Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | ||

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended March 31, 2015

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission file number 001-32417

Education Realty Trust, Inc.

Education Realty Operating Partnership, LP

(Exact Name of Registrant as Specified in Its Charter)

Maryland | 20-1352180 | |

Delaware | 20-1352332 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | |

999 South Shady Grove Road, Suite 600 Memphis, Tennessee | 38120 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s Telephone Number, Including Area Code (901) 259-2500

Not Applicable

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Education Realty Trust, Inc. Yes x No o

Education Realty Operating Partnership, LP Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Education Realty Trust, Inc. Yes x No o

Education Realty Operating Partnership, LP Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Education Realty Trust, Inc.

Large accelerated filer x | Accelerated filer o | |

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |

Education Realty Operating Partnership, LP

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Education Realty Trust, Inc. Yes o No x

Education Realty Operating Partnership, LP Yes o No x

As of May 4, 2015, Education Realty Trust, Inc. had 48,353,247 shares of common stock outstanding.

EXPLANATORY NOTE

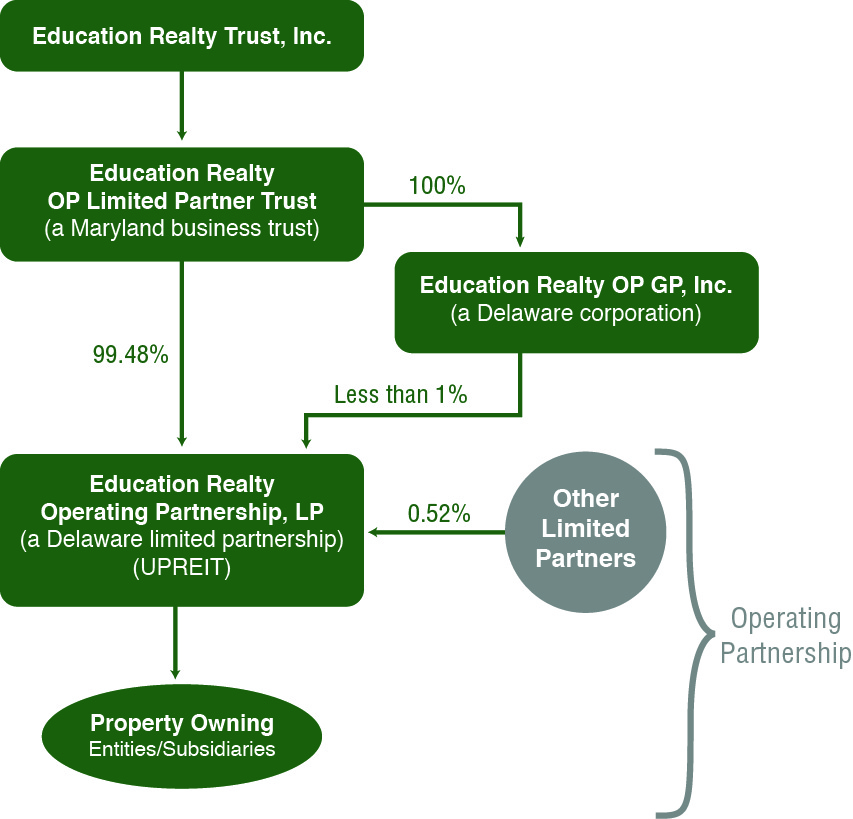

This report combines the reports on Form 10-Q for the quarterly period ended March 31, 2015 of Education Realty Trust, Inc. and Education Realty Operating Partnership, LP. Unless stated otherwise or the context otherwise requires, references to “EdR” mean only Education Realty Trust, Inc., a Maryland corporation, and references to "EROP" mean only Education Realty Operating Partnership, LP, a Delaware limited partnership. References to the "Trust," "we," "us," or "our" mean collectively EdR, EROP and those entities/subsidiaries owned or controlled by EdR and/or EROP. References to the "Operating Partnership" mean collectively EROP and those entities/subsidiaries owned or controlled by EROP. The following chart illustrates our corporate structure:

The general partner of EROP is Education Realty OP GP, Inc. (the “OP GP”), an entity that is indirectly wholly-owned by EdR. As of March 31, 2015, OP GP held an ownership interest in EROP of less than 1%. The limited partners of EROP are Education Realty OP Limited Partner Trust, a wholly-owned subsidiary of EdR, and other limited partners consisting of current and former members of management. The OP GP, as the sole general partner of EROP, has the responsibility and discretion in the management and control of the Operating Partnership, and the limited partners of EROP, in such capacity, have no authority to transact business for, or participate in the management activities of the Operating Partnership. Management operates EdR and the Operating Partnership as one business. The management of EdR consists of the same members as the management of the Operating Partnership.

The Trust is structured as an umbrella partnership real estate investment trust (“UPREIT”) and EdR contributes all net proceeds from its various equity offerings to the Operating Partnership. In return for those contributions, EdR receives an equal number of partnership units of EROP (the “OP Units”). Contributions of properties to the Trust can be structured as tax-deferred transactions through the issuance of OP Units. Holders of OP Units may tender their OP Units for redemption by the Operating Partnership in exchange for cash equal to the market price of EdR's common stock at the time of redemption or, at EdR's option, for shares of EdR's common stock. Pursuant to the partnership agreement of EROP, the number of shares to be issued upon the redemption of OP Units is equal to the number of OP Units being redeemed. Additionally, for every one share of common stock offered and sold by EdR for cash, EdR must contribute the net proceeds to EROP and, in return, EROP will issue one OP Unit to EdR.

The Trust believes that combining the quarterly reports on Form 10-Q of EdR and the Operating Partnership into this single report provides the following benefits:

• | enhances investors’ understanding of the Trust by enabling investors to view the business of EdR and the Operating Partnership as a whole in the same manner as management views and operates the business; |

• | eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure applies to both EdR and the Operating Partnership; and |

• | creates time and cost efficiencies through the preparation of one combined report instead of two separate reports. |

EdR consolidates the Operating Partnership for financial reporting purposes, and EdR essentially has no assets or liabilities other than its investment in the Operating Partnership. Therefore, the assets and liabilities of EdR and the Operating Partnership are the same on their respective financial statements. However, the Trust believes it is important to understand the few differences between EdR and the Operating Partnership in the context of how the entities operate as a consolidated company. All of the Trust's property ownership, development and related business operations are conducted through the Operating Partnership. EdR also issues public equity from time to time and guarantees certain debt of EROP. EdR does not have any indebtedness, as all debt is incurred by the Operating Partnership. The Operating Partnership holds all of the assets of the Trust, including the Trust’s ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for the net proceeds from EdR’s equity offerings, which are contributed to the capital of EROP in exchange for OP Units on the basis of one share of common stock for one OP Unit, the Operating Partnership generates all remaining capital required by the Trust's business, including as a result of the incurrence of indebtedness. These sources include, but are not limited to, the Operating Partnership’s working capital, net cash provided by operating activities, borrowings under its credit facilities, proceeds from mortgage indebtedness and debt issuances, and proceeds received from the disposition of certain properties. Noncontrolling interests, stockholders’ equity, and partners’ capital are the main areas of difference between the condensed consolidated financial statements of the Trust and those of the Operating Partnership. The noncontrolling interests in the Operating Partnership’s financial statements consist of the interests of unaffiliated partners in various consolidated joint ventures. The noncontrolling interests in the Trust's financial statements include the same noncontrolling interests at the Operating Partnership level. The differences between stockholders’ equity and partners’ capital result from differences in the type of equity issued by EdR and the Operating Partnership.

To help investors understand the significant differences between the Trust and the Operating Partnership, this report provides separate condensed consolidated financial statements for the Trust and the Operating Partnership. A single set of consolidated notes to such financial statements is presented that includes separate discussions for the Trust and the Operating Partnership when applicable (for example, noncontrolling interests, stockholders’ equity or partners’ capital, earnings per share or unit, etc.). A combined Management’s Discussion and Analysis of Financial Condition and Results of Operations section is also included that presents discrete information related to each entity, as applicable.

In order to highlight the differences between the Trust and the Operating Partnership, the separate sections in this report for the Trust and the Operating Partnership specifically refer to the Trust and the Operating Partnership. In the sections that combine disclosure of the Trust and the Operating Partnership, this report refers to actions or holdings as being actions or holdings of the Trust. Although the Operating Partnership is generally the entity that directly or indirectly enters into contracts and joint ventures and holds assets and debt, reference to the Trust is appropriate because the Trust operates its business through the Operating Partnership. The separate discussions of the Trust and the Operating Partnership in this report should be read in conjunction with each other to understand the results of the Trust on a consolidated basis and how management operates the Trust.

