and other recreational camping products is focused on building the Eureka! brand name and establishing the Company as a leader in tent design and innovation. The Company’s consumer camping tents and sleeping bags are produced by third

party manufacturing sources in Asia. Eureka! camping products are sold under license in Japan and Australia. Consumer marketing and promotion activities include: digital marketing and social media networks; print advertising and editorial

coverage in general outdoor magazines.

Eureka! commercial tents include party tents and accessories, sold primarily to general rental stores, and other commercial tents and accessories sold

directly to tent erectors. The Company’s commercial tent products range from 10’x10’ canopies to 120’ wide pole tents and other large scale frame structures and are primarily manufactured by the Company at the Company’s Binghamton, New York

location.

Eureka! also designs and manufactures large, heavy-duty tents and lightweight backpacking tents primarily for the U.S. military at its Binghamton,

New York location. Tents produced for military use in the last twelve months include modular general purpose tents, rapid deployment shelters and various lightweight one and two person tents. The Company manufactures military tent accessories like

fabric floors and insulated thermal liners and is also a subcontract manufacturer for other providers of military tents.

Jetboil portable outdoor cooking systems, single burner and two burner stoves, and accessories are sold in the U.S. and Canada through independent

sales representatives, primarily to camping and backpacking specialty stores, sporting goods stores, internet retailers, and direct to consumer via the Jetboil brand website. Marketing of Jetboil systems is focused on building brand awareness and

leadership in product features and innovation. Jetboil products are produced at both the Company’s operating location in Manchester, New Hampshire and by third party manufacturing sources in Asia. Jetboil products are sold in approximately 30

countries around the world. Markets outside of North America are accessed through a network of international distributors.

During fiscal 2018, the Company sold its Silva North America trademark rights to Silva Sweden AB.

Watercraft Recreation

The Company’s Watercraft Recreation segment designs and markets canoes and kayaks, including pedal-driven and Minn Kota motor-driven kayaks, under

the Ocean Kayaks and Old Town brand names for

family recreation, touring, angling and tripping. These brands are manufactured at the Company’s facility in Old Town, Maine.

The Company uses a rotational molding process for manufacturing mid- to high-end polyethylene kayaks and canoes and uses a thermoform molding

process in the manufacturing of lower priced models at its facility in Old Town, Maine. Watercraft Recreation accessory brands, including Carlisle

branded paddles, are produced primarily by third party sources located in North America and Asia.

The Company’s kayaks, canoes and accessories are sold through multiple channels in the U.S., Europe and the Pacific Basin with an emphasis on

independent specialty retailers and large outdoor retailers. The Company also sells equipment direct to consumers via the Old Town and Ocean Kayak websites. The Company has a network of distributors who sell Company products outside of North

America.

The Company’s Watercraft Recreation business competes in the mid- to high-end of the product category by introducing product innovations, creating

quality products and by focusing on the product-specific needs of each marketing channel. Consumer marketing and promotion activities include: digital marketing and social media networks; print advertising and editorial coverage in outdoor,

general interest and sport magazines; and direct marketing.

Diving

The Company manufactures and markets underwater diving products for recreational divers, which it sells and distributes under the SCUBAPRO brand name.

The Company markets a complete line of underwater diving and snorkeling equipment, including regulators, buoyancy compensators, dive computers and

gauges, wetsuits, masks, fins, snorkels and accessories. SCUBAPRO diving equipment is marketed to the premium segment and high performance technical diving market. Products are sold via select distribution to independent specialty dive stores

worldwide. These specialty dive stores generally provide a wide range of services to divers, including regular maintenance, product repair, diving education and travel programs. The Company also sells diving gear direct to consumers via the

SCUBAPRO website and to dive training centers, resorts, public safety units and armed forces around the world.

The Company’s consumer communication focuses on building brand awareness and highlighting exclusive product features and consumer benefits of its

product lines. The Company’s communication and distribution strategies reinforce the SCUBAPRO brand’s position as the industry’s quality and innovation leader. The Company markets its equipment in diving magazines, via websites, through social

media and through information and displays in dive specialty stores.

The Company manufactures regulators, dive computers, gauges, and instruments at its Italian and Indonesian facilities. The Company sources buoyancy

compensators, neoprene goods, plastic products, proprietary materials, and other components from third parties.

Financial Information for Business Segments

As noted above, the Company has four reportable business segments. See Note 12 to the consolidated financial statements included elsewhere in this

report for financial information concerning each business segment.

International Operations

See Note 12 to the consolidated financial statements included elsewhere in this report for financial information regarding the Company’s domestic and

international operations. See Note 1, subheading “Foreign Operations and Related Derivative Financial Instruments,” to the consolidated financial statements included elsewhere in this report, along with the information under “Risk Factors” below,

for information regarding risks related to the Company’s foreign operations.

Research and Development

The Company commits significant resources to new product research and development in each of its business segments. Fishing conducts its product research,

design, engineering and software development activities at its locations in Mankato and Little Falls, Minnesota; Alpharetta, Georgia; Toronto, Canada; and Eufaula, Alabama. Diving maintains research and development facilities in Zurich,

Switzerland and Casarza Ligure, Italy. Research and development activities for Watercraft Recreation are performed in Old Town, Maine. Product research, design and innovation for Camping products are conducted at the Company's Binghamton, New

York and Manchester, New Hampshire locations.

The Company expenses research and development costs as incurred, except for software development for new electronics products and bathymetry data collection

and processing. These software development and bathymetry data collection and processing costs are capitalized once technological feasibility is established and then amortized over the expected useful life of the software or database. The amounts

expensed by the Company in connection with research and development activities for each of the last three fiscal years are set forth in the Company’s Consolidated Statements of Operations included elsewhere in this report.

Industry and Competitive Environment

The Company believes its products compete favorably on the basis of product innovation, product performance and marketing support and, to a lesser extent,

price.

