Attached files

| file | filename |

|---|---|

| EX-32.2 - CERTIFICATION - Carbon Energy Corp | f10q0618ex32-2_carbonenergy.htm |

| EX-32.1 - CERTIFICATION - Carbon Energy Corp | f10q0618ex32-1_carbonenergy.htm |

| EX-31.2 - CERTIFICATION - Carbon Energy Corp | f10q0618ex31-2_carbonenergy.htm |

| EX-31.1 - CERTIFICATION - Carbon Energy Corp | f10q0618ex31-1_carbonenergy.htm |

| EX-10.2 - MEMBERSHIP INTEREST PURCHASE AGREEMENT - Carbon Energy Corp | f10q0618ex10-2_carbonenergy.htm |

| EX-10.1 - MEMBERSHIP INTEREST PURCHASE AGREEMENT - Carbon Energy Corp | f10q0618ex10-1_carbonenergy.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ Quarterly report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended June 30, 2018

or

☐ Transition report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ___________ to ____________

Commission File Number: 000-02040

| Carbon Energy Corporation |

| (Exact name of registrant as specified in its charter) |

| Delaware | 26-0818050 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) | |

| 1700 Broadway, Suite 1170, Denver, CO | 80290 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: (720) 407-7043

| (Former name, address and fiscal year, if changed since last report) |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

YES ☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Smaller reporting company | ☒ | ||

| Accelerated filer | ☐ | Emerging growth company | ☐ | ||

| Non-accelerated filer | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES ☐ NO ☒

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

At August 13, 2018, there were 7,700,619 issued and outstanding shares of the Company’s common stock, $0.01 par value.

Carbon Energy Corporation

TABLE OF CONTENTS

| Part I - FINANCIAL INFORMATION | |

| Item 1. Consolidated Financial Statements | 1 |

| Consolidated Balance Sheets (unaudited) | 1 |

| Consolidated Statements of Operations (unaudited) | 2 |

| Consolidated Statements of Stockholders’ Equity (unaudited) | 3 |

| Consolidated Statements of Cash Flows (unaudited) | 4 |

| Notes to the Consolidated Financial Statements (unaudited) | 5 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 32 |

| Item 4. Controls and Procedures | 44 |

| Part II - OTHER INFORMATION | |

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | 45 |

| Item 6. Exhibits | 45 |

PART I. FINANCIAL INFORMATION

CARBON ENERGY CORPORATION

Consolidated Balance Sheets

| June 30, | December 31, | |||||||

| (in thousands) | 2018 | 2017 | ||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 4,030 | $ | 1,650 | ||||

| Accounts receivable: | ||||||||

| Revenue | 4,713 | 2,206 | ||||||

| Trade receivable | 1,417 | - | ||||||

| Joint interest billings and other | 133 | 349 | ||||||

| Insurance receivable (Note 2) | 665 | 802 | ||||||

| Due from related parties | 1,158 | 2,075 | ||||||

| Commodity derivative asset | - | 215 | ||||||

| Prepaid expense, deposits and other current assets | 1,937 | 783 | ||||||

| Total current assets | 14,053 | 8,080 | ||||||

| Property and equipment (Note 4) | ||||||||

| Oil and gas properties, full cost method of accounting: | ||||||||

| Proved, net | 126,510 | 34,178 | ||||||

| Unproved | 3,577 | 1,947 | ||||||

| Other property and equipment, net | 2,134 | 737 | ||||||

| Total property and equipment, net | 132,221 | 36,862 | ||||||

| Investments in affiliates (Note 6) | 13,375 | 14,267 | ||||||

| Other long-term assets | 2,737 | 800 | ||||||

| Total assets | $ | 162,386 | $ | 60,009 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued liabilities (Note 11) | $ | 15,148 | $ | 11,218 | ||||

| Firm transportation contract obligations (Note 14) | 75 | 127 | ||||||

| Commodity derivative liability (Note 13) | 4,570 | - | ||||||

| Total current liabilities | 19,793 | 11,345 | ||||||

| Non-current liabilities: | ||||||||

| Firm transportation contract obligations (Note 14) | 123 | 134 | ||||||

| Production and property taxes payable | 550 | 520 | ||||||

| Warrant liability (Note 12) | - | 2,017 | ||||||

| Asset retirement obligations (Note 5) | 10,831 | 7,357 | ||||||

| Credit facility (Note 7) | 23,140 | 22,140 | ||||||

| Long-term debt | 78 | - | ||||||

| Credit facility-related party (Note 7) | 49,900 | - | ||||||

| Commodity derivative liability (Note 13) | 3,447 | - | ||||||

| Total non-current liabilities | 88,069 | 32,168 | ||||||

| Commitments (Note 14) | ||||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $0.01 par value; authorized 1,000,000 shares, 50,000 shares issued and outstanding at June 30, 2018 and no shares issued and outstanding at December 31, 2017 | 1 | - | ||||||

| Common stock, $0.01 par value; authorized 35,000,000 shares, 7,700,619 and 6,005,633 shares issued and outstanding at June 30, 2018 and December 31, 2017, respectively | 77 | 60 | ||||||

| Additional paid-in capital | 75,594 | 58,813 | ||||||

| Accumulated deficit | (42,424 | ) | (44,218 | ) | ||||

| Total Carbon stockholders’ equity | 33,247 | 14,655 | ||||||

| Non-controlling interests | 21,277 | 1,841 | ||||||

| Total stockholders’ equity | 54,524 | 16,496 | ||||||

| Total liabilities and stockholders’ equity | $ | 162,386 | $ | 60,009 | ||||

See accompanying notes to Consolidated Financial Statements.

| 1 |

CARBON ENERGY CORPORATION

Consolidated Statements of Operations

(Unaudited)

| Three

Months Ended June 30, | Six

Months Ended June 30, | |||||||||||||||

| (in thousands except per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

| Revenue: | ||||||||||||||||

| Natural gas sales | $ | 3,523 | $ | 4,023 | $ | 7,462 | $ | 8,017 | ||||||||

| Natural gas liquid sales | 550 | - | 713 | - | ||||||||||||

| Oil sales | 8,091 | 1,146 | 11,074 | 2,192 | ||||||||||||

| Commodity derivative gain (loss) | (6,022 | ) | 998 | (6,647 | ) | 3,141 | ||||||||||

| Other income | 6 | 10 | 19 | 20 | ||||||||||||

| Total revenue | 6,148 | 6,177 | 12,621 | 13,370 | ||||||||||||

| Expenses: | ||||||||||||||||

| Lease operating expenses | 3,970 | 1,501 | 6,058 | 2,706 | ||||||||||||

| Transportation and gathering costs | 1,498 | 525 | 2,353 | 1,015 | ||||||||||||

| Production and property taxes | 615 | 443 | 1,048 | 855 | ||||||||||||

| General and administrative | 2,542 | 1,748 | 5,491 | 3,494 | ||||||||||||

| General and administrative - related party reimbursement | (1,096 | ) | (225 | ) | (2,213 | ) | (300 | ) | ||||||||

| Depreciation, depletion and amortization | 1,979 | 662 | 3,471 | 1,234 | ||||||||||||

| Accretion of asset retirement obligations | 162 | 78 | 303 | 155 | ||||||||||||

| Total expenses | 9,670 | 4,732 | 16,511 | 9,159 | ||||||||||||

| Operating (loss) income | (3,522 | ) | 1,445 | (3,890 | ) | 4,211 | ||||||||||

| Other income and (expense): | ||||||||||||||||

| Interest expense | (1,201 | ) | (254 | ) | (2,203 | ) | (522 | ) | ||||||||

| Warrant derivative gain | - | 853 | 225 | 1,683 | ||||||||||||

| Equity investment loss | - | (7 | ) | - | - | |||||||||||

| Gain on derecognized equity investment in affiliate - Carbon California | - | - | 5,390 | - | ||||||||||||

| Investment in affiliates | 525 | - | 962 | - | ||||||||||||

| Total other (expense) income | (676 | ) | 592 | 4,374 | 1,161 | |||||||||||

| (Loss) income before income taxes | (4,198 | ) | 2,037 | 484 | 5,372 | |||||||||||

| Provision for income taxes | - | - | - | - | ||||||||||||

| Net (loss) income before non-controlling interests | (4,198 | ) | 2,037 | 484 | 5,372 | |||||||||||

| Net (loss) income attributable to non-controlling interests | (3,619 | ) | 33 | (2,505 | ) | 76 | ||||||||||

| Net (loss) income attributable to controlling interest | $ | (579 | ) | $ | 2,004 | $ | 2,989 | $ | 5,296 | |||||||

| Net income (loss) per common share: | ||||||||||||||||

| Basic | $ | (0.08 | ) | $ | 0.36 | $ | 0.41 | $ | 0.95 | |||||||

| Diluted | $ | (0.23 | ) | $ | 0.17 | $ | 0.20 | $ | 0.56 | |||||||

| Weighted average common shares outstanding: | ||||||||||||||||

| Basic | 7,693 | 5,620 | 7,346 | 5,554 | ||||||||||||

| Diluted | 7,693 | 6,588 | 7,662 | 6,458 | ||||||||||||

See accompanying notes to Consolidated Financial Statements.

