Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 JUNE 2018 - NEW JERSEY RESOURCES CORP | njrex322jun2018.htm |

| EX-32.1 - EXHIBIT 32.1 JUNE 2018 - NEW JERSEY RESOURCES CORP | njrex321jun2018.htm |

| EX-31.2 - EXHIBIT 31.2 JUNE 2018 - NEW JERSEY RESOURCES CORP | njrex312jun2018.htm |

| EX-31.1 - EXHIBIT 31.1 JUNE 2018 - NEW JERSEY RESOURCES CORP | njrex311jun2018.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10‑Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2018

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO | ||

Commission file number 001‑08359 | ||

NEW JERSEY RESOURCES CORPORATION | ||

(Exact name of registrant as specified in its charter) | ||

New Jersey | 22‑2376465 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

1415 Wyckoff Road, Wall, New Jersey 07719 | 732‑938‑1480 | |

(Address of principal executive offices) | (Registrant's telephone number, including area code) | |

Securities registered pursuant to Section 12 (b) of the Act: | ||

Common Stock ‑ $2.50 Par Value | New York Stock Exchange | |

(Title of each class) | (Name of each exchange on which registered) | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes: x No: o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes: x No: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

Large accelerated filer: x | Accelerated filer: o | |

Non-accelerated filer: o | (Do not check if a smaller reporting company) | |

Smaller reporting company: o | ||

Emerging growth company: o | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes: o No: x

The number of shares outstanding of $2.50 par value Common Stock as of August 3, 2018 was 88,276,811.

New Jersey Resources Corporation

TABLE OF CONTENTS

Page | |||

PART I. FINANCIAL INFORMATION | |||

ITEM 1. | |||

ITEM 2. | |||

ITEM 3. | |||

ITEM 4. | |||

PART II. OTHER INFORMATION | |||

ITEM 1. | |||

ITEM 1A. | |||

ITEM 2. | |||

ITEM 6. | |||

New Jersey Resources Corporation

GLOSSARY OF KEY TERMS

Adelphia | Adelphia Gateway, LLC |

AFUDC | Allowance for Funds Used During Construction |

AOCI | Accumulated Other Comprehensive Income |

ASC | Accounting Standards Codification |

ASU | Accounting Standards Update |

Bcf | Billion Cubic Feet |

BGSS | Basic Gas Supply Service |

BPU | New Jersey Board of Public Utilities |

CIP | Conservation Incentive Program |

CME | Chicago Mercantile Exchange |

CR&R | Commercial Realty & Resources Corp. |

DM | Dominion Energy Midstream Partners, L.P., a master limited partnership |

DM Common Units | Common units representing limited partnership interests in DM |

DRP | NJR Direct Stock Purchase and Dividend Reinvestment Plan |

Dths | Dekatherms |

EE | Energy Efficiency |

FASB | Financial Accounting Standards Board |

FCM | Futures Commission Merchant |

FERC | Federal Energy Regulatory Commission |

Financial margin | A non-GAAP financial measure, which represents revenues earned from the sale of natural gas less costs of natural gas sold including any transportation and storage costs, and excludes any accounting impact from the change in the fair value of certain derivative instruments |

FMB | First Mortgage Bond |

GAAP | Generally Accepted Accounting Principles of the United States |

Home Services and Other | Home Services and Other Operations |

ICE | Intercontinental Exchange |

IEC | Interstate Energy Company, LLC |

Iroquois | Iroquois Gas Transmission L.P. |

ISDA | The International Swaps and Derivatives Association |

ITC | Federal Investment Tax Credit |

MGP | Manufactured Gas Plant |

MLP | Master Limited Partnership |

Moody's | Moody's Investors Service, Inc. |

Mortgage Indenture | The Amended and Restated Indenture of Mortgage, Deed of Trust and Security Agreement between NJNG and U.S. Bank National Association dated as of September 1, 2014 |

MW | Megawatts |

MWh | Megawatt Hour |

NAESB | The North American Energy Standards Board |

NFE | Net Financial Earnings |

NJ RISE | New Jersey Reinvestment in System Enhancement |

NJCEP | New Jersey's Clean Energy Program |

NJDEP | New Jersey Department of Environmental Protection |

NJNG | New Jersey Natural Gas Company |

NJNG Credit Facility | NJNG's $250 million unsecured committed credit facility expiring in May 2019 |

NJR Credit Facility | NJR's $425 million unsecured committed credit facility expiring in September 2020 |

NJR or The Company | New Jersey Resources Corporation |

1

New Jersey Resources Corporation

GLOSSARY OF KEY TERMS (cont.) | |

NJRHS | NJR Home Services Company |

Non-GAAP | Not in accordance with Generally Accepted Accounting Principles of the United States |

NPNS | Normal Purchase/Normal Sale |

NYMEX | New York Mercantile Exchange |

O&M | Operation and Maintenance |

OCI | Other Comprehensive Income |

OPEB | Other Postemployment Benefit Plans |

PennEast | PennEast Pipeline Company, LLC |

PPA | Power Purchase Agreement |

PTC | Federal Production Tax Credit |

RAC | Remediation Adjustment Clause |

REC | Renewable Energy Certificate |

S&P | Standard & Poor's Financial Services, LLC |

SAFE | Safety Acceleration and Facility Enhancement |

SAVEGREEN | The SAVEGREEN Project® |

SBC | Societal Benefits Charge |

SEC | U.S. Securities and Exchange Commission |

SREC | Solar Renewable Energy Certificate |

SRL | Southern Reliability Link |

Steckman Ridge | Collectively, Steckman Ridge GP, LLC and Steckman Ridge, LP |

Talen | Talen Energy Marketing, LLC |

Tetco | Texas Eastern Transmission |

The Exchange Act | The Securities Exchange Act of 1934, as amended |

The Tax Act | An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget for Fiscal Year 2018, previously known as The Tax Cuts and Jobs Act of 2017 |

Trustee | U.S. Bank National Association |

U.S. | The United States of America |

USF | Universal Service Fund |

2

New Jersey Resources Corporation

INFORMATION CONCERNING FORWARD-LOOKING STATEMENTS

Certain statements contained in this report, including, without limitation, statements as to management expectations, assumptions and beliefs presented in Part I, Item 2. “Management's Discussion and Analysis of Financial Condition and Results of Operations,” Part I, Item 3. “Quantitative and Qualitative Disclosures About Market Risk,” Part II, Item I. “Legal Proceedings” and in the notes to the financial statements are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. Forward-looking statements can also be identified by the use of forward-looking terminology such as “anticipate,” “estimate,” “may,” “could,” “might,” “intend,” “expect,” “believe,” “will” “plan,” or “should,” or comparable terminology and are made based upon management's current expectations, assumptions and beliefs as of this date concerning future developments and their potential effect on us. There can be no assurance that future developments will be in accordance with management's expectations, assumptions or beliefs, or that the effect of future developments on us will be those anticipated by management.

We caution readers that the expectations, assumptions and beliefs that form the basis for forward-looking statements regarding customer growth, customer usage, qualifications for ITCs, PTCs and SRECs, future rate case proceedings, financial condition, results of operations, cash flows, capital requirements, future capital expenditures, market risk, effective tax rate and other matters for fiscal 2018 and thereafter include many factors that are beyond our ability to control or estimate precisely, such as estimates of future market conditions, the behavior of other market participants and changes in the debt and equity capital markets. The factors that could cause actual results to differ materially from our expectations, assumptions and beliefs include, but are not limited to, those discussed in Item 1A. Risk Factors of our Annual Report on Form 10-K for the fiscal year ended September 30, 2017, as well as the following:

• | risks associated with our investments in clean energy projects, including the availability of regulatory and tax incentives, the availability of viable projects, our eligibility for ITCs and PTCs, the future market for SRECs and electricity prices and operational risks related to projects in service; |

• | our ability to obtain governmental and regulatory approvals, land-use rights, electric grid connection (in the case of clean energy projects) and/or financing for the construction, development and operation of our unregulated energy investments, pipeline transportation systems and NJNG and Midstream’s infrastructure projects, including SRL, NJ RISE, PennEast and Adelphia, in a timely manner; |

• | risks associated with acquisitions and the related integration of acquired assets with our current operations; |

• | volatility of natural gas and other commodity prices and their impact on NJNG customer usage, NJNG’s BGSS incentive programs, our Energy Services segment operations and on our risk management efforts; |

• | the level and rate at which NJNG’s costs and expenses are incurred and the extent to which they are approved for recovery from customers through the regulatory process, including through future base rate case filings; |

• | the impact of a disallowance of recovery of environmental-related expenditures and other regulatory changes; |

• | the performance of our subsidiaries; |

• | operating risks incidental to handling, storing, transporting and providing customers with natural gas; |

• | access to adequate supplies of natural gas and dependence on third-party storage and transportation facilities for natural gas supply; |

• | the regulatory and pricing policies of federal and state regulatory agencies; |