Fishing: Minn Kota’s main competitors in the electric trolling

motors business are Motor Guide®, owned by Brunswick Corporation, and private label branded motors sourced primarily from manufacturers in Asia. Competition in this business is focused on technological innovation, product quality and durability as

well as product benefits and features for fishing.

The primary competitors in the marine battery charging business are Dual Pro™ and various Pro Mariner™ products. Competition in this business is based on

charging time, reliability and battery protection. The primary competitor in shallow water anchors is Power Pole®. Competition in this business is based on secure positioning, speed of deployment and quiet operation.

Humminbird’s main competitors in the market for on-boat electronics are Garmin™, Lowrance™, Simrad and Raymarine®. Competition in this

business is primarily focused on the quality of sonar imaging and display, easy to use graphical interfaces as well as the integration of mapping and GPS technology. Humminbird products contain marine cartography features. Competitors offering

marine cartography products include Navionics®, owned by Garmin, and C-Map®, owned by Navico. Competition in this business focuses primarily on quality of data and quantity of available charts for inland lakes and ocean shoreline.

Cannon’s main competitors in the downrigger market are Big Jon Sports®, Walker and Scotty®. Competition in this business primarily focuses on ease of

operation, speed and durability.

Camping: The Company’s Camping brands and products compete in the

sporting goods and specialty segments of the Camping market. Competitive brands with a strong position in the sporting goods channel include Coleman® and private label brands. The Company also competes with specialty companies such as Kelty®, The

North Face®, Marmot® and Big Agnes® on the basis of materials and innovative designs for consumers who want performance products priced at a value.

The Company’s portable outdoor cooking systems compete in the specialty and higher end performance backpacking and camping markets. The primary competitor in

portable outdoor cooking systems is MSR®. Competition in this market is based on product size and weight, ease of use, reliability and performance.

The Company’s competitors in the commercial tent market include Anchor Industries® and Aztec Tents for tension, frame and canopy tents. Competition in the

commercial tent business is based on price, quality, structure, styling, ease of installation and technical support.

The Company sells military tents via third party distributors who hold supply contracts primarily with the U.S. Government, as well as to international

governments. Such supply contracts can be for commercial off-the-shelf products in addition to products required to be built to unique specifications. Competitors in the military tent business include HDT®, Alaska Structures®, Camel, Outdoor

Venture, and Diamond Brand.

Watercraft Recreation: The Company primarily competes in this

segment in the kayak and canoe product categories of the paddlesports market. The Company’s main competitors in this market are Confluence Outdoor, Hobie Cat®, Wenonah Canoe, Jackson Kayak and Legacy Paddlesports™, each of which competes on the

basis of their product’s design, performance, quality and price.

Diving: The main competitors in the Diving segment include Aqua

Lung®, Suunto®, Atomic Aquatics, Oceanic, Cressi and Mares®. Competitive advantage in the life support product category of this segment, which consists of regulators, dive computers, and buoyancy compensators, is a function of product innovation,

performance, quality and safety. Competition in the general diving product category of fins, masks, snorkels and wetsuits is characterized by low barriers to entry and numerous competitors who compete on the basis of product innovation,

performance, quality and price.

Backlog

Unfilled orders for future delivery of products totaled approximately $61 million at September 28, 2018. For the majority of its products, the Company’s

businesses do not receive significant orders in advance of expected shipment dates.

Employees

At September 28, 2018, the Company had approximately 1,200 regular, full-time employees. The Company considers its employee relations to be excellent.

Temporary employees are utilized primarily to manage peaks in the seasonal manufacturing of products.

Patents, Trademarks and Proprietary Rights

The Company holds patents for various of the products it sells and regularly files applications for patents. The Company has numerous trademarks and trade

names which it considers important to its business, many of which are noted in this report. Historically, the Company has vigorously defended its intellectual property rights and expects to continue to do so.

Supply Chain and Sourcing of Materials

The Company manufactures some products that use parts or materials that, due to geographical distance, limited supplier capacity or availability or competing

demands for such parts or materials, are only available in a cost effective manner from a single vendor or require the Company to place orders several months in advance of required delivery.

The Company attempts to mitigate product availability and these supply chain risks when possible through the purchase of safety stock, use of forecast-based

supply contracts, and, to a lesser extent, with just in time inventory deliveries or supplier-owned inventory located close to the Company’s manufacturing locations. The Company strives to balance the businesses’ need to maintain adequate

inventory levels with the cost of holding such inventory by manufacturing to forecast for high volume products, utilizing build-to-order strategies wherever possible, and by having contract-manufactured products delivered to customers directly from

the supplier. The Company also seeks to manage its inventory through on-going product design and logistical initiatives with its suppliers to reduce lead times.

As most military contracts require utilization of domestic suppliers, the Company is limited to key vendors for materials used in its military tent business.

Seasonality

The Company’s products are warm-weather, outdoor recreation-related, which results in seasonal variations in sales and profitability. This seasonal

variability is due to customers’ increasing their inventories in the quarters ending March and June, the primary selling season for the Company’s outdoor recreation products, with lower inventory volumes during the quarters ending September and

December. The Company mitigates the seasonality of its businesses somewhat by encouraging customers to purchase and take delivery of products more evenly through the year. The following table shows, for the past three fiscal years, the total

consolidated net sales and operating profit or loss of the Company for each quarter, as a percentage of the total year.

|

Fiscal Year

|

||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

||||||||||||||||||||||

|

Quarter Ended

|

Net

Sales

|

Operating

Profit

|

Net

Sales

|

Operating

Profit

|

Net

Sales

|

Operating

Profit

|

||||||||||||||||||

|

December

|

21

|

%

|

11

|

%

|

19

|

%

|

1

|

%

|

20

|

%

|

(4

|

)%

|

||||||||||||

|

March

|

31

|

%

|

41

|

%

|

30

|

%

|

45

|

%

|

31

|

%

|

66

|

%

|

||||||||||||

|

June

|

31

|

%

|

51

|

%

|

32

|

%

|

54

|

%

|

32

|

%

|

59

|

%

|

||||||||||||

|

September

|

17

|

%

|

(3

|

)%

|

19

|

%

|

0

|

%

|

17

|

%

|

(21

|

)%

|

||||||||||||

|

100

|

%

|

100

|

%

|

100

|

%

|

100

|

%

|

100

|

%

|

100

|

%

|

|||||||||||||

Environment and Climate Change

The Company is subject to various supranational, federal, state and local environmental laws, ordinances, regulations, and other requirements of governmental

authorities. We believe we comply with such laws and regulations. Expenditures on environmental compliance have not had, and we believe in the future, are not expected to have, a material adverse effect on the Company’s capital expenditures,

earnings or competitive position. We do not believe that any direct or indirect consequences of legislation related to climate change will have a material adverse effect on our operating costs, facilities or products.

