Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Education Realty Trust, Inc. | ex321q2201810-qxceocertifi.htm |

| EX-32.4 - EXHIBIT 32.4 - Education Realty Trust, Inc. | ex324q2201810-qxcfocertifi.htm |

| EX-32.3 - EXHIBIT 32.3 - Education Realty Trust, Inc. | ex323q2201810-qxceocertifi.htm |

| EX-32.2 - EXHIBIT 32.2 - Education Realty Trust, Inc. | ex322q2201810-qxcfocertifi.htm |

| EX-31.4 - EXHIBIT 31.4 - Education Realty Trust, Inc. | ex314q2201810-qxcfocertifi.htm |

| EX-31.3 - EXHIBIT 31.3 - Education Realty Trust, Inc. | ex313q2201810-qxceocertifi.htm |

| EX-31.2 - EXHIBIT 31.2 - Education Realty Trust, Inc. | ex312q2201810-qxcfocertxtr.htm |

| EX-31.1 - EXHIBIT 31.1 - Education Realty Trust, Inc. | ex311q2201810-qxceocert.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | ||

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended June 30, 2018

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission file number 001-32417

Education Realty Trust, Inc.

Education Realty Operating Partnership, LP

(Exact Name of Registrant as Specified in Its Charter)

Maryland | 20-1352180 | |

Delaware | 20-1352332 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | |

999 South Shady Grove Road, Suite 600 Memphis, Tennessee | 38120 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s Telephone Number, Including Area Code (901) 259-2500

Not Applicable

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Education Realty Trust, Inc. Yes x No o

Education Realty Operating Partnership, LP Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Education Realty Trust, Inc. Yes x No o

Education Realty Operating Partnership, LP Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Education Realty Trust, Inc.

Large accelerated filer x | Accelerated filer o | |

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |

Emerging growth company o | ||

Education Realty Operating Partnership, LP

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o | |

Emerging growth company o | ||

If emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Education Realty Trust, Inc. Yes o No x

Education Realty Operating Partnership, LP Yes o No x

As of August 6, 2018, Education Realty Trust, Inc. had 80,604,618 shares of common stock outstanding.

EXPLANATORY NOTE

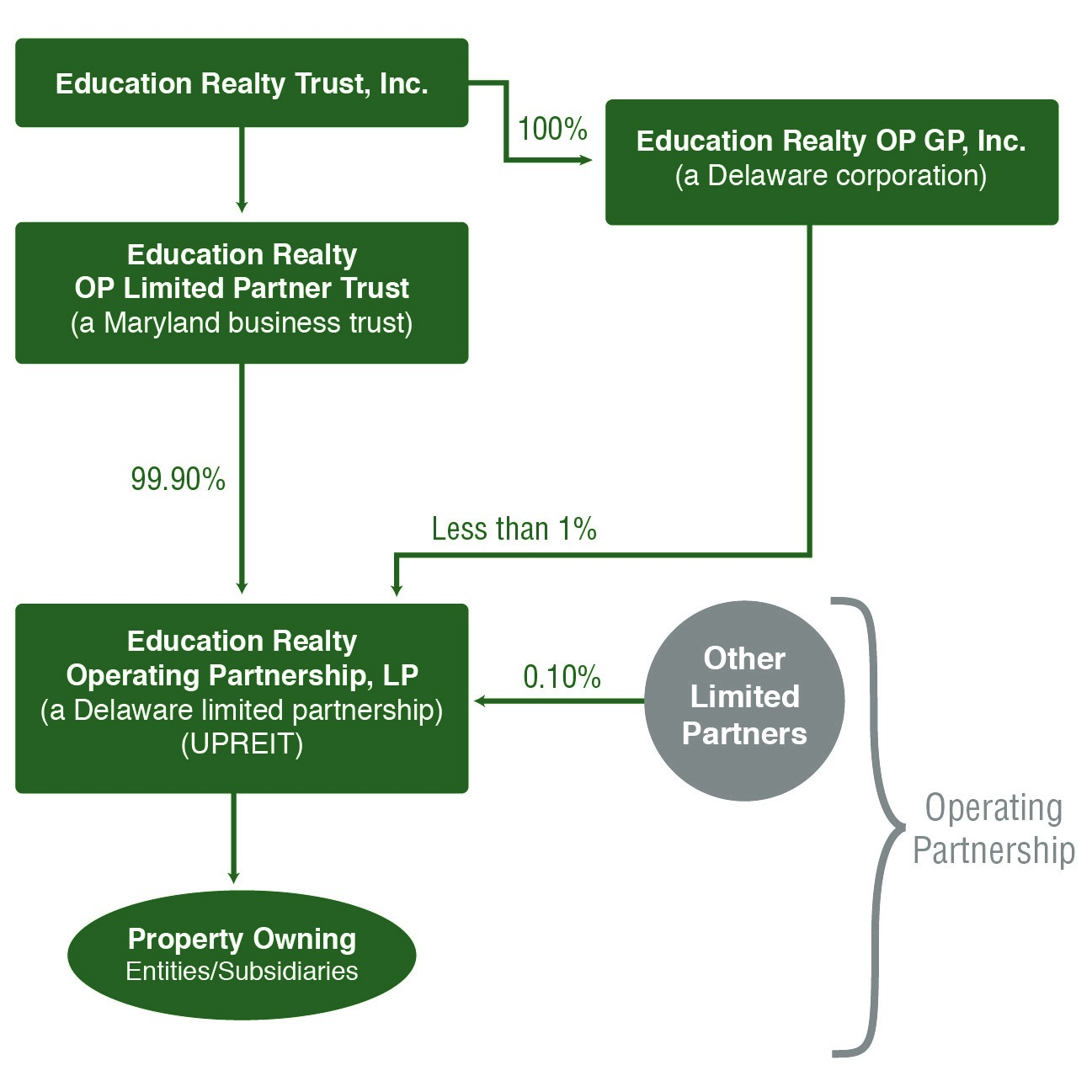

This report combines the reports on Form 10-Q for the quarterly period ended June 30, 2018 of Education Realty Trust, Inc. and Education Realty Operating Partnership, LP. Unless stated otherwise or the context otherwise requires, references to “EdR” mean only Education Realty Trust, Inc., a Maryland corporation, and references to “EROP” mean only Education Realty Operating Partnership, LP, a Delaware limited partnership. References to the "Trust," "we," "us" or "our" mean collectively EdR, EROP and those entities/subsidiaries owned or controlled by EdR and/or EROP. References to the "Operating Partnership" mean collectively EROP and those entities/subsidiaries owned or controlled by EROP. The following chart illustrates our corporate structure:

The general partner of EROP is Education Realty OP GP, Inc. (the “OP GP”), an entity that is wholly-owned by EdR. As of June 30, 2018, OP GP held an ownership interest in EROP of less than 1%. The limited partners of EROP are Education Realty OP Limited Partner Trust, a wholly-owned subsidiary of EdR, and other limited partners consisting of current and former members of management. The OP GP, as the sole general partner of EROP, has the responsibility and discretion in the management and control of the Operating Partnership, and the limited partners of EROP, in such capacity, have no authority to transact business for, or participate in the management activities of, the Operating Partnership. Management operates EdR and the Operating Partnership as one business. The management of EdR consists of the same members as the management of the Operating Partnership.

The Trust is structured as an umbrella partnership real estate investment trust (“UPREIT”) and EdR contributes all net proceeds from its various equity offerings to the Operating Partnership. In return for those contributions, EdR receives an equal number of partnership units of EROP (the “OP Units”). Contributions of properties to the Trust can be structured as tax-deferred transactions through the issuance of OP Units. Holders of OP Units may tender their OP Units for redemption by the Operating Partnership in exchange for cash equal to the market price of EdR's common stock at the time of redemption or, at EdR's option, for shares of EdR's common stock. Pursuant to the partnership agreement of EROP, the number of shares to be issued upon the redemption of OP Units is equal to the number of OP Units being redeemed. Additionally, for every one share of common stock offered and sold by EdR for cash, EdR must contribute the net proceeds to EROP and, in return, EROP will issue one OP Unit to EdR.

