Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from_____to ____

| INDOOR HARVEST CORP |

(Exact name of registrant as specified in its charter)

| Texas | 3590 | 45-5577364 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Indoor Harvest Corp 5300 East Freeway Suite A Houston, Texas 77020 (346) 310-3427 |

||

| (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) |

Daniel Weadock

Chief Executive Officer

5300 East Freeway Suite A

Houston, Texas 77020

(346) 310-3427

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Securities registered pursuant to Section 12(b) of the

Act: None Securities registered pursuant to Section

12(g) of the Act: None (Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an “emerging growth company”. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| (Do not check if a smaller reporting company) | Emerging growth company | ☒ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes ☐ No ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed first fiscal quarter: The aggregate market value of the 11,194,612 shares of voting stock held by nonaffiliates of the registrant, computed by reference to the closing price as reported on the OTCQB, as of the last business day of Indoor Harvest’s most recently completed second fiscal quarter (June 30, 2017), was $2,238,922.

We have 24,957,471 shares of common stock outstanding as of April 17, 2018.

TABLE OF

CONTENTS

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND INFORMATION

This Annual Report on Form 10-K, the other reports, statements, and information that we have previously filed or that we may subsequently file with the Securities and Exchange Commission, or SEC, and public announcements that we have previously made or may subsequently make include, may include, incorporate by reference or may incorporate by reference certain statements that may be deemed to be “forward- looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and are intended to enjoy the benefits of that act. Unless the context is otherwise, the forward-looking statements included or incorporated by reference in this Form 10-K and those reports, statements, information and announcements address activities, events or developments that Indoor Harvest, Corp. (hereinafter referred to as “we,” “us,” “our,” “our Company” or “Indoor Harvest”) expects or anticipates, will or may occur in the future. Any statements in this document about expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “will continue,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” and similar expressions. Accordingly, these statements involve estimates, assumptions and uncertainties, which could cause actual results to differ materially from those expressed in them. Any forward-looking statements are qualified in their entirety by reference to the factors discussed throughout this document. All forward-looking statements concerning economic conditions, rates of growth, rates of income or values as may be included in this document are based on information available to us on the dates noted, and we assume no obligation to update any such forward-looking statements. It is important to note that our actual results may differ materially from those in such forward-looking statements due to fluctuations in interest rates, inflation, government regulations, economic conditions and competitive product and pricing pressures in the geographic and business areas in which we conduct operations, including our plans, objectives, expectations and intentions and other factors discussed elsewhere in this Report.

Certain risk factors could materially and adversely affect our business, financial conditions and results of operations and cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us, and you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made and we do not undertake any obligation to update any forward-looking statement or statements to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events. The risks and uncertainties we currently face are not the only ones we face. New factors emerge from time to time, and it is not possible for us to predict which will arise. There may be additional risks not presently known to us or that we currently believe are immaterial to our business. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. If any such risks occur, our business, operating results, liquidity and financial condition could be materially affected in an adverse manner. Under such circumstances, you may lose all or part of your investment.

The industry and market data contained in this report are based either on our management’s own estimates or, where indicated, independent industry publications, reports by governmental agencies or market research firms or other published independent sources and, in each case, are believed by our management to be reasonable estimates. However, industry and market data is subject to change and cannot always be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares. We have not independently verified market and industry data from third-party sources. In addition, consumption patterns and customer preferences can and do change. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be verifiable or reliable.

Item 1. DESCRIPTION OF THE BUSINESS

Organization

We are a Texas corporation formed on November 23, 2011. Our principal executive office is located at 5300 East Freeway Suite A, Houston, Texas 77020. On August 3, 2017, we formed Alamo Acquisition, LLC, a wholly owned Texas limited liability company (“Alamo Acquisition Sub”). On August 4, 2017, we consummated a reverse triangular merger (the “Alamo Merger”) pursuant to which Alamo Acquisition Sub acquired all of the outstanding membership interests of Alamo CBD, LLC. (“Alamo CBD”), a Texas limited liability company. Upon closing of the Alamo Merger, the membership interests (“Alamo Surviver Members”) of Alamo CBD were exchanged for 7,584,008 shares of Indoor Harvest’s common stock, and thereafter Alamo CBD continued as our surviving wholly-owned subsidiary, and Alamo Acquisition Sub ceased to exist. Our common stock is quoted on the OTCQB under the symbol “INQD.”

Description of Business

Indoor Harvest, through its brand name Indoor Harvest®, is a technology company focused on enabling the production of biopharma grade cannabis for research and development of true pharma grade personalized medicines. We are also a provider of advanced cultivation methods and processes for the cannabis industry. Our integrated technology platform design allows us to manipulate the environment of the plant to influence its phenotypic expression. Among other things, we are also seeking to use the proprietary technology we have developed to become a registered producer and seller under the Controlled Substance Act (“CSA”) of pharmaceutical grade cannabis for research and targeted treatment of specific medical symptoms by third parties.

We have developed a patent pending high pressure aeroponic process of growing cultivars in an air or mist environment without the use of soil or an aggregate growing medium. Aeroponic production differs from both conventional hydroponics and in-vitro (plant tissue culture) growing. Unlike hydroponics, which uses water as a growing medium and essential minerals to sustain plant growth, aeroponics is conducted without a growing medium. Because water is used in aeroponics to transmit nutrients, it is sometimes considered a type of hydroponics. Our high pressure aeroponic process and production methods provide an ability to test the phenotypic plasticity of cannabis and to test and develop specific phenotypic response. Phenotypic plasticity refers to the changes in cannabis morphology and physiology due to its adaption to a unique environment and its impact on phytochemical production.

We have also developed a significant set of industry partnerships and relationships over the last 7 years uniquely positioning us to create fully integrated facilities designs for fully controlled and automated growing environments that would include not only our patent pending high pressure aeroponic systems but also a patent pending HVAC system design, leading LED lighting technology plus controls and sensors.

We, through Alamo CBD, have applied to produce and dispense low-tetrahydrocannabinol cannabis under the Texas Compassionate Use Program (“TCUP”). Tetrahydrocannabinol or “THC” is a psychotropic cannabinoid and is the principal psychoactive constituent of cannabis. We have signed a binding LOI with Zoned Properties, Inc. (“Zoned Properties”) outlining three independent pending agreements to complete research and development projects for licensed medical cannabis facilities to be located in Tempe, Arizona, Parachute, Colorado and Stockdale, Texas or other location to be determined after approval of a provisional license under the TCUP.

At the same time, we continue to explore other avenues of opportunity to deploy our technology in partnership with license holders in attractive jurisdictions.

The Company intends to generate revenue from the manufacture or co-manufacturing and sales of pharma grade cannabis to research and development organizations, through related engineering, project management, equipment leasing and technology licensing from constructed facilities in Tempe, Arizona and Parachute, Colorado and through the development and licensing of related environmental and climate recipes.

Our operational expenditures are primarily related to further developing our technology, launching and completing test trials, developing research partnerships and collaborations related to perfecting precise expressions of personalized medicine and the costs related to being a fully reporting company with the SEC.

Industry and Regulatory Overview

The United States federal government regulates drugs through the CSA (21 U.S.C. § 811), which places controlled substances, including cannabis, in a schedule. Cannabis is classified as a Schedule I drug, which is viewed as highly addictive and having no medical value. The United States Federal Drug Administration (“FDA”) has not approved the sale of cannabis for any medical application. Doctors may not prescribe cannabis for medical use under federal law, however, they can recommend its use under the First Amendment. In 2010, the United States Veterans Affairs Department clarified that veterans using medicinal cannabis will not be denied services or other medications that are denied to those using illegal drugs.

