Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - HUI YING FINANCIAL HOLDINGS Corp | s109343_ex32-2.htm |

| EX-31.1 - EXHIBIT 31.1 - HUI YING FINANCIAL HOLDINGS Corp | s109343_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - HUI YING FINANCIAL HOLDINGS Corp | s109343_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - HUI YING FINANCIAL HOLDINGS Corp | s109343_ex31-1.htm |

| EX-21.1 - EXHIBIT 21.1 - HUI YING FINANCIAL HOLDINGS Corp | s109343_ex21-1.htm |

UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 333-201037

HUI YING FINANCIAL HOLDINGS CORPORATION

(Exact name of registrant as specified in its charter)

| Nevada | 35-2507568 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) | |

Room 2403, Shanghai Mart Tower 2299 West Yan’an Road, Changning District Shanghai, China |

200336 | |

| (Address of principal executive offices) | (Zip Code) |

Issuer’s telephone number: +86 21-23570077

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☒ No ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Smaller reporting company | ☒ | ||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Emerging Growth Company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of the last business day of the Company’s most recently completed second fiscal quarter, there was no active public trading for its shares of common stock on OTC QB. Since the Company’s revenue is less than $75 million during the fiscal year ended 2017, the Company is a smaller reporting company.

As of March 19, 2018, there were 72,364,178 shares of the Company’s common stock issued and outstanding.

1

HUI YING FINANCIAL HOLDINGS CORPORATION

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2017

TABLE OF CONTENTS

i

Except where the context otherwise requires and for purposes of this Annual Report on Form 10-K (this “Report”) only:

| ● | “we,” “us,” “our company,” “our,” “the Company” and “Hui Ying Financial” refer to Hui Ying Financial Holdings Corporation; |

| ● | “China”, “Chinese” or the “PRC” refers to the People’s Republic of China, excluding, for the purposes of this Report only, Hong Kong, Macau and Taiwan; |

| ● | all references to “RMB” or “Chinese Yuan” is to the legal currency of the People’s Republic of China; |

| ● | all references to “U.S. dollars,” “dollars,” “USD” or “$” are to the legal currency of the United States; |

| ● | “peer-to-peer lending service providers” refers to marketplaces connecting borrowers and investors; and |

| ● | “Benefactum Beijing”, “variable interest entity” or “VIE” is to our variable interest entity, Benefactum Alliance Business Consultant (Beijing) Co., Ltd , that is 100% owned by PRC citizens, that holds the business operation licenses or approvals, and generally operates our various websites and mobile applications for our internet businesses or other businesses in which foreign investment is restricted or prohibited, and is consolidated into our consolidated financial statements in accordance with U.S. GAAP as if it were our wholly-owned subsidiary. |

Unless otherwise noted, all translations from Chinese Yuan to U.S. dollars using the exchange rate refers to the exchange rate quoted on http://www.oanda.com on December 31, 2017, which was RMB 6.5074 to USD$1.00. We make no representation that the Chinese Yuan amounts referred to in this Report could have been or could be converted into U.S. dollars at any particular rate or at all.

Note Regarding Forward-Looking Statements

This Report contains “forward-looking statements,” which are statements that relate to future events or our future operational or financial performance or prospects that are based upon beliefs of, and information currently available to, our management as well as estimates and assumptions made by our management. When used in the filings the words “anticipate”, “believe”, “estimate”, “expect”, “future”, “intend”, “plan” or the negative of these terms and similar expressions as they relate to us or our management identify forward looking statements. Such statements reflect the current view of our management with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this report entitled “Risk Factors”) as they relate to our industry, our operations and results of operations, and any businesses that we may acquire. Should one or more of the events described in these risk factors materialize, or should our underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although we believe that the expectations reflected in the forward looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the U.S. federal securities laws, we do not intend to update any of the forward-looking statements to conform them to actual results. The following discussion should be read in conjunction with our financial statements and the related notes that are included herein.

Overview

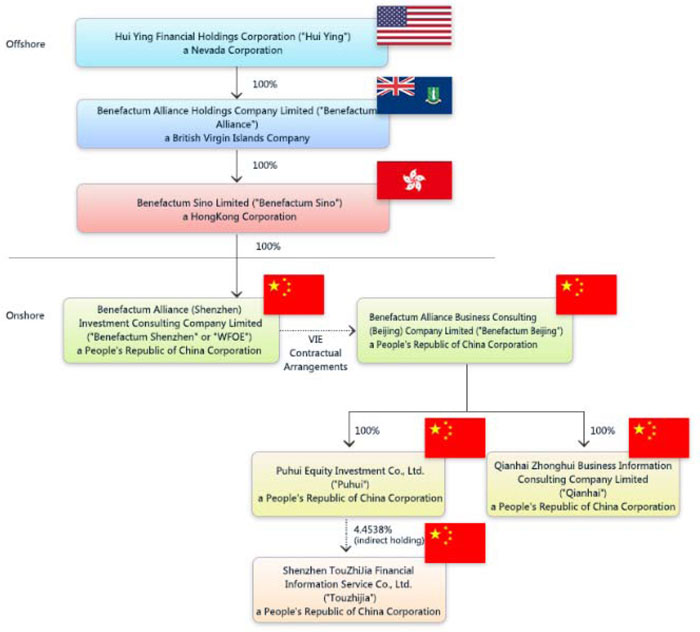

We are a holding company that, through our wholly-owned subsidiaries, Benefactum Alliance Holdings Company Limited, a British Virgin Islands company (“Benefactum Alliance”), Benefactum Sino Limited, a Hong Kong company (“Benefactum Sino”) and Benefactum Alliance (Shenzhen) Investment Consulting Company Limited, a People’s Republic of China company (“Benefactum Shenzhen” or “WFOE”) and our contractually controlled and managed company, Benefactum Alliance Business Consultant (Beijing) Co., Ltd., a People’s Republic of China company (“Benefactum Beijing”), operate an electronic online financial platform, www.hyjf.com, which is designed to match investors with small and medium-sized enterprises (“SMEs”) and individual borrowers in China. We believe our services provide an effective solution for under-served SME and individual borrowers who need access to financing. Since the launch of our marketplace in December 2013 through December 31, 2017 we have facilitated over $2.87 billion in loans. As of December 31, 2017, we had 367,893 registered investors and 24 institutional partners.

We generate revenue from our services that facilitate matching lenders, who we refer to as investors, with individual and SME borrowers. We typically charge borrowers a loan origination service fee between 1.5% and 3% of the loan amount, depending on the duration of the loan, for each effected loan facilitated by us. Additionally, we charge a separate fee from borrowers for each loan repayment facilitated by us, which is based on an agreed upon percentage approximately 0.3% on the borrowing times the duration of the loan.

In addition, in June 2017 we engaged a qualified non-banking financial institution to provide entrusted loans to SMEs. Through this process we, as the trustor, provide funds to a trustee, who enters into a three-party loan agreement with us and the borrower. The loans are typically short-term and are guaranteed by a third-party financing guarantor. This is one step forward towards our long-term strategy of building a financial ecosystem aimed at providing full service to our SME customers. We intend to expand our business in both online and offline sectors to meet the demands of various customers.

