Attached files

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM

10-K

☒ ANNUAL REPORT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the

fiscal year ended August 31,

2016

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the

transition period from ___________ to ___________.

Commission file

number 333-182071

AIM EXPLORATION INC.

(Exact

name of registrant as specified in its charter)

|

Nevada

|

|

67-0682135

|

|

(State

or Other Jurisdiction of Incorporation of

Organization)

|

|

(I.R.S.

Employer Identification No.)

|

179

S Green Valley Pkwy, Suite 300

Henderson,

Nevada 89012

(Address of

principal executive offices)

1-844-246-7378

(Registrant’s

telephone number, including area code)

Securities

registered under Section 12(g) of the Exchange Act: Common Stock,

$0.001 par value, Preferred Stock, $0.001 par

value

Indicate by check

mark if the registrant is a well-known seasoned issuer, as defined

in Rule 405 of the Securities Act. Yes ☐

No ☒

Indicate by check

mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes

☐ No ☒

Indicate by check

mark whether the registrant (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports), and (2) has

been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check

mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§ 229.405 of this chapter) is not contained

herein, and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information

statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. ☐

Indicate by check

mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definition of “ large accelerated

filer and “

accelerated filer ” and “ smaller reporting

company ”

in Rule 12b-2 of the Exchange Act. (Check one):

Large

accelerated filer ☐

Accelerated

filer ☐

Non-accelerated

filer ☐

Smaller reporting

company ☒

Indicate by check

mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act) Yes ☐ No

☒

Aggregate market

value of the voting and non-voting stock of the registrant held by

non-affiliates of the registrant as of the last day of the

Company’s most recently-completed second fiscal quarter

(February 29, 2016): $220,753.

As of

December 15, 2016 the

registrant’s outstanding stock consisted of 576,728,348 common shares and

210,000 preferred

shares.

TABLE

OF CONTENTS

|

Item

1.

|

Business

|

3

|

|

Item

1A.

|

Risk

Factors

|

13

|

|

Item

1B.

|

Unresolved Staff

Comments

|

13

|

|

Item

2.

|

Properties

|

13

|

|

Item

3.

|

Legal

Proceedings

|

13

|

|

Item

4.

|

Mine

Safety Disclosures

|

13

|

|

Item

5.

|

Market

for Common Equity, Related Stockholder Matters and Issuer Purchases

of Equity Securities

|

14

|

|

Item

6.

|

Selected Financial

Data

|

16

|

|

Item

7.

|

Management's

Discussion and Analysis of Financial Condition and Results of

Operations

|

16

|

|

Item

7A.

|

Quantitative and

Qualitative Disclosures About Market Risk

|

19

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

19

|

|

Item

9.

|

Changes in and

Disagreements With Accountants on Accounting and Financial

Disclosure

|

42

|

|

Item

9A.

|

Controls and

Procedures

|

42

|

|

Item

9B.

|

Other

Information

|

42

|

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

43

|

|

Item

11.

|

Executive

Compensation

|

45

|

|

Item

12.

|

Security Ownership

of Certain Beneficial Owners and Management and Related Stockholder

Matters

|

46

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

47

|

|

Item

14.

|

Principal

Accountant Fees and Services

|

47

|

|

Item

15.

|

Exhibits,

Financial Statement Schedules

|

48

|

2

PART

1

Item 1. BUSINESS

We are

an exploration stage company engaged in the acquisition and

exploration of mineral properties with the intent to take

properties into production. We were incorporated as a Nevada

state corporation on February 18, 2010. We acquired mining

concession properties in Peru during the fiscal year ended August

31, 2014.

We are

considered an exploratory stage company, as we are involved in the

examination and investigation of land that we believe may contain

valuable minerals, for the purpose of discovering the presence of

ore, if any, and its extent. There is no assurance that a

commercially viable mineral deposit exists on the Peruvian

properties, and further exploration will be required before a final

evaluation as to the economic and legal feasibility for our future

exploration is determined. We have no known reportable

reserves of any type of mineral. To date, we have not

discovered an economically viable mineral deposit on the property,

and there is no assurance that we will discover one.

As of

August 31, 2016, we had cash reserves of $417 and a working

capital deficit of $2,897,303.

We do not have sufficient funds to enable us to complete the

initial phase of our exploration programs for the mining claims,

and will require additional financing in order to do so. There

is no assurance that we will be able to obtain additional

financing. Both advanced exploration and an economic

determination will be contingent upon the results of our

preliminary exploration programs and our ability to raise

additional financing in order to proceed with advanced exploration

and an economic evaluation. There is no assurance that we

will be able to obtain any additional financing to fund our

exploration activities.

Philippine Mining Claims

Nature

of Ownership

On

August 3, 2016, the Company terminated its management agreement

with Paladino Management and Development Corp. to manage operations

on the ground in the Philippines. The Philippine government enacted

new legislation which made it no longer financially feasible to

continue the Philippine feldspar operations.

Peruvian

Property

On June

23, 2014, Aim Exploration, Inc. entered into a Mining Concession

Asset Acquisition Agreement (the “Agreement”) with

Percana Mining Corp. (“Percana”). Pursuant to the

Agreement, the Company has acquired three separate mining

concessions. Two of the concession titles are unencumbered and

these make up 40% of the mining concessions. These two concessions

are known as El Tunel Del Tiempo 1 code 11060780 and El Tunel Del

Tiempo 2 code 11060781, and the registered ownership of these two

concessions have been transferred to the Company. The third

concession property is Agujeros Negros MA-AG makes up the remaining

60%, the documentation has all been completed to transfer ownership

to the company however formal registration has not yet been

completed however it is expected to be completed soon. Meanwhile

however, the Company has a Contract of Mining Assignment providing

AIM with full rights and authorities over the

concession.

In

consideration for the above concessions, the Company has issued

15,750, 000 common shares to Percana in two separate blocks; the

first In consideration for the above concessions, the Company has

issued 63,000 restricted common shares (15,750,000 restricted

common shares pre-consolidation) (Note 6) to Percana in two

separate blocks; the first block consists of 25,200 common shares

(6,300,000 common shares pre-consolidation) which are to be held in

escrow until either the Company raises $1,000,000 or when Percana

waives this requirement. The second block consists of 37,800 common

shares (9,450,000 common shares pre-consolidation) which are to be

held in escrow until such time as the Company is satisfied the

formal registration has been completed at which time the shares may

be released out of escrow at the option of Percana. On April 25,

2016, the Company entered into an amendment to its Agreement with

Percana and issued an additional 15,687,000 common shares to

Percana to bring its post-consolidation shareholdings back to

15,750,000 common shares. Furthermore, under the terms of the

amended Agreement, the Company agreed to issue additional common

shares to Percana at any time common shares are issued to any

director and/or controlling shareholder of the Company, the number

of common shares issued to Percana to be equal to those issued to

the director and/or controlling shareholder.

These

Mining Concessions were acquired based on the assumption the

properties are rich in high grade Anthracite Coal, currently there

are 20 small tunnels on the property already producing anthracite

coal which was being mined by illegal miners. Testing of the coal

samples was performed indicating the presence of high-grade

anthracite coal. Prior to acquisition AIM reviewed a non-compliant

technical report prepared by Engineers/Geologists together with

hiring a US based firm Gustavson Associates to visit the property

and review the reports. The firm provided AIM with a report, which

included recommendation for further exploration.

One of

the Company’s director is also a director of

Percana.

The

Peruvian Property consists of

three separate mining concessions, all are within one contiguous

block of property, and all three concessions are located in the

Province of Otuzco, La Libertad region. The formal transfer for two

of the mining concessions known as El Tunel del Tiempo 1 (Unique

code # 01-0209106 – 200 hectares) and El Tunel del Tiempo 2

(Unique code # 01-0209206 – 200 hectares) was executed

August1, 2014 and made into public deed on August 5, 2014 within

the Peruvian Public Registries.

3

The

third mining concession, known as Agujeros Negros MA-AG (unique

code # 01-0184000, 600 hectares) is under contract with AIM, as a

Contract of Mining Assignment and Option to Purchase was executed

on August 1, 2014 and was made into a Public Deed on August 5,

2014. By the Assignment and Option AIM has an irrevocable and

exclusive option to purchase 100% of the rights and interests of

this mining concession. This option was registered into public deed

on August 5, 2014. The option to purchase is for 5 years from the

date of registration which was completed Oct 2, 2014, in addition

contained within the contract AIM has complete control over this

mining concession for a period of 5 years following formal

registration which was registered October 2, 2014. The option to

purchase was exercised and all documentation to transfer the

concessions to the company has been completed however formal

registration with the Peruvian authorities has not yet been

completed.

The

reason this concession was not formally transferred is the fact

that AIM wanted to perform additional due diligence as there was an

Arbitration process with the registered owners and the former

concession owners of 80% of the concession. Subsequent to this time

the former owners who commenced the arbitration process has

abandoned the arbitration thus nullifying the process.

Royalties

The

combined concessions are known as “The Black Hole”, the

first two concessions, El Tunel del Tiempo 1 & 2 do not have

royalties payable. The third concession, Agujeros Negros WA-AG has

a royalty consisting of payment of US $1.00 per each metric ton of

anthracite coal extracted from and sold. The royalty applies from

the time when the sales of anthracite coal reach US

$150,000.

