Attached files

| file | filename |

|---|---|

| EX-3.2 - EX 3.2 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex32jout201010k.htm |

| EX-23.2 - EX 23.2 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex232jout201010k.htm |

| EX-32.1 - EX32.1 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex321jout201010k.htm |

| EX-23.1 - EX 23.1 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex231jout201010k.htm |

| EX-31.2 - EX 31.2 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex312jout201010k.htm |

| EX-21.1 - EX 21.1 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex211jout201010k.htm |

| EX-31.1 - EX31.1 TO JOUT 2010 10-K - JOHNSON OUTDOORS INC | ex311tojout201010k.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[ X ]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended October 1, 2010

OR

|

[____]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ______ to ______

Commission file number 0-16255

JOHNSON OUTDOORS INC.

(Exact name of registrant as specified in its charter)

|

Wisconsin

|

39-1536083

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

555 Main Street, Racine, Wisconsin 53403

(Address of principal executive offices, including zip code)

(262) 631-6600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Exchange on Which Registered

|

|

Class A Common Stock, $.05 par value per share

|

NASDAQ Global MarketSM

|

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [ X ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [ X ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definition of "large accelerated filer,” “accelerated filer" and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large Accelerated Filer [ ]

Accelerated Filer [ ]

Non-Accelerated Filer [ ]

(do not check if a smaller reporting company)

Smaller Reporting Company [ X ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ X ]

As of November 30, 2010, 8,363,485 shares of Class A and 1,216,464 shares of Class B common stock of the registrant were outstanding. The aggregate market value of voting and non-voting Class A common stock of the registrant held by nonaffiliates of the registrant was approximately $51,702,952 on April 1, 2010 (the last business day preceding the registrant’s most recently completed second quarter) based on approximately 4,571,437 shares of Class A common stock held by nonaffiliates. For purposes of this calculation only, shares of all voting stock are deemed to have a market value of $11.31 per share, the closing price of the Class A common stock as reported on the NASDAQ Global MarketSM on April 1, 2010. Shares of common stock held by any executive officer or director of the registrant (including all shares beneficially owned by the Johnson Family) have been excluded from this computation because such persons may be deemed to be affiliates. This determination of affiliate status is not a conclusive determination for other purposes.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2011 Annual Meeting of the Shareholders of the Registrant are incorporated by reference into Part III of this report.

As used in this report, the terms "we," "us," "our," "Johnson Outdoors" and the "Company" mean Johnson Outdoors Inc. and its subsidiaries, unless the context indicates another meaning.

|

TABLE OF CONTENTS

|

Page

|

|

Business

|

1

|

|

Risk Factors

|

6

|

|

Properties

|

10

|

|

Legal Proceedings

|

11

|

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

12

|

|

Selected Financial Data

|

14

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

14

|

|

Quantitative and Qualitative Disclosures about Market Risk

|

21

|

|

Financial Statements and Supplementary Data

|

21

|

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

22

|

|

Controls and Procedures

|

22

|

|

Other Information

|

22

|

|

Directors, and Executive Officers and Corporate Governance

|

23

|

|

Executive Compensation

|

23

|

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

23

|

|

Certain Relationships and Related Transactions, and Director Independence

|

24

|

|

Principal Accountant Fees and Services

|

24

|

|

Exhibits and Financial Statement Schedules

|

24

|

|

Signatures

|

25

|

|

Exhibit Index

|

27

|

|

Consolidated Financial Statements

|

F-1

|

Forward Looking Statements

Certain matters discussed in this Form 10-K are “forward-looking statements,” and the Company intends these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and is including this statement for purposes of those safe harbor provisions. These forward-looking statements can generally be identified as such because they include phrases such as the Company “expects,” “believes,” “anticipates” or other words of similar meaning. Similarly, statements that describe the Company’s future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to differ materially from those currently anticipated.

Factors that could affect actual results or outcomes include the matters described under the caption "Risk Factors" in Item 1A of this report and the following: changes in consumer spending patterns; the Company’s success in implementing its strategic plan, including its focus on innovation and on cost-cutting and revenue enhancement initiatives; actions of and disputes with companies, including companies that compete with the Company; the Company’s success in managing inventory; the risk that the Company’s lenders may be unwilling to provide a waiver or amendment if the Company is in violation of its financial covenants and the cost to the Company of obtaining any waiver or amendment the lenders would be willing to provide; the risk of future writedowns of goodwill or other intangible assets; movements in foreign currencies or interest rates; ability of the Company’s customers to meet payment obligations; fluctuations in the prices of raw materials or the availability of raw materials used by the Company; the Company’s success in restructuring certain of its operations; the success of the Company’s suppliers and customers; the ability of the Company to deploy its capital successfully; unanticipated outcomes related to outsourcing certain manufacturing processes; unanticipated outcomes related to outstanding litigation matters; and adverse weather conditions. Shareholders, potential investors and other readers are urged to consider these factors in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included herein are only made as of the date of this filing. The Company assumes no obligation, and disclaims any obligation, to update such forward-looking statements to reflect subsequent events or circumstances.

Trademarks

We have registered the following trademarks, which are used in this report: Minn Kota®, Cannon®, Humminbird®, Fishin' Buddy®, Silva®, Eureka!®, Tech4O™, Geonav®, Old Town®, Ocean Kayak™, Necky®, Extrasport®, Carlisle®, Scubapro®, UWATEC® and SUBGEAR®.

PART I

ITEM 1. BUSINESS

Johnson Outdoors is a leading global manufacturer and marketer of branded seasonal, outdoor recreation products used primarily for fishing, diving, paddling and camping. The Company’s portfolio of well-known consumer brands has attained leading market positions due to continuous innovation, marketing excellence, product performance and quality. Company values and culture support innovation in all areas, promoting and leveraging best practices and synergies within and across its subsidiaries to advance the Company’s strategic vision set by executive management and approved by the Board of Directors. The Company is controlled by Helen P. Johnson-Leipold (Chairman and Chief Executive Officer), members of her family and related entities.

The Company was incorporated in Wisconsin in 1987 as successor to various businesses.

Marine Electronics

The Company’s Marine Electronic segment brands are: Minn Kota battery-powered fishing motors for quiet trolling or primary propulsion; Humminbird sonar and GPS equipment for fishfinding and navigation; Cannon downriggers for controlled-depth fishing; and Geonav large, leisure boat navigation technology.

Marine Electronics brands and related accessories are sold across the globe, with approximately 75% of sales coming from North America through large outdoor specialty retailers, such as Bass Pro Shops and Cabela’s, large retail store chains, marine products distributors, international distributors and original equipment manufacturers (OEM), such as Ranger Boats and Skeeter Boats.

Marine Electronics has achieved market share gains by focusing on product innovation, quality products and effective marketing. Such consumer marketing and promotion activities include: product placements on fishing-related television shows; print advertising and editorial coverage in outdoor, general interest and sport magazines; professional angler and tournament sponsorships; packaging and point-of-purchase materials and offers to increase consumer appeal and sales; branded websites; social media networks; and online promotions.

Outdoor Equipment

The Company’s Outdoor Equipment segment brands are: Eureka! consumer, commercial and military tents and accessories, sleeping bags, camping furniture and other recreational camping products; Silva field compasses and digital instruments; and Tech40 performance measurement instruments.

