Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 CFO SECTION 906 CERTIFICATION - CrossAmerica Partners LP | capl-ex322_8.htm |

| EX-32.1 - EX-32.1 CEO SECTION 906 CERTIFICATION - CrossAmerica Partners LP | capl-ex321_11.htm |

| EX-31.2 - EX-31.2 CFO SECTION 302 CERTIFICATION - CrossAmerica Partners LP | capl-ex312_10.htm |

| EX-31.1 - EX-31.1 CEO SECTION 302 CERTIFICATION - CrossAmerica Partners LP | capl-ex311_7.htm |

| EX-23.1 - EX-23.1 CONSENT OF INDEPENDENT AUDITOR - CrossAmerica Partners LP | capl-ex231_6.htm |

| EX-21.1 - EX-21.1 LIST OF SUBSIDIARIES - CrossAmerica Partners LP | capl-ex211_9.htm |

| EX-4.1 - EX-4.1 DESCRIPTION OF COMMON UNITS - CrossAmerica Partners LP | capl-ex41_128.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

|

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-35711

CROSSAMERICA PARTNERS LP

(Exact name of registrant as specified in its charter)

|

Delaware |

|

45-4165414 |

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

600 Hamilton Street, Suite 500 Allentown, PA |

|

18101 (Zip Code) (610) 625-8000 |

|

(Address of Principal Executive Offices) |

|

(Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Units |

CAPL |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of our common units based on the closing price on the New York Stock Exchange on June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, held by non-affiliates of the registrant was approximately $309.0 million.

As of February 21, 2020, the registrant had outstanding 37,023,114 common units.

Documents Incorporated by Reference: None.

The following is a list of certain acronyms and terms generally used in the industry and throughout this document:

|

CrossAmerica Partners LP and subsidiaries: |

|||

|

|

|

|

|

|

CrossAmerica Partners LP |

CrossAmerica, the Partnership, we, us, our |

||

|

|

|

|

|

|

LGP Operations LLC |

a wholly owned subsidiary of the Partnership |

||

|

|

|

|

|

|

LGW |

Lehigh Gas Wholesale LLC |

||

|

|

|

|

|

|

LGPR |

LGP Realty Holdings LP |

||

|

|

|

|

|

|

LGWS |

Lehigh Gas Wholesale Services, Inc. and subsidiaries |

||

|

|

|

||

|

CrossAmerica Partners LP related parties at any point during 2019: |

|||

|

|

|

|

|

|

Circle K |

Circle K Stores Inc., a Texas corporation, and a wholly owned subsidiary of Couche-Tard |

||

|

|

|

|

|

|

Couche-Tard |

Alimentation Couche-Tard Inc. (TSX: ATD.A ATD.B) |

||

|

Couche-Tard Board |

the Board of Directors of Couche-Tard |

||

|

|

|

|

|

|

CST |

CST Brands, LLC and subsidiaries, indirectly owned by Circle K |

||

|

|

|

|

|

|

CST Fuel Supply |

CST Fuel Supply LP is the parent of CST Marketing and Supply, indirectly owned by Circle K. Since July 1, 2015, we have owned a 17.5% limited partner interest in CST Fuel Supply. See Note 25 to the financial statements for information regarding the exchange of this investment for certain assets owned by Circle K. |

||

|

|

|

|

|

|

CST Marketing and Supply |

CST Marketing and Supply, LLC, indirectly owned by Circle K. It is CST’s wholesale motor fuel supply business, which provides wholesale fuel distribution to the majority of CST’s legacy U.S. retail convenience stores on a fixed markup per gallon. |

||

|

|

|

|

|

|

CST Services |

CST Services LLC, a wholly owned subsidiary of Circle K |

||

|

|

|

|

|

|

DMI |

Dunne Manning Inc. (formerly Lehigh Gas Corporation), an entity affiliated with the Topper Group |

||

|

|

|

|

|

|

DMP |

Dunne Manning Partners LLC, an entity affiliated with the Topper Group and controlled by Joseph V. Topper, Jr. Since November 19, 2019, DMP has owned 100% of the membership interests in the sole member of the General Partner. |

||

|

|

|

|

|

|

DMR |

Dunne Manning Realty LP, an entity affiliated with the Topper Group |

||

|

|

|

|

|

|

DMS |

Dunne Manning Stores LLC (formerly known as Lehigh Gas-Ohio, LLC), an entity affiliated with the Topper Group. DMS is an operator of retail motor fuel stations. DMS leases retail sites from us in accordance with a master lease agreement and purchases a significant portion of its motor fuel for these sites from us on a wholesale basis under rack plus pricing. The financial results of DMS are not consolidated with ours. |

||

|

|

|

|

|

|

General Partner |

CrossAmerica GP LLC, the General Partner of CrossAmerica, a Delaware limited liability company, indirectly owned by the Topper Group |

||

|

|

|

|

|

|

Topper Group |

Joseph V. Topper, Jr., collectively with his affiliates and family trusts that have ownership interests in the Partnership. Joseph V. Topper, Jr. is the founder of the Partnership and a member of the Board. The Topper Group is a related party and large holder of our common units. |

||

|

|

|

|

|

|

TopStar |

TopStar Inc., an entity affiliated with a family member of Joseph V. Topper, Jr. TopStar is an operator of convenience stores that leases retail sites from us but does not purchase fuel from us. |

||

|

|

|

||

|

|

|

||

1

|

|

|

|

|

|

Nice N Easy Assets |

The assets acquired from Nice N Easy Grocery Shoppes in November 2014 |

||

|

|

|

|

|

|

Landmark Assets |

The assets acquired from Landmark Industries in January 2015 |

||

|

|

|

|

|

|

Franchised Holiday Stores |

The franchised Holiday stores acquired in March 2016 |

||

|

|

|

|

|

|

Jet-Pep Assets |

The assets acquired from Jet-Pep, Inc. in November 2017 |

||

|

|

|

||

|

Other Defined Terms: |

|

||

|

|

|

|

|

|

Applegreen |

Applegreen plc or one of its subsidiaries |

||

|

|

|

|

|

|

ASC |

Accounting Standards Codification |

||

|

|

|

|

|

|

ASU |

Accounting Standards Update |

||

|

|

|

|

|

|

Board |

Board of Directors of our General Partner |

||

|

|

|

|

|

|

BP |

BP p.l.c. |

||

|

|

|

|

|

|

Branded Motor Fuels |

Motor fuels that are purchased from major integrated oil companies and refiners under supply agreements. We take legal title to the motor fuel when we receive it at the rack and generally arrange for a third-party transportation provider to take delivery of the motor fuel at the rack and deliver it to the appropriate sites in our network. |

||

|

|

|

|

|

|

Circle K Omnibus Agreement |

The Amended and Restated Omnibus Agreement, dated October 1, 2014, as amended effective January 1, 2016, February 1, 2018 and April 29, 2019 by and among CrossAmerica, the General Partner, DMI, DMS, CST Services and Joseph V. Topper, Jr., which amends and restates the original omnibus agreement that was executed in connection with CrossAmerica’s initial public offering on October 30, 2012. The terms of the Circle K Omnibus Agreement were approved by the conflicts committee of the Board. Pursuant to the Circle K Omnibus Agreement, CST Services agrees, among other things, to provide, or cause to be provided, to the Partnership certain management services. |

