Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE EXCHANGE ACT |

For the transition period from _________ to ________

Commission File No. 000-55127

![]()

| Blue Sphere Corporation | |

| (Exact name of registrant as specified in its charter) | |

| Nevada | 98-0550257 |

|

(State or other jurisdiction of

incorporation or organization) |

(I.R.S. Employer

Identification No.) |

| 301 McCullough Drive, 4th Floor, Charlotte, North Carolina 28262 | |

| (Address of principal executive offices) (zip code) | |

| 704-909-2806 | |

| (Registrant’s telephone number, including area code) | |

| (Former name, former address and former fiscal year, if changed since last report) | |

Securities registered pursuant to Section 12(b) of the Exchange Act of 1934: None.

Securities registered pursuant to Section 12(g) of the Exchange Act of 1934: Common Stock, $0.001 per share.

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | Smaller reporting company | ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $9,739,348.20, based on the closing sales price of the registrant’s common stock as of the last business day of its most recently completed second fiscal quarter. For purposes of calculating the aggregate market value of shares of our Common Stock held by non-affiliates as set forth on the cover page of this Annual Report on Form 10-K, we have assumed that all outstanding shares are held by non-affiliates, except for shares held by each of our executive officers, directors and 10% or greater stockholders. These assumptions should not be deemed to constitute an admission that all executive officers, directors and 10% or greater stockholders are, in fact, affiliates of our company, or that there are no other persons who may be deemed to be affiliates of our company. Further information concerning shareholdings of our officers, directors and principal stockholders is included or incorporated by reference in Part III, Item 12 of this Annual Report on Form 10-K.

As of April 16, 2018, there were 3,977,755 shares of the Registrant’s common stock, par value $0.001 per share (“Common Stock”), issued and outstanding.

TABLE OF CONTENTS

Our audited financial statements are stated in United States Dollars (“U.S. $”, “$” or “USD”) and are prepared in accordance with United States Generally Accepted Accounting Principles (“GAAP”). In this Annual Report, unless otherwise specified, all dollar amounts are expressed in United States Dollars. Any reference to a United States Dollar equivalent is approximate and based on the exchange rate at the time of the referenced transaction.

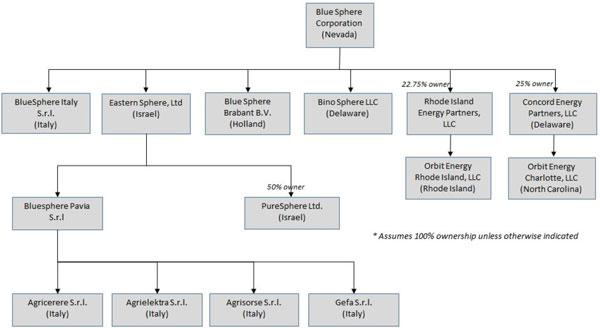

As used in this Annual Report, the terms “we”, “us”, “our”, “Blue Sphere” or the “Company” mean Blue Sphere Corporation and its subsidiaries, unless the context clearly requires otherwise.

Note Regarding Forward-Looking Statements

This report contains forward-looking statements. Forward-looking statements are projections in respect of future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks set out below, any of which may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks include, without limitation, (i) uncertainties regarding our ability to obtain adequate financing on a timely basis including financing for specific projects, (ii) the financial and operating performance of our projects, (iii) uncertainties regarding the market for and value of carbon credits, renewable energy credits and other environmental attributes, (iv) political and governmental risks associated with the countries in which we may operate, (v) unanticipated delays associated with project implementation including designing, constructing and equipping projects, as well as delays in obtaining required government permits and approvals, (vi) the development stage of our business and (vii) our lack of operating history.

This list is not an exhaustive list of the factors that may affect an of our forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on our forward-looking statements.

Forward-looking statements are made based on management’s beliefs, estimates and opinions on the date the statements are made and we undertake no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

1

Company Overview

We are an international Independent Power Producer (“IPP”) that is active in the global clean energy production and waste-to-energy and clean energy technology (“clean-tech”) markets. We aspire to become a key player in these rapidly growing markets by developing or acquiring projects with clean energy technologies, including but not limited to waste-to-energy facilities that generate clean energy, such as electricity, natural gas, heat, soil amendment and other by-products. These markets provide tremendous opportunity, insofar as we believe there is a virtually endless supply of waste and organic material that can be used to generate power and valuable by-products. In particular, the disposal of organic material to landfills in most parts of the world is a costly problem with environmentally-damaging consequences. We seek to offer a cost-effective, environmentally-safe alternative.

Waste-to-Energy and Clean Energy

Waste-to-Energy is the process of generating energy in the form of electricity, natural gas and/or heat from the treatment of various forms of waste. Most waste-to-energy processes produce electricity and/or heat directly through combustion, or produce a combustible fuel commodity, such as methane, methanol or ethanol. Generally, waste-to-energy technology includes the following:

Incineration

Incineration is the combustion of organic material such as waste with energy recovery, and is the most common waste-to-energy implementation. All new waste-to-energy plants in OECD countries (member and partner countries with the Organization for Economic Co-operation and Development) incinerating waste must meet strict emission standards, including those on nitrogen oxides, sulphur dioxide, heavy metals and dioxins. Hence, modern incineration plants are vastly different from the old types of plants, some of which recovered neither energy nor materials. Modern incinerators reduce the volume of the original waste by up to 96%, depending upon composition and degree of recovery of materials, such as metals from the ash for recycling.