The Trust believes that combining the quarterly reports on Form 10-Q of EdR and the Operating Partnership into this single report provides the following benefits:

• | enhances investors’ understanding of the Trust by enabling investors to view the business of EdR and the Operating Partnership as a whole in the same manner as management views and operates the business; |

• | eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure applies to both EdR and the Operating Partnership; and |

• | creates time and cost efficiencies through the preparation of one combined report instead of two separate reports. |

EdR consolidates the Operating Partnership for financial reporting purposes, and EdR essentially has no assets or liabilities other than its investment in the Operating Partnership. Therefore, the assets and liabilities of EdR and the Operating Partnership are the same in their respective financial statements. However, the Trust believes it is important to understand the few differences between EdR and the Operating Partnership in the context of how the entities operate as a consolidated company. All of the Trust's property ownership, development and related business operations are conducted through the Operating Partnership. EdR also issues public equity from time to time and guarantees certain debt of EROP. EdR does not have any indebtedness, as all debt is incurred by the Operating Partnership. The Operating Partnership holds all of the assets of the Trust, including the Trust’s ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for the net proceeds from EdR’s equity offerings, which are contributed to the capital of EROP in exchange for OP Units on the basis of one share of common stock for one OP Unit, the Operating Partnership generates all remaining capital required by the Trust's business, including as a result of the incurrence of indebtedness. These sources include, but are not limited to, the Operating Partnership’s working capital, net cash provided by operating activities, borrowings under its credit facilities, proceeds from mortgage indebtedness and debt issuances, and proceeds received from the disposition of certain properties. Noncontrolling interests, stockholders’ equity and partners’ capital are the main areas of difference between the consolidated financial statements of the Trust and those of the Operating Partnership. The noncontrolling interests in the Operating Partnership’s financial statements consist of the interests of unaffiliated partners in various consolidated joint ventures. The noncontrolling interests in the Trust's financial statements include the same noncontrolling interests at the Operating Partnership level. The differences between stockholders’ equity and partners’ capital result from differences in the type of equity issued by EdR and the Operating Partnership.

To help investors understand the significant differences between the Trust and the Operating Partnership, this report provides separate condensed consolidated financial statements for the Trust and the Operating Partnership. A single set of consolidated notes to such financial statements is presented that includes separate discussions for the Trust and the Operating Partnership when applicable (for example, noncontrolling interests, stockholders’ equity or partners’ capital, earnings per share or unit, etc.). A combined Management’s Discussion and Analysis of Financial Condition and Results of Operations section is also included that presents discrete information related to each entity, as applicable.

In order to highlight the differences between the Trust and the Operating Partnership, the separate sections in this report for the Trust and the Operating Partnership specifically refer to the Trust and the Operating Partnership. In the sections that combine disclosure of the Trust and the Operating Partnership, this report refers to actions or holdings as being actions or holdings of the Trust. Although the Operating Partnership is generally the entity that directly or indirectly enters into contracts and joint ventures and holds assets and debt, reference to the Trust is appropriate because the Trust operates its business through the Operating Partnership. The separate discussions of the Trust and the Operating Partnership in this report should be read in conjunction with each other to understand the results of the Trust on a consolidated basis and how management operates the Trust.

Education Realty Trust, Inc.

Education Realty Operating Partnership, LP

Form 10-Q

For the Quarter Ended June 30, 2018

Table of Contents

Page Number | |||

PART I - FINANCIAL INFORMATION | |||

Item 1. Condensed Consolidated Financial Statements of Education Realty Trust, Inc. and Subsidiaries: | |||

Condensed Consolidated Balance Sheets as of June 30, 2018 and December 31, 2017 | |||

Condensed Consolidated Statements of Income and Comprehensive Income for the three and six months ended June 30, 2018 and 2017 | |||

Condensed Consolidated Statements of Changes in Equity for the six months ended June 30, 2018 and 2017 | |||

Condensed Consolidated Statements of Cash Flows for the six months ended June 30, 2018 and 2017 | |||

Condensed Consolidated Financial Statements of Education Realty Operating Partnership, LP and Subsidiaries: | |||

Condensed Consolidated Balance Sheets as of June 30, 2018 and December 31, 2017 | |||

Condensed Consolidated Statements of Income and Comprehensive Income for the three and six months ended June 30, 2018 and 2017 | |||

Condensed Consolidated Statements of Changes in Partners' Capital and Noncontrolling Interests for the six months ended June 30, 2018 and 2017 | |||

Condensed Consolidated Statements of Cash Flows for the six months ended June 30, 2018 and 2017 | |||

Notes to Condensed Consolidated Financial Statements | |||

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations. | |||

Item 3. Quantitative and Qualitative Disclosures About Market Risk. | |||

Item 4. Controls and Procedures. | |||

PART II - OTHER INFORMATION | |||

Item 1. Legal Proceedings. | |||

Item 1A. Risk Factors. | |||

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds. | |||

Item 3. Defaults Upon Senior Securities. | |||

Item 4. Mine Safety Disclosures. | |||

Item 5. Other Information. | |||

Item 6. Exhibits. | |||

Signatures. | |||

PART I - Financial Information

Item 1. Financial Statements.

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except share and per share data)

(Unaudited)

June 30, 2018 | December 31, 2017 | ||||||

Assets: | |||||||

Collegiate housing properties, net | $ | 2,526,609 | $ | 2,424,304 | |||

Assets under development | 733,200 | 488,614 | |||||

Cash and cash equivalents | 9,502 | 24,787 | |||||

Restricted cash | 8,839 | 4,368 | |||||

Other assets | 56,529 | 73,091 | |||||

Total assets | $ | 3,334,679 | $ | 3,015,164 | |||

Liabilities: | |||||||

Unsecured debt, net of unamortized deferred financing costs | $ | 864,730 | $ | 933,449 | |||

Mortgage debt, net of unamortized deferred financing costs | 127,270 | — | |||||

Accounts payable and accrued expenses | 161,072 | 162,434 | |||||

Deferred revenue | 10,586 | 20,473 | |||||

Total liabilities | 1,163,658 | 1,116,356 | |||||

Commitments and contingencies (see Note 7) | — | — | |||||

Redeemable noncontrolling interests | 58,846 | 52,843 | |||||

Equity: | |||||||

Common stock, $0.01 par value per share, 200,000,000 shares authorized, 80,581,104 and 75,779,932 shares issued and outstanding as of June 30, 2018 and December 31, 2017, respectively | 805 | 757 | |||||

Preferred shares, $0.01 par value per share, 50,000,000 shares authorized, no shares issued and outstanding | — | — | |||||

Additional paid-in capital | 2,028,379 | 1,844,639 | |||||

Retained earnings | 43,747 | — | |||||

Accumulated other comprehensive income (loss) | 2,598 | (660 | ) | ||||

Total Education Realty Trust, Inc. stockholders’ equity | 2,075,529 | 1,844,736 | |||||

Noncontrolling interests | 36,646 | 1,229 | |||||

Total equity | 2,112,175 | 1,845,965 | |||||

Total liabilities and equity | $ | 3,334,679 | $ | 3,015,164 | |||

See accompanying notes to the condensed consolidated financial statements.

1

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Amounts in thousands, except per share data)

(Unaudited)

Three months ended June 30, | Six months ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues: | |||||||||||||||

Collegiate housing leasing revenue | $ | 74,190 | $ | 70,071 | $ | 161,939 | $ | 150,856 | |||||||

Third-party development consulting services | — | 1,156 | — | 2,971 | |||||||||||

Third-party management services | 599 | 831 | 1,504 | 1,776 | |||||||||||

Operating expense reimbursements | 1,593 | 1,984 | 3,667 | 4,237 | |||||||||||

Total revenues | 76,382 | 74,042 | 167,110 | 159,840 | |||||||||||

Operating expenses: | |||||||||||||||

Collegiate housing leasing operations | 32,165 | 30,338 | 64,339 | 59,215 | |||||||||||

Development and management services | 2,984 | 2,775 | 5,835 | 5,676 | |||||||||||

General and administrative | 8,605 | 3,338 | 11,524 | 6,765 | |||||||||||

Depreciation and amortization | 23,879 | 24,520 | 46,386 | 50,359 | |||||||||||

Ground lease expense | 2,647 | 2,462 | 6,435 | 6,022 | |||||||||||

Other operating expense | — | — | — | 500 | |||||||||||

Reimbursable operating expenses | 1,593 | 1,984 | 3,667 | 4,237 | |||||||||||

Total operating expenses | 71,873 | 65,417 | 138,186 | 132,774 | |||||||||||

Operating income | 4,509 | 8,625 | 28,924 | 27,066 | |||||||||||

Nonoperating (income) expenses: | |||||||||||||||

Interest expense, net of amounts capitalized | 4,122 | 3,062 | 8,873 | 6,090 | |||||||||||

Amortization of deferred financing costs | 350 | 358 | 713 | 779 | |||||||||||

Interest income | (21 | ) | (17 | ) | (64 | ) | (49 | ) | |||||||

Gain on consolidation of unconsolidated joint ventures | (34,259 | ) | — | (34,259 | ) | — | |||||||||