State legalization efforts conflict with the CSA, which makes cannabis use and possession illegal on a national level. On August 29, 2013, the U.S. Department of Justice (“DOJ”) issued a memorandum (“Cole Memo”) providing that where states and local governments enact laws authorizing cannabis-related use, and implement strong and effective regulatory and enforcement systems, the federal government will rely upon states and local enforcement agencies to address cannabis activity through the enforcement of their own state and local narcotics laws. The memorandum further stated that the DOJ’s limited investigative and prosecutorial resources will be focused on eight priorities (the “Eight Priorities”) to prevent unintended consequences of the state laws, as follows:

| ● | Preventing the distribution of marijuana to minors; | |

| ● | Preventing revenue from the sale of marijuana from going to criminal enterprises, gangs, and cartels; | |

| ● | Preventing the diversion of marijuana from states where it is legal under state law in some form to other states; | |

| ● | Preventing state-authorized marijuana activity from being used as a cover or pretext for the trafficking or other illegal drugs or other illegal activity; | |

| ● | Preventing violence and the use of firearms in the cultivation and distribution of marijuana; |

1

| ● | Preventing drugged driving and the exacerbation of other adverse public health consequences associated with marijuana use; | |

| ● | Preventing the growing of marijuana on public lands and the attendant public safety and environmental dangers posed by marijuana production on public lands, and | |

| ● | Preventing marijuana possession or use on federal property. |

On December 11, 2014, the DOJ issued another memorandum about its position and enforcement protocol with regard to Indian Country, stating that the Eight Priorities in the Cole Memo would guide the United States Attorneys’ cannabis enforcement efforts in Indian Country. On December 16, 2014, as a component of the federal spending bill, the Obama administration enacted regulations that prohibit the DOJ from using funds to prosecute state-based legal medical cannabis programs.

On January 4, 2018, the DOJ suspended the Cole Memo and replaced it with a new Memorandum titled with the subject “Marijuana Enforcement” from Attorney General Jeff Sessions which provides that each U.S. Attorney has the discretion to determine which types of cannabis-related cases should be federally prosecuted, thus ending the broad safe harbor provided under the Cole Memo.

As of January 4, 2018, 29 states, the District of Columbia and Guam allow their citizens to use medical cannabis through de-criminalization. Voters in the States of Alaska, California, Colorado, Maine, Massachusetts, Nevada, Oregon, and Washington have legalized cannabis for adult recreational use.

The Company continues to follow and monitor the actions and statements of the Trump administration, the DOJ and Congress’ positions on federal law and cannabis policy. As the possession and use of cannabis is illegal under the CSA, we could be deemed to be aiding and abetting illegal activities through the equipment we intend to sell in the U.S. and directly violating federal law if we should begin producing cannabis under State law. Under federal law, and more specifically the CSA, the possession, use, cultivation, and transfer of cannabis is illegal. Our equipment could be used by persons or entities engaged in the business of possession, use, cultivation, and/or transfer of cannabis.

As a result, law enforcement authorities, in their attempt to regulate the illegal use of cannabis, could seek to bring an action or actions against us, including, but not limited to, a claim of aiding and abetting another’s criminal activities or directly violating the CSA. The federal aiding and abetting statute provides that anyone who “commits an offense against the United States or aids, abets, counsels, commands, induces or procures its commission, is punishable as a principal” (18 U.S.C. §2(a).) Enforcement of federal law regarding cannabis would likely result in the Company being unable to proceed with our business plans, could expose us to potential criminal liability and could subject our properties to civil forfeiture which could lead to an entire loss of any investment in the Company. Any changes in banking, insurance or other business services may also affect our ability to operate our business.

Changes in Business Operations

From inception until August 4, 2017, the Company provided full service, state of the art design-build, engineering, procurement and construction services to the indoor and vertical farming industry. The Company provided production platforms, mechanical systems and complete custom designed build outs for both Controlled Environment Agriculture (“CEA”) and Building Integrated Agriculture (“BIA”), for two unique industries, produce and cannabis.

CEA is the process of manipulating any agricultural technology to allow the farmer an ability to manipulate a crop’s environment to desired conditions. Technologies include greenhouse production, hydroponics, aquaculture, aquaponics and aeroponics. Controlled variables may include temperature, lighting, humidity, pH and nutrient analysis.

BIA is the process of locating CEA methods on, or in, mixed use buildings to provide synergy with the buildings infrastructure and the agriculture process. Earliest examples of BIA include the use of hydroponics, aeroponics and aquaponics, where waste heat is captured through the building’s existing heating, ventilation and air conditioning system as well as the combined use of solar, rainwater collection and evaporative systems. Current operating examples include such buildings as Eli Zabar’s rooftop greenhouse, The Sun Works Center for Environmental Studies, Gotham Greens, Sky Vegetables, Top Sprouts, Cityscape Farms, Dongtan, Masdar City, AeroFarms, Solar 2, Lufa Farms, BrightFarms, FarmedHere, Green Sense Farms, Green Spirit Farms and Big Box Farms. The term building-integrated agriculture was coined by Dr. Ted Caplow in a paper delivered at the 2007 Passive and Low Energy Cooling Conference in Crete, Greece.

The Company began generating revenue in late 2015 from its products and design-build, engineering, procurement and construction management services. Our products were designed for the production of aeroponic and hydroponic leafy greens, micro-greens, fruiting plants and herbs. Our fixtures and systems could also be adapted for a variety of other uses such as horticulture research, medicinal plant production, pharmaceutical plant production, plant cloning and hardwood propagation.

In mid-2016, the Company began efforts to separate its produce and cannabis related operations due to ongoing feedback from both clients and potential institutional investors. It was determined that the Company’s involvement in the cannabis industry was creating conflicts for clients and potential institutional investors wishing to work with the Company from the produce industry due to the public perception and political issues surrounding the cannabis industry. By late-2016, the Company had decided to cease actively selling its products and services to the vertical farming industry and to focus on utilizing the Company’s developed technology and methods for the cannabis industry. On August 4, 2017, the Company ceased actively supporting business development of vertical farms for produce production.

Merger of Alamo CBD, LLC

On January 3, 2017, the Company signed a binding LOI with Alamo CBD to enter discussions to combine and create a medical cannabinoids pharmaceutical group. On August 3, 2017, we formed Alamo Acquisition Sub, a wholly owned Texas limited liability company.

On August 4, 2017, we consummated a reverse triangular merger (the “Alamo Merger”) pursuant to which Alamo Acquisition Sub acquired all of the outstanding membership interests of Alamo CBD, a Texas limited liability company. Upon closing of the Alamo Merger, the membership interests (“Alamo Surviver Members”) of Alamo CBD were exchanged for 7,584,008 shares of Indoor Harvest’s common stock, and Alamo CBD continued as our surviving wholly-owned subsidiary, and Alamo Acquisition Sub ceased to exist.

2

In addition to the foregoing, following the closing of the Alamo Merger, and Alamo CBD being successfully awarded a provisional or full license to produce and dispense cannabis in the State of Texas, Indoor Harvest will issue to the individual Alamo Surviver Members, an additional Eight Million Five Hundred Thousand Dollars ($8,500,000) of newly-issued shares of common stock of Indoor Harvest, par value $0.001, based upon the three (3) day average closing price of the Company’s common stock, as quoted on the OTCQB, prior to the time of issuance. However, there can be no assurance that Alamo CBD will be awarded such license in the near future or at all.