||

|

|

|

|

|

|

CST Fuel Supply Exchange |

Exchange Agreement, dated November 19, 2019, between the Partnership and Circle K. Pursuant to the CST Fuel Supply Exchange Agreement, Circle K has agreed to transfer to the Partnership certain owned and leased convenience store properties and related assets (including fuel supply agreements) and wholesale fuel supply contracts covering additional sites, and, in exchange, the Partnership has agreed to transfer to Circle K 100% of the limited partnership units in CST Fuel Supply. |

||

|

|

|

|

|

|

CST Merger |

The merger of Ultra Acquisition Corp., a Delaware corporation and an indirect, wholly owned subsidiary of Circle K (“Merger Sub”), with CST, with CST surviving the merger as a wholly owned subsidiary of Circle K, which closed on June 28, 2017. See CST Merger Agreement below. |

||

|

|

|

|

|

|

CST Merger Agreement |

CST’s Agreement and Plan of Merger entered into on August 21, 2016 with Circle K and Merger Sub. Under and subject to the terms and conditions of the CST Merger Agreement, on June 28, 2017, Merger Sub was merged with and into CST, with CST surviving the CST Merger as a wholly owned subsidiary of Circle K. |

||

|

|

|

|

|

|

DTW |

Dealer tank wagon contracts, which are variable cent per gallon priced wholesale motor fuel distribution or supply contracts; DTW also refers to the pricing methodology under such contracts |

||

|

|

|

|

|

|

EBITDA |

Earnings before interest, taxes, depreciation, amortization and accretion, a non-GAAP financial measure |

||

|

|

|

|

|

|

EICP |

The Partnership’s Lehigh Gas Partners LP Executive Income Continuity Plan, as amended |

||

|

|

|

|

|

|

EMV |

Payment method based upon a technical standard for smart payment cards, also referred to as chip cards |

||

|

|

|

|

|

2

|

Securities Exchange Act of 1934, as amended |

|||

|

|

|

|

|

|

ExxonMobil |

ExxonMobil Corporation |

||

|

|

|

|

|

|

FASB |

Financial Accounting Standards Board |

||

|

|

|

|

|

|

Form 10-K |

CrossAmerica’s Annual Report on Form 10-K for the year ended December 31, 2019 |

||

|

|

|

||

|

FTC |

U.S. Federal Trade Commission |

||

|

|

|

|

|

|

Getty Lease |

In May 2012, the Predecessor Entity, which represents the portion of the business of DMI and its subsidiaries and affiliates contributed to the Partnership in connection with the initial public offering, entered into a 15-year master lease agreement with renewal options of up to an additional 20 years with Getty Realty Corporation. |

||

|

|

|

|

|

|

GP Purchase |

Purchase by DMP from subsidiaries of Circle K of: 1) 100% of the membership interests in the sole member of the General Partner; 2) 100% of the Incentive Distribution Rights issued by the Partnership; and 3) an aggregate of 7,486,131 common units of the Partnership. These transactions closed on November 19, 2019. |

||

|

|

|

|

|

|

IDRs |

Incentive Distribution Rights represent the right to receive an increasing percentage of quarterly distributions after the target distribution levels have been achieved, as defined in our Partnership Agreement. As a result of the GP Purchase, DMP owned 100% of the outstanding IDRs from November 19, 2019 through February 6, 2020. See Note 25 to the financial statements for information regarding the elimination of the IDRs. |

||

|

|

|

|

|

|

Internal Revenue Code |

Internal Revenue Code of 1986, as amended |

||

|

|

|

|

|

|

IPO |

Initial public offering of CrossAmerica Partners LP on October 30, 2012 |

||

|

|

|

|

|

|

IRS |

Internal Revenue Service |

||

|

|

|

|

|

|

LIBOR |

London Interbank Offered Rate |

||

|

|

|

|

|

|

MD&A |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

||

|

|

|

|

|

|

Motiva |

Motiva Enterprises, LLC |

||

|

|

|

|

|

|

NTI |

CST’s new to industry stores opened after January 1, 2008, which is generally when CST began designing and operating its larger format stores that accommodate broader merchandise categories and food offerings and have more fuel dispensers than its legacy stores |

||

|

|

|

|

|

|

NYSE |

New York Stock Exchange |

||

|

|

|

|

|

|

Partnership Agreement |

The First Amended and Restated Agreement of Limited Partnership of CrossAmerica Partners LP, dated as of October 1, 2014, as amended; see Note 25 to the financial statements regarding the elimination of the IDRs, which triggered the need to further amend the Partnership Agreement |

||

|

|

|

|

|

|

Plan |

In connection with the IPO, the General Partner adopted the Lehigh Gas Partners LP 2012 Incentive Award Plan, a long-term incentive plan for employees, officers, consultants and directors of the General Partner and any of its affiliates who perform services for the Partnership |

||

|

|

|

|

|

|

Predecessor Entity |

Wholesale distribution contracts and real property and leasehold interests contributed to the Partnership in connection with the IPO |

||

|

|

|

|

|

|

Retail site |

A general term to refer to convenience stores, including those operated by commission agents, independent dealers, Circle K, DMS or lessee dealers, as well as company operated sites |

||

|

|

|

|

|

|

RIN |

Renewable identification number, an identifier used by governmental agencies to track a specific batch of renewable fuel |

||

|

|

|

|

|

|

SEC |

U.S. Securities and Exchange Commission |

||

|

|

|

|

|

|

Tax Cuts and Jobs Act |

On December 22, 2017, the U.S. government enacted tax legislation formally known as Public Law No. 115-97, commonly referred to as the Tax Cuts and Jobs Act |

||

3

|

|

|

|

|

|

Terms Discounts |

Discounts for prompt payment and other rebates and incentives from our suppliers for a majority of the gallons of motor fuel purchased by us, which are recorded within cost of sales. Prompt payment discounts are based on a percentage of the purchase price of motor fuel. |

||

|

|

|

|

|

|

Topper Group Omnibus Agreement |

The Topper Group Omnibus Agreement, effective January 1, 2020, by and among the Partnership, the General Partner and DMI. The terms of the Topper Group Omnibus Agreement were approved by the conflicts committee of the Board, which is composed of the independent directors of the Board. Pursuant to the Topper Group Omnibus Agreement, DMI agrees, among other things, to provide, or cause to be provided, to the Partnership certain management services at cost without markup. |

||

|

|

|

|

|

|

Transitional Omnibus Agreement |

Upon the closing of the GP Purchase, the Circle K Omnibus Agreement was terminated and the Partnership entered into a Transitional Omnibus Agreement, dated as of November 19, 2019, among the Partnership, the General Partner and Circle K. Pursuant to the Transitional Omnibus Agreement, Circle K has agreed, among other things, to continue to provide, or cause to be provided, to the Partnership certain management services, administrative and operating services, as provided under the Circle K Omnibus Agreement through June 30, 2020 with respect to certain services, unless earlier terminated or unless the parties extend the term of certain services. In addition, from January 1, 2020 until the closing of the CST Fuel Supply Exchange, the General Partner will provide Circle K with certain administrative and operational services, on the terms and conditions set forth in the Transitional Omnibus Agreement. |