Loss on extinguishment of debt | — | — | — | 22 | |||||||||||

Total nonoperating (income) expenses | (29,808 | ) | 3,403 | (24,737 | ) | 6,842 | |||||||||

Income before equity in earnings of unconsolidated entities, income taxes and gain on sale of collegiate housing properties | 34,317 | 5,222 | 53,661 | 20,224 | |||||||||||

Equity in earnings of unconsolidated entities | 6,889 | 129 | 6,831 | 384 | |||||||||||

Income before income taxes and gain on sale of collegiate housing properties | 41,206 | 5,351 | 60,492 | 20,608 | |||||||||||

Income tax (benefit) expense | (36 | ) | 353 | 30 | (532 | ) | |||||||||

Income before gain on sale of collegiate housing properties | 41,242 | 4,998 | 60,462 | 21,140 | |||||||||||

Gain on sale of collegiate housing properties | 20,979 | 691 | 42,337 | 691 | |||||||||||

Net income | 62,221 | 5,689 | 102,799 | 21,831 | |||||||||||

Less: Net loss attributable to the noncontrolling interests | (1,193 | ) | (371 | ) | (1,573 | ) | (386 | ) | |||||||

Net income attributable to Education Realty Trust, Inc. | $ | 63,414 | $ | 6,060 | $ | 104,372 | $ | 22,217 | |||||||

See accompanying notes to the condensed consolidated financial statements.

2

Three months ended June 30, | Six months ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Comprehensive income: | |||||||||||||||

Net income | $ | 62,221 | $ | 5,689 | $ | 102,799 | $ | 21,831 | |||||||

Other comprehensive income: | |||||||||||||||

Gain (loss) on cash flow hedging derivatives | 983 | (365 | ) | 3,258 | 713 | ||||||||||

Comprehensive income | 63,204 | 5,324 | 106,057 | 22,544 | |||||||||||

Less: Comprehensive loss attributable to the noncontrolling interests | (1,193 | ) | (371 | ) | (1,573 | ) | (386 | ) | |||||||

Comprehensive income attributable to Education Realty Trust, Inc. | $ | 64,397 | $ | 5,695 | $ | 107,630 | $ | 22,930 | |||||||

Earnings per share information: | |||||||||||||||

Net income attributable to Education Realty Trust, Inc. common stockholders per share – basic | $ | 0.81 | $ | 0.07 | $ | 1.34 | $ | 0.29 | |||||||

Net income attributable to Education Realty Trust, Inc. common stockholders per share – diluted | $ | 0.81 | $ | 0.07 | $ | 1.34 | $ | 0.28 | |||||||

Distributions per share of common stock | $ | 0.39 | $ | 0.38 | $ | 0.78 | $ | 0.76 | |||||||

Weighted average common shares outstanding: | |||||||||||||||

Weighted average common shares outstanding – basic | 77,101 | 73,623 | 76,660 | 73,566 | |||||||||||

Weighted average common shares outstanding – diluted | 77,250 | 73,841 | 76,820 | 73,795 | |||||||||||

See accompanying notes to the condensed consolidated financial statements.

3

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(Amounts in thousands, except shares)

(Unaudited)

Common Stock | Additional Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Noncontrolling Interests | Total | |||||||||||||||||||||

Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2016 | 73,075,455 | $ | 731 | $ | 1,802,852 | $ | — | $ | (3,564 | ) | $ | 1,422 | $ | 1,801,441 | ||||||||||||

Proceeds from issuance of common stock, net of offering costs | 110,092 | 1 | 403 | — | — | — | 404 | |||||||||||||||||||

Amortization of long-term incentive plan awards | 6 | — | 1,538 | — | — | — | 1,538 | |||||||||||||||||||

Surrender of shares to cover taxes on vesting of restricted stock | (3,283 | ) | — | (2,564 | ) | — | — | — | (2,564 | ) | ||||||||||||||||

Common stock issued to officers and directors | 12,654 | — | 480 | — | — | — | 480 | |||||||||||||||||||

Cash dividends | — | — | (33,555 | ) | (22,217 | ) | — | — | (55,772 | ) | ||||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | 4 | — | — | — | 4 | |||||||||||||||||||

Accretion of redeemable noncontrolling interests | — | — | (1,207 | ) | — | — | — | (1,207 | ) | |||||||||||||||||

Comprehensive income (loss) | — | — | — | 22,217 | 713 | (79 | ) | 22,851 | ||||||||||||||||||

Balance, June 30, 2017 | 73,194,924 | $ | 732 | $ | 1,767,951 | $ | — | $ | (2,851 | ) | $ | 1,343 | $ | 1,767,175 | ||||||||||||

Balance, December 31, 2017 | 75,779,932 | $ | 757 | $ | 1,844,639 | $ | — | $ | (660 | ) | $ | 1,229 | $ | 1,845,965 | ||||||||||||

Issuance of common stock, net of offering costs | 4,789,527 | 48 | 188,373 | — | — | — | 188,421 | |||||||||||||||||||

Reclassification of vested LTIP Units to redeemable noncontrolling interest | — | — | (2,856 | ) | — | — | — | (2,856 | ) | |||||||||||||||||

Amortization of long-term incentive plan awards | — | — | 1,534 | — | — | — | 1,534 | |||||||||||||||||||

Common stock issued to officers and directors | 11,645 | — | 400 | — | — | — | 400 | |||||||||||||||||||

Cash dividends | — | — | — | (59,177 | ) | — | — | (59,177 | ) | |||||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | (3,711 | ) | — | — | — | (3,711 | ) | |||||||||||||||||

Accretion of redeemable noncontrolling interests | — | — | — | (1,448 | ) | — | — | (1,448 | ) | |||||||||||||||||

Consolidation of previously unconsolidated joint ventures | — | — | — | — | — | 36,111 | 36,111 | |||||||||||||||||||

Comprehensive income (loss) | — | — | — | 104,372 | 3,258 | (694 | ) | 106,936 | ||||||||||||||||||

Balance, June 30, 2018 | 80,581,104 | $ | 805 | $ | 2,028,379 | $ | 43,747 | $ | 2,598 | $ | 36,646 | $ | 2,112,175 | |||||||||||||

See accompanying notes to the condensed consolidated financial statements.

4

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(Unaudited)

Six months ended June 30, | |||||||

2018 | 2017 | ||||||

Operating activities: | |||||||

Net income | $ | 102,799 | $ | 21,831 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 46,386 | 50,359 | |||||

Deferred tax expense | 31 | 1,078 | |||||

Excess tax benefit related to the vesting of restricted stock | — | (1,610 | ) | ||||

Loss on disposal of assets | 475 | — | |||||

Gain on sale of collegiate housing properties | (42,337 | ) | (691 | ) | |||

Noncash rent expense related to the straight-line adjustment for long-term ground leases | 2,340 | 2,349 | |||||

Loss on extinguishment of debt | — | 22 | |||||

Amortization of deferred financing costs | 713 | 779 | |||||

Distributions of earnings from unconsolidated entities | 3,078 | 287 | |||||

Noncash compensation expense related to stock-based incentive awards | 1,907 | 1,893 | |||||

Equity in earnings of unconsolidated entities | (6,831 | ) | (384 | ) | |||

Gain on consolidation of unconsolidated joint ventures | (34,259 | ) | — | ||||

Change in operating assets and liabilities | (7,723 | ) | (6,695 | ) | |||

Net cash provided by operating activities (net of acquisitions) | 66,579 | 69,218 | |||||

Investing activities: | |||||||

Property acquisitions | — | (127,647 | ) | ||||

Purchase of corporate assets | (965 | ) | (1,028 | ) | |||

Investment in collegiate housing properties | (8,492 | ) | (7,549 | ) | |||

Proceeds from sale of collegiate housing properties | 125,076 | 17,738 | |||||

Collections on notes receivable | 500 | — | |||||

Proceeds from disposal of property and related equity investment | 3,800 | — | |||||

Cash acquired in excess of cost of additional ownership interests acquired | 1,891 | — | |||||

Earnest money deposits | (225 | ) | (750 | ) | |||

Investment in assets under development | (277,948 | ) | (194,491 | ) | |||

Reimbursement of development related costs | 6,659 | — | |||||

Distributions from unconsolidated entities | 50 | 128 | |||||

Net cash used in investing activities | (149,654 | ) | (313,599 | ) | |||

See accompanying notes to the condensed consolidated financial statements.

