Attached files

| file | filename |

|---|---|

| EX-32.02 - EXHIBIT 32.02 - NortonLifeLock Inc. | a063017exhibit3202.htm |

| EX-32.01 - EXHIBIT 32.01 - NortonLifeLock Inc. | a063017exhibit3201.htm |

| EX-31.02 - EXHIBIT 31.02 - NortonLifeLock Inc. | a063017exhibit3102.htm |

| EX-31.01 - EXHIBIT 31.01 - NortonLifeLock Inc. | a063017exhibit3101.htm |

| EX-10.04 - EXHIBIT 10.04 - NortonLifeLock Inc. | a063017exhibit1004.htm |

| EX-10.03 - EXHIBIT 10.03 - NortonLifeLock Inc. | a063017exhibit1003.htm |

| EX-10.02 - EXHIBIT 10.02 - NortonLifeLock Inc. | a063017exhibit1002.htm |

| EX-10.01 - EXHIBIT 10.01 - NortonLifeLock Inc. | a063017exhibit1001.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended June 30, 2017

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to

Commission File Number 000-17781

Symantec Corporation

(Exact name of the registrant as specified in its charter)

Delaware | 77-0181864 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer Identification no.) | |

350 Ellis Street | ||

Mountain View, California | 94043 | |

(Address of principal executive offices) | (Zip code) | |

Registrant’s telephone number, including area code:

(650) 527-8000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | Emerging growth company o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The number of shares of Symantec common stock, $0.01 par value per share, outstanding as of July 28, 2017 was 612,800,923 shares.

SYMANTEC CORPORATION

FORM 10-Q

Quarterly Period Ended June 30, 2017

TABLE OF CONTENTS

Page | ||

2

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

SYMANTEC CORPORATION

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited, in millions, except share amounts which are reflected in thousands, and par value per share amounts)

June 30, 2017 | March 31, 2017 (1) | ||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 2,306 | $ | 4,247 | |||

Accounts receivable, net | 468 | 649 | |||||

Other current assets | 399 | 428 | |||||

Total current assets | 3,173 | 5,324 | |||||

Property and equipment, net | 895 | 937 | |||||

Intangible assets, net | 2,892 | 3,004 | |||||

Goodwill | 8,638 | 8,627 | |||||

Equity investments | 158 | 158 | |||||

Other long-term assets | 112 | 124 | |||||

Total assets | $ | 15,868 | $ | 18,174 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 121 | $ | 180 | |||

Accrued compensation and benefits | 206 | 272 | |||||

Current portion of long-term debt | — | 1,310 | |||||

Deferred revenue | 2,329 | 2,353 | |||||

Income taxes payable | 22 | 30 | |||||

Other current liabilities | 443 | 477 | |||||

Total current liabilities | 3,121 | 4,622 | |||||

Long-term debt | 6,202 | 6,876 | |||||

Long-term deferred revenue | 465 | 434 | |||||

Deferred income tax liabilities | 2,332 | 2,401 | |||||

Long-term income taxes payable | 261 | 251 | |||||

Other long-term obligations | 98 | 103 | |||||

Total liabilities | 12,479 | 14,687 | |||||

Commitments and contingencies | |||||||

Stockholders’ equity: | |||||||

Preferred stock, $0.01 par value: 1,000 shares authorized; 21 shares issued; 0 outstanding | — | — | |||||

Common stock and additional paid-in capital, $0.01 par value: 3,000,000 shares authorized; 610,991 and 608,019 shares issued and outstanding, respectively | 4,273 | 4,236 | |||||

Accumulated other comprehensive income | 10 | 12 | |||||

Accumulated deficit | (894 | ) | (761 | ) | |||

Total stockholders’ equity | 3,389 | 3,487 | |||||

Total liabilities and stockholders’ equity | $ | 15,868 | $ | 18,174 | |||

(1) | Derived from audited financial statements. |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

3

SYMANTEC CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, in millions, except per share amounts)

Three Months Ended | |||||||

June 30, 2017 | July 1, 2016 | ||||||

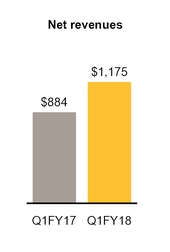

Net revenues | $ | 1,175 | $ | 884 | |||

Cost of revenues | 257 | 149 | |||||

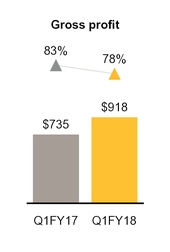

Gross profit | 918 | 735 | |||||

Operating expenses: | |||||||

Sales and marketing | 433 | 291 | |||||

Research and development | 233 | 170 | |||||

General and administrative | 149 | 84 | |||||

Amortization of intangible assets | 59 | 14 | |||||

Restructuring, transition and other | 88 | 70 | |||||

Total operating expenses | 962 | 629 | |||||

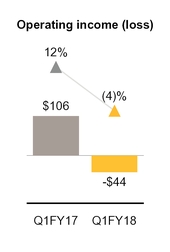

Operating income (loss) | (44 | ) | 106 | ||||

Interest income | 6 | 5 | |||||

Interest expense | (84 | ) | (27 | ) | |||

Other income (expense), net | (12 | ) | 13 | ||||

Income (loss) from continuing operations before income taxes | (134 | ) | 97 | ||||

Income tax expense (benefit) | (24 | ) | 31 | ||||

Income (loss) from continuing operations | (110 | ) | 66 | ||||

Income (loss) from discontinued operations, net of income taxes | (23 | ) | 69 | ||||

Net income (loss) | $ | (133 | ) | $ | 135 | ||

Income (loss) per share - basic: | |||||||

Continuing operations | $ | (0.18 | ) | $ | 0.11 | ||

Discontinued operations | $ | (0.04 | ) | $ | 0.11 | ||

Net income (loss) per share - basic | $ | (0.22 | ) | $ | 0.22 | ||

Income (loss) per share - diluted: | |||||||

Continuing operations | $ | (0.18 | ) | $ | 0.11 | ||

Discontinued operations | $ | (0.04 | ) | $ | 0.11 | ||

Net income (loss) per share - diluted | $ | (0.22 | ) | $ | 0.22 | ||

Weighted-average shares outstanding: | |||||||

Basic | 609 | 613 | |||||

Diluted | 609 | 620 | |||||

Cash dividends declared per common share | $ | 0.075 | $ | 0.075 | |||

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

4

SYMANTEC CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited, in millions)

Three Months Ended | |||||||

June 30, 2017 | July 1, 2016 | ||||||

Net income (loss) | $ | (133 | ) | $ | 135 | ||

Other comprehensive income (loss), net of taxes: | |||||||

Foreign currency translation adjustments | (2 | ) | (24 | ) | |||

Unrealized loss on available-for-sale securities | — | (1 | ) | ||||

Other comprehensive income (loss), net of taxes | (2 | ) | (25 | ) | |||

Comprehensive income (loss) | $ | (135 | ) | $ | 110 | ||

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

5

SYMANTEC CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in millions)

Three Months Ended | |||||||

June 30, 2017 | July 1, 2016 | ||||||

OPERATING ACTIVITIES: | |||||||

Net income (loss) | $ | (133 | ) | $ | 135 | ||

(Income) loss from discontinued operations, net of income taxes | 23 | (69 | ) | ||||

Adjustments to continuing operating activities: | |||||||

Depreciation and amortization, including debt issuance costs and discounts | 191 | 72 | |||||

Stock-based compensation expense | 147 | 49 | |||||

Deferred income taxes | (62 | ) | 33 | ||||

Other | 14 | 27 | |||||

Changes in operating assets and liabilities, net of acquisitions: | |||||||

Accounts receivable, net | 188 | 244 | |||||

Accounts payable | (32 | ) | (63 | ) | |||

Accrued compensation and benefits | (68 | ) | (52 | ) | |||

Deferred revenue | (21 | ) | (139 | ) | |||

Income taxes | 40 | (940 | ) | ||||

Other assets | 3 | (2 | ) | ||||

Other liabilities | (39 | ) | (35 | ) | |||

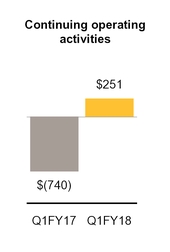

Net cash provided by (used in) continuing operating activities | 251 | (740 | ) | ||||

