Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - EXCO RESOURCES INC | d602781d8k.htm |

9/25/2013

KeyBanc 2013 DFW E&P Bus Tour

Exhibit 99.1

EXCO Resources, Inc. |

2

September Investor Presentation

Management Participants

Doug Miller

Chairman and CEO

Hal Hickey

President & COO

Mark Mulhern

CFO & EVP |

3

September Investor Presentation

Haynesville Shale: Operate ~400

horizontal wells

Eagle Ford Shale: Operate ~120

horizontal wells; developing within

partnership with KKR

Marcellus Shale: Operate ~110

horizontal wells

~650 employees

Conventional asset MLP structure

with Harbinger Group

25% equity ownership in LP and

50% interest in GP

1 rig operating in West Texas

EXCO operates ~150 Mmcfe/d

gross production

~110 employees

50% equity interest in midstream

gathering system in the core of the

Haynesville Shale

Currently flowing ~1.3 Bcf/d

~115 employees

EXCO Resources, Inc. Company Overview

Premier shale gas producer well positioned for future value creation

Renewed focus on opportunistic acquisition activity

–

Current acquisition economics remain cheaper to buy than to drill today

|

4

September Investor Presentation

Introduction

Solid year to date 2013 financial results

–

Resulting from discipline around capital deployment and cost management

Established foundation for additional future growth through Eagle

Ford and Haynesville acquisitions

Concentration of producing properties acquired will increase cash

flow

Partnerships with KKR, Harbinger and BG bolster our financial reach

Eagle Ford transaction allows EXCO to extend its proven operational

expertise |

5

September Investor Presentation

Strategic Focus

Grow EBITDA/Cash Flow of the company through successful

execution of recent acquisitions and evaluation of additional drilling

partnerships to minimize CAPEX and add production/revenue

Helps mitigate growth risks

Acquire

bankable

producing

properties

after

1

st

year

declines

Finance those acquisitions via net cash flows plus secured

(borrowing base) financing

Translate EBITDA growth into share price appreciation |

6

September Investor Presentation

Approximately 60% of purchase price allocated to proved developed wellbores

Significant cash flow from producing assets; trailing 12 month EBITDA of

approximately $165 million

Substantial proved assets provide cash flow for future development

Recent Acquisition Strategic Rationale

Eagle Ford: Farmout acreage

Eagle Ford: Potential to exploit additional horizons across play (Buda & Austin

Chalk) Eagle Ford: Operational efficiencies to be gained by shifting to

manufacturing development Haynesville: Bossier formation in DeSoto Parish;

operational efficiencies from existing EXCO infrastructure

Entry

into

Eagle

Ford

DIVERSIFIES

asset

base

Adds oil exposure with solid economic returns in the oil core area

120 producing wells reduces delineation risk

Extensive inventory of identified drilling locations

Significant PDP

Cash Flow

Eagle Ford

Acquisition

Upside Potential

Haynesville

Acquisition

FORTIFIES

LEADING

POSITION

in

the

core

DeSoto

Parish

Haynesville

area

and

adds

locations

Leverages our extensive experience and cost focused development program

Core area of EXCO’s operations; perfect bolt-on acquisition

Increases inventory of locations in key focus area |

7

September Investor Presentation

Financial Topics

Eagle Ford KKR Development Structure

2013 EBITDA and CAPEX Update

Liquidity Review |

8

September Investor Presentation

Eagle Ford KKR Development Structure

EXCO purchased 100% of the PDP assets in the Eagle Ford

The undeveloped Eagle Ford locations are drilled and developed under a development agreement

with entities advised by Kohlberg Kravis Roberts & Co. L.P. (“KKR”),

including KKR Financial Holdings LLC (NYSE: KFN)

KKR funded approximately $131 million of the initial land purchase price (represents 50%)

Joint development program on undeveloped assets, which EXCO assigns to KKR 50% of EXCO’s

working interest in undeveloped acreage, results in KKR funding 75% of the capital and

EXCO funding 25% Development plan is to drill approximately 300 wells over the next five

years; ~30 wells to be drilled by year end 2013

When wells have been drilled under the development agreement and

produced for one year, EXCO has the right

to offer to purchase KKR’s 75% working interest at fair market value

Borrowing Base collateral package limited to 25% interest in the

PUD locations (represents EXCO’s interest in the

undeveloped locations)

Structure provides EXCO with immediate capital for undeveloped land, development capital and a

stream of future producing buyout opportunities

KKR has notable experience in the Eagle Ford Shale

Early investors in Hilcorp’s Eagle Ford assets (sold to Marathon)