5

Six months ended June 30, | |||||||

2018 | 2017 | ||||||

Financing activities: | |||||||

Payment of mortgage and construction loans | (89,307 | ) | (32,950 | ) | |||

Borrowings under mortgage and construction loans | 129,400 | 146 | |||||

Debt issuance costs | (5,620 | ) | (493 | ) | |||

Borrowings on line of credit | 158,000 | 328,000 | |||||

Repayments of line of credit | (227,000 | ) | (3,000 | ) | |||

Proceeds from issuance of common stock | 187,119 | — | |||||

Payment of offering costs | — | (335 | ) | ||||

Contributions from noncontrolling interests | 904 | 11,054 | |||||

Dividends and distributions paid to common and restricted stockholders | (59,177 | ) | (55,772 | ) | |||

Dividends and distributions paid to noncontrolling interests | (22,058 | ) | (450 | ) | |||

Repurchases of common stock for payments of restricted stock tax withholding | — | (2,563 | ) | ||||

Net cash provided by financing activities | 72,261 | 243,637 | |||||

Net decrease in cash and cash equivalents and restricted cash | (10,814 | ) | (744 | ) | |||

Cash and cash equivalents and restricted cash, beginning of period | 29,155 | 42,313 | |||||

Cash and cash equivalents and restricted cash, end of period | $ | 18,341 | $ | 41,569 | |||

Reconciliation of cash and cash equivalents and restricted cash: | |||||||

Cash and cash equivalents | $ | 9,502 | $ | 33,496 | |||

Restricted cash | 8,839 | 8,073 | |||||

Total cash and cash equivalents and restricted cash | $ | 18,341 | $ | 41,569 | |||

Supplemental disclosure of cash flow information: | |||||||

Interest paid, net of amounts capitalized | $ | 8,638 | $ | 5,815 | |||

Income taxes paid | $ | 323 | $ | 195 | |||

Supplemental disclosure of noncash activities: | |||||||

Redemption of redeemable noncontrolling interests from unit holder to shares of common stock | $ | 1,031 | $ | 1,138 | |||

Capital expenditures in accounts payable and accrued expenses related to developments | $ | 69,850 | $ | 69,390 | |||

See accompanying notes to the condensed consolidated financial statements.

6

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except unit data)

(Unaudited)

June 30, 2018 | December 31, 2017 | ||||||

Assets: | |||||||

Collegiate housing properties, net | $ | 2,526,609 | $ | 2,424,304 | |||

Assets under development | 733,200 | 488,614 | |||||

Cash and cash equivalents | 9,502 | 24,787 | |||||

Restricted cash | 8,839 | 4,368 | |||||

Other assets | 56,529 | 73,091 | |||||

Total assets | $ | 3,334,679 | $ | 3,015,164 | |||

Liabilities: | |||||||

Unsecured debt, net of unamortized deferred financing costs | $ | 864,730 | $ | 933,449 | |||

Mortgage debt, net of unamortized deferred financing costs | 127,270 | — | |||||

Accounts payable and accrued expenses | 161,072 | 162,434 | |||||

Deferred revenue | 10,586 | 20,473 | |||||

Total liabilities | 1,163,658 | 1,116,356 | |||||

Commitments and contingencies (see Note 7) | — | — | |||||

Redeemable limited partner units | 7,296 | 4,353 | |||||

Redeemable noncontrolling interests | 51,550 | 48,490 | |||||

Partners' capital: | |||||||

General partner - 6,920 units outstanding as of June 30, 2018 and December 31, 2017 | 180 | 177 | |||||

Limited partners - 80,574,184 and 75,773,012 units issued and outstanding as of June 30, 2018 and December 31, 2017, respectively | 2,072,751 | 1,845,219 | |||||

Accumulated other comprehensive income (loss) | 2,598 | (660 | ) | ||||

Total partners' capital | 2,075,529 | 1,844,736 | |||||

Noncontrolling interests | 36,646 | 1,229 | |||||

Total capital | 2,112,175 | 1,845,965 | |||||

Total liabilities and partners' capital | $ | 3,334,679 | $ | 3,015,164 | |||

See accompanying notes to the condensed consolidated financial statements.

7

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Amounts in thousands, except per unit data)

(Unaudited)

Three months ended June 30, | Six months ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues: | |||||||||||||||

Collegiate housing leasing revenue | $ | 74,190 | $ | 70,071 | $ | 161,939 | $ | 150,856 | |||||||

Third-party development consulting services | — | 1,156 | — | 2,971 | |||||||||||

Third-party management services | 599 | 831 | 1,504 | 1,776 | |||||||||||

Operating expense reimbursements | 1,593 | 1,984 | 3,667 | 4,237 | |||||||||||

Total revenues | 76,382 | 74,042 | 167,110 | 159,840 | |||||||||||

Operating expenses: | |||||||||||||||

Collegiate housing leasing operations | 32,165 | 30,338 | 64,339 | 59,215 | |||||||||||

Development and management services | 2,984 | 2,775 | 5,835 | 5,676 | |||||||||||

General and administrative | 8,605 | 3,338 | 11,524 | 6,765 | |||||||||||

Depreciation and amortization | 23,879 | 24,520 | 46,386 | 50,359 | |||||||||||

Ground lease expense | 2,647 | 2,462 | 6,435 | 6,022 | |||||||||||

Other operating expense | — | — | — | 500 | |||||||||||

Reimbursable operating expenses | 1,593 | 1,984 | 3,667 | 4,237 | |||||||||||

Total operating expenses | 71,873 | 65,417 | 138,186 | 132,774 | |||||||||||

Operating income | 4,509 | 8,625 | 28,924 | 27,066 | |||||||||||

Nonoperating (income) expenses: | |||||||||||||||

Interest expense, net of amounts capitalized | 4,122 | 3,062 | 8,873 | 6,090 | |||||||||||

Amortization of deferred financing costs | 350 | 358 | 713 | 779 | |||||||||||

Interest income | (21 | ) | (17 | ) | (64 | ) | (49 | ) | |||||||

Gain on consolidation of unconsolidated joint ventures | (34,259 | ) | — | (34,259 | ) | — | |||||||||

Loss on extinguishment of debt | — | — | — | 22 | |||||||||||

Total nonoperating (income) expenses | (29,808 | ) | 3,403 | (24,737 | ) | 6,842 | |||||||||

Income before equity in earnings of unconsolidated entities, income taxes and gain on sale of collegiate housing properties | 34,317 | 5,222 | 53,661 | 20,224 | |||||||||||

Equity in earnings of unconsolidated entities | 6,889 | 129 | 6,831 | 384 | |||||||||||

Income before income taxes and gain on sale of collegiate housing properties | 41,206 | 5,351 | 60,492 | 20,608 | |||||||||||

Income tax (benefit) expense | (36 | ) | 353 | 30 | (532 | ) | |||||||||

Income before gain on sale of collegiate housing properties | 41,242 | 4,998 | 60,462 | 21,140 | |||||||||||

Gain on sale of collegiate housing properties | 20,979 | 691 | 42,337 | 691 | |||||||||||

Net income | 62,221 | 5,689 | 102,799 | 21,831 | |||||||||||

Less: Net loss attributable to the noncontrolling interests | (1,226 | ) | (381 | ) | (1,662 | ) | (431 | ) | |||||||

Net income attributable to Education Realty Operating Partnership L.P. | $ | 63,447 | $ | 6,070 | $ | 104,461 | $ | 22,262 | |||||||

See accompanying notes to the condensed consolidated financial statements.

8

Three months ended June 30, | Six months ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Comprehensive income: | |||||||||||||||

Net income | $ | 62,221 | $ | 5,689 | $ | 102,799 | $ | 21,831 | |||||||

Other comprehensive income: | |||||||||||||||

Gain (loss) on cash flow hedging derivatives | 983 | (365 | ) | 3,258 | 713 | ||||||||||

Comprehensive income | 63,204 | 5,324 | 106,057 | 22,544 | |||||||||||

Less: Comprehensive loss attributable to the noncontrolling interests | (1,226 | ) | (381 | ) | (1,662 | ) | (431 | ) | |||||||

Comprehensive income attributable to unitholders | $ | 64,430 | $ | 5,705 | $ | 107,719 | $ | 22,975 | |||||||

Earnings per unit information: | |||||||||||||||

Net income attributable to unitholders – basic and diluted | $ | 0.81 | $ | 0.07 | $ | 1.34 | $ | 0.29 | |||||||

Distributions per unit | $ | 0.39 | $ | 0.38 | $ | 0.78 | $ | 0.76 | |||||||

Weighted average units outstanding: | |||||||||||||||

Weighted average units outstanding – basic | 77,406 | 73,755 | 76,912 | 73,709 | |||||||||||

Weighted average units outstanding – diluted | 77,475 | 73,841 | 76,981 | 73,795 | |||||||||||

See accompanying notes to the condensed consolidated financial statements.