||

|

|

|

|

|

|

U.S. GAAP |

U.S. Generally Accepted Accounting Principles |

||

|

|

|

|

|

|

UST |

Underground storage tanks |

||

|

|

|

|

|

|

Valero |

Valero Energy Corporation and, where appropriate in context, one or more of its subsidiaries, or all of them taken as a whole |

||

|

|

|

|

|

|

WTI |

West Texas Intermediate crude oil |

||

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements, including in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include the information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, credit ratings, distribution growth, potential growth opportunities, potential operating performance improvements, potential improvements in return on capital employed, the effects of competition and the effects of future legislation or regulations. You can identify our forward-looking statements by the words “anticipate,” “estimate,” “believe,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “forecast,” “guidance,” “outlook,” “effort,” “target” and similar expressions. Such statements are based on our current plans and expectations and involve risks and uncertainties that could potentially affect actual results. These forward-looking statements include, among other things, statements regarding:

|

|

• |

future retail and wholesale gross profits, including gasoline, diesel and convenience store merchandise gross profits; |

|

|

• |

our anticipated level of capital investments, primarily through acquisitions, and the effect of these capital investments on our results of operations; |

|

|

• |

anticipated trends in the demand for, and volumes sold of, gasoline and diesel in the regions where we operate; |

|

|

• |

volatility in the equity and credit markets limiting access to capital markets; |

|

|

• |

our ability to integrate acquired businesses and to transition retail sites best suited for wholesale operations to dealer operated sites; |

|

|

• |

expectations regarding environmental, tax and other regulatory initiatives; and |

|

|

• |

the effect of general economic and other conditions on our business. |

In general, we based the forward-looking statements included in this report on our current expectations, estimates and projections about our company and the industry in which we operate. We caution you that these statements are not guarantees of future performance and involve risks and uncertainties we cannot predict. We anticipate that subsequent events and market developments will cause our estimates to change. In addition, we based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. Accordingly, our actual outcomes and results may differ materially from what we have expressed or forecasted in the forward-looking statements. Any differences could result from a variety of factors, including the following:

|

|

• |

the Topper Group’s business strategy and operations and the Topper Group’s conflicts of interest with us; |

|

|

• |

availability of cash flow to pay the current quarterly distributions on our common units; |

|

|

• |

the availability and cost of competing motor fuels; |

|

|

• |

motor fuel price volatility or a reduction in demand for motor fuels; |

|

|

• |

competition in the industries and geographical areas in which we operate; |

|

|

• |

the consummation of financing, acquisition or disposition transactions and the effect thereof on our business; |

|

|

• |

environmental compliance and remediation costs; |

|

|

• |

our existing or future indebtedness and the related interest expense and our ability to comply with debt covenants; |

|

|

• |

our liquidity, results of operations and financial condition; |

|

|

• |

failure to comply with applicable tax and other regulations or governmental policies; |

|

|

• |

future legislation and changes in regulations, governmental policies, immigration laws and restrictions or changes in enforcement or interpretations thereof; |

|

|

• |

future regulations and actions that could expand the non-exempt status of employees under the Fair Labor Standards Act; |

|

|

• |

future income tax legislation; |

|

|

• |

changes in energy policy; |

|

|

• |

increases in energy conservation efforts; |

|

|

• |

technological advances; |

|

|

• |

the impact of worldwide economic and political conditions; |

5

|

|

• |

weather conditions or catastrophic weather-related damage; |

|

|

• |

earthquakes and other natural disasters; |

|

|

• |

hazards and risks associated with transporting and storing motor fuel; |

|

|

• |

unexpected environmental liabilities; |

|

|

• |

the outcome of pending or future litigation; and |

|

|

• |

our ability to comply with federal and state laws and regulations, including those related to environmental matters, the sale of alcohol, cigarettes and fresh foods, employment and health benefits, including the Affordable Care Act, immigration and international trade. |

You should consider the areas of risk described above, as well as those set forth in the section entitled “Risk Factors” included in this Form 10-K, in connection with considering any forward-looking statements that may be made by us and our businesses generally. We cannot assure you that anticipated results or events reflected in the forward-looking statements will be achieved or will occur. The forward-looking statements included in this report are made as of the date of this report. We undertake no obligation to publicly release any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events after the date of this report.

6

Overview

We were formed as a Delaware limited partnership in 2011 primarily engaged in the wholesale distribution of motor fuel and the ownership and leasing of real estate used in the retail distribution of motor fuel. Through September 2019, we also generated revenues from the operation of company operated retail sites.

On November 19, 2019, subsidiaries of DMP purchased from subsidiaries of Circle K: 1) 100% of the membership interests in the sole member of the General Partner; 2) 100% of the IDRs issued by the Partnership; and 3) an aggregate of 7,486,131 common units of the Partnership. Joseph V. Topper, Jr. is the founder and, since November 19, 2019, chairman of the Board.

Through its control of DMP, the Topper Group controls the sole member of our General Partner and has the ability to appoint all of the members of the Board and to control and manage the operations and activities of the Partnership. As of February 21, 2020, the Topper Group also has beneficial ownership of a 47.7% limited partner interest in the Partnership.

Our principal executive office address is 600 Hamilton Street, Suite 500, Allentown, PA 18101, and our telephone number is (610) 625-8000. Our common units trade on the NYSE under the ticker symbol “CAPL.”

The financial statements reflect the consolidated results of the Partnership and its wholly owned subsidiaries. Our primary operations are conducted by the following consolidated wholly owned subsidiaries:

|

|

• |

LGW, which distributes motor fuels on a wholesale basis and generates qualifying income under Section 7704(d) of the Internal Revenue Code; |

|

|

• |

LGPR, which functions as the real estate holding company of CrossAmerica and holds assets that generate qualifying rental income under Section 7704(d) of the Internal Revenue Code; and |

|

|

• |

LGWS, which owns and leases (or leases and sub-leases) real estate and personal property used in the retail distribution of motor fuels, as well as provides maintenance and other services to its customers. In addition, LGWS sells motor fuel on a retail basis at sites operated by commission agents. Through September 2019, LGWS also distributed motor fuels on a retail basis and sold convenience merchandise items to end customers at company operated retail sites. Income from LGWS generally is not qualifying income under Section 7704(d) of the Internal Revenue Code. |

We conduct our business through two operating segments, Wholesale and Retail. As of December 31, 2019, we distributed motor fuel to approximately 1,300 sites located in 31 states.

Available Information

Our internet website is www.crossamericapartners.com. Information on this website is not part of this Form 10-K. Annual reports on our Form 10-K, quarterly reports on our Form 10-Q and our current reports on Form 8-K filed with (or furnished to) the SEC are available on this website under the “Investor Relations” tab and are free of charge, soon after such material is filed or furnished. In this same location, we also post our corporate governance guidelines, code of ethics and business conduct and the charters of the committees of our Board. These documents are available in print to any unitholder that makes a written request to CrossAmerica Partners L.P. Attn: Corporate Secretary, 600 Hamilton Street, Suite 500, Allentown, Pennsylvania 18101.

