Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - TENNANT CO | Financial_Report.xls |

| EX-21 - SUBSIDIARIES OF THE REGISTRANT - TENNANT CO | exhibit_21.htm |

| EX-23.1 - INDEPENDENT AUDITOR'S CONSENT - TENNANT CO | exhibit_23-1.htm |

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - TENNANT CO | exhibit_31-2.htm |

| EX-32.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 906 - TENNANT CO | exhibit_32-2.htm |

| EX-10.3 - SCHEDULE OF PARTIES TO MANAGEMENT AND EXECUTIVE EMPLOYMENT AGREEMENT - TENNANT CO | exhibit_10-3.htm |

| EX-32.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 906 - TENNANT CO | exhibit_32-1.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - TENNANT CO | exhibit_31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[ü] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2014 |

OR | |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from __________ to __________. |

Commission File Number 001-16191

TENNANT COMPANY

(Exact name of registrant as specified in its charter)

Minnesota | 41-0572550 | |

State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization | Identification No.) | |

701 North Lilac Drive, P.O. Box 1452 Minneapolis, Minnesota 55440 |

(Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code 763-540-1200

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of exchange on which registered | |

Common Stock, par value $0.375 per share | New York Stock Exchange | |

Preferred Share Purchase Rights | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. | ü | Yes | No | |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | ü | No | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ü | Yes | No | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | ü | Yes | No | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | [ü] | |||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. | |||||

Large accelerated filer | ü | Accelerated filer | |||

Non-accelerated filer | (Do not check if a smaller reporting company) | Smaller reporting company | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | ü | No | |

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2014, was $1,376,385,672. | ||||

As of January 30, 2015, there were 18,415,249 shares of Common Stock outstanding. | ||||

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2015 annual meeting of shareholders (the “2015 Proxy Statement”) are incorporated by reference in Part III.

Tennant Company

Form 10–K

Table of Contents

PART I | Page | ||||

PART II | |||||

PART III | |||||

PART IV | |||||

2

TENNANT COMPANY

2014

ANNUAL REPORT

Form 10–K

(Pursuant to Securities Exchange Act of 1934)

PART I

ITEM 1 – Business

General Development of Business

Tennant Company, a Minnesota corporation founded in 1870 and incorporated in 1909, is a world leader in designing, manufacturing and marketing solutions that empower customers to achieve quality cleaning performance, significantly reduce their environmental impact and help create a cleaner, safer, healthier world. Tennant is committed to creating and commercializing breakthrough, sustainable cleaning innovations to enhance its broad suite of products including: floor maintenance and outdoor cleaning equipment, chemical-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, and specialty surface coatings. Tennant products are used in retail establishments and distribution centers, factories and warehouses, public venues such as arenas and stadiums, office buildings, schools and universities, hospitals and clinics, parking lots and streets, and other environments. Customers include building service contract cleaners to whom organizations outsource facilities maintenance, as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

Segment and Geographic Area Financial Information

The Company has one reportable business segment. Sales to customers geographically located in the United States were $479.5 million, $422.6 million and $406.2 million for the years ended December 31, 2014, 2013 and 2012, respectively. Long-lived assets located in the United States were $82.2 million and $82.7 million as of the years ended December 31, 2014 and 2013, respectively. Additional financial information on the Company’s segment and geographic areas is provided throughout Item 8 and Note 17 of the Consolidated Financial Statements.

Principal Products, Markets and Distribution

The Company offers products and solutions mainly consisting of mechanized cleaning equipment, chemical-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, specialty surface coatings, and business solutions such as financing, rental and leasing programs. The Company offers their water-based sustainable cleaning innovation, ec-H2O™, on walk-behind and rider scrubbers. The Company’s suite of offerings are marketed and sold under the following brands: Tennant®, Nobles®, Green Machines™, Alfa Uma Empresa Tennant™ and Orbio®. The Orbio brand of products and solutions is developed and managed by Orbio Technologies, a group created by the Company to focus on expanding the opportunities for a category of sustainable On-Site Generation (OSG) technologies that create and dispense effective cleaning and antimicrobial solutions on site within a facility. The Company's principal markets include targeted vertical industries such as retail, manufacturing/warehousing, education, healthcare and hospitality, among others. The Company sells products directly in 15 countries and through distributors in more than 80 countries. The Company serves customers in these geographies via three geographically aligned business units: The Americas, which consists of North America and Latin America, EMEA, which consists of Europe, the Middle East and Africa, and APAC, which consists of the Asia Pacific region.

Raw Materials

The Company has not experienced any significant or unusual problems in the availability of raw materials or other product components. The Company has sole-source vendors for certain components. A disruption in supply from such vendors may disrupt the Company’s operations. However, the Company believes that it can find alternate sources in the event there is a disruption in supply from such vendors.

Intellectual Property

Although the Company considers that its patents, proprietary technologies, customer relationships, licenses, trademarks, trade names and brand names in the aggregate constitute a valuable asset, it does not regard its business as being materially dependent upon any single intellectual property.

Seasonality

Although the Company’s business is not seasonal in the traditional sense, the percentage of revenues in each quarter typically ranges from 22% to 28% of the total year. The first quarter tends to be at the low end of the range reflecting customers’ initial slow ramp up of capital purchases and the Company’s efforts to close out orders at the end of each year. The second and fourth quarters tend to be towards the high end of the range and the third quarter is typically in the middle of the range.

Working Capital

The Company funds operations through a combination of cash and cash equivalents and cash flows from operations. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. In addition, credit facilities are available for additional working capital needs or investment opportunities.

Major Customers

The Company sells its products to a wide variety of customers, none of which are of material importance in relation to the business as a whole. The customer base includes several governmental entities which generally have terms similar to other customers.

Backlog

The Company processes orders within two weeks, on average. Therefore, no significant backlogs existed at December 31, 2014 and 2013.

3

Competition

While there is no publicly available industry data concerning market share, the Company believes, through its own market research, that it is a world-leading manufacturer of floor maintenance and cleaning equipment. Significant competitors exist in all key geographic regions. However, the key competitors vary by region. The Company competes primarily on the basis of offering a broad line of high-quality, innovative products supported by an extensive sales and service network in major markets.

Certain of the Company’s competitors initiated legal and/or regulatory challenges in 2010 and 2011 in multiple jurisdictions challenging the Company's advertising claims pertaining to its ec-H2O™ water-based technology. These claims have been closed with no material impact to the Company.

Research and Development

The Company strives to be an industry leader in innovation and is committed to investing in research and development. The Company’s Global Innovation Center in Minnesota and engineers throughout its global locations are dedicated to various activities, including researching new technologies to create meaningful product differentiation, development of new products, improvements of existing product design or manufacturing processes and exploring new product applications with customers. In 2014, 2013 and 2012, the Company spent $29.4 million, $30.5 million and $29.3 million on research and development, respectively.

Environmental Compliance

Compliance with Federal, State and local provisions which have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, has not had, and the Company does not expect it to have, a material effect upon the Company’s capital expenditures, earnings or competitive position.

Employees

The Company employed 3,087 people in worldwide operations as of December 31, 2014.

Available Information

The Company makes available free of charge, through the Investor Relations website at investors.tennantco.com, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable when such material is filed electronically with, or furnished to, the Securities and Exchange Commission (“SEC”).

ITEM 1A – Risk Factors

The following are significant factors known to us that could materially adversely affect our business, financial condition or operating results.

We are subject to competitive risks associated with developing innovative products and technologies, including but not limited to, not expanding as rapidly or aggressively in the global market as our competitors, our customers not continuing to pay for innovation and competitive challenges to our products, technology and the underlying intellectual property.

Our products are sold in competitive markets throughout the world. Competition is based on product features and design, brand recognition, reliability, durability, technology, breadth of product offerings, price, customer relationships and after-sale service. Although we believe that the performance and price characteristics of our products will produce competitive solutions for our customers’ needs, our products generally cost more than our competitors’ products. This is due to our dedication to innovation and continued investments in research and development. We believe that customers will pay for the innovations and quality in our products. However, in the current economic environment, it may be difficult for us to compete with lower cost products offered by our competitors and there can be no assurance that our customers will continue to choose our products over products offered by our competitors. If our products, markets and services are not competitive, we may experience a decline in sales, pricing and market share, which adversely impacts revenues, margin and the success of our operations.