Process

Whereby Mineral Rights Are Acquired in Peru (Peruvian System of

Concessions)

In

Peru, any individual or company can solicit (through a

“Petition” to the Government, the grant of a mining

concession. Through an administrative process at INGEMMET (the

geological Mining and Metallurgical Institute), when all technical

and legal requirements are complied with, the Government will grant

the mining concession. The mining concession grants the titleholder

the right to explore, exploits, process, transport, market and

refine mineral whether it is metallic, non-metallic or coal

mineral. Once the concession is granted it must be registered at

the Public Registries and the concession titleholder can freely

transfer, assign, encumber or exercise over it any kind of

disposition act.

A

mining concession in Peru does not have duration of time limit.

However, it carries an obligation to pay annual Validity fees to

prevent cancellation from the Government as in Peru the nature of a

mining concession entails a duty for its development and production

in order to grant it added value. In the General Regime this is for

medium and large mining, the payment of validity fees is US$ 3.00

per hectare per year.

Rights

and Obligations: Concession titleholder’s rights

●

The properties are

all located on vacant land, and vacant land properties are entitled

to the free mining use of the surface land that corresponds to the

concession and outside of it, for its economic advantage without

the need for any additional request, however that being said the

titleholder does not have the right for the use of surface land

without formal consent, the properties are owned by the government

and for a total fee of approx. US$15,000.00 the surface rights are

readily available to AIM.

●

The right to

request from the mining authorities easements of third party lands

that are necessary for the reasonable use the

concession.

●

The right to free

trade of extracted minerals provided they have the respective

permits and authorizations.

●

To build on

neighboring concessions the labor work that is necessary for the

access, ventilation and drainage of their own concession, mineral

transport and safety of the workers.

●

The right to use

the water that is necessary for the domestic service of the staff

workers and for the operations of the concession, in accordance

with the legal provisions for these matters.

●

The right to

inspect the work of neighboring or adjacent mining concessions when

invasion is suspected or when there is danger of flooding, collapse

or dire due to the bad state of the labor work of the neighbors or

adjacent for the work they are carrying out.

Duties

of the Concession titleholders:

●

Validity fee

payment of US $3.00 per hectare, due June 30 every year. If not

paid for two years, concession returns to the Government. Fee to be

paid by AIM. (Paid)

●

Payment of penalty

fees if not in production is US $6.00 per year up to year seven

increasing to US $20.00 per year from year 12. After failure to pay

for two years the concession reverts to the Government. Fee to be

paid by AIM. (Paid)

●

Follow the

occupational health and safety provided for in Regulations of

Occupational Health and Safety.

●

Follow the

Environment Management Instruments.

We

confirm the Environmental Management permits are currently being

applied for and we expect to have these in place within the ensuing

six months.

4

Peruvian

Property Location

The

property is accessible by standard vehicles; all roadways are

drivable with the roadways being paved and or gravel roadways. The

driving time is approx. 3 hours from the city of Trujillo Peru. In

addition, there is roadway running through the property making it

feasible for exploration and drilling. The entire property consists

of 1,000 hectares. The official location of the property

is:

Republic:

Peru

Department: La

Libertad

Province:

Otuzco

District:

Huaranchal

Spot:

Between Huayobamba and Lajon

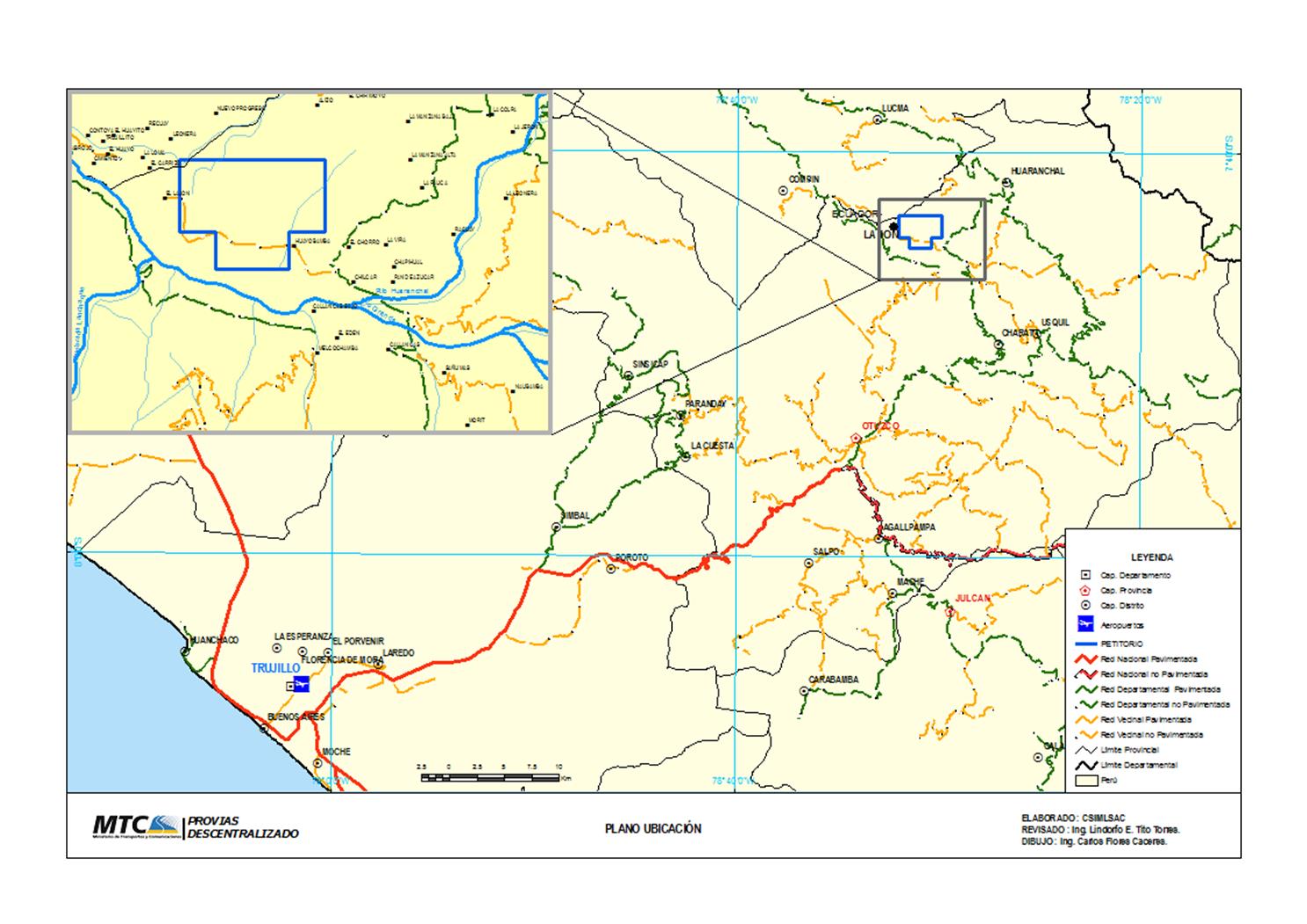

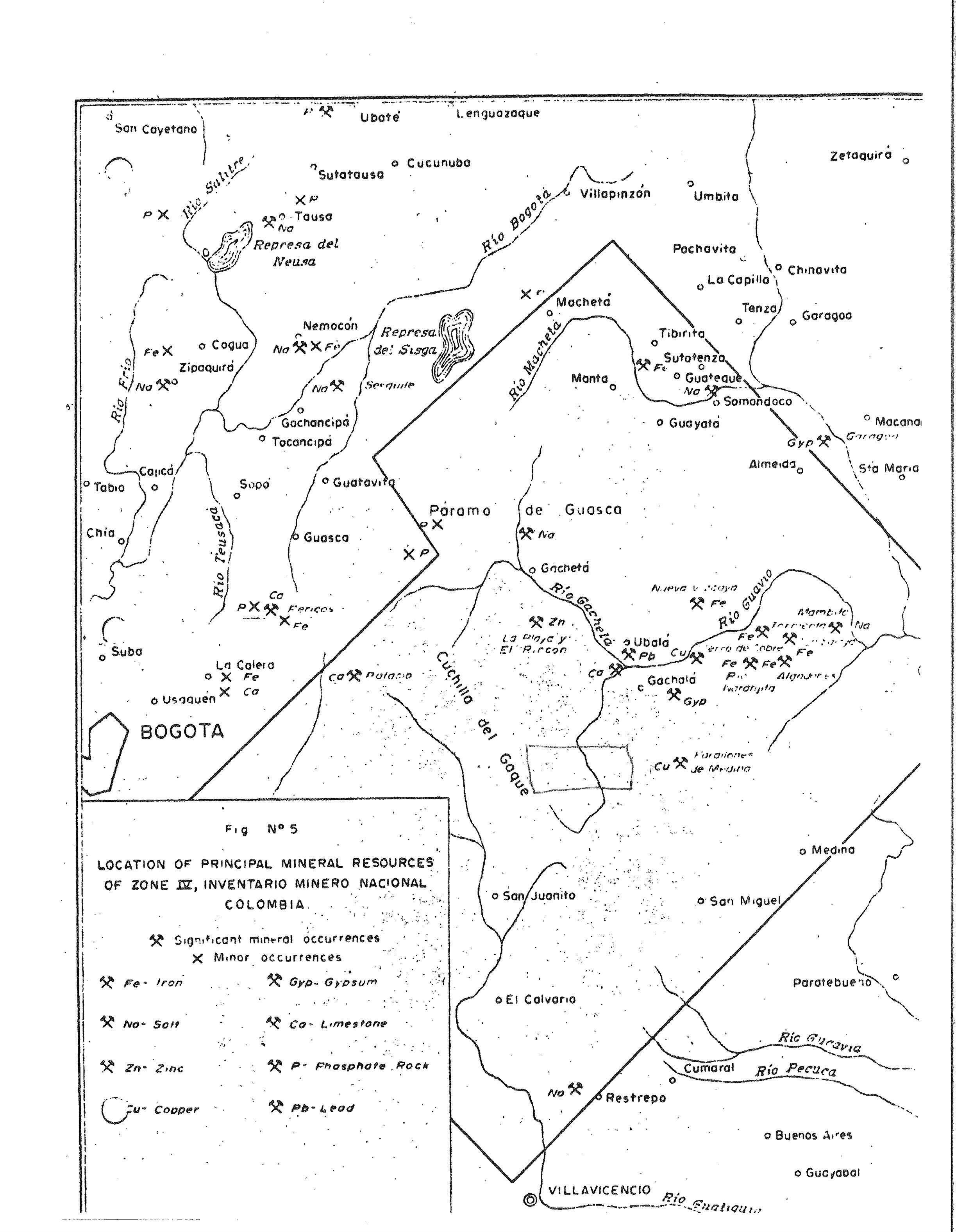

Figure

1 is a map that shows the location of the project and the

surrounding area. The coordinates near the centroid of the property

are 7° 44’ 13.06” S and 78° 31’

05.87” W. The property is 1,000 hectares and are all with one

contiguous block of property.

↑

North

Note:

This location map is copied from a previous geological report done

for the property by MTC and the map was completed in May of

2012.

5

Figure

1 Property Location

Geology

The

geology in the area of the property and surrounding areas in

general have a regional stratigraphy, composed in large percentage

of sequences of Mesozoic sedimentary rocks ranging from Jurassic in

the western sector, then the Lower Cretaceous superior and in the

northwest-northeast with Tertiary volcanic sequences, which cover

much of the region, and the upper most are alluvial deposits from

the recent Quaternary. There are also some Tertiary intrusive

bodies that outcrop in the southwest area of the

region.

The

local geology for the property consists of sedimentary units,

corresponding to the Chimú Chicama formations, Santa, Carhuaz

and Farrat, and the Alto Chicama River basin is characterized by

outcrops of Mesozoic rocks that have the have major folding and

fracturing. This folding is apparent in the Jurassic sedimentary

rocks (Chicama formation) at lower levels near the Alto Chicama

River. Chicama Formation is characterized by the presence of dark

gray shale with interbedded sandstones, and slate gray tuffaceous

quartz at some levels. The Chimú Formation is present in most

of the study area, and is the most noticeable towards the southwest

and Chicama formation is exposed near the river. These formations

are important because this is the horizon in the area of

greatest interest because of the presence of coal seams and

in some cases have the presence of sub-anthracite and anthracite,

occurring with some areas as "lenses" in the bituminous coal. The

following is the sedimentary sequence; sandstones, siltstones,

shale, and black shale (Cobbing et al., 1996: 73-74). The two

formations are exposed mostly in streams and Quina Shangala

(erosional cut within the property), covering most of the local

area. The Santa and Carhuaz formations, are not fully

differentiated in the study area, having found areas with shale,

siltstone, limestone, sandstone, quartzite and in some sectors they

have small "lenses" of bituminous coal, but are of smaller

magnitude. In summary these formations, especially the formation

Chimú, are of great interest, as possible sources for economic

development for the "Black Holes Property".

There

are granodioritic intrusive rocks that outcrop in the form of

stocks, with the presence of a large intrusive towards the left of

the village of Lajon (northwest corner of the property). This

area is heavily disturbed and altered, and has the presence of

metallic minerals, which is an association of the coal deposits of

the basin Chicama (usually Au.).

These

various Shangala features (used in sampling activities) are

essentially a creek that dissects perpendicular to the outcrops

surrounding the river Alto Chicama, both sectors have significant

levels of bituminous coal, quite broken, which could be of value in

the economic exploration to exploitation of the

property.

The

oldest rocks in the prospect of coal formations are the Upper

Jurassic Chicama and overlie rocks of the Chimú formation,

this being the one with the anthracite coal and sub-anthracites

plus it includes other sedimentary horizons with bituminous coal.

These formations and especially above the village of Chimú is

of great interest as a source of possible development of the mining

project because they are the carriers of coal in the area and this

is this geological unit which covers 80% of the area.

The

studies done by MTC and later by Gustavson are not done to NI43-101

or coal industry standards to report resources and reserves. The

property is currently without known reserves and current and

planned exploration programs are exploratory in

nature.

Current

and planned exploration:

The

previous work completed on or near the property has focused on

geologic mapping and sampling via trenches at the outcrop areas and

in old, existing tunnels. There are active small mining operations

on the northwest area of the property that has also added

information on the quality of the coal from the

property.

The

property’s evaluation and database will be greatly improved

by a program of additional geologic mapping, trenching and most of

all by completing 3-4 drill holes that provide core for sampling

and testing, but also will be an important guide to the structure

of the coal deposits. More drill holes are required to define

resources; the first suggested drilling program may define the need

for additional drill holes due to the structural complexity of the

coal beds.

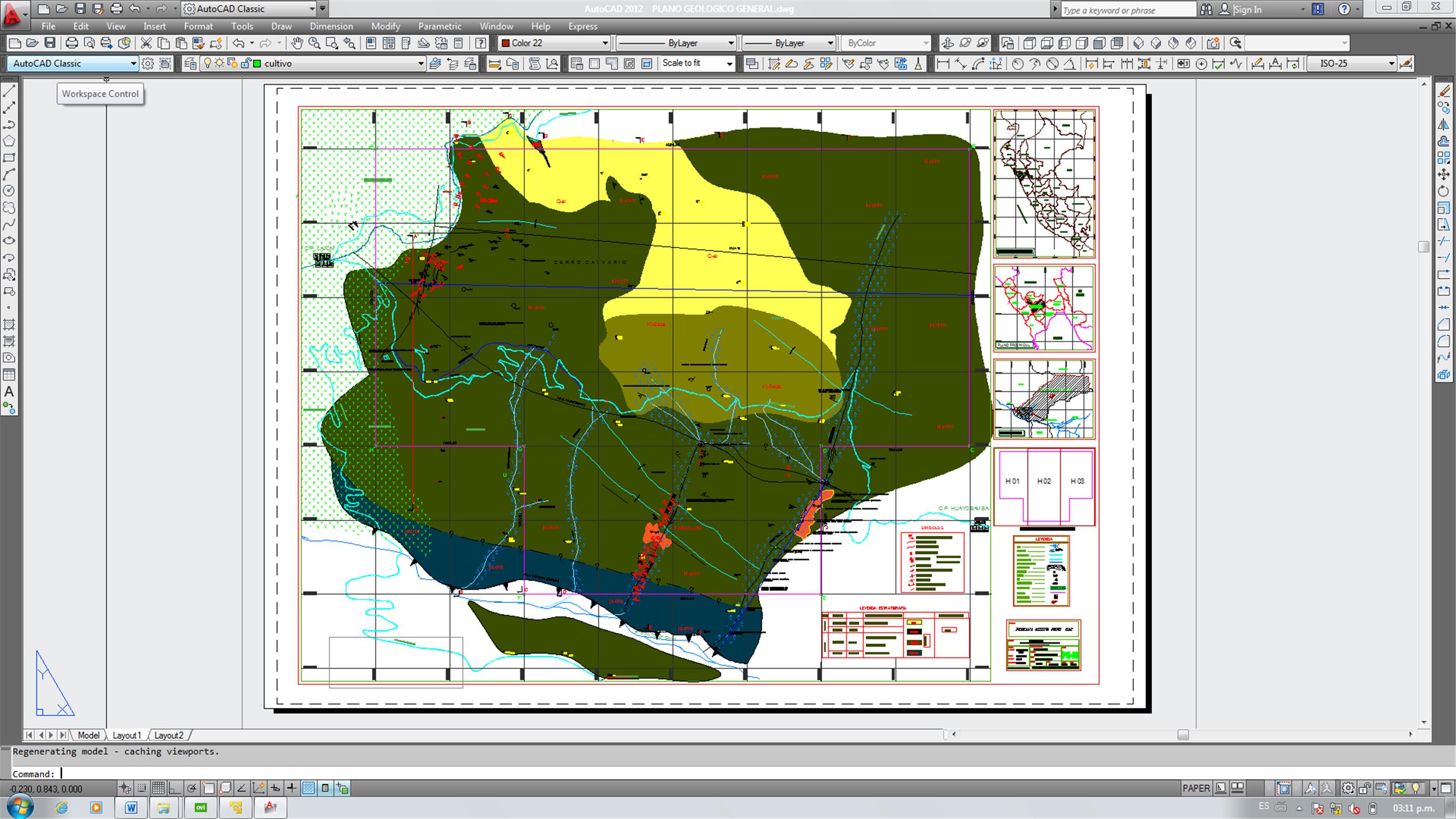

Figure

2 shows many relevant features of the property. The map is very

busy so some explanation is required.

