Attached files

| file | filename |

|---|---|

| EX-32.02 - EXHIBIT 32.02 - NortonLifeLock Inc. | a33117exhibit3202.htm |

| EX-32.01 - EXHIBIT 32.01 - NortonLifeLock Inc. | a33117exhibit3201.htm |

| EX-31.02 - EXHIBIT 31.02 - NortonLifeLock Inc. | a33117exhibit3102.htm |

| EX-31.01 - EXHIBIT 31.01 - NortonLifeLock Inc. | a33117exhibit3101.htm |

| EX-23.01 - EXHIBIT 23.01 - NortonLifeLock Inc. | a33117exhibit2301.htm |

| EX-21.01 - EXHIBIT 21.01 - NortonLifeLock Inc. | a33117exhibit2101.htm |

| EX-3.05 - EXHIBIT 3.05 - NortonLifeLock Inc. | a33117exhibit305arbylaws.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended March 31, 2017

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to

Commission File Number 000-17781

Symantec Corporation

(Exact name of the registrant as specified in its charter)

Delaware | 77-0181864 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer Identification no.) | |

350 Ellis Street | ||

Mountain View, California | 94043 | |

(Address of principal executive offices) | (zip code) | |

Registrant’s telephone number, including area code:

(650) 527-8000

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, par value $0.01 per share (Title of each class) | The NASDAQ Stock Market LLC (Name of each exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | Emerging growth company o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

Aggregate market value of the voting stock held by non-affiliates of the registrant, based upon the closing sale price of Symantec common stock on September 30, 2016 as reported on the NASDAQ Global Select Market: $15,559,432,822.

Number of shares outstanding of the registrant’s common stock as of April 28, 2017: 608,240,301

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2017 Annual Meeting of Stockholders are incorporated herein by reference into Part III of this Annual Report on Form 10-K where indicated. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended March 31, 2017.

SYMANTEC CORPORATION

FORM 10-K

For the Fiscal Year Ended March 31, 2017

TABLE OF CONTENTS

Page | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

“Symantec,” “we,” “us,” “our,” and “the Company” refer to Symantec Corporation and all of its subsidiaries. Symantec, the Symantec Logo and Norton are trademarks or registered trademarks of Symantec in the United States (“U.S.”) and other countries. Other names may be trademarks of their respective owners.

2

FORWARD-LOOKING STATEMENTS AND FACTORS THAT MAY AFFECT FUTURE RESULTS

The discussion below contains forward-looking statements, which are subject to safe harbors under the Securities Act of 1933, as amended (the “Securities Act”) and the Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include references to our ability to utilize our deferred tax assets, as well as statements including words such as “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “projects,” and similar expressions. In addition, projections of our future financial performance, anticipated growth and trends in our businesses and in our industries, the anticipated impacts of acquisitions, and of our restructurings, our intent to pay quarterly cash dividends in the future, the actions we intend to take as part of our new strategy, the expected impact of our new strategy and other characterizations of future events or circumstances are forward-looking statements. These statements are only predictions, based on our current expectations about future events and may not prove to be accurate. We do not undertake any obligation to update these forward-looking statements to reflect events occurring or circumstances arising after the date of this report. These forward-looking statements involve risks and uncertainties, and our actual results, performance, or achievements could differ materially from those expressed or implied by the forward-looking statements on the basis of several factors.

These and other risks are described under Item 1A, Risk Factors. We encourage you to read that section carefully.

3

PART I

Item 1. Business

Overview

Symantec Corporation is a global leader in cybersecurity. We operate our business on a global civilian cyber intelligence threat network that tracks a vast number of threats across the Internet from hundreds of millions of mobile devices, endpoints, and servers across the globe. We believe one of our competitive advantages is our database of threat indicators. This database allows us to reduce the number of false positives and provide faster and better protection for customers through our products. We are leveraging our capabilities to deliver integrated platforms for customers. We are also pioneering solutions in markets such as cloud security, digital safety, advanced threat protection, identity protection, information protection and cyber security services.

Founded in 1982, Symantec has operations in more than 40 countries. Our principal executive offices are located at 350 Ellis Street, Mountain View, California, 94043. Our Internet home page is located at www.symantec.com.

Strategy

Our strategy is to deliver comprehensive cyber security platforms for both enterprises and consumers.

Our enterprise security strategy is to deliver an Integrated Cyber Defense Platform that allows Symantec products to share threat intelligence and improve security outcomes for customers across all control points. Symantec is the leading vendor in protecting users, information, web and messaging across an integrated platform.

Our consumer digital safety strategy is to deliver the most comprehensive consumer digital safety solutions to help people protect their information, identities, devices and families.

Following the completion of the sale of our former information management business (“Veritas”) in the fourth quarter of fiscal 2016, we completed the acquisitions of Blue Coat, Inc. (“Blue Coat”) and LifeLock, Inc. (“LifeLock”) in fiscal 2017 in order to expand our offerings in both our operating segments, as described below.

Business highlights

During fiscal 2017, we took the following actions in support of our business:

• | With the divestiture of Veritas completed, we refocused Symantec as a pure cybersecurity company. In the second fiscal quarter, we completed the acquisition of Blue Coat, a provider of advanced web and cloud security solutions for global enterprises and governments, to complement our Enterprise Security offerings. The aggregate purchase price of the Blue Coat acquisition was $4.7 billion in net consideration, of which $4.5 billion consisted of cash consideration including the repayment of approximately $1.9 billion in Blue Coat’s debt. Following the closing of the Blue Coat acquisition, we appointed Blue Coat’s Chief Executive Officer as our Chief Executive Officer and Blue Coat’s President and Chief Operating Officer as our President and Chief Operating Officer, respectively, in the second quarter of fiscal 2017. In addition, we appointed Blue Coat’s Chief Financial Officer to the position of our Executive Vice President and Chief Financial Officer in the third quarter of fiscal 2017. |

• | In the fourth fiscal quarter, we completed the acquisition of LifeLock, a provider of proactive identity theft protection services for consumers and consumer risk management services for enterprises, for approximately $2.3 billion in net consideration. |

• | We increased the size of our Board of Directors and appointed representatives of Silver Lake Partners and Bain Capital to our Board of Directors. |

▪ | We released new products and services: |

◦ | We launched Symantec Endpoint Protection 14, a solution that fuses endpoint technologies with advanced machine learning and memory exploit mitigation in a single agent, delivering a multi-layered solution designed to stop a wide variety of advanced threats and respond at the endpoint. |

◦ | We introduced Symantec Endpoint Protection Cloud, a new solution for small and mid-sized businesses (SMBs) designed to protect them from targeted attacks and ransomware. Symantec Endpoint Protection Cloud is for organizations with fewer than 1,000 employees that are looking for an effective way to protect corporate and personal devices on the corporate network. |

◦ | We announced Cloud Workload Protection, a solution designed to deliver automated security policy enforcement and protect applications from unknown exploits inside of both Amazon Web Service and Microsoft Azure. Cloud Workload Protection automates security for public cloud workloads delivering metered usage billing, rapid workload discovery, increased visibility and elastic protection to help ensure safe cloud workload adoption. |

▪ | We integrated Blue Coat and Symantec products: |

◦ | We announced the integration of Symantec Data Loss Prevention (“DLP”) with Symantec CloudSOC (formerly Blue Coat’s Elastica CloudSOC Cloud Access Security Broker) and Cloud Data Protection products to address the needs of the cloud generation. This integrated solution provides visibility and control over all sensitive |

4

content that users upload, store and share via the cloud, protecting confidential information through the stages of its lifecycle.

