Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Diversified Restaurant Holdings, Inc. | c98386exv31w1.htm |

| EX-32.2 - EXHIBIT 32.2 - Diversified Restaurant Holdings, Inc. | c98386exv32w2.htm |

| EX-31.2 - EXHIBIT 31.2 - Diversified Restaurant Holdings, Inc. | c98386exv31w2.htm |

| EX-32.1 - EXHIBIT 32.1 - Diversified Restaurant Holdings, Inc. | c98386exv32w1.htm |

| EX-10.24 - EXHIBIT 10.24 - Diversified Restaurant Holdings, Inc. | c98386exv10w24.htm |

Table of Contents

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| þ | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 27, 2009

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 000-53577

DIVERSIFIED RESTAURANT HOLDINGS, INC.

(Exact name of small business issuer as specified in its charter)

| Nevada | 03-0606420 | |

| (State of other jurisdiction of Incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 27680 Franklin Rd. Southfield, MI |

48034 | |

| (Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code:

(248) 223-9160

(248) 223-9160

Securities registered under Section 12(b) of the Exchange Act:

None.

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $.0001 par value per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of

the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or

Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its

corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K

(§229.405) is not contained herein, and will not be contained, to the best of registrant’s

knowledge, in definitive proxy or information statements incorporated by reference in Part III of

this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated

filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o | Smaller reporting company þ | |||

| (Do not check if a smaller reporting company) |

||||||

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the

Act). Yes o No þ

State the aggregate market value of the voting and non-voting common equity held by non-affiliates

computed by reference to the price at which the common equity was last sold, or the average bid and

asked prices of such common equity, as of the last business day of the registrant’s most recently

completed second fiscal quarter.

5,806,521 common shares @ $5.25* = $30,484,235.25

* Average of bid and ask closing prices on June 30, 2009.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING

THE PRECEDING FIVE YEARS

THE PRECEDING FIVE YEARS

Indicate by check mark whether the registrant has filed all documents and reports required to be

filed by Section 12, 13, or 15(d) of the Securities Exchange Act of 1934 subsequent to the

distribution of securities under a plan confirmed by a court.

Yes o No o

Yes o No o

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as

of the latest practicable date.

18,876,000 common shares issued and outstanding as of March 26, 2010

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the Proxy Statement of the Issuer for its June 3, 2010 Annual Meeting of Shareholders

are incorporated by reference into Part III of this Annual Report.

TABLE OF CONTENTS

| Page | ||||||||

| 1 | ||||||||

| 1 | ||||||||

| 10 | ||||||||

| 16 | ||||||||

| 17 | ||||||||

| 17 | ||||||||

| 17 | ||||||||

| 17 | ||||||||

| 18 | ||||||||

| 18 | ||||||||

| 18 | ||||||||

| 18 | ||||||||

| 19 | ||||||||

| 19 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 20 | ||||||||

| 21 | ||||||||

| 21 | ||||||||

| Exhibit 10.24 | ||||||||

| Exhibit 31.1 | ||||||||

| Exhibit 31.2 | ||||||||

| Exhibit 32.1 | ||||||||

| Exhibit 32.2 | ||||||||

Table of Contents

PART I

The Registrant, Diversified Restaurant Holdings, Inc. and its subsidiaries are referred to in

this Annual Report on Form 10-K (“Annual Report”) as “Diversified”, “DRH”, “Company”, or in the

nominative “we” or “us” or the possessive

“our.”

Cautionary Statement Regarding Forward Looking Information

Certain statements contained in this Annual Report are “forward-looking statements” within the

meaning of the U.S. Private Securities Litigation Reform Act of 1995. All forward-looking

statements involve risks and uncertainties. All statements contained herein that are not clearly

historical in nature are forward-looking, and the word “anticipate,” “believe,” “expect,”

“estimate,” “project,” and similar expressions are generally intended to identify forward looking

statements. Any forward looking statement contained herein, in press releases, written statements

or other documents filed with the Securities and Exchange Commission, or in DRH’s communications

and discussions with investors and analysts in the normal course of business through meetings,

webcasts, phone calls and conference calls, regarding expectations with respect to sales, earnings,

cash flows, operating efficiencies, store openings, acquisitions, franchise sales, commodity

pricing, labor costs, or developments with respect to litigation or litigation costs are subject to

known and unknown risks, uncertainties and contingencies. Many of these risks, uncertainties, and

contingencies are beyond our control, and may cause actual results, performance or achievements to

differ materially from anticipated results, performance or achievements. Factors that might affect

such forward-looking statements include, among other things:

| • | Overall economic and business conditions; |

||

| • | The success of our marketing and other initiatives to attract customers; |

||

| • | Customer preferences; |

||

| • | Competitive factors in the restaurant industry; |

||

| • | Changes in tax requirements (including tax rate changes, new tax laws and revised tax

law interpretations); |

||

| • | Fluctuations in costs of commodities; |

||

| • | The internal and external costs of compliance with laws and regulations such as Section

404 of the Sarbanes-Oxley Act of 2002; and |

||

| • | Litigation against the Company. |

ITEM 1. BUSINESS

Introduction

Diversified Restaurant Holdings, Inc. is a leading Buffalo Wild Wings® (“BWW”)

franchisee that is rapidly expanding through organic growth and acquisitions. It operates 16

Buffalo Wild Wings restaurants: 11 in Michigan and five in Florida. DRH also created its own

unique, full-service restaurant concept: Bagger Dave’s Legendary Burgers and Fries®,

which falls within the fast-casual dining segment and was launched in January 2008. As of

February 22, 2010, we owned and operated three Bagger Dave’s® restaurants in Southeast Michigan

with the most recent store opening on February 21, 2010. We also have Franchise Disclosure

Documents filed in Michigan, Indiana and Ohio and one filing pending in Illinois for our Bagger

Dave’s concept.

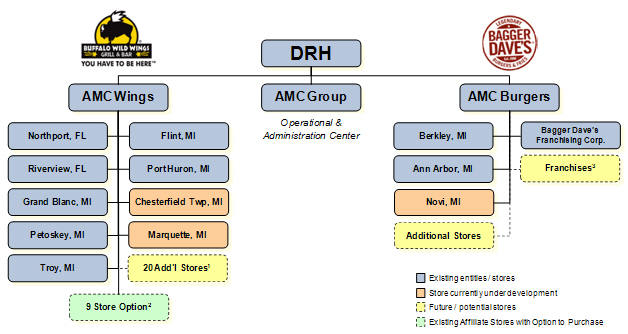

Diversified Restaurant Holdings, Inc. was formed as a holding company on September 25, 2006 under

the laws of the State of Nevada. We own all the stock in three wholly-owned, Michigan corporate

subsidiaries that were formed in March 2007: AMC Group, Inc., AMC Wings, Inc., and AMC Burgers,

Inc. AMC Group, Inc. operates as a management company and provides management services for all

restaurants owned by AMC Wings, AMC Burgers and affiliates. AMC Wings, Inc. owns all restaurants

developed under the Buffalo Wild Wing concept. AMC Burgers, Inc. owns all restaurants developed

under the Bagger Dave’s concept. AMC Burgers, Inc. also owns Bagger Dave’s Franchising

Corporation, which will be the franchisor for the Bagger Dave’s concept.

1

Table of Contents

We are located at 27680 Franklin Road, Southfield, Michigan, 48034. Our telephone number is (248)

223-9160. We can also be found on the internet at

www.diversifiedrestaurantholdings.com and

www.baggerdaves.com.

At the end of 2009, we converted to a 52/53 week fiscal year ending the last Sunday in December.

Our 2009 fiscal year ended December 27, 2009 and had 361 operating days. Our 2008 and 2007 fiscal

years ended December 31 of each year, and had 366 and 365 operating days, respectively.