Operations

Wholesale Segment

Our primary operation is the wholesale distribution of motor fuel. Our Wholesale segment generated 2019 revenues of $2.0 billion. The wholesale segment includes the wholesale distribution of motor fuel to lessee dealers, independent dealers, commission agents, DMS, Circle K and, through September 2019, company operated retail sites. We have exclusive motor fuel distribution contracts with lessee dealers who lease the property from us. We also have exclusive distribution contracts with independent dealers to distribute motor fuel but do not collect rent from the independent dealers. Similar to lessee dealers, we have motor fuel distribution agreements with DMS and Circle K and collect rent from both.

7

We are one of the ten largest independent distributors by motor fuel volume in the United States for ExxonMobil, BP and Shell, and we also distribute Chevron, Sunoco, Valero, Gulf, Citgo, Marathon and Phillips 66-branded motor fuels (approximately 82% of the motor fuel we distributed during 2019 was branded). We receive a fixed mark-up per gallon of motor fuel on approximately 82% of gallons sold to our customers. The remaining gallons are primarily DTW priced contracts with our customers. These contracts provide for variable, market-based pricing. An increase in DTW gross profit results from the acquisition cost of wholesale motor fuel declining at a faster rate as compared to the rate that retail motor fuel prices decline. Conversely, our DTW motor fuel gross profit declines when the cost of wholesale motor fuel increases at a faster rate as compared to the rate that retail motor fuel prices increase.

Regarding our supplier relationships, a majority of our total gallons of motor fuel purchased are subject to Terms Discounts for prompt payment and other rebates and incentives, which are recorded within cost of sales. Prompt payment discounts are based on a percentage of the purchase price of motor fuel. As such, the dollar value of these discounts increases and decreases corresponding with motor fuel prices. Therefore, in periods of lower wholesale motor fuel prices, our gross profit is negatively affected, and, in periods of higher wholesale motor fuel prices, our gross profit is positively affected (as it relates to these discounts). Based on our current volumes, we estimate a $10 per barrel change in the price of crude oil would impact our overall annual wholesale motor fuel gross profit by approximately $2 million related to these payment discounts.

The following table highlights the aggregate volume of motor fuel distributed by our Wholesale segment to each of our principal customer groups (in millions):

|

|

|

Gallons of Motor Fuel Distributed Year Ended December 31, |

|

|

Wholesale Fuel Distribution Sites End of Year |

|

||||||||||||||||||

|

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

||||||

|

Independent dealers (a) |

|

|

314.9 |

|

|

|

331.4 |

|

|

|

346.2 |

|

|

|

369 |

|

|

|

362 |

|

|

|

384 |

|

|

Lessee dealers |

|

|

391.8 |

|

|

|

322.1 |

|

|

|

309.6 |

|

|

|

648 |

|

|

|

500 |

|

|

|

438 |

|

|

DMS |

|

|

75.5 |

|

|

|

115.4 |

|

|

|

138.4 |

|

|

|

68 |

|

|

|

86 |

|

|

|

146 |

|

|

Circle K |

|

|

63.0 |

|

|

|

70.4 |

|

|

|

78.1 |

|

|

|

28 |

|

|

|

43 |

|

|

|

43 |

|

|

Commission agents |

|

|

128.9 |

|

|

|

140.7 |

|

|

|

86.3 |

|

|

|

169 |

|

|

|

170 |

|

|

|

181 |

|

|

Company operated retail sites |

|

|

29.9 |

|

|

|

67.3 |

|

|

|

73.4 |

|

|

|

— |

|

|

|

63 |

|

|

|

70 |

|

|

Total |

|

|

1,004.0 |

|

|

|

1,047.3 |

|

|

|

1,032.0 |

|

|

|

1,282 |

|

|

|

1,224 |

|

|

|

1,262 |

|

|

(a) |

Gallons distributed to independent dealers include gallons distributed to sub-wholesalers and commercial accounts, which are not included in the site counts reported above. |

Independent Dealer Sites

|

|

• |

The independent dealer owns or leases the property and owns all motor fuel and convenience store inventory. |

|

|

• |

We contract to exclusively distribute motor fuel to the independent dealer at a fixed mark-up per gallon or, in some cases, DTW. |

|

|

• |

Distribution contracts with independent dealers are typically seven to 10 years in length. |

|

|

• |

As of December 31, 2019, the average remaining distribution contract term was 5.3 years. |

Lessee Dealer Sites

|

|

• |

We own or lease the property and then lease or sublease the site to a dealer. |

|

|

• |

The lessee dealer owns all motor fuel and retail site inventory and sets its own pricing and gross profit margins. |

|

|

• |

We collect wholesale motor fuel margins at a fixed mark-up per gallon or, in some cases, DTW. |

|

|

• |

Under our distribution contracts, we agree to supply a particular branded motor fuel or unbranded motor fuel to a site or group of sites and arrange for all transportation. |

|

|

• |

Exclusive distribution contracts with dealers who lease property from us run concurrent in length to the retail site’s lease period (generally three to 10 years). |

|

|

• |

Leases are generally triple net leases. |

|

|

• |

As of December 31, 2019, the average remaining lease agreement term was 3.7 years. |

8

|

|

• |

We own or lease the property and then lease or sublease the site to DMS. |

|

|

• |

We entered into a 15-year motor fuel distribution agreement with DMS pursuant to which we distribute to DMS motor fuel at a fixed mark-up per gallon. |

|

|

• |

We entered into 15-year triple-net lease agreements with DMS pursuant to which DMS leases sites from us. |

|

|

• |

DMS owns motor fuel and retail site inventory and sets its own pricing and gross profit margin. |

|

|

• |

As of December 31, 2019, the average remaining term on our motor fuel distribution agreements with DMS was 7.8 years. The average remaining term on our lease agreements with DMS was 8.6 years. See Note 25 to the financial statements regarding the acquisition of retail and wholesale assets from the Topper Group and certain other parties, which will result in the termination of contracts with DMS. |

Circle K Sites

|

|

• |

In conjunction with the joint acquisitions of Nice N Easy Assets in 2014 and Landmark Assets with CST and the purchase of NTIs by us from CST in 2015, we own the property and lease the retail sites to Circle K. With respect to the Nice N Easy Asset and Landmark Asset acquisitions, we also entered into a 10-year motor fuel distribution agreement with CST, pursuant to which we distribute motor fuels to Circle K at a fixed mark-up per gallon. |

|

|

• |

We lease sites to Circle K under a 10-year triple-net master lease agreement. |

|

|

• |

Circle K owns all motor fuel and retail site inventory and sets its own pricing and gross profit margin. |

|

|

• |

As of December 31, 2019, the remaining term on our fuel distribution agreement with Circle K was 4.9 years. The average remaining term on our lease agreements with Circle K was 5.2 years. |

Rental Income

We also generate revenues through leasing or subleasing our real estate. We own or lease real and personal property and we lease or sublease that property to tenants, the substantial majority of which are wholesale customers as described above. As such, we manage our real estate leasing activities congruently with our Wholesale segment. We own approximately 61% of our properties that we lease to our dealers or utilize in our retail business. Our lease agreements with third-party landlords have an average remaining lease term of 5.8 years as of December 31, 2019. Not all of the rental income we earn is a qualifying source of income under Section 7704(d) of the Internal Revenue Code. For example, while Circle K owned our General Partner, rental income from Circle K was not qualifying income. Rental income from DMS is qualifying income because the Topper Group owns less than 10% of DMS.