Additionally, upon Alamo CBD successfully being registered and licensed by the Drug Enforcement Agency (“DEA”) to produce and dispense cannabis under federal law, Indoor Harvest will issue to the individual Alamo Surviver Members, an additional Two Million Five Hundred Thousand Dollars ($2,500,000) cash payment, or newly-issued shares of common stock of Indoor Harvest, par value $0.001, based upon the three (3) day average closing price of the Company’s common stock, as quoted on the OTCQB, prior to the time of issuance, at the option of the individual Alamo Surviver Member. A combination of cash and common stock may be elected by Alamo Surviver Member individually. However, there can be no assurance that Alamo CBD will be registered or licensed by the DEA, in the near future or at all.

On August 8, 2017, Chad Sykes, the Company’s Founder and Chief of Cultivation, returned 2,500,000 shares of common stock to the Company. Mr. Sykes voluntarily returned such shares in order to prevent dilution to the Company’s shareholders as a result of the merger and in order to facilitate the merger. The return of common stock by Chad Sykes was a non-cash transaction and reduced the common stock outstanding as of December 31, 2017. Mr. Sykes return of stock was valued $2,500, or at par value of $0.001 per share.

On September 6, 2017, the Company issued an aggregate of 7,584,008 shares of common stock to the members of Alamo CBD related to the Merger. The Company recorded goodwill at a fair value of $1,440,961 ($0.19 per share) based upon closing price per share of the Company’s common stock on the date the stock was issued. The Company subsumed into goodwill all intangible assets acquired in the transaction, which is Alamo CBD’s pending provisional or full license to produce and dispense cannabis in the State of Texas.

As of December 31,2017, the Company’s management decided to impair the goodwill created by the Alamo Merger, as there are doubts regarding when a license may be issued, as the license is pending and may, or may not ever be issued, and whether upon receipt of the license if it will lead to significant positive cash flows. The Company recorded an impairment of goodwill in the Statement of Operations for the year ended December 31, 2017.

Contractual Joint Venture with Alamo CBD and Vyripharm Enterprises, LLC

On March 23, 2017, Indoor Harvest entered into a Contractual Joint Venture Agreement by and between Vyripharm Enterprises, LLC (“Vyripharm”) and Alamo CBD, collectively the parties, pursuant to which the parties agreed to participate in an unincorporated joint venture (the “Joint Venture”) for the following business purposes:

| ● | The parties would work together to enhance the ability of Alamo CBD to apply for and obtain licensure, or a permit, to grow and/or dispense marijuana products for medical and/or consumer use, as the case may be: | |

| i. | In Texas, pursuant to the Texas Compassionate Use Act, as may be amended; | |

| ii. | In Colorado, pursuant to recent Colorado legislation permitting foreign ownership of entities that grow and/or dispense marijuana products for medical and/or consumer use; and | |

| iii. | Pursuant to recent United States Drug Enforcement Administration regulations which expand the opportunities for entities providing research involving marijuana and its chemical constituents, as referenced in 21 U.S.C. 822(a)(1) and 21 U.S.C. 823(a), et. seq. | |

| ● | To establish Alamo CBD as a supplier of a variety of medical use cannabis oil to Vyripharm for Vyripharm’s use in conducting research and development to create novel pharmaceutical and radiopharmaceutical compounds designed to image and treat certain debilitating diseases including, but not limited to epilepsy, post-traumatic stress disorder, Alzheimer’s, ALS, and other neurodegenerative diseases; and to establish Indoor Harvest as the project developer and engineering, procurement and construction group, in which Indoor Harvest is responsible for costs and efforts related to Alamo CBD’s efforts to become licensed under the Texas Compassionate Use Act and to meet its obligations under this Joint Venture agreement. |

The initial term of the Joint Venture was to be five (5) years following the effective date, and the Joint Venture Agreement could be extended beyond this initial term by mutual consent of the parties. Pursuant to the Joint Venture terms, the Company agreed to contribute a total of $5,000,000 on the basis of $1,000,000 per year for each of the first five (5) years of the Initial Term. Should the Company fail to make payment under the Joint Venture, the agreement would terminate and neither party would have further obligation to the other.

The Company paid an initial down payment of $250,000 under the Joint Venture Agreement on March 30, 2017.

Background for the Contractual Joint Venture

The purpose of the above-described change in business and Joint Venture was twofold, as follows:

| ● | It would separate the Company’s cannabis and produce related operations, as we indicated was previously a goal. | |

| ● | It would put in place all elements necessary for the resulting Joint Venture, of which the resulting public reporting company would have a significant on-going interest, to become a registered producer under the federal CSA to produce cannabis. |

As of December 1, 2017, only one entity, the University of Mississippi can legally manufacture cannabis to supply researchers involved in the various studies about using cannabis to treat maladies such as Post Traumatic Stress Disorder (“PTSD”) or Epilepsy. On August 12, 2016, the DOJ and the DEA issued a policy statement on cannabis issues, as follows:

| ● | It is well known that the DOJ and DEA have said that cannabis would continue to be classified as a Schedule 1 drug, like heroin. |

3

| ● | It is not so well known that the DOJ and DEA also reset the policy regarding entities that could legally manufacture cannabis to supply researchers involved in various clinical studies using cannabis to treat maladies such as PTSD or Epilepsy. |

According to the policy statement, the purpose of this policy reset is to increase the number of U.S. entities registered under the CSA to grow (manufacture) cannabis to supply researchers on the effectiveness of medical grade cannabis in treating these and other maladies.

The CSA under subsection 823(a)(1) provides, DEA is obligated to register only the number of bulk manufacturers of a given schedule I or II controlled substance that is necessary to “produce an adequate and uninterrupted supply of these substances under adequately competitive conditions for legitimate medical, scientific, research, and industrial purposes.”

The policy statement (Federal Register Vol. 81) provided additional explanation on how the DEA would evaluate applications for such registration consistent with the CSA and the obligations of the United States under the applicable international drug control treaty. The Company had reviewed these guidelines and believed all applicable requirements which could not be met by the Company alone would be met by the following:

| ● | Our previous Cannabis Pilot Agreement and completed technology trials with Canopy Growth Corporation, a Canadian licensed producer under the Marihuana for Medical Purposes Regulations, had demonstrated that our aeroponic technology could augment and improve the quality and production of cannabis for use in cannabis research. | |

| ● | We believed that the proposed combination with Alamo and the joint venture with Vyripharm Enterprises, LLC, in which the Company would have an equity interest due to its combination with Alamo, would meet all the additional guidelines and conditions set forth regarding the expected required experience in handling of a controlled substance and its related research with cannabis for pharmaceutical use that is one of the conditions of the policy statement. |

Voluntary Default of Joint Venture and Status of Application with DPS

As published in the Texas Department of Public Safety (“DPS”) Self-Evaluation Report, on page 543, question (D), dated September 29, 2017, the DPS originally interpreted the statute as requiring a market-based system by which the number and location of licensees are determined by market factors rather than by regulation – as not mandating or limiting the number of licensed distributors. It was originally understood that the applicants would be required to satisfy certain basic requirements prior to licensure, and the ability to maintain compliance with DPS guidelines will be evaluated through on-going audits and inspections.

In late 2016, the DPS modified its approach to restrict the number of licenses to three. This necessitated the development of a competitive review process, where three applicants were conditionally approved based on the review of the submitted application materials. Upon successful onsite inspection of their facilities, qualified applicants will be issued licenses. Because of this competitive review process, the Joint Venture group placed 16th out of 43 applicants and its application is currently considered pending by the DPS.