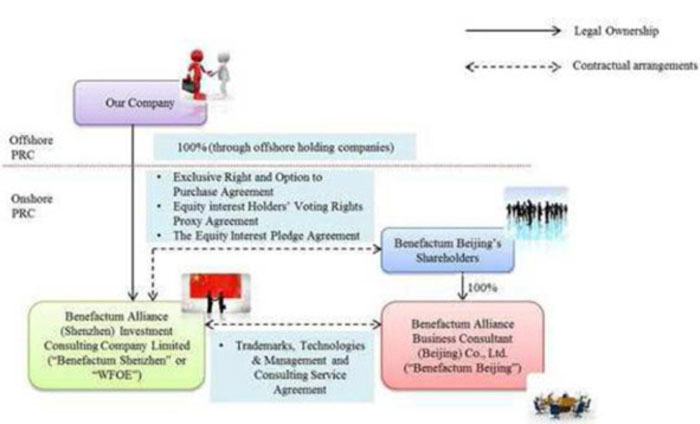

Due to PRC legal restrictions on foreign ownership and investment in, among other areas, value-added telecommunications services, which include internet content providers, or ICPs, we, similar to all other entities with foreign-incorporated holding company structures operating in our industry in China, have to operate our internet businesses and other businesses in which foreign investment is restricted or prohibited in the PRC through wholly foreign-owned enterprises, majority-owned entities and variable interest entities. Accordingly, we plan to continue to operate our online financial platform in China through Benefactum Beijing, which is wholly-owned by two Chinese shareholders, but is contractually controlled and managed through our wholly-owned WFOE.

The contractual arrangements between WFOE and Benefactum Beijing collectively enable us to exercise effective control over, and realize substantially all of the economic risks and benefits arising from Benefactum Beijing. See “Corporate History and Structure — Contractual Arrangements with Benefactum Beijing.” The contractual arrangements may not be as effective in providing operational control as direct ownership. See “Risk Factors — Risks Related to Our Corporate Structure.” As a result, we include the financial results of Benefactum Beijing in our consolidated financial statements in accordance with generally accepted accounting principles in the United States, or U.S. GAAP, as if it were our wholly-owned subsidiary.

We conduct our business primarily in Beijing, Shanghai and Shandong Province, People’s Republic of China. Our principal executive offices are located at Rooms 2401, 2402, 2403, 2404 and 2412 on 2299 Yan’an West Road, Shanghai, China.

2

Our Strategy

Our mission is to provide SMEs and individual borrowers with easy and effective access to affordable financing and provide investors with a safe and acceptable investment return. To achieve this goal, we have implemented the following strategies, each of which we intend to continue to expand:

| ● | Expand the base of borrowers on our platform by entering into cooperation agreements with guarantor institutions, pawn shops, micro credit companies and asset management companies |

We will continue to expand our base of SMEs and individual borrowers by entering into cooperation agreements with various partners, including without limitation, guarantor institutions, pawn shops, micro-credit companies and asset management companies, who can provide us with recommendations for new borrowers. Currently, our cooperative partners are located in Shandong, Inner Mongolia and other areas in China. Since the inception of our online platform, approximately 88.5% of the loans facilitated through our platform are for SME borrowers. We will continue expanding the number, type and areas of cooperative partners, and seek cooperation with internet companies, e-commerce companies, telecommunication companies and third-party payment platforms which are located throughout China.

| ● | Develop new consumer financing products and penetrate niche markets |

We are promoting new personal consumer financing products to individual borrowers, such as automobile financing and consumer financing. In addition, we will continue to design and develop diversified financing products to satisfy market demand.

Our platform also allows investors to diversify their wealth management strategies by providing easy access to various lending opportunities that can be designed with flexible terms.

| ● | Expand our base of investors to include mutual fund and other institutional investors |

Currently, all of our investors are individuals. We are introducing mutual fund or other institutional investors to increase our overall number and type of investors. In addition, we have implemented plans to attract more individual and institutional investors by cooperating with institutions so that the cost to the borrowers would be reduced if there are more funds available for loans.

| ● | Further enhance our risk management capabilities |

As loan volume in our marketplace grows and consumer financing products expand, we have implemented protocols to enhance our risk management capabilities. As for individual borrowers, we have improved the risk management model for individual credit control so that risk management testing will be more effective and reasonable. For SME borrowers, besides the due diligence process that our cooperative partners undertake, we have enhanced the onsite due diligence process and appointed a risk management team.

In addition, we have enhanced our cooperation with other third-party credit investigators to obtain more accurate information about the credit history of the borrowers so we can make reasonable and accurate assessments of borrower applications to reduce and avoid bad debts.

| ● | Continue to invest in our technology platform |

We have made significant investments in our proprietary technologies in the areas of data collection and processing algorithms to increase the precision, speed and scale at which we match the demand and supply of loans. Enhanced data analytics improves our conversion of online leads into successful borrowers and investors. With the further application of big data, we can acquire members of our target borrower and investor groups in a more focused and cost-efficient way. Furthermore, we will continue to leverage technology to further automate our processes and improve the safety and efficiency of matching the loans with investors. At the same time, we will also benefit from the operating leverage associated with our scalable platform as our loan volume increases. We believe these investments will facilitate the long-term growth of our marketplace.

| ● | Increase our merger and acquisition activities to enhance our competitive advantage in the financing technology ecosystem and to improve the efficiency of our products and services |

We will expand strategic relationships with internet financing companies, internet companies, technology companies and financing companies, by mergers and acquisitions to enhance our competitive advantage in the financing technology ecosystem and to improve the efficiency of our products and services

3

| ● | Various Product and Service Offerings |

As a long-term strategy, we are planning to build a financial ecosystem for SME customers that are under-served in China’s current financial system. We will seek to expand our intermediary and direct lending services, both online and offline, to meet the demands of various customers. As part of this initiative, we announced the launch of entrusted loan services on June 30, 2017, which leverages our improving financial condition and years of experience in providing financing solutions to our customers in China. We believe the new service allows us not only to generate new revenues but also to expand our scope beyond the existing service of being an intermediary between investors and borrowers through the online platform. We will continue to devise customized product and service offerings to meet customer demands and expand the scale and scope of our operations.

Our Business

We operate our business through an electronic online financial platform, www.hyjf.com (“website”), which is designed to match investors with SME and individual borrowers in China. We have developed user-friendly mobile applications for borrowers and investors (“mobile apps “, collectively with our website, the “platform”), which enable borrowers and investors alike to access our platform at any time or location that is convenient. We launched our first mobile application in September 2015. In calendar years 2017 and 2016, we facilitated over RMB4.12 billion (approximately $609.22 million) and RMB1.28 billion (approximately $188.14 million) in loans through our mobile apps, respectively, representing 46.58% and 22.54 % of the total amount of loans facilitated through our marketplace in the respective periods.

Our platform is also accessible to those who guarantee the loans for our borrowers (“third-party cooperative partners”). Apart from acting as guarantors, these third-party cooperative partners may, if they so choose, also use our platform for purposes of transferring their creditor rights on loans made by them outside our platform (“outside loans”). For this service, we charge these third-party cooperative partners similar loan origination service fees and repayment management fees.

We had 24 third-party cooperative partners as of December 31, 2017, consisting of five pawn shops, four guaranty companies, a micro-loan company, an asset management companies, three information technology companies, three financial consulting companies, four technology companies, and three financial services companies, which frequently serve as guarantors of loans on our platform.

