Exhibit 99.2

THIS DISCLOSURE STATEMENT IS BEING SUBMITTED FOR APPROVAL BUT HAS NOT

BEEN APPROVED BY THE BANKRUPTCY COURT. THIS IS NOT A SOLICITATION OF

ACCEPTANCE OR REJECTION OF THE PLAN. ACCEPTANCE OR REJECTION MAY NOT

BE SOLICITED UNTIL A DISCLOSURE STATEMENT HAS BEEN APPROVED BY THE

BANKRUPTCY COURT. THE INFORMATION IN THE DISCLOSURE STATEMENT IS

SUBJECT TO CHANGE. THIS DISCLOSURE STATEMENT IS NOT AN OFFER TO SELL

ANY SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY ANY SECURITIES.

IN THE UNITED STATES BANKRUPTCY COURT

FOR THE DISTRICT OF DELAWARE

| |

|

|

|

|

|

| |

|

|

|

|

) |

|

|

In re: |

|

) |

|

Chapter 11 |

|

|

) |

|

|

VISTEON

CORPORATION, et al.,1 |

|

) |

|

Case No. 09-11786 (CSS) |

|

|

) |

|

|

|

|

) |

|

Jointly Administered |

Debtors. |

|

) |

|

|

|

|

) |

|

|

| |

|

|

DEBTORS’ FOURTH AMENDED DISCLOSURE STATEMENT FOR THE FOURTH

AMENDED JOINT PLAN OF REORGANIZATION OF VISTEON CORPORATION

AND ITS DEBTOR AFFILIATES PURSUANT TO CHAPTER 11 OF THE UNITED

STATES BANKRUPTCY CODE

| |

|

|

|

PACHULSKI STANG ZIEHL & JONES LLP

|

|

KIRKLAND & ELLIS LLP |

Laura Davis Jones (DE Bar No. 2436)

|

|

James H. M. Sprayregen, P.C. (IL 6190206) |

James E. O’Neill (DE Bar No. 4042)

|

|

James J. Mazza, Jr. (IL 6275474) |

Timothy P. Cairns (DE Bar No. 4228)

|

|

Sienna R. Singer (IL 6287154) |

919 North Market Street, 17th Floor

|

|

300 North LaSalle |

Wilmington, Delaware 19899-8705

|

|

Chicago, Illinois 60654 |

Telephone: (302) 652-4100

|

|

Telephone: (312) 862-2000 |

|

|

|

|

|

Marc Kieselstein, P.C. (IL 6199255) |

|

|

Brian S. Lennon (NY 4215083) |

|

|

601 Lexington Avenue |

|

|

New York, New York 10022-4611 |

|

|

Telephone: (212) 446-4800 |

Attorneys for the Debtors and Debtors in Possession |

|

|

Dated: June 14, 2010 |

|

|

|

|

|

| 1 |

|

The Debtors in these chapter 11 cases, along with the last

four digits of each Debtor’s federal tax identification number, are: Visteon

Corporation (9512); ARS, Inc. (3590); Fairlane Holdings, Inc. (8091);

GCM/Visteon Automotive Leasing Systems, LLC (4060); GCM/Visteon Automotive

Systems, LLC (7103); Infinitive Speech Systems Corp. (7099); MIG-Visteon

Automotive Systems, LLC (5828); SunGlas, LLC (0711); The Visteon Fund (6029);

Tyler Road Investments, LLC (9284); VC Aviation Services, LLC (2712); VC

Regional Assembly & Manufacturing, LLC (3058); Visteon AC Holdings Corp.

(9371); Visteon Asia Holdings, Inc. (0050); Visteon Automotive Holdings, LLC

(8898); Visteon Caribbean, Inc. (7397); Visteon Climate Control Systems Limited

(1946); Visteon Domestic Holdings, LLC (5664); Visteon Electronics Corporation

(9060); Visteon European Holdings Corporation (5152); Visteon Financial

Corporation (9834); Visteon Global Technologies, Inc. (9322); Visteon Global

Treasury, Inc. (5591); Visteon Holdings, LLC (8897); Visteon International

Business Development, Inc. (1875); Visteon International Holdings, Inc. (4928);

Visteon LA Holdings Corp. (9369); Visteon Remanufacturing Incorporated (3237);

Visteon Systems, LLC (1903); Visteon Technologies, LLC (5291). The location of

the Debtors’ corporate headquarters and the service address for all the Debtors

is: One Village Center Drive, Van Buren Township, Michigan 48111. |

TABLE OF CONTENTS

| |

|

|

|

|

|

ARTICLE I. INTRODUCTION |

|

|

4 |

|

A. Rules of Interpretation |

|

|

4 |

|

|

|

|

|

|

ARTICLE II. OVERVIEW OF THE PLAN |

|

|

5 |

|

A. General Structure of the Plan |

|

|

5 |

|

B. Treatment of Claims and Interests |

|

|

9 |

|

C. Treatment of Claims and Interests Under the Plan |

|

|

10 |

|

D. Liquidation and Valuation Analyses |

|

|

16 |

|

E. Certain Factors to Be Considered Prior to Voting |

|

|

16 |

|

|

|

|

|

|

ARTICLE III. VOTING AND RIGHTS OFFERING SUBSCRIPTION PROCEDURES |

|

|

17 |

|

A. Vote Required for Acceptance by a Class |

|

|

18 |

|

B. Classes Not Entitled to Vote |

|

|

18 |

|

C. Solicitation Procedures |

|

|

19 |

|

D. Voting Procedures |

|

|

20 |

|

E. Rights Offering Subscription Procedures |

|

|

21 |

|

F. Confirmation Hearing |

|

|

22 |

|

G. Confirmation and Consummation of the Plan |

|

|

22 |

|

|

|

|

|

|

ARTICLE IV. GENERAL INFORMATION |

|

|

22 |

|

A. Overview of the Debtors’ History and Industry |

|

|

22 |

|

B. Visteon’s Products and Services |

|

|

23 |

|

C. Visteon’s Customers |

|

|

25 |

|

D. Visteon’s Corporate Structure |

|

|

26 |

|

E. Visteon’s Competition |

|

|

27 |

|

F. Executive Officers of the Debtors |

|

|

27 |

|

G. Employees |

|

|

27 |

|

H. Benefit Plans |

|

|

28 |

|

I. The Debtors’ Prepetition Capital Structure |

|

|

32 |

|

|

|

|

|

|

ARTICLE V. THE CHAPTER 11 CASES |

|

|

36 |

|

A. Events Leading to the Commencement of the Chapter 11 Cases |

|

|

36 |

|

B. Stabilization of Operations |

|

|

37 |

|

C. Appointment of Committees |

|

|

41 |

|

D. Operational Restructuring Activity, Liquidity Enhancements,

and Business Plan Development and Implementation |

|

|

43 |

|

E. Postpetition Financing |

|

|

48 |

|

F. Addressing Legacy Liabilities |

|

|

50 |

|

G. Analyzing Executory Contracts and Unexpired Leases |

|

|

51 |

|

H. Employee Incentive, Severance, and Retention Programs |

|

|

52 |

|

I. Analysis and Resolution of Claims |

|

|

54 |

|

J. Negotiations Relating to the Development of the Plan |

|

|

61 |

|

K. Alternative Plan Proposals |

|

|

64 |

|

| |

|

|

|

|

|

ARTICLE VI. PLAN SUMMARY |

|

|

65 |

|

A. Overview of Chapter 11 |

|

|

65 |

|

B. Overall Structure of the Plan |

|

|

67 |

|

C. Administrative and Priority Claims |

|

|

70 |

|

D. Sub Plans |

|

|

72 |

|

E. Classification of Claims and Interests |

|

|

72 |

|

F. Treatment of Classes of Claims and Interests |

|

|

73 |

|

G. Special Provision Governing Unimpaired Claims |

|

|

80 |

|

H. Provisions for Implementation of the Plan |

|

|

81 |

|

I. Rights Offering |

|

|

88 |

|

J. Entitlement to Funding of Cash Amount Recoveries |

|

|

91 |

|

K. Treatment of Executory Contracts and Unexpired Leases |

|

|

92 |

|

L. Procedures for Resolving Disputed Claims and Interests |

|

|

96 |

|

M. Provisions Governing Distributions |

|

|

98 |

|

N. Effect of Confirmation of the Plan |

|

|

106 |

|

O. Conditions Precedent to Consummation of the Plan |

|

|

110 |

|

P. Retention of Jurisdiction |

|

|

111 |

|

Q. Miscellaneous Provisions |

|

|

114 |

|

|

|

|

|

|

ARTICLE VII. SECURITIES LAW MATTERS |

|

|

119 |

|

A. Securities Law Matters Under the Rights Offering Sub Plan |

|

|

119 |

|

B. Securities Law Matters Under the Claims Conversion Sub Plan |

|

|

119 |

|

C. Section 1145 of the Bankruptcy Code |

|

|

120 |

|

D. Section 4(2) of the Securities Act/Regulation D |

|

|

121 |

|

E. Resales of New Common Stock/Rule 144 and Rule 144A |

|

|

121 |

|

|

|

|

|

|

ARTICLE VIII. STATUTORY REQUIREMENTS FOR CONFIRMATION OF THE PLAN |

|

|

123 |

|

A. The Confirmation Hearing |

|

|

123 |

|

B. Confirmation Standards |

|

|

123 |

|

C. Liquidation Analyses |

|

|

125 |

|

D. Valuation Analysis |

|

|

125 |

|

E. Financial Feasibility |

|

|

133 |

|

F. Acceptance by Impaired Classes |

|

|

133 |

|

G. Confirmation Without Acceptance By All Impaired Classes |

|

|

134 |

|

|

|

|

|

|

ARTICLE IX. PLAN-RELATED RISK FACTORS AND ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF

THE PLAN |

|

|

135 |

|

A. General |

|

|

135 |

|

B. Certain Bankruptcy Law Considerations |

|

|

135 |

|

C. Risk Factors That May Affect the Value of the Securities to Be Issued

Under the Plan |

|

|

138 |

|

D. Risk Factors That Could Negatively Impact the Debtors’ Business |

|

|

140 |

|

E. Risks Associated with Forward Looking Statements |

|

|

149 |

|

F. Disclosure Statement Disclaimer |

|

|

150 |

|

G. Liquidation Under Chapter 7 |

|

|

153 |

|

3

| |

|

|

|

|

|

ARTICLE X. CERTAIN FEDERAL INCOME TAX CONSEQUENCES |

|

|

153 |

|

A. Consequences to Holders of Allowed Class E Term Loan Facility Claims,

Class F 7.00% Senior Notes Claims and 8.25% Senior Notes Claims, and Class G

12.25% Senior Notes Claims |

|

|

154 |

|

B. Certain United States Federal Income Tax Consequences to the

Reorganized Debtors |

|

|

157 |

|

|

|

|

|

|

ARTICLE XI. RECOMMENDATION |

|

|

160 |

|

4

EXHIBITS

| |

|

|

|

Exhibit A

|

|

Fourth Amended Joint Plan of Reorganization of Visteon

Corporation and Its Debtor Affiliates Pursuant to Chapter 11 of

the United States Bankruptcy Code |

|

|

|

Exhibit B

|

|

Approved Disclosure Statement Order [To Be Filed] |

|

|

|

Exhibit C

|

|

The Reorganized Debtors’ Financial Projections |

|

|

|

Exhibit D

|

|

Liquidation Analyses |

|

|

|

Exhibit E

|

|

Term Loan Lender Proposal, Dated April 16, 2010 |

|

|

|

Exhibit F

|

|

Term Loan Lender Proposal, Dated May 7, 2010 |

5

DISCLAIMER

THE DISCLOSURE STATEMENT CONTAINS SUMMARIES OF CERTAIN PROVISIONS OF THE DEBTORS’ PLAN AND

CERTAIN OTHER DOCUMENTS AND FINANCIAL INFORMATION. THE INFORMATION INCLUDED IN THE DISCLOSURE

STATEMENT IS PROVIDED FOR THE PURPOSE OF SOLICITING ACCEPTANCES OF THE PLAN AND SHOULD NOT BE

RELIED UPON FOR ANY PURPOSE OTHER THAN TO DETERMINE WHETHER AND HOW TO VOTE ON THE PLAN. THE

DEBTORS BELIEVE THAT THESE SUMMARIES ARE FAIR AND ACCURATE. THE SUMMARIES OF THE FINANCIAL

INFORMATION AND THE DOCUMENTS WHICH ARE ATTACHED TO, OR INCORPORATED BY REFERENCE IN, THE

DISCLOSURE STATEMENT ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO SUCH INFORMATION AND

DOCUMENTS. IN THE EVENT OF ANY INCONSISTENCY OR DISCREPANCY BETWEEN A DESCRIPTION IN THE

DISCLOSURE STATEMENT AND THE TERMS AND PROVISIONS OF THE PLAN OR THE OTHER DOCUMENTS AND FINANCIAL

INFORMATION INCORPORATED IN THE DISCLOSURE STATEMENT BY REFERENCE, THE PLAN OR THE OTHER DOCUMENTS

AND FINANCIAL INFORMATION, AS THE CASE MAY BE, SHALL GOVERN FOR ALL PURPOSES.

THE STATEMENTS AND FINANCIAL INFORMATION CONTAINED IN THE DISCLOSURE STATEMENT HAVE BEEN MADE

AS OF THE DATE OF THE DISCLOSURE STATEMENT UNLESS OTHERWISE SPECIFIED. HOLDERS OF CLAIMS AND

INTERESTS REVIEWING THE DISCLOSURE STATEMENT SHOULD NOT ASSUME AT THE TIME OF SUCH REVIEW THAT

THERE HAVE BEEN NO CHANGES IN THE FACTS SET FORTH IN THE DISCLOSURE STATEMENT SINCE THE DATE OF THE

DISCLOSURE STATEMENT. EACH HOLDER OF A CLAIM ENTITLED TO VOTE ON THE PLAN SHOULD CAREFULLY REVIEW

THE PLAN, THE DISCLOSURE STATEMENT, AND THE PLAN SUPPLEMENT IN THEIR ENTIRETY BEFORE CASTING A

BALLOT. THE DISCLOSURE STATEMENT DOES NOT CONSTITUTE LEGAL, BUSINESS, FINANCIAL, OR TAX ADVICE.

ANY ENTITIES DESIRING ANY SUCH ADVICE SHOULD CONSULT WITH THEIR OWN ADVISORS.

NO ONE IS AUTHORIZED TO PROVIDE ANY INFORMATION WITH RESPECT TO THE PLAN OTHER THAN THAT WHICH

IS CONTAINED IN THE DISCLOSURE STATEMENT. NO REPRESENTATIONS CONCERNING THE DEBTORS OR THE VALUE

OF THEIR PROPERTY HAVE BEEN AUTHORIZED BY THE DEBTORS OTHER THAN AS SET FORTH IN THE DISCLOSURE

STATEMENT AND THE DOCUMENTS ATTACHED TO THE DISCLOSURE STATEMENT. ANY INFORMATION, REPRESENTATIONS,

OR INDUCEMENTS MADE TO OBTAIN AN ACCEPTANCE OF THE PLAN WHICH ARE OTHER THAN AS SET FORTH, OR

INCONSISTENT WITH, THE INFORMATION CONTAINED IN THE DISCLOSURE STATEMENT, THE DOCUMENTS ATTACHED TO

THE DISCLOSURE STATEMENT, AND THE PLAN SHOULD NOT BE RELIED UPON BY ANY HOLDER OF A CLAIM OR

INTEREST.

WITH RESPECT TO CONTESTED MATTERS, ADVERSARY PROCEEDINGS, AND OTHER PENDING, THREATENED, OR

POTENTIAL LITIGATION OR OTHER ACTIONS, THE DISCLOSURE STATEMENT DOES NOT CONSTITUTE, AND MAY NOT

1

BE CONSTRUED AS, AN ADMISSION OF FACT, LIABILITY, STIPULATION, OR WAIVER, BUT RATHER AS A

STATEMENT MADE IN THE CONTEXT OF SETTLEMENT NEGOTIATIONS PURSUANT TO RULE 408 OF THE FEDERAL RULES

OF EVIDENCE.

THE SECURITIES DESCRIBED IN THE DISCLOSURE STATEMENT TO BE ISSUED PURSUANT TO THE PLAN WILL BE

ISSUED WITHOUT REGISTRATION UNDER THE SECURITIES ACT, AS AMENDED, OR ANY SIMILAR FEDERAL, STATE, OR

LOCAL LAW, GENERALLY IN RELIANCE ON THE EXEMPTIONS SET FORTH IN SECTION 4(2) OF THE SECURITIES ACT

AND/OR SECTION 1145 OF THE BANKRUPTCY CODE.

THE DISCLOSURE STATEMENT HAS NOT BEEN APPROVED OR DISAPPROVED BY THE UNITED STATES SECURITIES

AND EXCHANGE COMMISSION, NOR HAS THE COMMISSION COMMENTED UPON THE ACCURACY OR ADEQUACY OF THE

STATEMENTS CONTAINED IN THE DISCLOSURE STATEMENT.

THE FINANCIAL INFORMATION CONTAINED IN OR INCORPORATED BY REFERENCE INTO THE DISCLOSURE

STATEMENT HAS NOT BEEN AUDITED, EXCEPT AS SPECIFICALLY INDICATED OTHERWISE.

