Attached files

| file | filename |

|---|---|

| EX-10.3 - SCHEDULE OF PARTIES TO MANAGEMENT AND EXECUTIVE EMPLOYMENT AGREEMENT - TENNANT CO | exhibit_10-3.htm |

| EX-32.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 906 - TENNANT CO | exhibit_32-2.htm |

| EX-32.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 906 - TENNANT CO | exhibit_32-1.htm |

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - TENNANT CO | exhibit_31-2.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - TENNANT CO | exhibit_31-1.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - TENNANT CO | exhibit_23-1.htm |

| EX-21 - SUBSIDIARIES OF THE REGISTRANT - TENNANT CO | exhibit_21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[ü] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2017 |

OR | |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from __________ to __________. |

Commission File Number 001-16191

TENNANT COMPANY

(Exact name of registrant as specified in its charter)

Minnesota | 41-0572550 | |

State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization | Identification No.) | |

701 North Lilac Drive, P.O. Box 1452 Minneapolis, Minnesota 55440 |

(Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code 763-540-1200

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of exchange on which registered | |

Common Stock, par value $0.375 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. | ü | Yes | No | |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | ü | No | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ü | Yes | No | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | ü | Yes | No | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | [ ] | |||

1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. | |||||

Large accelerated filer | ü | Accelerated filer | |||

Non-accelerated filer | (Do not check if a smaller reporting company) | Smaller reporting company | |||

Emerging growth company | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | [ ] | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | ü | No | |

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2017, was $1,292,419,327. | ||||

As of January 31, 2018, there were 17,881,327 shares of Common Stock outstanding. | ||||

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2018 annual meeting of shareholders (the “2018 Proxy Statement”) are incorporated by reference in Part III.

2

Tennant Company

Form 10–K

Table of Contents

PART I | Page | ||||

PART II | |||||

PART III | |||||

PART IV | |||||

3

TENNANT COMPANY

2017

ANNUAL REPORT

Form 10–K

(Pursuant to Securities Exchange Act of 1934)

PART I

ITEM 1 – Business

General Development of Business

Founded in 1870 by George H. Tennant, Tennant Company, a Minnesota corporation incorporated in 1909, began as a one-man woodworking business, evolved into a successful wood flooring and wood products company, and eventually into a manufacturer of floor cleaning equipment. Throughout its history, Tennant has remained focused on advancing our industry by aggressively pursuing new technologies and creating a culture that celebrates innovation.

Today, Tennant Company is a recognized leader of the cleaning industry. We are passionate about developing innovative and sustainable solutions that help our customers clean spaces more effectively, addressing indoor and outdoor cleaning challenges. Tennant Company operates in three geographic business units including the Americas, Europe, Middle East and Africa (EMEA) and Asia Pacific (APAC). In April 2017, Tennant Company completed its acquisition of the IPC Group, a multi-brand manufacturer of a broad range of cleaning and accessory equipment. With primary operations in Italy, the IPC Group significantly enhances Tennant's position in the EMEA region and brings to Tennant a broader product offering.

Tennant Company is committed to empowering our customers to create a cleaner, safer and healthier world with high-performance solutions that minimize waste, reduce costs, improve safety and further sustainability goals.

Segment and Geographic Area Financial Information

The Company has one reportable business segment. Sales to customers geographically located in the United States were $543.7 million, $525.3 million and $517.9 million for the years ended December 31, 2017, 2016 and 2015, respectively. Long-lived assets located in the United States were $108.0 and $109.2 million as of the years ended December 31, 2017 and 2016, respectively. Additional financial information on the Company’s segment and geographic areas is provided throughout Item 8 and Note 19 to the Consolidated Financial Statements.

Principal Products, Markets and Distribution

The Company offers products and solutions consisting of mechanized cleaning equipment, detergent-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, specialty surface coatings, and business solutions such as financing, rental and leasing programs, and machine-to-machine asset management solutions.

The Company's products are used in many types of environments including: Retail establishments, distribution centers, factories and warehouses, public venues such as arenas and stadiums, office buildings, schools and universities, hospitals and clinics, parking lots and streets, and more. The Company markets its offerings under the following brands: Tennant®, Nobles®, Green Machines™, Alfa Uma Empresa Tennant™, IRIS®, Superior Anodes, Waterstar and Orbio®. Orbio Technologies, which markets and sells Orbio-branded products and solutions, is a group created by the Company to focus on expanding the opportunities for the emerging category of On-Site Generation (OSG). OSG technologies create and dispense effective cleaning and antimicrobial solutions on site within a facility. Customers include contract cleaners to whom organizations outsource facilities maintenance, as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

In April 2017, the Company completed its acquisition of the IPC Group business ("IPC"). IPC manufactures a complete range of commercial cleaning products including mechanized cleaning equipment, wet & dry vacuum cleaners, cleaning tools & carts and high pressure washers. These products are sold into similar vertical market applications as those listed above, but also into office cleaning and hospitality vertical markets through a global direct sales and service organization and network of distributors. IPC markets products and services under the following valued brands: IPC, Gansow, Vaclensa, Portotecnica, Soteco and private-label brands.

Raw Materials

The Company has not experienced any significant or unusual problems in the availability of raw materials or other product components. The Company has sole-source vendors for certain components. A disruption in supply from such vendors may disrupt the Company’s operations. However, the Company believes that it can find alternate sources in the event there is a disruption in supply from such vendors.

Intellectual Property

Although the Company considers that its patents, proprietary technologies and trade secrets, customer relationships, licenses, trademarks, trade names and brand names in the aggregate constitute a valuable asset, it does not regard its business as being materially dependent upon any single item or category of intellectual property. We take appropriate measures to protect our intellectual property to the extent such intellectual property can be protected.

Seasonality

Although the Company’s business is not seasonal in the traditional sense, the percentage of revenues in each quarter typically ranges from 22% to 28% of the total year. The first quarter tends to be at the low end of the range reflecting customers’ initial slow ramp up of capital purchases and the Company’s efforts to close out orders at the end of each year. The second and fourth quarters tend to be towards the high end of the range and the third quarter is typically in the middle of the range.

4

Working Capital

The Company funds operations through a combination of cash and cash equivalents and cash flows from operations. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. In addition, credit facilities are available for additional working capital needs or investment opportunities.

Major Customers

The Company sells its products to a wide variety of customers, none of which are of material importance in relation to the business as a whole. The customer base includes several governmental entities which generally have terms similar to other customers.

Backlog

The Company processes orders within two weeks, on average. Therefore, no significant backlogs existed at December 31, 2017 and 2016.

Competition

Public industry data concerning global market share is limited; however, through an assessment of validated third party sources and sponsored third party market studies, the Company is confident in its position as a world-leading manufacturer of floor maintenance and cleaning equipment. Several global competitors compete with Tennant in virtually every geography of the world. However, small regional competitors are also significant competitors who vary by country, vertical market, product category or channel. The Company competes primarily on the basis of offering a broad line of high-quality, innovative products supported by an extensive sales and service network in major markets.

Research and Development

Tennant Company has a history of developing innovative technologies to create a cleaner, safer, healthier world. The Company is committed to its innovation leadership position through fulfilling its goal to annually invest 3% to 4% of annual sales to research and development. The Company’s innovation efforts are focused on solving our customers’ needs holistically addressing a broad array of issues, such as managing labor costs, enhancing productivity, and making cleaning processes more efficient and sustainable. Through core product development, partnerships and technology enablement we are creating new growth avenues for Tennant. These new avenues for growth go beyond cleaning equipment into business insights and service solutions. In 2017, 2016 and 2015, the Company spent $32.0 million, $34.7 million and $32.4 million on research and development, respectively.

Environmental Compliance

Compliance with Federal, State and local provisions which have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, has not had, and the Company does not expect it to have, a material effect upon the Company’s capital expenditures, earnings or competitive position.

Employees

The Company employed approximately 4,300 people in worldwide operations as of December 31, 2017.