Recent Acquisition

On February 1, 2010, subsequent to the end of fiscal year 2009, we exercised our option to acquire

nine Buffalo Wild Wings® Grill & Bar locations in Michigan and Florida from affiliates

of the Company for $3.1 million. Previously, DRH had a service agreement between AMC Group, Inc.

and Stallion, LLC, our affiliated restaurants’ cooperative management company, to manage and

operate the nine affiliated Buffalo Wild Wings restaurants. The Service Agreement called for AMC

Group, Inc. to collect from Stallion, LLC a service fee up to 8.00% of the gross revenue of each

restaurant under management. We received the right to exercise the purchase option as part of our

initial public offering in August 2008. The acquisition of these restaurants was financed through

six-year promissory notes that bear interest at 6% per year issued by the Company in favor of the

sellers.

The acquired BWW Michigan stores are in Sterling Heights, Fenton, Novi, Clinton Township, Ferndale

and Warren, while the Florida stores are in Brandon, Fish Hawk Ranch and Sarasota. The stores

range in age from 4 years to 10 years. In 2009, these restaurants generated $24.4 million in

revenue, and we received management and advertising fee revenue of $1.7 million. The acquisition

of the affiliated Buffalo Wild Wings locations allows us to fully realize the economic benefits

associated with these nine BWW stores in 2010 and beyond.

Background

We were founded by T. Michael Ansley, our President and CEO, in late 2004 as an operating center

for seven Buffalo Wild Wings locations that Mr. Ansley owned and operated as a franchisee. Mr.

Ansley opened our first affiliated BWW in December 1999, and since then has received numerous

awards from BWW, including:

| • | 2000 Operator of the Year |

||

| • | 2003 Highest Annual Restaurant Sales (Novi, Michigan) |

||

| • | 2004 Jimmy Disbrow Founder’s Award |

||

| • | 2004 Scott Lowery Franchise Development Award |

||

| • | 2004 Highest Annual Restaurant Sales (Novi, Michigan) |

||

| • | 2005 Highest Annual Restaurant Sales (Novi, Michigan) |

||

| • | 2006 Highest Annual Restaurant Sales (Novi, Michigan) |

In September 2007, Mr. Ansley was awarded Franchisee of the Year by the International Franchise

Association (“IFA”). The IFA’s membership consists of over 10,000 franchisees and 1,300 franchisor

companies and its mission is to protect, enhance and promote franchising.

DRH was formed in 2006 to provide the framework and financial flexibility to grow both as a

franchisee of BWW and to develop and grow our unique Bagger Dave’s Legendary Burgers and

Fries® restaurant concept.

We originated the Bagger Dave’s® concept with our first store opening in January 2008 in Berkeley,

Michigan, followed later that year with our second store in Ann Arbor, Michigan. We just opened

our third store in February 2010 which is located in Novi, Michigan.

2

Table of Contents

As of December 27, 2009, we operated 16 Buffalo Wild Wings in Michigan and in Florida.

| Buffalo Wild Wings Restaurants | Owned | Managed | Planned | Total | ||||||||||||

2006 |

9 | 9 | ||||||||||||||

2007 |

2 | 9 | 11 | |||||||||||||

2008 |

6 | 9 | 15 | |||||||||||||

2009 |

7 | 9 | 16 | |||||||||||||

2010 |

16 | * | 0 | 2 | 18 | |||||||||||

| * | Includes acquisition of nine affiliated stores on February 1, 2010 |

As of December 27, 2009 we were operating two Bagger Dave’s Legendary Burgers and Fries®.

| Bagger Dave’s Restaurants | Owned | Planned | Total | |||||||||

2008 |

2 | 2 | ||||||||||

2009 |

2 | 2 | ||||||||||

2010 |

3 | * | 3 | |||||||||

| * | Includes most-recent store

opened on February 21, 2010 |

Restaurant Concepts

Buffalo Wild Wings

We are a franchisee for Buffalo Wild Wings, Inc. (NASDAQ: BWLD), which as of December 27, 2009,

reported 652 Buffalo Wild Wing Grill & Bar® restaurants in 42 states that were either directly owned or

franchised.

The restaurants combine elements of both quick casual and casual dining styles, both of which are

part of a growing industry. The restaurants feature boldly-flavored, crave-able menu items in a

neighborhood atmosphere with an extensive multi-media system, full bar and open layout that creates

a distinctive dining experience for sports fans and families alike. The restaurants are

differentiated by the social environment created and the connection created among the restaurant

staff, guests and the local community. The inviting and energetic environment of the restaurants

is complemented by furnishings that can easily be rearranged to accommodate parties of various

sizes. Guests have the option of watching various sporting events on projection screens or up to

40 additional televisions, playing Buzztime Trivia (formerly NTN Trivia) or playing video games.

Typically, each of our BWW restaurants have 50 television displays that range in size from 27

inches to 108 inches that are generally tuned to various sporting events, especially sporting

events of primary interest in the local community.

Buffalo Wild Wings® restaurants have widespread appeal and have won dozens of “Best Wings” and

“Best Sports Bar” awards across the country. The BWW menu is competitively priced between the

quick casual and casual dining segments, featuring traditional chicken wings, boneless wings, and

other items including chicken tenders, Wild Flatbreads™, popcorn shrimp, specialty hamburgers and

sandwiches, wraps, Buffalito® soft tacos, appetizers and salads. The made-to-order menu items are

greatly enhanced by the bold flavor profile of BWW’s 14 signature sauces, which range in flavor

from Sweet BBQ™ to Blazin’®. The restaurants offer approximately 20 domestic and imported beers,

wines and liquor. The award-winning food and memorable experience drives guest visits and loyalty.

Our typical BWW restaurant derives approximately 75% of its revenues from food and 25% of its

revenue from alcohol sales, primarily draft beer.

Bagger Dave’s Legendary Burgers & Fries®

Bagger Dave’s Legendary Burgers and Fries is our first initiative to diversify our operations by

developing our own brand. The concept is focused on providing the best burgers available. Made

from a never-frozen, premium beef blend, we believe our guests will be craving our beef and turkey

burgers after their first bite. We have created a warm, inviting, and entertaining atmosphere

through friendly and memorable guest service, historical community photos that decorate the walls

and an electric train that runs above the dining room and bar areas.

3

Table of Contents

Bagger Dave’s® offers a full-service restaurant and bar at a fast casual price point for

friends and families in a casual, comfortable, smoke-free atmosphere. The menu features freshly

made burgers accompanied by more than 30 toppings from which to choose, fresh-cut fries, and

hand-dipped milkshakes. Signature items include Sloppy Dave’s BBQ™, Train Wreck

Burger™, and Bagger Dave’s Amazingly Delicious Turkey Black Bean Chili™. The guiding

principal of the Bagger Dave’s brand is genuine simplicity. The burgers are made from a USDA fresh

premium ground beef blend with no trimmings or Michigan fresh ground turkey. The burgers come in

the “Regular” (two patties) or “Small” (one patty) versions on fresh buns. Customers can choose

from burger “Legends” including

the Train Wreck Burger™, the Blues Burger™ and Sloppy Dave’s BBQ™ or guests have the freedom to

“Create Your Own Legend” which allows you to totally customize your burger choosing from a variety

of buns and more than 30 toppings, including custom house-made sauces presenting bold and exciting

new flavors. In addition, burger toppings include various cheeses, bacon, egg, guacamole and a

variety of complimentary toppings — sautéed mushrooms and onions, barbecue sauce, steak sauce and

other standard condiments.

Beyond legendary burgers, Bagger Dave’s offers our Amazingly Delicious Turkey Black Bean Chili, a

Veggie Black Bean burger, a grilled cheese sandwich, a BLT sandwich, salads and fresh-cut fries.

The fries are cut in-house from Idaho potatoes and cooked in canola oil using a seven-step

Belgian-style process producing a fry reminiscent of those served at community fairs. We also

offer Dave’s Sweet Potato Chips™, a Bagger Dave’s specialty using fresh cut premium sweet potatoes

from North Carolina. Customers can choose from our own signature dipping sauces of

honey/cinnamon/sea salt mix (especially good on the sweet potato chips) or honey mustard.

