Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - E TRADE FINANCIAL CORP | etfc-2017930xex321.htm |

| EX-31.2 - EXHIBIT 31.2 - E TRADE FINANCIAL CORP | etfc-2017930xex312.htm |

| EX-31.1 - EXHIBIT 31.1 - E TRADE FINANCIAL CORP | etfc-2017930xex311.htm |

| EX-10.1 - EXHIBIT 10.1 - E TRADE FINANCIAL CORP | etfc-2017930xex101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________

FORM 10-Q

______________________________________

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2017

Commission File Number 1-11921

________________________________

E TRADE Financial Corporation

TRADE Financial Corporation

TRADE Financial Corporation(Exact Name of Registrant as Specified in its Charter)

______________________________________________

Delaware | 94-2844166 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

11 Times Square, 32nd Floor, New York, New York 10036

(Address of principal executive offices and Zip Code)

(646) 521-4300

(Registrant’s telephone number, including area code)

_____________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer | ¨ | |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |

Emerging growth company ¨ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

As of October 31, 2017, there were 269,659,766 shares of common stock outstanding.

E*TRADE FINANCIAL CORPORATION

FORM 10-Q QUARTERLY REPORT

For the Quarter Ended September 30, 2017

TABLE OF CONTENTS

PART I | FINANCIAL INFORMATION | |

Item 1. | ||

Condensed Consolidated Statement of Income | ||

Condensed Consolidated Balance Sheet | ||

Condensed Consolidated Statement of Cash Flows | ||

Notes to Condensed Consolidated Financial Statements (Unaudited) | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

E*TRADE | Q3 2017 10-Q | i | |

Unless otherwise indicated, references to "the Company," "we," "us," "our," "E*TRADE" and "E*TRADE Financial" mean E*TRADE Financial Corporation and its subsidiaries, and references to the parent company mean E*TRADE Financial Corporation but not its subsidiaries.

E*TRADE, E*TRADE Financial, E*TRADE Bank, the Converging Arrows logo and OptionsHouse are registered trademarks of E*TRADE Financial Corporation in the United States and in other countries.

E*TRADE | Q3 2017 10-Q | ii | |

PART I

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. These statements discuss, among other things, our future plans, objectives, outlook, strategies, expectations and intentions relating to our business and future financial and operating results and the assumptions that underlie these matters and include statements regarding the Company's proposed transaction with Trust Company of America (TCA) and its benefits and timing, our business strategy, objectives and vision; our plans and ability to deliver new products and solutions; our ability to improve client acquisition and deepen relationships with existing clients; our ability to effectively monetize brokerage relationships by investing in agency mortgage-backed securities; our capital plan initiatives, the expected balance sheet size, any balance sheet growth and the incremental regulatory and reporting requirements that our balance sheet size and growth may require; our plans to run off our legacy mortgage and consumer loan portfolio; repurchases of our common stock, payment of dividends on our preferred stock; our ability to maintain required regulatory capital ratios; our plans for the payment of dividends from our subsidiaries to our parent company; proposed issuance of preferred stock and the expected financing of the proposed transaction; our target liquidity positions; our ability to identify and manage risks appropriately; and any other statement that is not historical in nature. These statements may be identified by the use of words such as "assume," "expect," "believe," "may," "will," "should," "anticipate," "intend," "plan," "estimate," "continue" and similar expressions. We caution that actual results could differ materially from those discussed in these forward-looking statements. Important factors that could contribute to our actual results differing materially from any forward-looking statements include, but are not limited to, the closing of the proposed transaction with TCA may not occur or may be delayed, regulatory risks associated with the transaction, unanticipated restructuring costs which may be incurred or undisclosed liabilities assumed, attempts to retain key TCA personnel may not succeed, expected synergies and other financial benefits may not be realized or integration plans may not be implemented as anticipated; changes in business, economic or political condition; performance, volume and volatility in the equity and capital markets; fluctuations in interest rates; customer demand for financial products and services; increased competition; cyber security threats, potential system disruptions and other security breaches; our ability to participate in consolidation opportunities in our industry; our ability to service our corporate debt; changes in government regulation or actions by our regulators; our ability to move capital to our parent company from our subsidiaries; adverse developments in litigation or regulatory matters; the timing and duration of, and the amount of shares repurchased and amount of cash expended in connection with, the share repurchase program; the availability, timing and size of any preferred stock issuance; and other factors discussed under Part II. Item 1A. Risk Factors and Part I. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Form 10-Q; and Part I. Item 1A. Risk Factors of our Annual Report on Form 10-K for the year ended December 31, 2016, filed with the Securities and Exchange Commission (SEC), which are incorporated herein by reference. By their nature forward-looking statements are not guarantees of future performance or results and are subject to risks, uncertainties and assumptions that are difficult to predict or quantify. Actual future results may vary materially from expectations expressed or implied in this report or any of our prior communications. The forward-looking statements contained in this report reflect our expectations only as of the date of this report. You should not place undue reliance on forward-looking statements, as we do not undertake to update or revise forward-looking statements to reflect the impact of circumstances or events that arise after the date the forward-looking statements were made, except as required by law.

E*TRADE | Q3 2017 10-Q | 1 | |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the consolidated financial statements and the related notes that appear elsewhere in this document and with the Annual Report on Form 10-K for the year ended December 31, 2016.

OVERVIEW

Company Overview

E*TRADE is a financial services company that provides online brokerage and related products and services primarily to individual retail investors. Our mission is to enhance the financial independence of traders and investors through a powerful digital offering and professional guidance. Our vision is to be the #1 digital broker and advisor to traders and investors, known for ease of use and the completeness of our offering.

Strategy

Our business strategy is centered on two key objectives: accelerating the growth of our core brokerage business to drive organic growth and improve competitive position, and generating robust earnings growth and healthy returns on capital to deliver long-term value for our stakeholders.

Accelerate Growth of Core Brokerage Business

• | Enhance overall customer experience |

We are focused on delivering cutting-edge trading solutions while improving our market position in investing products. Through these offerings, we aim to drive customer acquisition while deepening engagement with our existing customers.

• | Capitalize on value of corporate services channel |

We leverage our industry-leading position in corporate stock plan administration to improve client acquisition and engage with plan participants to bolster awareness of our full suite of offerings. Our corporate services channel is a strategically important driver of brokerage account and asset growth.

Generate Robust Earnings Growth and Healthy Returns on Capital

• | Utilize balance sheet to enhance returns |

We utilize our bank structure to effectively monetize brokerage relationships by investing stable, low-cost deposits primarily in agency mortgage-backed securities.

• | Put capital to work for shareholders |

We have put significant capital to work through balance sheet growth, share repurchases and acquisition activity. We are focused on generating and effectively deploying capital for the benefit of our shareholders.

Financial Performance

Our net revenue is generated primarily from net interest income, commissions and fees and service charges. Net interest income is largely impacted by the size of our balance sheet, our balance sheet mix, and average yields on our assets and liabilities. Net interest income is driven primarily from interest earned on investment securities and margin receivables, less interest paid on interest-bearing liabilities, including deposits, customer

E*TRADE | Q3 2017 10-Q | 2 | |

payables, corporate debt and other borrowings. Net interest income is also earned on our legacy mortgage and consumer loan portfolio which we expect to continue to run off in future periods. Commissions revenue is generated by customer trades and is largely impacted by trade volume and commission rates. Fees and service charges revenue is mainly impacted by order flow revenue, fees earned on off-balance sheet customer cash and other assets, and advisor management fees. Our net revenue is offset by non-interest expenses, the largest of which are compensation and benefits and advertising and market development.

Significant Events in the Third Quarter of 2017

Announced Trust Company of America acquisition

On October 19, 2017, we announced an agreement to acquire Trust Company of America, Inc. (TCA), a leading provider of technology solutions and custody services to the registered investment adviser market, for $275 million in cash. We anticipate funding the transaction through the issuance of non-cumulative perpetual preferred stock. The acquisition is expected to close in the second quarter of 2018, subject to customary closing conditions and regulatory approvals.

Completed OptionsHouse integration

In August 2017, we completed the integration of Aperture, LLC (dba OptionsHouse), which was acquired by the Company in 2016. Completion of the integration included the rollout of OptionsHouse features and functionality through E*TRADE.com and the transfer of retail brokerage accounts and customer-related balances of OptionsHouse to E*TRADE Securities LLC (E*TRADE Securities). Futures accounts and balances of E*TRADE Securities were transferred to E*TRADE Futures LLC (formerly known as Aperture, LLC).

Issued $1 billion of senior notes and redeemed higher cost corporate debt

We issued $600 million of 2.95% Senior Notes and $400 million of 3.80% Senior Notes and used the net proceeds, along with existing corporate cash, to redeem our outstanding $540 million of 5.375% Senior Notes and $460 million of 4.625% Senior Notes, resulting in a $58 million loss on early extinguishment of debt. This transaction reduces our annual corporate debt service costs from $50 million to $33 million.