| 2 |

CARBON ENERGY CORPORATION

Consolidated Statements of Stockholders’ Equity

(Unaudited)

(in thousands)

| Common Stock | Preferred Stock | Non- controlling | Accumulated | Total Stockholders' | ||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | APIC | interest | Deficit | Equity | |||||||||||||||||||||||||

| Balances, December 31, 2017 | 6,006 | 60 | - | - | 58,813 | 1,841 | (44,218 | ) | 16,496 | |||||||||||||||||||||||

| Stock based compensation | 39 | 1 | - | - | 482 | - | - | 483 | ||||||||||||||||||||||||

| Restricted shares : | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||

| Vested restricted stock | 20 | - | - | - | - | - | - | - | ||||||||||||||||||||||||

| Vested performance units | 108 | 1 | - | - | (1 | ) | - | - | - | |||||||||||||||||||||||

| Preferred share issuance | - | - | 50 | 1 | 4,999 | - | - | 5,000 | ||||||||||||||||||||||||

| Beneficial conversion feature | - | - | - | - | 1,125 | - | (1,125 | ) | - | |||||||||||||||||||||||

| Deemed dividend | - | - | - | - | 71 | - | (71 | ) | - | |||||||||||||||||||||||

| CCC warrant exercise - share issuance | 1,528 | 15 | - | - | 8,311 | 16,466 | - | 24,792 | ||||||||||||||||||||||||

| CCC warrant exercise - liability extinguishment | - | - | - | - | 1,792 | - | - | 1,792 | ||||||||||||||||||||||||

| Non-controlling interest contributions, net | - | - | - | - | - | 5,475 | - | 5,475 | ||||||||||||||||||||||||

| Step up in basis | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||

| Net income (loss) | - | - | - | - | - | (2,505 | ) | 2,989 | 484 | |||||||||||||||||||||||

| Balances, June 30, 2018 | 7,701 | $ | 77 | 50 | $ | 1 | $ | 75,594 | $ | 21,277 | $ | 42,424 | $ | 54,524 | ||||||||||||||||||

See accompanying notes to Consolidated Financial Statements.

| 3 |

CARBON ENERGY CORPORATION

Consolidated Statements of Cash Flows

(Unaudited)

| Six Months Ended | ||||||||

| June 30, | ||||||||

| (in thousands) | 2018 | 2017 | ||||||

| Cash flows from operating activities: | ||||||||

| Net income | $ | 484 | $ | 5,372 | ||||

| Items not involving cash: | ||||||||

| Depreciation, depletion and amortization | 3,471 | 1,234 | ||||||

| Accretion of asset retirement obligations | 303 | 155 | ||||||

| Unrealized commodity derivative loss (gain) | 5,587 | (3,023 | ) | |||||

| Warrant derivative gain | (225 | ) | (1,683 | ) | ||||

| Stock-based compensation expense | 483 | 539 | ||||||

| Equity investment income | (962 | ) | - | |||||

| (Gain) loss on derecognized equity investment in affiliate-Carbon California | (5,390 | ) | ||||||

| Amortization of debt issuance costs | 247 | - | ||||||

| Other | - | (72 | ) | |||||

| Net change in: | ||||||||

| Accounts receivable | (353 | ) | 1,331 | |||||

| Prepaid expenses, deposits and other current assets | 570 | (375 | ) | |||||

| Accounts payable, accrued liabilities, firm transportation contract obligations, and other long-term obligations | (2,600 | ) | (1,142 | ) | ||||

| Net cash provided by operating activities | 1,615 | 2,336 | ||||||

| Cash flows from investing activities: | ||||||||

| Development and acquisition of properties and equipment | (40,472 | ) | (1,182 | ) | ||||

| Cash received- Carbon California Acquisition | 275 | - | ||||||

| Other long-term assets | - | (15 | ) | |||||

| Investment in affiliates | - | (240 | ) | |||||

| Net cash used in investing activities | (40,197 | ) | (1,437 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Proceeds from credit facility | 31,502 | 600 | ||||||

| Proceeds from preferred shares | 5,000 | - | ||||||

| Payments on credit facility | (14 | ) | (1,300 | ) | ||||

| Payments of debt issuance costs | (511 | ) | ||||||

| Contributions from non-controlling interests | 5,000 | - | ||||||

| Distributions to non-controlling interests | (15 | ) | (43 | ) | ||||

| Net cash provided by (used in) financing activities | 40,962 | (743 | ) | |||||

| Net increase in cash and cash equivalents | 2,380 | 156 | ||||||

| Cash and cash equivalents, beginning of period | 1,650 | 858 | ||||||

| Cash and cash equivalents, end of period | $ | 4,030 | $ | 1,014 | ||||

See accompanying notes to Consolidated Financial Statements.

| 4 |

CARBON ENERGY CORPORATION

Notes to Consolidated Financial Statements

(Unaudited)

Note 1 - Organization

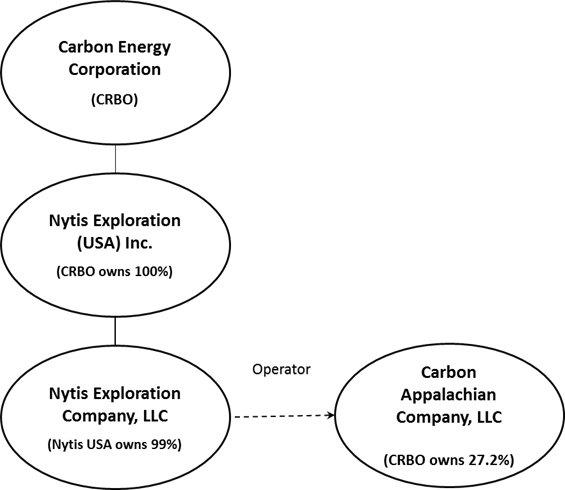

Carbon Energy Corporation, formerly known as Carbon Natural Gas Company, and its subsidiaries (referred to herein as “we”, “us”, the “Company” or “Carbon”) is an independent oil and gas company engaged in the exploration, development and production of oil and natural gas in the United States. The Company’s business is comprised of the assets and properties of Nytis Exploration (USA) Inc. (“Nytis USA”) and its subsidiary Nytis Exploration Company LLC (“Nytis LLC”) which conduct the Company’s operations in the Appalachian and Illinois Basins, Carbon California Operating Company, LLC (“CCOC”) and Carbon California Company, LLC (“Carbon California”) which conduct the Company’s operations in California, and the Company’s equity investment in Carbon Appalachian Company, LLC (“Carbon Appalachia”).

Appalachian and Illinois Basin Operations

In the Appalachian and Illinois Basins, Nytis LLC conducts our operations. The following illustrates this relationship as of June 30, 2018.

| 5 |

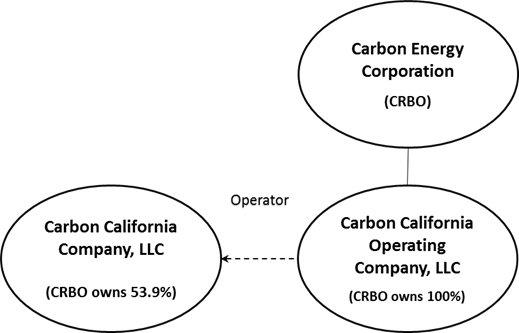

Ventura Basin Operations

In California, CCOC conducts our operations. On February 1, 2018, an entity managed by Yorktown Partners, LLC (“Yorktown”) exercised a warrant it held to purchase shares of our common stock at an exercise price of $7.20 per share (the “California Warrant”), resulting in the issuance of 1,527,778 shares of our common stock. In exchange, we received Yorktown’s Class A Units of Carbon California representing approximately 46.96% of the then outstanding Class A Units of Carbon California (a profits interest of approximately 38.59%). After giving effect to the exercise on February 1, 2018, we owned 56.4% of the voting and profits interests of Carbon California and Prudential Capital Energy Partners, L.P. (“Prudential”) owned 43.6%. On May 1, 2018, Carbon California closed the Seneca Acquisition. Following the exercise of the California Warrant by Yorktown and the Seneca Acquisition, we own 53.9% of the voting and profits interests, and Prudential owns the remainder of the interest, in Carbon California. As of February 1, 2018, we consolidate Carbon California for financial reporting purposes.

