Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - PIONEER ENERGY SERVICES CORP | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - PIONEER ENERGY SERVICES CORP | exhibit3111q2015.htm |

| EX-31.2 - EXHIBIT 31.2 - PIONEER ENERGY SERVICES CORP | exhibit3121q2015.htm |

| EX-32.1 - EXHIBIT 32.1 - PIONEER ENERGY SERVICES CORP | exhibit3211q2015.htm |

| EX-32.2 - EXHIBIT 32.2 - PIONEER ENERGY SERVICES CORP | exhibit3221q2015.htm |

| EX-10.1 - EXHIBIT 10.1 - PIONEER ENERGY SERVICES CORP | exhibit101-eustaceagreement.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

______________________________________________

FORM 10-Q

______________________________________________

(Mark one)

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2015

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-8182

PIONEER ENERGY SERVICES CORP.

(Exact name of registrant as specified in its charter)

_____________________________________________

TEXAS | 74-2088619 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

1250 NE Loop 410, Suite 1000 San Antonio, Texas | 78209 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (855) 884-0575

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o |

Non-accelerated filer | o | Smaller reporting company | o |

(Do not check if a small reporting company.) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of April 15, 2015, there were 64,245,852 shares of common stock, par value $0.10 per share, of the registrant outstanding.

PART I. FINANCIAL INFORMATION

Item 1. | Financial Statements |

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

March 31, 2015 | December 31, 2014 | ||||||

(unaudited) | (audited) | ||||||

(in thousands, except share data) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 35,678 | $ | 34,924 | |||

Receivables: | |||||||

Trade, net of allowance for doubtful accounts | 104,649 | 136,161 | |||||

Unbilled receivables | 29,957 | 38,002 | |||||

Insurance recoveries | 15,576 | 10,900 | |||||

Other receivables | 21,302 | 5,138 | |||||

Deferred income taxes | 8,529 | 10,998 | |||||

Inventory | 13,686 | 14,117 | |||||

Assets held for sale | 4,606 | 9,909 | |||||

Prepaid expenses and other current assets | 7,410 | 8,925 | |||||

Total current assets | 241,393 | 269,074 | |||||

Property and equipment, at cost | 1,572,884 | 1,702,273 | |||||

Less accumulated depreciation | 733,377 | 845,732 | |||||

Net property and equipment | 839,507 | 856,541 | |||||

Intangible assets, net of accumulated amortization of $42.1 million and $40.3 million at March 31, 2015 and December 31, 2014, respectively | 22,238 | 24,223 | |||||

Noncurrent deferred income taxes | 2,662 | 2,753 | |||||

Other long-term assets | 18,050 | 18,998 | |||||

Total assets | $ | 1,123,850 | $ | 1,171,589 | |||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 47,973 | $ | 64,305 | |||

Current portion of long-term debt | — | 27 | |||||

Deferred revenues | 33,920 | 3,315 | |||||

Accrued expenses: | |||||||

Payroll and related employee costs | 22,805 | 40,058 | |||||

Insurance premiums and deductibles | 12,264 | 12,829 | |||||

Insurance claims and settlements | 15,576 | 10,900 | |||||

Interest | 821 | 5,432 | |||||

Other | 9,978 | 10,326 | |||||

Total current liabilities | 143,337 | 147,192 | |||||

Long-term debt, less current portion | 430,000 | 455,053 | |||||

Noncurrent deferred income taxes | 62,224 | 69,578 | |||||

Other long-term liabilities | 5,207 | 4,702 | |||||

Total liabilities | 640,768 | 676,525 | |||||

Commitments and contingencies (Note 8) | |||||||

Shareholders’ equity: | |||||||

Preferred stock, 10,000,000 shares authorized; none issued and outstanding | — | — | |||||

Common stock $.10 par value; 100,000,000 shares authorized; 64,244,935 and 63,820,126 shares outstanding at March 31, 2015 and December 31, 2014, respectively | 6,465 | 6,414 | |||||

Additional paid-in capital | 472,802 | 472,457 | |||||

Treasury stock, at cost; 406,524 and 317,103 shares at March 31, 2015 and December 31, 2014, respectively | (3,389 | ) | (3,030 | ) | |||

Accumulated earnings | 7,204 | 19,223 | |||||

Total shareholders’ equity | 483,082 | 495,064 | |||||

Total liabilities and shareholders’ equity | $ | 1,123,850 | $ | 1,171,589 | |||

See accompanying notes to condensed consolidated financial statements.

2

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

Three months ended March 31, | |||||||

2015 | 2014 | ||||||

(in thousands, except per share data) | |||||||

Revenues: | |||||||

Drilling services | $ | 98,415 | $ | 117,957 | |||

Production services | 95,399 | 121,077 | |||||

Total revenues | 193,814 | 239,034 | |||||

Costs and expenses: | |||||||

Drilling services | 63,455 | 76,338 | |||||

Production services | 68,742 | 77,752 | |||||

Depreciation and amortization | 41,782 | 45,526 | |||||

General and administrative | 21,860 | 24,483 | |||||

Bad debt expense (recovery) | 319 | (124 | ) | ||||

Impairment charges | 5,990 | — | |||||

Gain on litigation | — | (2,876 | ) | ||||

Total costs and expenses | 202,148 | 221,099 | |||||

Income (loss) from operations | (8,334 | ) | 17,935 | ||||

Other expense: | |||||||

Interest expense, net of interest capitalized | (5,455 | ) | (12,388 | ) | |||

Loss on extinguishment of debt | — | (7,887 | ) | ||||

Other | (2,680 | ) | (202 | ) | |||

Total other expense | (8,135 | ) | (20,477 | ) | |||

Loss before income taxes | (16,469 | ) | (2,542 | ) | |||

Income tax (expense) benefit | 4,450 | (37 | ) | ||||

Net loss | $ | (12,019 | ) | $ | (2,579 | ) | |

Loss per common share—Basic | $ | (0.19 | ) | $ | (0.04 | ) | |

Loss per common share—Diluted | $ | (0.19 | ) | $ | (0.04 | ) | |

Weighted average number of shares outstanding—Basic | 63,991 | 62,542 | |||||

Weighted average number of shares outstanding—Diluted | 63,991 | 62,542 | |||||

See accompanying notes to condensed consolidated financial statements.

3

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

Three months ended March 31, | |||||||

2015 | 2014 | ||||||

(in thousands) | |||||||

Cash flows from operating activities: | |||||||

Net loss | $ | (12,019 | ) | $ | (2,579 | ) | |

Adjustments to reconcile net loss to net cash provided by operating activities: | |||||||

Depreciation and amortization | 41,782 | 45,526 | |||||

Allowance for doubtful accounts | 319 | (164 | ) | ||||

Loss (gain) on dispositions of property and equipment | 1,176 | (1,400 | ) | ||||

Stock-based compensation expense | 405 | 1,856 | |||||

Amortization of debt issuance costs, discount and premium | 413 | 869 | |||||

Loss on extinguishment of debt | — | 7,887 | |||||

Impairment charges | 5,990 | — | |||||

Deferred income taxes | (5,403 | ) | (1,364 | ) | |||

Change in other long-term assets | 440 | 4,193 | |||||

Change in other long-term liabilities | 503 | 651 | |||||

Changes in current assets and liabilities: | |||||||

Receivables | 40,274 | (5,158 | ) | ||||

Inventory | 431 | (518 | ) | ||||

Prepaid expenses and other current assets | 1,615 | 2,703 | |||||

Accounts payable | (19,472 | ) | 5,006 | ||||

Deferred revenues | 30,605 | 1,460 | |||||

Accrued expenses | (22,178 | ) | (17,733 | ) | |||

Net cash provided by operating activities | 64,881 | 41,235 | |||||

Cash flows from investing activities: | |||||||

Purchases of property and equipment | (45,675 | ) | (31,674 | ) | |||

Proceeds from sale of property and equipment | 6,276 | 5,516 | |||||

Proceeds from insurance recoveries | 37 | — | |||||

Net cash used in investing activities | (39,362 | ) | (26,158 | ) | |||

Cash flows from financing activities: | |||||||

Debt repayments | (25,002 | ) | (119,478 | ) | |||

Proceeds from issuance of debt | — | 320,000 | |||||

Debt issuance costs | (5 | ) | (6,138 | ) | |||

Change in restricted cash | — | (210,401 | ) | ||||

Tender premium costs | — | (5,479 | ) | ||||

Proceeds from exercise of options | 601 | 277 | |||||

Purchase of treasury stock | (359 | ) | (433 | ) | |||

Net cash used in financing activities | (24,765 | ) | (21,652 | ) | |||

Net increase (decrease) in cash and cash equivalents | 754 | (6,575 | ) | ||||

Beginning cash and cash equivalents | 34,924 | 27,385 | |||||

Ending cash and cash equivalents | $ | 35,678 | $ | 20,810 | |||

Supplementary disclosure: | |||||||

Interest paid | $ | 10,347 | $ | 21,854 | |||

Income tax paid | $ | 664 | $ | 876 | |||

Noncash investing and financing activity: | |||||||

Change in capital expenditure accruals | $ | 3,141 | $ | 5,243 | |||

See accompanying notes to condensed consolidated financial statements.