◦ | We integrated our Symantec DLP with our cloud-delivered Web Security Service, providing a seamless platform to help ensure a safe web experience and protect organizational data. |

◦ | We combined Symantec and Blue Coat’s security telemetry which has led to a series of significant protection improvements as well as discoveries of new attack campaigns. |

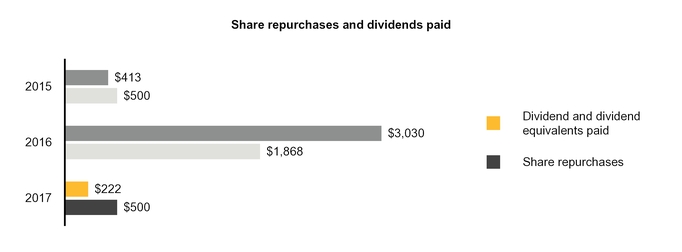

• | Symantec’s Board of Directors increased the company’s share repurchase authorization by $510 million. In the fourth fiscal quarter, Symantec entered into accelerated stock repurchase agreements to repurchase an aggregate of $500 million of the company’s common stock. |

Operating segments, products and services

Our operating segments are significant strategic business units that offer different products and services distinguished by customer needs. Our operating segments are: Consumer Digital Safety and Enterprise Security.

Consumer Digital Safety

Our Consumer Digital Safety segment focuses on providing a comprehensive Digital Safety solution to protect information, devices, networks and the identities of consumers. This solution includes our Norton-branded services, which provide multi-layer security across major desktop and mobile operating systems, public Wi-Fi connections, and home networks, to defend against increasingly complex online threats to individuals, families and small businesses, and our LifeLock-branded identity protection services. Our LifeLock-branded identity protection services primarily consist of identifying and notifying users of identity-related and other events and assisting users in remediating their impact. With the addition of LifeLock-branded identity protection services, we are providing a comprehensive digital safety platform designed to protect information across devices, customer identities and the connected home and family and accelerating our leadership in Consumer Digital Safety to protect all aspects of consumers’ digital lives.

Enterprise Security

Our Enterprise Security segment protects organizations so they can securely conduct business while leveraging new platforms and data. Our Enterprise Security segment includes our endpoint protection products, endpoint management, messaging protection products, information protection products, cyber security services, website security and advanced web and cloud security offerings. Our enterprise endpoint and network security and management offerings support evolving endpoints and networks, providing advanced threat protection while helping reduce cost and complexity. These solutions are delivered through various methods, such as software, appliance, Software-as-a-Service (“SaaS”) and managed services.

The addition of Blue Coat’s suite of network and cloud security products to our innovative Enterprise Security product portfolio has enhanced our threat protection and information protection products while providing us with complementary products, such as advanced web and cloud security solutions, that address the network and cloud security needs of enterprises. This augmentation of our product portfolio, together with the integration of Blue Coat’s large threat database with our global civilian cyber intelligence threat network, allows us to provide an integrated cyber defense platform, addressing both endpoint and network security, and offer differentiated security solutions. It also positions us well to introduce new cybersecurity solutions that address the ever-evolving threat landscape, the changes introduced by the shift to mobile and cloud along with the adoption of Internet of Things (IoT) devices. Our enhanced portfolio also positions us well to address the challenges created by regulatory and privacy concerns.

Financial information by segment and geographic region

For information regarding our revenue by segment, revenue by geographical area, and property and equipment by geographical area, see Note 2 to the Consolidated Financial Statements in this annual report. For information regarding the amount and percentage of our revenue contributed by each of our segments and our financial information, including information about geographic areas in which we operate, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations. For information regarding risks associated with our international operations, see Item 1A, Risk Factors.

Sales and go-to-market strategy

Our go-to-market network includes direct sales forces and broad e-commerce capabilities, as well as indirect sales resources that support our global partner ecosystem. We also maintain strategic relationships with a number of original equipment manufacturers (“OEMs”), Internet service providers (“ISPs”), wireless carriers, and retail and online stores through which we market and sell our products.

Consumer

We sell and market our consumer products and services to individuals, households and small businesses globally. We bring these products to market through direct marketing and co-marketing programs supported by our e-commerce and telesales platforms. In addition, we utilize Internet-based resellers, system builders, ISPs, employee benefits providers, wireless carriers, retailers, and OEMs to distribute our offerings worldwide.

5

Commercial

We sell and market our products and related services to small, medium and large customers through field sales and inside sales forces that leverage indirect sales partners around the world that are specifically trained and certified to sell our solutions. These partners include national solution providers, regional solution providers, national account resellers, global/federal system integrators and managed service providers. Our products and services are also available on our e-commerce platform, as well as through authorized distributors and OEMs, which incorporate our technologies into their products, bundle our products with their offerings, or serve as authorized resellers of our products.

Enterprise

We sell and market our products and related services to large enterprises, including government and public sector customers, through our field sales force. This field sales team is responsible for leveraging our global partner ecosystem primarily targeting senior executives and IT department personnel responsible for managing a company’s highest-order IT initiatives.

Research and development

Symantec embraces a global research and development strategy to drive organic innovation. Our engineers and researchers are focused on delivering new versions of existing product lines as well as developing entirely new offerings to drive the company’s leadership in cybersecurity. We also have a technology research organization focused on short, medium, and longer-term applied research projects, with the goal of transferring completed innovations into our product groups for commercialization.

Symantec’s Security Technology and Response organization consists of a global team of security engineers, threat analysts, and researchers that provide the underlying functionality, content, and support for many of our consumer, commercial and enterprise security products. Our security experts analyze threat telemetry collected through our vast cyber intelligence networks to protect our customers against current and emerging threats. Our research and development teams also leverage this vast amount of data and related insights to develop new technologies and approaches, including our Unified Security analytics platform, in order to improve security outcomes for our customers.

