Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - COGNIZANT TECHNOLOGY SOLUTIONS CORP | ctshexhibit3229-30x2018.htm |

| EX-32.1 - EXHIBIT 32.1 - COGNIZANT TECHNOLOGY SOLUTIONS CORP | ctshexhibit3219-30x2018.htm |

| EX-31.2 - EXHIBIT 31.2 - COGNIZANT TECHNOLOGY SOLUTIONS CORP | ctshexhibit3129-30x2018.htm |

| EX-31.1 - EXHIBIT 31.1 - COGNIZANT TECHNOLOGY SOLUTIONS CORP | ctshexhibit3119-30x2018.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

ý | Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||

For the quarterly period ended September 30, 2018 | |||

¨ | Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||

For the transition period from to | |||

Commission File Number 0-24429

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 13-3728359 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

Glenpointe Centre West 500 Frank W. Burr Blvd. Teaneck, New Jersey | 07666 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (201) 801-0233

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No: ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No: ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ý | Accelerated filer | ¨ |

Non-accelerated filer | ¨ | Smaller reporting company | ¨ |

Emerging growth company | ¨ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

Indicate the number of shares outstanding of each of the issuer’s class of common stock, as of October 23, 2018:

Class | Number of Shares | |

Class A Common Stock, par value $.01 per share | 579,028,009 | |

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

TABLE OF CONTENTS

Page | ||

PART I. | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 6. | ||

PART I. FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements (Unaudited).

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

(Unaudited)

(in millions, except par values)

September 30, 2018 | December 31, 2017 | ||||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 1,339 | $ | 1,925 | |||

Short-term investments | 3,424 | 3,131 | |||||

Trade accounts receivable, net of allowances of $68 and $65, respectively | 3,187 | 2,865 | |||||

Unbilled accounts receivable | — | 357 | |||||

Other current assets | 777 | 833 | |||||

Total current assets | 8,727 | 9,111 | |||||

Property and equipment, net | 1,362 | 1,324 | |||||

Goodwill | 3,037 | 2,704 | |||||

Intangible assets, net | 1,021 | 981 | |||||

Deferred income tax assets, net | 391 | 418 | |||||

Long-term investments | 93 | 235 | |||||

Other noncurrent assets | 643 | 448 | |||||

Total assets | $ | 15,274 | $ | 15,221 | |||

Liabilities and Stockholders’ Equity | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 223 | $ | 210 | |||

Deferred revenue | 244 | 383 | |||||

Short-term debt | 100 | 175 | |||||

Accrued expenses and other current liabilities | 2,126 | 2,071 | |||||

Total current liabilities | 2,693 | 2,839 | |||||

Deferred revenue, noncurrent | 72 | 104 | |||||

Deferred income tax liabilities, net | 157 | 146 | |||||

Long-term debt | 624 | 698 | |||||

Long-term income taxes payable | 490 | 584 | |||||

Other noncurrent liabilities | 260 | 181 | |||||

Total liabilities | 4,296 | 4,552 | |||||

Commitments and contingencies (See Note 13) | |||||||

Stockholders’ equity: | |||||||

Preferred stock, $0.10 par value, 15.0 shares authorized, none issued | — | — | |||||

Class A common stock, $0.01 par value, 1,000 shares authorized, 580 and 588 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively | 6 | 6 | |||||

Additional paid-in capital | 119 | 49 | |||||

Retained earnings | 11,041 | 10,544 | |||||

Accumulated other comprehensive income (loss) | (188 | ) | 70 | ||||

Total stockholders’ equity | 10,978 | 10,669 | |||||

Total liabilities and stockholders’ equity | $ | 15,274 | $ | 15,221 | |||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

1

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(in millions, except per share data)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues | $ | 4,078 | $ | 3,766 | $ | 11,996 | $ | 10,982 | |||||||

Operating expenses: | |||||||||||||||

Cost of revenues (exclusive of depreciation and amortization expense shown separately below) | 2,480 | 2,337 | 7,298 | 6,792 | |||||||||||

Selling, general and administrative expenses | 734 | 674 | 2,250 | 2,069 | |||||||||||

Depreciation and amortization expense | 119 | 107 | 340 | 297 | |||||||||||

Income from operations | 745 | 648 | 2,108 | 1,824 | |||||||||||

Other income (expense), net: | |||||||||||||||

Interest income | 47 | 34 | 128 | 97 | |||||||||||

Interest expense | (6 | ) | (6 | ) | (19 | ) | (18 | ) | |||||||

Foreign currency exchange gains (losses), net | (122 | ) | (16 | ) | (233 | ) | 41 | ||||||||

Other, net | (2 | ) | (2 | ) | (2 | ) | (2 | ) | |||||||

Total other income (expense), net | (83 | ) | 10 | (126 | ) | 118 | |||||||||

Income before provision for income taxes | 662 | 658 | 1,982 | 1,942 | |||||||||||

Provision for income taxes | (185 | ) | (164 | ) | (530 | ) | (421 | ) | |||||||

Income from equity method investments | — | 1 | 1 | 1 | |||||||||||

Net income | $ | 477 | $ | 495 | $ | 1,453 | $ | 1,522 | |||||||

Basic earnings per share | $ | 0.82 | $ | 0.84 | $ | 2.49 | $ | 2.56 | |||||||

Diluted earnings per share | $ | 0.82 | $ | 0.84 | $ | 2.48 | $ | 2.55 | |||||||

Weighted average number of common shares outstanding - Basic | 579 | 590 | 584 | 594 | |||||||||||

Dilutive effect of shares issuable under stock-based compensation plans | 1 | 2 | 1 | 2 | |||||||||||

Weighted average number of common shares outstanding - Diluted | 580 | 592 | 585 | 596 | |||||||||||

Dividends declared per common share | $ | 0.20 | $ | 0.15 | $ | 0.60 | $ | 0.30 | |||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

2

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(in millions)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Net income | $ | 477 | $ | 495 | $ | 1,453 | $ | 1,522 | |||||||

Other comprehensive income (loss), net of tax: | |||||||||||||||

Foreign currency translation adjustments | (12 | ) | 33 | (46 | ) | 100 | |||||||||

Change in unrealized gains and losses on cash flow hedges | (82 | ) | (22 | ) | (205 | ) | 56 | ||||||||

Change in unrealized gains and losses on available-for-sale securities | — | — | (6 | ) | 2 | ||||||||||

Other comprehensive income (loss) | (94 | ) | 11 | (257 | ) | 158 | |||||||||

Comprehensive income | $ | 383 | $ | 506 | $ | 1,196 | $ | 1,680 | |||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

3

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(Unaudited)

(in millions)

Class A Common Stock | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Total | |||||||||||||||||||

Shares | Amount | ||||||||||||||||||||||

Balance, December 31, 2017 | 588 | $ | 6 | $ | 49 | $ | 10,544 | $ | 70 | $ | 10,669 | ||||||||||||

Cumulative effect of changes in accounting principle(1) | — | — | — | 122 | (1 | ) | 121 | ||||||||||||||||

Net income | — | — | — | 1,453 | — | 1,453 | |||||||||||||||||

Other comprehensive income (loss) | — | — | — | — | (257 | ) | (257 | ) | |||||||||||||||

Common stock issued, stock-based compensation plans | 5 | — | 142 | — | — | 142 | |||||||||||||||||

Stock-based compensation expense | — | — | 199 | — | — | 199 | |||||||||||||||||

Repurchases of common stock | (13 | ) | — | (271 | ) | (723 | ) | — | (994 | ) | |||||||||||||

Dividends | — | — | — | (355 | ) | — | (355 | ) | |||||||||||||||

Balance, September 30, 2018 | 580 | $ | 6 | $ | 119 | $ | 11,041 | $ | (188 | ) | $ | 10,978 | |||||||||||

Class A Common Stock | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Total | |||||||||||||||||||

Shares | Amount | ||||||||||||||||||||||

Balance, December 31, 2016 | 608 | $ | 6 | $ | 358 | $ | 10,478 | $ | (114 | ) | $ | 10,728 | |||||||||||

Net income | — | — | — | 1,522 | — | 1,522 | |||||||||||||||||

Other comprehensive income (loss) | — | — | — | — | 158 | 158 | |||||||||||||||||

Common stock issued, stock-based compensation plans | 6 | — | 146 | — | — | 146 | |||||||||||||||||

Stock-based compensation expense | — | — | 161 | — | — | 161 | |||||||||||||||||

Repurchases of common stock | (24 | ) | — | (457 | ) | (1,100 | ) | — | (1,557 | ) | |||||||||||||

Dividends | — | — | — | (179 | ) | — | (179 | ) | |||||||||||||||

Balance, September 30, 2017 | 590 | $ | 6 | $ | 208 | $ | 10,721 | $ | 44 | $ | 10,979 | ||||||||||||

(1) | Reflects the adoption of accounting standards as described in Note 1. |

The accompanying notes are an integral part of the unaudited consolidated financial statements.