4

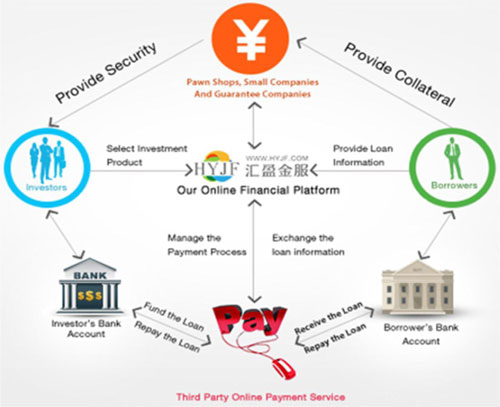

The following diagram illustrates our current business model:

Our Online Marketplace

Our platform embraces significant opportunities presented by a financial system that leaves many creditworthy individuals and SMEs underserved. We match qualified borrowers who have completed profiles that are available on the platform with investors. Once an investor decides to proceed with a specific loan, and the borrower accepts the terms of the loan, our system automatically generates electronic loan contracts for execution. When the closing conditions are satisfied, our system directs the investors to the third-party payment platform to consummate the loan. In addition, our platform allows third-party cooperative partners to assign outstanding loans to other registered investors on our platform. The loans we facilitate are usually short-term loans that range from one month to twelve months with interest rates ranging from 4.5% to 12%.

Online Loan Transaction Process

We provide a streamlined application process combining both online and offline features. To borrowers and investors alike, we have designed the process to appear simple, seamless and efficient, utilizing sophisticated, proprietary technology to make it possible. The entire process, from posting the loan application on our platform to disbursement of funds, takes no longer than 19 days but, more typically, only three to five days. At any given time, a borrower may have only one outstanding loan on our platform, and only after the outstanding loan is paid off, can the borrower enter into a new loan. At such time the borrower submits a new application, we undertake a new review of the borrower’s loan profile prior to making any determination as to whether to facilitate a new loan transaction. This restriction on lending prevents a borrower from borrowing a new loan to pay off the old loan resulting in an increase in the borrower’s total debt. The platform monitors and reviews borrowers, therefore preventing a “roll over” of loans.

We post borrower profiles and their loan information on our online platform, including loan amount, duration, interest rate or rate range they are willing to pay, borrower’s basic information, its total assets and credit score etc. Investors can browse the loan information on our platform and select loan products appropriate for them to invest in, based on their own availability of funds and their risk preferences. Set forth below is a description of the steps in a typical online loan transaction.

5

Step 1: Online Application Submission and Initial Assessment.

In order to access the services provided by our online financial platform, potential borrowers open an account with us and complete an online loan application form.

Our risk control department determines whether the potential borrower meets our minimum requirements based on initial discussions between our risk control department and the prospective borrower. We evaluate each borrower’s application and decide if we should process his/her application on a case-by-case basis. As part of this process, we conduct an analysis of the borrower’s financial conditions, loan amount and term, business industry and proposed use of the funds.

If the prospective borrower meets our minimum requirements, the application is forwarded to our third-party cooperative partners who guarantee the borrower’s loan after reviewing the borrower’s application materials.

As an alternative, the borrower may also propose a third-party guarantor to guarantee the repayment of its loan. In these instances, we also conduct an assessment of the referred guarantor’s credit-worthiness and financial standing using the same matrix as that for the borrower. The third-party guarantor will be jointly and severally liable with the borrower for the borrower’s debt.

Typically, as part of this process, prospective borrowers will be asked for documents to prove their identity and financial standing, including but not limited to business licenses, tax reports, audited financial statements and appraisal reports (for enterprise borrowers), national identification card and bank statements (for individual borrowers).

Step 2: Offline Anti-Fraud Investigation and Credit Assessment

Our risk control department reviews all borrower application materials and conducts its own due diligence, including third-party verification and onsite visits, and a review of the sufficiency of collateral provided. Our risk management model utilizes big data capabilities to systematically evaluate a borrower’s credit characteristics. After verifying the authenticity of the borrower’s submitted documents, we will assign a credit rating to the borrower based on its credit history, business activities being undertaken, assets and other criteria.

We have established a risk management model for SME borrowers. We use over 120 factors to evaluate SME borrowers, with a weighted total score of 400 and a minimum score of 60. Our risk assessment matrix can be classified into the following categories: enterprise quality assessment, operation and management assessment, repayment funding source assessment, and risk management assessment, and we use these four categories to evaluate SME borrowers. At the same time, we use a third-party system and publicly available credit reporting system to make necessary inquiries on SME borrowers, thereby establishing a risk management model suitable for China’s SME borrowers. Based on a borrower’s credit history, business activities, assets and other criteria, we classify the borrower’s credit rating into the following categories according to its weighted average score: AAA (> 90), AA+ (80-90), AA (70-80), AA- (60-70), and A (< 60). In the order of AAA to A, the expected quality of borrowers decreases, and the expected default rates ascends, even though there have been no defaults of borrowers since the inception of the platform. Explanations of each credit rating are as follows:

AAA: The SME borrower operates its business normally without the presence of any operational issues; it has abundant repayment funding sources, good financial standing, and no bad credit records. Borrowers with credit rating of AAA are expected to have a default rate of approximately 0%.

AA+: The SME borrower operates its business normally without the presence of any operational issues; it has multiple repayment funding sources, good financial standing, and no bad credit records or resolved bad records only.

AA: The SME borrower operates its business normally; it has multiple repayment funding sources, moderate to good financial standing, and resolved bad credit records or minor bad credit records, for which reasonable explanations are required by the Company.

6

AA-: The SME borrower operates its business normally; it has some repayment funding sources, moderate financial standing, and resolved bad credit records or minor bad credit records, for which reasonable explanations are required by the Company. For these borrowers, the Company facilitates loans under the condition that the borrower meets stricter collateral requirements asked by the guarantors.

A: Any SME borrowers that fail to meet the qualifications mentioned in AA- and above are unqualified to receive loans on our platform.

The following table sets forth the outstanding loan amounts for SME borrowers by credit rating at end of each period as indicated:

| (in US$ millions) | December 31, | December 31, | December 31, | |||||||||||||||||||||

| Credit Rating | 2017 | % Total | 2016 | % Total | 2015 | %Total | ||||||||||||||||||

| AAA | $ | — | — | $ | 10.1 | 4.7 | % | $ | 3.2 | 2.1 | % | |||||||||||||

| AA+ | 15.4 | 3.6 | % | 24.4 | 11.3 | % | 12.7 | 8.2 | % | |||||||||||||||

| AA | 415.1 | 96.3 | % | 170.5 | 79.2 | % | 132.6 | 85.3 | % | |||||||||||||||

| AA- | 0.8 | 0.2 | % | 10.3 | 4.8 | % | 6.8 | 4.4 | % | |||||||||||||||

| A | — | — | — | — | — | — | ||||||||||||||||||

| Total | $ | 431.2 | 100 | % | $ | 215.3 | 100 | % | $ | 155.4 | 100 | % | ||||||||||||

| As percentage of total loans outstanding | 98.8 | % | 87.5 | % | 83.5 | % | ||||||||||||||||||

We are also working on establishing a risk management model for individual borrowers. The model for individual borrowers will have over 440 factors, with a weighted total score of 1,085 and a minimum score of 550. The risk assessment matrix can be classified into the following six controlling categories: borrower’s basic information, existing assets, repayment ability, credit status, indebtedness status and behavioral analysis. At the same time, we obtain from the third-party the borrower’s relevant social activities, telephonic records, creditworthiness, indebtedness status, and these four factors form an all-dimensional holistic assessment mechanism, thereby establishing an objective and realistic risk management model for individual borrowers. Once the model is completely established, we will rely on this model for risk management of individual borrowers.

We have stringent requirements for the collateral in order to protect the investors’ interests. Generally, we only accept collateral that is highly liquid and adequate to repay the loan amount. Borrowers who intend to use real estate to secure their loans will first need to have the real estate appraised by qualified appraisers. The loan amount cannot be more than 80% of the value of the real estate. The collateral provided by borrowers is provided only to third-party guarantors, not to the investors.

Although we typically do not accept personal property as collateral, we may do so under exceptional circumstances when the personal property will be pledged and the loan amount is no more than 70% of the appraised value of the personal property.