Ongoing development partnership with Comstock Resources

Through its affiliate, RPM Energy, KKR has technical capabilities providing engineering and

geology expertise |

9

September Investor Presentation

Eagle Ford KKR Development Structure

Key points

–

KKR drilling return is capped at 1.2x invested drilling capital

–

Cash

flow

in

1

st

year

gets

credited

at

buyout

(KKR

generates

vast

majority

of

their

return

from

1

st

year

production)

–

PV-10 is calculated but EXCO is not buying at PV-10; we are paying

1.2x (EXCO expects to pay less than PV-10) invested drilling capital

and sharing excess profits beyond that amount

–

Producing properties expected to generate expanded borrowing

base capacity. EXCO’s additional required Eagle Ford buyout capital

should be manageable. Amounts to be financed outside of secured

borrowing base are estimated at ~$280 million over four years or

~$70 million per year |

10

September Investor Presentation

Note:

CNOOC

has

a

1/3

working

interest

that

is

not

included

in

the

table

above

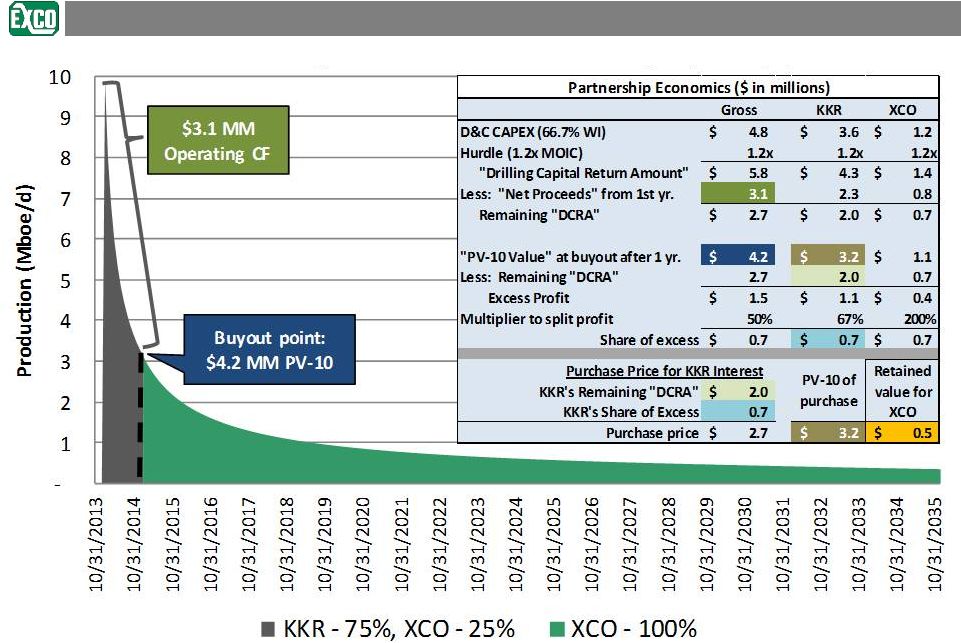

Quoted items are defined legal terms found in the KKR Participation Agreement filed with the

SEC Amounts in table may not foot due to rounding

Single Well Net Production Example (Mboe/d) |

11

September Investor Presentation

Total

Program

Illustrative

Example

–

300

wells

over

4

years

Capital to Drill

300 Eagle Ford Wells @ $7.2 million per well

$2.2 Billion total drilling

costs over 4 years of which

EXCO’s share is <20%

WI

Owner

WI

Share

Total

Capital

CNOOC

33.33%

$720

KKR

50%

1,080

EXCO

16.67%

360

$2,160

KKR Perspective –

Drilling

Fund Returns

KKR Invested Capital

$1,080

Return multiple

1.2X

$1,296

EXCO Invested Capital

$360

Return multiple

1.2X

$432

EXCO’s total Year 1 cash flows of $236

compares to its 16.67% share of capital

to drill ($360 million). EXCO’s share of

drilling capital will be a component of

the annual capital budget

EXCO Perspective –

Drilling

Fund Returns

EXCO will pay to KKR: $584 million for PDP

properties plus $211 million for the estimated

land return for a total of $795 million. 65% of

which can be funded through secured borrowings

leaving a $278 million shortfall to fund via cash

flow, additional debt or equity over a 4 year

period (~$70 million/year)

Drilling Capital Plan for Eagle Ford

KKR Return Contributions

EXCO Return Contributions

CNOOC

KKR

EXCO

Year 1 CF

DCRA

Year 1 CF

DCRA |

12

September Investor Presentation

2013

2014

2015

2016

2017

2018

2019+

GAS

3.75

$

4.00

$

4.15

$

4.25

$

4.50

$

4.75

$

5.00

$

OIL

100.00

$

90.00

$

90.00

$

85.00

$

82.50

$

80.00

$

80.00

$

Total Program Illustrative Example

($ in millions)