To reinforce the Bagger Dave’s name and brand, our burgers, sandwiches and fries/chips are served

in natural (brown) bags with our logo stamped prominently thereon and set in a cake tin.

Bagger Dave’s also offers hand dipped ice cream and milkshakes with a variety of free mix-ins.

We recently introduced a breakfast menu at the Novi location, which opened in February 2010, so it

will have a three-part service day. The breakfast menu includes the freedom to create a legendary

breakfast sandwich with the “Build Your Own Breakfast Sandwich” option offered with fresh,

high-quality branded English muffins and the many options for toppings and sauces available for the

“Create Your Own Legend.”

We believe our tagline captures it all: “Bagger Dave’s®. Legendary Tastes. Unforgettable

Experience. “More information on Bagger Dave’s® can be found on our website:

www.baggerdaves.com.

Growth Strategy

We firmly believe that a happy employee translates into a happy guest. A happy guest drives repeat

sales and word-of-mouth marketing — two key factors that are fundamental to same store sales growth

strategy. We believe that our core expertise is in the site selection, development, management,

quality guest service and operation of fast casual restaurants. We plan to grow by increasing the

number of restaurants in each of the two concepts we currently offer and by developing or acquiring

additional concepts that can be expanded profitably.

We are an experienced operator of 16 franchised Buffalo Wild Wings® (BWW) restaurants. We

currently operate eleven Buffalo Wild Wings Grill & Bar restaurants in Michigan (one in the

Northern Lower Peninsula and ten in the greater Detroit Metropolitan areas of Oakland, Macomb and

Genesee counties) and five in the Tampa/Sarasota, Florida region. We have a development agreement

with the franchisor of Buffalo Wild Wing restaurants to open an additional 22 Buffalo Wild Wing

restaurants by 2017. Twelve (12) of those restaurants are planned to be located in Michigan and

ten (10) of those restaurants are planned to be located in the Tampa, Florida region. We plan to

open two Buffalo Wild Wings restaurants in 2010. We plan to open one store in June of this year in

Marquette, Michigan and expect to open the second later in the year in Chesterfield, Michigan. We

expect to open additional stores if optimal locations are found and appropriate financing can be

secured.

In 2008, we established a new restaurant concept, Bagger Dave’s Legendary Burgers and Fries®. We

had two restaurants that began operations in 2008 and, on February 21, 2010, we opened our third

restaurant in Novi, Michigan. If our Bagger Dave’s® concept proves to be successful, as it has

with the first two stores, we plan to grow throughout the upper Midwest and, ultimately,

nationally. We believe that with the three stores currently

operating and the planned opening of a fourth store, we can demonstrate proof of concept and begin

franchising the Bagger Dave’s concept. We currently have Franchise Disclosure Documents filed in

Michigan, Indiana and Ohio and one pending in Illinois. Our plan is to continue to develop and

grow this concept as we concurrently expand our Buffalo Wild Wings franchises in Michigan and

Florida. We expect to maintain a 1.5 to 1 ratio of corporate-owned Bagger Dave’s to franchised

operations.

4

Table of Contents

Store Locations and Expansion Plans

Affiliated Buffalo Wild Wings Restaurants under Management in 2009 (Purchased Effective February 1,

2010)

| Approximate | Remodeled/ | |||||||||

| Population in | Planned | |||||||||

| Five-mile | Remodeling | |||||||||

| Opened | Location | Location Characteristics | Radius | or upgrade | ||||||

December 1999

|

Sterling Heights, MI | 6,542 square feet. Located directly in front of an AMC 30 cinema in a shopping center anchored by Walmart situated along the M-59 corridor. | 228,000 | July 2005, freshening is scheduled in 2010 | ||||||

April 2001

|

Fenton, MI | 6,105 square feet. Located in growing community off of U.S. Highway 23, just 45 minutes from Metropolitan Detroit. | 40,000 | July 2006, Gen. 4.1 remodel in 2011 | ||||||

June 2002

|

Novi, MI* *Ranked number one in sales by Buffalo Wild Wings Inc. in 2003, 2004, 2005, and 2006 |

6,815 square feet. Located in an outdoor lifestyle entertainment center facing 1-96, beside a 20 screen Emagine cinema complex in a growing, young-affluent suburb northwest of Detroit in Oakland County. | 145,000 | Gen. 4.1 remodel in June 2007 | ||||||

December 2003

|

Clinton Township, MI | 6,600 square feet. Stand alone restaurant located directly across the street from a Meijer Super Center in the heart of Macomb County, just north of Detroit. | 303,000 | Feb. 2009 | ||||||

June 2004

|

Brandon, FL | 6,600 square feet. Stand alone location at the end of the Cross-town Expressway in Brandon, Florida, just east of Tampa. | 198,000 | June 2009 | ||||||

March 2005

|

Ferndale, MI** **Consistently ranks in top 25 national Buffalo Wild Wing system-wide sales |

7,400 square feet. Located on Nine Mile Road, just north of Detroit in rejuvenated downtown Ferndale near the I-75 and I-696 interchange in the heart of Metropolitan Detroit. | 459,000 | June 2010 | ||||||

September 2005

|

Riverview (Fish Hawk Ranch, FL |

6,400 square feet. Located a mile from a community with about 6,700 new homes. Two potential new developments may add up to 6,400 more homes over the next several years once the economy in Florida recovers. | 127,000 | 2011 freshening | ||||||

March 2006

|

Sarasota, FL | 6,500 square feet. Located on Clark Road in Sarasota, the main artery out to Siesta Key. The location is the anchor end cap position in a small shopping center that features Moe’s, Atlanta Bread and other restaurants. | 138,000 | Feb. 2009 | ||||||

July 2006

|

Warren, MI*** ***Since opening ranks in top 25 Buffalo Wild Wing system-wide sales |

6,800 square feet. Located directly across from the General Motors Technology Center which employs over 22,000 people in this northern Detroit suburb. | 331,000 | 2011 freshening | ||||||

5

Table of Contents

Company-Owned Buffalo Wild Wings® Restaurants Operated in 2009

| Approximate | Remodeled/ | |||||||||

| Population in | Planned | |||||||||

| Five-mile | Remodeling | |||||||||

| Opened | Location | Location Characteristics | Radius | or Upgrade | ||||||

August 2007

|

North Port, FL | 6,400 square feet. Located in an end cap position of a shopping center anchored by a Super Walmart and Home Depot at Tamiami Trail (U.S. Route 41) and Sumter Road. | 63,000 | New | ||||||

August 2007

|

Riverview, FL | 6,400 square feet. Located in an end cap position of a shopping center anchored by a Sweet Bay (grocery store) and Office Max on Big Bend Road at U.S. 301 just off I-75. Other tenants include Five Guy’s Famous Burgers and Fries, Panera Bread, Fifth Third Bank, and Panda Express among several others. | 66,000 | New | ||||||

March 2008

|

Grand Blanc, MI | 6,000 square feet. Located in an out building directly in front of a new 14 screen movie theater with an IMAX theater (NCG Trillium Cinema). A Target, JCPenney and many other specialty shops are proposed for this shopping center which is about a mile off of I-75 just south of Flint, MI near Genesys Hospital (employs 3,000). | 56,000 | New | ||||||

August 2008

|

Petoskey, MI | 6,200 square feet. Located in an end cap position in a Lowe’s-anchored shopping center, near an adjacent Walmart, Home Depot, Cinema and new $160 million Victory Casino. | 14,000 Tourism | New | ||||||

July 2008

|

Troy, MI | 7,500 square feet. Located on Big Beaver Road at John R Road in a densely populated suburb of Detroit. The Troy Sports Complex anchors the center with 4 NHL size hockey rinks for recreational activities and leagues. Also in the center is Starbucks, Einstein Bagels, Olga’s Kitchen, Verizon Wireless, Kroger and many more. | 258,000 | New | ||||||