Net cash used in discontinued operating activities | (38 | ) | (30 | ) | |||

Net cash provided by (used in) operating activities | 213 | (770 | ) | ||||

INVESTING ACTIVITIES: | |||||||

Additions to property and equipment | (47 | ) | (22 | ) | |||

Payments for acquisitions, net of cash acquired | (8 | ) | — | ||||

Proceeds from maturities and sales of short-term investments | — | 30 | |||||

Other | 1 | 7 | |||||

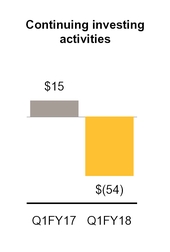

Net cash provided by (used in) investing activities | (54 | ) | 15 | ||||

FINANCING ACTIVITIES: | |||||||

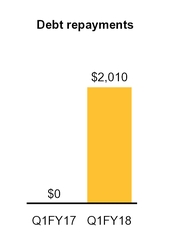

Repayments of debt and other obligations | (2,010 | ) | (17 | ) | |||

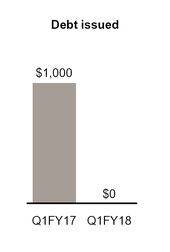

Proceeds from issuance of debt, net of issuance costs | — | 994 | |||||

Net proceeds from sales of common stock under employee stock benefit plans | 11 | 1 | |||||

Tax payments related to restricted stock units | (61 | ) | (24 | ) | |||

Dividends and dividend equivalents paid | (66 | ) | (68 | ) | |||

Other | — | 10 | |||||

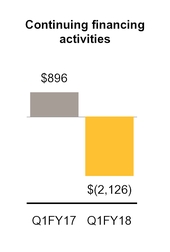

Net cash provided by (used in) financing activities | (2,126 | ) | 896 | ||||

Effect of exchange rate fluctuations on cash and cash equivalents | 26 | (16 | ) | ||||

Change in cash and cash equivalents | (1,941 | ) | 125 | ||||

Beginning cash and cash equivalents | 4,247 | 5,983 | |||||

Ending cash and cash equivalents | $ | 2,306 | $ | 6,108 | |||

Supplemental disclosure of cash flow information | |||||||

Income taxes paid, net of refunds | $ | 39 | $ | 953 | |||

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

6

SYMANTEC CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1. Description of Business and Significant Accounting Policies

Business

Symantec Corporation (“Symantec,” “we,” “us,” “our,” and the “Company” refer to Symantec Corporation and all of its subsidiaries) is a global leader in cybersecurity.

On August 1, 2016, we completed our acquisition of Blue Coat, Inc. (“Blue Coat”). On February 9, 2017, we completed our acquisition of LifeLock, Inc. (“LifeLock”). Blue Coat and LifeLock have been included in our consolidated results of operations since their respective acquisition dates.

Basis of presentation

The accompanying unaudited Condensed Consolidated Financial Statements have been prepared in accordance with generally accepted accounting principles (“GAAP”) in the United States of America (“U.S.”) for interim financial information. In the opinion of management, the unaudited Condensed Consolidated Financial Statements contain all adjustments, consisting only of normal recurring items, except as otherwise noted, necessary for the fair presentation of our financial position, results of operations, and cash flows for the interim periods. These unaudited Condensed Consolidated Financial Statements should be read in conjunction with the audited Consolidated Financial Statements and accompanying Notes thereto included in our Annual Report on Form 10-K for the fiscal year ended March 31, 2017. The results of operations for the three months ended June 30, 2017 are not necessarily indicative of the results expected for the entire fiscal year.

We have a 52/53-week fiscal year ending on the Friday closest to March 31. Unless otherwise stated, references to three month ended periods in this report relate to fiscal periods ended June 30, 2017 and July 1, 2016. The three months ended June 30, 2017 and July 1, 2016 each consisted of 13 weeks. Our 2018 fiscal year consists of 52 weeks and ends on March 30, 2018.

Recently adopted authoritative guidance

Employee Stock-Based Compensation. In the first quarter of fiscal 2018, we adopted new guidance to simplify accounting for share-based payment transactions. Prior to adoption, excess tax benefits resulting from the difference between the deduction for tax purposes and the compensation costs recognized for financial reporting were not recognized until the deduction reduced taxes payable. As a result of the new guidance, we now recognize excess tax benefits in the current accounting period. In addition, we elected to continue to estimate forfeitures rather than record the forfeitures as they occur. We adopted the change in accounting method using the modified retrospective method. We also elected to retrospectively apply the change in presentation of excess tax benefits recognized on stock-based compensation expense in our Condensed Consolidated Statements of Cash Flows from financing activities to operating activities. The cumulative effect of adopting the new accounting guidance was not material.

There have been no other material changes in our significant accounting policies as of and for the three months ended June 30, 2017, as compared to the significant accounting policies described in our Annual Report on Form 10-K for the fiscal year ended March 31, 2017.

Note 2. Segment Information

We have the following two reporting segments, which are the same as our operating segments:

• | Enterprise Security. Our Enterprise Security segment protects organizations so they can securely conduct business while leveraging new platforms and data. Our Enterprise Security segment includes our threat protection products, information protection products, cyber security services, website security and advanced web and cloud security offerings. Our enterprise endpoint and network security and management offerings support evolving endpoints and networks, providing advanced threat protection while helping reduce cost and complexity. These solutions are delivered through various methods, such as software, appliance, Software-as-a-Service (“SaaS”) and managed services. |

• | Consumer Digital Safety. Our Consumer Digital Safety segment focuses on providing a Digital Safety solution to protect information, devices, networks and the identities of consumers. This platform includes our Norton-branded services, which provide multi-layer security and identity protection on major desktop and mobile operating systems, to defend against increasingly complex online threats to individuals, families and small businesses. With the addition of LifeLock-branded identity protection services, we are accelerating our leadership in Consumer Digital Safety to protect all aspects of the consumer’s digital life. |

Operating segments are based upon the nature of our business and how our business is managed. Our Chief Operating Decision Makers (“CODM”), comprised of our Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”), use operating segment financial information to evaluate segment performance and to allocate resources.

7

There were no inter-segment sales for the periods presented. The following table summarizes the operating results of our reporting segments:

Three Months Ended | |||||||

(In millions) | June 30, 2017 | July 1, 2016 | |||||

Total Segments: | |||||||

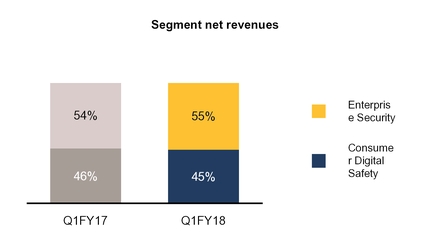

Net revenues | $ | 1,175 | $ | 884 | |||

Operating income | $ | 324 | $ | 253 | |||

Enterprise Security: | |||||||

Net revenues | $ | 646 | $ | 481 | |||

Operating income | $ | 94 | $ | 28 | |||

Consumer Digital Safety: | |||||||

Net revenues | $ | 529 | $ | 403 | |||

Operating income | $ | 230 | $ | 225 | |||

We do not allocate to our operating segments certain operating expenses that we manage separately at the corporate level and are not used in evaluating the results of, or in allocating resources to, our segments. These unallocated expenses consist of stock-based compensation expense, amortization of intangible assets, restructuring, transition and other charges, and acquisition and integration costs.

The following table provides a reconciliation of our total reportable segments’ operating income to our total operating income (loss):

Three Months Ended | |||||||

(In millions) | June 30, 2017 | July 1, 2016 | |||||

Total segment operating income | $ | 324 | $ | 253 | |||

Reconciling items: | |||||||

Stock-based compensation expense | 147 | 49 | |||||

Amortization of intangible assets | 114 | 20 | |||||

Restructuring, transition and other | 88 | 70 | |||||

Acquisition and integration costs | 19 | 8 | |||||

Total consolidated operating income (loss) from continuing operations | $ | (44 | ) | $ | 106 | ||

Note 3. Net Income (Loss) Per Share

Basic and diluted net income (loss) per share are computed on the basis of the weighted-average number of shares of common stock outstanding during the period. In the first quarter of fiscal 2017, diluted net income (loss) per share also includes the incremental effect of dilutive potential common shares outstanding during the period using the treasury stock method. Dilutive potential common shares include the dilutive effect of the shares’ underlying outstanding stock options, restricted stock units (“RSUs”), performance-based restricted stock units (“PRUs”), Employee Stock Purchase Plan (“ESPP”) and convertible notes. See Note 10 for more information on our stock-based compensation.

