Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - Simulations Plus, Inc. | simulations_8k-ex9901.htm |

| 8-K - CURRENT REPORT - Simulations Plus, Inc. | simulations_8k-041017.htm |

Exhibit 99.2

(NASDAQ:SLP) Investor Conference Call April 10, 2017

2 With the exception of historical information, the matters discussed in this presentation are forward - looking statements that involve a number of risks and uncertainties . The actual results of the Company could differ significantly from those statements . Factors that could cause or contribute to such differences include, but are not limited to : continuing demand for the Company’s products, competitive factors, the Company’s ability to finance future growth, the Company’s ability to produce and market new products in a timely fashion, the Company’s ability to continue to attract and retain skilled personnel, and the Company’s ability to sustain or improve current levels of productivity . Further information on the Company’s risk factors is contained in the Company’s quarterly and annual reports and filed with the Securities and Exchange Commission . Safe Harbor Statement

3 Highlights John DiBella VP of Marketing & Sales

4 • Major provider of software and consulting services for scientific R&D • Earliest drug discovery – when a chemist first draws a molecule • Preclinical development (lab and animals) through first - in - human trials • Safety research and risk assessment • Phase 2 and 3 clinical trials • Beyond patent life to supporting generic companies • 2QFY17 • Revenues up $542,000 (10.5%) to $5.71 million • Net income up $50,000 (4.4%) to $1.20 million • Software renewal rates: 89% (accounts); 96%(fees) • 20 new software clients added • Strong consulting pipeline resulted in significant increase in revenues • Current backlog remains high • Successfully adding modelers and scientists to team • 6MoFY17 • Revenues up $1.12 million (11.2%) to $11.12 million • Net income up $306,000 (13.6%) to $2.56 million • Diluted earnings per share up 12.3% to 15¢ per share • 43 new software clients added Overview

5 • Now in 3 rd and final year of $200,000/year collaboration for improved ocular dosing simulations • Established consortium of leading pharmaceutical companies • The global ophthalmic drugs market was valued at $16 billion in 2012, and was expected to reach an estimated value of $21.6 billion in 2018 • Prevalence of eye disorders is increasing as the population ages (e.g., diabetic retinopathy, macular degeneration) FDA Office of Generic Drugs (OGD) Funded Collaborations • In year two of 3 - year, $200,000/year collaboration for simulation of long - acting injectable microspheres • Formed consortium of industry partners, FDA scientists, and Simulations Plus • Added intramuscular dosing to GastroPlus (v9.5) • Developed enhancements to DDDPlus to simulate in vitro dissolution/release from polymer microspheres

* Yahoo! Data 4/7/2017 Two - year stock performance compared to DOW, NASDAQ, & S&P 500 *

7 Financial Overview John Kneisel Chief Financial Officer

8 Income Statement: 2QFY17 Versus 2QFY16 (in millions) Lancaster Buffalo 2QFY17 2QFY16 Diff % chg Net sales $ 4.04 $ 1.66 $ 5.71 $ 5.16 $ 0.54 10.5% Gross profit 3.31 0.84 4.15 3.90 0.25 6.5% Gross profit margin 82.0% 50.3% 72.8% 75.5% - 2.8% - 3.7% SG&A $ 1.34 $ 0.60 $ 1.95 $ 1.72 $ 0.23 13.1% R&D 0.40 0.01 0.41 0.46 (0.05) - 11.5% Total operating expenses 1.75 0.61 2.36 2.18 0.17 7.9% Income from operations 1.57 0.23 1.80 1.72 0.08 4.6% Income from operations before income taxes 1.56 0.23 1.79 1.69 0.09 5.5% Net income 1.06 0.14 1.20 1.15 0.05 4.4% Diluted earnings per share (in dollars) $ 0.069 $ 0.066 $ 0.002 3.4% EBITDA 1.98 0.322 2.302 2.177 0.125 5.7%