Anaerobic Digestion

Anaerobic digestion is a collection of processes by which microorganisms break down biodegradable material in the absence of oxygen. The process is used for industrial or domestic purposes to manage waste or to produce fuels. The digestion process begins with bacterial hydrolysis of the input materials. Insoluble organic polymers, such as carbohydrates, are broken down to soluble derivatives that become available for other bacteria. Acidogenic bacteria then convert the sugars and amino acids into carbon dioxide, hydrogen, ammonia, and organic acids. These bacteria convert these resulting organic acids into acetic acid, along with additional ammonia, hydrogen, and carbon dioxide. Finally, methanogens convert these products to methane and carbon dioxide. The methanogenic archaea populations play an indispensable role in anaerobic wastewater treatments. Anaerobic digesters can also be fed with purpose-grown energy crops, such as maize. Anaerobic digestion is widely used as a source of renewable energy. The process produces a biogas, consisting of methane, carbon dioxide and traces of other ‘contaminant’ gases. This biogas can be used directly as fuel, in combined heat and power gas engines or upgraded to natural gas-quality biomethane. The nutrient-rich digestate also produced can be used as fertilizer.

Gasification

Gasification is a process that converts organic or fossil fuel based carbonaceous materials into carbon monoxide, hydrogen and carbon dioxide. This is achieved by reacting the material at high temperatures (>700 °C), without combustion, with a controlled amount of oxygen and/or steam. The resulting gas mixture is called syngas (from synthesis gas or synthetic gas) or producer gas and is itself a fuel. The power derived from gasification and combustion of the resultant gas is considered to be a source of renewable energy if the gasified compounds were obtained from biomass. The advantage of gasification is that using the syngas is potentially more efficient than direct combustion of the original fuel because it can be combusted at higher temperatures or even in fuel cells, so that the thermodynamic upper limit to the efficiency defined by Carnot’s rule is higher or (in case of fuel cells) not applicable. Gasification can also begin with material which would otherwise have been disposed of such as biodegradable waste. In addition, the high-temperature process refines out corrosive ash elements such as chloride and potassium, allowing clean gas production from otherwise problematic fuels.

Pyrolysis

Pyrolysis is a thermochemical decomposition of organic material at elevated temperatures in the absence of oxygen (or any halogen). It involves the simultaneous change of chemical composition and physical phase, and is irreversible. Pyrolysis is a type of thermolysis, and is most commonly observed in organic materials exposed to high temperatures. It is one of the processes involved in charring wood, starting at 200–300 °C (390–570 °F). It also occurs in fires where solid fuels are burning. In general, pyrolysis of organic substances produces gas and liquid products and leaves a solid residue richer in carbon content, char. Extreme pyrolysis, which leaves mostly carbon as the residue, is called carbonization.

2

There are a number of other new and emerging technologies that can be used to produce energy from waste and other fuels without direct combustion. Many of these technologies have the potential to produce more electric power from the same amount of fuel than would be possible by direct combustion. This is mainly due to the separation of corrosive components (ash) from the converted fuel, thereby allowing higher combustion temperatures in, for example, boilers, gas turbines and fuel cells.

Clean Energy is the process of generating energy from natural and or renewable resources that limit or eliminate pollutants entering the atmosphere. Clean Energy production include electrical generation from sources such as solar, wind, hydro, natural gas and plant-based oils. For example, biofuel engine combined heat and power (CHP) plants use an adapted reciprocating gas engine, depending upon which biofuel is being used, and are otherwise very similar in design to a gas engine CHP plant. The advantage of using a biofuel is one of reduced hydrocarbon fuel consumption and thus reduced carbon emissions. These plants are generally manufactured as fully packaged units that can be installed within a plantroom or external plant compound with simple connections to the site’s electrical distribution and heating systems. Another variant of the above example is a wood gasifier CHP plant, whereby a wood pellet or wood chip biofuel is gasified in a zero-oxygen high temperature environment, resulting in gas that is then used to power a gas engine.

We Build, Own & Operate Projects and We Acquire Projects

Our business model is based on two main activities: we are a Build, Own & Operate (BOO) company, and we are a strategic acquirer of already constructed and operational facilities. Our BOO projects further fall into four primary phases of progress, making up our development cycle as follows:

| 1. | Pre-Development. In this phase, our business development team is evaluating project opportunities that may come from various sources such as: other developers, utility companies, strategic partners and land owners. In this phase, we are conducting site research, evaluating feedstock parameters, researching the availability for offtake agreements and reviewing regulatory issues surrounding a particular location. |

| 2. | Development Phase. In this phase, we begin deploying capital and committing to projects. This phase generally includes the issuance of term-sheets or letters of intent for the development of projects. We begin the formal and in-depth due-diligence process to further these projects. Once due-diligence has been completed and a decision to move forward has been made, the company begins to assemble the various elements of the project. At this time, amongst other processes: technology is selected, an engineering study is completed, development plans are created, third party EPC operators are engaged, deposits are made on properties, environmental studies begin, permitting begins, feedstock agreements are put in place, a power purchase agreement (“PPA”) is agreed to and project financing is sourced. The development phase can take one year or longer depending on the project size and complexity. |

| 3. | Construction Phase. In this phase, we complete a financial closing with our project finance partners and third party EPC and technology providers, the property is officially purchased or leased and a ground breaking occurs. After this site prep begins, materials are ordered, equipment is ordered and construction begins. Over the next year or longer: through our third party contractors, skilled technicians, laborers and managers build an advanced power plant that turns various forms waste into sources of clean energy and other by-products. |

| 4. | Operating Phase. This phase includes the acceptance of waste materials, the ramp-up of biological elements in the case of an anaerobic digester plant, connecting to the electrical and or gas grids or connecting directly to a large end user. Once the connection is in place and the waste ramp-up phase is complete, and through our third party contractors, the plant is now fully operational. In addition to other administrative functions, management or our third party contractors will now begin to maintain feedstock intake, equipment monitoring and maintenance. |

For our acquisition projects, we seek to acquire ongoing projects that are already constructed or operational.