Eureka! consumer tents, sleeping bags, camping furniture and other recreational camping products are mid- to high-price range products sold in the U.S. and Canada through independent sales representatives, primarily to sporting goods stores, catalog and mail order houses, camping and backpacking specialty stores, and through internet retailers. Marketing of the Company’s tents, sleeping bags and other recreational camping products is focused on building the Eureka! brand name and establishing the Company as a leader in tent design and innovation. The Company’s camping tents and sleeping bags are produced by third party manufacturing sources in Asia. Eureka! camping products are sold under license in Japan, Australia and Europe.

1

Eureka! commercial tents include party tents and accessories, sold primarily to general rental stores, and other commercial tents and accessories sold directly to tent erectors. The Company’s tent products range from 10’x10’ canopies to 120’ wide pole tents and other large scale frame structures and are manufactured by the Company at the Company’s Binghamton, New York location. Commercial tent accessories include lighting systems, interior lining options, and mounting brackets that allow the interior of the tents to be customized to suit the occasion.

Eureka! also designs and manufactures large, heavy-duty tents and lightweight backpacking tents for the military at its Binghamton, New York location. Tents produced for military use in the last twelve months include modular general purpose tents, rapid deployment shelters and various lightweight one and two person tents. The Company manufactures military tent accessories like fabric floors and tent liners and is also a subcontract manufacturer for other providers of military tents.

Silva field compasses are manufactured by the Company and marketed exclusively in North America where the Company owns Silva trademark rights. Tech40 digital instruments and other branded products are manufactured by third parties and are primarily sold in the North American market.

Watercraft

The Company’s Watercraft brands are: Old Town canoes and kayaks; Ocean Kayak; Necky kayaks; Carlisle paddles; and Extrasport personal flotation devices.

In its Old Town, Maine facility, the Company produces high quality Old Town kayaks, canoes and accessories for family recreation, touring and tripping. The Company uses a rotational molding process for manufacturing polyethylene kayaks and canoes to compete in the high volume, low and mid price range of the market. These kayaks and canoes feature stiffer and more durable hulls than higher priced boats. The Company uses a thermo-form molding process in the manufacturing of lower priced models. The Company also markets canoes built from Royalex (ABS) and wood.

During 2009, the Company consolidated operations for its U.S. paddle sports brands in Old Town, Maine, and closed its plant in Ferndale, Washington. Sit-on-top Ocean Kayaks and high performance Necky sea touring kayaks, which had formerly been produced in Ferndale, are now manufactured at the Old Town, Maine facility.

The Company also manufactures Watercraft products in New Zealand and contracts for manufacturing of Watercraft products with third parties in Michigan, Tunisia and the Czech Republic.

Watercraft accessory brands, including Extrasport personal flotation devices and Carlisle branded paddles, are produced primarily by third-party sources.

The Company’s kayaks, canoes and accessories are sold primarily through large outdoor specialty retailers, such as Bass Pro Shops and Cabela’s, large retail sporting goods stores and catalog and mail order houses in the U.S., Europe and the Pacific Basin.

The Company’s Watercraft business has grown by introducing product innovations, creating quality products and by focusing on the product-specific needs of each marketing channel. Consumer marketing and promotion activities include: print advertising and editorial coverage in outdoor, general interest and sport magazines; direct marketing; branded websites and social media networks.

Diving

The Company manufactures and markets underwater diving products for technical and recreational divers, which it sells and distributes under the SCUBAPRO, UWATEC, SUBGEAR and Seemann brand names.

The Company markets a complete line of underwater diving and snorkeling equipment, including regulators, buoyancy compensators, dive computers and gauges, wetsuits, masks, fins, snorkels and accessories. SCUBAPRO and UWATEC diving equipment is marketed to the premium segment of the market for both diving enthusiasts and more technical, advanced divers. SUBGEAR and Seemann products are marketed to the recreational diver interested in owning quality equipment at an affordable price. Products are sold via select distribution to independent specialty dive stores worldwide. These specialty dive stores generally provide a wide range of services to divers, including sales, service and repair, diving education and travel. The Company also sells diving gear to dive training centers and resorts.

2

The Company focuses on maintaining SCUBAPRO and UWATEC as the market leaders in innovation. The Company maintains research and development functions in the U.S. and holds a number of patents on proprietary products. The Company’s consumer communication focuses on building the brand and highlighting exclusive product features and consumer benefits of the SCUBAPRO and UWATEC product lines. The Company’s communication and distribution reinforce the SCUBAPRO and UWATEC brands’ position as the industry’s quality and innovation leader. The Company markets its equipment in diving magazines, via websites and through dive specialty stores. SUBGEAR and Seemann’s full line of dive equipment and accessories compete in the mid-market on the basis of quality at an affordable price.

The Company manufactures regulators, dive computers, gauges, and instruments at its Italian and Indonesian facilities. The Company sources buoyancy compensators, neoprene goods, plastic products, proprietary materials, and other components from third parties.

Financial Information for Business Segments

As noted above, the Company has four reportable business segments. See Note 14 to the consolidated financial statements included elsewhere in this report for financial information concerning each business segment.

International Operations

See Note 14 to the consolidated financial statements included elsewhere in this report for financial information regarding the Company’s domestic and international operations. See Note 1, subheading “Foreign Operations and Related Derivative Financial Instruments,” to the consolidated financial statements included elsewhere in this report for information regarding risks related to the Company’s foreign operations.

Research and Development

The Company commits significant resources to new product research and development in each of its business segments. Marine Electronics conducts all of its product research, design, engineering and software development activities at its locations in Mankato, Minnesota; Alpharetta and Atlanta, Georgia; Eufaula, Alabama; Shanghai, China; and Viareggio, Italy. Diving maintains research and development facilities in Spreitenbach, Switzerland; and Casarza Ligure, Italy. Research and development activities for Watercraft are performed in Bellingham, Washington. Product research, design and innovation for Outdoor Equipment products are conducted at the Company's Binghamton, New York location.

The Company expenses research and development costs as incurred, except for software development for new electronics products. These costs are capitalized once technological feasibility is established and then amortized over the expected life of the software. The amounts expensed by the Company in connection with research and development activities for each of the last two fiscal years are set forth in the Company’s Consolidated Statements of Operations included elsewhere in this report.

Industry and Competitive Environment

The Company believes its products compete favorably on the basis of product innovation, product performance and marketing support and, to a lesser extent, price.

Marine Electronics: Minn Kota’s main competitors in the electric trolling motors business are Motor Guide, owned by Brunswick Corporation, and private label branded motors sourced primarily from manufacturers in Asia. Competition in this business is focused on technological innovation, product quality and durability as well as product benefits and features for fishing. Humminbird’s main competitors in the fishfinder market are Lowrance and Garmin. Competition in this business is primarily focused on the quality of sonar imaging and display as well as the integration of mapping and GPS technology. Cannon’s main competitors in the downrigger market are Big Jon, Walker and Scotty. Competition in this business primarily focuses on ease of operation, speed and durability. Geonav’s main competitors in the marine navigation business are Raymarine, Garmin, Simrad, and Furuno. Competition in this business is primarily focused on innovative designs, quality, easy to use graphical interfaces, resolution of display imaging, leading edge processing power, sales and service capabilities and ease of product integration with related marine electronics devices.