4

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. Organization and Summary of Significant Accounting Policies

Business

Pioneer Energy Services Corp. provides drilling services and production services to a diverse group of independent and large oil and gas exploration and production companies throughout much of the onshore oil and gas producing regions of the United States and internationally in Colombia. We also provide two of our services (coiled tubing and wireline services) offshore in the Gulf of Mexico.

Our Drilling Services Segment provides contract land drilling services to a diverse group of oil and gas exploration and production companies through our four drilling divisions in the US, and internationally in Colombia. In addition to our drilling rigs, we provide the drilling crews and most of the ancillary equipment needed to operate our drilling rigs. We obtain our contracts for drilling oil and natural gas wells either through competitive bidding or through direct negotiations with existing or potential clients. Our drilling contracts generally provide for compensation on either a daywork or turnkey basis. Contract terms generally depend on the complexity and risk of operations, the on-site drilling conditions, the type of equipment used, and the anticipated duration of the work to be performed.

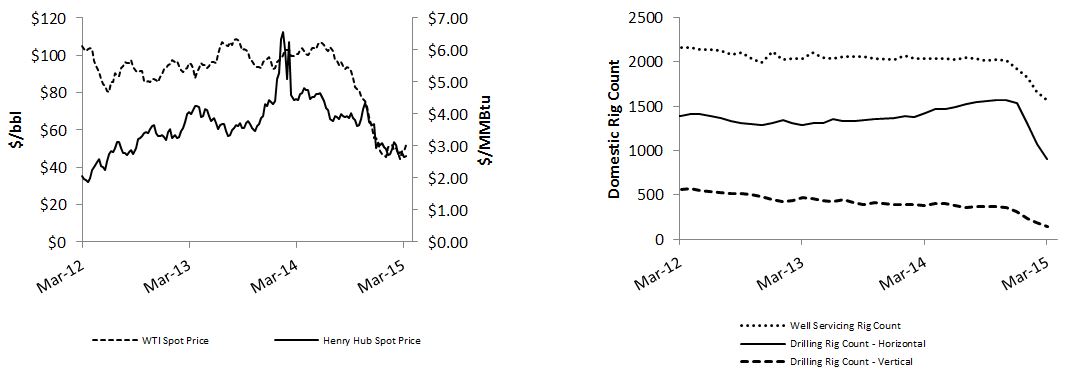

Since October 2014, domestic and international oil prices have declined significantly which resulted in a downturn in our industry. Mechanical and lower horsepower drilling rigs are the most impacted by the industry downturn and are typically the first rigs to become idle. During the first quarter of 2015, we sold 20 of our mechanical and lower horsepower electric rigs, and as of March 31, 2015, we have six remaining in our fleet, and an additional five classified as held for sale.

In April 2015, we deployed our first of five new-build 1,500 horsepower AC drilling rigs. We expect to deploy three new-build rigs in the third quarter and the final rig by the end of the year. Four of the new-build drilling rigs are under multi-year term contracts. The multi-year contract that was initially assigned to the fifth new-build drilling rig has been transferred to an existing AC rig in the Bakken that has a contract expiring in November 2015, thereby allowing us to market the fifth new-build rig to a new client in the Eagle Ford or Permian.

Excluding the rigs which we expect to sell in the near-term and considering the five new-build drilling rigs, we expect to end 2015 with a drilling fleet of 42 rigs, of which over 95% will be capable of drilling horizontally and over 90% purchased or built new within the last 15 years. The removal of older less capable rigs from our fleet and the recent and ongoing investments in the construction of new-builds is transforming our fleet into a young and highly capable fleet focused on the horizontal drilling market. We believe this positions us well to increase our market share in the significant shale basins in the US and to improve our profitability.

As of March 31, 2015, the drilling rigs in our fleet, excluding rigs classified as held for sale, are assigned to the following divisions:

Drilling Division | Rig Count | |

South Texas | 10 | |

West Texas | 5 | |

North Dakota | 10 | |

Appalachia | 4 | |

Colombia | 8 | |

37 | ||

As of March 31, 2015, 25 of our 37 drilling rigs are earning revenues under drilling contracts, 19 of which are earning under term contracts. Four of our drilling rigs in Colombia are currently working under term contracts that extend through mid-2015 and we are actively marketing our other four rigs to various operators in Colombia to diversify our client base.

5

In response to the dramatic decline in oil prices during recent months, term contracts for 16 of our drilling rigs have been early terminated, including nine of our 19 drilling rigs that are currently earning revenues under term contracts, resulting in approximately $53.1 million of early termination revenues. Revenues derived from these early terminations are deferred and recognized over the remainder of the original term of the drilling contracts. We recognized $11.3 million of revenue for early termination payments in the first quarter of 2015 and $0.3 million in the fourth quarter of 2014.

Our Production Services Segment provides a range of services to exploration and production companies, including well servicing, wireline services and coiled tubing services. Our production services operations are concentrated in the major United States onshore oil and gas producing regions in the Mid-Continent and Rocky Mountain states and in the Gulf Coast, both onshore and offshore. As of March 31, 2015, we have a fleet of 119 well servicing rigs, consisting of 108 rigs with 550 horsepower and 11 rigs with 600 horsepower, 126 wireline units and 17 coiled tubing units.

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements include the accounts of Pioneer Energy Services Corp. and our wholly owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation. The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of our management, all adjustments (consisting of normal, recurring accruals) necessary for a fair presentation have been included. We suggest that you read these condensed consolidated financial statements together with the consolidated financial statements and the related notes included in our annual report on Form 10-K for the fiscal year ended December 31, 2014.

In preparing the accompanying unaudited condensed consolidated financial statements, we make various estimates and assumptions that affect the amounts of assets and liabilities we report as of the dates of the balance sheets and income and expenses we report for the periods shown in the income statements and statements of cash flows. Our actual results could differ significantly from those estimates. Material estimates that are particularly susceptible to significant changes in the near term relate to our recognition of revenues and costs for turnkey contracts, our estimate of the allowance for doubtful accounts, our determination of depreciation and amortization expenses, our estimates of projected cash flows and fair values for impairment evaluations, our estimate of deferred taxes, our estimate of the liability relating to the self-insurance portion of our health and workers’ compensation insurance, and our estimate of compensation related accruals.

In preparing the accompanying unaudited condensed consolidated financial statements, we have reviewed events that have occurred after March 31, 2015, through the filing of this Form 10-Q, for inclusion as necessary.

Drilling Contracts

Our drilling contracts generally provide for compensation on either a daywork or turnkey basis. Contract terms generally depend on the complexity and risk of operations, the on-site drilling conditions, the type of equipment used, and the anticipated duration of the work to be performed. Spot market contracts generally provide for the drilling of a single well and typically permit the client to terminate on short notice. We enter into longer-term drilling contracts for our newly constructed rigs and/or during periods of high rig demand. Currently, we have contracts with original terms of six months to four years in duration.

6

As of March 31, 2015, we have 19 drilling rigs earning under term contracts, which if not renewed prior to the end of their terms, will expire as follows:

Term Contract Expiration by Period | ||||||||||||

Total Term Contracts | Within 6 Months | 6 Months to 1 Year | 1 Year to 18 Months | |||||||||

United States | 15 | 5 | 6 | 4 | ||||||||

Colombia | 4 | 4 | — | — | ||||||||

19 | 9 | 6 | 4 | |||||||||

With most long-term drilling contracts, we are entitled to receive a full or reduced rate of revenue from our clients if they choose to place a rig on standby or to early terminate the contract before its original expiration term. Generally, these revenues are billed and collected over the remaining term of the contract, as the rig is placed on standby rather than fully released from the contract, and thus may go back to work at the client's decision any time before the end of the contract. Some of our drilling contracts contain "make-whole" provisions whereby if we are able to secure additional work for the rig with another client, then each party is entitled to a make-whole payment. If the dayrates under the new contract are less than the dayrates in the original contract, we would be entitled to a reduced revenue dayrate from the terminating client, and likewise, the terminating client may be entitled to a payment from us if the new contract dayrates exceed those of the original contract. A client may also choose to early terminate the contract and make an upfront early termination payment based on a per day rate for the remaining term of the contract. Revenues derived from rigs placed on standby or from the early termination of long-term drilling contracts are deferred and recognized as the amounts become fixed or determinable, over the remainder of the original term or when the rig is sold.