Our Projects in All Phases

We are currently negotiating, developing, constructing or operating, as applicable, twenty (20) projects related to our strategy of acquisition, development or operations of waste-to-energy or clean-tech facilities, which includes developing projects for which we have entered into nonbinding letters of intent to acquire additional biogas facilities in Italy and to develop and construct waste-to-energy or clean-tech facilities in the United States, the Netherlands, the United Kingdom and Israel. We continue to evaluate a pipeline of similar projects in the pre-development phase in the countries listed below and we are also evaluating projects in other countries such as the Czech Republic, Poland, Canada and Mexico.

We currently own, in full or in part, the following operational projects:

United States (operating)

| ● | Charlotte, NC. Waste-to-energy Anaerobic Digester Plant, 5.2 MW (electricity). | |

| ● | Johnston, RI. Waste-to-energy Anaerobic Digester Plant, 3.2 MW (electricity). |

Italy (operating)

| ● | Soc. Agr. AGRICERERE S.r.l. Tromello, Italy. Waste-to-energy Anaerobic Digester Plant, 999 KW (electricity). | |

| ● | Soc. Agr. AGRIELEKTRA S.r.l. Alagna, Italy. Waste-to-energy Anaerobic Digester Plant, 999 KW (electricity). | |

| ● | Soc. Agr. AGRISORSE S.r.l. Garlasco, Italy. Waste-to-energy Anaerobic Digester Plant, 999 KW (electricity). | |

| ● | Soc. Agr. GEFA S.r.l. Dorno, Italy. Waste-to-energy Anaerobic Digester Plant, 999 KW (electricity). | |

| ● | Futuris Papia S.p.A. Udine, Italy. Waste-to-energy Anaerobic Digester Plant, 995 KW (electricity). |

3

We currently have nonbinding letters of intent to develop/acquire the following projects:

Italy (negotiating and/or conducting due diligence)

| ● | Cantu, Italy. Acquisition of Clean-Tech Energy Plant, 990 KW (electricity). | |

| ● | Agrilandia, Italy. Acquisition of Anaerobic Digester Plant, 1MW (electricity). | |

| ● | Ravena, Italy. Acquisition of Cogeneration Plant, 1MW (electricity). | |

| ● | Sardinia, Italy (Galileo). New Construction of four Anaerobic Digester Plants, combined 2.7 MMBtu Biogas (4MW equivalent) (electricity). |

The Netherlands (developing and negotiating)

| ● | Sterksel, NL. New Construction of Anaerobic Digester Plant, 10.0 MW (electricity). |

The United Kingdom (negotiating and/or conducting due diligence)

| ● | Corby, GB. New Construction of Gasification Plant, 10MW (electricity). |

We are currently negotiating nonbinding letters of intent to develop/acquire the following projects:

United States (negotiating and/or conducting due diligence)

| ● | Boise, Idaho. New Construction of Anaerobic Digester Plant, 62 MMBtu Biogas (7.3MW equivalent) (electricity). | |

| ● | Woodstock, CT. New Construction of Anaerobic Digester Plant, 28 MMBtu Biogas (3.3MW equivalent) (electricity). | |

| ● | Hartford, CT. New Construction of Anaerobic Digester Plant, 27 MMBtu Biogas (3.2MW equivalent) (electricity). |

Italy (negotiating and/or conducting due diligence)

| ● | Ostellato, Italy. New Construction of two Anaerobic Digester Plants, 1MW (electricity). | |

| ● | Riffle, Italy. Acquisition of two Anaerobic Digester Plants, 2MW (electricity). | |

| ● | Milan, Italy (Agatos). New Construction of Anaerobic Digester Plant, 19.7 MMBtu Biogas (1MW equivalent) (electricity). |

The Netherlands (negotiating and/or conducting due diligence)

| ● | Het Haantje, NL. Acquisition of Anaerobic Digester Plant, 1.5MW Plant (electricity). |

Israel (negotiating and/or conducting due diligence)

| ● | Rishon Lezion, IL. New Construction of Materials Recycling Facility and Anaerobic Digester Plant, 2.5MW (electricity). |

Canada (negotiating and/or conducting due diligence)

| ● | Alberta, Canada. New Construction of Anaerobic Digester, 64.58 MMBtu Biogas (7.6MW equivalent) (electricity). |

Greece (negotiating and/or conducting due diligence)

| ● | Kermos, GR (Thrace). New Construction of Anaerobic Digestion Plant, 3MW (electricity). | |

| ● | Neochori, GR (Thrace). New Construction of Anaerobic Digestion Plant, 3MW (electricity). | |

| ● | Fytorio, GR (Thrace). New Construction of Anaerobic Digestion Plant, 3MW (electricity). |

All references to energy output, whether in MW or MMBtu, are per hour and are approximations.

Our strategy is to continue to expand in the future, including through acquisition of additional projects. From time to time, we negotiate, conduct due diligence and enter into nonbinding letters of intent for projects that we are evaluating. However, until due diligence is complete, further negotiations are finalized and the parties have executed a definitive agreement, there can be no assurance that we will be able to enter into any development or acquisition transaction, on the terms in the applicable letter of intent, if any, or at all, or any other similar arrangements. In the case of new construction projects for which we have not entered into definitive agreements, the power output identified herein reflects management’s position, determined based on a review of relevant factors including, but not limited to, pre-existing relationships with purchasers in the region, demand, land and facility space, environmental and engineering analysis, and the availability of feedstock and other sources of input.

Our Projects in the United States

On October 19, 2012, we entered into definitive project agreements in respect of both the North Carolina and Rhode Island sites with Orbit Energy, Inc. (“Orbit”), pursuant to which we would be entitled to full ownership of each of the entities that owns the rights to implement the respective projects (Orbit Energy Charlotte, LLC in the case of the North Carolina project (“OEC”) and Orbit Energy Rhode Island, LLC in the case of the Rhode Island project (“OERI”)), subject to the satisfaction of certain conditions.

