Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - GRAHAM CORP | Financial_Report.xls |

| EX-31.1 - EX-31.1 - GRAHAM CORP | d347995dex311.htm |

| EX-32.1 - EX-32.1 - GRAHAM CORP | d347995dex321.htm |

| EX-31.2 - EX-31.2 - GRAHAM CORP | d347995dex312.htm |

| EX-23.1 - EX-23.1 - GRAHAM CORP | d347995dex231.htm |

| EX-21.1 - EX-21.1 - GRAHAM CORP | d347995dex211.htm |

| EX-10.26 - EX-10.26 - GRAHAM CORP | d347995dex1026.htm |

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2012

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 1-8462

GRAHAM CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 16-1194720 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) | |

| 20 Florence Avenue, Batavia, New York | 14020 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code 585-343-2216

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock (Par Value $.10) | NYSE MKT |

Securities registered pursuant to Section 12(g) of the Act:

Title of Class

Preferred Stock Purchase Rights

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ¨ |

Accelerated filer þ | Non-accelerated filer ¨ |

Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the voting stock held by non-affiliates of the registrant as of September 30, 2011, the last business day of the registrant’s most recently completed second fiscal quarter, was $154,745,644. The market value calculation was determined using the closing price of the registrant’s common stock on September 30, 2011, as reported on the NYSE MKT exchange. For purposes of the foregoing calculation only, all directors, officers and the Employee Stock Ownership Plan of the registrant have been deemed affiliates.

As of June 1, 2012, the registrant had outstanding 9,951,466 shares of common stock, $.10 par value, and 9,951,466 preferred stock purchase rights.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement, to be filed in connection with the registrant’s 2012 Annual Meeting of Stockholders to be held on July 26, 2012, are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this filing.

Table of Contents

GRAHAM CORPORATION

Annual Report on Form 10-K

Year Ended March 31, 2012

| PAGE | ||||||

| PART I |

||||||

| Item 1 |

1 | |||||

| Item 1A |

5 | |||||

| Item 1B |

14 | |||||

| Item 2 |

14 | |||||

| Item 3 |

14 | |||||

| Item 4 |

14 | |||||

| PART II |

||||||

| Item 5 |

14 | |||||

| Item 6 |

16 | |||||

| Item 7 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 17 | ||||

| Item 7A |

30 | |||||

| Item 8 |

32 | |||||

| Item 9 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 65 | ||||

| Item 9A |

65 | |||||

| Item 9B |

65 | |||||

| PART III |

||||||

| Item 10 |

66 | |||||

| Item 11 |

66 | |||||

| Item 12 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 66 | ||||

| Item 13 |

Certain Relationships and Related Transactions, and Director Independence |

66 | ||||

| Item 14 |

67 | |||||

| PART IV |

||||||

| Item 15 |

67 | |||||

| Note: | Portions of the registrant’s definitive Proxy Statement, to be issued in connection with the registrant’s 2012 Annual Meeting of Stockholders to be held on July 26, 2012, are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Annual Report on Form 10-K. |

Table of Contents

PART I

(Dollar amounts in thousands except per share data).

| Item 1. | Business |

Graham Corporation (“Graham,” the “Company,” “we,” “us” or “our”) designs, manufactures and sells custom-built vacuum and heat transfer equipment to customers worldwide. Our products include steam jet ejector vacuum systems, surface condensers for steam turbines, vacuum pumps and compressors, various types of heat exchangers, including helical coil heat exchangers marketed under the Heliflow® name, and plate and frame heat exchangers. Our products produce a vacuum, condense steam vapor or transfer heat, or perform a combination of these tasks. Our products are available in a variety of metals and non-metallic corrosion resistant materials.

We acquired Energy Steel & Supply Co. (“Energy Steel”) on December 14, 2010 as part of our strategy to diversify our products and broaden our offerings in the energy industry. Energy Steel is a nuclear code accredited fabrication and specialty machining company which provides products to the nuclear power generation industry, primarily in the U.S.

We were incorporated in Delaware in 1983 and are the successor to Graham Manufacturing Co., Inc., which was incorporated in New York in 1936. Our principal business location is in Batavia, New York. We maintain two wholly-owned subsidiaries, Graham Vacuum and Heat Transfer Technology (Suzhou) Co., Ltd., located in Suzhou, China and Energy Steel, located in Lapeer, Michigan. As of March 31, 2012, we had 346 full-time employees.

Our Products, Customers and Markets

Our products are used in a wide range of industrial process applications, including:

| • | Petroleum Refining |

| • | Chemical and Petrochemical Processing |

| — | fertilizer plants |

| — | ethylene, methanol and nitrogen producing plants |

| — | plastics, resins and fibers plants |

| — | petrochemical intermediate plants |

| — | coals-to-chemicals plants |

| — | gas-to-liquids plants |

| • | Power Generation /Alternative Energy |

| — | nuclear power generation |

| — | fossil fuel plants |

| — | biomass plants |

| — | cogeneration power plants |

| — | geothermal power plants |

| — | ethanol plants |

| • | Defense – U.S. Navy |

| — | propulsion systems for nuclear-powered aircraft carriers and other nuclear- powered vessels |

| • | Other |

| — | soap manufacturing plants |

1

Table of Contents

| — | air conditioning and water heating systems |

| — | food processing plants |

| — | pharmaceutical plants |

| — | liquefied natural gas production facilities |

Our principal customers are in the chemical, petrochemical, petroleum refining and power generating industries. They can be end users of our products in their manufacturing, refining and power generation processes, large engineering companies that build installations for companies in such industries, and/or the original equipment manufacturers, who combine our products with their equipment prior to its sale to end users.

Our products are sold by a team of sales engineers we employ directly and independent sales representatives located worldwide. There may be short periods of time, a fiscal year for example, where one customer may make up greater than 10% of our business. However, if this occurs in multiple years, it is usually not the same customer, or the same project, over the multi-year period.

Historically, 40% to 55% percent of our revenue has been generated from foreign sales. We believe that revenue from the sale of our products outside the U.S. will continue to account for a significant portion of our total revenue for the foreseeable future. We have invested significant resources in developing and maintaining our international sales operations and presence, and we intend to continue to make such investments in the future. As a result of the expansion of our presence in Asia, we expect that the Asian market will over time account for an increasing percentage of our revenue. However, partly offsetting the transition toward more international sales is our acquisition of Energy Steel, which primarily has domestic sales, as well as our increased focus on U.S. Navy opportunities. We expect our international sales to account for 40% to 50% of total revenue over the next few years.

A breakdown of our net sales by geographic area and product class for our fiscal years ended March 31, 2012, 2011 and 2010, which we refer to as fiscal 2012, fiscal 2011 and fiscal 2010, respectively, is contained in Note 13 to our consolidated financial statements included in Item 8 of Part II of this Annual Report on Form 10-K and such breakdown is incorporated into this Item 1 by reference. We refer to our fiscal year ending March 31, 2013 as fiscal 2013. Our backlog at March 31, 2012 was $94,934 compared with $91,096 at March 31, 2011.