4

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(in millions)

For the Nine Months Ended September 30, | |||||||

2018 | 2017 | ||||||

Cash flows from operating activities: | |||||||

Net income | $ | 1,453 | $ | 1,522 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 367 | 321 | |||||

Provision for doubtful accounts | 5 | 12 | |||||

Deferred income taxes | 46 | (46 | ) | ||||

Stock-based compensation expense | 199 | 161 | |||||

Other | 196 | (49 | ) | ||||

Changes in assets and liabilities: | |||||||

Trade accounts receivable | (313 | ) | (284 | ) | |||

Other current assets | 338 | 21 | |||||

Other noncurrent assets | (194 | ) | (65 | ) | |||

Accounts payable | (5 | ) | (5 | ) | |||

Deferred revenues, current and noncurrent | (116 | ) | (21 | ) | |||

Other current and noncurrent liabilities | (86 | ) | 4 | ||||

Net cash provided by operating activities | 1,890 | 1,571 | |||||

Cash flows from investing activities: | |||||||

Purchases of property and equipment | (281 | ) | (204 | ) | |||

Purchases of available-for-sale investment securities | (1,356 | ) | (2,163 | ) | |||

Proceeds from maturity or sale of available-for-sale investment securities | 1,516 | 2,352 | |||||

Purchases of held-to-maturity investment securities | (1,093 | ) | (1,015 | ) | |||

Proceeds from maturity of held-to-maturity investment securities | 750 | 208 | |||||

Purchases of other investments | (479 | ) | (363 | ) | |||

Proceeds from maturity or sale of other investments | 345 | 835 | |||||

Payments for business combinations, net of cash acquired | (479 | ) | (72 | ) | |||

Net cash (used in) investing activities | (1,077 | ) | (422 | ) | |||

Cash flows from financing activities: | |||||||

Issuance of common stock under stock-based compensation plans | 142 | 146 | |||||

Repurchases of common stock | (994 | ) | (1,557 | ) | |||

Repayment of term loan borrowings and capital lease obligations | (89 | ) | (62 | ) | |||

Net change in notes outstanding under the revolving credit facility | (75 | ) | — | ||||

Dividends paid | (352 | ) | (179 | ) | |||

Net cash (used in) financing activities | (1,368 | ) | (1,652 | ) | |||

Effect of exchange rate changes on cash and cash equivalents | (31 | ) | 46 | ||||

(Decrease) in cash and cash equivalents | (586 | ) | (457 | ) | |||

Cash and cash equivalents, beginning of year | 1,925 | 2,034 | |||||

Cash and cash equivalents, end of period | $ | 1,339 | $ | 1,577 | |||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

5

COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1 — Interim Consolidated Financial Statements | ||||

The terms “Cognizant,” “we,” “our,” “us” and “the Company” refer to Cognizant Technology Solutions Corporation and its subsidiaries unless the context indicates otherwise. We have prepared the accompanying unaudited consolidated financial statements included herein in accordance with generally accepted accounting principles in the United States of America, or U.S. GAAP, and Regulation S-X under the Securities Exchange Act of 1934, as amended, or the Exchange Act. The accompanying unaudited consolidated financial statements should be read in conjunction with our audited consolidated financial statements (and notes thereto) included in our Annual Report on Form 10-K for the year ended December 31, 2017. In our opinion, all adjustments considered necessary for a fair statement of the accompanying unaudited consolidated financial statements have been included and all adjustments are of a normal and recurring nature. Operating results for the interim periods are not necessarily indicative of results that may be expected to occur for the entire year.

Recently Adopted Accounting Pronouncements

Date Issued and Topic | Date Adopted and Method | Description | Impact |

May 2014 Revenue | January 1, 2018 Modified Retrospective | The new standard, as amended, sets forth a single comprehensive model for recognizing and reporting revenues. The standard also requires additional financial statement disclosures that enable users to understand the nature, amount, timing and uncertainty of revenues and cash flows relating to customer contracts. The standard allows for two methods of adoption: the full retrospective adoption, which requires the standard to be applied to each prior period presented, or the modified retrospective adoption, which requires the cumulative effect of adoption to be recognized as an adjustment to opening retained earnings in the period of adoption. | See Note 3 for the impact of adoption of this standard. |

November 2016 Statement of Cash Flows | January 1, 2018 Retrospective | This update requires restricted cash to be included with cash and cash equivalents when reconciling the beginning and ending amounts on the statement of cash flows. It also requires a reconciliation of such totals to the amounts on the statement of financial position and disclosure as to the nature of the restrictions. | There were no restricted cash balances as of September 30, 2018. The adoption of this update had no impact on our financial statements for the three and nine months ended September 30, 2018. |

February 2018 Income Statement - Reporting Comprehensive Income | January 1, 2018 In the period of adoption | This update provides an option for entities to reclassify stranded tax effects caused by the recently-enacted Tax Cuts and Jobs Act, or Tax Reform Act, from accumulated other comprehensive income to retained earnings. | We have early adopted this update as of January 1, 2018. The adoption resulted in a decrease of $1 million in accumulated other comprehensive income and a corresponding increase of $1 million to opening retained earnings. |

6

New Accounting Pronouncements

Date Issued and Topic | Effective Date | Description | Impact |

February 2016 Leases | January 1, 2019 | The new standard replaces the existing guidance on leases and requires the lessee to recognize a right-of-use asset and a lease liability for all leases with lease terms equal to or greater than twelve months. For finance leases, the lessee would recognize interest expense and amortization of the right-of-use asset, and for operating leases, the lessee would recognize total lease expense on a straight-line basis. The standard offers several practical expedients for transition and certain expedients specific to lessees or lessors. The standard allows for two methods of adoption: retrospective to each prior reporting period presented with the cumulative effect of adoption recognized at the beginning of the earliest period presented or retrospective to the beginning of the period of adoption through a cumulative-effect adjustment. | While we are continuing to evaluate the provisions of this standard, the primary effect will be to require recording of right-of-use assets and corresponding lease obligations for current operating leases. We expect the adoption of this standard to have a material impact on our consolidated statement of financial position, but not on the consolidated statements of operations or cash flows. As of December 31, 2017, our undiscounted operating lease commitments were $943 million. We are currently planning to elect the package of practical expedients which permits us to not reassess prior conclusions related to contracts containing leases, lease classification and initial direct costs. We intend to adopt the standard retrospectively to the beginning of the period of adoption through a cumulative-effect adjustment. |

March 2017 Nonrefundable Fees and Other Costs | January 1, 2019 | This update shortens the amortization period for certain callable debt securities held at a premium to the earliest call date. The amendments do not require an accounting change for securities held at a discount. Upon adoption, entities will be required to use a modified retrospective transition with the cumulative effect adjustment recognized to retained earnings as of the beginning of the period of adoption. | We do not expect the adoption of this update to have a material impact on our financial statements. |

August 2018 Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement (CCA) that is a Service Contract | January 1, 2020 | This update aligns the accounting for costs incurred to implement a CCA that is a service arrangement with the guidance on capitalizing costs associated with developing or obtaining internal-use software. The update clarifies that a customer should capitalize certain implementation costs and subsequently amortize such costs over the term of the hosting arrangement as operating expenses. | We are currently evaluating the effect this update will have on our consolidated financial statements and related disclosures. |

Note 2 — Internal Investigation and Related Matters | ||||

We have substantially completed our internal investigation focused on whether certain payments relating to Company-owned facilities in India were made improperly and in possible violation of the U.S. Foreign Corrupt Practices Act, or FCPA, and other applicable laws. The investigation, which began in 2016, has also examined various other payments made in small amounts in India that may not have complied with Company policy or applicable law. In September 2016, we voluntarily notified the U.S. Department of Justice, or DOJ, and Securities and Exchange Commission, or SEC, and are cooperating fully with both agencies. The investigation has been conducted under the oversight of the Audit Committee, with the assistance of outside counsel. In connection with the investigation, during the year ended December 31, 2016, we recorded out-of-period corrections related to $4 million of potentially improper payments between 2009 and 2016 that had been previously capitalized when they should have been expensed. These out-of-period corrections were not material to any previously issued financial statements. There were no adjustments recorded during 2018 and 2017 related to the amounts under investigation.