Available Information

The Company makes available free of charge, through the Investor Relations website at investors.tennantco.com, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable when such material is filed electronically with, or furnished to, the Securities and Exchange Commission (“SEC”).

Executive Officers of the Registrant

The list below identifies those persons designated as executive officers of the Company, including their age, positions held with the Company and their business experience during the past five or more years.

David W. Huml, Senior Vice President, EMEA, APAC and Global Marketing

David W. Huml (49) joined the Company in November 2014 as Senior Vice President, Global Marketing. In January 2016, he also assumed oversight for the Company's APAC business unit and in January 2017, he assumed oversight for the Company's EMEA business. From 2006 to October 2014, he held various positions with Pentair plc, a global manufacturer of water and fluid solutions, valves and controls, equipment protection and thermal management products, most recently as Vice President, Applied Water Platform. From 1992 to 2006, he held various positions with Graco Inc., a designer, manufacturer and marketer of systems and equipment to move, measure, control, dispense and spray fluid and coating materials, including Worldwide Director of Marketing, Contractor Equipment Division.

H. Chris Killingstad, President and Chief Executive Officer

H. Chris Killingstad (62) joined the Company in April 2002 as Vice President, North America and was named President and CEO in 2005. From 1990 to 2002, he was employed by The Pillsbury Company, a consumer foods manufacturer. From 1999 to 2002 he served as Senior Vice President and General Manager of Frozen Products for Pillsbury North America; from 1996 to 1999 he served as Regional Vice President and Managing Director of Pillsbury Europe, and from 1990 to 1996 was Regional Vice President of Häagen-Dazs Asia Pacific. He held the position of International Business Development Manager at PepsiCo Inc., from 1982-1990 and Financial Manager for General Electric, from 1978-1980.

Carol E. McKnight, Senior Vice President, Chief Administrative Officer

Carol E. McKnight (50) joined the Company in June 2014 as Senior Vice President of Global Human Resources. In 2017, Carol was named SVP and Chief Administrative Officer. Prior to joining Tennant, she was Vice President of Human Resources at ATK (Alliant Techsystems) where she held divisional and corporate leadership positions in the areas of compensation, talent management, talent acquisition and general human resource management. Prior to ATK, she was with New Jersey-based NRG Energy, Inc.

Jeffrey C. Moorefield, Senior Vice President, Global Operations

Jeffrey C. Moorefield (54) joined the Company in April 2015 as Senior Vice President, Global Operations. From 2001 to 2008 and 2010 to March 2015, he held various positions with Pentair plc, a global manufacturer of water and fluid solutions, valves and controls, equipment protection and thermal management products, most recently as Global Vice President of Operation - Technical Solutions. From 2008 to 2010, he was Head of Operations for Netshape Technology, a technical start-up company. From 1987 to 2001, he held various positions with Emerson Electric Company, a worldwide technology and engineering company, culminating in Vice President, Operations. From 1985 to 1987, he was a Design Engineer at Smith & Proffit Machine & Engineering, a custom equipment engineering company.

Thomas Paulson, Senior Vice President and Chief Financial Officer

Thomas Paulson (61) joined the Company in March 2006 as Vice President and Chief Financial Officer and was named Senior Vice President and Chief Financial Officer in October 2013. Prior to joining Tennant, he was Chief Financial Officer and Senior Vice President of Innovex from 2001 to February 2006. Prior to joining Innovex, a manufacturer of electronic interconnect solutions, he worked for The Pillsbury Company for over 19 years. He became a Vice President at Pillsbury in 1995 and was the Vice President of Finance for the $4 billion North American Foods Division for over two years before joining Innovex.

5

Jeffrey L. Cotter, Senior Vice President, General Counsel and Corporate Secretary

Jeffrey L. Cotter (50) joined the Company in September 2017 as Senior Vice President, General Counsel and Corporate Secretary. Previously, he was with G&K Services, Inc., starting in 2006 and from 2008 to 2017 serving as Vice President, General Counsel, and Corporate Secretary. Prior to G&K Services, Inc., he was a shareholder at Leonard, Street and Deinard P.A. (n/k/a Stinson Leonard Street LLP).

Richard H. Zay, Senior Vice President, The Americas and R&D

Richard H. Zay (47) joined the Company in June 2010 as Vice President, Global Marketing and was named Senior Vice President, Global Marketing in October 2013. In 2014, he was named Senior Vice President of the Americas business unit for Tennant and in 2018 he assumed responsibility for Tennant Research and Development as well. From 2006 to 2010, he held various positions with Whirlpool Corporation, a manufacturer of major home appliances, most recently as General Manager, KitchenAid Brand. From 1993 to 2006, he held various positions with Maytag Corporation, including Vice President, Jenn-Air Brand, Director of Marketing, Maytag Brand, and Director of Cooking Category Management.

ITEM 1A – Risk Factors

The following are significant factors known to us that could materially adversely affect our business, financial condition or operating results.

We may not be able to effectively manage organizational changes which could negatively impact our operating results or financial condition.

We are continuing to implement global standardized processes in our business despite lean staffing levels. We continue to consolidate and reallocate resources as part of our ongoing efforts to optimize our cost structure in the current economy. Our operating results may be negatively impacted if we are unable to implement new processes and manage organizational changes, which includes changes to our go-to-market strategy, systems and processes, simultaneous focus on expense control and growth and introduction of alternative cleaning methods. In addition, if we do not effectively realize and sustain the benefits that these transformations are designed to produce, we may not fully realize the anticipated savings of these actions or they may negatively impact our ability to serve our customers or meet our strategic objectives.

Our ability to effectively operate our Company could be adversely affected if we are unable to attract and retain key personnel and other highly skilled employees, provide employee development opportunities and create effective succession planning strategies.

Our growth strategy, expanding global footprint, changing workforce demographics and increased improvements in technology and business processes designed to enhance the customer experience are putting increased pressure on human capital strategies designed to recruit, retain and develop top talent.

Our continued success will depend on, among other things, the skills and services of our executive officers and other key personnel. Our ability to attract and retain highly qualified managerial, technical, manufacturing, research, sales and marketing personnel also impacts our ability to effectively operate our business. As the economy recovers and companies grow and increase their hiring activities, there is an inherent risk of increased employee turnover and the loss of valuable employees in key positions, especially in emerging markets. We believe the increased loss of key personnel within a concentrated region could adversely affect our sales growth.

In addition, there is a risk that we may not have adequate talent acquisition resources and employee development resources to support our future hiring needs and provide training and development opportunities to all employees. This, in turn, could impede our workforce from embracing change and leveraging the improvements we have made in technology and other business process enhancements.

We are subject to competitive risks associated with developing innovative products and technologies, including but not limited to, not expanding as rapidly or aggressively in the global market as our competitors, our customers not continuing to pay for innovation and competitive challenges to our products, technology and the underlying intellectual property.

Our products are sold in competitive markets throughout the world. Competition is based on product features and design, brand recognition, reliability, durability, technology, breadth of product offerings, price, customer relationships and after-sale service. Although we believe that the performance and price characteristics of our products will produce competitive solutions for our customers’ needs, our products are generally priced higher than our competitors’ products. This is due to our dedication to innovation and continued investments in research and development. We believe that customers will pay for the innovations and quality in our products. However, it may be difficult for us to compete with lower priced products offered by our competitors and there can be no assurance that our customers will continue to choose our products over products offered by our competitors. If our products, markets and services are not competitive, we may experience a decline in sales volume, an increase in price discounting and a loss of market share, which adversely impacts revenues, margin and the success of our operations.

Competitors may also initiate litigation to challenge the validity of our patents or claims, allege that we infringe upon their patents, violate our patents or they may use their resources to design comparable products that avoid infringing our patents. Regardless of whether such litigation is successful, such litigation could significantly increase our costs and divert management’s attention from the operation of our business, which could adversely affect our results of operations and financial condition.

Increases in the cost of, quality, or disruption in the availability of, raw materials and components that we purchase to manufacture our products could negatively impact our operating results or financial condition.