Available Information

The Company maintains a website at www.johnsonoutdoors.com. On its website, the Company makes available, free of charge, its Annual Report on Form 10-K,

quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as soon as reasonably practical after the reports have been electronically filed or furnished to the Securities and Exchange Commission. In addition, the

Company makes available on its website, free of charge, its (a) proxy statement for its annual meeting of shareholders; (b) Code of Business Conduct; (c) Code of Ethics for its Chief Executive Officer and Senior Financial and Accounting Officers;

and (d) the charters for the following committees of the Board of Directors: Audit; Compensation; Executive; and Nominating and Corporate Governance. Except as specifically provided herein, the Company is not including the information contained on

or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K. This report includes all material information about the Company that is included on the Company’s website and is

otherwise required to be included in this report. Copies of any materials the Company files with the Securities and Exchange Commission (SEC) can also be obtained free of charge through the SEC’s website at www.sec.gov. The SEC’s Public

Reference Room can be contacted at 100 F Street, N.E., Washington, D.C. 20549, or by calling 1 (800) 732-0330.

The risks described below are not the only risks we face. Additional risks that we do not yet know of or that we currently think are immaterial may also

impair our future business operations. If any of the events or circumstances described in the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. In such cases, the

trading price of our common stock could decline.

Our net sales and profitability depend on our ability to continue to conceive, design and market products that appeal to our consumers.

Our business depends on our ability to continue to conceive, design, manufacture and market new products and upon continued market acceptance of our product

offering. Rapidly changing consumer preferences and trends make it difficult to predict how long consumer demand for our existing products will continue or what new products will be successful. A decline in consumer demand for our products, our

failure to develop new products on a timely basis in anticipation of changing consumer preferences or the failure of our new products to achieve and sustain consumer acceptance could reduce our net sales and profitability.

Competition, consolidation and financial distress in our markets could reduce our net sales, profitability and cash flows.

We operate in highly competitive markets. We compete with several large domestic and foreign companies such as Brunswick, Navico, Garmin, Confluence Outdoor

and Aqua Lung International, with private label products sold by many of our retail customers and with other producers of outdoor recreation products. Some of our competitors have longer operating histories, stronger brand recognition and greater

financial, technical, marketing and other resources than us. In addition, we may face competition from new participants in our markets because some of the outdoor recreation product industries have limited barriers to entry. We experience price

competition for our products, and competition for shelf space at retailers, all of which may increase in the future. Consolidation of our retail markets could result in fewer but larger retail customers, which may further result in lower selling

prices or reduced sales volumes of our products or greater competition for shelf space in these retail markets. Further, financial distress or bankruptcies in our retail markets could negatively impact our operating results and cash flows. If we

cannot compete in our product markets successfully in the future, our net sales, profitability and cash flows will likely decline.

General economic conditions affect the Company’s results.

Our revenues are affected by economic conditions and consumer confidence worldwide, but especially in the United States and Europe. In times of economic

uncertainty, consumers tend to defer expenditures for discretionary items, which affects demand for our products. Moreover, our businesses are cyclical in nature, and their success is impacted by general economic conditions and specific economic

conditions affecting the regions and markets we serve, the overall level of consumer confidence in the economy and discretionary income levels. Any substantial deterioration in general economic conditions that diminishes consumer confidence or

discretionary income can reduce our sales and adversely affect our financial results. Moreover, declining economic conditions create the potential for future impairments of goodwill and other intangible and long-lived assets that may negatively

impact our financial condition and results of operations. The impact of weak consumer credit markets, corporate restructurings, layoffs, prolonged high unemployment rates, declines in the value of investments and residential real estate, higher

fuel prices and increases in federal and state taxation all can negatively affect our operating results.

Intellectual property disputes relating to our products could increase our costs.

Our industry is susceptible to litigation regarding patent infringement and infringement of other intellectual property rights. We could be either a plaintiff

or a defendant in trademark, patent and/or other intellectual property infringement or misappropriation claims and claims of breach of license from time to time. The prosecution or defense of any intellectual property litigation is both costly and

disruptive of the time and resources of our management and product development teams, even if the claim or defense against us is without merit. The scope of any patent or other intellectual property to which we have or may obtain rights also may

not prevent others from developing and selling competing products. The validity and breadth of claims covered in patents and other intellectual property involve complex legal and factual questions, and the resolution of such claims may be highly

uncertain, lengthy and expensive. In addition, our patents or other intellectual property may be held invalid upon challenge, or others may claim that we have improperly or invalidly sought patent or other intellectual property protection for our

technology, thus exposing us to direct or counter claims in any patent or intellectual property proceeding. We could also be required to pay substantial damages or settlement costs to resolve intellectual property litigation. Furthermore, we may

rely on trade secret law to protect technologies and proprietary information that we cannot or have chosen not to patent. Trade secrets, however, are difficult to protect. Although we attempt to maintain protection through confidentiality

agreements with necessary personnel, contractors and consultants, we cannot guarantee that such contracts will not be breached. In the event of a breach of a confidentiality agreement or the divulgence of proprietary information, we may not have

adequate legal remedies to maintain our trade secret protection. Litigation to determine the scope of intellectual property rights, even if ultimately successful, could be costly and could divert management’s attention away from the Company’s

business. Any of these negative events could adversely affect our profitability or operating results.