On June 30, 2017, the Company, Alamo CBD and Vyripharm entered into discussions to amend and extend the payment terms under the Joint Venture Agreement due to the group not being awarded one of the three initial provisional licenses to produce cannabis in Texas under the TCUP.

On August 7, 2017, after negotiations, the Company advised Vyripharm that it intended to voluntarily default on the Joint Venture Agreement and the Company wrote off the $250,000 down payment towards the Joint Venture investment and there is no further obligation by either party under the terms of the Joint Venture. The Company’s management determined that without a license to produce cannabis, the Company would not be able to fully utilize the intent of the Joint Venture partnership and the Company would be financially burdened by the ongoing Joint Venture terms. Both parties agreed that this decision would not impair either party’s ability to pursue a Joint Venture in the future, after the Company, or Alamo CBD, obtained license to produce cannabis. Should the Company voluntarily default on the Joint Venture, the agreement would terminate and neither party would have further obligation to the other.

The Company is a member and is working with the Medical Cannabis Association of Texas and expects both lobbying and legislative efforts currently being undertaken to result in the program being expanded, additional permits being awarded, and new legislation being introduced in 2019 to allow for a separate permitting process to conduct cannabis research in line with the CSA. There is no guarantee that these efforts will result in the Company obtaining a license or permit to produce cannabis in Texas or that legislation will be adopted allowing a separate licensing or permitting process for research purposes.

Our Current Product Portfolio

The Company designs fully integrated controlled environment facilities technology for the cannabis industry that enables the manipulation of the plants environment to influence the phenotypic expression of the plant. This precision agriculture technology will be critical to developing true pharma grade cannabis and real personalized cannabis medicines. Our integrated controlled environment facility design includes our patent pending high pressure aeroponics, patent pending HVAC system design, leading LED lighting technology, in addition to a variety of sensors and control technologies.

The Company has developed and maintains a portfolio of equipment designs to include the Company’s patent pending high pressure aeroponic designs as well as flood and drain and floating raft designs. On August 4, 2017, the Company ceased all direct operations within the vertical farming industry. The Company intends to sell its portfolio of vertical farming designs through third party reseller agreements. The Company currently has pending agreements under the terms of the merger agreement with Alamo CBD to resell the Company’s products by Civic Farms, LLC and Bright Orchard Developments, Ltd. No agreements have been executed as of the date of this filing. The Company has also begun early stage discussions with additional groups to resell the Company’s products. There is no guarantee the Company will be successful in securing licensing or reseller agreements. Below is a brief description of the Company’s products.

The Indoor Harvest® Modular HP-Aeroponics Platform

The system comprises of seven primary fixture components that consist of an Aeroponic Growth Tray (“AGT”), Aeroponic Growth Lid (“AGL”), Aeroponic Spray Manifold (“ASM”), Aeroponic Pressure Manifold (“APM”), Nutrient Delivery System (“NDS”), Water Reclamation and Recirculation System, and Lift Station. The combination of an AGT, AGL and ASM is known as an “HPA Table”. The combination of an APM and NDS is known as a “Nutrient Pump Skid”. Each of these individual modular fixtures are combined to create custom configurations suitable for any form of indoor growing environment.

4

Initially designed to produce leafy greens, micro-greens, fruiting plants and herbs, our fixtures can be easily adapted for a variety of other uses, such as horticultural research, medicinal plant production, plant cloning and hardwood propagation. A smaller version of our basic design was utilized at MITCityFarm and our larger system has been independently tested by Canopy Growth Corporation. The results of these and the Company’s own internal trials has shown the following benefits over a more traditional hydroponic system:

|

● Up to a 95% reduction in water usage | |

| ● Up to a 70% reduction in fertilizers | ||

| ● Accelerated growth rate | ||

| ● Increased plant biomass | ||

| ● Increased phytochemical content | ||

| ● Elimination of growing mediums | ||

| ● Sterile production |

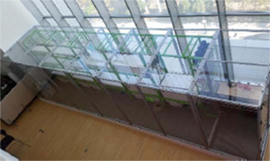

| Below are pictures of the Company’s HPA Table’s and Nutrient Pump Skid being installed at Tweed Marijuana, Inc., a subsidiary of Canopy Growth Corporation: | ||

|

|

|

The Indoor Harvest® Low Tide VFRack™ Platform

The Low Tide VFRack platform is an easy to install, commercial quality vertical farming system designed to produce microgreens, leafy greens and herbs. Each Low Tide VFRack™ System comes standard with 4 levels offering up to 128 sq. ft. of production or can support up to 18 individual 10”X20” trays per layer.

The system uses Botanicare 4ft X 8ft ID Low Tide Grow Trays and a 115 gallon or larger reservoir. Each unit comes complete with all pumps, plumbing, LED lighting and is ready to grow, just add plants and nutrients. The modular nature of the system allows for easy expansion. The Low Tide VFRack system is designed specifically for flood and drain operation and provides the following benefits:

|

● Integrated LED lighting | |

| ● Open slot face to accommodate unlevel floors | ||

| ● Plug and play installation | ||

| ● Reduced installation costs | ||

| ● Unistrut based platform |

| Below are pictures of the Company’s Low Tide VFRack platform that were installed at Moon Flowers Farms. |

|

|

The Indoor Harvest® Shallow Raft VFRack™ Platform

The Shallow Raft VFRack™ platform is an easy to install, commercial quality, shallow raft vertical farming system. Each Shallow Raft VFRack™ System comes standard with three levels, offering 216, 336, 432 and 864 plant sites. The system uses Botanicare 4ft X 8ft ID Grow Trays, 115 gallon or larger reservoir and 2ft X 4ft rafts and is designed for the production of leafy greens and herbs.

Each unit comes complete with all pumps, plumbing, LED lighting and is ready to grow, just add plants and nutrients. The modular nature of the system allows for easy expansion.

5

The Shallow Raft VFRack system is designed specifically for floating raft operation and provides the following benefits:

|

● Integrated LED lighting | |

| ● Open slot face to accommodate unlevel floors | ||

| ● Plug and play installation | ||

| ● Reduced installation costs | ||

| ● Unistrut based platform |

Below are pictures of the Company’s Shallow Raft VFRack:

|

|

Design-Build, Engineering, Procurement and Construction Services

On August 4, 2017, the Company ceased all outside Design-Build, Engineering Procurement and Construction (“DBEPC”) services for the Vertical Farming industry. The Company is currently in discussions with third party companies to handle the Company’s future DBEPC needs in the Cannabis industry. As part of our proprietary intellectual property and industry knowledge, we plan to continue to be actively involved in the design phase of these projects. Therein lies some of our core expertise and competitive advantage. No agreements have been executed and there is no assurance such agreements will be consummated.

Financing for Products and Services

On December 14, 2015, we entered into an agreement with Noesis, a financing provider for sellers of commercial building improvements, to provide financing programs for our products and services. Under the agreement, the Company would be provided access to multiple Noesis lenders that support lease/loan vehicles tailored for HVAC, lighting and controls, building equipment, municipalities and specialty projects. In addition, the Company was provided loan/lease vehicles for solar, energy service agreements and PACE vehicles. The Noesis platform provided a back-end proposal and quoting support system that integrates into the Company’s client sales platform. Due to the Company’s changes in business focus, the Company ceased offering financing through Noesis on August 4, 2017.