7

Step 3: Approval

Once the borrower is approved, we categorize the borrower’s credit facility into one or more of the following loan products and post it on our platform. We also post the relevant third-party guarantor’s information and its letter of guarantee. The information is accessible to all investors who have registered on our platform. They will have the option of accepting the credit facility per the terms offered online. Once a credit facility is accepted by an investor, our platform automatically prepares the necessary loan documents for execution by the parties online. The electronic signatures generated on platform are certified by China Financial Certification Authority, a financial security certification authority designated by People’s Bank of China.

| Product | Target Investors |

Term

of Loan |

Expected Return |

Minimum investment amount (RMB) |

Maximum investment amount (RMB) |

Fund-raising period |

Repayment

of Loan (for borrowers) |

Assignability (Yes/No) | ||||||||

| Xin Shou Zhuan Qu | For investors who have made no investments in anyproducts on our platform | 30 days | Generally 8.5% | 100 | 10,000 | No more than 19 days | Repay capital with interest when the loan is due | No | ||||||||

| Cai Fu Hui | For all registered platform users | 1 – 24 months | 4.5% - 12% | 100 | — | No more than 19 days | Repay capital with interest when the loan is due | Yes, but only after holding this product for at least 30 days | ||||||||

| Zun Xiang | Premium customers and private business customers | 6 - 12 months | 11% - 12% | 100,000 | — | No more than 19 days | Repay capital with interest when the loan is due | Yes, but only after holding this product for at least 30 days | ||||||||

| Hui Ji Hua | For all registered platform users | 7 days – 12 months | 4.5% - 11% | 1,000 | — | No more than 19 days | Repay capital with interest when the loan is due | Yes, but only after holding this product for at least 30 days | ||||||||

| You Xuan Zhai Quan | For all registered platform users | 30 days – 12 months | 6.5% - 11% | 10,000 | — | No more than 19 days | Repay capital with interest when the loan is due | Yes, but only after holding this product for at least 30 days | ||||||||

Zhai Quan Zhuan Rang*

|

For all registered platform users

|

Depending on the investment products

|

N/A

|

100

|

—

|

N/A

|

Repay capital with interest when the loan is due

|

Yes, but only after holding this product for at least 30 days and there will be a 0.5% assigning fee

| ||||||||

| Hui Xiao Fei | For all registered platform users | 12 months | N/A | 100 | — | No more than 19 days | 12 equal monthly payments | Yes |

* Zhai Quan Zhuan Rang is a service that allows investors to transfer their creditors’ rights. The minimum outstanding loan amount requirement before creditor rights may be transferred is not less than RMB 1,000. After holding an investment product for at least 30 days, the investor may then transfer this product at a price of at least 95% of the original price. The service was launched in October 2015. For the years ended December 31, 2017 and 2016, service revenues from Zhai Quan Zhuan Rang product amounted to $158,227 and $55,342, respectively. Revenue is recognized when the service is rendered and service fee is collected from transferor upon the completion of the transfer, which is classified under Revenues on the Income Statement, the same as loan origination service fee collected for other loan products.

Once we successfully match investors and borrowers through our online platform, we provide following services during the loan origination process:

a) Assisting in registering of liens or collaterals with relevant government agencies;

b) Verifying accuracy of documents and loan information and assisting in loan offering transactions. There are often times multiple investors involved in a single loan offering;

c) Facilitating communications with borrowers and guarantors through various means to ensure smooth closings of transactions; and

d) Coordinating with third-party online payment depository institutions to transfer funds upon closing.

8

Step 4: Funding

Since the inception of our online platform in December 2013 through July 2017, we had contracted with a licensed third-party online payment service, Hui Fu Tian Xia Limited Company (“ChinaPnR”), to assist in the disbursement and repayment of loans. Individual borrowers were charged a processing fee by ChinaPnR in the amount of 0.11% to 0.25% (which varies depending on the bank they use) of the loan amount when it was deposited in their ChinaPnR account. For SME borrowers, they paid RMB 10 per deposit. When borrowers withdrew money from their ChinaPnR account, they would have to pay a processing fee of 0.05% of the withdrawing amount plus RMB1 or just RMB1, depending on how soon they wish for the withdrawal to be effected. When the loan was repaid to ChinaPnR, ChinaPnR would disburse the loan and interest back to the investors, who were not charged for the service provided by ChinaPnR.

However, in February 2017, the CBRC released the Guidance to regulate funds depositories for online lending intermediaries. The Guidance defines depositories as commercial banks that provide online lending fund depository services. In compliance with the regulatory requirement, we engaged Jiangxi Bank, a qualified banking financial institution, in March 2017 as our funding depository service provider. Upon successful system transition from China PnR to Jiangxi Bank in July 2017, Jiangxi Bank started to assist in the disbursement and repayment of loans. Both the investor and the borrower open accounts with Jiangxi Bank and authorize Jiangxi Bank to manage their accounts. The investor funds the loan amount in his/her account with Jiangxi Bank, which disburses loan amount to the borrower net of our service fees, which is remitted to us.

Currently, investors are not charged for deposits made to their accounts in Jiangxi Bank. However, borrowers are charged a processing fee by Jiangxi Bank in the amount of 0.10% (with a minimum of RMB2) of the loan amount when the funds are deposited into the borrower’s Jiangxi Bank account. When borrowers and investors withdraw money from their Jiangxi Bank accounts, they pay a processing fee of RMB1 per transaction.

Our dedicated team closely monitors the whole process and solves any issues promptly to ensure closing of loan transactions are handled in a timely and accurate manner. Once loans are closed and funds are transferred, we consider our loan origination service being rendered. We then recognize revenue from fees collected from loan origination services. The fees are simultaneously deducted from loan proceeds upon transfer of funds from lenders and remitted to our account on the same day. In most cases, the fees will be in our account on the same day or next business day but occasionally may take up to three business days due to bank or internal processing delay. The fees are not refundable. We retain borrowers’ loan records in our system as a part of their credit profile and for reference in their future financing applications.

Step 5: Post-Funding Supervisory

After the debt financing is provided to the borrower, the guarantor monitors the borrower’s performance and provides the platform with the feedback on the borrower’s credit condition, contract performance and debt repayment capabilities. The guarantor initially monitors and examines the borrower’s performance within one month after the loan is provided to the borrower. For longer-term loans, the guarantor conducts additional rounds of examination every two months after the first round. For every round of examinations, the guarantors examine borrowers’ performance from multiple aspects, including reviewing their most recent credit histories, monthly cash flows, operational activities, debt repayment capabilities, and occurrence of any contract breaches. If no material changes are found, a Post-Funding Supervisory Report is provided to the company within five business days after the examination. Examinations are conducted for two primary reasons. First, we create a separate credit file for each borrower on our platform. The Post-Funding Supervisory Reports allow us to update the borrower profiles in a timely manner with additional information and recent business developments. Post-Funding Supervisory Reports ensure the completeness of the borrower profiles. Moreover, additional rounds of examinations give us timely access to the borrower’s financial and operational issues that could potentially result in credit events. In this case, the additional examinations enable the Company to recognize any risks earlier and take actions to avoid losses more promptly than we would have been without the examinations. As noted previously, after the initial examination, the guarantor conducts additional rounds of examination every two months. The two-month period is a minimum requirement that we set and is determined based upon our risk management experience and estimation of the average cash cycle among our borrowers. In practice, we may recommend our guarantors, or the guarantors themselves may choose, to conduct examinations more frequently as needed to better protect their interests. For example, if the default rate of a particular industry or a geographical area surges during a period of time, we would recommend the guarantors to conduct more frequent and detailed examinations.