4

Our North Carolina Project

Design and Development

On June 5, 2014, OEC entered into the NC Turnkey Agreement with Auspark, which amended and restated an original agreement dated April 30, 2014. Pursuant to the NC Turnkey Agreement, Auspark provided the design, supply, engineering, permitting, procurement, assembly, construction, installation, commissioning and delivery of the North Carolina facility (the “North Carolina Facility”), for the fixed price of $17,350,000, payable in accordance with meeting scheduled milestones, with the final payment becoming due upon delivery of a final completion certificate. Payments under the NC Turnkey Agreement were funded by York Renewable Energy Partners LLC (“York”), our joint venture partner for the North Carolina project.

The term of the NC Turnkey Agreement was based on the project construction and workflow completion plan, subject to amendment pursuant to the terms of the agreement. Austep (defined below) guaranteed Auspark’s performance under the NC Turkey Agreement. Upon effectiveness of the BULA, we had anticipated that the NC Turnkey Agreement would be transferred to Andion (defined below), which did not happen. On October 9, 2017, the NC Turnkey Agreement was terminated. For more information, see the subsection below entitled “Austep Liquidation/Restructuring and Continuity of Performance at the North Carolina Facility and the Rhode Island Facility”.

On February 8, 2018, OEC entered into a professional services agreement with ES Engineering Services, LLC, pursuant to which it will perform specified services to complete outstanding development activities at the North Carolina Facility; the agreement anticipates the completion such services by April 30, 2019. OEC is currently negotiating an agreement for specified upgrade and retrofit development services to be performed at the North Carolina Facility.

The Amended OEC Purchase Agreement

On November 19, 2014, we signed an amended and restated purchase agreement with Orbit for the North Carolina project (the “Amended OEC Purchase Agreement”). Subject to the terms of the Amended OEC Purchase Agreement, Orbit transferred full ownership of OEC to us in exchange for our agreeing to pay Orbit a development fee of $900,000, reimbursement of $17,764 of Orbit’s expenses, and an amount equal to 30% of the distributable cash flow from the North Carolina project after the project achieves a post-recoupment 30% internal rate of return computed on the basis of any and all benefits from tax credits, depreciation and other incentives of any nature. We also agreed to use high solid anaerobic digester units designed by Orbit (the “HSAD Units”) and to retain Orbit to implement and operate the HSAD Units for an annual management fee of $187,500 (the “OEC Management Fee”), subject to certain conditions. The Amended OEC Purchase Agreement provided that we had until December 15, 2014 to pay Orbit the development fee and reimbursement amount, which was extended to January 15, 2015 upon payment by us to Orbit of $75,000. We did not subsequently pay Orbit the development fee and reimbursement amount and, pursuant to the terms of the Amended OEC Purchase Agreement, ownership of OEC reverted back to Orbit on January 15, 2015.

Concord Energy Partners, LLC

On January 30, 2015, (i) the Company, Concord Energy Partners, LLC, a Delaware limited liability company (“Concord”) and York entered into a development and indemnification agreement (the “Concord Development and Indemnification Agreement”), pursuant to which in 2015 York funded Concord’s payment to us of $1,250,000 in development fees used for developing the project, and Concord issued us 250 Series B units of Concord (“Concord Series B Units”) and issued 750 Series A units of Concord (“Concord Series A Units”) to York, and (ii) we and York entered into an amended and restated limited liability company operating agreement (the “Concord LLC Agreement”) to establish the Concord Series A Units and Concord Series B Units and admit us and York as 25% and 75% members of Concord, respectively. Pursuant to the foregoing agreements, York also agreed to fund Concord’s payment to us of two equal installments of $587,500 upon (a) mechanical completion of the North Carolina project and (b) commercial operation of the North Carolina project. We have received payment of the first installment.

Pursuant to the Concord LLC Agreement, our right to receive distributions from Concord are subject to certain priorities in favor of York, as follows:

| (a) | York’s nine percent (9%) rate of return on the $500,000 capital contribution to Concord to fund liquidated damages to Duke Energy pursuant to the Duke PPA since the commercial operations had not been commenced within 60 days of December 31, 2015; | |

| (b) | The repayment of York’s $500,000 capital contribution to Concord to fund liquidated damages to Duke Energy pursuant to the Duke PPA since the commercial operations had not been commenced within 60 days of December 31, 2015; | |

| (c) | The amount of any excess profits from “feedstock tipping fees” shall be distributed with twenty percent (20%) going to York, and eighty percent (80%) going to us; | |

| (d) | The amount of any excess profits from “thermal energy” shall be distributed equally between us and York; and | |

| (e) | Any amount remaining will be distributed pro-rata to us and York in proportion to York and our respective ownership of Concord. |

5

In addition, our right to receive distributions upon a liquidation event of Concord are subject to certain priorities in favor of York, as follows:

| (a) | York’s nine percent (9%) rate of return on its unrecovered capital contributions to Concord; | |

| (b) | The repayment of York’s unrecovered capital contributions to Concord; and | |

| (c) | Any amount remaining will be distributed pro-rata to us and York in proportion to York and our respective ownership of Concord. |

Pursuant to the Concord LLC Agreement, Concord is managed by a board of managers initially consisting of three managers (the “Concord Board”). So long as York owns more than 50% of the membership interests of Concord, York is entitled to appoint two of the Concord Board’s three managers. So long as we own no less than 50% of the membership interests of Concord that we acquired pursuant to the Concord Development and Indemnification Agreement, we are entitled to appoint one manager of the Concord Board. York will make capital contributions to Concord in accordance with the budgeted investment amount for the North Carolina project set forth in the Concord LLC Agreement. In the event that the Concord Board determines in good faith that additional equity capital is needed by Concord and is in the best interests of the North Carolina project, the Concord Board may determine the amount of additional equity capital needed and issue new units to raise the necessary funds. In this case, if we do not exercise our pre-emptive right with respect to such units, our percentage interest in Concord would be reduced accordingly. The Concord LLC Agreement also contains certain restrictions on our right to transfer our membership interests in Concord to third parties. If we propose to sell any equity or assets relating to or in connection with the development, construction or operation of an energy generation facility to a third party prior to January 30, 2020, Entropy Investment Management LLC, an affiliate of York that provides project financing for renewable energy projects, will have a right of first refusal to acquire all or a portion of such sale.