Our sales growth, expanding geographical footprint and continued use of sole source vendors (concentration risk), coupled with suppliers’ potential credit issues, could lead to an increased risk of a breakdown in our supply chain. There is an increased risk of defects due to the highly configured nature of our purchased component parts that could result in quality issues, returns or production slow-downs. In addition, modularization may lead to more sole sourced products and as we seek to outsource the design of certain key components, we risk loss of proprietary control and becoming more reliant on a sole source. There is also a risk that the vendors we choose to supply our parts and equipment fail to comply with our quality expectations, thus damaging our reputation for quality and negatively impacting sales.

6

The SEC has adopted rules regarding disclosure of the use of “conflict minerals” (commonly referred to as tin, tantalum, tungsten and gold) which are mined from the Democratic Republic of the Congo in products we manufacture or contract to manufacture. These rules have required and will continue to require due diligence and disclosure efforts. There are and will continue to be costs associated with complying with this disclosure requirement, including costs to determine which of our products are subject to the rules and the source of any "conflict minerals" used in these products. Since our supply chain is complex, ultimately we may not be able to sufficiently discover the origin of the conflict minerals used in our products through the due diligence procedures that we implement. If we are unable to or choose not to provide appropriate disclosure, customers may choose not to purchase our products. Alternatively, if we choose to use only suppliers offering conflict free minerals, we cannot be sure that we will be able to obtain metals, if necessary, from such suppliers in sufficient quantities or at competitive prices. Any one or a combination of these various factors could harm our business, reduce market demand for our products, and adversely affect our profit margins, net sales, and overall financial results.

We may not be able to upgrade and evolve our information technology systems as quickly as we wish and we may encounter difficulties as we upgrade and evolve these systems to support our growth strategy and business operations, which could adversely impact our abilities to accomplish anticipated future cost savings and better serve our customers.

We have many information technology systems that are important to the operation of our business and are in need of upgrading in order to effectively implement our growth strategy. Given our greater emphasis on customer-facing technologies, we may not have adequate resources to upgrade our systems at the pace which the current business environment demands. Additionally, significantly upgrading and evolving the capabilities of our existing systems could lead to inefficient or ineffective use of our technology due to lack of training or expertise in these evolving technology systems. These factors could lead to significant expenses, adversely impacting our results of operations and hinder our ability to offer better technology solutions to our customers.

Inadequate funding or insufficient innovation of new technologies may result in an inability to develop and commercialize new innovative products and services.

We strive to develop new and innovative products and services to differentiate ourselves in the marketplace. New product development relies heavily on our financial and resource investments in both the short term and long term. If we fail to adequately fund product development projects or fund a project which ultimately does not gain the market acceptance we anticipated, we risk not meeting our customers' expectations, which could result in decreased revenues, declines in margin and loss of market share.

We may consider acquisition of suitable candidates to accomplish our growth objectives. We may not be able to successfully integrate the businesses we acquire to achieve operational efficiencies, including synergistic and other benefits of acquisition.

We may consider, as part of our growth strategy, supplementing our organic growth through acquisitions of complementary businesses or products. We have engaged in acquisitions in the past, such as the acquisition of the IPC Group, and we believe future acquisitions may provide meaningful opportunities to grow our business and improve profitability. Acquisitions allow us to enhance the breadth of our product offerings and expand the market and geographic participation of our products and services.

However, our success in growing by acquisition is dependent upon identifying businesses to acquire, integrating the newly acquired businesses with our existing businesses and complying with the terms of our credit facilities. We may incur difficulties in the realignment and integration of business activities when assimilating the operations and products of an

acquired business or in realizing projected efficiencies, cost savings, revenue synergies and profit margins. Acquired businesses may not achieve the levels of revenue, profit, productivity or otherwise perform as expected. We are also subject to incurring unanticipated liabilities and contingencies associated with an acquired entity that are not identified or fully understood in the due diligence process. Current or future acquisitions may not be successful or accretive to earnings if the acquired businesses do not achieve expected financial results.

In addition, we may record significant goodwill or other intangible assets in connection with an acquisition. We are required to perform impairment tests at least annually and whenever events indicate that the carrying value may not be recoverable from future cash flows. If we determine that any intangible asset values need to be written down to their fair values, this could result in a charge that may be material to our operating results and financial condition.

We may not be able to generate sufficient cash to service all of our indebtedness, and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

In April 2017, in connection with the acquisition of IPC Cleaning S.p.A., we entered into a new senior credit facility and indenture, and issued debt totaling approximately $400,000, consisting of a $100,000 term loan and $300,000 of senior notes, which funded the acquisition and replaced our current debt facility. The new senior credit facility also includes a revolving facility in an amount up to $200,000. We cannot provide assurance that our business will generate sufficient cash flow from operations to meet all our debt service requirements, to pay dividends, to repurchase shares of our common stock, and to fund our general corporate and capital requirements.

Our ability to satisfy our debt obligations will depend upon our future operating performance. We do not have complete control over our future operating performance because it is subject to prevailing economic conditions, and financial, business and other factors.

Our current and future debt service obligations and covenants could have important consequences. These consequences include, or may include, the following:

• | our ability to obtain financing for future working capital needs or acquisitions or other purposes may be limited; |

• | our funds available for operations, expansions, dividends or other distributions, or stock repurchases may be reduced because we dedicate a significant portion of our cash flow from operations to the payment of principal and interest on our indebtedness; |

• | our ability to conduct our business could be limited by restrictive covenants; and |

• | our vulnerability to adverse economic conditions may be greater than less leveraged competitors and, thus, our ability to withstand competitive pressures may be limited. |

Restrictive covenants in our senior credit facility and in our indenture place limits on our ability to conduct our business. Covenants in our senior credit facility and indenture include those that restrict our ability to make acquisitions, incur debt, encumber or sell assets, pay dividends, engage in mergers and consolidations, enter into transactions with affiliates, make investments and permit our subsidiaries to enter into certain restrictive agreements. The senior credit facility additionally contains certain financial covenants. We cannot provide assurance that we will be able to comply with these covenants in the future.

7

We may encounter financial difficulties if the United States or other global economies experience an additional or continued long-term economic downturn, decreasing the demand for our products and negatively affecting our sales growth.

Our product sales are sensitive to declines in capital spending by our customers. Decreased demand for our products could result in decreased revenues, profitability and cash flows and may impair our ability to maintain our operations and fund our obligations to others. In the event of a continued long-term economic downturn in the U.S. or other global economies, our revenues could decline to the point that we may have to take cost-saving measures, such as restructuring actions. In addition, other fixed costs would have to be reduced to a level that is in line with a lower level of sales. A long-term economic downturn that puts downward pressure on sales could also negatively affect investor perception relative to our publicly stated growth targets.

We may encounter risks to our IT infrastructure, such as access and security, that may not be adequately designed to protect critical data and systems from theft, corruption, unauthorized usage, viruses, sabotage or unintentional misuse.

Global cybersecurity threats and incidents can range from uncoordinated individual attempts to gain unauthorized access to IT systems to sophisticated and targeted measures known as advanced persistent threats, directed at the Company, its products and its customers. We seek to deploy comprehensive measures to deter, prevent, detect, react to and mitigate these threats, including identity and access controls, data protection, vulnerability assessments, continuous monitoring of our IT networks and systems and maintenance of backup and protective systems.

Despite these efforts, cybersecurity incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data and confidential or proprietary information (our own or that of third parties) and the disruption of business operations. The potential consequences of a material cybersecurity incident include financial loss, reputational damage, litigation with third parties, theft of intellectual property, diminution in the value of our investment in research, development and engineering, and increased cybersecurity protection and remediation costs due to the increasing sophistication and proliferation of threats, which in turn could adversely affect our competitiveness and results of operations.

We may be unable to conduct business if we experience a significant business interruption in our computer systems, manufacturing plants or distribution facilities for a significant period of time.