3

Outdoor Equipment: The Company’s outdoor equipment brands and products compete in the sporting goods and specialty segments of the outdoor equipment market. Competitive brands with a strong position in the sporting goods channel include Coleman and private label brands. The Company also competes with specialty companies such as The North Face, Kelty and Slumberjack on the basis of materials and innovative designs for consumers who want performance products priced at a value.

Commercial tent market competitors include Anchor Industries and Aztec for tension and frame tents, along with canopies based on structure and styling.

The Company sells military tents to prime vendors and third party distributors who hold supply contracts from the U.S. Government. Such supply contracts can be for commercial off-the-shelf products in addition to products required to be built to unique specifications. Competitors in the military tent business include Base-X, DHS Systems, Alaska Structures, Camel, Outdoor Venture, and Diamond Brand.

Watercraft: The Company primarily competes in the kayak and canoe product categories of the paddlesports market. The Company’s main competitors in this market are Confluence Watersports, Pelican, Wenonah Canoe and Legacy Paddlesports, each of which primarily competes on the basis of their design, performance, quality and price.

Diving: The main competitors in Diving include Aqualung/U.S. Divers, Oceanic, Mares, Cressi-sub, and Suunto. Competitive advantage in the life support product category of this segment, which consists of regulators, dive computers, and buoyancy compensators, is a function of product innovation, performance, quality and safety. Competition in the general diving product category of fins, masks, snorkels and wetsuits is characterized by low barriers to entry and numerous competitors who compete on the basis of product innovation, performance, quality and price.

Employees

At October 1, 2010, the Company had approximately 1,255 regular, full-time employees. The Company considers its employee relations to be excellent. Temporary employees are utilized primarily to manage peaks in the seasonal manufacturing of products.

Patents, Trademarks and Proprietary Rights

The Company owns various patents covering the Humminbird Side Imaging™ sonar technology used in its fishfinder products. Side Imaging sonar technology is used across a broad range of the Company’s Humminbird product portfolio and has been a key driver behind the brand’s growth over the past four years. The Company also holds various patents for diving products and electric motors, amongst other products, and regularly files applications for patents.

The Company has numerous trademarks and trade names which it considers important to its business, many of which are noted in this report. Historically, the Company has vigorously defended its intellectual property rights and the Company expects to continue to do so.

Supply Chain and Sourcing of Materials

The Company manufactures some products that use materials that, due to geographical distance, limited supplier capacity or competing demands for such materials, are only available in a cost effective manner from a single vendor or require the Company to place orders several months in advance of required delivery. The Company has experienced component shortages in its Marine Electronics and Diving businesses as component suppliers have been slow to increase their productive capacity after reducing it during the recent global recession.

4

The Company mitigates such product availability and supply chain risks through purchase of safety stocks, forecast-based supply contracts, and to a lesser extent with just in time inventory deliveries or supplier-owned inventory located close to the Company’s manufacturing locations. The Company strives to balance the imperative of holding adequate inventory with the cost of holding such inventory by manufacturing to forecast for high volume products, utilizing build-to-order strategies wherever possible, and by having contract manufactured products delivered to customers directly from suppliers.

As military contracts require utilization of domestic suppliers, the Company is limited to key vendors for materials used in its military tent business. Interruption or loss in the availability of these materials could have a material adverse impact on the sales and operating results of the Company’s Outdoor Equipment business.

Most of the Company’s products are made using materials that are generally in adequate supply and are available from a variety of third party suppliers.

Seasonality

The Company’s products are outdoor recreation-related, which results in seasonal variations in sales and profitability. This seasonal variability is due to customers’ increasing their inventories in the quarters ending March and June, the primary selling season for the Company’s outdoor recreation products, with lower inventory volumes during the quarters ending September and December. The Company mitigates the seasonality of its businesses somewhat by encouraging customers to purchase and take delivery of products more evenly through the year. The following table shows, for the past two fiscal years, the total net sales and operating profit or loss of the Company for each quarter, as a percentage of the total year.

|

Year Ended

|

|||||||||||||||||

| 2010 | 2009 | ||||||||||||||||

|

Quarter Ended

|

Net

Sales

|

Operating

Profit

|

Net

Sales

|

Operating

Profit

|

|||||||||||||

|

December

|

18 | % | -24 | % | 20 | % | -1918 | % | |||||||||

|

March

|

30 | % | 55 | % | 30 | % | 2127 | % | |||||||||

|

June

|

32 | % | 92 | % | 32 | % | 3888 | % | |||||||||

|

September

|

20 | % | -23 | % | 18 | % | -3997 | % | |||||||||

| 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||

Environment and Climate Change

The Company is subject to various supra national, federal, state and local environmental laws, ordinances, regulations, and other requirements of governmental authorities. We believe we comply with such laws and regulations. Expenditures on environmental compliance have not, and we believe in the future, will not have, a material effect on the Company’s capital expenditures, earnings or competitive position. We do not believe that any direct or indirect consequences of legislation related to climate change will have a material effect on our operating costs, facilities or products.

Available Information

The Company maintains a website at www.johnsonoutdoors.com. On its website, the Company makes available, free of charge, its Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as soon as reasonably practical after the reports have been electronically filed or furnished to the Securities and Exchange Commission. In addition, the Company makes available on its website, free of charge, its (a) Code of Business Conduct; (b) Code of Ethics for its Chief Executive Officer and Senior Financial and Accounting Officers; and (c) the charters for the following committees of the Board of Directors: Audit; Compensation; Executive; and Nominating and Corporate Governance. The Company is not including the information contained on or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K. This report includes all material information about the Company that is included on the Company’s website and is otherwise required to be included in this report. Copies of any materials the Company files with the SEC can also be obtained free of charge through the SEC’s website at www.sec.gov. The SEC’s Public Reference Room can be contacted at 100 F Street, N.E., Washington, D.C. 20549, or by calling 1 (800) 732-0330.

5

ITEM 1A. RISK FACTORS

The risks described below are not the only risks we face. Additional risks that we do not yet know of or that we currently think are immaterial may also impair our future business operations. If any of the events or circumstances described in the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. In such cases, the trading price of our common stock could decline.

Our net sales and profitability depend on our ability to continue to conceive, design and market products that appeal to our consumers.

Our business depends on our ability to continue to conceive, design, manufacture and market new products and upon continued market acceptance of our product offering. Rapidly changing consumer preferences and trends make it difficult to predict how long consumer demand for our existing products will continue or what new products will be successful. A decline in consumer demand for our products, our failure to develop new products on a timely basis in anticipation of changing consumer preferences or the failure of our new products to achieve and sustain consumer acceptance could reduce our net sales and profitability.

Competition in our markets could reduce our net sales and profitability.

We operate in highly competitive markets. We compete with several large domestic and foreign companies such as Brunswick, Lowrance, Confluence and Aqualung/U.S. Divers, with private label products sold by many of our retail customers and with other producers of outdoor recreation products. Some of our competitors have longer operating histories, stronger brand recognition and greater financial, technical, marketing and other resources than us. In addition, we may face competition from new participants in our markets because the outdoor recreation product industries have limited barriers to entry. We experience price competition for our products, and competition for shelf space at retailers, all of which may increase in the future. If we cannot compete in our product markets successfully in the future, our net sales and profitability will likely decline.

General economic conditions affect the Company’s results.