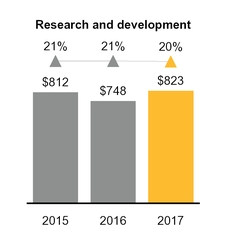

Research and development expenses were $823 million, $748 million, and $812 million in fiscal 2017, 2016, and 2015, respectively, representing approximately 20%, 21% and 21% of revenue in fiscal 2017, 2016 and 2015, respectively. The percentage fluctuates between periods as a result of a variety of factors, including changes in sales level and foreign currency exchange rates. We believe that technical leadership is essential to our success, and we expect to continue to commit substantial resources to research and development.

Support

Symantec has support facilities throughout the world, staffed by technical product experts knowledgeable in the operating environments in which our products are deployed. Our technical support experts assist customers with issue resolution and threat detection.

Our consumer support program provides self-help online services and phone, chat, and email support to consumers worldwide. Most of our Norton Security products come with automatic downloads of the latest virus definitions, application bug fixes, and patches, as well as a “Virus Protection Promise,” which in some markets provides free virus removal services to customers whose protected computers become infected. Our LifeLock offerings come with support 24x7x365 and remediation services during normal business hours.

We provide customers various levels of enterprise support offerings. Our enterprise security support program offers annual maintenance support contracts, including content, upgrades, and technical support. Our standard technical support includes: self-service options delivered by telephone or electronically during the contracted-for hours, immediate patches for severe problems, periodic software updates, and access to our technical knowledge base and frequently asked questions.

Significant customers

In each of fiscal 2017, 2016 and 2015, no customer accounted for more than 10% of our total net revenues. Two distributors and one distributor accounted for more than 10% of our gross accounts receivable as of March 31, 2017 and April 1, 2016, respectively.

Acquisitions

Our strategy will be complemented by business combinations that fit strategically and meet specific profitability hurdles. Our acquisitions are designed to enhance the features and functionality of our existing products and extend our product leadership in core markets. We consider time-to-market, synergies with existing products, and potential market share gains when evaluating the economics of acquisitions of technologies, product lines, or companies. We may acquire or dispose of other technologies, products, and companies in the future. See Note 6 to the Consolidated Financial Statements for information regarding our acquisitions in fiscal 2017.

Competition

Our markets are consolidating, highly competitive, and subject to rapid changes in technology. The competitive landscape has changed significantly over the past few years, with new competition arising. Much of the market growth has come from startups whose focus is on solving a specific customer issue or delivering a niche-oriented product and from larger integration providers that increasingly are looking to put various types of protection into their platforms. We are focused on delivering

6

comprehensive customer solutions, integrating across our broad product portfolio and partnering with other technology providers to differentiate ourselves from the competition. We believe that the principal competitive factors necessary to be successful in our industry include product quality and effectiveness, time-to-market, price, reputation, financial stability, breadth of product offerings, customer support, brand recognition, and effective sales and marketing efforts.

In addition to the competition we face from direct competitors, we face indirect or potential competition from retailers, application providers, operating system providers, network equipment manufacturers, and other OEMs who may provide various solutions and functions in their current and future products. We also compete for access to retail distribution channels and for spending at the retail level and in corporate accounts. In addition, we compete with other software companies, operating system providers, network equipment manufacturers, and other OEMs to acquire technologies, products, or companies and to publish software developed by third parties. We also compete with other software companies in our effort to place our products on the computer equipment sold to consumers and enterprises by OEMs.

Most of the channels in which our products are offered are highly competitive. Some of our consumer competitors are intensely focused on customer acquisition, which has led competitors to offer their technology for free, engage in aggressive marketing, or enter into competitive partnerships. We view our competitive landscape as follows:

• | Our primary security competitors are McAfee (formerly Intel Security), Microsoft Corporation (“Microsoft”), and Trend Micro Inc. There are also several freeware providers and regional security companies that we compete against. |

• | For our consumer backup offerings, our primary competitors are Carbonite, Inc. and Dell EMC. |

• | In Identity Protection, our competitors are the credit bureaus that include Experian, Equifax, and TransUnion, as well as others, such as Affinion, EWS, Intersections, CSID, and LexisNexis. |

• | In the Secure Socket Layer Certificate market, our primary competitors are Comodo Group, Inc., DigiCert, Inc. and Let’s Encrypt. |

• | In the email security market, our primary competitors are Proofpoint, Inc. and Microsoft. |

• | Our primary competitors in the managed security services business are SecureWorks Corporation and International Business Machines Corporation (“IBM”). |

• | Our principal competitors in the web security gateway market are McAfee, Zscaler, Inc. (“Zscaler”), Forcepoint LLC and Cisco Systems, Inc. (“Cisco”). In addition, we expect additional competition from other established and emerging companies as the web security gateway market continues to develop and expand through further consolidation. |

• | Our principal competitors in the cloud security services market are Zscaler and Cisco. In addition, we expect additional competition from other established and emerging companies as the market for security-as-a-service continues to develop and expand and as consolidation occurs. |

• | Our principal competitors in the advanced threat protection market and incident response, analytics and forensics market include McAfee, IBM and Dell EMC as well as independent security vendors such as Palo Alto Networks Inc., FireEye, Inc., Niksun and Trend Micro Inc. Further, as new IT budgets are created to support next-generation threat protection, we expect to compete with more highly specialized vendors as well as larger vendors that may continue to acquire or bundle their products. |

• | Our principal competitors in the WAN optimization market are Riverbed Technology, Inc. and Cisco. In addition, we expect additional competition from other established and emerging companies as the WAN optimization market continues to develop and expand and as consolidation occurs. |

Intellectual property

Protective measures

We regard some of the features of our internal operations, software, and documentation as proprietary and rely on copyright, patent, trademark and trade secret laws, confidentiality procedures, contractual arrangements, and other measures to protect our proprietary information. Our intellectual property is an important and valuable asset that enables us to gain recognition for our products, services, and technology and enhance our competitive position.

As part of our confidentiality procedures, we generally enter into non-disclosure agreements with our employees, distributors, and corporate partners and we enter into license agreements with respect to our software, documentation, and other proprietary information. These license agreements are generally non-transferable and have either a perpetual or subscription based time limited term. We also educate our employees on trade secret protection and employ measures to protect our facilities, equipment, and networks.

Trademarks, patents, copyrights, and licenses

Symantec and the Symantec logo are trademarks or registered trademarks in the U.S. and other countries. In addition to Symantec and the Symantec logo, we have used, registered, or applied to register other specific trademarks and service marks to help distinguish our products, technologies, and services from those of our competitors in the U.S. and foreign countries and jurisdictions. We enforce our trademark, service mark, and trade name rights in the U.S. and abroad. The duration of our trademark registrations varies from country to country, and in the U.S. we generally are able to maintain our trademark rights and renew any trademark registrations for as long as the trademarks are in use.