The New OEC Purchase Agreement

On January 30, 2015, we entered into the Orbit Energy Charlotte, LLC Membership Interest Purchase Agreement by and among the Company, Orbit, Concord, and OEC (the “New OEC Purchase Agreement”), pursuant to which (i) Concord purchased all of Orbit’s right, title and interest in and to the membership interests of OEC (the “OEC Interests”), (ii) Orbit abandoned all economic and ownership interest in the OEC Interests in favor of Concord, (iii) Orbit ceased to be a member of OEC and (iv) Concord was admitted as the sole member of OEC, in exchange for consideration of $917,764.

Under the Amended OEC Purchase Agreement and the New OEC Purchase Agreement, we had agreed to pay to Orbit the costs of evaluating and incorporating into the North Carolina project Orbit’s high solids anaerobic digestion technology and two HSAD Units designed by Orbit. Orbit was unable to design and install this technology into the North Carolina project, and we never paid or became obligated to pay any costs pursuant thereto. Instead, digesters were designed and provided by Auspark LLC (“Auspark”), and have been incorporated into the North Carolina project.

The New OEC Purchase Agreement also carried forward from the Amended OEC Purchase Agreement, and we indemnified York with respect to, our obligation to pay Orbit all amounts owed under the Amended OEC Purchase Agreement, including an amount equal to thirty percent (30%) of the North Carolina project’s distributable cash flow after we and the other equity investors in the North Carolina project fully recoup their respective investments in the North Carolina project (such investments to be calculated solely as amounts expended in and for the construction of the North Carolina project) and the North Carolina project achieves a thirty percent (30%) internal rate of return(the “NC Participation Fee”). The calculation of the project’s internal rate of return would take into account and be computed on the basis of any and all benefits from tax credits, depreciation and other incentives of any nature.

On January 13, 2017, the Company and Orbit entered into an agreement to eliminate the Company’s obligations to Orbit under the New OEC Purchase Agreement, the Concord LLC Agreement, the New OERI Purchase Agreement (defined below), and the Rhode Island LLC Agreement (defined below). In connection with the North Carolina project and the Rhode Island project, in exchange for an assignment to us of any rights to the NC Participation Fee and RI Participation Fee (defined below), and the termination of the OEC Management Fee and OERI Management Fee (defined below), Orbit received $200,000.

The Operations of the North Carolina Project

On June 5, 2014, OEC entered into a Service, Maintenance and Operation Agreement (the “Austep NC O&M Agreement”) with Austep USA, whereby Austep USA would perform the day-to-day operation, management, service, and maintenance operations at the North Carolina Facility, for a term of 10 years beginning on the date that the facility achieved substantial completion, as was defined in the NC Turnkey Agreement. Austep guaranteed Austep USA’s performance under the agreement. Upon effectiveness of the BULA, we had anticipated that the Austep NC O&M Agreement would be transferred to Andion, which would become responsible for performance thereunder. For more information, see the subsection below entitled “Austep Liquidation/Restructuring and Continuity of Performance at the North Carolina Facility and the Rhode Island Facility”. On October 9, 2017, the Austep NC O&M Agreement was terminated.

On February 20, 2018, OEC entered into an interim operations and management agreement with ES Engineering Services, LLC, pursuant to which it will perform the day-to-day operation, management, service, and maintenance operations at the North Carolina Facility on a short-term basis, while the parties negotiate and finalize a long-term agreement.

6

OEC and Duke Energy Carolinas, LLC (“Duke Energy”) are parties to an Amended and Restated Renewable Energy Purchase Agreement, dated October 12, 2012 and amended on April 25, 2013, January 31, 2014, January 29, 2015 and September 30, 2016 (as amended, the “Duke PPA”), pursuant to which OEC has agreed to sell, and Duke has agreed to purchase, the energy output of OEC’s facility, subject to the terms and conditions of the Duke PPA. Among other things, the Duke PPA required OEC to commence commercial operations by December 31, 2015 or, if not operational within 60 days of such date, pay Duke Energy $500,000 of liquidated damages, which would then extend the deadline for commercial operation to March 30, 2016. Since the commercial operations had not been commenced within 60 days of December 31, 2015, OEC was required to pay $500,000 of liquidated damages to Duke Energy pursuant to the Duke PPA during the first quarter of 2016, and York contributed these funds to OEC. The deadline for commercial operation was thereafter extended to November 23, 2016 by amendment to the Duke PPA. The Duke PPA is effective until August 21, 2030. The loss of Duke Energy as a customer of OEC could have a material adverse effect on the Company.

The Duke PPA further provides that OEC is responsible for certain interconnections fees and the costs and charges in connection with delivering power to the delivery point. OEC is responsible for delivering 100% of the output nameplate capacity of 5.2MW, and Duke Energy is responsible for purchasing up to the nameplate capacity. During the term of the Duke PPA, the bundled price payable to OEC is fixed per MWh, together with fixed prices per year for specified categories of RECs, as well as minimum REC requirements and purchase obligations during the term. Duke Energy is not responsible for purchasing additional energy or renewable energy attributes which exceeds 10% of the facility’s nameplate capacity. If OEC does not deliver up to the nameplate capacity, it must pay damages equal to specified replacement REC costs.