We rely on our computer systems, manufacturing plants and distribution facilities to efficiently operate our business. If we experience an interruption in the functionality in any of these items for a significant period of time for any reason, we may not have adequate business continuity planning contingencies in place to allow us to continue our normal business operations on a long-term basis. In addition, the increase in customer facing technology raises the risk of a lapse in business operations. Therefore, significant long-term interruption in our business could cause a decline in sales, an increase in expenses and could adversely impact our financial results.

Our global operations are subject to laws and regulations that impose significant compliance costs and create reputational and legal risk.

Due to the international scope of our operations, we are subject to a complex system of commercial, tax and trade regulations around the world. Recent years have seen an increase in the development and enforcement of laws regarding trade, tax compliance, labor and safety and anti-corruption, such as the U.S. Foreign Corrupt Practices Act, and similar laws from other countries. Our numerous foreign subsidiaries and affiliates are governed by laws, rules and business practices that differ from those of the U.S., but because we are a U.S. based company, oftentimes they are also subject to U.S. laws which can create a conflict. Despite our due diligence, there is a risk that we do not have adequate resources or comprehensive processes to stay current on changes in laws or regulations applicable to us worldwide and maintain compliance with those changes. Increased compliance requirements may lead to increased costs and erosion of desired profit margin. As a result, it is possible that the activities of these entities may not comply with U.S. laws or business practices or our Business Ethics Guide. Violations of the U.S. or local laws may result in severe criminal or civil sanctions, could disrupt our business, and result in an adverse effect on our reputation, business and results of operations or financial condition. We cannot predict the nature, scope or effect of future regulatory requirements to which our operations might be subject or the manner in which existing laws might be administered or interpreted.

In addition to the foregoing, the European Union adopted a comprehensive General Data Privacy Regulation (the "GDPR") in May 2016 that will replace the current EU Data Protection Directive and related country-specific legislation. The GDPR will become fully effective in May 2018. GDPR requires companies to satisfy new requirements regarding the handling of personal and sensitive data, including its use, protection and the ability of persons whose data is stored to correct or delete such data about themselves. Failure to comply with GDPR requirements could result in penalties of up to 4% of worldwide revenue.

Actions of activist investors or others could disrupt our business.

Public companies have been the target of activist investors. One investor which owns approximately 5% of our outstanding common stock recently filed a Schedule 13D with the Securities and Exchange Commission which stated its belief that we should undertake a strategic review process regarding a consolidation transaction with a third party. In the event such investor or another third party, such as an activist investor, continues to pursue such belief or proposes to change our governance policies, board of directors, or other aspects of our operations, our review and consideration of such proposals may create a significant distraction for our management and employees. This could negatively impact our ability to execute our business plans and may require our management to expend significant time and resources. Such proposals may also create uncertainties with respect to our financial position and operations and may adversely affect our ability to attract and retain key employees.

8

Foreign currency exchange rate fluctuations, particularly the strengthening of the U.S. dollar against other major currencies, could result in declines in our reported net sales and net earnings.

We earn revenues, pay expenses, own assets and incur liabilities in countries using functional currencies other than the U.S. dollar. Because our consolidated financial statements are presented in U.S. dollars, we translate revenues and expenses into U.S. dollars at the average exchange rate during each reporting period, as well as assets and liabilities into U.S. dollars at exchange rates in effect at the end of each reporting period. Therefore, increases or decreases in the value of the U.S. dollar against other major currencies will affect our net revenues, net earnings, earnings per share and the value of balance sheet items denominated in foreign currencies as we translate them into the U.S. dollar reporting currency. We use derivative financial instruments to hedge our estimated transactional or translational exposure to certain foreign currency-denominated assets and liabilities as well as our foreign currency denominated revenue. While we actively manage the exposure of our foreign currency market risk in the normal course of business by utilizing various foreign exchange financial instruments, these instruments involve risk and may not effectively limit our underlying exposure from foreign currency exchange rate fluctuations or minimize the effects on our net earnings and the cash volatility associated with foreign currency exchange rate changes. Fluctuations in foreign currency exchange rates, particularly the strengthening of the U.S. dollar against major currencies, could materially affect our financial results.

We are subject to product liability claims and product quality issues that could adversely affect our operating results or financial condition.

Our business exposes us to potential product liability risks that are inherent in the design, manufacturing and distribution of our products. If products are used incorrectly by our customers, injury may result leading to product liability claims against us. Some of our products or product improvements may have defects or risks that we have not yet identified that may give rise to product quality issues, liability and warranty claims. Quality issues may also arise due to changes in parts or specifications with suppliers and/or changes in suppliers. If product liability claims are brought against us for damages that are in excess of our insurance coverage or for uninsured liabilities and it is determined we are liable, our business could be adversely impacted. Any losses we suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may have a negative impact on our business and operating results. We could experience a material design or manufacturing failure in our products, a quality system failure, other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. Any unforeseen product quality problems could result in loss of market share, reduced sales and higher warranty expense.

The integration of IPC's operations into ours following its acquisition could create additional risks for our internal controls over financial reporting.

We intend to integrate IPC into our control environment and subject it to internal control testing during 2018, which means that deficiencies in our internal control over financial reporting as a combined company may not be identified until then. Any such undiscovered deficiencies, if material, could result in misstatements of our results of operations, restatements of our financial statements, declines in the trading price of our common stock or otherwise have a material adverse effect on our business, reputation, results of operations, financial condition or cash flows.

ITEM 1B – Unresolved Staff Comments

None.

ITEM 2 – Properties

The Company’s corporate offices are owned by the Company and are located in the Minneapolis, Minnesota, metropolitan area. Manufacturing facilities located in Minneapolis, Minnesota; Holland, Michigan; Chicago, Illinois; and Uden, the Netherlands are owned by the Company. Manufacturing facilities located in Louisville, Kentucky; São Paulo, Brazil; and Shanghai, China are leased to the Company. Sales offices, warehouse and storage facilities are leased in various locations in North America, Europe, Japan, China, Australia, New Zealand and Latin America. The Company’s facilities are in good operating condition, suitable for their respective uses and adequate for current needs.

In April 2017, the Company completed its acquisition of IPC. IPC has five major manufacturing facilities, all located in Italy, and 11 sales branches located in the United States, Brazil, Europe, India and China. IPC owns its manufacturing facilities located in the Italian cities of Venice, Cremona and Reggio Emilia as well as its manufacturing facility located in the Province of Padua. Another manufacturing facility located in the Province of Padua is leased to IPC. In addition, IPC uses a dedicated, third party plant in Germany that specially manufactures heavy–duty stainless steel scrubbers and sweepers to IPC designs. IPC also owns a minor tools and supplies assembly operation in China to service local customers. The facilities are in good operating condition, suitable for their respective uses and adequate for current needs.

Further information regarding the Company’s property and lease commitments is included in the Contractual Obligations section of Item 7 and in Note 15 to the Consolidated Financial Statements.

ITEM 3 – Legal Proceedings

There are no material pending legal proceedings other than ordinary routine litigation incidental to the Company’s business.

ITEM 4 – Mine Safety Disclosures

Not applicable.

9

PART II

ITEM 5 – Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

MARKET INFORMATION – Tennant's common stock is traded on the New York Stock Exchange, under the ticker symbol TNC. As of February 15, 2018, there were 324 shareholders of record. The common stock price was $61.80 per share on February 15, 2018. The accompanying chart shows the high and low sales prices for the Company’s shares for each full quarterly period over the past two years as reported by the New York Stock Exchange:

2017 | 2016 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First Quarter | $ | 76.10 | $ | 64.30 | $ | 55.71 | $ | 45.92 | |||||||

Second Quarter | 75.00 | 69.15 | 56.33 | 49.97 | |||||||||||

Third Quarter | 76.80 | 60.05 | 66.54 | 52.51 | |||||||||||

Fourth Quarter | 73.15 | 60.30 | 76.80 | 60.21 | |||||||||||

DIVIDEND INFORMATION – Cash dividends on Tennant’s common stock have been paid for 73 consecutive years. Tennant’s annual cash dividend payout increased for the 46th consecutive year to $0.84 per share in 2017, an increase of $0.03 per share over 2016. Dividends are generally declared each quarter. On February 15, 2018, the Company announced a quarterly cash dividend of $0.21 per share payable March 15, 2018, to shareholders of record on February 28, 2018.