Education Realty Trust, Inc.

Education Realty Operating Partnership, LP

Form 10-Q

For the Quarter Ended March 31, 2015

Table of Contents

Page Number | |||

PART I - FINANCIAL INFORMATION | |||

Item 1. Condensed Consolidated Financial Statements of Education Realty Trust, Inc. and Subsidiaries: | |||

Condensed Consolidated Balance Sheets as of March 31, 2015 and December 31, 2014 | |||

Condensed Consolidated Statements of Income and Comprehensive Income for the three months ended March 31, 2015 and 2014 | |||

Condensed Consolidated Statements of Changes in Equity for the three months ended March 31, 2015 and 2014 | |||

Condensed Consolidated Statements of Cash Flows for the three months ended March 31, 2015 and 2014 | |||

Condensed Consolidated Financial Statements of Education Realty Operating Partnership, LP and Subsidiaries: | |||

Condensed Consolidated Balance Sheets as of March 31, 2015 and December 31, 2014 | |||

Condensed Consolidated Statements of Income and Comprehensive Income for the three months ended March 31, 2015 and 2014 | |||

Condensed Consolidated Statements of Changes in Partners' Capital and Noncontrolling Interests for the three months ended March 31, 2015 and 2014 | |||

Condensed Consolidated Statements of Cash Flows for the three months ended March 31, 2015 and 2014 | |||

Notes to Condensed Consolidated Financial Statements | |||

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations. | |||

Item 3. Quantitative and Qualitative Disclosures About Market Risk. | |||

Item 4. Controls and Procedures. | |||

PART II - OTHER INFORMATION | |||

Item 1. Legal Proceedings. | |||

Item 1A. Risk Factors. | |||

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds. | |||

Item 3. Defaults Upon Senior Securities. | |||

Item 4. Mine Safety Disclosures. | |||

Item 5. Other Information. | |||

Item 6. Exhibits. | |||

Signatures. | |||

PART I - Financial Information

Item 1. Financial Statements.

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except share and per share data)

(Unaudited)

March 31, 2015 | December 31, 2014 | ||||||

Assets: | |||||||

Collegiate housing properties, net | $ | 1,574,006 | $ | 1,586,009 | |||

Assets under development | 171,039 | 120,702 | |||||

Cash and cash equivalents | 23,640 | 18,385 | |||||

Restricted cash | 9,149 | 10,342 | |||||

Other assets | 74,421 | 76,199 | |||||

Total assets | $ | 1,852,255 | $ | 1,811,637 | |||

Liabilities: | |||||||

Mortgage and construction loans, net of unamortized premium | $ | 230,988 | $ | 249,637 | |||

Unsecured revolving credit facility | 72,000 | 24,000 | |||||

Unsecured term loans | 187,500 | 187,500 | |||||

Senior unsecured notes | 250,000 | 250,000 | |||||

Accounts payable and accrued expenses | 87,171 | 76,869 | |||||

Deferred revenue | 18,383 | 17,301 | |||||

Total liabilities | 846,042 | 805,307 | |||||

Commitments and contingencies (see Note 7) | — | — | |||||

Redeemable noncontrolling interests | 13,648 | 14,512 | |||||

Equity: | |||||||

Common stock, $0.01 par value per share, 200,000,000 shares authorized, 48,330,648 and 47,999,427 shares issued and outstanding as of March 31, 2015 and December 31, 2014, respectively | 483 | 480 | |||||

Preferred shares, $0.01 par value, 50,000,000 shares authorized, no shares issued and outstanding | — | — | |||||

Additional paid-in capital | 1,029,280 | 1,034,683 | |||||

Accumulated deficit | (34,968 | ) | (41,909 | ) | |||

Accumulated other comprehensive loss | (6,904 | ) | (4,465 | ) | |||

Total Education Realty Trust, Inc. stockholders’ equity | 987,891 | 988,789 | |||||

Noncontrolling interests | 4,674 | 3,029 | |||||

Total equity | 992,565 | 991,818 | |||||

Total liabilities and equity | $ | 1,852,255 | $ | 1,811,637 | |||

See accompanying notes to the condensed consolidated financial statements.

1

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Amounts in thousands, except per share data)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Revenues: | |||||||

Collegiate housing leasing revenue | $ | 60,383 | $ | 50,711 | |||

Third-party development consulting services | 597 | 802 | |||||

Third-party management services | 1,053 | 1,018 | |||||

Operating expense reimbursements | 2,096 | 2,014 | |||||

Total revenues | 64,129 | 54,545 | |||||

Operating expenses: | |||||||

Collegiate housing leasing operations | 24,140 | 22,168 | |||||

Development and management services | 2,702 | 2,341 | |||||

General and administrative | 2,639 | 2,118 | |||||

Depreciation and amortization | 15,866 | 13,783 | |||||

Ground lease expense | 2,848 | 1,899 | |||||

Loss on impairment of collegiate housing properties | — | 1,910 | |||||

Reimbursable operating expenses | 2,096 | 2,014 | |||||

Total operating expenses | 50,291 | 46,233 | |||||

Operating income | 13,838 | 8,312 | |||||

Nonoperating (income) expenses: | |||||||

Interest expense | 5,941 | 5,601 | |||||

Amortization of deferred financing costs | 516 | 503 | |||||

Interest income | (38 | ) | (70 | ) | |||

Loss on extinguishment of debt | — | 649 | |||||

Total nonoperating expenses | 6,419 | 6,683 | |||||

Income before equity in losses of unconsolidated entities, income taxes and gain on sale of collegiate housing properties | 7,419 | 1,629 | |||||

Equity in losses of unconsolidated entities | (194 | ) | (22 | ) | |||

Income before income taxes and gain on sale of collegiate housing properties | 7,225 | 1,607 | |||||

Income tax expense | 78 | 45 | |||||

Income before gain on sale of collegiate housing properties | 7,147 | 1,562 | |||||

Gain on sale of collegiate housing properties | — | 10,902 | |||||

Net income | 7,147 | 12,464 | |||||

Less: Net income attributable to the noncontrolling interests | 206 | 398 | |||||

Net income attributable to Education Realty Trust, Inc. | $ | 6,941 | $ | 12,066 | |||

See accompanying notes to the condensed consolidated financial statements.

2

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Comprehensive income: | |||||||

Net income | $ | 7,147 | $ | 12,464 | |||

Other comprehensive loss: | |||||||

Loss on cash flow hedging derivatives | (2,439 | ) | (1,363 | ) | |||

Comprehensive income | $ | 4,708 | $ | 11,101 | |||

Less: comprehensive income attributable to the noncontrolling interests | 206 | 398 | |||||

Comprehensive income attributable to Education Realty Trust, Inc. | $ | 4,502 | $ | 10,703 | |||

Earnings per share information: | |||||||

Net income attributable to Education Realty Trust, Inc. common stockholders per share – basic and diluted | $ | 0.14 | $ | 0.31 | |||

Distributions per share of common stock | $ | 0.36 | $ | 0.33 | |||

Weighted average common shares outstanding: | |||||||

Weighted average common shares outstanding – basic | 48,179 | 38,338 | |||||

Weighted average common shares outstanding – diluted | 48,501 | 38,684 | |||||

See accompanying notes to the condensed consolidated financial statements.

3

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(Amounts in thousands, except shares)

(Unaudited)

Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Noncontrolling Interests | Total | |||||||||||||||||||||

Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2013 | 38,246,718 | $ | 1,148 | $ | 813,540 | $ | (88,964 | ) | $ | — | $ | 4,245 | $ | 729,969 | ||||||||||||

Common stock offering costs | — | — | (14 | ) | — | — | — | (14 | ) | |||||||||||||||||

Amortization of restricted stock | 45,906 | 1 | (241 | ) | — | — | — | (240 | ) | |||||||||||||||||

Cash dividends | — | — | (12,652 | ) | — | — | (525 | ) | (13,177 | ) | ||||||||||||||||

Comprehensive income (loss) | — | — | — | 12,066 | (1,363 | ) | 102 | 10,805 | ||||||||||||||||||

Balance, March 31, 2014 | 38,292,624 | $ | 1,149 | $ | 800,633 | $ | (76,898 | ) | $ | (1,363 | ) | $ | 3,822 | $ | 727,343 | |||||||||||

Balance, December 31, 2014 | 47,999,427 | $ | 480 | $ | 1,034,683 | $ | (41,909 | ) | $ | (4,465 | ) | $ | 3,029 | $ | 991,818 | |||||||||||

Issuances of common stock, net of offering costs | 327,605 | 3 | 11,497 | — | — | 11,500 | ||||||||||||||||||||

Amortization of restricted stock and long-term incentive plan awards | 3,616 | 355 | — | — | 355 | |||||||||||||||||||||

Cash dividends | — | — | (17,299 | ) | — | — | — | (17,299 | ) | |||||||||||||||||

Contributions from noncontrolling interests | — | — | — | — | — | 1,667 | 1,667 | |||||||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | 44 | — | — | — | 44 | |||||||||||||||||||

Comprehensive income (loss) | — | — | — | 6,941 | (2,439 | ) | (22 | ) | 4,480 | |||||||||||||||||

Balance, March 31, 2015 | 48,330,648 | $ | 483 | $ | 1,029,280 | $ | (34,968 | ) | $ | (6,904 | ) | $ | 4,674 | $ | 992,565 | |||||||||||

See accompanying notes to the condensed consolidated financial statements.