7

We have approximately 2,100 patents, in addition to foreign patents and pending U.S. and foreign patent applications, which relate to various aspects of our products and technology. The duration of our patents is determined by the laws of the country of issuance and for the U.S. is typically 17 years from the date of issuance of the patent or 20 years from the date of filing of the patent application resulting in the patent, which we believe is adequate relative to the expected lives of our products.

Our products are protected under U.S. and international copyright laws and laws related to the protection of intellectual property and proprietary information. We take measures to label such products with the appropriate proprietary rights notices, and we actively enforce such rights in the U.S. and abroad. However, these measures may not provide sufficient protection, and our intellectual property rights may be challenged. In addition, we license some intellectual property from third parties for use in our products, and generally must rely on the third party to protect the licensed intellectual property rights. While we believe that our ability to maintain and protect our intellectual property rights is important to our success, we also believe that our business as a whole is not materially dependent on any particular patent, trademark, license, or other intellectual property right.

Seasonality

As is typical for many large technology companies, our business is seasonal. Orders are generally higher in our third and fourth fiscal quarters and lower in our first and second fiscal quarters. Revenue generally reflects similar seasonal patterns but to a lesser extent than orders because revenue is not recognized until an order is shipped or services are performed and other revenue recognition criteria are met, and because a significant portion of our in-period revenue comes from our deferred revenue balance.

Employees

As of March 31, 2017, we employed more than 13,000 people worldwide.

Available information

Our Internet home page is located at www.symantec.com. We make available free of charge our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after we electronically file such material with the Securities and Exchange Commission (“SEC”) on our investor relations website located at www.symantec.com/invest. The information contained, or referred to, on our website is not part of this annual report unless expressly noted. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding our filings at http://www.sec.gov. In addition, you may read and copy any filing that we make with the SEC at the public reference room maintained by the SEC, located at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information about the public reference room.

Item 1A. Risk Factors

A description of the risk factors associated with our business is set forth below. The list is not exhaustive and you should carefully consider these risks and uncertainties before investing in our common stock.

If we are unsuccessful at addressing our business challenges, our business and results of operations may be adversely affected and our ability to invest in and grow our business could be limited.

For the last few years, we have experienced a number of transitions as we have attempted to revitalize our business model, improve execution and innovate new products and services. These transitions have involved changes to management and other key personnel, shifts in our strategic direction and, more recently, changes to our corporate structure as a result of the divestiture of Veritas and the acquisition of Blue Coat. In particular, in connection with our acquisition of Blue Coat, we experienced changes to our executive team during the second and third quarters of fiscal 2017, appointing three former Blue Coat executive officers to the positions of Chief Executive Officer, President and Chief Operating Officer, and Executive Vice President and Chief Financial Officer. Transitions of these kind can be disruptive, can result in the loss of institutional focus and employee morale and make the execution of business strategies more difficult. We are also focused on addressing dynamic and accelerating market trends, such as the continued decline in the PC market, the market shifts towards mobility, the continued transition towards cloud-based solutions and architectural shifts in the provision of security, all of which has made it more difficult for us to compete effectively and requires us to improve our product and service offerings. We may experience delays in the anticipated timing of activities related to our efforts to address these challenges and higher than expected or unanticipated execution costs. In addition, we are vulnerable to increased risks associated with these efforts and the broad range of geographic regions in which we and our customers and partners operate. If we do not succeed in these efforts, or if these efforts are more costly or time-consuming than expected, our business and results of operations may be adversely affected, which could limit our ability to invest in and grow our business.

Fluctuations in demand for our products and services are driven by many factors, and a decrease in demand for our products could adversely affect our financial results.

We are subject to fluctuations in demand for our products and services due to a variety of factors, including market transitions, general economic conditions, competition, product obsolescence, technological change, shifts in buying patterns, financial difficulties and budget constraints of our current and potential customers, awareness of security threats to IT systems and other factors. While such factors may, in some periods, increase product sales, fluctuations in demand can also negatively impact our product sales. If demand for our products and solutions declines, whether due to general economic conditions or a shift in buying patterns, our revenues and margins would likely be adversely affected.

Additionally, since Blue Coat’s business historically experienced a major product refresh cycle approximately once every five

8

years, as hardware appliances reach the end of their useful life, we anticipate that we will experience fluctuations in demand as we enter and exit cycles in which many of our customers refresh their install base of hardware appliance products with our latest equipment, replacing older versions of the hardware that have reached the end of their useful life and are no longer supported under maintenance contracts. Our appliances generally have a five year end-of-life date from the date of purchase, which we expect will extend refresh cycles for our hardware appliances over a multi-year period and reduce the impact of a product refresh cycle in any one period. However, we cannot assure you that we will not experience uneven demand for these products in any one period, causing our business and results of operations to be adversely affected.

A refresh cycle also creates an opportunity for our competitors to try to displace our existing product deployments for our customers, who may be more inclined to consider other product solutions at a time when they otherwise need to replace our existing products that have reached the end of their useful life. The extent to which customers decide to refresh by purchasing products from our current or future competitors as opposed to purchasing our new products may significantly impact our current period product revenues as well as future service revenue.

Our business depends on customers renewing their arrangements for maintenance, subscriptions, managed security services and SaaS offerings.

A large portion of our revenue is derived from arrangements for maintenance, subscriptions, managed security services and SaaS offerings, yet existing customers have no contractual obligation to purchase additional solutions after the initial subscription or contract period. Our customers’ renewal rates may decline or fluctuate as a result of a number of factors, including their level of satisfaction with our solutions or our customer support, customer budgets and the pricing of our solutions compared with the solutions offered by our competitors, any of which may cause our revenue to grow more slowly than expected, if at all. Accordingly, we must invest significant time and resources in providing ongoing value to our customers. If these efforts fail, or if our customers do not renew for other reasons, or if they renew on terms less favorable to us, our revenue may decline and our business will suffer.

If we are unable to develop new and enhanced products and services that achieve widespread market acceptance, or if we are unable to continually improve the performance, features, and reliability of our existing products and services or adapt our business model to keep pace with industry trends, our business and operating results could be adversely affected.