Product recalls and other claims could affect our financial position and results of operations.

As a manufacturer and distributor of consumer products, we could be required to repurchase or recall one or more of our products if they are found to not meet

quality or safety standards or be defective. A repurchase or recall of our products could be costly to us and could damage the reputation of our brands. If we were required to remove, or voluntarily remove our products from the market, our

reputation could be tarnished and we might have large quantities of finished products that we could not sell. As a result, product recalls could have a material adverse effect on our business, results of operations and financial condition.

Impairment charges could impact our future financial position and results of operations.

We test our goodwill, other indefinite-lived intangible assets and other long-lived assets for impairment on an annual basis or when an event occurs that

might reduce the fair value of the reporting unit or applicable asset or group of assets below its carrying value. Various uncertainties, including significant adverse changes in business climate, adverse actions by regulators, unanticipated

competition, loss of key customers, a downturn in the economy or in discretionary income levels or changes in consumer preferences could impact the expected cash flows to be generated by an asset or group of assets, and may result in an impairment

of those assets. Although any such impairment charge would be a non-cash expense, any impairment of our assets could materially increase our expenses and reduce our profitability.

Sales of our products are seasonal, which causes our operating results to vary from quarter to quarter.

Sales of our products are seasonal. Historically, our net sales and profitability have peaked in our second and third fiscal quarters due to the buying

patterns of our customers for our products. Seasonal variations in operating results may also cause us to increase our debt levels and interest expense primarily in the second and third fiscal quarters as we fund our working capital requirements.

The trading price of shares of our common stock fluctuates and investors in our common stock may experience substantial losses.

The trading price of our common stock has been volatile and may continue to be volatile in the future. The trading price of our common stock could decline or

fluctuate in response to a variety of factors, including:

| • |

the timing of our announcements or those of our competitors concerning significant product developments, acquisitions or financial performance;

|

| • |

fluctuation in our quarterly operating results;

|

| • |

substantial sales of our common stock;

|

| • |

general stock market conditions; or

|

| • |

other economic or external factors.

|

You may be unable to sell your stock at or above your purchase price.

A limited number of our shareholders can exert significant influence over the Company.

As of October 17, 2018, Helen P. Johnson-Leipold, members of her family and related entities (hereinafter the Johnson Family), held approximately 76% of the

voting power of both classes of our common stock taken as a whole. This voting power would permit these shareholders, if they chose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning

the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions. Moreover, certain members of the Johnson Family have entered into a voting trust agreement covering

approximately 96% of our outstanding class B common shares. This voting trust agreement permits these shareholders, if they continue to choose to act together, to exert significant influence over the outcome of shareholder votes, including votes

concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions.

We may experience difficulties in integrating strategic acquisitions.

We have, as part of our strategy, historically pursued strategic acquisitions. The pursuit of future growth through acquisitions involves significant risks

that could have a material adverse effect on our business. Risks associated with integrating strategic acquisitions include:

| • |

the acquired business may experience losses which could adversely affect our profitability;

|

| • |

unanticipated costs relating to the integration of acquired businesses may increase our expenses and reduce our profitability;

|

| • |

the possible failure to obtain any necessary consents to the transfer of licenses or other material agreements of the acquired company;

|

| • |

the possible failure to maintain customer, licensor and other relationships of the acquired company after the closing of the transaction with the acquired company;

|

| • |

difficulties in achieving planned cost savings and synergies may increase our expenses;

|

| • |

diversion of our management’s attention could impair their ability to effectively manage our other business operations;

|

| • |

unanticipated management or operational problems or liabilities may adversely affect our profitability and financial condition; and/or

|

| • |

breaches of the representations or warranties or other violations of the contractual obligations required by the acquisition agreement of other parties to the

acquisition transaction and any contractual remedies related thereto may not adequately protect or compensate us.

|

We are dependent upon certain key members of management.

Our success will depend to a significant degree on the abilities and efforts of our senior management. Moreover, our success depends on our ability to

attract, retain and motivate qualified management, marketing, technical and sales personnel. These people are in high demand and often have competing employment opportunities. The labor market for skilled employees is highly competitive and we may

lose key employees or be forced to increase their compensation to retain these people. Employee turnover could significantly increase our recruitment, training and other related employee costs. The loss of key personnel, or the failure to attract

qualified personnel, could have a material adverse effect on our business, financial condition or results of operations.

Sources of and fluctuations in market prices of raw materials can affect our operating results.

The primary raw materials we use in manufacturing our products are metals, resins and packaging materials. These materials are generally available from a

number of suppliers, but we have chosen to concentrate our sourcing with a limited number of vendors for each commodity or purchased component. We believe our sources of raw materials are reliable and adequate for our needs. However, the

development of future sourcing issues related to the availability of these materials as well as significant fluctuations in the market prices of these materials may have an adverse effect on our financial results.

Our profitability is also affected by significant fluctuations in the prices of the raw materials we use in our products, including the effect of fluctuations

in foreign currency exchange rates on raw materials and purchased components. We may not be able to pass along any price increases in our raw materials or other component costs to our customers. As a result, an increase in the cost of raw

materials, labor or other costs associated with the manufacturing of our products could increase our costs of sales and reduce our gross margins.

Financial distress in supply chain and shortage of raw materials or components of supply.

Deteriorating industry conditions can adversely affect our supply base. Lower production levels at our major suppliers and volatility in certain raw material

and energy costs may result in severe financial distress among many companies within our supply base. Financial distress within our supply base and/or our suppliers’ inability to obtain credit from lending institutions could lead to commercial

disputes and possible supply chain interruptions to our business. In addition, potential adverse industry conditions may require us to provide financial assistance or other measures to ensure uninterrupted production of key components or materials

used in the production of our products which could have a material adverse effect on our existing and future revenues and net income.