THE FINANCIAL PROJECTIONS, ATTACHED HERETO AS EXHIBIT C AND DESCRIBED IN THE

DISCLOSURE STATEMENT, HAVE BEEN PREPARED BY THE DEBTORS’ MANAGEMENT TOGETHER WITH THEIR ADVISORS.

THE FINANCIAL PROJECTIONS, WHILE PRESENTED WITH NUMERICAL SPECIFICITY, ARE NECESSARILY BASED ON A

VARIETY OF ESTIMATES AND ASSUMPTIONS WHICH, THOUGH CONSIDERED REASONABLE BY THE DEBTORS’ MANAGEMENT

AND THEIR ADVISORS, MAY NOT ULTIMATELY BE REALIZED, AND ARE INHERENTLY SUBJECT TO SIGNIFICANT

BUSINESS, ECONOMIC, COMPETITIVE, INDUSTRY, REGULATORY, MARKET, AND FINANCIAL UNCERTAINTIES AND

CONTINGENCIES, MANY OF WHICH ARE BEYOND THE DEBTORS’ CONTROL. THE DEBTORS CAUTION THAT NO

REPRESENTATIONS CAN BE MADE AS TO THE ACCURACY OF THESE PROJECTIONS OR TO THE ABILITY TO ACHIEVE

THE PROJECTED RESULTS. SOME ASSUMPTIONS INEVITABLY WILL NOT MATERIALIZE. FURTHER, EVENTS AND

CIRCUMSTANCES OCCURRING SUBSEQUENT TO THE DATE ON WHICH THE FINANCIAL PROJECTIONS WERE PREPARED MAY

BE DIFFERENT FROM THOSE ASSUMED OR, ALTERNATIVELY, MAY HAVE BEEN UNANTICIPATED, AND, THUS, THE

OCCURRENCE OF THESE EVENTS MAY AFFECT FINANCIAL RESULTS IN A MATERIALLY ADVERSE OR MATERIALLY

BENEFICIAL MANNER. THEREFORE, THE FINANCIAL PROJECTIONS MAY NOT BE RELIED UPON AS A GUARANTEE OR

OTHER ASSURANCE OF THE ACTUAL RESULTS THAT WILL OCCUR.

PLEASE REFER TO ARTICLE IX OF THE DISCLOSURE STATEMENT, ENTITLED “PLAN-RELATED RISK FACTORS

AND ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF THE PLAN” FOR A DISCUSSION OF CERTAIN FACTORS

THAT A CREDITOR VOTING ON THE PLAN SHOULD CONSIDER.

2

FOR A VOTE ON THE PLAN TO BE COUNTED, THE BALLOT INDICATING ACCEPTANCE OR REJECTION OF THE

PLAN MUST BE RECEIVED BY KURTZMAN CARSON CONSULTANTS, LLC, THE DEBTORS’ CLAIMS AND SOLICITATION

AGENT (“KCC”) NO LATER THAN 5:00 P.M. PREVAILING PACIFIC TIME, ON [•], 2010. SUCH BALLOTS

SHOULD BE CAST IN ACCORDANCE WITH THE SOLICITATION PROCEDURES DESCRIBED IN FURTHER DETAIL IN

ARTICLE III OF THE DISCLOSURE STATEMENT. ANY BALLOT RECEIVED AFTER THE VOTING DEADLINE SHALL NOT BE

COUNTED UNLESS OTHERWISE DETERMINED BY THE DEBTORS IN THEIR SOLE AND ABSOLUTE DISCRETION.

THE CONFIRMATION HEARING WILL COMMENCE ON [•], 2010 AT [•] A.M./P.M. PREVAILING EASTERN TIME,

BEFORE THE HONORABLE CHRISTOPHER S. SONTCHI, UNITED STATES BANKRUPTCY JUDGE, IN THE UNITED STATES

BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE, 824 NORTH MARKET STREET, WILMINGTON, DELAWARE 19801.

THE DEBTORS MAY CONTINUE THE CONFIRMATION HEARING FROM TIME TO TIME WITHOUT FURTHER NOTICE OTHER

THAN AN ADJOURNMENT ANNOUNCED IN OPEN COURT OR A NOTICE OF ADJOURNMENT FILED WITH THE BANKRUPTCY

COURT AND SERVED ON THE MASTER SERVICE LIST AND THE ENTITIES WHO HAVE FILED AN OBJECTION TO THE

PLAN, WITHOUT FURTHER NOTICE TO PARTIES IN INTEREST. THE BANKRUPTCY COURT, IN ITS DISCRETION AND

BEFORE THE CONFIRMATION HEARING, MAY PUT IN PLACE ADDITIONAL PROCEDURES GOVERNING THE CONFIRMATION

HEARING. THE PLAN MAY BE MODIFIED, IF NECESSARY, PRIOR TO, DURING, OR AS A RESULT OF THE

CONFIRMATION HEARING, WITHOUT FURTHER NOTICE TO PARTIES IN INTEREST.

THE PLAN OBJECTION DEADLINE IS [•], 2010, AT 5:00 P.M. PREVAILING EASTERN TIME. ALL PLAN

OBJECTIONS MUST BE FILED WITH THE BANKRUPTCY COURT AND SERVED ON THE DEBTORS AND CERTAIN OTHER

PARTIES IN INTEREST IN ACCORDANCE WITH THE DISCLOSURE STATEMENT ORDER SO THAT THEY ARE RECEIVED ON

OR BEFORE THE PLAN OBJECTION DEADLINE.

3

ARTICLE I.

INTRODUCTION

On May 28, 2009, (the “Petition Date”), the above captioned debtors and debtors in

possession (collectively, the “Debtors,” and with their non-Debtor affiliates,

“Visteon”) filed voluntary petitions for relief under chapter 11 of the Bankruptcy Code in

the United States Bankruptcy Court for the District of Delaware (the “Chapter 11 Cases”).

On May 29, 2009, the Bankruptcy Court entered an order jointly administering the Chapter 11 Cases

pursuant to Bankruptcy Rule 1015(b) under the lead case: Visteon Corporation; Case No. 09-11786.

The Debtors are operating their business and managing their properties as debtors in possession

pursuant to sections 1107(a) and 1108 of the Bankruptcy Code. No trustee has been appointed in the

Chapter 11 Cases. On June 8, 2009, the United States Trustee for the District of Delaware (the

“United States Trustee”) appointed an official committee of unsecured creditors

(the “Creditors’ Committee”) pursuant to section 1102 of title 11 of the United States

Code, 11 U.S.C. §§ 101-1532 (the “Bankruptcy Code”) [Docket No. 178].

The Debtors filed a plan of reorganization and accompanying disclosure statement with the

Bankruptcy Court on December 17, 2009 [Docket Nos. 1475, 1476], a first amended plan of

reorganization and accompanying disclosure statement with the Bankruptcy Court on March 15, 2010

[Docket Nos. 2544, 2545], a second amended plan of reorganization and accompanying disclosure

statement with the Bankruptcy Court on May 7, 2010 [Docket Nos. 3011, 3012], and a third amended

plan of reorganization and accompanying disclosure statement with the Bankruptcy Court on May 24,

2010 [Docket Nos. 3191, 3192]. The Debtors submit this fourth amended disclosure statement (the

“Disclosure Statement”) pursuant to section 1125 of the Bankruptcy Code for purposes of

soliciting votes to accept or reject the Fourth Amended Joint Plan of Reorganization of Visteon

Corporation and its Debtor Affiliates Pursuant to Chapter 11 of the Bankruptcy Code (the

“Plan”), a copy of which is attached to the Disclosure Statement as Exhibit A.2

This Disclosure Statement sets forth certain information regarding the Debtors’

prepetition operations and financial history, their reasons for seeking protection under chapter

11, and significant events that have occurred during the Chapter 11 Cases. This Disclosure

Statement also describes certain terms and provisions of the Plan, certain effects of Confirmation

of the Plan, certain risk factors associated with the Plan and the securities to be issued under

the Plan, and the manner in which distributions will be made under the Plan. In addition, this

Disclosure Statement discusses the requirements for Confirmation of the Plan and the voting

procedures that holders of Claims and Interests entitled to vote on the Plan must follow for their

votes to be counted.

| A. |

|

Rules of Interpretation |

The following rules for interpretation and construction shall apply to the Disclosure

Statement: (1) whenever from the context it is appropriate, each term, whether stated in the

singular or the plural, shall include both the singular and the plural, and pronouns stated in the

|

|

|

| 2 |

|

Capitalized terms used in the Disclosure Statement and not

otherwise defined shall have the meanings ascribed to such terms in Article I.A

of the Plan. |

4

masculine, feminine, or neuter gender shall include the masculine, feminine, and the neuter

gender; (2) unless otherwise specified, any reference in the Disclosure Statement to a contract,

instrument, release, indenture, or other agreement or document being in a particular form or on

particular terms and conditions means that such document shall be substantially in such form or

substantially on such terms and conditions; (3) unless otherwise specified, any reference in the