Competitors may also initiate litigation to challenge the validity of our patents or claims, allege that we infringe upon their patents, violate our patents or they may use their resources to design comparable products that avoid infringing our patents. Regardless of whether such litigation is successful, such litigation could significantly increase our costs and divert management’s attention from the operation of our business, which could adversely affect our results of operations and financial condition.

Foreign currency exchange rate fluctuations, particularly the strengthening of the U.S. dollar against other major currencies, could result in declines in our reported net sales and net earnings.

We earn revenues, pay expenses, own assets and incur liabilities in countries using functional currencies other than the U.S. dollar. Because our consolidated financial statements are presented in U.S. dollars, we translate revenues and expenses into U.S. dollars at the average exchange rate during each reporting period, as well as assets and liabilities into U.S. dollars at exchange rates in effect at the end of each reporting period. Therefore, increases or decreases in the value of the U.S. dollar against other major currencies will affect our net revenues, net earnings, earnings per share and the value of balance sheet items denominated in foreign currencies as we translate them into the U.S. dollar reporting currency. While we typically use derivative financial instruments to hedge our transactional exposure to certain foreign currency-denominated assets and liabilities, we do not typically hedge the translation of our foreign-denominated functional currencies into our U.S. dollar reporting currency. Fluctuations in foreign currency exchange rates, particularly the strengthening of the U.S. dollar against major currencies, could materially affect our financial results.

4

We may encounter financial difficulties if the United States or other global economies experience an additional or continued significant long-term economic downturn, decreasing the demand for our products and negatively affecting our sales growth.

Our product sales are sensitive to declines in capital spending by our customers. Decreased demand for our products could result in decreased revenues, profitability and cash flows and may impair our ability to maintain our operations and fund our obligations to others. In the event of a continued significant long-term economic downturn in the U.S. or other global economies, our revenues could decline to the point that we may have to take cost-saving measures, such as restructuring actions. These actions would be particularly challenging due to the increase in employee headcount over the past few years. In addition, other fixed costs would have to be reduced to a level that is in line with a lower level of sales. A long-term economic downturn that puts downward pressure on sales could also lower street credibility relative to our publicly stated growth targets.

Our ability to effectively operate our Company could be adversely affected if we are unable to attract and retain key personnel and other highly skilled employees, provide employee development opportunities and create effective succession planning strategies.

Our continued success will depend on, among other things, the skills and services of our executive officers and other key personnel. Our ability to attract and retain highly qualified managerial, technical, manufacturing, research, sales and marketing personnel also impacts our ability to effectively operate our business. As the economy recovers and companies grow and increase their hiring activities, there is an inherent risk of increased employee turnover and the loss of valuable employees in key positions, especially in emerging markets. We believe the increased loss of key personnel within a concentrated region could adversely affect our sales growth.

In addition, there is a risk that there may not be adequate talent acquisition resources in place to support the hiring of new employees in a timely and efficient manner to appropriately align with our growth strategy. The lack of talent acquisition resources could also inhibit our ability to provide training and development opportunities to all employees. This, in turn, could impede our workforce from embracing change and leveraging the improvements we have made in technology and other business process enhancements.

We may not be able to upgrade and evolve our information technology systems as quickly as we wish and we may encounter difficulties as we upgrade and evolve these systems, which could adversely impact our abilities to accomplish anticipated future cost savings, better serve our customers and protect against information system disruption, corruption or intrusions.

We have many information technology systems that are important to the operation of our business and are in need of upgrading in order to effectively implement our growth strategy. Given our greater emphasis on customer-facing technologies, we may not have adequate resources to upgrade our systems at the pace which the current business environment demands. This could increase the risk that the Information Technology infrastructure, such as access and security, is not adequately designed to protect critical data and systems from theft, corruption, unauthorized usage, viruses, sabotage or unintentional misuse. Additionally, significantly upgrading and evolving the capabilities of our existing systems could lead to inefficient or ineffective use of our technology due to lack of training or expertise in these evolving technology systems. These factors could lead to significant expenses, adversely impacting our results of operations and hinder our ability to offer better technology solutions to our customers.

Increases in the cost of, quality, or disruption in the availability of, raw materials and components that we purchase to manufacture our products could negatively impact our operating results or financial condition.

Our sales growth, expanding geographical footprint and continued use of sole source vendors (concentration risk), coupled with suppliers’ potential credit issues, could lead to an increased risk of a breakdown in our supply chain. There is an increased risk of defects due to the highly configured nature of our purchased component parts that could result in quality issues, returns or production slow-downs. In addition, modularization may lead to more sole sourced products and as we seek to outsource the design of certain key components, we risk loss of proprietary control and becoming more reliant on a sole source. There is also a risk that the vendors we chose to supply our parts and equipment fail to comply with our quality expectations, thus damaging our reputation for quality and negatively impacting sales.

The SEC has adopted rules regarding disclosure of the use of “conflict minerals” (commonly referred to as tin, tantalum, tungsten and gold) which are mined from the Democratic Republic of the Congo in products we manufacture or contract to manufacture. These rules have required and will continue to require due diligence and disclosure efforts. There are and will continue to be costs associated with complying with this disclosure requirement, including costs to determine which of our products are subject to the rules and the source of any "conflict minerals" used in these products. Since our supply chain is complex, ultimately we may not be able to sufficiently discover the origin of the conflict minerals used in our products through the due diligence procedures that we implement. If we are unable to, or choose not to certify that our products are conflict mineral free, customers may choose not to purchase our products. Alternatively, if we choose to use only suppliers offering conflict free minerals, we cannot be sure that we will be able to obtain metals, if necessary, from such suppliers in sufficient quantities or at competitive prices. Any one or a combination of these various factors could harm our business, reduce market demand for our products, and adversely affect our profit margins, net sales, and overall financial results.

We may not be able to effectively manage organizational changes which could negatively impact our operating results or financial condition.

We are continuing to implement global standardized processes in our business despite lean staffing levels. We continue to consolidate and reallocate resources as part of our ongoing efforts to optimize our cost structure in the current economy. Our operating results may be negatively impacted if we are unable to implement new processes and manage organizational changes. In addition, if we do not effectively realize and sustain the benefits that these transformations are designed to produce, we may not fully realize the anticipated savings of these actions or they may negatively impact our ability to serve our customers or meet our strategic objectives.

5

Our global operations are subject to laws and regulations that impose significant compliance costs and create reputational and legal risk.

Due to the international scope of our operations, we are subject to a complex system of commercial, tax and trade regulations around the world. Recent years have seen an increase in the development and enforcement of laws regarding trade, tax compliance, labor and safety and anti-corruption, such as the U.S. Foreign Corrupt Practices Act, and similar laws from other countries. Our numerous foreign subsidiaries and affiliates are governed by laws, rules and business practices that differ from those of the U.S., but because we are a U.S. based company, oftentimes they are also subject to U.S. laws which can create a conflict. Despite our due diligence, there is a risk that we do not have adequate resources or comprehensive processes to stay current on changes in laws or regulations applicable to us worldwide and maintain compliance with those changes. Increased compliance requirements may lead to increased costs and erosion of desired profit margin. As a result, it is possible that the activities of these entities may not comply with U.S. laws or business practices or our Business Ethics Guide. Violations of the U.S. or local laws may result in severe criminal or civil sanctions, could disrupt our business, and result in an adverse effect on our reputation, business and results of operations or financial condition. We cannot predict the nature, scope or effect of future regulatory requirements to which our operations might be subject or the manner in which existing laws might be administered or interpreted.

We may be unable to conduct business if we experience a significant business interruption in our computer systems, manufacturing plants or distribution facilities for a significant period of time.

We rely on our computer systems, manufacturing plants and distribution facilities to efficiently operate our business. If we experience an interruption in the functionality in any of these items for a significant period of time for any reason, including unauthorized access to our systems, we may not have adequate business continuity planning contingencies in place to allow us to continue our normal business operations on a long-term basis. In addition, the increase in customer facing technology raises the risk of a lapse in business operations. Therefore, significant long-term interruption in our business could cause a decline in sales, an increase in expenses and could adversely impact our financial results.

Inadequate funding or insufficient innovation of new technologies may result in an inability to develop and commercialize new innovative products and services.