Additionally, in the event of catastrophic acts of nature such as fires, tsunamis, hurricanes and earthquakes or a rapid increase in production demands,

either we, or our suppliers may experience supply shortages of raw materials or components. This could be caused by a number of factors, including a lack of production line capacity or manpower or working capital constraints. As our industry

consolidates its supply base in order to manage the costs of purchased goods and services, there is greater dependence on fewer sources of supply for certain components and materials used in our products, which could increase the possibility of a

supply shortage of any particular component. If we or one of our own suppliers experience a supply shortage, we may become unable to produce the affected products if we cannot procure the components from another source. Such production

interruptions could impede a ramp-up in production and could have a material adverse effect on our business, results of operations and financial condition.

We consider the production capacities and financial condition of suppliers in our selection process, and expect that they will meet our delivery

requirements. However, there can be no assurance that strong demand, capacity limitations, shortages of raw materials, labor disputes or other problems will not result in any shortages or delays in the supply of components to us.

Currency exchange rate fluctuations could adversely affect the Company’s results.

We have significant foreign operations, for which the functional currencies are denominated primarily in euros, Swiss francs, Hong Kong dollars and Canadian

dollars. As the values of the currencies of the foreign countries in which we have operations increase or decrease relative to the U.S. dollar, the sales, expenses, profits, losses, assets and liabilities of our foreign operations, as reported in

our consolidated financial statements, increase or decrease, accordingly. Approximately 16% of our revenues for the year ended September 28, 2018 were denominated in currencies other than the U.S. dollar. Approximately 7% were denominated in euros

and approximately 6% were denominated in Canadian dollars with the remaining 3% denominated in various other foreign currencies. We may mitigate a portion of the impact of fluctuations in certain foreign currencies on our operations through the

purchase of foreign currency swaps, forward contracts and options to hedge known commitments denominated in foreign currencies or to reduce the risk of changes in foreign currency exchange rates on foreign currency borrowings.

Because we rely on foreign suppliers and we sell products in foreign markets, we are susceptible to numerous international business risks

that could increase our costs or disrupt the supply of our products.

Our international operations subject us to risks, including:

| • |

economic and political instability;

|

| • |

restrictive actions by foreign governments;

|

| • |

opportunity costs and reputational damage related to the presence of counterfeit versions of the Company’s products in such foreign markets;

|

| • |

greater difficulty enforcing intellectual property rights and weaker laws protecting intellectual property rights;

|

| • |

changes in tariffs, import duties or import or export restrictions;

|

| • |

timely shipping of product and unloading of product, including the timely rail/truck delivery to our warehouses and/or a customer’s warehouse of our products;

|

| • |

complications in complying with the laws and policies of the United States affecting the importation of goods, including tariffs, duties, quotas and taxes;

|

| • |

required compliance with U.S. laws that impact the Company’s operations in foreign jurisdictions that do not impact local operating companies; and

|

| • |

complications in complying with trade and foreign tax laws.

|

Any of these risks could disrupt the supply of our products or increase our expenses. In particular, the uncertainty regarding the ability of certain

European countries to continue to service their sovereign debt obligations and the related financial restructuring efforts by European governments, as well as the impact of the decision of the United Kingdom to withdraw from the European Union, may

cause the value of several European currencies, including the euro, to fluctuate, which may adversely affect our non-U.S. dollar sales and earnings. As we have manufacturing operations in Italy, a significant disruption of the political or

financial systems there could put these manufacturing operations at risk, which could ultimately adversely affect our profitability or operating results.

Uncertainty over global tariffs, or the financial impact of tariffs, may negatively affect our results.

Recent changes in U.S. domestic and global tariff frameworks have increased our costs of producing goods and resulted in additional risks to our supply chain.

More tariff changes are also possible. We have developed strategies to mitigate previously implemented and, in some cases, proposed tariff increases, but there is no assurance we will be able to continue to mitigate the impact of tariff increases

in substantial part on our financial and operating results. Further, uncertainties about future tariff changes could result in mitigation actions undertaken by us that could prove to be detrimental to our business and our relationships with our

customers and suppliers.

The recently implemented tariffs are estimated to negatively impact our fiscal 2019 operating profit in the range of $6 million to $9 million, which includes

any expected benefit of mitigation efforts contemplated by us and which are identified to date.

We may be subject to disruptions or failures in our information technology systems and network infrastructures that could have a material

adverse effect on our business.

We rely on the efficient and uninterrupted operation of complex information technology systems and network infrastructures to operate our business. We also

hold data in various company-owned and third party data center facilities upon which our business depends. A disruption, infiltration or failure of these information technology systems or any of these data centers as a result of software or

hardware malfunctions, system implementations or upgrades, computer viruses, third-party security breaches, employee error, theft or misuse, malfeasance, power disruptions, natural disasters or accidents could cause breaches of data security, loss

of intellectual property and critical data and the release and misappropriation of sensitive competitive information. Any of these events could result in the loss of key information, impair our production and supply chain processes, harm our

competitive position, damage our reputation with customers, cause us to incur significant costs to remedy any damages and ultimately materially and adversely affect our business, results of operations and financial condition. While we have

implemented a number of protective measures, such measures may not be adequate or implemented properly to prevent or fully address the adverse effect of such events.

Cyber security vulnerabilities, threats and more sophisticated and targeted computer crime could pose a risk to our systems, networks,

products, solutions, services and data.

Increased global cyber security vulnerabilities, threats, computer viruses and more sophisticated and targeted cyber-related attacks, as well as cyber

security failures resulting from human error and technological errors, pose a risk to our systems, products and data as well as potentially to our employees’, customers’ and suppliers’ data. We attempt to mitigate these risks by employing a number

of measures, including employee training, monitoring and testing, and maintenance of protective systems and contingency plans, but we remain potentially vulnerable to additional known or unknown threats. There is no assurance the impact from such

threats will not be material to our financial results or reputation and it could result in security breaches, theft, lost or corrupted data, misappropriation of sensitive, confidential or personal data or information, loss of trade secrets and

commercially valuable information, production downtimes and operational disruptions, any of which may adversely affect our profitability or operating results.