9

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN PARTNERS' CAPITAL AND NONCONTROLLING INTERESTS

(Amounts in thousands, except units)

(Unaudited)

General Partner | Limited Partners | Accumulated Other Comprehensive Income (Loss) | Noncontrolling Interests | Total | |||||||||||||||||||||

Units | Amount | Units | Amount | ||||||||||||||||||||||

Balance, December 31, 2016 | 6,920 | $ | 178 | 73,068,535 | $ | 1,803,405 | $ | (3,564 | ) | $ | 1,422 | $ | 1,801,441 | ||||||||||||

Vesting of restricted stock and restricted stock units | — | — | 12,654 | 480 | — | — | 480 | ||||||||||||||||||

Issuance of units in exchange for contributions of equity offering proceeds and redemption of units | — | — | 110,092 | 404 | — | — | 404 | ||||||||||||||||||

Amortization of long-term incentive plan awards | — | — | 6 | 1,538 | — | — | 1,538 | ||||||||||||||||||

Surrender of shares to cover taxes on vesting of restricted shares | — | — | (3,283 | ) | (2,564 | ) | — | — | (2,564 | ) | |||||||||||||||

Distributions | — | (3 | ) | — | (55,769 | ) | — | — | (55,772 | ) | |||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | — | 4 | — | — | 4 | ||||||||||||||||||

Accretion of redeemable noncontrolling interests | — | — | — | (1,207 | ) | — | — | (1,207 | ) | ||||||||||||||||

Comprehensive income (loss) | — | 1 | — | 22,216 | 713 | (79 | ) | 22,851 | |||||||||||||||||

Balance, June 30, 2017 | 6,920 | $ | 176 | 73,188,004 | $ | 1,768,507 | $ | (2,851 | ) | $ | 1,343 | $ | 1,767,175 | ||||||||||||

Balance, December 31, 2017 | 6,920 | $ | 177 | 75,773,012 | $ | 1,845,219 | $ | (660 | ) | $ | 1,229 | $ | 1,845,965 | ||||||||||||

Vesting of restricted stock and restricted stock units | — | — | 11,645 | 400 | — | — | 400 | ||||||||||||||||||

Issuance of units in exchange for contributions of equity offering proceeds and redemption of units | — | — | 4,789,527 | 188,421 | — | — | 188,421 | ||||||||||||||||||

Reclassification of vested LTIP Units to redeemable noncontrolling interest | — | — | — | (2,856 | ) | — | — | (2,856 | ) | ||||||||||||||||

Amortization of long-term incentive plan awards | — | — | — | 1,534 | — | — | 1,534 | ||||||||||||||||||

Distributions | — | (3 | ) | — | (59,174 | ) | — | — | (59,177 | ) | |||||||||||||||

Adjustments to reflect redeemable noncontrolling interests at fair value | — | — | — | (3,711 | ) | — | — | (3,711 | ) | ||||||||||||||||

Accretion of redeemable noncontrolling interests | — | — | — | (1,448 | ) | — | — | (1,448 | ) | ||||||||||||||||

Consolidation of previously unconsolidated joint ventures | — | — | — | — | — | 36,111 | 36,111 | ||||||||||||||||||

Comprehensive income (loss) | — | 6 | — | 104,366 | 3,258 | (694 | ) | 106,936 | |||||||||||||||||

Balance, June 30, 2018 | 6,920 | $ | 180 | 80,574,184 | $ | 2,072,751 | $ | 2,598 | $ | 36,646 | $ | 2,112,175 | |||||||||||||

See accompanying notes to the condensed consolidated financial statements.

10

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(Unaudited)

Six months ended June 30, | |||||||

2018 | 2017 | ||||||

Operating activities: | |||||||

Net income | $ | 102,799 | $ | 21,831 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 46,386 | 50,359 | |||||

Deferred tax expense | 31 | 1,078 | |||||

Excess tax benefit related to the vesting of restricted stock | — | (1,610 | ) | ||||

Loss on disposal of assets | 475 | — | |||||

Gain on sale of collegiate housing properties | (42,337 | ) | (691 | ) | |||

Noncash rent expense related to the straight-line adjustment for long-term ground leases | 2,340 | 2,349 | |||||

Loss on extinguishment of debt | — | 22 | |||||

Amortization of deferred financing costs | 713 | 779 | |||||

Distributions of earnings from unconsolidated entities | 3,078 | 287 | |||||

Noncash compensation expense related to stock-based incentive awards | 1,907 | 1,893 | |||||

Equity in earnings of unconsolidated entities | (6,831 | ) | (384 | ) | |||

Gain on consolidation of unconsolidated joint ventures | (34,259 | ) | — | ||||

Change in operating assets and liabilities | (7,723 | ) | (6,695 | ) | |||

Net cash provided by operating activities (net of acquisitions) | 66,579 | 69,218 | |||||

Investing activities: | |||||||

Property acquisitions | — | (127,647 | ) | ||||

Purchase of corporate assets | (965 | ) | (1,028 | ) | |||

Investment in collegiate housing properties | (8,492 | ) | (7,549 | ) | |||

Proceeds from sale of collegiate housing properties | 125,076 | 17,738 | |||||

Collections on notes receivable | 500 | — | |||||

Proceeds from disposal of property and related equity investment | 3,800 | — | |||||

Cash acquired in excess of cost of additional ownership interests acquired | 1,891 | — | |||||

Earnest money deposits | (225 | ) | (750 | ) | |||

Investment in assets under development | (277,948 | ) | (194,491 | ) | |||

Reimbursement of development related costs | 6,659 | — | |||||

Distributions from unconsolidated entities | 50 | 128 | |||||

Net cash used in investing activities | (149,654 | ) | (313,599 | ) | |||

Financing activities: | |||||||

Payment of mortgage and construction loans | (89,307 | ) | (32,950 | ) | |||

Borrowings under mortgage and construction loans | 129,400 | 146 | |||||

Debt issuance costs | (5,620 | ) | (493 | ) | |||

Borrowings on line of credit | 158,000 | 328,000 | |||||

Repayments of line of credit | (227,000 | ) | (3,000 | ) | |||

Proceeds from issuance of common units in exchange for contributions | 187,119 | — | |||||

Payment of offering costs | — | (335 | ) | ||||

See accompanying notes to the condensed consolidated financial statements.

11

Six months ended June 30, | |||||||

2018 | 2017 | ||||||

Contributions from noncontrolling interests | 904 | 11,054 | |||||

Distributions paid on unvested restricted stock and long-term incentive plan awards | (305 | ) | (279 | ) | |||

Distributions paid to unitholders | (58,872 | ) | (55,493 | ) | |||

Distributions paid to noncontrolling interests | (22,058 | ) | (450 | ) | |||

Repurchases of units for payments of restricted stock tax withholding | — | (2,563 | ) | ||||

Net cash provided by financing activities | 72,261 | 243,637 | |||||

Net decrease in cash and cash equivalents and restricted cash | (10,814 | ) | (744 | ) | |||

Cash and cash equivalents and restricted cash, beginning of period | 29,155 | 42,313 | |||||

Cash and cash equivalents and restricted cash, end of period | $ | 18,341 | $ | 41,569 | |||

Reconciliation of cash and cash equivalents and restricted cash: | |||||||

Cash and cash equivalents | $ | 9,502 | $ | 33,496 | |||

Restricted cash | 8,839 | 8,073 | |||||

Total cash and cash equivalents and restricted cash | $ | 18,341 | $ | 41,569 | |||

Supplemental disclosure of cash flow information: | |||||||

Interest paid, net of amounts capitalized | $ | 8,638 | $ | 5,815 | |||

Income taxes paid | $ | 323 | $ | 195 | |||

Supplemental disclosure of noncash activities: | |||||||

Redemption of redeemable noncontrolling interests from unit holder to shares of common stock | $ | 1,031 | $ | 1,138 | |||

Capital expenditures in accounts payable and accrued expenses related to developments | $ | 69,850 | $ | 69,390 | |||

See accompanying notes to the condensed consolidated financial statements.