Our future success depends on our ability to respond to the rapidly changing needs of our customers by developing or introducing new products, product upgrades and services on a timely basis. We have in the past incurred, and will continue to incur, significant research and development expenses as we strive to remain competitive. Additionally, we must continually address the challenges of dynamic and accelerating market trends, such as the emergence of advanced persistent threats in the security space, the continued decline in the PC market and the market shift towards mobility and the increasing transition towards cloud-based solutions, all of which have made it more difficult for us to compete effectively. For example, we have been increasingly investing in solutions that address the cloud security market, particularly our acquisition of Blue Coat, but we cannot be certain that the cloud security market will develop at a rate or in the manner we expect or that we will be able to compete successfully with more established competitors in the cloud security market. Customers may require features and capabilities that our current solutions do not have. Our failure to develop solutions that satisfy customer preferences in a timely and cost-effective manner may harm our ability to renew our subscriptions with existing customers and to create or increase demand for our solutions and may adversely impact our operating results. New product development and introduction involves a significant commitment of time and resources and is subject to a number of risks and challenges including:

• | Managing the length of the development cycle for new products and product enhancements, which has frequently been longer than we originally expected; |

• | Adapting to emerging and evolving industry standards and to technological developments by our competitors and customers; |

• | Extending the operation of our products and services to new and evolving platforms, operating systems and hardware products, such as mobile devices; |

• | Entering into new or unproven markets with which we have limited experience; |

• | Managing new product and service strategies for the markets in which we operate; |

• | Addressing trade compliance issues affecting our ability to ship our products; |

• | Developing or expanding efficient sales channels; and |

• | Obtaining sufficient licenses to technology and technical access from operating system software vendors on reasonable terms to enable the development and deployment of interoperable products, including source code licenses for certain products with deep technical integration into operating systems. |

If we are not successful in managing these risks and challenges, or if our new products, product upgrades and services are not technologically competitive or do not achieve market acceptance, our business and operating results could be adversely affected.

We operate in a highly competitive environment, and our competitors may gain market share in the markets for our products that could adversely affect our business and cause our revenues to decline.

We operate in intensely competitive markets that experience rapid technological developments, changes in industry

9

standards, changes in customer requirements and frequent new product introductions and improvements. If we are unable to anticipate or react to these competitive challenges or if existing or new competitors gain market share in any of our markets, our competitive position could weaken and we could experience a decline in our sales that could adversely affect our business and operating results. To compete successfully, we must maintain an innovative research and development effort to develop new products and services and enhance existing products and services, effectively adapt to changes in the technology or product rights held by our competitors, appropriately respond to competitive strategies and effectively adapt to technological changes and changes in the ways that our information is accessed, used and stored within our enterprise and consumer markets. If we are unsuccessful in responding to our competitors or to changing technological and customer demands, our competitive position and our financial results could be adversely affected.

Our competitors include software vendors that offer software products that directly compete with our product offerings. In addition to competing with these vendors directly for sales to end-users of our products, we compete with them for the opportunity to have our products bundled with the product offerings of our strategic partners such as computer hardware OEMs and ISPs. Our competitors could gain market share from us if any of these strategic partners replace our products with the products of our competitors or if these partners more actively promote our competitors’ products than our products. In addition, software vendors who have bundled our products with theirs may choose to bundle their software with their own or other vendors’ software or may limit our access to standard product interfaces and inhibit our ability to develop products for their platform. In the future, further product development by these vendors could cause our software applications and services to become redundant, which could significantly impact our sales and financial results.

We face growing competition from network equipment, computer hardware manufacturers, large operating system providers and other technology companies, as well as from companies in the identity threat protection space such as credit bureaus. Many of these competitors are increasingly developing and incorporating into their products data protection software that competes at some levels with our product offerings. Our competitive position could be adversely affected to the extent that our customers perceive the functionality incorporated into these products as replacing the need for our products.

Security protection is also offered by some of our competitors at prices lower than our prices or, in some cases is offered free of charge. Some companies offer the lower-priced or free security products within their computer hardware or software products that we believe are inferior to our products and SaaS offerings. Our competitive position could be adversely affected to the extent that our customers perceive these security products as replacing the need for more effective, full featured products and services, such as those that we provide. The expansion of these competitive trends could have a significant negative impact on our sales and financial results by causing, among other things, price reductions of our products, reduced profitability and loss of market share.

Many of our competitors have greater financial, technical, sales, marketing or other resources than we do and consequently, may have the ability to influence customers to purchase their products instead of ours. Further consolidation within our industry or other changes in the competitive environment could result in larger competitors that compete with us on several levels. We also face competition from many smaller companies that specialize in particular segments of the markets in which we compete.

Reduced trust in our SSL/TLS certificates could adversely affect our website security business.

Our website security business depends on the widespread acceptance of the digital certificates we provide to enable communications security infrastructure. We have in the past issued, and may in the future issue, SSL/TLS certificates out of compliance with the requirements of the Certificate Authority and Browser Forum Baseline Requirements. Failures of this kind could cause popular browsers to reduce or eliminate trust in our SSL/TSL certificates or the related roots or otherwise disrupt our position as a leading certificate authority. For example, Google recently issued a proposal to reduce trust in our SSL/TSL certificates based on our past issuance of non-compliant certificates. If any popular browser reduced trust in our SSL/TSL certificates or roots, it would damage our brand and cause our SSL/TSL certificates to fail to interoperate, resulting in customer attrition for our website security business, which could adversely affect our results of operations and our stock price.

Fluctuations in our quarterly financial results have affected the trading price of our outstanding securities in the past and could affect the trading price of outstanding securities in the future.

Our quarterly financial results have fluctuated in the past and are likely to vary significantly in the future due to a number of factors, many of which are outside of our control. If our quarterly financial results or our predictions of future financial results fail to meet our expectations or the expectations of securities analysts and investors, the trading price of our outstanding securities could be negatively affected. Any volatility in our quarterly financial results may make it more difficult for us to raise capital in the future or pursue acquisitions that involve issuances of our stock. Our operating results for prior periods may not be effective predictors of our future performance.

Factors associated with our industry, the operation of our business, and the markets for our products may cause our quarterly financial results to fluctuate, including:

• | Fluctuations in demand for any of our products and services; |

• | Entry of new competition into our markets; |

• | Competitive pricing pressure for one or more of our classes of products; |

• | Our ability to timely complete the release of new or enhanced versions of our products; |

• | How well we execute our strategy and operating plans and the impact of changes in our business operations or business model that could result in significant restructuring charges; |

10

• | The impact of future acquisitions; |

• | Fluctuations in foreign currency exchange rates; |

• | The number, severity, and timing of threat outbreaks (e.g. worms, viruses, malware, ransomware and other malicious threats); |

• | Our resellers making a substantial portion of their purchases near the end of each quarter; |

• | Enterprise customers’ tendency to negotiate site licenses near the end of each quarter; |

• | Our sales cycle, which may lengthen as the complexity of products and competition in our markets increases; |

• | The timing of and rate and discounts at which customers replace older versions of the hardware that reach end of life; |

• | Cancellation, deferral, or limitation of orders by customers; |

• | Changes in the mix or type of products sold; |

• | Movements in interest rates; |

• | The rate of adoption of new product technologies and new releases of operating systems; |

• | Changes in accounting rules; |

• | Weakness or uncertainty in general economic or industry conditions in any of the multiple markets in which we operate that could reduce customer demand and ability to pay for our products and services; |

• | Political and military instability, which could slow spending within our target markets, delay sales cycles, and otherwise adversely affect our ability to generate revenues and operate effectively; |

• | Budgetary constraints of customers, which are influenced by corporate earnings and government budget cycles and spending objectives; |

• | Disruptions in our business operations or target markets caused by, among other things, earthquakes, floods, or other natural disasters affecting our headquarters located in Silicon Valley, California, an area known for seismic activity, or our other locations worldwide; |

• | Acts of war or terrorism; |

• | Intentional disruptions by third parties; and |

• | Health or similar issues, such as a pandemic. |

Any of the foregoing factors could cause the trading price of our outstanding securities to fluctuate significantly.