9

Since the inception of the platform there have been no credit events giving rise to the possibility of a borrower default. However, we expect that if a guarantor recognizes a credit event with any material changes that could potentially result in a negative turn in a borrower’s financial standing and ability to repay its loan, the guarantor will notify us immediately, or at least within the same day, so that our management can take prompt action to minimize the risk of non-payment. Although we have instituted a minimum two-month period for rounds of examinations, each guarantor has its own terms of disclosure requirements and/or additional examinations included in their guarantee contracts signed with the borrowers and may determine to put in place additional controls to detect a possible credit default prior to an examination. For example, most of our guarantors require borrowers to report monthly on the usage of loans guaranteed by them, the occurrence of any new borrowings and updated financial statements etc. Guarantors may also monitor the borrowers’ credit status through reviewing their monthly credit reports on the People’s Bank of China’s Credit Record Center website. Besides these standard checks, guarantors may also require borrowers to report any significant events, such as equity restructuring and merger & acquisition etc., at least thirty days in advance. With the additional reporting and examinations, the guarantors have comprehensive knowledge on the borrowers’ operational condition and credit status. If any potential default risk is recognized, the guarantors will notify our platform immediately to discuss the severity of the situation and the necessity to take actions to prevent a default.

We do not expect any significant impact on the risk reserve fund since we have a process in place for payment from the fund and reimbursement to the risk reserve fund. In the event of any negative credit event, our management will determine the proper action to take to avert or minimize the risk of non-payment. One week before the loan is due, the risk control department informs Jiangxi Bank (China PnR prior to July 2017), our third-party cooperative partners and the borrower and supervises the repayment of the loan.

Step 6: Collections

Towards the end of each loan term, we provide repayment service to ensure the loan repayment process is handled smoothly through our online platform. All loans originated through our online platform are repaid through our online platform and the terms are agreed upon at the time of the original loan agreement. When loans approach its maturity, our team will typically send our notices to borrowers via several means to remind them of the repayment deadlines. We will then calculate the amounts to be repaid by borrowers, including the principals, accrued interests and service charges, and provide repayment notices to borrowers 7 days before the maturity day. On the maturity day, borrowers log onto their accounts opened with our online platform, transfer funds into their depository accounts in Jiangxi Bank’s depositary system, and process the repayment through our online system. When the borrower repays the loan to Jiangxi Bank, they deposit the loan repayment management fee along with the principal loan amount and interest. Jiangxi Bank then disburses the principal loan amount and interest back to the investor and remits the repayment management fee to us.

The use of our online system is a part of our service provided in connection with the repayment process. Borrowers authorize our platform to send instructions to Jiangxi Bank’s fund depositary system, which, following pre-established rules, deduct calculated repayment amounts from borrower’s depositary accounts and transfer the funds to lender’s depositary accounts. We also help with making arrangement with release of liens or collateral if applicable. Our system closely monitors the whole repayment process and solves any issues promptly to ensure the repayment proceeds arrive at lender accounts in a timely and accurate manner. It’s only up to this point that we consider our loan repayment service has been rendered, we then recognize revenue for repayment services upon the completion of the repayment services. Once loans are successfully repaid, we also retain borrowers’ repayment records through our online platform for a minimum of 3 to 5 years per regulatory requirement, as part of their credit profile and for reference in their future financing applications such as loan amount to be granted or interest rate charged.

Our platform is capable of monitoring and tracking payment activity. With built-in payment tracking functionality and automated missed payment notifications, the platform allows us to monitor the performance of outstanding loans on a real-time basis. Although we are not exposed to credit risks, we assist the investors in collection as a service to the investors.

In the event of a non- or partial repayment of a loan by the borrower, the third-party guarantor will primarily be responsible for the payment of the outstanding amount.

10

In the event the third-party guarantor defaults on the payment, we will pay the investor the sum owed from the reserve fund (See description of Risk Reserve Fund below) and then commence our collection proceedings. We may assist the guarantor with the sale or auction of collateral or directly initiate actions to recover payment from the guarantor and/or borrower.

Though there have been few cases since our platform’s inception where borrowers prepaid their loans, there are prepayment terms available in our agreement with borrowers and investors. If the borrowers prepay within 8 days before loan maturity, they still need to pay the full interests accrued as if the loans were repaid at the end of the loan term, which amounts are specified in the agreement when entered. If the borrowers prepay more than 8 days (inclusive) before loan maturity, they need to pay interests accrued up to the date of prepayment plus extra three days’ interests to the investors. In either case, however, according to our agreement, the borrowers would still be obligated to pay our platform the full amount of the loan repayment management fee as if the loans were repaid at the end of the loan term.

Third-Party Cooperative Partners Guarantees

Our cooperative partners are party to cooperation agreements. The performance by the cooperative partner is unconditional pursuant to the terms and conditions of the cooperation agreement.

Our management has been in the lending business for more than a decade and has established a network of industry resources including access to many financing guarantors who know many potential borrowers. Since inception in 2013, our online platform has established good brand awareness in the industry and some guarantors come to us proactively. We typically select qualified and sizable guarantors as our platform’s cooperative partners. They refer borrowers to us and assume financing guarantee responsibility. Factors we consider when selecting a cooperative guarantor include its license and qualification, total assets, business process, risk control capability and credit status etc. We conduct an Offline Anti-Fraud Investigation of guarantors by reviewing their credit history, legal disputes, and/or using third-party verifications. However, we do not perform a credit assessment of the guarantors like we perform for borrowers, therefore there are no underlying credit ratings for third-party guarantors. We will also conduct on-site due diligence and sign a cooperative agreement with the guarantor including acceptable methods of liens and collaterals. After that, the guarantor can start referring borrowers to our platform and provide loan guarantee. Guarantors usually charge a separate fee for their loan guarantee service. Guarantors will sign a separate loan guarantee agreement with borrowers and upon receipt of loan proceeds, borrowers will pay guarantors a separate guaranty fee, which is usually around 2% of the loan principal. This arrangement is made offline between the guarantors and borrowers.

Cooperative partners provide investigative reports on the veracity and credit condition of the borrower for every financing project being recommended. After the debt financing is provided to the borrower, the cooperative partner will monitor the borrower’s performance and will provide the platform with the feedback on the borrower’s credit condition, contract performance and debt repayment capabilities. For the financing project, which the cooperative partner has recommended, and has provided the guaranty, the cooperative partner will deposit a certain proportion of the loan into risk reserve fund, thereby fulfilling its duty with a cash deposit. The cooperative partner provides a guaranty letter/guaranty agreement for the financing project it has recommended, providing guaranty for the timely repayment of loans. The terms provided by the cooperation partner are the same terms offered by third-party guarantors who the borrower may propose to guarantee its loan.

Third-Party Creditor Loan Assignment Process

The process described above also applies to third-party creditors (“Creditor Partner(s)”) that seek to sell their rights as creditors on third-party loans with borrowers who are not borrowers on our platform (“Original Borrowers”). This service generated revenues in the amount of $1,740,693 and $493,975 in 2017 and 2016, respectively. Since the inception of the platform, no Original Borrower or Creditor Partner has defaulted on any loan payments, which would have required disbursement of funds from the risk reserve fund. In the loan assignment process, Creditor Partners assume the role of borrowers on our platform and revenues are recognized following the same revenue recognition policy as to other borrowers, which are classified under Revenues on our Income Statement. While the transaction process for Creditor Partners is largely similar to those for individuals and SME borrowers, there are certain procedural differences, as follows:

11

Step 1: Online Application Submission and Initial Assessment

Similar to individual and SME borrowers, Creditor Partners are required to open an account with us and send us the application materials before a third-party loan may be listed and sold on our platform. These Creditor Partners are usually the third-party cooperative partners discussed above, who refer borrowers to our platform and provide loan guarantee. As we have established cooperative relationships with these Creditor Partners, a prior determination has already been made that they have met our minimum requirements and no additional verification is conducted during the application process. Nonetheless, we re-evaluate these partners’ creditability from time to time, usually every one to three months.