• | timing of qualifying for ITCs due to delays or failures to complete planned solar projects and the resulting effect on our effective tax rate and earnings; |

• | the results of legal or administrative proceedings with respect to claims, rates, environmental issues, gas cost prudence reviews and other matters; |

• | risks related to cyberattacks or failure of information technology systems; |

• | changes in rating agency requirements and/or credit ratings and their effect on availability and cost of capital to our Company; |

• | our ability to comply with current and future regulatory requirements; |

• | the impact of volatility in the equity and credit markets on our access to capital; |

• | the impact to the asset values and resulting higher costs and funding obligations of our pension and postemployment benefit plans as a result of potential downturns in the financial markets, lower discount rates, revised actuarial assumptions or impacts associated with the Patient Protection and Affordable Care Act; |

• | commercial and wholesale credit risks, including the availability of creditworthy customers and counterparties, and liquidity in the wholesale energy trading market; |

• | accounting effects and other risks associated with hedging activities and use of derivatives contracts; |

• | our ability to optimize our physical assets; |

• | any potential need to record a valuation allowance for our deferred tax assets; |

• | changes to tax laws and regulations; |

• | weather and economic conditions; |

• | our ability to comply with debt covenants; |

• | demographic changes in our service territory and their effect on our customer growth; |

• | the impact of natural disasters, terrorist activities and other extreme events on our operations and customers; |

• | the costs of compliance with present and future environmental laws, including potential climate change-related legislation; |

• | environmental-related and other uncertainties related to litigation or administrative proceedings; |

• | risks related to our employee workforce; and |

• | risks associated with the management of our joint ventures and partnerships, and investment in a master limited partnership. |

While we periodically reassess material trends and uncertainties affecting our results of operations and financial condition in connection with the preparation of management's discussion and analysis of results of operations and financial condition contained in our Quarterly and Annual Reports on Form 10-Q and Form 10-K, respectively, we do not, by including this statement, assume any obligation to review or revise any particular forward-looking statement referenced herein in light of future events.

3

New Jersey Resources Corporation

Part I

ITEM 1. FINANCIAL STATEMENTS

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

Three Months Ended | Nine Months Ended | |||||||||||||

June 30, | June 30, | |||||||||||||

(Thousands, except per share data) | 2018 | 2017 | 2018 | 2017 | ||||||||||

OPERATING REVENUES | ||||||||||||||

Utility | $ | 104,538 | $ | 121,362 | $ | 631,389 | $ | 602,464 | ||||||

Nonutility | 438,897 | 336,161 | 1,636,394 | 1,129,633 | ||||||||||

Total operating revenues | 543,435 | 457,523 | 2,267,783 | 1,732,097 | ||||||||||

OPERATING EXPENSES | ||||||||||||||

Gas purchases: | ||||||||||||||

Utility | 53,080 | 47,124 | 227,268 | 220,889 | ||||||||||

Nonutility | 422,734 | 299,971 | 1,489,041 | 1,005,231 | ||||||||||

Related parties | 2,156 | 2,076 | 6,392 | 6,259 | ||||||||||

Operation and maintenance | 69,447 | 55,613 | 182,307 | 160,183 | ||||||||||

Regulatory rider expenses | 5,542 | 5,216 | 36,915 | 37,710 | ||||||||||

Depreciation and amortization | 20,320 | 20,760 | 64,634 | 60,348 | ||||||||||

Energy and other taxes | 7,822 | 8,796 | 45,855 | 42,382 | ||||||||||

Total operating expenses | 581,101 | 439,556 | 2,052,412 | 1,533,002 | ||||||||||

OPERATING (LOSS) INCOME | (37,666 | ) | 17,967 | 215,371 | 199,095 | |||||||||

Other income, net | 2,682 | 3,273 | 11,589 | 12,387 | ||||||||||

Interest expense, net of capitalized interest | 11,037 | 11,164 | 34,740 | 33,215 | ||||||||||

(LOSS) INCOME BEFORE INCOME TAXES AND EQUITY IN EARNINGS OF AFFILIATES | (46,021 | ) | 10,076 | 192,220 | 178,267 | |||||||||

Income tax (benefit) provision | (28,534 | ) | (5,816 | ) | (47,801 | ) | 20,134 | |||||||

Equity in earnings of affiliates | 3,213 | 3,065 | 9,670 | 10,455 | ||||||||||

NET (LOSS) INCOME | $ | (14,274 | ) | $ | 18,957 | $ | 249,691 | $ | 168,588 | |||||

(LOSS) EARNINGS PER COMMON SHARE | ||||||||||||||

Basic | $(0.16) | $0.22 | $2.85 | $1.95 | ||||||||||

Diluted | $(0.16) | $0.22 | $2.84 | $1.94 | ||||||||||

DIVIDENDS DECLARED PER COMMON SHARE | $0.2725 | $0.255 | $0.818 | $0.765 | ||||||||||

WEIGHTED AVERAGE SHARES OUTSTANDING | ||||||||||||||

Basic | 87,888 | 86,408 | 87,493 | 86,257 | ||||||||||

Diluted | 87,888 | 87,267 | 87,884 | 87,088 | ||||||||||

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Unaudited)

Three Months Ended | Nine Months Ended | ||||||||||||

June 30, | June 30, | ||||||||||||

(Thousands) | 2018 | 2017 | 2018 | 2017 | |||||||||

Net (loss) income | $ | (14,274 | ) | $ | 18,957 | $ | 249,691 | $ | 168,588 | ||||

Other comprehensive (loss) income, net of tax | |||||||||||||

Unrealized (loss) gain on available for sale securities, net of tax of $854, $2,375, $9,071 and $(2,801), respectively | (2,364 | ) | (3,622 | ) | (25,055 | ) | 3,301 | ||||||

Reclassifications of losses to net income on available for sale securities, net of tax of $0, $0, $(858) and $0, respectively | — | — | 11,647 | — | |||||||||

Adjustment to postemployment benefit obligation, net of tax of $(104), $(217), $(344) and $(651), respectively | 272 | 318 | 784 | 953 | |||||||||

Other comprehensive (loss) income | $ | (2,092 | ) | $ | (3,304 | ) | $ | (12,624 | ) | $ | 4,254 | ||

Comprehensive (loss) income | $ | (16,366 | ) | $ | 15,653 | $ | 237,067 | $ | 172,842 | ||||

See Notes to Unaudited Condensed Consolidated Financial Statements

4

New Jersey Resources Corporation

Part I

ITEM 1. FINANCIAL STATEMENTS (Continued)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

Nine Months Ended | |||||||

June 30, | |||||||

(Thousands) | 2018 | 2017 | |||||

CASH FLOWS FROM OPERATING ACTIVITIES | |||||||

Net income | $ | 249,691 | $ | 168,588 | |||

Adjustments to reconcile net income to cash flows from operating activities | |||||||

Unrealized loss (gain) on derivative instruments | 25,904 | (42,534 | ) | ||||

Gain on sale of available for sale securities | (5,332 | ) | (7,287 | ) | |||

Gain on sale of businesses | (4,687 | ) | — | ||||

Depreciation and amortization | 64,634 | 60,348 | |||||

Amortization of acquired wholesale energy contracts | 17,813 | — | |||||

Allowance for equity used during construction | (3,730 | ) | (2,738 | ) | |||

Allowance for doubtful accounts | 1,672 | 916 | |||||

Deferred income taxes | 17,351 | 48,024 | |||||

Deferred income tax benefit due to tax legislation | (73,784 | ) | — | ||||

Manufactured gas plant remediation costs | (13,624 | ) | (6,923 | ) | |||

Equity in earnings, net of distributions received from equity investees | (935 | ) | (334 | ) | |||

Cost of removal - asset retirement obligations | (93 | ) | (363 | ) | |||

Contributions to postemployment benefit plans | (4,708 | ) | (4,640 | ) | |||

Tax benefit from stock-based compensation | 2,841 | 1,284 | |||||

Changes in: | |||||||

Components of working capital | 64,527 | (26,843 | ) | ||||

Other noncurrent assets | 41,793 | 27,930 | |||||

Other noncurrent liabilities | 13,224 | 7,668 | |||||

Cash flows from operating activities | 392,557 | 223,096 | |||||

CASH FLOWS USED IN INVESTING ACTIVITIES | |||||||

Expenditures for: | |||||||

Utility plant | (130,727 | ) | (92,833 | ) | |||

Solar and wind equipment | (88,416 | ) | (121,958 | ) | |||

Midstream and other | (4,879 | ) | (933 | ) | |||

Cost of removal | (42,683 | ) | (23,001 | ) | |||

Investments in equity investees | (14,496 | ) | (24,097 | ) | |||

Distribution from equity investees in excess of equity in earnings | 2,515 | 2,179 | |||||

Cash paid related to acquisition | (10,000 | ) | — | ||||

(Deposits to) withdrawal from restricted cash construction fund | (52 | ) | 1,302 | ||||

