Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - Education Realty Trust, Inc. | exhibit232consent.htm |

| 10-K/A - 10-K/A - Education Realty Trust, Inc. | edramendno2form10-k_aforde.htm |

| EX-32.1 - EXHIBIT 32.1 - Education Realty Trust, Inc. | exhibit321.htm |

| EX-32.2 - EXHIBIT 32.2 - Education Realty Trust, Inc. | exhibit322.htm |

| EX-31.1 - EXHIBIT 31.1 - Education Realty Trust, Inc. | exhibit311.htm |

| EX-31.2 - EXHIBIT 31.2 - Education Realty Trust, Inc. | exhibit312.htm |

INDEPENDENT AUDITORS' REPORT

The Board of Directors and Stockholders of

Education Realty Trust, Inc.

Memphis, Tennessee

We have audited the accompanying financial statements of University Village - Greensboro, LLC, which comprise the balance sheet as of December 31, 2012, and the related statements of operations and comprehensive income (loss), changes in members' deficit, and cash flows for the year then ended, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

1

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of University Village - Greensboro, LLC as of December 31, 2012, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matter

The accompanying balance sheet of University Village – Greensboro, LLC as of December 31, 2011, and the related statements of operations and comprehensive income (loss), changes in members' deficit and cash flows for the years ended December 31, 2011 and 2010 were not audited by us and, accordingly, we do not express an opinion or any other form of assurance on them.

Memphis, Tennessee

April 1, 2013

2

University Village – Greensboro, LLC

Notes to Financial Statements

December 31, 2012, 2011 (unaudited) and 2010 (unaudited)

1. Organization and description of business

University Village – Greensboro, LLC (the "Company"), a Delaware Limited Liability Company, which was formed on April 28, 2006 for the purpose of constructing and owning a 600-bedroom collegiate housing facility (the "Facility") adjacent to the campus of the University of North Carolina at Greensboro (the "University"). The Facility is managed by EdR Management, Inc. ("EdRM"). The Company is owed by College Park Apartments, Inc. and EDR Greensboro, LLC, a wholly-owned subsidiary of Education Realty Operating Partnership, LP, collectively (the "Members"). EdRM and EDR Greensboro, LLC are ultimately owned by Education Realty Trust, Inc. The Company shall continue until December 31, 2076, unless earlier terminated in accordance with the provisions of the agreement.

2. Summary of significant accounting policies

Use of estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America ("GAAP") requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates; however, in the opinion of management, such differences will not be material to the financial statements.

Restricted cash

Restricted cash includes escrow accounts held by lender for the purpose of paying taxes and funding capital improvements.

Collegiate housing property

Land, land improvements, buildings and improvements, and furniture and equipment are recorded at cost. Buildings and improvements are depreciated over fifteen to forty years, land improvements are depreciated over fifteen years and furniture and equipment are depreciated over three to seven years. Depreciation is computed using the straight-line method for financial reporting purposes over the estimated useful life.

2. Summary of significant accounting policies (continued)

Collegiate housing property (continued)

Management assesses impairment of long-lived assets to be held and used whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Management uses an estimate of future undiscounted cash flows of the related asset based on its intended use to determine whether the carrying value is recoverable. If the Company determines that the carrying value of an asset is not recoverable, the fair value of the asset is estimated and an impairment loss is recorded to the extent the carrying value exceeds estimated fair value. Management estimates fair value using discounted cash flow models, market appraisals if available, and other market participation data.

Deferred financing costs

Deferred financing costs represent costs incurred in connection with acquiring debt. The deferred financing costs incurred for the year ended December 31, 2010 were $237,026 and are being amortized over the term of the related debt using a method that approximates the effective interest rate method. Debt issuance costs amortized during the construction period were capitalized as part of the Facility costs. Amortization expense totaled $23,703 for the years ended December 31, 2012 and 2011 and $16,044 for the year ended December 31, 2010. As of December 31, 2012 and 2011, accumulated amortization totaled $59,256 and $35,554, respectively. Deferred financing costs, net of amortization, are included in other assets in the accompanying balance sheets.

Income taxes

The Company is treated as a partnership for federal and state income tax purposes. Therefore, federal and state taxable income and any applicable tax credits are included in the income tax returns of the Members and any income tax liability thereto is borne by Members. The Company has determined that it does not have any material unrecognized tax benefits or obligations as of December 31, 2012 and 2011. Tax years 2009 and after remain subject to examination by federal and state taxing authorities.

