Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - GRAHAM CORP | Financial_Report.xls |

| EX-31.1 - EX-31.1 - GRAHAM CORP | d901996dex311.htm |

| EX-21.1 - EX-21.1 - GRAHAM CORP | d901996dex211.htm |

| EX-23.1 - EX-23.1 - GRAHAM CORP | d901996dex231.htm |

| EX-31.2 - EX-31.2 - GRAHAM CORP | d901996dex312.htm |

| EX-32.1 - EX-32.1 - GRAHAM CORP | d901996dex321.htm |

| EX-3.2 - EX-3.2 - GRAHAM CORP | d901996dex32.htm |

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 1-8462

GRAHAM CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 16-1194720 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 20 Florence Avenue, Batavia, New York | 14020 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code 585-343-2216

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock (Par Value $.10) | NYSE |

Securities registered pursuant to Section 12(g) of the Act:

Title of Class

Preferred Stock Purchase Rights

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ¨ |

Accelerated filer þ | Non-accelerated filer ¨ |

Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the voting stock held by non-affiliates of the registrant as of September 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, was $273,126,754. The market value calculation was determined using the closing price of the registrant’s common stock on September 30, 2014, as reported on the NYSE (the exchange on which the registrant’s common stock was then listed). For purposes of the foregoing calculation only, all directors, officers and the Employee Stock Ownership Plan of the registrant have been deemed affiliates.

As of May 22, 2015, the registrant had outstanding 10,138,983 shares of common stock, $.10 par value.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement, to be filed in connection with the registrant’s 2015 Annual Meeting of Stockholders to be held on July 30, 2015, are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this filing.

Table of Contents

GRAHAM CORPORATION

Annual Report on Form 10-K

Year Ended March 31, 2015

| PAGE | ||||||

| PART I |

||||||

| Item 1 |

1 | |||||

| Item 1A |

6 | |||||

| Item 1B |

16 | |||||

| Item 2 |

16 | |||||

| Item 3 |

16 | |||||

| Item 4 |

16 | |||||

| PART II |

||||||

| Item 5 |

17 | |||||

| Item 6 |

18 | |||||

| Item 7 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 | ||||

| Item 7A |

30 | |||||

| Item 8 |

31 | |||||

| Item 9 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 64 | ||||

| Item 9A |

64 | |||||

| Item 9B |

64 | |||||

| PART III |

||||||

| Item 10 |

65 | |||||

| Item 11 |

65 | |||||

| Item 12 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 65 | ||||

| Item 13 |

Certain Relationships and Related Transactions, and Director Independence |

65 | ||||

| Item 14 |

66 | |||||

| PART IV |

||||||

| Item 15 |

66 | |||||

| Note: | Portions of the registrant’s definitive Proxy Statement, to be issued in connection with the registrant’s 2015 Annual Meeting of Stockholders to be held on July 30, 2015, are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Annual Report on Form 10-K. |

Table of Contents

PART I

(Dollar amounts in thousands except per share data)

| Item 1. |

Graham Corporation (“we,” “us,” “our”) is a global business that designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. Energy markets include oil refining, cogeneration, nuclear and alternative power. For the defense industry, our equipment is used in nuclear propulsion power systems for the U.S. Navy. Graham’s global brand is built upon our world-renowned engineering expertise in vacuum and heat transfer technology, responsive and flexible service and unsurpassed quality. We design and manufacture custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. We are also a leading nuclear code accredited fabrication and specialty machining company. We supply components used inside reactor vessels and outside containment vessels of nuclear power facilities. Our equipment can also be found in other diverse applications such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning.

Our corporate headquarters are located in Batavia, New York. We have production facilities co-located with our headquarters in Batavia and also at our wholly-owned subsidiary, Energy Steel & Supply Co. (“Energy Steel”), located in Lapeer, Michigan. We also have a wholly-owned foreign subsidiary, Graham Vacuum and Heat Transfer Technology (Suzhou) Co., Ltd. (“GVHTT”), located in Suzhou, China. GVHTT provides sales and engineering support for us in the People’s Republic of China and management oversight throughout Southeast Asia.

We were incorporated in Delaware in 1983 and are the successor to Graham Manufacturing Co., Inc., which was incorporated in New York in 1936. As of March 31, 2015, we had 397 employees. Our stock is traded on the NYSE under the ticker symbol “GHM”.

Unless indicated otherwise, dollar figures in this Annual Report on Form 10-K are reported in thousands.

Our Products, Customers and Markets

Our products are used in a wide range of industrial process applications primarily in energy markets, including:

| • | Petroleum Refining |

| — | conventional oil refining |

| — | oil sands extraction |

| • | Defense |

| — | propulsion systems for nuclear-powered aircraft carriers and submarines |

| • | Chemical and Petrochemical Processing |

| — | fertilizer plants |

| — | ethylene, methanol and nitrogen producing plants |

| — | plastics, resins and fibers plants |

| — | petrochemical intermediate plants |

| — | coal-to-chemicals plants |

| — | gas-to-liquids plants |

| • | Power Generation /Alternative Energy |

| — | nuclear power generation |

| — | fossil fuel plants |

1

Table of Contents

| — | biomass plants |

| — | cogeneration power plants |

| — | geothermal power plants |

| — | ethanol plants |

| • | Other |

| — | soap manufacturing plants |

| — | air conditioning and water heating systems |

| — | food processing plants |

| — | pharmaceutical plants |

| — | liquefied natural gas production facilities |

Our customers include end users of our products in their manufacturing, refining and power generation processes, large engineering companies that build installations for companies in such industries, and the original equipment manufacturers, who combine our products with their equipment prior to its sale to end users.

Our products are sold by a team of sales engineers we employ directly as well as by independent sales representatives located worldwide. There may be short periods of time, a fiscal year for example, where one customer may make up greater than 10% of our business. However, if this occurs in multiple years, it is usually not the same customer, or the same project, over such a multi-year period.

Over a business cycle, domestic sales will generally range between 40% to 60% of total sales. The mix of domestic and international sales can vary from year to year.

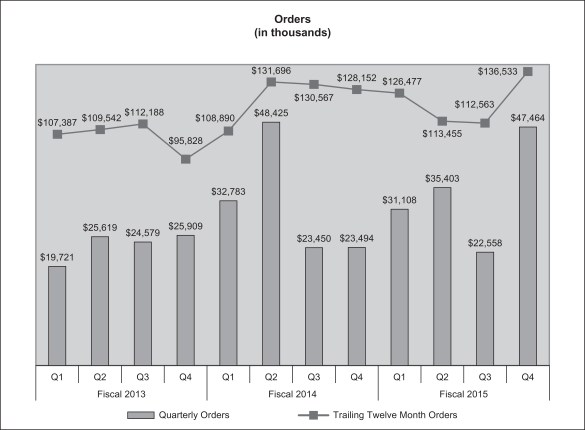

A breakdown of our net sales by geographic area and product class for our fiscal years ended March 31, 2015, 2014 and 2013, which we refer to as “fiscal 2015,” “fiscal 2014” and “fiscal 2013”, respectively, is contained in Note 13 to our consolidated financial statements included in Item 8 of Part II of this Annual Report on Form 10-K and such breakdown is incorporated into this Item 1 by reference. We refer to our fiscal year ending March 31, 2016 as “fiscal 2016”. Our backlog at March 31, 2015 was $113,811, compared with $112,108 at March 31, 2014.