December 2008

|

Flint, MI | 6,400 square feet. Located in an end cap position in a strip mall anchored by TJ Maxx and Hobby Lobby and directly across the street from the Genesee Valley Center, a large regional indoor mall with Sears, Macy’s and JCPenney. | 105,000 | New | ||||||

July 2009

|

Port Huron, MI | 6,500 square feet. Located on M-25, a main thoroughfare just North of Port Huron, MI in an end cap position in a strip mall directly across the street from the Birchwood Mall, a large regional indoor mall with Sears, Macy’s, Target and JC Penny as anchors. There is also a 10 screen movie theater at the mall. | 49,000 | New | ||||||

6

Table of Contents

BWW Restaurants under Development — Planned Opening in 2010

We plan to open two Buffalo Wild Wing® restaurants in 2010, the first in Marquette, Michigan and

the second in Chesterfield Township, Michigan. We plan to fund the startup of these restaurants

through our current capital resources and by loans from either existing lending sources or other

suitable funding sources. These loans will be recorded as liabilities on our balance sheet and the

furniture, equipment and leasehold improvements will be

recorded as capital assets on the balance sheet of each separate affiliated legal entity that owns

the restaurant. The financial statements of these wholly-owned subsidiaries will be combined with

our balance sheet on a consolidated basis for reporting purposes. We are also looking for

opportunities to open a third Buffalo Wild Wings location in 2010.

Company-Owned Bagger Dave’s® Restaurants in 2009 and Early 2010

| Approximate | ||||||||

| Population in | ||||||||

| Five-mile | ||||||||

| Opened | Location | Location Characteristics | Radius | |||||

January 2008

|

Berkley, MI | 3,472 square feet. Located on Coolidge Highway near Twelve Mile Rd. in a stand-alone location. One of the densest areas in Metro Detroit, with approximately 16,000 residents within one mile. Nearby is William Beaumont Hospital, which employs close to 12,000 employees. | 331,000 | |||||

August 2008

|

Ann Arbor, MI | 3,800 square feet. Located in shopping center on Eisenhower Blvd. near Ann Arbor-Saline Rd. across from a new Whole Foods and an REI. One mile from University of Michigan stadium and 1/2 mile from large, popular shopping mall. High performing Panera Bread anchors the center. | 150,000 | |||||

February 2010

|

Novi, MI | 4,200 square feet. Located on an end cap position with patio space in the Novi Town Center shopping complex at the corner of Grand River Ave. and Novi Road. This is a high traffic center that includes Potbelly, Biggby Coffee, AT&T Cellular, Pei Wei and Bonefish restaurant. This restaurant also offers a newly designed breakfast service option. | 150,000 | |||||

Bagger Dave’s® Restaurants — Future Development

Management continuously searches for premium locations suitable to new restaurant development and

may open a fourth Bagger Dave’s in 2010 if the appropriate location and funding can be secured.

Site Selection

We conduct extensive analysis to determine the location of each new restaurant. Proximity to

businesses (office buildings, movie theaters, manufacturing plants, hospitals, etc) and leveraging

high-traffic venues are a key success criteria for our business.

We prefer a strong end-cap position in a well-anchored shopping center or life style entertainment

center. Movie theaters are also a major traffic driver for the Buffalo Wild Wings Grill & Bar®

concept. Three of our locations are

directly beside or in front of movie theaters. However, we do not rule out freestanding locations

if the opportunity meets certain economic criteria. We operate two stand-alone building locations

at this time.

7

Table of Contents

With our Bagger Dave’s Legendary Burgers & Fries®, we have applied similar criteria with a focus on

lunch and breakfast traffic opportunities. Designed to be a smaller, family-oriented restaurant

with an English pub type atmosphere the signature food item is the “Create Your Own Legend” burger

and breakfast sandwich that can be built with a wide array of toppings and our own signature

sauces.

Restaurant Operations

We believe that high quality restaurant management, valuing our employees, and providing fast,

friendly service to our guests will be the keys to our continued success.

Management and Staffing. When a restaurant is opened, we imbed our core values: cleanliness,

service and organization. Extraordinary efforts are devoted to ensuring that all stores exemplify

these ideals, making it a part of our corporate culture. Our restaurants are generally staffed

with one manager and between two and four assistant managers. The manager has responsibility for day-to-day

operations and is responsible for maintaining the standards of quality and performance we have

established. We have regional managers to supervise the operation of our restaurants including the

continuing development of each restaurant’s management team. Through regular visits to the

restaurants, the regional managers ensure adherence to all aspects of our concept, strategy and

standards of quality. We also have Secret Shoppers that regularly visit our restaurants and

provide customer satisfaction scores which each restaurant is graded on monthly.

Training and Development. Successful restaurant operations, customer satisfaction, quality and

cleanliness begin with the employee — a key component of our strategy. Consequently, we pride

ourselves on well organized training and very competitive incentive programs, many of which we

believe are unparalleled in the restaurant industry.

Aside from very competitive base salaries and benefits, management in incentivized with a strong

performance-based bonus program. We also provide group health insurance and tuition reimbursement

programs.

We emphasize growth from within the organization as much as possible, giving our employees the

opportunity to develop and advance. This philosophy helps build a strong loyal management team

with, we believe, better employee retention than our competitors. However, when necessary, we will

hire from the outside, but we will only hire candidates that meet or exceed our stringent criteria.

Restaurants. We typically operate BWW restaurants of around 6,000 square feet in size based on our

assessment of the population and opportunity in the area. We have a continuous capital improvement

plan for our restaurants and plan major renovations every 5 years. Nine of our 16 Buffalo Wild

Wing® restaurants are current with Generation 4.1 design criteria, three will be freshened-up in

2010 and one is scheduled for a Buffalo Wild Wings® Generation 4.1 upgrade in 2011. The

improvements will include high definition flat screen televisions and projectors. We also attempt

to increase seating capacity whenever possible.

Bagger Dave’s® will have a typical footprint of approximately 3,500 to 4,500 square feet plus an

outside seating area where feasible. We plan to establish this concept in the Detroit Metropolitan

market and then expand it throughout the Midwest, with an ultimate goal of possibly franchising the

concept nationally. We have added breakfast at our newest store that opened in February 2010 and

plan to offer a breakfast menu at our other locations as well. We can add breakfast with limited

impact on hourly labor costs and only 12-15 additional food items. With the exception of coffee

equipment, no additional kitchen equipment investment is required.

Metrics. We use several metrics to evaluate and improve each restaurant’s performance that

include: sales growth, ticket times, table turns, guest satisfaction, secret shopper scores, Guest

Experience Management (GEM) scores obtained through guest feedback via the internet, hourly labor

cost, and cost of sales (COS).

Purchasing and Quality

Our purchasing operations for the BWW restaurants is primarily through channels established by

Buffalo Wild Wings corporate operations. We do, however, negotiate directly with most of these

channels as to price and delivery terms. Where we purchase directly, we seek to obtain the highest

quality ingredients, products and supplies from reliable sources at competitive prices. For Bagger

Dave’s, we have been able to leverage our BWW purchasing power and develop supply sources at a more

reasonable cost than would be expected for a smaller restaurant concept.

8

Table of Contents

To maximize our purchasing efficiencies, our centralized purchasing staff typically negotiates

fixed-price contracts (usually for a one-year period) or, where appropriate, commodity-price based

contracts.

Marketing and Advertising

In 2009, we spent an approximately 2% of all restaurant sales on marketing efforts. Charitable

donations in our communities and developing local public relations is a major component of our

marketing efforts. We support programs that build traffic at the grass roots level. During 2009,

we participated in numerous local store marketing events for both Buffalo Wild Wings and Bagger

Dave’s throughout the communities that we service.