Operational Activities

Design Partnership with Freight Farms

On December 17, 2015, we entered into a design partnership with Freight Farms to jointly explore new cultivar platforms. Freight Farms, makers of the Leafy Green Machine shipping container farms, would leverage Indoor Harvest’s unique expertise as the leading design-build firm of indoor farms to explore innovative new applications for its Leafy Green Machine. Freight Farms launched in 2010 to create a more sustainable and connected food system by creating highly sustainable farms in shipping containers.

The companies planned to work together to explore how Freight Farms’ containerized approach to indoor farming could be deployed in new ways to reach into untapped markets, including those internationally, as well as applications for non-profits and pharmaceutical research. Freight Farms is already deployed by academic institutions, restaurants, wholesale produce distributors and small business owners. No projects ever materialized from this agreement and due to changes in the Company’s business as of August 4, 2017, no future projects are expected to be initiated.

MOA with IGES Canada Ltd.

On January 27, 2016 the Company entered into a Memorandum of Agreement (“MOA”) with IGES Canada Ltd. (“IGESCA”), a Canadian company that is a technology solution integrator in the vertical farming market. The MOA sets forth terms for a relationship between the Company and IGESCA to grow, market and sell vertical farming solutions globally.

Subject to the terms of the MOA, IGESCA and Indoor Harvest agreed to partner to market and sell Indoor Harvest’s solutions in conjunction with the IGESCA business platform to clients globally. Our responsibilities included delivering turnkey engineering, procurement and construction solutions for CEA facilities, ongoing support and access to financing options through Noesis for designated projects. The responsibilities of IGESCA include identifying new and concluding project engagements from the current potential portfolio of 15 facilities, ongoing operations and regulatory navigation.

Both Indoor Harvest and IGESCA agreed that any intellectual property, which was jointly developed and filed through activities covered under the MOA, could be used by either party for sales/marketing purposes with the consent of the other party which was to be set forth in initial guidance. All other intellectual property used in the implementation of the MOA would remain the property of the party that provided it. This property could be used by either party for purposes covered by the MOA but consent would be obtained from the owner of the property before using it for purposes not covered by the MOA. The MOA was to remain in effect for a period of three (3) years from the date of signing unless earlier terminated.

6

On July 13, 2016, we entered into a DBEPC, maximum guaranteed price agreement, for a 40,000 sq. ft. vertical farm project in Johnstown Ontario with IGESCA. The project was estimated at $11,374,500 with 5% of the total, $568,725 due upon the start of design work. Originally contracted to begin work on September 23, 2016, the project continued to run into delays and IGES was unable to secure funding for the project. On August 4, 2017, the Company ceased all efforts to support IGESCA projects due to changes in the Company’s business plans, to include five other pending projects which included Welland, Tyendinaga, Kingston, Galipeau and Easton.

TexAg Ventures, LLC

On July 27, 2016, we entered into a DBEPC, cost plus agreement, with TexAg Ventures, LLC, to provide full design and engineering, system prototyping and system testing of a custom vertical farming platform. An initial deposit of $35,000 was required to begin prototyping. Design and engineering services were to be provided free and remaining project costs would be deemed construction coordination services and billed at cost plus. As of September 30, 2016, 100% of the design work had been completed but the client had not provided the required deposit to begin prototyping. On August 4, 2017, we ceased efforts to support the project due to changes in the Company’s business plans.

Head North Agreement

In the Company’s initial effort to separate its cannabis and produce operations, on August 22, 2016 we entered into a memorandum of agreement with Head North LLC (“Head North”) to provide Head North with an exclusive period to negotiate an acquisition, merger, or joint venture, of our cannabis related operations in exchange for certain funding obligations.

On September 2, 2016, the Company received an executed subscription agreement for $375,000 of our Series A Preferred shares related to the terms outlined in our MOA. On September 23, 2016, we issued 30-day notice to Head North that we were terminating the agreement under Section VIII due to default under the terms of the MOA and a failure to fund its subscription.

Current Operations

On May 31, 2017, the Company notified Canopy Growth that it had completed the majority of work under Phase Two of its Cannabis Pilot. The Company installed 13 HPA Table systems and 1 custom built Nutrient Pump Skid at Canopy Growth for an internal economic pilot. During Phase Two, the Company submitted proposals to Canopy Growth for three designs for potential New IP development. Canopy Growth did not pursue these proposals to develop New IP and chose to procure only the Company’s HPA Table system and a custom built Nutrient Pump Skid that was integrated into existing fertigation and mechanical systems at Canopy Growth. As a result of integration into existing facilities, the Company provided Canopy Growth with a limited warranty. The Company additionally informed Canopy Growth that it would not seek continued development under the Cannabis Pilot. As a result, the Cannabis Pilot expired on December 18, 2017.

On July 10, 2017, Indoor Harvest Corp. entered into a Cultivation Design Agreement with Bright Orchard Developments, Ltd., for the design of an aeroponic cannabis production facility by a pending licensed producer in Canada.

On October 11, 2017, the Company entered into a binding letter of intent (“LOI”) with Zoned Properties outlining three pending independent agreements to complete research and development projects for licensed medical cannabis facilities to be located in Tempe, Arizona, Parachute, Colorado and Stockdale, Texas or other location to be determined after approval of a provisional license under the TCUP. Zoned Properties is an OTCQX quoted Company and strategic real estate development firm whose primary mission is to identify, develop, and lease sophisticated, safe, and sustainable properties in emerging industries, including the licensed medical cannabis industry.

Under the terms of the binding LOI, the two companies plan to work together to mutually agree upon terms, provisions and obligations of three simultaneous, independent agreements.

| ● | Tempe Arizona Research Cultivation Site – an agreement for the development and installation of a research cultivation site utilizing Indoor Harvest’s cultivation technology and equipment within at most 2,500 square feet of space at Zoned Properties’ Tempe Medical Marijuana Business Park. | |

| ● | Parachute Colorado Production Facility – an agreement for the development and operation of Zoned Properties’ Parachute Medical Marijuana Business Park and for Indoor Harvest to engage Zoned Properties as the exclusive Strategic Development Advisory. | |

| ● | Texas Compassionate Use Program Applicant – an agreement for Indoor Harvest to engage Zoned Properties as the exclusive Strategic Development Advisory for Indoor Harvest’s anticipated future development located in Stockdale, Texas or at another location to be determined. |

Execution of any of the three individual agreements is subject to, among other things, satisfactory due diligence and the negotiation and execution of definitive agreements, each of which will contain customary representations, warranties, covenants and closing conditions. There is no assurance that any or all of the agreements will be executed nor consummated.

The binding LOI includes non-refundable payments totaling $50,000 by Indoor Harvest to Zoned Properties. The payments are consideration for entering into the binding LOI and represents a 20% deposit to be applied towards the assignment of the Parachute Development Rights which have been valued at $250,000 within the binding LOI.

On October 26, 2017, the Company entered into a LOI with Harvest Air, LLC (“Harvest Air”) and on November 1, 2017, entered into a LOI with Biological Innovations and Optimization Systems, LLC (“BIOS Lighting”). The two companies plan to collaborate with Indoor Harvest towards the development of a fully integrated platform designed to provide cannabis producers the ability to manage and record phenotypic plasticity in the cannabis plant. By combining Indoor Harvest’s proven aeroponic methods, Harvest Air’s HVAC designs, and customized lighting solutions from BIOS Lighting, the three Companies plan to demonstrate an ability to manipulate and control phenotypic expression in the cannabis plant for the purpose of research and production of pharmaceuticals.