KKR

XCO

KKR

XCO

KKR

XCO

Drilling & completion capital invested

1,080

$

360

$

Undrilled locations

300

300

Undrilled locations

300

300

Drilling multiple

1.2x

1.2x

AFE (8/8ths)

7.2

$

7.2

$

Remaining value at buyout PV-10 (50% NRI)

3.0

$

1.0

$

Capital return

1,296

$

432

$

WI%

66.7%

66.7%

Fair market value at buyout PV-10 (50% NRI)

900

$

300

$

Less: First year cash flow

712

$

236

$

Share of capital

75.0%

25.0%

Remaining required drilling return

584

$

196

$

Total drilling program capital

1,080

$

360

$

Remaining value at buyout PV-0 (50% NRI)

5.5

$

1.8

$

Fair market value at buyout PV-0 (50% NRI)

1,650

$

525

$

Fair Market Value at Buyout

900

$

300

$

Drilling Capital Return Amount

584

$

196

$

2/3 of difference btwn FMV and DCRA

211

$

208

$

Allocation of Fair Market Value

795

$

404

$

KKR

XCO

KKR

XCO

KKR

XCO

Land investment

131

$

131

$

First year cash flow

712

$

236

$

Investment

1,211

$

1,286

$

Drilling investment

1,080

360

Remaining required drilling return

584

-

Buyout drilling

-

584

Land return

211

-

Return (PV-10 based)

1,507

$

1,436

$

Buyout land

-

211

Fair market value at buyout PV-10

-

1,200

Multiple on invested capital

1.24x

1.12x

Total invested capital

1,211

$

1,286

$

Total return

1,507

$

1,436

$

Return (PV-0 based)

1,507

$

2,411

$

Multiple on invested capital

1.24x

1.88x

Project Cash Flow

Drilling & Completion Capital

Fair Maket Value At Buyout

Multiple on Invested Capital

Invested Capital

Return on Capital Invested

Note:

Assumptions

above

based

on

internal

EXCO

acquisition

economics

and

the

following

forward

NYMEX

price

deck.

Forecasted

cash flow

based on EXCO’s internal type curve estimate of 445 Mboe. Actual results could vary

materially. |

13

September Investor Presentation

Liquidity Review

EXCO/ HGI

Partnership

TGGT

($ in thousands)

6/30/2013

7/31/2013

6/30/2013

6/30/2013

Cash and restricted cash

118,600

$

85,660

$

17,223

$

14,926

$

Amount drawn on bank credit facility

474,234

$

735,000

$

369,000

$

450,000

$

Asset sale tranche

-

269,096

-

-

Term loan

-

300,000

-

-

2018 Senior Notes

750,000

750,000

-

-

Total debt

1,224,234

$

2,054,096

$

369,000

$

450,000

$

Bank borrowing base

900,000

$

1,469,096

$

470,000

$

600,000

$

Amount drawn on bank credit facility

474,234

1,304,096

369,000

450,000

Available for borrowing

425,766

$

165,000

$

101,000

$

150,000

$

Plus: Cash and restricted cash

118,600

85,660

17,223

14,926

Less: Letters of credit

6,888

6,888

525

-

Liquidity

537,478

$

243,772

$

117,698

$

164,926

$

EXCO Resources

Chesapeake asset transaction financed with new $1.6 billion credit facility made up

of the following:

–

$900 million senior secured line of credit

–

$400 million asset sale requirement tranche (reduced to ~$269 million with KKR land

purchase)

–

$300

million

1

st

lien

term

loan |

14

September Investor Presentation

Conclusions

Scheduled quarterly acquisitions of producing properties

Producing properties that can be readily financed through a

secured borrowing base

Acquisitions help offset declining reserve base

Lowers overall risk of business and increases predictability of

cash flows |

| 15

September Investor Presentation

This

presentation

contains

forward-looking

statements,

as

defined

in

Section

27A

of

the

Securities

Act

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

or

the

Exchange

Act.

These

forward-looking

statements

relate

to,

among

other

things,

the

following:

•

our future financial and operating performance and results;

•

our business strategy;

•

market prices for oil, natural gas and natural gas liquids;

•

our future use of derivative financial instruments; and

•

our plans and forecasts.

We

have

based

these

forward-looking

statements

on

our

current

assumptions,

expectations

and

projections

about

future

events.

We use the words "may," "expect," "anticipate," "estimate,"

"believe," "continue," "intend," "plan," "budget" and other similar words to identify forward-looking statements. The statements that contain these words should be

read

carefully

because

they

discuss

future

expectations,

contain

projections

of

results

of

operations

or

our

financial

condition

and/or

state

other

"forward-looking"

information.