Repurchased 4.6 million shares of our common stock

We continue to execute on our stock repurchase plan, under which the Board of Directors has authorized a $1 billion repurchase of shares of our common stock. During the three months ended September 30, 2017, the Company repurchased 4.6 million shares of common stock at an average price of $40.64 for a total of $187 million. As of September 30, 2017, $813 million remained available for additional repurchases. As of October 31, 2017, we have subsequently repurchased an additional 1.0 million shares of common stock at an average price of $43.53.

E*TRADE | Q3 2017 10-Q | 3 | |

Key Performance Metrics

Management monitors a number of customer activity and company metrics to evaluate the Company’s performance. The most significant of these are displayed below along with the percentage variance for the three months ended September 30, 2017 from the same period in 2016, where applicable, and includes OptionsHouse from the September 12, 2016 acquisition date.

Customer Activity Metrics:

E*TRADE | Q3 2017 10-Q | 4 | |

| ||

| ||

E*TRADE | Q3 2017 10-Q | 5 | |

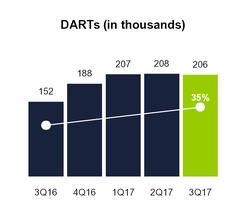

Daily Average Revenue Trades (DARTs) is the predominant driver of commissions revenue from our customers. DARTs were 205,763 and 207,065 for the three and nine months ended September 30, 2017, respectively, compared to 151,905 and 156,368 for the same periods in 2016.

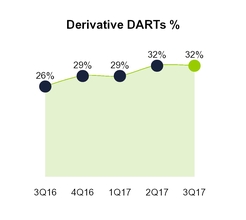

Derivative DARTs percentage is the mix of options and futures as a component of total DARTs and is a key driver of commissions revenue. Derivative DARTs represented 32% and 31% of total DARTs for the three and nine months ended September 30, 2017, respectively, compared to 26% and 25% for the same periods in 2016.

Average commission per trade is an indicator of changes in our customer mix, product mix and/or product pricing. Average commission per trade was $7.76 and $8.54 for the three and nine months ended September 30, 2017, respectively, compared to $10.97 and $10.81 for the same periods in 2016. Average commission per trade for the three and nine months ended September 30, 2017 was impacted by our reduced commission rates for equity and options trades effective March 13, 2017, which were as follows:

• | Stock, options and exchange-traded fund (ETF) trade commissions reduced to $6.95 from $9.99 |

• | For active traders, commissions reduced to $4.95 from $7.99 and options charges reduced to $0.50 per contract from $0.75; trades required for active trader tier reduced to 30 per quarter from 150 |

Customer margin balances represents credit extended to customers to finance their purchases of securities by borrowing against securities they own and is a key driver of net interest income. Customer margin balances were $8.5 billion and $6.8 billion at September 30, 2017 and 2016, respectively. Customer margin for periods prior to September 30, 2017, includes OptionsHouse balances which were held by a third party clearing firm. In connection with the integration of OptionsHouse, $0.4 billion of customer margin held by the third party clearing firm was transferred to our balance sheet and is reflected as margin receivables at September 30, 2017.

Managed products represents customer assets in our Managed Investment Portfolio, Unified Managed Account, Adaptive Portfolio, and Fixed Income Separately Managed Account products. Managed products are a driver of fees and service charges revenue. Managed products were $4.9 billion and $3.7 billion at September 30, 2017 and 2016, respectively.

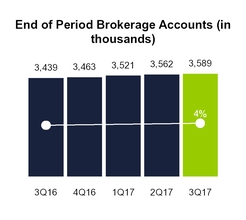

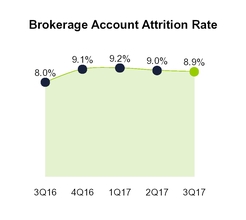

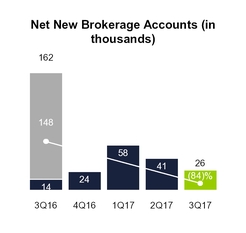

End of period brokerage accounts, net new brokerage accounts and brokerage account attrition rate are indicators of our ability to attract and retain brokerage customers. End of period brokerage accounts were 3.6 million and 3.4 million at September 30, 2017 and 2016, respectively. Net new brokerage accounts were 26,225 and 125,711 for the three and nine months ended September 30, 2017, respectively, and 161,885 and 225,434 for the same periods in 2016. Our annualized brokerage account attrition rate was 8.9% and 9.1% for the three and nine months ended September 30, 2017, respectively, compared to 8.0% and 8.1% for the same periods in 2016. During the three and nine months ended September 30, 2017, our annualized net new brokerage account growth rate was 2.9% and 4.8% respectively, compared to 1.7% and 3.2% for the same periods in 2016. End of period brokerage accounts and net new brokerage accounts for the three months ended September 30, 2016 include 147,761 accounts from the OptionsHouse acquisition.

Customer assets is an indicator of the value of our relationship with the customer. An increase generally indicates that the use of our products and services by existing and new customers is expanding. Changes in this metric are also driven by changes in the valuations of our customers' underlying securities. Customer assets were $365.3 billion and $306.8 billion at September 30, 2017 and 2016, respectively.

Net new brokerage assets is total inflows to new and existing brokerage accounts less total outflows from closed and existing brokerage accounts. The net new brokerage assets metric is a general indicator of the use of our products and services by new and existing brokerage customers. Net new brokerage assets were $2.2 billion and $9.0 billion for the three and nine months ended September 30, 2017, respectively, compared to $5.4 billion and $9.9 billion for the same periods in 2016. During the three and nine months ended September 30, 2017, our annualized net new brokerage asset growth rate was 2.9% and 4.4%, respectively, compared to 2.7% and 3.4% for the same periods in 2016. Net new brokerage assets for the three months ended September 30, 2016 includes $3.7 billion from the OptionsHouse acquisition.

E*TRADE | Q3 2017 10-Q | 6 | |

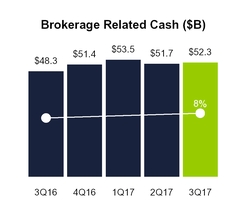

Brokerage related cash is an indicator of the level of engagement with our brokerage customers and is a key driver of net interest income as well as fees and service charges revenue, which includes fees earned on customer cash held by third parties. Brokerage related cash was $52.3 billion and $48.3 billion at September 30, 2017 and 2016, respectively.

Company Metrics:

E*TRADE | Q3 2017 10-Q | 7 | |

Operating margin is the percentage of net revenue that results in income before income taxes and is an indicator of the Company's profitability. Operating margin was 37% and 44% for the three and nine months ended September 30, 2017, respectively, compared to 46% and 44% for the same periods in 2016.

Adjusted operating margin is a non-GAAP measure that provides useful information about our ongoing operating performance by excluding the provision (benefit) for loan losses and losses on early extinguishment of debt, which are not viewed as key factors governing our investment in the business and are excluded by management when evaluating operating margin performance. Adjusted operating margin was 42% and 39% for the three and nine months ended September 30, 2017, respectively, compared to 34% and 35% for the same periods in 2016. See Earnings Overview for a reconciliation of this non-GAAP measure to the most directly comparable GAAP measure.

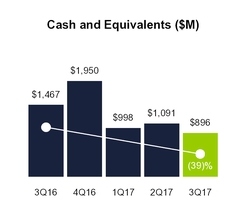

Corporate cash, a non-GAAP measure, is a component of cash and equivalents and represents the primary source of capital above and beyond the capital deployed in our regulated subsidiaries. Corporate cash was $309 million and $306 million at September 30, 2017 and 2016, respectively, while cash and equivalents was $896 million and $1.5 billion for the same periods. See Liquidity and Capital Resources for a reconciliation of corporate cash to cash and equivalents.

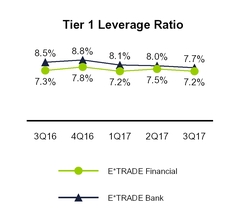

Tier 1 leverage ratio is an indicator of capital adequacy for E*TRADE Financial and E*TRADE Bank. Tier 1 leverage ratio is Tier 1 capital divided by adjusted average assets for leverage capital purposes. E*TRADE Financial's Tier 1 leverage ratio was 7.2% and 7.3% at September 30, 2017 and 2016, respectively. E*TRADE Bank's Tier 1 leverage ratio was 7.7% and 8.5% at September 30, 2017 and 2016, respectively. See Liquidity and Capital Resources for additional information, including the calculation of regulatory capital ratios.

Allowance for loan losses is an estimate of probable losses inherent in the loan portfolio as of the balance sheet date, as well as the forecasted losses, including economic concessions to borrowers, over the estimated remaining life of loans modified as troubled debt restructurings (TDRs). Allowance for loan losses was $94 million and $235 million at September 30, 2017 and 2016, respectively.

Interest-earning assets, along with net interest margin, is an indicator of our ability to generate net interest income. Average interest-earning assets were $54.8 billion and $51.8 billion for the three and nine months ended September 30, 2017, respectively, compared to $44.5 billion and $42.9 billion for the same periods in 2016.