In response to the dramatic decline in oil prices during recent months, term contracts for 16 of our drilling rigs have been early terminated, including nine of our 19 drilling rigs that are currently earning revenues under term contracts, resulting in approximately $53.1 million of early termination revenues. Revenues derived from these early terminations are deferred and recognized over the remainder of the original term of the drilling contracts. We recognized $11.3 million of revenue for early termination payments in the first quarter of 2015 and $0.3 million in the fourth quarter of 2014.

Unbilled Accounts Receivable

The asset “unbilled receivables” represents revenues we have recognized in excess of amounts billed on drilling contracts and production services completed but not yet invoiced. We typically invoice our clients at 15-day intervals during the performance of daywork drilling contracts and upon completion of the daywork contract. Turnkey drilling contracts are invoiced upon completion of the contract.

Our unbilled receivables totaled $30.0 million at March 31, 2015, of which $28.7 million represented revenue recognized but not yet billed on daywork drilling contracts in progress at March 31, 2015 and $1.3 million related to unbilled receivables for our Production Services Segment. At December 31, 2014, our unbilled receivables totaled $38.0 million, of which $32.8 million represented revenue recognized but not yet billed on daywork drilling contracts in progress at December 31, 2014, $0.8 million related to turnkey drilling contract revenues, and $4.4 million related to unbilled receivables for our Production Services Segment.

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets include items such as insurance, rent deposits and fees. We routinely expense these items in the normal course of business over the periods these expenses benefit. Prepaid expenses and other current assets also include the current portion of prepaid taxes in Colombia which are creditable against future income taxes and the current portion of deferred mobilization costs for certain drilling contracts that are recognized on a straight-line basis over the contract term.

Intangible Assets

Substantially all of our intangible assets were recorded in connection with the acquisitions of production services businesses and are subject to amortization. We evaluate for potential impairment of long-lived tangible and intangible

7

assets subject to amortization when indicators of impairment are present. Circumstances that could indicate a potential impairment include significant adverse changes in industry trends, economic climate, legal factors, and an adverse action or assessment by a regulator. More specifically, significant adverse changes in industry trends include significant declines in revenue rates, utilization rates, oil and natural gas market prices and industry rig counts. In performing an impairment evaluation, we estimate the future undiscounted net cash flows from the use and eventual disposition of long-lived tangible and intangible assets grouped at the lowest level that cash flows can be identified. For our Production Services Segment, we perform an impairment evaluation and estimate future undiscounted cash flows for the individual reporting units (well servicing, wireline and coiled tubing). If the sum of the estimated future undiscounted net cash flows is less than the carrying amount of the asset group, then we would determine the fair value of the asset group. The amount of an impairment charge would be measured as the difference between the carrying amount and the fair value of these assets. The assumptions used in the impairment evaluation for long-lived assets are inherently uncertain and require management judgment.

Other Long-Term Assets

Other long-term assets consist of noncurrent prepaid taxes in Colombia which are creditable against future income taxes, debt issuance costs net of amortization, cash deposits related to the deductibles on our workers’ compensation insurance policies and the long-term portion of deferred mobilization costs.

Other Current Liabilities

Our other accrued expenses include accruals for items such as property tax, sales tax, Colombian net wealth tax, professional and other fees. We routinely expense these items in the normal course of business over the periods these expenses benefit.

Other Long-Term Liabilities

Our other long-term liabilities consist of the noncurrent portion of liabilities associated with our long-term compensation plans and other deferred liabilities.

Related-Party Transactions

During the three months ended March 31, 2015 and 2014, the Company paid approximately $7,000 and $107,000, respectively, for trucking and equipment rental services, which represented arms-length transactions, to Gulf Coast Lease Service, a trucking and construction company. Joe Freeman, our Senior Vice President of Well Servicing, serves as the President of Gulf Coast Lease Services, which is owned and operated by Mr. Freeman's two sons. Mr. Freeman does not receive compensation from Gulf Coast Lease Service, and he serves primarily in an advisory role to his sons.

Recently Issued Accounting Standards

Revenue Recognition. In May 2014, the FASB issued ASU No. 2014-09, a comprehensive new revenue recognition standard that will supersede nearly all existing revenue recognition guidance. The standard outlines a single comprehensive model for revenue recognition based on the core principle that a company will recognize revenue when promised goods or services are transferred to clients, in an amount that reflects the consideration to which an entity expects to be entitled in exchange for those goods or services. We are required to apply this new standard beginning with our first quarterly filing in 2017. We are currently evaluating the potential impact of this guidance, but at this time, do not expect that the adoption of this new standard will have a material effect on our financial position or results of operations.

Debt Issuance Costs. On April 7, 2015, the FASB issued Accounting Standards Update ASU No. 2015-03, Simplifying the Presentation of Debt Issuance Costs, which requires that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and measurement guidance for debt issuance costs are not affected by the amendments in this ASU. This ASU requires retrospective adoption and will be effective for us beginning with our first quarterly filing in 2016. Early adoption is permitted. We do not expect this adoption to have a material impact on our financial statements.

8

Reclassifications

Certain amounts in the financial statements for the prior years have been reclassified to conform to the current year’s presentation.

2. Property and Equipment

During the three months ended March 31, 2015 and 2014, we had capital expenditures of $48.8 million and $36.9 million, respectively, which includes $0.7 million and $48,000, respectively, of capitalized interest costs incurred during the construction periods of new-build drilling rigs and other drilling equipment. Capital expenditures during 2015 primarily relate to our five new-build drilling rigs which began construction during 2014, as well as unit additions to our production services fleets. As of March 31, 2015 and December 31, 2014, capital expenditures incurred for property and equipment not yet placed in service was $94.9 million and $82.7 million, respectively.

During the three months ended March 31, 2015, we recorded total losses on disposition of our property and equipment of $1.2 million in our drilling and production services costs and expenses, primarily for the sales of 20 of our mechanical and lower horsepower electric drilling rigs and other drilling equipment which we sold in March 2015 for aggregate net proceeds of $23.3 million, $17.2 million of which was recognized as a receivable at March 31, 2015. During the three months ended March 31, 2014, we recorded total gains on disposition of our property and equipment of $1.4 million in our drilling and production services costs and expenses, $1.1 million of which was related to the sale of our trucking assets in February 2014.

We recorded impairment charges on our property and equipment of $6.0 million during the three months ended March 31, 2015 in order to reduce the carrying values of two drilling rigs, two wireline units and other drilling equipment which we have classified as held for sale, to their estimated fair values, based on expected sales prices. As of March 31, 2015, our condensed consolidated balance sheet reflects assets held for sale of $4.6 million, which represents five drilling rigs, six wireline units and one real estate property. In April 2015, we sold one drilling rig for $1.5 million, for which we recognized a gain on sale of $0.7 million.

We evaluate for potential impairment of long-lived tangible and intangible assets subject to amortization when indicators of impairment are present. Circumstances that could indicate a potential impairment include significant adverse changes in industry trends, economic climate, legal factors, and an adverse action or assessment by a regulator. More specifically, significant adverse changes in industry trends include significant declines in revenue rates, utilization rates, oil and natural gas market prices and industry rig counts. In performing an impairment evaluation, we estimate the future undiscounted net cash flows from the use and eventual disposition of long-lived tangible and intangible assets grouped at the lowest level that cash flows can be identified. For our Production Services Segment, we perform an impairment evaluation and estimate future undiscounted cash flows for the individual reporting units (well servicing, wireline and coiled tubing). For our Drilling Services Segment, we perform an impairment evaluation and estimate future undiscounted cash flows for individual domestic drilling rig assets and for our Colombian drilling rig assets as a group. If the sum of the estimated future undiscounted net cash flows is less than the carrying amount of the asset group, then we would determine the fair value of the asset group. The amount of an impairment charge would be measured as the difference between the carrying amount and the fair value of these assets. The assumptions used in the impairment evaluation for long-lived assets are inherently uncertain and require management judgment.