The Company’s discussions with the DOJ and SEC have progressed to a point where the Company can now reasonably estimate a probable loss and has recorded an accrual of $28 million, or FCPA Accrual, in the caption “Accrued expenses and other

7

current liabilities” in our consolidated statements of financial position. There can be no assurance as to the timing of a final resolution of these matters with the DOJ and SEC.

Note 3 — Revenues | ||||

Adoption of ASC Topic 606, “Revenue from Contracts with Customers”

On January 1, 2018, we adopted ASC Topic 606, “Revenue from Contracts with Customers,” or the New Revenue Standard, using the modified retrospective method applied to contracts that were not completed as of January 1, 2018. Results for reporting periods beginning after January 1, 2018 are presented under the New Revenue Standard, while prior period amounts are not adjusted and continue to be reported in accordance with our historic accounting policies. For contracts that were modified before the effective date, the Company aggregated the effect of all contract modifications prior to identifying performance obligations and allocating transaction price in accordance with the practical expedient ASC 606-10-65-1-(f)-4. Upon adoption of the New Revenue Standard on January 1, 2018, we recorded a net increase to opening retained earnings of approximately $121 million, after a tax impact of $37 million. The impact of adoption primarily relates to (1) changes in the method used to measure progress on our fixed-price application maintenance, consulting and business process services contracts, (2) the longer period of amortization for costs to fulfill a contract, (3) the timing of revenue recognition and allocation of purchase price on our software license contracts, (4) the reclassification of balances representing receivables, as defined by the New Revenue Standard, from Unbilled accounts receivable to Trade accounts receivable, net, (5) the reclassification of balances representing contract assets, as defined by the New Revenue Standard, from Unbilled accounts receivable to Other current assets, as well as (6) the income tax impact of the above items, as applicable.

8

The following tables compare the financial statement line items materially affected by the adoption of the New Revenue Standard as of and for the three and nine months ended September 30, 2018 to the pro-forma amounts had the previous guidance been in effect, or Pro-forma Amounts:

September 30, 2018 | ||||||||||||

As Reported | Pro-forma Amounts | Impacts of the New Revenue Standard | ||||||||||

(in millions) | ||||||||||||

Assets: | ||||||||||||

Trade accounts receivable, net(1), (2) | $ | 3,187 | $ | 3,073 | $ | 114 | ||||||

Unbilled accounts receivable(1), (3) | — | 432 | (432 | ) | ||||||||

Other current assets(2), (3) | 777 | 457 | 320 | |||||||||

Total current assets | 2 | |||||||||||

Other noncurrent assets(4) | 643 | 589 | 54 | |||||||||

Total assets | $ | 56 | ||||||||||

Liabilities: | ||||||||||||

Deferred revenue(2) | $ | 244 | $ | 417 | $ | (173 | ) | |||||

Total current liabilities | (173 | ) | ||||||||||

Deferred revenue, noncurrent(2) | 72 | 106 | (34 | ) | ||||||||

Deferred income tax liabilities, net(5) | 157 | 100 | 57 | |||||||||

Total liabilities | (150 | ) | ||||||||||

Stockholders’ equity: | ||||||||||||

Retained earnings | 11,041 | 10,835 | 206 | |||||||||

Total stockholders’ equity | 206 | |||||||||||

Total liabilities and stockholders’ equity | $ | 56 | ||||||||||

Three Months Ended September 30, 2018 | Nine Months Ended September 30, 2018 | |||||||||||||||||||||||

As Reported | Pro-forma Amounts | Impacts of the New Revenue Standard | As Reported | Pro-forma Amounts | Impacts of the New Revenue Standard | |||||||||||||||||||

(in millions) | (in millions) | |||||||||||||||||||||||

Revenues(2) | $ | 4,078 | $ | 4,045 | $ | 33 | $ | 11,996 | $ | 11,911 | $ | 85 | ||||||||||||

Cost of revenues (4) | 2,480 | 2,484 | (4 | ) | 7,298 | 7,317 | (19 | ) | ||||||||||||||||

Selling, general and administrative expenses | 734 | 734 | — | 2,250 | 2,250 | — | ||||||||||||||||||

Depreciation and amortization expense | 119 | 119 | — | 340 | 340 | — | ||||||||||||||||||

Income from operations | 745 | 708 | 37 | 2,108 | 2,004 | 104 | ||||||||||||||||||

Other income (expense), net | (83 | ) | (84 | ) | 1 | (126 | ) | (127 | ) | 1 | ||||||||||||||

Income before provision for income taxes(5) | 662 | 624 | 38 | 1,982 | 1,877 | 105 | ||||||||||||||||||

Provision for income taxes | (185 | ) | (178 | ) | (7 | ) | (530 | ) | (510 | ) | (20 | ) | ||||||||||||

Income (loss) from equity method investment | — | — | — | 1 | 1 | — | ||||||||||||||||||

Net income | $ | 477 | $ | 446 | $ | 31 | $ | 1,453 | $ | 1,368 | $ | 85 | ||||||||||||

Basic earnings per share | $ | 0.82 | $ | 0.77 | $ | 0.05 | $ | 2.49 | $ | 2.34 | $ | 0.15 | ||||||||||||

Diluted earnings per share | $ | 0.82 | $ | 0.77 | $ | 0.05 | $ | 2.48 | $ | 2.34 | $ | 0.14 | ||||||||||||

(1) | Reflects the reclassification of balances representing receivables, as defined by the New Revenue Standard, from Unbilled accounts receivable to Trade accounts receivable, net. |

(2) | Reflects the impact of changes in the method used to measure progress on our fixed-price application maintenance, consulting and business process services contracts and the timing of revenue recognition and allocation of purchase price on our software license contracts. |

(3) | Reflects the reclassification of balances representing contract assets, as defined by the New Revenue Standard, from Unbilled accounts receivable to Other current assets. |

(4) | Reflects the impact of a longer period of amortization for costs to fulfill a contract. |

(5) | Reflects the income tax impact of the above items. |

9

Revenue Recognition

We recognize revenues as we transfer control of deliverables (products, solutions and services) to our customers in an amount reflecting the consideration to which we expect to be entitled. To recognize revenues, we apply the following five step approach: (1) identify the contract with a customer, (2) identify the performance obligations in the contract, (3) determine the transaction price, (4) allocate the transaction price to the performance obligations in the contract, and (5) recognize revenues when a performance obligation is satisfied. We account for a contract when it has approval and commitment from all parties, the rights of the parties are identified, payment terms are identified, the contract has commercial substance and collectability of consideration is probable. The Company applies judgment in determining the customer’s ability and intention to pay, which is based on a variety of factors including the customer’s historical payment experience.

We may enter into arrangements that consist of multiple performance obligations. Such arrangements may include any combination of our deliverables. To the extent a contract includes multiple promised deliverables, we apply judgment to determine whether promised deliverables are capable of being distinct and are distinct in the context of the contract. If these criteria are not met, the promised deliverables are accounted for as a combined performance obligation. For arrangements with multiple distinct performance obligations, we allocate consideration among the performance obligations based on their relative standalone selling price. Standalone selling price is the price at which we would sell a promised good or service separately to the customer. When not directly observable, we typically estimate standalone selling price by using the expected cost plus a margin approach. We typically establish a standalone selling price range for our deliverables, which is reassessed on a periodic basis or when facts and circumstances change.