8

The components of net income (loss) per share are as follows:

Three Months Ended | |||||||

(In millions, except per share data) | June 30, 2017 | July 1, 2016 | |||||

Income (loss) from continuing operations | $ | (110 | ) | $ | 66 | ||

Income (loss) from discontinued operations, net of income taxes | (23 | ) | 69 | ||||

Net income (loss) | $ | (133 | ) | $ | 135 | ||

Income (loss) per share - basic: | |||||||

Continuing operations | $ | (0.18 | ) | $ | 0.11 | ||

Discontinued operations | $ | (0.04 | ) | $ | 0.11 | ||

Net income (loss) per share - basic | $ | (0.22 | ) | $ | 0.22 | ||

Income (loss) per share - diluted: | |||||||

Continuing operations | $ | (0.18 | ) | $ | 0.11 | ||

Discontinued operations | $ | (0.04 | ) | $ | 0.11 | ||

Net income (loss) per share - diluted | $ | (0.22 | ) | $ | 0.22 | ||

Weighted-average shares outstanding - basic | 609 | 613 | |||||

Dilutive potential shares | — | 7 | |||||

Weighted-average shares outstanding - diluted | 609 | 620 | |||||

The following have been excluded from the computation of diluted net income (loss) per share because their effect would have been anti-dilutive:

As of | |||||

(In millions) | June 30, 2017 | July 1, 2016 | |||

Convertible shares | 91 | — | |||

RSUs and PRUs | 33 | 2 | |||

Stock options and ESPP | 20 | — | |||

Total | 144 | 2 | |||

Under the treasury stock method, our Convertible Senior Notes will generally have a dilutive impact on earnings when our average stock price for the period exceeds approximately $16.77 per share for the 2.5% Convertible Senior Notes and $20.41 per share for the 2.0% Convertible Senior Notes. During the three months ended June 30, 2017, the conversion feature of both notes was anti-dilutive due to a loss from continuing operations.

Note 4. Restructuring, Transition and Other Costs

Our restructuring, transition and other costs and liabilities consist primarily of severance, facilities, transition and other related costs. Severance costs generally include severance payments, outplacement services, health insurance coverage, and legal costs. Included in other exit and disposal costs are advisory fees incurred in connection with restructuring events and consulting and disentanglement costs to prune selected lines of business that do not fit either our growth, margin or strategic objectives. Facilities costs, which are also included in other exit and disposal costs, generally include rent expense and lease termination costs, less estimated sublease income. Transition costs primarily consist of consulting charges associated with the implementation of new enterprise resource planning systems and costs to automate business processes. Restructuring, transition and other costs are managed at the corporate level and are not allocated to our reportable segments. See Note 2 for information regarding the reconciliation of total segment operating income to total consolidated operating income (loss).

Fiscal 2017 Plan

We initiated a restructuring plan in the first quarter of fiscal 2017 to reduce complexity by means of long-term structural improvements (the “Fiscal 2017 Plan”). We expect to reduce headcount and close certain facilities in connection with the restructuring plan. We expect total costs incurred in connection with the Fiscal 2017 Plan to range between $430 million and $480 million, of which approximately $185 million to $195 million is expected to be for severance and termination benefits and $205 million to $230 million is expected to be for other exit and disposal costs primarily consisting of contract termination and relocation costs and advisory fees. The remainder is expected to be in the form of asset write-offs. These actions are expected to be completed in fiscal 2018. As of June 30, 2017, liabilities for excess facility obligations at several locations around the world are expected to be paid throughout the respective lease terms, the longest of which extends through fiscal 2022. Additionally, we expect continuing significant transition costs associated with the implementation of a new enterprise resource planning system and costs to automate business processes.

9

Restructuring, transition and other costs summary

For the three months ended June 30, 2017 we incurred the following restructuring, transition and other costs:

(In millions) | June 30, 2017 | ||

Severance and termination costs | $ | 27 | |

Other exit and disposal costs | 32 | ||

Asset write-offs | 1 | ||

Transition costs | 28 | ||

Total restructuring, transition and other | $ | 88 | |

Restructuring liabilities summary

As of June 30, 2017 and March 31, 2017, the restructuring liabilities are included in accounts payable, other current liabilities and other long-term obligations in our Condensed Consolidated Balance Sheets.

(In millions) | Balance as of March 31, 2017 | Costs, Net of Adjustments | Cash Payments | Non-Cash Charges | Balance as of June 30, 2017 | Cumulative Incurred to Date for FY17 Plan | |||||||||||||||||

Severance and termination costs | $ | 20 | $ | 27 | $ | (32 | ) | $ | — | $ | 15 | $ | 103 | ||||||||||

Other exit and disposal costs | 26 | 32 | (20 | ) | (7 | ) | 31 | 111 | |||||||||||||||

Asset write-offs | — | 1 | — | (1 | ) | — | 24 | ||||||||||||||||

Total | $ | 46 | $ | 60 | $ | (52 | ) | $ | (8 | ) | $ | 46 | $ | 238 | |||||||||

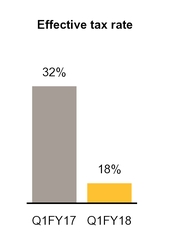

Note 5. Income Taxes

The following table summarizes our effective tax rate for income (loss) from continuing operations for the periods presented:

Three Months Ended | |||||||

(In millions, except percentages) | June 30, 2017 | July 1, 2016 | |||||

Income (loss) from continuing operations before income taxes | $ | (134 | ) | $ | 97 | ||

Income tax expense (benefit) | $ | (24 | ) | $ | 31 | ||

Effective tax rate | 18 | % | 32 | % | |||

Our effective tax rate for loss from continuing operations for the three months ended June 30, 2017 differs from the federal statutory income tax rate primarily due to the benefits of lower-taxed international earnings, the research and development tax credit, and excess tax benefits related to stock-based compensation, partially offset by various permanent differences.

Our effective tax rate for income from continuing operations for the three months ended July 1, 2016 differs from the federal statutory income tax rate primarily due to the benefits of lower-taxed international earnings, domestic manufacturing incentives and the research and development tax credit, partially offset by state income taxes.

For the three months ended June 30, 2017, we recorded income tax expense on discontinued operations of $41 million. For the three months ended July 1, 2016, we recorded income tax expense on discontinued operations of $16 million. See Note 12 for further details regarding discontinued operations.

We are a U.S.-based multinational company subject to tax in multiple U.S. and international tax jurisdictions. A substantial portion of our international earnings were generated from subsidiaries organized in Ireland and Singapore. Our results of operations would be adversely affected to the extent that our geographical mix of income becomes more weighted toward jurisdictions with higher tax rates and would be favorably affected to the extent the relative geographic mix shifts to lower tax jurisdictions. Any change in our mix of earnings is dependent upon many factors and is therefore difficult to predict.

The timing of the resolution of income tax examinations is highly uncertain, and the amounts ultimately paid, if any, upon resolution of the issues raised by the taxing authorities may differ materially from the amounts accrued for each year. Although potential resolution of uncertain tax positions involve multiple tax periods and jurisdictions, it is reasonably possible that the gross unrecognized tax benefits related to these audits could decrease, whether by payment, release, or a combination of both, in the next 12 months by $12 million, which could reduce our income tax provision and therefore benefit the resulting effective tax rate.

We continue to monitor the progress of ongoing income tax controversies and the impact, if any, of the expected expiration of the statute of limitations in various taxing jurisdictions.

10

Note 6. Goodwill and Intangible Assets

Goodwill

The changes in the carrying amount of goodwill by segment are as follows:

(In millions) | Consumer Digital Safety | Enterprise Security | Total | ||||||||

Net balance as of March 31, 2017 | $ | 2,549 | $ | 6,078 | $ | 8,627 | |||||

Acquisitions | 2 | 5 | 7 | ||||||||

Translation adjustments | 1 | 3 | 4 | ||||||||

Net balance as of June 30, 2017 | $ | 2,552 | $ | 6,086 | $ | 8,638 | |||||

Intangible assets, net

June 30, 2017 | March 31, 2017 | ||||||||||||||||||||||

(In millions) | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | |||||||||||||||||

Customer relationships | $ | 1,650 | $ | (382 | ) | $ | 1,268 | $ | 1,646 | $ | (322 | ) | $ | 1,324 | |||||||||

Developed technology | 1,007 | (284 | ) | 723 | 1,006 | (229 | ) | 777 | |||||||||||||||

Finite-lived trade names and other | 46 | (28 | ) | 18 | 46 | (26 | ) | 20 | |||||||||||||||

Total finite-lived intangible assets | 2,703 | (694 | ) | 2,009 | 2,698 | (577 | ) | 2,121 | |||||||||||||||

Indefinite-lived trade names | 864 | — | 864 | 864 | — | 864 | |||||||||||||||||

In-process research and development | 19 | — | 19 | 19 | — | 19 | |||||||||||||||||

Total intangible assets | $ | 3,586 | $ | (694 | ) | $ | 2,892 | $ | 3,581 | $ | (577 | ) | $ | 3,004 | |||||||||