Step 2: Offline Anti-Fraud Investigation and Credit Assessment

Since these Creditor Partners use our platform in order to transfer their rights on third-party loans that were made outside of our platform, they are responsible for conducting their own due diligence investigation into the Original Borrower’s credit-worthiness. Nonetheless, our risk control department conducts its own due diligence on the creditor’s rights sought to be sold and the Original Borrower’s credit-worthiness, using the same standards discussed above. As part of this process, our risk control department reviews the loan contract between the Creditor Partner and the Original Borrower to determine whether the Original Borrower has agreed to the proposed sale of creditor’s rights. We contact the Original Borrower directly to ensure that they have received notice of proposed sale from the Creditor Partner.

Step 3: Approval

Once the Creditor Partner is approved, we categorize the partner’s credit facility into one or more of the loan products discussed under “Step 3: Approval” above and post the loan on our platform. Investors will then have access to information regarding the Original Borrower, the rights that are being transferred, the collateral that secures the amounts borrowed, if any, and other details related to the right to transfer. We will also post the Creditor Partner’s “letter of promise,” which promises that they will guarantee the loans and require them deposit 2% to 5% of the loan amount into the risk reserve fund as usual.

Once a credit facility is accepted by an investor, our platform automatically prepares the necessary assignment documents for online execution by the parties.

Steps 4 to 6: Funding, Post-Funding Supervisory and Collections

The procedures of Funding, Post-Funding Supervisory and Collections are similar with those discussed above for individuals and SME’s. However, because the Creditor Partners usually have a high credit-rating due to their pre-established cooperative relationship with us, we do not require them to provide additional guarantees when they seek to sell their creditor rights on our platform. Therefore, in the event the Original Borrower defaults and the Creditor Partner also defaults on the payment, we will pay the investor the sum owed from the reserve fund (See description of Risk Reserve Fund below).

Fees

For our services that match investors and borrowers through our online platform, we typically charge borrowers and Creditor Partners a loan origination service fee between 1.5% to 3% of the loan amount facilitated by us (or proceeds of sale of the creditors’ rights, as the case may be) depending on, among other things, the duration of the loan. The loan origination service fee is payable when the borrowers or Creditor Partners receive the loans (or in the case of Creditor Partners, the proceeds of the sale of their creditors’ rights) in their accounts with Jiangxi Bank (or China PnR prior to July 2017), which will separate the loan origination service fee from the loan amount (or proceeds of sale, as the case may be) and send it to our account. Additionally, we charge a separate fee from borrowers for each loan repayment facilitated by us, which is based on an agreed upon percentage around 0.3% on the borrowing times the duration of the loan. The loan repayment management fee is payable when the borrower or Creditor Partner repays its loan. In a transaction involving the sale of a Credit Partner’s creditor’s rights, the amount of fees charged to the Credit Partner is the same as that charged to a borrower. In addition to the loan amount, they would have to deposit the repayment management fee to their accounts with Jiangxi Bank, who will allocate the loan repayment to the investors’ accounts and repayment management fee to our account. Currently, we do not charge any service fees to our investors.

12

Risk Management

Traditional risk management tools and the types of consumer finance data available in developed economies, such as widely available consumer credit reporting services, are currently at an early stage of development in China. We believe our risk management capabilities provide us with a competitive advantage in attracting capital to our marketplace by providing investors with the comfort that they are investing in high quality loans through a sustainable marketplace.

We primarily manage credit risk on behalf of the investors by doing the following:

i. We evaluate the borrower’s repayment ability utilizing our pre-transaction credit and fraud detection assessment using our big data credit assessment system. Our risk management model utilizes big data capabilities to automatically evaluate a borrower’s credit characteristics. Potential borrowers who do not meet our credit assessment grade will be denied loans.

ii. We offer a risk reserve fund which is 2-5% of all the credit extended to the borrowers (in December 2017, we have started to stop requiring new contributions from most of the borrowers and guarantors to the risk reserve fund. Existing reserve funds are being returned to borrowers and /or guarantors as loans mature and are repaid. See description of Risk Reserve Fund below).

iii. Each loan transaction facilitated on our platform is guaranteed by a third-party guarantor who is jointly and severally liable for the loan, except for the third-party loan assignment, in which case Creditor Partners seek to sell their rights as creditors on third-party loans with borrowers who are not borrowers on our platform. Since these Creditor Partners are usually our third-party cooperative partners with pre-established cooperative relationship with us, we do not require them to provide a third-party guarantor when they seek to sell their creditor rights on our platform. They will provide a “letter of promise,” which promises that they will guarantee the loan if the Original Borrower defaults and we require them to deposit 2% to 5% of the loan amount into the risk reserve fund as usual.

Risk management is the core task in the financial activities in which we engage. Our risk management department functions independently, creates detailed risk management policies, loan management rules, and operation manuals. The risk management department provides an independent expert assessment on the borrowers’ credentials in accordance with our loan policy and resolutely denies the applications of unqualified borrowers.

Credit review is a key part of risk management. The risk management department evaluates every application carefully without being affected by any subjective considerations. Determining the borrower’s credentials is a key principle in the credit review. With respect to an individual borrower’s loan application, the risk management department utilizes the risk management model for individual credit loans, and this model both realistically and effectively establishes 440 assessment points for comprehensive evaluations. Weighing different factors, this model requires the individual borrower to reach a threshold of 550 points in order to qualify for personal loans.

For business loans, the risk management department is required to perform on-site visits, inspect the business’ operating conditions, financial condition, use of loan proceeds, and the business owner’s individual reputations, among other factors. The risk management department first provides a risk assessment report and then approves a loan with respect to the underlying project.

In the internet era, our platform utilizes a third-party credit assessment system for our personal loan business. The borrower’s true financial condition and credit history provided by third-party credit assessment agencies greatly assist our evaluation of the borrower’s loan application. An important role of the risk management in the financial business is to minimize the risk of investor’s investment and to protect the safety of the platform.

A key aspect of the Company’s risk management is the full-tracking risk management. As a basic requirement of loan management, the risk management department sets up three management modules: pre-lending, during-lending, and post-lending. “Pre-lending management” emphasizes due diligence, including on-site inspections in order to obtain first-hand materials. “During-lending management” emphasizes standardized operations and execution of operating procedures according to the contract in order to avoid omissions or mistakes. “Post-lending management” emphasizes pre-warning mechanism and implements all-around debt collection mechanism for post-due debt, including on-site inspection, account review, control of material assets, exposure of delinquent activities, and legal recourse of litigation in order to protect the investor’s rights.

13

After the debt financing is provided to the borrower, the guarantor will monitor the borrower’s performance and will provide the platform with the feedback on the borrower’s credit condition, contract performance and debt repayment capabilities. In the event of any material development resulting in a negative turn in a borrower’s financial standing and potential ability to repay its loan, our management will determine the proper action to take to avert or minimize the risk of non-payment.

Finally, if enforcement action needs to be taken, we assist the investors in taking all legal recourse against the defaulted party. As an intermediary between the borrower and the investor, we deem ourselves to be independent from the debtor-creditor relationship and do not believe that we are a proper party to any lawsuits arising from the borrowers’ and/or guarantors’ defaults. However, we may offer necessary assistance to the investors, such as by disclosing the information of the borrowers and/or guarantors, provided that such disclosure is permitted under any relevant agreement and pertinent laws.