For performance obligations where control is transferred over time, revenues are recognized based on the extent of progress towards completion of the performance obligation. The selection of the method to measure progress towards completion requires judgment and is based on the nature of the deliverables to be provided. Revenues related to fixed-price contracts for application development and systems integration services, consulting or other technology services are recognized as the service is performed using the cost to cost method, under which the total value of revenues is recognized on the basis of the percentage that each contract’s total labor cost to date bears to the total expected labor costs. Revenues related to fixed-price application maintenance, testing and business process services are recognized based on our right to invoice for services performed for contracts in which the invoicing is representative of the value being delivered, in accordance with the practical expedient in ASC 606-10-55-18. If our invoicing is not consistent with value delivered, revenues are recognized as the service is performed based on the cost to cost method described above. The cost to cost method requires estimation of future costs, which is updated as the project progresses to reflect the latest available information; such estimates and changes in estimates involve the use of judgment. The cumulative impact of any revision in estimates is reflected in the financial reporting period in which the change in estimate becomes known and any anticipated losses on contracts are recognized immediately. Revenues related to fixed-price hosting and infrastructure services are recognized based on our right to invoice for services performed for contracts in which the invoicing is representative of the value being delivered, in accordance with the practical expedient in ASC 606-10-55-18. If our invoicing is not consistent with value delivered, revenues are recognized on a straight-line basis unless revenues are earned and obligations are fulfilled in a different pattern. The revenue recognition method applied to the types of contracts described above provides the most faithful depiction of performance towards satisfaction of our performance obligations; for example, the cost to cost method is used when the value of services provided to the customer is best represented by the costs expended to deliver those services.

Revenues related to our non-hosted software license arrangements that do not require significant modification or customization of the underlying software are recognized when the software is delivered as control is transferred at a point in time. For software license arrangements that require significant functionality enhancements or modification of the software, revenues for the software license and related services are recognized as the services are performed in accordance with the methods described above. In software hosting arrangements, the rights provided to the customer, such as ownership of a license, contract termination provisions and the feasibility of the client to operate the software, are considered in determining whether the arrangement includes a license or a service. Sales and usage-based fees promised in exchange for licenses of intellectual property are not recognized as revenue until the uncertainty related to the variable amounts is resolved. Revenues related to software maintenance and support are generally recognized on a straight-line basis over the contract period.

Revenues related to our time-and-materials, transaction-based or volume-based contracts are recognized over the period the services are provided in a manner that corresponds with the value transferred to the customer to-date relative to the remaining services to be provided.

Revenues also include the reimbursement of out-of-pocket expenses. Our warranties generally provide a customer with assurance that the related deliverable will function as the parties intended because it complies with agreed-upon specifications and is therefore not considered an additional performance obligation in the contract.

10

From time to time, we may enter into arrangements with third party suppliers to resell products or services. In such cases, we evaluate whether we are the principal (i.e. report revenues on a gross basis) or agent (i.e. report revenues on a net basis). In doing so, we first evaluate whether we control the good or service before it is transferred to the customer. If we control the good or service before it is transferred to the customer, we are the principal; if not, we are the agent. Determining whether we control the good or service before it is transferred to the customer may require judgment.

Our contracts may be modified to add, remove or change existing performance obligations. The accounting for modifications to our contracts involves assessing whether the services added to an existing contract are distinct and whether the pricing is at the standalone selling price. Services added that are not distinct are accounted for on a cumulative catch up basis, while those that are distinct are accounted for prospectively, either as a separate contract if the additional services are priced at the standalone selling price, or as a termination of the existing contract and creation of a new contract if not priced at the standalone selling price. Services added to our application development and systems integration service contracts are typically not distinct, while services added to our other contracts, including application maintenance, testing and business process services contracts, are typically distinct.

Incentive revenues, volume discounts, or any other form of variable consideration is estimated using either the sum of probability weighted amounts in a range of possible consideration amounts (expected value), or the single most likely amount in a range of possible consideration amounts (most likely amount), depending on which method better predicts the amount of consideration to which we may be entitled. We include in the transaction price variable consideration only to the extent it is probable that a significant reversal of revenues recognized will not occur when the uncertainty associated with the variable consideration is resolved. Our estimates of variable consideration and determination of whether to include estimated amounts in the transaction price may involve judgment and are based largely on an assessment of our anticipated performance and all information that is reasonably available to us.

We assess the timing of the transfer of goods or services to the customer as compared to the timing of payments to determine whether a significant financing component exists. As a practical expedient, we do not assess the existence of a significant financing component when the difference between payment and transfer of deliverables is a year or less. If the difference in timing arises for reasons other than the provision of finance to either the customer or us, no financing component is deemed to exist. The primary purpose of our invoicing terms is to provide customers with simplified and predictable ways of purchasing our services, not to receive or provide financing from or to customers. We do not consider set up or transition fees paid upfront by our customers to represent a financing component, as such fees are required to encourage customer commitment to the project and protect us from early termination of the contract.

Costs to Fulfill

Recurring operating costs for contracts with customers are recognized as incurred. Certain eligible, nonrecurring costs incurred in the initial phases of our application maintenance, business process outsourcing and infrastructure services contracts (i.e. set-up or transition costs) are capitalized when such costs (1) relate directly to the contract, (2) generate or enhance resources of the Company that will be used in satisfying the performance obligation in the future, and (3) are expected to be recovered. These costs are expensed ratably over the estimated life of the customer relationship, including expected renewals. In determining the estimated life of the customer relationship, we evaluate the average contract term, on a portfolio basis by nature of the services to be provided, and apply judgment to evaluate the rate of technological and industry change. Capitalized amounts are monitored regularly for impairment. Impairment losses are recorded when projected remaining undiscounted operating cash flows are not sufficient to recover the carrying amount of the capitalized costs to fulfill.

The following table presents information related to the capitalized costs to fulfill, such as set-up or transition activities, for the nine months ended September 30, 2018. Costs to fulfill are recorded in "Other noncurrent assets" in our consolidated statements of financial position. Costs to obtain contracts were immaterial for the periods disclosed.

Costs to Fulfill | ||||

(in millions) | ||||

Balance - January 1, 2018 | $ | 303 | ||

Amortization expense | (50 | ) | ||

Costs capitalized | 132 | |||

Other | (2 | ) | ||

Balance - September 30, 2018 | $ | 383 | ||

11

Trade Accounts Receivable and Contract Balances

We classify our right to consideration in exchange for deliverables as either a receivable or a contract asset. A receivable is a right to consideration that is unconditional (i.e. only the passage of time is required before payment is due). For example, we recognize a receivable for revenues related to our time and materials and transaction or volume-based contracts when earned regardless of whether amounts have been billed. We present such receivables in Trade accounts receivable, net in our consolidated statements of financial position at their net estimated realizable value. We maintain an allowance for doubtful accounts to provide for the estimated amount of receivables that may not be collected. The allowance is based upon an assessment of customer creditworthiness, historical payment experience, the age of outstanding receivables and other applicable factors.

A contract asset is a right to consideration that is conditional upon factors other than the passage of time. Contract assets are presented in Other current assets in our consolidated statements of financial position and primarily relate to unbilled amounts on fixed-price contracts utilizing the cost to cost method of revenue recognition. The table below shows significant movements in contract assets:

Contract Assets | ||||

(in millions) | ||||

Balance - January 1, 2018 | $ | 306 | ||

Revenues recognized during the period but not billed | 290 | |||

Amounts reclassified to accounts receivable | (273 | ) | ||

Other | (3 | ) | ||

Balance - September 30, 2018 | $ | 320 | ||

Our contract liabilities, or deferred revenue, consist of advance payments and billings in excess of revenues recognized. We classify deferred revenue as current or noncurrent based on the timing of when we expect to recognize the revenues. The noncurrent portion of deferred revenue is included in other noncurrent liabilities in our consolidated statements of financial position.

The table below shows significant movements in the deferred revenue balances (current and noncurrent) for the period disclosed:

Deferred Revenue | ||||

(in millions) | ||||

Balance - January 1, 2018 | $ | 431 | ||

Amounts billed but not recognized as revenues | 116 | |||

Revenues recognized related to the opening balance of deferred revenue | (230 | ) | ||

Other | (1 | ) | ||

Balance - September 30, 2018 | $ | 316 | ||

Our contract assets and liabilities are reported in a net position on a contract by contract basis at the end of each reporting period. The difference between the opening and closing balances of our contract assets and deferred revenues primarily results from the timing difference between our performance obligations and the customer’s payment. We receive payments from customers based on the terms established in our contracts, which vary by contract type.

Revenues recognized during the nine months ended September 30, 2018 for performance obligations satisfied or partially satisfied in previous periods were immaterial.

