Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - STEWART INFORMATION SERVICES CORP | v378438_8k.htm |

Summer 2014 Investor Presentation Stewart Information Services Corporation

2 Forward - looking Statements Certain statements in this news release are "forward - looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 . Such forward - looking statements relate to future, not past, events and often address our expected future business and financial performance . These statements often contain words such as "expect," "anticipate," "intend," "plan," "believe," "seek," "will," "foresee" or other similar words . Forward - looking statements by their nature are subject to various risks and uncertainties that could cause our actual results to be materially different than those expressed in the forward - looking statements . These risks and uncertainties include, among other things, the tenuous economic conditions ; adverse changes in the level of real estate activity ; changes in mortgage interest rates, existing and new home sales, and availability of mortgage financing ; our ability to respond to and implement technology changes, including the completion of the implementation of our enterprise systems ; the impact of unanticipated title losses on the need to strengthen our policy loss reserves ; any effect of title losses on our cash flows and financial condition ; the impact of vetting our agency operations for quality and profitability ; changes to the participants in the secondary mortgage market and the rate of refinancings that affect the demand for title insurance products ; regulatory non - compliance, fraud or defalcations by our title insurance agencies or employees ; our ability to timely and cost - effectively respond to significant industry changes and introduce new products and services ; the outcome of pending litigation ; the impact of changes in governmental and insurance regulations, including any future reductions in the pricing of title insurance products and services ; our dependence on our operating subsidiaries as a source of cash flow ; the continued realization of expense savings from our continual focus on aligning our operations to quickly adapt our costs to transaction volumes and market conditions ; our ability to access the equity and debt financing markets when and if needed ; our ability to grow our international operations ; and our ability to respond to the actions of our competitors . These risks and uncertainties, as well as others, are discussed in more detail in our documents filed with the Securities and Exchange Commission, including our Annual Report on Form 10 - K for the year ended December 31 , 2013 , our quarterly reports on Form 10 - Q, and our Current Reports on Form 8 - K . We expressly disclaim any obligation to update any forward - looking statements contained in this news release to reflect events or circumstances that may arise after the date hereof, except as may be required by applicable law .

3 Non - GAAP Disclosures This presentation may contain certain financial measures that are not presented in accordance with generally accepted accounting principles (GAAP), including but not limited to, losses and litigation expenses arising from non - predictable title losses and adjusted pretax title margin, which is adjusted to exclude net realized investment gains or losses and reserve adjustments . Although these exclusions represent actual gains, losses or expenses to the Company, they may mask the periodic income and financial and operating trends associated with the Company’s business . The Company is presenting these non - GAAP financial measures because they provide the Company’s management and investors with additional insight into the operational performance of the Company relative to earlier periods and relative to the Company’s competitors . The Company does not intend for these non - GAAP financial measures to be a substitute for any GAAP financial information . In this presentation these non - GAAP financial measures have been presented with, and reconciled to, the most directly comparable GAAP financial measures . Investors should use these non - GAAP financial measures only in conjunction with the comparable GAAP financial measures .

4 Investment Highlights • Trusted provider in $12+ billion domestic industry • Well positioned to capitalize on the ongoing real estate recovery and heightened regulatory environment • Corporate strategy to grow revenue, reduce fixed costs and enhance margins • Continued diversification into complementary real estate services with counter and non - cyclical components • Title losses returning to historical average loss ratios • Increasing premium rates, improving remittance percentages and diversified revenue sources bolster profitability going forward

5 First Quarter 2014 & Full Year 2013 Highlights • Pretax loss of $18.6 million in 1Q14 and pretax gain of $101.1 million in full year 2013. • Net loss attributable to Stewart of $12.1 million in 1Q14 ( - $0.54 per share) and net earnings attributable to Stewart of $63.0 million in 2013 ($2.60 per share). Of note, 2013 benefited from the release of a deferred tax asset valuation allowance of $10.3 million ($0.42 per share). • Operating revenues decreased $35.9 million ( - 8.5%) in 1Q14 from the same quarter in 2013. Operating revenues increased $17.6 million for the full year 2013 (+1.3%). • Title revenues were down $23.9 million ( - 6.2%) in 1Q14 from the same quarter in 2013. Title revenues increased $65.5 million (+3.8%) in 2013.