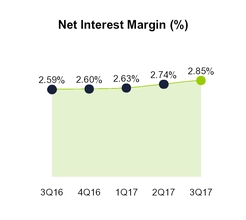

Net interest margin is a measure of the net yield on our average interest-earning assets. Net interest margin is calculated for a given period by dividing the annualized sum of net interest income by average interest-earning assets. Net interest margin was 2.85% and 2.74% for the three and nine months ended September 30, 2017, respectively, compared to 2.59% and 2.67% for the same periods in 2016.

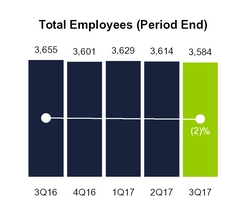

Total employees were 3,584 and 3,655 at September 30, 2017 and 2016, respectively.

E*TRADE | Q3 2017 10-Q | 8 | |

Regulatory Developments

In April 2016, the U.S. Department of Labor published its final fiduciary regulations under the Employee Retirement Income Security Act of 1974 and the Internal Revenue Code of 1986. Certain aspects of these regulations began to take effect in June 2017. These regulations generally subject particular persons, such as broker-dealers and other financial advisers providing investment advice to individual retirement accounts and other qualified retirement plans and accounts, to fiduciary duties and additional regulatory restrictions for a wider range of customer interactions. The remaining aspects of these regulations are currently scheduled to take effect on January 1, 2018. During this transition period, the Department of Labor indicated in Field Assistance Bulletin 2017-02 issued in May 2017, that it will not take enforcement actions against impacted parties that are in reasonable compliance with the regulations. The Company is in the process of implementing the remaining applicable components for compliance.

The Company has historically not been subject to certain regulatory requirements that apply to banking organizations with $50 billion or more in total consolidated assets as defined by each applicable regulation. Total consolidated assets of $50 billion, which is measured in accordance with each applicable regulation, but generally on the basis of the average of the four most recent quarters, is a meaningful regulatory threshold as U.S. banking organizations become subject to a number of additional and, in some cases, more stringent regulatory requirements once they reach that size. The Company surpassed $50 billion in total consolidated assets on a four quarter average in the first quarter of 2017.

The Company expects these regulatory requirements, not all of which have been finalized, to start becoming applicable to it in 2018. The Company has begun implementing policies, procedures, systems and governance structures that are designed to comply with the requirements. Additionally, while savings and loan holding companies are currently excluded from the scope of certain regulations that apply to bank holding companies, the Company expects it will ultimately be subject to these requirements. For additional information see Part I. Item 1. Business of our Annual Report on Form 10-K for the year ended December 31, 2016.

E*TRADE | Q3 2017 10-Q | 9 | |

EARNINGS OVERVIEW

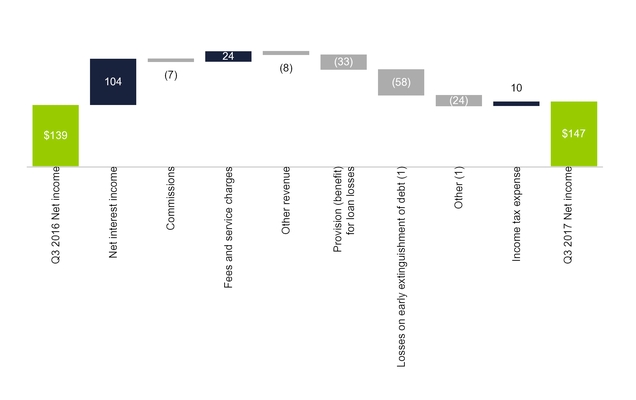

We generated net income of $147 million and $485 million on total net revenue of $599 million and $1.7 billion for the three and nine months ended September 30, 2017, respectively. The following chart provides a reconciliation of net income for the three months ended September 30, 2016 to net income for the three months ended September 30, 2017 (dollars in millions):

(1) | Total non-interest expense increased $82 million for the periods presented which includes $58 million of losses on early extinguishment of debt. |

E*TRADE | Q3 2017 10-Q | 10 | |

The significant components of the consolidated statement of income are as follows (dollars in millions except per share amounts):

Three Months Ended September 30, | Variance | Nine Months Ended September 30, | Variance | ||||||||||||||||||||||||||

2017 vs. 2016 | 2017 vs. 2016 | ||||||||||||||||||||||||||||

2017 | 2016 | Amount | % | 2017 | 2016 | Amount | % | ||||||||||||||||||||||

Net interest income | $ | 391 | $ | 287 | $ | 104 | 36 | % | $ | 1,066 | $ | 860 | $ | 206 | 24 | % | |||||||||||||

Total non-interest income | 208 | 199 | 9 | 5 | % | 663 | 572 | 91 | 16 | % | |||||||||||||||||||

Total net revenue | 599 | 486 | 113 | 23 | % | 1,729 | 1,432 | 297 | 21 | % | |||||||||||||||||||

Provision (benefit) for loan losses | (29 | ) | (62 | ) | 33 | (53 | )% | (142 | ) | (131 | ) | (11 | ) | 8 | % | ||||||||||||||

Total non-interest expense | 405 | 323 | 82 | 25 | % | 1,106 | 930 | 176 | 19 | % | |||||||||||||||||||

Income before income tax expense | 223 | 225 | (2 | ) | (1 | )% | 765 | 633 | 132 | 21 | % | ||||||||||||||||||

Income tax expense | 76 | 86 | (10 | ) | (12 | )% | 280 | 208 | 72 | 35 | % | ||||||||||||||||||

Net income | $ | 147 | $ | 139 | $ | 8 | 6 | % | $ | 485 | $ | 425 | $ | 60 | 14 | % | |||||||||||||

Preferred stock dividends | 12 | — | 12 | 100 | % | 25 | — | 25 | 100 | % | |||||||||||||||||||

Net income available to common shareholders | $ | 135 | $ | 139 | $ | (4 | ) | (3 | )% | $ | 460 | $ | 425 | $ | 35 | 8 | % | ||||||||||||

Diluted earnings per common share | $ | 0.49 | $ | 0.51 | $ | (0.02 | ) | (4 | )% | $ | 1.67 | $ | 1.52 | $ | 0.15 | 10 | % | ||||||||||||

Net income increased 6% to $147 million and 14% to $485 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. Net income available to common shareholders was $135 million and $460 million for the three and nine months ended September 30, 2017, respectively, which reflects payments of $12 million and $25 million in preferred stock dividends, respectively, compared to net income available to common shareholders of $139 million and $425 million during the same periods in 2016. The increase in net income for both periods in 2017 was driven by higher interest income due to a larger balance sheet and higher interest rates, as well as higher fees and service charges revenue. We recognized a benefit for loan losses of $29 million and $142 million for the three and nine months ended September 30, 2017, respectively, compared to $62 million and $131 million for the same periods in 2016. Net income for the three and nine months ended September 30, 2017 also included $11 million and $27 million, respectively, of pre-tax costs primarily incurred in connection with the OptionsHouse integration and preparation for the incremental regulatory and reporting requirements that our balance sheet growth requires, as well as pre-tax losses on early extinguishment of debt of $58 million. Non-interest expense for the three and nine months ended September 30, 2017 also included higher advertising and market development expenses driven by our new advertising campaign, as well as increased communications expense. These expenses were partially offset by lower restructuring and acquisition-related activities and an income tax benefit related to the revaluation of certain net state deferred tax assets. Net income for the nine months ended September 30, 2016 included an income tax benefit related to the release of a valuation allowance against certain state deferred tax assets.

E*TRADE | Q3 2017 10-Q | 11 | |

Net Revenue

The components of net revenue and the resulting variances are as follows (dollars in millions):

Three Months Ended September 30, | Variance | Nine Months Ended September 30, | Variance | ||||||||||||||||||||||||||

2017 vs. 2016 | 2017 vs. 2016 | ||||||||||||||||||||||||||||

2017 | 2016 | Amount | % | 2017 | 2016 | Amount | % | ||||||||||||||||||||||

Net interest income | $ | 391 | $ | 287 | $ | 104 | 36 | % | $ | 1,066 | $ | 860 | $ | 206 | 24 | % | |||||||||||||

Commissions | 100 | 107 | (7 | ) | (7 | )% | 332 | 320 | 12 | 4 | % | ||||||||||||||||||

Fees and service charges | 92 | 68 | 24 | 35 | % | 276 | 188 | 88 | 47 | % | |||||||||||||||||||

Gains on securities and other, net | 6 | 14 | (8 | ) | (57 | )% | 23 | 34 | (11 | ) | (32 | )% | |||||||||||||||||

Other revenue | 10 | 10 | — | — | % | 32 | 30 | 2 | 7 | % | |||||||||||||||||||

Total non-interest income | 208 | 199 | 9 | 5 | % | 663 | 572 | 91 | 16 | % | |||||||||||||||||||

Total net revenue | $ | 599 | $ | 486 | $ | 113 | 23 | % | $ | 1,729 | $ | 1,432 | $ | 297 | 21 | % | |||||||||||||

Net Interest Income

Net interest income increased 36% to $391 million and 24% to $1.1 billion for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. Net interest income is earned primarily through investment securities, margin receivables and our legacy mortgage and consumer loan portfolio, offset by funding costs.