Proceeds from sale of property, net of closing costs | — | 9,443 | |||||

Proceeds from sale of businesses, net of closing costs | 27,916 | — | |||||

Proceeds from sale of available for sale securities, net | 6,616 | 6,639 | |||||

Cash flows used in investing activities | (254,206 | ) | (243,259 | ) | |||

CASH FLOWS (USED IN) FROM FINANCING ACTIVITIES | |||||||

Proceeds from long-term debt | 225,000 | — | |||||

Payments of long-term debt | (133,717 | ) | (43,454 | ) | |||

(Payments of) proceeds from short-term debt, net | (208,900 | ) | 141,700 | ||||

Proceeds from sale-leaseback transaction | 7,820 | 9,587 | |||||

Payments of common stock dividends | (71,334 | ) | (65,909 | ) | |||

Proceeds from waiver discount issuance of common stock | 41,677 | — | |||||

Proceeds from issuance of common stock | 13,572 | 13,802 | |||||

Purchases of treasury stock | — | (6,355 | ) | ||||

Tax withholding payments related to net settled stock compensation | (13,625 | ) | (4,595 | ) | |||

Cash flows (used in) from financing activities | (139,507 | ) | 44,776 | ||||

Change in cash and cash equivalents | (1,156 | ) | 24,613 | ||||

Cash and cash equivalents at beginning of period | 2,226 | 37,546 | |||||

Cash and cash equivalents at end of period | $ | 1,070 | $ | 62,159 | |||

CHANGES IN COMPONENTS OF WORKING CAPITAL | |||||||

Receivables | $ | (5,757 | ) | $ | (26,487 | ) | |

Inventories | 63,838 | 4,003 | |||||

Recovery of gas costs | 28,524 | (4,610 | ) | ||||

Gas purchases payable | 28,041 | 11,929 | |||||

Prepaid and accrued taxes | (22,993 | ) | (22,820 | ) | |||

Accounts payable and other | 5,213 | (3,973 | ) | ||||

Restricted broker margin accounts | (29,497 | ) | 27,314 | ||||

Customers' credit balances and deposits | (745 | ) | (12,873 | ) | |||

Other current assets | (2,097 | ) | 674 | ||||

Total | $ | 64,527 | $ | (26,843 | ) | ||

SUPPLEMENTAL DISCLOSURES OF CASH FLOWS INFORMATION | |||||||

Cash paid (received) for: | |||||||

Interest (net of amounts capitalized) | $ | 35,295 | $ | 30,128 | |||

Income taxes | $ | 4,195 | $ | (4,178 | ) | ||

Accrued capital expenditures | $ | 30,019 | $ | 32,826 | |||

Inception gain on natural gas swap contract recognized as non-cash proceeds from sale of business | $ | 14,579 | $ | — | |||

See Notes to Unaudited Condensed Consolidated Financial Statements

5

New Jersey Resources Corporation

Part I

ITEM 1. FINANCIAL STATEMENTS (Continued)

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

ASSETS

(Thousands) | June 30, 2018 | September 30, 2017 | ||||

PROPERTY, PLANT AND EQUIPMENT | ||||||

Utility plant, at cost | $ | 2,318,091 | $ | 2,241,324 | ||

Construction work in progress | 175,882 | 119,318 | ||||

Solar and wind equipment, real estate properties and other, at cost | 665,194 | 843,142 | ||||

Construction work in progress | 39,890 | 7,286 | ||||

Total property, plant and equipment | 3,199,057 | 3,211,070 | ||||

Accumulated depreciation and amortization, utility plant | (510,242 | ) | (489,122 | ) | ||

Accumulated depreciation and amortization, solar and wind equipment, real estate properties and other | (115,412 | ) | (112,207 | ) | ||

Property, plant and equipment, net | 2,573,403 | 2,609,741 | ||||

CURRENT ASSETS | ||||||

Cash and cash equivalents | 1,070 | 2,226 | ||||

Customer accounts receivable | ||||||

Billed | 201,104 | 196,467 | ||||

Unbilled revenues | 7,099 | 7,202 | ||||

Allowance for doubtful accounts | (5,630 | ) | (5,181 | ) | ||

Regulatory assets | 21,456 | 50,791 | ||||

Gas in storage, at average cost | 136,284 | 202,063 | ||||

Materials and supplies, at average cost | 13,885 | 11,944 | ||||

Prepaid and accrued taxes | 47,017 | 24,764 | ||||

Derivatives, at fair value | 23,192 | 30,081 | ||||

Restricted broker margin accounts | 53,141 | 25,827 | ||||

Assets held for sale | 206,898 | — | ||||

Other | 31,377 | 33,260 | ||||

Total current assets | 736,893 | 579,444 | ||||

NONCURRENT ASSETS | ||||||

Investments in equity method investees | 187,808 | 172,585 | ||||

Regulatory assets | 348,079 | 375,919 | ||||

Derivatives, at fair value | 11,886 | 9,164 | ||||

Available for sale securities | 25,009 | 65,752 | ||||

Intangible assets, net | 23,610 | 41,084 | ||||

Other noncurrent assets | 70,700 | 74,818 | ||||

Total noncurrent assets | 667,092 | 739,322 | ||||

Total assets | $ | 3,977,388 | $ | 3,928,507 | ||

See Notes to Unaudited Condensed Consolidated Financial Statements

6

New Jersey Resources Corporation

Part I

ITEM 1. FINANCIAL STATEMENTS (Continued)

CAPITALIZATION AND LIABILITIES

(Thousands, except share data) | June 30, 2018 | September 30, 2017 | ||||

CAPITALIZATION | ||||||

Common stock, $2.50 par value; authorized 150,000,000 shares; outstanding June 30, 2018 — 88,211,744; September 30, 2017 — 86,555,507 | $ | 226,189 | $ | 222,258 | ||

Premium on common stock | 274,138 | 219,696 | ||||

Accumulated other comprehensive loss, net of tax | (15,880 | ) | (3,256 | ) | ||

Treasury stock at cost and other; shares June 30, 2018 — 2,263,550; September 30, 2017 — 2,347,380 | (80,405 | ) | (70,039 | ) | ||