Our business models present execution and competitive risks.

In recent years, our SaaS offerings have become increasingly critical in our business. Our competitors are rapidly developing and deploying SaaS offerings for consumers and business customers. Pricing and delivery models are evolving. Devices and form factors influence how users access services in the cloud. We are making significant investments in, and devoting significant resources to develop and deploy, our own SaaS strategies, including our acquisition of Blue Coat in August 2016. We cannot assure you that our investments in and development of SaaS offerings will achieve the expected returns for us or that we will be able to compete successfully in the marketplace. In addition to software development costs, we are incurring costs to build and maintain infrastructure to support SaaS offerings. These costs may reduce the operating margins we have previously achieved. Whether we are successful in this business model depends on our execution in a number of areas, including:

• | Continuing to innovate and bring to market compelling cloud-based experiences that generate increasing traffic and market share; and |

• | Ensuring that our SaaS offerings meet the reliability expectations of our customers and maintain the security of their data. |

We may need to change our pricing models to compete successfully.

The intense competition we face in the sales of our products and services and general economic and business conditions can put pressure on us to change our prices. If our competitors offer deep discounts on certain products or services or develop products that the marketplace considers more valuable, we may need to lower prices or offer other favorable terms in order to compete successfully. Any such changes may reduce margins and could adversely affect operating results. Additionally, the increasing prevalence of cloud and SaaS delivery models offered by us and our competitors may unfavorably impact pricing in both our on-premise enterprise software business and our cloud business, as well as overall demand for our on-premise software product and service offerings, which could reduce our revenues and profitability. Our competitors may offer lower pricing on their support offerings, which could put pressure on us to further discount our product or support pricing.

Any broad-based change to our prices and pricing policies could cause our revenues to decline or be delayed as our sales force implements and our customers adjust to the new pricing policies. We or our competitors may bundle products for promotional purposes or as a long-term go-to-market or pricing strategy or provide guarantees of prices and product implementations. These practices could, over time, significantly constrain the prices that we can charge for certain of our products. If we do not adapt our pricing models to reflect changes in customer use of our products or changes in customer

11

demand, our revenues could decrease. The increase in open source software distribution may also cause us to change our pricing models.

Defects, disruptions or risks related to the provision of our SaaS offerings could impair our ability to deliver our services and could expose us to liability, damage our brand and reputation or otherwise negatively impact our business.

Our SaaS offerings may contain errors or defects that users identify after they begin using them that could result in unanticipated service interruptions, which could harm our reputation and our business. Since our customers use our SaaS offerings for mission-critical protection from threats to electronic information, endpoint devices, and computer networks, any errors, defects, disruptions in service or other performance problems with our SaaS offerings could significantly harm our reputation and may damage our customers’ businesses. If that occurs, customers could elect not to renew, or delay or withhold payment to us, we could lose future sales or customers may make warranty or other claims against us, which could result in an increase in our provision for doubtful accounts, an increase in collection cycles for accounts receivable or the expense and risk of litigation.

We currently serve our SaaS-based customers from hosting facilities located across the globe. Damage to, or failure of, any significant element of these hosting facilities could result in interruptions in our service, which could harm our customers and expose us to liability. Interruptions or failures in our service delivery could cause customers to terminate their subscriptions with us, could adversely affect our renewal rates, and could harm our ability to attract new customers. Our business would also be harmed if our customers believe that our SaaS offerings are unreliable.

We collect, use, disclose, store or otherwise process personal information, which subjects us to privacy and data security laws and contractual commitments, and our actual or perceived failure to comply with such laws and commitments could harm our business.

We collect, use, store or disclose (collectively, “process”) an increasingly large amount of personal information, including from employees and customers, in connection with the operation of our business. The volume, variety and velocity of the personal information we process increased significantly as a result of our acquisition of LifeLock in February 2017, as its identity and fraud protection offerings rely on large data repositories of personal information and consumer transactions. The personal information we process is subject to an increasing number of federal, state, local and foreign laws regarding privacy and data security, as well as contractual commitments. Any failure or perceived failure by us to comply with such obligations may result in governmental enforcement actions, fines, litigation, or public statements against us by consumer advocacy groups or others and could cause our customers to lose trust in us, which could have an adverse effect on our reputation and business. Our customers may also accidentally disclose their passwords or store them on a device that is lost or stolen, creating the perception that our systems are not secure against third-party access.

Additionally, if third parties that we work with, such as vendors or developers, violate applicable laws or our policies, such violations may also place personal information at risk and have an adverse effect on our business. Changes to applicable privacy or data security laws could impact how we process personal information, and therefore limit the effectiveness of our products, services or features, or our ability to develop new products, services or features.

Our acquisitions and divestitures create special risks and challenges that could adversely affect our future financial results.

As part of our business strategy, we may acquire or divest businesses or assets. These activities can involve a number of special risks and challenges, including:

• | Complexity, time and costs associated with managing these transactions, including the integration of acquired business operations, workforce, products, and technologies; |

• | Diversion of management time and attention; |

• | Loss or termination of employees, including costs associated with the termination or replacement of those employees; |

• | Assumption of liabilities of the acquired business or assets, including litigation related to the acquired business or assets; |

• | The addition of acquisition-related debt as well as increased expenses and working capital requirements; |

• | Dilution of stock ownership of existing stockholders; |

• | Increased or unexpected costs, unanticipated delays or failure to meet contractual obligations; and |

• | Substantial accounting charges for restructuring and related expenses, write-off of in-process research and development, impairment of goodwill, amortization of intangible assets, and stock-based compensation expense. |

If integration of our acquired businesses is not successful, we may not realize the potential benefits of an acquisition or suffer other adverse effects. To integrate acquired businesses, we must integrate and manage the personnel and technology systems of the acquired operations. We also must effectively integrate the different cultures of acquired business organizations into our own in a way that aligns various interests, and may need to enter new markets in which we have no or limited experience and where competitors in such markets have stronger market positions. Moreover, to be successful, some acquisitions, particularly acquisitions of large, complex companies, such as Blue Coat and LifeLock, depend on large-scale product, technology and sales force integrations that are difficult to complete on a timely basis or at all, and may be more susceptible to the special risks and

12

challenges described above.