E*TRADE | Q3 2017 10-Q | 12 | |

The following table presents average balance sheet data and interest income and expense data, as well as the related net interest margin, yields and rates prepared on the basis required by the SEC’s Industry Guide 3, "Statistical Disclosure by Bank Holding Companies" (dollars in millions):

Three Months Ended September 30, | |||||||||||||||||||||

2017 | 2016 | ||||||||||||||||||||

Average Balance | Interest Inc./Exp. | Average Yield/ Cost | Average Balance | Interest Inc./Exp. | Average Yield/ Cost | ||||||||||||||||

Cash and equivalents | $ | 905 | $ | 2 | 1.06 | % | $ | 1,989 | $ | 2 | 0.42 | % | |||||||||

Cash required to be segregated under federal or other regulations | 759 | 3 | 1.26 | % | 1,885 | 2 | 0.33 | % | |||||||||||||

Available-for-sale securities | 19,064 | 102 | 2.13 | % | 13,301 | 66 | 1.99 | % | |||||||||||||

Held-to-maturity securities | 22,162 | 153 | 2.77 | % | 15,937 | 109 | 2.73 | % | |||||||||||||

Margin receivables | 8,096 | 87 | 4.26 | % | 6,479 | 60 | 3.68 | % | |||||||||||||

Loans (1) | 3,024 | 37 | 4.95 | % | 4,202 | 46 | 4.44 | % | |||||||||||||

Broker-related receivables and other | 829 | 1 | 0.45 | % | 696 | — | 0.13 | % | |||||||||||||

Subtotal interest-earning assets | 54,839 | 385 | 2.80 | % | 44,489 | 285 | 2.56 | % | |||||||||||||

Other interest revenue (2) | — | 28 | — | 24 | |||||||||||||||||

Total interest-earning assets | 54,839 | 413 | 3.01 | % | 44,489 | 309 | 2.77 | % | |||||||||||||

Total non-interest-earning assets (3) | 4,952 | 4,793 | |||||||||||||||||||

Total assets | $ | 59,791 | $ | 49,282 | |||||||||||||||||

Deposits | $ | 40,758 | $ | 1 | 0.01 | % | $ | 32,285 | $ | 1 | 0.01 | % | |||||||||

Customer payables | 8,463 | 1 | 0.06 | % | 7,592 | 2 | 0.06 | % | |||||||||||||

Broker-related payables and other | 1,301 | — | 0.00 | % | 1,258 | — | 0.00 | % | |||||||||||||

Other borrowings | 831 | 6 | 2.91 | % | 409 | 4 | 4.15 | % | |||||||||||||

Corporate debt | 1,002 | 12 | 4.64 | % | 993 | 13 | 5.40 | % | |||||||||||||

Subtotal interest-bearing liabilities | 52,355 | 20 | 0.15 | % | 42,537 | 20 | 0.19 | % | |||||||||||||

Other interest expense (4) | — | 2 | — | 2 | |||||||||||||||||

Total interest-bearing liabilities | 52,355 | 22 | 0.17 | % | 42,537 | 22 | 0.20 | % | |||||||||||||

Total non-interest-bearing liabilities | 820 | 719 | |||||||||||||||||||

Total liabilities | 53,175 | 43,256 | |||||||||||||||||||

Total shareholders' equity | 6,616 | 6,026 | |||||||||||||||||||

Total liabilities and shareholders' equity | $ | 59,791 | $ | 49,282 | |||||||||||||||||

Excess interest earning assets over interest bearing liabilities/net interest income/net interest margin | $ | 2,484 | $ | 391 | 2.85 | % | $ | 1,952 | $ | 287 | 2.59 | % | |||||||||

(1) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

(2) | Represents interest income on securities loaned. |

(3) | Non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate interest income. |

(4) | Represents interest expense on securities borrowed. |

E*TRADE | Q3 2017 10-Q | 13 | |

Nine Months Ended September 30, | |||||||||||||||||||||

2017 | 2016 | ||||||||||||||||||||

Average Balance | Interest Inc./Exp. | Average Yield/ Cost | Average Balance | Interest Inc./Exp. | Average Yield/ Cost | ||||||||||||||||

Cash and equivalents | $ | 1,045 | $ | 6 | 0.83 | % | $ | 1,730 | $ | 5 | 0.40 | % | |||||||||

Cash required to be segregated under federal or other regulations | 1,263 | 9 | 0.90 | % | 1,540 | 4 | 0.33 | % | |||||||||||||

Available-for-sale securities | 17,958 | 282 | 2.09 | % | 13,149 | 198 | 2.01 | % | |||||||||||||

Held-to-maturity securities | 19,823 | 410 | 2.76 | % | 14,993 | 319 | 2.84 | % | |||||||||||||

Margin receivables | 7,383 | 228 | 4.12 | % | 6,553 | 185 | 3.77 | % | |||||||||||||

Loans (1) | 3,319 | 121 | 4.86 | % | 4,505 | 146 | 4.33 | % | |||||||||||||

Broker-related receivables and other | 1,029 | 2 | 0.24 | % | 470 | 1 | 0.21 | % | |||||||||||||

Subtotal interest-earning assets | 51,820 | 1,058 | 2.72 | % | 42,940 | 858 | 2.67 | % | |||||||||||||

Other interest revenue (2) | — | 74 | — | 65 | |||||||||||||||||

Total interest-earning assets | 51,820 | 1,132 | 2.91 | % | 42,940 | 923 | 2.87 | % | |||||||||||||

Total non-interest-earning assets (3) | 5,051 | 4,882 | |||||||||||||||||||

Total assets | $ | 56,871 | $ | 47,822 | |||||||||||||||||

Deposits | $ | 37,862 | $ | 3 | 0.01 | % | $ | 31,243 | $ | 3 | 0.01 | % | |||||||||

Customer payables | 8,611 | 4 | 0.06 | % | 6,988 | 4 | 0.07 | % | |||||||||||||

Broker-related payables and other | 1,233 | — | 0.00 | % | 1,351 | — | 0.00 | % | |||||||||||||

Other borrowings | 667 | 16 | 3.23 | % | 418 | 13 | 4.23 | % | |||||||||||||

Corporate debt | 996 | 39 | 5.14 | % | 994 | 40 | 5.40 | % | |||||||||||||

Subtotal interest-bearing liabilities | 49,369 | 62 | 0.17 | % | 40,994 | 60 | 0.19 | % | |||||||||||||

Other interest expense (4) | — | 4 | — | 3 | |||||||||||||||||

Total interest-bearing liabilities | 49,369 | 66 | 0.18 | % | 40,994 | 63 | 0.20 | % | |||||||||||||

Total non-interest-bearing liabilities | 1,033 | 1,010 | |||||||||||||||||||

Total liabilities | 50,402 | 42,004 | |||||||||||||||||||

Total shareholders' equity | 6,469 | 5,818 | |||||||||||||||||||

Total liabilities and shareholders' equity | $ | 56,871 | $ | 47,822 | |||||||||||||||||

Excess interest earning assets over interest bearing liabilities/net interest income/net interest margin | $ | 2,451 | $ | 1,066 | 2.74 | % | $ | 1,946 | $ | 860 | 2.67 | % | |||||||||

(1) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

(2) | Represents interest income on securities loaned. |

(3) | Non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate interest income. |

(4) | Represents interest expense on securities borrowed. |

Average interest-earning assets increased 23% to $54.8 billion and 21% to $51.8 billion for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The fluctuation in interest-earning assets is generally driven by changes in interest-bearing liabilities, primarily deposits and customer payables. Average interest-bearing liabilities increased 23% to $52.4 billion and 20% to $49.4 billion for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase was primarily due to higher deposits as a result of transferring customer cash held by third parties to our balance sheet. For additional information on our balance sheet growth and customer cash held by third parties, see Balance Sheet Overview.

Net interest margin increased 26 basis points to 2.85% and 7 basis points to 2.74% for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. Net interest margin is driven by the mix of asset and liability average balances and the interest rates earned or paid on those balances. The increase during the three and nine months ended September 30, 2017, compared to the same period in 2016, is due to higher interest rates earned on increased margin receivable balances

E*TRADE | Q3 2017 10-Q | 14 | |

and higher securities lending activities, partially offset by the continued run-off of our higher yielding legacy mortgage and consumer loan portfolio.

Commissions

Commissions revenue decreased 7% to $100 million and increased 4% to $332 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The main factors that affect commissions revenue are DARTs, average commission per trade and the number of trading days.

DARTs volume increased 35% to 205,763 and 32% to 207,065 for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016, mainly driven by the inclusion of OptionsHouse accounts and the strength of the equity markets. Derivative DARTs represented 32% and 31% of trading volume for the three and nine months ended September 30, 2017, respectively, compared to 26% and 25% of trading volume for the same periods in 2016.