We strive to develop new and innovative products and services to differentiate ourselves in the marketplace. New product development relies heavily on our financial and resource investments in both the short term and long term. If we fail to adequately fund product development projects or fund a project which ultimately does not gain the market acceptance we anticipated, we risk not meeting our customers' expectations, which could result in decreased revenues, declines in margin and loss of market share.

We are subject to product liability claims and product quality issues that could adversely affect our operating results or financial condition.

Our business exposes us to potential product liability risks that are inherent in the design, manufacturing and distribution of our products. If products are used incorrectly by our customers, injury may result leading to product liability claims against us. Some of our products or product improvements may have defects or risks that we have not yet identified that may give rise to product quality issues, liability and warranty claims. Quality issues may also arise due to changes in parts or specifications with suppliers and/or changes in suppliers. If product liability claims are brought against us for damages that are in excess of our insurance coverage or for uninsured liabilities and it is determined we are liable, our business could be adversely impacted. Any losses we suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may have a negative impact on our business and operating results. We could experience a material design or manufacturing failure in our products, a quality system failure, other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. Any unforeseen product quality problems could result in loss of market share, reduced sales, and higher warranty expense.

ITEM 1B – Unresolved Staff Comments

None.

ITEM 2 – Properties

The Company’s corporate offices are owned by the Company and are located in the Minneapolis, Minnesota, metropolitan area. Manufacturing facilities are located in Minneapolis, Minnesota; Holland, Michigan; Louisville, Kentucky; Uden, The Netherlands; Falkirk, United Kingdom; São Paulo, Brazil; and Shanghai, China. Sales offices, warehouse and storage facilities are leased in various locations in North America, Europe, Japan, China, Australia, New Zealand and Latin America. The Company’s facilities are in good operating condition, suitable for their respective uses and adequate for current needs. Further information regarding the Company’s property and lease commitments is included in the Contractual Obligations section of Item 7 and in Note 13 of the Consolidated Financial Statements.

ITEM 3 – Legal Proceedings

There are no material pending legal proceedings other than ordinary routine litigation incidental to the Company’s business.

ITEM 4 – Mine Safety Disclosures

Not applicable.

6

PART II

ITEM 5 – Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

MARKET INFORMATION – Tennant's common stock is traded on the New York Stock Exchange, under the ticker symbol TNC. As of January 30, 2015, there were 397 shareholders of record. The common stock price was $65.21 per share on January 30, 2015.The accompanying chart shows the high and low sales prices for the Company’s shares for each full quarterly period over the past two years as reported by the New York Stock Exchange:

2014 | 2013 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First Quarter | $ | 67.70 | $ | 58.21 | $ | 49.82 | $ | 44.07 | |||||||

Second Quarter | 76.52 | 61.71 | 51.62 | 44.50 | |||||||||||

Third Quarter | 76.25 | 67.09 | 62.50 | 49.64 | |||||||||||

Fourth Quarter | 74.81 | 64.30 | 68.70 | 58.05 | |||||||||||

DIVIDEND INFORMATION – Cash dividends on Tennant’s common stock have been paid for 70 consecutive years. Tennant’s annual cash dividend payout increased for the 43rd consecutive year to $0.78 per share in 2014, an increase of $0.06 per share over 2013. Dividends are generally declared each quarter. On February 18, 2015, the Company announced a quarterly cash dividend of $0.20 per share payable March 16, 2015, to shareholders of record on March 2, 2015.

DIVIDEND REINVESTMENT OR DIRECT DEPOSIT OPTIONS – Shareholders have the option of reinvesting quarterly dividends in additional shares of Company stock or having dividends deposited directly to a bank account. The Transfer Agent should be contacted for additional information.

TRANSFER AGENT AND REGISTRAR – Shareholders with a change of address or questions about their account may contact:

Wells Fargo Bank, N.A.

Shareowner Services

P.O. Box 64874

St. Paul, MN 55164-0854

(800) 468-9716

EQUITY COMPENSATION PLAN INFORMATION – Information regarding equity compensation plans required by Regulation S-K Item 201(d) is incorporated by reference in Item 12 of this annual report on Form 10-K from the 2015 Proxy Statement.

SHARE REPURCHASES – On April 25, 2012, the Board of Directors authorized the repurchase of 1,000,000 shares of our common stock. Share repurchases are made from time to time in the open market or through privately negotiated transactions, primarily to offset the dilutive effect of shares issued through our share-based compensation programs. Our credit agreements and Private Shelf Agreement restrict the payment of dividends or repurchasing of stock if, after giving effect to such payments, our leverage ratio is greater than 2.00 to 1, in such case limiting such payments to an amount ranging from $50.0 million to $75.0 million during any fiscal year.

For the Quarter Ended December 31, 2014 | Total Number of Shares Purchased (1) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||

October 1–31, 2014 | 7,592 | $ | 64.97 | 7,500 | 405,569 | |||||||

November 1–30, 2014 | — | — | — | 405,569 | ||||||||

December 1–31, 2014 | — | — | — | 405,569 | ||||||||

Total | 7,592 | $ | 64.97 | 7,500 | 405,569 | |||||||

(1) Includes 92 shares delivered or attested to in satisfaction of the exercise price and/or tax withholding obligations by employees who exercised stock options or restricted stock under employee share-based compensation plans.

7

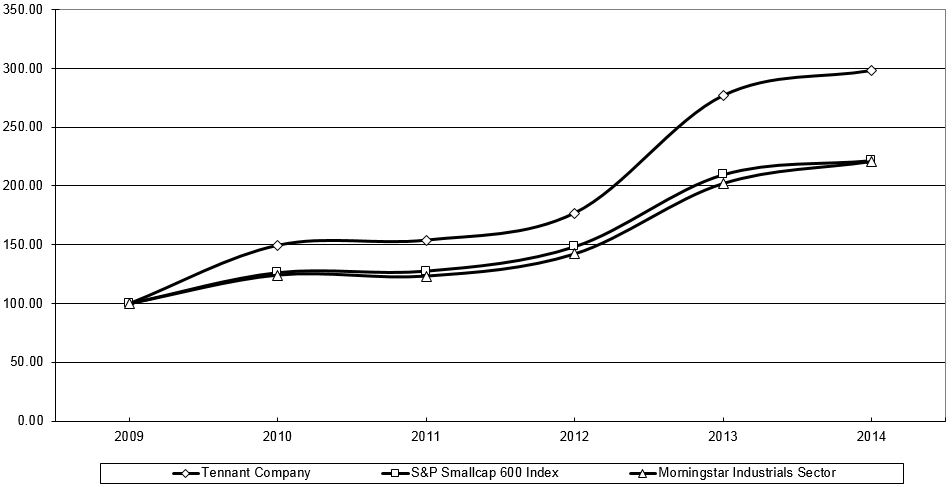

STOCK PERFORMANCE GRAPH – The following graph compares the cumulative total shareholder return on Tennant’s common stock to two indices: S&P SmallCap 600 and Morningstar Industrials Sector. The graph below compares the performance for the last five fiscal years, assuming an investment of $100 on December 31, 2009, including the reinvestment of all dividends.

5-YEAR CUMULATIVE TOTAL RETURN COMPARISON

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||

Tennant Company | $100 | $150 | $154 | $177 | $277 | $298 | |||||

S&P SmallCap 600 | $100 | $126 | $128 | $148 | $210 | $222 | |||||

Morningstar Industrials Sector | $100 | $124 | $123 | $142 | $202 | $221 | |||||

8

ITEM 6 – Selected Financial Data

(In thousands, except shares and per share data)

Years Ended December 31 | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||||||

Financial Results: | ||||||||||||||||||||||||

Net Sales | $ | 821,983 | $ | 752,011 | $ | 738,980 | $ | 753,998 | $ | 667,667 | ||||||||||||||

Cost of Sales | 469,556 | 426,103 | 413,684 | (2) | 434,817 | (3) | 383,341 | (4) | ||||||||||||||||

Gross Margin - % | 42.9 | 43.3 | 44.0 | 42.3 | 42.6 | |||||||||||||||||||

Research and Development Expense | 29,432 | 30,529 | 29,263 | 27,911 | 25,957 | |||||||||||||||||||

% of Net Sales | 3.6 | 4.1 | 4.0 | 3.7 | 3.9 | |||||||||||||||||||

Selling and Administrative Expense | 250,898 | 232,976 | (1) | 234,114 | (2) | 241,625 | (3) | 221,235 | (4) | |||||||||||||||