Our Strengths

Our core strengths include the following:

| • | We have strong brand recognition. Over the past 75 years, we believe that we have built a reputation for top quality, reliable products and high standards of customer service. We have also established a large installed application base. As a result, the Graham name is well known not only by our existing customers, but also by many of our potential customers. We believe that the recognition of the Graham brand allows us to capitalize on market opportunities in both existing and potential markets. Moreover, our wholly-owned subsidiary, Energy Steel, has a 30-year history of providing products and support to its customers, especially the U.S. nuclear power industry, and has a recognized brand name in its markets. |

| • | We custom engineer and manufacture high quality products and systems that address the particular needs of our customers. With 75 years of engineering expertise, we believe that we are well respected for our knowledge in vacuum and heat transfer technologies. We maintain strict quality control and manufacturing standards in order to manufacture products of the highest quality. |

| • | We have a global presence. Our products are used worldwide, and we have sales representatives located in many countries throughout the world. |

| • | We have a strong reputation. We believe that we have a solid reputation of both placing customers first and standing behind our products. We believe that our relationships are strong with our existing customer base, as well as with our key suppliers. |

| • | We have a highly trained workforce. We maintain a long-tenured, skilled and flexible workforce. |

2

Table of Contents

| • | We have a strong balance sheet. We maintain significant cash and investments on hand, and no bank debt. Our defined benefit pension plan obligations are fully funded. |

| • | We have a high quality credit facility. Our credit facility provides us with a $25,000 borrowing capacity that is expandable at our option at any time to provide up to a total of $50,000 in borrowing capacity. |

Our Strategy

Our objectives are to capture more market share within the geographies and industries we serve, expand our geographic markets, grow our presence in the energy industry and continually improve our results of operations. Our strategy to accomplish our objectives includes:

| • | Capitalize on the strength of the Graham and Energy Steel brands in order to both win more business in our traditional markets and enter other markets. |

| • | Identify and consummate acquisition and organic growth opportunities where we believe our brand strength will provide us with the ability to expand and complement our core business. We intend to accomplish this objective by extending our existing product lines, moving into complementary product lines and expanding our global sales presence in order to further broaden our existing markets and reach additional markets. Our acquisition of Energy Steel was in furtherance of this portion of our business strategy. |

| • | Maximize the benefits from our acquisition of Energy Steel. We plan to expand our market penetration with Energy Steel’s current customer base in the domestic nuclear industry. We also intend to identify additional domestic and international opportunities to serve the nuclear industry. |

| • | Expand our market presence in the Navy’s Nuclear Propulsion Program. We plan to capitalize on our success in securing the nuclear carrier order by successfully executing our existing order for this program. We also plan to expand our market presence into additional defense-related programs, including nuclear submarine projects. |

| • | Invest in people and capital equipment to meet the long-term growth in demand for our products in the oil refining, petrochemical processing and power generating industries, especially in emerging markets. |

| • | Deliver highest quality products and solutions that enable our customers to achieve their operating objectives and that differentiate us from our competitors, and which, we believe, allow us to win new orders based on value. |

In order to effectively implement our strategies, we also believe that we must continually work to improve our company. These efforts include:

| • | Investing in engineering resources and technology in order to advance our vacuum and heat transfer technology market penetration. |

| • | Enhancing our engineering and manufacturing capacities, especially in connection with the design of our products, in order to more quickly respond to existing and future customer demand and to minimize underutilization of capacity. |

| • | Accelerating our ability to quickly and efficiently bid on available contracts by continuing to implement front-end bid automation and design processes. |

| • | Expanding our capabilities and penetrating the existing sales channel and customer base in the nuclear market. |

| • | Implementing and expanding upon our operational efficiencies through a flexible manufacturing flow model and other cost efficiencies. |

| • | Continuing to focus on improving quality to eliminate errors and rework, and reduce lead time. |

| • | Develop a cross trained, flexible workforce able to adjust to variable product demand by our customers. |

3

Table of Contents

Competition

Our business is highly competitive. The principal bases on which we compete include technology, price, performance, reputation, delivery, and quality. Our competitors in our primary markets include:

NORTH AMERICA

| Market |

Principle Competitors | |

| Refining vacuum distillation |

Gardner Denver, Inc. | |

| Chemicals/Petrochemicals |

Croll Reynolds Company, Inc.; Schutte Koerting; Gardner Denver, Inc. | |

| Turbomachinery Original Equipment Manufacturer (“OEM”) — refining, petrochemical |

Ambassador; KEMCO; SPX Heat Transfer | |

| Turbomachinery OEM — power and power producer |

Holtec; Thermal Engineering International (USA), Inc.; KEMCO; SPX Heat Transfer | |

| HVAC |

Alfa Laval AB; APV; Xylem; Ambassador | |

| Nuclear |

Dubose, Consolidated, Tioga, Nova, Joseph Oats, Energy & Process |

INTERNATIONAL

| Market |

Principle Competitors | |

| Refining vacuum distillation |

Gardner Denver, Inc.; GEA Wiegand GmbH; Edwards, Ltd.; Korting Hannover AG | |

| Chemicals/Petrochemicals |

Croll Reynolds Company, Inc.; Schutte Koerting; Gardner Denver, Inc.; GEA Wiegand GmbH; Korting Hannover AG; Edwards, Ltd. | |

| Turbomachinery OEM — refining, petrochemical |

DongHwa Entec Co., Ltd.; Hangzhou Turbine Equipment Co., Ltd.; Chem Process Systems, Mazda (India), Oeltechnik GmbH; KEMCO | |

| Turbomachinery OEM — power and power producer |

Holtec; Thermal Engineering International; KEMCO; SPX Heat Transfer, Chem Process Systems, Mazda (India) |

Intellectual Property

Our success depends in part on our proprietary technology. We rely on a combination of patent, copyright, trademark, trade secret laws and contractual confidentiality provisions to establish and protect our proprietary rights. We also depend heavily on the brand recognition of the Graham name in the marketplace.

Availability of Raw Materials

Historically, we have not been materially adversely impacted by the availability of raw materials.

Working Capital Practices

Our business does not require us to carry significant amounts of inventory or materials beyond what is needed for work in process. We do not provide rights to return goods, or payment terms to customers that we consider to be extended in the context of the industries we serve. However, we do provide for warranty claims.

4

Table of Contents

Environmental Matters

We believe that we are in material compliance with existing environmental laws and regulations. We do not anticipate that our compliance with federal, state and local laws regulating the discharge of material in the environment or otherwise pertaining to the protection of the environment will have a material adverse effect upon our capital expenditures, earnings or competitive position.

Seasonality

No material part of our business is seasonal in nature. However, our business is highly cyclical in nature as it depends on the willingness of our customers to invest in major capital projects.

Research and Development Activities

During fiscal 2012, fiscal 2011 and fiscal 2010, we spent $3,197, $2,576 and $3,824, respectively, on research and development activities related to new products and services, or the improvement of existing products and services.

Information Regarding International Sales

The sale of our products outside the U.S. has accounted for a significant portion of our total revenue during our last three fiscal years. Approximately 46%, 55% and 55% of our revenue in fiscal 2012, fiscal 2011 and fiscal 2010, respectively, resulted from foreign sales. Sales in Asia constituted approximately 17%, 22% and 33% of our revenue in fiscal 2012, fiscal 2011 and fiscal 2010, respectively. Sales in the Middle East constituted approximately 16%, 16% and 10% of our revenue in fiscal 2012, fiscal 2011 and fiscal 2010, respectively. Our foreign sales and operations are subject to numerous risks, as discussed under the heading “Risk Factors” in Item 1A of Part I and elsewhere in this Annual Report on Form 10-K.