On or about November 18, 2016, the North Carolina Facility connected to the grid, began commissioning and thereafter commenced commercial operations and started to provide output to Duke Energy pursuant to the Duke PPA. The North Carolina Facility is currently in the mechanical completion and ramp-up phase of the project. Commencement of the commercial operations includes the gradual intake of waste from the facility’s feedstock suppliers, increasing the parasitic load to the digesters, completing the waste-water-treatment resources and completing all other mechanical features needed for the facility to operate at full capacity. The Company estimates that the North Carolina project will be fully completed by the end of the first quarter of 2019.

As of December 31, 2017, we have recorded equity earnings in the amount of $931,771 from nonconsolidated affiliates in 2017 with respect to the North Carolina project.

Our Rhode Island Project

Design and Development

On April 7, 2015, OERI entered into the RI Turnkey Agreement with Auspark, which amended and restated an original agreement dated April 30, 2014. Pursuant to the RI Turnkey Agreement, Auspark provided the design, supply, engineering, permitting, procurement, assembly, construction, installation, commissioning and delivery of the Rhode Island facility (the “Rhode Island Facility”), for the fixed price of $13,800,000, payable in accordance with meeting scheduled milestones, with the final payment becoming due upon delivery of a final completion certificate. Payments under the RI Turnkey Agreement were funded by York, our joint venture partner for the Rhode Island project.

7

The term of the RI Turnkey Agreement was based on the project construction and workflow completion plan, subject to amendment pursuant to the terms of the agreement. Austep (defined below) guaranteed Auspark’s performance under the RI Turkey Agreement. Upon effectiveness of the BULA, we had anticipated that the RI Turnkey Agreement would be transferred to Andion (defined below), which did not happen. On October 9, 2017, the Austep RI Turnkey Agreement was terminated. For more information, see the subsection below entitled “Austep Liquidation/Restructuring and Continuity of Performance at the North Carolina Facility and the Rhode Island Facility”.

On February 8, 2018, OERI entered into a professional services agreement with ES Engineering Services, LLC, pursuant to which it will perform specified services to complete outstanding development activities at the Rhode Island Facility; the agreement anticipates the completion such services by April 30, 2019. OERI is currently negotiating an agreement for specified upgrade and retrofit development services to be performed at the Rhode Island Facility.

The Amended OEC Purchase Agreement

On January 7, 2015, we signed an amended and restated purchase agreement with Orbit for the Rhode Island project (the “Amended OERI Purchase Agreement”). Subject to the terms of the Amended OERI Purchase Agreement, Orbit transferred full ownership of OERI to us in exchange for our agreeing to pay Orbit a development fee of $300,000, reimbursement of $86,432 of Orbit’s expenses, and an amount equal to 30% of the distributable cash flow from the Rhode Island project after the project achieves a post-recoupment 30% internal rate of return computed on the basis of any and all benefits from tax credits, depreciation and other incentives of any nature. We also agreed to use HSAD Units designed by Orbit and to retain Orbit to implement and operate the HSAD Units for an annual management fee of $187,500 (the “OERI Management Fee”), subject to certain conditions. The Amended OERI Purchase Agreement provided that we had until January 22, 2015 to pay Orbit the development fee and reimbursement amount, which was extended to February 28, 2015 in exchange for payment by us to Orbit of $31,000. We did not subsequently pay Orbit the development fee and reimbursement amount and, pursuant to the terms of the Amended OERI Purchase Agreement, ownership of OERI reverted back to Orbit.

Rhode Island Energy Partners, LLC

On April 8, 2015, (i) the Company, Rhode Island Energy Partners, LLC, a Delaware limited liability company (“Rhode Island”) and York entered into a development and indemnification agreement (the “Rhode Island Development and Indemnification Agreement”), pursuant to which York funded Rhode Island’s payment to us of development fees of $1,541,900 used for developing the project, and Rhode Island issued us 2,275 Series B units of Rhode Island (“Rhode Island Series B Units), and issued 7,725 Series A units of Rhode Island (“Rhode Island Series A Units”) to York, and (ii) we and York entered into an amended and restated limited liability company operating agreement (the “Rhode Island LLC Agreement”) to establish the Rhode Island Series A Units and Rhode Island Series B Units and admit us and York as 22.75% and 77.25% members of Rhode Island, respectively. Pursuant to the foregoing agreements, York also agreed to fund Concord’s payment to us of three equal installments of $562,500 upon (a) signing of the Rhode Island Development and Indemnification Agreement, (b) the later of (x) the date of mechanical completion of the Rhode Island project and (y) the date on which an executed interconnection agreement between OERI and National Grid, including receipt of any regulatory approvals from the Rhode Island Public Utility Commission, is delivered by OERI, and (c) commercial operation of the Rhode Island project. To date, York has made payments of the first and the third installments.

Pursuant to the Rhode Island LLC Agreement, our right to receive distributions from OERI are subject to certain priorities in favor of York, as follows:

| (a) | The amount of any excess profits from “feedstock tipping fees” shall be distributed with twenty percent (20%) going to York, and eighty percent (80%) going to us; | |

| (b) | The amount of any excess profits from “thermal energy” shall be distributed equally between us and York; and | |

| (c) | Any amount remaining will be distributed pro-rata to us and York in proportion to York and our respective ownership in Rhode Island. |

In addition, our right to receive distributions upon a liquidation event of Rhode Island are subject to certain priorities in favor of York, as follows:

| (a) | York’s nine percent (9%) rate of return on the sum of all obligations guaranteed by York in connection with the Rhode Island project; | |

| (b) | York’s nine percent (9%) rate of return on its unrecovered capital contributions to Rhode Island; | |

| (c) | The repayment of York’s unrecovered capital contributions to Rhode Island; and | |

| (d) | Any amount remaining will be distributed pro-rata to us and York in proportion to York and our respective ownership in Rhode Island. |