Buffalo Wild Wings®. We pay a marketing fee to Buffalo Wild Wings equal to 3% of revenue. Also the

restaurants that are located in the Metropolitan Detroit, Michigan market contribute approximately 0.5%

of revenue to the regional cooperative of franchisees, which is included in our 2% annual marketing

budget. We have established the BWW restaurants we manage in the Michigan and Florida markets

through coordinated local store marketing efforts and operating strengths that focus on the guest

experience. We constantly strive to improve our operational efficiency with comprehensive training

designed to enhance the service level to our guests, in order to increase location sales and the

corresponding service fee revenue. Our BWW locations have also benefited from increasing brand

awareness of Buffalo Wild Wings, which is supported by national advertising on ESPN and CBS during

key sports seasons, such as football and the March Madness NCAA basketball tournaments.

Our Buffalo Wild Wings stores participated in more than 30 local events in 2009 including the Oak

Apple Run (Royal Oak, Michigan), the Woodward Dream Cruise (Ferndale, Michigan), the Boys and Girls

Club Walk (Royal Oak, Michigan), the Children’s Leukemia Walk (in Milford and Petoskey, Michigan),

Sterling Fest (in Sterling Heights, Michigan), SudsFest (in Tampa, Florida), the Taste of Brandon

(Brandon, Florida) and the Sarasota Pumpkin Festival (Sarasota, Florida). In addition, we sponsored

more than 50 sports teams and held more than 80 fundraising nights, raising more than $8,000 for

local non-profit organizations.

Bagger Dave’s®. The advertising and marketing plan for developing the Bagger Dave’s® brand relies

on local media, specials, promotions and community events. We are also building our marketing

reach with our current guests through such efforts as an email and social media platforms. We

strongly believe that a large part of Bagger Dave’s® growth has been accomplished through

word-of-mouth.

Bagger Dave’s participated in more than 10 events in the communities we service including the Oak

Apple Run (Royal Oak, Michigan), the Woodward Dream Cruise (Ferndale, Michigan), the Boys and Girls

Club Walk (Royal

Oak, Michigan), the Children’s Leukemia Walk (in Milford, Michigan). Bagger Dave’s also sponsored

local sports teams and held various fundraising nights at their locations.

Information Technology

We believe that technology can help to provide a competitive advantage and enable our strategy for

growth through efficient restaurant operations, information analysis and ease and speed of guest

service. We have an integrated information system that manages the flow of information from each

restaurant to the corporate offices. The systems are designed for improving operating

efficiencies, enable rapid analysis of marketing and financial information, and reduce

administrative time. We are equipping our Bagger Dave’s restaurants with the ability for guests to

order on line and pick up their order at their convenience.

Competition

Competition in the restaurant industry is intense. Because the nature of our restaurant concepts

are “fast casual,” we compete with both national casual dining chains, such as Applebee’s, T.G.I.

Friday’s and Chili’s, as well as national fast food chains, such as McDonald’s, Burger King and

Arby’s, and local chains and independently-operated restaurants. Competition in the casual dining

and fast food segments of the restaurant industry is expected to remain intense with respect to

price, service, location, concept and the type and quality of food. There is also intense

competition for real estate sites, qualified management personnel and hourly restaurant staff.

Many of our competitors have been in existence longer than we have and they may be better

established in markets where we are currently or may be located in the future. Further, many of

these competitors have greater financial and other resources and more established market presence.

Accordingly, we must plan to continually evolve our restaurants, maintain high quality standards

and treat our guests in a manner that encourages them to return. We have an advantage with the

Buffalo Wild Wings restaurants because as they grow their brand and expand nationally, it helps our

marketing efforts. With the Bagger Dave’s concept, we focus on the underdeveloped, mid-range price

point sector of the restaurant industry, bracketed on the low end by Wendy’s and at the upper end

by Red Robin. Our pricing communicates value to the guest in a comfortable, welcoming atmosphere

providing full-service, unlike many competitors in the fast-casual segment.

9

Table of Contents

Employees

As of December 27, 2009, we had 413 employees consisting of 395 employees at our restaurants and 18

employees at our corporate offices. None of our employees are covered by a collective bargaining

agreement. We strive to promote from within and provide highly competitive wages and benefits. We

value our employees and their input and believe this philosophy contributes to a low turnover

ratio, even at the hourly wage level, relative to industry standards.

Trademarks, Service Marks and Trade Secrets

Our domestically-registered trademarks and service marks include, among others, Bagger Dave’s

Legendary Burgers & Fries®, Sloppy Dave’s BBQ®, Train Wreck

Burger®, Bagger Dave’s Amazingly Delicious Turkey Black Bean Chili™, and Dave’s Sweet

Potato Chips™. We place considerable value on our trademarks, service marks and trade secrets and

believe they are important to our brand-building efforts and the marketing of our Bagger Dave’s®

restaurant concept. We intend to actively enforce and defend our intellectual property, however,

we cannot predict whether the steps taken by us to protect our proprietary rights will be adequate

to prevent misappropriation of these rights or the use by others of restaurant features based upon

or similar to our concepts.

Although we believe we have sufficient protections concerning our trademarks and service marks, we

may face claims of infringement that could interfere with our efforts to market our brands.

The Buffalo Wild Wings® registered service mark is owned by Buffalo Wild Wings, Inc.

Available Information

We are subject to the informational reporting requirements of the Securities Exchange Act of 1934

and, therefore, we file periodic reports, proxy statements and other information with the

Securities and Exchange Commission (the “SEC”). The SEC maintains an Internet website

(www.sec.gov) that contains reports, proxy statements and other information for registrants that

file electronically. Additionally, such reports may be read and copied at the Public Reference

Room of the SEC at 100 F Street NE, Washington, D.C. 20549.

We

maintain a corporate Internet website at

www.diversifiedrestaurantholdings.com. On our website,

we make available, free of charge, certain key documents that we have filed with the SEC, including

our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Proxy Materials related to our

Annual Meeting of Shareholders. Our website also features a hyperlink to a portion of the SEC’s

website where all of the reports we have filed with or furnished to the SEC may be accessed free of

charge. None of the other information found on our website is incorporated into this Annual Report

or any other report we file with, or furnish to, the SEC.

ITEM 1A. RISK FACTORS

The following risk factors could affect our business, financial condition and/or results of

operations. These risk factors should be considered in connection with evaluating the

forward-looking statements contained in this Annual Report because they could cause the actual

results and conditions to differ materially from those projected in our forward-looking statements.

Before you buy our common stock, you should know that investing in our common stock involves

risks, including the risks described below. The risks that are highlighted below are not the only

ones we face. If the adverse effects referred to in any of these risks actually occur, our

business, financial condition or operations could be adversely affected. In that case, the trading

price of our common stock could decline, and our stockholders may lose all or part of their

investment.

We May Not Be Able To Manage Our Growth

Our Company’s expansion strategy will depend upon our ability to open and operate additional

restaurants profitably. The opening of new restaurants will depend on a number of factors, many of

which are beyond our control. These factors include, among others, the availability of management,

restaurant staff and other personnel, the cost and availability of suitable restaurant locations,

cost effective and timely planning, design and build-out of restaurants, acceptable leasing or

financial terms, acceptable financing and securing required governmental permits. Although we have

formulated our business plans and expansion strategies based on certain assumptions, we anticipate

that, as with most business ventures, we will be subject to changing conditions. Our assessments

regarding timing and the opening of new restaurants as well as a variety of other factors may not

prove to be correct, and/or such new restaurants may not be operated profitably.

10

Table of Contents

Uncertainty of Market Acceptance

In the course of expansion of our concepts, we will enter new markets in which we may have limited

operating experience. There can be no assurance that we will be able to achieve success in our new

markets or in our new

stores. New restaurants typically require several months of operation before achieving normal

profitability. When we enter highly competitive new markets or territories in which we have not yet

established a market presence, the adverse effects on revenue and profit margins may be greater and

more prolonged than anticipated.