6 Income Statement (non - GAAP, in $000 except per share) 2014 2013 % Change 2013 2012 % Change Revenues Direct 149,689 159,646 -6.2% 750,031 723,539 3.7% Agency 213,673 227,662 -6.1% 1,046,378 1,007,380 3.9% Total Title Revenue 363,362 387,308 -6.2% 1,796,409 1,730,919 3.8% Mortgage Services 24,078 36,069 -33.2% 117,145 158,107 -25.9% Total Operating Revenues 387,440 423,377 -8.5% 1,913,554 1,889,026 1.3% Investment Income/Other Gains 3,998 336 1089.9% 14,426 21,386 -32.5% Total Revenues 391,438 423,713 -7.6% 1,927,980 1,910,412 0.9% Agency Retention (174,679) (187,065) -6.6% (848,437) (829,070) 2.3% Net Revenues 216,759 236,648 -8.4% 1,079,543 1,081,342 -0.2% Expenses Employee Costs 139,784 136,830 2.2% 571,026 542,461 5.3% Other Operating Expenses 67,737 63,796 6.2% 280,259 286,496 -2.2% Title Losses 22,767 23,563 -3.4% 106,318 140,030 -24.1% Depreciation 4,395 4,358 0.8% 17,920 17,783 0.8% Interest Expense 662 954 -30.6% 2,956 5,235 -43.5% Total Expenses 235,344 229,501 2.5% 978,479 992,005 -1.4% Earnings Earnings Before Taxes and Noncontrolling Interests (18,585) 7,147 101,065 89,339 Income Tax 7,958 (2,389) (28,481) 29,639 Noncontrolling Interests (1,478) (1,551) (9,558) (9,795) Net Income (Loss) (12,106) 3,206 63,026 109,183 Net Margin -3.1% 0.8% 3.3% 5.7% Per Share Net Income (Loss) Per Share - Diluted (0.54) 0.15 2.60 4.61 Net Income (Loss) Per Share - Basic (0.54) 0.15 2.85 5.66 Three Months Ended March Full Year

7 Balance Sheet (in $000, except per share) March December 2014 2013 Assets Cash & Cash Equivalents 120,342 194,289 Statutory Reserve Funds 454,206 450,564 Investments - Short Term 34,719 38,335 Investments - Other 114,028 96,671 Other Assets 309,189 301,312 Goodwill & Intangibles 244,135 244,888 Total Assets 1,276,619 1,326,059 Liabilities Notes Payable 4,315 5,827 Convertible Senior Notes 27,141 27,119 Loss Reserves 495,250 506,888 Other Liabilities 97,363 123,135 Total Liabilities 624,069 662,970 Equity Total Shareholders' Equity 652,550 663,089 Total Liabilities and Shareholders' Equity Total Liabilities and Shareholders' Equity 1,276,619 1,326,059 Other Return on Equity, TTM* 7.3% 9.5% Debt-to-Equity 4.6% 4.7% Book Value/Share 28.98 29.47 Tangible Book Value/Share 18.14 18.59 * ROE for periods above include effect of non-recurring tax benefit of $10.3 million in 4Q 2013. Debt levels will be managed so as not to exceed rating agency guidelines of maximum debt-to-tangible capital of 30%.