Our failure to adequately protect personal information could have a material adverse effect on our business.

A wide variety of local, state, national, and international laws, directives and regulations apply to the collection, use, retention, protection, disclosure,

transfer, and other processing of personal data (including with respect to the European Union's General Data Protection Regulation). These data protection and privacy-related laws and regulations continue to evolve and may result in ever-increasing

regulatory and public scrutiny and escalating levels of enforcement and sanctions and increased costs of compliance. Our failure to comply with applicable laws and regulations, or to protect such data, could result in enforcement actions against

us, including fines, imprisonment of company officials and public censure, claims for damages by end-customers and other affected individuals, damage to our reputation and loss of goodwill (both in relation to existing end-customers and prospective

end-customers), any of which could have a material adverse effect on our operations, financial performance, and business. Changing definitions of personal data and personal information, within the European Union, the United States, and elsewhere

may limit or inhibit our ability to operate or expand our business, including limiting strategic partnerships that may involve the sharing of data. The evolving data protection regulatory environment may require significant management attention and

financial resources to analyze and modify our information technology infrastructure to meet these changing requirements all of which could reduce our operating margins and impact our operating results and financial condition.

Future terror attacks, war, natural disasters or other catastrophic events beyond our control could negatively impact our business.

Terror attacks, war or other civil disturbances, natural disasters and other catastrophic events could lead to economic instability and decreased demand for

our products, which could negatively impact our business, financial condition, results of operations and cash flows. In the past, terrorist attacks have caused instability in global financial markets and the industries in which we compete and have

negatively affected spending on consumer discretionary products. In addition, our facilities are located throughout the world and could be subject to damage from terrorism incidents or from fires, floods, earthquakes or other natural or man-made

disasters. Terrorist incidents could also lead to increased border security which could in turn negatively impact our global supply chain by causing shipping delays or shortages in key materials or components, increasing the cost of such goods or

requiring us to keep greater inventories, any of which may adversely impact our business, results of operations, financial condition or cash flows.

The inability to successfully defend claims asserted by taxing authorities could adversely affect our financial condition, results of

operations and cash flows.

We conduct business in many countries, which requires us to interpret the income tax laws and rulings in each of those taxing jurisdictions. Due to the

subjectivity of tax laws in or between those jurisdictions, as well as the subjectivity of factual interpretations, our estimates of income tax liabilities may differ from actual payments or assessments. Claims from taxing authorities related to

these differences could have an adverse impact on our financial condition, results of operations and cash flows.

The effective tax rate of the Company may be negatively impacted by future changes to tax laws in global jurisdictions in which we operate.

Changes in tax laws or tax rulings could have a material impact on our effective tax rate. Many countries in the European Union, as well as a number of other

countries and organizations such as the Organization for Economic Cooperation and Development, are actively considering changes to existing tax laws. Certain proposals could include recommendations that could increase our tax obligations in many

countries where we do business. Any changes in the taxation of our activities in such jurisdictions may result in a material increase in our effective tax rate.

We are subject to environmental, safety and human rights regulations.

We are subject to supranational, federal, state, local and foreign laws and other legal requirements related to the generation, storage, transport, treatment

and disposal of materials as a result of our manufacturing and assembly operations. These laws include the Resource Conservation and Recovery Act (as amended), the Clean Air Act (as amended) and the Comprehensive Environmental Response,

Compensation and Liability Act (as amended). Risk of environmental liability and changes associated with maintaining compliance with environmental laws is inherent in the nature of our business and there is no assurance that material liabilities

or changes would not arise.

The Company is also subject to the requirement of Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act and SEC rules related thereto

to conduct due diligence and disclose and report on whether certain minerals and metals, known as “conflict minerals,” are contained in the Company’s products and whether they originate from the Democratic Republic of Congo (“DRC”) and adjoining

countries. We may face reputational challenges if we determine that certain of our products contain minerals not determined to be conflict free or if we are unable to sufficiently verify the origins of all conflict minerals used in our products

through the procedures we implement.

We rely on our credit facilities to provide us with sufficient working capital to operate our business.

Historically, we have relied upon our existing credit facilities to provide us with adequate working capital to operate our business. If our lenders reduce

or terminate our access to amounts under our credit facilities, we may not have sufficient capital to fund our working capital needs and/or we may need to secure additional capital or financing to fund our working capital requirements or to repay

outstanding debt under our credit facilities. We can make no assurance that we will be successful in ensuring our availability of amounts under our credit facilities or in connection with raising additional capital and that any amount, if raised,

will be sufficient to meet our cash flow requirements. If we are not able to maintain our borrowing availability under our credit facilities and/or raise additional capital when needed, we may be forced to sharply curtail our efforts to

manufacture and promote the sale of our products or to curtail our operations.

Our debt covenants may limit our ability to complete acquisitions, incur debt, make investments, sell assets, merge or complete other

significant transactions.

Our credit facilities and certain other of our debt instruments include limitations on a number of our activities in the event of a default, and in some cases

regardless of whether a default has occurred, including our ability to:

| • |

incur additional debt;

|

| • |

create liens on our assets or make guarantees;

|

| • |

make certain investments or loans; or

|

| • |

dispose of or sell assets, make acquisitions above certain amounts or enter into a merger or similar transaction.

|

The restrictive covenants in our credit facilities may limit our ability to engage in acts that may be in our best long term interests. A breach of any of

the restrictive covenants in our credit facilities could result in a default under these facilities. If a default occurs, the lenders under our credit facilities may elect to declare all outstanding borrowings, together with accrued interest, to

be immediately due and payable, to terminate any commitments they have to provide further borrowings and to exercise any other rights they have under the facilities or applicable law.

Our shares of common stock are thinly traded and our stock price may be volatile.