Employees

As of March 31, 2012, we employed approximately 349 persons, including 3 part-time employees. We believe that our relationship with our employees is good.

Available Information

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Therefore, we file periodic reports, proxy statements and other information with the Securities and Exchange Commission. The SEC maintains an Internet website (located at www.sec.gov) that contains reports, proxy statements and other information for registrants that file electronically. Additionally, such reports may be read and copied at the Public Reference Room of the SEC at 100 F Street NE, Washington, D.C. 20549. Information regarding the SEC’s Public Reference Room can be obtained by calling 1-800-SEC-0330.

We maintain an Internet website located at www.graham-mfg.com. On our website, we provide a link to the SEC’s Internet website that contains the reports, proxy statements and other information we file electronically. We do not provide this information on our website because it is more cost effective for us to provide a link to the SEC’s website. Copies of all documents we file with the SEC are available in print for any stockholder who makes a request. Such requests should be made to our Corporate Secretary at our corporate headquarters. The other information found on our website is not part of this or any other report we file with, or furnish to, the SEC.

| Item 1A. | Risk Factors |

Our business and operations are subject to numerous risks, many of which are described below and elsewhere in this Annual Report on Form 10-K. If any of the events described below or elsewhere in this Annual Report on Form 10-K occur, our business and results of operations could be harmed. Additional risks and uncertainties that are not presently known to us, or which we currently deem to be immaterial, could also harm our business and results of operations.

5

Table of Contents

Risks related to our business

The industries in which we operate are cyclical, and downturns in such industries may adversely affect our operating results.

Historically, a substantial portion of our revenue has been derived from the sale of our products to companies in the chemical, petrochemical, petroleum refining and power generating industries and to the U.S. Department of Defense, or to firms that design and construct facilities for these industries. The core industries in which our products are used are, to varying degrees, cyclical and have historically experienced severe downturns. Although we believe there will be a long-term expansion of demand for our products in the petrochemical, petroleum refining and power generating industries, during 2008 we entered a sudden downturn in the demand for our products. Historically, previous cyclical downturns have lasted from one to several years. Although the downturn that began in 2008 appears to have begun to moderate and we have seen signals of economic recovery in our markets, we have no way to predict whether any recovery will be sustainable. A renewed downturn could force us to reduce our infrastructure, which would make it difficult for us to quickly recover in the subsequent up cycle. A sustained or renewed deterioration in any of the cyclical industries we serve would materially harm our business and operating results because our customers would not likely have the resources necessary to purchase our products, nor would they likely have the need to build additional facilities or improve existing facilities.

We serve markets that are capital intensive. Volatility and disruption of the capital and credit markets and adverse changes in the global economy may negatively impact our operating results. Such volatility and disruption may also negatively impact our ability to access additional financing if and when needed.

Although we believe that our long-term growth prospects remain strong, we also expect that the recent state of the capital and credit markets caused a slow-down in spending by our customers as many of them continue to evaluate their project plans. Although we believe that we are in the initial stages of an economic recovery, if adverse economic and credit conditions persist, return or worsen, we would likely experience decreased revenue from our operations attributable to decreases in the spending levels of our customers. Moreover, adverse economic and credit conditions might also have a negative adverse effect on our cash flows if customers demand that we accept smaller project deposits and less frequent progress payments. In addition, adverse economic and credit conditions could put downward pricing pressure on us. Any of the foregoing could have a material adverse effect on our business and results of operations.

Adverse conditions in the capital and credit markets could also have an adverse effect on our ability to obtain additional financing on commercially reasonable terms, or at all, should we determine such financing is desirable to maintain or expand our business.

The larger markets we serve are the petroleum refining and petrochemical industries which are both cyclical in nature and dependent on the price of crude oil and natural gas. As a result, volatility in the price of oil and natural gas may negatively impact our operating results.

Although we believe that the global consumption of crude oil and natural gas will increase over the course of the next 20 years and that such increased consumption will result in a need to continually increase global capacity, the price of crude oil and natural gas has been very volatile. Many of our products are purchased in connection with oil refinery construction, revamps and upgrades. During times of significant volatility in the market for crude oil or natural gas, our customers may refrain from placing orders until the market stabilizes. If our customers refrain from placing orders, we could experience decreased revenue from our operations attributable to decreases in the spending levels of our customers.

Our business is highly competitive. If we are unable to successfully implement our business strategy and compete against entities with greater resources than us, we risk losing market share to current and future competitors.

Some of our present and potential competitors may have substantially greater financial, marketing, technical or manufacturing resources. Our competitors may also be able to respond more quickly to new technologies or

6

Table of Contents

processes and changes in customer demands and they may be able to devote greater resources towards the development, promotion and sale of their products than we can. Competitors may have a cost advantage and be able to respond to customer needs at a lower pricing level. This may affect our ability to secure business and maintain our level of profitability. In addition, our current and potential competitors may make strategic acquisitions or establish cooperative relationships among themselves or with third parties that increase their ability to address the needs of our customers. Moreover, customer buying patterns can change if customers become more price sensitive and accepting of low cost suppliers. If we cannot compete successfully against current or future competitors, our business will be materially harmed.

The loss of, or significant reduction or delay in, purchases by our largest customers could reduce our revenue and adversely affect our results of operations.

A small number of customers has accounted for a substantial portion of our historical net sales. For example, sales to our top ten customers accounted for 43%, 46% and 44% of consolidated sales in fiscal 2012, 2011 and 2010, respectively. We expect that a limited number of customers will continue to represent a substantial portion of our sales for the foreseeable future. The loss of any of our major customers, a decrease or delay in orders or anticipated spending by such customers, or a delay in the production of existing orders could materially adversely affect our revenues and results of operations.

A large percentage of our sales occur outside of the U.S. As a result, we are subject to the economic, political, regulatory and other risks of international operations.

For fiscal 2012, 46% of our revenue was from customers located outside of the U.S. Moreover, we maintain a subsidiary and a facility in China. We believe that revenue from the sale of our products outside the U.S. will continue to account for a significant portion of our total revenue for the foreseeable future. We intend to continue to expand our international operations to the extent that suitable opportunities become available. Our foreign operations and sales could be adversely affected as a result of:

| • | nationalization of private enterprises and assets; |

| • | political or economic instability in certain countries and regions, such as the recent uprisings and instability throughout the Middle East; |

| • | differences in foreign laws, including increased difficulties in protecting intellectual property and uncertainty in enforcement of contract rights; |

| • | the possibility that foreign governments may adopt regulations or take other actions that could directly or indirectly harm our business and growth strategy; |

| • | credit risks; |

| • | currency fluctuations; |

| • | tariff and tax increases; |

| • | export and import restrictions and restrictive regulations of foreign governments; |

| • | shipping products during times of crisis or wars; |

| • | our failure to comply with U.S. laws regarding doing business in foreign jurisdictions, such as the Foreign Corrupt Practices Act; and |

| • | other factors inherent in foreign operations. |

The global economic recovery is likely to be led by emerging markets, which could result in lower profit margins and increased competition.