Note:

this figure is also from the MTC Report of 2012 and shows many

features of the property that are describe and explained in the

text of this report.

6

Figure

2 Property Map showing Site Specific Features

The

outline of the property is shown by a lavender line that defines a

rectangle shape that is extended to the south. There is no north

arrow, but there are grid lines that show north-south and

east-west. The Alto Chicama River is in the south (bottom) of the

figure and the features, some with red markings that cross the

property in a northeast to southwest direction, are the features

referred to as Shangalas. The small black marks towards the

northwest are the small mines mentioned above.

The

main feature from Figure 2 that will aid the exploration and

drilling effort is the existing road that crosses the center of the

property and is shown as a light blue, meandering line. The

importance of this existing road is that it will give easy access

to the center of the property where the proposed drill holes can be

located. The coal deposits proposed to define first are south of

the road and by setting up at various locations along the road and

drilling at an angle towards the south will provide the best

possibility to intersect and sample the coal seams. Four drill

holes along the road can be spaced to provide data points to define

some resources as Indicated. The exact drill sites will be defined

in a combination of future site visits and geologic mapping, which

is the first phase of exploration.

The

cost and timing for the Phase I of drill hole siting and mapping is

estimated at about $35,000 and will be started as soon as AIM has

the necessary funds, the process is expected to take approximately

10 days. The planning for Phase 2, drilling, sampling, analysis and

possible more trenching is estimated at $350,000 to include a

drilling contractor, geologic support, sample analysis and

reporting and could complete the 4 drilling program in 6 weeks.

This data provided by Phase 1 and Phase 2 could then be utilized to

develop a NI43-101 Resource Report and possible a Preliminary

Economic Assessment (PEA).

The

cost and timing for the required permitting for the property is as

follows:

COSTS BREAKDOWN

|

DESCRIPTION

|

COSTS $

|

TIME

|

|

1. ENVIRONMENTAL

IMPACT STUDY

|

50,000

|

6

months

|

|

Conceptual

hydrological and hydrogeological study

|

25,000

|

|

|

2. START OF MINING

OPERATIONS

|

|

4

months

|

|

Authorization of

the surface land (titleholder)

|

14,999

|

|

|

Mine

plan

|

15,000

|

|

|

Detailed

Ventilation Study

|

10,000

|

|

|

Detailed

Geomechanics Study

|

10,000

|

|

|

Seismic risk

studies

|

7,000

|

|

|

Design of

explosives storage

|

2,000

|

|

|

Occupational Health

and Safety Plan

|

2,000

|

|

|

Design of tailings

storage

|

15,000

|

|

|

3. CLOSURE

PLAN

|

35,000

|

4

months

|

|

4. PREPARATION OF

FILE OF WATER USE ISSUED BY ANA

|

7,000

|

1

month

|

|

5. PREPARATION OF

FILE FOR DISPOSAL OF WATER (DIGESA AND ANA)

|

5,000

|

1

month

|

|

6. LEGAL COSTS

ASSOCIATED TO OBTAIN ALL THE AFOREMENTIONED PERMITS

|

50,000

|

Throughout the

process

|

|

TOTAL

COSTS $

|

$247,999

|

|

Summary

Gustavson

Associates based out of Boulder Colorado provided the technical

information on the Peruvian property. Gustavson Associates is a

mining consulting firm with over 30 years of extensive

international experience. Mr. Karl D. Gurr of Gustavson Associates

completed a site visit of the property together with visiting the

Port of Salaverry located in Trujillo Peru and has reviewed

numerous reports. Mr. Karl Gurr is a Registered Member of the

Society of Mining Engineers and has degrees in Geology and Mining

Engineering with over 25 years of direct experience in the coal

industry, which defines Mr. Gurr’s status as a qualified

person. As stated Mr. Gurr performed a property visit and a

visit to the Port of Salaverry and confirms that the property is a

known coal bearing area with sufficient past geologic study to

merit additional work (exploration) to better define coal resource

and eventually a plan for mining the resource. Any further

exploration will be overseen and supervised by or through Mr. Gurr

and will be focused on providing additional information to advance

the project and to do it in a cost effective manner. Mr. Gurr

has confirmed the infrastructure and property access already exists

and the Port of Salaverry has the capability to store and ship the

produced coal.

In

addition to Mr. Gurr’s visit we solicited the efforts of

mining engineer and geologist Manuel Chumpitaz Cama. Mr. Cama has

known the property for many years and he attended to extractive of

coal samples from various mine tunnels within the property. Through

the supervision of Mr. Cama samples of coal were taken from the

property and delivered to the local university lab for testing.

Following is the official results of the testing.

The

legal and permitting information was provided to AIM by their team

of Peruvian legal advisors based in Lima Peru.