Our revenues are affected by economic conditions and consumer confidence worldwide, but especially in the United States and Europe. In times of economic uncertainty, consumers tend to defer expenditures for discretionary items, which affects demand for our products. Moreover, our businesses are cyclical in nature, and their success is impacted by economic conditions, the overall level of consumer confidence in the economy and discretionary income levels. Any substantial deterioration in general economic conditions that diminish consumer confidence or discretionary income can reduce our sales and adversely affect our financial results. Moreover, declining economic conditions create the potential for future impairments of goodwill and other intangible assets that may negatively impact our financial condition and results of operations. The impact of weak consumer credit markets; corporate restructurings; layoffs; declines in the value of investments and residential real estate; higher fuel prices and increases in federal and state taxation all can negatively affect our operating results.

Intellectual property disputes relating to our products could increase our costs.

Our industry is susceptible to litigation regarding patent infringement and infringement of other intellectual property rights. We could be either a plaintiff or a defendant in trademark and patent infringement claims and claims of breach of license from time to time. For example, the Company filed a patent infringement lawsuit in January of this year against a competitor for infringement of the Company’s Side Imaging™ sonar technology patents. That lawsuit and the prosecution or defense of any intellectual property litigation is both costly and disruptive of the time and resources of our management, even if the claim or defense against us is without merit. We could also be required to pay substantial damages or settlement costs to resolve intellectual property litigation.

6

Furthermore, we may rely on trade secret law to protect technologies and proprietary information that we cannot or have chosen not to patent. Trade secrets, however, are difficult to protect. Although we attempt to maintain protection through confidentiality agreements with necessary personnel, contractors and consultants, we cannot guarantee that such contracts will not be breached. Further, confidentiality agreements may conflict with other agreements which personnel, contractors and consultants have signed with prior employers or clients. In the event of a breach of a confidentiality agreement or the divulgence of proprietary information, we may not have adequate legal remedies to maintain our trade secret protection. Litigation to determine the scope of intellectual property rights, even if ultimately successful, could be costly and could divert management’s attention away from the Company’s business.

Impairment charges could impact our future financial position and results of operations.

We test our goodwill and other intangible assets with indefinite useful lives for impairment on an annual basis during the fourth quarter of our fiscal year or on an interim basis if an event occurs that might reduce the fair value of the reporting unit below its carrying value. Various uncertainties, including significant adverse changes in business climate, adverse actions by regulators, unanticipated competition, loss of key customers or changes in consumer preferences could impact the expected cash flows to be generated by an intangible asset or group of intangible assets, and may result in an impairment of those assets. Although any such impairment charge would be a non-cash expense, any impairment of our intangible assets could materially increase our expenses and reduce our profitability.

Sales of our products are seasonal, which causes our operating results to vary from quarter to quarter.

Sales of our products are seasonal. Historically, our net sales and profitability have peaked in the second and third fiscal quarters due to the buying patterns of our customers for our products. Seasonal variations in operating results may also cause us to increase our debt levels and interest expense primarily in the second and third fiscal quarters.

The trading price of shares of our common stock fluctuates and investors in our common stock may experience substantial losses.

The trading price of our common stock has been volatile and may continue to be volatile in the future. The trading price of our common stock could decline or fluctuate in response to a variety of factors, including:

| ● | the timing of our announcements or those of our competitors concerning significant product developments, acquisitions or financial performance; | |

| ● | fluctuation in our quarterly operating results; | |

| ● | substantial sales of our common stock; | |

| ● | general stock market conditions; or | |

| ● | other economic or external factors. |

You may be unable to sell your stock at or above your purchase price.

A limited number of our shareholders can exert significant influence over the Company.

As of November 30, 2010, Helen P. Johnson-Leipold, members of her family and related entities (hereinafter the Johnson Family), held approximately 78% of the voting power of both classes of our common stock taken as a whole. This voting power would permit these shareholders, if they chose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions. Moreover, certain members of the Johnson Family have entered into a voting trust agreement covering approximately 96% of our outstanding class B common shares. This voting trust agreement permits these shareholders, if they continue to choose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions.

7

We may experience difficulties in integrating strategic acquisitions.

We have, as part of our strategy, historically pursued acquisitions. The pursuit of future growth through acquisitions, including participation in joint ventures, involves significant risks that could have a material adverse effect on our business. Risks associated with integrating strategic acquisitions include:

| ● | the acquired business may experience losses which could adversely affect our profitability; | |

| ● | unanticipated costs relating to the integration of acquired businesses may increase our expenses; | |

| ● | possible failure to obtain any necessary consents to the transfer of licenses or other agreements of the acquired company; | |

| ● | possible failure to maintain customer, licensor and other relationships after the closing of the transaction of the acquired company; | |

| ● | difficulties in achieving planned cost savings and synergies may increase our expenses; | |

| ● | diversion of our management’s attention could impair their ability to effectively manage our other business operations; and | |

| ● | unanticipated management or operational problems or liabilities may adversely affect our profitability and financial condition. |

We are dependent upon certain key members of management.

Our success will depend to a significant degree on the abilities and efforts of our senior management. Moreover, our success depends on our ability to attract, retain and motivate qualified management, marketing, technical and sales personnel. These people are in high demand and often have competing employment opportunities. The labor market for skilled employees is highly competitive and we may lose key employees or be forced to increase their compensation to retain these people. Employee turnover could significantly increase our training and other related employee costs. The loss of key personnel, or the failure to attract qualified personnel, could have a material adverse effect on our business, financial condition or results of operations.

Sources of and fluctuations in market prices of raw materials can affect our operating results.

The primary raw materials we use in manufacturing our products are metals, resins and packaging materials. These materials are generally available from a number of suppliers, but we have chosen to concentrate our sourcing with a limited number of vendors for each commodity or purchased component. We believe our sources of raw materials are reliable and adequate for our needs. However, the development of future sourcing issues related to the availability of these materials as well as significant fluctuations in the market prices of these materials may have an adverse effect on our financial results.

Our profitability is also affected by significant fluctuations in the prices of the raw materials we use in our products. We may not be able to pass along any price increases in our raw materials to our customers. As a result, an increase in the cost of raw materials, labor or other costs associated with the manufacturing of our products could increase our costs of sales and reduce our gross margins.

Currency exchange rate fluctuations could adversely affect the Company’s results.

We have significant foreign operations, for which the functional currencies are denominated primarily in euros, Swiss francs, Japanese yen and Canadian dollars. As the values of the currencies of the foreign countries in which we have operations increase or decrease relative to the U.S. dollar, the sales, expenses, profits, losses, assets and liabilities of our foreign operations, as reported in our consolidated financial statements, increase or decrease, accordingly. Approximately 27% of our revenues for the year ended October 1, 2010 were denominated in currencies other than the U.S. dollar. Approximately 15% were denominated in euros, with the remaining 12% denominated in various other foreign currencies. We may mitigate a portion of the fluctuations in certain foreign currencies through the purchase of foreign currency swaps, forward contracts and options to hedge known commitments, primarily for purchases of inventory and other assets denominated in foreign currencies or to reduce the risk of changes in foreign currency exchange rates on foreign currency borrowings.

8

Because we rely on foreign suppliers and we sell products in foreign markets, we are susceptible to numerous international business risks that could increase our costs or disrupt the supply of our products.