% of Net Sales | 30.5 | 31.0 | 31.7 | 32.0 | 33.1 | |||||||||||||||||||

Gain on Sale of Business | — | — | (784 | ) | (2) | — | — | |||||||||||||||||

% of Net Sales | — | — | (0.1 | ) | — | — | ||||||||||||||||||

Profit from Operations | 72,097 | 62,403 | (1) | 62,703 | (2) | 49,645 | (3) | 37,134 | (4) | |||||||||||||||

% of Net Sales | 8.8 | 8.3 | 8.5 | 6.6 | 5.6 | |||||||||||||||||||

Total Other Expense, Net | (2,559 | ) | (2,525 | ) | (2,813 | ) | (915 | ) | (2,407 | ) | ||||||||||||||

Profit Before Income Taxes | 69,538 | 59,878 | (1) | 59,890 | (2) | 48,730 | (3) | 34,727 | (4) | |||||||||||||||

% of Net Sales | 8.5 | 8.0 | 8.1 | 6.5 | 5.2 | |||||||||||||||||||

Income Tax Expense (Benefit) | 18,887 | 19,647 | (1) | 18,306 | (2) | 16,017 | (3) | (76 | ) | (4) | ||||||||||||||

Effective Tax Rate - % | 27.2 | 32.8 | 30.6 | 32.9 | (0.2 | ) | ||||||||||||||||||

Net Earnings | 50,651 | 40,231 | (1) | 41,584 | (2) | 32,713 | (3) | 34,803 | (4) | |||||||||||||||

% of Net Sales | 6.2 | 5.3 | 5.6 | 4.3 | 5.2 | |||||||||||||||||||

Per Share Data: | ||||||||||||||||||||||||

Basic Net Earnings | $ | 2.78 | $ | 2.20 | (1) | $ | 2.24 | (2) | $ | 1.74 | (3) | $ | 1.85 | (4) | ||||||||||

Diluted Net Earnings | $ | 2.70 | $ | 2.14 | (1) | $ | 2.18 | (2) | $ | 1.69 | (3) | $ | 1.80 | (4) | ||||||||||

Diluted Weighted Average Shares | 18,740,858 | 18,833,453 | 19,102,016 | 19,360,428 | 19,332,103 | |||||||||||||||||||

Cash Dividends | $ | 0.78 | $ | 0.72 | $ | 0.69 | $ | 0.68 | $ | 0.59 | ||||||||||||||

Financial Position: | ||||||||||||||||||||||||

Total Assets | $ | 486,932 | $ | 456,306 | $ | 420,760 | $ | 424,262 | $ | 403,668 | ||||||||||||||

Total Debt | 28,137 | 31,803 | 32,323 | 36,455 | 30,828 | |||||||||||||||||||

Total Shareholders’ Equity | 280,651 | 263,846 | 235,054 | 220,852 | 216,133 | |||||||||||||||||||

Current Ratio | 2.4 | 2.4 | 2.2 | 2.2 | 2.1 | |||||||||||||||||||

Debt-to-Capital Ratio | 9.1 | % | 10.8 | % | 12.1 | % | 14.2 | % | 12.5 | % | ||||||||||||||

Cash Flows: | ||||||||||||||||||||||||

Net Cash Provided by Operations | $ | 59,362 | $ | 59,814 | $ | 47,566 | $ | 56,909 | $ | 42,530 | ||||||||||||||

Capital Expenditures, Net of Disposals | (19,292 | ) | (14,655 | ) | (14,595 | ) | (13,301 | ) | (9,934 | ) | ||||||||||||||

Free Cash Flow | 40,070 | 45,159 | 32,971 | 43,608 | 32,596 | |||||||||||||||||||

Other Data: | ||||||||||||||||||||||||

Depreciation and Amortization | $ | 20,063 | $ | 20,246 | $ | 20,872 | $ | 21,418 | $ | 21,192 | ||||||||||||||

Number of employees at year-end | 3,087 | 2,931 | 2,816 | 2,865 | 2,793 | |||||||||||||||||||

The results of operations from our 2011 acquisition has been included in the Selected Financial Data presented above since its acquisition date.

(1) 2013 includes restructuring charges of $3,017 pre-tax ($2,938 after-tax or $0.15 per diluted share) and a tax benefit of $582 (or $0.03 per diluted share) related to the retroactive reinstatement of the 2012 U.S. Federal Research and Development ("R&D") Tax Credit.

(2) 2012 includes a gain on sale of business of $784 pre-tax ($508 after-tax or $0.03 per diluted share), a restructuring charge of $760 pre-tax ($670 after-tax or $0.04 per diluted share) and tax benefits from an international entity restructuring of $2,043 (or $0.11 per diluted share).

(3) 2011 includes a Product Line Obsolescence charge of $4,300 pre-tax ($3,811 after-tax or $0.20 per diluted share) and an international executive severance charge of $1,217 (or $0.06 per diluted share).

9

(4) 2010 includes a tax benefit from the international entity restructuring of $10,913 (or $0.56 per diluted share), a workforce redeployment charge of $1,671 pre-tax ($1,196 after-tax or $0.06 per diluted share), inventory revaluation from change in functional currency designation due to international entity restructuring of $647 pre-tax ($453 after-tax or $0.02 per diluted share) and a revision of our 2008 workforce reduction reserve of $277 pre-tax ($173 after-tax or $0.01 per diluted share).

ITEM 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

Tennant Company is a world leader in designing, manufacturing and marketing solutions that empower customers to achieve quality cleaning performance, significantly reduce their environmental impact and help create a cleaner, safer, healthier world. Tennant is committed to creating and commercializing breakthrough, sustainable cleaning innovations to enhance its broad suite of products including: floor maintenance and outdoor cleaning equipment, chemical-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, and specialty surface coatings. Tennant products are used in retail establishments and distribution centers, factories and warehouses, public venues such as arenas and stadiums, office buildings, schools and universities, hospitals and clinics, parking lots and streets, and other environments. Customers include building service contract cleaners to whom organizations outsource facilities maintenance, as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

Net Sales in 2014 totaled $822.0 million, up from $752.0 million in the prior year primarily due to strong sales to strategic accounts and through distribution, continued demand for new products such as the T17 rider scrubber, gains in commercial, industrial and outdoor equipment and selling price increases. 2014 organic sales growth, excluding the unfavorable impact of foreign currency exchange of approximately 1.0%, was up approximately 10.3% with growth in all major geographical regions. 2014 Gross Profit margin decreased 40 basis points to 42.9% from 43.3% in 2013 primarily due to strong sales to strategic accounts and through distribution that tend to have lower gross profit margins and also costs related to hiring and training additional manufacturing employees to support the higher levels of production. Selling and Administrative Expense (“S&A Expense”) increased 7.7%, but decreased 50 basis points as a percentage of Net Sales, from $233.0 million in 2013 to $250.9 million in 2014 primarily due to investments in direct sales, distribution and marketing to build organic sales. This was somewhat offset by continued cost controls and improved operating efficiencies that favorably impacted S&A Expense in 2014. Operating Profit increased 15.5% and Operating Profit margin increased 50 basis points to 8.8% in 2014 from 8.3% in 2013 due to higher Net Sales and lower R&D Expense and S&A Expense, somewhat offset by lower Gross Margin, as a percentage of Net Sales. Net Earnings for 2014 were favorably impacted by a lower tax rate compared to 2013 due to the mix in taxable earnings by country and favorable settlements on tax positions from prior years.

Net Earnings for 2013 were $1.4 million less than 2012. The decrease in net earnings resulted primarily from 2013 restructuring charges of $3.0 million pre-tax ($2.9 million after-tax) being somewhat offset by a tax benefit of $0.6 million related to the retroactive reinstatement of the 2012 U.S. Federal R&D Tax Credit. 2013 Gross Profit margin decreased 70 basis points to 43.3% from 44.0% in 2012 due to changes in selling channel mix and mix of products sold. Net Sales in 2013 totaled $752.0 million, up from $739.0 million in the prior year primarily due to increased sales of industrial equipment and high demand for newly introduced products which were somewhat offset by lower sales of city cleaning equipment. 2013 organic sales growth, excluding the impact of foreign currency exchange, was up approximately 2.8% with growth in North America, Latin America and Asia Pacific being somewhat offset by declines in Europe due to challenging economic conditions. S&A Expense decreased 0.5%, or 70 basis points, as a percentage of Net Sales, from $234.1 million in 2012 to $233.0 million in 2013 due to continued tight cost controls and improved operating leverage. Operating Profit decreased 0.5% and Operating Profit margin declined 20 basis points to 8.3% in 2013 from 8.5% in 2012 due to two restructuring charges taken during 2013 totaling $3.0 million and increased investment in R&D activities.