Our Strengths

Our core strengths include:

| • | We have strong brand recognition. Over the past 79 years, we believe that we have built a reputation for top quality, reliable products and high standards of customer service. We have also established a large installed application base. As a result, the Graham name is well known not only by our existing customers, but also by many of our potential customers. We believe that the recognition of the Graham brand allows us to capitalize on market opportunities in both existing and potential markets. Moreover, our wholly-owned subsidiary, Energy Steel, has more than a 30 year history of providing products and support to its customers, especially the U.S. nuclear power industry, and is a recognized brand name in its markets. |

| • | We custom engineer and manufacture high quality products and systems that address the particular needs of our customers. With 79 years of engineering expertise, we believe that we are renowned for our knowledge in vacuum and heat transfer technologies. We maintain strict quality control and manufacturing standards in order to manufacture products of the highest quality. |

| • | We have a global presence. Our products are used worldwide, and we have sales representatives located in many countries throughout the world. |

| • | We have a strong reputation. We believe that we have a well-deserved reputation for both placing customers first and for standing behind our products. We believe that our relationships are strong both with our existing customer base as well as with our key suppliers. |

| • | We have a highly trained workforce. We maintain a long-tenured, highly skilled and extremely flexible workforce. |

2

Table of Contents

| • | We have a strong balance sheet. We maintain significant cash and investments on hand, and no bank debt, which we believe provides us with the flexibility to pursue our business strategy. Our defined benefit pension plan obligations are over funded. |

| • | We have a high quality credit facility. Our credit facilities provide us with a $30,000 borrowing capacity that is expandable at our option to provide us with up to a total of $55,000 in borrowing capacity. |

Our Strategy

We intend to strategically leverage and deploy our assets, including but not limited to, financial, technical, manufacturing and know-how, in order to capture expanded market share within the geographies and industries we serve, to expand revenue opportunities in adjacent and countercyclical markets and to continually improve our results of operations in order to:

| • | Generate sustainable earnings growth; |

| • | Reduce earnings volatility; |

| • | Improve our operating performance; |

| • | Generate strong cash flow from operations; and |

| • | Improve value provided to our customers. |

To accomplish our objectives and strategic focus, we believe that we must:

| • | Successfully deploy corporate assets to expand market share in currently served industries, access and develop a stronger presence in industries where we do not have a historically strong presence, and pursue acquisitions, partnerships or other business combinations in order to enter new geographic or industrial markets or new product lines. |

| • | Capitalize on the strength of the Graham and Energy Steel brands in order to both win more business in our traditional markets as well as enter new markets. |

| • | Identify organic growth opportunities and consummate acquisitions where we believe our brand strength will provide us with the ability to expand and will complement our core businesses. We intend to extend our existing product lines, move into complementary product lines and expand our global sales presence in order to further broaden our existing markets and reach additional markets. |

| • | Expand our market penetration in the domestic nuclear industry. We also intend to identify additional domestic and international opportunities to serve the commercial nuclear power industry. |

| • | Expand our market presence in the U.S. Navy’s Nuclear Propulsion Program. We plan to demonstrate our proficiency by successfully executing the complex Nuclear Propulsion Program orders that are currently in our backlog by controlling both cost and risk, providing high-quality custom fabrication to exacting military quality control requirements and through disciplined project management. We intend to become a preferred supplier of equipment to the Nuclear Propulsion Program for both surface and submarine vessels. |

| • | Continue to invest in people and capital equipment to meet the anticipated long-term growth in demand for our products in the oil refining, petrochemical processing and power generation industries, especially in emerging markets. |

| • | Continue to deliver the highest quality products and solutions that enable our customers to achieve their operating objectives. We believe that our high quality and technical expertise differentiates us from our competitors and allows us to win new orders based on value. |

In order to effectively implement our strategy, we also believe that we must continually invest in and leverage our unique customer value enhancing differentiators, the keys of which are listed below:

| • | Invest in engineering resources and technology in order to advance our vacuum and heat transfer technology market penetration. |

| • | Enhance our engineering capacity and capability, especially in connection with product design, in order to more quickly respond to existing and future customer demands. |

3

Table of Contents

| • | Invest in our manufacturing facilities to expand capacity where needed and identify out-sourced capacity to complement internal capacity. |

| • | Accelerate our ability to quickly and efficiently bid on available projects through our ongoing implementation of front-end bid automation and design processes. |

| • | Expand our capabilities and penetrate the existing sales channel and customer base in the nuclear market. |

| • | Invest in resources to further serve the U.S. Navy in our core competency areas of engineering and manufacturing, where our commercial capabilities meet U.S. Navy requirements. |

| • | Implement and expand upon our operational efficiencies through our ongoing refinement of our flexible manufacturing flow model as well as our achievement of other cost efficiencies. |

| • | Focus on improving quality to eliminate errors and rework, thereby reducing lead time. |

| • | Develop a cross-trained, flexible workforce able to adjust to variable product demand by our customers. |

Competition

Our business is highly competitive. The principal bases on which we compete include technology, price, performance, reputation, delivery, and quality. Our competitors in our primary markets include:

NORTH AMERICA

| Market |

Principal Competitors | |

| Refining vacuum distillation |

Gardner Denver, Inc. | |

| Chemicals/petrochemicals |

Croll Reynolds Company, Inc.; Schutte Koerting; Gardner Denver, Inc. | |

| Turbomachinery Original Equipment Manufacturer (“OEM”) — refining, petrochemical |

Ambassador; KEMCO; SPX Heat Transfer; Donghwa Entec Co., Ltd..; Oeltechnik GmbH | |

| Turbomachinery OEM — power and power producer |

Holtec; Thermal Engineering International (USA), Inc.; KEMCO; SPX Heat Transfer; Maarky Thermal Systems | |

| Nuclear |

Dubose, Consolidated, Tioga, Nova, Joseph Oats, Energy & Process, Nusource | |

| Navy Nuclear Propulsion Program / Defense |

DC Fabricators, Joseph Oats, Triumph Aerospace, Xylem, PCC |

INTERNATIONAL

| Market |

Principal Competitors | |

| Refining vacuum distillation |

Gardner Denver, Inc.; GEA Wiegand GmbH; Edwards, Ltd.; Korting Hannover AG | |

| Chemicals/petrochemicals |

Croll Reynolds Company, Inc.; Schutte Koerting; Gardner Denver, Inc.; GEA Wiegand GmbH; Korting Hannover AG; Edwards, Ltd. | |

| Turbomachinery OEM — refining, petrochemical |

Donghwa Entec Co., Ltd.; Hangzhou Turbine Equipment Co., Ltd.; Chem Process Systems, Mazda (India), Oeltechnik GmbH; KEMCO | |

| Turbomachinery OEM — power and power producer |

Holtec; Thermal Engineering International; KEMCO; SPX Heat Transfer, Chem Process Systems, Mazda (India) |

4

Table of Contents

Intellectual Property

Our success depends in part on our ability to protect our proprietary technology. We rely on a combination of patent, copyright, trademark, trade secret laws and contractual confidentiality provisions to establish and protect our proprietary rights. We also depend heavily on the brand recognition of the Graham and Energy Steel names in the marketplace.