Retained earnings | 1,045,920 | 867,984 | ||||

Common stock equity | 1,449,962 | 1,236,643 | ||||

Long-term debt | 1,220,166 | 997,080 | ||||

Total capitalization | 2,670,128 | 2,233,723 | ||||

CURRENT LIABILITIES | ||||||

Current maturities of long-term debt | 40,527 | 165,375 | ||||

Short-term debt | 57,100 | 266,000 | ||||

Gas purchases payable | 188,158 | 160,115 | ||||

Gas purchases payable to related parties | 1,150 | 1,152 | ||||

Accounts payable and other | 97,874 | 96,878 | ||||

Dividends payable | 24,037 | 23,586 | ||||

Accrued taxes | 1,291 | 2,031 | ||||

Regulatory liabilities | 7,482 | 78 | ||||

New Jersey Clean Energy Program | 15,533 | 14,202 | ||||

Derivatives, at fair value | 43,398 | 46,544 | ||||

Liabilities held for sale | 4,182 | — | ||||

Customers' credit balances and deposits | 26,212 | 26,957 | ||||

Total current liabilities | 506,944 | 802,918 | ||||

NONCURRENT LIABILITIES | ||||||

Deferred income taxes | 244,161 | 514,708 | ||||

Deferred investment tax credits | 4,055 | 4,297 | ||||

Deferred gain | 9,300 | 27,728 | ||||

Derivatives, at fair value | 21,604 | 11,330 | ||||

Manufactured gas plant remediation | 140,821 | 149,000 | ||||

Postemployment employee benefit liability | 130,968 | 128,888 | ||||

Regulatory liabilities | 211,431 | 14,507 | ||||

Asset retirement obligation | 28,574 | 31,420 | ||||

Other | 9,402 | 9,988 | ||||

Total noncurrent liabilities | 800,316 | 891,866 | ||||

Commitments and contingent liabilities (Note 12) | ||||||

Total capitalization and liabilities | $ | 3,977,388 | $ | 3,928,507 | ||

See Notes to Unaudited Condensed Consolidated Financial Statements

7

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. NATURE OF THE BUSINESS

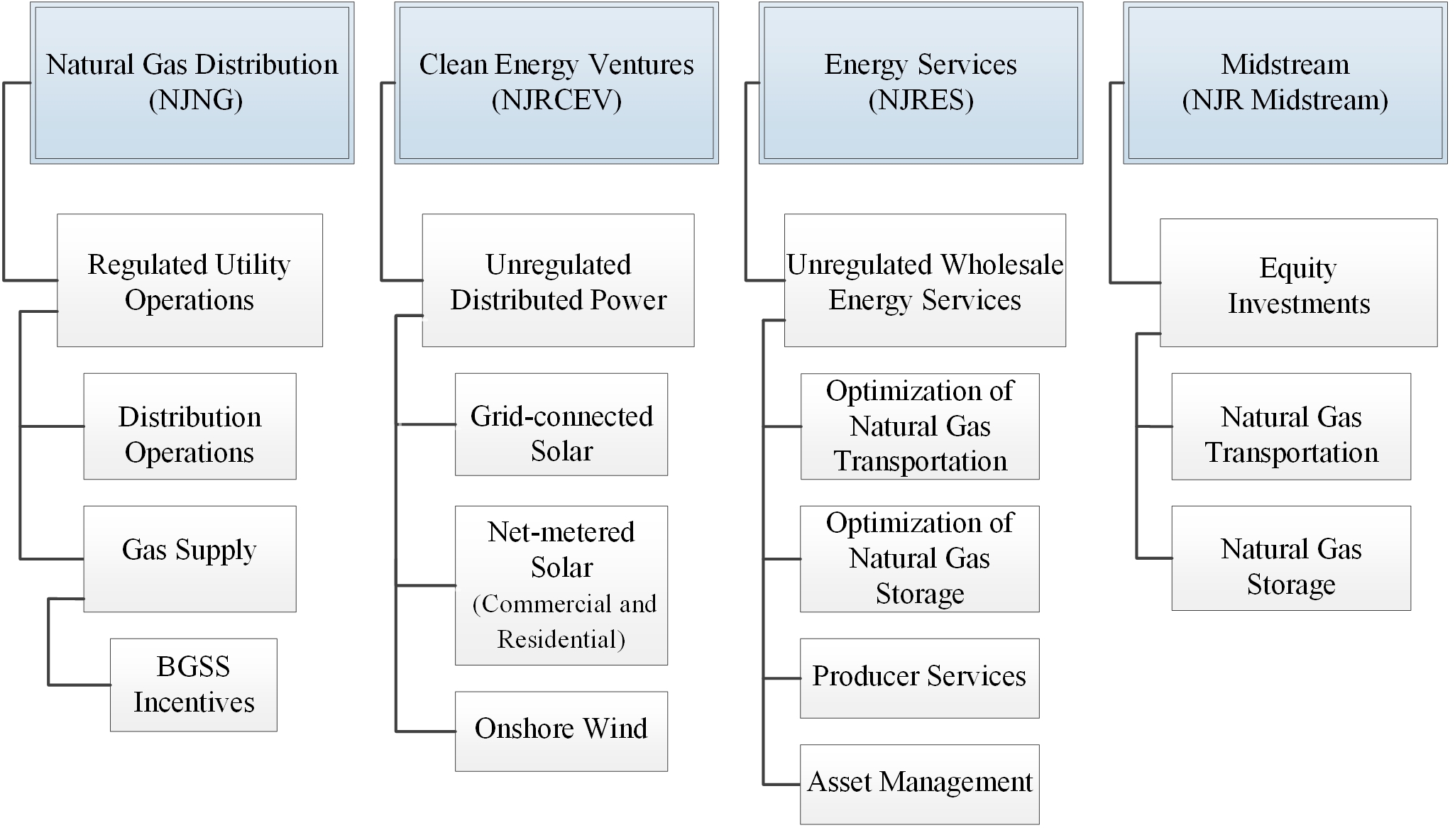

New Jersey Resources Corporation provides regulated gas distribution services and operates certain unregulated businesses primarily through the following subsidiaries:

New Jersey Natural Gas Company provides natural gas utility service to approximately 537,700 retail customers in central and northern New Jersey and is subject to rate regulation by the BPU. NJNG comprises the Natural Gas Distribution segment.

NJR Clean Energy Ventures Corporation, the Company's clean energy subsidiary, comprises the Clean Energy Ventures segment and consists of the Company's capital investments in commercial and residential solar projects located throughout New Jersey and onshore wind investments in Iowa, Kansas, Wyoming and Pennsylvania. On June 1, 2018, Clean Energy Ventures completed the sale of its membership interest in a 9.7 MW wind farm in Two Dot, Montana, see Note 16. Dispositions for more details.

NJR Energy Services Company comprises the Energy Services segment. Energy Services maintains and transacts around a portfolio of natural gas storage and transportation capacity contracts and provides physical wholesale energy and energy management services in the U.S. and Canada. From July 2017 through February 2018, NJR Retail Services Company provided retail natural gas supply and transportation services to commercial and industrial customers in Delaware, Maryland, Pennsylvania and New Jersey, as part of the Energy Services segment. NJR Retail Services was sold to an unrelated third party on February 28, 2018, see Note 16. Dispositions for more details.

NJR Midstream Holdings Corporation, which comprises the Midstream segment, invests in energy-related ventures through its subsidiaries, NJR Steckman Ridge Storage Company, which holds the Company's 50 percent combined ownership interest in Steckman Ridge, located in Pennsylvania and NJR Pipeline Company, which holds the Company's 20 percent ownership interest in PennEast. See Note 6. Investments in Equity Investees for more information.

NJR Retail Holdings Corporation has two principal subsidiaries, NJR Home Services Company, which provides heating, central air conditioning, standby generators, solar and other indoor and outdoor comfort products to residential homes throughout New Jersey, and Commercial Realty & Resources Corporation, which owns commercial real estate. NJR Home Services Company and Commercial Realty & Resources Corporation are included in Home Services and Other operations.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying Unaudited Condensed Consolidated Financial Statements have been prepared by NJR in accordance with the rules and regulations of the SEC and GAAP. The September 30, 2017 Balance Sheet data is derived from the audited financial statements of the Company. These Unaudited Condensed Consolidated Financial Statements should be read in conjunction with the consolidated financial statements and the notes thereto included in NJR's 2017 Annual Report on Form 10-K.

The Unaudited Condensed Consolidated Financial Statements include the accounts of NJR and its subsidiaries. In the opinion of management, the accompanying Unaudited Condensed Consolidated Financial Statements reflect all adjustments necessary for a fair presentation of the results of the interim periods presented. These adjustments are of a normal and recurring nature. Because of the seasonal nature of NJR's utility and wholesale energy services operations, in addition to other factors, the financial results for the interim periods presented are not indicative of the results that are to be expected for the fiscal year ending September 30, 2018. Intercompany transactions and accounts have been eliminated.

Sales Tax Accounting

Sales tax that is collected from customers is presented in both operating revenues and operating expenses on the Unaudited Condensed Consolidated Statements of Operations totaled $5.9 million and $37.8 million during the three and nine months ended June 30, 2018, respectively, and $6.6 million and $34.7 million during the three and nine months ended June 30, 2017, respectively. Effective January 1, 2017, the New Jersey sales tax rate decreased from 7 percent to 6.875 percent. Effective January 1, 2018, the New Jersey sales tax rate decreased again to 6.625 percent.

8

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Gas in Storage

The following table summarizes gas in storage, at average cost by segment as of:

June 30, 2018 | September 30, 2017 | |||||||||||

($ in thousands) | Gas in Storage | Bcf | Gas in Storage | Bcf | ||||||||

Energy Services | $ | 86,889 | 34.7 | $ | 122,884 | 53.9 | ||||||

Natural Gas Distribution | 49,395 | 13.8 | 79,179 | 21.8 | ||||||||

Total | $ | 136,284 | 48.5 | $ | 202,063 | 75.7 | ||||||

Available for Sale Securities

Available for sale securities are carried at fair value on the Unaudited Condensed Consolidated Balance Sheets. Total unrealized gains and losses associated are included as a part of accumulated other comprehensive income, a component of common stock equity. Reclassifications of realized gains or losses out of other comprehensive income into earnings are recorded in other income, net on the Unaudited Condensed Consolidated Statements of Operations based on average cost.

Management evaluates its equity securities for other-than-temporary impairment on a quarterly basis, and more frequently when economic, market or other concerns warrant such evaluation. Consideration is given to the length of time and the extent to which the fair value has been less than cost; the financial condition and near term prospects of the issuer; whether the market decline was affected by macroeconomic conditions, changes in tax laws, regulations or other governmental policies; and whether the Company has the intent to sell the security or more likely than not will be required to sell the security before the recovery of its amortized cost basis. If the decline in value of our equity securities is determined to be other-than-temporary, an impairment is recognized through earnings within other income, net on the Unaudited Condensed Consolidated Statements of Operations.

During the nine months ended June 30, 2018, NJR sold shares of its available for sale securities and received proceeds of approximately $6.6 million and recognized a pre-tax gain of $5.3 million. There were no sales of available for sale securities during the three months ended June 30, 2018. During the three and nine months ended June 30, 2017, NJR received proceeds of approximately $3.4 million and $6.6 million, and realized a pre-tax gain of $2.8 million and $5.4 million, respectively.

In September 2015, the Company exchanged its ownership interest in Iroquois for approximately 1.84 million DM Common Units. The investment in DM is included as part of the Company's equity investments in the Midstream segment. The exchange of ownership interests in Iroquois for DM was considered a contribution of real estate into another real estate venture. As a result, the Company recorded a deferred gain of $24.6 million on the Unaudited Condensed Consolidated Balance Sheets, based on the difference between the carrying amount of its investment in Iroquois and the fair value of the DM Common Units on the closing date of the transaction. The deferred gain will be recognized in other income, net on the Unaudited Condensed Consolidated Statements of Operations upon completion of the earnings process, typically through the sale of the related securities, or other earnings event.