Our international operations subject us to risks, including:

| ● | economic and political instability; | |

| ● | restrictive actions by foreign governments; | |

| ● | greater difficulty enforcing intellectual property rights and weaker laws protecting intellectual property rights; | |

| ● | changes in import duties or import or export restrictions; | |

| ● | timely shipping of product and unloading of product, including the timely rail/truck delivery to our warehouses and/or a customer’s warehouse of our products; | |

| ● | complications in complying with the laws and policies of the United States affecting the importation of goods, including duties, quotas and taxes; and | |

| ● | complications in complying with trade and foreign tax laws. |

Any of these risks, including the cost of compliance with trade and foreign tax laws, could disrupt the supply of our products or increase our expenses.

We are subject to environmental and safety regulations.

We are subject to supra national, federal, state, local and foreign laws and other legal requirements related to the generation, storage, transport, treatment and disposal of materials as a result of our manufacturing and assembly operations. These laws include the Resource Conservation and Recovery Act (as amended), the Clean Air Act (as amended) and the Comprehensive Environmental Response, Compensation and Liability Act (as amended). We believe that our existing environmental management system is adequate and we have no current plans for substantial capital expenditures in the environmental area. We do not currently anticipate any material adverse impact on our results of operations, financial condition or competitive position as a result of compliance with federal, state, local and foreign environmental laws or other legal requirements. However, risk of environmental liability and changes associated with maintaining compliance with environmental laws is inherent in the nature of our business and there is no assurance that material liabilities or changes would not arise.

We rely on our credit facilities to provide us with sufficient working capital to operate our business.

Historically, we have relied upon our existing credit facilities to provide us with adequate working capital to operate our business. The availability of borrowing amounts under our revolving credit facilities is generally dependent upon the amount and quality of the accounts receivable and inventory collateralizing our credit facilities. As a result, the bankruptcy of a major customer could have a significant negative impact on the availability of borrowing amounts under our revolving credit facilities. If our lenders reduce or terminate our access to amounts under our credit facilities, we may not have sufficient capital to fund our working capital needs and/or we may need to secure additional capital or financing to fund our working capital requirements or to repay outstanding debt under our credit facilities. We can make no assurance that we will be successful in ensuring our availability of amounts under our credit facilities or in connection with raising additional capital and that any amount, if raised, will be sufficient to meet our cash requirements. If we are not able to maintain our borrowing availability under our credit facilities and/or raise additional capital when needed, we may be forced to sharply curtail our efforts to manufacture and promote the sale of our products or to curtail our operations. Ultimately, we may be forced to cease operations.

9

Our debt covenants may limit our ability to complete acquisitions, incur debt, make investments, sell assets, merge or complete other significant transactions.

Our credit facilities and certain other of our debt instruments include limitations on a number of our activities, including our ability to:

| ● | incur additional debt; | |

| ● | create liens on our assets or make guarantees; | |

| ● | make certain investments or loans; | |

| ● | pay dividends; or | |

| ● | dispose of or sell assets or enter into a merger or similar transaction. |

Our credit facilities also contain a number of financial covenants. The restrictive covenants in our credit facilities may limit our ability to engage in acts that may be in our best long term interests. A breach of any of the restrictive covenants in our credit facilities could result in a default under these facilities. If a default occurs, the lenders under our credit facilities may elect to declare all outstanding borrowings, together with accrued interest, to be immediately due and payable, to terminate any commitments they have to provide further borrowings and to exercise any other rights they have under the facilities or applicable law.

Because our common stock is thinly traded, its market price may fluctuate significantly more than the stock market in general or the stock prices of similar companies, which are exchanged, listed or quoted on NASDAQ. We believe there are 4,585,841 shares of our Class A common stock held by nonaffiliates as of November 30, 2010. Thus, our common stock will be less liquid than the stock of companies with broader public ownership, and as a result, the trading price for our shares of common stock may be more volatile. Among other things, trading of a relatively small volume of our common stock may have a greater impact on the trading price for our stock than would be the case if our public float were larger.

ITEM 2. PROPERTIES

The Company maintains both leased and owned manufacturing, warehousing, distribution and office facilities throughout the world. The Company believes that its facilities are well maintained and have capacity adequate to meet its current needs.

See Note 7 to the consolidated financial statements included elsewhere in this report for a discussion of the Company’s lease obligations.

As of October 1, 2010, the Company’s principal manufacturing (identified with an asterisk) and other locations are:

Alpharetta, Georgia (Marine Electronics)

Antibes, France (Diving)

Barcelona, Spain (Diving)

Basingstoke, Hampshire, England (Diving)

Batam, Indonesia* (Diving and Outdoor Equipment)

Bellingham, Washington (Watercraft)

Binghamton, New York* (Outdoor Equipment)

Brignais, France (Watercraft)

Brussels, Belgium (Diving)

Burlington, Ontario, Canada (Marine Electronics, Outdoor Equipment, Watercraft)

Chai Wan, Hong Kong (Diving)

Chatswood, Australia (Diving)

El Cajon, California (Diving)

Eufaula, Alabama* (Marine Electronics)

Casarza Ligure, Italy* (Diving)

Great Yarmouth, Norfolk, United Kingdom (Watercraft)

Spreitenbach, Switzerland (Diving)

Mankato, Minnesota* (Marine Electronics)

Napier, New Zealand* (Watercraft)

Old Town, Maine* (Watercraft)

Shanghai, China (Marine Electronics)

Silverdale, New Zealand* (Watercraft)

Viareggio, Italy (Marine Electronics)

Wendelstein, Germany (Diving)

Yokahama, Japan (Diving)

10

The Company’s corporate headquarters is located in a leased facility in Racine, Wisconsin.

ITEM 3. LEGAL PROCEEDINGS

See Note 15 to the consolidated financial statements included elsewhere in this report for a discussion of legal proceedings.

ITEM 4. [REMOVED AND RESERVED]

11

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF

EQUITY SECURITIES

Certain information with respect to this item is included in Notes 11 and 12 to the Company's consolidated financial statements included elsewhere in this report. The Company’s Class A common stock is traded on the NASDAQ Global MarketSM under the symbol: JOUT. There is no public market for the Company’s Class B common stock. However, the Class B common stock is convertible at all times at the option of the holder into shares of Class A common stock on a share for share basis. As of November 30, 2010, the Company had 723 holders of record of its Class A common stock and 35 holders of record of its Class B common stock. We believe the number of beneficial owners of our Class A common stock on that date was substantially greater.

A summary of the high and low closing prices for the Company’s Class A common stock during each quarter of the years ended October 1, 2010 and October 2, 2009 is as follows:

|

First Quarter

|

Second Quarter

|

Third Quarter

|

Fourth Quarter

|

|||||||||||||||||||||||||||||

|

2010

|

2009

|

2010

|

2009

|

2010

|

2009

|

2010

|

2009

|

|||||||||||||||||||||||||

|

Stock prices:

|

||||||||||||||||||||||||||||||||

|

High

|

$ | 10.75 | $ | 11.93 | $ | 11.52 | $ | 7.59 | $ | 14.67 | $ | 7.80 | $ | 13.21 | $ | 9.89 | ||||||||||||||||

|

Low

|

8.65 | 5.10 | 10.25 | 4.68 | 11.00 | 5.00 | 8.96 | 5.30 | ||||||||||||||||||||||||

The Company did not declare any dividends during the fiscal years ended October 1, 2010 or October 2, 2009. The Company declared a cash dividend on October 1, 2008, with a record date of October 16, 2008, which was paid on October 30, 2008 of $0.055 per share to Class A common shareholders and $0.05 per share to Class B shareholders. On December 4, 2008, the Company’s Board of Directors voted to suspend quarterly dividends to shareholders.