As of June 30, 2017, future amortization expense related to intangible assets that have finite lives is as follows by fiscal year:

(In millions) | June 30, 2017 | ||

Remainder of 2018 | $ | 337 | |

2019 | 428 | ||

2020 | 407 | ||

2021 | 296 | ||

2022 | 235 | ||

Thereafter | 306 | ||

Total | $ | 2,009 | |

11

Note 7. Debt

The following table summarizes components of our debt:

(In millions, except percentages) | June 30, 2017 | March 31, 2017 | Effective Interest Rate | |||||||

2.75% Senior Notes due June 15, 2017 | $ | — | $ | 600 | 2.79 | % | ||||

Senior Term Loan A-1 due May 10, 2019 | 800 | 1,000 | LIBOR plus (1) | |||||||

Senior Term Loan A-2 due August 1, 2019 | 800 | 800 | LIBOR plus (1) | |||||||

Senior Term Loan A-3 due August 1, 2019 | 200 | 200 | LIBOR plus (1) | |||||||

4.2% Senior Notes due September 15, 2020 | 750 | 750 | 4.25 | % | ||||||

2.5% Convertible Senior Notes due April 1, 2021 | 500 | 500 | 3.76 | % | ||||||

Senior Term Loan A-5 due August 1, 2021 | 500 | 1,710 | LIBOR plus (1) | |||||||

2.0% Convertible Senior Notes due August 15, 2021 | 1,250 | 1,250 | 2.66 | % | ||||||

3.95% Senior Notes due June 15, 2022 | 400 | 400 | 4.05 | % | ||||||

5.0% Senior Notes due April 15, 2025 | 1,100 | 1,100 | 5.23 | % | ||||||

Total principal amount | 6,300 | 8,310 | ||||||||

Less: Unamortized discount and issuance costs | (98 | ) | (124 | ) | ||||||

Total debt | 6,202 | 8,186 | ||||||||

Less: Current portion | — | (1,310 | ) | |||||||

Total long-term portion | $ | 6,202 | $ | 6,876 | ||||||

(1) | The senior term facilities bear interest at a rate equal to the London Interbank Offered Rate (“LIBOR”) plus a margin of 1.50% to 1.75% based on the current debt rating of our non-credit-enhanced, senior unsecured long-term debt and our underlying loan agreements. |

The future maturities of debt by fiscal year are as follows as of June 30, 2017:

(In millions) | June 30, 2017 | |||

Remainder of 2018 | $ | — | ||

2019 | — | |||

2020 | 1,800 | |||

2021 | 1,250 | |||

2022 | 1,750 | |||

Thereafter | 1,500 | |||

Total future maturities of debt | $ | 6,300 | ||

Debt repayments

We prepaid principal amounts of $1.2 billion of our Senior Term Loan A-5 and $200 million of our Senior Term Loan A-1 during the first quarter of fiscal 2018. In addition, during the first quarter of fiscal 2018, the $600 million principal balance of our 2.75% Senior Notes due June 15, 2017 matured and was settled by a cash payment.

Note 8. Fair Value Measurements

Assets measured and recorded at fair value on a recurring basis

Our cash equivalents consist primarily of money market funds with original maturities of three months or less at the time of purchase, and the carrying amount is a reasonable estimate of fair value. Our short-term investments consist of investment securities with original maturities greater than three months and marketable equity securities, and are included in our other current assets in the Condensed Consolidated Balance Sheets.

12

The following table summarizes our assets measured at fair value on a recurring basis, by level, within the fair value hierarchy:

June 30, 2017 | March 31, 2017 | ||||||||||||||||||||||

(In millions) | Fair Value | Cash and Cash Equivalents | Short-Term Investments | Fair Value | Cash and Cash Equivalents | Short-Term Investments | |||||||||||||||||

Cash | $ | 480 | $ | 480 | $ | — | $ | 1,183 | $ | 1,183 | $ | — | |||||||||||

Non-negotiable certificates of deposit | 39 | 39 | — | 15 | 15 | — | |||||||||||||||||

Level 1 (Quoted prices in active markets for identical assets): | |||||||||||||||||||||||

Money market | 1,298 | 1,298 | — | 2,532 | 2,532 | — | |||||||||||||||||

U.S. government securities | 102 | 102 | — | 94 | 94 | — | |||||||||||||||||

Marketable equity securities | 8 | — | 8 | 9 | — | 9 | |||||||||||||||||

Total level 1 | 1,408 | 1,400 | 8 | 2,635 | 2,626 | 9 | |||||||||||||||||

Level 2 (Significant other observable inputs): | |||||||||||||||||||||||

U.S. agency securities | 64 | 64 | — | 75 | 75 | — | |||||||||||||||||

Commercial paper | 323 | 323 | — | 348 | 348 | — | |||||||||||||||||

Total level 2 | 387 | 387 | — | 423 | 423 | — | |||||||||||||||||

Total | $ | 2,314 | $ | 2,306 | $ | 8 | $ | 4,256 | $ | 4,247 | $ | 9 | |||||||||||

There were no transfers between fair value measurement levels during the three months ended June 30, 2017.

Fair value of debt

As of June 30, 2017 and March 31, 2017, the total fair value of our debt was $6.4 billion and $8.3 billion, respectively, based on Level 2 inputs.

Note 9. Stockholders' Equity

Dividends

The following table summarizes dividends declared and paid and dividend equivalents paid for the periods presented:

Three Months Ended | |||||||

(In millions, except per share data) | June 30, 2017 | July 1, 2016 | |||||

Dividends declared and paid | $ | 46 | $ | 46 | |||

Dividend equivalents paid | 20 | 22 | |||||

Total dividends and dividend equivalents paid | $ | 66 | $ | 68 | |||

Cash dividends declared per common share | $ | 0.075 | $ | 0.075 | |||

Our RSUs and PRUs are entitled to dividend equivalents to be paid in the form of cash upon vesting for each share of the underlying unit.

On August 2, 2017, we declared a cash dividend of $0.075 per share of common stock to be paid on September 13, 2017 to all stockholders of record as of the close of business on August 21, 2017. All shares of common stock issued and outstanding and all shares of unvested restricted stock and performance-based stock as of the record date will be entitled to the dividend and dividend equivalents, respectively. Any future dividends and dividend equivalents will be subject to the approval of our Board.

13

Stock repurchase program

As of June 30, 2017, the remaining balance of our share repurchase authorization is $800 million and does not have an expiration date.

Accelerated stock repurchase agreement

During the fourth quarter of fiscal 2017, we entered into an accelerated stock repurchase (“ASR”) agreement with financial institutions to repurchase an aggregate of $500 million of our common stock. Pursuant to the ASR agreement, we made an upfront payment of $500 million to the financial institutions and received and retired an initial delivery of 14.2 million shares of our common stock. In the first quarter of fiscal 2018, we completed the ASR and received and retired an additional delivery of 2.2 million shares of our common stock. The total shares received and retired under the terms of the ASR agreement were 16.4 million, with an average price paid per share of $30.51.

Changes in accumulated other comprehensive income by component

Components of accumulated other comprehensive income, on a net of tax basis, were as follows:

(In millions) | Foreign Currency Translation Adjustments | Unrealized Gain on Available-For-Sale Securities | Total | ||||||||

Balance as of March 31, 2017 | $ | 7 | $ | 5 | $ | 12 | |||||

Other comprehensive loss before reclassifications | (2 | ) | — | (2 | ) | ||||||

Balance as of June 30, 2017 | $ | 5 | $ | 5 | $ | 10 | |||||

Note 10. Stock-Based Compensation

Stock-based compensation expense

The following table presents the stock-based compensation expense recognized in our Condensed Consolidated Statements of Operations:

Three Months Ended | |||||||

(In millions) | June 30, 2017 | July 1, 2016 | |||||

Cost of revenues | $ | 6 | $ | 3 | |||

Sales and marketing | 43 | 14 | |||||

Research and development | 41 | 15 | |||||

General and administrative | 57 | 17 | |||||

Total stock-based compensation expense | 147 | 49 | |||||

Tax benefit associated with stock-based compensation expense | (51 | ) | (15 | ) | |||

Total net stock-based compensation expense | $ | 96 | $ | 34 | |||

14

The following table summarizes additional information related to our stock-based compensation:

Three Months Ended | |||||||

(In millions, except per grant data) | June 30, 2017 | July 1, 2016 | |||||

Restricted stock units: | |||||||

Weighted-average fair value per grant | $ | 29.91 | $ | 17.30 | |||

Awards granted | 7.1 | 8.5 | |||||

Total fair value of awards released | $ | 170 | $ | 77 | |||

Total unrecognized compensation expense | $ | 370 | $ | 273 | |||

Weighted-average remaining vesting period | 2.0 years | 2.2 years | |||||

Performance-based restricted stock units: | |||||||

Weighted-average fair value per grant | $ | 33.96 | $ | 17.30 | |||

Awards granted | 2.5 | 1.3 | |||||

Total fair value of awards released | $ | 21 | $ | 2 | |||

Total unrecognized compensation expense | $ | 191 | $ | 44 | |||

Weighted-average remaining vesting period | 1.4 years | 1.5 years | |||||

Stock options: | |||||||

Total intrinsic value of stock options exercised | $ | 17 | $ | — | |||

Total unrecognized compensation expense | $ | 119 | $ | — | |||

Weighted-average remaining vesting period | 1.4 years | — | |||||

Note 11. Commitments and Contingencies

Indemnifications

In the ordinary course of business, we may provide indemnifications of varying scope and terms to customers, vendors, lessors, business partners, subsidiaries and other parties with respect to certain matters, including, but not limited to, losses arising out of our breach of agreements or representations and warranties made by us. In addition, our bylaws contain indemnification obligations to our directors, officers, employees and agents, and we have entered into indemnification agreements with our directors and certain of our officers to give such directors and officers additional contractual assurances regarding the scope of the indemnification set forth in our bylaws and to provide additional procedural protections. We maintain director and officer insurance, which may cover certain liabilities arising from our obligation to indemnify our directors and officers. It is not possible to determine the aggregate maximum potential loss under these indemnification agreements due to the limited history of prior indemnification claims and the unique facts and circumstances involved in each particular agreement. Such indemnification agreements might not be subject to maximum loss clauses. Historically, we have not incurred material costs as a result of obligations under these agreements and we have not accrued any liabilities related to such indemnification obligations in our Condensed Consolidated Financial Statements.

In connection with the sale of our former information management business (“Veritas”), we assigned several leases to Veritas Technologies LLC or its related subsidiaries. As a condition to consenting to the assignments, certain lessors required us to agree to indemnify the lessor under the applicable lease with respect to certain matters, including, but not limited to, losses arising out of Veritas Technologies LLC or its related subsidiaries’ breach of payment obligations under the terms of the lease. As with our other indemnification obligations discussed above and in general, it is not possible to determine the aggregate maximum potential loss under these indemnification agreements due to the limited history of prior indemnification claims and the unique facts and circumstances involved in each particular agreement. As with our other indemnification obligations, such indemnification agreements might not be subject to maximum loss clauses and to date, generally under our real estate obligations, we have not incurred material costs as a result of such obligations under our leases and have not accrued any liabilities related to such indemnification obligations in our Condensed Consolidated Financial Statements.

We provide limited product warranties and the majority of our software license agreements contain provisions that indemnify licensees of our software from damages and costs resulting from claims alleging that our software infringes on the intellectual property rights of a third party. Historically, payments made under these provisions have been immaterial. We monitor the conditions that are subject to indemnification to identify if a loss has occurred.

Litigation contingencies

GSA

During the first quarter of fiscal 2013, we were advised by the Commercial Litigation Branch of the Department of Justice’s (“DOJ”) Civil Division and the Civil Division of the U.S. Attorney’s Office for the District of Columbia that the government is investigating our compliance with certain provisions of our U.S. General Services Administration (“GSA”) Multiple Award Schedule Contract No. GS-35F-0240T effective January 24, 2007, including provisions relating to pricing, country of origin, accessibility, and the disclosure of commercial sales practices.

15

As reported on the GSA’s publicly-available database, our total sales under the GSA Schedule contract were approximately $222 million from the period beginning January 2007 and ending September 2012. We have fully cooperated with the government throughout its investigation and in January 2014, representatives of the government indicated that their initial analysis of our actual damages exposure from direct government sales under the GSA schedule was approximately $145 million; since the initial meeting, the government’s analysis of our potential damages exposure relating to direct sales has increased. The government has also indicated they are going to pursue claims for certain sales to California, Florida, and New York as well as sales to the federal government through reseller GSA Schedule contracts, which could significantly increase our potential damages exposure.

In 2012, a sealed civil lawsuit was filed against Symantec related to compliance with the GSA Schedule contract and contracts with California, Florida, and New York. On July 18, 2014, the Court-imposed seal expired, and the government intervened in the lawsuit. On September 16, 2014, the states of California and Florida intervened in the lawsuit, and the state of New York notified the Court that it would not intervene. On October 3, 2014, the DOJ filed an amended complaint, which did not state a specific damages amount. On October 17, 2014, California and Florida combined their claims with those of the DOJ and the relator on behalf of New York in an Omnibus Complaint, and a First Amended Omnibus Complaint was filed on October 8, 2015; the state claims also do not state specific damages amounts.

It is possible that the litigation could lead to claims or findings of violations of the False Claims Act, and could be material to our results of operations and cash flows for any period. Resolution of False Claims Act investigations can ultimately result in the payment of somewhere between one and three times the actual damages proven by the government, plus civil penalties in some cases, depending upon a number of factors. Our current estimate of the low end of the range of the probable estimated loss from this matter is $25 million, which we have accrued. This amount contemplates estimated losses from both the investigation of compliance with the terms of the GSA Schedule contract as well as possible violations of the False Claims Act. There is at least a reasonable possibility that a loss may have been incurred in excess of our accrual for this matter, however, we are currently unable to determine the high end of the range of estimated losses resulting from this matter.

EDS & NDI

On January 24, 2011, a class action lawsuit was filed against us and our previous e-commerce vendor Digital River, Inc.; the lawsuit alleged violations of California’s Unfair Competition Law, the California Legal Remedies Act and unjust enrichment related to prior sales of Extended Download Service (“EDS”) and Norton Download Insurance (“NDI”). On March 31, 2014, the U.S. District Court for the District of Minnesota certified a class of all people who purchased these products between January 24, 2005 and March 10, 2011. In August 2015, the parties executed a settlement agreement pursuant to which we would pay the plaintiffs $30 million, which we accrued. On October 8, 2015, the Court granted preliminary approval of the settlement, which was subsequently paid into escrow by us. The Court granted final approval on April 22, 2016, and entered judgment in the case. Objectors to the settlement have appealed to the Eighth Circuit Court of Appeals (“Eighth Circuit”), challenging the Court’s approval of the settlement, and the decision granting approval was affirmed by the Eighth Circuit on April 28, 2017. The time for the objectors to appeal the Eighth Circuit’s ruling has now expired without any appeal being filed. This matter is therefore now closed.

Finjan

On August 28, 2013, Finjan, Inc. (“Finjan”) filed a complaint against Blue Coat Systems, Inc. in the U.S. District Court for the Northern District of California alleging that certain Blue Coat products infringe six of Finjan’s U.S. patents. On August 4, 2015, a jury returned a verdict that certain Blue Coat products infringe five of the Finjan patents-in-suit and awarded Finjan lump-sum damages of $40 million. On November 20, 2015, the trial court entered a judgment in favor of Finjan on the jury verdict and certain non-jury legal issues. On July 28, 2016, in its ruling on post-trial motions the trial court denied Blue Coat’s motions seeking a new trial or judgment as a matter of law and denied Finjan’s request for enhanced damages and attorneys’ fees. In August 2016, we completed our acquisition of Blue Coat. We intend to vigorously contest the judgment and have filed an appeal with the Federal Circuit Court of Appeals. Our current best estimated loss and related interest with respect to the jury verdict is $40 million, which was accrued by Blue Coat and assumed by us as a part of the acquisition of Blue Coat.

Other

We are involved in a number of other judicial and administrative proceedings that are incidental to our business. Although adverse decisions (or settlements) may occur in one or more of the cases, it is not possible to estimate the possible loss or losses from each of these cases. The final resolution of these lawsuits, individually or in the aggregate, is not expected to have a material adverse effect on our business, results of operations, financial condition or cash flows.

Note 12. Discontinued Operations

On January 29, 2016, we completed the sale of Veritas. The results of Veritas are presented as discontinued operations in our Condensed Consolidated Statements of Operations and thus have been excluded from continuing operations and segment results for all reported periods.