The following table presents rental income (in millions), including rental income from commission agents that is included in the Retail segment, and the number of sites from which rental income was generated:

|

|

|

Rental Income Year Ended December 31, |

|

|

Sites from which Rental Income was Generated End of Year |

|

||||||||||||||||||

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|||||||

|

Total |

|

$ |

90.1 |

|

|

$ |

85.6 |

|

|

$ |

86.3 |

|

|

|

1,003 |

|

|

|

880 |

|

|

|

885 |

|

CST Fuel Supply

In 2015, we purchased a 17.5% limited partner interest in CST Fuel Supply. We receive pro rata distributions from CST Fuel Supply related to CST Marketing and Supply’s distribution of motor fuel to the majority of CST’s legacy U.S. retail sites.

See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Developments” for a discussion of the CST Fuel Supply Exchange.

9

Our Retail segment generated 2019 revenues of $456 million. The Retail segment includes the retail sale of motor fuel at retail sites operated by commission agents and through September 2019, the sale of convenience merchandise items and the retail sale of motor fuel at company operated retail sites.

Subsequent to an acquisition, we evaluate the eventual long-term operation of each retail site acquired: (a) to be converted into a lessee dealer; (b) to be operated as a company operated retail site; or (c) other strategic alternatives, including selling the site. By converting retail sites into lessee dealers, we continue to benefit from motor fuel distribution volumes as well as rental income from lease or sublease arrangements while reducing operating expenses.

In June 2019, we entered into master fuel supply and master lease agreements with Applegreen. During the third quarter of 2019, we dealerized 46 company operated Upper Midwest sites.

As a result, we have not had any company operated sites since September 30, 2019. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Developments” for discussion of the Partnership entering into an agreement to acquire retail and wholesale assets from the Topper Group and certain other parties by the end of the second quarter of 2020.

Commission Sites

|

|

• |

We own or lease the property and then lease or sublease the site to the commission agent, who pays rent to us and operates all the non-fuel related operations at the sites for its own account. |

|

|

• |

We own the motor fuel inventory, set the motor fuel pricing and generate revenue from the retail sale of motor fuels to the end customer. |

|

|

• |

We pay the commission agent a commission for each gallon of motor fuel sold. |

|

|

• |

LGW distributes motor fuel on a wholesale basis to LGWS, which owns the motor fuel inventory and distributes motor fuel to commission sites. LGW records qualifying wholesale motor fuel distribution gross income and LGWS records the non-qualifying retail gross income. |

|

|

• |

As of December 31, 2019, the average remaining motor fuel distribution and lease agreement term for our commission agents was 0.8 years. |

Company Operated Sites

|

|

• |

As noted above, we have not had any company operated sites since September 30, 2019. |

|

|

• |

We owned or leased the property, operated the retail site and retained all profits from motor fuel and retail site operations. |

|

|

• |

We owned the merchandise inventory and retained the profits from the sale of convenience merchandise items. |

|

|

• |

We owned the motor fuel inventory and set the motor fuel pricing. |

|

|

• |

We maintained inventory from the time of the purchase of motor fuel from third-party suppliers until the retail sale to the end customer. On average, we maintained approximately 5-days’ worth of motor fuel sales in inventory at each site. |

|

|

• |

LGW distributed on a wholesale basis all of the motor fuel required by our company operated sites to LGWS, which owned the motor fuel inventory and distributed motor fuel to retail customers. LGW recorded qualifying wholesale motor fuel distribution gross income and LGWS recorded the non-qualifying retail distribution gross income. |

10

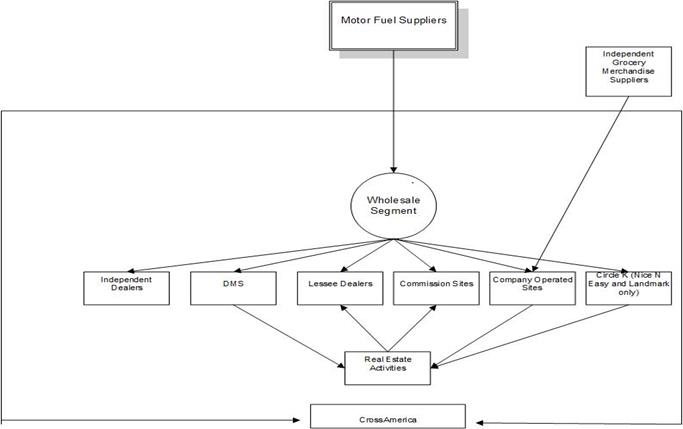

The following chart depicts how motor fuel is procured and distributed to our customer groups and how convenience merchandise items were procured and distributed to our company operated retail sites. The chart also depicts the relationship of our real estate activities to our customer groups.

Recent Developments

See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Developments” for a discussion of completed and anticipated transactions affecting our business in 2020 and forward.

Business Strategy and Objective

Our primary business objective is to generate sufficient cash flows from operations to make quarterly cash distributions to our unitholders and, over time, to increase our quarterly cash distributions. The amount of any distribution is subject to the discretion of the Board, and the Board may modify or revoke the cash distribution policy at any time. Our Partnership Agreement does not require us to pay any distributions.

Our business strategy to achieve our objective of paying and, over time, increasing our quarterly cash distributions, is focused on the following key initiatives:

|

|

• |

Expand within and beyond our existing markets through acquisitions. Since our IPO and through February 21, 2020, we have completed acquisitions for a total of approximately 600 fee and leasehold sites for total consideration of approximately $1.0 billion; |

|

|

• |

Enhance our real estate business’ cash flows by owning or leasing sites in prime locations; |

|

|

• |

Increase our Wholesale segment by expanding market share and growing rental income over time; |

|

|

• |

Maintain strong relationships with major integrated oil companies and refiners; and |

|

|

• |

Convert company operated retail sites acquired in future transactions that are best suited for wholesale operations to lessee dealer sites to provide for more stable cash flows and maximize qualifying income. |

11

We believe our competitive strengths will allow us to capitalize on our strategic opportunities, including:

|

|

• |

Stable cash flows from real estate rent income and wholesale motor fuel distribution; |

|

|

• |

Established history of acquiring sites and successfully integrating these sites and operations into our existing business; |

|

|

• |

Long-term relationships with major integrated oil companies and other key suppliers, which support our negotiations with and enable us to collaboratively work with our suppliers to maximize benefits to the Partnership; and |

|

|

• |

Prime real estate locations in areas with high traffic and considerable motor fuel consumption. |

Supplier Arrangements

We distribute Branded Motor Fuel under the Exxon, Mobil, BP, Shell, Chevron, Sunoco, Valero, Gulf, Citgo, Marathon and Phillips 66 brands to our customers. Branded Motor Fuels are purchased directly or indirectly through Circle K from major integrated oil companies and refiners under supply agreements. For 2019, our Wholesale segment purchased approximately 26%, 22%, 15% and 12% of its motor fuel from ExxonMobil, BP, Circle K and Motiva, respectively. We generally purchase the motor fuel at the supplier’s applicable terminal rack price, which typically changes daily. Certain suppliers offer volume rebates or incentive payments to drive volumes and provide an incentive for branding new locations. Certain suppliers require that all or a portion of any such incentive payments be repaid to the supplier in the event that the sites are rebranded within a stated number of years. We also purchase unbranded motor fuel for distribution at a rack price. As of December 31, 2019, our supply agreements had a weighted-average remaining term of approximately 6.1 years.