Disclosure Statement to an existing document, schedule, or exhibit, whether or not filed, shall

mean such document, schedule, or exhibit, as it may have been or may be amended, modified, or

supplemented; (4) any reference to an Entity as a holder of a Claim or Interest includes that

Entity’s successors and assigns; (5) unless otherwise specified, all references in the Disclosure

Statement to Articles are references to Articles of the Disclosure Statement; (6) unless otherwise

specified, all references in the Disclosure Statement to exhibits are references to exhibits to the

Disclosure Statement; (7) the words “herein,” “hereof,” and “hereto” refer to the Disclosure

Statement in its entirety rather than to a particular portion of the Disclosure Statement;

(8) captions and headings to Articles are inserted for convenience of reference only and are not

intended to be a part of or to affect the interpretation of the Disclosure Statement; (9) unless

otherwise set forth in the Disclosure Statement, the rules of construction set forth in section

102 of the Bankruptcy Code shall apply; (10) any term used in capitalized form in the Disclosure

Statement that is not otherwise defined in the Disclosure Statement, Plan, or exhibits to the

Disclosure Statement Order, but that is used in the Bankruptcy Code or the Bankruptcy Rules shall

have the meaning assigned to such term in the Bankruptcy Code or the Bankruptcy Rules, as

applicable; (11) all references to docket numbers of documents filed in the Chapter 11 Cases are

references to the docket numbers under the Bankruptcy Court’s CM/ECF system; (l2) all references to

statutes, regulations, orders, rules of courts, and the like shall mean as amended from time to

time, unless otherwise stated; (13) in computing any period of time prescribed or allowed, the

provisions of Bankruptcy Rule 9006(a) shall apply, and if the date on which a transaction may occur

pursuant to the Disclosure Statement shall occur on a day that is not a Business Day, then such

transaction shall instead occur on the next succeeding Business Day; and (14) unless otherwise

specified, all references in the Disclosure Statement to monetary figures shall refer to currency

of the United States of America.

ARTICLE II.

OVERVIEW OF THE PLAN

| A. |

|

General Structure of the Plan |

The Plan is comprised of two mutually exclusive sub plans—the Rights Offering Sub Plan and the

Claims Conversion Sub Plan (together, the “Sub Plans”). The Plan Support Agreement has

been executed and delivered by holders of more than two-thirds in amount of the 12.25% Senior Notes

Claims and two-thirds in aggregate amount of the 7.00% Senior Notes Claims and the 8.25% Senior

Notes Claims. A separate plan support agreement has also been executed with the Creditors’

Committee (the “Committee Plan Support Agreement”), pursuant to which the Creditors’

Committee will support the Plan, except in certain limited circumstances. Following is a general

description of each Sub Plan.

5

| |

1. |

|

The Rights Offering Sub Plan |

The Debtors will seek to consummate the Rights Offering Sub Plan in the event the following

new capital is raised: (a) $950.0 million through a Rights Offering of New Visteon Common Stock to

holders of 12.25% Senior Notes Claims, 7.00% Senior Notes Claims, and 8.25% Senior Notes Claims

(collectively, the “Note Holders”), who qualify as accredited investors, as such term is

defined in Rule 501(a) of Regulation D of the Securities Act (the “Eligible Holders”),

through a private placement under section 4(2) of the Securities Act; (b) a $300.0 million direct

purchase commitment from the Investors; and (c) the Exit Financing Facility. If the Term Loan

Lenders vote as a Class to accept the Plan, the Term Loan Facility Claims will be paid in full in

Cash. If the Term Loan Lender Class votes to reject the Plan, the Debtors shall have the option

to seek reinstatement of the Term Loan Facility pursuant to section 1124(2) of the Bankruptcy Code,

subject to the reasonable consent of the Requisite Investors, and thereafter pay each holder of the

Allowed Term Loan Facility Claims its Pro Rata portion of an amount in Cash to be determined by the

Debtors (subject to the reasonable consent of the Requisite Investors) (the “Reinstatement

Recovery”). Reinstatement of the Term Loan Facility could provide the Estates with significant

savings through retroactive application of the non-default, LIBOR plus 3.0% interest rate in lieu

of the default interest rate during the pendency of these Chapter 11 Cases. The Debtors would also

have the option to reduce the amount of the Exit Financing Facility dollar-for-dollar by the amount

of the Term Loan Facility that is permanently reinstated under the Plan. If the Debtors are not

successful in reinstating the Term Loan Facility Claims, the Debtors shall satisfy the Term Loan

Facility Claims in full in Cash. Under either scenario, the Term Loan Facility Claims would be

Unimpaired.

Under the Rights Offering Sub Plan, all Note Holders shall be entitled to receive a Pro Rata

distribution of 5.0% of the Distributable Equity, or 4.9% of the Distributable Equity if Class J

votes to accept the Plan, and all Eligible Holders shall be entitled to participate in a Rights

Offering for the remaining 95.0% of New Visteon Common Stock, or 93.1% of New Visteon Common Stock

if Class J votes to accept the Plan.3 Each Non-Eligible Holder, (i.e., a Note Holder not

permitted to participate in a rights offering under section 4(2) of the Securities Act) shall also

receive the lesser of (i) its Pro Rata share of $50.0 million in Cash or (ii) 40.0% of the amount

of such holder’s Allowed Claim in Cash, on account of the value of the Subscription Rights which

such Non-Eligible Holder would have been entitled to had such Non-Eligible Holder been an Eligible

Holder. Holders of the 12.25% Senior Notes Claims will receive additional consideration on

account of guarantees from Visteon Corporation’s wholly-owned domestic operating subsidiaries (the

“Domestic Subsidiary Guarantees”) in the form of their Pro Rata share of warrants to

purchase New Visteon Common Stock on terms described in the warrant agreement attached as

Exhibit B to the Plan (the “Warrant Agreement”). The Cash Recovery Backstop

Investors, a subset of the Investors, shall fund the aggregate Cash Amount provided to Non-Eligible

Holders and, therefore, such Cash distribution will have no impact on the Debtors’ Cash

availability. The Equity Commitment Agreement entered into by the Debtors

|

|

|

| 3 |

|

Under the Rights Offering Sub Plan, Note Holders shall

receive 4.9% of New Visteon Common Stock if Class J votes to accept the Plan or

5.0% of New Visteon Common Stock if Class J votes to reject the Plan. The 4.9%

or 5.0% of New Visteon Common Stock distributed to the Note Holders shall be

subject to dilution from the Management Equity Incentive Program, and if

applicable, the Old Equity Warrants and the 93.1% or 95.0% of New Visteon

Common Stock offered through the Rights Offering shall be subject to dilution

from the Guaranty Equity Amount and the Management Equity Incentive Program,

and if applicable, the Old Equity Warrants. |

6

and Investors in connection with the Rights Offering Sub Plan provides that any shares of New

Visteon Common Stock that are not purchased through the Rights Offering, or distributed to holders

of the 12.25% Senior Notes Claims, as described above, shall be purchased by the Investors subject

to the terms and conditions of the Equity Commitment Agreement.

Holders of General Unsecured Claims against the Debtor Entity Visteon International Holdings,

Inc. (“VIHI”) will be paid in full in Cash due to VIHI’s interest in valuable foreign stock

holding companies and position in the Debtors’ corporate structure, which makes direct Claims

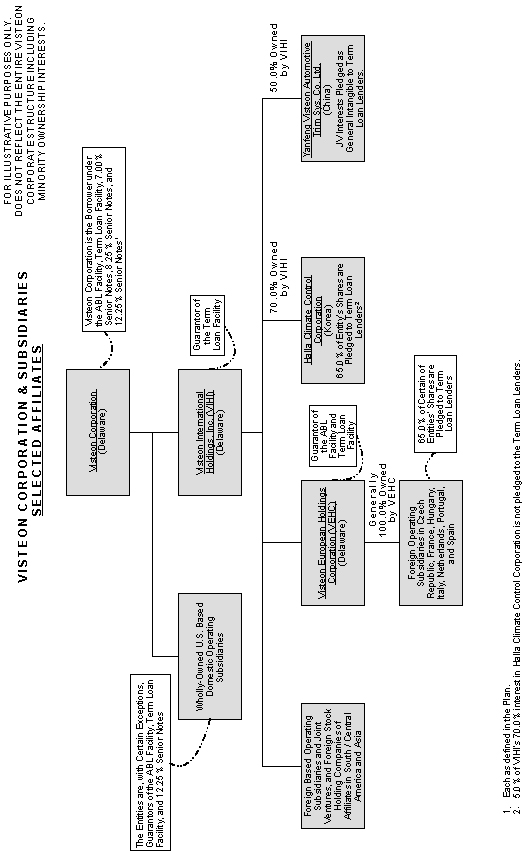

against VIHI structurally superior to other General Unsecured Claims.4 Each remaining

holder of a General Unsecured Claim will receive a Cash recovery equal to the lesser of (x) such

holder’s Pro Rata share of $141.0 million in Cash or (y) 50.0% recovery of the amount of such

holder’s Allowed Class H Claim.