16

The following table presents information regarding certain components of income (loss) from discontinued operations, net of income taxes:

Three Months Ended | |||||||

(In millions) | June 30, 2017 | July 1, 2016 | |||||

Net revenues | $ | 19 | $ | 72 | |||

Cost of revenues | (3 | ) | (3 | ) | |||

Operating expenses | (1 | ) | (24 | ) | |||

Gain on sale of Veritas | 3 | 38 | |||||

Other income, net | — | 2 | |||||

Income from discontinued operations before income taxes | 18 | 85 | |||||

Income taxes expense | 41 | 16 | |||||

Income (loss) from discontinued operations, net of income taxes | $ | (23 | ) | $ | 69 | ||

During the first quarter of fiscal 2017, we received an additional payment which represented a purchase price adjustment for the sale of Veritas.

Note 13. Subsequent Events

In June 2017 and July 2017, we entered into definitive agreements to acquire Fireglass, Ltd. (“Fireglass”) and Skycure, Ltd. (“Skycure”), respectively. Both acquisitions closed in our second quarter of fiscal 2018. The consideration for the acquisitions of Fireglass and Skycure was approximately $225 million and $205 million, respectively, and primarily consisted of cash.

On August 2, 2017, we entered into a definitive agreement to sell our website security and related public key infrastructure products to Thoma Bravo, LLC’s portfolio company DigiCert, Inc. (“DigiCert”). We expect to receive approximately $950 million in upfront cash proceeds and approximately a 30% equity interest in the common stock of the DigiCert business. The transaction, which has been unanimously approved by our Board of Directors, is expected to be completed in our third quarter of fiscal 2018, subject to the satisfaction of customary closing conditions. We expect that effective in our second quarter of fiscal 2018, the financial results of our website security business will be presented as discontinued operations on the Condensed Consolidated Statements of Income when we meet the criteria for the website security business to be classified as held for sale on our Condensed Consolidated Balance Sheets.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-looking statements and factors that may affect future results

The discussion below contains forward-looking statements, which are subject to safe harbors under the Securities Act of 1933, as amended (the “Securities Act”) and the Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include references to our ability to utilize our deferred tax assets, as well as statements including words such as “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “projects,” and similar expressions. In addition, projections of our future financial performance, anticipated growth and trends in our businesses and in our industries, the anticipated impacts of acquisitions, and of our restructurings, our intent to pay quarterly cash dividends in the future, the actions we intend to take as part of our new strategy, the expected impact of our new strategy and other characterizations of future events or circumstances are forward-looking statements. These statements are only predictions, based on our current expectations about future events and may not prove to be accurate. We do not undertake any obligation to update these forward-looking statements to reflect events occurring or circumstances arising after the date of this report. These forward-looking statements involve risks and uncertainties, and our actual results, performance, or achievements could differ materially from those expressed or implied by the forward-looking statements on the basis of several factors, including those that we discuss in Risk Factors, set forth in Part I, Item 1A, of our annual report on Form 10-K for the fiscal year ended March 31, 2017 and in Part II Item 1A, of this quarterly report on Form 10-Q. We encourage you to read those sections carefully.

OVERVIEW

Our business

Symantec Corporation is a global leader in cybersecurity. We operate our business on a global civilian cyber intelligence threat network and track a vast number of threats across the Internet from hundreds of millions of mobile devices, endpoints, and servers across the globe. We believe one of our competitive advantages is our database of threat indicators. This database allows us to reduce the number of false positives and provide faster and better protection for customers through our products. We are leveraging our capabilities to deliver integrated platforms for customers. We are also pioneering solutions in markets such as cloud security, digital safety, advanced threat protection, identity protection, information protection and cyber security services.

17

Fiscal calendar

We have a 52/53-week fiscal year ending on the Friday closest to March 31. The three months ended June 30, 2017 (“Q1FY18”) and July 1, 2016 (“Q1FY17”), both consisted of 13 weeks. Our 2018 fiscal year consists of 52 weeks and ends on March 30, 2018.

Strategy

Our strategy is to deliver comprehensive cyber security platforms for both enterprises and consumers.

Our enterprise security strategy is to deliver an Integrated Cyber Defense Platform that allows Symantec products to share threat intelligence and improve security outcomes for customers across all control points. Symantec is the leading vendor in protecting users, information, web and messaging across an integrated platform.

Our consumer digital safety strategy is to deliver the most comprehensive consumer digital safety solutions to help people protect their information, identities, devices and families.

Our financial highlights and results of operations

Our financial highlights and results of operations discuss our business and overall analysis of financial and other highlights affecting the company and analyze our financial results comparing Q1FY18 to Q1FY17. This interim Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with the MD&A in our Annual Report on Form 10-K for the fiscal year ended March 31, 2017.

The results of our former information management business (“Veritas”) are presented as discontinued operations in our Condensed Consolidated Statements of Operations and thus have been excluded from continuing operations and segment results for all reported periods. The following discussion relates to our current segment reporting structure and our continuing operations unless stated otherwise.

Our operating segments

Our operating segments are significant strategic business units that offer different products and services distinguished by customer needs. Our operating segments are: Enterprise Security and Consumer Digital Safety.

• | Enterprise Security. Our Enterprise Security segment protects organizations so they can securely conduct business while leveraging new platforms and data. Our Enterprise Security segment includes our endpoint protection products, endpoint management, messaging protection products, information protection products, cyber security services, website security and advanced web and cloud security offerings. Our enterprise endpoint and network security and management offerings support evolving endpoints and networks, providing advanced threat protection while helping reduce cost and complexity. These solutions are delivered through various methods, such as software, appliance, Software-as-a-Service (“SaaS”) and managed services. |

• | Consumer Digital Safety. Our Consumer Digital Safety segment focuses on providing a comprehensive Digital Safety solution to protect information, devices, networks and the identities of consumers. This solution includes our Norton-branded services, which provide multi-layer security across major desktop and mobile operating systems, public Wi-Fi connections, and home networks, to defend against increasingly complex online threats to individuals, families and small businesses, and our LifeLock-branded identity protection services. Our LifeLock-branded identity protection services primarily consist of identifying and notifying users of identity-related and other events and assisting users in remediating their impact. With the addition of LifeLock-branded identity protection services, we are providing a comprehensive digital safety platform designed to protect information across devices, customer identities and the connected home and family and accelerating our leadership in Consumer Digital Safety to protect all aspects of consumers’ digital lives. |

For further description of our operating segments see Note 2 to the Condensed Consolidated Financial Statements.

18

Financial highlights and business trends

The following charts provide an overview of key financial metrics in millions, except for percentage of revenues.

Here are our key financial results for continuing operations:

• | Revenue increased by 33%, driven by a 34% and 31% increase in revenue from our Enterprise Security and Consumer Digital Safety segments, respectively, primarily due to the acquisitions of Blue Coat, Inc. (“Blue Coat”) and LifeLock, Inc. (“LifeLock”). |

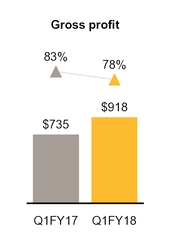

• | Our gross margin decreased five percentage points primarily due to $53 million of revenue we excluded as a result of the revaluations of LifeLock and Blue Coat deferred revenue to fair value at the time of the acquisitions and increased amortization expense of $49 million primarily related to the acquired Blue Coat and LifeLock intangible assets. |

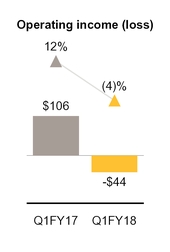

• | Our operating margin decreased sixteen percentage points primarily due to increased stock-based compensation expense and amortization of intangible assets of $95 million and $45 million, respectively. These increases were due in large part to the assumption of equity awards and amortization of intangible assets acquired in connection with the Blue Coat and LifeLock acquisitions. |

• | Cash paid for income taxes decreased $914 million, primarily due to the one-time payment during Q1FY17 related to the gain on sale from the divestiture of Veritas during fiscal 2016. |

• | During Q1FY18, we repaid debt totaling $2.0 billion as part of our plan to deleverage our balance sheet. |

We expect our operating margin to fluctuate in future periods as a result of a number of factors, including our operating results and the timing and amount of expenses incurred.

19

RESULTS OF OPERATIONS

Segment operating results

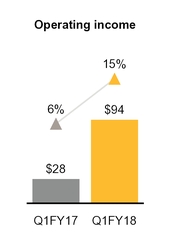

Enterprise Security Segment

Our Enterprise Security segment protects organizations so they can securely conduct business while leveraging new platforms and data. The following tables are in millions except for percentage of revenues.

Revenue increased $165 million, or 34% primarily due to revenue from sales of Blue Coat network protection products, which were absent in Q1FY17. Due to the revaluation of deferred revenue to the fair value at the time we acquired Blue Coat, we excluded $23 million of revenue we otherwise would have recognized in Q1FY18. Operating income increased $66 million, or 236%, primarily due to the contribution of the Blue Coat acquisition and a reduction in expenses from ongoing cost savings initiatives.