Note 2 - Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information. Accordingly, they do not include all the information and footnotes required by GAAP for complete financial statements. In the opinion of management, the accompanying unaudited condensed consolidated financial statements include all adjustments (consisting of normal and recurring accruals) considered necessary to present fairly our financial position as of June 30, 2018, and our results of operations and cash flows for the three and six months ended June 30, 2018 and 2017. Operating results for the three and six months ended June 30, 2018, are not necessarily indicative of the results that may be expected for the full year because of the impact of fluctuations in prices received for oil and natural gas, natural production declines, the uncertainty of exploration and development drilling results and other factors. The unaudited condensed consolidated financial statements and related notes included in this Quarterly Report on Form 10-Q should be read in conjunction with our consolidated financial statements and related notes included in our Annual Report on Form 10-K for the year ended December 31, 2017. Except as disclosed herein, there have been no material changes to the information disclosed in the notes to the consolidated financial statements included in our 2017 Annual Report on Form 10-K.

Principles of Consolidation

The unaudited condensed consolidated financial statements include the accounts of Carbon, CCOC, Carbon California and Nytis USA and its consolidated subsidiary, Nytis LLC. Carbon owns 100% of Nytis USA and CCOC. Nytis USA owns approximately 99% of Nytis LLC. Carbon owns 53.9% of Carbon California.

Nytis LLC also holds an interest in 64 oil and gas partnerships. For partnerships where we have a controlling interest, the partnerships are consolidated. We are currently consolidating, on a pro-rata basis, 47 partnerships. In these instances, we reflect the non-controlling ownership interest in partnerships and subsidiaries as non-controlling interests on our unaudited consolidated statements of operations and reflect the non-controlling ownership interests in the net assets of the partnerships as non-controlling interests within stockholders’ equity on our unaudited consolidated balance sheet. All significant intercompany accounts and transactions have been eliminated.

| 6 |

In accordance with established practice in the oil and gas industry our unaudited condensed consolidated financial statements also include our pro-rata share of assets, liabilities, income, lease operating costs and general and administrative expenses of the oil and gas partnerships in which we have a non-controlling interest.

Non-majority owned investments that do not meet the criteria for pro-rata consolidation are accounted for using the equity method when we have the ability to significantly influence the operating decisions of the investee. When we do not have the ability to significantly influence the operating decisions of an investee, the cost method is used. All transactions, if any, with investees have been eliminated in the accompanying unaudited condensed consolidated financial statements.

Effective February 1, 2018, Yorktown exercised the California Warrant, which resulted in us acquiring Yorktown’s ownership interest in Carbon California in exchange for shares of our common stock. On May 1, 2018, Carbon California closed the Seneca Acquisition. Following the exercise of the California Warrant by Yorktown and the Seneca Acquisition, we own 53.9%, of the voting and profits interests, and Prudential owns the remainder of the interest, in Carbon California.

Insurance Receivable

Insurance receivable is comprised of an insurance receivable for the loss of property as a result of wildfires that impacted Carbon California in December 2017. The Company filed claims with its insurance provider and is in receipt of partial funds associated with the claims as of June 30, 2018. Therefore, the Company has determined the receivable is collectible and is included in insurance receivable on the unaudited consolidated balance sheets.

Long-term Assets

Long-term assets are comprised of debt issuance costs, bonds, and fees associated with a registration statement for a possible equity raise. We have recorded debt issuance costs and amortize the balance over the life of the loan. As of June 30, 2018, we have approximately $1.0 million of deferred financing costs associated with our credit facility and Carbon California’s Senior Revolving Notes within long-term assets. See note 7. As of June 30, 2018, we have incurred approximately $1.5 million for the outside professional services in conjunction with the completion of a registration statement for a possible equity raise. We will continue to accumulate deferred financing costs until the completion of the registration statement and a successful equity raise. If the raise is unsuccessful, the amount will be immediately expensed.

Investments in Affiliates

Investments in non-consolidated affiliates are accounted for under either the cost or equity method of accounting, as appropriate. The cost method of accounting is generally used for investments in affiliates in which we have has less than 20% of the voting interests of a corporate affiliate or less than a 3% to 5% interest of a partnership or limited liability company and do not have significant influence. Investments in non-consolidated affiliates, accounted for using the cost method of accounting, are recorded at cost and impairment assessments for each investment are made annually to determine if a decline in the fair value of the investment, other than temporary, has occurred. A permanent impairment is recognized if a decline in the fair value occurs.

If we hold between 20% and 50% of the voting interest in non-consolidated corporate affiliates or generally greater than a 3% to 5% interest of a partnership or limited liability company and can exert significant influence or control (e.g., through our influence with a seat on the board of directors or management of operations), the equity method of accounting is generally used to account for the investment. Equity method investments will increase or decrease by our share of the affiliate’s profits or losses and such profits or losses are recognized in our unaudited consolidated statements of operations. For our equity method investment in Carbon Appalachia, we use the hypothetical liquidation at book value method to recognize our share of the affiliate’s profits or losses. We review equity method investments for impairment whenever events or changes in circumstances indicate that an other than temporary decline in value has occurred.

Related Party Transactions

Management Reimbursements

In our role as manager of Carbon California and Carbon Appalachia, we receive management reimbursements. We received approximately $750,000 and $1.5 million for the three and six months ended June 30, 2018, from Carbon Appalachia, and $50,000 for the one month ended January 31, 2018, from Carbon California. These reimbursements are included in general and administrative - related party reimbursement on our unaudited consolidated statements of operations. Effective February 1, 2018, the management reimbursements received from Carbon California are eliminated at consolidation. This elimination includes $350,000 for the period February 1, 2018, through June 30, 2018.

In addition to the management reimbursements, approximately $298,000 and $595,000 in general and administrative expenses were reimbursed for the three and six months ended June 30, 2018, from Carbon Appalachia, and $14,000 for the one month ended January 31, 2018, by Carbon California. General and administrative expenses reimbursed by Carbon California and eliminated in consolidation were approximately $42,000 for the period February 1, 2018, through June 30, 2018.

| 7 |

Operating Reimbursements

In our role as operator of Carbon California and Carbon Appalachia, we receive reimbursements of operating expenses. These expenses are recorded directly to receivable – due from related party on our unaudited consolidated balance sheets and are therefore not included in our operating expenses on our unaudited consolidated statements of operations.

Carbon California Credit Facilities

The credit facilities of Carbon California, including the Senior Revolving Notes, Carbon California Notes and Carbon California 2018 Subordinated Notes (all defined below), are held by Prudential or its affiliates. See note 7.

Preferred Stock

In April 2018, we issued 50,000 shares of Preferred Stock to Yorktown. See note 9.

Old Ironsides Membership Interest Purchase Agreement

On May 4, 2018, we entered into a Membership Interest Purchase Agreement with Old Ironsides. See note 6.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to makes estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. There have been no changes in our critical accounting estimates from those that were disclosed in the 2017 Annual Report on Form 10-K. Actual results could differ from these estimates.

Earnings (Loss) Per Common Share

Basic earnings per common share is computed by dividing the net income (loss) attributable to common stockholders for the period by the weighted average number of common shares outstanding during the period. The shares of restricted common stock granted to our officers, directors and employees are included in the computation of basic net income per share only after the shares become fully vested. Diluted earnings per common share includes both the vested and unvested shares of restricted stock and the potential dilution that could occur upon exercise of warrants to acquire common stock computed using the treasury stock method, which assumes that the increase in the number of shares is reduced by the number of shares which could have been repurchased by us with the proceeds from the exercise of warrants (which were assumed to have been made at the average market price of the common shares during the reporting period). We issued 50,000 shares of Series B Convertible Preferred Stock, par value $0.01 per share (the “Preferred Stock”), and the difference between the carrying amount of the Preferred Stock in equity and the fair value of the Preferred Stock) is treated as a dividend for purposes of calculating earnings per common share. The Preferred Stock deemed dividend could potentially dilute basic earnings per common share in the future.