4

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Operating activities: | |||||||

Net income | $ | 7,147 | $ | 12,464 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 15,866 | 13,783 | |||||

Gain on sale of collegiate housing property | — | (10,902 | ) | ||||

Noncash rent expense related to the straight-line adjustment for long-term ground leases | 1,201 | 1,212 | |||||

Loss on impairment of collegiate housing properties | — | 1,910 | |||||

Loss on extinguishment of debt | — | 649 | |||||

Amortization of deferred financing costs | 516 | 503 | |||||

Amortization of unamortized debt premiums | (207 | ) | (193 | ) | |||

Distributions of earnings from unconsolidated entities | 44 | 12 | |||||

Noncash compensation expense related to stock-based incentive awards | 671 | 616 | |||||

Equity in losses of unconsolidated entities | 194 | 22 | |||||

Change in operating assets and liabilities (net of acquisitions) | 3,397 | (2,893 | ) | ||||

Net cash provided by operating activities | 28,829 | 17,183 | |||||

Investing activities: | |||||||

Purchase of corporate assets | (257 | ) | (219 | ) | |||

Restricted cash | 1,193 | (16,908 | ) | ||||

Insurance proceeds received on property losses | — | 1,428 | |||||

Investment in collegiate housing properties | (2,884 | ) | (2,905 | ) | |||

Proceeds from sale of collegiate housing properties | — | 40,007 | |||||

Notes receivable | (1,717 | ) | (125 | ) | |||

Earnest money deposits | (200 | ) | (110 | ) | |||

Investment in assets under development | (43,781 | ) | (51,295 | ) | |||

Investments in unconsolidated entities | (53 | ) | (1,919 | ) | |||

Net cash used in investing activities | (47,699 | ) | (32,046 | ) | |||

See accompanying notes to the condensed consolidated financial statements.

5

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Financing activities: | |||||||

Payment of mortgage and construction notes | (33,986 | ) | (36,682 | ) | |||

Borrowings under mortgage and construction loans | 15,544 | 3,929 | |||||

Borrowings on unsecured term loan | — | 187,500 | |||||

Debt issuance costs | (39 | ) | (1,540 | ) | |||

Debt extinguishment costs | — | (356 | ) | ||||

Borrowings on line of credit | 48,000 | 64,000 | |||||

Repayments of line of credit | — | (201,000 | ) | ||||

Proceeds from issuance of common stock | 10,569 | — | |||||

Payment of offering costs | (29 | ) | (14 | ) | |||

Purchase and return of equity to noncontrolling interests | — | (542 | ) | ||||

Contributions from noncontrolling interests | 1,693 | — | |||||

Dividends and distributions paid to common and restricted stockholders | (17,299 | ) | (12,652 | ) | |||

Dividends and distributions paid to noncontrolling interests | (115 | ) | (115 | ) | |||

Repurchases of common stock for payments of restricted stock tax withholding | (213 | ) | (769 | ) | |||

Net cash provided by financing activities | 24,125 | 1,759 | |||||

Net increase (decrease) in cash and cash equivalents | 5,255 | (13,104 | ) | ||||

Cash and cash equivalents, beginning of period | 18,385 | 22,073 | |||||

Cash and cash equivalents, end of period | $ | 23,640 | $ | 8,969 | |||

Supplemental disclosure of cash flow information: | |||||||

Interest paid, net of amounts capitalized | $ | 3,287 | $ | 6,477 | |||

Supplemental disclosure of noncash activities: | |||||||

Redemption of redeemable noncontrolling interests from unit holder | $ | 960 | $ | — | |||

Capital expenditures in accounts payable and accrued expenses related to developments | $ | 24,939 | $ | 15,525 | |||

See accompanying notes to the condensed consolidated financial statements.

6

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except unit data)

(Unaudited)

March 31, 2015 | December 31, 2014 | ||||||

Assets: | |||||||

Collegiate housing properties, net | $ | 1,574,006 | $ | 1,586,009 | |||

Assets under development | 171,039 | 120,702 | |||||

Cash and cash equivalents | 23,640 | 18,385 | |||||

Restricted cash | 9,149 | 10,342 | |||||

Other assets | 74,421 | 76,199 | |||||

Total assets | $ | 1,852,255 | $ | 1,811,637 | |||

Liabilities: | |||||||

Mortgage and construction loans, net of unamortized premium | $ | 230,988 | $ | 249,637 | |||

Unsecured revolving credit facility | 72,000 | 24,000 | |||||

Unsecured term loans | 187,500 | 187,500 | |||||

Senior unsecured notes | 250,000 | 250,000 | |||||

Accounts payable and accrued expenses | 87,171 | 76,869 | |||||

Deferred revenue | 18,383 | 17,301 | |||||

Total liabilities | 846,042 | 805,307 | |||||

Commitments and contingencies (see Note 7) | — | — | |||||

Redeemable limited partner units | 8,877 | 10,081 | |||||

Redeemable noncontrolling interests | 4,771 | 4,431 | |||||

Partners' capital: | |||||||

General partner - 6,920 units outstanding as of March 31, 2015 and December 31, 2014, respectively | 190 | 191 | |||||

Limited partners - 48,323,728 and 47,992,507 units issued and outstanding as of March 31, 2015 and December 31, 2014, respectively | 994,605 | 993,063 | |||||

Accumulated other comprehensive loss | (6,904 | ) | (4,465 | ) | |||

Total partners' capital | 987,891 | 988,789 | |||||

Noncontrolling interests | 4,674 | 3,029 | |||||

Total partners' capital | 992,565 | 991,818 | |||||

Total liabilities and partners' capital | $ | 1,852,255 | $ | 1,811,637 | |||

See accompanying notes to the condensed consolidated financial statements.

7

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Amounts in thousands, except per unit data)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Revenues: | |||||||

Collegiate housing leasing revenue | $ | 60,383 | $ | 50,711 | |||

Third-party development consulting services | 597 | 802 | |||||

Third-party management services | 1,053 | 1,018 | |||||

Operating expense reimbursements | 2,096 | 2,014 | |||||

Total revenues | 64,129 | 54,545 | |||||

Operating expenses: | |||||||

Collegiate housing leasing operations | 24,140 | 22,168 | |||||

Development and management services | 2,702 | 2,341 | |||||

General and administrative | 2,639 | 2,118 | |||||

Depreciation and amortization | 15,866 | 13,783 | |||||

Ground lease expense | 2,848 | 1,899 | |||||

Loss on impairment of collegiate housing properties | — | 1,910 | |||||

Reimbursable operating expenses | 2,096 | 2,014 | |||||

Total operating expenses | 50,291 | 46,233 | |||||

Operating income | 13,838 | 8,312 | |||||

Nonoperating (income) expenses: | |||||||

Interest expense | 5,941 | 5,601 | |||||

Amortization of deferred financing costs | 516 | 503 | |||||

Interest income | (38 | ) | (70 | ) | |||

Loss on extinguishment of debt | — | 649 | |||||

Total nonoperating expenses | 6,419 | 6,683 | |||||

Income before equity in losses of unconsolidated entities, income taxes and gain on sale of collegiate housing properties | 7,419 | 1,629 | |||||

Equity in losses of unconsolidated entities | (194 | ) | (22 | ) | |||

Income before income taxes and gain on sale of collegiate housing properties | 7,225 | 1,607 | |||||

Income tax expense | 78 | 45 | |||||

Income before gain on sale of collegiate housing properties | 7,147 | 1,562 | |||||

Gain on sale of collegiate housing properties | — | 10,902 | |||||

Net income | 7,147 | 12,464 | |||||

Less: Net income attributable to the noncontrolling interests | 166 | 298 | |||||

Net income attributable to Education Realty Operating Partnership | $ | 6,981 | $ | 12,166 | |||

See accompanying notes to the condensed consolidated financial statements.