Availability of Raw Materials

Historically, we have not been materially adversely impacted by the availability of raw materials.

Working Capital Practices

Our business does not require us to carry significant amounts of inventory or materials beyond what is needed for work in process. We do not provide rights to return goods, or payment terms to customers that we consider to be extended in the context of the industries we serve. However, we do provide for warranty claims.

Environmental Matters

We believe that we are in material compliance with applicable existing environmental laws and regulations. We do not anticipate that our compliance with federal, state and local laws regulating the discharge of material in the environment or otherwise pertaining to the protection of the environment will have a material adverse effect upon our capital expenditures, earnings or competitive position.

Seasonality

No material part of our business is seasonal in nature. However, our business is highly cyclical in nature as it depends on the willingness of our customers to invest in major capital projects.

Research and Development Activities

During fiscal 2015, fiscal 2014 and fiscal 2013, we spent $3,585, $3,436 and $3,579, respectively, on research and development activities related both to new products and services and the ongoing improvement of existing products and services.

Information Regarding International Sales

The sale of our products outside the U.S. accounted for a significant portion of our total revenue during our last three fiscal years. Approximately 36%, 38% and 47% of our revenue in fiscal 2015, fiscal 2014 and fiscal 2013, respectively, resulted from foreign sales. Sales in Asia constituted approximately 8%, 11% and 16% of our revenue in fiscal 2015, fiscal 2014 and fiscal 2013, respectively. Sales in the Middle East constituted approximately 8%, 4% and 14% of our revenue in fiscal 2015, fiscal 2014 and fiscal 2013, respectively. Our foreign sales and operations are subject to numerous risks, as discussed under the heading “Risk Factors” in Item 1A of Part I and elsewhere in this Annual Report on Form 10-K.

Employees

As of March 31, 2015, we had 397 employees. We believe that our relationship with our employees is good.

Available Information

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Therefore, we file periodic reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). The SEC maintains a website (located at www.sec.gov) that contains reports, proxy statements and other information for registrants that file electronically. Additionally, such reports may be read and copied at the Public Reference Room of the SEC at 100 F Street NE, Washington, D.C. 20549. Information regarding the SEC’s Public Reference Room can be obtained by calling 1-800-SEC-0330.

5

Table of Contents

We maintain a website located at www.graham-mfg.com. On our website, we provide a link to the SEC’s website that contains the reports, proxy statements and other information we file electronically. We do not provide this information on our website because it is more cost effective for us to provide a link to the SEC’s website. Copies of all documents we file with the SEC are available in print for any stockholder who makes a request. Such requests should be made to our Corporate Secretary at our corporate headquarters. The other information found on our website is not part of this or any other report we file with, or furnish to, the SEC.

| Item 1A. |

Our business and operations are subject to numerous risks, many of which are described below and elsewhere in this Annual Report on Form 10-K. If any of the events described below or elsewhere in this Annual Report on Form 10-K occur, our business and results of operations could be harmed. Additional risks and uncertainties that are not presently known to us, or which we currently deem to be immaterial, could also harm our business and results of operations.

Risks related to our business

The industries in which we operate are cyclical, and downturns in such industries may adversely affect our operating results.

A substantial portion of our revenue is derived from the sale of our products to companies in the chemical, petrochemical, petroleum refining and power generating industries and to the U.S. Navy, or to firms that design and construct facilities for these industries. The core industries in which our products are used are highly cyclical and have historically experienced severe downturns. The dramatic decline in global oil prices in the second half of calendar year 2014 that translated into an abrupt contraction in orders in the energy markets is the most recent example of the cyclical nature of our markets. We believe that for the long-term, we are in an expansion for demand for our products in the petrochemical, petroleum refining and power generating industries, however, the recent decline in oil prices confirms that cyclical downturns will occur periodically. A sustained or renewed deterioration in any of the industries we serve would materially harm our business and operating results because our customers would not likely have the resources necessary to purchase our products, nor would they likely have the need to build additional facilities or improve existing facilities. A cyclical downturn can occur suddenly and result in extremely different financial performance sequentially from quarter to quarter or on an annual comparative basis due to an inability to rapidly adjust costs.

The larger markets we serve include the petroleum refining and petrochemical industries. These industries are both highly cyclical in nature and dependent on the price of crude oil and natural gas as well as on the differential between the two prices. As a result, volatility in the prices of oil and natural gas may negatively impact our operating results.

The prices of crude oil and natural gas have historically been very volatile, as evidenced by the approximately 50% decline in oil prices in the second half of calendar 2014. Importantly, this caused a steep decline in orders from the energy markets. The increased supply and reduction of cost of natural gas in North America has also caused a significant change in the global energy markets in the past few years. During times of significant volatility in the market for crude oil or natural gas, our customers often refrain from placing orders until the market stabilizes. If our customers refrain from placing orders with us, our revenue would decline and there could be a material adverse effect on our business and results of operations. We believe that the global consumption of crude oil and natural gas will increase over the course of the next 20 years and that such increased consumption will result in a need to continually increase global capacity. Many of our products are purchased in connection with oil refinery construction, revamps and upgrades to expand global capacity.

The relative costs of oil, natural gas, nuclear power, hydropower and numerous forms of alternative energy production may have a material adverse impact on our business and operating results.

Global and regional energy supply comes from many sources, including oil, natural gas, coal, hydro, nuclear, solar, wind, geothermal and biomass, among others. A cost or supply shift among these sources could negatively impact our business opportunities going forward. A demand shift, where technological advances favor the utilization of one or a few sources of energy may also impact demand for our products. If demand shifts in a manner that increases energy utilization outside of our traditional customer base or expertise, our business and

6

Table of Contents

financial results could be materially adversely affected. In addition, governmental policy can affect the relative importance of various forms of energy sources. Non-fossil based sources may require government tax incentives to foster investment.

Our business is highly competitive. If we are unable to successfully implement our business strategy and compete against entities with greater resources than us or against competitors who have a relative cost advantage, we risk losing market share to current and future competitors.

We encounter intense competition in all of our markets. Some of our present and potential competitors may have substantially greater financial, marketing, technical or manufacturing resources. Our competitors may also be able to respond more quickly to new technologies or processes and changes in customer demands and they may be able to devote greater resources towards the development, promotion and sale of their products. Certain of our competitors may also have a cost advantage compared to us and may compete against us based on price. This may affect our ability to secure new business and maintain our level of profitability. In addition, our current and potential competitors may make strategic acquisitions or establish cooperative relationships among themselves or with third parties that increase their ability to address the needs of our customers. Moreover, customer buying patterns can change if customers become more price sensitive and accepting of lower cost suppliers. If we cannot compete successfully against current or future competitors, our business will be materially adversely affected.

A change in our end use customers, our markets, or a change in the engineering procurement and construction companies serving our markets could harm our business and negatively impact our financial results.