On March 15, 2018, the FERC issued a policy revision indicating that it no longer will allow interstate natural gas and oil pipelines held by a MLP to recover an income tax allowance in cost-of-service rates. The policy revision had a material negative impact on the value of NJR's investment in DM Common Units. As a result, the Company evaluated the decrease in fair value of its available-for-sale securities and determined that the decline was other-than-temporary. Accordingly, the Company recognized an other-than-temporary impairment of $17.8 million, $14.8 million, net of tax, as of March 31, 2018.

Since the deferred gain was established based upon the difference in the fair value of the DM Common Units acquired and the carrying value of the ownership of Iroquois, concurrent with the impairment charge to earnings, the Company reduced the amount of the deferred gain for the DM Common Units. This reduction of the deferred gain of $17.8 million was also recorded in other income, net on the Unaudited Condensed Consolidated Statements of Operations.

As of June 30, 2018, the Company's available for sale securities had a fair value of $25 million and total unrealized losses were $3.2 million, $2.4 million, net of deferred income tax benefit. The remaining deferred gain associated with the Company’s investment in DM Common Units totaled $6.8 million. As of September 30, 2017, the Company's available for sale securities had a fair value of $65.8 million and total unrealized gains were $12.8 million, $7.7 million, net of deferred income tax expense.

On July 18, 2018, the FERC finalized its March 15, 2018 policy regarding the tax treatment of MLP pipelines. Natural gas pipelines within an MLP structure, where the parent is a taxable entity and consolidates the financial results of the MLP on its federal income tax return, will be allowed to include an income tax allowance in its cost-of-service rates.

9

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Customer Accounts Receivable

Customer accounts receivable include outstanding billings from the following subsidiaries as of:

(Thousands) | June 30, 2018 | September 30, 2017 | |||||||||

Energy Services | $ | 145,373 | 72 | % | $ | 150,322 | 77 | % | |||

Natural Gas Distribution (1) | 48,495 | 24 | 37,432 | 19 | |||||||

Clean Energy Ventures | 3,163 | 2 | 2,655 | 1 | |||||||

Home Services and Other Operations | 4,073 | 2 | 6,058 | 3 | |||||||

Total | $ | 201,104 | 100 | % | $ | 196,467 | 100 | % | |||

(1) | Does not include unbilled revenues of $7.1 million and $7.2 million as of June 30, 2018 and September 30, 2017, respectively. |

Loans Receivable

NJNG currently provides loans, with terms ranging from three to 10 years, to customers that elect to purchase and install certain energy efficient equipment in accordance with its BPU-approved SAVEGREEN program. The loans are recognized at net present value on the Unaudited Condensed Consolidated Balance Sheets. The Company recorded $9.9 million and $8.9 million in other current assets and $40 million and $40.4 million in other noncurrent assets as of June 30, 2018 and September 30, 2017, respectively, on the Unaudited Condensed Consolidated Balance Sheets, related to the loans.

NJNG's policy is to establish an allowance for doubtful accounts when loan balances are in arrears for more than 60 days. As of June 30, 2018 and September 30, 2017, there was no allowance for doubtful accounts established for the SAVEGREEN loans.

Assets Held for Sale

In March 2018, Clean Energy Ventures committed to a plan to sell its wind assets and expects that the sale will be completed within the next 12 months. Accordingly, the Company classified its wind assets and related liabilities as held for sale on the Unaudited Condensed Consolidated Balance Sheets, which resulted in depreciation expense on wind assets no longer being recorded. The wind assets classified as held for sale are measured at the lower of their carrying value or fair value less cost to sell. On June 1, 2018, Clean Energy Ventures completed the sale of its membership interest in a 9.7 MW wind farm in Two Dot, Montana, see Note 16. Dispositions for more details.

The major classes of assets and liabilities included within the disposal group as held for sale are as follows:

(Thousands) | March 31, 2018 | Assets Sold | Other Adjustments | June 30, 2018 | |||||||||||

Assets held for sale: | |||||||||||||||

Property, plant and equipment - wind equipment, at cost | $ | 244,972 | $ | (20,688 | ) | $ | — | $ | 224,284 | ||||||

Property, plant and equipment - accumulated depreciation, wind equipment | (21,561 | ) | 3,060 | — | (18,501 | ) | |||||||||

Prepaid and accrued taxes | 1,226 | (77 | ) | (295 | ) | 854 | |||||||||

Other noncurrent assets | 261 | — | — | 261 | |||||||||||

$ | 224,898 | $ | (17,705 | ) | $ | (295 | ) | $ | 206,898 | ||||||

Liabilities held for sale: | |||||||||||||||

Accounts payable and other | $ | — | $ | 186 | $ | — | $ | 186 | |||||||

Asset retirement obligation | 4,262 | (266 | ) | — | 3,996 | ||||||||||

$ | 4,262 | $ | (80 | ) | $ | — | $ | 4,182 | |||||||

10

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Recently Adopted Updates to the Accounting Standards Codification

Inventory

In July 2015, the FASB issued ASU No. 2015-11, an amendment to ASC 330, Inventory, which requires entities to measure most inventory “at the lower of cost or net realizable value,” thereby simplifying the current guidance under which an entity must measure inventory at the lower of cost or market. The Company adopted the new guidance in the first quarter of fiscal 2018 and applied the new provisions on a prospective basis, which did not impact its financial position, results of operations or cash flows upon adoption.

Tax

In March 2018, the FASB issued ASU No. 2018-05, an amendment to ASC 840, Income Taxes, which provides relief to entities in their calculation of the effects of the Tax Act by allowing them to record provisional amounts for certain income tax effects to address circumstances in which an entity does not have the necessary information available, prepared or analyzed to complete the accounting. These provisional amounts are subject to change as information and assumptions are updated throughout the measurement period, which may not extend beyond one year from the enactment date. The new guidance was effective immediately upon issuance and thus, the Company adopted the new guidance in the second quarter of fiscal 2018 and applied the new provision on a prospective basis.

Other Recent Updates to the Accounting Standards Codification

Revenue

In May 2014, the FASB issued ASU No. 2014-09, and added Topic 606, Revenue from Contracts with Customers, to the ASC. ASC 606 supersedes ASC 605, Revenue Recognition, as well as most industry-specific guidance, and prescribes a single, comprehensive revenue recognition model designed to improve financial reporting comparability across entities, industries, jurisdictions and capital markets. In August 2015, the FASB issued ASU No. 2015-14, which defers the implementation of the new guidance for one year. The new guidance will not be early adopted and will be effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year.

The Company concluded that its tariff based sales of natural gas will be within the scope of the new guidance. However, it does not anticipate any modification to the pattern of revenue recognition from such sales. The Company also evaluated its renewable asset PPA arrangements and does not anticipate any modification to the pattern of revenue recognition of the related electricity, capacity and REC sales. Revenues from RECs sold as part of a bundled arrangement will be recognized in the same period as the related generation, consistent with current practice.

Based on the review of customer contracts to date, the Company does not anticipate a material impact to its financial position, results of operations or cash flows upon adoption. Additionally, the Company does not expect significant changes to its business processes, systems or internal controls over financial reporting upon adoption. The Company anticipates new disclosures as a result of the implementation of ASC 606, including the disclosure of performance obligations, disaggregated revenues and contract balances, and currently expects to transition to the new guidance using the modified retrospective approach.

Financial Instruments

In January 2016, the FASB issued ASU No. 2016-01, an amendment to ASC 825, Financial Instruments, to address certain aspects of the recognition, measurement, presentation and disclosure of financial instruments. The standard affects investments in equity securities that do not result in consolidation and are not accounted for under the equity method and the presentation of certain fair value changes for financial liabilities measured at fair value. It also simplifies the impairment assessment of equity investments without a readily determinable fair value by requiring a qualitative assessment. The guidance is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year. The amendment will be applied on a modified retrospective basis. The Company evaluated the amendment and noted that, upon adoption, subsequent changes to the fair value of the Company’s available for sale securities will be recorded in the Consolidated Statement of Operations as opposed to other comprehensive income. Upon adoption, any amounts recorded in accumulated other comprehensive income related to available for sale securities will be reclassified to the opening balance of retained earnings in the year of adoption. The Company does not expect any other material impacts to its financial position, results of operations or cash flows upon adoption.