12

EDUCATION REALTY TRUST, INC. AND SUBSIDIARIES

EDUCATION REALTY OPERATING PARTNERSHIP, L.P. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Organization and description of business

Education Realty Trust, Inc. ("EdR" and collectively with its consolidated subsidiaries, the “Trust”) was organized in the state of Maryland on July 12, 2004 and commenced operations effective with the initial public offering that was completed on January 31, 2005. Through the Trust's controlling interest in both the sole general partner and the majority owning limited partner of Education Realty Operating Partnership L.P. ("EROP" and collectively with its consolidated subsidiaries, the "Operating Partnership"), the Trust is one of the largest developers, owners and managers of collegiate housing communities in the United States in terms of beds owned and under management. The Trust is a self-administered and self-managed REIT that is publicly traded on the New York Stock Exchange under the ticker symbol "EDR". Under the Articles of Incorporation, as amended, restated and supplemented, the Trust is authorized to issue up to 200 million shares of common stock and 50 million shares of preferred stock, each having a par value of $0.01 per share.

The sole general partner of EROP is Education Realty OP GP, Inc. (“OP GP”), an entity that is wholly-owned by EdR. As of June 30, 2018, OP GP held an ownership interest in EROP of less than 1%. The limited partners of EROP are Education Realty OP Limited Partner Trust, a wholly-owned subsidiary of EdR, and other limited partners consisting of current and former members of management. OP GP, as the sole general partner of EROP, has the responsibility and discretion in the management and control of EROP, and the limited partners of EROP, in such capacity, have no authority to transact business for, or participate in the management activities of, EROP. Management operates the Trust and the Operating Partnership as one business. The management of the Trust consists of the same members as the management of the Operating Partnership. EdR consolidates the Operating Partnership for financial reporting purposes, and EdR does not have significant assets other than its investment in the Operating Partnership. Therefore, the assets and liabilities of the Trust and the Operating Partnership are the same on their respective financial statements. Unless otherwise indicated, the accompanying Notes to the Condensed Consolidated Financial Statements apply to both the Trust and the Operating Partnership.

The Trust also provides real estate facility management, development and other advisory services through its taxable REIT subsidiaries ("TRS"), EDR Management Inc. (the “Management Company”), a Delaware corporation that performs collegiate housing management activities. EDR Development LLC (the “Development Company”), a Delaware limited liability company and wholly-owned subsidiary of the Management Company, which provides development consulting services for third-party collegiate housing communities, is a disregarded entity for federal income tax purposes, and all assets owned and income earned by our Development Company are deemed to be owned and earned by our Management Company.

Pending Mergers

As disclosed in a Current Report on Form 8-K dated June 25, 2018, the Trust entered into a definitive agreement and plan of merger ("Merger Agreement") with Greystar Student Housing Growth and Income LTP, LP and certain other affiliates of Greystar Real Estate Partners LLC (collectively referred to as "Greystar") pursuant to which, upon closing, all outstanding shares of common stock, OP units and units of limited partnership interest in University Towers Operating Partnership, LP (other than the OP units and units of limited partnership interest in University Towers Operating Partnership, LP held by us and our subsidiaries) are to be converted into the right to receive $41.50 in cash (referred to as the "Mergers"). The pending Mergers are subject to customary closing conditions, including, but not limited to, the approval of the Mergers by EdR’s stockholders.

The Merger Agreement may be terminated under certain circumstances by the Trust. In addition, Greystar may terminate the Merger Agreement under certain circumstances and subject to certain restrictions. Upon a termination of the Merger Agreement, under certain circumstances, the Trust will be required to pay a termination fee to Greystar of either $50,634,537 or $118,147,254 depending on the timing and circumstances of the termination. In certain other circumstances, Greystar will be required to pay the Trust a termination fee of $200,000,000 upon termination of the Merger Agreement.

During the six months ended June 30, 2018, the Trust recognized $5.3 million of Merger-related expenses presented within general and administrative expenses in the condensed consolidated statement of income and comprehensive income. We expect

13

that additional expenses will be incurred in connection with the closing of the Mergers; however, all such Merger-related expenses incurred by the Trust will not reduce the Merger consideration.

2. Summary of significant accounting policies

Basis of presentation

The accompanying condensed consolidated financial statements have been prepared on the accrual basis of accounting in conformity with accounting principles generally accepted in the United States (“GAAP”). The accompanying condensed consolidated financial statements of the Trust represent the assets and liabilities and operating results of the Trust and its majority owned subsidiaries.

All intercompany balances and transactions have been eliminated in the accompanying condensed consolidated financial statements.

Principles of consolidation

The Trust accounts for interests in partnerships, joint ventures and other similar entities in which it holds an ownership interest in accordance with the variable interest entity (“VIE”) guidance. Under the VIE model, the Trust consolidates an entity when it has control to direct the activities of the VIE and where it is determined to be the primary beneficiary. Under the voting interest model, the Trust consolidates an entity when it controls the entity through the ownership of a majority voting interest.

All of the Trust's property ownership, development and related business operations are conducted through the Operating Partnership. See the assets and liabilities of the Operating Partnership in the accompanying condensed consolidated financial statements.

Interim financial information

The accompanying unaudited interim condensed consolidated financial statements include all adjustments, consisting only of normal recurring adjustments that, in the opinion of management, are necessary for a fair presentation of the Trust's and the Operating Partnership's financial position, results of operations and cash flows for such periods. Because of the seasonal nature of the business, the operating results and cash flows are not necessarily indicative of results that may be expected for any other interim periods or for the full fiscal year. These financial statements should be read in conjunction with the Trust's and the Operating Partnership's consolidated financial statements and related notes included in the Trust's Annual Report on Form 10-K for the year ended December 31, 2017, as filed with the Securities and Exchange Commission (the "SEC") on February 27, 2018.

Use of estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Restricted cash

Restricted cash includes (i) escrow accounts held by lenders for the purpose of paying taxes and insurance and funding capital improvements, (ii) certain security deposits received from tenants and (iii) retainage held by financial institutions.

During the three months ended December 31, 2017, the Trust early adopted Accounting Standards Update ("ASU") 2016-18, "Statement of Cash Flows (Topic 230): Restricted Cash" ("ASU 2016-18"). ASU 2016-18 requires that a statement of cash flows explain the change during the period in the total of cash, cash equivalents and restricted cash. Therefore, amounts generally described as restricted cash should be included with cash and cash equivalents when reconciling the beginning of period and end of period total amounts shown on the statement of cash flows, and transfers between cash and cash equivalents and restricted cash are no longer presented within the statement of cash flows.

14

As a result of the adoption of ASU 2016-18, cash flows related to restricted cash within the investing section of the statement of cash flows have been retrospectively adjusted for the six months ended June 30, 2017, as follows (dollars in thousands):

As Previously Reported | As Adjusted per ASU 2016-18 | Effect of Change | ||||||||||

Six months ended June 30, 2017: | ||||||||||||

Investing activities: | ||||||||||||

Restricted cash | $ | (235 | ) | $ | — | $ | 235 | |||||

Net cash used in investing activities | (313,834 | ) | (313,599 | ) | 235 | |||||||

Net change in cash and cash equivalents and restricted cash | $ | (979 | ) | $ | (744 | ) | $ | 235 | ||||

Cash and cash equivalents and restricted cash, beginning of year | 34,475 | 42,313 | 7,838 | |||||||||

Cash and cash equivalents and restricted cash, June 30, 2017 | $ | 33,496 | $ | 41,569 | $ | 8,073 | ||||||

Collegiate housing properties

Land, land improvements, buildings and improvements, and furniture, fixtures and equipment are recorded at cost. Buildings and improvements are depreciated over 15 to 40 years, land improvements are depreciated over 15 years and furniture, fixtures and equipment are depreciated over 3 to 7 years. Depreciation is computed using the straight-line method for financial reporting purposes over the estimated useful life.

The Trust capitalizes interest based on the weighted average interest cost of the total debt and capitalizes internal development costs while developments are ongoing as assets under development. When the property opens, these costs, along with other direct costs of the development, are transferred into the applicable asset category and depreciation commences.

Acquired collegiate housing communities’ results of operations are included in the Trust’s results of operations from the respective dates of acquisition. Appraisals, estimates of cash flows and other valuation techniques are used to allocate the purchase price of acquired property between land, land improvements, buildings and improvements, furniture, fixtures and equipment and identifiable intangibles, such as amounts related to in-place leases. Acquisition costs related to the acquisition of real estate properties are capitalized if they are not deemed to be business combinations.

Management assesses impairment of long-lived assets to be held and used whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Management uses an estimate of future undiscounted cash flows of the related asset based on its intended use to determine whether the carrying value is recoverable. If the Trust determines that the carrying value of an asset is not recoverable, the fair value of the asset is estimated and an impairment loss is recorded to the extent the carrying value exceeds estimated fair value. Management estimates fair value using discounted cash flow models, market appraisals if available and other market participant data. During the six months ended June 30, 2018 and 2017, there were no impairment losses recognized.