Since October 2014, domestic and international oil prices have declined significantly which resulted in a downturn in our industry. Mechanical and lower horsepower drilling rigs are the most impacted by the industry downturn and are typically the first rigs to become idle. During the first quarter of 2015, we sold 20 of our mechanical and lower horsepower electric rigs, and as of March 31, 2015, we have six remaining in our fleet, and an additional five classified as held for sale.

We performed impairment testing on all the mechanical and lower horsepower drilling rigs in our fleet as of December 31, 2014, which resulted in a total impairment of $71.0 million to reduce the carrying value of these assets to their estimated fair values. We also performed an impairment test on our drilling rigs in Colombia as of December 31, 2014. Our net book value in these rigs was $87.5 million and our analysis indicated that the carrying value of these assets was recoverable and thus there was no impairment present at December 31, 2014. Our assessment of the current

9

market conditions, our projected financial performance and the industry outlook has led us to conclude that no major changes have occurred that would warrant further impairment testing as of March 31, 2015.

In order to estimate our future undiscounted cash flows from the use and eventual disposition of these assets, we incorporated probabilities of selling these rigs in the near term, versus working them at a significantly reduced expected rate of utilization through the end of their remaining useful lives. The most significant assumptions used in our analysis are the expected margin per day and utilization, as well as the estimated proceeds upon any future sale or disposal of the rig. Although we believe the assumptions and estimates used in our analysis are reasonable and appropriate, different assumptions and estimates could materially impact the analysis and resulting conclusions. If the demand for our drilling services remains at current levels or declines further and any of our rigs become idle for an extended amount of time, including our rigs in Colombia for which the current term contract is set to expire by mid-2015, then our estimated cash flows may further decrease, and the probability of a near term sale may increase. If any of the foregoing were to occur, we may incur additional impairment charges.

3. Debt

Our debt consists of the following (amounts in thousands):

March 31, 2015 | December 31, 2014 | ||||||

Senior secured revolving credit facility | $ | 130,000 | $ | 155,000 | |||

Senior notes | 300,000 | 300,000 | |||||

Other | — | 80 | |||||

430,000 | 455,080 | ||||||

Less current portion | — | (27 | ) | ||||

$ | 430,000 | $ | 455,053 | ||||

Senior Secured Revolving Credit Facility

We have a credit agreement, as amended on September 22, 2014, with Wells Fargo Bank, N.A. and a syndicate of lenders which provides for a senior secured revolving credit facility, with sub-limits for letters of credit and swing-line loans, of up to an aggregate principal amount of $350 million, all of which matures on September 22, 2019 (the “Revolving Credit Facility”). In addition, at our request, and with the lenders' consent, the aggregate commitments of the lenders under the Revolving Credit Facility may be increased up to an additional $100 million provided that no default exists, all representations and warranties are true and correct, and compliance with financial covenants as set forth in the Revolving Credit Facility is met immediately prior to and after giving effect thereto. The Revolving Credit Facility contains customary mandatory prepayments from the proceeds of certain asset dispositions or debt issuances, which are applied to reduce outstanding revolving and swing-line loans and letter of credit exposure, but in no event will reduce the borrowing availability under the Revolving Credit Facility to less than $350 million.

Borrowings under the Revolving Credit Facility bear interest, at our option, at the LIBOR rate or at the bank prime rate, plus an applicable per annum margin that ranges from 2.0% to 3.0% and 1.0% to 2.0%, respectively. The LIBOR margin and bank prime rate margin currently in effect are 2.25% and 1.25%, respectively. The Revolving Credit Facility requires a commitment fee due quarterly based on the average daily unused amount of the commitments of the lenders, a fronting fee due for each letter of credit issued, and a quarterly letter of credit fee due based on the average undrawn amount of letters of credit outstanding during such period.

Our obligations under the Revolving Credit Facility are secured by substantially all of our domestic assets (including equity interests in Pioneer Global Holdings, Inc. and 65% of the outstanding equity interests of any first-tier foreign subsidiaries owned by Pioneer Global Holdings, Inc., but excluding any equity interest in, and any assets of, Pioneer Services Holdings, LLC) and are guaranteed by certain of our domestic subsidiaries, including Pioneer Global Holdings, Inc. Borrowings under the Revolving Credit Facility are available for acquisitions, working capital and other general corporate purposes.

10

As of April 27, 2015, we had $110.0 million outstanding under our Revolving Credit Facility and $18.5 million in committed letters of credit, which resulted in borrowing availability of $221.5 million under our Revolving Credit Facility. There are no limitations on our ability to access this borrowing capacity provided there is no default, all representations and warranties are true and correct, and compliance with financial covenants under the Revolving Credit Facility is maintained. At March 31, 2015, we were in compliance with our financial covenants under the Revolving Credit Facility. Our total consolidated leverage ratio was 1.9 to 1.0, our senior consolidated leverage ratio was 0.6 to 1.0, and our interest coverage ratio was 7.3 to 1.0. The financial covenants contained in our Revolving Credit Facility include the following:

• | A maximum total consolidated leverage ratio that cannot exceed 4.00 to 1.00; |

• | A maximum senior consolidated leverage ratio, which excludes unsecured and subordinated debt, that cannot exceed 2.50 to 1.00; |

• | A minimum interest coverage ratio that cannot be less than 2.50 to 1.00; and |

• | If our senior consolidated leverage ratio is greater than 2.00 to 1.00 at the end of any fiscal quarter, our minimum asset coverage ratio cannot be less than 1.00 to 1.00. |

The Revolving Credit Facility does not restrict capital expenditures or repurchases of capital stock as long as (a) no event of default exists under the Revolving Credit Facility or would result from such capital expenditures or repurchases of capital stock, (b) after giving effect to such capital expenditures or repurchases of capital stock there is availability under the Revolving Credit Facility equal to or greater than $25 million and (c) the senior consolidated leverage ratio as of the last day of the most recent reported fiscal quarter is less than 2.00 to 1.00. In addition, the repurchase of capital stock requires, on a pro-forma basis, compliance with the maximum total leverage ratio and minimum interest coverage ratio as set forth in the Revolving Credit Facility, both before and after giving effect to such repurchase. If the senior consolidated leverage ratio as of the last day of the most recent reported fiscal quarter is equal to or greater than 2.00 to 1.00, then capital expenditures are limited to $100 million for the fiscal year. The capital expenditure threshold may be increased by any unused portion of the capital expenditure threshold from the immediate preceding fiscal year up to $30 million.

At March 31, 2015, our senior consolidated leverage ratio was not greater than 2.00 to 1.00 and therefore, we were not subject to the capital expenditure threshold restrictions listed above.

The Revolving Credit Facility has additional restrictive covenants that, among other things, limit the incurrence of additional debt, investments, liens, dividends, acquisitions, prepayments of indebtedness, asset dispositions, mergers and consolidations, transactions with affiliates, hedging contracts, sale leasebacks and other matters customarily restricted in such agreements. In addition, the Revolving Credit Facility contains customary events of default, including without limitation, payment defaults, breaches of representations and warranties, covenant defaults, cross-defaults to certain other material indebtedness in excess of specified amounts, certain events of bankruptcy and insolvency, judgment defaults in excess of specified amounts, failure of any guaranty or security document supporting the credit agreement and change of control.

Senior Notes

In March 2010 and November 2011, we issued an aggregate $425 million of unregistered senior notes with a coupon interest rate of 9.875% that were set to mature in 2018 (the “2010 and 2011 Senior Notes”). The net proceeds from the 2010 issuance were used to repay a portion of the borrowings outstanding under our Revolving Credit Facility and a portion of the net proceeds from the 2011 issuance were used to fund the acquisition of the coiled tubing business in December 2011. In order to reduce our overall interest expense and lengthen the overall maturity of our senior indebtedness, during 2014, we redeemed all of our outstanding 2010 and 2011 Senior Notes, funded primarily by proceeds from the issuance of our 2014 Senior Notes and additional borrowings under our Revolving Credit Facility, as well as some cash on hand.

In March 2014, we issued $300 million of unregistered senior notes with a coupon interest rate of 6.125% that are due in 2022 (the “2014 Senior Notes”). The 2014 Senior Notes were sold at 100% of their face value. After deductions were made for the $6.1 million for underwriters’ fees and other debt offering costs, we received $293.9 million of net proceeds which were used to fund the repayment of $300 million of aggregate principal amount of 2010 and 2011

11

Senior Notes in March and May 2014. During the three months ended March 31, 2014, we recognized a loss on debt extinguishment of $7.9 million for the redemption of $99.5 million of 2010 and 2011 Senior Notes in March 2014, which included redemption premiums of $5.5 million, $1.2 million of net unamortized discount and $1.2 million of unamortized debt issuance costs.