In periods when we report a net loss, all shares of restricted stock are excluded from the calculation of diluted weighted average shares outstanding because of its anti-dilutive effect on loss per share. As a result, all restricted stock is excluded from the calculation of diluted earnings per common share for the three months ended June 30, 2018. Potentially dilutive securities (restricted stock awards) included in the calculation of diluted earnings per share totaled 275,913 for the three months ended June 30, 2018. Potentially dilutive securities that are anti-dilutive totaled 275,913 for the three months ended June 30, 2018 and 967,525 for the three months ended June 30, 2017. The dilutive units did not have a material impact on our earnings per common share calculations for any of the periods presented.

The following table sets forth the calculation of basic and diluted income per share:

| Three months

ended June 30, | Six months

ended June 30, | |||||||||||||||

| (in thousands except per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

| Net income | $ | (579 | ) | $ | 2,004 | $ | 2,989 | $ | 5,296 | |||||||

| Less: warrant derivative gain | - | (853 | ) | (225 | ) | (1,683 | ) | |||||||||

| Less: beneficial conversion feature | (1,125 | ) | - | (1,125 | ) | - | ||||||||||

| Less: deemed dividend for convertible preferred shares | (71 | ) | - | (71 | ) | - | ||||||||||

| Diluted net (loss) income | $ | (1,775 | ) | $ | 1,151 | $ | 1,568 | $ | 3,613 | |||||||

| Basic weighted-average common shares outstanding during the period | 7,693 | 5,620 | 7,346 | 5,554 | ||||||||||||

| Add dilutive effects of warrants and non-vested shares of restricted stock | - | 968 | 316 | 904 | ||||||||||||

| Diluted weighted-average common shares outstanding during the period | 7,693 | 6,588 | 7,662 | 6,458 | ||||||||||||

| Basic net (loss) income per common share | $ | (0.08 | ) | $ | 0.36 | $ | 0.41 | $ | 0.95 | |||||||

| Diluted net (loss) income per common share | $ | (0.23 | ) | $ | 0.17 | $ | 0.20 | $ | 0.56 | |||||||

| 8 |

Recently Adopted Accounting Pronouncement

In May 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standard Update (“ASU”) 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”), which establishes a comprehensive new revenue recognition standard designed to depict the transfer of goods or services to a customer in an amount that reflects the consideration the entity expects to receive in exchange for those goods or services. In March 2016, the FASB released certain implementation guidance through ASU 2016-08 (collectively with ASU 2014-09, the “Revenue ASUs”) to clarify principal versus agent considerations. The Revenue ASUs allow for the use of either the full or modified retrospective transition method, and the standard is effective for annual reporting periods beginning after December 15, 2017 including interim periods within that period, with early adoption permitted for annual reporting periods beginning after December 15, 2016. We adopted the guidance using the modified retrospective method with the effective date of January 1, 2018. We did not record a cumulative-effect adjustment to the opening balance of retained earnings as no adjustment was necessary. The adoption of the Revenue ASUs did not impact net income or cash flows. See note 10 for the new disclosures required by the Revenue ASUs.

Recently Issued Accounting Pronouncements

In February 2016, the FASB issued ASU 2016-02, “Leases (Topic 842)” (“ASU 2016-02”), which establishes a comprehensive new lease standard designed to increase transparency and comparability among organizations by recognizing lease assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. In transition, lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach. The modified retrospective approach includes a number of optional practical expedients that entities may elect to apply. An entity that elects to apply the practical expedients will, in effect, continue to account for leases that commence before the effective date in accordance with previous GAAP standards. ASU 2016-02 is effective for public companies for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. We are currently evaluating the impact of the adoption of this standard on our financial statements.

There were various updates recently issued by the FASB, most of which represented technical corrections to the accounting literature or application to specific industries and are not expected to a have a material impact on our reported financial position, results of operations, or cash flows.

Note 3 - Acquisitions and Divestitures

Acquisition of Majority Control of Carbon California

Carbon California was formed in 2016 by us and entities managed by Yorktown and Prudential to acquire producing assets in the Ventura Basin of California.

In connection with the entry into the limited liability company agreement of Carbon California, we received Class B Units and issued to Yorktown the California Warrant exercisable for shares of our common stock. The exercise price for the California Warrant was payable exclusively with Class A Units of Carbon California held by Yorktown and the number of shares of our common stock for which the California Warrant was exercisable was determined, as of the time of exercise, by dividing (a) the aggregate unreturned capital of Yorktown’s Class A Units of Carbon California by (b) the exercise price. The California Warrant had a term of seven years and included certain standard registration rights with respect to the shares of our common stock issuable upon exercise of the California Warrant.

The issuance of the Class B Units and the California Warrant were in contemplation of each other, and under non-monetary related party guidance, we accounted for the California Warrant, at issuance, based on the fair value of the California Warrant as of the date of grant (February 15, 2017) and recorded a long-term warrant liability with an associated offset to Additional Paid in Capital (“APIC”). Future changes to the fair value of the California Warrant are recognized in earnings. We accounted for the fair value of the Class B Units at their estimated fair value at the date of grant, which became our investment in Carbon California with an offsetting entry to APIC. Additionally, we accounted for our 17.81% profits interest in Carbon California as an equity method investment until January 31, 2018.

| 9 |

On February 1, 2018, Yorktown exercised the California Warrant resulting in the issuance of 1,527,778 shares of our common stock in exchange for Yorktown’s Class A Units of Carbon California representing approximately 46.96% of the outstanding Class A Units of Carbon California (a profits interest of approximately 38.59%). After giving effect to the exercise on February 1, 2018, we owned 56.4% of the voting and profits interests of Carbon California. On May 1, 2018, Carbon California closed the Seneca Acquisition. Following the exercise of the California Warrant by Yorktown and the Seneca Acquisition, we own 53.9% of the voting and profits interests, and Prudential owns the remainder of the interest, in Carbon California.

The exercise of the California Warrant and the acquisition of the additional ownership interest is accounted for as a step acquisition in which we obtained control in accordance with ASC 805, Business Combinations (“ASC 805”) (referred to herein as the “Carbon California Acquisition”). We recognized 100% of the identifiable assets acquired, liabilities assumed and the non-controlling interest at their respective fair value as of the date of the acquisition. We exchanged 1,527,778 common shares at a fair value of approximately $8.3 million ($5.45 per share), for 11,000 Class A Units of Carbon California, representing a 38.59% ownership interest in Carbon California. We followed the fair value method to allocate the consideration transferred to the identifiable net assets acquired and non-controlling interest (“NCI”) on a preliminary basis as follows:

| Amount

(in thousands) | ||||

| Fair value of Carbon common shares transferred as consideration | $ | 8,326 | ||

| Fair value of NCI | 16,466 | |||

| Fair value of previously held interest | 7,244 | |||

| Fair value of business acquired | $ | 32,036 | ||

Assets acquired and liabilities assumed

| Amount

(in thousands) | ||||

| Cash | $ | 275 | ||

| Accounts receivable: | ||||

| Joint interest billings and other | 690 | |||

| Receivable - related party | 1,610 | |||

| Prepaid expense, deposits, and other current assets | 1,723 | |||

| Oil and gas properties: | ||||

| Proved | 56,477 | |||

| Unproved | 1,495 | |||

| Other property and equipment, net | 877 | |||

| Other long-term assets | 475 | |||

| Accounts payable and accrued liabilities | (6,054 | ) | ||

| Commodity derivative liability - short-term | (916 | ) | ||

| Commodity derivative liability - long-term | (1,729 | ) | ||

| Asset retirement obligations - short-term | (384 | ) | ||

| Asset retirement obligations - long-term | (2,537 | ) | ||

| Subordinated Notes, related party, net | (8,874 | ) | ||

| Senior Revolving Notes, related party | (11,000 | ) | ||

| Notes payable | (92 | ) | ||

| Total net assets acquired | $ | 32,036 | ||

The preliminary fair value of the assets acquired and liabilities assumed were determined using various valuation techniques, including an income approach. The fair value measurements were primarily based on significant inputs that are not directly observable in the market and are considered Level 3 under the fair value measurements and disclosure framework.

On the date of the acquisition, we derecognized our equity investment in Carbon California and recognized a gain of approximately $5.4 million based on the fair value of our previously held interest compared to its carrying value.