8

Pursuant to the Rhode Island LLC Agreement, Rhode Island is managed by a board of managers initially consisting of three managers (the “Rhode Island Board”). So long as York owns more than 50% of the membership interests of Rhode Island, York is entitled to appoint two of the Rhode Island Board’s three managers. So long as we own no less than 50% of the membership interests of Rhode Island that we acquired pursuant to the Rhode Island Development and Indemnification Agreement, we are entitled to appoint one manager of the Rhode Island Board. York will make capital contributions to Rhode Island in accordance with the budgeted investment amount for the North Carolina project set forth in the Concord LLC Agreement. In the event that the Rhode Island Board determines in good faith that additional equity capital is needed by Rhode Island and is in the best interests of the Rhode Island project, the Rhode Island Board may determine the amount of additional capital needed and issue new units to raise the necessary funds. In this case, if we do not exercise our pre-emptive right with respect to such units, our percentage interest in Rhode Island would be reduced accordingly. The Rhode Island LLC Agreement also contains certain restrictions on our right to transfer our membership interests in Rhode Island to third parties. If we propose to sell any equity or assets relating to or in connection with the development, construction or operation of an energy generation facility to a third party prior to April 8, 2020, Entropy Investment Management LLC will have a right of first refusal to acquire all or a portion of such sale.

The New OERI Purchase Agreement

On April 8, 2015, we entered into the Orbit Energy Rhode Island, LLC Membership Interest Purchase Agreement by and among the Company, Orbit, Rhode Island and OERI (the “New OERI Purchase Agreement”), pursuant to which (i) Rhode Island purchased all of Orbit’s right, title and interest in and to the membership interests of OERI (the “OERI Interests”), (ii) Orbit abandoned all economic and ownership interest in the OERI Interests in favor of Rhode Island, (iii) Orbit ceased to me a member of OERI and (iv) Rhode Island was admitted as the sole member of OERI, in exchange for consideration of $386,432.

Under the Amended OERI Purchase Agreement and the New OERI Purchase Agreement, we had agreed to pay to Orbit the costs of evaluating and incorporating into the Rhode Island project Orbit’s high solids anaerobic digestion technology and two HSAD Units designed by Orbit. Orbit was unable to design and install this technology into the Rhode Island project, and we never paid or became obligated to pay any costs pursuant thereto. Instead, digesters designed and provided by Auspark LLC, the project’s engineering, procurement, construction and technology provider, have been incorporated into the Rhode Island project.

The New OERI Purchase Agreement also carried forward from the Amended OERI Purchase Agreement, and we indemnified York with respect to, our obligation to pay Orbit all amounts owed under the Amended OERI Purchase Agreement, including an amount equal to thirty percent (30%) of the Rhode Island project’s distributable cash flow after we and the other equity investors in the Rhode Island project fully recoup our respective investments in the Rhode Island project (such investments to be calculated solely as amounts expended in and for the construction of the Rhode Island project) and the Rhode Island project achieves a thirty percent (30%) internal rate of return (the “RI Participation Fee”). The calculation of the project’s internal rate of return would take into account and be computed on the basis of any and all benefits from tax credits, depreciation and other incentives of any nature.

On January 13, 2017, the Company and Orbit entered into an agreement to eliminate the Company’s obligations to Orbit under the New OEC Purchase Agreement, the Concord LLC Agreement, the New OERI Purchase Agreement, and the Rhode Island LLC Agreement. In connection with the North Carolina project and the Rhode Island project, in exchange for an assignment to us of any rights to the NC Participation Fee and RI Participation Fee, and the termination of the OEC Management Fee and OERI Management Fee, Orbit received $200,000.

The Operations of the Rhode Island Project

On February 20, 2018, OERI entered into an interim operations and management agreement with ES Engineering Services, LLC, pursuant to which it will perform the day-to-day operation, management, service, and maintenance operations at the Rhode Island Facility on a short-term basis, while the parties negotiate and finalize a long-term agreement.

OERI and The Narragansett Electric Company d/b/a National Grid (“National Grid”) are parties to a Power Purchase Agreement, dated May 26, 2011 and amended on April 11, 2013, December 9, 2013, January 9, 2015 and May 27, 2016 (as amended, the “National Grid PPA”), pursuant to which OERI has agreed to sell, and National Grid has agreed to purchase, the energy output of OERI’s facility, subject to the terms and conditions of the National Grid PPA. Among other things, the National Grid PPA required OERI to commence commercial operations by December 31, 2015, which could be extended up to six months by OERI upon deposit of $22,500 of collateral. Since commercial operations were not commenced by December 31, 2015, OERI paid an additional “Development Period Security” of $22,500 pursuant to the National Grid PPA, such funds having been contributed to OERI by York. On May 27 2016, National Grid agreed to modify the date to commence commercial operations to June 30, 2017. As an incentive and evidence of good faith to achieve commercial operation, OERI posted additional collateral in the amount of $22,500, such funds having been contributed to OERI by York. The National Grid PPA is effective for 15 years from the date commercial operations are commenced, which may be extended by 6 years at the option of National Grid. The loss of National Grid as a customer of OERI could have a material adverse effect on the Company.

The National Grid PPA further provides that OERI is responsible for certain interconnections fees, subject to an adjustment based on MWh sold under the agreement, and the costs and charges in connection with delivering power to the interconnection point. OERI is responsible for delivering 100% of the output nameplate capacity of up to 3.2MW, and National Grid is responsible for purchasing up to our nameplate capacity. National Grid is not responsible for purchasing additional energy in excess of the specified maximum amount. During the term of the agreement, National Grid will pay a fixed bundled price per MWh for energy and RECs, subject to escalation by a factor of 2% annually. If OERI fails to deliver energy in accordance with the National Grid PPA, it will be responsible for specified replacement damages.