A global economic recovery is likely to be led by emerging markets. In the event that a global economic recovery is led by emerging markets, we could face increased competition from lower cost suppliers, which in turn could lead to lower profit margins on our products. In addition, if the global economic recovery is led by emerging markets, the pace of such recovery could be slower than the pace of prior recoveries. Customers in

7

Table of Contents

emerging markets may also place less emphasis on our high quality and brand name than do customers in the U.S. and certain of the other industrialized countries where we compete. If we are forced to compete for business with customers that place less emphasis on quality and brand recognition than our current customers or the pace of any economic recovery is slower than the pace of prior recoveries, our results of operations could be materially adversely impacted.

The operations of our Chinese subsidiary may be adversely affected by China’s evolving economic, political and social conditions.

We conduct our business in China primarily through a wholly-owned Chinese subsidiary. The results of operations and future prospects of our Chinese subsidiary are subject to evolving economic, political and social developments in China. In particular, the results of operations of our Chinese subsidiary may be adversely affected by, among other things, changes in China’s political, economic and social conditions, changes in policies of the Chinese government, changes in laws and regulations or in the interpretation of existing laws and regulations, changes in foreign exchange regulations, measures that may be introduced to control inflation, such as interest rate increases, and changes in the rates or methods of taxation. In addition, changes in demand could result from increased competition from local Chinese manufacturers who have cost advantages or who may be preferred suppliers. Also, Chinese commercial laws, regulations and interpretations applicable to non-Chinese owned market participants such as us are rapidly changing. These laws, regulations and interpretations could impose restrictions on our ownership or operations of our interests in China and have a material adverse effect on our business.

Intellectual property rights are difficult to enforce in China.

Chinese commercial law is relatively undeveloped compared with the commercial law in many of our other major markets and limited protection of intellectual property is available in China as a practical matter. Although we take precautions in the operations of our Chinese subsidiary to protect our intellectual property, any local design or manufacture of products that we undertake in China could subject us to an increased risk that unauthorized parties will be able to copy or otherwise obtain or use our intellectual property, which could harm our business. We may also have limited legal recourse in the event we encounter patent or trademark infringers.

Uncertainties with respect to the Chinese legal system may adversely affect the operations of our Chinese subsidiary.

Our Chinese subsidiary is subject to laws and regulations applicable to foreign investment in China. There are uncertainties regarding the interpretation and enforcement of laws, rules and policies in China. The Chinese legal system is based on written statutes, and prior court decisions have limited precedential value. Because many laws and regulations are relatively new and the Chinese legal system is still evolving, the interpretations of many laws, regulations and rules are not always uniform. Moreover, the relative inexperience of China’s judiciary in many cases creates additional uncertainty as to the outcome of any litigation, and the interpretation of statutes and regulations may be subject to government policies reflecting domestic political changes. Finally, enforcement of existing laws or contracts based on existing law may be uncertain and sporadic. For the preceding reasons, it may be difficult for us to obtain swift or equitable enforcement of laws ostensibly designed to protect companies like ours.

Changes in energy policy regulations could adversely affect our business.

Energy policy in the U.S. and in the other countries where we sell our products is evolving rapidly and we anticipate that energy policy will continue to be an important legislative priority in the jurisdictions where we sell our products. It is difficult, if not impossible, to predict the changes in energy policy that could occur. The elimination of, or a change in, any of the current rules and regulations in any of our markets could create a regulatory environment that makes our end users less likely to purchase our products, which would have a material adverse effect on our business.

8

Table of Contents

Efforts to reduce large U.S. federal budget deficits could result in government cutbacks in defense spending or in reduced incentives to pursue alternative energy projects, resulting in reduced demand for our products.

Our business strategy calls for us to continue to pursue defense-related projects as well as projects for end users in the alternative energy markets in the U.S. In recent years the U.S. federal government has incurred large budget deficits. In the event that the U.S. federal government defense spending is reduced or alternative energy related incentives are reduced or eliminated in an effort to reduce federal budget deficits, projects related to defense or alternative energy may become less plentiful. The impact of such reductions could have an adverse affect on our business growth opportunities.

Changes in tax policies and tax rates in the U.S. could result in adverse impacts for domestic manufacturing investments, resulting in reduced demand for our products.

Our business is dependent on significant manufacturing investment in the U.S. and the impact of changes to U.S. tax policy around investment and capital spending depreciation can reduce our customers’ willingness to invest in domestic capacity. The impact of such reductions could have a materially adverse affect on our business and operations.

Political and regulatory developments could make the utilization and growth of nuclear power as an energy source less desirable.

On March 11, 2011, a major earthquake and tsunami struck Japan and caused substantial damage to the nuclear generating units at the Fukushima Daiichi generating plant. The events in Japan have created uncertainties worldwide regarding, among other things, the desirability of operating existing nuclear power plants and building new or replacement nuclear power plants. Should public opinion or political pressure result in the closing of existing nuclear facilities or otherwise result in the failure of the nuclear power industry to grow, especially within the U.S., the business and growth prospects of Energy Steel could be materially adversely impacted.

In addition, the U.S. Nuclear Regulatory Commission, or NRC, continues to perform additional operational and safety reviews of nuclear facilities in the U.S. It is possible that the NRC could take action or impose regulations that adversely affects the demand for Energy Steel’s products and services, or otherwise delays or prohibits construction of new nuclear power generation facilities, even temporarily. If any such event were to occur, the business or operations of Energy Steel could be materially adversely impacted.

A decrease in supply or cost of the materials used in our products could harm our profit margins.

Our profitability depends in part on the price and continuity of supply of the materials used in the manufacture of our products, which in many instances are supplied by a limited number of sources. The availability and costs of these commodities may be influenced by, among other things, market forces of supply and demand, changes in world politics, labor relations between the producers and their work forces, export quotas, and inflation. Any restrictions on the supply of the materials used by us in manufacturing our products could significantly reduce our profit margins, which could harm our results of operations. Likewise, any efforts we may engage in to mitigate restrictions on the supply or price increases of materials by entering into long-term purchase agreements, by implementing productivity improvements or by passing cost increases on to our customers may not be successful. In addition, the ability of our suppliers to meet quality and delivery requirements can also impact our ability to meet commitments to customers. Future shortages or lower cost of raw materials could result in decreased sales as well as margins, or otherwise materially adversely affect our business.

If we are unable to effectively outsource a portion of our production during times when we are experiencing strong demand, our results of operations might be adversely affected. In addition, outsourcing may negatively affect our profit margins.

When we experience strong demand for our products, our business strategy calls for us to increase manufacturing capacity through outsourcing selected fabrication processes. We could experience difficulty in out-

9

Table of Contents

sourcing if customers demand that our products be manufactured by us exclusively. Furthermore, our ability to effectively outsource production could be adversely affected by worldwide manufacturing capacity. If we are unable to effectively outsource our production capacity when circumstances warrant, our results of operations could be materially adversely affected and we might not be able to deliver products to our customers on a timely basis. In addition, outsourcing to complete our products and services can increase the costs associated with such products and services. If we rely too heavily on outsourcing and are not able to increase our own production capacity during times when there is high demand for our products and services, our profit margins may be negatively impacted.

Our exposure to fixed-price contracts could negatively impact our results of operations.