From the time of the November 2017 Jet-Pep Assets acquisition through October 31, 2018, we purchased motor fuel for our Jet-Pep Assets from Circle K at Circle K’s cost plus terminal and administration fees of $0.015 per gallon. Circle K’s cost to supply these sites included price fluctuations associated with index-based motor fuel pricing for pipeline delivery and the generation and sale of RINs. Effective November 1, 2018, we amended our contract with Circle K such that our cost is based on a rack-based price, which reduces our exposure to price fluctuations inherent in the previous pricing methodology. We completed the upgrades of dispensers and the rebranding of substantially all these sites to a major fuel supplier in the third quarter of 2019 and anticipate continuing to see a positive impact on volume and fuel margin.

Competition

Our Wholesale segment competes with other motor fuel distributors. Major competitive factors for us include, among others, customer service, price and quality of service and availability of products.

The convenience store industry is highly competitive and characterized by ease of entry and constant change in the number and type of retailers offering products and services of the type we sold in our retail sites. We compete with other retail site chains, independently owned retail sites, motor fuel stations, supermarkets, drugstores, discount stores, dollar stores, club stores and hypermarkets. Major competitive factors include, among others, location, ease of access, product and service selection, motor fuel brands, pricing, customer service, store appearance, and cleanliness.

Seasonality

Our business exhibits substantial seasonality due to our wholesale and retail sites being located in certain geographic areas that are affected by seasonal weather and temperature trends and associated changes in retail customer activity during different seasons. Historically, sales volumes have been highest in the second and third quarters (during the summer activity months) and lowest during the winter months in the first and fourth quarters.

Trade Names, Service Marks and Trademarks

We are a wholesale distributor of motor fuel for various major integrated oil companies and are licensed to market/resell motor fuel under their respective motor fuel brands.

We are not aware of any facts that would negatively affect our continuing use of any trademarks, trade names or service marks.

12

Environmental Laws and Regulations

We are subject to extensive federal, state and local environmental laws and regulations, including those relating to USTs, the release or discharge of materials into the air, water and soil, waste management, pollution prevention measures, storage, handling, use and disposal of hazardous materials, the exposure of persons to hazardous materials, greenhouse gas emissions, and characteristics, composition, storage and sale of motor fuel and the health and safety of our employees. We incorporate by reference into this section our disclosures included in Note 2 under the captions “Environmental Matters” and “Asset Retirement Obligations” and Note 10 under the caption “Asset Retirement Obligations” to the financial statements.

Other Regulatory Matters

Our retail sites were subject to regulation by federal, state, and/or local agencies and to licensing and regulations by state and local health, sanitation, safety, fire and other departments relating to the development and operation of retail sites, including regulations relating to zoning and building requirements and the preparation and sale of food.

Our retail sites were also subject to federal, state and/or local laws governing such matters as wage rates, overtime, working conditions and citizenship requirements. At the federal, state and local levels, there are proposals under consideration from time to time to increase minimum wage rates and modify or restrict immigration policies.

Employees

The General Partner manages our operations and activities, Under the Transitional Omnibus Agreement, employees of Circle K provided management services to us through December 31, 2019. As of December 31, 2019, pursuant to the Circle K Omnibus Agreement, 104 employees of Circle K provided substantial management services to us.

On January 1, 2020, certain employees of Circle K became employees of the Topper Group, and together with existing employees of the Topper Group, have provided similar services to the Partnership under the Topper Group Omnibus Agreement.

If any of the following risks were to occur, our business, financial condition or results of operations could be materially and adversely affected. In that case, we might not be able to pay distributions on our common units, the trading price of our common units could decline and you could lose all or part of your investment. Also, please read “Cautionary Statement Regarding Forward-Looking Statements.”

Limited partner interests are inherently different from the capital stock of a corporation although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business.

Risks Relating to Our Industry and Our Business

We may not have sufficient distributable cash from operations to enable us to pay our quarterly distribution following the establishment of cash available for distribution and payment of fees and expenses.

We may not have sufficient cash each quarter to pay quarterly distribution at current levels or at all.

The amount of cash we can distribute on our common units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things:

|

|

• |

demand for motor fuel products in the markets we serve, including seasonal fluctuations, and the margin per gallon we earn selling and distributing motor fuel; |

|

|

• |

the wholesale price of motor fuel and its impact on the payment discounts we receive; |

|

|

• |

seasonal trends in the industries in which we operate; |

|

|

• |

supply, and the impact that severe storms could have to our suppliers’ and customers’ operations; |

|

|

• |

competition from other companies that sell motor fuel products or operate retail sites in our targeted market areas; |

13

|

|

• |

the inability to identify and acquire suitable sites or to negotiate acceptable leases for such sites; |

|

|

• |

the potential inability to obtain adequate financing to fund our expansion; |

|

|

• |

the level of our operating costs, including payments to the Topper Group under the Topper Group Omnibus Agreement; |

|

|

• |

prevailing economic conditions; |

|

|

• |

regulatory actions affecting the supply of or demand for motor fuel, our operations, our existing contracts or our operating costs; and |

|

|

• |

volatility of prices for motor fuel. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors such as:

|

|

• |

the level and timing of capital expenditures we make; |

|

|

• |

the restrictions contained in our credit facility; |

|

|

• |

our debt service requirements and other liabilities; |

|

|

• |

the cost of acquisitions, if any; |

|

|

• |

fluctuations in our working capital needs; |

|

|

• |

our ability to borrow under our credit facility and access capital markets on favorable terms, or at all; and |

|

|

• |

the amount, if any, of cash reserves established by our General Partner in its discretion. |

Incurring additional debt may significantly increase our interest expense and financial leverage and issuing additional limited partner interests may result in significant unitholder dilution and would increase the aggregate amount of cash required to maintain the cash distribution rate which could materially decrease our ability to pay distributions. Consequently, there is no guarantee that we will distribute quarterly cash distributions to our unitholders in any quarter.

The amount of cash we have available for distribution to unitholders depends primarily on our cash flow rather than on our profitability, which may prevent us from making cash distributions, even during periods when we record net income.

The amount of cash we have available for distribution depends primarily on our cash flow, and not solely on profitability, which will be affected by non-cash items. As a result, we may make cash distributions during periods when we record losses for financial accounting purposes and may not make cash distributions during periods when we record net income for financial accounting purposes.

If we are unable to make acquisitions on economically acceptable terms, our future growth and ability to increase distributions to unitholders will be limited.