We

do

not

undertake

any

obligation

to

update

or revise publicly any forward-looking statements, except as required by applicable

securities law. These statements also involve risks and uncertainties that could cause our actual results or financial condition to materially

differ from our expectations in this presentation, including, but not limited to:

•

fluctuations in the prices of oil, natural gas and natural gas liquids;

•

the availability of foreign oil, natural gas and natural gas liquids;

•

future capital requirements and availability of financing;

•

our ability to meet our current and future debt service obligations;

•

disruption of credit and capital markets and the ability of financial institutions to honor

their commitments; •

estimates of reserves and economic assumptions;

•

geological concentration of our reserves;

•

risks associated with drilling and operating wells;

•

exploratory risks, primarily related to our activities in shale formations including our

recent acquisition in the Eagle Ford shale; •

risks

associated

with

operation

of

natural

gas

pipelines

and

gathering

systems;

•

discovery, acquisition, development and replacement of oil and natural gas reserves;

•

cash flow and liquidity;

•

timing and amount of future production of oil and natural gas;

•

availability of drilling and production equipment;

•

marketing of oil and natural gas;

•

political and economic conditions and events in oil-producing and natural

gas-producing countries; •

title to our properties;

•

litigation;

•

competition;

•

general economic conditions, including costs associated with drilling and operation of our

properties; •

environmental or other governmental regulations, including legislation to reduce emissions of

greenhouse gases, legislation of derivative financial instruments, regulation of hydraulic fracture

stimulation and elimination of income tax incentives available to our industry;

•

receipt and collectability of amounts owed to us by purchasers of our production and

counterparties to our derivative financial instruments; •

decisions whether or not to enter into derivative financial instruments;

•

potential acts of terrorism;

•

our

ability

to

manage

joint

ventures

with

third

parties

including

the

resolution

of

any

material

disagreements

and

our

partners’

ability

to

satisfy

obligations

under

these

arrangements;

•

actions of third party co-owners of interests in properties in which we also own an

interest; •

fluctuations in interest rates; and

•

our ability to effectively integrate companies and properties that we acquire.. Forward Looking Statements |

16

September Investor Presentation

We

believe

that

it

is

important

to

communicate

our

expectations

of

future

performance

to

our

investors.

However,

events

may

occur

in

the

future

that

we

are

unable

to

accurately

predict,

or

over

which

we

have

no

control.

We

caution users of the financial statements not to place undue reliance on a forward-looking

statement. When considering our forward-looking statements, keep in mind the risk factors and other cautionary statements in this

presentation,

and

the

risk

factors

included

in

our

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2012,

filed

with

the

Securities

and

Exchange

Commission,

or

the

SEC,

on

February

21,

2013,

and

our

Quarterly

Reports

on

Form 10-Q.

Our

revenues,

operating

results

and

financial

condition

substantially

depend

on

prevailing

prices

for

oil

and

natural

gas

and

the

availability

of

capital

from

our

credit

agreement,

or

the

EXCO

Resources

Credit

Agreement.

Declines

in

oil

or

natural

gas

prices

may

have

a

material

adverse

effect

on

our

financial

condition,

liquidity,

results

of

operations,

the

amount

of

oil

or

natural

gas

that

we

can

produce

economically

and

the

ability

to

fund

our

operations.

Historically,

oil

and

natural

gas

prices

and

markets

have

been

volatile,

with

prices

fluctuating

widely,

and

they

are

likely

to

continue

to

be

volatile.

The

SEC

permits

oil

and

gas

companies,

in

their

filings

with

the

SEC,

to

disclose

not

only

"proved"

reserves

(i.e.,

quantities

of

oil

and

gas

that

are

estimated

to

be

recoverable

with

a

high

degree

of

confidence),

but

also

"probable"

reserves (i.e., quantities of oil and gas that are as likely as not to be recovered) as well as

"possible" reserves (i.e., additional quantities of oil and gas that might be recovered, but with a lower probability than probable reserves). In

addition

unless

otherwise

noted,

certain

proved

reserve

numbers

and

other

reserve

numbers

provided

herein

are

not

SEC

“case”

numbers

using

flat

commodity

prices,

but

a

management

case

price

deck

using

escalating

prices

for

a

period

of

time.

As

noted

above,

statements

of

reserves

are

only

estimates

and

may

not

correspond

to

the

ultimate

quantities

of

oil

and

gas

recovered.

Any

reserve

estimates

provided

in

this

presentation

that

are

not

specifically

designated as being estimates of proved reserves may include estimated reserves not necessarily

calculated in accordance with, or contemplated by, the SEC's latest reserve reporting guidelines. Investors are urged to consider closely

the

disclosure

in

our

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2012,

which

is

available

on

our

website

at

www.excoresources.com

under

the

Investor

Relations

tab

or

by

calling

us

at

214-368-2084.

Forward Looking Statements (Continued) |