DIVIDEND REINVESTMENT OR DIRECT DEPOSIT OPTIONS – Shareholders have the option of reinvesting quarterly dividends in additional shares of Company stock or having dividends deposited directly to a bank account. The Transfer Agent should be contacted for additional information.

TRANSFER AGENT AND REGISTRAR – Shareholders with a change of address or questions about their account may contact:

Equiniti Trust Company

Shareowner Services

P.O. Box 64874

St. Paul, MN 55164-0854

(800) 468-9716

EQUITY COMPENSATION PLAN INFORMATION – The following table provides information about shares of the Company's Common Stock that may be issued under the Company's equity compensation plans, as of December 31, 2017.

Plan Category | (a) Number of securities to be issued upon exercise of outstanding options, warrants and rights(1) | (b) Weighted-average exercise price of outstanding options, warrants and rights(2) | (c) Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column a)) | |||

Equity compensation plans approved by security holders | 1,304,385 | $47.47 | 1,155,110 | |||

Equity compensation plans not approved by security holders | — | — | — | |||

Total | 1,304,385 | $47.47 | 1,155,110 | |||

(1)Amount includes outstanding awards under the 1997 Non-Employee Director Stock Option Plan, the 2007 Stock Incentive Plan, the Amended and Restated 2010 Stock Incentive Plan, each as amended, and the 2017 Stock Incentive Plan (the "Plans"). Amount includes shares of Common Stock that may be issued upon exercise of outstanding stock options under the Plans. Amount also includes shares of Common Stock that may be paid in cash upon exercise of outstanding stock appreciation rights under the Plans. Amount also includes shares of Common Stock that may be issued upon settlement of restricted stock units and deferred stock units (phantom stock) under the Plans. Stock appreciation rights, restricted stock units and deferred stock units may be settled in cash, stock or a combination of both. Column (a) includes the number of shares that could be issued upon a complete distribution of all outstanding stock options and stock appreciation rights (1,135,608) and restricted stock units and deferred stock units (168,777).

(2)Column (b) includes the weighted-average exercise price for outstanding stock options and stock appreciation rights.

10

SHARE REPURCHASES – On October 31, 2016, the Board of Directors authorized the repurchase of an additional 1,000,000 shares of our common stock. This is in addition to the 393,965 shares remaining under our prior repurchase program. Share repurchases are made from time to time in the open market or through privately negotiated transactions, primarily to offset the dilutive effect of shares issued through our share-based compensation programs. As of December 31, 2017, our 2017 Credit Agreement restricts the payment of dividends or repurchasing of stock if, after giving effect to such payments and assuming no default exists or would result from such payment, our leverage ratio is greater than 2.50 to 1, in such case limiting such payments to an amount ranging from $50.0 million to $75.0 million during any fiscal year based on our leverage ratio after giving effect to such payment. Our Senior Notes due 2025 also contain certain restrictions, which are generally less restrictive than those contained in the 2017 Credit Agreement.

For the Quarter Ended December 31, 2017 | Total Number of Shares Purchased(1) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||

October 1–31, 2017 | 228 | $ | 68.94 | — | 1,393,965 | |||||||

November 1–30, 2017 | 922 | 67.35 | — | 1,393,965 | ||||||||

December 1–31, 2017 | — | — | — | 1,393,965 | ||||||||

Total | 1,150 | $ | 67.66 | — | 1,393,965 | |||||||

(1) | Includes 1,150 shares delivered or attested to in satisfaction of the exercise price and/or tax withholding obligations by employees who exercised stock options or restricted stock under employee share-based compensation plans. |

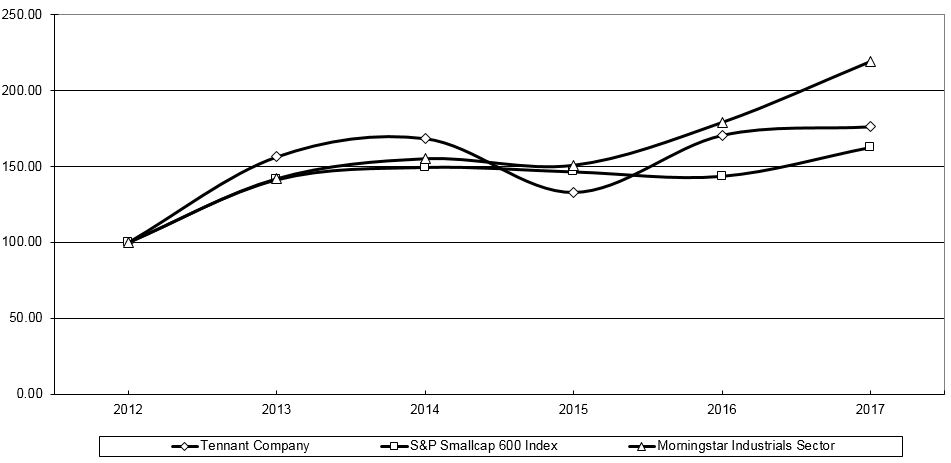

STOCK PERFORMANCE GRAPH – The following graph compares the cumulative total shareholder return on Tennant’s common stock to two indices: S&P SmallCap 600 and Morningstar Industrials Sector. The graph below compares the performance for the last five fiscal years, assuming an investment of $100 on December 31, 2012, including the reinvestment of all dividends.

5-YEAR CUMULATIVE TOTAL RETURN COMPARISON

2012 | 2013 | 2014 | 2015 | 2016 | 2017 | ||||||

Tennant Company | $100 | $156 | $168 | $133 | $171 | $176 | |||||

S&P SmallCap 600 | $100 | $141 | $149 | $147 | $144 | $163 | |||||

Morningstar Industrials Sector | $100 | $142 | $155 | $151 | $179 | $219 | |||||

11

ITEM 6 – Selected Financial Data

(In thousands, except shares and per share data)

Years Ended December 31 | 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||||||

Financial Results: | ||||||||||||||||||||||||

Net Sales | $ | 1,003,066 | $ | 808,572 | $ | 811,799 | $ | 821,983 | $ | 752,011 | ||||||||||||||

Cost of Sales | 598,645 | (1) | 456,977 | 462,739 | 469,556 | 426,103 | ||||||||||||||||||

Gross Margin - % | 40.3 | 43.5 | 43.0 | 42.9 | 43.3 | |||||||||||||||||||

Research and Development Expense | 32,013 | 34,738 | 32,415 | 29,432 | 30,529 | |||||||||||||||||||

% of Net Sales | 3.2 | 4.3 | 4.0 | 3.6 | 4.1 | |||||||||||||||||||

Selling and Administrative Expense | 345,364 | (1) | 248,210 | 252,270 | (2) | 250,898 | 232,976 | (3) | ||||||||||||||||

% of Net Sales | 34.4 | 30.7 | 31.1 | 30.5 | 31.0 | |||||||||||||||||||

Profit from Operations | 27,044 | (1) | 68,498 | 53,176 | (2) | 72,097 | 62,403 | (3) | ||||||||||||||||

% of Net Sales | 2.7 | 8.5 | 6.6 | 8.8 | 8.3 | |||||||||||||||||||

Income Tax Expense | 4,913 | (1) | 19,877 | 18,336 | (2) | 18,887 | 19,647 | (3) | ||||||||||||||||

Effective Tax Rate - % | (380.2 | ) | 29.9 | 36.4 | 27.2 | 32.8 | ||||||||||||||||||

Net (Loss) Earnings Attributable to Tennant Company | (6,195 | ) | (1) | 46,614 | 32,088 | 50,651 | 40,231 | |||||||||||||||||