Average commission per trade decreased 29% to $7.76 and 21% to $8.54 for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. Average commission per trade is impacted by customer mix and differing commission rates on various trade types (e.g. equities, derivatives, stock plan and mutual funds). Average commission per trade for the three and nine months ended September 30, 2017 was impacted by reduced commission rates implemented in March 2017 as well as the lower price structure for customer accounts associated with the OptionsHouse acquisition. We have also experienced increased trading activity from certain customers, qualifying them for lower commission rates due to our new active trader pricing. This increased engagement is a key driver behind the decrease in average commission per trade.

Fees and Service Charges

The components of fees and service charges and the resulting variances are as follows (dollars in millions):

Three Months Ended September 30, | Variance | Nine Months Ended September 30, | Variance | ||||||||||||||||||||||||||

2017 vs. 2016 | 2017 vs. 2016 | ||||||||||||||||||||||||||||

2017 | 2016 | Amount | % | 2017 | 2016 | Amount | % | ||||||||||||||||||||||

Order flow revenue | $ | 33 | $ | 24 | $ | 9 | 38 | % | $ | 98 | $ | 68 | $ | 30 | 44 | % | |||||||||||||

Money market funds and sweep deposits revenue(1) | 23 | 13 | 10 | 77 | % | 71 | 31 | 40 | 129 | % | |||||||||||||||||||

Mutual fund service fees | 10 | 9 | 1 | 11 | % | 29 | 27 | 2 | 7 | % | |||||||||||||||||||

Advisor management fees | 9 | 8 | 1 | 13 | % | 26 | 21 | 5 | 24 | % | |||||||||||||||||||

Foreign exchange revenue | 6 | 6 | — | — | % | 20 | 15 | 5 | 33 | % | |||||||||||||||||||

Reorganization fees | 5 | 4 | 1 | 25 | % | 13 | 11 | 2 | 18 | % | |||||||||||||||||||

Other fees and service charges | 6 | 4 | 2 | 50 | % | 19 | 15 | 4 | 27 | % | |||||||||||||||||||

Total fees and service charges | $ | 92 | $ | 68 | $ | 24 | 35 | % | $ | 276 | $ | 188 | $ | 88 | 47 | % | |||||||||||||

(1) | Includes revenue earned on average customer cash held by third parties based on the federal funds rate or LIBOR plus a negotiated spread or other contractual arrangements with the third party institutions. |

Fees and service charges increased 35% to $92 million and 47% to $276 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase in fees and service charges was largely driven by an increase in revenue earned on customer cash held by third parties, which was impacted by a higher interest rate environment, partially offset by lower average balances. The gross yield on customer cash held by third parties for the three and nine months ended September 30, 2017 of approximately 120 and 85 basis points compares to approximately 45 and 40 basis

E*TRADE | Q3 2017 10-Q | 15 | |

points for the same periods in 2016. In addition, fees and service charges benefited from increased order flow revenue resulting primarily from higher options trading activity and improved rates.

Gains on Securities and Other, Net

The components of gains on securities and other, net and the resulting variances are as follows (dollars in millions):

Three Months Ended September 30, | Variance | Nine Months Ended September 30, | Variance | ||||||||||||||||||||||||||

2017 vs. 2016 | 2017 vs. 2016 | ||||||||||||||||||||||||||||

2017 | 2016 | Amount | % | 2017 | 2016 | Amount | % | ||||||||||||||||||||||

Gains on available-for-sale securities | $ | 7 | $ | 17 | $ | (10 | ) | (59 | )% | $ | 25 | $ | 46 | $ | (21 | ) | (46 | )% | |||||||||||

Hedge ineffectiveness | (2 | ) | (4 | ) | 2 | (50 | )% | (5 | ) | (8 | ) | 3 | (38 | )% | |||||||||||||||

Equity method investment income (loss) and other | 1 | 1 | — | — | % | 3 | (4 | ) | 7 | (175 | )% | ||||||||||||||||||

Gains on securities and other, net | $ | 6 | $ | 14 | $ | (8 | ) | (57 | )% | $ | 23 | $ | 34 | $ | (11 | ) | (32 | )% | |||||||||||

Provision (Benefit) for Loan Losses

We recognized a benefit for loan losses of $29 million and $142 million for the three and nine months ended September 30, 2017, respectively, compared to a benefit of $62 million and $131 million for the same periods in 2016. The timing and magnitude of the provision (benefit) for loan losses is affected by many factors that could result in variability. These benefits reflected better than expected performance of our portfolio as well as recoveries in excess of prior estimates, including recoveries of previous charge-offs. The benefit for loan losses for the nine months ended September 30, 2017 also reflected approximately $70 million of benefit recognized in the second quarter of 2017 resulting from refined default assumptions based on the sustained outperformance of converted mortgage loans that had been amortizing for 12 months or longer. For additional information on management's estimate of the allowance for loan losses, see Concentrations of Credit Risk and Summary of Critical Accounting Policies and Estimates.

E*TRADE | Q3 2017 10-Q | 16 | |

Non-Interest Expense

The components of non-interest expense and the resulting variances are as follows (dollars in millions):

Three Months Ended September 30, | Variance | Nine Months Ended September 30, | Variance | ||||||||||||||||||||||||||

2017 vs. 2016 | 2017 vs. 2016 | ||||||||||||||||||||||||||||

2017 | 2016 | Amount | % | 2017 | 2016 | Amount | % | ||||||||||||||||||||||

Compensation and benefits | $ | 139 | $ | 123 | $ | 16 | 13 | % | $ | 408 | $ | 374 | $ | 34 | 9 | % | |||||||||||||

Advertising and market development | 38 | 27 | 11 | 41 | % | 123 | 100 | 23 | 23 | % | |||||||||||||||||||

Clearing and servicing | 29 | 26 | 3 | 12 | % | 94 | 75 | 19 | 25 | % | |||||||||||||||||||

Professional services | 25 | 26 | (1 | ) | (4 | )% | 71 | 70 | 1 | 1 | % | ||||||||||||||||||

Occupancy and equipment | 28 | 24 | 4 | 17 | % | 84 | 71 | 13 | 18 | % | |||||||||||||||||||

Communications | 29 | 22 | 7 | 32 | % | 90 | 65 | 25 | 38 | % | |||||||||||||||||||

Depreciation and amortization | 20 | 20 | — | — | % | 60 | 60 | — | — | % | |||||||||||||||||||

FDIC insurance premiums | 8 | 6 | 2 | 33 | % | 24 | 18 | 6 | 33 | % | |||||||||||||||||||

Amortization of other intangibles | 9 | 5 | 4 | 80 | % | 27 | 15 | 12 | 80 | % | |||||||||||||||||||

Restructuring and acquisition-related activities | 4 | 25 | (21 | ) | (84 | )% | 12 | 28 | (16 | ) | (57 | )% | |||||||||||||||||

Losses on early extinguishment of debt | 58 | — | 58 | 100 | % | 58 | — | 58 | 100 | % | |||||||||||||||||||

Other non-interest expenses | 18 | 19 | (1 | ) | (5 | )% | 55 | 54 | 1 | 2 | % | ||||||||||||||||||

Total non-interest expense | $ | 405 | $ | 323 | $ | 82 | 25 | % | $ | 1,106 | $ | 930 | $ | 176 | 19 | % | |||||||||||||

Compensation and Benefits

Compensation and benefits expense increased 13% to $139 million and 9% to $408 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase was primarily driven by increased incentive compensation during the three and nine months ended September 30, 2017.

Advertising and Market Development

Advertising and market development expense increased 41% to $38 million and 23% to $123 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase was primarily due to higher spending as we launched our new advertising campaign during the three months ended June 30, 2017.

Clearing and Servicing

Clearing and servicing expense increased 12% to $29 million and 25% to $94 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase was primarily related to higher trading volume compared to the same periods in 2016.

Communications

Communications expense increased 32% to $29 million and 38% to $90 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase was primarily driven by increased market data fees resulting from higher trading activity. Additionally, during the three months ended June 30, 2017, we updated our accrual estimate for professional users of real time market data and recognized $9 million related to previous usage.

E*TRADE | Q3 2017 10-Q | 17 | |

Restructuring and Acquisition-Related Activities

Restructuring and acquisition-related activities were $4 million and $12 million for the three and nine months ended September 30, 2017, respectively, compared to $25 million and $28 million the same periods in 2016. Restructuring and acquisition-related activities during the three and nine months ended September 30, 2016 reflected $18 million and $21 million, respectively, of restructuring costs related to the realignment of our core brokerage business and $7 million of acquisition related expense from the OptionsHouse acquisition.

Losses on Early Extinguishment of Debt

Losses on early extinguishment of debt were $58 million for both the three and nine months ended September 30, 2017. During the third quarter of 2017, we issued $600 million of 2.95% Senior Notes and $400 million of 3.80% Senior Notes and used the net proceeds, along with existing corporate cash, to redeem our outstanding $540 million of 5.375% Senior Notes and $460 million of 4.625% Senior Notes, which resulted in a $58 million loss on early extinguishment of debt.

Operating Margin

Operating margin was 37% and 44% for the three and nine months ended September 30, 2017, respectively, compared to 46% and 44% for the same periods in 2016. Adjusted operating margin, a non-GAAP measure, was 42% and 39% the three and nine months ended September 30, 2017, respectively, compared to 34% and 35% for the same periods in 2016.

