Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - E TRADE FINANCIAL CORP | d444837d8k.htm |

E*TRADE

Financial Corporation KBW Securities Brokerage & Market Structure Conference

Matthew Audette, Chief Financial Officer

November 28, 2012

©

2012 E*TRADE Financial Corporation all rights

reserved. Exhibit 99.1

|

©

2012 E*TRADE Financial Corporation all rights reserved

Safe Harbor Statement

This presentation contains certain forward-looking statements regarding our business

strategy and the related impact, our strategic and capital plans, certain deleveraging

and cost-savings initiatives, the continuation of current trends,

future

events

and

the

future

performance

of

the

Company.

E*TRADE

claims

the

protection

of

the

safe

harbor

for forward-looking statements contained in the Private Securities Litigation Reform Act

of 1995 for all forward- looking statements. Various factors, including risks

and uncertainties referred to in the prospectus supplement related to this offering as

well as in the 10-K, 10-Q and other reports incorporated in the prospectus supplement

could cause our actual results to differ materially from those indicated by our projections or

other forward-looking statements.

Notice to investors

2

Non-GAAP Financial Measures

In addition to financial results prepared in accordance with Generally Accepted Accounting

Principles, or GAAP, this presentation will also contain certain non-GAAP financial

measures. Management uses these non-GAAP measures to evaluate our performance

and in planning for future periods. Management believes that adjusting GAAP measures by

excluding

or

including

certain

items

is

helpful

to

investors

and

analysts

who

may

wish

to

use

some

or

all

of

this

information to analyze our current performance, prospects and valuation. It is important to

note these non-GAAP measures

involve

judgment by

management and

should

be

considered

in

addition

to,

not

as

a

substitute for,

the most

directly comparable measures calculated and prepared in accordance with GAAP. Investors and

potential investors are encouraged to review the reconciliation of non-GAAP

financial measures with their most direct comparable GAAP financial measures included

as an appendix to this presentation. This

presentation presents data as of September 30, 2012, unless otherwise indicated.

|

Improve market

position in retail brokerage •

Accelerate growth of the customer franchise

•

Continue to enhance the customer experience, improve satisfaction and retention

Capitalize on value of complementary brokerage businesses

•

Corporate Services Group

•

Market making operations

Enhance position in retirement & investing

•

Expand brand position for awareness and preference

•

Grow customer share of wallet

Continue to manage and de-risk the Bank

•

Mitigate

credit

losses

on

legacy

loan

portfolio

and

enhance

risk

profile

•

Build out enterprise risk management function

Strengthen overall financial and franchise position

•

Improve capital ratios through de-risking and de-leveraging

•

Focus on ultimately deploying excess Bank capital to parent to pay off corporate debt

•

Increase focus on cost reductions and efficiencies: Targeting $100M in run-rate

reductions Business strategy

©

2012 E*TRADE Financial Corporation all rights reserved

3 |

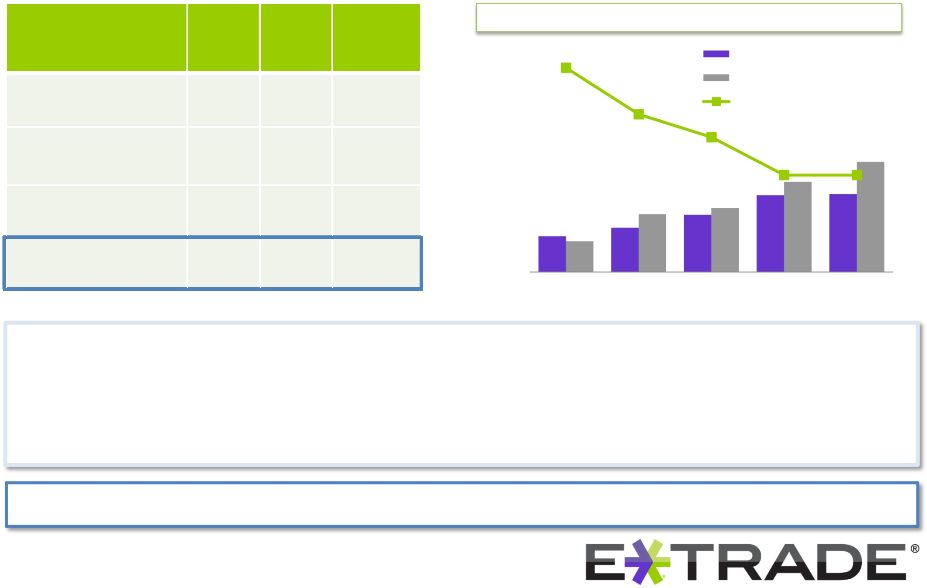

$0.9B

$(2.2)B

$(1.3)B

$(0.9)B

$0.0B

$0.2B

Pre-tax income:

($ M)

Last 4 quarters

Driver

Long-term impact

of current strategy

Revenue

$1,907

$2,150

Provision

($403)

$0

Servicing

($64)

$0

FDIC expenses

($112)

($56)

Other operating expenses

($1,005)

($1,005)

Expenses, total

($1,181)

($1,061)

Operating income

$323

$1,089

Corporate interest expense

($181)

$0

Other

($51)

($51)

Pre-tax income

$91

$1,038

Should reduce to $0 as excess Bank capital is

deployed to parent to pay off corporate debt

$1.0B

Long-term

impact to

current

strategy

(1)

$0.1B

Net interest spread should improve to 300bps

with normalized rate environment

Should reduce to $0 as legacy portfolio runs off

Should reduce to $0 as legacy portfolio runs off

Should reduce by half as risk profile improves

Strengthen overall financial and franchise position

Long-term impact of current strategy to improve earnings

©

2012 E*TRADE Financial Corporation all rights reserved

4

$1.5

$0.5

($0.5)

($1.5)

($2.5)

($3.5)

2006

2007

2008

2009

2010

2011

Earnings before interest, taxes and credit costs

Provision / credit cost

Interest & other expense

Last 4

quarters |

©

2012 E*TRADE Financial Corporation all rights reserved

5

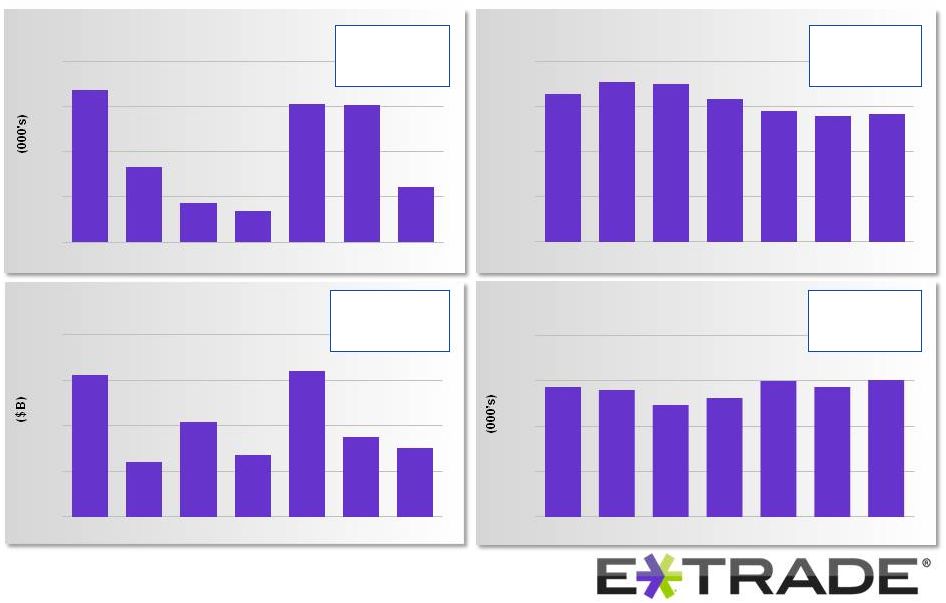

Strategic and Capital Plan submitted to Fed and OCC in June 2012 •

Outlined assumptions for capital levels and distributions under various operating conditions

over next 5 years •

Includes the assumption that the Bank begins distributing capital to the Parent by the

end of 2013 •

Plan assumes the Bank will dividend capital to the Parent above Tier 1 leverage ratio of 9.5%

•

9.5% target decreases by 50 bps each year beginning in 2014, ultimately settling at 8.0%

Capital ratios as of

9/30/12

Bank

Parent

Well-

capitalized

threshold

Total capital to

risk-weighted assets

(2)

19.3%

14.3%

10.0%

Tier 1 capital to

risk-weighted assets

(2)

18.0%

13.0%

6.0%

Tier 1 common

(3)

18.0%

10.9%

7.0%

Tier 1 leverage

(2)

7.9%

5.8%

5.0%

Bank excess capital / Corporate debt

(4)

Reducing balance sheet size / improving leverage ratio is integral to the successful execution

of the Capital Plan 3Q 08

3Q 09

3Q 10

3Q 11

3Q 12

Excess Tier 1 leverage

Excess Risk-based capital

Corporate debt

©

2012 E*TRADE Financial Corporation all rights reserved

Strengthen overall financial and franchise position

Focused on deleveraging to improve most constraining ratio: Tier

1 leverage

5

(5)

($B)