% of Net Sales | (0.6 | ) | 5.8 | 4.0 | 6.2 | 5.3 | ||||||||||||||||||

Per Share Data: | ||||||||||||||||||||||||

Basic Net (Loss) Earnings Attributable to Tennant Company | $ | (0.35 | ) | (1) | $ | 2.66 | $ | 1.78 | (2) | $ | 2.78 | $ | 2.20 | (3) | ||||||||||

Diluted Net (Loss) Earnings Attributable to Tennant Company | $ | (0.35 | ) | (1) | $ | 2.59 | $ | 1.74 | (2) | $ | 2.70 | $ | 2.14 | (3) | ||||||||||

Diluted Weighted Average Shares | 17,695,390 | 17,976,183 | 18,493,447 | 18,740,858 | 18,833,453 | |||||||||||||||||||

Cash Dividends | $ | 0.84 | $ | 0.81 | $ | 0.80 | $ | 0.78 | $ | 0.72 | ||||||||||||||

Financial Position: | ||||||||||||||||||||||||

Total Assets | $ | 993,977 | $ | 470,037 | $ | 432,295 | $ | 486,932 | $ | 456,306 | ||||||||||||||

Total Debt | 376,839 | 36,194 | 24,653 | 28,137 | 31,803 | |||||||||||||||||||

Total Tennant Company Shareholders’ Equity | 296,503 | 278,543 | 252,207 | 280,651 | 263,846 | |||||||||||||||||||

Current Ratio | 1.8 | 2.2 | 2.2 | 2.4 | 2.4 | |||||||||||||||||||

Debt-to-Capital Ratio | 56.0 | % | 11.5 | % | 8.9 | % | 9.1 | % | 10.8 | % | ||||||||||||||

Cash Flows: | ||||||||||||||||||||||||

Net Cash Provided by Operations | $ | 54,174 | $ | 57,878 | $ | 45,232 | $ | 59,362 | $ | 59,814 | ||||||||||||||

Capital Expenditures, Net of Disposals | (17,926 | ) | (25,911 | ) | (24,444 | ) | (19,292 | ) | (14,655 | ) | ||||||||||||||

Free Cash Flow | 36,248 | 31,967 | 20,788 | 40,070 | 45,159 | |||||||||||||||||||

Other Data: | ||||||||||||||||||||||||

Depreciation and Amortization | $ | 43,253 | $ | 18,300 | $ | 18,031 | $ | 20,063 | $ | 20,246 | ||||||||||||||

Number of employees at year-end | 4,297 | 3,236 | 3,164 | 3,164 | 3,087 | |||||||||||||||||||

The results of operations from our 2017 acquisition of the IPC Group have been included in the Selected Financial Data presented above since its acquisition date on April 6, 2017.

(1) | 2017 includes a fair value step-up adjustment to acquired inventory in cost of sales of $7,245 pre-tax ($5,237 after-tax, or $0.30 per diluted share), pre-tax acquisition costs, restructuring charges and a pension settlement charge in selling and administrative expense of $10,560, $10,519 and $6,373, respectively ($9,748, $7,559 and $4,020 after-tax, or $0.55, $0.43 and $0.23 per diluted share, respectively). 2017 also includes pre-tax acquisition-related financing costs and acquisition costs in total other expense, net of $7,378 and $814, respectively ($4,619 and $660 after-tax, or $0.26 and $0.04 per diluted share, respectively). In addition, 2017 net loss attributable to Tennant Company includes a $2,388 net income tax expense ($0.14 per diluted share) as a result of the impacts of the 2017 tax reform legislation. |

(2) | 2015 includes restructuring charges of $3,744 pre-tax ($3,095 after-tax or $0.17 per diluted share) and a non-cash impairment of long-lived assets of $11,199 pre-tax ($10,822 after-tax or $0.58 per diluted share). |

(3) | 2013 includes restructuring charges of $3,017 pre-tax ($2,938 after-tax or $0.15 per diluted share) and a tax benefit of $582 (or $0.03 per diluted share) related to the retroactive reinstatement of the 2012 U.S. Federal Research and Development ("R&D") Tax Credit. |

12

ITEM 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

Tennant Company is a world leader in designing, manufacturing and marketing solutions that empower customers to achieve quality cleaning performance, significantly reduce environmental impact and help create a cleaner, safer, healthier world. Tennant is committed to creating and commercializing breakthrough, sustainable cleaning innovations to enhance its broad suite of products, including: floor maintenance and outdoor cleaning equipment, detergent-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, specialty surface coatings and asset management solutions. Tennant products are used in many types of environments including: Retail establishments, distribution centers, factories and warehouses, public venues such as arenas and stadiums, office buildings, schools and universities, hospitals and clinics, parking lots and streets, and more. Customers include contract cleaners to whom organizations outsource facilities maintenance, as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

In April 2017, the Company completed its acquisition of the IPC Group business. IPC manufactures a complete range of commercial cleaning products including mechanized cleaning equipment, wet & dry vacuum cleaners, cleaning tools & carts and high pressure washers. These products are sold into similar vertical market applications as those listed above, but also into office cleaning and hospitality vertical markets through a global direct sales and service organization and network of distributors. IPC markets products and services under the following valued brands: IPC, Gansow, Vaclensa, Portotecnica, Soteco and private-label brands.

Historical Results

The following table compares the historical results of operations for the years ended December 31, 2017, 2016 and 2015 in dollars and as a percentage of Net Sales (in thousands, except per share amounts and percentages):

2017 | % | 2016 | % | 2015 | % | |||||||||||||||

Net Sales | $ | 1,003,066 | 100.0 | $ | 808,572 | 100.0 | $ | 811,799 | 100.0 | |||||||||||

Cost of Sales | 598,645 | 59.7 | 456,977 | 56.5 | 462,739 | 57.0 | ||||||||||||||

Gross Profit | 404,421 | 40.3 | 351,595 | 43.5 | 349,060 | 43.0 | ||||||||||||||

Operating Expense: | ||||||||||||||||||||

Research and Development Expense | 32,013 | 3.2 | 34,738 | 4.3 | 32,415 | 4.0 | ||||||||||||||

Selling and Administrative Expense | 345,364 | 34.4 | 248,210 | 30.7 | 252,270 | 31.1 | ||||||||||||||

Impairment of Long-Lived Assets | — | — | — | — | 11,199 | 1.4 | ||||||||||||||

Loss on Sale of Business | — | — | 149 | — | — | — | ||||||||||||||

Total Operating Expense | 377,377 | 37.6 | 283,097 | 35.0 | 295,884 | 36.4 | ||||||||||||||

Profit from Operations | 27,044 | 2.7 | 68,498 | 8.5 | 53,176 | 6.6 | ||||||||||||||

Other Income (Expense): | ||||||||||||||||||||

Interest Income | 2,405 | 0.2 | 330 | — | 172 | — | ||||||||||||||

Interest Expense | (25,394 | ) | (2.5 | ) | (1,279 | ) | (0.2 | ) | (1,313 | ) | (0.2 | ) | ||||||||

Net Foreign Currency Transaction Losses | (3,387 | ) | (0.3 | ) | (392 | ) | — | (954 | ) | (0.1 | ) | |||||||||

Other Expense, Net | (1,960 | ) | (0.2 | ) | (666 | ) | (0.1 | ) | (657 | ) | (0.1 | ) | ||||||||

Total Other Expense, Net | (28,336 | ) | (2.8 | ) | (2,007 | ) | (0.2 | ) | (2,752 | ) | (0.3 | ) | ||||||||

(Loss) Profit Before Income Taxes | (1,292 | ) | (0.1 | ) | 66,491 | 8.2 | 50,424 | 6.2 | ||||||||||||

Income Tax Expense | 4,913 | 0.5 | 19,877 | 2.5 | 18,336 | 2.3 | ||||||||||||||

Net (Loss) Earnings Including Noncontrolling Interest | (6,205 | ) | (0.6 | ) | 46,614 | 5.8 | 32,088 | 4.0 | ||||||||||||

Net Loss Attributable to Noncontrolling Interest | (10 | ) | — | — | — | — | — | |||||||||||||

Net (Loss) Earnings Attributable to Tennant Company | $ | (6,195 | ) | (0.6 | ) | $ | 46,614 | 5.8 | $ | 32,088 | 4.0 | |||||||||

Net (Loss) Earnings Attributable to Tennant Company per Share | $ | (0.35 | ) | $ | 2.59 | $ | 1.74 | |||||||||||||

13

Net Sales

Net Sales in 2017 totaled $1,003.1 million, a 24.1% increase as compared to Net Sales of $808.6 million in 2016.