Competition

The food service industry is intensely competitive. Because of the nature of our concept as “fast

casual,” we will compete with national casual dining chains, such as Applebee’s, T.G.I. Friday’s

and Chili’s, national fast food chains, such as McDonald’s, Burger King and Arby’s, as well as

local chains and independently-operated restaurants. Competition in the casual dining and fast food

segments of the restaurant industry is expected to remain intense with respect to price, service,

location, concept and the type and quality of food. There is also intense competition for real

estate sites, qualified management personnel and hourly restaurant staff. Some of our competitors

have been in existence longer than we have and they may be better established in markets where we

are currently or may be located in the future. Further, many of these competitors have greater

financial and other resources and a more established market presence than we have.

Government Regulations

The restaurant industry is subject to numerous federal, state and local governmental regulations,

including those relating to the preparation and sale of food and alcoholic beverages, sanitation,

public health, fire codes, zoning and building requirements. Termination of the liquor license for

any restaurant would adversely affect the revenues of that restaurant and the failure to obtain

such licenses would adversely affect our expansion plans. We are also subject to laws governing our

relationships with employees, including benefit, wage and hour laws, and laws and regulations

relating to workers’ compensation insurance rates, unemployment and other taxes, working and safety

conditions and citizenship or immigration status. If legislation is enacted to remove the tip

credit (the difference between minimum wage and tipped employee minimum wage), our cost of labor

would increase dramatically and adversely affect our profits. In certain states we may be subject

to “dram-shop” statutes, which generally provide that a person injured by an intoxicated person has

the right to recover damages from an establishment that wrongfully served alcoholic beverages to

the intoxicated person. While we carry liquor liability coverage, a judgment against us under a

dram shop statute in excess of our insurance coverage, or any inability to continue to obtain such

insurance coverage at reasonable costs, could have a material adverse effect on us. Failure to

comply with any of these regulations or increases in the minimum wage rate, employee benefit costs

or other costs associated with employees, could adversely affect us.

Unionization of the Hourly Work Force

The possible enactment of the Employee Free Choice Act (EFCA) could have a material impact on our

business. This proposed “card check” legislation would eliminate our Team Members’ fundamental

right to a private ballot election in deciding whether or not to join a union. If the law resulted

in the unionization of our workforce, it would increase our costs significantly and reduce our

ability to generate a profit.

Certain Factors Affecting the Restaurant Industry

The restaurant industry is affected by national, regional and local economic conditions, changing

consumer tastes and spending priorities, health concerns and trends, demographic trends, traffic

patterns and the type, number and location of competing restaurants. Multi-unit chains such as ours

can also be adversely affected by publicity

resulting from food quality, illness, injury or other health concerns or operating issues stemming

from one restaurant or a limited number of restaurants. Dependence on fresh produce and meats also

subjects us to the risk that shortages or interruptions in supply, particularly of chicken wings

and ground beef, caused by unfavorable weather or other conditions, could adversely affect the

availability, quality or cost of food supplies. In addition, factors such as inflation, increased

food, labor and employee benefit costs, and the availability of qualified management and hourly

employees may also adversely affect the restaurant industry in general and our restaurants in

particular. We may be the subject of litigation based on discrimination, personal injury and other

claims. None of the foregoing factors can be predicted with any degree of certainty and any one or

more of these factors could have a material adverse effect on our financial condition and results

of operations. Our continued success will depend in part on our ability to identify and respond

appropriately to changing conditions.

11

Table of Contents

Need For Additional Financing

We currently plan to open between two (2) and four (4) new restaurants in 2010. The Company

anticipates that cash from operations, equipment leasing, lender based financing and landlord

construction contributions (when available) will be sufficient to fund our expansion plans for

2010. These estimates may prove to be inaccurate. Availability of credit may be limited due to the

unstable U.S. economy and tighter restrictions placed on traditional lending sources. To continue

our expansion at the same or a higher level, we anticipate that additional funding will be

necessary. We may not be able to obtain such additional financing or we may not be able to obtain

it on favorable terms.

Dependence on Key Personnel

Our ability to develop and market our products and to maintain a competitive position depends, in

large part, on our ability to attract and retain qualified personnel. There can be no assurance

that we will be able to attract and retain such personnel. In particular, we are presently

dependent upon the services of T. Michael Ansley, David G. Burke and Jason T. Curtis. We do not

have employment agreements with any of our employees. Our inability to retain the full-time

services of any of these people or attract other qualified individuals could have an adverse effect

on us, and there would likely be a difficult transition period in finding replacements for any of

them.

Trademarks, Service Marks and Trade Secrets

We place considerable value on our trademarks, service marks and trade secrets. We intend to

actively enforce and defend our intellectual property. We may not be successful in enforcing our

intellectual property rights. Our intellectual property may not have the value we believe it holds

and may be determined to violate or infringe the property rights of others if our rights are

challenged. Any of the foregoing adverse results could materially and negatively impact our

financial condition and operations.

Adverse Effect of Undesignated Stock and Anti-Takeover Provisions

Our authorized capital includes 10,000,000 shares of “blank check” preferred stock. Accordingly,

our Board of Directors has the authority to issue any or all of the shares of preferred stock,

including the authority to establish one or more series, and to fix the powers, preferences, rights

and limitations of such class or series, without seeking stockholder approval. Further, as a Nevada

corporation, the Company is subject to provisions of the Nevada Business Corporations Act (“NBCA”)

regarding “control share acquisitions” and “business combinations.” In the future, we may consider

adopting anti-takeover measures. The authority of the Board to issue undesignated stock and the

anti-takeover provisions of the NBCA, as well as any future anti-takeover measures adopted by us,

may, in

certain circumstances, delay, deter or prevent takeover attempts and other changes in our control

which is not approved by management and the Board of Directors. As a result, our stockholders may

lose opportunities to dispose of their shares at favorable prices generally available in takeover

attempts or that may be available under a merger proposal and the market price, voting and other

rights of the holders of Common Stock may also be affected. See “Description of Securities.”

No Assurance of Profitability

We may experience operating losses as we develop and implement our business plan. As a result, we

may not be able to achieve or maintain profitability.

Possible Issuance of Additional Shares without Stockholder Approval Could Dilute Stockholders

As of the date of this Annual Report, we have an aggregate of 18,876,000 shares of common stock

outstanding. In addition, our directors have a total of 144,000 options to purchase shares of

common stock at $2.50 per share,. Of these options, 94,000 are fully vested as of the date of this

Annual Report and 50,000 will vest on July 30, 2010. Although there are currently no other

material plans, agreements, commitments or undertakings with respect to the issuance of additional

shares of common stock or securities convertible into any such shares, if any shares are issued in

the future, they would further dilute the percentage ownership of our common stock held by our

stockholders.

12

Table of Contents

Penny Stock Regulations Could Inhibit the Trading Of Our Stock in the Secondary Market

The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in

“penny stocks”. Penny stocks generally are equity securities with a price of less than $5.00 (other

than securities registered on certain national securities exchanges or quoted on the NASDAQ system,

provided that current price and volume information with respect to transactions in such securities

is furnished by the exchange or system). Prior to a transaction in a penny stock, a broker-dealer

is required to:

| • | deliver a standardized risk disclosure document prepared by the SEC that provides

information about penny stocks and the nature and level of risks in the penny stock market; |

||

| • | provide the customer with current bid and offer quotations for the penny stock; |

||

| • | explain the compensation of the broker-dealer and its salesperson in the transaction; |

||

| • | provide monthly account statements showing the market value of each penny stock held in

the customer’s account; and |

||

| • | make a special written acknowledgment that the penny stock is a suitable investment for

the purchaser and receive the purchaser’s written agreement to the transaction. |

These requirements may have the effect of reducing the level of trading activity in the secondary

market for a stock that becomes subject to the penny stock rules. If our share price drops below

$5.00, our shares could be subject to the penny stock rules. As such, investors might find it more

difficult to sell their shares.