Allowed Class J Interests are not entitled to receive a distribution and shall be deemed

automatically cancelled under the Rights Offering Sub Plan, provided, however, if Class J votes to

accept the Plan, each holder of an Allowed Class J Interest shall receive its Pro Rata portion of

2.0% of the Distributable Equity and Old Equity Warrants to purchase shares of New Visteon Common

Stock at an exercise price of $58.80 per share. Thus, only if Class J Interests accept the

Plan as a Class will Class J Interests receive a distribution. The Rights Offering Sub Plan

also contemplates Reorganized Visteon’s entry into a new $300.0 million working capital facility,

which is projected to be undrawn upon emergence from chapter 11.

| |

2. |

|

The Claims Conversion Sub Plan |

The Plan shall “toggle” from the Rights Offering Sub Plan to the Claims Conversion Sub Plan in

the event sufficient capital is not raised under the Rights Offering Sub Plan to satisfy the Term

Loan Facility Claims in full in Cash. Under the Claims Conversion Sub Plan, Reorganized Visteon

shall issue New Visteon Common Stock to the Term Loan Lenders and the Note Holders in the following

percentages based on their relative priorities and positions in the Debtors’ capital structure:

84.9% to 86.2% the holders of the Term Loan Facility Claims; 6.3% to 6.5% to the holders of the

12.25% Senior Notes Claims; and 7.5% to 8.6% to the holders of the 7.00% Senior Notes Claims and

8.25% Senior Notes Claims. Under the Claims Conversion Sub Plan, holders of General Unsecured

Claims will receive the same recovery provided under the Rights Offering Sub Plan—i.e., the lesser

of (a) such holder’s Pro Rata share of $141.0 million in Cash or (b) 50.0% recovery of the amount

of such holder’s Allowed Class H Claim. General Unsecured Claims against VIHI also will be paid in

Cash in full, subject to a $20.0 million cap.5

Under the Claims Conversion Sub Plan, holders of the Term Loan Facility Claims would receive

the highest percentage of New Visteon Common Stock based on the first Lien they hold against the

Debtors’ most valuable assets, including certain Debtor foreign stock holding

|

|

|

| 4 |

|

The Debtors estimate that there will be a total of $3.4

million in Allowed General Unsecured Claims against VIHI. If however, Allowed

General Unsecured Claims against VIHI exceed $20.0 million, then holders of

such Claims shall receive their Pro Rata share of $20.0 million in Cash.

Article IV.D herein contains a chart which illustrates the structural

superiority of Claims against VIHI as compared to other General Unsecured

Claims that do not have the Domestic Subsidiary Guarantees. |

| |

| 5 |

|

General Unsecured Claims against VIHI shall be satisfied

first, up to $20.0 million, under both the Rights Offering Sub Plan and Claims

Conversion Sub Plan. |

7

companies (the “Foreign Stock Holding Companies”) and at least 65.0% of the Foreign

Stock Holding Companies’ equity interests in their foreign subsidiaries. After the Term Loan

Facility Claims are satisfied in full (including postpetition default interest and fees),6

the Note Holders shall receive the remaining shares of New Visteon Common Stock. Holders of 12.25%

Senior Notes Claims will receive a higher Pro Rata percentage of New Visteon Common Stock than

holders of 7.00% Senior Notes Claims and 8.25% Senior Notes Claims on account of the Domestic

Subsidiary Guarantees. Holders of Interests in Class J will not receive a recovery under the

Claims Conversion Sub Plan and shall be deemed to reject the Plan if the Debtors pursue

Confirmation of the Claims Conversion Sub Plan. The Claims Conversion Sub Plan contemplates

Reorganized Visteon’s entry into a new $150.0 million working capital facility, which is projected

to be undrawn upon emergence from chapter 11.

| |

3. |

|

The Plan Support Agreement |

The Plan Support Agreement entered into in connection with the Plan by and among the Debtors

and the Consenting Note Holders (in sufficient number and holdings to assure their respective

Classes’ acceptance of the Plan) provides that the parties thereto shall support the Plan in all

aspects, including the findings of the valuation analysis prepared by the Debtors and their

advisors, as described in further detail in Article VIII.D (the “Valuation Analysis”).

In certain limited circumstances, the Consenting Note Holders have the right to terminate the

Plan Support Agreement and withdraw their support for the Plan. Those termination rights are

enumerated in Section 7.1 of the Plan Support Agreement. For example, under Section 7.1(e)(2) of

the Plan Support Agreement, the Consenting Note Holders may terminate the Plan Support Agreement

and shall not be required to support the Plan if (a) the representations and warranties made by the

Debtors in connection with the Equity Commitment Agreement fail to be true and correct so as to be

reasonably expected to result in a Material Adverse Effect, as such term is defined in the Equity

Commitment Agreement, or (b) the Debtors fail to materially perform or comply with any covenants

contained in the Equity Commitment Agreement. The Plan Support Agreement permits the Debtors to

commence expedited proceedings in the Bankruptcy Court to determine whether a termination event has

actually occurred under the Plan Support Agreement. Furthermore, if the Consenting Note Holders

were to terminate the Plan Support Agreement pursuant to Section 7.1(e) thereof after the Debtors

have solicited votes on the Plan, the Debtors shall not be required to re-solicit, but the

Consenting Note Holders shall be deemed to have rejected the Plan and may also formally object to

Confirmation of the Plan.

On the other hand, if the representations and warranties made by the Investors in connection

with the Equity Commitment Agreement fail to be true and correct so as to be reasonably expected to

prohibit, materially delay or materially and adversely impact the Investors’ performance of their

obligations under the Equity Commitment Agreement, or the Investors fail to materially perform or

comply with any covenants contained in the Equity Commitment Agreement, the Debtors may terminate

the Equity Commitment Agreement and proceed with Confirmation of the Claims Conversion Sub Plan.

The Debtors may also terminate

|

|

|

| 6 |

|

The estimated Allowed amount of the Term Loan Facility

Claims is $1.629 billion, including postpetition interest at the default rate.

To the extent Class E votes to reject the Plan and the Debtors succeed in

reinstating the Term Loan Facility Claims, the Allowed amount of the Term Loan

Facility Claims may be calculated at the non-default interest rate in lieu of

the default interest rate. |

8

the Equity Commitment Agreement and proceed with Confirmation of the Claims Conversion Sub

Plan if the Investors, together with the proceeds from the Rights Offering, do not deliver the

capital contemplated by the Rights Offering Sub Plan. Under the circumstances described above, the

Consenting Note Holders would remain bound by the Plan Support Agreement and would thus be required

to support Confirmation of the Claims Conversion Sub Plan. Lastly, if the Equity Commitment

Agreement fails to close within the timeframe specified in section 10.1(b)(iii) of the Equity

Commitment Agreement, the Debtors may terminate the Equity Commitment Agreement and proceed with

Confirmation of the Claims Conversion Sub Plan with the Consenting Note Holders’ support secured

pursuant to the Plan Support Agreement.

| |

4. |

|

The Committee Plan Support Agreement |

The Committee Plan Support Agreement obligates the Creditors’ Committee, subject to its

exercise of a fiduciary out and certain conditions, to (a) support entry of an order approving the

Disclosure Statement; (b) prepare a recommendation letter supporting the Plan for inclusion in

Visteon’s solicitation package; and (c) support confirmation of the Plan. However, the Creditors’

Committee may terminate the Committee Plan Support Agreement if (i) the Debtors’ chapter 11 cases

are dismissed or converted to chapter 7 cases, (ii) an examiner with expanded powers or a trustee

under chapter 7 or chapter 11 is appointed, (iii) the Debtors withdraw the Plan, (iv) any court has

by final, non-appealable order declared the Committee Plan Support Agreement unenforceable, or (v)

there is a materially adverse change or modification to the Plan or a related document without the

Creditors’ Committee’s consent. Also, the Committee Plan Support Agreement terminates

automatically if the Note Holder Plan Support Agreement is terminated under certain conditions.