Although we have long-term relationships with many of our end use customers and with many engineering, procurement and construction companies, the project management requirements, pricing levels and costs to support each customer and customer type are often different. As our markets continue to grow, and new market opportunities expand, we could see a shift in pricing as a result of facing competitors with lower production costs, which may have a material adverse impact on our results of operations and financial results. In certain developing geographies, the relative importance of cost versus quality may lead to decisions which look at short-term costs instead of total long-term cost of operations.

The loss of, or significant reduction or delay in, purchases by our largest customers could reduce our revenue and adversely affect our results of operations.

A small number of customers has accounted for a substantial portion of our historical net sales. For example, sales to our top ten customers accounted for 38%, 32% and 41% of consolidated net sales in fiscal 2015, 2014 and 2013, respectively. We expect that a limited number of customers will continue to represent a substantial portion of our sales for the foreseeable future. The loss of any of our major customers, a decrease or delay in orders or anticipated spending by such customers or a delay in the production of existing orders could materially adversely affect our revenues and results of operations.

A large percentage of our sales occur outside of the U.S. As a result, we are subject to the economic, political, regulatory and other risks of international operations.

For fiscal 2015, 36% of our revenue was from customers located outside of the U.S. Moreover, we maintain a subsidiary and a sales office in China. We believe that revenue from the sale of our products outside the U.S. will continue to account for a significant portion of our total revenue for the foreseeable future. We intend to continue to expand our international operations to the extent that suitable opportunities become available. Our foreign operations and sales could be adversely affected as a result of:

| • | nationalization of private enterprises and assets; |

| • | political or economic instability in certain countries and regions, such as the ongoing instability throughout the Middle East or portions of the former Soviet Union; |

7

Table of Contents

| • | differences in foreign laws, including increased difficulties in protecting intellectual property and uncertainty in enforcement of contract rights; |

| • | the possibility that foreign governments may adopt regulations or take other actions that could directly or indirectly harm our business and growth strategy; |

| • | credit risks; |

| • | currency fluctuations; |

| • | tariff and tax increases; |

| • | export and import restrictions and restrictive regulations of foreign governments; |

| • | shipping products during times of crisis or wars; |

| • | our failure to comply with U.S. laws regarding doing business in foreign jurisdictions, such as the Foreign Corrupt Practices Act; and |

| • | other factors inherent in maintaining foreign operations. |

Global demand growth could be led by emerging markets, which could result in lower profit margins and increased competition.

The increase in global demand could be led by emerging markets. If this is the case, we may face increased competition from lower cost suppliers, which in turn could lead to lower profit margins on our products. Customers in emerging markets may also place less emphasis on our high quality and brand name than do customers in the U.S. and certain other industrialized countries where we compete. If we are forced to compete for business with customers that place less emphasis on quality and brand recognition than our current customers, our results of operations could be materially adversely affected.

The operations of our Chinese subsidiary may be adversely affected by China’s evolving economic, political and social conditions.

We conduct our business in China primarily through a wholly-owned Chinese subsidiary. The results of operations and future prospects of our Chinese subsidiary are subject to evolving economic, political and social developments in China. In particular, the results of operations of our Chinese subsidiary may be adversely affected by, among other things, changes in China’s political, economic and social conditions, changes in policies of the Chinese government, changes in laws and regulations or in the interpretation of existing laws and regulations, changes in foreign exchange regulations, measures that may be introduced to control inflation, such as interest rate increases, and changes in the rates or methods of taxation. In addition, changes in demand could result from increased competition from local Chinese manufacturers who have cost advantages or who may be preferred suppliers for Chinese end users. Also, Chinese commercial laws, regulations and interpretations applicable to non-Chinese owned market participants, such as us, are continually changing. These laws, regulations and interpretations could impose restrictions on our ownership or operations of our interests in China and have a material adverse effect on our business.

Intellectual property rights are difficult to enforce in China, which could harm our business.

Chinese commercial law is relatively undeveloped compared with the commercial law in many of our other major markets and limited protection of intellectual property is available in China as a practical matter. Although we take precautions in the operations of our Chinese subsidiary to protect our intellectual property, any local design or manufacture of products that we undertake in China could subject us to an increased risk that unauthorized parties will be able to copy or otherwise obtain or use our intellectual property, which could harm our business. We may also have limited legal recourse in the event we encounter patent or trademark infringers, which could have a material adverse effect on our business and results of operations.

Uncertainties with respect to the Chinese legal system may adversely affect the operations of our Chinese subsidiary.

Our Chinese subsidiary is subject to laws and regulations applicable to foreign investment in China. There are uncertainties regarding the interpretation and enforcement of laws, rules and policies in China. The Chinese

8

Table of Contents

legal system is based on written statutes, and prior court decisions have limited precedential value. Because many laws and regulations are relatively new and the Chinese legal system is still evolving, the interpretations of many laws, regulations and rules are not always uniform. Moreover, the relative inexperience of China’s judiciary in many cases creates additional uncertainty as to the outcome of any litigation, and the interpretation of statutes and regulations may be subject to government policies reflecting domestic political agendas. Finally, enforcement of existing laws or contracts based on existing law may be uncertain and sporadic. For the preceding reasons, it may be difficult for us to obtain swift or equitable enforcement of laws ostensibly designed to protect companies like ours, which could have a material adverse effect on our business and results of operations.

Changes in energy policy regulations could adversely affect our business.

Energy policy in the U.S. and in the other countries where we sell our products is evolving rapidly and we anticipate that energy policy will continue to be an important legislative priority in the jurisdictions where we sell our products. It is difficult, if not impossible, to predict the changes in energy policy that could occur. The elimination of, or a change in, any of the current rules and regulations in any of our markets could create a regulatory environment that makes our end users less likely to purchase our products, which would have a material adverse effect on our business. Government subsidies or taxes, which favor or disfavor certain energy sources compared with others, could have a material adverse effect on our business and operating results.

Regulations related to “conflict minerals” may cause us to incur additional expenses and could limit the supply and/or increase the cost of certain metals used in manufacturing our products.

SEC rules require disclosures of specified minerals, known as conflict minerals, that are necessary to the functionality or production of products manufactured or contracted to be manufactured by companies filing public reports. This rule, which became effective for the 2013 calendar year, requires companies to perform due diligence, disclose, and report whether such minerals originate from the Democratic Republic of Congo or an adjoining country. This rule could affect sourcing at competitive prices and availability in sufficient quantities of certain minerals used in the manufacture of our products. Moreover, the number of suppliers who provide conflict-free minerals may become limited. In addition, there may be significant costs associated with complying with the disclosure requirements. We also may not be able to sufficiently verify the origins of the relevant conflict minerals used in our products through the due diligence procedures that we have implemented, which could harm our reputation.

Efforts to reduce large U.S. federal budget deficits could result in government cutbacks in defense spending or in reduced incentives to pursue alternative energy projects, resulting in reduced demand for our products, which could harm our business and results of operations.