The following limitations apply to the ability of the Company to pay dividends:

| ● | Pursuant to the Company’s revolving credit and security agreement, dated September 29, 2009, the Company is limited in the amount of restricted payments (primarily dividends and repurchases of common stock) made during each fiscal year. The Company may declare, and pay, dividends in accordance with historical practices, but in no event may the aggregate amount of all dividends for any fiscal year exceed 25% of the Company’s net income for that fiscal year. | |

| ● | The Company’s Articles of Incorporation provide that no dividend, other than a dividend payable in shares of the Company’s common stock, may be declared or paid upon the Class B common stock unless such dividend is declared or paid upon both classes of common stock. Whenever a dividend (other than a dividend payable in shares of Company common stock) is declared or paid upon any shares of Class B common stock, at the same time there must be declared and paid a dividend on shares of Class A common stock equal in value to 110% of the amount per share of the dividend declared and paid on shares of Class B common stock. Whenever a dividend is payable in shares of Company common stock, such dividend must be declared or paid at the same rate on the Class A common stock and the Class B common stock. |

12

Total Shareholder Return

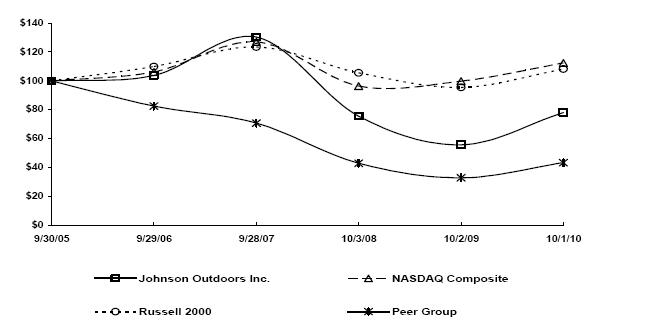

The graph below compares on a cumulative basis the yearly percentage change since September 30, 2005 in the total return (assuming reinvestment of dividends) to shareholders on the Class A common stock with (a) the total return (assuming reinvestment of dividends) on The NASDAQ Stock Market-U.S. Index; (b) the total return (assuming reinvestment of dividends) on the Russell 2000 Index; and (c) the total return (assuming reinvestment of dividends) on a self-constructed peer group index. The peer group consists of Arctic Cat Inc., Brunswick Corporation, Callaway Golf Company, Escalade Inc., Marine Products Corporation and Nautilus, Inc. The graph assumes $100 was invested on September 30, 2005 in the Company’s Class A common stock, The NASDAQ Stock Market-U.S. Index, the Russell 2000 Index and the peer group indices.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Johnson Outdoors Inc., the NASDAQ Composite Index,

the Russell 2000 Index and a Peer Group

* $100 invested on 9/30/05 in stock or index, including reinvestment of dividends.

Indexes calculated on month-end basis.

|

9/30/2005

|

9/29/2006

|

9/28/2007

|

10/3/2008

|

10/2/2009

|

10/1/2010

|

|||||||||||||||||||

|

Johnson Outdoors Inc.

|

$ | 100.0 | $ | 103.8 | $ | 130.3 | $ | 75.5 | $ | 55.7 | $ | 78.1 | ||||||||||||

|

NASDAQ Composite

|

100.0 | 106.2 | 127.0 | 96.4 | 99.8 | 112.5 | ||||||||||||||||||

|

Russell 2000 Index

|

100.0 | 109.9 | 123.5 | 105.7 | 95.5 | 108.3 | ||||||||||||||||||

|

Peer Group

|

100.0 | 82.6 | 70.8 | 42.9 | 32.8 | 43.3 | ||||||||||||||||||

The information in this section titled “Total Shareholder Return” shall not be deemed to be “soliciting material” or “filed” with the Securities and Exchange Commission or subject to Regulation 14A or 14C promulgated by the Securities and Exchange Commission or subject to the liabilities of section 18 of the Securities Exchange Act of 1934, as amended, and this information shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

13

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Executive Overview

The Company designs, manufactures and markets high quality recreational products for the outdoor enthusiast. Through a combination of innovative products, strong marketing, a talented and passionate workforce and efficient distribution, the Company sets itself apart from the competition. Its subsidiaries operate as a network that promotes innovation and leverages best practices and synergies, following the strategic vision set by executive management and approved by the Company’s Board of Directors.

During fiscal 2010, the Company made significant progress towards its three year plan to achieve sustained profitable growth by focusing on cost structure reductions, enhanced product value, targeted revenue gains and strong balance sheet management. The Company continued its investment in future products, such as Marine Electronics’ Geonav® brand. Since 2009, the Company has invested approximately $3.3 million in equipment and software development to expand its large leisure boat navigation systems product offerings.

As outdoor recreation markets and global economic conditions overall have begun to stabilize from the recent global recession, the Company’s revenues during fiscal 2010 improved by over 7% from the prior year. Moreover, improved fixed cost absorption from increased sales, improved operational efficiency and aggressive working capital management efforts have driven a substantial increase in profits.

Results of Operations

Summary consolidated financial results from continuing operations for the fiscal years presented were as follows:

|

(millions, except per share data)

|

2010

|

2009

|

||||||

|

Net sales

|

$ | 382.4 | $ | 356.5 | ||||

|

Gross profit

|

153.5 | 132.8 | ||||||

|

Operating expenses

|

138.9 | 132.5 | ||||||

|

Operating profit

|

14.6 | 0.3 | ||||||

|

Interest expense

|

5.1 | 9.9 | ||||||

|

Net income (loss)

|

6.5 | (9.7 | ) | |||||

14

The Company’s sales and operating profit (loss) by business segment are summarized as follows:

|

(millions)

|

2010

|

2009

|

||||||

|

Net sales:

|

||||||||

|

Marine Electronics

|

$ | 185.4 | $ | 165.3 | ||||

|

Outdoor Equipment

|

48.7 | 41.4 | ||||||

|

Watercraft

|

64.0 | 69.4 | ||||||

|

Diving

|

85.1 | 80.8 | ||||||

|

Other/corporate/eliminations

|

(0.8 | ) | (0.4 | ) | ||||

| $ | 382.4 | $ | 356.5 | |||||

|

Operating profit (loss):

|

||||||||

|

Marine Electronics

|

$ | 13.9 | $ | 9.3 | ||||

|

Outdoor Equipment

|

5.9 | 3.4 | ||||||

|

Watercraft

|

1.8 | (6.2 | ) | |||||

|

Diving

|

3.0 | 1.6 | ||||||

|

Other/corporate/eliminations

|

(10.0 | ) | (7.8 | ) | ||||

| $ | 14.6 | $ | 0.3 | |||||

See Note 14 in the notes to the consolidated financial statements included elsewhere in this report for the definition of segment net sales and operating profit.

Fiscal 2010 vs Fiscal 2009

Net Sales

The initial recovery of outdoor recreational markets from the recent global recession helped drive net sales up to $382.4 million in 2010 compared to $356.5 million in 2009, an increase of 7.3% or $25.9 million. Sales increased in all of the Company’s business units with the exception of Watercraft. Foreign currency translations favorably impacted 2010 net sales by $3.1 million in comparison to 2009.