For assets and liabilities accounted for as business combinations, including the Carbon California Acquisition, to determine the fair value of the assets acquired, the Company primarily used the income approach and made market assumptions as to projections of estimated quantities of oil and natural gas reserves, future production rates, future commodity prices including price differentials as of the date of closing, future operating and development costs, a market participant weighted average cost of capital, and the condition of vehicles and equipment. The determination of the fair value of the accounts payable and accrued liabilities assumed required significant judgement, including estimates relating to production assets.

| 10 |

Seneca Acquisition

In October 2017, Carbon California signed a Purchase and Sale Agreement to acquire 309 operated and one non-operated oil wells covering approximately 5,700 gross acres (5,500 net), and fee interests in and to certain lands, situated in the Ventura Basin, together with associated wells, pipelines, facilities, equipment and other property rights for a purchase price of $43.0 million, subject to customary and standard purchase price adjustments, from Seneca Resources Corporation (the “Seneca Acquisition”). We contributed approximately $5.0 million to Carbon California to fund our portion of the purchase price, through the $5.0 Preferred Stock issuance, with Prudential contributing $5.0 million. Carbon California funded the remaining purchase price from cash, increased borrowings under the Senior Revolving Notes and $3.0 million in proceeds from the issuance of Senior Subordinated Notes. The Seneca Acquisition closed on May 1, 2018 with an effective date as of October 1, 2017.

Utilizing the assistance of third-party valuation specialists, we considered various factors in our estimate of fair value of the acquired assets including (i) reserves, (ii) production rates, (iii) future operating and development costs, (iv) future commodity prices, including price differentials, (v) future cash flows, and (vi) working conditions and expected lives of vehicles and equipment.

We determined that substantially all of the fair value of the assets acquired related to proved oil and gas properties and, as such the Seneca Acquisition does not meet the definition of a business. Therefore, we have accounted for the transaction as an asset acquisition and allocated the purchase price based on the relative fair value of the assets acquired.

The fair value of the production assets were determined using the income approach using Level 3 inputs according the ASC 820, Fair Value, hierarchy. The fair value of the other assets was determined using the market approach using Level 3 inputs. The determination of the fair value of the oil and gas and other property and equipment acquired and accounts payable and accrued liability assumed, required significant judgement, including estimates relating to the production assets and the other transaction costs. We recorded $639,000 in ARO, and $330,000 in assumed liabilities in connection with the Seneca Acquisition. We incurred transaction costs related to the Seneca Acquisition in the amount of $318,000. As this acquisition was determined to be an asset acquisition, transaction costs were capitalized to oil and gas properties- proved, net on the balance sheet. Below is the summary of the assets acquired (in thousands):

| Identifiable assets acquired: | ||||

| Assets: | ||||

| Proved oil and gas properties | $ | 37,386 | ||

| Unproved oil and gas properties | 100 | |||

| Other property and equipment | 545 | |||

| Intangible assets | 300 | |||

| Total identified assets | $ | 38,331 | ||

Consolidation of Carbon California and Seneca Acquisition Unaudited Pro Forma Results of Operations

Below are unaudited consolidated results of operations for the three and six months ended June 30, 2018 and 2017, as though the Carbon California Acquisition and the Seneca Acquisition had been completed as of January 1, 2017. The Carbon California Acquisition closed February 1, 2018, and the Seneca Acquisition closed May 1, 2018, and accordingly, our unaudited consolidated statements of operations for the quarter ended June 30, 2018, includes Carbon California’s results of operations for the quarter, and the Seneca Acquisition results of operations for the period May 1, 2018 through June 30, 2018.

| Unaudited

Pro Forma Consolidated Results For Three Months Ended June 30, | Unaudited

Pro Forma Consolidated Results For Six Months Ended June 30, | |||||||||||||||

| (in thousands, except per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

| Revenue | $ | 8,180 | $ | 14,092 | $ | 20,283 | $ | 27,054 | ||||||||

| Net (loss) income before non-controlling interests | (3,013 | ) | 4,730 | 4,256 | 8,704 | |||||||||||

| Net (loss) income attributable to non-controlling interests | (3,619 | ) | 33 | (2,504 | ) | 76 | ||||||||||

| Net (loss) income attributable to controlling interests | $ | 607 | $ | 4,697 | $ | 7,739 | $ | 8,628 | ||||||||

| Net income per share (basic) | $ | 0.27 | $ | 0.84 | $ | 1.01 | $ | 1.54 | ||||||||

| Net income per share (diluted) | $ | 0.09 | $ | 0.58 | $ | 0.84 | $ | 1.18 | ||||||||

| 11 |

Note 4 - Property and Equipment

Net property and equipment as of June 30, 2018 and December 31, 2017, consists of the following:

| (in thousands) | June 30, 2018 | December 31, 2017 | ||||||

| Oil and gas properties: | ||||||||

| Proved oil and gas properties | $ | 211,602 | $ | 114,893 | ||||

| Unproved properties not subject to depletion | 3,577 | 1,947 | ||||||

| Accumulated depreciation, depletion, amortization and impairment | (85,092 | ) | (80,715 | ) | ||||

| Net oil and gas properties | 130,087 | 36,125 | ||||||

| Furniture and fixtures, computer hardware and software, and other equipment | 3,631 | 1,758 | ||||||

| Accumulated depreciation and amortization | (1,497 | ) | (1,021 | ) | ||||

| Net other property and equipment | 2,134 | 737 | ||||||

| Total net property and equipment | $ | 132,221 | $ | 36,862 | ||||

We had approximately $3.5 million and $1.9 million, at June 30, 2018 and December 31, 2017, respectively, of unproved oil and gas properties not subject to depletion. At June 30, 2018 and December 31, 2017, our unproved properties consist principally of leasehold acquisition costs in the following areas:

| (in thousands) | June

30, 2018 | December 31,

2017 | ||||||

| Ventura Basin | $ | 1,595 | $ | - | ||||

| Illinois Basin: | ||||||||

| Indiana | 432 | 432 | ||||||

| Illinois | 136 | 136 | ||||||

| Appalachian Basin: | ||||||||

| Kentucky | 919 | 915 | ||||||

| Ohio | 66 | 66 | ||||||

| West Virginia | 429 | 398 | ||||||

| Total unproved properties not subject to depletion | $ | 3,577 | $ | 1,947 | ||||

During the three and six months ended June 30, 2018 and 2017, there were no expiring leasehold costs that were reclassified into proved property. The excluded properties are assessed for impairment at least annually. Subject to industry conditions, evaluations of most of these properties and the inclusion of their costs in amortized capital costs is expected to be completed within five years.

We capitalized overhead applicable to acquisition, development and exploration activities of approximately $119,000 and $190,000 for the three and six months ended June 30, 2018, respectively. For the three and six months ended June 30, 2017, we capitalized overhead applicable to acquisition, development, and exploration activities of approximately $56,000 and $131,000, respectively.

| 12 |

Depletion expense related to oil and gas properties for the three and six months ended June 30, 2018 was approximately $1.8 million, or $0.77 per Mcfe, and $3.1 million, or $0.80 per Mcfe, respectively. For the three and six months ended June 30, 2017, depletion expense was approximately $539,000, or $0.40 per Mcfe, and $1.1 million, or $0.41 per Mcfe, respectively.

Note 5 - Asset Retirement Obligation

Our asset retirement obligations (“ARO”) relate to future costs associated with the plugging and abandonment of oil and gas wells, removal of equipment and facilities from leased acreage and returning such land to its original condition. The fair value of a liability for an ARO is recorded in the period in which it is incurred or acquired, and the cost of such liability is recorded as an increase in the carrying amount of the related long-lived asset by the same amount. The liability is accreted each period and the capitalized cost is depleted on a units-of-production basis as part of the full cost pool. Revisions to estimated AROs result in adjustments to the related capitalized asset and corresponding liability.

The estimated ARO liability is based on estimated economic lives, estimates as to the cost to abandon the wells in the future, and federal and state regulatory requirements. The liability is discounted using a credit-adjusted risk-free rate estimated at the time the liability is incurred or acquired or increased as a result of a reassessment of expected cash flows and assumptions inherent in the estimation of the liability. Upward revisions to the liability could occur due to changes in estimated abandonment costs or well economic lives, or if federal or state regulators enact new requirements regarding the abandonment of wells. AROs are valued utilizing Level 3 fair value measurement inputs (see note 12).

The following table is a reconciliation of the ARO:

| Six

Months Ended June 30, | ||||||||

| (in thousands) | 2018 | 2017 | ||||||

| Balance at beginning of period | $ | 7,737 | $ | 5,120 | ||||

| Accretion expense | 303 | 155 | ||||||

| Additions from Carbon California Company, LLC | 2,921 | - | ||||||

| Additions from Seneca Acquisition | 639 | - | ||||||

| Additions during period | - | 5 | ||||||

| 11,600 | 5,280 | |||||||

| Less: ARO recognized as a current liability | (769 | ) | (183 | ) | ||||

| Balance at end of period | $ | 10,831 | $ | 5,097 | ||||

Note 6 - Investments in Affiliates

Carbon California

Carbon California was formed in 2016 by us and entities managed by Yorktown and Prudential to acquire producing assets in the Ventura Basin in California. On February 15, 2017, we, Yorktown and Prudential entered into a limited liability company agreement (the “Carbon California LLC Agreement”) of Carbon California, a Delaware limited liability company.