Our business strategy calls for us to continue to pursue defense-related projects as well as projects for end users in the alternative energy markets in the U.S. In recent years the U.S. federal government has incurred large budget deficits. In the event that U.S. federal government defense spending is reduced or alternative energy related incentives are reduced or eliminated in an effort to reduce federal budget deficits, projects related to defense or alternative energy may become less plentiful. The impact of such reductions could have a material adverse effect on our business and results of operations, as well as our growth opportunities.

U.S. Navy orders are subject to annual government funding. A disruption in expected funding could adversely impact our business.

One of our growth strategies is to increase our penetration of U.S. Navy related opportunities. Projects for the U.S. Navy and its contractors generally have a much longer order-to-shipment time period than our commercial orders. The time between receipt of an order to complete shipment can take three to five years, or possibly longer. Annual government funding is required to continue the production of this equipment. Disruption of government funding, short or long term, could impact the ability for us to continue our production activity on these orders. Such a disruption, should it occur, could adversely impact the sales and profitability of our business.

9

Table of Contents

Changes in tax policies and tax rates in the U.S. could result in adverse impacts for domestic manufacturing investments, resulting in reduced demand for our products.

Our business is dependent on significant manufacturing investment in the U.S. The impact of changes to U.S. tax policy around capital investment and related depreciation could reduce our customers’ willingness to invest in domestic capacity. The impact of such reductions could have a materially adverse affect on our business and operations.

We serve markets that are capital intensive. Volatility and disruption of the capital and credit markets and adverse changes in the global economy may negatively impact our operating results. Such volatility and disruption may also negatively impact our ability to access additional financing if and when needed.

If adverse economic and credit conditions occur, we would likely experience decreased revenue from our operations attributable to decreases in the spending levels of our customers. Moreover, adverse economic and credit conditions might also have a negative adverse effect on our cash flows if customers demand that we accept smaller project deposits and less frequent progress payments. In addition, adverse economic and credit conditions could lead to increased downward pricing pressure. Any of the foregoing could have a material adverse effect on our business and results of operations.

Adverse conditions in the capital and credit markets could also have a material adverse effect on our ability to obtain additional financing on commercially reasonable terms, or at all, should we determine such financing is necessary or desirable to maintain or expand our business or effectively pursue our business strategy.

Political and regulatory developments could make the utilization and growth of nuclear power as an energy source less desirable, which would harm the business and results of operations of our subsidiary Energy Steel.

A global event, such as a major earthquake or terrorist activity, may impact the desirability of operating nuclear power plants. These events can create uncertainties worldwide regarding, among other things, the desirability of operating existing nuclear power plants and the building of new or replacement nuclear power plants. Should public opinion or political pressure result in the closing of existing nuclear facilities or otherwise result in the failure of the nuclear power industry to grow, especially within the U.S., the business, results of operations and growth prospects of our subsidiary Energy Steel in the nuclear market could be materially adversely impacted.

In addition, the U.S. Nuclear Regulatory Commission, or NRC, performs operational and safety reviews of nuclear facilities in the U.S. It is possible that the NRC could take actions or impose regulations that adversely affect the demand for Energy Steel’s products and services, or otherwise delay or prohibit construction of new nuclear power generation facilities, even temporarily. If any such event were to occur, the business or operations of Energy Steel could be materially adversely impacted.

A change in supply or cost of the materials used in our products could harm our profit margins.

Our profitability depends in part on the price and continuity of supply of the materials used in the manufacture of our products which, in many instances, are supplied by a limited number of sources. The availability and costs of these commodities may be influenced by, among other things, market forces of supply and demand, changes in world politics, labor relations between the producers and their work forces, export quotas, and inflation. Any restrictions on the supply of the materials used by us in manufacturing our products could significantly reduce our profit margins, which could harm our results of operations. Likewise, any efforts we may engage in to mitigate restrictions on the supply or price increases of materials by entering into long-term purchase agreements, by implementing productivity improvements or by passing cost increases on to our customers may not be successful. In addition, the ability of our suppliers to meet quality and delivery requirements can also impact our ability to meet commitments to customers. Future shortages or lower cost of raw materials could result in decreased sales as well as margins, or otherwise materially adversely affect our business.

We are subject to contract cancellations and delays by our customers, which may adversely affect our operating results.

The value of our backlog as of March 31, 2015 was $113,811. Our backlog can be significantly affected by the timing of large orders. The amount of our backlog at March 31, 2015 is not necessarily indicative of future

10

Table of Contents

backlog levels or the rate at which our backlog will be recognized as sales. Although historically the amount of modifications and terminations of our orders has not been material compared with our total contract volume, customers can, and sometimes do, terminate or modify their orders. This generally occurs more often in times of end market or capital market turmoil. As evidence of this, we had two orders totaling $5,895 cancelled in the fourth quarter of fiscal 2015. We cannot predict whether cancellations will occur or accelerate in the future. Although certain of our contracts in backlog may contain provisions allowing for us to assess cancellation charges to our customers to compensate us for costs incurred on cancelled contracts, cancellations of purchase orders or modifications made to existing contracts could substantially and materially reduce our backlog and, consequently, our future sales and results of operations. Moreover, delay of contract execution by our customers can result in volatility in our operating results.

Our current backlog contains a number of large orders from the U.S. Navy project. In addition, we are continuing to pursue business in these end markets which offer large multi-year projects which have an added risk profile beyond that of our historic customer base. A delay, long term extension or cancellation in any of these projects could have a material adverse effect on our business and results of operations.

Our accounts receivables and unbilled revenue may be at potential risk if a project is terminated or canceled or if our customers encounter financial difficulties.

Our contracts often require us to satisfy or achieve certain milestones in order to receive payment for the work performed. In general, payments to us are such that we are ahead of our costs, however, if the customer does not proceed with the completion of the project or if the customer defaults on its payment obligations, we may face difficulties in collecting payment of amounts due to us. If we are unable to collect amounts owed to us, this would have an adverse effect on our results of operations, financial position and cash flows.

If we are unable to effectively outsource a portion of our production during times when we are experiencing strong demand, our results of operations might be adversely affected. In addition, outsourcing may negatively affect our profit margins.

We from time to time increase our manufacturing capacity through outsourcing selected fabrication processes. We could experience difficulty in outsourcing if customers demand that our products be manufactured by us exclusively. Furthermore, our ability to effectively outsource production could be adversely affected by worldwide manufacturing capacity. If we are unable to effectively outsource our production capacity when circumstances warrant, our results of operations could be materially adversely affected and we might not be able to deliver products to our customers on a timely basis. In addition, any disputes between us and the entities that we outsource to may delay our ability to fulfill our obligations to our customers, which may harm our reputation and in turn could have a material adverse effect on our business and results of operations. Further, outsourcing to complete our products and services can increase the costs associated with such products and services. If we rely too heavily on outsourcing and are not able to increase our own production capacity during times when there is high demand for our products and services, our profit margins may be negatively impacted.

Our exposure to fixed-price contracts and the timely completion of such contracts could negatively impact our results of operations.