The 2014 Senior Notes will mature on March 15, 2022 with interest due semi-annually in arrears on March 15 and September 15 of each year. We have the option to redeem the 2014 Senior Notes, in whole or in part, at any time on or after March 15, 2017 in each case at the redemption price specified in the Indenture dated March 18, 2014 (the Indenture) plus any accrued and unpaid interest and any additional interest (as defined in the Indenture) thereon to the date of redemption. Prior to March 15, 2017, we may also redeem the 2014 Senior Notes, in whole or in part, at a “make-whole” redemption price specified in the 2014 Indenture, plus any accrued and unpaid interest and any additional interest thereon to the date of redemption. In addition, prior to March 15, 2017, we may, on one or more occasions, redeem up to 35% of the aggregate principal amount of the 2014 Senior Notes at a redemption price equal to 106.125% of the principal amount thereof, plus accrued and unpaid interest and additional interest, if any, to the redemption date, with the net cash proceeds of certain equity offerings, provided that at least 65% of the aggregate principal amount of the 2014 Senior Notes remains outstanding after the occurrence of such redemption and that the redemption occurs within 120 days of the date of the closing of such equity offering.

In accordance with a registration rights agreement with the holders of our 2014 Senior Notes, we filed an exchange offer registration statement on Form S-4 with the Securities and Exchange Commission that became effective on October 2, 2014. The exchange offer registration statement enabled the holders of our Senior Notes to exchange their senior notes for publicly registered notes with substantially identical terms. References to the “Senior Notes” herein include the senior notes issued in the exchange offer.

If we experience a change of control (as defined in the Indenture), we will be required to make an offer to each holder of the Senior Notes to repurchase all or any part of the Senior Notes at a purchase price equal to 101% of the principal amount of each Senior Note, plus accrued and unpaid interest, if any to the date of repurchase. If we engage in certain asset sales, within 365 days of such sale we will be required to use the net cash proceeds from such sale, to the extent we do not reinvest those proceeds in our business, to make an offer to repurchase the Senior Notes at a price equal to 100% of the principal amount of each Senior Note, plus accrued and unpaid interest to the repurchase date.

The Indenture, among other things, limits our ability and the ability of certain of our subsidiaries to:

• | pay dividends on stock, repurchase stock, redeem subordinated indebtedness or make other restricted payments and investments; |

• | incur, assume or guarantee additional indebtedness or issue preferred or disqualified stock; |

• | create liens on our or their assets; |

• | enter into sale and leaseback transactions; |

• | sell or transfer assets; |

• | pay dividends, engage in loans, or transfer other assets from certain of our subsidiaries; |

• | consolidate with or merge with or into, or sell all or substantially all of our properties to any other person; |

• | enter into transactions with affiliates; and |

• | enter into new lines of business. |

The Senior Notes are not subject to any sinking fund requirements. The Senior Notes are fully and unconditionally guaranteed, jointly and severally, on a senior unsecured basis by certain of our existing domestic subsidiaries and by certain of our future domestic subsidiaries. (See Note 9, Guarantor/Non-Guarantor Condensed Consolidated Financial Statements.)

Debt Issuance Costs

Costs incurred in connection with the Revolving Credit Facility were capitalized and are being amortized using the straight-line method over the term of the Revolving Credit Facility which matures in September 2019. Costs incurred

12

in connection with the issuance of our 2014 Senior Notes were capitalized and are being amortized using the straight-line method (which approximates amortization using the interest method) over the term of the Senior Notes which mature in March 2022.

Capitalized debt costs related to the issuance of our long-term debt were $9.4 million and $9.8 million as of March 31, 2015 and December 31, 2014, respectively. We recognized $0.4 million and $0.6 million of associated amortization during the three months ended March 31, 2015 and 2014, respectively.

4. | Fair Value of Financial Instruments |

ASC Topic 820, Fair Value Measurements and Disclosures, defines fair value and provides a hierarchal framework associated with the level of subjectivity used in measuring assets and liabilities at fair value.

At March 31, 2015 and December 31, 2014, our financial instruments consist primarily of cash, trade and other receivables, trade payables and long-term debt. The carrying value of cash, trade and other receivables, and trade payables are considered to be representative of their respective fair values due to the short-term nature of these instruments.

The fair value of our long-term debt is estimated using a discounted cash flow analysis, based on rates that we believe we would currently pay for similar types of debt instruments. This discounted cash flow analysis is based on inputs defined by ASC Topic 820 as level 2 inputs, which are observable inputs for similar types of debt instruments. The following table presents the supplemental fair value information about long-term debt at March 31, 2015 and December 31, 2014 (amounts in thousands):

March 31, 2015 | December 31, 2014 | ||||||||||||||

Carrying Amount | Fair Value | Carrying Amount | Fair Value | ||||||||||||

Total debt | $ | 430,000 | $ | 366,634 | $ | 455,080 | $ | 415,785 | |||||||

5. | Earnings Per Common Share |

The following table presents a reconciliation of the numerators and denominators of the basic income per share and diluted income per share computations (amounts in thousands, except per share data):

Three months ended March 31, | |||||||

2015 | 2014 | ||||||

Basic | |||||||

Net loss | $ | (12,019 | ) | $ | (2,579 | ) | |

Weighted-average shares | 63,991 | 62,542 | |||||

Loss per common share—Basic | $ | (0.19 | ) | $ | (0.04 | ) | |

Diluted | |||||||

Net loss | $ | (12,019 | ) | $ | (2,579 | ) | |

Weighted-average shares | |||||||

Outstanding | 63,991 | 62,542 | |||||

Diluted effect of outstanding stock options, restricted stock and restricted stock unit awards | — | — | |||||

63,991 | 62,542 | ||||||

Loss per common share—Diluted | $ | (0.19 | ) | $ | (0.04 | ) | |

Potentially dilutive stock options, restricted stock and restricted stock unit awards representing a total of 5,104,618 and 4,146,460 shares of common stock for the three months ended March 31, 2015 and 2014, respectively, were excluded from the computation of diluted weighted average shares outstanding due to their antidilutive effect.

13

6. | Stock-Based Compensation Plans |

We grant stock option and restricted stock awards with vesting based on time of service conditions. We also grant restricted stock unit awards with vesting based on time of service conditions, and in certain cases, subject to performance and market conditions. We recognize compensation cost for stock option, restricted stock and restricted stock unit awards based on the fair value estimated in accordance with ASC Topic 718, Compensation—Stock Compensation. For our awards with graded vesting, we recognize compensation expense on a straight-line basis over the service period for each separately vesting portion of the award as if the award was, in substance, multiple awards.

The following table summarizes the compensation expense recognized for stock option, restricted stock and restricted stock unit awards during the three months ended March 31, 2015 and 2014 (amounts in thousands):

Three months ended March 31, | |||||||

2015 | 2014 | ||||||

Stock option awards | $ | 264 | $ | 343 | |||

Restricted stock awards | 124 | 153 | |||||

Restricted stock unit awards | 17 | 1,360 | |||||

$ | 405 | $ | 1,856 | ||||

Stock Options

We grant stock option awards which generally become exercisable over a three-year period and expire ten years after the date of grant. Our stock-based compensation plans require that all stock option awards have an exercise price that is not less than the fair market value of our common stock on the date of grant. We issue shares of our common stock when vested stock option awards are exercised.

We estimate the fair value of each option grant on the date of grant using a Black-Scholes option pricing model. The following table summarizes the assumptions used in the Black-Scholes option pricing model based on a weighted-average calculation for the three months ended March 31, 2015 and 2014:

Three months ended March 31, | |||||

2015 | 2014 | ||||

Expected volatility | 64 | % | 66 | % | |

Risk-free interest rates | 1.4 | % | 1.7 | % | |

Expected life in years | 5.52 | 5.49 | |||

Options granted | 341,638 | 221,440 | |||

Grant-date fair value | $2.31 | $4.87 | |||

The assumptions used in the Black-Scholes option pricing model are based on multiple factors, including historical exercise patterns of homogeneous groups with respect to exercise and post-vesting employment termination behaviors, expected future exercising patterns for these same homogeneous groups and volatility of our stock price. As we have not declared dividends since we became a public company, we did not use a dividend yield. In each case, the actual value that will be realized, if any, will depend on the future performance of our common stock and overall stock market conditions. There is no assurance the value an optionee actually realizes will be at or near the value we have estimated using the Black-Scholes options-pricing model.