Prior to February 1, 2018, we held 17.81% of the voting and profits interests, Yorktown held 38.59% of the voting and profits interests and Prudential held 43.59% of the voting and profits interests in Carbon California. On February 1, 2018, Yorktown exercised the California Warrant, pursuant to which Yorktown obtained additional shares of common stock in us in exchange for the transfer and assignment by Yorktown of all its rights in Carbon California. Following the exercise of the California Warrant by Yorktown, we owned 56.4% of the voting and profits interests, and Prudential held the remainder of the interests, in Carbon California. On May 1, 2018, Carbon California closed the Seneca Acquisition. Following the exercise of the California Warrant by Yorktown and the Seneca Acquisition, we own 53.9% of the voting and profits interests, and Prudential owns the remainder of the interests, in Carbon California. We consolidate Carbon California for financial reporting purposes.

On February 15, 2017, Carbon California (i) issued and sold Class A Units to Yorktown and Prudential for an aggregate cash consideration of $22.0 million, (ii) entered into a Note Purchase Agreement (the “Note Purchase Agreement”) with Prudential Legacy Insurance Company of New Jersey and Prudential Insurance Company of America for the issuance and sale of up to $25.0 million of Senior Secured Revolving Notes (the “Senior Revolving Notes”) due February 15, 2022 and (iii) entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with Prudential for the issuance and sale of $10.0 million of Senior Subordinated Notes (the “Subordinated Notes”) due February 15, 2024. We are not a guarantor of the Senior Revolving Notes or the Subordinate Notes.

| 13 |

The closing of the Note Purchase Agreement and the Securities Purchase Agreement on February 15, 2017, resulted in the sale and issuance by Carbon California of (i) Senior Revolving Notes in the principal amount of $10.0 million and (ii) Subordinated Notes in the original principal amount of $10.0 million. The maximum principal amount available under the Senior Revolving Notes is based upon the borrowing base attributable to Carbon California’s proved oil and gas reserves which is to be determined at least semi-annually. As of June 30, 2018, the borrowing base was $41.0 million, of which $38.5 million was outstanding.

Net proceeds from the offering transaction were used by Carbon California to complete the acquisitions of oil and gas assets in the Ventura Basin of California, which acquisitions also closed on February 15, 2017. The remainder of the net proceeds were used to fund field development projects, to fund a future complementary acquisition and for general working capital purposes of Carbon California.

For the period February 15, 2017 (inception) through January 31, 2018, based on our 17.8% interest in Carbon California, our ability to appoint a member to the board of directors and our role of manager of Carbon California, we accounted for our investment in Carbon California under the equity method of accounting as we believed we exerted significant influence. We used the Hypothetical Liquidation at Book Value Method (“HLBV”) to determine our share of profits or losses in Carbon California and adjusted the carrying value of our investment accordingly. The HLBV is a balance-sheet approach that calculates the amount each member of Carbon California would have received if Carbon California were liquidated at book value at the end of each measurement period. The change in the allocated amount to each member during the period represents the income or loss allocated to that member. In the event of liquidation of Carbon California, to the extent that Carbon California has net income, available proceeds are first distributed to members holding Class B units and any remaining proceeds are then distributed to members holding Class A Units. For the period February 15, 2017 (inception) through January 31, 2018, Carbon California incurred a net loss of which our share (as a holder of Class B Units for that period) was zero.

In connection with our entry into the Carbon California LLC Agreement, we received the aforementioned Class B Units and issued to Yorktown the California Warrant. The exercise price for the California Warrant was payable exclusively with Class A Units of Carbon California held by Yorktown and the number of shares of our common stock for which the California Warrant was exercisable was determined, as of the time of exercise, by dividing (a) the aggregate unreturned capital of Yorktown’s Class A Units of Carbon California by (b) the exercise price. The California Warrant had a term of seven years and included certain standard registration rights with respect to the shares of our common stock issuable upon exercise of the California Warrant. On February 1, 2018, Yorktown exercised the California Warrant. As a result of the warrant exercise, Carbon holds 11,000 Class A Units of Carbon California and all of the Class B units, resulting in an aggregate Sharing Percentage of 56.4%. Effective February 1, 2018, the Company consolidates Carbon California in its unaudited condensed consolidated financial statements.

On May 1, 2018, Carbon California entered into an agreement with Prudential Capital Energy Partners, L.P. for the issuance and sale of $3.0 million of unsecured notes due February 15, 2024, bearing interest of 12% per annum (the “Carbon California 2018 Subordinated Notes”). Prudential received 585 Class A Units, representing an approximately 2% additional sharing percentage, for the issuance of the Carbon California 2018 Subordinated Notes. Carbon California valued this unit issuance based on the relative fair value by valuing the units at $1,000 per unit and aggregating the amount with the outstanding Carbon California 2018 Subordinated Notes of $3.0 million. The Company then allocated the non-cash value of the units of approximately $490,000, which was recorded as a discount to the Carbon California 2018 Subordinated Notes. As of June 30, 2018, Carbon California had an outstanding discount of $482,000 associated with these notes, which is presented net of the Carbon California 2018 Subordinated Notes within Credit facility-related party on the unaudited consolidated balance sheets. As of June 30, 2018, the Company has $58,000 of deferred costs offsetting the Carbon California 2018 Subordinated Notes.

Carbon Appalachia

Carbon Appalachia was formed in 2016 by us, Yorktown and entities managed by Old Ironsides Energy LLC (“Old Ironsides”) to acquire producing assets in the Appalachian Basin in Kentucky, Tennessee, Virginia and West Virginia.

Outlined below is a summary of (i) our contributions, (ii) our resulting percentage of Class A unit ownership and iii) our overall resulting Sharing Percentage of Carbon Appalachia after giving effect to the Class C Unit ownership. Holders of units within each class of units participate in profit or losses and distributions according to their proportionate share of each class of units (“Sharing Percentage”). Each contribution and its use are described in summary following the table.

| Timing | Capital Contribution | Resulting

Class A Units (%) | Resulting

Sharing % | |||||||

| April 2017 | $0.24 million | 2.00 | % | 2.98 | % | |||||

| August 2017 | $3.71 million | 15.20 | % | 16.04 | % | |||||

| September 2017 | $2.92 million | 18.55 | % | 19.37 | % | |||||

| November 2017 | Warrant exercise | 26.50 | % | 27.24 | % | |||||

| 14 |

On April 3, 2017, we, Yorktown and Old Ironsides, entered in to a limited liability company agreement (the “Carbon Appalachia LLC Agreement”), with an initial equity commitment of $100.0 million, of which $37.0 million has been contributed as of June 30, 2018.

Pursuant to the Carbon Appalachia LLC Agreement, we acquired a 2.0% interest in Carbon Appalachia for $240,000 of Class A Units associated with our initial equity commitment of $2.0 million. We also have the ability to earn up to an additional 14.7% of Carbon Appalachia distributions (represented by Class B Units) after certain return thresholds to the holders of Class A Units are met. The Class B Units were acquired for no cash consideration.

In addition, we acquired a 1.0% interest represented by Class C Units which were obtained in connection with the contribution to Carbon Appalachia of a portion of our working interest in undeveloped properties in Tennessee. If Carbon Appalachia agrees to drill horizontal Chattanooga Shale wells on these properties, it will pay 100% of the cost of drilling and completion of the first 20 wells to earn a 75% working interest in such properties. We, through our subsidiary, Nytis LLC, will retain a 25% working interest in the properties. There was no activity associated with these properties in 2017 nor during the first six months of 2018.

In 2017, Carbon Appalachia Enterprises, LLC, formerly known as Carbon Tennessee Company, LLC (“CAE”), a subsidiary of Carbon Appalachia, entered into a 4-year $100.0 million (with $1.5 million sublimit for letters of credit) senior secured asset-based revolving credit facility with LegacyTexas Bank with an initial borrowing base of $10.0 million (the “CAE Credit Facility”).

The CAE Credit Facility borrowing base was adjusted for acquisitions completed in 2017. Most recently, on April 30, 2018, the CAE Credit Facility was amended, which increased the borrowing base to $70.0 million with redeterminations as of April 1 and October 1 each year. As of June 30, 2018, there was approximately $38.0 million outstanding under the CAE Credit Facility.