In addition to collaborative research and development, the group plans to develop advanced automation strategies to control the growth of cultivars with high pressure aeroponics by integrating power generation, HVAC, LED lighting systems, phytometric devices, and near-infrared technologies, into a fully integrated facilities package. By using real time measurements of plant physiological processes and precision management of the production facility environment, the group intends to offer scalable solutions and production methods designed specifically for cannabis phytochemistry and precise phytochemical production.

7

Prototype development will take place in Tempe, Arizona, as part of Indoor Harvest’s planned cannabis technology development described below. In exchange for Harvest Air and BIOS Lighting support and services, Indoor Harvest has agreed to exclusively utilize any developed hardware or strategies provided by both companies in its future developments in Parachute, Colorado and Stockdale, Texas, or other location in Texas approved under the TCUP as described in more detail below.

Tempe Arizona Research Cultivation Site

The Company plans to install 20 HPA Tables at an existing licensed medical cannabis production facility at Zoned Properties’ Tempe Medical Marijuana Business Park. The purpose of this project is to conduct a demonstration of the Company’s aeroponic technology while integrating LED and HVAC designs, provided by BIOS Lighting and Harvest Air, respectively. The resulting demonstration will be compared to traditional flood irrigation, HVAC and lighting methods. The Company plans to prepare a case study and white paper to showcase industry adoption value and to serve as a proof of concept for the construction of larger facilities in Parachute, Colorado and Stockdale, Texas, or other location in Texas approved under the TCUP.

Both Zoned Properties and Indoor Harvest plan to work together in good faith to mutually agree upon the terms, provisions and obligations of an agreement for the development, installation, and research of Indoor Harvest’s cultivation technology and equipment within at most 2,500 square feet of space at Zoned Properties’ Tempe Medical Marijuana Business Park located at 410 S. Madison Dr. Tempe, Arizona 85281. The Company expects to generate revenue from the Tempe, Arizona facility through future leasing and licensing agreements. The 20 HPA Table installation is expected to produce over 206 pounds of cannabis annually at under $150 per pound in cost of goods with an expected breakeven point of 430 pounds for the equipment. There is no assurance that any or all of the agreements will be executed nor consummated.

Parachute Colorado Production Facility

The Company has secured rights to develop Zoned Properties Parachute Medical Marijuana Business Park. The Company intends to construct a 25,000 square foot facility based on the technology developed and tested at the Tempe Arizona Research Cultivation Site and to generate revenue through the leasing of the facility and licensing of the Company’s technology to either a medical or recreational licensee, which has yet to be determined. The Company would additionally conduct research and development towards creating specific environmental and climate recipes for the production of cannabis in order to produce and replicate a desired phenotypic response. The Company also expects to file an application with the DEA to register the facility under the CSA and to obtain rights to acquire the operating license from the licensee upon changes in Colorado law, which currently does not allow direct ownership by a publicly traded Company.

Both Zoned Properties and Indoor Harvest plan to work together in good faith to mutually agree upon the terms, provisions and obligations of an agreement for the assignment and/or sale of Zoned Properties’ Parachute Development Rights for the Parachute Marijuana Business Park located at Lot #7 N. Diamond Loop Rd, Parachute, Colorado 81635. The agreement would include: (a) the assignment and/or sale of the Parachute Development Rights from Zoned Properties to Indoor Harvest, and (b) the engagement by Indoor Harvest of Zoned Properties as the exclusive Strategic Development Advisor for the Parachute Property. The Company has paid a $25,000 deposit towards securing these rights. There is no assurance that any or all of the additional agreements will be executed or that the Company will be successful in registering the facility with the DEA.

Texas Compassionate Use Program Applicant

We, through our wholly owned subsidiary Alamo CBD, have applied to produce and dispense low-THC cannabis under the TCUP. The Company plans to partner with Zoned Properties, Harvest Air and BIOS Lighting to develop a 50,000 square foot facility in Stockdale, Texas or other location to be determined after approval of a provisional license under the TCUP. Zoned Properties and Indoor Harvest will work together in good faith to mutually agree upon the terms, provisions and obligations of an Agreement for Indoor Harvest to engage Zoned Properties as the exclusive Strategic Development Advisory for Indoor Harvest’s development in Texas under the TCUP. The Company also expects to file an application with the DEA to register the facility under the CSA. The Company expects to generate revenue through the production and sale of cannabis under the TCUP. There is no assurance that any or all of the agreements will be executed or that the Company will be successful in obtaining a license to produce cannabis in Texas or in registering the completed facility with the DEA.

As published in the Texas DPS Self-Evaluation Report, on page 543, question (D), dated September 29, 2017, the DPS originally interpreted the statute as requiring a market-based system by which the number and location of licensees are determined by market factors rather than by regulation – as not mandating or limiting the number of licensed distributors. It was originally understood that the applicants would be required to satisfy certain basic requirements prior to licensure, and the ability to maintain compliance with DPS guidelines will be evaluated through on-going audits and inspections.

In late 2016, the DPS modified its approach to restrict the number of licenses to three. This necessitated the development of a competitive review process, where three applicants were conditionally approved based on the review of the submitted application materials. Upon successful onsite inspection of their facilities, qualified applicants will be issued licenses. Because of this competitive review process, Alamo CBD placed 16th out of 43 applicants and its application is currently considered pending by the DPS. The Company and other pending applicants have questioned the last-minute modification in approach by the DPS and the lack of transparency in the reviewing process.

The Company is a member of and is working with the Medical Cannabis Association of Texas and expects both lobbying and legislative efforts currently being undertaken to result in the program being expanded, additional permits being awarded, and new legislation being introduced in 2019 to allow for a separate permitting process to conduct cannabis research in line with the CSA. There is no guarantee that these efforts will result in the Company obtaining a license or permit to produce cannabis in Texas or that legislation will be adopted allowing a separate licensing or permitting process for research purposes.

8

Research and Development

MIT CityFarm (MIT OPenAg)

On September 18, 2013, the Company entered into a Letter Agreement for the Transfer of Materials (“MIT Agreement”) with the Massachusetts Institute of Technology in response to a MIT Media Lab request for aeroponic system components and fixtures manufactured by Indoor Harvest to be used for the purpose of developing a wall facade aeroponic and hydroponic system, also known as the “Food Server”, as part of MIT’s Media Lab “Changing Places” project (“MITCityFarm”). Indoor Harvest was responsible for providing technical assistance and materials as a “Technical Systems Adviser”. Per the Company’s role as a Technical Systems Adviser, the Company was exposed to research that showed the potential for using aeroponics, LED lighting, controlled environments and sensor technologies in the development of environmental and climate recipes to achieve a specific phenotypic response of cultivars.