12

Remaining Performance Obligations

ASC 606 requires that we disclose the aggregate amount of transaction price that is allocated to performance obligations that have not yet been satisfied as of September 30, 2018. This disclosure is not required for:

(1) | contracts with a duration of one year or less as determined under ASC 606, |

(2) | contracts for which we recognize revenues based on the right to invoice for services performed, |

(3) | variable consideration allocated entirely to a wholly unsatisfied performance obligation or to a wholly unsatisfied promise to transfer a distinct good or service that forms part of a single performance obligation in accordance with ASC 606-10-25-14(b), for which the criteria in ASC 606-10-32-40 have been met, or |

(4) | variable consideration in the form of a sales-based or usage based royalty promised in exchange for a license of intellectual property. |

Many of our performance obligations meet one or more of these exemptions. As of September 30, 2018, the aggregate amount of transaction price allocated to remaining performance obligations, other than those meeting the exclusion criteria above, was $2,014 million, of which approximately 70% is expected to be recognized as revenues within 2 years.

Disaggregation of Revenues

The table below presents disaggregated revenues from contracts with customers by customer location, service line and contract-type for each of our business segments. We believe this disaggregation best depicts how the nature, amount, timing and uncertainty of our revenues and cash flows are affected by industry, market and other economic factors.

Three Months Ended | ||||||||||||||||||||

September 30, 2018 | ||||||||||||||||||||

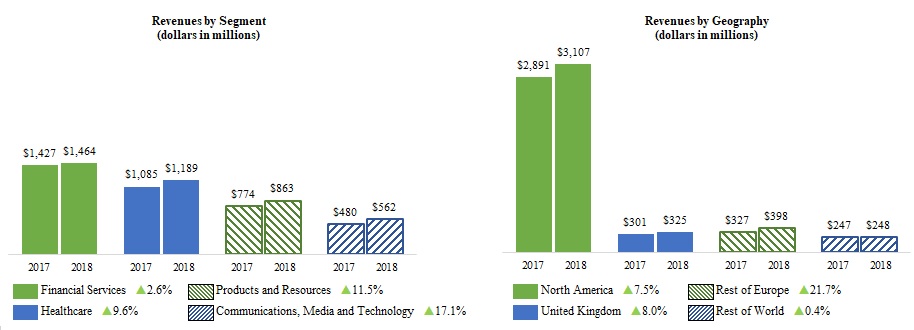

Financial Services | Healthcare | Products and Resources | Communications, Media and Technology | Total | ||||||||||||||||

(in millions) | ||||||||||||||||||||

Revenues | ||||||||||||||||||||

Geography: | ||||||||||||||||||||

North America | $ | 1,033 | $ | 1,084 | $ | 609 | $ | 381 | $ | 3,107 | ||||||||||

United Kingdom | 127 | 23 | 90 | 85 | 325 | |||||||||||||||

Rest of Europe | 170 | 69 | 109 | 50 | 398 | |||||||||||||||

Europe - Total | 297 | 92 | 199 | 135 | 723 | |||||||||||||||

Rest of World | 134 | 13 | 55 | 46 | 248 | |||||||||||||||

Total | $ | 1,464 | $ | 1,189 | $ | 863 | $ | 562 | $ | 4,078 | ||||||||||

Service line: | ||||||||||||||||||||

Consulting and technology services | $ | 902 | $ | 645 | $ | 512 | $ | 292 | $ | 2,351 | ||||||||||

Outsourcing services | 562 | 544 | 351 | 270 | 1,727 | |||||||||||||||

Total | $ | 1,464 | $ | 1,189 | $ | 863 | $ | 562 | $ | 4,078 | ||||||||||

Type of contract: | ||||||||||||||||||||

Time and materials | $ | 954 | $ | 464 | $ | 374 | $ | 354 | $ | 2,146 | ||||||||||

Fixed-price | 453 | 452 | 392 | 187 | 1,484 | |||||||||||||||

Transaction or volume-based | 57 | 273 | 97 | 21 | 448 | |||||||||||||||

Total | $ | 1,464 | $ | 1,189 | $ | 863 | $ | 562 | $ | 4,078 | ||||||||||

13

Nine Months Ended | ||||||||||||||||||||

September 30, 2018 | ||||||||||||||||||||

Financial Services | Healthcare | Products and Resources | Communications, Media and Technology | Total | ||||||||||||||||

(in millions) | ||||||||||||||||||||

Revenues | ||||||||||||||||||||

Geography: | ||||||||||||||||||||

North America | $ | 3,133 | $ | 3,167 | $ | 1,766 | $ | 1,083 | $ | 9,149 | ||||||||||

United Kingdom | 357 | 68 | 266 | 253 | 944 | |||||||||||||||

Rest of Europe | 497 | 191 | 327 | 138 | 1,153 | |||||||||||||||

Europe - Total | 854 | 259 | 593 | 391 | 2,097 | |||||||||||||||

Rest of World | 407 | 40 | 165 | 138 | 750 | |||||||||||||||

Total | $ | 4,394 | $ | 3,466 | $ | 2,524 | $ | 1,612 | $ | 11,996 | ||||||||||

Service line: | ||||||||||||||||||||

Consulting and technology services | $ | 2,658 | $ | 1,896 | $ | 1,492 | $ | 859 | $ | 6,905 | ||||||||||

Outsourcing services | 1,736 | 1,570 | 1,032 | 753 | 5,091 | |||||||||||||||

Total | $ | 4,394 | $ | 3,466 | $ | 2,524 | $ | 1,612 | $ | 11,996 | ||||||||||

Type of contract: | ||||||||||||||||||||

Time and materials | $ | 2,842 | $ | 1,364 | $ | 1,122 | $ | 995 | $ | 6,323 | ||||||||||

Fixed-price | 1,384 | 1,406 | 1,120 | 545 | 4,455 | |||||||||||||||

Transaction or volume-based | 168 | 696 | 282 | 72 | 1,218 | |||||||||||||||

Total | $ | 4,394 | $ | 3,466 | $ | 2,524 | $ | 1,612 | $ | 11,996 | ||||||||||

Note 4 — Business Combinations | ||||

During the nine months ended September 30, 2018, we completed two business combinations for total consideration of approximately $492 million, inclusive of contingent consideration. The acquisition of Bolder Healthcare Solutions, a privately-held U.S. provider of revenue cycle management solutions to the healthcare industry expands our healthcare consulting, technology and business process services portfolio and strengthens our position in digital healthcare technology and operations. The acquisition of Hedera Consulting, a privately-held company specializing in business advisory and data analytics services across a number of industries expands our consulting, business insight and digital transformation capabilities in Belgium and the Netherlands.

14

These acquisitions were not material, either individually or in the aggregate, to our operations, financial position or operating cash flow. Accordingly, pro forma results have not been presented. These acquisitions were included in our unaudited consolidated financial statements as of the date on which the businesses were acquired. We have allocated the purchase price related to these transactions to tangible and intangible assets and liabilities, including non-deductible goodwill, based on their estimated fair values. We will finalize the purchase price allocation as soon as practicable within the measurement period, but in no event later than one year following the date of acquisition. The allocations of preliminary purchase price to the fair value of the aggregate assets acquired and liabilities assumed were as follows:

Fair Value | Weighted Average Useful Life | ||||

(in millions) | |||||

Cash | $ | 9 | |||

Current assets | 37 | ||||

Property, plant and equipment and other noncurrent assets | 7 | ||||

Non-deductible goodwill (1) | 344 | ||||

Customer relationship intangible assets | 122 | 9.7 years | |||

Other intangible assets | 26 | 2.4 years | |||

Current liabilities | (14 | ) | |||

Noncurrent liabilities | (39 | ) | |||

Purchase price | $ | 492 | |||

(1) The primary items that generated goodwill are the value of the acquired assembled workforces and synergies between the acquired companies and us, neither of which qualify as an amortizable intangible asset.

Note 5 — Realignment Charges | ||||

In 2017, we began a realignment of our business to accelerate the shift to digital services and solutions while improving the overall efficiency of our operations. As part of this realignment, for the three and nine months ended September 30, 2017, we incurred $19 million and $69 million, respectively, in pre-tax charges. These charges included severance costs primarily related to our voluntary separation program announced in May 2017, lease termination costs and advisory fees related to non-routine shareholder matters and charges related to the development of our realignment and return of capital programs. Further, during the three months ended September 30, 2018, we incurred $11 million in pre-tax severance costs as part of an involuntary separation program. Our realignment initiatives are intended to further improve our cost structure primarily by optimizing our resource pyramid. The total costs related to the realignment are reported in "Selling, general and administrative expenses" in our consolidated statements of operations.