7

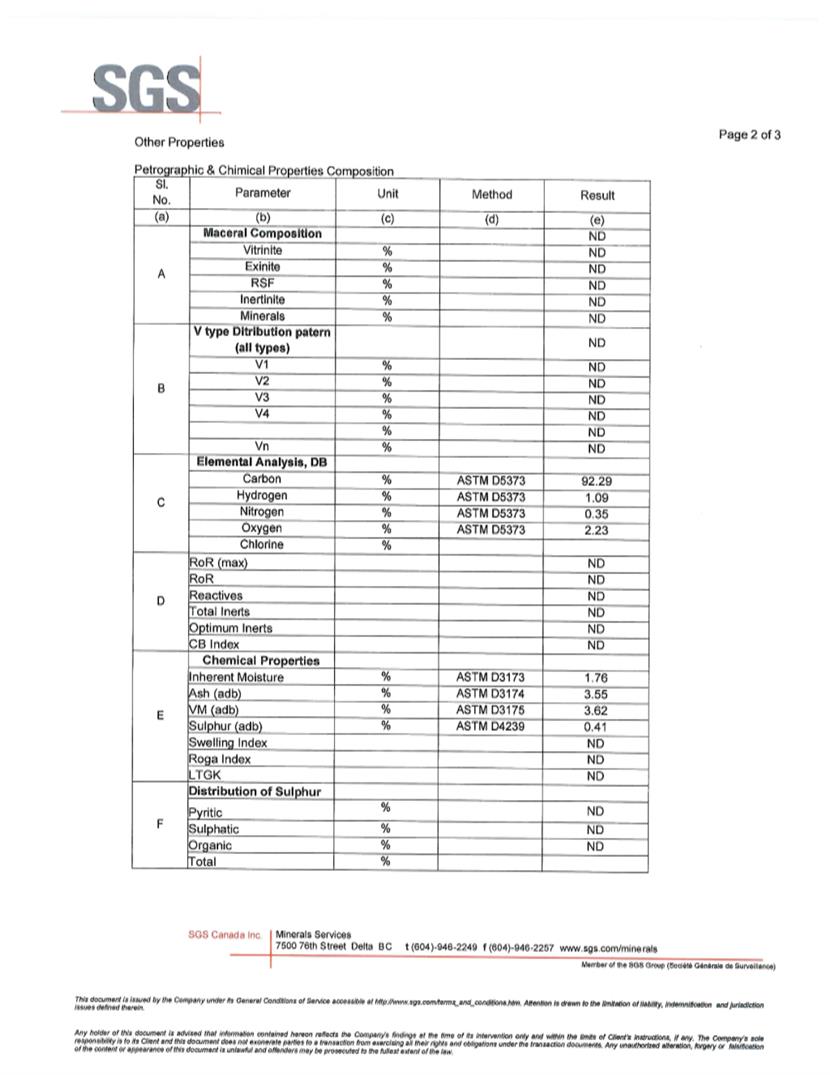

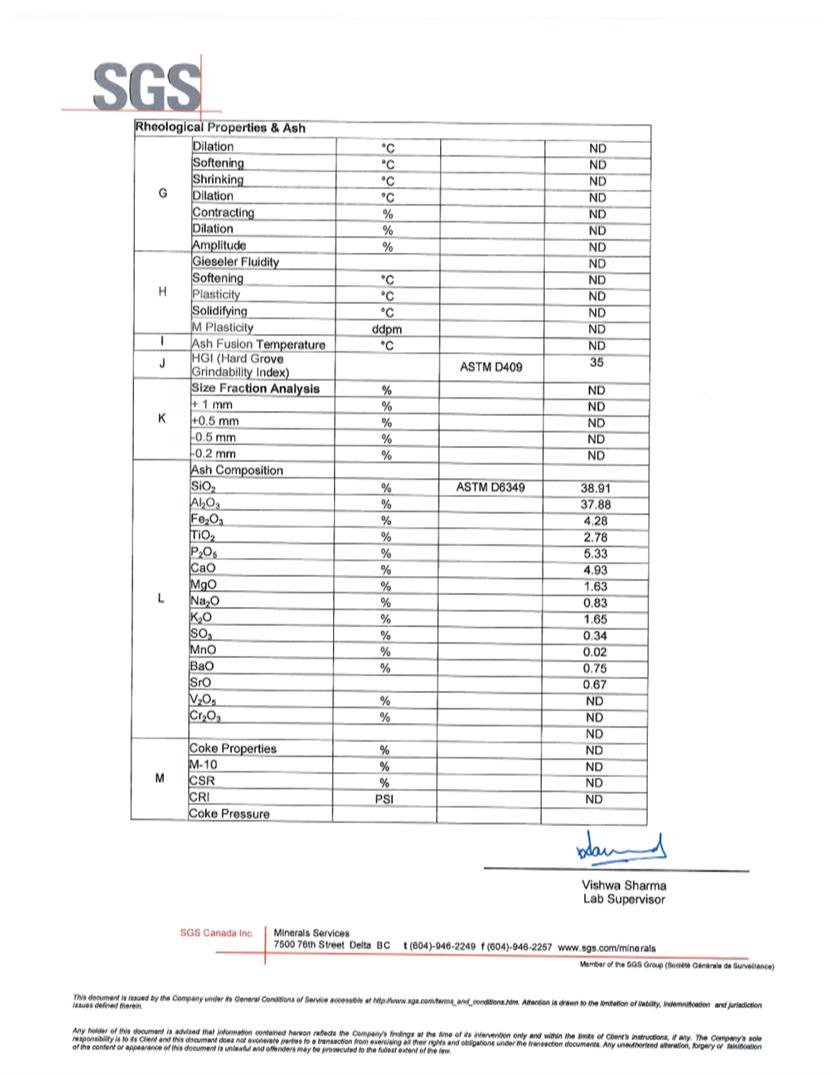

Analysis of Coal Samples

The

following report was obtained from world-renowned SGS Canada

Inc.:

8

9

10

WE WILL REQUIRE

SIGNIFICANT ADDITIONAL FINANCING IN ORDER TO CONTINUE OUR

EXPLORATION ACTIVITIES AND OUR ASSESSMENT OF THE COMMERCIAL

VIABILITY OF OUR PROPERTIES. EVEN IF WE DISCOVER COMMERCIAL

RESERVES OF PRECIOUS METALS ON OUR MINERAL PROPERTY, WE CAN PROVIDE

NO ASSURANCE THAT WE WILL BE ABLE TO SUCCESSFULLY ADVANCE INTO

COMMERCIAL PRODUCTION.

While

we are very optimistic the properties contain minerals we are not

sure. Our business plan calls for significant expenditures in

connection with the exploration of the property. We will,

however, require additional financing in order to complete the

remaining phases of the exploration program, and to conduct the

economic evaluation that would be necessary for us to assess

whether sufficient mineral reserves exist to justify commercial

exploitation. We currently are in the exploration stage and

have no revenue from operations. We currently do not have any

arrangements in place for additional financing, and we may not be

able to obtain financing on terms that are acceptable to us, or at

all. If we are unable to obtain additional financing, we will

not be able to continue our exploration activities and our

assessment of the commercial viability of the property.

Further, if we are able to establish that development of the

property is commercially viable, our inability to raise additional

financing at this stage would result in our inability to place the

property into production and recover our investment.

11

Competition

We are

a junior mineral resource exploration company. We compete

with other mineral resource exploration companies for financing and

for the acquisition of new mineral properties. Many of the

mineral resource exploration companies with whom we compete have

greater financial and technical resources than those available to

us. Accordingly, these competitors may be able to spend

greater amounts on acquisitions of mineral properties of merit, on

exploration of their mineral properties and on development of their

mineral properties. In addition, they may be able to afford

more geological expertise in the targeting and exploration of

mineral properties. This competition could result in

competitors having mineral properties of greater quality and

interest to prospective investors who may finance additional

exploration and development. This competition could adversely

impact on our ability to achieve the financing necessary for us to

conduct further exploration of our mineral properties.

We will

also compete with other junior mineral exploration companies for

financing from a limited number of investors that are prepared to

make investments in junior mineral exploration companies. The

presence of competing junior mineral exploration companies may

impact on our ability to raise additional capital in order to fund

our exploration programs if investors are of the view that

investments in competitors are more attractive based on the merit

of the mineral properties under investigation and the price of the

investment offered to investors.

We will

also compete with other junior and senior mineral companies for

available resources, including, but not limited to, professional

geologists, camp staff, helicopter or float planes, mineral

exploration supplies and drill rigs.

As

at August 31, 2016, we had cash reserves of $417 and

working capital deficit of $2,897,303. We do not have sufficient

funds to enable us to complete this initial phase of our

exploration programs for the mining claims. We will require

additional financing in order to commence the initial phases of

exploration of the properties. There is no assurance that

will be able to obtain additional financing. Both advanced

exploration and an economic determination will be contingent upon

the results of our preliminary exploration programs and our ability

to raise additional financing in order to proceed with advanced

exploration and an economic evaluation. There is no assurance

that we will be able to obtain any additional financing to fund our

exploration activities.

Patents,

Trademarks, Franchises, Royalty Agreements or Labor

Contracts

We have

no current plans for any registrations such as patents, trademarks,

copyrights, franchises, concessions, royalty agreements or labor

contracts. We will assess the need for any copyright, trademark or

patent applications on an ongoing basis.

Research

and Development

We have

not spent any amounts on research and development activities during

the year ended August 31, 2016. We anticipate that we will

not incur any expenses on research and development over the next 12

months. Our planned expenditures on our operations or a

business combination are summarized under the section of this

annual report entitled “Management’s Discussion and

Analysis of Financial Position and Results of

Operations”.

Employees

and Employment Agreements

At

present, we have no employees other than our executive officers and

directors. We presently do not have pension, health, annuity,

insurance, stock options, profit sharing or similar benefit plans;

however, we may adopt such plans in the future. There are

presently no personal benefits available to any officers, directors

or employees.

12

Item 1A. RISK FACTORS

As a

“smaller reporting company”, we are not required to

provide the information required by this Item.

Item 1B. UNRESOLVED STAFF COMMENTS

As a

“smaller reporting company”, we are not required to

provide the information required by this Item.

Item 2. PROPERTIES

Descriptions of the

leases concerning our mining facilities can be found in Item 1 of

this report on Form 10-K. We do not currently own any property or

real estate of any kind. Our executive offices are located at

701 North Green Valley Parkway, Suite 200, Henderson Nevada,

89012.

Item 3. LEGAL PROCEEDINGS

A

company called Tarpon Bay commenced legal action with the company

as at August 30, 2016 claiming the company owed them $78,678. The

company is disputing the claim and it is currently in the hands of

the courts. This relates to the S-1 registration statement that

became effective June 1, 2015. The S-1 that was registered in the

name of Southridge Capital and the amount of the claim represents

the “standby fee”. In view of the fact that the equity

line of credit with Southridge Capital was completed wrong and

could not be utilized technically Southridge or Tarpon Bay was not

on “standby”. The S-1 registration statement was

approved by Southridge (Tarpon Bay) in- house legal department

prior to submitting to the SEC for registration." There are no

proceedings in which any of our directors, officers or affiliates,

or any registered or beneficial stockholder, is an adverse party or

has a material interest adverse to our interest.

Item 4. MINE SAFETY DISCLOSURES

Not

applicable.

13

PART

II

Item 5. MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER

MATTERS AND ISSUER PURCHASES

OF EQUITY SECURITIES

Market

Information

There

is no established public trading market for our securities and a

regular trading market may not develop, or if developed, may not be

sustained. A shareholder in all likelihood, therefore, will

not be able to resell his or her securities should he or she desire

to do so when eligible for public resales.

Furthermore, it is

unlikely that a lending institution will accept our securities as

pledged collateral for loans unless a regular trading market

develops. We would like to register our shares for resale by

our selling stockholders and then obtain a trading symbol to trade

our shares over the OTC Bulletin Board. However, there is no

assurance that we will be successful in getting our common stock

quoted on the OTC Bulletin Board.

Number

of Holders

As of

December 15, 2016, we had approximately 45 shareholders of

record of our common stock.

As of

December 15, 2016, we had 2 shareholders of record of our preferred

stock.

Dividend

Policy

We have

not declared any cash dividends on our common stock since our

inception and do not anticipate paying such dividends in the

foreseeable future. We plan to retain any future earnings for

use in our business. Any decisions as to future payments of

dividends will depend on our earnings and financial position and

such other facts, as the Board of Directors deems

relevant.

Recent

Sales of Unregistered Securities; Use of Proceeds from Registered

Securities

On

October 28, 2015, Aim Exploration Inc. (the “Company”)

entered into a Note Purchase Agreement with Tangiers

Investment Group, LLC (“Tangiers” or

“Holder” in the event of assignment or succession) for

the sale of a 10% convertible promissory note (the

“Note”), in the principal amount of $330,000 (the

“Principal Sum”), convertible into shares of common

stock of the Company. Upon execution of the Note, Tangiers

delivered $75,000 to the Company. The Note has an original issue

discount of $7,500, which Tangiers retained for due diligence and

legal bills related to the transaction. The financing closed on

October 28, 2015 (the “Closing Date”). The Effective

Date is that day when the Note is executed by both parties and the

delivery of the first payment of consideration is made (the

“Effective Date”).