Adjusted operating margin is a non-GAAP measure calculated by dividing adjusted income before income tax expense by total net revenue. Adjusted income before income tax expense excludes the provision (benefit) for loan losses and losses on early extinguishment of debt. The following table provides a reconciliation of adjusted income before income tax expense and adjusted operating margin, non-GAAP measures, to the most directly comparable GAAP measures (dollars in millions):

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||||||||||

Amount | Operating Margin % | Amount | Operating Margin % | Amount | Operating Margin % | Amount | Operating Margin % | ||||||||||||||||

Income before income tax expense / operating margin | $ | 223 | 37% | $ | 225 | 46% | $ | 765 | 44% | $ | 633 | 44% | |||||||||||

Add back impact of pre-tax items: | |||||||||||||||||||||||

Provision (benefit) for loan losses | (29 | ) | (62 | ) | (142 | ) | (131 | ) | |||||||||||||||

Losses on early extinguishment of debt | 58 | — | 58 | — | |||||||||||||||||||

Subtotal | 29 | (62 | ) | (84 | ) | (131 | ) | ||||||||||||||||

Adjusted income before income tax expense / adjusted operating margin | $ | 252 | 42% | $ | 163 | 34% | $ | 681 | 39% | $ | 502 | 35% | |||||||||||

E*TRADE | Q3 2017 10-Q | 18 | |

Income Tax Expense

Income tax expense was $76 million and $280 million for the three and nine months ended September 30, 2017, respectively, compared to $86 million and $208 million for the same periods in 2016. The effective tax rates were 34% and 37% for the three and nine months ended September 30, 2017, respectively, compared to 38% and 33% for the same periods in 2016.

The effective tax rates of 34% and 37% for the three and nine months ended September 30, 2017, respectively, include tax benefits related to the revaluation of certain net state deferred tax assets and to the adoption of amended accounting guidance for employee share-based compensation. See Note 1—Organization, Basis of Presentation and Summary of Significant Accounting Policies for additional information on the adoption of the amended accounting guidance. The effective tax rate of 33% for the nine months ended September 30, 2016 was impacted by a tax benefit related to the release of valuation allowances against certain state deferred tax assets.

E*TRADE | Q3 2017 10-Q | 19 | |

BALANCE SHEET OVERVIEW

The following table sets forth the significant components of the consolidated balance sheet (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

Assets: | ||||||||||||||

Cash and equivalents | $ | 896 | $ | 1,950 | $ | (1,054 | ) | (54 | )% | |||||

Segregated cash | 696 | 1,460 | (764 | ) | (52 | )% | ||||||||

Securities(1) | 42,093 | 29,643 | 12,450 | 42 | % | |||||||||

Margin receivables | 8,535 | 6,731 | 1,804 | 27 | % | |||||||||

Loans receivable, net | 2,838 | 3,551 | (713 | ) | (20 | )% | ||||||||

Receivables from brokers, dealers and clearing organizations(2) | 1,108 | 1,056 | 52 | 5 | % | |||||||||

Goodwill and other intangibles, net | 2,664 | 2,690 | (26 | ) | (1 | )% | ||||||||

Deferred tax assets, net | 416 | 756 | (340 | ) | (45 | )% | ||||||||

Other(3) | 1,129 | 1,162 | (33 | ) | (3 | )% | ||||||||

Total assets | $ | 60,375 | $ | 48,999 | $ | 11,376 | 23 | % | ||||||

Liabilities and shareholders’ equity: | ||||||||||||||

Deposits | $ | 41,543 | $ | 31,682 | $ | 9,861 | 31 | % | ||||||

Customer payables | 8,716 | 8,159 | 557 | 7 | % | |||||||||

Payables to brokers, dealers and clearing organizations(4) | 1,392 | 983 | 409 | 42 | % | |||||||||

Other borrowings | 609 | 409 | 200 | 49 | % | |||||||||

Corporate debt | 991 | 994 | (3 | ) | — | % | ||||||||

Other liabilities | 476 | 500 | (24 | ) | (5 | )% | ||||||||

Total liabilities | 53,727 | 42,727 | 11,000 | 26 | % | |||||||||

Shareholders’ equity | 6,648 | 6,272 | 376 | 6 | % | |||||||||

Total liabilities and shareholders’ equity | $ | 60,375 | $ | 48,999 | $ | 11,376 | 23 | % | ||||||

(1) | Includes balance sheet line items available-for-sale and held-to-maturity securities. |

(2) | Includes deposits paid for securities borrowed of $484 million and $774 million as of September 30, 2017 and December 31, 2016, respectively. |

(3) | Includes balance sheet line items property and equipment, net and other assets. |

(4) | Includes deposits received for securities loaned of $1.3 billion and $926 million as of September 30, 2017 and December 31, 2016, respectively. |

Cash and Equivalents

Cash and equivalents decreased 54% to $896 million during the nine months ended September 30, 2017 and includes corporate cash of $309 million as of September 30, 2017. Cash and equivalents will fluctuate based on a variety of factors, including, among other drivers, liquidity needs at the parent, customer activity at our regulated subsidiaries, and the timing of investments at E*TRADE Bank. For additional information on our use of cash and equivalents, including corporate cash, see Liquidity and Capital Resources.

Segregated Cash

Cash required to be segregated under federal or other regulations decreased 52% to $696 million during the nine months ended September 30, 2017. The level of segregated cash is driven largely by customer payables and securities lending balances we hold as liabilities compared with the amount of margin receivables and securities borrowed balances we hold as assets. The excess represents customer cash that we are required by our regulators to segregate for the exclusive benefit of our brokerage customers. At

E*TRADE | Q3 2017 10-Q | 20 | |

September 30, 2017 and December 31, 2016, $800 million and $500 million, respectively, of reverse repurchase agreements between E*TRADE Securities and E*TRADE Bank, representing investments that were segregated under federal or other regulations by E*TRADE Securities, were eliminated in consolidation.

Securities

Available-for-sale and held-to-maturity securities are summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

Available-for-sale securities: | ||||||||||||||

Debt securities: | ||||||||||||||

Agency mortgage-backed securities | $ | 17,663 | $ | 12,634 | $ | 5,029 | 40 | % | ||||||

Other debt securities | 1,503 | 1,251 | 252 | 20 | % | |||||||||

Total debt securities | 19,166 | 13,885 | 5,281 | 38 | % | |||||||||

Publicly traded equity securities(1) | 7 | 7 | — | — | % | |||||||||

Total available-for-sale securities | $ | 19,173 | $ | 13,892 | $ | 5,281 | 38 | % | ||||||

Held-to-maturity securities: | ||||||||||||||

Agency mortgage-backed securities | $ | 19,850 | $ | 12,868 | $ | 6,982 | 54 | % | ||||||

Other debt securities | 3,070 | 2,883 | 187 | 6 | % | |||||||||

Total held-to-maturity securities | $ | 22,920 | $ | 15,751 | $ | 7,169 | 46 | % | ||||||

Total investments in securities | $ | 42,093 | $ | 29,643 | $ | 12,450 | 42 | % | ||||||

(1) | Consists of Community Reinvestment Act investments in a mutual fund. |

Securities represented 70% and 60% of total assets at September 30, 2017 and December 31, 2016, respectively. We classify debt securities as available-for-sale or held-to-maturity based on our investment strategy and management’s assessment of our intent and ability to hold the debt securities until maturity.

The increase in total investments in securities during the nine months ended September 30, 2017 was primarily due to net purchases as a result of our efforts to grow the balance sheet by transferring customer cash held by third parties to our balance sheet.

Margin Receivables

Margin receivables increased 27% to $8.5 billion during the nine months ended September 30, 2017. The increase in margin receivables was primarily driven by improved market sentiment increasing demand for additional margin lending. During the three months ended September 30, 2017, we also transferred $0.4 billion of customer margin balances held by a third party clearing firm to E*TRADE Securities in connection with the integration of OptionsHouse.

E*TRADE | Q3 2017 10-Q | 21 | |

Loans Receivable, Net

Loans receivable, net are summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

One- to four-family | $ | 1,531 | $ | 1,950 | $ | (419 | ) | (21 | )% | |||||

Home equity | 1,197 | 1,556 | (359 | ) | (23 | )% | ||||||||

Consumer and other | 192 | 250 | (58 | ) | (23 | )% | ||||||||

Total loans receivable | 2,920 | 3,756 | (836 | ) | (22 | )% | ||||||||

Unamortized premiums, net | 12 | 16 | (4 | ) | (25 | )% | ||||||||

Allowance for loan losses | (94 | ) | (221 | ) | 127 | (57 | )% | |||||||

Total loans receivable, net | $ | 2,838 | $ | 3,551 | $ | (713 | ) | (20 | )% | |||||

Loans receivable, net decreased 20% to $2.8 billion during the nine months ended September 30, 2017. During the three months ended June 30, 2017 the Company sold certain loans with a carrying value of $41 million for proceeds that approximated book value. We expect the remaining legacy mortgage and consumer loan portfolio to continue its run-off for the foreseeable future. As our portfolio has seasoned and substantially all interest-only loans have converted to amortizing, we continue to assess underlying performance, the economic environment, and the value of the portfolio in the marketplace. While it is our intention to hold these loans, if the markets improve our strategy could change. For additional information on management's estimate of the allowance for loan losses, see Concentrations of Credit Risk and Summary of Critical Accounting Policies and Estimates.