A substantial portion of our sales is derived from fixed-price contracts, which may involve long-term fixed price commitments to customers. While we believe our contract management processes are strong, we nevertheless could experience difficulties in executing large contracts, including but not limited to, cost overruns, supplier failures and customer disputes. To the extent that any of our fixed-price contracts are delayed, our subcontractors fail to perform, contract counterparties successfully assert claims against us, the original cost estimates in these or other contracts prove to be inaccurate or the contracts do not permit us to pass increased costs on to our customers, our profitability from a particular contract may decrease or losses may be incurred, which, in turn, could adversely affect our results of operations.

We are subject to contract cancellations and delays by our customers, which may adversely affect our operating results.

The dollar amount of our backlog as of March 31, 2012 was $94,934. Our backlog can be significantly affected by the timing of large orders, and the amount of our backlog at March 31, 2012 is not necessarily indicative of future backlog levels or the rate at which our backlog will be recognized as sales. Although historically the amount of modifications and terminations of our orders has not been material compared with our total contract volume, customers can, and sometimes do, terminate or modify their orders. We cannot predict whether cancellations will occur or accelerate in the future. Although certain of our contracts in backlog may contain provisions allowing for us to assess cancellation charges to our customers to compensate us for costs incurred on cancelled contracts, cancellations of purchase orders or modifications made to existing contracts could substantially and materially reduce our backlog and, consequently, our future sales and results of operations. Moreover, delay of contract execution by our customers can result in volatility in our operating results.

Three orders in our backlog which include the U.S. Navy project and projects for new U.S. nuclear plants, are expected to account for approximately 15% of fiscal 2013 revenue. A delay or cancellation in any of these projects could have a material adverse effect on our results of operations.

The loss of any member of our management team and our inability to make up for such loss with a qualified replacement could harm our business.

Competition for qualified management and key technical personnel in our industry is intense. Moreover our technology is highly specialized and it may be difficult to replace the loss of any of our key technical personnel. Many of the companies with which we compete for management and key technical personnel have greater financial and other resources than we do or are located in geographic areas which may be considered by some to be more desirable places to live. If we are not able to retain any of our key management or technical personnel, our business could be materially harmed.

Our acquisition strategy may not be successful or may increase business risk.

The success of our acquisition strategy will depend, in part, on our ability to identify suitable companies or businesses to purchase and then successfully negotiate and close the acquisition. In addition, our ability to integrate acquisitions and realize the anticipated benefits from combining the acquisition with our historical business, operations and management. We cannot provide any assurances that we will be able to complete the acquisitions and then integrate the business and operations of those acquisitions without encountering difficulties,

10

Table of Contents

including unanticipated costs, difficulty in retaining customers and supplier or other relationships, failure to retain key employees, diversion of our management’s attention, failure to integrate information and accounting systems or establish and maintain proper internal control over financial reporting. Moreover, as part of the integration process, we must incorporate an acquisition’s existing business culture and compensation structure with our existing business. If we are not able to efficiently integrate an acquisition’s business and operations into our organization in a timely and efficient manner, or at all, the anticipated benefits of the acquisition may not be realized, or it may take longer to realize these benefits than we currently expect, either of which could materially harm our business or results of operations.

Our acquisition of Energy Steel might subject us to unknown liabilities.

Energy Steel may have unknown liabilities, including, but not limited to, product liability, workers’ compensation liability, tax liability and liability for improper business practices. Although we are entitled to indemnification from the seller of Energy Steel for these and other matters, we could experience difficulty enforcing those obligations or we could incur material liabilities for the past activities of Energy Steel. Such liabilities and related legal or other costs could materially harm our business or results of operations.

Our intangible assets substantially increased as a result of our acquisition of Energy Steel. Should a portion of these intangible assets be impaired, results of operations could be materially adversely affected.

Our balance sheet includes intangible assets, including goodwill and other separately identifiable intangible assets, primarily as a result of our acquisition of Energy Steel. The value of these intangible assets may increase in the future if we complete additional acquisitions as part of our overall business strategy. We are required to review our intangible assets for impairment on an annual basis, or more frequently if certain indicators of permanent impairment arise. Factors that could indicate that our intangible assets are impaired could include, among other things, a decline in our stock price and market capitalization, lower than projected operating results and cash flows, and slower than expected growth rates in our markets. If a portion of our intangible assets becomes impaired as a result of such a review, the impaired portion of such assets would have to be written-off during that period. Such a write-off could have a material adverse effect on our results of operations.

If we are unable to make necessary capital investments or respond to pricing pressures, our business may be harmed.

In order to remain competitive, we need to invest continuously in manufacturing, customer service and support, research and development and marketing. From time to time we also have to adjust the prices of our products to remain competitive. We may not have available sufficient financial or other resources to continue to make investments, necessary to lower our production costs and help us maintain our competitive position, which would materially harm our business.

If we fail to introduce enhancements to our existing products or to keep abreast of technological changes in our markets, our business and results of operations could be adversely affected.

Although technologies in the vacuum and heat transfer areas are well established, we believe our future success depends, in part, on our ability to enhance our existing products and develop new products in order to continue to meet customer demands. Our failure to introduce new or enhanced products on a timely and cost-competitive basis, or the development of processes that make our existing technologies or products obsolete, could materially harm our business and results of operations.

If third parties infringe upon our intellectual property or if we were to infringe upon the intellectual property of third parties, we may expend significant resources enforcing or defending our rights or suffer competitive injury.

Our success depends in part on our proprietary technology. We rely on a combination of patent, copyright, trademark, trade secret laws and confidentiality provisions to establish and protect our proprietary rights. If we fail to successfully enforce our intellectual property rights, our competitive position could suffer. We may also be

11

Table of Contents

required to spend significant resources to monitor and police our intellectual property rights. Similarly, if we were found to have unintentionally infringed on the intellectual property rights of others, our competitive position could suffer. Furthermore, other companies may develop technologies that are similar or superior to our technologies, duplicate or reverse engineer our technologies or design around our patents. Any of the foregoing could have a material adverse effect on our business and results of operations.

In some instances, litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties that our products infringe their intellectual property rights. Any litigation or claims brought by or against us, whether with or without merit, could result in substantial costs to us and divert the attention of our management, which could materially harm our business and results of operations. In addition, any intellectual property litigation or claims against us could result in the loss or compromise of our intellectual property and proprietary rights, subject us to significant liabilities, require us to seek licenses on unfavorable terms, prevent us from manufacturing or selling certain products or require us to redesign certain products, any of which could materially harm our business and results of operations.

If we become subject to product liability, warranty or other claims, our results of operations and financial condition could be adversely affected.

The manufacture and sale of our products exposes us to potential product liability claims, including those that may arise from failure to meet product specifications, misuse or malfunction of, design flaws in our products, or use of our products with systems not manufactured or sold by us. For example, our equipment is installed in facilities that operate dangerous processes and the misapplication, improper installation or failure of our equipment may result in exposure to potentially hazardous substances, personal injury or property damage.

Provisions contained in our contracts with customers that attempt to limit our damages may not be enforceable or may fail to protect us from liability for damages and we may not negotiate such contractual limitations of liability in certain circumstances. Although we carry liability insurance that we believe is adequate to protect us from product liability claims based on our historical experience, our insurance may not cover all liabilities nor may our historical experience reflect any liabilities we may face in the future. We also may not be able to continue to maintain such insurance at a reasonable cost or on reasonable terms, or at all. Any material liability not covered by provisions in our contracts or by insurance could have a material adverse effect on our business and financial condition.