Consumer Digital Safety Segment

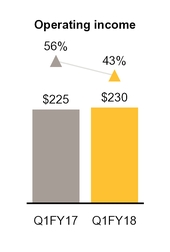

Our Consumer Digital Safety segment focuses making it simple for customers to be productive and protected at home and at work. The following tables are in millions except for percentage of revenues.

Revenue increased $126 million, or 31%, primarily due to revenue from sales of LifeLock products, which were absent in Q1FY17. Due to the revaluation of deferred revenue to fair value at the time we acquired LifeLock, we excluded $30 million of revenue we otherwise would have recognized in Q1FY18. While the trend of declining revenues from sales of Norton-branded products continued in Q1FY18, we continued to benefit from the shift to subscription-based contracts and combined packaging of consumer products, resulting in a lower decline in Q1FY18 as compared to Q1FY17. Our operating income remained relatively flat due to a relatively lower operating margin from LifeLock products.

20

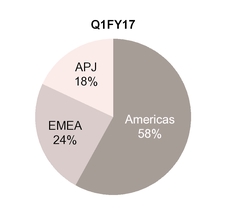

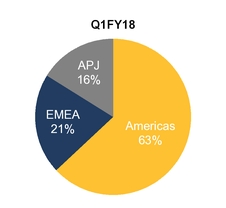

Net revenues by geographic region

Revenue by country as presented below is based on the billing location of the customer.

Total: | $ | 884 | million | Total: | $ | 1,175 | million | ||||

Note: Americas include U.S., Canada and Latin America; EMEA includes Europe, Middle East and Africa; APJ includes Asia Pacific and Japan.

Fluctuations in the U.S. dollar compared to foreign currencies unfavorably impacted our international revenue by approximately $11 million for Q1FY18 as compared to Q1FY17. Our percentage of revenues from the Americas increased primarily as a result of LifeLock sales which are entirely U.S. based.

Our international sales are expected to continue to be a significant portion of our revenue. As a result, we expect revenue to continue to be affected by foreign currency exchange rates as compared to the U.S. dollar. We are unable to predict the extent to which revenue in future periods will be impacted by changes in foreign currency exchange rates. If international sales become a greater portion of our total sales in the future, changes in foreign currency exchange rates may have a potentially greater impact on our revenue and operating results.

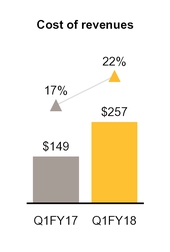

Cost of revenues

Cost of revenues consists primarily of technical support costs, costs of billable services, fees to original equipment manufacturers under revenue-sharing agreements, hardware costs, and fulfillment costs, as well as intangible asset amortization expense, and is presented below in millions except for percentage of revenues.

Our cost of revenues increased $108 million primarily due to costs related to sales of the acquired Blue Coat and LifeLock products, including $49 million of increased amortization expense primarily related to the acquired Blue Coat and LifeLock intangible assets.

21

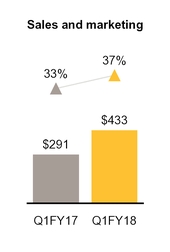

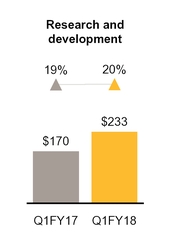

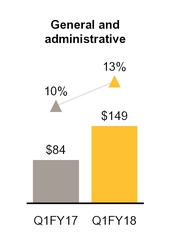

Operating expenses

The following charts are in millions except for percentage of revenues.

In general, our operating expenses increased in Q1FY18 compared to Q1FY17 as a result of increased headcount and facility costs associated with the acquisitions of Blue Coat and LifeLock during fiscal 2017.

Sales and marketing expense increased $142 million primarily as a result of increased expenses from the Blue Coat and LifeLock acquisitions, which included increases of $64 million of advertising and promotional expense, largely related to LifeLock, and $29 million of stock-based compensation expense. These increases were partially offset by a reduction of expenses from ongoing cost savings initiatives.

Research and development expense increased $63 million primarily as a result of increased expenses from the Blue Coat and LifeLock acquisitions, which included an increase of $26 million of stock-based compensation expense. These increases were partially offset by a reduction of expenses from ongoing cost savings initiatives.

General and administrative expense increased $65 million primarily as a result of increased expenses from the Blue Coat and LifeLock acquisitions, which included an increase of $40 million of stock-based compensation expense. These increases were partially offset by a reduction of expenses from ongoing cost savings initiatives.

Our stock-based compensation expense included in operating expenses increased $95 million, primarily due to the equity awards assumed in the Blue Coat and LifeLock acquisitions and the expected level of achievement for performance-based restricted stock units (“PRUs”). Our stock-based compensation expense will continue to fluctuate in future periods as a result of a number of factors including the achievement levels of PRU performance conditions.

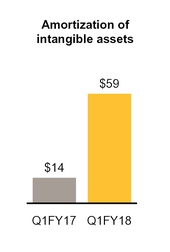

Amortization of intangible assets increased $45 million primarily due to the intangible assets acquired in the Blue Coat and LifeLock acquisitions.

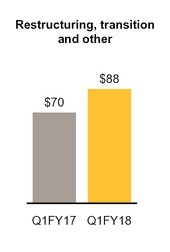

Restructuring, transition and other

We initiated a restructuring plan in the first quarter of fiscal 2017 to reduce complexity by means of long-term structural improvements. We expect to reduce headcount and close certain facilities in connection with the restructuring plan. These actions are expected to be completed in fiscal 2018. On an annual basis, we expect this restructuring plan to generate net cost efficiencies and cost synergies which, when completed, will favorably impact our continuing operating expenses under our

22

commitment to realize cost savings of $580 million, including cost synergies from the Blue Coat and LifeLock acquisitions. In connection with this restructuring plan, we expect to incur approximately $195 million to $245 million in expenses in the remaining quarters of fiscal 2018.

Additionally, we expect continuing significant transition costs associated with the implementation of a new enterprise resource planning system and costs to automate business processes. See Note 4 to the Condensed Consolidated Financial Statements for further information on our restructuring, transition and other costs.

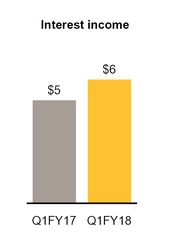

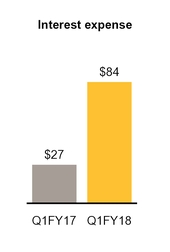

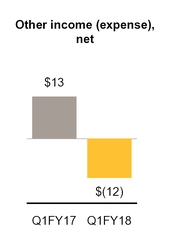

Non-operating expense, net

The following charts are in millions.

Non-operating expense, net, increased $81 million primarily driven by an increase in interest expense of $57 million, mainly related to our increased borrowings subsequent to Q1FY17. See Note 7 to the Condensed Consolidated Financial Statements for more information about our debt. In addition, non-operating expense, net, further increased by $15 million resulting from a net foreign currency remeasurement loss for Q1FY18 compared to a net gain for Q1FY17.

Provision for income taxes

The following charts are in millions except for percentages.

Our effective tax rate for loss from continuing operations for Q1FY18 differs from the federal statutory income tax rate primarily due to the benefits of lower-taxed international earnings, the research and development tax credit, and excess tax benefits related to stock-based compensation as a result of the new accounting guidance, partially offset by permanent differences.

Our effective tax rate for income from continuing operations for Q1FY17 differs from the federal statutory income tax rate primarily due to the benefits of lower-taxed international earnings, domestic manufacturing incentives and the research and development tax credit, partially offset by state income taxes.

For the three months ended June 30, 2017, we recorded income tax expense on discontinued operations of $41 million. For the three months ended July 1, 2016, we recorded income tax expense on discontinued operations of $16 million. See Note 12 for further details regarding discontinued operations.

23

We are a U.S.-based multinational company subject to tax in multiple U.S. and international tax jurisdictions. A substantial portion of our international earnings were generated from subsidiaries organized in Ireland and Singapore. Our results of operations would be adversely affected to the extent that our geographical mix of income becomes more weighted toward jurisdictions with higher tax rates and would be favorably affected to the extent the relative geographic mix shifts to lower tax jurisdictions. Any change in our mix of earnings is dependent upon many factors and is therefore difficult to predict.

The timing of the resolution of income tax examinations is highly uncertain, and the amounts ultimately paid, if any, upon resolution of the issues raised by the taxing authorities may differ materially from the amounts accrued for each year. Although potential resolution of uncertain tax positions involve multiple tax periods and jurisdictions, it is reasonably possible that the gross unrecognized tax benefits related to these audits could decrease, whether by payment, release, or a combination of both, in the next 12 months by $12 million, which could reduce our income tax provision and therefore benefit the resulting effective tax rate.