During the three months ended March 31, 2015 and 2014, 156,500 and 46,900 stock options were exercised at a weighted-average exercise price of $3.84 and $5.90, respectively. We receive a tax deduction for certain stock option exercises during the period the options are exercised, generally for the excess of the fair market value of our stock on the date of exercise over the exercise price of the options. In accordance with ASC Topic 718, we reported all excess tax benefits resulting from the exercise of stock options as financing cash flows in our condensed consolidated statement of cash flows.

14

Restricted Stock

Historically, we have generally granted restricted stock awards that vest over a three-year period with a fair value based on the closing price of our common stock on the date of the grant. However, beginning in 2013, we began granting restricted stock awards with a vesting period of one year. When restricted stock awards are granted, or when restricted stock unit awards are converted to restricted stock, shares of our common stock are considered issued, but subject to certain restrictions. We did not grant any restricted stock awards during the three months ended March 31, 2015 or 2014.

Restricted Stock Units

We grant restricted stock unit awards with vesting based on time of service conditions only (“time-based RSUs”), and we grant restricted stock unit awards with vesting based on time of service, which are also subject to performance and market conditions (“performance-based RSUs”). Shares of our common stock are issued to recipients of restricted stock units only when they have satisfied the applicable vesting conditions.

The following table summarizes the number and weighted-average grant-date fair value of the restricted stock unit awards granted during the three months ended March 31, 2015 and 2014:

Three months ended March 31, | ||||||||

2015 | 2014 | |||||||

Time-based RSUs: | ||||||||

Time-based RSUs granted | 151,919 | 347,335 | ||||||

Weighted-average grant-date fair value | $ | 4.08 | $ | 8.44 | ||||

Performance-based RSUs: | ||||||||

Performance-based RSUs granted | 294,666 | 321,606 | ||||||

Weighted-average grant-date fair value | $ | 4.49 | $ | 9.90 | ||||

Our time-based RSUs generally vest over a three-year period, with fair values based on the closing price of our common stock on the date of grant.

Our performance-based RSUs generally cliff vest after 39 months from the date of grant and are granted at a target number of issuable shares, for which the final number of shares of common stock is adjusted based on our actual achievement levels that are measured against predetermined performance conditions. The number of shares of common stock awarded will be based upon the Company’s achievement in certain performance conditions, as compared to a predefined peer group, over the performance period, generally three years.

Approximately one-third of the performance-based RSUs granted during 2012 and 2013, and half of the performance-based RSUs granted during 2014 and 2015, are subject to a market condition based on relative total shareholder return, as compared to that of our predetermined peer group, and therefore the fair value of these awards is measured using a Monte Carlo simulation model. Compensation expense for awards with a market condition is reduced only for estimated forfeitures; no adjustment to expense is otherwise made, regardless of the number of shares issued. The remaining performance-based RSUs are subject to performance conditions, based on our EBITDA and return on capital employed, relative to our predetermined peer group, and therefore the fair value is based on the closing price of our common stock on the date of grant, applied to the estimated number of shares that will be awarded. Compensation expense ultimately recognized for awards with performance conditions will be equal to the fair value of the restricted stock unit award based on the actual outcome of the service and performance conditions.

In April 2015, we determined that 64.1% of the target number of shares granted during 2012 were actually earned based on the Company’s achievement of certain performance measures, as compared to the predefined peer group, over the performance period from January 1, 2012 through December 31, 2014. The performance-based RSUs granted during 2012 vested and were converted to common stock at the end of April 2015. As of March 31, 2015, we estimated that our actual achievement level for the performance-based RSUs granted during 2013, 2014 and 2015 will be approximately 80%, 100% and 100% of the predetermined performance conditions, respectively.

15

7. | Segment Information |

We have two operating segments referred to as the Drilling Services Segment and the Production Services Segment which is the basis management uses for making operating decisions and assessing performance.

Drilling Services Segment—Our Drilling Services Segment provides contract land drilling services to a diverse group of oil and gas exploration and production companies through our four drilling divisions in the US, and internationally in Colombia.

As of March 31, 2015, the drilling rigs in our fleet, excluding rigs classified as held for sale, are assigned to the following divisions:

Drilling Division | Rig Count | |

South Texas | 10 | |

West Texas | 5 | |

North Dakota | 10 | |

Appalachia | 4 | |

Colombia | 8 | |

37 | ||

Production Services Segment—Our Production Services Segment provides a range of services to exploration and production companies, including well servicing, wireline services and coiled tubing services. Our production services operations are concentrated in the major United States onshore oil and gas producing regions in the Mid-Continent and Rocky Mountain states and in the Gulf Coast, both onshore and offshore. As of March 31, 2015, we have a fleet of 119 well servicing rigs, consisting of 108 rigs with 550 horsepower and 11 rigs with 600 horsepower, 126 wireline units and 17 coiled tubing units.

The following tables set forth certain financial information for our two operating segments and corporate as of and for the three months ending March 31, 2015 and 2014 (amounts in thousands):

As of and for the three months ended March 31, 2015 | |||||||||||||||

Drilling Services Segment | Production Services Segment | Corporate | Total | ||||||||||||

Identifiable assets | $ | 697,248 | $ | 380,036 | $ | 46,566 | $ | 1,123,850 | |||||||

Revenues | $ | 98,415 | $ | 95,399 | $ | — | $ | 193,814 | |||||||

Operating costs | 63,455 | 68,742 | — | 132,197 | |||||||||||

Segment margin | $ | 34,960 | $ | 26,657 | $ | — | $ | 61,617 | |||||||

Depreciation and amortization | $ | 23,600 | $ | 17,833 | $ | 349 | $ | 41,782 | |||||||

Capital expenditures | $ | 33,056 | $ | 15,457 | $ | 303 | $ | 48,816 | |||||||

As of and for the three months ended March 31, 2014 | |||||||||||||||

Drilling Services Segment | Production Services Segment | Corporate | Total | ||||||||||||

Identifiable assets | $ | 780,786 | $ | 403,923 | $ | 241,668 | $ | 1,426,377 | |||||||

Revenues | $ | 117,957 | $ | 121,077 | $ | — | $ | 239,034 | |||||||

Operating costs | 76,338 | 77,752 | — | 154,090 | |||||||||||

Segment margin | $ | 41,619 | $ | 43,325 | $ | — | $ | 84,944 | |||||||

Depreciation and amortization | $ | 29,239 | $ | 16,019 | $ | 268 | $ | 45,526 | |||||||

Capital expenditures | $ | 21,256 | $ | 15,343 | $ | 318 | $ | 36,917 | |||||||

16

The following table reconciles the segment profits reported above to income from operations as reported on the consolidated statements of operations for the three months ended March 31, 2015 and 2014 (amounts in thousands):

Three months ended March 31, | |||||||

2015 | 2014 | ||||||

Segment margin | $ | 61,617 | $ | 84,944 | |||

Depreciation and amortization | (41,782 | ) | (45,526 | ) | |||

General and administrative | (21,860 | ) | (24,483 | ) | |||

Bad debt recovery | (319 | ) | 124 | ||||

Impairment charges | (5,990 | ) | — | ||||

Gain on litigation | — | 2,876 | |||||

Income from operations | $ | (8,334 | ) | $ | 17,935 | ||

The following table sets forth certain financial information for our international operations in Colombia as of and for the three months ended March 31, 2015 and 2014 (amounts in thousands):

As of and for the three months ended March 31, | |||||||

2015 | 2014 | ||||||

Identifiable assets | $ | 135,184 | $ | 153,158 | |||

Revenues | $ | 19,961 | $ | 22,164 | |||

Identifiable assets for our international operations in Colombia include five drilling rigs that are owned by our Colombia subsidiary and three drilling rigs that are owned by one of our domestic subsidiaries and leased to our Colombia subsidiary.

8. | Commitments and Contingencies |

In connection with our operations in Colombia, our foreign subsidiaries have obtained bonds for bidding on drilling contracts, performing under drilling contracts, and remitting customs and importation duties. We have guaranteed payments of $39.0 million relating to our performance under these bonds as of March 31, 2015.

Due to the nature of our business, we are, from time to time, involved in litigation or subject to disputes or claims related to our business activities, including workers’ compensation claims and employment-related disputes. Legal costs relating to these matters are expensed as incurred. In the opinion of our management, none of the pending litigation, disputes or claims against us will have a material adverse effect on our financial condition, results of operations or cash flow from operations.