The CAE Credit Facility is guaranteed by each of CAE’s existing and future direct or indirect subsidiaries (subject to certain exceptions). CAE’s obligations and those of CAE’s subsidiary guarantors under the CAE Credit Facility are secured by essentially all of CAE’s tangible and intangible personal and real property (subject to certain exclusions).

Interest is payable quarterly and accrues on borrowings under the CAE Credit Facility at a rate per annum equal to either (i) the base rate plus an applicable margin between 0.00% and 1.00% or (ii) the Adjusted LIBOR rate plus an applicable margin between 3.00% and 4.00% at our option. The actual margin percentage is dependent on the CAE Credit Facility utilization percentage. CAE is obligated to pay certain fees and expenses in connection with the CAE Credit Facility, including a commitment fee for any unused amounts of 0.50%.

The CAE Credit Facility contains affirmative and negative covenants that, among other things, limit CAE’s ability to (i) incur additional debt; (ii) incur additional liens; (iii) sell, transfer or dispose of assets; (iv) merge or consolidate, wind-up, dissolve or liquidate; (v) make dividends and distributions on, or repurchases of, equity; (vi) make certain investments; (vii) enter into certain transactions with our affiliates; (viii) enter into sales-leaseback transactions; (ix) make optional or voluntary payments of debt; (x) change the nature of our business; (xi) change our fiscal year to make changes to the accounting treatment or reporting practices; (xii) amend constituent documents; and (xiii) enter into certain hedging transactions.

The affirmative and negative covenants are subject to various exceptions, including basket amounts and acceptable transaction levels. In addition, the CAE Credit Facility requires CAE’s compliance, on a consolidated basis, with (i) a maximum Debt/EBITDA ratio of 3.5 to 1.0 and (ii) a minimum current ratio of 1.0 to 1.0.

CAE may at any time repay the loans under the CAE Credit Facility, in whole or in part, without penalty. CAE must pay down borrowings under the CAE Credit Facility or provide mortgages of additional oil and natural gas properties to the extent that outstanding loans and letters of credit exceed the borrowing base.

In connection with our entry into the Carbon Appalachia LLC Agreement, and Carbon Appalachia engaging in certain transactions during 2017, we received the aforementioned Class B Units and issued to Yorktown a warrant to purchase approximately 408,000 shares of our common stock at an exercise price of $7.20 per share (the “Appalachia Warrant”). The Appalachia Warrant was payable exclusively with Class A Units of Carbon Appalachia held by Yorktown and the number of shares of our common stock for which the Appalachia Warrant was exercisable was determined, as of the time of exercise, by dividing (a) the aggregate unreturned capital of Yorktown’s Class A Units of Carbon Appalachia plus a required 10% internal rate of return by (b) the exercise price.

On November 1, 2017, Yorktown exercised the Appalachia Warrant, resulting in the issuance of approximately 432,000 shares of our common stock in exchange for Class A Units representing approximately 7.95% of then outstanding Class A Units of Carbon Appalachia. We accounted for the exercise through extinguishment of the warrant liability associated with the Appalachia Warrant of approximately $1.9 million and the receipt of Yorktown’s Class A Units as an increase to investment in affiliates in the amount of approximately $2.9 million. After giving effect to the exercise, we own 26.5% of Carbon Appalachia’s outstanding Class A Units along with 100% of its Class C Units.

| 15 |

The issuance of the Class B Units and the Appalachia Warrant were in contemplation of each other, and under non-monetary related party guidance, we accounted for the Appalachia Warrant, at issuance, based on the fair value of the Appalachia Warrant as of the date of grant (April 3, 2017) and recorded a warrant liability with an associated offset to APIC. Future changes to the fair value of the Appalachia Warrant are recognized in earnings. We accounted for the fair value of the Class B Units at their estimated fair value at the date of grant, which became our investment in Carbon Appalachia with an offsetting entry to APIC.

As of the grant date of the Appalachia Warrant, we estimated that the fair market value of the Appalachia Warrant was approximately $1.3 million, and the fair value of the Class B Units was approximately $924,000. The difference in the fair value of the Appalachia Warrant from the grant date though its exercise on November 1, 2017, was approximately $619,000 and was recognized in warrant derivative gain in our consolidated statements of operations for the year ended December 31, 2017.

Based on our 27.24% combined Class A and Class C interest (and our ability as of June 30, 2018 to earn up to an additional 14.7%) in Carbon Appalachia, our ability to appoint a member to the board of directors and our role of manager of Carbon Appalachia, we are accounting for our investment in Carbon Appalachia under the equity method of accounting as we believe we exert significant influence. We use the HLBV to determine our share of profits or losses in Carbon Appalachia and adjust the carrying value of our investment accordingly. Our investment in Carbon Appalachia is represented by our Class A and C interests, which we acquired by contributing approximately $6.9 million in cash and unevaluated property. In the event of liquidation of Carbon Appalachia, available proceeds are first distributed to members holding Class C Units then to holders of Class A Units until their contributed capital is recovered with an internal rate of return of 10%. Any additional distributions would then be shared between holders of Class A, Class B and Class C Units. For the three and six months ended June 30, 2018, Carbon Appalachia earned net income, of which our share is approximately $504,000 and $917,000, respectively. The ability of Carbon Appalachia to make distributions to its owners, including us, is dependent upon the terms of its credit facility, which currently prohibit distributions unless agreed to by the lender.

As of June 30, 2018, Carbon Appalachia is in compliance with all CAE Credit Facility covenants.

The following table sets forth selected historical unaudited consolidated statements of operations and production data for Carbon Appalachia.

| (in thousands) | As

of June 30, 2018 | |||

| Current assets | $ | 21,475 | ||

| Total oil and gas properties, net | $ | 83,541 | ||

| Total other property and equipment, net | $ | 10,842 | ||

| Other long-term assets | $ | 1,109 | ||

| Current liabilities | $ | 14,531 | ||

| Non-current liabilities | $ | 58,028 | ||

| Total members’ equity | $ | 44,408 | ||

| Three months ended | April 3, 2017 to | |||||||

| (in thousands) | June 30, 2018 | June 30, 2017 | ||||||

| Revenues | $ | 18,679 | $ | 1,557 | ||||

| Operating expenses | 16,221 | 1,757 | ||||||

| Income from operations | 2,458 | (200 | ) | |||||

| Net income | $ | 1,853 | $ | (329 | ) | |||

| Six months ended | April 3, 2017 to | |||||||

| (in thousands) | June 30, 2018 | June 30, 2017 | ||||||

| Revenues | $ | 44,422 | $ | 1,557 | ||||

| Operating expenses | 39,756 | 1,757 | ||||||

| Income from operations | 4,666 | (200 | ) | |||||

| Net income | $ | 3,479 | $ | (329 | ) | |||

| 16 |

Old Ironsides Membership Interest Purchase Agreement

On May 4, 2018, we entered into a Membership Interest Purchase Agreement (the “MIPA”) with Old Ironsides. Old Ironsides owns 73.5%, and we own the remaining 26.5%, of the issued and outstanding Class A Units of Carbon Appalachia. We also own all of the Class B and Class C units of Carbon Appalachia. Pursuant to the MIPA, we may acquire all of Old Ironsides’ membership interests of Carbon Appalachia. Following the closing of the transaction, we would own 100% of the issued and outstanding ownership interests in Carbon Appalachia, and Carbon Appalachia will become a wholly-owned subsidiary of ours.

Subject to the terms and conditions of the MIPA, we will pay Old Ironsides, approximately $58.0 million at closing, subject to adjustment, in accordance with the MIPA. We intend to fund the acquisition through the issuance of additional equity, for which we have already filed a registration statement.

The MIPA contains termination rights for us and Old Ironsides, including, among others, if the closing of the transaction has not occurred on or before October 15, 2018. The MIPA may also be terminated by mutual written consent of us and Old Ironsides.

Investments in Affiliates

During the three and six months ended June 30, 2018, we recorded total equity method income of approximately $525,000 and $952,000, respectively. For the six months ended June 30, 2017, we recorded total equity method income of approximately $7,000. Additionally, on February 1, 2018, as a result of the Carbon California Acquisition, we derecognized our equity investment in Carbon California and recognized a gain of approximately $5.4 million based on the fair value of our previously held interest compared to its carrying value.

Note 7 - Credit Facilities

Our Credit Facility

In 2016, we entered into a 4-year $100.0 million senior secured asset-based revolving credit facility with LegacyTexas Bank. LegacyTexas Bank is the initial lender and acts as administrative agent.