$3.5

$3.0

$2.5

$2.0

$1.5

$1.0

$0.5

$- |

©

2012 E*TRADE Financial Corporation all rights reserved

6

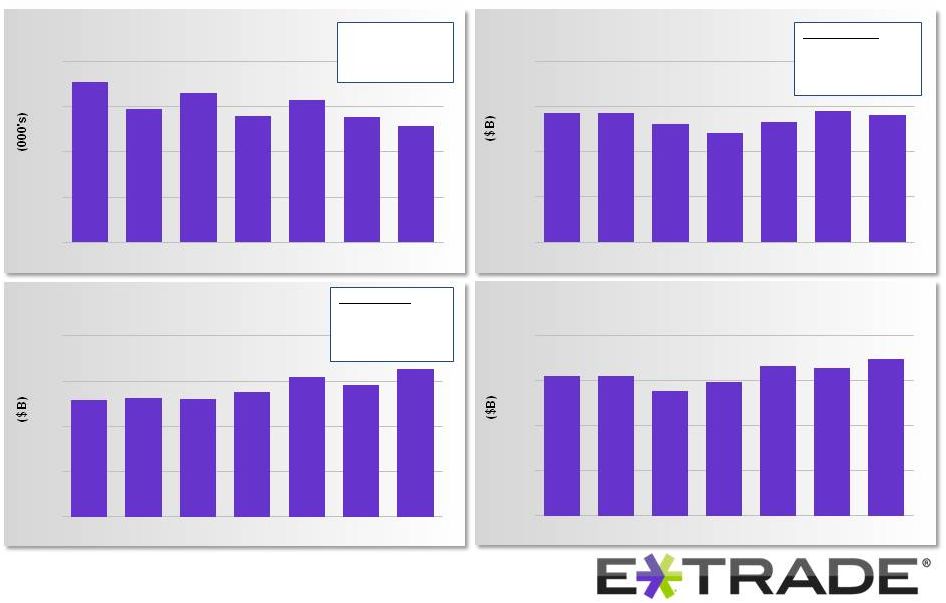

Drivers of change in balance sheet size

Focused on deleveraging to improve most constraining ratio: Tier

1 leverage

Strengthen overall financial and franchise position

$55

$50

$45

$40

2Q 2012

$49.2

$2.2

$(1.3)

$0.3

$50.4

$(3.0)

$(1.3)

$46.1

customer net

selling

deleveraging

actions

other

3Q 2012

planned

deleveraging

actions

October

customer net

buying

4Q 2012

pro forma

Deleveraging actions

completed during 3Q 2012

Deleveraging actions identified or

completed for 4Q 2012

TOTAL

Reduce wholesale borrowings

$520M

Transfer sweep deposits

$1,200M

Transfer customer deposits

$470M

Reduce wholesale borrowings

$900M

Default new customer cash to

money funds

$300M

Convert customer payables to money

funds

(6)

$900M

Total

$1,290M

Total

$3,000M

$4,290M |

7

Strengthen overall financial and franchise position

Debt refinancing to significantly improve cash flow and reduce interest burden

Improved maturity profile

•

Lowest Senior Note coupons in the Company’s history

•

Improves annual earnings by approximately $60M or

$0.21 per share

(7)

•

Improves pro forma debt service coverage ratio for parent

cash to 3.9X from 2.6X

•

Lengthens maturity profile, eliminating nearest maturity

and extending weighted average maturity by +1 year

•

Call features allow prepayment flexibility

Transaction benefits

Weighted average maturity:

Pre-refi = 4.3 years

Post-refi = 5.5 years

Improved earnings

(7)

Transaction overview

•

Launched transaction to refinance debt on 11/5

•

Successfully raised $1.3B in Senior notes –

closed on 11/14

•

Issued call notice for $930M of Springing Lien Notes due

2017 and $243M of 7.875% Senior Notes due 2015

•

Will extinguish called notes on 12/1

Pre-

refi

Post-refi

$1.0

$0.8

$0.6

$0.4

$0.2

$0.0

2013

2014

2015

2016

2017

2018

2019

©

2012 E*TRADE Financial Corporation all rights reserved

Maturity

2015

2016

2017

Coupon

7.875%

6.75%

12.50%

Balance

$243

$435

$930

GAAP interest

expense

$19

$29

$137

After tax

$12

$18

$99

Total

10.25%

$1,608

$185

$129

2016

2017

2019

6.75%

6.00%

6.38%

$435

$505

$800

$29

$30

$51

$18

$19

$32

Total

6.36%

$1,740

$110

$69

$75

$60

Savings |

Consolidated

DTA of $1.3B ($0.3B at parent; $1.0B at Bank)

Ability to include more in regulatory capital with ongoing

profitability

Source of corporate cash as subsidiaries reimburse the

parent for use of its DTA

Approximately 16 years to use; expect to utilize the full

amount

(8)