The components of the consolidated Net Sales change for 2017 as compared to 2016, and 2016 as compared to 2015, were as follows:

Growth Elements | 2017 v. 2016 | 2016 v. 2015 | |

Organic Growth: | |||

Volume | (0.1%) | 1.1% | |

Price | 1.5% | —% | |

Organic Growth | 1.4% | 1.1% | |

Foreign Currency | 0.5% | (1.0%) | |

Acquisitions | 22.2% | (0.5%) | |

Total | 24.1% | (0.4%) | |

The 24.1% increase in consolidated Net Sales for 2017 as compared to 2016 was driven by:

• | 22.2% from the April 2017 acquisition of the IPC Group and the expansion of our commercial floor coatings business through the August 2016 acquisition of the Florock® brand. |

• | An organic sales increase of approximately 1.4% which excludes the effects of foreign currency exchange and acquisitions, due to an approximate 1.5% price increase, partially offset by a volume decrease of 0.1%. The price increase was the result of selling price increases, typically in the range of 2% to 4% in most geographies, with an effective date of February 1, 2017. The impact to gross margin was minimal as these selling price increases were taken to offset inflation. The slight volume decrease was primarily due to increased sales in Latin America and EMEA being more than offset by volume decreases in North America. Sales of new products introduced within the past three years totaled 48% of equipment revenue in 2017. This compares to 37% of equipment revenue in 2016 from sales of new products introduced within the past three years. |

• | A favorable impact from foreign currency exchange of approximately 0.5%. |

The 0.4% decrease in consolidated Net Sales for 2016 as compared to 2015 was primarily due to the following:

• | An unfavorable impact from foreign currency exchange of approximately 1.0%. |

• | An unfavorable net impact of 0.5% resulting from the sale of our Green Machines outdoor city cleaning line, partially offset by the acquisition of the Florock brand. |

• | An organic sales increase of approximately 1.1% which excludes the effects of foreign currency exchange and acquisitions and divestitures, due to an approximate 1.1% volume increase. The volume increase was primarily due to strong sales of industrial equipment and sales of new products, particularly in the Americas region, being somewhat offset by lower sales of commercial equipment, particularly within the APAC region. Sales of new products introduced within the past three years totaled 37% of equipment revenue in 2016. This compares to 26% of equipment revenue in 2015 from sales of new products introduced within the past three years. There was essentially no price increase in 2016 due to no significant new selling list price increases since prior year selling list price increases with an effective date of February 1, 2015. |

The following table sets forth annual Net Sales by geographic area and the related percentage change from the prior year (in thousands, except percentages):

2017 | % | 2016 | % | 2015 | |||||||||||||

Americas | $ | 640,274 | 5.5 | $ | 607,026 | 2.6 | $ | 591,405 | |||||||||

Europe, Middle East and Africa | 273,738 | 112.1 | 129,046 | (7.7 | ) | 139,834 | |||||||||||

Asia Pacific | 89,054 | 22.8 | 72,500 | (10.0 | ) | 80,560 | |||||||||||

Total | $ | 1,003,066 | 24.1 | $ | 808,572 | (0.4 | ) | $ | 811,799 | ||||||||

Americas – In 2017, Americas Net Sales increased 5.5% to $640.3 million as compared with $607.0 million in 2016. The direct impact of the IPC Group and Florock acquisitions favorably impacted Net Sales by approximately 4.4%. In addition, a favorable direct impact of foreign currency translation exchange effects within the Americas impacted Net Sales by approximately 0.4% in 2017. As a result, organic sales growth in the Americas favorably impacted Net Sales by approximately 0.7% due to strong sales performance in Latin America, particularly Brazil and Mexico, from focused go-to-market strategies in our direct channel. This was partially offset by lower sales in North America, where sales growth through the distribution channel were more than offset by service sales.

In 2016, Americas Net Sales increased 2.6% to $607.0 million as compared with $591.4 million in 2015. The primary drivers of the increase in Net Sales were strong sales of industrial equipment, sales of new products and robust sales in Latin America. The direct impact of the Florock acquisition favorably impacted Net Sales by approximately 0.7%. An unfavorable direct impact of foreign currency translation exchange effects within the Americas impacted Net Sales by approximately 0.5% in 2016. As a result, organic sales increased approximately 2.4% in 2016 within the Americas.

Europe, Middle East and Africa – EMEA Net Sales in 2017 increased 112.1% to $273.7 million as compared to 2016 Net Sales of $129.0 million. In 2017, the direct impact of the IPC Group acquisition favorably impacted Net Sales by approximately 105.3%. In addition, a favorable direct impact of foreign currency translation exchange effects within EMEA impacted Net Sales by approximately 1.3% in 2017. As a result, organic sales growth in EMEA favorably impacted Net Sales in 2017 by approximately 5.5% due to strong sales growth in most European countries from strong demand in both the direct and distributor channels being partially offset by lower sales in the UK.

EMEA Net Sales in 2016 decreased 7.7% to $129.0 million as compared to 2015 Net Sales of $139.8 million. In 2016, organic sales growth was achieved in all regions except the UK and the Central Eastern Europe, Middle East and Africa markets primarily due to Brexit and challenging economic conditions, respectively. In 2016, there was an unfavorable impact on Net Sales of approximately 5.9% as a result of the sale of our Green Machines outdoor city cleaning line in January 2016. In addition, the direct impact of foreign currency exchange effects within EMEA unfavorably impacted Net Sales by approximately 2.0% in 2016. As a result, organic sales increased approximately 0.2% in 2016 within EMEA.

Asia Pacific – APAC Net Sales in 2017 increased 22.8% to $89.1 million as compared to 2016 Net Sales of $72.5 million. In 2017, the direct impact of the IPC Group acquisition favorably impacted Net Sales by approximately 22.7%. In addition, a favorable direct impact of foreign currency translation exchange effects within APAC impacted Net Sales by approximately 0.1% in 2017. As a result, organic sales growth in APAC was essentially flat due to sales growth in China from strong sales through the direct and distributor channels being offset by sales declines primarily in Korea and Singapore resulting from a challenging economic environment.

14

APAC Net Sales in 2016 decreased 10.0% to $72.5 million as compared to 2015 Net Sales of $80.6 million. Organic sales decreased approximately 10.0% in 2016 with lower sales of commercial and industrial equipment. Organic sales declines in all of our Asian markets were primarily due to economic slowdowns in the region and fewer large deals. Direct foreign currency translation exchange effects had essentially no impact on Net Sales in 2016 within APAC.

Gross Profit

Gross Profit margin was 320 basis points lower in 2017 compared to 2016 due primarily to the $7.2 million, or approximately 70 basis points, fair value inventory step-up flow through related to our acquisition of the IPC Group and field service productivity challenges related to a high number of open service trucks of $5.1 million, or approximately 50 basis points. In addition, Gross Profit margin was unfavorably impacted by mix of sales by channel and region, primarily resulting from higher sales through the distribution in North America and lower gross margins from the IPC Group. The near-term unfavorable impacts from investments in manufacturing automation initiatives and high levels of raw material cost inflation also contributed to lower Gross Profit margin in 2017.

Gross Profit margin was 43.5% in 2016, an increase of 50 basis points as compared to 2015. Gross Profit margin in 2016 was favorably impacted by product mix (with relatively higher sales of industrial equipment and lower sales of commercial equipment), partially offset by manufacturing productivity challenges in North America.