8 Summary Cash Flow Statement (in $000) March March December December 2014 2013 2013 2012 Cash Flow Net Cash (Used) Provided by Operations (50,189) (3,390) 87,187 120,522 Capex (4,283) (4,259) (17,282) (16,752) Proceeds (purchases) of investments, net (13,215) (21,024) (55,975) (25,752) Decreases (increases) in notes receivable - - (1,002) (463) Collections on notes receivable - 86 2,666 959 Changes due to the sale and deconsolidation of subsidiaries - 101 - 1,566 Proceeds from the sale of land, buildings, and equipment 281 81 2,168 4,713 Cash paid to purchase interest in subsidiaries - (296) (14,921) (1,183) Net proceeds from the sale of equity investees - - 3,090 - Cash received (paid) for cost basis investments and other assets 24 72 2,894 384 Notes payable, net (1,512) (55) (1,053) (5,242) Purchase of remaining interest of consolidated subsidiaries - (723) (5,051) (1,621) Cash payments for settlement of convertible debt - (742) (742) - Distributions to minority shareholders (1,478) (2,226) (9,239) (9,512) Effects of changes in foreign currency exchange rates (3,575) (787) (4,877) 1,821 All other, net - - (2,111) (1,745) Net Increase (Decrease) in Cash and Cash Equivalents (73,947) (33,162) (14,248) 67,695 Three Months Full Year

9 Title Insurance Residential • Provides independent, third - party closing and settlement services while acting as a trusted advisor to parties in the real estate transaction • Searching, examining and insuring the condition of the title to real property, thereby providing security of ownership to homeowners • Agency operations through roughly 3,000 independent issuing agencies Commercial • Significant presence of commercial expertise in major markets poised for future growth • Strong underwriting expertise and service is extremely valuable in complex commercial transactions • Growing commercial market offers cyclical diversity from residential real estate trends • Fitch upgraded Stewart ’ s Insurer Financial Strength (IFS) rating to A - from BBB+ (Outlook Stable) in August 2013 International • #1 market share in Canadian markets served and presence in the U.K., Continental Europe, Australia, Latin America, Mexico, and the Caribbean – Stewart had international revenues of $100.6 million in 2013 and $22.0 million in 1Q14 • Global footprint enables single point of contact for international commercial markets -- Stewart had $2.2 million in international commercial revenues in 1Q14 and $10.4 million in 2013

10 Mortgage Services Business Lines • Mortgage origination services include post - closing management, loan review, valuation and due diligence • Component servicing business includes call center services, loss mitigation support, short sale and deed - in - lieu services as well as transfer support and servicing file review • Default support services include foreclosure file review, foreclosure audits, REO asset management and REO rental management • Real estate technology includes title production systems, web - based title search tools to facilitate the examination process and eRecording technology for county courthouses Strategy – Reposition for More Sustainable Results • Expand product and services set within the origination and servicing support marketplace to include services such as loan due diligence, quality control, settlement services, compliance solutions, collateral valuation, and centralized title -- Stewart has recently purchased DataQuick Title, LandSafe and Wetzel Trott and acquired the assets of Allonhill and DataQuick Appraisal • Diversify customer base and expand services provided to existing customers • Capitalize on our expertise in providing high quality, tailored, on - demand outsourcing • Effectively manage the default - related business lines as market volumes decline Long - term Target • Corporate goal of achieving 25% of revenue – net of agent retention – from mortgage services

11 Revenues and Pre - tax Earnings Trends $ Millions Pre - tax Earnings Revenue ($1,500) ($1,000) ($500) $0 $500 $1,000 $1,500 $2,000 $2,500 2006 2007 2008 2009 2010 2011 2012 2013 $(300) $(200) $(100) $- $100 $200 $300 $400 $500

12 Stewart Operating Revenues Trailing Twelve Months - $ Millions $0 $500 $1,000 $1,500 $2,000 $2,500 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Direct Title Agency Title Mortgage Services

13 Direct Title Revenues and Orders Trailing Twelve Months - $ Millions Direct Title Revenue Orders Opened Orders Closed $500 $600 $700 $800 $900 $1,000 $1,100 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 200,000 400,000 600,000 800,000 1,000,000 Orders Revenue

14 Independent Agency Network • Focus is on quality and profitability over market share growth to reduce risk and consistently improve operational performance. • Leading the industry in assisting independent agencies prepare for Consumer Financial Protection Bureau (CFPB) compliance and enabling them to meet the changing market and regulatory requirements for settlement services providers. • Average annual remittance per agency continues to increase while the key profitability driver, the policy loss ratio, continues to decrease. • Emphasis on capturing a higher percentage of business from current agencies and signing new high - quality agencies in states with conditions favorable to increasing profitability. • Our disciplined approach is achieving the desired results in this important market segment.