Repairs, maintenance and major improvements

The cost of ordinary repairs and maintenance are charged to operations when incurred. Major improvements that extend the life of an asset are capitalized and depreciated over the remaining useful life of the asset. The lender requires the Company to maintain a reserve account for future capital expenditures. This amount is classified as restricted cash in the accompanying balance sheets as the funds are not available for general use.

2. Summary of significant accounting policies (continued)

8

Other comprehensive income (loss)

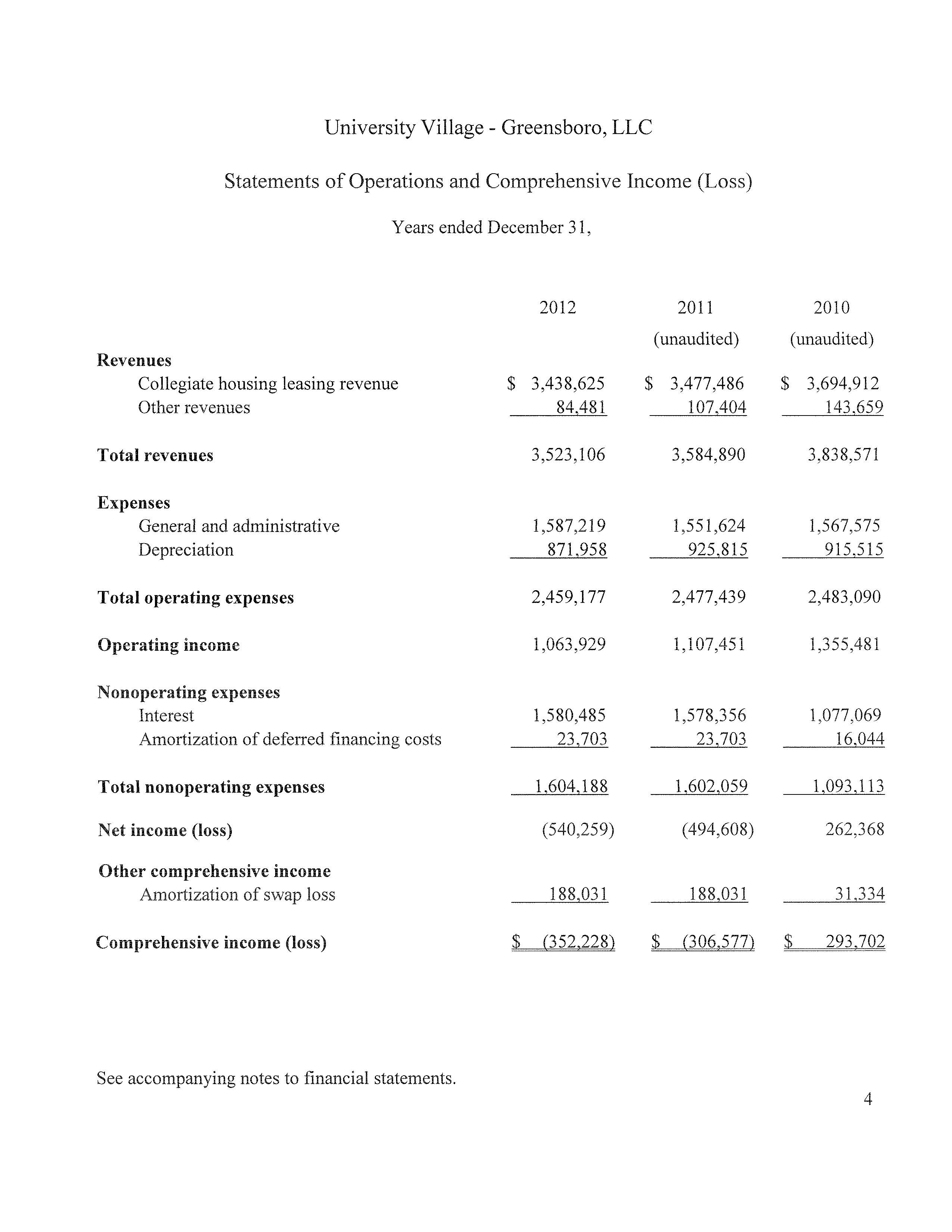

The Company follows the authoritative guidance issued by the Financial Accounting Standards Board relating to the reporting and display of comprehensive income and its components. Members' deficit includes accumulated other comprehensive loss related to the interest rate swap agreement (Note 4) of $1,128,192, $1,316,224, and $1,504,256 at December 31, 2012, 2011 and 2010, respectively.