Realignment charges were as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

(in millions) | |||||||||||||||

Employee separations | $ | 11 | $ | 14 | $ | 11 | $ | 53 | |||||||

Advisory fees | — | 5 | — | 15 | |||||||||||

Lease termination costs | — | — | 1 | 1 | |||||||||||

Total realignment costs | $ | 11 | $ | 19 | $ | 12 | $ | 69 | |||||||

15

Note 6 — Investments | ||||

Our investments were as follows:

September 30, 2018 | December 31, 2017 | ||||||

(in millions) | |||||||

Short-term investments: | |||||||

Equity investment securities | $ | 25 | $ | 25 | |||

Available-for-sale investment securities | 1,801 | 1,972 | |||||

Held-to-maturity investment securities | 1,133 | 745 | |||||

Time deposits | 465 | (1) | 389 | ||||

Total short-term investments | $ | 3,424 | $ | 3,131 | |||

Long-term investments: | |||||||

Equity and cost method investments | $ | 75 | $ | 74 | |||

Held-to-maturity investment securities | 18 | 161 | |||||

Total long-term investments | $ | 93 | $ | 235 | |||

(1) | Includes $405 million in restricted time deposits as of September 30, 2018. See Note 9. |

Equity Investment Securities

Our equity investment securities consist of a U.S. dollar denominated investment in a fixed income mutual fund. Unrealized losses for the three and nine months ended September 30, 2018 and 2017 were immaterial. The value of the fixed income mutual fund is based on the net asset value, or NAV, of the fund, with appropriate consideration of the liquidity and any restrictions on disposition of our investment in the fund. There were no realized gains or losses on equity securities during the three and nine months ended September 30, 2018 and 2017.

Available-for-Sale Investment Securities

Our available-for-sale investment securities consist of U.S. dollar denominated investments primarily in U.S. Treasury notes, U.S. government agency debt securities, municipal debt securities, non-U.S. government debt securities, U.S. and international corporate bonds, certificates of deposit, commercial paper, debt securities issued by supranational institutions, and asset-backed securities, including securities backed by auto loans, credit card receivables, and other receivables. Our investment guidelines are to purchase securities which are investment grade at the time of acquisition. We monitor the credit ratings of the securities in our portfolio on an ongoing basis.

The amortized cost, gross unrealized gains and losses and fair value of available-for-sale investment securities at September 30, 2018 were as follows:

Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||

(in millions) | |||||||||||||||

U.S. Treasury and agency debt securities | $ | 647 | $ | — | $ | (10 | ) | $ | 637 | ||||||

Corporate and other debt securities | 431 | — | (5 | ) | 426 | ||||||||||

Certificates of deposit and commercial paper | 317 | — | — | 317 | |||||||||||

Asset-backed securities | 321 | — | (3 | ) | 318 | ||||||||||

Municipal debt securities | 104 | — | (1 | ) | 103 | ||||||||||

Total available-for-sale investment securities | $ | 1,820 | $ | — | $ | (19 | ) | $ | 1,801 | ||||||

16

The amortized cost, gross unrealized gains and losses and fair value of available-for-sale investment securities at December 31, 2017 were as follows:

Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||

(in millions) | |||||||||||||||

U.S. Treasury and agency debt securities | $ | 667 | $ | — | $ | (6 | ) | $ | 661 | ||||||

Corporate and other debt securities | 439 | — | (2 | ) | 437 | ||||||||||

Certificates of deposit and commercial paper | 450 | — | — | 450 | |||||||||||

Asset-backed securities | 297 | — | (2 | ) | 295 | ||||||||||

Municipal debt securities | 130 | — | (1 | ) | 129 | ||||||||||

Total available-for-sale investment securities | $ | 1,983 | $ | — | $ | (11 | ) | $ | 1,972 | ||||||

The fair value and related unrealized losses of available-for-sale investment securities in a continuous unrealized loss position for less than 12 months and for 12 months or longer were as follows as of September 30, 2018:

Less than 12 Months | 12 Months or More | Total | |||||||||||||||||||||

Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||||||||

(in millions) | |||||||||||||||||||||||

U.S. Treasury and agency debt securities | $ | 296 | $ | (4 | ) | $ | 336 | $ | (6 | ) | $ | 632 | $ | (10 | ) | ||||||||

Corporate and other debt securities | 258 | (3 | ) | 134 | (2 | ) | 392 | (5 | ) | ||||||||||||||

Certificates of deposit and commercial paper | 198 | — | — | — | 198 | — | |||||||||||||||||

Asset-backed securities | 168 | (1 | ) | 137 | (2 | ) | 305 | (3 | ) | ||||||||||||||

Municipal debt securities | 62 | (1 | ) | 40 | — | 102 | (1 | ) | |||||||||||||||

Total | $ | 982 | $ | (9 | ) | $ | 647 | $ | (10 | ) | $ | 1,629 | $ | (19 | ) | ||||||||

The fair value and related unrealized losses of available-for-sale investment securities in a continuous unrealized loss position for less than 12 months and for 12 months or longer were as follows as of December 31, 2017:

Less than 12 Months | 12 Months or More | Total | |||||||||||||||||||||

Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||||||||

(in millions) | |||||||||||||||||||||||

U.S. Treasury and agency debt securities | $ | 519 | $ | (4 | ) | $ | 124 | $ | (2 | ) | $ | 643 | $ | (6 | ) | ||||||||

Corporate and other debt securities | 297 | (1 | ) | 126 | (1 | ) | 423 | (2 | ) | ||||||||||||||

Certificates of deposit and commercial paper | 49 | — | — | — | 49 | — | |||||||||||||||||

Asset-backed securities | 193 | (1 | ) | 94 | (1 | ) | 287 | (2 | ) | ||||||||||||||

Municipal debt securities | 107 | (1 | ) | 18 | — | 125 | (1 | ) | |||||||||||||||

Total | $ | 1,165 | $ | (7 | ) | $ | 362 | $ | (4 | ) | $ | 1,527 | $ | (11 | ) | ||||||||

The unrealized losses for the above securities as of September 30, 2018 and December 31, 2017 were primarily attributable to changes in interest rates. At each reporting date, we perform an evaluation of impaired available-for-sale securities to determine if the unrealized losses are other-than-temporary. We do not consider any of the investments to be other-than-temporarily impaired as of September 30, 2018. The gross unrealized gains and losses in the above tables were recorded, net of tax, in "Accumulated other comprehensive income (loss)" in our consolidated statements of financial position.

17

The contractual maturities of our fixed income available-for-sale investment securities as of September 30, 2018 are set forth in the following table:

Amortized Cost | Fair Value | ||||||

(in millions) | |||||||

Due within one year | $ | 579 | $ | 578 | |||

Due after one year up to two years | 474 | 466 | |||||

Due after two years up to three years | 407 | 400 | |||||

Due after three years | 39 | 39 | |||||

Asset-backed securities | 321 | 318 | |||||

Total available-for-sale investment securities | $ | 1,820 | $ | 1,801 | |||

Asset-backed securities were excluded from the maturity categories because the actual maturities may differ from the contractual maturities since the underlying receivables may be prepaid without penalties. Further, actual maturities of debt securities may differ from those presented above since certain obligations provide the issuer the right to call or prepay the obligation prior to scheduled maturity without penalty.

Proceeds from sales of available-for-sale investment securities and the gross gains and losses that have been included in earnings as a result of those sales were as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

(in millions) | |||||||||||||||

Proceeds from sales of available-for-sale investment securities | $ | 490 | $ | 375 | $ | 1,049 | $ | 2,020 | |||||||

Gross gains | $ | — | $ | — | $ | — | $ | 1 | |||||||

Gross losses | (1 | ) | (1 | ) | (3 | ) | (2 | ) | |||||||

Net realized (losses) on sales of available-for-sale investment securities | $ | (1 | ) | $ | (1 | ) | $ | (3 | ) | $ | (1 | ) | |||

Held-to-Maturity Investment Securities

Our held-to-maturity investment securities consist of Indian rupee denominated investments primarily in commercial paper, corporate bonds and government debt securities. Our investment guidelines are to purchase securities that are investment grade at the time of acquisition. We monitor the credit ratings of the securities in our portfolio on an ongoing basis.