Tennant continues to invest in innovative product development with 3.6% of 2014 Net Sales spent on R&D. During 2014, we continued to invest in developing innovative new products for our traditional core business, as well as in our Orbio Technologies Group, which is focused on advancing a suite of sustainable cleaning technologies. New products are a key driver of sales growth. Eighteen new products were launched in 2014, including a line of walk-behind burnishers, a mid-size battery-powered rider scrubber, a mid-size rider sweeper with optimized dust control, the Orbio os3 system and a new line of Alfa essentials.

We ended 2014 with a Debt-to-Capital ratio of 9.1%, $93.0 million in Cash and Cash Equivalents compared to $81.0 million at the end of 2013, and Shareholders’ Equity of $280.7 million. During 2014, we generated operating cash flows of $59.4 million. Total debt was $28.1 million as of December 31, 2014, compared to $31.8 million at the end of 2013.

10

Historical Results

The following table compares the historical results of operations for the years ended December 31, 2014, 2013 and 2012 in dollars and as a percentage of Net Sales (in thousands, except per share amounts and percentages):

2014 | % | 2013 | % | 2012 | % | |||||||||||||||

Net Sales | $ | 821,983 | 100.0 | $ | 752,011 | 100.0 | $ | 738,980 | 100.0 | |||||||||||

Cost of Sales | 469,556 | 57.1 | 426,103 | 56.7 | 413,684 | 56.0 | ||||||||||||||

Gross Profit | 352,427 | 42.9 | 325,908 | 43.3 | 325,296 | 44.0 | ||||||||||||||

Operating Expense: | ||||||||||||||||||||

Research and Development Expense | 29,432 | 3.6 | 30,529 | 4.1 | 29,263 | 4.0 | ||||||||||||||

Selling and Administrative Expense | 250,898 | 30.5 | 232,976 | 31.0 | 234,114 | 31.7 | ||||||||||||||

Gain on Sale of Business | — | — | — | — | (784 | ) | (0.1 | ) | ||||||||||||

Total Operating Expenses | 280,330 | 34.1 | 263,505 | 35.0 | 262,593 | 35.5 | ||||||||||||||

Profit from Operations | 72,097 | 8.8 | 62,403 | 8.3 | 62,703 | 8.5 | ||||||||||||||

Other Income (Expense): | ||||||||||||||||||||

Interest Income | 302 | — | 390 | 0.1 | 1,069 | 0.1 | ||||||||||||||

Interest Expense | (1,722 | ) | (0.2 | ) | (1,761 | ) | (0.2 | ) | (2,517 | ) | (0.3 | ) | ||||||||

Net Foreign Currency Transaction Losses | (690 | ) | (0.1 | ) | (671 | ) | (0.1 | ) | (1,403 | ) | (0.2 | ) | ||||||||

Other (Expense) Income, Net | (449 | ) | (0.1 | ) | (483 | ) | (0.1 | ) | 38 | — | ||||||||||

Total Other Expense, Net | (2,559 | ) | (0.3 | ) | (2,525 | ) | (0.3 | ) | (2,813 | ) | (0.4 | ) | ||||||||

Profit Before Income Taxes | 69,538 | 8.5 | 59,878 | 8.0 | 59,890 | 8.1 | ||||||||||||||

Income Tax Expense | 18,887 | 2.3 | 19,647 | 2.6 | 18,306 | 2.5 | ||||||||||||||

Net Earnings | $ | 50,651 | 6.2 | $ | 40,231 | 5.3 | $ | 41,584 | 5.6 | |||||||||||

Net Earnings per Diluted Share | $ | 2.70 | $ | 2.14 | $ | 2.18 | ||||||||||||||

Consolidated Financial Results

Net Earnings for 2014 were $50.7 million, or $2.70 per diluted share, compared to $40.2 million, or $2.14 per diluted share for 2013. Net Earnings were impacted by:

• | An increase in Net Sales of 9.3%, primarily due to increased sales to strategic accounts and through distribution, continued demand for new products, gains in commercial, industrial and outdoor equipment, and selling list price increases, typically in the range of 2 percent to 4 percent in most geographies, in March 2014. |

• | A 40 basis point decrease in Gross Profit margin due to strong sales to strategic accounts and through distribution that tend to have lower gross profit margins and also costs related to hiring and training additional manufacturing employees to support the higher levels of production. |

• | A decrease in S&A Expense as a percentage of Net Sales of 50 basis points due to continued cost controls and improved operating efficiencies, somewhat offset by investments in direct sales, distribution and marketing to build organic sales. |

Net Earnings for 2013 were $40.2 million, or $2.14 per diluted share, compared to $41.6 million, or $2.18 per diluted share for 2012. Net Earnings were impacted by:

• | An increase in Net Sales of 1.8%, primarily due to increased sales of industrial equipment and high demand for newly introduced products that were somewhat offset by lower sales of city cleaning equipment. |

• | A 70 basis point decrease in Gross Profit margin due to changes in selling channel mix and mix of products sold. |

• | A decrease in S&A Expense as a percentage of Net Sales of 70 basis points due to continued tight cost controls and improved operating efficiencies. |

• | Two restructuring actions totaling $3.0 million (pre-tax) during 2013 or 40 basis points as a percentage of Net Sales. |

• | A $0.6 million tax benefit related to the 2012 R&D tax credit that was retroactively enacted in January 2013. |

Net Sales

In 2014, consolidated Net Sales were $822.0 million, an increase of 9.3% as compared to 2013. Consolidated Net Sales were $752.0 million in 2013, an increase of 1.8% as compared to 2012.

The components of the consolidated Net Sales change for 2014 as compared to 2013, and 2013 as compared to 2012, were as follows:

Growth Elements | 2014 v. 2013 | 2013 v. 2012 | |

Organic Growth: | |||

Volume | 9.3% | 1.8% | |

Price | 1.0% | 1.0% | |

Organic Growth | 10.3% | 2.8% | |

Foreign Currency | (1.0%) | (1.0%) | |

Total | 9.3% | 1.8% | |

The 9.3% increase in consolidated Net Sales for 2014 as compared to 2013 was primarily due to sales volume increases to strategic accounts and through distribution, continued demand for new products such as the T17 rider scrubber and gains in commercial, industrial and outdoor equipment. Sales of new products introduced since the 2012 fourth quarter were 12% of equipment sales in 2014. The impact from direct foreign currency translation exchange was approximately neutral to Net Sales for the first nine months of 2014, and was approximately 3.0% unfavorable in the 2014 fourth quarter primarily due to the strengthening of the U.S. dollar throughout the quarter, resulting in a 2014 full year impact that was approximately 1.0% unfavorable. We expect a larger unfavorable foreign currency impact in 2015.

The 1.8% increase in consolidated Net Sales for 2013 as compared to 2012 was primarily due to sales volume increases due to increased sales of industrial equipment and demand for newly introduced products.

The following table sets forth annual Net Sales by operating segment and the related percentage change from the prior year (in thousands, except percentages):

2014 | % | 2013 | % | 2012 | |||||||||||||

Americas | $ | 569,004 | 10.6 | $ | 514,544 | 4.7 | $ | 491,661 | |||||||||

Europe, Middle East and Africa | 165,686 | 5.4 | 157,208 | (5.4 | ) | 166,208 | |||||||||||

Asia Pacific | 87,293 | 8.8 | 80,259 | (1.1 | ) | 81,111 | |||||||||||

Total | $ | 821,983 | 9.3 | $ | 752,011 | 1.8 | $ | 738,980 | |||||||||

11

Americas – In 2014, Americas Net Sales increased 10.6% to $569.0 million as compared with $514.5 million in 2013. The primary driver of the increase in Net Sales was attributable to higher sales to strategic accounts, including sales of scrubbers in North America, scrubbers equipped with ec-H2O technology and walk-behind burnishers. Unfavorable direct foreign currency translation exchange effects decreased Net Sales by approximately 1.0%.