9 Income Statement: 6MoFY17 Versus 6MoFY16 (in millions) Lancaster Buffalo 6MoFY17 6MoFY16 Diff % chg Net sales $ 7.74 $ 3.39 $ 11.12 $ 10.00 $ 1.12 11.2% Gross profit 6.33 1.91 8.2 7.7 $ 0.6 7.6% Gross profit margin 81.8% 56.3% 74.0% 76.5% - 2.5% - 3.3% SG&A $ 2.59 $ 1.22 $ 3.81 $ 3.40 $ 0.41 12.1% R&D 0.68 0.02 0.70 0.81 (0.11) - 14.0% Total operating expenses 3.27 1.24 4.51 4.21 0.30 7.1% Income from operations 3.06 0.67 3.72 3.44 0.28 8.1% Income from operations before income taxes 3.09 0.67 3.75 3.41 0.34 10.1% Net income 2.14 0.42 2.56 2.25 0.31 13.6% Diluted earnings per share (in dollars) $ 0.147 0.131 0.016 12.3% EBITDA 3.93 0.86 4.79 4.02 0.76 19.0%

10 Consolidated Revenues: Fiscal Quarter ( pro forma prior to 2012; in millions) 4.01 4.57 5.94 3.71 4.84 5.16 6.01 3.96 5.42 5.71 $0 $1 $2 $3 $4 $5 $6 $7 Q1 Q2 Q3 Q4 2009 2010 2011 2012 2013 2014 2015 2016 2017

11 Consolidated Net Income: Fiscal Quarter ( pro forma prior to 2012; in millions) $0.33 $0.47 $0.53 $0.17 $0.44 $0.85 $0.74 $0.21 $0.56 $0.91 $1.05 $0.17 $0.76 $0.84 $0.87 $0.35 $0.59 $1.06 $0.99 $0.24 $0.69 $0.81 $1.31 $0.22 $0.53 $0.97 $1.85 $0.49 $1.11 $1.15 $1.91 $0.79 $1.36 $1.20 $ - $0.50 $1.00 $1.50 $2.00 $2.50 Q1 Q2 Q3 Q4 2009 2010 2011 2012 2013 2014 2015 2016 2017

12 Consolidated Diluted Earnings Per Share 0 0.02 0.04 0.06 0.08 0.1 0.12 Q1 Q2 Q3 Q4 $0.03 $0.06 $0.11 $0.03 $0.06 $0.07 $0.11 $0.05 $0.08 $0.07 Quarterly EPS FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

13 Consolidated EBITDA: Fiscal Quarter ( in millions) 1.20 1.35 2.30 0.67 1.22 1.97 3.33 1.19 2.22 2.18 3.28 1.51 2.48 2.30 $0 $1 $2 $3 $4 Q1 Q2 Q3 Q4 2009 2010 2011 2012 2013 2014 2015 2016 2017

14 Returning Cash to Shareholders (in millions) 0.8 0.8 2.2 0 0.5 0.5 0.6 0.81 0.81 0.81 0.84 0.84 0.84 0.85 0.85 0.85 0.85 0.85 0.86 0.86 12.7 11.4 9.3 9.8 10 10.1 10.6 11 7.8 8.6 5.8 6.1 6.4 8.6 7.2 7.1 8.8 8 8.8 7.4 8.6 $0 $1 $1 $2 $2 $3 $0 $2 $4 $6 $8 $10 $12 $14 Dividend Paid Cash on Hand Cash paid $2.5M TSRL Cash paid $2.1M for Cognigen Cash paid $720K for Cognigen

15 Selected Balance Sheet Items (in millions, except where indicated) February 28, 2017 August 31, 2016 Cash and cash equivalents $ 7.427* $ 8.030* Cash per share ( in Dollars ) $ 0.43 $ 0.47 Total current assets 13.989 12.700 Total assets 28.761 27.814 Total current liabilities 2.140 2.126 Total liabilities 4.896 5.082 Current ratio 6.54x 5.98x Shareholders’ equity 23.865 22.733 Total liabilities and shareholders’ equity 28.761 27.814 Shareholders’ equity per diluted share( in Dollars ) $1.370 $1.335 * Cash as of April 7, 2017 ~$8.6 million.