In the third quarter of 2017 we introduced a securities-based lending product, where customers can borrow up to 50% of the market value of securities pledged as collateral. Activity for these loans is reflected as consumer and other within loans receivable, net and related disclosures.

Deposits

Deposits are summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

Sweep deposits | $ | 36,507 | $ | 26,362 | $ | 10,145 | 38 | % | ||||||

Savings deposits | 3,011 | 3,185 | (174 | ) | (5 | )% | ||||||||

Other deposits | 2,025 | 2,135 | (110 | ) | (5 | )% | ||||||||

Total deposits | $ | 41,543 | $ | 31,682 | $ | 9,861 | 31 | % | ||||||

Deposits represented 77% and 74% of total liabilities at September 30, 2017 and December 31, 2016, respectively. At September 30, 2017, approximately 92% of our customer deposits were covered by FDIC insurance. Deposits increased $9.9 billion during the nine months ended September 30, 2017 primarily as a result of transferring customer cash held by third parties to our balance sheet.

E*TRADE | Q3 2017 10-Q | 22 | |

The majority of the deposits balance, specifically sweep deposits, is included in brokerage related cash, which is reported as a customer activity metric. Total brokerage related cash is summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

Sweep deposits(1) | $ | 36,507 | $ | 26,362 | $ | 10,145 | 38 | % | ||||||

Customer payables | 8,716 | 8,159 | 557 | 7 | % | |||||||||

Subtotal | 45,223 | 34,521 | 10,702 | 31 | % | |||||||||

Customer cash held by third parties(2) | 7,076 | 16,848 | (9,772 | ) | (58 | )% | ||||||||

Total brokerage related cash | $ | 52,299 | $ | 51,369 | $ | 930 | 2 | % | ||||||

(1) | Sweep deposits are held at bank subsidiaries and are included in the deposits line item on our consolidated balance sheet. |

(2) | Customer cash held by third parties is maintained at unaffiliated financial institutions outside E*TRADE Financial and includes money market funds and sweep deposit accounts. Prior to September 30, 2017, customer cash held by third parties also included OptionsHouse customer cash held by a third party clearing firm. These balances were transferred to E*TRADE Securities during the three months ended September 30, 2017, in connection with the integration of OptionsHouse. Customer cash held by third parties is not reflected on our consolidated balance sheet and is not immediately available for liquidity purposes. |

We offer an extended insurance sweep deposit account (ESDA) program to our brokerage customers. The ESDA program utilizes our bank subsidiaries, in combination with additional third party program banks, to allow customers the ability to have aggregate deposits they hold in the ESDA program insured up to $1,250,000 for each category of legal ownership. As of September 30, 2017, approximately 99% of sweep deposits were in the ESDA program.

Customer cash held by third parties is maintained at unaffiliated financial institutions. The components of customer cash held by third parties are summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

Sweep deposits held by unaffiliated financial institutions | $ | 6,360 | $ | 14,943 | $ | (8,583 | ) | (57 | )% | |||||

Customer cash held by third party clearing firm(1) | — | 1,634 | (1,634 | ) | (100 | )% | ||||||||

Municipal funds and other | 716 | 271 | 445 | 164 | % | |||||||||

Customer cash held by third parties | $ | 7,076 | $ | 16,848 | $ | (9,772 | ) | (58 | )% | |||||

(1) | Represents OptionsHouse customer cash held by a third party clearing firm that was transferred to E*TRADE Securities during the three months ended September 30, 2017 in connection with the integration of OptionsHouse. |

As of September 30, 2017, approximately $3.4 billion of customer cash held by third parties was available for balance sheet growth. The timing of our balance sheet growth will be impacted by a variety of factors, including the capital requirements applicable to both the Company and E*TRADE Bank.

Other Borrowings

Other borrowings are summarized as follows (dollars in millions):

Variance | ||||||||||||||

September 30, | December 31, | 2017 vs. 2016 | ||||||||||||

2017 | 2016 | Amount | % | |||||||||||

FHLB advances | $ | 200 | $ | — | $ | 200 | 100 | % | ||||||

Trust preferred securities | 409 | 409 | — | — | % | |||||||||

Total other borrowings | $ | 609 | $ | 409 | $ | 200 | 49 | % | ||||||

E*TRADE | Q3 2017 10-Q | 23 | |

Other borrowings increased 49% to $609 million during the nine months ended September 30, 2017 as we utilized Federal Home Loan Bank (FHLB) advances for short-term liquidity and funding requirements. See Liquidity and Capital Resources for additional information on liquidity and funding sources at E*TRADE Bank.

LIQUIDITY AND CAPITAL RESOURCES

We have established liquidity and capital policies to support the successful execution of our business strategy, while maintaining ongoing and sufficient liquidity through the business cycle. We believe liquidity is of critical importance to the Company and especially important for E*TRADE Bank and our broker-dealer subsidiaries. The objective of our policies is to ensure that we can meet our corporate, banking and broker-dealer liquidity needs under both normal operating conditions and under periods of stress in the financial markets.

Liquidity

Our corporate liquidity needs are primarily driven by capital needs at E*TRADE Bank and E*TRADE Securities as well as by the principal and interest due on our corporate debt and the amount of dividend payments on our preferred stock. Our banking and brokerage subsidiaries' liquidity needs are driven primarily by the level and volatility of our customer activity. Management maintains a set of liquidity sources and monitors certain business trends and market metrics closely in an effort to ensure we have sufficient liquidity. Potential loans by E*TRADE Bank to the parent company and its other non-bank subsidiaries are subject to various quantitative, arm’s length, collateralization, capital and other requirements.

Parent Company Liquidity

The parent company's primary source of liquidity is corporate cash. Corporate cash, a non-GAAP measure, is a component of cash and equivalents; see the consolidated statement of cash flows within Item 1. Condensed Consolidated Financial Statements (Unaudited) for information on cash and equivalents activity. We define corporate cash as cash held at the parent company and subsidiaries, excluding bank, broker-dealer, and futures commission merchant (FCM) subsidiaries that require regulatory approval or notification prior to the payment of certain dividends to the parent company.

We believe corporate cash is a useful measure of the parent company’s liquidity as it is the primary source of capital above and beyond the capital deployed in our regulated subsidiaries. Corporate cash can fluctuate in any given quarter and is impacted primarily by the following:

• | Dividends from subsidiaries |

• | Non-cumulative preferred stock dividends |

• | Share repurchases |

• | Debt service costs |

• | Acquisitions and investments |

• | Tax payments and the reimbursement from the parent company's subsidiaries for the use of its deferred tax assets |

• | Other overhead and expense reimbursements through cost sharing arrangements |

E*TRADE | Q3 2017 10-Q | 24 | |

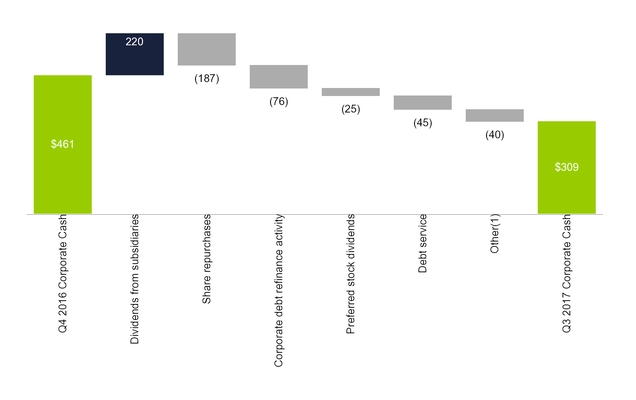

The following chart provides a roll forward of corporate cash at December 31, 2016 to corporate cash at September 30, 2017 (dollars in millions):

(1) Other activity includes contributions to subsidiaries and parent company overhead, offset by reimbursements from subsidiaries for use of the parent's deferred tax assets and related proceeds under overhead cost sharing arrangements.

The following table provides a reconciliation of consolidated cash and equivalents to corporate cash, a non-GAAP measure (dollars in millions):

September 30, | December 31, | September 30, | |||||||||

2017 | 2016 | 2016 | |||||||||

Consolidated cash and equivalents | $ | 896 | $ | 1,950 | $ | 1,467 | |||||

Less: Cash at regulated subsidiaries(1) | (587 | ) | (1,489 | ) | (1,161 | ) | |||||

Corporate cash | $ | 309 | $ | 461 | $ | 306 | |||||

(1) Reported net of corporate cash on deposit at E*TRADE Bank that is eliminated in consolidation.

Corporate cash decreased $152 million to $309 million during the nine months ended September 30, 2017. Corporate cash included dividends of $220 million from E*TRADE Securities to the parent company during the nine months ended September 30, 2017. Corporate cash also included the impact of share repurchases, corporate debt refinance activity, preferred stock dividends, debt service, overhead cost sharing arrangements between the parent and our operating subsidiaries, and the impact of annual incentive compensation payments in the nine months ended September 30, 2017.