Legal Actions Could Have an Adverse Affect on Us

We could face legal action from a franchisor, government agency, employee or customer. Many state

and federal laws govern our industry and if we fail to comply with these laws we could be liable

for damages or penalties. Further, we may face litigation from customers alleging that we were

responsible for some illness or injury they suffered at or after a visit to our restaurants, or

that we have problems with food quality or operations. We may also face litigation resulting from

employer-employee relations, including age discrimination, sexual harassment, gender discrimination

or local, state and federal labor law violations as an example. Expensive litigation may adversely

affect both our revenue and profits.

An Increase in the Cost of Our Food Products Could Adversely Affect Our Operating Results

Our primary food products are fresh chicken wings and ground beef. Any

material increase in the cost of fresh chicken wings or ground beef could adversely affect

operating results. Our cost of sales could be significantly affected by increases in the cost of

fresh chicken wings and ground beef, which can result from a number of factors, including

seasonality, increases in the cost of grain, disease and other factors that affect availability,

and greater international demand for domestic chicken and beef products. We also depend on our

franchisor, as it relates to chicken wings, to negotiate prices and deliver product to us at a

reasonable cost. Chicken wing prices averaged $1.69 per pound in 2009, $0.44 per pound higher than

the average of $1.25 in 2008. Our franchisor’s chicken wing purchase contract expired after the

March 2008 quarter and we are currently buying product at the spot rate. Wing costs averaged $2.02

per pound in January and February, 2010. This increase will negatively impact our profits in the

first quarter of 2010.

Failure to Gain Acceptance in Florida Could Have a Negative Impact on Our Operations

The Buffalo Wild Wings concept may not gain acceptance in the Florida market. If we fail to gain

acceptance in the Florida market, this could impede our financial performance.

The Bagger Dave’s Concept May Not Be Accepted

The Bagger Dave’s concept developed by us may not be accepted. If the public does not accept the

Bagger Dave’s concept, this would have a severe negative impact on our financial performance.

13

Table of Contents

If We Are Unable To Open New Restaurants in a Timely Manner, We May Suffer Negative Consequences

If we are unable to successfully open new restaurants in a timely manner, our revenue growth rate

and profits may be adversely affected. We must open restaurants in a timely and profitable manner

to successfully expand our business. In the past we have experienced delays in restaurant openings

and we may face similar delays in the future. These delays may trigger financial penalties by the

franchisor as provided in Area Development Agreements. These delays may not meet market

expectations, which may negatively affect our stock price. Further, future restaurants may not meet

operating results similar to those of existing locations. Our ability to expand successfully will

depend on the following factors:

| • | Locating and securing quality locations in new and existing markets; |

||

| • | Negotiating acceptable leases or purchase agreements; |

||

| • | Securing acceptable financing for new locations; |

||

| • | Cost effective designs by us and franchisors; |

||

| • | Timely planning and build-out of restaurants; |

||

| • | Obtaining and maintaining required local, state and federal government approvals and

permits related to construction of the restaurants and the sale of food and alcoholic

beverages; |

||

| • | Creating brand awareness in new markets; and |

||

| • | General economic conditions. |

The Opening of Other Restaurants Close To Our Existing Restaurants May Reduce Our Operating

Performance

New restaurants added to our existing markets, whether by us, other franchisees or the franchisor

may take sales away from our restaurants. We intend to open restaurants in our existing markets and

this may impact revenues earned by our existing restaurants. Also, the franchisor or other

franchisees could open restaurants in neighboring territories that may affect the sales of our

existing restaurants as well. These activities may reduce overall operational performance.

Actions by the Franchisor Could Negatively Affect Our Business and Operating Results

Our BWW restaurant business depends in part on decisions made by our franchisor. For example,

these decisions affect marketing and product costs. Business decisions made by our franchisor could

adversely impact our operating performance.

Compliance with the Sarbanes-Oxley Act May Be Costly

As we move forward, we may have to continue to implement accounting

procedures to comply with the Sarbanes-Oxley Act of 2002. These procedures may require us to incur

substantial audit and internal control related expenses in the future.

If We Fail To Attract and Retain Qualified Employees, We Will Be Unable To Operate Effectively

The success of our restaurants depends on our ability to attract, motivate and retain a sufficient

number of qualified restaurant employees, including managers, kitchen staff and wait staff. We may

not be able to attract and retain qualified personnel to operate and manage our restaurants. Our

inability to recruit and retain these individuals may delay the planned openings of new restaurants

and increase turnover at existing restaurants. This could impact our expansion strategy and lead to

higher labor costs, which would negatively impact our operating results. Further, the loss of any

or our key executive officers would likely adversely impact our performance.

14

Table of Contents

Changes in Consumer Preferences or Discretionary Consumer Spending Could Negatively Impact Our

Business

The success of our business depends, in part, upon the popularity of both Buffalo, New York-style

chicken wings and hamburgers. We also depend on trends of consumers eating away from home more

often. Shifts away from these current trends could impact our sales negatively. These shifts may

include consumer dietary changes as they avoid foods with high cholesterol, fat or carbohydrate

content, which are offered on our menus. Negative publicity related to these issues could also

impact our financial performance. Smoking bans by state or local governments could adversely affect

our performance as well. Michigan has enacted a smoking ban which goes into effect May 1, 2010.

Economic conditions could affect consumer discretionary spending, which could impact the amount of

money they have to spend in our restaurants, again negatively impacting our revenue and profits.

We Are Susceptible To Adverse Trends and Economic Conditions in Michigan and Florida

The Michigan economy is tied to a large degree to the automotive industry. This area is susceptible

to strikes, industry lay-offs and general economic contraction, which could negatively affect

customer counts and consumer discretionary spending, and which in turn would adversely impact our

revenue and profits. The Florida economy is heavily tied to the real estate market. Any continued

decline in the residential real estate market may have a negative impact on our individual customer

base, whether through loss of value or lack of new construction jobs, and may result in decreased

sales at our Florida locations.

We Could Be Adversely Impacted By Weather in Florida

Our locations in Florida are and will be located in the Tampa, Sarasota and Bradenton markets along

the Gulf of Mexico. This area is prone to tropical storm and hurricane conditions and the impact

from such storms could cause substantial damage to one or more restaurants and this could

negatively impact our financial performance. Further, future property insurance deductibles and

premiums could negatively impact our profits.

Our Ability to Raise Capital In The Future May Be Limited, Which Could Adversely Impact Our

Business

Changes in our operating plans, acceleration of our expansion plans, lower than anticipated sales,

increased expenses or other events, including those described in this section, may cause us to seek

additional debt or equity financing. Such financing may not be available on acceptable terms, or at

all, and our failure to raise capital when needed could negatively impact our growth and other

plans as well as our financial condition and results of operations. Additional equity financing, if

available may be dilutive to the holders of our common stock and may involve significant cash

payment obligations and covenants and/or financial ratios that restrict our ability to operate and

expand.

Our Current Insurance May Not Provide Adequate Levels of Coverage against Claims

We currently maintain insurance that is customary and required in our franchise agreements and

leases. However, there are types of losses we may incur that cannot be insured against or that we

believe are not economically reasonable to insure against, such as losses due to natural disasters

or terrorism. Such damages from loses may cause direct economic impact to us and our restaurants.

Improper

Food Handling May Adversely Affect Our Business

There are health risks associated with eating improperly handled or prepared food items. Negative

publicity resulting from improper handling of food items may adversely affect our sales and impact

our revenue and profits negatively. Although we carry insurance for these types of events, the

coverage may not be sufficient and we may sustain losses.

Risks of Continuing Losses and Financial Covenant Violations

There can be no assurances that in the future the Company will be in compliance with all covenants

of its current or future debt agreements or that its lenders would waive any violations of such

covenants. Non-compliance with debt covenants by the Company could have a material adverse effect

on the Company’s business, results of operations and financial condition.