Strengthen overall financial and franchise position

Deferred tax asset: Embedded value realized with ongoing profitability

©

2012 E*TRADE Financial Corporation all rights reserved

8

Consolidated DTA = $1.3B;

only 6%

is included in regulatory capital

excluded from

regulatory

capital

Included in

regulatory

capital

$ B

Bank DTA = $1.0B;

only 26% is included in regulatory capital

$ B

$0.08

$1.27

excluded from

regulatory

capital

Included in

regulatory

capital

$0.3

$0.7

DTA

Pre-tax income equivalent

Parent company

Bank

$3.5B

$1.3B

4.0

3.0

2.0

1.0

0.0 |

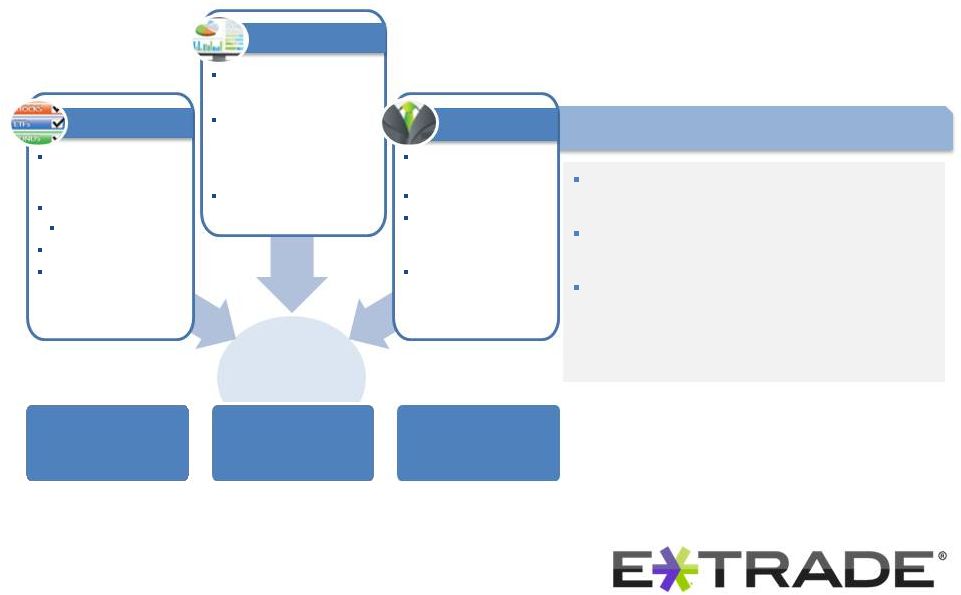

Redesigned

public website Leading-edge platforms

Award-winning iconic brand & advertising

Committed to grow as a recognized leader with iconic brand and advertizing

(9)

(10)

(11)

Improve market position in retail brokerage

9

©

2012 E*TRADE Financial Corporation all rights reserved

|

©

2012 E*TRADE Financial Corporation all rights reserved

10

Improve market position in retail brokerage

Lower

attrition

Increase

net new assets /

share of wallet

Grow

high quality

account base

Increase asset-based

and commission-

based revenue

Key initiatives to drive success

•

Create leading online broker

experience:

•

E*TRADE.com

•

E*TRADE 360

•

E*TRADE Mobile

•

Education & research

•

E*TRADE Community

•

Focus on customer dissatisfiers

•

Continuous process improvement

•

Deliver best-in-class trading

experience:

•

E*TRADE.com

•

E*TRADE Pro

•

E*TRADE Mobile

•

Expand product engagement

through:

•

Platform enhancements

•

Idea generating tools

•

Education for all traders on

products, platforms, strategies and

risk management

•

Expand brand as a trusted

retirement and investing

provider

•

Deliver retirement advice &

planning:

•

Financial Consultants

•

Online planning tools

•

Managed Products

•

Increase awareness of needs-

based investing solutions:

•

Mutual funds

•

Fixed income

•

ETFs

•

Deepen relationships with

high-potential customers

Improve

customer experience

Enhance retail

trading offering

Grow retirement

& investing |

Net new

brokerage accounts

Net new brokerage

assets

(13)

Annualized brokerage

account attrition

(12)

2010: 12.2%

2011: 10.3%

YTD 2012: 8.7%

2010: 54k

2011: 99k

YTD 2012: 110k

2010: $8.1B

2011: $9.7B

YTD 2012: $8.1B

Average brokerage

assets per account

(14)