We continue to monitor the progress of ongoing income tax controversies and the impact, if any, of the expected expiration of the statute of limitations in various taxing jurisdictions.

LIQUIDITY AND CAPITAL RESOURCES

Sources and uses of cash

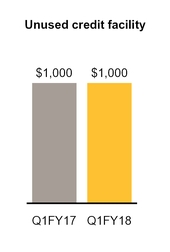

We have historically relied on cash flow from operations, borrowings under credit facilities, issuances of debt and equity securities, and the sale of a business, for our liquidity needs. As of June 30, 2017, we had cash, cash equivalents and short-term investments of $2.3 billion, of which $8 million is included in our other current assets. We also have an unused credit facility of $1.0 billion resulting in a liquidity position of approximately $3.3 billion. As of June 30, 2017, $1.5 billion in cash, cash equivalents, and short-term investments were held by our foreign subsidiaries. We have provided U.S. deferred taxes on a portion of our undistributed foreign earnings sufficient to address the incremental U.S. tax that would be due if we needed such portion of these funds to support our operations in the U.S.

Our principal cash requirements primarily consist of acquisitions, operating expenses and working capital, payment of taxes, capital expenditures, payment of principal and interest on debt, and restructuring, transition and integration costs. Also, we may engage, from time to time, in the open market purchase of our notes prior to their maturity. Furthermore, our capital allocation strategy contemplates a quarterly cash dividend. In addition, we regularly evaluate our ability to repurchase shares of our common stock.

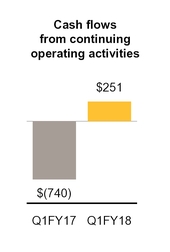

Cash flows

The following charts summarize cash provided by (used in) our Condensed Consolidated Statements of Cash Flows for Q1FY17 and Q1FY18, in millions.

Continuing operating activities

Our primary source of cash from continuing operating activities has been from cash collections from our customers. Due to seasonality, our orders are generally higher in our third and fourth fiscal quarters and lower in our first and second fiscal quarters. We therefore expect cash inflows from continuing operating activities to be affected by fluctuations in billings and timing of collections.

Our primary uses of cash from our continuing operating activities include payments for income taxes, payments for compensation and related costs, payments to our resellers and distribution partners, and other general corporate expenditures.

The change in cash from continuing operating activities in Q1FY18 compared to Q1FY17 was primarily due to decreased tax payments of $914 million related to income taxes paid in Q1FY17 and increased changes in working capital in Q1FY18, partially offset by lower income from continuing operations, adjusted for non-cash items.

24

Restructuring Plan. We initiated a restructuring plan in Q1FY17 to reduce complexity by means of long-term structural improvements. We expect to reduce headcount and close certain facilities in connection with this restructuring plan. The total remaining cash payments in connection with the restructuring plan are expected to be approximately $235 million to $270 million. These actions are expected to be completed in fiscal 2018. See Note 4 to the Condensed Consolidated Financial Statements for more information on our restructuring plans.

Continuing investing activities

Our investing cash flows consist primarily of capital expenditures and investment purchases and proceeds. The change in continuing investing activities in Q1FY18 compared to Q1FY17 was primarily due to reduced proceeds from maturities and sales of short-term investments of $30 million and increased additions to property and equipment of $25 million.

Short-term investments. In order to achieve greater investment diversification and higher yields while maintaining our objectives of preservation of capital, liquidity, and safety, we plan to maintain our increased holdings of short-term investments.

Fireglass and Skycure acquisitions. In June 2017 and July 2017, we entered into definitive agreements to acquire Fireglass, Ltd. (“Fireglass”) and Skycure, Ltd. (“Skycure”), respectively. Both acquisitions closed in July 2017, subsequent to Q1FY18. The consideration for the acquisitions of Fireglass and Skycure was approximately $225 million and $205 million, respectively, and primarily consisted of cash.

Sale of Website Security business. On August 2, 2017, we entered into a definitive agreement to sell our website security and related public key infrastructure products to Thoma Bravo, LLC’s portfolio company DigiCert, Inc. (“DigiCert”). We expect to receive approximately $950 million in upfront cash proceeds and approximately a 30% equity interest in the common stock of the DigiCert business. The sale is expected to close in our third quarter of fiscal 2018, subject to the satisfaction of customary closing conditions. The transaction proceeds, net of expected taxes and expenses, are expected to be used to repay debt.

Continuing financing activities

Our financing cash flows consist primarily of issuances and repayments of debt, payment of dividends and dividend equivalents to stockholders, and tax payments related to the settlement of restricted stock units (“RSUs”). The change in continuing financing activities in Q1FY18 compared to Q1FY17 was primarily due to increased repayments on debt of $2.0 billion, reduced borrowings of $994 million and increased tax payments related to the settlement of RSUs of $37 million.

Borrowings. Proceeds from and repayments of borrowings fluctuate from year to year based on the amounts paid to fund acquisitions, and debt repayments. The charts below set forth total debt issued, repaid and the amount of unused credit facility for Q1FY17 and Q1FY18, in millions.

As a part of our plan to deleverage our balance sheet, we may from time to time in the future make optional repayments of our debt obligations, which may include repurchases of our outstanding debt, depending on various factors, such as market conditions.

Interest payments on $2.3 billion of our variable-rate borrowings are subject to change based on market interest rates.

See Note 7 to the Condensed Consolidated Financial Statements for further information on our debt repayments and borrowings.

Dividends. On August 2, 2017, we declared a cash dividend of $0.075 per share of common stock to be paid on September 13, 2017, to all stockholders of record as of the close of business on August 21, 2017. All shares of common stock issued and outstanding and all shares of unvested restricted stock and performance-based stock as of the record date will be entitled to the dividend and dividend equivalents, respectively. Any future dividends and dividend equivalents will be subject to the approval of our Board.

See Note 9 to the Condensed Consolidated Financial Statements for more information on our share repurchases and dividends and dividend equivalents.

25

Contractual obligations

Except for the repayment of our Senior Notes, settlement of our Senior Term Facility, and related interest payments on borrowings, there were no significant changes during the three months ended June 30, 2017 to the contractual obligations disclosed in Management’s Discussion and Analysis of Financial Condition and Results of Operations, set forth in Part II, Item 7, of our Annual Report on Form 10-K for the fiscal year ended March 31, 2017.

The table below sets forth these changes as of June 30, 2017, but does not update the other line items in the contractual obligations table that appear in the section of our Annual Report on Form 10-K described above:

Payments Due by Fiscal Period | |||||||||||||||||||

(In millions) | Total | Remainder of 2018 | 2019 - 2020 | 2021 - 2022 | Thereafter | ||||||||||||||

Debt (1) | $ | 6,300 | $ | — | $ | 1,800 | $ | 3,000 | $ | 1,500 | |||||||||

Interest payments on debt (2) | 968 | 156 | 382 | 230 | 200 | ||||||||||||||

Total | $ | 7,268 | $ | 156 | $ | 2,182 | $ | 3,230 | $ | 1,700 | |||||||||

(1) | See Note 7 to the Condensed Consolidated Financial Statements for further information on our debt. |

(2) | Interest payments were calculated based on the contractual terms of the related Senior Notes, Convertible Senior Notes and Senior Term Facilities. Interest on variable rate debt was calculated using the interest rate in effect as of June 30, 2017. See Note 7 to the Condensed Consolidated Financial Statements for further information on the Senior Notes, Convertible Senior Notes and Senior Term Facilities. |

Indemnifications

In the ordinary course of business, we may provide indemnifications of varying scope and terms to customers, vendors, lessors, business partners, subsidiaries and other parties with respect to certain matters, including, but not limited to, losses arising out of our breach of agreements or representations and warranties made by us. In addition, our bylaws contain indemnification obligations to our directors, officers, employees and agents, and we have entered into indemnification agreements with our directors and certain of our officers to give such directors and officers additional contractual assurances regarding the scope of the indemnification set forth in our bylaws and to provide additional procedural protections. We maintain director and officer insurance, which may cover certain liabilities arising from our obligation to indemnify our directors and officers. It is not possible to determine the aggregate maximum potential loss under these indemnification agreements due to the limited history of prior indemnification claims and the unique facts and circumstances involved in each particular agreement. Such indemnification agreements might not be subject to maximum loss clauses. Historically, we have not incurred material costs as a result of obligations under these agreements and we have not accrued any liabilities related to such indemnification obligations in our Condensed Consolidated Financial Statements.