On March 14, 2017, the Company ceased all support for the MIT OpenAg Initiative, formerly MITCityFarm, due to previous decisions by MITCityFarm principals, in which the terms of the MIT Agreement were not honored due to concerns over the Company’s involvement with cannabis. The MIT Agreement required the acknowledgement by MITCityFarm, of the use of any source materials, such as the Company’s aeroponic designs, in any publications reporting its use. The MIT Agreement was incorporated as exhibit 10.2 of the Company’s Form S-1 filing made with the SEC on March 5, 2014.

| Below are pictures of the Company’s installation of aeroponic and hydroponic systems at MITCityFarm: | ||

|

|

|

Canopy Growth Cannabis Pilot

Based on knowledge gained while working with MITCityFarm, the Company saw a business opportunity to use the Company’s technology and methods within the cannabis industry. On December 18, 2014, the Company entered into a Cannabis Production Pilot Agreement (“Cannabis Pilot”) with Canopy Growth Corporation (formerly Tweed Marijuana Inc.), a Canadian company. Canopy Growth Corporation (“Canopy Growth”) is a Toronto Stock Exchange listed company. Its wholly owned subsidiaries Tweed Inc., Tweed Farms Inc. (formerly Prime1 Construction Services Corp.), Bedrocan Canada and Spectrum Cannabis are licensed producers of medical cannabis in Canada. The principal activities of Canopy Growth are the production and sale of cannabis through its wholly owned subsidiaries as regulated by the Marihuana for Medical Purposes Regulations. The Cannabis Pilot was broken into two separate phases, as follows:

| ● | During Phase One, tests were conducted using prototypes provided by Indoor Harvest. The purpose of Phase One was to test the initial design and evaluate the root mass development of various strains of cannabis chosen by Canopy Growth. Two trials were conducted during Phase One. Phase One recorded the growth rate, phytocannabinoid production, water usage, fertilizer usage and labor using the aeroponics systems provided by Indoor Harvest. | |

| ● | During Phase Two, Canopy Growth was given the option to request Design Build services to be provided by Indoor Harvest. Indoor Harvest provided these services free of charge and provided projected costs associated with the manufacture and installation of new aeroponic designs (“New IP”). Canopy Growth was then provided the option to purchase equipment from Indoor Harvest based on these projected costs. |

Phase One Cannabis Pilot

Trial 1: Strain Ghost Train Haze

In March 2015, we began a first trial under the Cannabis Pilot. A Cannabis Sativa dominant strain, Ghost Train Haze, was selected and 8 plants were grown in a 64-cubic foot root chamber HPA Table prototype using a “Screen of Green” cultivation method, in which plants are cropped and trained to produce a higher yield from a single plant. The initial Cannabis Pilot utilized 1040 watts of illumitex® brand LED lighting using the F3 Spectrum and 2,000 watts of Mogul based HPS lighting. The system was operated drain to waste, in which no water was recirculated or recaptured. The following results were recorded under the initial Cannabis Pilot.

| ● | An increase of up to 91% in average dry yield under HPS lighting when compared to the existing average. |

| ● | An increase of up to 71% in average dry yield under LED lighting when compared to the existing average. |

| ● | An increase of up to 117% in liters of water per day/plant under HPS lighting. |

| ● | An increase of up to 183% in liters of water per day/plant under LED lighting. |

| ● | A decrease of up to 21% in nutrient use under HPS lighting and no change under LED lighting. |

Trial 2: Strain UK Cheese

In December 2015, we began a second trial under our Cannabis Pilot with Canopy Growth and similar results were achieved confirming the initial trial results. The second trial utilized an increased plant count of 20 plants per HPA Table prototype and the strain selected was UK Cheese, a Cannabis Sativa and Cannabis Indica hybrid. The second trial also tested root mass differences between a prototype 64 cubic foot and a 32-cubic foot root chamber. The second trial utilized 1040 watts of illumitex® brand LED lighting using the X5 Spectrum and 2,000 watts of Double Ended based HPS lighting and used a “Screen of Green” cultivation method. The following results from the second trial were recorded:

| ● | An increase of up to 86% in average dry yield under HPS lighting when compare to the existing average. |

| ● | An increase of up to 25% in average dry yield under LED lighting when compared to the existing average. |

9

| ● | An increase of up to 89% in liters of water per day/plant under HPS lighting. |

| ● | An increase of up to 70% in liters of water per day/plant under LED lighting. |

| ● | A decrease of up to 69% in nutrient use under HPS lighting and 72% decrease under LED lighting. |

Trial 1 and 2 Summary

Indoor Harvest provided minimal instructional input during both trials. The Company believes the results of the Cannabis Pilot show the potential for the Company’s technology and that without any significant instructional support, operators can achieve significant gains in yield and reductions in costs. There was a noticeable difference recorded in the morphology of the Cannabis strains tested utilizing the Company’s aeroponic platforms over the baseline using drip irrigation and a coco medium. During the first trial, the strain tested showed a significant increase in the size of the plants fan leaves over the baseline methods leading to a potential increase of up to 150% in produced biomass.

The aeroponic systems provided showed a significant increase in growth rate during the vegetative stage, as compared to baseline methods. Additionally, there were noticeable differences in the development of roots under certain conditions and difference we’re recorded in phenotypic response. The results of both trials showed an ability to provide greater control over the root environment, provided an ability to monitor nutrient uptake, provided an increase in yield, showed a dramatic decrease in nutrient use and provided an ability to prevent contamination by eliminating mediums. The Company believes that with further development of additional automation, integration of LED, HVAC and controls that we can continue to improve on the performance of the Company’s technology and methods. All trials were conducted using primarily a drain to waste configuration in which system runoff was not recaptured or recycled.

Phase Two Cannabis Pilot

On July 6, 2016, we entered into Phase Two of our Cannabis Pilot with Canopy Growth Corporation and signed a design-build, DBEPC, cost plus contract with Tweed, a subsidiary of Canopy Growth, to construct a high Pressure Aeroponic production system.

On May 31, 2017, the Company notified Canopy Growth that it had completed the majority of work under Phase Two of its Cannabis Pilot. The Company installed 13 HPA Table systems and 1 custom built Nutrient Pump Skid at Canopy Growth for an internal economic pilot. The Company submitted proposals to Canopy Growth for three designs for potential New IP development under the Cannabis Pilot. Canopy Growth did not pursue these proposals and chose to integrate the Company’s HPA Table fixtures and a custom-built Nutrient Pump Skid into previously existing facility fertigation and mechanical systems at Canopy Growth. This integration further proved the Company’s fixture-based design allowing for custom installations based on an operator’s specifications. Canopy Growth has ongoing rights to purchase additional equipment from Indoor Harvest through a fixed cost plus agreement but is under no obligation to do so. The Phase Two Cannabis Pilot expired December 18, 2017.

| Below are pictures from Phase One and Phase Two of the Company’s Cannabis Pilot with Canopy Growth. | ||

|

|

|

Tempe Arizona Demonstration Pilot

The Company has entered into letters of intent with Harvest Air and BIOS Lighting to collaborate with Indoor Harvest toward the development of a fully integrated platform designed to provide cannabis producers the ability to manage and record phenotypic plasticity in the cannabis plant. By combining Indoor Harvest’s proven patent pending aeroponic methods, Harvest Air’s patent pending HVAC designs, and patented lighting solutions from BIOS Lighting, the three companies plan to demonstrate an ability to manipulate and control phenotypic expression in the cannabis plant for the purpose of research and production of pharmaceuticals and to design modular facility infrastructure.

In addition to collaborative research and development, the group plans to develop advanced automation strategies to control the growth of cultivars with high pressure aeroponics by integrating power generation, HVAC, LED lighting systems, phytometric devices, and near-infrared technologies, into a fully integrated facilities package. By using real time measurements of plant physiological processes and precision management of the production facility environment, the group intends to offer scalable solutions and production methods designed specifically for Cannabis phytochemistry and precise phytochemical production.

Prototype development is planned to take place in Tempe, Arizona, as part of Indoor Harvest’s planned partnership with Zoned Properties. In exchange for Harvest Air and BIOS Lighting support and services, Indoor Harvest has agreed to exclusively utilize any developed hardware or strategies provided by the partners in developments at Parachute, Colorado and Stockdale, Texas, or other location in Texas approved under the TCUP.