8

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Comprehensive income: | |||||||

Net income | $ | 7,147 | $ | 12,464 | |||

Other comprehensive loss: | |||||||

Loss on cash flow hedging derivatives | (2,439 | ) | (1,363 | ) | |||

Comprehensive income | 4,708 | 11,101 | |||||

Less: comprehensive income attributable to the noncontrolling interests | 166 | 298 | |||||

Comprehensive income attributable to unitholders | $ | 4,542 | $ | 10,803 | |||

Earnings per unit information: | |||||||

Net income attributable to unitholders - basic | $ | 0.14 | $ | 0.32 | |||

Net income attributable to unitholders - diluted | $ | 0.14 | $ | 0.31 | |||

Weighted average units outstanding: | |||||||

Weighted average units outstanding – basic | 48,432 | 38,615 | |||||

Weighted average units outstanding – diluted | 48,501 | 38,684 | |||||

See accompanying notes to the condensed consolidated financial statements.

9

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN PARTNERS' CAPITAL AND NONCONTROLLING INTERESTS

(Amounts in thousands, except units)

(Unaudited)

General Partner | Limited Partners | Accumulated Other Comprehensive Loss | Noncontrolling Interests | Total | |||||||||||||||||||||

Units | Amount | Units | Amount | ||||||||||||||||||||||

Balance, December 31, 2013 | 6,920 | $ | 190 | 38,239,798 | $ | 725,534 | $ | — | $ | 4,245 | $ | 729,969 | |||||||||||||

Payment of offering costs | — | — | — | (14 | ) | — | — | (14 | ) | ||||||||||||||||

Amortization of restricted stock awards | — | — | 45,906 | (240 | ) | — | — | (240 | ) | ||||||||||||||||

Distributions | — | (2 | ) | — | (12,650 | ) | — | (525 | ) | (13,177 | ) | ||||||||||||||

Comprehensive income (loss) | — | 3 | — | 12,063 | (1,363 | ) | 102 | 10,805 | |||||||||||||||||

Balance, March 31, 2014 | 6,920 | $ | 191 | 38,285,704 | $ | 724,693 | $ | (1,363 | ) | $ | 3,822 | $ | 727,343 | ||||||||||||

Balance, December 31, 2014 | 6,920 | $ | 191 | 47,992,507 | $ | 993,063 | $ | (4,465 | ) | $ | 3,029 | $ | 991,818 | ||||||||||||

Issuance of units in exchange for contributions of equity offering proceeds and redemption of units | — | — | 327,605 | 11,500 | — | — | 11,500 | ||||||||||||||||||

Amortization of restricted stock and long-term incentive plan awards | — | — | 3,616 | 355 | — | — | 355 | ||||||||||||||||||

Distributions | — | (2 | ) | — | (17,297 | ) | — | — | (17,299 | ) | |||||||||||||||

Contributions from noncontrolling interests | — | — | — | — | — | 1,667 | 1,667 | ||||||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | — | 44 | — | — | 44 | ||||||||||||||||||

Comprehensive income (loss) | — | 1 | — | 6,940 | (2,439 | ) | (22 | ) | 4,480 | ||||||||||||||||

Balance, March 31, 2015 | 6,920 | $ | 190 | 48,323,728 | $ | 994,605 | $ | (6,904 | ) | $ | 4,674 | $ | 992,565 | ||||||||||||

See accompanying notes to the condensed consolidated financial statements.

10

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Operating activities: | |||||||

Net income | $ | 7,147 | $ | 12,464 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 15,866 | 13,783 | |||||

Gain on sale of collegiate housing property | — | (10,902 | ) | ||||

Noncash rent expense related to the straight-line adjustment for long-term ground leases | 1,201 | 1,212 | |||||

Loss on impairment of collegiate housing properties | — | 1,910 | |||||

Loss on extinguishment of debt | — | 649 | |||||

Amortization of deferred financing costs | 516 | 503 | |||||

Amortization of unamortized debt premiums | (207 | ) | (193 | ) | |||

Distributions of earnings from unconsolidated entities | 44 | 12 | |||||

Noncash compensation expense related to stock-based incentive awards | 671 | 616 | |||||

Equity in losses of unconsolidated entities | 194 | 22 | |||||

Change in operating assets and liabilities (net of acquisitions): | 3,397 | (2,893 | ) | ||||

Net cash provided by operating activities | 28,829 | 17,183 | |||||

Investing activities: | |||||||

Purchase of corporate assets | (257 | ) | (219 | ) | |||

Restricted cash | 1,193 | (16,908 | ) | ||||

Insurance proceeds received on property losses | — | 1,428 | |||||

Investment in collegiate housing properties | (2,884 | ) | (2,905 | ) | |||

Proceeds from sale of collegiate housing properties | — | 40,007 | |||||

Notes receivable | (1,717 | ) | (125 | ) | |||

Earnest money deposits | (200 | ) | (110 | ) | |||

Investment in assets under development | (43,781 | ) | (51,295 | ) | |||

Investments in unconsolidated entities | (53 | ) | (1,919 | ) | |||

Net cash used in investing activities | (47,699 | ) | (32,046 | ) | |||

Financing activities: | |||||||

Payment of mortgage and construction notes | (33,986 | ) | (36,682 | ) | |||

Borrowings under mortgage and construction loans | 15,544 | 3,929 | |||||

Borrowings on unsecured term loan | — | 187,500 | |||||

Debt issuance costs | (39 | ) | (1,540 | ) | |||

Debt extinguishment costs | — | (356 | ) | ||||

Borrowings on line of credit | 48,000 | 64,000 | |||||

Repayments of line of credit | — | (201,000 | ) | ||||

Proceeds from issuance of common units in exchange for contributions | 10,569 | — | |||||

Payment of offering costs | (29 | ) | (14 | ) | |||

Purchase and return of equity to noncontrolling interests | — | (542 | ) | ||||

Contributions from noncontrolling interests | 1,693 | — | |||||

See accompanying notes to the condensed consolidated financial statements.

11

Three Months Ended March 31, | |||||||

2015 | 2014 | ||||||

Distributions paid on unvested restricted stock awards | (8 | ) | (17 | ) | |||

Distributions paid to unitholders | (17,291 | ) | (12,635 | ) | |||

Distributions paid to noncontrolling interests | (115 | ) | (115 | ) | |||

Repurchases of units for payments of restricted stock tax withholding | (213 | ) | (769 | ) | |||

Net cash provided by financing activities | 24,125 | 1,759 | |||||

Net increase (decrease) in cash and cash equivalents | 5,255 | (13,104 | ) | ||||

Cash and cash equivalents, beginning of period | 18,385 | 22,073 | |||||

Cash and cash equivalents, end of period | $ | 23,640 | $ | 8,969 | |||

Supplemental disclosure of cash flow information: | |||||||

Interest paid, net of amounts capitalized | $ | 3,287 | $ | 6,477 | |||

Supplemental disclosure of noncash activities: | |||||||

Redemption of redeemable noncontrolling interests from unit holder | $ | 960 | $ | — | |||

Capital expenditures in accounts payable and accrued expenses related to developments | $ | 24,939 | $ | 15,525 | |||

See accompanying notes to the condensed consolidated financial statements.

12

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Organization and description of business

Education Realty Trust, Inc. ("EdR" and collectively with its consolidated subsidiaries, the “Trust”) was organized in the state of Maryland on July 12, 2004 and commenced operations effective with the initial public offering that was completed on January 31, 2005. Through the Trust's controlling interest in both the sole general partner and the majority owning limited partner of Education Realty Operating Partnership L.P. ("EROP" and collectively with its consolidated subsidiaries, the "Operating Partnership"), the Trust is one of the largest developers, owners and managers of collegiate housing communities in the United States in terms of beds owned and under management. The Trust is a self-administered and self-managed real estate investment trust ("REIT") that is publicly traded on the New York Stock Exchange under the ticker symbol "EDR." Under the Articles of Incorporation, as amended, the Trust is authorized to issue up to 200 million shares of common stock and 50 million shares of preferred stock, each having a par value of $0.01 per share.