Furthermore, if a customer suffers damage as a result of an event related to one of our products, even if we are not at fault, they may reduce their business with us. We may also incur significant warranty claims, which are not covered by insurance. In the event a customer ceases doing business with us as a result of a product malfunction or defect, perceived or actual, or if we incur significant warranty costs in the future, there could be a material adverse effect on our business and results of operations.

We are subject to foreign currency fluctuations which may adversely affect our operating results.

We are exposed to the risk of currency fluctuations between the U.S. dollar and the currencies of the countries in which we sell our products to the extent that such sales are not based on U.S. dollars. Currency movements can affect sales in several ways, the foremost being our ability to compete for orders against foreign competitors that base their prices on relatively weaker currencies. Business lost due to competition for orders against competitors using a relatively weaker currency cannot be quantified. In addition, cash can be adversely impacted by the conversion of sales made by us in a foreign currency to U.S. dollars. While we may enter into currency exchange rate hedges from time to time to mitigate these types of fluctuations, we cannot remove all fluctuations or hedge all exposures and our earnings are impacted by changes in currency exchange rates. In addition, if the counter-parties to such exchange contracts do not fulfill their obligations to deliver the contractual foreign currencies, we could be at risk for fluctuations, if any, required to settle the obligation. At March 31, 2012, we held no forward foreign currency exchange contracts.

12

Table of Contents

We face potential liability from asbestos exposure and similar claims.

We are a defendant in a number of lawsuits alleging illnesses from exposure to asbestos or asbestos-containing products and seeking unspecified compensatory and punitive damages. We cannot predict with certainty the outcome of these lawsuits or whether we could become subject to any similar, related or additional lawsuits in the future. In addition, because some of our products are used in systems that handle toxic or hazardous substances, any failure or alleged failure of our products in the future could result in litigation against us. For example, a claim could be made under various regulations for the adverse consequences of environmental contamination. Any litigation brought against us, whether with or without merit, could result in substantial costs to us as well as divert the attention of our management, which could materially harm our business and results of operations.

Risks related to the ownership of our common stock

Provisions contained in our certificate of incorporation and bylaws could impair or delay stockholders’ ability to change our management and could discourage takeover transactions that our stockholders might consider to be in their best interests.

Provisions of our certificate of incorporation and bylaws could impede attempts by our stockholders to remove or replace our management and could discourage others from initiating a potential merger, takeover or other change of control transaction, including a potential transaction at a premium over the market price of our common stock, that our stockholders might consider to be in their best interests. Such provisions include:

| • | We could issue shares of preferred stock with terms adverse to our common stock. Under our certificate of incorporation, our Board of Directors is authorized to issue shares of preferred stock and to determine the rights, preferences and privileges of such shares without obtaining any further approval from the holders of our common stock. We could issue shares of preferred stock with voting and conversion rights that adversely affect the voting power of the holders of our common stock, or that have the effect of delaying or preventing a change in control of our company. |

| • | Only a minority of our directors may be elected in a given year. Our bylaws provide for a classified Board of Directors, with only approximately one-third of our Board elected each year. This provision makes it more difficult to effect a change of control because at least two annual stockholder meetings are necessary to replace a majority of our directors. |

| • | Our bylaws contain advance notice requirements. Our bylaws also provide that any stockholder who wishes to bring business before an annual meeting of our stockholders or to nominate candidates for election as directors at an annual meeting of our stockholders must deliver advance notice of their proposals to us before the meeting. Such advance notice provisions may have the effect of making it more difficult to introduce business at stockholder meetings or nominate candidates for election as director. |

| • | Our certificate of incorporation requires supermajority voting to approve a change of control transaction. Seventy-five percent of our outstanding shares entitled to vote are required to approve any merger, consolidation, sale of all or substantially all of our assets and similar transactions if the other party to such transaction owns 5% or more of our shares entitled to vote. In addition, a majority of the shares entitled to vote not owned by such 5% or greater stockholder are also required to approve any such transaction. |

| • | Amendments to our certificate of incorporation require supermajority voting. Our certificate of incorporation contains provisions that make its amendment require the affirmative vote of both 75% of our outstanding shares entitled to vote and a majority of the shares entitled to vote not owned by any person who may hold 50% or more of our shares unless the proposed amendment was previously recommended to our stockholders by an affirmative vote of 75% of our Board. This provision makes it more difficult to implement a change to our certificate of incorporation that stockholders might otherwise consider to be in their best interests without approval of our Board. |

13

Table of Contents

| • | Amendments to our bylaws require supermajority voting. Although our Board of Directors is permitted to amend our bylaws at any time, our stockholders may only amend our bylaws upon the affirmative vote of both 75% of our outstanding shares entitled to vote and a majority of the shares entitled to vote not owned by any person who owns 50% or more of our shares. This provision makes it more difficult for our stockholders to implement a change they may consider to be in their best interests without approval of our Board. |

| Item 1B. | Unresolved Staff Comments |

Not applicable.

| Item 2. | Properties |

Our corporate headquarters, located at 20 Florence Avenue, Batavia, New York, consists of a 45,000 square foot building. Our manufacturing facilities, also located in Batavia, consist of approximately 33 acres and contain about 216,000 square feet in several buildings, including 162,000 square feet in manufacturing facilities, 48,000 square feet for warehousing and a 6,000 square-foot building for product research and development. We also lease approximately 15,000 square feet of office space and 45,000 square feet of manufacturing facilities for our subsidiary, Energy Steel, located in Lapeer, Michigan. Additionally, we lease a U.S. sales office in Houston, Texas and our Chinese subsidiary leases a sales and engineering office in Suzhou, China.

We believe that our properties are generally in good condition, are well maintained, and are suitable and adequate to carry on our business.

| Item 3. | Legal Proceedings |

The information required by this Item 3 is contained in Note 15 to our consolidated financial statements included in Item 8 of Part II of this Annual Report on Form 10-K and is incorporated herein by reference.

| Item 4. | Mine Safety Disclosures |

Not applicable.

PART II

(Amounts in thousands, except per share data)

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is traded on the NYSE MKT exchange under the symbol “GHM”. As of June 1, 2012, there were 9,951 shares of our common stock outstanding that were held by approximately 143 stockholders of record.

14

Table of Contents

The following table shows the high and low per share prices of our common stock for the periods indicated, as reported by the NYSE MKT.

| High | Low | |||||||

| Fiscal year 2012 |

||||||||

| First quarter |

$ | 26.30 | $ | 17.74 | ||||

| Second quarter |

21.24 | 15.00 | ||||||

| Third quarter |

24.98 | 14.36 | ||||||

| Fourth quarter |

25.04 | 19.26 | ||||||

| Fiscal year 2011 |

||||||||

| First quarter |

$ | 19.60 | $ | 13.50 | ||||

| Second quarter |

17.99 | 13.52 | ||||||

| Third quarter |

21.00 | 14.75 | ||||||

| Fourth quarter |

24.58 | 19.08 | ||||||

Subject to the rights of any preferred stock we may then have outstanding, the holders of our common stock are entitled to receive dividends as may be declared from time to time by our Board of Directors out of funds legally available for the payment of dividends. Dividends declared per share by our Board of Directors for each of the four quarters of each of fiscal 2012 and fiscal 2011 were $.02. There can be no assurance that we will pay cash dividends in any future period or that the level of cash dividends paid by us will remain constant.