The amortized cost, gross unrealized gains and losses and fair value of held-to-maturity investment securities at September 30, 2018 were as follows:

Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||

(in millions) | |||||||||||||||

Short-term investments: | |||||||||||||||

Corporate and other debt securities | $ | 677 | $ | — | $ | (3 | ) | $ | 674 | ||||||

Commercial paper | 456 | — | (2 | ) | 454 | ||||||||||

Total short-term held-to-maturity investments | 1,133 | — | (5 | ) | 1,128 | ||||||||||

Long-term investments: | |||||||||||||||

Corporate and other debt securities | 6 | — | — | 6 | |||||||||||

Commercial paper | 12 | — | — | 12 | |||||||||||

Total held-to-maturity investment securities | $ | 1,151 | $ | — | $ | (5 | ) | $ | 1,146 | ||||||

18

The amortized cost, gross unrealized gains and losses and fair value of held-to-maturity investment securities at December 31, 2017 were as follows:

Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||

(in millions) | |||||||||||||||

Short-term investments: | |||||||||||||||

Corporate and other debt securities | $ | 346 | $ | — | $ | (1 | ) | $ | 345 | ||||||

Commercial paper | 399 | — | (2 | ) | 397 | ||||||||||

Total short-term held-to-maturity investments | 745 | — | (3 | ) | 742 | ||||||||||

Long-term investments: | |||||||||||||||

Corporate and other debt securities | 161 | — | (1 | ) | 160 | ||||||||||

Total held-to-maturity investment securities | $ | 906 | $ | — | $ | (4 | ) | $ | 902 | ||||||

The fair value and related unrealized losses of held-to-maturity investment securities in a continuous unrealized loss position for less than 12 months and for 12 months or longer were as follows as of September 30, 2018:

Less than 12 Months | 12 Months or More | Total | |||||||||||||||||||||

Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||||||||

(in millions) | |||||||||||||||||||||||

Corporate and other debt securities | $ | 469 | $ | (2 | ) | $ | 168 | $ | (1 | ) | $ | 637 | $ | (3 | ) | ||||||||

Commercial paper | 454 | (2 | ) | — | — | 454 | (2 | ) | |||||||||||||||

Total | $ | 923 | $ | (4 | ) | $ | 168 | $ | (1 | ) | $ | 1,091 | $ | (5 | ) | ||||||||

The fair value and related unrealized losses of held-to-maturity investment securities in a continuous unrealized loss position for less than 12 months and for 12 months or longer were as follows as of December 31, 2017:

Less than 12 Months | 12 Months or More | Total | |||||||||||||||||||||

Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||||||||

(in millions) | |||||||||||||||||||||||

Corporate and other debt securities | $ | 473 | $ | (2 | ) | $ | — | $ | — | $ | 473 | $ | (2 | ) | |||||||||

Commercial paper | 394 | (2 | ) | — | — | 394 | (2 | ) | |||||||||||||||

Total | $ | 867 | $ | (4 | ) | $ | — | $ | — | $ | 867 | $ | (4 | ) | |||||||||

At each reporting date, the Company performs an evaluation of held-to-maturity securities to determine if the unrealized losses are other-than-temporary. We do not consider any of the investments to be other-than-temporarily impaired as of September 30, 2018.

The contractual maturities of our fixed income held-to-maturity investment securities as of September 30, 2018 are set forth in the following table:

Amortized Cost | Fair Value | ||||||

(in millions) | |||||||

Due within one year | $ | 1,133 | $ | 1,128 | |||

Due after one year up to two years | 12 | 12 | |||||

Due after two years | 6 | 6 | |||||

Total held-to-maturity investment securities | $ | 1,151 | $ | 1,146 | |||

During the nine months ended September 30, 2018 and the year ended December 31, 2017, there were no transfers of investments between our available-for-sale and held-to-maturity investment portfolios.

19

Note 7 — Accrued Expenses and Other Current Liabilities | ||||

Accrued expenses and other current liabilities were as follows:

September 30, 2018 | December 31, 2017 | ||||||

(in millions) | |||||||

Compensation and benefits | $ | 1,053 | $ | 1,272 | |||

Customer volume and other incentives | 320 | 289 | |||||

Derivative financial instruments | 67 | 5 | |||||

FCPA Accrual | 28 | — | |||||

Income taxes | 158 | 48 | |||||

Professional fees | 114 | 100 | |||||

Travel and entertainment | 57 | 32 | |||||

Other | 329 | 325 | |||||

Total accrued expenses and other current liabilities | $ | 2,126 | $ | 2,071 | |||

Note 8 — Debt | ||||

In 2014, we entered into a credit agreement with a commercial bank syndicate, or, as amended, the Credit Agreement, providing for a $1,000 million unsecured term loan and a $750 million unsecured revolving credit facility. All notes drawn to date under the revolving credit facility have been less than 90 days in duration. The term loan and the revolving credit facility both mature in November 2019. We are required under the Credit Agreement to make scheduled quarterly principal payments on the term loan, with a final payment of $625 million due on the term loan due in November 2019. We are currently evaluating alternative financing arrangements. We were in compliance with all debt covenants and representations as of September 30, 2018.

Short-term Debt

The following summarizes our short-term debt balances as of:

September 30, 2018 | December 31, 2017 | |||||||

(in millions) | ||||||||

Notes outstanding under revolving credit facility | $ | — | $ | 75 | ||||

Term loan - current maturities | 100 | 100 | ||||||

Total short-term debt | $ | 100 | $ | 175 | ||||

Long-term Debt

The following summarizes our long-term debt balances as of:

September 30, 2018 | December 31, 2017 | |||||||

(in millions) | ||||||||

Term loan, due November 2019 | $ | 725 | $ | 800 | ||||

Less: | ||||||||

Current maturities | (100 | ) | (100 | ) | ||||

Deferred financing costs | (1 | ) | (2 | ) | ||||

Long-term debt, net of current maturities | $ | 624 | $ | 698 | ||||

20

Note 9 — Income Taxes | ||||

On December 22, 2017, the United States enacted the Tax Reform Act, which significantly revised the U.S. corporate income tax law for tax years beginning after December 31, 2017 by (among other provisions):

• | reducing the U.S. federal statutory corporate income tax rate from 35% to 21% for tax years beginning after December 31, 2017; |

• | implementing a modified territorial tax system that includes a one-time transition tax on all accumulated undistributed earnings of foreign subsidiaries; |

• | providing for a full deduction on future dividends received from foreign affiliates; and |

• | imposing a U.S. income tax on global intangible low-taxed income, or GILTI. |

During the fourth quarter of 2017, in accordance with the SEC Staff Accounting Bulletin ("SAB") No. 118 - Income Tax Accounting Implications of the Tax Cuts and Jobs Act, we recorded a one-time provisional net income tax expense of $617 million, which was comprised of: (i) the one-time transition tax expense on accumulated undistributed earnings of foreign subsidiaries of $635 million, (ii) foreign and U.S. state income tax expense that will be applicable upon repatriation of the accumulated undistributed earnings of our foreign subsidiaries, other than our Indian subsidiaries, of $53 million, partially offset by (iii) an income tax benefit of $71 million resulting from the revaluation of U.S. net deferred income tax liabilities to the new lower U.S. income tax rate. During the three months ended September 30, 2018, we recognized a $5 million reduction to the provision for income taxes as we finalized our calculation of the one-time net income tax expense related to the enactment of the Tax Reform Act, bringing the final one-time cost to $612 million. The Company has elected to pay the transition tax on undistributed earnings in installments through the year 2024.

Our effective income tax rates were as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||

Effective income tax rate | 27.9 | % | 24.9 | % | 26.7 | % | 21.7 | % | |||

The effective tax rate for the nine months ended September 30, 2017 was impacted by the recognition of income tax benefits previously unrecognized in our consolidated financial statements related to several uncertain tax positions totaling $72 million. The recognition of these benefits in the first quarter of 2017 was based on management’s reassessment regarding whether certain unrecognized tax benefits met the more-likely-than-not threshold in light of the lapse in the statute of limitations as to a portion of such benefits. The estimate of our 2018 annual effective income tax rate reflects the current interpretation of the Tax Reform Act, including the GILTI provision and may change as we receive additional clarification and guidance and as the interpretation of the Tax Reform Act evolves over time.