9. | Guarantor/Non-Guarantor Condensed Consolidated Financial Statements |

Our Senior Notes are fully and unconditionally guaranteed, jointly and severally, on a senior unsecured basis by all existing domestic subsidiaries, except for Pioneer Services Holdings, LLC. The subsidiaries that generally operate our non-U.S. business concentrated in Colombia do not guarantee our Senior Notes. The non-guarantor subsidiaries do not have any payment obligations under the Senior Notes, the guarantees or the Indenture.

In the event of a bankruptcy, liquidation or reorganization of any non-guarantor subsidiary, such non-guarantor subsidiary will pay the holders of its debt and other liabilities, including its trade creditors, before it will be able to distribute any of its assets to us. In the future, any non-U.S. subsidiaries, immaterial subsidiaries and subsidiaries that we designate as unrestricted subsidiaries under the Indenture will not guarantee the Senior Notes. As of March 31, 2015, there were no restrictions on the ability of subsidiary guarantors to transfer funds to the parent company.

As a result of the guarantee arrangements, we are presenting the following condensed consolidated balance sheets, statements of operations and statements of cash flows of the issuer, the guarantor subsidiaries and the non-guarantor subsidiaries.

17

CONDENSED CONSOLIDATED BALANCE SHEETS

(unaudited, in thousands)

March 31, 2015 | |||||||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Eliminations | Consolidated | |||||||||||||||

ASSETS | |||||||||||||||||||

Current assets: | |||||||||||||||||||

Cash and cash equivalents | 29,518 | (2,789 | ) | 8,949 | — | $ | 35,678 | ||||||||||||

Receivables, net of allowance | 1,498 | 135,621 | 35,130 | (765 | ) | 171,484 | |||||||||||||

Intercompany receivable (payable) | (24,836 | ) | 51,588 | (26,752 | ) | — | — | ||||||||||||

Deferred income taxes | 643 | 6,507 | 1,379 | — | 8,529 | ||||||||||||||

Inventory | — | 6,741 | 6,945 | — | 13,686 | ||||||||||||||

Assets held for sale | — | 4,606 | — | — | 4,606 | ||||||||||||||

Prepaid expenses and other current assets | 975 | 4,917 | 1,518 | — | 7,410 | ||||||||||||||

Total current assets | 7,798 | 207,191 | 27,169 | (765 | ) | 241,393 | |||||||||||||

Net property and equipment | 4,134 | 750,412 | 85,711 | (750 | ) | 839,507 | |||||||||||||

Investment in subsidiaries | 780,143 | 112,204 | — | (892,347 | ) | — | |||||||||||||

Intangible assets, net of accumulated amortization | — | 22,238 | — | — | 22,238 | ||||||||||||||

Noncurrent deferred income taxes | 116,290 | — | 2,662 | (116,290 | ) | 2,662 | |||||||||||||

Other long-term assets | 9,871 | 1,796 | 6,383 | — | 18,050 | ||||||||||||||

Total assets | $ | 918,236 | $ | 1,093,841 | $ | 121,925 | $ | (1,010,152 | ) | $ | 1,123,850 | ||||||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||||||||||

Current liabilities: | |||||||||||||||||||

Accounts payable | $ | 721 | $ | 44,009 | $ | 3,243 | — | $ | 47,973 | ||||||||||

Current portion of long-term debt | — | — | — | — | — | ||||||||||||||

Deferred revenues | — | 33,920 | — | — | 33,920 | ||||||||||||||

Accrued expenses | 3,263 | 52,664 | 6,282 | (765 | ) | 61,444 | |||||||||||||

Total current liabilities | 3,984 | 130,593 | 9,525 | (765 | ) | 143,337 | |||||||||||||

Long-term debt, less current portion | 430,000 | — | — | — | 430,000 | ||||||||||||||

Noncurrent deferred income taxes | (313 | ) | 178,827 | — | (116,290 | ) | 62,224 | ||||||||||||

Other long-term liabilities | 733 | 4,278 | 196 | — | 5,207 | ||||||||||||||

Total liabilities | 434,404 | 313,698 | 9,721 | (117,055 | ) | 640,768 | |||||||||||||

Total shareholders’ equity | 483,832 | 780,143 | 112,204 | (893,097 | ) | 483,082 | |||||||||||||

Total liabilities and shareholders’ equity | $ | 918,236 | $ | 1,093,841 | $ | 121,925 | $ | (1,010,152 | ) | $ | 1,123,850 | ||||||||

December 31, 2014 | |||||||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Eliminations | Consolidated | |||||||||||||||

ASSETS | |||||||||||||||||||

Current assets: | |||||||||||||||||||

Cash and cash equivalents | $ | 27,688 | $ | (5,516 | ) | $ | 12,752 | $ | — | $ | 34,924 | ||||||||

Receivables, net of allowance | 1,641 | 151,048 | 37,512 | — | 190,201 | ||||||||||||||

Intercompany receivable (payable) | (24,836 | ) | 55,567 | (30,728 | ) | (3 | ) | — | |||||||||||

Deferred income taxes | 1,827 | 8,196 | 975 | — | 10,998 | ||||||||||||||

Inventory | — | 7,208 | 6,909 | — | 14,117 | ||||||||||||||

Assets held for sale | — | 9,909 | — | — | 9,909 | ||||||||||||||

Prepaid expenses and other current assets | 1,217 | 6,554 | 1,154 | — | 8,925 | ||||||||||||||

Total current assets | 7,537 | 232,966 | 28,574 | (3 | ) | 269,074 | |||||||||||||

Net property and equipment | 4,179 | 763,994 | 89,118 | (750 | ) | 856,541 | |||||||||||||

Investment in subsidiaries | 830,185 | 116,799 | — | (946,984 | ) | — | |||||||||||||

Intangible assets, net of accumulated amortization | — | 24,223 | — | — | 24,223 | ||||||||||||||

Noncurrent deferred income taxes | 111,286 | — | 2,753 | (111,286 | ) | 2,753 | |||||||||||||

Other long-term assets | 10,122 | 1,955 | 6,921 | — | 18,998 | ||||||||||||||

Total assets | $ | 963,309 | $ | 1,139,937 | $ | 127,366 | $ | (1,059,023 | ) | $ | 1,171,589 | ||||||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||||||||||

Current liabilities: | |||||||||||||||||||

Accounts payable | $ | 735 | $ | 57,910 | $ | 5,660 | $ | — | $ | 64,305 | |||||||||

Current portion of long-term debt | — | 27 | — | — | 27 | ||||||||||||||

Deferred revenues | — | 3,315 | — | — | 3,315 | ||||||||||||||

Accrued expenses | 11,109 | 64,063 | 4,376 | (3 | ) | 79,545 | |||||||||||||

Total current liabilities | 11,844 | 125,315 | 10,036 | (3 | ) | 147,192 | |||||||||||||

Long-term debt, less current portion | 455,000 | 53 | — | — | 455,053 | ||||||||||||||

Noncurrent deferred income taxes | 138 | 180,726 | — | (111,286 | ) | 69,578 | |||||||||||||

Other long-term liabilities | 513 | 3,658 | 531 | — | 4,702 | ||||||||||||||

Total liabilities | 467,495 | 309,752 | 10,567 | (111,289 | ) | 676,525 | |||||||||||||

Total shareholders’ equity | 495,814 | 830,185 | 116,799 | (947,734 | ) | 495,064 | |||||||||||||

Total liabilities and shareholders’ equity | $ | 963,309 | $ | 1,139,937 | $ | 127,366 | $ | (1,059,023 | ) | $ | 1,171,589 | ||||||||

18

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited, in thousands)

Three months ended March 31, 2015 | |||||||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Eliminations | Consolidated | |||||||||||||||

Revenues | $ | — | $ | 173,853 | $ | 19,961 | $ | — | $ | 193,814 | |||||||||

Costs and expenses: | |||||||||||||||||||

Operating costs | — | 116,672 | 15,525 | — | 132,197 | ||||||||||||||

Depreciation and amortization | 349 | 37,677 | 3,756 | — | 41,782 | ||||||||||||||

General and administrative | 5,075 | 16,255 | 668 | (138 | ) | 21,860 | |||||||||||||

Bad debt expense (recovery) | — | 319 | — | — | 319 | ||||||||||||||

Impairment charges | — | 5,990 | — | — | 5,990 | ||||||||||||||

Intercompany leasing | — | (1,215 | ) | 1,215 | — | — | |||||||||||||

Total costs and expenses | 5,424 | 175,698 | 21,164 | (138 | ) | 202,148 | |||||||||||||

Income (loss) from operations | (5,424 | ) | (1,845 | ) | (1,203 | ) | 138 | (8,334 | ) | ||||||||||