Our senior credit facility contains provisions pertaining to the maintenance of a maximum funded debt to earnings before interest expense, income taxes, depreciation and amortization, or EBITDA, ratio and a minimum level of earnings before interest expense and income taxes to interest ratio as well as restrictions on the payment of dividends to stockholders. The facility limits the payment of dividends to stockholders to 25% of net income if our maximum funded debt to EBITDA ratio is greater than 2.0 to 1. As of March 31 and June 1, we did not have any funded debt outstanding. More information regarding our senior credit facility can be found in Note 8 to the Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K.

We maintain a stock repurchase program that permits us to repurchase up to 1,000 shares of our common stock either in the open market or through privately negotiated transactions. The stock repurchase program terminates at the earlier of the expiration of the program on July 27, 2012, when all 1,000 shares authorized thereunder are repurchased or when the Board of Directors otherwise determines to terminate the program. We intend to use cash on hand to fund any stock repurchases under the program. As of March 31, 2012, 623 shares of our common stock remain available for repurchase under the stock repurchase program.

15

Table of Contents

| Item 6. | Selected Financial Data |

GRAHAM CORPORATION — FIVE YEAR SUMMARY OF SELECTED FINANCIAL DATA

(Amounts in thousands, except per share data)

(for fiscal years ended March 31)

| 2012 | 2011(2) | 2010 | 2009 | 2008(1) | ||||||||||||||||

| Operations: |

||||||||||||||||||||

| Net sales |

$ | 103,186 | $ | 74,235 | $ | 62,189 | $ | 101,111 | $ | 86,428 | ||||||||||

| Gross profit |

32,635 | 21,851 | 22,231 | 41,712 | 34,162 | |||||||||||||||

| Gross profit percentage |

31.6 | % | 29.4 | % | 35.7 | % | 41.3 | % | 39.5 | % | ||||||||||

| Net income |

10,553 | 5,874 | 6,361 | 17,467 | 15,034 | |||||||||||||||

| Cash dividends |

793 | 790 | 788 | 754 | 493 | |||||||||||||||

| Common stock: |

||||||||||||||||||||

| Basic earnings from continuing operations per share |

$ | 1.06 | $ | .59 | $ | .64 | $ | 1.72 | $ | 1.52 | ||||||||||

| Diluted earnings from continuing operations per share |

1.06 | .59 | .64 | 1.71 | 1.49 | |||||||||||||||

| Stockholders’ equity per share |

8.20 | 7.47 | 7.01 | 6.21 | 4.86 | |||||||||||||||

| Dividends declared per share |

.08 | .08 | .08 | .075 | .05 | |||||||||||||||

| Market price range of common stock |

||||||||||||||||||||

| High |

26.30 | 24.58 | 21.84 | 54.91 | 30.48 | |||||||||||||||

| Low |

14.36 | 13.50 | 8.70 | 6.85 | 6.30 | |||||||||||||||

| Average common shares outstanding — diluted |

9,998 | 9,958 | 9,937 | 10,195 | 10,085 | |||||||||||||||

| Financial data at March 31: |

||||||||||||||||||||

| Cash and cash equivalents and investments |

$ | 41,688 | $ | 43,083 | $ | 74,590 | $ | 46,209 | $ | 36,793 | ||||||||||

| Working capital |

52,730 | 44,493 | 56,704 | 49,547 | 36,998 | |||||||||||||||

| Capital expenditures |

3,243 | 1,979 | 1,003 | 1,492 | 1,027 | |||||||||||||||

| Depreciation |

1,685 | 1,334 | 1,107 | 993 | 862 | |||||||||||||||

| Total assets |

114,977 | 118,071 | 108,979 | 86,924 | 70,711 | |||||||||||||||

| Long-term debt, including capital lease obligations |

203 | 116 | 144 | 31 | 36 | |||||||||||||||

| Stockholders’ equity |

81,620 | 73,655 | 69,074 | 61,111 | 48,536 | |||||||||||||||

| (1) | Per share data has been adjusted to reflect a two-for-one stock split declared on July 31, 2008. The stock split was paid in the form of a dividend. |

| (2) | The financial data presented for fiscal 2011 includes the financial results of Energy Steel from the date of acquisition, which was December 14, 2010. See Note 2 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K. |

16

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

(Amounts in thousands, except per share data)

Overview

We are a global designer and manufacturer of custom-engineered ejectors, vacuum systems, condensers, liquid ring pump packages and heat exchangers to the refining and petrochemical industries, and a nuclear code accredited supplier of components and raw materials to the nuclear power generating market. Our equipment is used in critical applications in the petrochemical, oil refining and electric power generation industries, including nuclear, cogeneration and geothermal plants. Our equipment can also be found in alternative energy, including ethanol, biodiesel and coal and gas-to-liquids, as well as other diverse applications, such as metal refining, pulp and paper processing, shipbuilding, (the nuclear propulsion program of the U.S. Navy), water heating, refrigeration, desalination, soap manufacturing, food processing, pharmaceuticals, and heating, ventilating and air conditioning.

Our corporate offices are located in Batavia, New York and we have production facilities in both Batavia, New York and at our wholly-owned subsidiary, Energy Steel & Supply Co., located in Lapeer, Michigan. We also have a wholly-owned foreign subsidiary, Graham Vacuum and Heat Transfer Technology (Suzhou) Co., Ltd., located in Suzhou, China, which supports sales orders from China and provides engineering support and supervision of subcontracted fabrication.

On December 14, 2010, we acquired Energy Steel to advance our strategy to diversify our products and broaden our offerings to the energy industry. This transaction was accounted for under the acquisition method of accounting. Accordingly, the results of Energy Steel were included in our consolidated financial statements and comparisons to our prior fiscal year will be enhanced by the inclusion of Energy Steel in this fiscal year’s results.

Highlights

Highlights for fiscal 2012, include:

| • | Net income and income per diluted share for fiscal 2012, were $10,553 and $1.06 compared with net income and income per diluted share of $5,874 and $0.59 for fiscal 2011. |

| • | Net sales for fiscal 2012 were a record $103,186, up 39% compared with $74,235 for fiscal 2011. |

| • | Orders received in fiscal 2012 of $106,709 were up 69% compared with fiscal 2011, when orders were $63,222. |

| • | Backlog on March 31, 2012 was a record $94,934, up 4% from backlog of $91,096 on March 31, 2011. |

| • | Gross profit and operating margins for fiscal 2012 were 31.6% and 16.6% compared with 29.4% and 11.8%, respectively, for fiscal 2011. |

| • | Cash and short-term investments at March 31, 2012 were $41,688 compared with $43,083 as of March 31, 2011, down 3%. |

| • | At fiscal year end, we had a solid balance sheet that was free of bank debt and provided financial flexibility. |

Forward-Looking Statements

This report and other documents we file with the Securities and Exchange Commission include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

These statements involve known and unknown risks, uncertainties and other factors that may cause actual results to be materially different from any future results implied by the forward-looking statements. Such factors include, but are not limited to, the risks and uncertainties identified by us under the heading “Risk Factors” in Item 1A and elsewhere in this Annual Report on Form 10-K.