In 2013, Americas Net Sales increased 4.7% to $514.5 million as compared with $491.7 million in 2012. The primary driver of the increase in Net Sales was attributable to higher sales of equipment in North America, including scrubbers equipped with ec-H2O technology and sweepers, and continued growth in Latin America. Unfavorable direct foreign currency translation exchange effects decreased Net Sales by approximately 1.0%.

Europe, Middle East and Africa – Europe, Middle East and Africa (“EMEA”) Net Sales in 2014 increased 5.4% to $165.7 million as compared to 2013 Net Sales of $157.2 million. An organic sales increase of approximately 4.4% was primarily due to higher sales of outdoor equipment, including strong sales of 500ze lithium-ion battery-powered sweepers. Favorable direct foreign currency exchange effects increased EMEA Net Sales by approximately 1.0% in 2014.

EMEA Net Sales in 2013 decreased 5.4% to $157.2 million as compared to 2012 Net Sales of $166.2 million. An organic sales decrease of approximately 7.4% was primarily due to decreases in sales of city cleaning equipment due to tight municipal spending in Europe, somewhat offset by increased sales to strategic accounts. Favorable direct foreign currency exchange effects increased EMEA Net Sales by approximately 2.0% in 2013.

Asia Pacific – Asia Pacific Net Sales in 2014 increased 8.8% to $87.3 million as compared to 2013 Net Sales of $80.3 million. An organic sales increase of approximately 12.8% was primarily due to strong sales performance in China, Japan, Southeast Asia and Korea. Unfavorable direct foreign currency exchange effects decreased Net Sales by approximately 4.0% in 2014.

Asia Pacific Net Sales in 2013 decreased 1.1% to $80.3 million as compared to 2012 Net Sales of $81.1 million. An organic sales increase of approximately 4.4% was primarily due to increased sales of equipment in China and also sales growth in Australia and Japan. Unfavorable direct foreign currency exchange effects decreased Net Sales by approximately 5.5% in 2013.

Gross Profit

Gross Profit margin was 42.9% in 2014, a decrease of 40 basis points as compared to 2013. Gross Profit margin in 2014 was unfavorably impacted by stronger sales to sales channels that tend to have lower gross margins and also costs related to hiring and training additional manufacturing employees and temporary workers to support the higher levels of production, including the continued ramp up to meet the growing demand for new products.

Gross Profit margin was 43.3% in 2013, a decrease of 70 basis points as compared to 2012. Gross Profit margin in 2013 was unfavorably impacted by changes in selling channel mix and the mix of products sold.

Operating Expenses

Research and Development Expense – R&D Expense decreased $1.1 million, or 3.6%, in 2014 as compared to 2013. As a percentage of Net Sales, 2014 R&D Expense decreased 50 basis points to 3.6% in 2014 from 4.1% in the prior year primarily due to the timing of new product development projects. We continued to invest in developing innovative new products for our traditional core business, as well as our Orbio business.

R&D Expense increased $1.3 million, or 4.3%, in 2013 as compared to 2012. As a percentage of Net Sales, 2013 R&D Expense increased 10 basis points to 4.1% in 2013 from 4.0% in the prior year. R&D Expense increased in 2013 as we made additional investments in developing innovative new products for our traditional core business, as well as our Orbio business.

Selling and Administrative Expense – S&A Expense increased by $17.9 million, or 7.7%, in 2014 compared to 2013. As a percentage of Net Sales, 2014 S&A Expense decreased 50 basis points to 30.5% from 31.0% in 2013 due to continued cost controls and improved operating efficiencies, somewhat offset by investments in direct sales, distribution and marketing to build organic sales that unfavorably impacted S&A Expense.

S&A Expense decreased by $1.1 million, or 0.5%, in 2013 compared to 2012. As a percentage of Net Sales, 2013 S&A Expense decreased 70 basis points to 31.0% due to continued tight cost controls and improved operating efficiencies. Included in the lower S&A Expense during 2013 were two restructuring actions totaling $3.0 million, or 40 basis points as a percentage of Net Sales.

Other Income (Expense)

Interest Income – Interest Income was $0.3 million in 2014, a decrease of $0.1 million from 2013. The decrease between 2014 and 2013 was due to decreases in interest rates on cash invested.

Interest Income was $0.4 million in 2013, a decrease of $0.7 million from 2012. The decrease between 2013 and 2012 was due to decreases in interest rates on cash invested.

Interest Expense – Interest Expense was $1.7 million in 2014 as compared to $1.8 million in 2013. This decrease was primarily due to lower interest rates on long-term adjustable rate borrowings.

Interest Expense was $1.8 million in 2013 as compared to $2.5 million in 2012. This decrease was primarily due to lower interest rates on long-term adjustable rate borrowings.

Net Foreign Currency Transaction Losses – Net Foreign Currency Transaction Losses were $0.7 million in 2014 and 2013.

Net Foreign Currency Transaction Losses were $0.7 million in 2013 as compared to Losses of $1.4 million in 2012. The favorable decrease from the prior year was due to fluctuations in foreign currency rates in the normal course of business.

Income Taxes

The overall effective income tax rate was 27.2%, 32.8% and 30.6% in 2014, 2013 and 2012, respectively.

The tax expense for 2013 included a $0.1 million tax benefit associated with restructuring charges of $3.0 million. The tax expense also included a first quarter discrete tax benefit of $0.6 million for the enactment of the Federal R&D credit retroactively impacting the tax year ended December 31, 2012. Excluding these special items, the 2013 overall tax rate would have been 32.3%.

The decrease in the 2014 overall effective tax rate as compared to the prior year, excluding the effect of the 2013 one-time charges, was primarily related to the mix in our full year taxable earnings by country and favorable settlements on prior years' tax positions.

The tax expense for 2012 included a $2.0 million tax benefit associated with an international entity restructuring which materially decreased the overall effective tax rate. Excluding this tax benefit, the overall effective tax rate would have been 34.0%.

12

We do not have any plans to repatriate the undistributed earnings of non-U.S. subsidiaries. Any repatriation from foreign subsidiaries that would result in incremental U.S. taxation is not being considered. It is management's belief that reinvesting these earnings outside the U.S. is the most efficient use of capital.

Liquidity and Capital Resources

Liquidity – Cash and Cash Equivalents totaled $93.0 million at December 31, 2014, as compared to $81.0 million as of December 31, 2013. Cash and Cash Equivalents held by our foreign subsidiaries totaled $15.8 million as of December 31, 2014, as compared to $13.4 million as of December 31, 2013. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. Our current ratio was 2.4 as of December 31, 2014 and December 31, 2013, and our working capital was $201.5 million and $183.8 million, respectively.

Our Debt-to-Capital ratio was 9.1% as of December 31, 2014, compared with 10.8% as of December 31, 2013. Our capital structure was comprised of $28.1 million of Debt and $280.7 million of Shareholders’ Equity as of December 31, 2014.

Cash Flow Summary – Cash provided by (used in) our operating, investing and financing activities is summarized as follows (in thousands):

2014 | 2013 | 2012 | |||||||||

Operating Activities | $ | 59,362 | $ | 59,814 | $ | 47,566 | |||||

Investing Activities: | |||||||||||

Purchases of Property, Plant and Equipment, Net of Disposals | (19,292 | ) | (14,655 | ) | (14,595 | ) | |||||

Acquisitions of Businesses, Net of Cash Acquired | — | (750 | ) | (750 | ) | ||||||

Proceeds from Sale of Business | 1,416 | 4,261 | 1,014 | ||||||||

Decrease (Increase) in Restricted Cash | 6 | (253 | ) | 3,089 | |||||||

Financing Activities | (28,038 | ) | (21,495 | ) | (34,932 | ) | |||||

Effect of Exchange Rate Changes on Cash and Cash Equivalents | (1,476 | ) | 122 | 209 | |||||||

Net Increase in Cash and Cash Equivalents | $ | 11,978 | $ | 27,044 | $ | 1,601 | |||||

Operating Activities – Cash provided by operating activities was $59.4 million in 2014, $59.8 million in 2013 and $47.6 million in 2012. In 2014, cash provided by operating activities was driven primarily by $50.7 million of Net Earnings and increases in Accounts Payable somewhat offset by increases in Inventories and Receivables. The increase in Inventories was in support of higher sales levels and the launches of many new products. The increase in Receivables was due to higher sales levels, the variety of terms offered and mix of business. Cash provided by operating activities was $0.5 million lower in 2014 as compared to 2013 primarily due to increases year over year in working capital to support the growth in sales.