Any of the foregoing, and other factors, could harm our ability to achieve anticipated levels of profitability or other financial benefits from our divested or acquired businesses or assets or to realize other anticipated benefits of divestitures or acquisitions, such as anticipated operating efficiencies or other cost savings.

If we fail to manage our sales and distribution channels effectively, or if our partners choose not to market and sell our products to their customers, our operating results could be adversely affected.

We sell our products to customers around the world through multi-tiered sales and distribution networks.

Sales through these different channels involve distinct risks, including the following:

Direct Sales. A significant portion of our revenues from enterprise products is derived from sales by our direct sales force to end-users. Special risks associated with direct sales include:

• | Longer sales cycles associated with direct sales efforts; |

• | Difficulty in hiring, retaining, and motivating our direct sales force, particularly through periods of transition in our organization; and |

• | Substantial amounts of training for sales representatives to become productive in selling our products and services, including regular updates to cover new and revised products, and associated delays and difficulties in recognizing the expected benefits of investments in new products and updates. |

Indirect Sales Channels. A significant portion of our revenues is derived from sales through indirect channels, including distributors that sell our products to end-users and other resellers. This channel involves a number of risks, including:

• | Our lack of control over the timing of delivery of our products to end-users; |

• | Our resellers and distributors are generally not subject to minimum sales requirements or any obligation to market our products to their customers; |

• | Our reseller and distributor agreements are generally nonexclusive and may be terminated at any time without cause; |

• | Our resellers and distributors frequently market and distribute competing products and may, from time to time, place greater emphasis on the sale of these products due to pricing, promotions, and other terms offered by our competitors; and |

• | The consolidation of electronics retailers has increased their negotiating power with respect to hardware and software providers such as us. |

OEM Sales Channels. A portion of our revenues is derived from sales through our OEM partners that incorporate our products into, or bundle our products with, their products. Our reliance on this sales channel involves many risks, including:

• | Our lack of control over the volume of systems shipped and the timing of such shipments; |

• | Our OEM partners are generally not subject to minimum sales requirements or any obligation to market our products to their customers; |

• | Our OEM partners may terminate or renegotiate their arrangements with us and new terms may be less favorable due to competitive conditions in our markets and other factors; |

• | Sales through our OEM partners are subject to changes in general economic conditions, strategic direction, competitive risks, and other issues that could result in a reduction of OEM sales; |

• | The development work that we must generally undertake under our agreements with our OEM partners may require us to invest significant resources and incur significant costs with little or no assurance of ever receiving associated revenues; |

• | The time and expense required for the sales and marketing organizations of our OEM partners to become familiar with our products may make it more difficult to introduce those products to the market; and |

• | Our OEM partners may develop, market, and distribute their own products and market and distribute products of our competitors, which could reduce our sales. |

If we fail to manage our sales and distribution channels successfully, these channels may conflict with one another or otherwise fail to perform as we anticipate, which could reduce our sales and increase our expenses as well as weaken our competitive position. Some of our distribution partners have experienced financial difficulties in the past, and if our partners suffer financial difficulties in the future because of general economic conditions or for other reasons, these partners may delay paying their obligations to us and we may have reduced sales or increased bad debt expense that could adversely affect our operating results. In addition, reliance on multiple channels subjects us to events that could cause unpredictability in demand, which could increase the risk that we may be unable to plan effectively for the future, and could result in adverse operating results in future periods.

Over the long term we intend to invest in research and development activities, and these investments may achieve delayed, or lower than expected, benefits which could harm our operating results.

While we continue to focus on managing our costs and expenses, over the long term, we also intend to invest significantly in

13

research and development activities as we focus on organic growth through internal innovation in each of our business segments. We believe that we must continue to dedicate a significant amount of resources to our research and development efforts to maintain our competitive position, and that the level of these investments will increase in future periods as the Blue Coat acquisition has expanded our focus areas. We recognize the costs associated with these research and development investments earlier than the anticipated benefits, and the return on these investments may be lower, or may develop more slowly, than we expect. If we do not achieve the benefits anticipated from these investments, or if the achievement of these benefits is delayed, our operating results may be adversely affected.

Changes in industry structure and market conditions could lead to charges related to discontinuances of certain of our products or businesses and asset impairments.

In response to changes in industry and market conditions, we may be required to strategically reallocate our resources and consider restructuring, disposing of or otherwise exiting businesses. Any decision to limit investment in or dispose of or otherwise exit businesses may result in the recording of special charges, such as inventory and technology-related write-offs, workforce reduction costs, charges relating to consolidation of excess facilities or claims from third parties who were resellers or users of discontinued products. Our estimates with respect to the useful life or ultimate recoverability of our carrying basis of assets, including purchased intangible assets, could change as a result of such assessments and decisions. Although in certain instances our supply agreements allow us the option to cancel, reschedule and adjust our requirements based on our business needs prior to firm orders being placed, our loss contingencies may include liabilities for contracts that we cannot cancel, reschedule or adjust with contract manufacturers and suppliers.

Further, our estimates relating to the liabilities for excess facilities are affected by changes in real estate market conditions. Additionally, we are required to evaluate goodwill impairment on an annual basis and between annual evaluations in certain circumstances, and future goodwill impairment evaluations may result in a charge to earnings.

Our inability to successfully recover from a disaster or other business continuity event could impair our ability to deliver our products and services and harm our business.

We are heavily reliant on our technology and infrastructure to provide our products and services to our customers. For example, we host many of our products using third-party data center facilities and we do not control the operation of these facilities. These facilities are vulnerable to damage, interruption or performance problems from earthquakes, hurricanes, floods, fires, power loss, telecommunications failures and similar events. They are also subject to break-ins, computer viruses, sabotage, intentional acts of vandalism and other misconduct. The occurrence of a natural disaster or an act of terrorism, a decision to close the facilities without adequate notice or other unanticipated problems could result in lengthy interruptions in the delivery of our products and services.

Furthermore, our business administration, human resources and finance services depend on the proper functioning of our computer, telecommunication and other related systems and operations. A disruption or failure of these systems or operations because of a disaster or other business continuity event could cause data to be lost or otherwise delay our ability to complete sales and provide the highest level of service to our customers. In addition, we could have difficulty producing accurate financial statements on a timely basis, which could adversely affect the trading value of our stock. Although we endeavor to ensure there is redundancy in these systems and that they are regularly backed-up, there are no assurances that data recovery in the event of a disaster would be effective or occur in an efficient manner, including the operation of our global civilian cyber intelligence threat network.