Revenue recognition

The Company requires students to execute lease contracts that are typically 50 weeks in length and include 12 equal monthly payments. Generally, the Company requires each executed lease contract to be accompanied by a signed parental guarantee. Receivables are recorded when billed. Revenues and related lease incentives and nonrefundable application and service fees are recognized on a straight-line basis over the term of the contracts.

Advertising

Advertising costs are expenses as incurred and totaled approximately $56,000, $46,000 and $44,000 for the years ended December 31, 2012, 2011 and 2010, respectively.

3. Collegiate housing property

Collegiate housing property consists of the following at December 31, 2012 and 2011:

2012 | 2011 | ||||||

Land | $ | 3,736,707 | $ | 3,736,707 | |||

Land improvements | 1,620,431 | 1,612,302 | |||||

Buildings and improvements | 19,410,812 | 19,391,903 | |||||

Furniture, fixtures and equipment | 1,611,803 | 1,531,178 | |||||

26,379,753 | 26,272,090 | ||||||

Accumulated depreciation | (4,919,867) | (4,047,909) | |||||

Collegiate housing property | $ | 21,459,886 | $ | 22,224,181 | |||

4. Mortgage

The Company initially entered into construction loans for a total of $25,221,173 for the construction of the Facility. Additionally, the Company entered into a cash settled forward-starting interest rate swap ("Swap") with Regions Bank on July 21, 2006 in order to hedge against the risk of increasing interest rates during the construction period. The Company chose to designate the Swap as a cash flow hedge based on 10 years of forecasted interest payments on the first, previously un-hedged,

4. Mortgage (continued)

9

long-term borrowing issued between May 1, 2008 and January 31, 2009. The Swap had the following terms: a notional amount of $21,500,000, a fixed annual interest rate of 5.77% measured against the 3-month USD-LIBOR index, an effective date of September 15, 2008 and a maturity date of September 15, 2018. The hedging relationship qualified as highly effective; therefore, the fair value of the Swap was recorded in other comprehensive loss in the accompanying balance sheets.

On October 15, 2008, the Company terminated the Swap for $2,101,636 in cash. Prior to the actual refinancing of the debt, the Company changed its best estimate of the date of refinancing the construction loans and reclassified a total of $566,045 from other comprehensive loss to current expense. As discussed below, the construction loans were refinanced on June 23, 2010, and the Company began amortizing the other comprehensive loss into interest expense. Amortization of the Swap will continue through December 31, 2018. Amounts amortized into interest expense were $188,031 for the years ended December 31, 2012 and 2011, and $31,334 for the year ended December 31, 2010. The expected amount to be amortized into interest expense for 2013 is $188,031.

On June 23, 2010, the Company signed a $24,400,000 note to replace the prior construction financing. The note bears a fixed interest rate equal to 5.620% and required payment of interest only through the first two years. Beginning August 1, 2012, the Company began to pay monthly principal and interest payments of $140,383 per the note agreement. The note is being amortized over a thirty year period, but has a maturity date of July 1, 2020. The note is secured by the collegiate housing property.

Future maturities of the debt at December 31, 2012, are as follows:

2013 | $ | 309,171 | ||

2014 | 327,255 | |||

2015 | 346,397 | |||

2016 | 362,872 | |||

2017 | 387,884 | |||

Thereafter | 22,546,199 | |||

$ | 24,279,778 | |||

5. Related party transactions

The management and daily operations of the Facility are conducted by EdRM. This includes leasing, resident relations, billing and collections of rent, payment of indebtedness and expenses, capital asset management, and administrative services. All employees that manage the Facility are employees of EdRM.

Management fees are calculated as 5% of total revenues and amounted to $175,185, $177,196 and $188,050 for the years ended December 31, 2012, 2011 and 2010, respectively.

10

6. Subsequent Events

The Company evaluated the effect subsequent events would have on the financial statements through April 1, 2013, which is the date the financial statements were available to be issued.