A substantial portion of our sales is derived from fixed-price contracts, which may involve long-term fixed price commitments by us to our customers. While we believe our contract management processes are strong, we nevertheless could experience difficulties in executing large contracts, including but not limited to, cost overruns, supplier failures and customer disputes. To the extent that any of our fixed-price contracts are delayed, our subcontractors fail to perform, contract counterparties successfully assert claims against us, the original cost estimates in these or other contracts prove to be inaccurate or the contracts do not permit us to pass increased costs on to our customers, our profitability from a particular contract may decrease or losses may be incurred, which, in turn, could have a material adverse effect on our business and results of operations.

11

Table of Contents

We utilize percentage of completion accounting on the majority of our sales. Changes in estimates for production could result in a reduction or elimination of previously reported sales and earnings.

For the majority of our sales, cost of goods sold and operating profit are recognized using percentage of completion method of accounting. This accounting method requires updated recognition of sales and cost for each project on a quarterly basis. If the portion of a project is under or over-estimated, a correction is required to be made in the current period. Corrections for large projects could significantly impact short term financial results. Large revisions could reverse sales, costs and earnings reported in prior periods.

If we lose any member of our management team and we experience difficulty in finding a qualified replacement, our business would be harmed.

Competition for qualified management and key technical and sales personnel in our industry is intense. Moreover, our technology is highly specialized and it may be difficult to replace the loss of any of our key technical and sales personnel. Many of the companies with which we compete for management and key technical and sales personnel have greater financial and other resources than we do or are located in geographic areas which may be considered by some to be more desirable places to live. If we are not able to retain any of our key management, technical or sales personnel, it could have a material adverse effect on our business and results of operations.

A dramatic short-term change in our end markets and our reaction to it may impact our ability to execute our strategic plan over the long term.

Execution of our strategic plan requires us to invest in our equipment, people and other resources with a view toward the long term. Achieving our long-term objectives may require us to pre-invest and add costs to our business before the matching revenue occurs. This is necessary to ensure that the development of our employees is such that we may effectively serve our customers. When there is a dramatic and unforeseen change in market conditions, which affects our customers and therefore our business, we may have to choose between continuing to pre-invest, which will impact near-term profitability or to eliminate costs which may impede our long-term ability to execute our strategic plan.

During certain high demand periods, there can be a shortage of skilled production workers, especially those with high-end welding capabilities. We could experience difficulty hiring or replacing those individuals, which could adversely affect our business.

Our fabrication processes require highly skilled production workers, especially welders. Welding has not been an educational field that has been popular over the past few decades as manufacturing has moved overseas. If we were to be unable to retain, hire or train an adequate number of individuals with high-end welding capability, this could impact our ability to achieve our financial objectives. In addition, if demand for highly skilled production workers were to significantly outstrip supply, wages for these skilled workers could dramatically increase in our and related industries and that could affect our financial performance.

If we are unable to make necessary capital investments or respond to pricing pressures, our business may be harmed.

In order to remain competitive, we need to invest continuously in manufacturing, customer service and support, research and development and marketing. From time to time we also have to adjust the prices of our products to remain competitive. We may not have available sufficient financial or other resources to continue to make the investment necessary to lower our production costs and help us maintain our competitive position, which could have a material adverse effect on our business and results of operations.

Our acquisition strategy may not be successful or may increase business risk.

The success of our acquisition strategy will depend, in part, on our ability to identify suitable companies or businesses to purchase and then successfully negotiate and close acquisition transactions. In addition, our success depends in part on our ability to integrate acquisitions and realize the anticipated benefits from combining the acquisition with our historical business, operations and management. We cannot provide any assurances that we

12

Table of Contents

will be able to complete any acquisitions and then successfully integrate the business and operations of those acquisitions without encountering difficulties, including unanticipated costs, difficulty in retaining customers and supplier or other relationships, failure to retain key employees, diversion of our management’s attention, failure to integrate information and accounting systems or establish and maintain proper internal control over financial reporting. Moreover, as part of the integration process, we must incorporate an acquisition’s existing business culture and compensation structure with our existing business. If we are not able to efficiently integrate an acquisition’s business and operations into our organization in a timely and efficient manner, or at all, the anticipated benefits of the acquisition may not be realized, or it may take longer to realize these benefits than we currently expect, either of which could have a material adverse effect on our business or results of operations.

Should a portion of our intangible assets be impaired, results of operations could be materially adversely affected.

Our balance sheet includes intangible assets, including goodwill and other separately identifiable intangible assets, primarily as a result of our acquisition of Energy Steel. The value of these intangible assets may increase in the future if we complete additional acquisitions as part of our overall business strategy. We are required to review our intangible assets for impairment on an annual basis, or more frequently if certain indicators of permanent impairment arise. Factors that could indicate that our intangible assets are impaired could include, among other things, a decline in our stock price and market capitalization, lower than projected operating results and cash flows, and slower than expected growth rates in our markets. If a portion of our intangible assets becomes impaired as a result of such a review, the impaired portion of such assets would have to be written-off during that period. Such a write-off could have a material adverse effect on our business and results of operations.

If we become subject to product liability, warranty or other claims, our results of operations and financial condition could be adversely affected.

The manufacture and sale of our products exposes us to potential product liability claims, including those that may arise from failure to meet product specifications, misuse or malfunction of our products, design flaws in our products, or use of our products with systems not manufactured or sold by us. For example, our equipment is installed in facilities that operate dangerous processes and the misapplication, improper installation or failure of our equipment may result in exposure to potentially hazardous substances, personal injury or property damage.

Provisions contained in our contracts with customers that attempt to limit our damages may not be enforceable or may fail to protect us from liability for damages and we may not negotiate such contractual limitations of liability in certain circumstances. Our insurance may not cover all liabilities nor may our historical experience reflect any liabilities we may face in the future. Our risk of liability may increase as we manufacture more complex or larger projects. We also may not be able to continue to maintain such insurance at a reasonable cost or on reasonable terms, or at all. Any material liability not covered by provisions in our contracts or by insurance could have a material adverse effect on our business and financial condition.

Furthermore, if a customer suffers damage as a result of an event related to one of our products, even if we are not at fault, they may reduce their business with us. We may also incur significant warranty claims, which are not covered by insurance. In the event a customer ceases doing business with us as a result of a product malfunction or defect, perceived or actual, or if we incur significant warranty costs in the future, there could be a material adverse effect on our business and results of operations.

If we fail to introduce enhancements to our existing products or to keep abreast of technological changes in our markets, our business and results of operations could be adversely affected.

Although technologies in the vacuum and heat transfer areas are well established, we believe our future success depends, in part, on our ability to enhance our existing products and develop new products in order to continue to meet customer demands. Our failure to introduce new or enhanced products on a timely and cost-competitive basis, or the development of processes that make our existing technologies or products obsolete could have a material adverse effect on our business and results of operations.

13

Table of Contents

If third parties infringe upon our intellectual property or if we were to infringe upon the intellectual property of third parties, we may expend significant resources enforcing or defending our rights or suffer competitive injury.