11

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

In June 2016, the FASB issued ASU No. 2016-13, an amendment to ASC 326, Financial Instruments - Credit Losses, which changes the impairment model for certain financial assets that have a contractual right to receive cash, including trade and loan receivables. The new model requires recognition based upon an estimation of expected credit losses rather than recognition of losses when it is probable that they have been incurred. An entity will apply the amendment through a cumulative-effect adjustment to retained earnings as of the beginning of the first reporting period in which the guidance is effective. The guidance is effective for the Company’s fiscal year ending September 30, 2021, and interim periods within that year, with early adoption permitted. The Company is currently evaluating the amendment to understand the impact on its financial position, results of operations and cash flows upon adoption and will apply the new guidance to its trade and loan receivables on a modified retrospective basis.

Leases

In February 2016, the FASB issued ASU No. 2016-02, an amendment to ASC 842, Leases, which provides for a comprehensive overhaul of the lease accounting model and changes the definition of a lease within the accounting literature. Under the new standard, all leases with a term greater than one year will be recorded on the balance sheet. Amortization of the related asset will be accounted for using one of two approaches prescribed by the guidance. Additional disclosures will be required to allow the user to assess the amount, timing and uncertainty of cash flows arising from leasing activities. A modified retrospective transition approach is required for leases existing at the time of adoption.

In January 2018, the FASB issued ASU No. 2018-01, a further amendment to ASC 842, Leases, which was introduced by ASC No. 2016-02, as discussed above. This update provides an optional practical expedient that allows companies to not evaluate existing or expired land easements that were not previously accounted for under Topic 840 as leases. The Company expects to elect this practical expedient upon adoption. The guidance is effective for the Company’s fiscal year ending September 30, 2020, and interim periods within that year, with early adoption permitted.

In July 2018, the FASB issued ASU No. 2018-11, which provides an optional transition method to ASC 842 that allows the Company to recognize a cumulative effect adjustment to the opening balance of retained earnings in the period of adoption. At this time, the Company does not plan to early adopt the new guidance and expects to transition on a modified retrospective basis. While the Company is currently evaluating the full impact of the standard and its related updates, it expects to recognize additional assets and liabilities arising from current operating leases to its financial position upon adoption.

Statement of Cash Flows

In August 2016, the FASB issued ASU No. 2016-15, an amendment to ASC 230, Statement of Cash Flows, which addresses eight specific cash flow issues for which there has been diversity in practice. The guidance is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year with early adoption permitted. Upon adoption, the amendment will be applied on a retrospective basis. The Company does not expect any material impacts to its cash flows upon adoption.

In November 2016, the FASB issued ASU No. 2016-18, an amendment to ASC 230, Statement of Cash Flows, which requires that any amounts that are deemed to be restricted cash or restricted cash-equivalents be included in cash and cash-equivalent balances on the cash flow statement and, therefore, transfers between cash and restricted cash accounts will no longer be recognized within the statement of cash flows. The guidance is effective for the Company’s fiscal year ending September 30, 2019, with early adoption permitted. Upon adoption, the amendment will be applied on a retrospective basis. Based on the Company's historical restricted cash balances, it does not expect any material impacts to its financial position, results of operations or cash flows upon adoption.

Business Combinations

In January 2017, the FASB issued ASU No. 2017-01, an amendment to ASC 805, Business Combinations, clarifying the definition of a business in the ASC, which is intended to reduce the complexity surrounding the assessment of a transaction as an asset acquisition or business combination. The amendment provides an initial fair value screen to reduce the number of transactions that would fit the definition of a business, and when the screen threshold is not met, provides an updated model that further clarifies the characteristics of a business. The guidance is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year, with early adoption permitted. Upon adoption, the amendment will be applied on a prospective basis. The amendment could potentially have material impacts on future transactions that the Company may enter into by altering the Company’s conclusion on the accounting applied to acquisitions.

12

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Gains and Losses from the Derecognition of Nonfinancial Assets

In February 2017, the FASB issued ASU No. 2017-05, an amendment to ASC 610-20, Other Income - Gains and Losses from the Derecognition of Nonfinancial Assets, which clarifies the scope and accounting related to the derecognition of nonfinancial assets, including partial sales and contributions of nonfinancial assets to a joint venture or other non-controlled investee. The guidance is effective concurrently with ASC 606, which is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year with early adoption permitted. ASU No. 2017-05 may be applied retrospectively for all periods presented or retrospectively with a cumulative-effect adjustment at the date of adoption. The Company has a deferred gain of $6.8 million related to nonfinancial assets on the balance sheet and upon adoption, it would be recognized under the new accounting guidance as a cumulative effect adjustment to the opening balance of retained earnings for the first quarter of fiscal 2019.

Compensation - Retirement Benefits

In March 2017, the FASB issued ASU No. 2017-07, an amendment to ASC 715, Compensation - Retirement Benefits, which changes the presentation of net periodic benefit cost on the income statement by requiring companies to present all components of net periodic benefit cost, other than service cost, outside a subtotal of income from operations. The amendment also states that only the service cost component of net periodic benefits costs is eligible for capitalization, when applicable. The amendment establishes a practical expedient that permits entities to use their previously disclosed service and other costs in their pension and other postretirement benefit plan footnotes in the prior comparative periods as the estimation basis when applying the retrospective presentation of these costs in the income statement. The guidance is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year, with early adoption permitted. Upon adoption, the amendment will be applied on a retrospective basis for income statement presentation and changes to capitalization of costs will be applied on a prospective basis. The Company is continuing to evaluate the amendment to fully understand the impact on the Company's financial position, results of operations and cash flows upon adoption. The Company is also monitoring industry specific developments on this guidance to determine the appropriate treatment of these changes in a rate regulated environment.

Stock Compensation

In May 2017, the FASB issued ASU No. 2017-09, an amendment to ASC 718, Compensation - Stock Compensation, which clarifies the accounting for changes to the terms or conditions of share-based payments. The guidance is effective for the Company’s fiscal year ending September 30, 2019, and interim periods within that year, with early adoption permitted. Upon adoption, the amendments will be applied prospectively to awards modified on or after the adoption date. The Company is currently evaluating the amendments to understand the impact on the Company's financial position, results of operations and cash flows upon adoption.

In June 2018, the FASB issued ASU No. 2018-07, an amendment to ASC 718, Compensation - Stock Compensation, which expands the scope of Topic 718 to include share-based payment transactions for acquiring goods and services from non-employees. The guidance is effective for the Company’s fiscal year ending September 30, 2020, and interim periods within that year, with early adoption permitted. The Company is currently evaluating the impact of the amendment on the Company’s financial position, results of operations and cash flows upon adoption.

Derivatives and Hedging

In August 2017, the FASB issued ASU No. 2017-12, an amendment to ASC 815, Derivatives and Hedging, which is intended to make targeted improvements to the accounting for hedging activities by better aligning an entity’s risk management activities and financial reporting for hedging relationships. These amendments modify the accounting for both nonfinancial and financial risk components and align the recognition and presentation of the effects of the hedging instrument and the hedged item in the financial statements. Additionally, the amendments are intended to simplify the application of the hedge accounting guidance and provide relief to companies by easing certain hedge documentation requirements. The guidance is effective for the Company’s fiscal year ending September 30, 2020, and interim periods within that year, with early adoption permitted. Upon adoption, the transition requirements and elections will be applied to hedging relationships existing on the date of adoption. The Company does not currently apply hedge accounting to any of its risk management activities and thus does not expect the amendments to have an impact on its financial position, results of operations and cash flows upon adoption.

Reporting Comprehensive Income

In February 2018, the FASB issued ASU No. 2018-02, an amendment to ASC 220, Income Statement - Reporting Comprehensive Income, which allows for the reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects of the Tax Act. The guidance is effective for the Company’s fiscal year ending September 30, 2020, and

13

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

interim periods within that year, with early adoption permitted. Upon adoption, the amendments can be applied either in the period of adoption, or retrospectively to each period in which the effects of the Tax Act are recognized. The Company is currently evaluating the amendments to understand the impact on its financial position and results of operations upon adoption.

3. REGULATION

NJNG is subject to cost-based regulation, therefore, it is permitted to recover authorized operating expenses and earn a reasonable return on its utility capital investments based on the BPU's approval. The impact of the ratemaking process and decisions authorized by the BPU allows NJNG to capitalize or defer certain costs that are expected to be recovered from its customers as regulatory assets and to recognize certain obligations representing amounts that are probable future expenditures as regulatory liabilities in accordance with accounting guidance applicable to regulated operations.

NJNG's recovery of costs is facilitated through its base rates, BGSS and other regulatory tariff riders. NJNG is required to make annual filings to the BPU for review of its BGSS, CIP and various other programs and related rates. Annual rate changes are typically requested to be effective at the beginning of the following fiscal year. All rate and program changes are subject to proper notification and BPU review and approval. In addition, NJNG is also permitted to implement certain BGSS rate changes on an interim basis with proper notification to the BPU.