In 2013, cash provided by operating activities was driven by $40.2 million of Net Earnings and an increase in Accounts Payable, somewhat offset by increases in Inventories and Receivables. The increase in Inventories was in support of the launches of many new products. The increase in Receivables was due to a variety of terms offered and mix of business. Cash provided by operating activities was $12.2 million higher in 2013 as compared to 2012 primarily due to a $15.0 million discretionary contribution made to the U.S. Pension Plan in 2012 and there were no contributions made in 2013.

For 2014, we used operating profit and operating profit margin as key indicators of financial performance and the primary metrics for performance-based incentives.

Two metrics used by management to evaluate how effectively we utilize our net assets are “Accounts Receivable Days Sales Outstanding” (“DSO”) and “Days Inventory on Hand” (“DIOH”), on a first-in, first-out (“FIFO”) basis. The metrics are calculated on a rolling three month basis in order to more readily reflect changing trends in the business. These metrics for the quarters ended December 31 were as follows (in days):

2014 | 2013 | 2012 | |||

DSO | 62 | 61 | 60 | ||

DIOH | 84 | 81 | 78 | ||

DSO increased 1 day in 2014 as compared to 2013 primarily due to the variety of terms offered and mix of business having a larger unfavorable impact than the favorable trend of continued proactive management of our receivables by enforcing tighter credit limits and continuing to successfully collect past due balances.

DIOH increased 3 days in 2014 as compared to 2013 primarily due to increased levels of inventory in support of higher sales levels and the launches of many new products somewhat offset by progress from inventory reduction initiatives.

Investing Activities – Net cash used for investing activities was $17.9 million in 2014, $11.4 million in 2013 and $11.2 million in 2012. Net capital expenditures were $19.3 million during 2014 as compared to $14.7 million in 2013 and $14.6 million in 2012. Our 2014 capital expenditures included investments in tooling related to new product development, and manufacturing and information technology process improvement projects. Proceeds from Sale of Business provided $1.4 million in 2014 and $4.3 million in 2013.

Capital expenditures in 2013 included investments in tooling related to new product development, and manufacturing and information technology process improvement projects. Capital expenditures in 2012 included tooling related to new product development, manufacturing equipment and information technology process improvement projects.

Financing Activities – Net cash used for financing activities was $28.0 million in 2014, $21.5 million in 2013 and $34.9 million in 2012. In 2014, payments of dividends used $14.5 million, payments of Long-Term Debt used $2.0 million and payments of Short-Term Debt used $1.5 million. In 2013, payments of dividends used $13.2 million and payments of Long-Term Debt used $1.1 million, partially offset by Short-Term Borrowings of $1.5 million. In 2012, payments of dividends and Long-Term Debt used $12.8 million and $3.0 million, respectively. Our annual cash dividend payout increased for the 43rd consecutive year to $0.78 per share in 2014, an increase of $0.06 per share over 2013.

Proceeds from the issuance of Common Stock generated $2.3 million in 2014, $8.3 million in 2013 and $4.2 million in 2012.

On April 25, 2012, the Board of Directors authorized the repurchase of 1,000,000 shares of our common stock. At December 31, 2014, there were 405,569 remaining shares authorized for repurchase.

There were 225,034 shares repurchased in 2014 in the open market, 434,118 shares repurchased in 2013 and 621,340 shares repurchased during 2012, at average repurchase prices of $62.64 during 2014, $51.04 during 2013 and $40.78 during 2012. Our Credit Agreement with JPMorgan Chase Bank limits the payment of dividends and repurchases of stock to amounts ranging from $50.0 million to $75.0 million per fiscal year based on our leverage ratio after giving effect to such payments for the life of the agreement.

13

Indebtedness – As of December 31, 2014, we had committed lines of credit totaling approximately $125.0 million and uncommitted lines of credit totaling approximately $87.4 million. There were $10.0 million in outstanding borrowings under our JPMorgan facility (described below) and $18.0 million in outstanding borrowings under our Prudential facility (described below) as of December 31, 2014. In addition, we had stand alone letters of credit of approximately $2.4 million outstanding and bank guarantees in the amount of approximately $0.2 million. Commitment fees on unused lines of credit for the year ended December 31, 2014 were $0.3 million.

Our most restrictive covenants are part of our 2011 Credit Agreement with JPMorgan (as defined below), which are the same covenants in our Shelf Agreement (as defined below) with Prudential (as defined below), and require us to maintain an indebtedness to EBITDA ratio of not greater than 3.00 to 1 and to maintain an EBITDA to interest expense ratio of no less than 3.50 to 1 as of the end of each quarter. As of December 31, 2014, our indebtedness to EBITDA ratio was 0.34 to 1 and our EBITDA to interest expense ratio was 52.86 to 1.

Credit Facilities

JPMorgan Chase Bank, National Association

On April 25, 2013, we entered into Amendment No. 1 to our 2011 Credit Agreement which amends the Credit Agreement, dated as of May 5, 2011, with JPMorgan Chase Bank, N. A. (“JPMorgan”), as administrative agent and collateral agent, U.S. Bank National Association, as syndication agent, Wells Fargo Bank, National Association, and RBS Citizens, N.A., as co-documentation agents, and the Lenders (including JPMorgan) from time to time party thereto (the “2011 Credit Agreement”). Under the original terms, the 2011 Credit Agreement provides us and certain of our foreign subsidiaries access to a senior unsecured credit facility until May 5, 2016, in the amount of $125.0 million, with an option to expand by up to $62.5 million to a total of $187.5 million. Borrowings may be denominated in U.S. Dollars or certain other currencies. The 2011 Credit Agreement contains a $100.0 million sublimit on borrowings by foreign subsidiaries.

Amendment No. 1 to the 2011 Credit Agreement principally provides the following changes to the 2011 Credit Agreement:

• | extends the maturity date of the 2011 Credit Agreement to March 1, 2018; |

• | changes the fees for committed funds under the 2011 Credit Agreement to an annual rate ranging from 0.20% to 0.35%, depending on our leverage ratio; |

• | changes the per annum interest rate on Eurocurrency borrowings to adjusted LIBOR plus an additional spread of 1.30% to 1.90%, depending on our leverage ratio; |

• | changes the Alternate Base Rate at which borrowings bear interest to a rate per annum equal to the greatest of (a) the prime rate, (b) the federal funds rate plus 0.50% and (c) the adjusted LIBOR rate for a one month period plus 1.0%, plus, in any such case, an additional spread of 0.30% to 0.90%, depending on our leverage ratio; and |

• | changes related to new or recently revised financial regulations. |

The 2011 Credit Agreement gives the Lenders a pledge of 65% of the stock of certain first tier foreign subsidiaries. The obligations under the 2011 Credit Agreement are also guaranteed by certain of our first tier domestic subsidiaries.

The 2011 Credit Agreement contains customary representations, warranties and covenants, including but not limited to covenants restricting our ability to incur indebtedness and liens and merge or consolidate with another entity. Further, the 2011 Credit Agreement contains the following covenants:

• | a covenant requiring us to maintain an indebtedness to EBITDA ratio as of the end of each quarter of not greater than 3.00 to 1; |

• | a covenant requiring us to maintain an EBITDA to interest expense ratio as of the end of each quarter of no less than 3.50 to 1; |

• | a covenant restricting us from paying dividends or repurchasing stock if, after giving effect to such payments, our leverage ratio is greater than 2.00 to 1, in such case limiting such payments to an amount ranging from $50.0 million to $75.0 million during any fiscal year based on our leverage ratio after giving effect to such payments; and |

• | a covenant restricting our ability to make acquisitions, if, after giving pro-forma effect to such acquisition, our leverage ratio is greater than 2.75 to 1, in such case limiting acquisitions to $25.0 million. |

As of December 31, 2014, we were in compliance with all covenants under the Credit Agreement. There was $10.0 million in outstanding borrowings under this facility at December 31, 2014, with a weighted average interest rate of 1.46%.

Prudential Investment Management, Inc.