When a collegiate housing community has met the criteria to be classified as held for sale, the fair value less cost to sell such asset is estimated. If the fair value less cost to sell the asset is less than the carrying amount of the asset, an impairment charge is recorded for the estimated loss. Depreciation expense is no longer recorded once a collegiate housing community has met the held for sale criteria. Dispositions that represent a strategic shift in the business will qualify for treatment as discontinued operations. The property dispositions during the six months ended June 30, 2018 and 2017 did not qualify for treatment as discontinued operations and, as a result, the operations of the properties are included in continuing operations in the accompanying condensed consolidated statements of income and comprehensive income through the date of disposition.

During August 2016, the Trust committed and finalized plans to demolish and redevelop Players Club, an off-campus community that serves Florida State University. Depreciation estimates were revised to reflect the shortened remaining useful life. The Trust recorded $1.1 million and $2.9 million, respectively, of accelerated depreciation during the three and six months ended June 30, 2017, respectively, related to the change in estimate. The impact on net income attributable to EdR common stockholders per share - basic and diluted for the three and six months ended June 30, 2017 was $0.02 and $0.04, respectively. The community is still under development as of June 30, 2018.

15

Redeemable noncontrolling interests (the Trust) / redeemable limited partners (EROP)

The Trust follows the guidance issued by the Financial Accounting Standards Board ("FASB") regarding the classification and measurement of redeemable securities. The Trust classifies redeemable noncontrolling interests, which include redeemable interests in consolidated joint ventures with puts exercisable by the joint venture partners and units of limited partnership interest in University Towers Operating Partnership, LP and in the Operating Partnership in the mezzanine section of the accompanying condensed consolidated balance sheets.

The Trust also has certain noncontrolling interests with put options at substantially fixed prices. These noncontrolling interests are accounted for as noncontrolling interests redeemable at other than fair value. The Trust accounts for the change in redemption value through the use of an accretion model from the date of inception to the expected redemption date. Changes in redemption value are recorded in equity, either through retained earnings or additional paid-in capital (absent any retained earnings). The impact of the changes in redemption value (accretion) is included in earnings per share using the two-class method.

In the accompanying condensed consolidated balance sheets of the Operating Partnership, the redeemable units of limited partnership in the Operating Partnership are classified as redeemable limited partners, and the redeemable interests in consolidated joint ventures with puts exercisable by the joint venture partners and units of limited partnership interest in University Towers Operating Partnership, LP are classified as redeemable noncontrolling interests. The redeemable noncontrolling interests / redeemable limited partner units are adjusted to the greater of carrying value or fair market value based on the price per share of EdR's common stock or redemption value at the end of each respective reporting period.

Common stock issuances and offering costs

Specific incremental costs directly attributable to the issuance of EdR common stock are charged against the gross proceeds of the related issuance. Accordingly, underwriting commissions and other stock issuance costs are reflected as a reduction of additional paid-in capital in the accompanying condensed consolidated statements of changes in equity.

The Trust is structured as an umbrella partnership REIT ("UPREIT") and contributes all proceeds from its various equity offerings to EROP. For every one share of common stock offered and sold by EdR for cash, EdR must contribute the net proceeds to EROP and, in return, EROP will issue one OP Unit to EdR.

Income taxes

EdR qualifies as a REIT under the Internal Revenue Code of 1986, as amended (the "Code"). EdR is generally not subject to federal, state and local income taxes on any of its taxable income that it distributes if it distributes at least 90% of its REIT taxable income for each tax year to its stockholders and meets certain other requirements. If EdR fails to qualify as a REIT for any taxable year, EdR will be subject to federal, state and local income taxes (including any applicable alternative minimum tax) on its taxable income.

The Trust has elected to treat certain of its subsidiaries, including the Management Company, as TRSs. A TRS is subject to federal, state and local income taxes. The Management Company provides management services and through the Development Company provides development services, which if directly provided by the Trust would jeopardize EdR’s REIT status. Deferred tax assets and liabilities are recognized based on the difference between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted tax rates in effect in the years in which those temporary differences are expected to reverse.

The Trust had no unrecognized tax benefits as of June 30, 2018 and December 31, 2017. The Trust and its subsidiaries file federal and state income tax returns. As of June 30, 2018, open tax years generally included tax years for 2014, 2015, 2016 and 2017. The Trust’s policy is to include interest and penalties related to unrecognized tax benefits in general and administrative expenses. For the three and six months ended June 30, 2018 and 2017, the Trust had no interest or penalties recorded related to unrecognized tax benefits.

16

Goodwill and other intangible assets

Goodwill is tested annually at the reporting unit level for impairment as of December 31 and is tested for impairment more frequently if events and circumstances indicate that the assets might be impaired. An impairment loss is recognized to the extent that the carrying amount exceeds the asset’s fair value. The accumulated impairment loss recorded is $0.4 million. No additional impairment has been recorded through June 30, 2018. The carrying value of goodwill was $3.1 million as of June 30, 2018 and December 31, 2017, of which $2.1 million was recorded on the management services segment and $0.9 million was recorded on the development consulting services segment. Goodwill is not subject to amortization.

Other intangible assets generally include in-place leases acquired in connection with acquisitions of collegiate housing properties. As of June 30, 2018 and December 31, 2017, gross in-place leases totaled $19.9 million and $12.2 million, respectively, and are being amortized over the estimated life of the remaining lease term, which is less than one year for student housing leases. Amortization expense totaled $2.0 million and $3.0 million for the three months ended June 30, 2018 and 2017, respectively. Amortization expense totaled $2.0 million and $6.4 million for the six months ended June 30, 2018 and 2017, respectively. As of June 30, 2018 and December 31, 2017, accumulated amortization totaled $13.1 million and $11.1 million, respectively. The carrying value of other intangible assets related to in-place leases was $6.7 million and $1.2 million as of June 30, 2018 and December 31, 2017, respectively.

Investment in unconsolidated entities

The Trust accounts for its investments in unconsolidated joint ventures using the equity method whereby the costs of an investment are adjusted for the Trust’s share of earnings of the respective investment reduced by distributions received. The earnings and distributions of the unconsolidated joint ventures are allocated based on each owner’s respective ownership interests. These investments are classified as other assets or accrued expenses, depending on whether the distributions exceed the Trust’s contributions and share of earnings in the joint ventures, in the accompanying condensed consolidated balance sheets (see Note 5).

Revenue recognition

The Trust recognizes revenue related to leasing activities at the collegiate housing communities owned by the Trust, management fees related to managing third-party collegiate housing communities, development consulting fees related to the general oversight of third-party collegiate housing development and operating expense reimbursements for payroll and related expenses incurred for third-party collegiate housing communities managed by the Trust.

Collegiate housing leasing revenue — Collegiate housing leasing revenue is comprised of all activities related to leasing and operating the collegiate housing communities and includes predominantly lease and lease-related revenues accounted for under Accounting Standards Codification ("ASC") 840. These lease and lease-related revenues include leasing apartments by the bed, food services and providing certain ancillary services. Students are required to execute lease contracts with payment schedules that vary from semester to monthly payments. Generally, the Trust requires each executed leasing contract to be accompanied by a signed parental guarantee. Receivables are recorded when billed. Revenues and nonrefundable application and service fees are recognized on a straight-line basis over the term of the lease contracts.

Deferred revenue related to collegiate housing revenue consists primarily of prepaid rent and deferred straight line rent revenue and totaled $10.6 million and $20.5 million at June 30, 2018 and December 31, 2017, respectively.

Third-party development services revenue — Third-party development services represent a single performance obligation for the delivery of a completed collegiate housing property. Third-party development fees generally represent 3% to 5% of the total cost of a project and are estimated and stipulated in the contract subject to adjustment for changes in the total cost of the project. Management has determined that the development fee and construction oversight fee outlined in the contract represent variable consideration, and the transaction price should be estimated based on the most likely amount, which will generally be the amount set forth in the contract for such fees. The Trust recognizes the development fee and construction oversight fee based on the percentage of the total project completed to date as control of the work in process transfers to the owner as construction is performed. In addition, some development consulting contracts include a provision whereby the Trust can participate in project savings resulting from successful cost management efforts and earn an additional development fee. Management believes that the additional development fee also represents variable consideration and should be estimated based on the expected value method subject to the constraint for factors outside the entity's control that could result in a significant reversal of previously recognized revenue. Variable consideration related to the additional development fee is reassessed each quarter to determine whether the uncertainties associated with such fee are sufficiently resolved to produce an estimate of the expected value that would not be probable of resulting in a significant reversal of previously recognized revenue. During the

17

six months ended June 30, 2017, there was $0.6 million of additional fees related to cost-savings included in third-party development services revenue. At June 30, 2018 and December 31, 2017, there was no unearned revenue from customers relating to development consulting services.