Regulatory assets and liabilities included on the Unaudited Condensed Consolidated Balance Sheets are comprised of the following:

(Thousands) | June 30, 2018 | September 30, 2017 | ||||

Regulatory assets-current | ||||||

New Jersey Clean Energy Program | $ | 15,533 | $ | 14,202 | ||

Underrecovered gas costs | 5,693 | 9,910 | ||||

Derivatives at fair value, net | 230 | 9,010 | ||||

Conservation Incentive Program | — | 17,669 | ||||

Total current regulatory assets | $ | 21,456 | $ | 50,791 | ||

Regulatory assets-noncurrent | ||||||

Environmental remediation costs | ||||||

Expended, net of recoveries | $ | 29,647 | $ | 28,547 | ||

Liability for future expenditures | 140,821 | 149,000 | ||||

Deferred income taxes | 16,796 | 21,795 | ||||

SAVEGREEN | 7,410 | 16,302 | ||||

Postemployment and other benefit costs | 133,179 | 141,433 | ||||

Deferred storm damage costs | 11,401 | 13,030 | ||||

Other noncurrent regulatory assets | 8,825 | 5,812 | ||||

Total noncurrent regulatory assets | $ | 348,079 | $ | 375,919 | ||

Regulatory liabilities-current | ||||||

Conservation Incentive Program | $ | 6,637 | $ | — | ||

Derivatives at fair value, net | 845 | 78 | ||||

Total current regulatory liabilities | $ | 7,482 | $ | 78 | ||

Regulatory liabilities-noncurrent | ||||||

Tax Act impact (1) | $ | 206,832 | $ | — | ||

Cost of removal obligation | — | 7,902 | ||||

Derivatives at fair value, net | 466 | 146 | ||||

New Jersey Clean Energy Program | 2,484 | 5,795 | ||||

Other noncurrent regulatory liabilities | 1,649 | 664 | ||||

Total noncurrent regulatory liabilities | $ | 211,431 | $ | 14,507 | ||

(1) | Includes an adjustment related to the re-measurement of NJNG's net deferred tax liabilities to reflect the change in federal tax rates enacted in the Tax Act, which is net of sales tax collected from customers. For a more detailed discussion, see Note 11. Income Taxes. |

14

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Regulatory filings and/or actions that occurred during the current fiscal year include the following:

The Tax Act

• | On December 22, 2017, the Tax Act was signed into law, which resulted in a reduction in the federal corporate tax rate. As a result, NJNG recorded a regulatory liability, which included the revaluation of its deferred income taxes and the accounting of the income tax effects on the revaluation. The revaluation was based on certain assumptions and estimations NJNG made with respect to its deferred taxes, as well as the effects from the Tax Act, and as such are subject to change if and when assumptions are updated. See Note 11. Income Taxes for a more detailed discussion on the Tax Act. |

On January 31, 2018, the BPU issued an Order which directed New Jersey utilities to submit filings to the BPU by March 2, 2018, to propose the prospective change in base rates as a result of the Tax Act to be effective April 1, 2018, the method to return to customers the overcollection of taxes in base rates from January 1, 2018, through March 31, 2018, and an outline of the method by which the excess deferred taxes would be returned to customers. The excess deferred taxes are primarily related to timing differences associated with utility plant depreciation and are subject to IRS normalization rules, which require amortization over the remaining life of the utility plant.

On March 1, 2018, NJNG submitted its required filing to the BPU proposing a $19.7 million base rate reduction and customer refunds of approximately $31 million, which is inclusive of state sales tax. On March 26, 2018, the BPU approved, on an interim basis, the $19.7 million rate reduction, effective April 1, 2018. On May 22, 2018, the BPU also approved the refund of the $31 million, which included interest at the Company’s short-term debt rate as specified in the Company’s last base rate case. These credits were returned to customer accounts in June 2018.

BGSS and CIP

• | On March 26, 2018, the BPU approved NJNG's petition on a final basis to maintain NJNG's BGSS rate for residential and small commercial customers, increase to its balancing charge rate, which resulted in a $3.7 million increase to the annual revenues credited to BGSS and a decrease to its CIP rates, which resulted in a $16.2 million annual recovery decrease that was effective October 1, 2017. |

• | On May 29, 2018, NJNG filed its annual petition with the BPU to maintain its BGSS rate for residential and small commercial customers and increase its balancing charge rate, resulting in a $10.8 million increase to the annual revenues credited to BGSS, as well as a decrease in CIP rate, which will result in a $30.9 million annual recovery decrease, effective October 1, 2018. |

Energy Efficiency Programs

• | On October 20, 2017, the BPU approved NJNG's filing to decrease its EE recovery rate, which will result in an annual decrease of $3.9 million, effective November 1, 2017. |

• | On March 28, 2018, NJNG filed a petition with the BPU requesting continuation of existing SAVEGREEN programs and the addition of new programs through December 2024, with investments of approximately $341 million. |

• | On May 25, 2018, NJNG filed a petition with the BPU to decrease its EE recovery rate, which will result in an annual decrease of $7 million, anticipated to be effective January 1, 2019. |

Societal Benefits Clause

• | On June 22, 2018, NJNG filed its annual USF compliance filing to increase rates, which will result in a $7.3 million annual increase, anticipated to be effective October 1, 2018. |

• | On July 25, 2018, the BPU approved NJNG's annual SBC filing requesting to recover remediation expenses incurred through June 30, 2017, a reduction in the RAC, which will result in an annual decrease of $2.4 million and to increase the NJCEP factor, which will result in an annual increase of $1.8 million, effective September 1, 2018. |

Infrastructure Programs

• | On July 24, 2018, NJNG updated its annual petition with the BPU that was filed on March 29, 2018, which requested a base rate increase for the recovery of SAFE II and NJ RISE capital investment costs related to the 12-months ending June 30, 2018, and was based on estimates. The filing was updated to reflect actual results, with changes to base rates in the amount of $6.8 million annually, anticipated to be effective October 1, 2018. |

15

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

4. DERIVATIVE INSTRUMENTS

The Company is subject primarily to commodity price risk due to fluctuations in the market price of natural gas, SRECs and electricity. To manage this risk, the Company enters into a variety of derivative instruments including, but not limited to, futures contracts, physical forward contracts, financial options and swaps to economically hedge the commodity price risk associated with its existing and anticipated commitments to purchase and sell natural gas, SRECs and electricity. In addition, the Company is exposed to foreign currency and interest rate risk, The Company may utilize foreign currency derivatives to hedge Canadian dollar denominated gas purchases and/or sales and interest rate derivatives to reduce exposure to fluctuations in interest rates. All of these types of contracts are accounted for as derivatives. Accordingly, all of the financial and certain of the Company's physical derivative instruments are recorded at fair value on the Unaudited Condensed Consolidated Balance Sheets. For a more detailed discussion of the Company's fair value measurement policies and level disclosures associated with NJR's derivative instruments, see Note 5. Fair Value.

Energy Services

Energy Services chooses not to designate its financial commodity and physical forward commodity derivatives as accounting hedges or to elect NPNS. The changes in the fair value of these derivatives are recorded as a component of gas purchases or operating revenues, as appropriate for Energy Services, on the Unaudited Condensed Consolidated Statements of Operations as unrealized gains or losses. For Energy Services at settlement, realized gains and losses on all financial derivative instruments are recognized as a component of gas purchases and realized gains and losses on all physical derivatives follow the presentation of the related unrealized gains and losses as a component of either gas purchases or operating revenues.

Energy Services also enters into natural gas transactions in Canada and, consequently, is exposed to fluctuations in the value of Canadian currency relative to the U.S. dollar. Energy Services may utilize foreign currency derivatives to lock in the exchange rate associated with natural gas transactions denominated in Canadian currency. The derivatives may include currency forwards, futures, or swaps and are accounted for as derivatives. These derivatives are typically used to hedge demand fee payments on pipeline capacity, storage and gas purchase agreements.

As a result of Energy Services entering into transactions to borrow natural gas, commonly referred to as “park and loans,” an embedded derivative is recognized relating to differences between the fair value of the amount borrowed and the fair value of the amount that will ultimately be repaid, based on changes in the forward price for natural gas prices at the borrowed location over the contract term. This embedded derivative is accounted for as a forward sale in the month in which the repayment of the borrowed gas is expected to occur, and is considered a derivative transaction that is recorded at fair value on the Unaudited Condensed Consolidated Balance Sheets, with changes in value recognized in current period earnings.

Expected production of SRECs is hedged through the use of forward and futures contracts. All contracts require the Company to physically deliver SRECs through the transfer of certificates as per contractual settlement schedules. The Company applies NPNS accounting to SREC forward and futures contracts entered into on or before December 31, 2015. Effective for contracts executed on or after January 1, 2016, Energy Services no longer elects NPNS accounting treatment on all SREC forward sales contracts and recognizes changes in the fair value of these derivatives as a component of operating revenues. Upon settlement of the contract, the related revenue is recognized when the SREC is transferred to the counterparty. NPNS is a contract-by-contract election and, where appropriate, the Company can and may elect normal accounting for certain contracts.