Operating Expenses

Research and Development Expense – Tennant continues to invest in innovative product development with 3.2% of 2017 Net Sales spent on Research and Development ("R&D"). We continue to invest in developing innovative new products and technologies and the advancement of detergent-free products, fleet management and other sustainable technologies. There were 32 new products and product variants launched in 2017 including a new family of T500 commercial walk-behind scrubbers, the enhanced IRIS® Web Based Fleet Management System, the i-mop, the V3e compact dry canister vacuum, the T350 stand-on commercial scrubber and the A140 micro-scrubber. In 2017, our newly acquired IPC Group business also launched many new products and product variants across all product lines.

R&D Expense decreased $2.7 million, or 7.8%, in 2017 as compared to 2016. As a percentage of Net Sales, 2017 R&D Expense decreased 110 basis points compared to the prior year. The decrease in R&D spending was primarily due to headcount reduction related to the first quarter 2017 restructuring action.

R&D Expense increased $2.3 million, or 7.2%, in 2016 as compared to 2015. As a percentage of Net Sales, 2016 R&D Expense increased 30 basis points compared to the prior year. New products are a key driver of sales growth. There were 10 new products and product variants launched in 2016 including three models of emerging market floor machines, two models of the M17 battery-powered sweeper-scrubber, three large next-generation cleaning machines: the M20 and M30 integrated sweeper-scrubbers, and the T20 heavy-duty industrial rider scrubber, and two models of the commercial dryer/air mover.

Selling and Administrative Expense – Selling and Administrative Expense ("S&A Expense") increased by $97.2 million, or 39.1%, in 2017 compared to 2016. As a percentage of Net Sales, 2017 S&A Expense increased 370 basis points to 34.4% from 30.7% in 2016. S&A Expense was unfavorably impacted by $15.7 million, or 160 basis points, and $10.6 million, or 110 basis points, of amortization expense and acquisition costs, respectively, related to our acquisition of the IPC Group. In addition, S&A Expense was unfavorably impacted by $10.5 million, or 100 basis points, and $6.4 million, or 60 basis points, of restructuring charges taken in the 2017 first and fourth quarters and pension settlement charges, respectively. Excluding these costs, S&A Expense was 50 basis points lower in 2017 compared to 2016 due primarily to our continued balance of disciplined spending control with investments in key growth initiatives.

S&A Expense decreased by $4.1 million, or 1.6%, in 2016 compared to 2015. As a percentage of Net Sales, 2016 S&A Expense decreased 40 basis points to 30.7% from 31.1% in 2015 due to two restructuring charges totaling $3.7 million we recorded in 2015 to reduce our infrastructure costs that did not repeat in 2016. In addition, there was a net favorable impact to S&A Expense in 2016 as a result of disciplined spending control more than offsetting investments in key growth initiatives.

Profit from Operations

Operating Profit was $27.0 million, or 2.7% of Net Sales, in 2017, as compared to Operating Profit of $68.5 million, or 8.5% of Net Sales, in 2016. 2017 Operating Profit was $41.5 million lower than 2016 Operating Profit due primarily to $15.7 million of amortization expense related to IPC intangible assets, $10.6 million of acquisition costs and a $7.2 million fair value inventory step-up flow through, all related to our acquisition of the IPC Group. We also recorded $10.5 million of restructuring charges in 2017 to better align our global resources and expense structure. In addition, we recorded pension settlement charges of $6.4 million due to our termination of the U.S. Pension Plan in May 2017. These unfavorable impacts were partially offset by operating profit obtained from the IPC acquisition, reduced expenses resulting from our first quarter 2017 restructuring charge and tight management of controllable costs.

Operating Profit was $68.5 million in 2016, as compared to Operating Profit of $53.2 million in the prior year which included $11.2 million for the pre-tax non-cash Impairment of Long-Lived Assets as a result of the classification of our Green Machines assets as held for sale and also the $3.7 million pre-tax restructuring charges recorded in 2015. Operating Profit margin increased 190 basis points to 8.5% in 2016 from 6.6% in 2015. 2016 Operating Profit was also favorably impacted by higher Gross Profit despite the lower Net Sales in 2016 as compared to 2015. Due to the overall strengthening of the U.S. dollar relative to other currencies in 2016, foreign currency exchange reduced Operating Profit by approximately $1.2 million.

Total Other Expense, Net

Interest Income – Interest Income was $2.4 million in 2017, an increase of $2.1 million from 2016. The increase between 2017 and 2016 was primarily due to interest income related to foreign currency swap activities.

Interest Income was $0.3 in 2016, an increase of $0.1 million from 2015. The increase between 2016 and 2015 was due to higher levels of cash deposits.

Interest Expense – Interest Expense was $25.4 million in 2017, as compared to $1.3 million in 2016. The higher Interest Expense in 2017 was primarily due to carrying a higher level of debt on our Consolidated Balance Sheets related to our acquisition activities as well as a $6.2 million charge to expense the debt issuance costs for loans which were refinanced or repaid, as further described in the Liquidity and Capital Resources section that follows.

There was no significant change in Interest Expense in 2016 as compared to 2015.

15

Net Foreign Currency Transaction Losses – Net Foreign Currency Transaction Losses were $3.4 million in 2017 as compared to $0.4 million in 2016. The unfavorable change in the impact from foreign currency transactions in 2017 was primarily due to fluctuations in foreign currency rates, specifically between the Euro and U.S. dollar, settlements of transactional hedging activity in the normal course of business and a $1.1 million mark-to-market adjustment of a foreign exchange call option, an instrument held in connection with our acquisition of the IPC Group on April 6, 2017.

Net Foreign Currency Transaction Losses were $0.4 million in 2016 as compared to $1.0 million in 2015. The favorable change in the impact from foreign currency transactions in 2016 was due to fluctuations in foreign currency rates and settlements of transactional hedging activity in the normal course of business.

Other Expense, Net – Other Expense, Net was $2.0 million in 2017 as compared to $0.7 million in 2016. The unfavorable change in Other Expense, Net was due primarily to the additional expense recorded as a result of the acquisition of the IPC Group.

There was no significant change in Other Expense, Net in 2016 as compared to 2015.

(Loss) Profit Before Income Taxes

Loss Before Income Taxes for 2017 was $1.3 million compared to Profit Before Income Taxes of $66.5 million for 2016 and $50.4 million in 2015.

The breakdown of (Loss) Profit Before Income Taxes between U.S. and foreign operations for each year ended December 31 was as follows:

2017 | % | 2016 | % | 2015 | % | ||||||||

U.S. operations | $ | 7,465 | (577.8) | $ | 54,018 | 81.2 | $ | 51,189 | 101.5 | ||||

Foreign operations | (8,757 | ) | 677.8 | 12,473 | 18.8 | (765 | ) | (1.5 | ) | ||||

Total | $ | (1,292 | ) | 100.0 | $ | 66,491 | 100.0 | $ | 50,424 | 100.0 | |||

Profit Before Income Taxes from U.S. operations decreased by $46.6 million in 2017 compared to 2016. The decrease resulted primarily from $10.6 million of acquisition costs related to our acquisition of the IPC Group, $6.4 million of pension settlement charges recorded in 2017 as a result of the termination of the U.S. Pension Plan in May 2017 and $4.9 million of restructuring charges recorded in 2017 to better align our global resources and expense structure. In addition, Interest Expense recorded in Profit Before Income Taxes from U.S. operations during 2017 was $23.4 higher compared to 2016 primarily due to carrying a higher level of debt on our Consolidated Balance Sheets related to our acquisition activities as well as a $6.2 million charge to expense the debt issuance costs for loans which were refinanced or repaid as part of our acquisition of the IPC Group.

(Loss) Profit Before Income Taxes from foreign operations decreased by $21.2 million in 2017 compared to 2016. The decrease resulted primarily from $15.7 million of amortization expense related to IPC intangible assets in 2017, a $7.2 million fair value inventory step-up flow through as a result of our acquisition of the IPC Group and $5.6 million of restructuring charges recorded in 2017 to better align our global resources and expense structure. These unfavorable impacts were partially offset by Profit Before Income Taxes obtained from the IPC acquisition.