The credit facility has a maximum availability of $100.0 million (with a $500,000 sublimit for letters of credit), which availability is subject to the amount of the borrowing base. The initial borrowing base established under the credit facility was $17.0 million. The borrowing base is subject to semi-annual redeterminations in March and September. On March 30, 2018, the borrowing base was increased from $23.0 to $25.0 million, of which approximately $23.1 million was outstanding as of June 30, 2018. Our effective interest rate as of June 30, 2018 was 5.54%. In July 2018, the borrowing base was increased from $25.0 million to $28.0 million.

The credit facility is guaranteed by each of our existing and future subsidiaries (subject to certain exceptions). Our obligations and those of our subsidiary guarantors under the credit facility are secured by essentially all of our tangible and intangible personal and real property (subject to certain exclusions).

Interest is payable quarterly and accrues on borrowings under the credit facility at a rate per annum equal to either (i) the base rate plus an applicable margin between 0.50% and 1.50% or (ii) the Adjusted LIBOR rate plus an applicable margin between 3.50% and 4.50% at our option. The actual margin percentage is dependent on the credit facility utilization percentage. We are obligated to pay certain fees and expenses in connection with the credit facility, including a commitment fee for any unused amounts of 0.50%.

The credit facility contains affirmative and negative covenants that, among other things, limit our ability to (i) incur additional debt; (ii) incur additional liens; (iii) sell, transfer or dispose of assets; (iv) merge or consolidate, wind-up, dissolve or liquidate; (v) make dividends and distributions on, or repurchases of, equity; (vi) make certain investments; (vii) enter into certain transactions with our affiliates; (viii) enter into sales-leaseback transactions; (ix) make optional or voluntary payments of debt; (x) change the nature of our business; (xi) change our fiscal year to make changes to the accounting treatment or reporting practices; (xii) amend constituent documents; and (xiii) enter into certain hedging transactions.

The affirmative and negative covenants are subject to various exceptions, including basket amounts and acceptable transaction levels. In addition, the credit facility requires our compliance, on a consolidated basis, with (i) a maximum Debt/EBITDA ratio of 3.5 to 1.0 and (ii) a minimum current ratio of 1.0 to 1.0.

On March 27, 2018, the credit facility was amended to revise the calculation of the Leverage Ratio from a Debt/EBITDA ratio to a Net Debt/Adjusted EBITDA ratio, reset the testing period used in the determination of Adjusted EBITDA, eliminated the minimum current ratio and substituted alternative liquidity requirements, including maximum allowed current liabilities in relation to current assets, a minimum cash balance requirement of $750,000 and maximum aged trade payable requirements. As of June 30, 2018, we were in compliance with our financial covenants.

We may at any time repay the loans under the credit facility, in whole or in part, without penalty. We must pay down borrowings under the credit facility or provide mortgages of additional oil and natural gas properties to the extent that outstanding loan and letters of credit exceed the borrowing base.

| 17 |

As required under the terms of the credit facility, we entered into derivative contracts with fixed pricing for a certain percentage of our production. We are a party to an ISDA Master Agreement with BP Energy Company that established standard terms for the derivative contracts and an inter-creditor agreement with LegacyTexas Bank and BP Energy Company whereby any credit exposure related to the derivative contracts entered into by the Company and BP Energy Company is secured by the collateral and backed by the guarantees supporting the credit facility.

Carbon California – Credit Facilities

Effective as of February 1, 2018, our ownership in Carbon California increased to 56.4% due to the exercise of the California Warrant. As a result of this transaction, we consolidate Carbon California for financial reporting purposes.

On May 1, 2018, Carbon California closed the Seneca Acquisition. Following the exercise of the California Warrant by Yorktown and the Seneca Acquisition, we own 53.92% of the voting and profits interests, and Prudential owns the remainder of the interests, in Carbon California.

The table below summarizes the notes payable outstanding for Carbon California as of June 30, 2018 (in thousands):

| Senior Revolving Notes, related party, due February 15, 2022 | $ | 38,500 | ||

| Subordinated Notes, related party, due February 15, 2024 | 13,000 | |||

| Long-term debt | 78 | |||

| Total gross notes payable | 51,578 | |||

| Less: Deferred notes costs | (232 | ) | ||

| Less: Notes discount | (1,368 | ) | ||

| Total net notes payable | $ | 49,978 |

Carbon California- Senior Revolving Notes, Related Party

On February 15, 2017, Carbon California entered into the Note Purchase Agreement with Prudential Legacy Insurance Company of New Jersey and Prudential Insurance Company of America for the issuance and sale of the Senior Revolving Notes due February 15, 2022. We are not a guarantor of the Senior Revolving Notes. The closing of the Note Purchase Agreement on February 15, 2017, resulted in the sale and issuance by Carbon California of Senior Revolving Notes in the principal amount of $10.0 million. The maximum principal amount available under the Senior Revolving Notes is based upon the borrowing base attributable to Carbon California’s proved oil and gas reserves which is to be determined at least semi-annually. As of June 30, 2018, the borrowing base was $41.0 million, of which $38.5 million was outstanding.

Carbon California may elect to incur interest at either (i) 5.0% plus the London interbank offered rate (“LIBOR”) or (ii) 4.00% plus Prime Rate (which is defined as the interest rate published daily by JPMorgan Chase Bank, N.A.). As of June 30, 2018, the effective borrowing rate for the Senior Revolving Notes was 8.29%. In addition, the Senior Revolving Notes include a commitment fee for any unused amounts at 0.50% as well as an annual administrative fee of $75,000, payable on February 15 each year.

The Senior Revolving Notes are secured by all the assets of Carbon California. The Senior Revolving Notes require Carbon California, as of January 1 and July 1 of each year, to hedge its anticipate proved developed products production at such time for year one, two and three at a rate of 75%, 65% and 50%, respectively. Carbon California may make principal payments in minimum installments of $500,000. Distributions to equity members are generally restricted.

Carbon California incurred fees directly associated with the issuance of the Senior Revolving Notes and amortizes these fees over the life of the Senior Revolving Notes. The current portion of these fees are included in prepaid expense and deposits and the long-term portion is included in other long-term assets for a combined value of $944,000. During the three and six months ended June 30, 2018, Carbon California amortized fees of $48,000 and $77,000, respectively. For the three and six months ended June 30, 2017, the Carbon California amortized $14,000 and $43,000, respectively.

The Note Purchase Agreement requires Carbon California to maintain certain financial and non-financial covenants which include the following ratios: total leverage ratio, senior leverage ratio, interest coverage ratio, current ratio, and other qualitative covenants as defined in the Note Purchase Agreement. As of June 30, 2018, Carbon California was in compliance with its financial covenants.

Carbon California Subordinated Notes

On February 15, 2017, Carbon California entered into the Securities Purchase Agreement with Prudential Capital Energy Partners, L.P. for the issuance and sale of the Subordinated Notes due February 15, 2024, bearing interest of 12% per annum. We are not a guarantor of the Subordinated Notes. The closing of the Securities Purchase Agreement on February 15, 2017, resulted in the sale and issuance by Carbon California of Subordinated Notes in the original principal amount of $10.0 million.

Prudential received an additional 1,425 Class A Units, representing 5% of total sharing percentage, for the issuance of the Subordinated Notes. Carbon California valued this unit issuance based on the relative fair value by valuing the units at $1,000 per unit and aggregating the amount with the outstanding Subordinated Notes of $10.0 million. The Company then allocated the non-cash value of the units of approximately $1.3 million, which was recorded as a discount to the Subordinated Notes. As of June 30, 2018, Carbon California had an outstanding discount of $923,000, which is presented net of the Subordinated Notes within Credit facility-related party on the unaudited consolidated balance sheets.

| 18 |

The Subordinated Notes require Carbon California, as of January 1 and July 1 of each year, to hedge its anticipated production at such time for year one, two and three at a rate of 67.5%, 58.5% and 45%, respectively.

Prepayment of the Subordinated Notes is currently not available. After February 15, 2019, prepayment is allowed at 100%, subject to a 3.0% fee of outstanding principal. Prepayment is not subject to such fee after February 17, 2020. Distributions to equity members are generally restricted.

The Securities Purchase Agreement requires Carbon California to maintain certain financial and non-financial covenants, which include the following ratios: total leverage ratio, senior leverage ratio, interest coverage ratio, asset coverage ratio, current ratio, and other qualitative covenants as defined in the Securities Purchase Agreement. As of June 30, 2018, Carbon California was in compliance with its financial covenants.

Carbon California-2018 Subordinated Notes

On May 1, 2018, Carbon California entered into an agreement with Prudential for the issuance and sale of the Carbon California 2018 Subordinated Notes.