Natural Gas Distribution

Changes in fair value of NJNG's financial commodity derivatives are recorded as a component of regulatory assets or liabilities on the Unaudited Condensed Consolidated Balance Sheets. The Company elects NPNS accounting treatment on all physical commodity contracts that NJNG entered into on or before December 31, 2015, and accounts for these contracts on an accrual basis. Accordingly, physical natural gas purchases are recognized in regulatory assets or liabilities on the Unaudited Condensed Consolidated Balance Sheets when the contract settles and the natural gas is delivered. The average cost of natural gas is charged to expense in the current period earnings based on the BGSS factor times the therm sales. Effective for contracts executed on or after January 1, 2016, NJNG no longer elects NPNS accounting treatment on all physical forward commodity contracts. However, since NPNS is a contract-by-contract election, where it makes sense to do so, NJNG can and may elect certain contracts to be normal. Because NJNG recovers these amounts through future BGSS rates as increases or decreases to the cost of natural gas in NJNG’s tariff for gas service, the changes in fair value of these contracts are deferred as a component of regulatory assets or liabilities on the Unaudited Condensed Consolidated Balance Sheets.

16

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

In June 2015, NJNG entered into a treasury lock transaction to fix a benchmark treasury rate of 3.26 percent associated with a $125 million debt issuance that was finalized in May 2018. This debt issuance coincided with the maturity of NJNG's $125 million, 5.6 percent notes that came due May 15, 2018. This treasury lock was settled on March 13, 2018, which coincided with the pricing of the new debt being issued. Settlement of the treasury lock resulted in a $2.6 million loss, which is recorded as a component of regulatory assets on the Unaudited Condensed Consolidated Balance Sheets and will be amortized in earnings over the term of the $125 million, 4.01 percent notes that were issued on May 11, 2018.

Home Services and Other

On January 26, 2018, NJR entered into a variable-for-fixed interest rate swap on its existing $100 million variable rate term loan, which fixed the variable rate at 2.84 percent. The swap will terminate on August 16, 2019, which coincides with the maturity of the debt. The change in the fair value of the interest rate swap is recorded as interest expense on the Unaudited Condensed Consolidated Statements of Operations.

Fair Value of Derivatives

The following table reflects the fair value of NJR's derivative assets and liabilities recognized on the Unaudited Condensed Consolidated Balance Sheets as of:

Fair Value | |||||||||||||||||

June 30, 2018 | September 30, 2017 | ||||||||||||||||

(Thousands) | Balance Sheet Location | Asset Derivatives | Liability Derivatives | Asset Derivatives | Liability Derivatives | ||||||||||||

Derivatives not designated as hedging instruments: | |||||||||||||||||

Natural Gas Distribution: | |||||||||||||||||

Physical commodity contracts | Derivatives - current | $ | 57 | $ | 286 | $ | 151 | $ | 72 | ||||||||

Financial commodity contracts | Derivatives - current | 323 | 117 | — | 1,149 | ||||||||||||

Interest rate contracts | Derivatives - current | — | — | — | 8,467 | ||||||||||||

Energy Services: | |||||||||||||||||

Physical commodity contracts | Derivatives - current | 6,847 | 17,660 | 14,588 | 16,589 | ||||||||||||

Derivatives - noncurrent | 2,474 | 13,267 | 7,127 | 8,710 | |||||||||||||

Financial commodity contracts | Derivatives - current | 15,728 | 25,151 | 15,302 | 20,267 | ||||||||||||

Derivatives - noncurrent | 9,324 | 8,163 | 2,033 | 2,620 | |||||||||||||

Foreign currency contracts | Derivatives - current | — | 184 | 40 | — | ||||||||||||

Derivatives - noncurrent | — | 174 | 4 | — | |||||||||||||

Home Services and Other: | |||||||||||||||||

Interest rate contracts | Derivatives - current | 237 | — | — | — | ||||||||||||

Derivatives - noncurrent | 88 | — | — | — | |||||||||||||

Total fair value of derivatives | $ | 35,078 | $ | 65,002 | $ | 39,245 | $ | 57,874 | |||||||||

Offsetting of Derivatives

The Company transacts under master netting arrangements or equivalent agreements that allow it to offset derivative assets and liabilities with the same counterparty. However, the Company’s policy is to present its derivative assets and liabilities on a gross basis at the contract level unit of account on the Unaudited Condensed Consolidated Balance Sheets.

17

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The following table summarizes the reported gross amounts, the amounts that the Company has the right to offset but elects not to, financial collateral, as well as the net amounts the Company could present on the Unaudited Condensed Consolidated Balance Sheets but elects not to.

(Thousands) | Amounts Presented on Balance Sheets (1) | Offsetting Derivative Instruments (2) | Financial Collateral Received/Pledged (3) | Net Amounts (4) | ||||||||||||

As of June 30, 2018: | ||||||||||||||||

Derivative assets: | ||||||||||||||||

Energy Services | ||||||||||||||||

Physical commodity contracts | $ | 9,321 | $ | (3,461 | ) | $ | (200 | ) | $ | 5,660 | ||||||

Financial commodity contracts | 25,052 | (16,800 | ) | 360 | 8,612 | |||||||||||

Total Energy Services | $ | 34,373 | $ | (20,261 | ) | $ | 160 | $ | 14,272 | |||||||

Natural Gas Distribution | ||||||||||||||||

Physical commodity contracts | $ | 57 | $ | (6 | ) | $ | — | $ | 51 | |||||||

Financial commodity contracts | 323 | (117 | ) | — | 206 | |||||||||||

Total Natural Gas Distribution | $ | 380 | $ | (123 | ) | $ | — | $ | 257 | |||||||

Home Services and Other | ||||||||||||||||

Interest rate contracts | $ | 325 | $ | — | $ | — | $ | 325 | ||||||||

Total Home Services and Other | $ | 325 | $ | — | $ | — | $ | 325 | ||||||||

Derivative liabilities: | ||||||||||||||||

Energy Services | ||||||||||||||||

Physical commodity contracts | $ | 30,927 | $ | (3,461 | ) | $ | — | $ | 27,466 | |||||||

Financial commodity contracts | 33,314 | (16,800 | ) | (16,154 | ) | 360 | ||||||||||

Foreign currency contracts | 358 | — | — | 358 | ||||||||||||

Total Energy Services | $ | 64,599 | $ | (20,261 | ) | $ | (16,154 | ) | $ | 28,184 | ||||||

Natural Gas Distribution | ||||||||||||||||

Physical commodity contracts | $ | 286 | $ | (6 | ) | $ | — | $ | 280 | |||||||

Financial commodity contracts | 117 | (117 | ) | 206 | 206 | |||||||||||

Total Natural Gas Distribution | $ | 403 | $ | (123 | ) | $ | 206 | $ | 486 | |||||||

As of September 30, 2017: | ||||||||||||||||

Derivative assets: | ||||||||||||||||

Energy Services | ||||||||||||||||

Physical commodity contracts | $ | 21,715 | $ | (2,173 | ) | $ | (200 | ) | $ | 19,342 | ||||||

Financial commodity contracts | 17,335 | (14,121 | ) | — | 3,214 | |||||||||||

Foreign currency contracts | 44 | — | — | 44 | ||||||||||||

Total Energy Services | $ | 39,094 | $ | (16,294 | ) | $ | (200 | ) | $ | 22,600 | ||||||

Natural Gas Distribution | ||||||||||||||||

Physical commodity contracts | $ | 151 | $ | (20 | ) | $ | — | $ | 131 | |||||||

Total Natural Gas Distribution | $ | 151 | $ | (20 | ) | $ | — | $ | 131 | |||||||

Derivative liabilities: | ||||||||||||||||

Energy Services | ||||||||||||||||

Physical commodity contracts | $ | 25,299 | $ | (2,173 | ) | $ | — | $ | 23,126 | |||||||

Financial commodity contracts | 22,887 | (14,121 | ) | (8,766 | ) | — | ||||||||||

Total Energy Services | $ | 48,186 | $ | (16,294 | ) | $ | (8,766 | ) | $ | 23,126 | ||||||

Natural Gas Distribution | ||||||||||||||||

Physical commodity contracts | $ | 72 | $ | (20 | ) | $ | — | $ | 52 | |||||||

Financial commodity contracts | 1,149 | — | (1,149 | ) | — | |||||||||||

Interest rate contracts | 8,467 | — | — | 8,467 | ||||||||||||

Total Natural Gas Distribution | $ | 9,688 | $ | (20 | ) | $ | (1,149 | ) | $ | 8,519 | ||||||

(1) | Derivative assets and liabilities are presented on a gross basis on the balance sheet as the Company does not elect balance sheet offsetting under ASC 210-20. |

(2) | Includes transactions with NAESB netting election, transactions held by FCMs with net margining and transactions with ISDA netting. |

(3) | Financial collateral includes cash balances at FCMs as well as cash received from or pledged to other counterparties. |

(4) | Net amounts represent presentation of derivative assets and liabilities if the Company were to elect balance sheet offsetting under ASC 210-20. |

18

New Jersey Resources Corporation

Part I

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)