On

April 1, 2016, Tangiers delivered another $18,302 to the Company.

During the year, Rockwell Capital (“Rockwell”) assumed

$92,000 of the Tangiers note. Subsequent to August 31, 2016, the

Rockwell note was assumed by a private party, and the balance of

the Tangiers note was paid in full by a director of the

Company.

The Note bears interest at

the rate of 10% per annum. All interest and principal must be

repaid one (1) year after the Effective Date (the “Maturity

Date”). The Note is convertible into common stock, at

Tangiers’ option, at the lower of (i) $0.10 per share or (ii)

50% of the lowest trading price of the Company’s common stock

during the 25 consecutive trading days prior to the date on which

Tangiers elects to convert all or part of the Note (the

“Conversion Price”).

14

The

Note may be prepaid by the Company, in whole or in party, according

to the following: if under 30 days from the Effective Date,

Prepayment amount shall be 100% of Principal sum plus accrued

interest; between 31 and 60 days, 110% of Principal Sum plus

accrued interest; between 61 and 90 days, 120% of Principal Sum

plus accrued interest; between 91 and 120 days, 130% of Principal

Sum plus accrued interest; between 121 and 150 days, 140% of the

Principal Sum plus accrued interest; and between 151 and 180 days,

150% of Principal Sum plus accrued interest. After 180 days from

the Effective Date, the Note may not be prepaid without written

consent from the Holder.

In the

event of a default, the Note may be accelerated by Tangiers,

whereby the outstanding balance is immediately due and payable in

cash at 150% of the outstanding Principal Sum of the Note. In

addition, an interest rate of the lesser of 18% per annum or the

maximum rate permitted under law will be applied to the outstanding

balance. Tangiers is prohibited from owning more than 9.99% of the

Company’s outstanding shares pursuant to the

Note.

The

Company claims an exemption from the registration requirements of

the Securities Act of 1933, as amended (the “Act”) for

the private placement of these securities pursuant to Section 4(2)

of the Act and/or Regulation D promulgated there under since, among

other things, the transaction did not involve a public

offering, Tangiers is an accredited investor, Tangiers had

access to information about the Company and their investment,

Tangiers took the securities for investment and not resale, and the

Company took appropriate measures to restrict the transfer of the

securities.

Related

to entering into the Note, the parties documented their intention

that the Company’s obligations to repay under the terms of

the Note be secured by certain assets, represented by the Security

Agreement and Memorandum of Security Agreement, entered into by the

parties on October 28, 2015.

On

October 28, 2015, the Company entered into a Strategic Consulting

Agreement with Tangiers for strategic advising and consulting

services. The Term is twelve months, although it may be terminated

at any time. As consideration for providing consulting services,

the Company shall pay Tangiers one hundred twenty thousand dollars

($120,000) in restricted shares of the Company’s common

stock, payable in four equal installments of $30,000 per month

each, due at ninety-day intervals. Additionally, the Company shall

issue to Tangiers 500,000 five-year warrants with an exercise price

of fifteen cents ($.15) a share and a cashless exercise option. The

Company also granted Tangiers the option to purchase up to fifteen

thousand (15,000) tons of coal per month (FOB) at a fifteen percent

(15%) discount to market on a to be determined

formula.

On that

same date, the Company entered into an Investment Agreement and

Registration Rights Agreement with Tangiers (the “Investment

Agreement”) through which the Company has agreed to issue and

sell to Tangiers an indeterminate number of shares of the

Company’s common stock, par value of $.001 per share, up to

an aggregate purchase price of five million dollars ($5,000,000).

The Company is obligated to register these shares to be sold under

the Investment Agreement on Form S-1.

On

August 14, 2015, the Company issued to Auctus Fund, LLC a

convertible promissory note in the principal amount of $76,750, in

connection with a securities purchase agreement entered into by the

parties on August 14, 2015. The note accrues interest at a rate of

10% per annum, with a maturity date of May 14, 2016. The holder of

the note may convert any or all of the principal outstanding into

shares of the Company’s common stock at a price equal to 55%

of the lowest trading price of the common stock during the fifteen

trading days prior to issuing a notice of conversion to the

Company. During the year, Rockwell Capital (“Rockwell”)

assumed $40,000 of the Auctus note. Subsequent to August 31, 2016,

the Rockwell note was assumed by a private party.

On

August 31, 2015, the Company issued to St. George Investments LLC a

convertible promissory note in the principal amount of $40,000, in

connection with a securities purchase agreement entered into by the

parties on August 31, 2015. The purchase price for this note and

warrant (as described in the securities purchase agreement) shall

be $25,000, computed as follows: original principal balance of

$40,000, less a $10,000 original issue discount and $5,000 to cover

lender’s legal fees, accounting costs, due diligence, and

other transaction costs incurred in connection with the note.

Interest does not accrue on the outstanding principal. The note

matures six months after the purchase price is delivered to the

Company by the lender. The holder of the note may convert any or

all of the principal outstanding into shares of the Company’s

common stock at a price equal to 60% of the lowest trading price of

the common stock during the twenty trading days prior to issuing a

notice of conversion to the Company. Subsequent to August 31, 2016,

a private party assumed the St. George note.

On

September 17, 2015, the Company issued to EMA Financial, LLC a

convertible promissory note in the principal amount of $40,000, in

connection with a securities purchase agreement entered into by the

parties on September 17, 2015. The note accrues interest at a rate

of 12% per annum, with a maturity date of September 17, 2016. The

holder of the note may convert any or all of the principal

outstanding into shares of the Company’s common stock at a

price equal to 55% of the lowest trading price of the common stock

during the 20 trading days prior to issuing a notice of conversion

to the Company.

On

January 12, 2016, the Company issued to Yoshar Trading, LLC a

convertible promissory note in the principal amount of $30,000, in

connection with a Securities Purchase Agreement entered into by the

parties on January 12, 2016. The note accrues interest at a rate of

10% per annum, with a maturity date of January 12, 2017. The holder

of the note may convert any or all of the principal outstanding

into shares of the Company’s common stock at a price equal to

55% of the lowest trading price of the common stock during the 20

trading days prior to issuing a notice of conversion to the

Company.

15

Equity

Compensation Plan Information

We do

not have in effect any compensation plans under which our equity

securities are authorized for issuance and we do not have any

outstanding stock options.

Purchase

of Equity Securities by the Issuer and Affiliated

Purchasers

We did

not purchase any of our shares of common stock or other securities

during our fourth quarter of our fiscal year ended August 31,

2016.

Item 6. SELECTED FINANCIAL DATA

As a

“smaller reporting company”, we are not required to

provide the information required by this Item.

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You

should read the following discussion and analysis in conjunction

with our financial statements, including the notes thereto,

included in this Report. Some of the information contained in

this Report may contain forward-looking statements within the

meaning of Section 27A of the Securities Exchange Act of 1933, as

amended (the “Act”) and Section 21E of the Securities

Exchange Act of 1934, as amended (the “Exchange Act”).

This information may involve known and unknown risks,

uncertainties and other factors which may cause our actual results,

performance or achievements to be materially different from future

results, performance or achievements expressed or implied by any

forward-looking statements. Forward-looking statements which

involve assumptions and describe our future plans, strategies and

expectations, are generally identifiable by the use of the words

“may,” “will,” “should,”

“expect,” “anticipate,”

“estimate,” “believe,” “intend”

or “project” or the negative of these words or other

variations on these words or comparable terminology. These

forward-looking statements are based on assumptions that may be

incorrect, and there can be no assurance that the projections

included in these forward-looking statements will come to pass.

Our actual results could differ materially from those

expressed or implied by the forward looking statements as a result

of various factors. We undertake no obligation to update

publicly any forward-looking statements for any reason, even if new

information becomes available or other events occur in the

future.

Purchase

of Significant Equipment

We do

not intend to purchase any significant equipment over the next

twelve months.

Personnel

Plan

We do

not expect any material changes in the number of employees over the

next 12-month period (although we may enter into employment or

consulting agreements with our officers or directors). We do

and will continue to outsource contract employment as

needed.

16

Results

of Operations for the Fiscal Year Ended August 31, 2016 compared

to the Fiscal Year Ended August 31, 2015

We did

not earn any revenues for the period from February 18, 2010

(Inception) to August 31, 2016. We incurred a net loss in the

amount of $1,141,304 during the

fiscal year ended August 31, 2016, compared to a net loss of

$1,448,618 for the fiscal year ended August 31, 2015. These

operating expenses were comprised of mineral property expenditures

of $22,916 (2015: recapture of

$21,843), consulting fees of $70,437 (2015: $128,451), filing fees

of $15,831 (2015: $15,923), finder’s fees of $15,000 (2015:

$113,603), foreign exchange gain of $61,517 (2015: loss of $664); management

fees of $216,000 (2015: $241,500), office and general fees of

$54,710 (2015: $70,142),

professional fees of $105,409 (2015: $306,925), and public

relations expense of $72,854 (2015: $180,452). We wrote-down

accounts receivable of $45,800 (2015: $Nil), wrote-down accounts

payable by $Nil (2015: $11,285), and incurred the following

expenses related to the convertible: accretion of $529,914 (2015:

$85,329), interest expense of $62,431 (2015: $49,112), finance

costs of $197,571 (2015: $305,998) from amortization of debt

discounts and excess of derivative liability over the face value of

the notes, and a change in the fair value of the derivative

liability of $206,052 (2015: $16,353).