The Term Loan Lenders believe the proposed agreements (x) contain no definitive date by which

the new capital must be delivered, (y) excuse the Investors from any liability for breach of their

commitments, and (z) would likely suspend confirmation in the event the Investors or Note Holders

litigate regarding the toggle. The Debtors believe the Term Loan Lenders completely misinterpret

the Equity Commitment Agreement and Plan Support Agreement and disagree with the Term Loan Lenders’

assertions.

| B. |

|

Treatment of Claims and Interests |

The Plan divides all Claims (except Administrative Claims, Professional Claims, DIP Facility

Claims, and Priority Tax Claims) and all Interests into various Classes. Listed below is a summary

of the Classes of Claims and Interests under the Plan.

| |

|

|

| Class |

|

Claim or Interest |

| A

|

|

ABL Claims |

| B

|

|

Secured Tax Claims |

| C

|

|

Other Secured Claims |

| D

|

|

Other Priority Claims |

| E

|

|

Term Loan Facility Claims |

| F

|

|

7.00% Senior Notes Claims and 8.25% Senior Notes Claims |

| G

|

|

12.25% Senior Notes Claims |

9

| |

|

|

| Class |

|

Claim or Interest |

H

|

|

General Unsecured Claims |

I

|

|

Intercompany Claims |

J

|

|

Interests in Visteon Corporation |

K

|

|

Intercompany Interests |

L

|

|

Section 510(b) Claims |

2. Unclassified Claims

In accordance with section 1123(a)(1) of the Bankruptcy Code, the Plan does not classify

Administrative Claims, Professional Claims, DIP Facility Claims, or Priority Tax Claims. These

Claims are therefore excluded from the Classes of Claims set forth in Article III of the Plan.

| |

|

|

|

|

|

|

|

|

| |

|

|

|

Estimated Aggregate |

|

Estimated Aggregate |

|

Projected |

| |

|

|

|

Amount of Allowed |

|

Amount of Allowed |

|

Recovery |

| |

|

|

|

Claims Under Rights |

|

Claims Under Claims |

|

Under the |

| Claim |

|

Plan Treatment |

|

Offering Sub Plan |

|

Conversion Sub Plan |

|

Plan |

| |

Administrative and |

|

Paid in full in Cash. |

|

$225.0

million7 |

|

$105.0 million |

|

100% |

Professional Claims |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DIP Facility |

|

Paid in full in |

|

$75.0 million |

|

$75.0 million |

|

100% |

Claims |

|

Cash, unless otherwise |

|

|

|

|

|

|

|

|

agreed. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Priority Tax |

|

Paid in full in Cash. |

|

$5.3 million |

|

$5.3 million |

|

100% |

Claims |

|

|

|

|

|

|

|

|

C. Treatment of Claims and Interests Under the Plan

The table below summarizes the Classes of Claims and Interests under the Plan, the treatment

of such Classes, the voting rights of such Classes, and the projected recovery, if any, under each

Sub Plan for such Classes. To the extent of any inconsistency between the summaries contained in

the Disclosure Statement and those set forth in the Plan, the Plan shall govern. These projected

recoveries are based upon certain assumptions contained in the Valuation Analysis. As more fully

described below, the Debtors’ assumed reorganization value of the New Visteon Common Stock was

derived from commonly accepted valuation techniques and is not an estimate of the trading value for

such securities.

|

|

|

| 7 |

|

The estimate of Allowed Administrative Claims and

Professional Claims does not include amounts paid by the Debtors in the

ordinary course of business during the Chapter 11 Cases. Included within the

estimate of Administrative Claims and Professional Claims under the Rights

Offering Sub Plan are approximately $120.0 million in fees that would be

incurred in connection with the Rights Offering, which include fees to be paid

pursuant to the Equity Commitment Agreement together with other professional

fees to be paid by the Debtors, $50.0 million in Professional Claims, $25.0

million in Cure payments, and $30.0 million in 503(b)(9) Claims. Included

within the estimate of Administrative Claims and Professional Claims under the

Claims Conversion Sub Plan are $50.0 million in Professional Claims, $25.0

million in Cure payments, and $30.0 million in 503(b)(9) Claim. |

10

The Debtors have not completed full reconciliation of the Class H General Unsecured Claims and

have accordingly developed low and high-end ranges of estimates for the ultimate amount of Allowed

General Unsecured Claims, as set forth below. The amount of Allowed General Unsecured Claims will

impact the Cash availability of the Debtors and, in turn, the value of the New Visteon Common Stock

to be distributed to the Note Holders under the Rights Offering Sub Plan and the Note Holders and

Term Loan Lenders under the Claims Conversion

Sub Plan. The range of estimates for the Class H General Unsecured Claims is based upon a

number of assumptions, including, the following.

1. Low-End Claims Estimate

The Debtors’ low-end estimate of Allowed Class H General Unsecured Claims assumes, among other

things, that: (a) no Claims will be Allowed against the Debtors on account of the Visteon UK

Pension Plan (the “VUK Pension Plan”), as such Claims have been withdrawn by the claimants,

or the Visteon Engineering Services Pension Plan (the “VES Pension Plan”); (b) no Claims

will be Allowed against the Debtors on account of the termination of the Visteon Corporation

Supplemental Executive Retirement Plan (the “SERP”), the Visteon Corporation Pension Parity

Plan (the “PPP”), and the Visteon Corporation Executive Separation Allowance Plan (the

“ESAP”); (c) certain customer Claims, including warranty and services contract Claims, will

not ultimately be Allowed based on mutually agreed to contractual amendments or Claim waivers; and

(d) contingent litigation Claims will be resolved in amounts at the low-end of possible litigation

outcomes.

8

2. High-End Claims Estimate

In contrast, the high-end estimates for Allowed Class H General Unsecured Claims assume

maximum liability for a number of contingent, unliquidated, and Disputed Claims including (a)

Allowed Claims for approximately $30.9 million against the Debtors on account of the termination of

the SERP, PPP, and ESAP and (b) certain litigation related Claims will be Allowed at the high-range

of possible litigation outcomes (but not at the face amount stated on the relevant Proof of

Claim).9

Neither the high nor the low-end estimates on which the recoveries stated below

are based project allowance of any Claims on account of the VUK Pension Plan, the VES Pension Plan,

and certain customer contract and warranty Claims.

Holders of Class H General Unsecured Claims are projected to receive a 50.0% recovery on their

Claims based on the Debtors’ Claims estimate. However, to the extent the amount of Allowed Class

H General Unsecured Claims exceeds $282.0 million, a 69.0% increase over the Debtors’ high-end

Claims projection, holders of Allowed Class H General Unsecured Claims would receive less than a

50.0% recovery on their Claims.

|

|

|

|

8 |

|

The VUK Pension Plan and VES Pension Plan are discussed

further in Article V.I. The SERP, PPP, and ESAP are discussed further in Article IV.H. |

| |

|

9 |

|

The Claims arising from agreements with Ford are discussed further in Article V.F. |

11

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Rights Offering Sub Plan |

|

Claims Conversion Sub Plan |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated |

| |

|

|

|

|

|

|

|

Estimated |

|

|

|

Range of |

| |

|

|

|

Estimated Range |

|

|

|

Range of % |

|

|

|

% |

| |

|

Type of Claim |

|

of Allowed |

|

|

|

Recovery of |

|

|

|

Recovery |

| |

|

or Equity |

|

Claims or |

|

Treatment of |

|

under the |

|

Treatment of |

|

of under |

| Class |

|

Interest |

|

Interests |

|

Claim/Interest |

|

Plan |

|

Claim/Interest |

|

the

Plan10 |

A

|

|

ABL Claims

|

|

$127.15 million

|

|

Paid in full in Cash.

|

|

|

100 |

% |

|

Paid in full in

Cash.

|

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B

|

|

Secured Tax Claims

|

|

$2.5 million

|

|

Paid in full in Cash.

|

|

|

100 |

% |

|

Paid in full in

Cash.

|

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C

|

|

Other Secured Claims

|

|

$2.85 million

|

|

Paid in full in Cash.

|

|

|

100 |

% |

|

Paid in full in

Cash.

|

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D

|

|

Other Priority

Claims

|

|

$0.01 million

|

|

Paid in full in Cash.

|

|

|

100 |

% |

|

Paid in full in

Cash.

|

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E

|

|

Term Loan Facility

Claims

|

|

$1.629 billion11

|

|

Paid in full in

Cash if Class E

accepts the Plan.

|

|

|

100 |

% |

|

Pro Rata share of

85.0% – 86.2% of

shares of New

Visteon Common Stock.