Net sales for the Marine Electronics business increased $20.1 million, or 12.2% during 2010 on double-digit growth in Minn Kota and Humminbird brands in all channels and markets. The increase was primarily the result of successful new products and improved general economic conditions.

Outdoor Equipment net sales increased $7.3 million in 2010, or 17.6%, primarily due to double-digit growth in the Eureka brand across consumer and military markets.

Net sales for the Watercraft business decreased $5.4 million, or 7.8%, due to declines in sales in the specialty channel in the U.S. and Europe.

The Diving business saw an increase in sales of $4.3 million, or 5.3%, due in large part to the new SUBGEAR brand and increased SCUBAPRO demand. Currency translation favorably impacted 2010 Diving net sales by $0.8 million, or 1.0%.

Gross Profit

Gross profit of $153.5 million was 40.1% of net sales on a consolidated basis for the year ended October 1, 2010 compared to $132.8 million or 37.2% of net sales in the prior year. The gross profit increase of $20.7 million was primarily attributable to the 7.3% increase in sales volume during 2010 as compared to 2009. During the prior year, manufacturing plants were operated at reduced capacity at certain points during the year in light of low sales volumes and in order to reduce inventories. This resulted in higher unabsorbed costs in our manufacturing plants which were expensed during the prior year. Increased volumes in the current year increased efficiency and improved the margins in all business units.

15

Gross profit in the Marine Electronics business increased $11.9 million from the prior year primarily due to an increase in volume and improved as a percent of net sales from 35.5% in 2009 to 38.1% in the current year.

Gross profit in the Outdoor Equipment business increased $4.1 million from 2009, and improved as a percent of net sales from 33.6% in the prior year to 37.0% in 2010.

Despite a decrease in sales, gross profit in the Watercraft segment was 35.1% of net sales in 2010 and was $1.3 million higher than 2009 levels, which were equal to 30.5% of net sales. The increase in gross profit was due primarily to savings from restructuring actions taken at the end of the prior year, as well as the non-recurring costs related to those actions and inventory reserves taken at the end of the prior year.

Gross profit for the Diving segment increased by $3.4 million from 48.2% of net sales in 2009 to 49.7% of net sales in 2010 primarily as a result of increased volumes.

Operating Expenses

Operating expenses increased from the prior year by $6.5 million. The increase was mainly attributable to higher sales related expenses and bonus and profit sharing accruals taken in the current year.

Operating expenses for the Marine Electronics segment increased by $7.3 million from 2009 levels. This increase was due mainly to the increase in direct expenses as result of higher sales volumes and bonus and profit sharing accruals taken in the current year.

Outdoor Equipment operating expenses increased by $1.6 million from 2009 due to primarily to increases in direct expenses as a result of higher sales volumes and bonus and profit sharing accruals in the current year.

The Watercraft business saw a decline in operating expenses of $6.6 million from the prior year due primarily to cost savings achieved as a result of the closure of the Ferndale manufacturing location in the prior year. In addition, prior year expenses included the recognition of $2.6 million of restructuring costs related to this closure and $1.3 million of accelerated depreciation related to consolidating production facilities in Old Town.

Operating expenses for the Diving business increased by $2.0 million due primarily to bonus and profit sharing expense recognized in the current year as well as the $0.7 million unfavorable impact of currency translation.

Operating Results

The Company recognized an operating profit of $14.6 million in 2010 compared to an operating profit of $0.3 million in fiscal 2009. Primary factors driving the increase in operating profit margins were the higher volumes in the current year offset in part by bonus and profit sharing expenses recognized in the current year. Marine Electronics operating profit increased by $4.6 million from the prior year. Outdoor Equipment operating profit increased $2.5 million over the prior year. Watercraft operating profit improved by $8.0 million from the prior year and Diving operating profit increased $1.4 million from the prior year.

Other Income and Expenses

Interest income decreased from the prior year by $0.1 million. Interest expense decreased from the prior year by $4.9 million, due largely to lower principal balances, interest rate decreases during 2010 and charges associated with terminating the Company’s former debt agreements incurred during 2009.

Other expense reflected currency losses of $1.2 million recognized by the Company in fiscal 2010 compared to $0.8 million in fiscal 2009. Currency losses were offset in part by market gains on deferred compensation plan assets of $0.7 million in 2010 compared to $0.1 million in the prior year.

16

Pretax Income (Loss) and Income Taxes

The Company recognized pretax income of $9.2 million in fiscal 2010, compared to a pretax loss of $10.1 million in fiscal 2009. The Company recorded income tax expense of $2.7 million in 2010, an effective rate of 28.9%, compared to $0.4 million of income tax benefit in fiscal 2009, an effective rate of 4.0%.

Net Income/Loss

The Company recognized net income of $6.5 million in fiscal 2010, or $0.68 per diluted share, compared to a net loss of $9.7 million in fiscal 2009, or $1.06 per diluted share.

Financial Condition, Liquidity and Capital Resources

The Company’s cash flows from operating, investing and financing activities, as reflected in the consolidated statements of cash flows, is summarized in the following table:

|

(millions)

|

2010

|

2009

|

||||||

|

Cash provided by (used for):

|

||||||||

|

Operating activities

|

$ | 19.8 | $ | 30.6 | ||||

|

Investing activities

|

(9.3 | ) | (15.9 | ) | ||||

|

Financing activities

|

(7.6 | ) | (32.7 | ) | ||||

|

Effect of exchange rate changes on cash and cash equivalents

|

2.5 | 4.1 | ||||||

|

Increase (decrease) in cash and cash equivalents

|

$ | 5.4 | (13.9 | ) | ||||

Operating Activities

The following table sets forth the Company’s working capital position at the end of each of the past two years:

|

(millions)

|

2010

|

2009

|

||||||

|

Current assets

|

$ | 160.1 | $ | 142.4 | ||||

|

Current liabilities

|

67.0 | 60.8 | ||||||

|

Working capital

|

$ | 93.1 | $ | 81.6 | ||||

|

Current ratio

|

2.4:1

|

2.3:1

|

||||||

Cash flows provided by operations totaled $19.8 million and $30.6 million in fiscal 2010 and 2009, respectively. The most significant driver in the decrease in cash flows from operations year over year was a $23.3 million decrease in inventory levels in the prior year, followed by a $12.6 million increase in inventory levels in 2010. This change was offset in part by an increase in 2010 net earnings as well as an increase in accounts payable and accrued liabilities of $13.1 million vs. a decrease of $10.4 million in the prior year.

Depreciation and amortization charges were $10.0 million in fiscal 2010 and $12.9 million in fiscal 2009, which included the write off of $1.0 million of deferred financing costs related to the Company’s previous debt agreement.

Investing Activities

Cash flows used for investing activities were $9.3 million and $15.9 million in fiscal 2010 and 2009, respectively. Payments on interest rate swaps used $6.7 million of cash and the purchase of Navicontrol used $1.0 million of cash in fiscal 2009. Expenditures for property, plant and equipment were $10.0 and $8.3 million in fiscal 2010 and 2009, respectively. In general, the Company’s ongoing capital expenditures are primarily related to tooling for new products and facilities and information systems improvements.