Because our common stock is thinly traded, its market price may fluctuate significantly more than the stock market in general or the stock prices of similar

companies, which are exchanged, listed or quoted on NASDAQ. We believe there are approximately 4,955,000 shares of our Class A common stock held by non-affiliates as of October 17, 2018. Thus, our common stock will be less liquid than the stock of

companies with broader public ownership, and as a result, the trading price for our shares of common stock may be more volatile. Among other things, trading of a relatively small volume of our common stock may have a greater impact on the trading

price for our stock than would be the case if our public float were larger.

Our business is susceptible to adverse weather conditions or events.

Our success is in part affected by adverse weather conditions, including fires, floods, tornadoes, severe cold and other natural disasters. Such events have

the tendency to create fluctuations in demand for our products which may impact our borrowing costs, increase our expenses and reduce our profitability. Moreover, our profitability is affected by our ability to successfully manage our inventory

levels and demand for our products, which, in part depends upon the efficient operation of our production and delivery systems. These systems are vulnerable to damage or interruption from the aforementioned natural disasters. Such natural

disasters could adversely impact our ability to meet delivery requirements of our customers, which may result in our need to incur extra costs to expedite production and delivery of product to meet customer demand. Any of these events could

negatively impact our profitability.

Not Applicable

The Company maintains leased and owned manufacturing, warehousing, distribution and office facilities throughout the world. The Company believes

that its facilities are well maintained and have capacity adequate to meet its current needs.

See Note 5 to the consolidated financial statements included elsewhere in this report for a discussion of the Company’s lease obligations.

As of September 28, 2018, the Company’s principal manufacturing (identified with an asterisk) and other locations are:

Alpharetta, Georgia (Fishing)

Antibes, France (Diving)

Barcelona, Spain (Diving)

Batam, Indonesia* (Diving)

Binghamton, New York* (Camping)

Brussels, Belgium (Diving)

Burlington, Ontario, Canada (Fishing, Camping, Watercraft Recreation)

Casarza Ligure, Italy* (Diving)

Chai Wan, Hong Kong (Diving)

Chatswood, Australia (Diving)

El Cajon, California (Diving)

Eufaula, Alabama* (Fishing)

Little Falls, Minnesota (Fishing)

Manchester, New Hampshire* (Camping)

Mankato, Minnesota* (Fishing)

Mexicali, Mexico* (Fishing)

Old Town, Maine* (Watercraft Recreation)

Toronto, Canada (Fishing)

Nuremberg, Germany (Diving)

Zurich, Switzerland (Diving)

The Company’s corporate headquarters is located in a facility in Racine, Wisconsin.

In the normal course of business, we may be involved in various legal proceedings from time to time. As of the date of the filing of this Report, we are not

involved in any litigation involving amounts deemed to be material to the business or financial condition of the Company.

None.

PART II

|

ITEM 5.

|

Market Information

Certain information with respect to this item is included in Notes 9 and 10 to the Company’s consolidated financial statements included elsewhere in this

report. The Company’s Class A common stock is traded on the NASDAQ Global Select MarketSM under the symbol: JOUT. There is no public market for the Company’s Class B common stock. However, the Class B common stock is convertible at all

times at the option of the holder into shares of Class A common stock on a share for share basis. As of October 17, 2018, the Company had approximately 540 holders of record of its Class A common stock and 24 holders of record of its Class B common

stock. We believe the number of beneficial owners of our Class A common stock on that date was substantially greater.

A summary of the high and low closing prices for the Company’s Class A common stock during each quarter of the years ended September 28, 2018, September 29,

2017 and September 30, 2016 is as follows:

|

First Quarter

|

Second Quarter

|

Third Quarter

|

Fourth Quarter

|

|||||||||||||||||||||||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

2018

|

2017

|

2016

|

2018

|

2017

|

2016

|

2018

|

2017

|

2016

|

|||||||||||||||||||||||||||||||||||||

|

Stock prices:

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

High

|

$

|

75.21

|

$

|

44.86

|

$

|

24.24

|

$

|

74.48

|

$

|

37.77

|

$

|

22.99

|

$

|

86.66

|

$

|

48.85

|

$

|

26.75

|

$

|

105.16

|

$

|

73.28

|

$

|

36.62

|

||||||||||||||||||||||||

|

Low

|

59.92

|

34.72

|

21.43

|

60.16

|

31.68

|

19.69

|

61.82

|

33.38

|

20.79

|

78.92

|

46.68

|

26.09

|

||||||||||||||||||||||||||||||||||||

Dividends

The Company’s Articles of Incorporation provide that no dividend, other than a dividend payable in shares of the Company’s common stock, may be declared or

paid upon the Class B common stock unless such dividend is declared or paid upon both classes of common stock. Whenever a dividend (other than a dividend payable in shares of Company common stock) is declared or paid upon any shares of Class B

common stock, at the same time there must be declared and paid a dividend on the shares of Class A common stock equal in value to 110% of the amount per share of the dividend declared and paid on the shares of Class B common stock. Whenever a

dividend is payable in shares of Company common stock, such dividend must be declared or paid at the same rate on the Class A common stock and the Class B common stock.

Quarterly dividends declared in the first quarter of fiscal 2018 were $0.10 per share of Class A common stock, $0.12 per share for each of the second and

third fiscal quarters of fiscal 2018 and $0.14 per share for the fourth fiscal quarter of 2018. Quarterly dividends declared per share of Class B common stock were $0.09 for the first quarter of fiscal 2018, $0.11 per share for each of the second

and third fiscal quarters of 2018 and $0.13 per share for the fourth fiscal quarter of 2018. Total dividends declared in fiscal 2018 were $4,746. Cash dividends paid in fiscal 2018 totaled $4,350 and dividends payable of $1,384 were included in

current liabilities at September 28, 2018.

While the Board of Directors of the Company presently intends to continue the payment of regular quarterly cash dividends on the Company’s common stock, they

monitor and evaluate the Company’s dividend payment practice quarterly and may elect to increase, decrease or not pay a dividend at any time. The Company’s ability to pay dividends could be affected by future business performance, liquidity,

capital needs, alternative investment opportunities and compliance with debt covenants in its loan agreements.