The sole general partner of EROP is Education Realty OP GP, Inc. (“OP GP”), an entity that is indirectly wholly-owned by EdR. As of March 31, 2015, OP GP held an ownership interest in EROP of less than 1%. The limited partners of EROP are Education Realty OP Limited Partner Trust, a wholly-owned subsidiary of EdR, and other limited partners consisting of current and former members of management. OP GP, as the sole general partner of EROP, has the responsibility and discretion in the management and control of EROP, and the limited partners of EROP, in such capacity, have no authority to transact business for, or participate in the management activities of EROP. Management operates the Trust and the Operating Partnership as one business. The management of the Trust consists of the same members as the management of the Operating Partnership. EdR consolidates the Operating Partnership for financial reporting purposes, and EdR does not have significant assets other than its investment in the Operating Partnership. Therefore, the assets and liabilities of the Trust and the Operating Partnership are the same on their respective financial statements. Unless otherwise indicated, the accompanying Notes to the Condensed Consolidated Financial Statements apply to both the Trust and the Operating Partnership.

The Trust also provides real estate facility management, development and other advisory services through the following taxable REIT subsidiaries ("TRSs"):

• | EDR Management Inc. (our “Management Company”), a Delaware corporation performing collegiate housing management activities; and |

• | EDR Development LLC (our “Development Company”), a Delaware limited liability company providing development consulting services for third party collegiate housing communities. |

2. Summary of significant accounting policies

Basis of presentation

The accompanying condensed consolidated financial statements have been prepared on the accrual basis of accounting in conformity with accounting principles generally accepted in the United States (“GAAP”). The accompanying condensed consolidated financial statements of the Trust represent the assets and liabilities and operating results of the Trust and its majority owned subsidiaries.

All intercompany balances and transactions have been eliminated in the accompanying condensed consolidated financial statements.

Interim financial information

The accompanying unaudited interim financial statements include all adjustments, consisting only of normal recurring adjustments that, in the opinion of management, are necessary for a fair presentation of the Trust's financial position, results of operations and cash flows for such periods. Because of the seasonal nature of the business, the operating results and cash flows are not necessarily indicative of results that may be expected for any other interim periods or for the full fiscal year. These financial statements should be read in conjunction with the Trust's consolidated financial statements and related notes included

13

in the Trust's Annual Report on Form 10-K for the year ended December 31, 2014, as filed with the Securities and Exchange Commission (the "SEC") on February 27, 2015.

Use of estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Cash and cash equivalents

All highly-liquid investments with a maturity of three months or less when purchased are considered cash equivalents. Restricted cash is excluded from cash for the purpose of preparing the condensed consolidated statements of cash flows. The Trust maintains cash balances in various banks. At times, the amounts of cash may exceed the amount the Federal Deposit Insurance Corporation (“FDIC”) insures. As of March 31, 2015, the Trust had $11.9 million cash on deposit that was uninsured by the FDIC or in excess of the FDIC limits.

Restricted cash

Restricted cash includes resident security deposits, as required by law in certain states, and escrow accounts held by lenders for the purpose of paying taxes, insurance, principal and interest and funding capital improvements.

Notes receivable

On August 26, 2013, the Trust provided a $0.5 million promissory loan to College Park Apartments, Inc. ("CPA"), the Trust's partner in the unconsolidated joint venture University Village-Greensboro LLC (see Note 5), at an interest rate of 10% per annum and a maturity date of August 1, 2020. Under the loan, CPA can make one draw per calendar quarter. As of March 31, 2015 and December 31, 2014, $0.4 million was outstanding. The loan is secured by CPA's interest in the joint venture.

On March 20, 2015, the Trust provided a $1.7 million promissory loan to Concord Eastridge, Inc, the Trust's partner in the joint venture at Roosevelt Point, at an interest rate equal to 2% plus London InterBank Offered Rate ("LIBOR") per annum compounded monthly and a maturity date of March 1, 2017. The loan is secured by Concord Eastridge's interest in the joint venture. As of March 31, 2015, $1.7 million was outstanding.

Collegiate housing properties

Land, land improvements, buildings and improvements, and furniture, fixtures and equipment are recorded at cost. Buildings and improvements are depreciated over 15 to 40 years, land improvements are depreciated over 15 years and furniture, fixtures, and equipment are depreciated over 3 to 7 years. Depreciation is computed using the straight-line method for financial reporting purposes over the estimated useful life.

For assets under development, the Trust capitalizes interest and internal development costs as assets under development. Capitalized interest is determined using the weighted average interest costs of total debt. When the property opens, these costs, along with other direct costs of the development, are transferred into the applicable asset category and depreciation commences.

Acquired collegiate housing communities’ results of operations are included in the Trust’s results of operations from the respective dates of acquisition. Appraisals, estimates of cash flows and other valuation techniques are used to allocate the purchase price of acquired property between land, land improvements, buildings and improvements, furniture, fixtures and equipment and identifiable intangibles such as amounts related to in-place leases. Acquisition costs are expensed as incurred and are included in general and administrative expenses in the accompanying condensed consolidated statements of income and comprehensive income.

Management assesses impairment of long-lived assets to be held and used whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Management uses an estimate of future undiscounted cash flows of the related asset based on its intended use to determine whether the carrying value is recoverable. If the Trust determines that the carrying value of an asset is not recoverable, the fair value of the asset is estimated and an impairment loss

14

is recorded to the extent the carrying value exceeds estimated fair value. Management estimates fair value using discounted cash flow models, market appraisals if available, and other market participant data.

During the three months ended March 31, 2014, the Trust recorded a $1.9 million loss on impairment of collegiate housing properties. The impairment losses were due to a change in circumstances that indicated the respective carrying value may not be recoverable. The change in circumstances for the property could be attributable to changes in property specific market conditions, changes in anticipated future use and/or leasing results or a combination of these factors.

When a collegiate housing community has met the criteria to be classified as held for sale, the fair value less cost to sell such asset is estimated. If the fair value less cost to sell the asset is less than the carrying amount of the asset, an impairment charge is recorded for the estimated loss. Depreciation expense is no longer recorded once a collegiate housing community has met the held for sale criteria. Only dispositions that represent a strategic shift in the business will qualify for treatment as discontinued operations. The two property dispositions during the three months ended March 31, 2014 did not qualify for treatment as discontinued operations.

Redeemable noncontrolling interests (the Trust) / redeemable limited partners (EROP)

The Trust follows the guidance issued by the Financial Accounting Standards Board ("FASB") regarding the classification and measurement of redeemable securities. The Trust classifies redeemable noncontrolling interests, which include redeemable interests in consolidated joint ventures and units of limited partnership interest in University Towers Operating Partnership, LP and in the Operating Partnership in the mezzanine section of the accompanying condensed consolidated balance sheets. In the accompanying condensed consolidated balance sheets of the Operating Partnership, the redeemable units of limited partnership in the Operating Partnership are classified as redeemable limited partners. The redeemable noncontrolling interest units / redeemable limited partner units are adjusted to the greater of carrying value or fair market value based on the common share price of EdR at the end of each respective reporting period.

Common stock issuances and offering costs

Specific incremental costs directly attributable to the issuance of EdR common stock are charged against the gross proceeds of the related issuance. Accordingly, underwriting commissions and other stock issuance costs are reflected as a reduction of additional paid-in capital in the accompanying condensed consolidated statement of changes in equity.

The Trust is structured as an umbrella partnership REIT ("UPREIT") and contributes all proceeds from its various equity offerings to EROP. For every one share of common stock offered and sold by EdR for cash, EdR must contribute the net proceeds to EROP and, in return, EROP will issue one OP Unit to EdR.

During October 2014, the Trust entered into agreements to establish an at-the-market equity offering program ("ATM Program") authorized to sell a maximum of $150.0 million in additional shares of EdR common stock. The Trust sold 0.3 million shares under these distribution agreements during the three months ended March 31, 2015 and received net proceeds of $10.5 million. The Trust used the net proceeds to repay debt, fund its development pipeline and for general corporate purposes.

On November 20, 2014, the Board authorized a 1-for-3 reverse stock split of shares of EdR common stock, effective December 1, 2014. On April 30, 2015, the Operating Partnership entered into a Second Amended and Restated Agreement of Limited Partnership, which reduced the number of units of limited partnership of the Operating Partnership (the "OP Units") outstanding as a result of the 1-for-3 reverse stock split the Trust completed in December 2014. Accordingly, every three issued and outstanding shares of EdR common stock and OP Units prior to the split were reduced to one. All shares and units and related per-share and per-unit information presented in these financial statements for periods prior to the effective date have been retroactively adjusted to reflect the decreased number of shares and OP Units.