Third-party management services revenue — Third-party management services typically cover all aspects of community operations, including residence life and student development, marketing, leasing administration, strategic relationships, information systems and accounting services. These services represent a single performance obligation to operate the community on behalf of the owner. These services are provided pursuant to multi-year management agreements under which management fees are typically 3% to 5% of leasing revenue. As the management fees vary based on the property revenues, the fees represent variable consideration. Revenues are recognized over time as the services are provided. Each monthly service period represents a distinct obligation, and revenue is recognized based on the expected value of the contractual percentage of actual revenues. Payment is typically received in the month following completion of the monthly service period.

Operating expense reimbursements — As part of the development agreements, there are certain costs the Trust pays on behalf of universities or third-party owners and investors. These costs are included in reimbursable operating expenses and are required to be reimbursed to the Trust by the universities or third-party owners and investors. The Trust also has certain payroll and related expenses as part of our management agreements that we pay on behalf of the property owners. These costs are included in reimbursable operating expenses and are also required to be reimbursed to the Trust by the property owners. The Trust acts as the principal in all of these activities as the expenses are incurred in connection with our third-party development and management services. The expense and revenue related to these reimbursements are recognized and paid when incurred and service is provided.

Earnings per share

Earnings per Share - The Trust

Basic earnings per share is calculated by dividing net income available to common stockholders after accretion of certain redeemable noncontrolling interests by weighted average shares of common stock outstanding, including outstanding units in the Operating Partnership designated as LTIP Units ("LTIP Units"). Diluted earnings per share is calculated similarly, except that it includes the dilutive effect of the assumed exercise of potentially dilutive securities and the shares issuable upon settlement of the Forward Agreements (see Note 9) using the treasury stock method. The Trust follows the authoritative guidance regarding the determination of whether certain instruments are participating securities. All unvested share-based payment awards that contain nonforfeitable rights to dividends or dividend equivalents are included in the computation of earnings per share under the two-class method. This results in shares of unvested restricted stock and LTIP Units being included in the computation of basic earnings per share for all periods presented. When noncontrolling interests are redeemable at other than fair value, increases or decreases in the carrying amount of the redeemable noncontrolling interests are reflected in earnings per share using the two-class method.

Earnings per OP Unit - EROP

Basic earnings per unit is calculated by dividing net income available to unitholders after accretion of certain redeemable noncontrolling interests by the weighted average number of units of limited partnership interest in the Operating Partnership ("OP Units") and LTIP Units outstanding. Diluted earnings per unit is calculated similarly, except that it includes the dilutive effect of the assumed exercise of potentially dilutive securities and the shares issuable upon settlement of the Forward Agreements using the treasury stock method. EROP follows the authoritative guidance regarding the determination of whether certain instruments are participating securities.

Recent accounting pronouncements

In June 2018, the FASB issued ASU 2018-07, "Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment Accounting." The ASU is intended to reduce the cost and complexity and to improve financial reporting for nonemployee share-based payments. The ASU expands the scope of Topic 718, "Compensation-Stock Compensation" (which currently only includes share-based payments to employees) to include share-based payments issued to nonemployees for goods or services. Consequently, the accounting for share-based payments to nonemployees and employees will be substantially aligned. The ASU supersedes Subtopic 505-50, "Equity-Equity-Based payments to Non-Employees." The ASU is effective for the Trust for fiscal years beginning after December 15, 2018, including interim periods within that fiscal year. Early adoption is permitted but no earlier than a company’s adoption date of Topic 606, "Revenue from Contracts with Customers." The adoption of this guidance is not expected to have a material impact on the Trust’s condensed consolidated financial statements.

18

In August 2017, the FASB issued ASU 2017-12, "Derivatives and Hedging: Targeted Improvements to Accounting for Hedging Activities" ("ASU 2017-12"). The purpose of this updated guidance is to better align a company’s financial reporting for hedging activities with the economic objectives of those activities. The transition guidance provides companies with the option of early adopting the new standard using a modified retrospective transition method in any interim period after issuance of the update, or alternatively requires adoption for fiscal years beginning after December 15, 2018. The Trust early adopted ASU 2017-12 as of January 1, 2018. ASU 2017-12 required the Trust to recognize the cumulative effect of initially applying ASU 2017-12 as an adjustment to accumulated other comprehensive income with a corresponding adjustment to the opening balance of retained earnings as of the beginning of 2018. The adoption had no impact on the accompanying condensed consolidated financial statements other than enhanced disclosures.

In February 2016, the FASB issued ASU 2016-02, "Leases (Topic 842)" ("ASU 2016-02"), which requires a lessee to recognize in the statement of financial position a liability to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset for the lease term. ASU 2016-02 is effective for annual reporting periods beginning after December 15, 2018, and interim periods within those years, on a modified retrospective basis. The Trust's primary revenue is collegiate housing lease and lease-related revenue; as such, the Trust is a lessor on a significant number of leases. The Trust is continuing to evaluate the potential impact of the ASU and believes it will continue to account for its leases in substantially the same manner due to the short-term nature (less than 12 months) of its leases. The most significant change anticipated relates to ground lease agreements under which the Trust is the lessee, which could result in recording the right-of-use asset and related liability on the balance sheet. The Trust’s ground lease payments generally vary based upon percentages of property revenues. and variable lease payments are excluded from the calculation of right-of-use assets and related liabilities. Therefore, a substantial portion of the Trust’s annual ground rent payments will be excluded from the calculations of the right-of-use assets and related liabilities. The Trust plans to adopt ASU 2016-02 effective January 1, 2019 and is continuing to evaluate and quantify the effect that ASU 2016-02 will have on its consolidated financial statements and related disclosures.

In May 2014, the FASB issued ASU 2014-09, "Revenue from Contracts with Customers (Topic 606)" ("ASU 2014-09"), as amended by ASU 2015-04 to defer the effective date. The guidance outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes most current revenue recognition guidance, including the guidance on real estate derecognition for most transactions. ASU 2014-09 provides that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods and services. ASU 2014-09 became effective for annual reporting periods beginning after December 15, 2017 and interim periods within those years and permits the use of either a full retrospective method or a modified retrospective method. The standard also allows the use of certain practical expedients described below. Since the issuance of ASU 2014-09, the FASB has issued ASU 2016-08, which is intended to improve the understandability of the implementation guidance regarding principal versus agent considerations, and has issued ASU 2016-10 to clarify the identification of performance obligations and the implementation guidance related to licensing. The FASB also issued ASU 2016-12 to provide further implementation guidance in some areas and add practical expedients. The effective dates of these amendments are the same as ASU 2014-09. The Trust adopted the new revenue standard using the modified retrospective approach as of January 1, 2018, and has completed its assessment of its revenue streams to identify any differences in the timing, measurement or presentation of revenue recognition under the new standard. The adoption of this standard did not have an impact on the consolidated financial statements on the date of adoption, as a substantial portion (approximately 89%) of revenue consists of lease and lease-related income from leasing arrangements, which is specifically excluded from ASU 2014-09. The Trust's other non-lease related revenue streams, which have been evaluated under ASU 2014-09 and related guidance, include but are not limited to third-party development services, third-party management services and operating expense reimbursements. The Trust utilized the practical expedient to recognize the cumulative effect of initially applying the new standard as an adjustment to the opening balance of retained earnings only for contracts that are not completed at January 1, 2018. There was no impact to opening retained earnings related to adopting the guidance because there were no third-party development consulting agreements outstanding at December 31, 2017. Based on management's analysis of the Trust’s non-lease related revenue streams, the primary impact of the new revenue standard is enhanced disclosures that depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors, and there was no material impact to our consolidated results of operations for the adoption of the standard for the six months ended June 30, 2018. As the Trust utilized the modified retrospective approach, the comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods.

Prior to adoption of ASU 2014-09, gains for real estate sales transactions were recognized and then reduced by exposure to loss related to any continuing involvement at the time of sale. Upon adoption of ASU 2014-09, any continuing involvement must be analyzed as a separate performance obligation in the contract and a portion of the sales price allocated to each performance obligation. When the continuing involvement performance obligation is satisfied, the sales price allocated to it will be

19

recognized. The Trust had no sales of real estate with continuing involvement during the six months ended June 30, 2018 or in any prior periods that would require cumulative adjustment as of January 1, 2018.

3. Acquisition and development of real estate investments

Acquisition of additional ownership interests in previously unconsolidated joint ventures