We are involved in an ongoing dispute with the Indian Income Tax Department, or ITD, in connection with which we received a notice in March 2018 asserting that the ITD is owed additional taxes on our previously disclosed 2016 India Cash Remittance, the transaction undertaken by our principal operating subsidiary in India, or CTS India, to repurchase shares from its shareholders, which are non-Indian Cognizant entities, valued at $2.8 billion. As a result of that transaction, undertaken pursuant to a plan approved by the Madras High Court in Chennai, India, we previously paid $135 million in Indian income taxes, which we believe are all the applicable taxes owed for this transaction under Indian law. The ITD is asserting that we owe an additional 33 billion Indian rupees ($455 million at the September 30, 2018 exchange rate) related to the 2016 India Cash Remittance. In addition to the dispute on the 2016 India Cash Remittance, we are involved in another ongoing dispute with the ITD relating to a 2013 transaction undertaken by CTS India to repurchase shares from its shareholders valued at $523 million (the two disputes collectively referred to as the ITD Dispute), for which we also believe we have paid all the applicable taxes owed. Accordingly, we have not recorded any reserves for these matters as of September 30, 2018. The ITD Dispute is ongoing, and no final decision has been reached.

In March 2018, the ITD placed an attachment on certain of our India bank accounts, relating to the 2016 India Cash Remittance. In April 2018, the Madras High Court granted our application for a stay of the actions of the ITD and lifted the ITD’s attachment of our bank accounts. As part of the interim stay order, we have deposited 5 billion Indian rupees ($68 million at the September 30, 2018 exchange rate) representing 15% of the disputed tax amount related to the 2016 India Cash Remittance, to be kept in a segregated account by the ITD. This amount is presented in "Other current assets" on our consolidated statement of financial position. In addition, in April 2018 the court placed a lien on certain time deposits of CTS India in the amount of 28 billion Indian rupees ($387 million at the September 30, 2018 exchange rate), which is the remainder of the disputed tax amount related to the 2016 India Cash Remittance. The affected time deposits are considered restricted assets and we have reported them in “Short-

21

term investments” on our consolidated statement of financial position. As of September 30, 2018, the restricted time deposits balance was $405 million, including accumulated interest. There were no restricted time deposits as of December 31, 2017.

Note 10 — Derivative Financial Instruments | ||||

In the normal course of business, we use foreign exchange forward contracts to manage foreign currency exchange rate risk. The estimated fair value of the foreign exchange forward contracts considers the following items: discount rate, timing and amount of cash flow and counterparty credit risk. Derivatives may give rise to credit risks from the possible non-performance by counterparties. Credit risk is generally limited to the fair value of those contracts that are favorable to us. We have limited our credit risk by entering into derivative transactions only with highly-rated financial institutions, limiting the amount of credit exposure with any one financial institution and conducting an ongoing evaluation of the creditworthiness of the financial institutions with which we do business. In addition, all the assets and liabilities related to our foreign exchange forward contracts set forth in the below table are subject to International Swaps and Derivatives Association, or ISDA, master netting arrangements or other similar agreements with each individual counterparty. These master netting arrangements generally provide for net settlement of all outstanding contracts with the counterparty in the case of an event of default or a termination event. We have presented all the assets and liabilities related to our foreign exchange forward contracts on a gross basis, with no offsets, in our accompanying unaudited consolidated statements of financial position. There is no financial collateral (including cash collateral) posted or received by us related to our foreign exchange forward contracts.

The following table provides information on the location and fair values of derivative financial instruments included in our unaudited consolidated statements of financial position as of:

September 30, 2018 | December 31, 2017 | |||||||||||||||||

Designation of Derivatives | Location on Statements of Financial Position | Assets | Liabilities | Assets | Liabilities | |||||||||||||

(in millions) | ||||||||||||||||||

Foreign exchange forward contracts – Designated as cash flow hedging instruments | Other current assets | $ | 4 | $ | — | $ | 134 | $ | — | |||||||||

Other noncurrent assets | — | — | 20 | — | ||||||||||||||

Accrued expenses and other current liabilities | — | 66 | — | — | ||||||||||||||

Other noncurrent liabilities | — | 48 | — | — | ||||||||||||||

Total | 4 | 114 | 154 | — | ||||||||||||||

Foreign exchange forward contracts – Not designated as hedging instruments | Other current assets | 3 | — | — | — | |||||||||||||

Accrued expenses and other current liabilities | — | 1 | — | 5 | ||||||||||||||

Total | 3 | 1 | — | 5 | ||||||||||||||

Total | $ | 7 | $ | 115 | $ | 154 | $ | 5 | ||||||||||

Cash Flow Hedges

We have entered into a series of foreign exchange forward contracts that are designated as cash flow hedges of Indian rupee denominated payments in India. These contracts are intended to partially offset the impact of movement of exchange rates on future operating costs and are scheduled to mature each month during 2018, 2019 and the first nine months of 2020. Under these contracts, we purchase Indian rupees and sell U.S. dollars. The changes in fair value of these contracts are initially reported in the caption “Accumulated other comprehensive income (loss)” in our consolidated statements of financial position and are subsequently reclassified to earnings in the same period the forecasted Indian rupee denominated payments are recorded in earnings. As of September 30, 2018, we estimate that $50 million, net of tax, of net losses related to derivatives designated as cash flow hedges recorded in accumulated other comprehensive income (loss) is expected to be reclassified into earnings within the next 12 months.

22

The notional value of our outstanding contracts by year of maturity and the net unrealized gains included in accumulated other comprehensive income (loss) for such contracts were as follows as of:

September 30, 2018 | December 31, 2017 | ||||||

(in millions) | |||||||

2018 | $ | 360 | $ | 1,185 | |||

2019 | 1,215 | 720 | |||||

2020 | 555 | — | |||||

Total notional value of contracts outstanding | $ | 2,130 | $ | 1,905 | |||

Net unrealized (losses) gains included in accumulated other comprehensive income (loss), net of taxes | $ | (90 | ) | $ | 115 | ||

Upon settlement or maturity of the cash flow hedge contracts, we record the gains or losses, based on our designation at the commencement of the contract, with the related hedged Indian rupee denominated expense reported within cost of revenues and selling, general and administrative expenses. Hedge ineffectiveness was immaterial for all periods presented.

The following table provides information on the location and amounts of pre-tax gains and losses on our cash flow hedges for the three months ended September 30:

Change in Derivative Gains/Losses Recognized in Accumulated Other Comprehensive Income (Loss) (effective portion) | Location of Net Derivative Gains Reclassified from Accumulated Other Comprehensive Income (Loss) into Income (effective portion) | Net Gains Reclassified from Accumulated Other Comprehensive Income (Loss) into Income (effective portion) | |||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||||

(in millions) | |||||||||||||||||

Foreign exchange forward contracts – Designated as cash flow hedging instruments | $ | (96 | ) | $ | 6 | Cost of revenues | $ | 6 | $ | 29 | |||||||

Selling, general and administrative expenses | 1 | 5 | |||||||||||||||

Total | $ | 7 | $ | 34 | |||||||||||||

The following table provides information on the location and amounts of pre-tax gains and losses on our cash flow hedges for the nine months ended September 30:

Change in Derivative Gains/Losses Recognized in Accumulated Other Comprehensive Income (Loss) (effective portion) | Location of Net Derivative Gains Reclassified from Accumulated Other Comprehensive Income (Loss) into Income (effective portion) | Net Gains Reclassified from Accumulated Other Comprehensive Income (Loss) into Income (effective portion) | |||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||||

(in millions) | |||||||||||||||||

Foreign exchange forward contracts – Designated as cash flow hedging instruments | $ | (201 | ) | $ | 165 | Cost of revenues | $ | 54 | $ | 75 | |||||||

Selling, general and administrative expenses | 9 | 14 | |||||||||||||||

Total | $ | 63 | $ | 89 | |||||||||||||

The activity related to the change in net unrealized gains and losses on our cash flow hedges included in accumulated other comprehensive income (loss) is presented in Note 12.

23

Other Derivatives

We use foreign exchange forward contracts to provide an economic hedge against balance sheet exposures to certain monetary assets and liabilities denominated in currencies, primarily the Indian rupee, British pound and Euro, other than the functional currency of our foreign subsidiaries. We entered into a series of foreign exchange forward contracts that are scheduled to mature in 2018. Realized gains or losses and changes in the estimated fair value of these derivative financial instruments are recorded in the caption "Foreign currency exchange gains (losses), net" in our consolidated statements of operations.