Research and development expenses were $6,376 for the year ended December 31, 2017, and $16,184 for the year ended December 31, 2016.

Intellectual Property

The Company relies on a combination of patent law, trademark laws, trade secrets, confidentiality provisions and other contractual provisions to protect our proprietary rights, which are primarily our brand names, product designs and marks.

The Company’s primary trademark is “Indoor Harvest.” This trademark was registered (Registration. Number 4,795,471) in the United States on August 18, 2015. This registration will stay active as long as the Company continues to use the trademark in commerce. A declaration of “continued use” of the trademark under 15 U.S.C. § 1058 is due after February 18, 2021 and before February 18, 2022. An optional declaration of “incontestability” of the trademark, which makes the validity of the trademark harder to challenge by competitors or infringers, is also planned to be filed under 15 U.S.C. § 1065 after Feb. 18, 2021 and before February 18, 2022.

10

The Company filed a patent application (Serial Number 14/120,275) with the United States patent office related to an invention titled: “modular aeroponic system and related methods.” The inventor is Chad Sykes, our sole Founder and Chief of Cultivation, who assigned the patent application to the Company. The application has priority to May 14, 2013. The Company and the patent office have exchanged correspondence on several occasions related to the scope of the patent rights requested.

The Company filed a continuation patent application, in the first quarter of 2018, based on the most recent correspondence from the patent office. In that action, the patent office asked the Company to justify the patentability of its invention over several prior art references in related technology fields. The Company prepared a response, through its intellectual property counsel, Buche & Associates, P.C. While the patent application is still under review, the Company continues to use the term “patent pending” on all published materials related to the invention. There is no guarantee that a patent will be granted.

Plan of Expanded Operations

Our plan of expanded operations for the next 12 months, assuming we secure the necessary funding, is set forth in “Liquidity and Capital Resources” section below.

Sales and Marketing

We intend to offer our products through licensing and reseller agreements. We are currently developing our marketing plans for both production and technology sales, which may include some or all of the following marketing methods:

| ● | Internet and Social Media. - Allows us to build an online presence, community and engage with our Industry Peer Groups |

| ● | Internet Mail - The use of online mail campaigns allows us to build a database of subscribers to reach a broader audience within targeted markets. A direct online campaign may consist of a letter of introduction and monthly newsletters. |

| ● | Marketing materials which will include a brochure highlighting our company featuring our products and services. |

| ● | Trade Shows and Special Events - We intend to participate in industry trade shows and events in order to create market awareness for its products and services. We may also cross promote, co-brand and sponsor key conferences and other industry events as relevant and appropriate. |

Marketing our products in the U.S. in state and local jurisdictions where cannabis is legal is still uncertain due to the uncertain legal status of the growth, sale and use of cannabis due to conflicting laws under which what is illegal federally is to varying extents legal under certain state laws to the contrary, and even greater uncertainty as to what would constitute ancillary illegal activities such as aiding or abetting if any such direct actions are deemed illegal. The Company cannot predict with any accuracy whether even if direct illegality laws were enforced, whether any ancillary related laws such as aiding and abetting would, if ever, be enforced. If such laws are enforced this could adversely affect the Company’s planned and current operations.

Competition and Market Position

Vertically Integrated Companies

Broadly speaking we compete with vertically integrated technology companies seeking to produce pharma grade cannabis for research and development of new personalized medicines. Companies in this space would include some of the current global players like Canopy Growth and Aurora along with smaller players like Surna, Terra Tech and GB Sciences.

Production Competition

There are a number of companies seeking to take the development and manufacture of pharmaceutical grade cannabis to the next level and they would certainly be considered competitors. These companies would include Bedrocan, CanniMed, BOL Pharma, and Sira Naturals.

Since 1968, the University of Mississippi has been the sole registered producer of cannabis and its constituents under the CSA. Working under a contract with the National Institute on Drug Abuse (“NIDA”), University of Mississippi supplies cannabis and its constituents to the NIDA Drug Supply Program, which is the sole source supply of cannabis used by researchers to study its potential harmful and beneficial effects. However, certain members of the scientific community have questioned the standards employed by University of Mississippi. In a 2017 PBS NewsHour report, the quality of the University of Mississippi’s cannabis was questioned, and the report contained accusations of mold contamination and that in some instances, cannabis tested positive for lead. The University of Mississippi produces cannabis primarily on a 12-acre outdoor farm, under direct sunlight, exposed to the elements, with no ability to control environmental or climate related impact of phenotypic response.

Cannabis contains over 113 cannabinoids and over 200 terpenes, as well as hundreds of other chemical compounds. In 1998, research conducted by S. Ben-Shabat and Raphael Mechoulam, introduced the phrase “Entourage Effect” to cannabinoid science. The Entourage Effect represents a novel endogenous cannabinoid molecular route. This new scientific discovery opens up the ability to provide whole plant and whole person caregiver synergy treatments over isolated compound pharmacological dosages. Other cannabinoids and terpenes that contribute to the clinical effects of cannabis have been espoused as an Entourage Effect.

The Entourage Effect is a combination of chemicals produced through the phenotypic response of cannabis. Phenotypic response, while governed by the specific genotype, can be manipulated and altered by changes in the environment and climate selected during production. It is therefore known, that precise control over both the environment and climate conditions can produce specific, and consistent phenotypic response in cannabis. Indoor Harvest has developed tested and proven technology and methods through the use of Building Integrated Agriculture that can allow such precise control over environmental and climate conditions. This allows Indoor Harvest to produce a superior quality and consistent Entourage Effect over the production methods of the University of Mississippi and provides researchers another pathway for discovery by providing an ability to develop specific phenotypic response specific to the research being conducted. The Company believes this provides a competitive advantage and offering currently not being provided to cannabis researchers or developers of cannabis medicines.

11

Technology Competition

There are two companies that currently manufacture high pressure aeroponic systems, Agrihouse™ and Aerofarms™. These companies are currently engaged in the manufacture and sales of commercial aeroponic vertical farming systems for produce production and have had limited or no use in the cannabis industry. These systems can only be used in a single mode with high pressure aeroponics and offer limited sizing options. Our system is capable of operating in dual modes, both low pressure and high pressure, and our aeroponic system is available in optional sizes that our competitors currently do not offer. There are also companies such as general Hydroponics® and Botanicare® that manufacture aeroponic and hydroponic growing systems for the hobbyist. These systems are only available in low pressure aeroponics and require individual reservoirs. They also are offered in limited sizes and are not designed for commercial operation. These systems only provide a single mode of operation.

Additionally, we have one established aeroponic competitor in the cannabis industry, AEssense Corporation. AEssense has developed an aeroponic platform under the brand name AEtrium. The AEtrium is a full system design, which utilizes low pressure aeroponics as opposed to high pressure aeroponics. The AEtrium is a standalone, full system design and not a fixture-based design such that Indoor Harvest has developed. We believe our fixture-based design and facilities approach allows us to develop fully customized installations that our competitors cannot offer.

We will be a small competitor in the industry. Many of our competitors have substantially greater financial, marketing, personnel and other resources than we do. We believe based upon management’s knowledge of the industry that we are the first company to develop and offer a fixture based, fully integrated aeroponic biomanufacturing platform for the cannabis industry. Instead of relying on a product-based design, we have developed individual fixtures that can be used in whole, or in part, to create a variety of modular designs of any scale, or size. By breaking our platform down into individual, independent fixtures, we offer a level of customizability that currently is not offered by our competitors.

Manufacturing