2010: $49k

2011: $54k

YTD 2012: $59k

Improve market position in retail brokerage

Accelerate growth of the customer franchise

©

2012 E*TRADE Financial Corporation all rights reserved

11

60

45

30

15

0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

51

25

13

10

46

46

18

12%

9%

6%

3%

0%

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

9.9%

10.7%

10.5%

9.5%

8.7%

8.4%

8.5%

$5.0

$3.8

$2.5

$1.3

$0.0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

$3.9

$1.5

$2.6

$1.7

$4.0

$2.2

$1.9

$80

$60

$40

$20

$

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

$57

$56

$49

$52

$60

$57

$60 |

©

2012 E*TRADE Financial Corporation all rights reserved

12

DARTs

Average cost:

2010: 12bps

2011: 11bps

YTD 2012: 12bps

2010: 151k

2011: 157k

YTD 2012: 141k

Average yield:

2010: 442bps

2011: 413bps

YTD 2012: 395bps

Retirement assets

Improve market position in retail brokerage

Accelerate growth of the customer franchise

177

148

165

140

157

139

129

$5.7

$5.7

$5.2

$5.3

$5.8

$5.6

$4.8

Customer margin

receivables

200

150

100

50

0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

12

©

2012 E*TRADE Financial Corporation all rights reserved

$8

$6

$4

$2

$0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Brokerage-related

cash

$40

$30

$20

$10

$0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

$26

$26

$26

$28

$31

$33

$29

$40

$30

$20

$10

$0

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

$31

$31

$28

$30

$33

$33

$35 |

#1 ranking

in Kiplinger’s 2012 Best Online Brokers

-

five stars in Investment

Choices

Financial Consultant network highlights

Increased Financial Consultant headcount by over

40% since year-end 2010

Estimated 12% share of our customers’

investible

assets (36% for active traders; 10% for investors)

(15)

Identified segments best served by proactive

engagement with Financial Consultants

—

1-year post assignment seeing significant

improvement in engagement and retention

Accounts &

assets

8,100+ mutual funds

—

4,600 no-load

—

6,900 NTF

50,000+ bonds

Managed Accounts

(MIP & UMA)

Integrated into

advertising

Headcount of 270

Increased asset

penetration 1 year post

assignment

Complementary

retirement & portfolio

consultations

Products

†

Services

Financial

Consultants

Enhance position in retirement & investing

†

Unified Managed Accounts and Managed Investment Portfolios are offered by E*TRADE Capital

Management ©

2012 E*TRADE Financial Corporation all rights reserved

13

SM

Every ETF sold

Chartered Retirement

Planning Counselors

Retirement education

80+ Comm. Free

$34.6 billion in

retirement assets

20% of $174 billion of

brokerage-related assets

796k retirement

accounts

28% of brokerage accounts

$1.1 billion in managed

accounts

(2.5 years post inception) |

Market making

business Leveraging world class technologies and superior execution

capabilities

Leading market share in ADRs; growing market share in

National Market Securities

Growing base of external customers, comprising 45+ external

clients

(47% y/y growth), and accounting for approximately half

of market making revenue

Corporate Services Group

Build on market leadership with 1,400+ corporate clients,

representing +20% of S&P 500

Foster strategically important channel for new brokerage

accounts, accounting for 25-30% of gross new accounts

1.1 million accounts; $23B in vested and $48B in unvested

options

Proceeds retention of 35%+ 3 months post exercise,

and 15%+ 12 months post exercise

Principal transactions revenue ($M)

Stock plan administration for

public companies

E*TRADE

#2 Player

#3 Player

6+ other providers

Capitalize on value of complementary brokerage businesses

©

2012 E*TRADE Financial Corporation all rights reserved

14

22%

48%

20%

10%

$30

$25

$20

$15

$10

$5

$0

$30

$24

$27

$25

$24

$21

$22 |

©

2012 E*TRADE Financial Corporation all rights reserved

15

Improvement in asset composition…

…Funding mix also continues to improve

•

Legacy loan portfolio now accounts for less than 30% of

average interest-earning assets, down from 55% in 3Q 2007

•

Average loan portfolio balances are down 64% from peak in

3Q 2007

•

Bank risk weighted assets are down 42% from peak in 3Q

2007, while average total assets are down 24%

•

More expensive wholesale funding channel now accounts

for only 17% of average interest-bearing liabilities, down

from 38% at its peak in 3Q 2007

•

Average wholesale funding is down 65% from its peak in 3Q

2007

•

Balance sheet strategy going forward is liability-driven, by

brokerage cash

Favorable mix shift in assets (lower risk) and liabilities (lower-cost)