Our strategy to grow our business and increase distributions to unitholders is dependent on our ability to make acquisitions that result in an increase in cash flow. Our growth strategy is based, in large part, on our expectation of ongoing divestitures of retail and wholesale fuel distribution assets by industry participants. We may be unable to make accretive acquisitions for any of the following reasons:

|

|

• |

we are unable to identify attractive acquisition candidates or negotiate acceptable purchase contracts for them; |

|

|

• |

we are unable to raise financing for such acquisitions on economically acceptable terms, for example, if the market price for our common units declines; |

|

|

• |

we are outbid by competitors; or |

|

|

• |

we or the seller are unable to obtain any necessary consents. |

If we are unable to make acquisitions on economically acceptable terms, our future growth and ability to increase distributions to unitholders will be limited. In addition, if we consummate any future acquisitions, our capitalization and results of operations may change significantly. We may also consummate acquisitions, which at the time of consummation we believe will be accretive, but ultimately may not be accretive and may in fact result in a decrease in distributable cash flow per unit as a result of incorrect assumptions in our evaluation of such acquisitions, unforeseen consequences, or other external events beyond our control. If any of these events occurred, our future growth could be adversely affected.

14

Any acquisitions are subject to substantial risks that could adversely affect our business, financial condition and results of operations and reduce our ability to make distributions to unitholders.

Any acquisitions involve potential risks, including, among other things:

|

|

• |

the validity of our assumptions about revenues, demand, capital expenditures and operating costs of the acquired business or assets, as well as assumptions about achieving synergies with our existing business; |

|

|

• |

the incurrence of substantial unforeseen environmental and other liabilities arising out of the acquired businesses or assets, including liabilities arising from the operation of the acquired businesses or assets prior to our acquisition, for which we are not indemnified or for which the indemnity is inadequate; |

|

|

• |

the costs associated with additional debt or equity capital, which may result in a significant increase in our interest expense and financial leverage resulting from any additional debt incurred to finance the acquisition, or the issuance of additional common units on which we will make distributions, either of which could offset the expected accretion to our unitholders from any such acquisition and could be exacerbated by volatility in the equity or debt capital markets; |

|

|

• |

a failure to realize anticipated benefits, such as increased available distributable cash flow, an enhanced competitive position or new customer relationships; |

|

|

• |

the inability to timely and effectively integrate the operations of recently acquired businesses or assets, particularly those in new geographic areas or in new lines of business; |

|

|

• |

unforeseen difficulties operating in new and existing product areas or new and existing geographic areas; |

|

|

• |

a decrease in our liquidity by using a significant portion of our available cash or borrowing capacity to finance the acquisition; |

|

|

• |

the incurrence of other significant charges, such as impairment of goodwill or other intangible assets, asset devaluation or restructuring charges; |

|

|

• |

performance from the acquired assets and businesses that is below the forecasts we used in evaluating the acquisition; |

|

|

• |

a significant increase in our working capital requirements; |

|

|

• |

competition in our targeted market areas; |

|

|

• |

customer or key employee loss from the acquired businesses and the inability to hire, train or retain qualified personnel to manage and operate such acquired businesses; and |

|

|

• |

diversion of our management’s attention from other business concerns. |

In addition, our ability to purchase or lease additional sites involves certain potential risks, including the inability to identify and acquire suitable sites or to negotiate acceptable leases or subleases for such sites and difficulties in adapting our distribution and other operational and management systems to an expanded network of sites.

Our reviews of businesses or assets proposed to be acquired are inherently imperfect because it generally is not practicable to perform a perfect review of businesses and assets involved in each acquisition. Even a detailed review of assets and businesses may not necessarily reveal existing or potential problems, nor will it permit a buyer to become sufficiently familiar with the assets or businesses to fully assess their deficiencies and potential. For example, inspections may not always be performed on every asset, and environmental problems, such as groundwater contamination, are not necessarily observable even when an inspection is undertaken. Unitholders will not have the opportunity to evaluate the economic, financial and other relevant information that we will consider in determining the application of our funds and other resources toward the acquisition of certain businesses or assets.

15

Volatility in crude oil and wholesale motor fuel costs affect our business, financial condition and results of operations and our ability to make distributions to unitholders.

For 2019, motor fuel revenues accounted for 93% of our total revenues and motor fuel gross profit accounted for 50% of total gross profit. Wholesale motor fuel costs are directly related to, and fluctuate with, the price of crude oil. Volatility in the price of crude oil, and subsequently wholesale motor fuel prices, is caused by many factors, including general political, regulatory and economic conditions, acts of war, terrorism or armed conflict, instability in oil producing regions, particularly in the Middle East and South America, and the value of U.S. dollars relative to other foreign currencies, particularly those of oil producing nations. In addition, the supply of motor fuel and our wholesale purchase costs could be adversely affected in the event of a shortage or oversupply of product, which could result from, among other things, interruptions of fuel production at oil refineries, new supply sources, sustained increases or decreases in global demand or the fact that our motor fuel contracts do not guarantee an uninterrupted, unlimited supply of motor fuel.

Significant increases and volatility in wholesale motor fuel costs could result in lower gross profit dollars, as an increase in the retail price of motor fuel could impact consumer demand for motor fuel and convenience merchandise and could result in lower wholesale motor fuel gross profit dollars. Dramatic increases in oil prices reduce retail motor fuel gross profits because wholesale motor fuel costs typically increase faster than retailers are able to pass them along to customers. In addition, significant decreases in oil prices and the corresponding decreases in wholesale motor fuel sales prices can result in lower revenues and gross profit margins, as our wholesale motor fuel gross profits include discounts from our suppliers calculated as a percentage of the cost of wholesale motor fuel. As the market prices of crude oil, and, correspondingly, the market prices of wholesale motor fuel, experience significant and rapid fluctuations, we attempt to pass along wholesale motor fuel price changes to our customers through retail price changes; however, we are not always able to do so immediately. The timing of any related increase or decrease in sales prices is affected by competitive conditions in each geographic market in which we operate. As such, our revenues and gross profit for motor fuel can increase or decrease significantly and rapidly over short periods of time and potentially adversely impact our business, financial condition, results of operations and ability to make distributions to our unitholders. The volatility in crude oil and wholesale motor fuel costs and sales prices makes it extremely difficult to forecast future motor fuel gross profits or predict the effect that future wholesale costs and sales price fluctuations will have on our operating results and financial condition.

Seasonality in wholesale motor fuel costs and sales, as well as merchandise sales, affect our business, financial condition and results of operations and our ability to make distributions to unitholders.

Oil prices, wholesale motor fuel costs, motor fuel sales volumes, motor fuel gross profits and merchandise sales often experience seasonal fluctuations. For example, consumer demand for motor fuel typically increases during the summer driving season and typically falls during the winter months. Travel, recreation and construction are typically higher in these months in the geographic areas in which we operate, increasing the demand for motor fuel and merchandise that we sell. Therefore, our revenues are typically higher in the second and third quarters of our fiscal year. A significant change in any of these factors, including a significant decrease in consumer demand (other than typical seasonal variations), could materially affect our motor fuel and merchandise volumes, motor fuel gross profit and overall customer traffic, which in turn could have a material adverse effect on our business, financial condition, results of operations and cash available for distribution to our unitholders.

The failure to complete our acquisition of certain retail and wholesale assets from the Topper Group and certain other parties in a timely manner or at all could negatively impact the trading price of our common units and have an adverse effect on our business, financial condition, results of operations and cash available for distribution to our unitholders.