Revenues

We have

had no operating revenues since our inception on February 18, 2010

to August 31, 2016.

Expenses

We

incurred a net loss in the amount of $1,141,304 during the fiscal year ended August

31, 2016, compared to a net loss of $1,448,618 for the fiscal year

ended August 31, 2015. These operating expenses were

comprised of mineral property expenditures of $22,916 (2015: recapture of $21,843),

consulting fees of $70,437 (2015: $128,451), filing fees of $15,831

(2015: $15,923), finder’s fees of $15,000 (2015: $113,603),

foreign exchange gain of $61,517 (2015: loss of $664); management fees

of $216,000 (2015: $241,500), office and general fees of $54,710

(2015: $70,142), professional fees of $105,409 (2015: $306,925),

and public relations expense of $72,854 (2015: $180,452). We

wrote-down accounts receivable of $45,800 (2015: $Nil), wrote-down

accounts payable by $Nil (2015: $11,285), and incurred the

following expenses related to the convertible: accretion of

$529,914 (2015: $85,329), interest expense of $62,431 (2015:

$49,112), finance costs of $197,571 (2015: $305,998) from

amortization of debt discounts and excess of derivative liability

over the face value of the notes, and a change in the fair value of

the derivative liability of $206,052 (2015: $16,353).

Liquidity

and Capital Resources

As at

August 31, 2016, we had cash reserves of $417 and working capital

deficit of $2,227,835. As at August 31, 2015, we had cash

reserves of $2,349 and working capital deficit of

$1,209,747.

Cash

Used in Operating Activities

Net

cash used in operating activities was $409,984 during the fiscal

year ended August 31, 2016, compared to $812,788 for the fiscal

year ended August 31, 2015.

Cash

from Financing Activities

We have

funded our business to date primarily from the issuance of

convertible notes, loans from related parties, as well as sales of

our common stock. During the fiscal year ended August 31,

2016, we raised a total of $408,052 in financing activities.

This was comprised of the issuance of convertible debt in the

amount of $215,000, loans received in the amount of $69,350, and

loans from our director and key management personnel of

$123,702. During the fiscal year ended August 31, 2015, we

raised a total of $813,275 in financing activities. This was

comprised of the issuance of convertible debt in the amount of

$385,553, offset by payment on convertible notes of $47,250,

issuance of convertible debt to related parties in the amount of

$170,000, and loans from our director and key management personnel

of $304,972

17

Off-Balance

Sheet Arrangements

We have

no significant off-balance sheet arrangements that have or are

reasonably likely to have a current or future effect on our

financial condition, changes in financial condition, revenues or

expenses, results of operations, liquidity, capital expenditures or

capital resources that is material to stockholders.

We have

not attained profitable operations and are dependent upon obtaining

financing to pursue marketing and distribution activities.

For these reasons, there is substantial doubt that we will be

able to continue as a going concern.

Critical

Accounting Policies

The

discussion and analysis of our financial condition and results of

operations are based upon our financial statements, which have been

prepared in accordance with the accounting principles generally

accepted in the United States of America. Preparing financial

statements requires management to make estimates and assumptions

that affect the reported amounts of assets, liabilities, revenue,

and expenses. These estimates and assumptions are affected by

management’s application of accounting policies. We

believe that understanding the basis and nature of the estimates

and assumptions involved with the following aspects of our

financial statements is critical to an understanding of our

financial statements.

Basis

of Accounting

Our

Company’s financial statements are prepared using the accrual

method of accounting. The Company has elected an August

year-end.

Cash

Equivalents

Our

Company considers all highly liquid investments purchased with an

original maturity of three months or less to be cash

equivalents.

Use

of Estimates and Assumptions

The

preparation of financial statements in conformity with generally

accepted accounting principles requires management to make

estimates and assumptions that affect the reported amounts of

assets and liabilities and disclosure of contingent assets and

liabilities at the date of the financial statements and the

reported amounts of revenues and expenses during the reporting

period. Actual results could differ from those

estimates.

Stock-Based

Compensation

Our

Company records stock-based compensation in accordance with ASC

718, Compensation – Stock Based Compensation, using the fair

value method. All transactions in which goods or services are

the consideration received for the issuance of equity instruments

are accounted for based on the fair value of the consideration

received or the fair value of the equity instrument issued,

whichever is more reliably measurable. Equity instruments

issued to employees and the cost of the services received as

consideration are measured and recognized based on the fair value

of the equity instruments issued.

Recently

Issued Accounting Pronouncements

Our

Company has evaluated all the recent accounting pronouncements and

believes that none of them will have a material effect on the

company’s financial statement.

Contractual

Obligations

As a

“smaller reporting company” we are not required to

provide tabular disclosure obligations.

18

Item 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT

MARKET RISK

As a

“smaller reporting company” we are not required to

provide the information required by this Item.

Item

8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

19

AIM

EXPLORATION INC.

CONSOLIDATED

FINANCIAL STATEMENTS

August

31, 2016

20

Report

of Independent Registered Public Accounting Firm

Consolidated

Balance Sheets of August 31, 2016 and 2015

Consolidated

Statements of Operations for the years ended August 31, 2016 &

2015

Consolidated

Statements of Stockholder’s Equity (Deficit)

Consolidated

Statements of Cash Flows for the years ended August 31, 2016 and

2015

Notes

to Consolidated Financial Statements

21

REPORT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Stockholders

and Board of Directors

AIM

Exploration Inc.

701

North Green Valley Parkway, Suite 200

Henderson, NV

89012

We have audited the accompanying consolidated balance sheets

of AIM Exploration Inc. (the

“Company”) as of August 31, 2016 and 2015, and the

related consolidated statements of operations, changes in

stockholders’ equity (deficit), and cash flows for the years

then ended. These financial statements are the responsibility of

the Company’s management. Our responsibility is to express an

opinion on these financial statements based on our

audit.

We conducted our audits in accordance with the standards of the

Public Company Accounting Oversight Board (United States of

America). Those standards require that we plan and perform the

audits to obtain reasonable assurance about whether the financial

statements are free of material misstatement. The Company is not

required to have, nor were we engaged to perform, an audit of its

internal control over financial reporting. Our audits included

consideration of internal control over financial reporting as a

basis for designing audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on

the effectiveness of the Company’s internal control over

financial reporting. Accordingly, we express no such opinion. An

audit includes examining, on a test basis, evidence supporting the

amounts and disclosures in the financial statements. An audit also

includes assessing the accounting principles used and significant

estimates made by management, as well as evaluating the overall

financial statement presentation. We believe that our audits

provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to the above

present fairly, in all material respects, the financial position

of AIM Exploration Inc. as of August 31, 2016

and 2015, and the results of their operations and cash flows for

the year then ended, in conformity with accounting principles

generally accepted in the United States of

America.

The accompanying consolidated financial statements have been

prepared assuming that the Company will continue as a going

concern. As described in Note 3 to the financial statements, the

Company has incurred an accumulated deficit from inception to

August 31, 2016. This raises substantial doubt about the

Company’s ability to continue as a going concern.

Management’s plans in regard to this matter are also

described in Note 3. The financial statements do not include any

adjustments that might result from the outcome of this

uncertainty.

/s/Anton & Chia, LLP

Newport Beach, California

December 15,

2016

22

AIM

EXPLORATION INC.

CONSOLIDATED

BALANCE SHEETS

|

ASSETS

|

Aug 31,

2016

|

Aug 31,

2015

(Restated)

|

|

CURRENT

ASSETS

|

|

|

|

Cash

|

$417

|

$2,349

|

|

Loans

receivable

|

–

|

45,800

|

|

Deposits

|

72,873

|

39,303

|

|

Total

Current Assets

|

73,290

|

87,452

|

|

|

|

|

|

Mineral

property

|

342,656

|

326,969

|

|

|

|

|

|

TOTAL

ASSETS

|

$415,946

|

$414,421

|

|

|

|

|

|

LIABILITIES

AND STOCKHOLDERS’ DEFICIT

|

|

|

|

|

|

|

|

CURRENT

LIABILITIES

|

|

|

|

Accounts payable

and accrued liabilities

|

$211,601

|

$214,513

|

|

Loans

payable

|

69,350

|

–

|

|

Loans payable

– related party

|

598,955

|

478,453

|

|

Convertible note

– related party

|

191,264

|

103,762

|

|

Convertible note,

net of unamortized discount

|

433,446

|

86,707

|

|

Derivative

liability

|

796,509

|

571,687

|

|

TOTAL

LIABILITIES

|

2,301,125

|

1,455,122

|

|

|

|

|

|

STOCKHOLDERS'

DEFICIT

|

|

|

|

Capital

Stock

|

|

|

|

Authorized

|

|

|

|

250,000,000

shares of common stock, $0.001 par value Issued and outstanding

22,392,729 shares (356,400 shares outstanding as at August 31,

2015)

|

|

|

|

1,000,000 shares of

preferred stock, $0.001 par value Issued and

outstanding 100,000 shares (Nil as at August 31, 2015)

|

145,707

|

89,200

|

|

Additional paid in

capital

|

871,507

|

626,098

|

|

Shares

receivable

|

(5,090)

|

–

|

|

Accumulated

deficit

|

(2,897,303)

|

(1,755,999)

|

|

|

|

|

|

TOTAL

STOCKHOLDERS' DEFICIT

|

(1,885,179)

|

(1,040,701)

|

|

TOTAL

LIABILITIES AND STOCKHOLDERS' DEFICIT

|

$415,946

|

$414,421

|

The

accompanying notes are an integral part of these consolidated

financial statements

24

AIM EXPLORATION INC.