Debt premiums

Differences between the estimated fair value of debt and the principal value of debt assumed in connection with collegiate housing property acquisitions are amortized over the term of the related debt as an offset to interest expense using the effective interest method. As of March 31, 2015 and December 31, 2014, net unamortized debt premiums totaled $1.3 million and $1.5 million, respectively. These amounts are included in mortgage and construction loans in the accompanying condensed consolidated balance sheets.

15

Income taxes

EdR qualifies as a REIT under the Internal Revenue Code of 1986, as amended (the "Code'). EdR is generally not subject to federal, state and local income taxes on any of its taxable income that it distributes if it distributes at least 90% of its REIT taxable income for each tax year to its stockholders and meets certain other requirements. If EdR fails to qualify as a REIT for any taxable year, EdR will be subject to federal, state and local income taxes (including any applicable alternative minimum tax) on its taxable income.

The Trust has elected to treat certain of its subsidiaries, including the Management Company, as TRSs. A TRS is subject to federal, state and local income taxes. Our Management Company provides management services and through our Development Company, provides development services, which if directly provided by the Trust would jeopardize EdR’s REIT status. Deferred tax assets and liabilities are recognized based on the difference between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted tax rates in effect in the years in which those temporary differences are expected to reverse.

Goodwill and other intangible assets

Goodwill is tested annually for impairment as of December 31, and is tested for impairment more frequently if events and circumstances indicate that the assets might be impaired. An impairment loss is recognized to the extent that the carrying amount exceeds the asset’s fair value. The accumulated impairment loss recorded as of December 31, 2008 was $0.4 million. No additional impairment has been recorded through March 31, 2015. The carrying value of goodwill was $3.1 million as of March 31, 2015 and December 31, 2014, of which $2.1 million was recorded on the management services segment and $0.9 million was recorded on the development consulting services segment. Goodwill is not subject to amortization. Other intangible assets generally include in-place leases acquired in connection with acquisitions and are amortized over the estimated life of the lease/contract term. The carrying value of other intangible assets was $0.2 million and $0.4 million as of March 31, 2015 and December 31, 2014, respectively.

Investment in unconsolidated entities

The Trust accounts for its investments in unconsolidated joint ventures using the equity method whereby the costs of an investment are adjusted for the Trust’s share of earnings of the respective investment reduced by distributions received. The earnings and distributions of the unconsolidated joint ventures are allocated based on each owner’s respective ownership interests. These investments are classified as other assets or accrued expenses, depending on whether the distributions exceed the Trust’s contributions and share of earnings in the joint ventures, in the accompanying condensed consolidated balance sheets (see Note 5).

Stock-based compensation

On May 4, 2011, the Trust’s stockholders approved the Education Realty Trust, Inc. 2011 Omnibus Equity Incentive Plan (the “2011 Plan”). The 2011 Plan replaced the Education Realty Trust, Inc. 2004 Incentive Plan (“2004 Plan”) in its entirety. The 2011 Plan is described more fully in Note 9. Compensation costs related to share-based payments are recognized in the accompanying condensed consolidated financial statements in accordance with authoritative guidance.

Earnings per share

Earnings per Share - The Trust

Basic earnings per share is calculated by dividing net earnings available to common stockholders by weighted average shares of common stock outstanding, including outstanding LTIP Units (as defined in Note 9). Diluted earnings per share is calculated similarly, except that it includes the dilutive effect of the assumed exercise of potentially dilutive securities. The Trust follows the authoritative guidance regarding the determination of whether certain instruments are participating securities. All unvested share-based payment awards that contain nonforfeitable rights to dividends or dividend equivalents are included in the computation of earnings per share under the two-class method. This results in shares of unvested restricted stock and LTIP Units being included in the computation of basic earnings per share for all periods presented.

Earnings per OP Unit - EROP

Basic earnings per unit is calculated by dividing net earnings available to unitholders by the weighted average number of OP Units and LTIP Units outstanding. Diluted earnings per unit is calculated similarly, except that it includes the dilutive effect of

16

the assumed exercise of potentially dilutive securities. EROP follows the authoritative guidance regarding the determination of whether certain instruments are participating securities.

Fair value measurements

The Trust follows the guidance contained in FASB Accounting Standards Codification 820, Fair Value Measurements and Disclosures ("ASC 820"). Fair value is generally defined as the exit price at which an asset or liability could be exchanged in a current transaction between willing unrelated parties, other than in a forced liquidation or sale. ASC 820 establishes a fair value hierarchy, giving the highest priority to quoted prices in active markets and the lowest priority to unobservable data, and requires disclosures for assets and liabilities measured at fair value based on their level in the hierarchy.

The fair value framework requires the categorization of assets and liabilities into three levels based upon the assumptions used to value the assets or liabilities. Level 1 provides the most reliable measure of fair value, whereas Level 3 generally requires significant management judgment. The three levels are defined as follows:

• | Level 1 - Unadjusted quoted prices in active markets for identical assets or liabilities at the measurement date. |

• | Level 2 - Observable inputs other than those included in Level 1, for example, quoted prices for similar assets or liabilities in active markets or quoted prices for identical assets or liabilities in inactive markets. |

• | Level 3 - Unobservable inputs reflecting management's own assumption about the inputs used in pricing the asset or liability at the measurement date. |

Derivative instruments and hedging activities

All derivative financial instruments are recorded on the balance sheet at fair value. Changes in fair value are recognized either in earnings or as other comprehensive income (loss), depending on whether the derivative has been designated as a fair value or cash flow hedge and whether it qualifies as part of a hedging relationship, the nature of the exposure being hedged, and how effective the derivative is at offsetting movements in underlying exposure. Hedge accounting is discontinued when it is determined that the derivative is no longer effective in offsetting changes in the fair value or cash flows of a hedged item; the derivative expires or is sold, terminated, or exercised; it is no longer probable that the forecasted transaction will occur; or management determines that designating the derivative as a hedging instrument is no longer appropriate. The Trust uses interest rate swaps to effectively convert a portion of its variable rate debt to fixed rate, thus reducing the impact of changes in interest rates on interest payments (see Notes 6 and 10). These instruments are designated as cash flow hedges and the interest differential to be paid or received is recorded as interest expense.

Recent accounting pronouncements

In April 2015, the FASB issued ASU 2015-03, "Interest - Imputation of Interest (Subtopic 835-30)" ("ASU 2015-03"). ASU 2015-03 simplifies the presentation of debt issuance costs and requires that debt issuance costs be presented in the balance sheet as a direct deduction from the carrying amount of debt liability, consistent with debt discounts or premiums. The recognition and measurement guidance for debt issuance costs would not be affected by the amendments in ASU 2015-03. ASU 2015-03 is effective for annual reporting periods beginning after December 15, 2015, and interim periods within those fiscal years. The Trust is currently evaluating the provisions of this guidance.

In February 2015, the FASB issued ASU 2015-02, "Consolidation (Topic 810)" ("ASU 2015-02"), which amends the consolidation requirements in ASC 810, Consolidation. ASU 2015-02 affects reporting entities that are required to evaluate whether they should consolidate certain legal entities. All legal entities are subject to reevaluation under the revised consolidation model. Specifically, the amendments: (i) modify the evaluation of whether limited partnerships and similar legal entities are variable interest entities ("VIEs") or voting interest entities, (ii) eliminate the presumption that a general partner should consolidate a limited partnership, (iii) affect the consolidated analysis of reporting entities that are involved with VIEs, particularly those that have fee arrangements and related party relationships and (iv) provide a scope exception for certain entities. ASU 2015-02 is effective for annual reporting periods beginning after December 15, 2015, and interim periods within those fiscal years. The Trust is currently evaluating the provisions of this guidance.

In May 2014, the FASB issued ASU 2014-09, "Revenue from Contracts with Customers (Topic 606)" ("ASU 2014-09"). The guidance outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes most current revenue recognition guidance, including the guidance on real estate derecognition for most transactions. ASU 2014-09 provides that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods and services. ASU 2014-09 is effective for annual reporting periods beginning after December 15, 2016, and

17

interim periods within those years and permits the use of either the retrospective or cumulative effect transition method. The Trust is currently evaluating the provisions of this guidance.