16 Marketing and Sales John DiBella VP of Marketing and Sales

17 End - to - end M&S Solutions Provider N H O OH O CH 3 CH 3 CH 3 ADMET Predictor™ GastroPlus ™ MedChem Studio™ MedChem Designer™ DDDPlus ™ MembranePlus™ Consulting Services and Collaborations Discovery Preclinical Clinical PKPlus™ KIWI™

18 • Version 9.5 released in April 2017 ‒ Intramuscular dosing model – optional add - on model ‒ Antibody - drug conjugate (ADC) models for biologics • Version 8.1 released in January 2017 ‒ 64 - bit compatibility & minor bug fixes ‒ Rebuilt toxicity models • Version 4.0 still licensed by clients ‒ Many features merged into ADMET Predictor 8.0 as optional add - on to consolidate under one GUI Software Product News • Version 5.5 scheduled for mid - 2017 ‒ New dosage form options for immediate & controlled release formulations ‒ Tighter integration with GastroPlus: options for analyzing data collected from experiments • Version 1.5 scheduled for mid - 2017 ‒ Ability to model multiple compounds to optimize in vitro drug - drug interaction parameters ‒ New models to analyze data collected from hepatocyte studies (expands user base) • Version 1.5 scheduled for mid - 2017 ‒ Addresses several items reported from prospects/clients during testing ‒ Numerous evaluations ongoing/planned

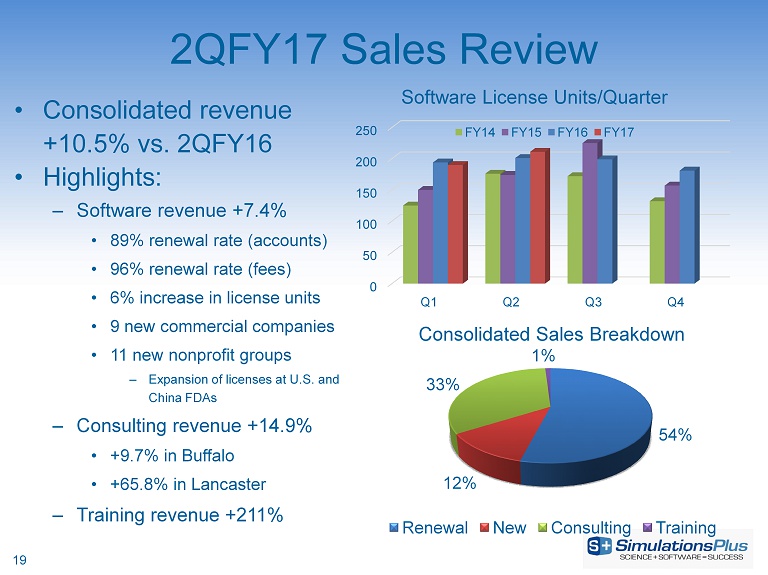

2QFY17 Sales Review • Consolidated revenue +10.5% vs. 2QFY16 • Highlights: – Software revenue +7.4% • 89% renewal rate (accounts) • 96% renewal rate (fees) • 6% increase in license units • 9 new commercial companies • 11 new nonprofit groups – Expansion of licenses at U.S. and China FDAs – Consulting revenue +14.9% • +9.7% in Buffalo • +65.8% in Lancaster – Training revenue +211% 54% 12% 33% 1% Consolidated Sales Breakdown Renewal New Consulting Training 0 50 100 150 200 250 Q1 Q2 Q3 Q4 Software License Units/Quarter FY14 FY15 FY16 FY17 19

6MoFY17 Sales Review • Consolidated revenue +11.2% vs. 6MoFY16 • Highlights: – Software revenue +7.3% • 88% renewal rate (accounts) • 96% renewal rate (fees) • 2% increase in license units • 22 new commercial companies • 21 new nonprofit groups – Expansion of licenses at U.S. EPA and CDC – Consulting revenue +18% • +14.5% in Buffalo • +42.2% in Lancaster – Training revenue +56.1% 52% 12% 35% 1% Consolidated Sales Breakdown Renewal New Consulting Training 0 50 100 150 200 250 Q1 Q2 Q3 Q4 Software License Units/Quarter FY14 FY15 FY16 FY17 20

2QFY17 Software Revenue – by Region Europe 33% North America 44% Asia 23% South America <1% Japan = 59% India = 22% China = 19% Korea = <1% 21

2Q17 Marketing Activities Website Content • Created video production room in Lancaster – Producing more video content for promotional/branding purposes • Increased focus on SEO performance Workshops and Conferences • GastroPlus PBPK workshops held in Orlando, Tokyo & San Diego – Full slate of workshops scheduled around the globe in 2017 • Hosted several onsite trainings at individual companies Strategic Digital Marketing Initiatives • Hosted 3 webinars on ADMET Predictor/GastroPlus modeling applications • Continued with active social media campaigns – Twitter/LinkedIn/Facebook followers have increased 15% vs. April 2016 – GastroPlus User Group membership increased 17% vs. April 2016 22