In January 2020, in connection with the Partnership’s strategic decision to reestablish retail capability, the Partnership entered into an asset purchase agreement with the Topper Group and certain other parties to acquire certain retail and wholesale assets (the “Retail Acquisition”). The Retail Acquisition is expected to close prior to the end of the second quarter of 2020 and is subject to customary closing conditions.

Although reestablishing a retail capability is expected to provide us with the strategic flexibility to maximize the value of all of our assets and pursue a greater variety of acquisitions, there can be no assurance that we will realize the expected benefits or strategic objectives of the Retail Acquisition, even if the Retail Acquisition is consummated as planned.

A failure to complete the Retail Acquisition may result in negative publicity, negative impressions of us in the financial markets and investment community and negative responses from customers, partners and other third parties. There can be no assurance that our business, financial condition, results of operations and cash available for distribution to our unitholders will not be adversely affected, as compared to our condition prior to the announcement of the Retail Acquisition, if the Retail Acquisition is not consummated.

16

Both the wholesale motor fuel distribution and the retail motor fuel industries are characterized by intense competition and fragmentation, and our failure to effectively compete could adversely affect our business, financial condition and results of operations and reduce our ability to make distributions to unitholders.

The markets for distribution of wholesale motor fuel and the sale of retail motor fuel are highly competitive and fragmented, which results in narrow margins. We have numerous competitors, and some may have significantly greater resources and name recognition than we do. We rely on our ability to provide value added reliable services and to control our operating costs to maintain our margins and competitive position. If we were to fail to maintain the quality of our services, any or all of our wholesale customers could choose alternative distribution sources and expected retail customers could purchase from other retailers, each decreasing our margins. Furthermore, there can be no assurance that major integrated oil companies will not decide to distribute their own products in direct competition with us or that large wholesale customers will not attempt to buy directly from the major integrated oil companies. The occurrence of any of these events could have a material adverse effect on our business, results of operations and our ability to make distributions to our unitholders.

Changes in credit or debit card expenses could reduce our gross profit, especially on motor fuel sold at company-operated retail sites.

We expect a significant portion of sales at our company-operated retail sites will involve payment using credit or debit cards. We expect to be assessed fees as a percentage of transaction amounts and not as a fixed dollar amount or percentage of our gross profits. Higher motor fuel prices result in higher credit and debit card expenses, and an increase in credit or debit card use or an increase in fees would have a similar effect. Therefore, credit and debit card fees charged on motor fuel purchases that are more expensive as a result of higher motor fuel prices are not necessarily accompanied by higher gross profits. In fact, such fees may cause lower gross profits. Lower gross profits on motor fuel sales caused by higher fees may decrease our overall gross profit and could have a material adverse effect on our business, financial condition, results of operations and cash available for distribution to our unitholders.

New entrants or increased competition in the convenience store industry could result in reduced gross profits.

Upon consummation of the Retail Acquisition, we expect to compete with numerous other convenience store chains, independent convenience stores, supermarkets, drugstores, discount warehouse clubs, motor fuel service stations, mass merchants, fast food operations and other similar retail outlets. Several non-traditional retailers, including supermarkets and club stores, compete directly with convenience stores.

General economic, financial and political conditions that are largely out of our control could adversely affect our business, financial condition and results of operations and reduce our ability to make distributions to unitholders.

Recessionary economic conditions, higher interest rates, higher motor fuel and other energy costs, inflation, increases in commodity prices, higher levels of unemployment, higher consumer debt levels, higher tax rates and other changes in tax laws or other economic factors may affect consumer spending or buying habits, and could adversely affect the demand for motor fuel and convenience items we will sell at our retail sites. Unfavorable economic conditions, higher motor fuel prices and unemployment levels can affect consumer confidence, spending patterns and miles driven, with many customers “trading down” to lower priced products in certain categories when unfavorable conditions exist. These factors can lead to sales declines in both motor fuel and general merchandise, and in turn have an adverse impact on our business, financial condition and results of operations.

A tightening of credit in the financial markets or an increase in interest rates may make it more difficult for wholesale customers and suppliers to obtain financing and, depending on the degree to which it occurs, there may be a material increase in the nonpayment or other nonperformance by our customers and suppliers. Even if our credit review and analysis mechanisms work properly, we may experience financial losses in our dealings with these third parties. A material increase in the nonpayment or other nonperformance by our wholesale customers and/or suppliers could adversely affect our business, financial condition, results of operations and cash available for distribution to our unitholders.

Examples of other general economic, financial and political conditions could include:

|

|

• |

a general or prolonged decline in, or shocks to, regional or broader macro-economics; |

|

|

• |

regulatory changes that could impact the markets in which we operate, such as immigration or trade reform laws or regulations prohibiting or limiting hydraulic fracturing, which could reduce demand for our goods and services or lead to pricing, currency, or other pressures; and |

|

|

• |

deflationary economic pressures, which could hinder our ability to operate profitably in view of the challenges inherent in making corresponding deflationary adjustments to our cost structure. |

17

The nature of these types of risks, which are often unpredictable, makes them difficult to plan for, or otherwise mitigate, and they are generally uninsurable, which compounds their potential impact on our business.

Terrorist attacks and threatened or actual war or armed conflict may adversely affect our business.

Our business is affected by general economic conditions and fluctuations in consumer confidence and spending, which can decline as a result of numerous factors outside of our control. Terrorist attacks or threats, whether within the United States or abroad, rumors or threats of war, actual conflicts involving the United States or its allies, or military or trade disruptions impacting our suppliers or our customers may adversely impact our operations. Specifically, strategic targets such as energy related assets may be at greater risk of future terrorist attacks than other targets in the United States. These occurrences could have an adverse impact on energy prices, including prices for motor fuels, and an adverse impact on our operations. Any or a combination of these occurrences could have a material adverse effect on our business, financial condition, results of operations and cash available for distribution to our unitholders.

Changes in consumer behavior and travel as a result of changing economic conditions, labor strikes or otherwise could adversely affect our business, financial condition and results of operations and reduce our ability to make distributions to unitholders.

In the retail motor fuel industry, customer traffic is generally driven by consumer preferences and spending trends, growth rates for commercial truck traffic and trends in travel and weather. Changes in economic conditions generally, or in the regions in which we operate, could adversely affect consumer spending patterns and travel in our markets. In particular, weakening economic conditions may result in decreases in miles driven and discretionary consumer spending and travel, which affect spending on motor fuel and convenience items. In addition, changes in the types of products and services demanded by consumers or labor strikes in the construction industry or other industries that employ customers who visit retail sites, may adversely affect our sales and gross profit. Additionally, negative publicity or perception surrounding motor fuel suppliers could adversely affect reputation and brand image, which may negatively affect our motor fuel sales and gross profit. Similarly, advanced technology and increased use of hybrid cars or cars using alternative fuels would reduce demand for motor fuel. Our success depends on our ability to anticipate and respond in a timely manner to changing consumer demands and preferences while continuing to sell products and services that remain relevant to the consumer and thus generally have a positive impact overall merchandise gross profit.

We will be subject to extensive government laws and regulations concerning store merchandise items and operations upon consummation of the Retail Acquisition, and the cost of compliance with such laws and regulations can be material.