Other income (expense): | |||||||||||||||||||

Equity in earnings of subsidiaries | (5,463 | ) | (4,589 | ) | — | 10,052 | — | ||||||||||||

Interest expense, net of interest capitalized | (5,455 | ) | (4 | ) | 4 | — | (5,455 | ) | |||||||||||

Other | 9 | 452 | (3,003 | ) | (138 | ) | (2,680 | ) | |||||||||||

Total other (expense) income | (10,909 | ) | (4,141 | ) | (2,999 | ) | 9,914 | (8,135 | ) | ||||||||||

Income (loss) before income taxes | (16,333 | ) | (5,986 | ) | (4,202 | ) | 10,052 | (16,469 | ) | ||||||||||

Income tax (expense) benefit | 4,314 | 523 | (387 | ) | — | 4,450 | |||||||||||||

Net income (loss) | $ | (12,019 | ) | $ | (5,463 | ) | $ | (4,589 | ) | $ | 10,052 | $ | (12,019 | ) | |||||

Three months ended March 31, 2014 | |||||||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Eliminations | Consolidated | |||||||||||||||

Revenues | $ | — | $ | 216,870 | $ | 22,164 | $ | — | $ | 239,034 | |||||||||

Costs and expenses: | |||||||||||||||||||

Operating costs | — | 139,487 | 14,603 | — | 154,090 | ||||||||||||||

Depreciation and amortization | 269 | 41,864 | 3,393 | — | 45,526 | ||||||||||||||

General and administrative | 6,735 | 17,198 | 688 | (138 | ) | 24,483 | |||||||||||||

Bad debt expense (recovery) | — | (124 | ) | — | — | (124 | ) | ||||||||||||

Gain on litigation | (2,876 | ) | — | — | — | (2,876 | ) | ||||||||||||

Intercompany leasing | — | (1,215 | ) | 1,215 | — | — | |||||||||||||

Total costs and expenses | 4,128 | 197,210 | 19,899 | (138 | ) | 221,099 | |||||||||||||

Income (loss) from operations | (4,128 | ) | 19,660 | 2,265 | 138 | 17,935 | |||||||||||||

Other income (expense): | |||||||||||||||||||

Equity in earnings of subsidiaries | 12,885 | 575 | — | (13,460 | ) | — | |||||||||||||

Interest expense, net of interest capitalized | (12,399 | ) | 7 | 4 | — | (12,388 | ) | ||||||||||||

Loss on extinguishment of debt | (7,887 | ) | — | — | — | (7,887 | ) | ||||||||||||

Other | 3 | 671 | (738 | ) | (138 | ) | (202 | ) | |||||||||||

Total other (expense) income | (7,398 | ) | 1,253 | (734 | ) | (13,598 | ) | (20,477 | ) | ||||||||||

Income (loss) before income taxes | (11,526 | ) | 20,913 | 1,531 | (13,460 | ) | (2,542 | ) | |||||||||||

Income tax (expense) benefit | 8,947 | (8,028 | ) | (956 | ) | — | (37 | ) | |||||||||||

Net income (loss) | $ | (2,579 | ) | $ | 12,885 | $ | 575 | $ | (13,460 | ) | $ | (2,579 | ) | ||||||

19

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited, in thousands)

Three months ended March 31, 2015 | |||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Consolidated | ||||||||||||

Cash flows from operating activities | $ | 26,802 | $ | 41,146 | $ | (3,067 | ) | $ | 64,881 | ||||||

Cash flows from investing activities: | |||||||||||||||

Purchases of property and equipment | (268 | ) | (44,667 | ) | (740 | ) | (45,675 | ) | |||||||

Proceeds from sale of property and equipment | 22 | 6,250 | 4 | 6,276 | |||||||||||

Proceeds from insurance recoveries | 37 | — | — | 37 | |||||||||||

(209 | ) | (38,417 | ) | (736 | ) | (39,362 | ) | ||||||||

Cash flows from financing activities: | |||||||||||||||

Debt repayments | (25,000 | ) | (2 | ) | — | (25,002 | ) | ||||||||

Debt issuance costs | (5 | ) | — | — | (5 | ) | |||||||||

Proceeds from exercise of options | 601 | — | — | 601 | |||||||||||

Purchase of treasury stock | (359 | ) | — | — | (359 | ) | |||||||||

(24,763 | ) | (2 | ) | — | (24,765 | ) | |||||||||

Net increase (decrease) in cash and cash equivalents | 1,830 | 2,727 | (3,803 | ) | 754 | ||||||||||

Beginning cash and cash equivalents | 27,688 | (5,516 | ) | 12,752 | 34,924 | ||||||||||

Ending cash and cash equivalents | $ | 29,518 | $ | (2,789 | ) | $ | 8,949 | $ | 35,678 | ||||||

Three months ended March 31, 2014 | |||||||||||||||

Parent | Guarantor Subsidiaries | Non-Guarantor Subsidiaries | Consolidated | ||||||||||||

Cash flows from operating activities | $ | 4,044 | $ | 16,734 | $ | 20,457 | $ | 41,235 | |||||||

Cash flows from investing activities: | |||||||||||||||

Purchases of property and equipment | (212 | ) | (24,300 | ) | (7,162 | ) | (31,674 | ) | |||||||

Proceeds from sale of property and equipment | — | 5,394 | 122 | 5,516 | |||||||||||

(212 | ) | (18,906 | ) | (7,040 | ) | (26,158 | ) | ||||||||

Cash flows from financing activities: | |||||||||||||||

Debt repayments | (119,472 | ) | (6 | ) | — | (119,478 | ) | ||||||||

Proceeds from issuance of debt | 320,000 | — | — | 320,000 | |||||||||||

Debt issuance costs | (6,138 | ) | — | — | (6,138 | ) | |||||||||

Change in restricted cash | (210,401 | ) | — | — | (210,401 | ) | |||||||||

Tender premium costs | (5,479 | ) | — | — | (5,479 | ) | |||||||||

Proceeds from exercise of options | 277 | — | — | 277 | |||||||||||

Purchase of treasury stock | (433 | ) | — | — | (433 | ) | |||||||||

(21,646 | ) | (6 | ) | — | (21,652 | ) | |||||||||

Net increase (decrease) in cash and cash equivalents | (17,814 | ) | (2,178 | ) | 13,417 | (6,575 | ) | ||||||||

Beginning cash and cash equivalents | 28,368 | (2,059 | ) | 1,076 | 27,385 | ||||||||||

Ending cash and cash equivalents | $ | 10,554 | $ | (4,237 | ) | $ | 14,493 | $ | 20,810 | ||||||

20

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Statements we make in the following discussion that express a belief, expectation or intention, as well as those that are not historical fact, are forward-looking statements that are subject to risks, uncertainties and assumptions. Our actual results, performance or achievements, or industry results, could differ materially from those we express in the following discussion as a result of a variety of factors, including general economic and business conditions and industry trends, levels and volatility of oil and gas prices, the continued demand for drilling services or production services in the geographic areas where we operate, decisions about exploration and development projects to be made by oil and gas exploration and production companies, the highly competitive nature of our business, technological advancements and trends in our industry and improvements in our competitors' equipment, the loss of one or more of our major clients or a decrease in their demand for our services, future compliance with covenants under our senior secured revolving credit facility and our senior notes, operating hazards inherent in our operations, the supply of marketable drilling rigs, well servicing rigs, coiled tubing and wireline units within the industry, the continued availability of drilling rig, well servicing rig, coiled tubing and wireline unit components, the continued availability of qualified personnel, the success or failure of our acquisition strategy, including our ability to finance acquisitions, manage growth and effectively integrate acquisitions, the political, economic, regulatory and other uncertainties encountered by our operations, and changes in, or our failure or inability to comply with, governmental regulations, including those relating to the environment. We have discussed many of these factors in more detail elsewhere in this report and in our Annual Report on Form 10-K for the year ended December 31, 2014, including under the headings “Special Note Regarding Forward-Looking Statements” in the Introductory Note to Part I and “Risk Factors” in Item 1A. These factors are not necessarily all the important factors that could affect us. Unpredictable or unknown factors we have not discussed in this report or in our Annual Report on Form 10-K for the year ended December 31, 2014 could also have material adverse effects on actual results of matters that are the subject of our forward-looking statements. All forward-looking statements speak only as of the date on which they are made and we undertake no obligation to publicly update or revise any forward-looking statements whether as a result of new information, future events or otherwise. We advise our shareholders that they should (1) be aware that important factors not referred to above could affect the accuracy of our forward-looking statements and (2) use caution and common sense when considering our forward-looking statements.

Company Overview