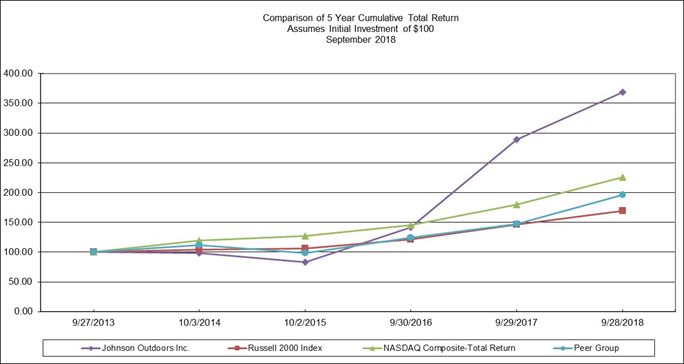

Total Shareholder Return

The graph below compares on a market cap weighted cumulative basis the yearly percentage change since September 27, 2013 in the total return (assuming

reinvestment of dividends) to shareholders on the Class A common stock with (a) the total return (assuming reinvestment of dividends) on The NASDAQ Stock Market-U.S. Index; (b) the total return (assuming reinvestment of dividends) on the Russell

2000 Index; and (c) the total return (assuming reinvestment of dividends) on a self-constructed peer group index. The Company’s peer group consists of Black Diamond Inc., Brunswick Corporation, Callaway Golf Company, Escalade Inc., Garmin Ltd.,

Marine Products Corporation, Malibu Boats Inc. and Nautilus, Inc. The graph assumes $100 was invested on September 27, 2013 in the Company’s Class A common stock, The NASDAQ Stock Market-U.S. Index, the Russell 2000 Index and the peer group index.

|

*

|

$100 invested on September 27, 2013 in stock or index, including reinvestment of dividends.

|

Indices calculated on a mid-month basis.

|

9/27/2013

|

10/3/2014

|

10/2/2015

|

9/30/2016

|

9/29/2017

|

9/28/2018

|

|||||||||||||||||||

|

Johnson Outdoors Inc.

|

$

|

100.0

|

$

|

98.1

|

$

|

83.1

|

$

|

142.0

|

$

|

288.9

|

$

|

368.9

|

||||||||||||

|

NASDAQ Composite

|

100.0

|

119.8

|

127.5

|

145.7

|

180.2

|

225.5

|

||||||||||||||||||

|

Russell 2000 Index

|

100.0

|

104.2

|

106.5

|

121.5

|

146.7

|

169.0

|

||||||||||||||||||

|

Peer Group

|

100.0

|

112.3

|

98.7

|

124.4

|

147.1

|

195.8

|

||||||||||||||||||

The information in this section titled “Total Shareholder Return” shall not be deemed to be “soliciting material” or “filed” with the Securities and Exchange

Commission or subject to Regulation 14A or 14C promulgated by the Securities and Exchange Commission or subject to the liabilities of section 18 of the Securities Exchange Act of 1934, as amended, and this information shall not be deemed to be

incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

The following table presents selected consolidated financial data, which should be read along with the Company’s consolidated financial statements and the

notes to those statements and with “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in or referred to elsewhere in this report. The operating results for the years ended September 28, 2018,

September 29, 2017 and September 30, 2016 and the balance sheet data as of September 28, 2018 and September 29, 2017, are derived from the Company’s audited consolidated financial statements included elsewhere herein. The operating results for the

years ended October 2, 2015 and October 3, 2014, and the balance sheet data as of September 30, 2016, October 2, 2015 and October 3, 2014 are derived from the Company’s audited consolidated financial statements which are not included in this

report. The historical results are not necessarily indicative of results to be expected for future periods.

|

(thousands, except per share data)

|

September 28

2018

|

September 29

2017

|

September 30

2016

|

October 2

2015

|

October 3

2014

|

|||||||||||||||

|

OPERATING RESULTS

|

||||||||||||||||||||

|

Net sales

|

$

|

544,268

|

$

|

490,565

|

$

|

433,727

|

$

|

430,489

|

$

|

425,410

|

||||||||||

|

Gross profit

|

241,860

|

210,940

|

176,462

|

171,733

|

168,613

|

|||||||||||||||

|

Impairment losses

|

—

|

—

|

6,197

|

—

|

8,475

|

|||||||||||||||

|

Operating expenses

|

178,839

|

165,349

|

147,371

|

153,880

|

143,447

|

|||||||||||||||

|

Operating profit

|

63,021

|

45,591

|

22,894

|

17,853

|

16,691

|

|||||||||||||||

|

Interest expense

|

203

|

757

|

727

|

865

|

788

|

|||||||||||||||

|

Other (income) expense, net

|

(5,288

|

)

|

(3,376

|

)

|

(1,488

|

)

|

1,235

|

(1,519

|

)

|

|||||||||||

|

Income before income taxes

|

68,106

|

48,210

|

23,655

|

15,753

|

17,422

|

|||||||||||||||

|

Income tax expense

|

27,437

|

13,053

|

10,154

|

5,137

|

8,299

|

|||||||||||||||

|

Net income

|

$

|

40,669

|

$

|

35,157

|

$

|

13,501

|

$

|

10,616

|

$

|

9,123

|

||||||||||

|

Weighted average common shares - Dilutive

|

9,996

|

9,920

|

9,855

|

9,727

|

9,635

|

|||||||||||||||

|

Net income per common share - Diluted:

|

||||||||||||||||||||

|

Class A

|

$

|

4.05

|

$

|

3.51

|

$

|

1.34

|

$

|

1.06

|

$

|

0.90

|

||||||||||

|

Class B

|

4.05

|

3.51

|

1.34

|

1.06

|

0.90

|

|||||||||||||||

|

Dividends declared, per common share*:

|

||||||||||||||||||||

|

Class A

|

$

|

0.48

|

$

|

0.37

|

$

|

0.32

|

$

|

0.31

|

$

|

0.38

|

||||||||||