3. Acquisition and development of real estate investments

Acquisition of collegiate housing properties

2014 Acquisitions

During the year ended December 31, 2014, the following collegiate housing property acquisitions were completed:

Name | Primary University Served | Acquisition Date | # of Beds | # of Units | Contract Price (in thousands) | |||||||

109 Tower | Florida International University Miami, Florida | Aug 2014 | 542 | 149 | $ | 43,500 | ||||||

District on Apache | Arizona State University Tempe, Arizona | Sept 2014 | 900 | 279 | $ | 89,800 | ||||||

Combined acquisition costs for these purchases were $0.9 million. These acquisitions were funded with proceeds from the follow-on equity offering in June 2014, draws on the Fourth Amended Revolver and the Fifth Amended Revolver (see Note 6) and cash on hand. A summary follows of the fair values of the assets acquired and the liabilities assumed as of the dates of the acquisitions (in thousands):

109 Tower | District on Apache | Total | ||||||||||

Collegiate housing properties | $ | 43,384 | $ | 89,216 | $ | 132,600 | ||||||

In-place leases | — | 643 | 643 | |||||||||

Other assets | 200 | 36 | 236 | |||||||||

Current liabilities | (746 | ) | (1,341 | ) | (2,087 | ) | ||||||

Total net assets acquired | $ | 42,838 | $ | 88,554 | $ | 131,392 | ||||||

The contracted purchase price of $133.3 million, reflected in the table above, net of $2.1 million in assumed liabilities, represents a net asset value of $131.2 million. The $0.2 million difference between this amount and the net assets reflected in the second table above represents working capital and other assets that were not part of the contractual purchase price, but were acquired.

During 2014, the Trust also purchased the remaining 30% of its joint venture partner's interest in The Retreat at Oxford and a portion of its joint venture partner's interest in Roosevelt Point (see Note 8).

As the collegiate housing communities acquired in 2014 were acquired subsequent to March 31, 2014, there were no actual revenue or net income (loss) recognized in the accompanying condensed consolidated statement of income and comprehensive income for the three months ended March 31, 2014.

The unaudited pro forma information had the acquisition date been January 1 is as follows (in thousands, except per share and per unit amounts):

Three Months Ended March 31, 2014 | ||||

Total revenue (1) | $ | 56,692 | ||

Net income attributable to the Trust (1) | $ | 13,061 | ||

Net income attributable to common shareholders - basic and diluted | $ | 0.34 | ||

Net income attributable to EROP (1) | $ | 13,168 | ||

Net income attributable to unitholders - basic and diluted | $ | 0.34 | ||

(1) As the 109 Tower opened for 2014/2015 lease year, the supplemental proforma revenue and net income for the period January 1, 2014 - March 31, 2014 only includes the District on Apache.

18

Development of collegiate housing properties

During 2014, the Trust developed the following communities which opened during the 2014/2015 lease year. The costs incurred to date represent the balance capitalized in collegiate housing properties, net as of December 31, 2014 (dollars in thousands):

Name | Primary University Served | Bed Count | Costs Incurred as of December 31, 2014 | Internal Development Costs Capitalized | Interest Costs Capitalized | |||||||||||||

Three months ended March 31, 2014 | ||||||||||||||||||

The Lotus (1) | University of Colorado | 195 | $ | 27,800 | $ | 42 | $ | 66 | ||||||||||

Haggin Hall (2) | University of Kentucky | 396 | 23,840 | 30 | 75 | |||||||||||||

Champions Court I (2) | University of Kentucky | 740 | 47,368 | 30 | 226 | |||||||||||||

Champions Court II (2) | University of Kentucky | 427 | 24,329 | 27 | 116 | |||||||||||||

Woodland Glen I & II (2) | University of Kentucky | 818 | 45,730 | 31 | 199 | |||||||||||||

605 West (3) | Duke University | 384 | 45,258 | 48 | 167 | |||||||||||||

The Oaks on the Square - Phase III (4) | University of Connecticut | 116 | 12,482 | 26 | 26 | |||||||||||||

Total owned communities | 3,076 | 226,807 | 234 | 875 | ||||||||||||||

The Marshall (5) | University of Minnesota | 994 | 93,976 | 33 | 125 | |||||||||||||

Total joint ventures | 994 | 93,976 | 33 | 125 | ||||||||||||||

Total | 4,070 | $ | 320,783 | $ | 267 | $ | 1,000 | |||||||||||

(1) In November 2011, the Trust purchased a collegiate housing property near the University of Colorado, Boulder (The Lotus). The Trust developed additional housing on the existing land, which opened for the 2014/2015 lease year.

(2) In December 2011, the Trust was selected by the University of Kentucky to develop, own and manage new collegiate housing on its campus. This project will be financed through the ONE PlanSM. Phase I opened in August 2013 and Phase II, which includes these communities, opened for the 2014-2015 lease year. The third phase is under development.

(3) In March 2013, the Trust announced an agreement with Javelin 19 Investments, LLC ("Javelin 19") to develop, own and manage 605 West, a new collegiate housing property near Duke University. The Trust is the majority owner and managing member of the joint venture and manages the community, which opened in August 2014. For a period of five years from the date on which the property receives its initial certificate of occupancy, Javelin 19 has the right to require the Trust to purchase Javelin 19’s 10% interest in the joint venture at a price to be determined.

(4) In 2010, LeylandAlliance LLC and the Trust entered into an agreement to develop the first two phases of Storrs Center, a mixed-use town center project, adjacent to the University of Connecticut. The Trust developed, owns and manages the collegiate housing properties in these first two phases and both phases include commercial and residential offerings. The first phase opened in August 2012 and the second phase opened in August 2013. LeylandAlliance LLC and the Trust subsequently entered into additional agreements to develop the third and fourth phases of the project. The third phase opened in August 2014 and the fourth phase is under development.

(5) In 2012, Trust entered into an agreement to develop, own and manage a mixed-use development located two blocks from University of Minnesota. The Trust holds a 50% interest in the joint venture and manages the community, which opened in August 2014. The Trust does not consolidated the joint venture and its investment in the community of $18.1 million and $18.4 million as of March 31, 2015 and December 31, 2014, respectively, is classified as other assets in the accompanying condensed consolidated balance sheets.

19

The following represents a summary of active developments as of March 31, 2015, including development costs and costs capitalized (dollars in thousands):

Three Months Ended March 31, | |||||||||||||||||||||||||

Name | Primary University Served | Bed Count | Costs Incurred as of March 31, 2015 | Internal Development Costs Capitalized | Interest Costs Capitalized | ||||||||||||||||||||

2015 | 2014 | 2015 | 2014 | ||||||||||||||||||||||

Woodland Glen III, IV & V | University of Kentucky | 1,610 | $ | 92,578 | $ | 90 | $ | 31 | $ | 799 | $ | 92 | |||||||||||||

The Oaks on the Square - Phase IV | University of Connecticut | 390 | 24,286 | 47 | — | 163 | — | ||||||||||||||||||

The Retreat at Louisville (1) | University of Louisville | 656 | 34,294 | 57 | — | 160 | — | ||||||||||||||||||

Limestone Park I & II | University of Kentucky | 1,141 | 15,676 | 85 | — | 106 | — | ||||||||||||||||||

Retreat at Oxford - Phase II | University of Mississippi | 350 | 4,205 | 3 | — | 7 | — | ||||||||||||||||||

Total - owned communities | 4,147 | 171,039 | 282 | 31 | 1,235 | 92 | |||||||||||||||||||

Georgia Heights (2) | University of Georgia | 292 | 10,303 | 49 | 56 | 106 | 27 | ||||||||||||||||||

Total - joint venture | 292 | 10,303 | 49 | 56 | 106 | 27 | |||||||||||||||||||

Total active projects under development | 4,439 | $ | 181,342 | $ | 331 | $ | 87 | $ | 1,341 | $ | 119 | ||||||||||||||

(1) In June 2014, the Trust announced an agreement with a subsidiary of Landmark Property Holdings, LLC ("Landmark") to develop, own and manage cottage-style collegiate housing property adjacent to The University of Louisville. The Trust is the majority owner and managing member of the joint venture and will manage the community once completed.

(2) In 2013, Trust entered into an agreement to develop, own and manage a mixed-use development adjacent to the main entrance of the University of Georgia. The Trust holds a 50% interest in the joint venture and will manage the community once the development is completed. The Trust does not consolidate the joint venture and its investment in the community of $10.3 million and $10.2 million as of March 31, 2015 and December 31, 2014, respectively, is classified as other assets in the accompanying condensed consolidated balance sheets.

All costs related to the development of collegiate housing communities are classified as assets under development in the accompanying condensed consolidated balance sheets until the community is completed and opened.