23 Buffalo Division Update Re - imagining the future of science - based research and development Ted Grasela President

24 Consulting Services • Strategic and synergistic benefits of the Buffalo (Cognigen) acquisition are being realized, as evidence by the record first quarter for Buffalo • Strong collaborations between Buffalo and Lancaster scientists have identified new and innovative ways of using modeling and simulation to bringing value to our clients • Consulting projects help shape management and regulatory decision - making process • Successful projects help drive additional consulting and software sales

25 Status Report - Consulting • In FY2017 working with 25 companies on 38 drugs, 65 projects – 6 new companies in FY2017 – 33 new projects in FY17 – 15 projects expanded scope in FY17 – 3 projects with reduced scope – 32 outstanding proposals with 20 different companies • In FY2017 presented 6 posters, published 1 peer - reviewed manuscript; 3 invited presentations, and 1 book chapter published – Working on 17 publications and 5 conference abstracts • Most common therapeutic area is oncology, followed by neurology, endocrinology, and infectious disease – ~45% of projects result directly in regulatory interaction.

26 Posters of Note • Lead Antimalarial Identification Using In Silico Prediction Methods and Simulation. – American Society for Clinical Pharmacology and Therapeutics – Morris D, Woltosz W, Lawless M, Grasela T, Clark R. • Modeling and simulation strategy to support eslicarbazepine acetate (ESL) development in pediatric patients in the treatment of partial - onset seizures. – Interactive Session on Pharmacometrics Applications to Pediatric Drug Development – American Conference on Pharmacometrics – Sunkaraneni S, Bihorel S, Ludwig E, Fiedler - Kelly J, Morris D, Hopkins S, Gallupi G, Blum D. Predicted K i = 0.0250 µ M (0.0110 µ g/mL) Effective Conc = 10* K i = 0.250 µ M (0.110 µ g/mL) Target concentration = 0.110 µ g/mL) Dosing Regimen: 100 mg, followed by 50 mg at 6, 24, and 48 hours

27 • Jill Fiedler - Kelly, has been appointed as a Member - at - Large to the American Society for Clinical Pharmacology and Therapeutics (ASCPT) Board of Directors for a 3 year term • ASCPT was founded in 1900, and consists of over 2,200 professionals whose primary interest is to advance the science and practice of clinical pharmacology and translational medicine for the therapeutic benefit of patients and society. ASCPT is the largest scientific and professional organization serving the disciplines of Clinical Pharmacology and Translational Medicine. Scientific Community Engagement

28 • Continued to work on $4.7 million contract with a major foundation to implement a KIWI platform for global teams engaged in model - based drug development; 5 - year term contingent on satisfactory completion of milestones • Project builds on our extensive process - related research; enables substantial enhancements to the KIWI platform • Enhancements will provide a scaffold with broad applicability and will be available to academic and industry clients of KIWI • Currently have 8 KIWI licenses • Have several KIWI demonstrations ongoing with research groups ranging from academics to large pharma • Have hired 3 full stack developers and a software quality assurance manager KIWI Update

29 Buffalo division is strong and growing • Consulting activities continuing to expand, and realizing synergies with Lancaster division for PBPK modeling in clinical pharmacology • Successful recruiting and on - boarding of software engineers and scientists to sustain growth patterns • Foundation contract accelerating KIWI platform development and is a major step forward in our long - term vision for the product • Continued interest in the academic and industry communities regarding licensing the product Summary

30 Final Summary John DiBella VP of Marketing & Sales

31 • 2QFY17 • Revenues up 10.5% to $5.71 million • Net income up by 4.4%, to $1.20 million or 7¢ per share, compared to $1.15 million, or 7¢ per share in 2QFY16 • 6MoFY17 • Revenues up 11.2% or $1.12 million to $11.12 million • Net income up 13.6% to $2.56 million, d iluted earnings per share up 15¢ per share from 13¢ per share in 6MoFY16 • California and Buffalo divisions both performing well • Expected synergies being realized • Addressing regulatory agency focus on applying PBPK modeling in clinical pharmacology & safety research • New guidance documents issued by FDA and EMA helping drive interest • 5 - year, $4.7 million contract with research foundation • Offers potential for additional such contracts with other organizations • We believe Simulations Plus continues to lead the trend toward greater use of modeling and simulation in research & development Summary