Any errors, defects, disruptions or other performance problems with our products and services could harm our reputation and may damage our customers’ businesses. For example, we may experience disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, human or software errors, capacity constraints due to an overwhelming number of users accessing our website simultaneously, fraud or security attacks. In some instances, we may not be able to identify the cause or causes of these performance problems within an acceptable period of time. Interruptions in our products and services, including the operation of our global civilian cyber intelligence threat network, could impact our revenues or cause customers to cease doing business with us. In addition, our business would be harmed if any of events of this nature caused our customers and potential customers to believe our services are unreliable. Our operations are dependent upon our ability to protect our technology infrastructure against damage from business continuity events that could have a significant disruptive effect on our operations. We could potentially lose customer data or experience material adverse interruptions to our operations or delivery of services to our clients in a disaster recovery scenario.

We may experience difficulties in realizing the expected benefits of the acquisition of Blue Coat and LifeLock and may continue to incur significant acquisition-related costs and transition costs in connection with these acquisitions.

We completed the acquisition of Blue Coat in the second quarter of fiscal 2017 and LifeLock in the fourth quarter of fiscal 2017. We have invested and continue to invest substantial monetary and other resources in the integration of these companies. The success of each acquisition depends in part on our ability to realize the anticipated business opportunities, including certain cost savings and operational efficiencies or synergies and growth prospects from combining the respective companies with Symantec in an efficient and effective manner. We may never realize these business opportunities and growth prospects. We may incur additional costs to maintain employee morale and to retain key employees. Management cannot ensure that the elimination of duplicative costs or the realization of other efficiencies will offset the transaction and integration costs in the near term or at all.

Additionally, we may encounter difficulties surrounding the integration of these companies, which could delay or prevent our achievement of the expected benefits from the respective acquisition. Moreover, risks specific to the acquired businesses could

14

also delay or prevent our achievement of the expected benefits from the respective acquisition. For example, since LifeLock’s identity and fraud protection products depend extensively upon continued access to and receipt of credible, timely and complete data from external sources, including data received from customers, vendors who are also competitors and fulfillment partners, the value we derive from the LifeLock acquisition, our competitive position and our business, results of operations, and financial condition could be harmed as a result of our loss of access to data sources or reliance on sources that prove to be ineffective or inaccurate.

As a result of our acquisition of LifeLock, our Consumer Digital Safety segment became subject to increased regulation, which could impede our ability to market and provide our services or adversely affect our business, financial position and results of operations.

As a result of our acquisition of LifeLock, a portion of our Consumer Digital Safety segment became subject to increased regulation, including a wide variety of federal, state, and local laws and regulations, including the Fair Credit Reporting Act, the Gramm-Leach-Bliley Act, the Federal Trade Commission Act (“FTC Act”), and comparable state laws that are patterned after the FTC Act. Moreover, LifeLock entered into consent decrees and similar arrangements with the Federal Trade Commission (the “FTC”) and 35 states’ attorneys general in 2010, and a settlement with the FTC in 2015 relating to allegations that certain of LifeLock’s advertising and marketing practices constituted deceptive acts or practices in violation of the FTC Act, which impose additional restrictions on the LifeLock business within our Consumer Digital Safety segment, including prohibitions against making any misrepresentation of “the means, methods, procedures, effects, effectiveness, coverage, or scope of” LifeLock’s identity theft protection services. Any of the laws and regulations that apply to our business are subject to revision or new or changed interpretations, and we cannot predict the impact of such changes on our business.

Additionally, as a result of our LifeLock acquisition, aspects of our Consumer Digital Safety segment are subject to the broad regulatory, supervisory, and enforcement powers of the Consumer Financial Protection Bureau (CFPB) and may exercise authority with respect to our services, or the marketing and servicing of those services, by overseeing our financial institution or credit reporting agency customers and suppliers, or by otherwise exercising its supervisory, regulatory, or enforcement authority over consumer financial products and services.

Any cost reduction initiatives that we undertake may not deliver the results we expect, and these actions may adversely affect our business.

In May 2016 we announced a fiscal 2017 restructuring plan to be achieved by the end of fiscal 2018. This initiative could result in disruptions to our operations. Any cost-cutting measures could also negatively impact our business by delaying the introduction of new products or technologies, interrupting service of additional products, or impacting employee retention. In addition, we cannot be sure that the cost reduction and streamlining initiatives will be as successful in reducing our overall expenses as we expect or that additional costs will not offset any such reductions or streamlining. If our operating costs are higher than we expect or if we do not maintain adequate control of our costs and expenses, our results of operations will suffer.

Our international operations involve risks that could increase our expenses, adversely affect our operating results, and require increased time and attention of our management.

We derive a substantial portion of our revenues from customers located outside of the U.S. and we have significant operations outside of the U.S., including engineering, sales, customer support, and production. We have expanded through our acquisition of Blue Coat and expect further expansion of our international operations, but such expansion is contingent upon our identification of growth opportunities. Our international operations are subject to risks in addition to those faced by our domestic operations, including:

• | Potential loss of proprietary information due to misappropriation or laws that may be less protective of our intellectual property rights than U.S. laws or that may not be adequately enforced; |

• | Requirements of foreign laws and other governmental controls, including trade and labor restrictions and related laws that reduce the flexibility of our business operations; |

• | Regulations or restrictions on the use, import, or export of encryption technologies that could delay or prevent the acceptance and use of encryption products and public networks for secure communications; |

• | Local business and cultural factors that differ from our normal standards and practices, including business practices that we are prohibited from engaging in by the Foreign Corrupt Practices Act and other anti-corruption laws and regulations; |

• | Central bank and other restrictions on our ability to repatriate cash from our international subsidiaries or to exchange cash in international subsidiaries into cash available for use in the U.S.; |

• | Fluctuations in currency exchange rates, economic instability and inflationary conditions could reduce our customers’ ability to obtain financing for software products or could make our products more expensive or could increase our costs of doing business in certain countries; |

• | Limitations on future growth or inability to maintain current levels of revenues from international sales if we do not invest sufficiently in our international operations; |

• | Longer payment cycles for sales in foreign countries and difficulties in collecting accounts receivable; |

• | Difficulties in staffing, managing, and operating our international operations, including difficulties related to administering our stock plans in some foreign countries; |

15

• | Difficulties in coordinating the activities of our geographically dispersed and culturally diverse operations; |

• | Seasonal reductions in business activity in the summer months in Europe and in other periods in other countries; |

• | Costs and delays associated with developing software and providing support in multiple languages; and |

• | Political unrest, war, or terrorism, or regional natural disasters, particularly in areas in which we have facilities. |

A significant portion of our transactions outside of the U.S. is denominated in foreign currencies. Accordingly, our revenues and expenses will continue to be subject to fluctuations in foreign currency rates. For example, in recent periods the U.S. dollar has strengthened significantly against the Euro and other major currencies, which has adversely impacted our reported international revenue. We expect to be affected by fluctuations in foreign currency rates in the future, especially if international sales continue to grow as a percentage of our total sales or our operations outside the U.S. continue to increase.