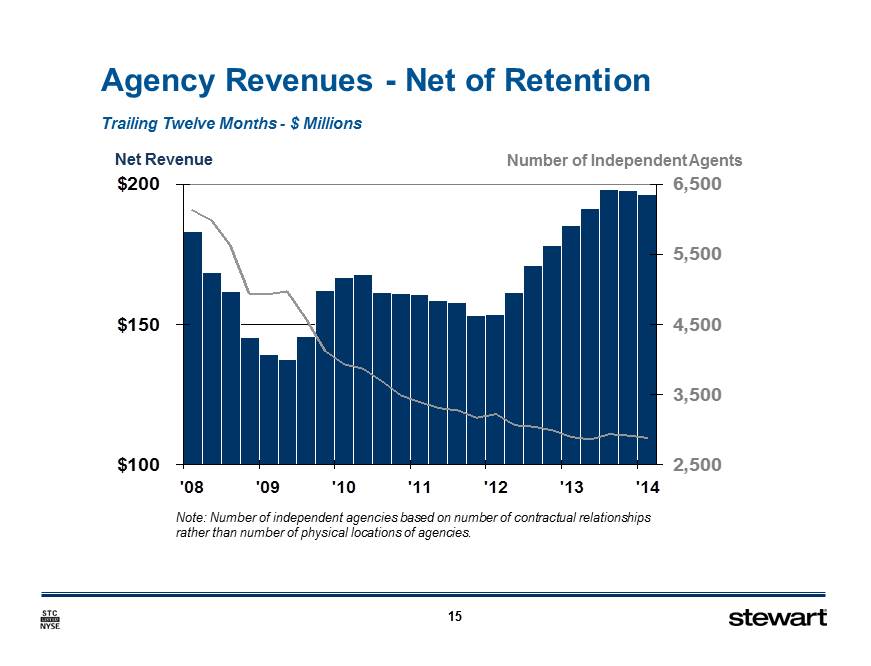

15 Agency Revenues - Net of Retention Number of Independent Agents Note: Number of independent agencies based on number of contractual relationships rather than number of physical locations of agencies. $100 $150 $200 '08 '09 '10 '11 '12 '13 '14 2,500 3,500 4,500 5,500 6,500 Trailing Twelve Months - $ Millions Net Revenue

16 Agency Retention Rates Differences in independent agency retention rates largely driven by geography Source: Form 9 filings for respective underwriters for year ended December 31, 2013. STC retention rates were used in the calculations because competitor rates are not included in SEC or statutory filings. STC FNF FAF Overall Retention Rate 81.2% 78.4% 79.7% Difference from STC -2.8% -1.5% Excluding Florida and California (using STC Retention Rates) 81.4% 83.9% 87.5% Difference from STC 2.5% 6.1%

17 Stewart Mortgage Services Revenues Trailing Twelve Months - $ Millions Note: Years prior to 2012 not restated for change in segment reporting effective with Q4 2012 reporting. Impact in any given year would not be material to revenues. $0 $20 $40 $60 $80 $100 $120 $140 $160 $180 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Focused Non - title Revenues and Profits As Mortgage Services transitions to a more sustainable revenue base, both segment revenues and profitability will likely remain depressed over the next several quarters.