17

Financing Activities

The following table sets forth the Company’s debt and capital structure at the end of the past two fiscal years:

|

(millions)

|

2010

|

2009

|

||||||

|

Current debt

|

$ | 8.9 | $ | 15.5 | ||||

|

Long-term debt

|

14.9 | 16.1 | ||||||

|

Total debt

|

23.8 | 31.6 | ||||||

|

Shareholders’ equity

|

126.4 | 115.8 | ||||||

|

Total capitalization

|

$ | 150.2 | $ | 147.4 | ||||

|

Total debt to total capitalization

|

15.8 | % | 21.4 | % | ||||

Cash flows used for financing activities totaled $7.6 million in fiscal 2010 compared to $32.7 million in 2009. Payments on long-term debt were $0.6 million and $60.0 million in fiscal 2010 and 2009, respectively.

On September 29, 2009, the Company and certain of its subsidiaries entered into new credit facilities which consisted of five separate Term Loan Agreements, each dated as of September 29, 2009 (the "Term Loan Agreements" or "Term Loans"), between the Company or one of its subsidiaries and Ridgestone Bank ("Ridgestone"). The Company also entered into a Revolving Credit and Security Agreement dated as of September 29, 2009 among the Company, certain of the its subsidiaries, PNC Bank, National Association, as lender, as administrative agent and collateral agent, and the other lenders named therein (the "Revolving Credit Agreement" or "Revolver" and collectively, with the Term Loans, the "Debt Agreements").

The Term Loan Agreements provide for aggregate term loan borrowings of $15.9 million with maturity dates ranging from 15 to 25 years from the date of the Term Loan Agreement. Each Term Loan requires monthly payments of principal and interest. Interest on $9.0 million of the aggregate outstanding amount of the Term Loans is based on the prime rate plus 2.0%, and the remainder on the prime rate plus 2.75%. The Term Loans are guaranteed in part under the United States Department of Agriculture Rural Development program and are secured by certain real and tangible properties of the Company’s subsidiaries.

The Revolving Credit Agreement, maturing in September 2012, provides for funding of up to $69.0 million.

On November 5, 2009, the Company closed on its Canadian asset backed credit facility (“Canadian Revolver” and collectively, with the Revolving Credit Agreement, the “Revolvers”), increasing its total seasonal debt availability by $4.0 million for the period July 15th through November 15th, and by $6.0 million for the period November 16th through July 14th.

The Revolvers are secured with a first priority lien on working capital assets and certain patents and trademarks of the Company and its subsidiaries and a second lien on land, buildings, machinery and equipment of the Company's domestic subsidiaries. As cash collections related to secured assets are applied against the balance outstanding under the Revolvers, the liability is classified as current. The interest rate on the Revolvers is based primarily on LIBOR plus 3.25% with a minimum LIBOR floor of 2.0%.

As noted above borrowing availability under the Revolvers is based on certain eligible working capital assets, primarily accounts receivable and inventory of the Company and its subsidiaries. The Revolvers contain a seasonal line reduction that reduces the maximum amount of borrowings to $50.0 million from mid-July to mid-November, consistent with the Company's reduced working capital needs throughout that period, and requires an annual seasonal pay down to $25.0 million for 60 consecutive days during the three month period beginning August 1st.

18

At October 1, 2010, the Company had borrowings outstanding under the Revolvers of $7.5 million. The Company’s remaining borrowing availability under the Revolvers was approximately $18.2 million at October 1, 2010.

The Company incurred $0.2 million of financing fees during the year ended October 1, 2010 in conjunction with the execution of its Canadian Revolver which were capitalized and will be amortized over the life of the related debt. During the year ended October 2, 2009, the Company incurred and capitalized approximately $1.5 million of financing fees in conjunction with the execution of the Debt Agreements and $1.3 million of financing fees in conjunction with the modification to the Company’s then-existing debt agreements.

See Note 16 to the consolidated financial statements found elsewhere in this report regarding certain amendments entered into by the Company and certain of its subsidiaries in connection with the Company’s Revolvers.

In response to the increasing volatility of foreign exchange rates, the Company initiated a foreign currency hedging program in the first quarter of fiscal 2011. The Company’s goal is to reduce the economic effects of fluctuating foreign exchange rates on the cost of U.S. dollar denominated purchases by its foreign subsidiaries. The program utilizes foreign currency forward contracts to hedge a notional amount of approximately $5.8 million of purchases over a term of less than one year. The Company may expand or reduce this program based on future economic and business conditions.

Off Balance Sheet Arrangements

The Company utilizes letters of credit primarily as security for the payment of future claims under its workers compensation insurance. Letters of credit outstanding at October 1, 2010 were $2.6 million compared to less than $0.1 million on October 2, 2009 as the Company had collateralized $2.2 million of its potential future workers compensation claims with cash at the end of fiscal 2009 in order to facilitate the closing of its debt agreements.

The Company anticipates making contributions to its defined benefit pension plans of $0.4 million through September 30, 2011.

The Company has no other off-balance sheet arrangements.

Impact of Inflation

Certain components used in the Company’s products are exposed to commodity price changes. The Company manages this risk through instruments such as purchase orders and non-cancelable supply contracts. Primary commodity price exposures include costs associated with metals, resins and packaging materials.

The Company anticipates that changing costs of basic raw materials may impact future operating costs and, accordingly, the prices of its products. The Company is involved in continuing programs to mitigate the impact of cost increases through changes in product design and identification of sourcing and manufacturing efficiencies. Price increases and, in certain situations, price decreases are implemented for individual products, when appropriate.

The Company’s results of operations and financial condition are presented based on historical cost. The Company does not believe that inflation has significantly affected its results of operations.

Critical Accounting Policies and Estimates

The Company’s management discussion and analysis of its financial condition and results of operations are based upon the Company’s consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the U.S. The preparation of these financial statements requires the Company to make estimates and judgments that affect the reported amounts of its assets, liabilities, sales and expenses, and related footnote disclosures. On an on going basis, the Company evaluates its estimates for product returns, bad debts, inventories, long lived assets and goodwill, income taxes, warranty obligations, pensions and other post-retirement benefits, and litigation. The Company bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

19

The Company believes the following critical accounting policies affect its more significant judgments and estimates used in the preparation of its consolidated financial statements. Management has discussed these policies with the Audit Committee of the Company’s Board of Directors.

Revenue Recognition

The Company recognizes revenue when all of the following criteria have been met:

| ● | Persuasive evidence of an arrangement exists. Contracts, internet commerce agreements, and customer purchase orders are generally used to determine the existence of an arrangement. | |

| ● | All substantial risk of ownership transfers to the customer. Shipping documents and customer acceptance, when applicable, are used to verify delivery. | |

| ● | The fee is fixed or determinable. This is assessed based on the payment terms associated with the transaction and whether the sales price is subject to refund or adjustment. | |

| ● | Collectibility is reasonably assured. We assess collectibility based on the creditworthiness of the customer as determined by credit checks and analysis, as well as by the customer’s payment history. |

Estimated costs of returns and allowances and discounts are accrued as a reduction to sales when revenue is recognized.

Allowance for Doubtful Accounts

Allowances for doubtful accounts are estimated by the individual operating companies based on estimates of losses related to customer accounts receivable balances. Estimates are developed by using standard quantitative measures based on historical losses, adjusting for current economic conditions and, in some cases, evaluating specific customer accounts for risk of loss. The establishment of reserves requires the use of judgment and assumptions regarding the potential for losses on receivable balances. Though the Company considers these balances adequate and proper, changes in economic conditions in specific markets in which the Company operates and any specific customer collection issues the Company identifies could have a favorable or unfavorable effect on required reserve balances.

Inventories