17

Table of Contents

Forward-looking statements may also include, but are not limited to, statements about:

| • | the current and future economic environments affecting us and the markets we serve; |

| • | expectations regarding investments in new projects by our customers; |

| • | sources of revenue and anticipated revenue, including the contribution from the growth of new products, services and markets; |

| • | plans for future products and services and for enhancements to existing products and services; |

| • | our operations in foreign countries; |

| • | our ability to continue to pursue our acquisition and growth strategy; |

| • | our ability to expand nuclear power work into new markets; |

| • | our ability to successfully execute our existing contracts; |

| • | estimates regarding our liquidity and capital requirements; |

| • | timing of conversion of backlog to sales; |

| • | our ability to attract or retain customers; |

| • | the outcome of any existing or future litigation; and |

| • | our ability to increase our productivity and capacity. |

Forward-looking statements are usually accompanied by words such as “anticipate,” “believe,” “estimate,” “may,” “might”, “intend,” “appear”, “expect” and similar expressions. Actual results could differ materially from historical results or those implied by the forward-looking statements contained in this report.

Undue reliance should not be placed on our forward-looking statements. Except as required by law, we undertake no obligation to update or announce any revisions to forward-looking statements contained in this report, whether as a result of new information, future events or otherwise.

Fiscal 2013 and the Near-Term Market Conditions

During fiscal 2012, bidding activity remained active. We believe the business environment is continuing to improve and that our customers are more inclined to procure the equipment needed for their projects. This supports our belief that our oil refining, petrochemical and related markets are in the early stages of a business recovery. While there continues to be uncertainty as to whether a sustained global economic recovery is occurring, we believe current signs (such as order activity during our fourth quarter of fiscal 2012) continue to be more positive than in the past few years.

Near-term demand trends that we believe are affecting our customers’ investments include:

| • | As the world recovers from the global recession, many emerging economies continue to have relatively strong economic growth. This expansion is driving growing energy requirements and the need for more refined petroleum products. Although uncertainty in the capital and sovereign debt markets continues, there has been some improved access to capital, which has resulted in the release of certain previously stalled projects. |

| • | The expansion of the economies of oil producing Middle Eastern countries, their desire to extract greater value from their oil and gas resources, and the continued global growth in demand for oil and refined products has renewed investment activity in that region. We do not believe that the ongoing political unrest in the Middle East has impacted our business. Moreover, the planned timeline of refinery projects in the major Middle Eastern countries is encouraging. |

| • | Asian countries, specifically China and India, are experiencing renewed demand for refined petroleum products such as gasoline. This renewed demand is driving increased investment in petrochemical and |

18

Table of Contents

| refining projects. Although economic growth in Asia appears to be moderating to a lower level, we believe that it remains a fast growing area and Chinese and Indian investments in refining, petrochemical and energy facilities appear to continue to be strong. |

| • | South America, specifically Brazil, Venezuela and Colombia, is seeing increased refining and petrochemical investments that are driven by their expanding economies and increased local demand for gasoline and other products that are made from oil as the feedstock. |

| • | The U.S. refining market has recently exhibited improvement, including demand in orders of short cycle and spare parts. Historically, these types of orders have suggested a recovery, as delayed spending is released. We expect that the U.S. refining markets will not return to the levels experienced during the last up cycle, but that such markets will improve compared with its levels over the past few years. We also expect that the U.S. refining markets will continue to be an important aspect of our business. |

| • | We are beginning to see renewed signs of planned investments in the U.S. to convert greater percentages of crude oil to transportation fuels, such as revamping distillation columns to extract residual higher-value components from the low-value waste stream. We are also seeing renewed investment to expand the flexibility of facilities to allow them to utilize multiple feed stocks. |

| • | Investments, including foreign investments, in North American oil sands projects have recently increased, especially for extraction projects in Alberta. Such investments suggest that downstream spending involving our equipment might increase in the next one to three years. |

| • | The recent dramatic change in natural gas costs in the U.S. has led to a revival in the U.S. petrochemical market and a recent interest toward potential major investment. There are numerous projects in planning or initial engineering phases for the construction of new petrochemical producing facilities, including ethylene, ammonia and urea facilities. We historically have had strong market share within these facilities. Proposed ethylene capacity expansion and re-opening of mothballed facilities, in the U.S., as well as downstream products, are being discussed by petrochemical producers for the first time in well over a decade. Lower natural gas costs is a relatively recent phenomena, having occurred over the past three years and is driven by technology advancements in drilling, creating a significant increase in supply. This has made the U.S. production of raw material for ethylene, ethane (which is a side product of natural gas production) globally competitive with naphtha (the alternative feedstock for ethylene used in most of the world). We believe investment in U.S. petrochemical markets could be significant. |

| • | Although investment in new nuclear power capacity in the U.S. and internationally may become subject to increased uncertainty due to political and social pressures, which were augmented by the tragic earthquake and tsunami that occurred in Japan in March 2011. The need for additional safety and back up redundancies at the 104 existing domestic nuclear plants could increase demand for Energy Steel’s products in the near-term. |

| • | Investments in existing U.S. nuclear plants to extend their operating life and add incremental capacity are expected to continue. |

| • | Investment in new U.S. nuclear reactor projects planned for the Summer (South Carolina) and Vogtle (Georgia) facilities suggest continued growth in the domestic nuclear market, although such growth may be slowed by the perceptions related to the Fukajima accident in Japan. |

We expect that the consequences of these near-term trends, and specifically projected expansion in petrochemical and oil refining that will most likely occur outside of North America, primarily in the growing Asian and South American markets, will result in more pressure on our pricing and gross margins, as these markets historically provided lower margins than North American refining markets. A counter to margin pressure from international markets may come from investments in new petrochemical capacity built in North America and the timing of such investments.

Because of continued global economic and financial uncertainty and the risk associated with growth in emerging economies, we also expect that we will have continued volatility in our order pattern. We continue to

19

Table of Contents

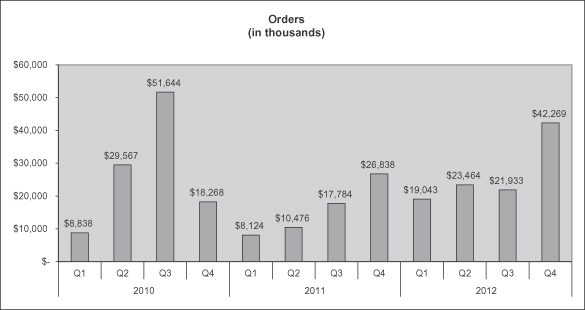

expect our new order levels to remain volatile, resulting in both strong and weak quarters. As the chart below indicates, quarterly orders can vary significantly.

We believe that looking at our order level in any one quarter does not provide an accurate indication of our future expectations or performance. Rather, we believe that looking at our orders and backlog over a one to two year period provides a better measure of our business. In the near future we expect to see smaller value projects than what we had seen during the last expansion cycle. This will require more orders for us to achieve a similar revenue level and will adversely impact our ability to realize margin gains through volume leverage. Our quarterly order levels for fiscal 2012, fiscal 2011 and fiscal 2010, respectively, are set forth in the table below.

Mix Shift: Expected Stronger International Growth in Refining and Chemical Processing with Domestic Growth in Nuclear Power and U.S. Navy Projects