15

Table of Contents

ITEM 2. PROPERTIES

We do not own any real property for use in our operations or otherwise. We do rent space from third

parties on the terms described more specifically below:

| Monthly | ||||||||||

| Location | Landlord | Rent | Lease Ends | Options | ||||||

Company Headquarters

21751 W. Eleven Mile Rd Ste 208 Southfield, MI 48076 |

David M. Tisdale & Company | $ | 3,835 | 4/30/2010 | none | |||||

AMC North Port, Inc.

4301 Aiden Lane North Port, FL 34286 |

North Port Gateway, LLC | $ | 6,129 | 8/5/2017 | Two 5 year Options | |||||

AMC Riverview, Inc.

10605 Big Bend Road Riverview, FL 33569 |

Shoppes of Southbay, LLC | $ | 9,600 | 8/27/2017 | Two 5 year Options | |||||

Berkley Burgers, Inc.

2972 Coolidge Ave. Berkley, MI 48072 |

TM Apple, LLC (affiliate) | $ | 6,306 | 1/13/2023 | Three 5 year Options | |||||

AMC Grand Blanc, Inc.

8251 Trillium Circle #102 Grand Blanc, MI 48439 |

Trillium Circle, LLC | $ | 10,282 | 3/16/2018 | Two 5 year Options | |||||

AMC Troy, Inc.

1873 East Big Beaver Rd. Troy, MI 48083 |

Troy Sports Center, LLC | $ | 13,750 | 9/1/2018 | Two 5 year Options | |||||

AMC Petoskey, Inc.

2180 Anderson Rd. #150 Petoskey, MI 49770 |

Terra Management Company | $ | 9,042 | 8/9/2018 | Two 5 year Options | |||||

Ann Arbor Burgers, Inc.

859 W. Eisenhower Parkway Ann Arbor, MI 48103 |

8600 Associates Limited Partnership | $ | 6,899 | 6/28/2018 | Two 5 year Options | |||||

AMC Flint, Inc.

3192 S. Linden Road Flint, MI 48507 |

Ramco Gershenson Properties Trust | $ | 4,800 | 12/21/2018 | Three 5 year Options | |||||

AMC Port Huron, Inc.

4355 24th Avenue, Suite 1 Port Huron, MI 48059 |

Port Builders, Inc. et al | $ | 6,500 | 6/1/2019 | Three 5 year Options | |||||

Berkley Burgers, Inc. is the only subsidiary renting from an affiliate. (See Certain

Relationships and Related Transactions and Director Independence)

The Company currently has no policy with respect to investments or interests in real estate

mortgages, securities or interests in persons primarily engaged in real estate activities.

16

Table of Contents

ITEM 3. LEGAL PROCEEDINGS

Occasionally, we are a defendant in litigation arising in the ordinary course of our business,

including claims arising from personal injuries, contract claims, dram shop claims, employment

related claims and claims from guests or employees alleging injury, illness or other food quality,

health or operational concerns. To date, none of these types of litigation, most of which are

typically covered by insurance, has had a material effect on us. We have insured and continue to

insure against most of these types of claims. A judgment on any claim not covered by or in excess

of our insurance coverage could adversely affect our financial condition or results of operations.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES |

||

Market Information. The Company’s common stock is traded on the OTC Bulletin Board under the symbol

DFRH; however, trading in our stock is very limited, and there are no assurances that this trading

market will expand or even continue. Our stock was granted a trading symbol on October 6, 2008 and

during the quarter ending December 27, 2009, the range of bid prices was $4.00 to $5.40. These bid

prices reflect inter-dealer prices, without retail mark

ups or mark downs or commissions and may not represent actual transactions. The Company’s transfer

agent is Fidelity Transfer Company, 8915 S. 700 E, Suite 102, Sandy, Utah 84070.

Holders. As of March 26, 2010, there were approximately 123 record holders of 18,876,000 shares of

the Company’s common stock.

Dividend Policy. We have not declared or paid any cash dividends on our common stock and we do not

intend to declare or pay any cash dividend in the foreseeable future. The payment of dividends, if

any, is within the discretion of our Board of Directors and will depend on our earnings, if any,

our capital requirements and financial condition and such other factors as our Board of Directors

may consider.

Securities Authorized for Issuance Under Equity Compensation. We have not authorized the issuance

of any of our securities in connection with any form of equity compensation plan.

Recent Sales of Unregistered Securities. During the fourth quarter of 2009, the twelve warrant

holders listed below exercised warrants to purchase the Company’s common stock. The warrants were

originally granted in connection with a private placement made by the Company in November 2006

prior to registration. These sales were similarly made pursuant to a private placement exemption

from registration. Each of the warrants was exercised at the exercise price of $1.00 per share of

our common stock for the consideration and on the date listed below:

| Shares of Common | ||||||||

| Investor | Date of Purchase | Stock Acquired | Consideration Paid | |||||

Eric Samuelson

|

November 30, 2009 | 150,000 | Surrender and forgiveness of $150,000 note granted to Mr. Samuelson by the Company in exchange for loan from Mr. Samuleson to the Company of $142,500 | |||||

David Ligotti

|

November 30, 2009 | 100,000 | Surrender and forgiveness of $100,000 note granted to Mr. Ligotti by the Company in exchange for loan from Mr. Ligotti to the Company of $95,000 | |||||

17

Table of Contents

| Shares of Common | ||||||||

| Investor | Date of Purchase | Stock Acquired | Consideration Paid | |||||

Gregory Stevens

|

November 30, 2009 | 100,000 | Surrender and forgiveness of $100,000 note granted to Mr. Stevens by the Company in exchange for loan from Mr. Stevens to the Company of $95,000 | |||||

John Bowling

|

December 30, 2009 | 100,000 | $100,000 cash | |||||

John R. Burke

|

November 27, 2009 and December 30, 2009 (50,000 ea) | 100,000 | $100,000 cash | |||||

Bruce Stewart

|

November 24, 2009 | 50,000 | $50,000 cash | |||||

Norma Stewart

|

November 24, 2009 | 50,000 | $50,000 cash | |||||

Edie Dopking

|

December 8, 2009 | 50,000 | $50,000 cash | |||||

Kenneth Bush

|

December 30, 2009 | 25,000 | $25,000 cash | |||||

John Eric Bush

|

December 30, 2009 | 25,000 | $25,000 cash | |||||

Steve Waddle

|

December 30, 2009 | 25,000 | $25,000 cash | |||||

Larry Timmons

|

December 30, 2009 | 25,000 | $25,000 cash | |||||

On July 30, 2007, each member of the Board of Directors was granted 30,000 stock options that vest

ratably over three years and expire after six years. The option price is $2.50 per share. As of

March 26, 2010, Directors with 20,000 vested and unexercised options include T. Michael Ansley,

Gregory Stevens, David G. Burke and David Ligotti. Director Jay Alan Dusenberry exercised his

option to purchase 6,000 shares of our common stock at $2.50 per share on October 12, 2009 pursuant

to a private placement exemption. Mr. Dusenberry has 14,000 vested and unexercised options as of

March 26, 2010.

ITEM 6. SELECTED FINANCIAL DATA

Not Applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

Management’s Discussion and Analysis of Financial Condition and Results of Operation included at

pages F-1 through F-9 of this Annual Report is incorporated herein by reference.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not Applicable.

ITEM 8. CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The Consolidated Financial Statements, Notes to Consolidated Financial Statements and the Reports

of Independent Registered Accounting Firm included at pages F-10 through F-32 of this Annual Report

are incorporated herein by reference.

18

Table of Contents

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

The Audit Committee of the Board of Directors of Diversified Restaurant Holdings, Inc. annually

considers and recommends to the Board the selection of independent public accountants. On April 21,

2009 after an evaluation process as recommended by DRH’s Audit Committee, the Board of Directors

appointed Silberstein Ungar, PLLC (“SU”, formerly known as Maddox Ungar Silberstein, PLLC) as DRH’s

independent auditors for the 2009 fiscal year, replacing Rehmann Robson, PC (“Rehmann”).