On July 29, 2009, we entered into a Private Shelf Agreement (the “Shelf Agreement”) with Prudential Investment Management, Inc. (“Prudential”) and Prudential affiliates from time to time party thereto. The Shelf Agreement provides us and our subsidiaries access to an uncommitted, senior secured, maximum aggregate principal amount of $80.0 million of debt capital. The Shelf Agreement contains representations, warranties and covenants, including but not limited to covenants restricting our ability to incur indebtedness and liens and to merge or consolidate with another entity.

On May 5, 2011, we entered into Amendment No. 1 to our Private Shelf Agreement (the “Amendment”).

The Amendment principally provides the following changes to the Shelf Agreement:

• | elimination of the security interest in our personal property and subsidiaries; |

• | an amendment to the maximum leverage ratio to not greater than 3.00 to 1 for any period ending on or after March 31, 2011; |

• | an amendment to our restriction regarding the payment of dividends or repurchase of stock to restrict us from paying dividends or repurchasing stock if, after giving effect to such payments, our leverage ratio is greater than 2.00 to 1, in such case limiting such payments to an amount ranging from $50.0 million to $75.0 million during any fiscal year based on our leverage ratio after giving effect to such payments; and |

• | an amendment to Permitted Acquisitions restricting our ability to make acquisitions, if, after giving pro-forma effect to such acquisition, our leverage ratio is greater than 2.75 to 1, in such case limiting acquisitions to $25.0 million. |

On July 24, 2012, we entered into Amendment No. 2 to our Private Shelf Agreement (“Amendment No. 2”), which amends the Shelf Agreement. The principal change effected by Amendment No. 2 is an extension of the Issuance Period for Shelf Notes under the Shelf Agreement. The Issuance Period now expires on July 24, 2015.

14

As of December 31, 2014, there was $18.0 million in outstanding borrowings under this facility; the $8.0 million Series A notes issued in March 2011 with a fixed interest rate of 4.00% and a seven-year term serially maturing from 2014 to 2018; and the $10.0 million Series B notes issued in June 2011 with a fixed interest rate of 4.10% and a 10-year term serially maturing from 2015 to 2021. The first payment of $2.0 million on Series A notes was made during the first quarter of 2014. We were in compliance with all covenants of the Shelf Agreement as of December 31, 2014.

The Royal Bank of Scotland Citizens, N.A.

On September 14, 2010, we entered into an overdraft facility with The Royal Bank of Scotland Citizens, N.A. in the amount of 2.0 million Euros or approximately $2.4 million. There was no balance outstanding on this facility as of December 31, 2014.

HSBC Bank (China) Company Limited, Shanghai Branch

On June 20, 2012, we entered into a banking facility with the HSBC Bank (China) Company Limited, Shanghai Branch in the amount of $5.0 million. During the first quarter of 2014, we repaid previous borrowings under this facility amounting to $1.5 million and, as of December 31, 2014, there were no outstanding borrowings on this facility.

Collateralized Borrowings

Collateralized borrowings represent deferred sales proceeds on certain leasing transactions with third-party leasing companies. These transactions are accounted for as borrowings, with the related assets capitalized as property, plant and equipment and depreciated straight-line over the lease term.

Capital Lease Obligations

Capital lease obligations outstanding are primarily related to sale-leaseback transactions with third-party leasing companies whereby we sell our manufactured equipment to the leasing company and lease it back. The equipment covered by these leases is rented to our customers over the lease term.

Contractual Obligations – Our contractual obligations as of December 31, 2014, are summarized by period due in the following table (in thousands):

Total | Less Than 1 Year | 1 - 3 Years | 3 - 5 Years | More Than 5 Years | |||||||||||||||

Long-term debt(1) | $ | 28,000 | $ | 3,429 | $ | 6,857 | $ | 14,857 | $ | 2,857 | |||||||||

Interest payments on long-term debt(1) | 2,457 | 787 | 1,157 | 396 | 117 | ||||||||||||||

Capital leases | 130 | 130 | — | — | — | ||||||||||||||

Interest payments on capital leases | 8 | 8 | — | — | — | ||||||||||||||

Retirement benefit plans(2) | 1,474 | 1,474 | — | — | — | ||||||||||||||

Deferred compensation arrangements(3) | 7,660 | 1,014 | 847 | 700 | 5,099 | ||||||||||||||

Operating leases(4) | 18,368 | 7,738 | 7,605 | 2,471 | 554 | ||||||||||||||

Purchase obligations(5) | 61,616 | 61,616 | — | — | — | ||||||||||||||

Other(6) | 9,537 | 9,537 | — | — | — | ||||||||||||||

Total contractual obligations | $ | 129,250 | $ | 85,733 | $ | 16,466 | $ | 18,424 | $ | 8,627 | |||||||||

(1)Long-term debt represents borrowings through our Credit Agreement with JPMorgan and our Shelf Agreement with Prudential. Our Credit Agreement with JPMorgan does not have specified repayment terms; therefore, repayment is due upon expiration of the agreement on March 1, 2018. Interest payments on our Credit Agreement were calculated using the December 31, 2014 LIBOR rate based on the assumption that the principal would be repaid in full upon the expiration of the agreement. Our borrowings under our Shelf Agreement with Prudential have 7 and 10 year terms, serially maturing from 2014 to 2021 with fixed interest rates of 4.00% and 4.10%, respectively.

(2)Our retirement benefit plans, as described in Note 11 of the Consolidated Financial Statements, require us to make contributions to the plans from time to time. Our plan obligations totaled $10.5 million as of December 31, 2014. Contributions to the various plans are dependent upon a number of factors including the market performance of plan assets, if any, and future changes in interest rates, which impact the actuarial measurement of plan obligations. As a result, we have only included our 2015 expected contribution in the contractual obligations table.

(3)The unfunded deferred compensation arrangements covering certain current and retired management employees totaled $7.7 million as of December 31, 2014. Our estimated distributions in the contractual obligations table are based upon a number of assumptions including termination dates and participant distribution elections.

(4)Operating lease commitments consist primarily of office and warehouse facilities, vehicles and office equipment as discussed in Note 13 of the Consolidated Financial Statements.

(5)Purchase obligations include all known open purchase orders, contractual purchase commitments and contractual obligations as of December 31, 2014.

(6)Other obligations include collateralized borrowings as discussed in Note 8 of the Consolidated Financial Statements and residual value guarantees as discussed in Note 13 of the Consolidated Financial Statements.

Total contractual obligations exclude our gross unrecognized tax benefits of $3.0 million and accrued interest and penalties of $0.6 million as of December 31, 2014. We expect to make cash outlays in the future related to uncertain tax positions. However, due to the uncertainty of the timing of future cash flows, we are unable to make reasonably reliable estimates of the period of cash settlement, if any, with the respective taxing authorities. For further information related to unrecognized tax benefits, see Note 14 of the Consolidated Financial Statements.

15

Newly Issued Accounting Guidance

Revenues from Contracts with Customers

In May 2014, the Financial Accounting Standards Board issued Accounting Standards Update (ASU) No. 2014-09, Revenue from Contracts with Customers (Topic 606). This ASU will replace all existing revenue recognition standards and significantly expand the disclosure requirements for revenue arrangements. This guidance requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. This guidance provides a five-step analysis of transactions to determine when and how revenue is recognized. Other major provisions include capitalization of certain contract costs, consideration of time value of money in the transaction price, and allowing estimates of variable consideration to be recognized before contingencies are resolved in certain circumstances. This guidance also requires enhanced disclosures regarding the nature, amount, timing and uncertainty of revenue and cash flows arising from an entity's contracts with customers. The provisions of ASU 2014-09 are effective for annual periods beginning after December 15, 2016, including interim periods within that reporting period, and early application is not permitted. The new standard may be adopted retrospectively for all periods presented, or adopted using a modified retrospective approach. Under the retrospective approach, the fiscal 2016 and 2015 financial statements would be adjusted to reflect the effects of applying the new standard on those periods. Under the modified retrospective approach, the new standard would only be applied for the period beginning January 1, 2017 to new contracts and those contracts that are not yet complete at January 1, 2017, with a cumulative catch-up adjustment recorded to beginning retained earnings for existing contracts that still require performance. Management is currently evaluating the methods of adoption allowed by the new standard and the effect the standard is expected to have on our financial statements and related disclosures.

No other new accounting pronouncements issued during 2014 but not yet effective have had, or are expected to have, a material impact on our results of operations or financial position.

Critical Accounting Policies and Estimates