4. Disposition of real estate investments

During the three months ended March 31, 2014, the Trust sold two owned off-campus communities, College Station at W. Lafayette and the Reserve on West 31st, containing 1,680 beds for a combined sales price of approximately $41.9 million resulting in total proceeds of approximately $40.0 million. The net income attributable to these properties is included in the continuing operations on the accompanying condensed consolidated statements of income and comprehensive income for the three months ended March 31, 2014. The Trust recognized a $10.9 million gain on these dispositions.

5. Investments in unconsolidated entities

As of March 31, 2015 and December 31, 2014, the Trust had investments in the following unconsolidated joint ventures (see Note 2), which are accounted for under the equity method:

• | a 50% interest in 1313 5th Street MN Holdings, LLC, a Delaware limited liability company, which owns the collegiate housing property referred to as The Marshall at the University of Minnesota; |

• | a 50% interest in West Clayton Athens GA Owner, LLC, a Delaware limited liability company, which owns the collegiate housing property referred to as Georgia Heights at the University of Georgia; |

• | a 25% interest in University Village-Greensboro LLC, a Delaware limited liability company, which owns the collegiate housing property referred to as University Village - Greensboro; and |

• | a 10% interest in Elauwit Networks, a South Carolina limited liability company. |

The Trust participates in major operating decisions of, but does not control, these entities; therefore, the equity method is used to account for these investments.

20

The following is a summary of the results of operations related to the Trust's unconsolidated joint ventures for the three months ended March 31, 2015 and 2014 (in thousands):

Results of Operations of Unconsolidated Entities: For the three months ended March 31, | 2015 | 2014 | |||||

Revenues | $ | 8,517 | $ | 5,012 | |||

Net loss | (661 | ) | (1,025 | ) | |||

Equity in losses of unconsolidated entities | $ | (194 | ) | $ | (22 | ) | |

As of March 31, 2015 and December 31, 2014, liabilities are recorded totaling $1.7 million related to investments in unconsolidated entities where distributions exceeded contributions and equity in earnings and the Trust has historically provided financial support; therefore, these investments are classified in accrued expenses in the accompanying condensed consolidated balance sheets (see Note 2).

6. Debt

Revolving credit facility

On November 19, 2014, the Operating Partnership entered into a Fifth Amended and Restated Credit Agreement (the “Fifth Amended Revolver”). The Fifth Amended Revolver amended and restated that certain Fourth Amended and Restated Credit Agreement (the "Fourth Amended Revolver"). The Fifth Amended Revolver has a maximum availability of $500.0 million and an accordion feature to $1.0 billion, which may be exercised during the first four years subject to satisfaction of certain conditions. The Fifth Amended Revolver is scheduled to mature on November 19, 2018.

EdR serves as the guarantor for any funds borrowed by the Operating Partnership under the Fifth Amended Revolver. The interest rate per annum applicable to the Fifth Amended Revolver is, at the Operating Partnership’s option, equal to a base rate or the LIBOR plus an applicable margin based upon our leverage. As of March 31, 2015, the interest rate applicable to the Fifth Amended Revolver was 1.43%. If amounts are drawn, due to the fact that the Fifth Amended Revolver bears interest at variable rates, cost approximates the fair value. As of March 31, 2015, the outstanding balance under the Fifth Amended Revolver was $72.0 million, thus, our remaining availability was $428.0 million.

The Fifth Amended Revolver contains customary affirmative and negative covenants and contains financial covenants that, among other things, require the maintenance of certain minimum ratios of EBITDA (earnings before payment or charges of interest, taxes, depreciation, amortization or extraordinary items) as compared to interest expense and total fixed charges. The financial covenants also include consolidated net worth and leverage ratio tests, and distributions are prohibited in excess of 95% of FFO except to comply with the legal requirements to maintain REIT status. As of March 31, 2015, the Operating Partnership was in compliance with all covenants of the Fifth Amended Revolver.

Unsecured term loan facility

On January 13, 2014, the Operating Partnership and certain subsidiaries entered into an unsecured term loan facility under a Credit Agreement (the "Credit Agreement"), which was subsequently amended and restated on November 19, 2014 (the "Amended and Restated Credit Agreement"). The Amended and Restated Credit Agreement removed certain subsidiaries as borrowers and amended certain financial covenants to align with the Fifth Amended Revolver.

Under the Amended and Restated Credit Agreement, the unsecured term loans have an aggregate principal amount of $187.5 million, consisting of a $122.5 million Tranche A term loan with a seven-year maturity (the “Tranche A Term Loan”) and a $65.0 million Tranche B term loan with a five-year maturity (the “Tranche B Term Loan” and, together with the Tranche A Term Loan, the “Term Loans”). The Tranche A Term Loan matures on January 13, 2021 and the Tranche B Term Loan matures on January 13, 2019. The Credit Agreement contains an accordion feature pursuant to which the Borrowers may request that the total aggregate amount of the Term Loans be increased to $250.0 million, which may be allocated to Tranche A or Tranche B, subject to certain conditions, including obtaining commitments from any one or more lenders to provide such additional commitments. The Operating Partnership used proceeds from the Term Loan to repay a portion of the outstanding balance under the Fourth Amended Revolver.

The interest rate per annum on the Tranche A Term Loan is, at the Operating Partnership’s option, equal to a base rate or LIBOR plus an applicable margin ranging from 155 to 225 basis points. The interest rate per annum on the Tranche B Term

21

Loan is, at the Operating Partnership’s option, equal to a base rate or LIBOR plus an applicable margin ranging from 120 to 190 basis points. The applicable margin for the Term Loans is based on leverage.

The Amended and Restated Credit Agreement contains customary affirmative and restrictive covenants substantially similar to those contained in the Fifth Amended Revolver. EdR serves as the guarantor for any funds borrowed under the Amended and Restated Credit Agreement. As of March 31, 2015, the Operating Partnership was in compliance with all covenants of the Credit Agreement.

In connection with entering into the Credit Agreement, the Operating Partnership entered into multiple interest rate swaps with notional amounts totaling $187.5 million to hedge the interest payments on the LIBOR-based Term Loans (see Note 10). As of March 31, 2015, the effective interest rate on the Tranche A Term Loan was 3.85% (weighted average swap rate of 2.30% plus the current margin of 1.55%) and the effective interest rate on the Tranche B Term Loan was 2.86% (weighted average swap rate of 1.66% plus the current margin of 1.20%).

Senior unsecured notes

On November 24, 2014, the Operating Partnership completed the public offering of $250.0 million senior unsecured notes (the "Senior Unsecured Notes") under an existing shelf registration. The 10-year Senior Unsecured Notes were issued at 99.991% of par value with a coupon of 4.6% per annum and are fully and unconditionally guaranteed by EdR. Interest on the Senior Unsecured Notes is payable semi-annually on June 1 and December 1 of each year, with the first payment beginning on June 1, 2015. The Senior Unsecured Notes will mature on December 1, 2024. The terms of Senior Unsecured Notes contain certain covenants that restrict the ability of EdR, and the Operating Partnership to incur additional secured and unsecured indebtedness. In addition, the Operating Partnership must maintain a minimum ratio of unencumbered asset value to unsecured debt, as well as minimum interest coverage level. As of March 31, 2015, the Operating Partnership was in compliance with all covenants of the Senior Unsecured Notes.

Mortgage and construction debt

As of March 31, 2015 and December 31, 2014, mortgage and construction notes payable consist of the following, which were secured by the underlying collegiate housing properties (amounts in thousands):

Outstanding Balance at | ||||||||||||||||

Property | March 31, 2015 | December 31, 2014 | Interest Rate at March 31, 2015 | Interest Rate Type | Initial Maturity Date | |||||||||||

Various Communities(1) | $ | 21,600 | $ | 21,696 | 5.67 | % | Fixed | 1/1/2020 | ||||||||

Various Communities(2) | 55,271 | 55,523 | 6.02 | % | Fixed | 1/1/2019 | ||||||||||

Various Communities(3) | 16,063 | 16,137 | 5.45 | % | Fixed | 1/1/2017 | ||||||||||

Master Secured Credit Facility | 92,934 | 93,356 | 5.84 | % | (4) | |||||||||||

The Suites at Overton Park | 24,090 | 24,216 | 4.16 | % | (5) | Fixed | 4/1/2016 | (5) | ||||||||

The Centre at Overton Park | 22,608 | 22,697 | 5.60 | % | (5) | Fixed | 1/1/2017 | (5) | ||||||||

University Towers | 34,000 | 34,000 | 2.29 | % | (6) | Variable | 7/1/2016 | (6) | ||||||||

Mortgage Debt | 80,698 | 80,913 | 3.77 | % | (4) | |||||||||||