Risk Reserve Fund

In order to better protect our investors’ interests, we have voluntarily established a risk reserve fund which is generally equivalent to 2% to 5% of all credit extended to borrowers. The determination of the reserve fund ratio is made by referencing the overdue default loan data for the industry in which the borrower operates its business. Our risk control department starts with the industry default loan data and credit trend then adjusts it appropriately with information collected from current and past borrower profiles in the same industry on our platform, also taking into consideration communications with and updates from guarantors including changes in guarantee fees they charge borrowers and other measures they would take in providing guarantees. Based on the research results, the risk control department then sets the reserve fund ratio for the industry and reviews and adjusts it regularly if necessary, usually every quarter to six months. The risk reserve account is currently maintained with Jiangxi Bank and China Construction Bank. Under our risk reserve fund arrangement, if a loan is delinquent for a certain period of time, usually within three business days, we will withdraw a sum from the risk reserve fund to repay the investor.

Prior to an application for credit being made on our platform, the borrower (or if a guarantor is needed for the borrower, the guarantor) is required to provide an amount equal to 2% to 5% of the aggregate amount of the loan, which is deposited directly into the risk reserve fund. If the borrower cannot be matched with an investor within the fundraising period (no more than 19 days), all amounts deposited by the borrower or guarantor in the risk reserve fund, as the case may be, will be returned. If the borrower is successfully matched with an investor, the risk reserve fund will be refunded to the borrower if the loan is paid in full at maturity.

In the event that a borrower defaults in repaying the loan when it is due, we advise the guarantor of such default. If the guarantor cannot make the repayment within the period as stipulated (usually three days), we withdraw a sum equivalent to the outstanding loan amount with interest and penalty at a rate of 0.06% per day from the risk reserve fund to repay investors within three business days.

When more than one loan becomes delinquent and the borrower and/or guarantor fail(s) to repay investors, we will use the risk reserve fund to cover the loans in the order in which they become due. When deciding to draw upon the reserve fund to pay back an investor, we calculate the reserve fund to determine whether there are sufficient funds to repay. If the reserve fund is insufficient to repay investors, the fund shall be allocated on a pro rata basis. We notify investors and the third-party guarantors, or Creditor Partner, as the case may be, via website, text messages, email and then we implement a pre-set payment plan with the investors for each overdue loan transaction in which they receive their corresponding pro rata distribution of the reserve fund. In case of a default by a borrower, the investor bears the risk of not receiving a timely repayment or an investment failure, and the cooperative partners, through a series of protective measures, protect the investors’ interest to the maximum possible degree. The defaulting borrower and/or guarantor is/are obligated to reimburse the risk reserve fund account up to the outstanding loan amount owed with interest and penalty at a rate of 0.06% per day on the outstanding loan amount, which will be recorded as part of the balance of the risk reserve fund liability on our balance sheet. According to our Intermediary Service Agreement signed for each loan between the borrower, investors, and the platform, the interest and penalty are paid to investors for the period between the time of a borrower default and the time of a risk-reserve-fund repayment. After the repayment is withdrawn from the risk reserve fund, the guarantor is responsible for collecting loan repayments from the borrower and re-contributing funds to the risk reserve fund. Thus, the guarantor is entitled to the interest and penalty for this period of time.

14

Since the inception of the platform, no borrower has defaulted on any loan payments. All investors through the platform have timely received repayment of their investment funds. Our platform has not used the reserve fund to advance the repayment to investors, and our cooperative partners have not had to advance any payments as part of their obligation as guarantors.

As a transaction intermediary, we do not assume credit risk for the loans facilitated through our online platform and our risk reserve liability is limited to the balance of risk reserve fund that the borrowers or guarantors deposit with us. When loans that are facilitated through our online platform default, we do not record allowance for loan losses on our consolidated financial statements and if we use risk reserve fund to repay investors, we will make a footnote disclosure to risk reserve fund on withdraws for delinquent loans and subsequent reimbursements by borrowers or guarantors if any.

In March 2017, the Office of Task Force Responsible for Special Rectification of Risks in Internet Finance in Beijing issued Notice for Factual Acknowledge by and Rectification of Online Lending Information Intermediaries in Beijing (the “Notice”), pursuant to which, P2P platforms in Beijing are prohibited from setting up risk reserve fund or security fund for the purpose of providing guarantees to loans or promoting to investors regarding such types of funds. P2P platforms in Beijing have the same transition period to be compliant with the Notice as set forth in the Interim Measures.

Our PRC legal counsel has advised us that the Notice is still subject to further clarification and implementation measures for its enforcement, such as a clear definition of the risk reserve fund, and we believe P2P platforms in Beijing are prohibited from setting up and promoting risk reserve funds by committing their own capital. Our platform, however, sets up the risk reserve fund by requiring borrowers and/or guarantors to contribute their capital equal to 2% to 5% of the loan amount. Nevertheless, starting in December 2017, we have started to stop requiring new contributions from most of the borrowers and guarantors to the risk reserve fund, and stopped advertising the establishment of risk reserve funds on the platform. Existing reserve funds are being returned to borrowers and /or guarantors as loans mature and are repaid. As a result, we do not believe we are in violation of the Notice and there is currently no communication from regulatory agencies regarding such violation. We have not distributed a formal notice to our existing borrowers and/or guarantors about the regulations as the Notice is widely known, and it is expected that participants in this industry are aware of the Notice. If it is determined that we are in violation of the Notice, we would return the existing risk reserve contributions within the time frame provided by the regulatory agency. If there is no such time frame provided or required, we expect we would return the contributions in cash to our borrowers and guarantors within 3 to 5 business days or as soon thereafter as practicable.

As of December 31, 2017, balance of our risk reserve fund was approximately $ 12.1 million.

Information Technology & Cyber Security

Information technology is an important component of an internet company. We have an expert team possessing a depth of technical know-how and expertise, and we have carefully assembled a team of experts to operate the platform, communicate via the network, and for system maintenance.

Our technology team consists of three major working groups, responsible for different technical areas but at the same time mutually supportive of one another’s tasks. The structure working group is responsible for developing the system’s source code and constituting the system’s structure to meet the business needs. The testing working group is responsible for the necessary testing of the already developed operable system in order to examine its reliability and user’s experiences, thereby providing testing data and implementing needed modifications to the operating system. The operation maintenance working group is responsible for the necessary maintenance and inspection of the website’s technical system, including building fire wall, placing patches, preventing hackers’ attacks, thereby ensuring the normal operation of the system.

15

Our technology department has established a comprehensive system for managing web technology. To prevent external infiltration and theft of data and other illegal activities, we have established three levels of prevention mechanisms, thereby effectively implementing preventions from physical, technical, and authorization aspects.

Our system security protection is implemented from protective archiving and evaluation based on levels of information system security, disaster recovery, and information security. First, we have already entered into a cooperation agreement with Alibaba Cloud Computing, ensuring that the servers used on our platform are well protected and maintained. With respect to the data security on the platform’s computers, besides backing up all data with Alibaba Cloud Computing, our platform also backs up all operation data in order to prevent any data loss and ensure the reliable and prompt reading and retrieving data, therefore guaranteeing the normal operation of the platform.

As a platform used by both investors and borrowers, we have established an emergency response mechanism in the event of an emergency and built a back-up database in order to restore the platform’s operations and minimize downtime of the platform.