E*TRADE | Q3 2017 10-Q | 25 | |

During the three and nine months ended September 30, 2017, we used $76 million of corporate cash along with the net proceeds from the issuance of $1 billion of senior notes, to redeem our higher cost corporate debt, and to pay the associated redemption premiums, accrued and unpaid interest and related fees and expenses. This transaction decreased our annual corporate debt service costs from $50 million to $33 million. We maintain corporate cash at a minimum of two times our scheduled annual corporate debt service payments and scheduled maturities over the next 12 months. As we do not have any scheduled maturities of corporate debt in the coming year, our current minimum under this methodology is approximately $66 million; however, we are currently targeting $200 million in corporate cash for future periods. Our nearest maturity of interest-bearing corporate debt is August 2022.

On June 23, 2017, we entered into an unsecured committed revolving credit facility with certain lenders, which replaced our previous secured committed revolving credit facility entered into in November 2014 and increased our total borrowing capacity under the facility to $300 million. The Company has the ability to borrow against the credit facility for working capital and general corporate purposes. The unsecured committed revolving credit facility will mature on June 23, 2020. At September 30, 2017, there was no outstanding balance under this revolving credit facility.

On October 19, 2017, we announced an agreement to acquire TCA for $275 million in cash. We anticipate funding the transaction through the issuance of non-cumulative perpetual preferred stock. Based on this structure, we do not expect the acquisition to impact our ability to maintain a 6.5% Tier 1 leverage ratio.

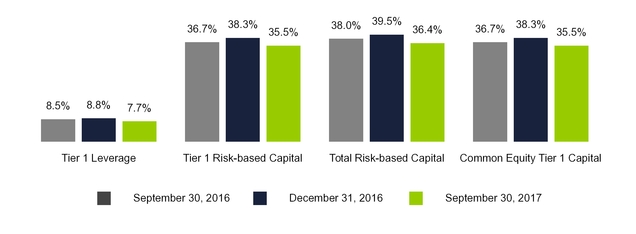

E*TRADE Bank Liquidity

E*TRADE Bank relies on bank cash and deposits for liquidity needs. Management believes that within deposits, sweep deposits are of particular importance as they are a stable source of liquidity for E*TRADE Bank. We have the ability to generate liquidity in the form of additional deposits by raising the yield on our customer deposit products and by bringing additional deposits onto our balance sheet. Sweep deposits on our balance sheet as of September 30, 2017 increased $10.1 billion compared to December 31, 2016. We utilize our sweep deposit platform to efficiently manage our balance sheet size.

We may utilize wholesale funding sources for short-term liquidity and contingency funding requirements. Our ability to borrow these funds is dependent upon the continued availability of funding in the wholesale borrowings market. In addition, we can borrow from the Federal Reserve Bank of Richmond's discount window to meet short-term liquidity requirements, although it is not viewed as a primary source of funding. At September 30, 2017, E*TRADE Bank had approximately $5.1 billion and $0.9 billion in additional collateralized borrowing capacity with the FHLB and the Federal Reserve Bank of Richmond, respectively.

E*TRADE Securities Liquidity

E*TRADE Securities relies on customer payables, securities lending, and internal and external lines of credit to provide liquidity and to fund margin lending. At September 30, 2017, E*TRADE Securities' external liquidity lines totaled approximately $1.1 billion and included the following:

• | A 364-day, $450 million senior unsecured committed revolving credit facility with a syndicate of banks, with a maturity date of June 2018 and a commitment fee of 0.35% on unused balances |

• | Secured committed lines of credit with two unaffiliated banks, aggregating to $175 million, with a maturity date of June 2018 and a commitment fee of 0.15% on unused balances |

• | Unsecured uncommitted lines of credit with two unaffiliated banks, aggregating to $75 million, of which $50 million matures in June 2018 and the remaining line has no maturity date |

• | Secured uncommitted lines of credit with several unaffiliated banks, aggregating to $375 million with no maturity date |

The revolving credit facility contains certain covenants, including maintenance covenants related to E*TRADE Securities' minimum consolidated tangible net worth and regulatory net capital ratio. There were

E*TRADE | Q3 2017 10-Q | 26 | |

no outstanding balances for any of these lines at September 30, 2017. E*TRADE Securities also maintains lines of credit with the parent company and E*TRADE Bank.

Liquidity Coverage Ratio

As a result of the Company's balance sheet growth, we will be subject to the modified liquidity coverage ratio (LCR) requirement beginning April 1, 2018. The purpose of the LCR is to require banking organizations to hold minimum amounts of high-quality liquid assets (HQLA) based on a percentage of their net cash outflows over a 30-day period. Bank and savings and loan holding companies with total consolidated assets of $50 billion or more, based on the average of the four most recent quarters, are subject to a modified LCR requiring them to hold HQLA in an amount equal to at least 70% of their projected net cash outflows over a 30-day period. The Company believes the LCR is an important measure of liquidity and has been managing against it in preparation for the applicability of these requirements. In addition, beginning October 1, 2018, we will be required to disclose certain quantitative and qualitative information related to our LCR calculation after each calendar quarter.

Capital Resources

Bank Capital Requirements

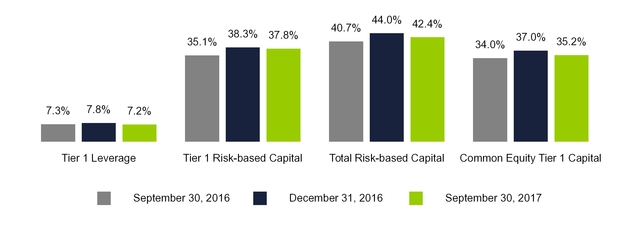

The Dodd-Frank Act requires all companies, including savings and loan holding companies, that directly or indirectly control an insured depository institution, to serve as a source of strength for the institution. The Company and E*TRADE Bank are subject to regulatory capital requirements. Some of these requirements are still subject to phase-in periods, including certain deductions from and adjustments to regulatory capital. These requirements are currently scheduled to be fully implemented in 2018, though proposed rulemaking may impact the phase-in periods or certain deductions. For additional information on bank regulatory requirements and phase-in periods, see Overview—Regulatory Developments as well as Part I. Item 1. Business—Regulation in our Annual Report on Form 10-K for the year ended December 31, 2016. At September 30, 2017, our regulatory capital ratios for E*TRADE Financial were well above the minimum ratios required to be "well capitalized." E*TRADE Financial's current Tier 1 Leverage ratio threshold of 6.5% was reduced from 7.0% in July 2017. E*TRADE Financial's capital ratios are as follows:

E*TRADE | Q3 2017 10-Q | 27 | |

E*TRADE Financial's capital ratios are calculated as follows (dollars in millions):

September 30, | December 31, | September 30, | |||||||||

2017 | 2016 | 2016 | |||||||||

E*TRADE Financial shareholders’ equity | $ | 6,648 | $ | 6,272 | $ | 6,316 | |||||

Deduct: | |||||||||||

Preferred stock | (394 | ) | (394 | ) | (394 | ) | |||||

E*TRADE Financial Common Equity Tier 1 capital before regulatory adjustments | $ | 6,254 | $ | 5,878 | $ | 5,922 | |||||

Add: | |||||||||||

(Gains) losses in other comprehensive income on available-for-sale debt securities, net of tax | 50 | 139 | (37 | ) | |||||||

Deduct: | |||||||||||

Goodwill and other intangible assets, net of deferred tax liabilities | (2,014 | ) | (2,029 | ) | (2,043 | ) | |||||

Disallowed deferred tax assets | (472 | ) | (505 | ) | (556 | ) | |||||

E*TRADE Financial Common Equity Tier 1 capital | 3,818 | 3,483 | 3,286 | ||||||||

Add: | |||||||||||

Preferred stock | 394 | 394 | 394 | ||||||||

Deduct: | |||||||||||

Disallowed deferred tax assets | (112 | ) | (267 | ) | (284 | ) | |||||

E*TRADE Financial Tier 1 capital | $ | 4,100 | $ | 3,610 | $ | 3,396 | |||||

Add: | |||||||||||

Allowable allowance for loan losses | 94 | 124 | 128 | ||||||||

Non-qualifying capital instruments subject to phase-out (trust preferred securities) | 414 | 414 | 414 | ||||||||

E*TRADE Financial total capital | $ | 4,608 | $ | 4,148 | $ | 3,938 | |||||

E*TRADE Financial average assets for leverage capital purposes | $ | 59,835 | $ | 49,113 | $ | 49,240 | |||||

Deduct: | |||||||||||

Goodwill and other intangible assets, net of deferred tax liabilities | (2,014 | ) | (2,029 | ) | (2,043 | ) | |||||

Disallowed deferred tax assets | (584 | ) | (772 | ) | (840 | ) | |||||

E*TRADE Financial adjusted average assets for leverage capital purposes | $ | 57,237 | $ | 46,312 | $ | 46,357 | |||||