7. Members' Interest

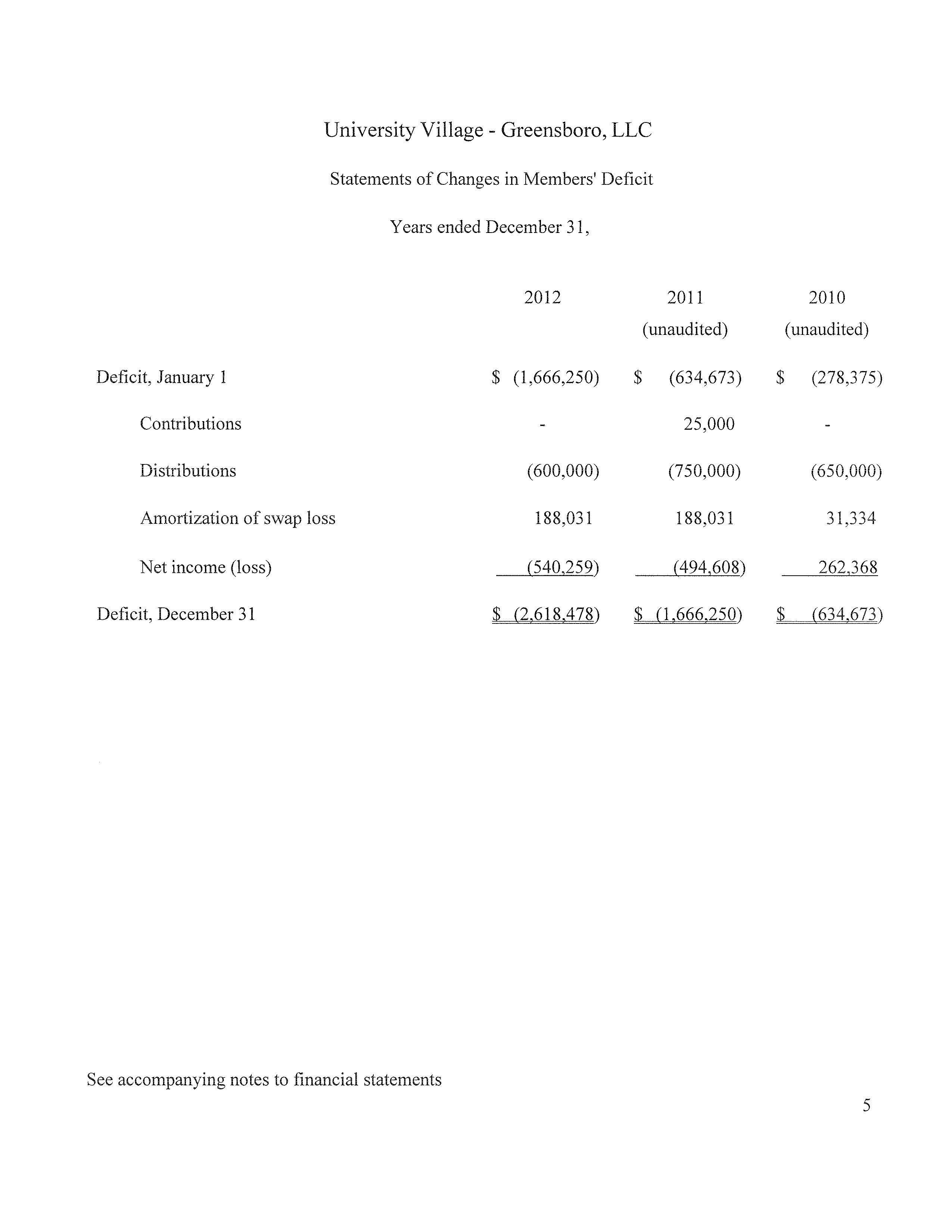

The Company operates under a Limited Liability Company Agreement ("Agreement") between College Park Apartments, Inc. ("CPA") and EDR Greensboro, LLC ("EDR"). As an initial capital contribution, CPA transferred land to the Company valued at $3,400,000, less the repayment of any indebtedness secured by the land, for a 50% interest in the Company. EDR was required to contribute $1,000 and guarantee the repayment of the construction loans in order to receive a 50% interest in the Company. In 2011, EDR contributed $25,000 in cash to cover excess costs incurred with implementation of an internet upgrade. Distributions are made from excess cash availability, effectively 25% to EDR and 75% to CPA.

8. Concentration of Risk

The Company is subject to the risks involved with ownership and operation of residential real estate at the University. These risks include, among others, those normally associated with changes in the demand for housing by students, enrollment trends at the University, competition for tenants, creditworthiness of tenants, changes in tax laws, interest rate levels, the availability of financing, and potential liability under environmental and other laws.

9. Litigation

The Company is party to various legal and administrative proceedings arising in the normal course of business. The resolution of these matters is subject to many uncertainties, and the ultimate outcome of the proceedings cannot presently be determined. The Company believes that any liabilities resulting from these matters are not expected to have a material impact on the financial statements.

11