Our Products

As discussed above, we categorize the borrower credit facility into one or more loan products and post it on our platform. Those products include Xin Shou Zhuan Qu, Cai Fu Hui, Zun Xiang, Hui Ji Hua, You Xuan Zhai Quan, Zhai Quan Zhuan Rang and Hui Xiao Fei. For more detail regarding these products, please refer to the table listed under the “Step 3: Approval” of the transaction process.

Customers

Our customers comprise mainly Chinese individuals and SMEs. All of our investors are individuals while our borrowers include both individuals and SMEs. Our SME borrower clients are mainly from the heavy industry, wholesale, public transportation and restaurant industries. No one customer or group of customers’ accounts for 10% or more of our revenue. For the year ended December 31, 2017, SME borrowers and individual borrowers accounted for approximately 84.1% and 15.9% of the loan amounts facilitated through our platform, respectively.

Currently, most of our investors are in Shanghai, Shandong, Heilongjiang, Jiangsu, Henan and Jiangxi etc. provinces, and most of our borrowers are currently in Shandong province. All of our current borrowers are referred to us by our guarantors, whose businesses operate only in Mainland China. US-based investors and borrowers are prohibited from borrowing funds or being investors. Prospective borrowers and investors must be Chinese citizens or enterprises located in the PRC in order to register for an account and submit borrowing or investing applications through our platform. Our “Registration Agreement” and “Intermediary Service Agreement” also requires that the borrowers and investors represent and confirm that they are Chinese citizens or enterprises located in the PRC at the time of registration and submission of borrowing or investing applications, respectively, or they won’t be able to proceed. In addition, when submitting an application, a confirmation window will pop up, requesting borrowers or investors to confirm that they are located in the PRC before they can proceed with the submission. In the event that a non-PRC based citizen or enterprise is able to register and submit an application, upon our review of such application, including the implementation of our Step 1 and Step 2 protocols, such an application would be rejected and such registration would be terminated.

Marketing

The borrowers are made known to us primarily via two means, our own platform and referrals from third-party guarantors. The general public may get access to our platform and submit a borrower profile online. We also obtain borrowers through referrals from financial institutions we partner with. As of December 31, 2017, we have entered into cooperation agreements with 24 cooperative partners, including five pawn shops, four guaranty companies, a micro-loan company, an asset management company, three information technology companies, three financial consulting company, four technology companies, and three financial services companies. Besides online investors, we also attract investors through cooperative relationships with institutions. To obtain investors more efficiently, Benefactum Beijing has entered into co-operative agreements with third-party referral service providers, pursuant to which those service providers will refer potential investors to Benefactum Beijing while Benefactum Beijing will pay those service providers service fees based on the value of loans those referred investors actually lend through Benefactum Beijing.

16

Seasonality

We experience seasonality in our business, reflecting seasonal fluctuations in internet usage and traditional personal consumption patterns, as our individual borrowers typically use their borrowing proceeds to finance their personal consumption needs. For example, we generally experience lower transaction value on our online consumer finance marketplace during national holidays in China, particularly during the Chinese New Year holiday season in the first quarter of each year. While our rapid growth has somewhat masked this seasonality, our results of operations could be affected by such seasonality in the future.

Employees

As of December 31, 2017, we have 160 employees, located in Shanghai, Beijing and in Shandong province in China. The following table sets forth the number of our employees by function as of the same date:

| Functional Area | Number

of Employees |

% of Total | ||||||

| Senior management | 4 | 2.50 | % | |||||

| Product and service | 17 | 10.63 | % | |||||

| Marketing | 15 | 9.38 | % | |||||

| Human resources and administrative | 11 | 6.88 | % | |||||

| IT | 49 | 30.63 | % | |||||

| Accounting | 7 | 4.38 | % | |||||

| Legal | 2 | 1.25 | % | |||||

| Risk management | 24 | 15.00 | % | |||||

| Operations | 31 | 19.38 | % | |||||

| Total | 160 | 100 | % | |||||

As required by regulations in China, we participate in various employee social security plans that are organized by local governments, including pension, unemployment insurance, childbirth insurance, work-related injury insurance, medical insurance and housing insurance. We are required under Chinese law to make contributions to employee benefit plans at specified percentages of the salaries, bonuses and certain allowances of our employees, up to a maximum amount specified by the local government from time to time.

We believe that we maintain a good working relationship with our employees and to date, we have not experienced any significant labor disputes.

Competition

The online financial platform industry in China is intensely competitive. In light of the low barriers of entry in this industry, more players may enter this market which would result in increased competition. We anticipate that more established internet, technology and financial services companies that possess large, existing user bases, substantial financial resources and established distribution channels may enter the market in the future. Based on our research conducted in the database of Wang Dai Zhi Jia (www.wdzj.com), a third-party information platform that specializes in providing information in China’s internet finance industry, we believe the following companies are our major competitors in the various business segments set forth below:

Shanghai Lujiazui International Financial Assets Trading Market Inc. (“Lujinsuo”)- Lujinsuo is the only financial assets trading information service platform that runs its business through the trading platform of the State Counsel of China. It provides investment and financing services to SMEs and individuals. As of December 31, 2017, it had approximately 32.9 million registered users. Lujinsuo offers what is known as “financial instruments beneficial rights transfer” information services to financial and non-financial companies. This is a process in which the borrowers (usually companies) pledge their bank acceptance bills, and then transfer the beneficial interests to investors. Lujinsuo’s role is an informational intermediary between the holders of bank acceptance bills and the investors.

17

Yirendai Ltd. (“Yirendai”) – Yirendai is a leading online consumer financial platform in China connecting investors and individual borrowers. According to Yirendai reports, they facilitated RMB 47.41 billion ($7.29 billion) in loans from their inception in March 2012 through June 30, 2017. According to the database of Wang Dai Zhi Jia, Yirendai facilitated RMB 4.92 billion (approximately $755.94 million) in loans in December 2017 and was ranked the 7th in the industry. Leveraging the extensive experience of their parent company CreditEase, they have large client bases consisting of underserved investors and individual borrowers in China

Kaixindai Financing Service Jiangsu Co., Ltd. (“Kaixindai”) – Co-founded by China Development Bank, Kaixindai is a state-owned internet finance platform that aims at providing safe, stable and convenient internet lending intermediary services to SMEs and individuals. It facilitated RMB 41.88 billion (approximately $6.16 billion) in loans from December 2012 through June 2017. According to Wang Dai Zhi Jia, Kaixindai facilitated RMB 33.85 million (approximately $5.20 million) in loans in December 2017 and was ranked the 313th in the industry.

We also compete with other financial products and companies that attract borrowers, investors or both. With respect to borrowers, we compete with other online financial platforms and traditional financial institutions, such as financing business units in commercial banks, credit card issuers and other financing companies. With respect to investors, we primarily compete with other investment products and asset classes, such as equities, bonds, investment trust products, bank savings accounts and real estate.

Intellectual Property

Trademark

Our business is dependent on a combination of trademarks, trademark application, trade secrets and industry know-how, copyright and patent, in order to protect our intellectual property rights. We have submitted trademark and patent applications for “Benefactum Beijing” in mainland China.

Set forth below is a detailed description of our trademarks under application.

| Country | Trademark | Application Number | Classes* | Status | ||||

| Mainland China |  |

19915412 | 9 | Approved | ||||

| Mainland China | |

19915413 | 35 | Approved | ||||

| Mainland China | |

19915414 | 36 | Approved | ||||

| Mainland China | |

19915415 | 38 | Approved | ||||

| Mainland China | |

19915411 | 42 | Approved | ||||

| Mainland China |  |

16773973 | 36 | Approved | ||||

| Mainland China |  |

16774073 | 36 | Approved | ||||

| Mainland China |  |

17945485 | 36 | Approved | ||||

| Mainland China | |