CONSOLIDATED

STATEMENTS OF OPERATIONS

|

|

12 months

ended

Aug 31,

2016

|

12 months

ended

Aug 31,

2015

(Restated)

|

|

|

|

|

|

REVENUE

|

|

|

|

Total

Revenue

|

$-

|

$-

|

|

|

|

|

|

Gross

Profit

|

-

|

-

|

|

|

|

|

|

MINERAL

PROPERTY OPERATIONS

|

|

|

|

Acquisition

expenses

|

–

|

(37,556)

|

|

Exploration

expenses

|

22,916

|

15,713

|

|

Total

Mineral Property Operations

|

22,916

|

(21,843)

|

|

|

|

|

|

EXPENSES

|

|

|

|

Accretion

|

529,914

|

85,329

|

|

Consulting

fees

|

70,437

|

128,451

|

|

Filling

fees

|

15,831

|

15,923

|

|

Finder’s

fees

|

15,000

|

113,603

|

|

Foreign exchange

(gain) loss

|

(61,658)

|

664

|

|

Management

fees

|

216,000

|

241,500

|

|

Office &

general

|

54,710

|

70,142

|

|

Professional

fees

|

105,409

|

306,925

|

|

Public

relations

|

72,854

|

180,452

|

|

|

|

|

|

Total

Expenses

|

1,018,638

|

1,142,989

|

|

|

|

|

|

Net

Loss

|

(1,041,554)

|

(1,121,146)

|

|

|

|

|

|

Interest

expense

|

(62,431)

|

(49,112)

|

|

Finance

costs

|

(197,571)

|

(305,998)

|

|

Change

in fair value of derivative liability

|

206,052

|

16,353

|

|

Write-down

of accounts receivable

|

(45,800)

|

–

|

|

Write-down

of accounts payable

|

–

|

11,285

|

|

|

|

|

|

Total

Other Expense

|

(99,750)

|

(327,472)

|

|

|

|

|

|

Net

Loss

|

$(1,141,304)

|

$(1,448,618)

|

|

|

|

|

|

BASIC

AND DILUTED LOSS PER COMMON SHARE

|

$(0.05)

|

$(0.01)

|

|

WEIGHTED

AVERAGE NUMBER OF COMMON SHARES OUTSTANDING

|

6,391,865

|

353,784

|

|

BASIC

AND DILUTED LOSS PER PREFERRED SHARE

|

$(0.00)

|

$(0.00)

|

|

WEIGHTED

AVERAGE NUMBER OF PREFERRED SHARES OUTSTANDING

|

100,000

|

99,452

|

The

accompanying notes are an integral part of these consolidated

financial statements

25

AIM EXPLORATION INC.

CONSOLIDATED

STATEMENTS OF STOCKHOLDERS’ EQUITY (DEFICIT)

|

|

Common Stock

|

Preferred Stock

|

|

|

|

|

||

|

|

Number of

|

Amount

|

Number of

|

Amount

|

Additional Paid-in Capital

|

Share Subscriptions Receivable

|

Accumulated Deficit

|

Total

|

|

|

shares

|

$

|

shares

|

$

|

$

|

$

|

$

|

$

|

|

Balance

at inception – February 18, 2010

|

-

|

-

|

-

|

-

|

-

|

-

|

-

|

-

|

|

Founders

shares, issued for cash

|

40,000

|

10,000

|

-

|

-

|

-

|

(10,000)

|

-

|

-

|

|

Net

Loss to August 31, 2010

|

-

|

-

|

-

|

-

|

-

|

-

|

(29,400)

|

(29,400)

|

|

Balance, August 31, 2010

|

40,000

|

10,000

|

-

|

-

|

-

|

(10,000)

|

(29,400)

|

(29,400)

|

|

Subscription

Received

|

-

|

-

|

-

|

-

|

-

|

10,000

|

-

|

10,000

|

|

Common

stock issued for cash

|

160,000

|

40,000

|

-

|

-

|

-

|

-

|

-

|

40,000

|

|

Net

loss for the year ended August 31, 2011

|

-

|

-

|

-

|

-

|

-

|

-

|

(18,939)

|

(18,939)

|

|

Balance, August 31, 2011

|

200,000

|

50,000

|

-

|

-

|

-

|

-

|

(48,339)

|

1,661

|

|

Net

loss to August 31, 2012

|

–

|

–

|

–

|

–

|

-

|

-

|

(28,109)

|

(28,109)

|

|

|

|

|

|

|

|

|

|

|

|

Balance, August 31, 2012

|

200,000

|

50,000

|

-

|

-

|

-

|

-

|

(76,448)

|

(26,448)

|

|

Sale

of common stock 18,000,000 common shares at $0.001 par

value

|

72,000

|

18,000

|

-

|

-

|

-

|

-

|

-

|

18,000

|

|

Imputed

Interest

|

-

|

-

|

-

|

-

|

2,035

|

-

|

-

|

2,035

|

|

Net

loss for the year ended August 31, 2013

|

-

|

-

|

-

|

-

|

-

|

-

|

(47,901)

|

(47,901)

|

|

Balance, August 31, 2013

|

272,000

|

68,000

|

-

|

-

|

2,035

|

-

|

(124,349)

|

(54,314)

|

|

15,750,000

common shares at $0.001 par value

|

63,000

|

15,750

|

-

|

-

|

311,219

|

-

|

-

|

326,969

|

|

Net

loss for the year ended August 31, 2014

|

-

|

-

|

-

|

-

|

-

|

-

|

(183,032)

|

(183,032)

|

|

Balance, August 31, 2014

|

335,000

|

83,750

|

-

|

-

|

313,254

|

-

|

(307,381)

|

89,623

|

|

Shares

issued for services

|

1,400

|

350

|

1,000,000

|

100

|

192,550

|

-

|

-

|

193,000

|

|

Shares

issued in deposit

|

20,000

|

5,000

|

-

|

-

|

-

|

-

|

-

|

5,000

|

|

Convertible

debt discount

|

-

|

-

|

-

|

-

|

99,630

|

-

|

-

|

99,630

|

|

Gain

on repurchase of convertible note

|

-

|

-

|

-

|

-

|

20,664

|

-

|

-

|

20,664

|

|

Net

loss for the year ended August 31, 2015

|

-

|

-

|

-

|

-

|

-

|

-

|

(1,448,618)

|

(1,448,618)

|

|

Balance, August 31, 2015 (Restated)

|

356,400

|

89,100

|

1,000,000

|

100

|

626,098

|

-

|

(1,755,999)

|

(1,040,701)

|

The

accompanying notes are an integral part of these consolidated

financial statements

26

AIM EXPLORATION INC.

CONSOLIDATED

STATEMENTS OF STOCKHOLDERS’ EQUITY (DEFICIT)

(Continued)

|

|

Common

Stock

|

Preferred

Stock

|

|

|

|

|

||

|

|

Number

of

|

Amount

|

Number

of

|

Amount

|

Additional

Paid-in Capital

|

Share

Subscriptions Receivable (Refundable)

|

Accumulated

Deficit

|

Total

|

|

|

shares

|

$

|

shares

|

$

|

$

|

$

|

$

|

$

|

|

Shares

issued for services

|

1,286,494

|

715

|

-

|

-

|

125,875

|

-

|

-

|

126,590

|

|

Shares

issued for debt

|

3,200,000

|

3,200

|

-

|

-

|

-

|

-

|

-

|

3,200

|

|

Shares

issued on conversion of notes

|

1,862,835

|

36,905

|

-

|

-

|

119,534

|

-

|

-

|

156,439

|

|

Shares

issued for mineral property

|

15,687,000

|

15,687

|

-

|

-

|

-

|

-

|

-

|

15,687

|

|

Shares

to be returned to treasury

|

-

|

-

|

-

|

-

|

-

|

(5,090)

|

-

|

(5,090)

|

|

Net

loss for the year ended August 31, 2016

|

-

|

-

|

-

|

-

|

-

|

-

|

(1,141,304)

|

(1,141,304)

|

|

|

|

|

|

|

|

|

|

|

|

Balance, August 31, 2016

|

22,392,729

|

145,607

|

1,000,000

|

100

|

871,507

|

(5,090)

|

(2,897,303)

|

(1,885,179)

|

The

accompanying notes are an integral part of these consolidated

financial statements

27

AIM EXPLORATION INC.

CONSOLIDATED

STATEMENTS OF CASH FLOWS

|

|

12 months

ended

August 31,

2016

|

12 months

ended

August 31,

2015

(Restated)

|

|

|

|

|

|

OPERATING

ACTIVITIES

|