Our success depends in part on our proprietary technology. We rely on a combination of patent, copyright, trademark, trade secret laws and confidentiality provisions to establish and protect our proprietary rights. If we fail to successfully enforce our intellectual property rights, our competitive position could suffer. We may also be required to spend significant resources to monitor and police our intellectual property rights. Similarly, if we were found to have infringed on the intellectual property rights of others, our competitive position could suffer. Furthermore, other companies may develop technologies that are similar or superior to our technologies, duplicate or reverse engineer our technologies or design around our proprietary technologies. Any of the foregoing could have a material adverse effect on our business and results of operations.

In some instances, litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties that our products infringe their intellectual property rights. Any litigation or claims brought by or against us, whether with or without merit, could result in substantial costs to us and divert the attention of our management, which could materially harm our business and results of operations. In addition, any intellectual property litigation or claims against us could result in the loss or compromise of our intellectual property and proprietary rights, subject us to significant liabilities, require us to seek licenses on unfavorable terms, prevent us from manufacturing or selling certain products or require us to redesign certain products, any of which could have a material adverse effect on our business and results of operations.

We are subject to foreign currency fluctuations which may adversely affect our operating results.

We are exposed to the risk of currency fluctuations between the U.S. dollar and the currencies of the countries in which we sell our products to the extent that such sales are not based on U.S. dollars. Currency movements can affect sales in several ways, the foremost being our ability to compete for orders against foreign competitors that base their prices on relatively weaker currencies. Business lost due to competition for orders against competitors using a relatively weaker currency cannot be quantified. In addition, cash can be adversely impacted by the conversion of sales made by us in a foreign currency to U.S. dollars. While we may enter into currency exchange rate hedges from time to time to mitigate these types of fluctuations, we cannot remove all fluctuations or hedge all exposures and our earnings are impacted by changes in currency exchange rates. In addition, if the counter-parties to such exchange contracts do not fulfill their obligations to deliver the contractual foreign currencies, we could be at risk for fluctuations, if any, required to settle the obligation. Any of the foregoing could adversely affect our business and results of operations. At March 31, 2015, we held no forward foreign currency exchange contracts.

Changes in our effective tax rate and tax policies may impact our profitability.

We are subject to income and other taxes in the U.S. and China. A change in tax laws or interpretation of tax laws, introduction of new tax accounting standards and regulation, our global mix of earnings, the ability to utilize deferred tax assets and changes in uncertain tax positions could affect our effective tax rate and impact the financial performance of the company. Changes in tax laws of other jurisdictions could impact the profitability of our competitors, which could affect our competitive position relative to those competitors.

Security threats and other sophisticated computer intrusions could harm our information systems, which in turn could harm our business and financial results.

We utilize information systems and computer technology throughout our business. We store sensitive data, proprietary information and perform engineering designs and calculations on these systems. Information systems are subject to threats and sophisticated computer crimes, which pose a risk to the stability and security of our business. A failure or breach in security could expose our company as well as our customers and suppliers to risks of misuse of information, compromising confidential information and technology, destruction of data, production disruptions and other business risks which could damage our reputation, competitive position and financial results of our operations. In addition, defending ourselves against these threats may increase costs or slow

14

Table of Contents

operational efficiencies of our business. If any of the foregoing were to occur, it could have a material adverse effect on our business and results of operations.

We face potential liability from asbestos exposure and similar claims that could result in substantial costs to us as well as divert attention of our management, which could have a material adverse effect on our business and results of operations.

We are a defendant in a number of lawsuits alleging illnesses from exposure to asbestos or asbestos-containing products and seeking unspecified compensatory and punitive damages. We cannot predict with certainty the outcome of these lawsuits or whether we could become subject to any similar, related or additional lawsuits in the future. In addition, because some of our products are used in systems that handle toxic or hazardous substances, any failure or alleged failure of our products in the future could result in litigation against us. For example, a claim could be made under various regulations for the adverse consequences of environmental contamination. Any litigation brought against us, whether with or without merit, could result in substantial costs to us as well as divert the attention of our management, which could have a material adverse effect on our business and results of operations.

Any failure to comply with the United States Foreign Corrupt Practices Act could adversely impact our competitive position and subject us to penalties and other adverse consequences, which could harm our business and results of operations.

We are subject to the United States Foreign Corrupt Practices Act, which generally prohibits U.S. companies from engaging in bribery or making other prohibited payments to foreign officials for the purpose of obtaining or retaining business. Many foreign companies, including some of our competitors, are not subject to these prohibitions. Corruption, extortion, bribery, pay-offs, theft and other fraudulent practices occur from time-to-time in certain of the jurisdictions in which we may operate or sell our products. While we strictly prohibit our employees and agents from engaging in such conduct and have established procedures, controls and training to prevent such conduct from occurring, it is possible that our employees or agents will engage in such conduct and that we might be held responsible. If our employees or other agents are alleged or are found to have engaged in such practices, we could incur significant costs and suffer severe penalties or other consequences that may have a material adverse effect on our business, financial condition and results of operations.

Risks related to the ownership of our common stock

Provisions contained in our certificate of incorporation and bylaws could impair or delay stockholders’ ability to change our management and could discourage takeover transactions that our stockholders might consider to be in their best interests.

Provisions of our certificate of incorporation and bylaws could impede attempts by our stockholders to remove or replace our management and could discourage others from initiating a potential merger, takeover or other change of control transaction, including a potential transaction at a premium over the market price of our common stock, that our stockholders might consider to be in their best interests. Such provisions include:

| • | We could issue shares of preferred stock with terms adverse to our common stock. Under our certificate of incorporation, our Board of Directors is authorized to issue shares of preferred stock and to determine the rights, preferences and privileges of such shares without obtaining any further approval from the holders of our common stock. We could issue shares of preferred stock with voting and conversion rights that adversely affect the voting power of the holders of our common stock, or that have the effect of delaying or preventing a change in control of our company. |

| • | Only a minority of our directors may be elected in a given year. Our bylaws provide for a classified Board of Directors, with only approximately one-third of our Board elected each year. This provision makes it more difficult to effect a change of control because at least two annual stockholder meetings are necessary to replace a majority of our directors. |

| • | Our bylaws contain advance notice requirements. Our bylaws also provide that any stockholder who wishes to bring business before an annual meeting of our stockholders or to nominate candidates for elec- |

15

Table of Contents

| tion as directors at an annual meeting of our stockholders must deliver advance notice of their proposals to us before the meeting. Such advance notice provisions may have the effect of making it more difficult to introduce business at stockholder meetings or nominate candidates for election as director. |

| • | Our certificate of incorporation requires supermajority voting to approve a change of control transaction. Seventy-five percent of our outstanding shares entitled to vote are required to approve any merger, consolidation, sale of all or substantially all of our assets and similar transactions if the other party to such transaction owns 5% or more of our shares entitled to vote. In addition, a majority of the shares entitled to vote not owned by such 5% or greater stockholder are also required to approve any such transaction. |

| • | Amendments to our certificate of incorporation require supermajority voting. Our certificate of incorporation contains provisions that make its amendment require the affirmative vote of both 75% of our outstanding shares entitled to vote and a majority of the shares entitled to vote not owned by any person who may hold 50% or more of our shares unless the proposed amendment was previously recommended to our stockholders by an affirmative vote of 75% of our Board. This provision makes it more difficult to implement a change to our certificate of incorporation that stockholders might otherwise consider to be in their best interests without approval of our Board. |

| • | Amendments to our bylaws require supermajority voting. Although our Board of Directors is permitted to amend our bylaws at any time, our stockholders may only amend our bylaws upon the affirmative vote of both 75% of our outstanding shares entitled to vote and a majority of the shares entitled to vote not owned by any person who owns 50% or more of our shares. This provision makes it more difficult for our stockholders to implement a change they may consider to be in their best interests without approval of our Board. |

| Item 1B. |

Not applicable.