Continue to manage and de-risk the Bank

15

©

2012 E*TRADE Financial Corporation all rights reserved

Agency securities, cash, and other

Legacy loans

Brokerage-related deposits and other

Wholesale funding

60

50

40

30

20

10

0

60

50

40

30

20

10

0

1Q

2007

1Q

2007

3Q

2007

1Q

2008

3Q

2008

1Q

2009

3Q

2009

1Q

2010

3Q

2010

1Q

2011

3Q

2011

1Q

2012

3Q

2012

1Q

2012

3Q

2012

3Q

2007

1Q

2008

3Q

2008

1Q

2009

3Q

2009

1Q

2010

3Q

2010

1Q

2011

3Q

2011 |

©

2012 E*TRADE Financial Corporation all rights reserved

16

Continue to manage and de-risk the Bank

Mitigate credit losses on legacy loan portfolio

Delinquencies

Loans 30-89 days past due

Provision for loan losses

Down 68%

from peak

in Q4 08

Down 73%

from peak

In 3Q 08

$1,200

$1,000

$800

$600

$400

$200

$0

$600

$500

$400

$300

$200

$100

$0

($ B)

Loan Balance

9/30/07

(16)

Paydowns

(17)

Charge-offs

Loan Balance

9/30/12

(16)

Average age

1-4 Family loans

Home equity

Consumer

TOTAL

$17

$12

$3

$32

($10)

($5)

($2)

($17)

($1)

($3)

($0)

($4)

$6

$4

$1

$11

6.4 yrs

6.7 yrs

8.8 yrs

©

2012 E*TRADE Financial Corporation all rights reserved

16

66% decline

Untimely reported borrower

bankruptcies

Provision

Qualitative reserve |

©

2012 E*TRADE Financial Corporation all rights reserved

17

Coverage of non-modified loans

Coverage of modified loans

Components of allowance for loan losses

(18)

Continue to manage and de-risk the Bank

Mitigate credit losses on legacy loan portfolio

1.2

0.9

0.6

0.3

0.0

4Q 10

1Q 10

2Q 10

3Q 10

1Q 11

2Q 11

3Q 11

4Q 11

1Q 12

2Q 12

3Q 12

90+ days past due non-modified loans

General reserve as a % of 90+ days past due non-modified loans

Modified loans

Prior charge-offs

Total expected losses on modified loans

1.8

1.2

0.6

0.0

1.8

1.2

0.6

0.0

80%

60%

40%

20%

0%

80%

60%

40%

20%

0%

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

©

2012 E*TRADE Financial Corporation all rights reserved

17

(18)

General reserve

= Expected losses over next 12 months for non-modified loans

Specific Valuation Allowance

= Expected losses over remaining life of modified loans

Qualitative reserve

= Accounts for factors not directly considered in our quantitative model

(19) |

Continue to

manage and de-risk the Bank Optimize value of customer deposits

Average interest earning assets & net interest spread

Current drivers of net interest spread

1Q 10

2Q 10

3Q 10

4Q 10

1Q 11

2Q 11

3Q 11

4Q 11

1Q 12

2Q 12

3Q 12

$42.4

$41.0

$39.7

$41.5

$42.7

$42.9

$42.6

$42.7

$44.9

$44.8

$44.9

2.96%

2.89%

2.95%

2.88%

2.84%

2.89%

2.81%

2.66%

2.49%

2.44%

2.28%

©

2012 E*TRADE Financial Corporation all rights reserved

18

•

Deleveraging actions and resulting smaller balance sheet

•

Proactive and scheduled rundown of wholesale borrowings

•

Runoff of higher yielding legacy loan portfolio

•

Declining marginal reinvestment rate on agency securities |

•

Avg loan size: $461k

•

84% of non-TDR portfolio is

adjustable for rate or amortization

•

Over $2.7B has previously reset

Continue to manage and de-risk the Bank

Visibility into future drivers of net interest spread

•

Loan portfolio continues to run off at approximately 20%

per year

•

Nearly 90% of 1-4 family loans resetting in the remainder

of 2012 are expected to reset to a lower payment

•

Majority of home equity lines do not begin to amortize

until after 2015, and balances continue to decline

•

Hedges on wholesale funding channels require us to

continue issuing short-term debt for next several years

Average cost 3-4%

1-4 family mortgages

Home equity lines of credit

•

Avg loan size: $74K

(20)

•

Avg est increase at conversion:

$150-200/mo. payment

2011

and prior

2011

and prior

19

$0.01

$0.2

$0.2

$0.3

$0.8

$1.0

0%

20%

40%

60%

80%

100%

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

$2.4

2012

2013

2014

2015

2016

2017

payment resets by year

Prior first-time resets

First-time resets

% of total first

time resets

0.0

1.0

2.0

3.0

4.0

5.0

8.0

Wholesale funding obligations will

expire over next ten years

$0.2

0.09

$0.2

$0.2

$0.9

$1.4

$0.4

0%

20%

40%

60%

80%

100%

$0.0

$0.4

$0.8

$1.2

$1.6

2012

2013

2014

2015

2016

2017

I/O to amortizing conversions

Prior conversions

Conversions

% of total conversions

6.0

7.0

$

©

2012 E*TRADE Financial Corporation all rights reserved

$0.9

$1.8 |

•

Prolonged low interest rate environment

•

Home prices

•

Weak consumer / investor confidence

•

Heightened regulatory sensitivity

Environmental

Challenges

•

Mitigate credit losses on legacy loan portfolio

•

Improve capital structure

•

Complete regulatory transition to OCC & Fed

•

Build out enterprise risk management function

E*TRADE

Challenges

•

Accelerate growth of customer franchise

•

Expand brand as a trusted retirement and investing

provider

•

Cost reduction / efficiency gains

E*TRADE

Opportunities

Challenges and opportunities

©

2012 E*TRADE Financial Corporation all rights reserved

20 |

|

(1)

Excludes

impact

of

the

debt

exchange.

In

the

third

quarter

of

2009,

the

Company

exchanged

$1.7

billion

aggregate

principal

amount

of

interest-bearing

corporate

debt

for

an

equal

principal

amount of

newly-

issued

non-interest-bearing

convertible

debentures.

This

Debt

Exchange

resulted

in

a

non-cash

pre-tax

charge

of

$968

million.

The

following

table

provides

a

reconciliation

of

GAAP

net loss

to

non-

GAAP

net

loss

for

FY2009:

Appendix

(a)

Under

the

regulatory

guidelines

for

risk-based

capital,

on-balance

sheet

assets

and

credit

equivalent

amounts

of

derivatives

and

off-balance

sheet

items

are

assigned

to

one

of

several

broad

risk

categories

according

to

the

obligor

or,

if

relevant,

the

guarantor

or

the

nature

of

any

collateral.

The

aggregate

dollar

amount

in

each

risk

category

is

then

multiplied

by

the

risk

weight

associated

with

that

category.

The

resulting

weighted

values

from

each

of

the

risk

categories

are

aggregated

for

determining

total

risk-weighted

assets.

($000s)

FY 2009

Pre-tax loss

(1,835,431)

$

Add back: non-cash charge on Debt Exchange

968,254

Adjusted pre-tax loss

(867,177)

$

Q3 2012

Shareholders' equity

5,093.9

$

DEDUCT:

Losses in OCI on AFS debt securities and cash flow hedges, net of tax

(307.6)

Goodwill and other intangible assets, net of deferred tax liabilities

1,897.6

ADD:

Qualifying restricted core capital elements (TRUPs)

433.0

Subtotal

3,936.9

DEDUCT:

Disallowed servicing assets and deferred tax assets

1,259.1

Tier 1 capital

2,677.8

ADD:

Allowable allowance for loan losses

261.6

Total capital

2,939.4

$

Total average assets

49,400.8

$

DEDUCT:

Goodwill and other intangible assets, net of deferred tax liabilities

1,897.6

Subtotal

47,503.2

DEDUCT:

Disallowed servicing assets and deferred tax assets

1,259.1

Average total assets for leverage capital purposes

46,244.1

$

Total risk-weighted assets

(a)

20,614.9

$

Tier 1 leverage ratio (Tier 1 capital / Average total assets for

leverage

capital purposes)

5.8%

Tier 1 capital / Total risk-weighted assets

13.0%

Total capital / Total risk-weighted assets

14.3%

22

(2)

The

parent

total

capital

to

risk-weighted

assets,

Tier

1

capital

to

risk-weighted

assets

and

Tier

1

leverage

capital

ratios

are

based

on

the

Federal

Reserve

regulatory

minimum

well-capitalized

threshold,

although

the

parent

is

not

currently

subject

to

capital

requirements.

See

the

below

table

(dollars

in

millions)

and

the

Company’s

Form

10-Q

filed

November

1,

2012

for

a

reconciliation

of

those

non-

GAAP

measures

to

the

comparable

GAAP

measures.

©

2012 E*TRADE Financial Corporation all rights reserved

|

Appendix

(3)

The

parent

Tier

1

common

ratio

is

Tier

1

capital

less

elements

of

Tier

1

capital

that

are

not

in

the

form

of

common

equity,

such

as

trust

preferred

securities,

divided

by

total

risk-weighted

assets

for

the

holding

company.

The

holding

company

is

not

yet

held

to

the

capital

requirements;

as

such,

the

7.0%

well-capitalized

threshold

is

not

based

on

regulatory

guidance.

See

below

table

(dollars

in

millions)

and

the

Company’s

Form

10-Q

filed

November

1,

2012

for

a

reconciliation

of

the

non-GAAP

measure

of

Tier

1

common

ratio

to

the

comparable

GAAP

measure.

(4)

Excess

to

regulatory

well

capitalized

minimums.

Debt

outstanding

does

not

include

the

Company’s

new

notes

issued

subsequent

to

3Q

2012

quarter-end.