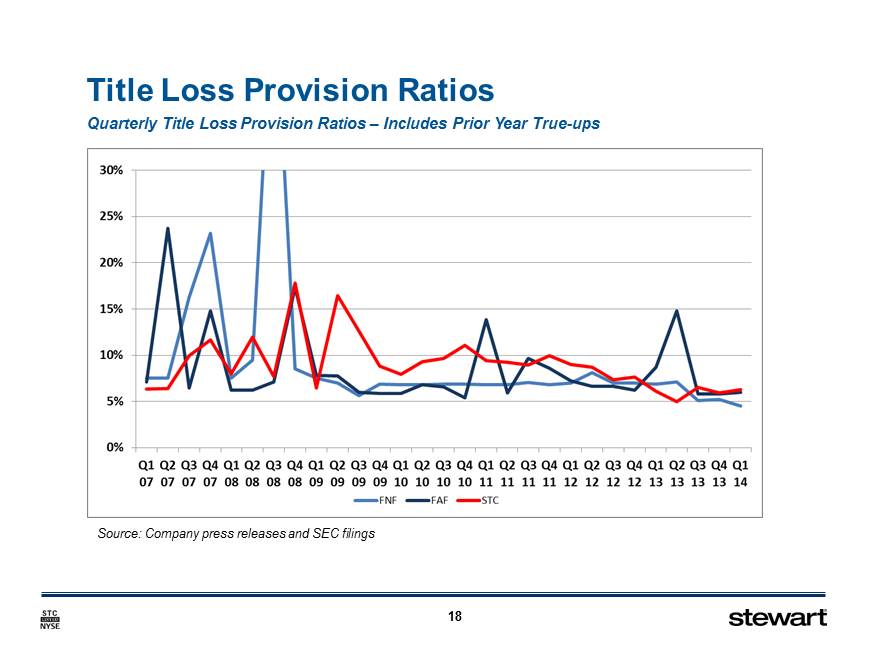

18 Title Loss Provision Ratios Quarterly Title Loss Provision Ratios – Includes Prior Year True - ups Source: Company press releases and SEC filings

19 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 Ultimate Loss Ratios by Policy Year Actuarial Claims as a % of Net Statutory Premiums Written – U.S. Operations Only Source: ALTA, Family - Company Aggregates Stewart First American Fidelity Claims Paid

20 Market Conditions Positives • Home prices continue to increase – a 5 percent rise in home prices increases revenue per transaction in the mid - 3 percent range • Commercial real estate market remaining solid • Interest rates remain at historically low levels • HARP extension to 2015 • Full benefit of 2013 state pricing increases seen in 2014 Concerns • Mortgage originations expected to fall in 2014 on a material decline in refinance volumes • Uncertain regulatory economic environment: Dodd - Frank, CFPB • J ob growth rates remain muted even as macro trends improve • Potential loss of mortgage interest deduction for homes and tax treatment of commercial real estate

21 0 1 2 3 4 5 6 7 8 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 U.S. Existing Housing Sales Seasonally Adjusted Annualized Rate – Millions $8,000 Tax Credit Normal Market Bubble Fannie Mae ® April 2014 National Association of REALTORS ® Last Normal Market in 2002

22 2014 Strategic Priorities • Lead the market in providing compliant, trusted and tailored real estate services in concert with changing regulatory environment • Expand commercial market share • Repositioning Mortgage Services to excel in a normalized real estate market • Expanding footprint of direct operations, primarily in western states • Continue rationalizing title production costs through standardization, automation, and centralization

23 CEO Matt Morris CFO Allen Berryman Nat Otis Ted Jones, PhD SVP, Financial Planning & Strategic Analysis Senior Vice President Director of Investor Relations Chief Economist nat.otis@stewart.com ted@stewart.com 713.625.8360 direct 713.625.8014 direct 800.729.1900, extension 8360 800.729.1900, extension 8014

Summer 2014 Investor Presentation Appendix Stewart Information Services Corporation