| Item 2. |

Our corporate headquarters, located at 20 Florence Avenue, Batavia, New York, consists of a 45,000 square foot building. Our manufacturing facilities, also located in Batavia, consist of approximately 33 acres and contain about 260,000 square feet in several buildings, including 206,000 square feet in manufacturing facilities, 48,000 square feet for warehousing and a 6,000 square-foot building for product research and development. We also lease approximately 15,000 square feet of office space and 45,000 square feet of manufacturing facilities for our subsidiary, Energy Steel, located in Lapeer, Michigan. Additionally, we lease an approximately 1,500 square foot U.S. sales office in Houston, Texas and GVHTT leases an approximately 4,900 square foot sales and engineering office in Suzhou, China.

We believe that our properties are generally in good condition, are well maintained, and are suitable and adequate to carry on our business.

| Item 3. |

The information required by this Item 3 is contained in Note 15 to our consolidated financial statements included in Item 8 of Part II of this Annual Report on Form 10-K and is incorporated herein by reference.

| Item 4. |

Not applicable.

16

Table of Contents

PART II

(Amounts in thousands, except per share data)

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is traded on the NYSE exchange under the symbol “GHM”. As of May 22, 2015, there were 10,139 shares of our common stock outstanding that were held by approximately 148 stockholders of record.

The following table shows the high and low per share prices of our common stock for the periods indicated(1).

| High | Low | |||||||

| Fiscal year 2015 |

||||||||

| First quarter |

$ | 34.88 | $ | 26.20 | ||||

| Second quarter |

35.35 | 27.99 | ||||||

| Third quarter |

34.65 | 26.06 | ||||||

| Fourth quarter |

28.86 | 20.58 | ||||||

| Fiscal year 2014 |

||||||||

| First quarter |

$ | 31.41 | $ | 22.36 | ||||

| Second quarter |

38.96 | 30.26 | ||||||

| Third quarter |

41.94 | 32.95 | ||||||

| Fourth quarter |

37.23 | 30.23 | ||||||

Subject to the rights of any preferred stock we may then have outstanding, the holders of our common stock are entitled to receive dividends as may be declared from time to time by our Board of Directors out of funds legally available for the payment of dividends. Dividends declared per share by our Board of Directors for the first, second, third and fourth quarters of fiscal 2015 were $.04, $.04, $.04 and $.08, respectively. Dividends declared per share for the first, second, third and fourth quarters of fiscal 2014 were $.03, $.03, $.03 and $.04, respectively. There can be no assurance that we will pay cash dividends in any future period or that the level of cash dividends paid by us will remain constant.

Our senior credit facility contains provisions pertaining to the maintenance of a maximum funded debt to earnings before interest expense, income taxes, depreciation and amortization, or EBITDA, ratio and a minimum level of earnings before interest expense and income taxes to interest ratio as well as restrictions on the payment of dividends to stockholders. The facility limits the payment of dividends to stockholders to 25% of net income if our funded debt to EBITDA ratio is greater than 2.0 to 1. As of March 31 and May 30, 2015 we did not have any funded debt outstanding. More information regarding our senior credit facility can be found in Note 7 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K.

On January 29, 2015, our Board of Directors authorized a stock repurchase program. Under the stock repurchase program, up to $18,000 of our common stock is permitted to be repurchased by us from time to time either in the open market or through privately negotiated transactions.

| (1) | The historical prices for our common stock prior to May 2, 2014 is based on the high and low per share prices on the NYSE MKT exchange, where our common stock was then listed. On such date our common stock began trading on the NYSE. |

17

Table of Contents

| Item 6. |

GRAHAM CORPORATION — FIVE YEAR SUMMARY OF SELECTED FINANCIAL DATA

(Amounts in thousands, except per share data)

(for fiscal years ended March 31)

| 2015 | 2014 | 2013 | 2012 | 2011(1) | ||||||||||||||||

| Operations: |

||||||||||||||||||||

| Net sales |

$ | 135,169 | $ | 102,218 | $ | 104,973 | $ | 103,186 | $ | 74,235 | ||||||||||

| Gross profit |

41,804 | 31,812 | 31,822 | 32,635 | 21,851 | |||||||||||||||

| Gross profit percentage |

30.9 | % | 31.1 | % | 30.3 | % | 31.6 | % | 29.4 | % | ||||||||||

| Net income |

14,735 | 10,145 | 11,148 | 10,553 | 5,874 | |||||||||||||||

| Cash dividends |

2,026 | 1,308 | 899 | 793 | 790 | |||||||||||||||

| Common stock: |

||||||||||||||||||||

| Basic earnings from continuing operations per share |

$ | 1.46 | $ | 1.01 | $ | 1.11 | $ | 1.06 | $ | .59 | ||||||||||

| Diluted earnings from continuing operations per share |

1.45 | 1.00 | 1.11 | 1.06 | .59 | |||||||||||||||

| Stockholders’ equity per share |

11.50 | 10.49 | 9.30 | 8.20 | 7.47 | |||||||||||||||

| Dividends declared per share |

.20 | .13 | .09 | .08 | .08 | |||||||||||||||

| Market price range of common stock |

||||||||||||||||||||

| High |

35.35 | 41.94 | 24.80 | 26.30 | 24.58 | |||||||||||||||

| Low |

20.58 | 22.36 | 16.20 | 14.36 | 13.50 | |||||||||||||||

| Average common shares outstanding — diluted |

10,143 | 10,104 | 10,051 | 9,998 | 9,958 | |||||||||||||||

| Financial data at March 31: |

||||||||||||||||||||

| Cash and cash equivalents and investments |

$ | 60,271 | $ | 61,146 | $ | 51,692 | $ | 41,688 | $ | 43,083 | ||||||||||

| Working capital |

81,367 | 71,346 | 64,026 | 52,730 | 44,493 | |||||||||||||||

| Capital expenditures |

5,300 | 5,263 | 1,655 | 3,243 | 1,979 | |||||||||||||||

| Depreciation |

2,079 | 1,977 | 1,851 | 1,685 | 1,334 | |||||||||||||||

| Total assets |

154,654 | 141,634 | 126,733 | 114,977 | 118,071 | |||||||||||||||

| Long-term debt, including capital lease obligations |

98 | 136 | 127 | 203 | 116 | |||||||||||||||

| Stockholders’ equity |

116,551 | 105,908 | 92,995 | 81,620 | 73,655 | |||||||||||||||

| (1) | The financial data presented for fiscal 2011 includes the financial results of Energy Steel from the date of acquisition, which was December 14, 2010. |

18

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

(Amounts in thousands, except per share data)

Overview