|

|

|

100 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Subject to the

Reinstatement

Recovery if Class E

rejects the Plan. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

The estimated Claim recoveries provided in this Disclosure

Statement do not account for dilution by the Management Equity Incentive Program. |

| |

|

11 |

|

The estimated Allowed amount of the Term Loan Facility

Claims includes postpetition interest at the default rate. To the extent Class

E votes to reject the Plan and the Debtors succeed in reinstating the Term Loan

Facility Claims, the Allowed amount of the Term Loan Facility Claims may be

calculated at the base interest rate in lieu of the default interest rate. |

12

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Rights Offering Sub Plan |

|

Claims Conversion Sub Plan |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated |

| |

|

|

|

|

|

|

|

Estimated |

|

|

|

Range of |

| |

|

|

|

Estimated Range |

|

|

|

Range of % |

|

|

|

% |

| |

|

Type of Claim |

|

of Allowed |

|

|

|

Recovery of |

|

|

|

Recovery |

| |

|

or Equity |

|

Claims or |

|

Treatment of |

|

under the |

|

Treatment of |

|

of under |

| Class |

|

Interest |

|

Interests |

|

Claim/Interest |

|

Plan |

|

Claim/Interest |

|

the

Plan |

F

|

|

7.00% Senior Notes Claims and

8.25% Senior Notes Claims

|

|

$668.23 million

|

|

For Eligible

Holders, (i) Pro

Rata Allocation of

4.9% or 5.0% of the

Distributable Equity

and (ii) Pro Rata

Allocation of

Subscription

Rights.12

|

|

7.9% – 8.2%

(for Eligible

Holders)

|

|

Pro Rata share of

7.5% – 8.6% of

shares of New

Visteon Common

Stock.

|

|

21.0% – 25.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For

Non-Eligible

Holders, (i) Pro

Rata Allocation of

4.9% or 5.0% of the

Distributable Equity

and (ii) the Cash

Amount.

|

|

48.16% – 48.2%

(for Non-Eligible

Holders) |

|

|

|

|

|

|

|

| 12 |

|

The estimated range of recovery for Eligible Holders in

Class F reflects an approximate $0.34 per share discount to $0.15 per

share premium (if Class J Interests vote to accept the Plan) or $0.41 to

$0.91 per share discount (if Class J Interests vote to reject the Plan) at

which New Visteon Common Stock may be purchased upon an Eligible Holder’s

exercise of Subscription Rights at $27.69 per share as compared to the

Plan’s valuation of the New Visteon Common Stock at $27.54 per share under

the high-end Claims estimate and $28.03 per share under the low-end Claims

estimate, or $28.10 per share under the high-end Claims estimate and

$28.60 per share under the low-end Claims estimate (depending on whether

Class J Interests vote to accept the Plan). If Class J votes to reject

the Plan, holders of Allowed Class F Claims would receive 5.0%, instead of

4.9%, of the Distributable Equity Value in Reorganized Visteon. |

13

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Rights Offering Sub Plan |

|

Claims Conversion Sub Plan |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated |

| |

|

|

|

|

|

|

|

Estimated |

|

|

|

Range of |

| |

|

|

|

Estimated Range |

|

|

|

Range of % |

|

|

|

% |

| |

|

Type of Claim |

|

of Allowed |

|

|

|

Recovery of |

|

|

|

Recovery |

| |

|

or Equity |

|

Claims or |

|

Treatment of |

|

under the |

|

Treatment of |

|

of under |

| Class |

|

Interest |

|

Interests |

|

Claim/Interest |

|

Plan |

|

Claim/Interest |

|

the

Plan |

G

|

|

12.25% Senior Note Claims

|

|

$202.36 million

|

|

For Eligible

Holders, (i) Pro

Rata Allocation of

4.9% or 5.0% of the

Distributable

Equity, (ii) Pro

Rata Allocation of

Subscription Rights,

and (iii) Pro Rata

portion of the

Guaranty Equity

Amount.13

|

|

28.7% – 30.3%

(for Eligible

Holders)

|

|

Pro Rata share of

6.3% – 6.5% shares

of New Visteon

Common Stock.

|

|

|

58.0 – 62.0 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For

Non-Eligible

Holders, (i) Pro

Rata Allocation of

4.9% or 5.0% of the

Distributable

Equity, (ii) the

Cash Amount, and

(iii) the Pro Rata

portion of the

Guaranty Equity

Amount.

|

|

69.5% – 70.3%

(for Non-Eligible

Holders)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H

|

|

General Unsecured Claims

|

|

$107.96 million –

$166.76 million

|

|

The lesser of: (i)

the Pro Rata share

of $141.0 million or

(ii) 50.0% recovery

of the amount of

such holder’s

Allowed Class H

Claim.14

|

|

|

50.0 |

% |

|

The lesser of: (i)

the Pro Rata share

of $141.0 million

or (ii) 50%

recovery of the

amount of such

holder’s Allowed

Class H Claim.

|

|

|

50.0 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I

|

|

Intercompany Claims

|

|

$16.39 billion

|

|

No recovery, but may

be reinstated in the

discretion of the

Reorganized Debtors.

|

|

|

N/A |

|

|

No recovery, but

may be reinstated

in the discretion

of the Reorganized

Debtors.

|

|

|

N/A |

|

|

|

|

| 13 |

|

The estimated range of recovery for Eligible Holders in

Class G reflects an approximate $0.34 per share discount to $0.15 per share

premium (if Class J Interests vote to accept the Plan) or $0.41 to $0.91 per

share discount (if Class J Interests vote to reject the Plan) at which New

Visteon Common Stock may be purchased upon an Eligible Holder’s exercise of

Subscription Rights at $27.69 per share as compared to the Plan’s valuation of

the New Visteon Common Stock at $27.54 per share under the high-end Claims

estimate and $28.03 per share under the low-end Claims estimate, or $28.10 per

share under the high-end Claims estimate and $28.60 per share under the low-end

Claims estimate (depending on whether Class J Interests vote to accept the

Plan). If Class J votes to reject the Plan, holders of Allowed Class G Claims

would receive 5.0%, instead of 4.9%, of the Distributable Equity Value in

Reorganized Visteon. |

| |

| 14 |

|

General Unsecured Claims against VIHI shall be satisfied

first, up to $20.0 million, under both the Rights Offering Sub Plan and Claims Conversion Sub Plan. |

14

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Rights Offering Sub Plan |

|

Claims Conversion Sub Plan |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated |

| |

|

|

|

|

|

|

|

Estimated |

|

|

|

Range of |

| |

|

|

|

Estimated Range |

|

|

|

Range of % |

|

|

|

% |

| |

|

Type of Claim |

|

of Allowed |

|

|

|

Recovery of |

|

|

|

Recovery |

| |

|

or Equity |

|

Claims or |

|

Treatment of |

|

under the |

|

Treatment of |

|

of under |

| Class |

|

Interest |

|

Interests |

|

Claim/Interest |

|

Plan |

|

Claim/Interest |

|

the

Plan |

J

|

|

Interests in Visteon

Corporation15

|

|

N/A

|

|

Cancelled, provided,

however, if Class J

accepts the Plan,

Pro Rata share of

(i) 2.0% of the

Distributable Equity

and (ii) the Old

Equity Warrants.

|

|

|

N/A |

|

|

Cancelled.

|

|

|

0.0 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

K

|

|

Intercompany Interests

|

|

N/A

|

|

No recovery, but may

be reinstated in the

discretion of the

Reorganized Debtors.

|

|

|

N/A |

|

|

No recovery, but

may be reinstated

in the discretion

of the Reorganized

Debtors.

|

|

|

N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

L

|

|

Section 510(b) Claims

|

|

N/A

|

|

No recovery.

|

|

|

0.0 |

% |

|

No recovery.

|

|

|

0.0 |

% |

The Debtors’ Claims and Solicitation Agent has received approximately 3,300 Proofs of

Claim totaling approximately $7.9 billion (excluding Intercompany Claims). Approximately 55 Proofs

of Claim, totaling approximately $5.9 billion, represent the Term Loan Facility Claims, the 7.00%

Senior Notes Claims, the 8.25% Senior Notes Claims, and the 12.25% Senior Notes Claims for which

the Debtors have recorded approximately $2.5 billion in aggregate liability. The Debtors believe

the Claim amounts in excess of $2.5 billion are duplicative and will ultimately be resolved through

the Plan or omnibus objections to Claims. Additionally, Proofs of Claims in the amount of $1.064

billion, which were filed on account of pension termination liabilities will be disallowed because

the Pension Plans are to be maintained by the Reorganized Debtors. Lastly, the Debtors believe that

approximately 530 Proofs of Claim, totaling approximately $240.0 million, will ultimately be

disallowed by the Bankruptcy Court primarily because these Claims appear to be duplicative or

unsubstantiated. While the Debtors have not reconciled all filed Proofs of Claim against their

books and records, they believe that many of the remaining filed Proofs of Claim are invalid,

untimely, duplicative, or overstated, and, therefore, have assumed for purposes of estimating

recoveries that such Claims shall be reduced in amount or expunged from the Claims Register. On

the other hand, additional Proofs of Claim may be filed after the Bar Date, which could be Allowed

by the Bankruptcy Court. Accordingly, the ultimate number and Allowed amount of Claims asserted

against the Debtors are not presently known and the final resolution of such Claims could result in

a material adjustment to the recoveries and Claim estimates provided above.

|

|

|

| 15 |

|

Two percent of the Distributable Equity equates to

approximately $27.3 million to $27.7 million in value to be distributed to

Class J Interests at the Plan’s value, if Class J accepts the Plan. In

addition, the Old Equity Warrants also are estimated to be worth approximately

$7.2 million based on Black-Scholes calculation. |

15

D. Liquidation and Valuation Analyses

The Debtors believe that each of the Sub Plans provides the same or a greater recovery for

holders of Allowed Claims and Interests as would be achieved in a liquidation pursuant to chapter 7

of the Bankruptcy Code because of, among other things, the additional Administrative Claims

generated by conversion to a chapter 7 case, the administrative costs of liquidation and associated

delays in connection with a chapter 7 liquidation, and the negative impact on the

market for the Debtors’ assets caused by attempting to sell a large number of assets in a

short time frame, each of which likely would diminish the value of the Debtors’ assets available

for distributions.