(5)

Strategic

and

Capital

Plan

composed

of

the

Company’s

assumptions

and

targets.

Any

capital

distributions

would

be

subject

to

regulatory

approval

at

that

time.

(6)

Approximately

$1

billion

in

customer

payables

balances

have

received

regulatory

approval

for

conversion

to

money

funds,

with

approximately

$900M

scheduled

for

completion

during

Q4

2012

and

the

remainder

scheduled

during

Q1

2013.

(7)

Schedule

and

estimated

improvement

to

earnings

is

for

illustrative

purposes

and

does

not

attempt

to

forecast

future

tax

rates.

Therefore,

it

assumes

a

general

corporate

effective

tax

rate

of

38%.

The

GAAP

interest

expense

column

includes

stated

cash

interest

expense

on

the

notes,

as

well

as

2013

scheduled

amortization

of

the

original

issue

discount

on

the

12.5%

Springing

Lien

Notes

due

2017.

The

after-tax

row

accounts

for

the

non-deductibility

of

a

portion

of

the

interest

expense

on

the

2017

notes.

(8)

Assumes

tax

rate

of

38%.

(9)

E*TRADE

Securities

ratings

for

Online

Broker

by

SmartMoney

Magazine,

May

2012

Broker

Survey,

based

on

the

following

categories:

Trading

Tools

(5

stars),

Customer

Service

(4

stars),

Banking

Services

(4

stars),

Mutual

Funds

&

Investment

Products

(4

stars),

Research

(5

stars),

and

Commissions

and

Fees

(2

stars).

SmartMoney

is

a

registered

trademark,

a

joint

publishing

venture

between

Dow

Jones

&

Company,

Inc.

and

Hearst

SM

Partnership.

(10)

E*TRADE

Securities

ratings

for

Barron's

annual

ranking

of

the

Best

Online

Brokers

(March

12,

2012),

based

on

Trade

Experience

and

Technology,

Usability,

Mobile,

Range

of

Offerings,

Research

Amenities,

Portfolio

Analysis

&

Reports,

Customer

Service

&

Education

and

Costs.

E*TRADE

overall

ranked

#10.

(11)

E*TRADE

Securities

ratings

for

Online

Broker

by

Kiplinger

Personal

Finance,

November

2012

Online

Broker

Survey,

based

on

the

following

categories:

Investment

Choices

(5

stars),

Customer

Service

(5

stars),

User

Experience(4.5

stars),

Research

and

Tools

(4

stars),

Banking

(3.5

stars),

and

Fees

&

Commissions

(2.5

stars).

©

2012

The

Kiplinger

Washington

Editors.

All

rights

reserved.

(12)

The

attrition

rate

is

calculated

by

dividing

attriting

(a)

brokerage

accounts,

by

total

brokerage

accounts,

for

the

previous

period

end.

This

measure

is

presented

annually

and

on

an

annualized

basis

(where

it

appears

quarterly).

(a)

Attriting

brokerage

accounts:

Gross

new

brokerage

accounts,

less

net

new

brokerage

accounts.

(13)

The

net

new

brokerage

assets

metrics

treat

asset

flows

between

E*TRADE

entities

in

the

same

manner

as

unrelated

third

party

accounts.

(14)

Average

brokerage

assets

per

account

is

calculated

as

the

sum

of

security

holdings

and

brokerage

related

cash

divided

by

end

of

period

brokerage

accounts.

23

Q3 2012

Shareholders' equity

5,093.9

$

DEDUCT:

Losses in OCI on AFS debt securities and cash flow hedges, net of tax

(307.6)

Goodwill and other intangible assets, net of deferred tax liabilities

1,897.6

Subtotal

3,503.9

DEDUCT:

Disallowed servicing assets and deferred tax assets

1,259.1

Tier 1 common

2,244.8

$

Total risk-weighted assets

20,614.9

$

Tier 1 common ratio (Tier 1 common / Total risk-weighted assets)

10.9%

©

2012 E*TRADE Financial Corporation all rights reserved

|

Appendix

(15) Based on data as of 6/30/12.

(16) Represents unpaid principal balances.

(17)

(18) Increased the qualitative reserve in Q4 2011 in anticipation of losses related to a

review of modification policies and practices pursuant to regulatory transition. Review was completed in Q1 2012:

Certain modified loans were charged-off against previously established SVA and the

qualitative reserve. (19) The total expected losses on TDRs includes both the

previously recorded charge-offs and the specific valuation allowance. (20) Excludes

$0 balance home equity lines of credit. 24

©

2012 E*TRADE Financial Corporation all rights reserved

Net paydowns includes paydowns on loans as well as limited origination activity, home equity

advances, repurchase activity, limited sale and securitization activities and transfers to real estate owned

assets. |