25 $0.0 $0.5 $1.0 $1.5 $2.0 $2.5 $3.0 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 $3 $5 $7 $9 $11 $13 $15 $17 Residential Lending Vs. Industry Premiums Forecast Fannie Mae ® April 2014 2011 - 2014 Lending Likely Understates Title Revenues Due to Cash Sales Double Normal Effective Lending – $ Trillions Statutory Title Premiums $ Billions Effective Lending = Purchase Lending + 60 Percent of Refinance Lending Data Sources : Lending = Fannie Mae ® , Title Premiums = CDS Research, Demotech and ALTA ®

26 Stewart Net Operating Revenues Trailing 12 Months - $ Millions $0 $250 $500 $750 $1,000 $1,250 $1,500 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Direct Title Agency Net of Retention Mortgage Services

27 Title Revenues by Regulatory Oversight Source: Form 9 filings (Schedule T) as compiled by ALTA

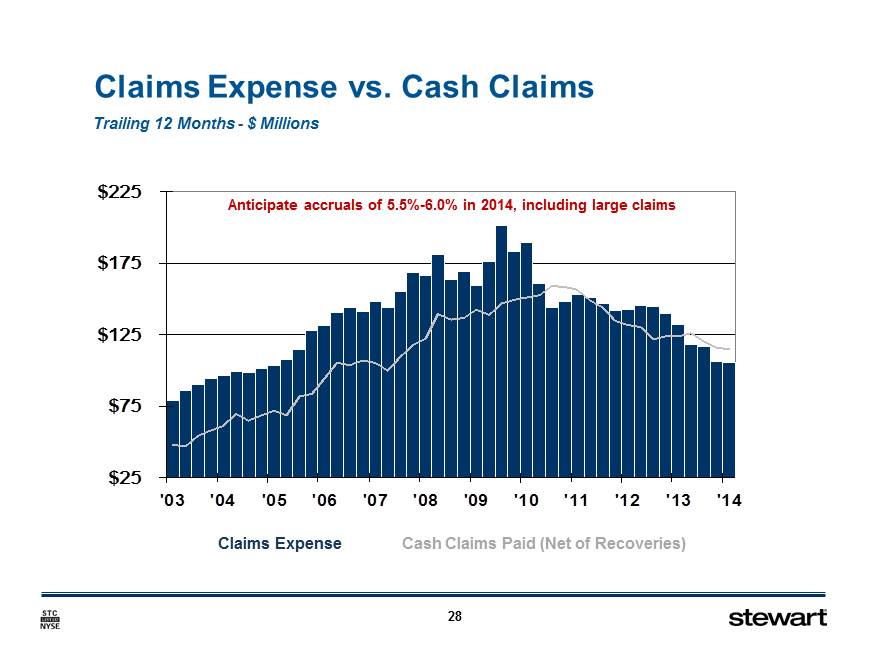

28 $25 $75 $125 $175 $225 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Claims Expense vs. Cash Claims Trailing 12 Months - $ Millions Anticipate accruals of 5.5% - 6.0% in 2014, including large claims Claims Expense Cash Claims Paid (Net of Recoveries)

29 Employee Expenses 20% 25% 30% 35% 40% '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 As a Percentage of Operating Revenues Trailing 12 Months

30 Other Operating Expenses 10% 13% 15% 18% 20% 23% 25% '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 As a Percentage of Operating Revenues Trailing 12 Months

31 Statutory Surplus and Operating Leverage Thousands Multiple

32 Debt - to - Capital and Debt - to - Equity

33 Book Value and Tangible Book Value Per Share

34 Mortgage Services – Products & Services Origination Servicing Capital Markets Centralized Title & Closing Collections Due Diligence Valuation Services Military Servicing Support Compliance Reviews Home Equity Title Solutions Default Title & REO Closing Securitization Support Home Equity Valuations Default Valuations Title Research & Curative Loan Quality Control REO Asset Management Portfolio Valuations Imaging/Data Capture Component Loss Mitigation Investor Oversight Call Center Services Imaging/Data Capture Consulting Services Customized Outsourcing Customized Outsourcing Servicing QC Consulting Services