The Debtors have prepared liquidation analyses, attached hereto as Exhibit D and

discussed in Article VIII.C (the “Liquidation Analyses”), and a Valuation Analysis to

assist holders of Claims and Interests in evaluating each of the Sub Plans. The Liquidation

Analyses were prepared in connection with the filing of the plan of reorganization on March 15,

2010 but have been updated to reflect a later Effective Date and other variables dependent upon

timing. The Liquidation Analyses compare the Creditor recoveries to be realized if the Debtors

were to be liquidated in a hypothetical case under chapter 7 of the Bankruptcy Code with the

distributions to holders of Allowed Claims and Interests under each of the Sub Plans. The analyses

are based upon the value of the Debtors’ assets and liabilities as of a certain date, and

incorporate various estimates and assumptions, including a hypothetical conversion to a chapter 7

liquidation as of a certain date. Further, each analysis is subject to potentially material

changes including with respect to economic and business conditions and legal rulings. Therefore,

the actual liquidation value of the Debtors could vary materially from the estimates provided in

the Liquidation Analyses, and the actual total enterprise value and reorganization equity value of

the Reorganized Debtors could vary materially from the estimates contained in the Valuation

Analysis.

E. Certain Factors to Be Considered Prior to Voting

There are a variety of factors that all holders of Claims entitled to vote on the Plan should

consider prior to voting to accept or reject the Plan. Some of these factors, which are described

in more detail in Article IX and Article X, are as follows and may impact recoveries under the

Plan:

| |

• |

|

Unless otherwise specifically indicated, the financial information contained in

the Disclosure Statement has not been audited and is based on an analysis of data

available at the time of the preparation of the Plan and Disclosure Statement. |

| |

| |

• |

|

Article X describes certain significant federal tax consequences of the

transactions contemplated by the Plan that may affect the Debtors, including the

realization of cancellation of indebtedness income, reduction of net operating loss

(“NOL”) carryforwards and unrealized built-in losses, and the limitations that

may apply to the Debtors’ usage of those NOLs and unrealized built-in-losses. Article

X also describes the federal tax consequences of the transactions contemplated by the

Plan that may affect holders of Claims and Interests, including the recognition of

taxable income by such holders. Holders of Claims and Interests are urged to |

16

| |

|

|

consult

with their own tax advisors regarding the federal, state, local, and foreign tax

consequences of the Plan. |

| |

• |

|

Although the Debtors believe that the Plan complies with all applicable

provisions of the Bankruptcy Code, the Debtors cannot assure such compliance nor that

the Bankruptcy Court will confirm the Plan. |

| |

| |

• |

|

The Debtors may request Confirmation without the acceptance of all Impaired

Classes entitled to vote in accordance with section 1129(b) of the Bankruptcy Code. |

| |

| |

• |

|

Any delays of either Confirmation or Consummation could result in, among other

things, increased Administrative Claims and Professional Claims. |

| |

| |

• |

|

Only if Class J Interests vote as a Class to accept the Plan, and the Debtors

pursue Confirmation of the Rights Offering Sub Plan, will Class J Interests receive a

distribution under the Plan. |

| |

| |

• |

|

If holders of Class E Term Loan Facility Claims vote as a Class to reject the

Plan, and the Debtors pursue Confirmation of the Rights Offering Sub Plan, the Term

Loan Facility Claims may be subject to the Reinstatement Recovery at the Debtors’

discretion and subject to the reasonable consent of the Requisite Investors. |

While these factors could affect distributions available to holders of Allowed Claims under

the Plan, the occurrence or impact of such factors will not necessarily affect the validity of the

vote of the Impaired Classes entitled to vote to accept or reject the Plan (the “Voting

Classes”) or necessarily require a re-solicitation of the votes of holders of Claims in such

Voting Classes.

AS DESCRIBED FURTHER IN ARTICLE VI.M.1.I HEREIN, HOLDERS OF ALLOWED CLAIMS THAT WOULD BE IN

VIOLATION OF ANY APPLICABLE LAWS OR REGULATIONS OF ANY APPLICABLE GOVERNMENTAL UNIT AS A RESULT OF

THE RECEIPT OF SHARES OF NEW VISTEON COMMON STOCK PURSUANT TO THE PLAN SHALL NOT BE ENTITLED TO

RECEIVE SUCH SHARES UNLESS AND UNTIL SUCH HOLDERS ARE IN COMPLIANCE WITH ANY SUCH APPLICABLE LAWS

OR REGULATIONS OF ANY APPLICABLE GOVERNMENTAL UNIT.

17

ARTICLE III.

VOTING AND RIGHTS OFFERING SUBSCRIPTION PROCEDURES

The following Classes are the only Classes entitled to vote to accept or reject the Plan:

| |

|

|

|

|

|

|

| |

|

|

|

|

|

Status Under the |

| |

|

|

|

Status Under Rights |

|

Claims Conversion |

| Class |

|

Claim or Interest |

|

Offering Sub Plan |

|

Sub Plan |

E

|

|

Term Loan Facility Claims

|

|

Unimpaired

|

|

Impaired |

F

|

|

7.00% Senior Notes Claims and

8.25% Senior Notes Claims

|

|

Impaired

|

|

Impaired |

G

|

|

12.25% Senior Notes Claims

|

|

Impaired

|

|

Impaired |

H

|

|

General Unsecured Claims

|

|

Impaired

|

|

Impaired |

J

|

|

Interests in Visteon Corporation

|

|

Impaired

|

|

Impaired |

If your Claim or Interest is not included in these Classes, you are not entitled to vote

and you will not receive a Solicitation

Package.16

A. Vote Required for Acceptance by a Class

Under the Bankruptcy Code, acceptance of a plan of reorganization by a Class of Claims or

Interests is determined by calculating the number and the amount of Claims or Interests voting to

accept, based on the actual total Allowed Claims or Interests voting on the Plan. Acceptance by a

Class requires more than one-half of the number of total Allowed Claims or Interests in the Class

to vote in favor of the Plan and at least two-thirds in dollar amount of the total Allowed Claims

or Interests in the Class to vote in favor of the Plan.

B. Classes Not Entitled to Vote

Under the Bankruptcy Code, Creditors are not entitled to vote if their contractual rights are

Unimpaired by the Plan or if they will receive no distribution of property under the Plan. All

non-voting Classes of Claims or Interests shall receive the same recovery under the Rights Offering

Sub Plan and Claims Conversion Sub Plan. Based on this standard, the following Classes will not be

entitled to vote on the Plan:

| |

|

|

|

|

|

|

| Class |

|

Claim or Interest |

|

Status |

|

Voting Rights |

A

|

|

ABL Claims

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

B

|

|

Secured Tax Claims

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

C

|

|

Other Secured Claims

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

D

|

|

Other Priority Claims

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

I

|

|

Intercompany Claims

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

K

|

|

Intercompany Interests

|

|

Unimpaired

|

|

Conclusively

Presumed to Accept |

L

|

|

Section 510(b) Claims

|

|

Impaired

|

|

Deemed to Reject |

|

|

|

| 16 |

|

Capitalized terms used in this Article III but not defined

in the Disclosure Statement or the Plan shall have the meanings ascribed to

them in the Solicitation Procedures attached as Exhibit 5 to the

Disclosure Statement Order, to be attached hereto as Exhibit B once

approved. |

18

C. Solicitation Procedures

| |

1. |

|

Claims and Solicitation Agent |

The Debtors retained KCC to, among other things, act as Claims and Solicitation Agent in

connection with the solicitation of votes to accept or reject the Plan.

The following materials shall constitute the Solicitation Package:

| |

• |

|