9

On or about June 23, 2017, the Rhode Island Facility connected to the grid, began commissioning and thereafter commenced commercial operations and started to provide output to National Grid pursuant to the National Grid PPA. The Rhode Island Facility is currently in the mechanical completion and ramp-up phase of the project. Commencement of the commercial operations includes the gradual intake of waste from the facility’s feedstock suppliers, increasing the parasitic load to the digesters, completing the waste-water-treatment resources and completing all other mechanical features needed for the facility to operate at full capacity. The Company estimates that the Rhode Island project will be fully completed by the end of the first quarter of 2019.

As of December 31, 2017, we have recorded equity earnings from nonconsolidated affiliates in the amount of $5,405,000, and we have recorded revenue from development fees in the amount of $562,500 in 2017, with respect to the Rhode Island project.

Austep Liquidation /Restructuring and Continuity of Performance at the North Carolina Facility and the Rhode Island Facility

From the Official Records, the Company learned that on June 20, 2017, Austep was put in voluntary liquidation by shareholders’ resolution pursuant the Italian Civil Code and on June 30, 2017, Austep filed a petition in the Bankruptcy Court of Milan (the “Milan Court”) for a creditors’ settlement procedure pursuant to Italian Bankruptcy Law. On July 6, 2017, the Milan Court approved Austep’s petition for a creditors’ settlement procedure providing for Austep to submit (i) a final debt restructuring plan and (ii) a request for certification of the restructuring agreement’s debts.

According to the Official Records, on June 29, 2017, Austep entered into a Business Unit Lease Agreement (BULA) with Andion Italy S.r.l., with the intent of assuring the regular operation of certain operations and agreements by Andion. Andion is wholly owned by Arcus Holdings Sa, a Luxembourg entity owned by White Cloud Capital II SCSp, which controls Austep Holdings S.p.A. Austep Holdings S.p.A. wholly-owns Austep and Austep USA, and Austep USA wholly-owns Auspark LLC and Austep Rhode Island LLC. Andion is not subject to the liquidation/restructuring of Austep. The BULA provided for, among other things, the transfer of Austep’s entire United States operations. Upon effectiveness of the BULA, we had anticipated that the NC Turnkey Agreement, Austep NC O&M Agreement and RI Turnkey Agreement would be transferred to Andion, which did not happen.

As described in more detail above, the NC Turnkey Agreement, Austep NC O&M Agreement and RI Turnkey Agreement relating to Austep’s involvement with the North Carolina Facility and the Rhode Island Facility were terminated, and both OEC and OERI have entered into agreements pursuant to which ES Engineering Services, LLC will perform development and day-to-day operation, management, service, and maintenance operations at the North Carolina Facility and the Rhode Island Facility.

Our Projects in Italy

Our 2015 SPV Facilities

Acquisition of our 2015 SPV Facilities

On May 14, 2015, we entered into a Share Purchase Agreement (the “Italy Projects Agreement”) with Volteo Energie S.p.A., Agriholding S.r.l., and Overland S.r.l. (each, a “Seller” and collectively, the “Sellers”) through our indirect, wholly-owned subsidiary, Bluesphere Pavia S.r.l. (formerly Bluesphere Italy S.r.l.) (“Bluesphere Pavia”). Pursuant to the Italy Projects Agreement, we agreed to purchase one hundred percent (100%) of the share capital of Agricerere S.r.l., Agrielektra S.r.l., Agrisorse S.r.l. and Gefa S.r.l (each, an “SPV” and collectively, the “SPVs”) from the Sellers, who collectively held all of the outstanding share capital of each SPV. Each SPV is engaged in the owning and operating of an anaerobic digestion biogas plant for the production and sale of electricity (each, a “2015 SPV Facility” and collectively, the “2015 SPF Facilities”) to Gestore del Servizi Energetici GSE, S.p.A., a state-owned company, pursuant to the SPVs PPA. All references to, and descriptions of, the Italy Projects Agreement incorporate the terms of an amendment to the same entered into by the parties on December 14, 2015.

Pursuant to the Italy Projects Agreement, we agreed to pay an aggregate purchase price of €5,600,000 for all of the SPVs, which, upon the application of certain credits applied, was adjusted to €5,200,000 (USD $5,646,628) (the “Purchase Price”). Fifty percent (50%) of the Purchase Price, less certain credits, was due to the Sellers on the Closing Date and the remaining balance along with interest at a rate of two percent (2%) per year (the “Deferred Payment”), less certain credits, is due to the Sellers on the third anniversary of the Closing Date. The Purchase Price was subject to certain adjustments and to an adjustment based on the actual EBITDA results in the 18 months following the Closing Date, per the following mechanism:

| (a) | If the actual EBITDA in the 18 months following the Closing Date divided by 1.5 is greater than € 934,519, then the Deferred Payment shall be increased by the amount equal to fifty percent (50%) of the difference. | |

| (b) | If the actual EBITDA in the 18 months following the Closing Date divided by 1.5 is lesser than € 934,519, then the Deferred Payment shall be reduced by the amount of the amount necessary to maintain a Purchase Price that yields an Equity IRR of twenty-five percent (25%), but not more than 35% of the remaining balance. |

10

Under the Italy Projects Agreement, EBITDA is defined as “total cash revenues received minus all cash expenditures made during the relevant period excluding principle and interest payments due to the bank and taxes”.

Pursuant to the Italy Projects Agreement, the Company will reimburse the Sellers the VAT amount that was requested and will be requested by the SPVs for the fiscal year of 2014 on or before December 14, 2018. The reimbursed amount will not exceed €1,160,425 and will be refunded to the Sellers only after the amount is refunded to Bluesphere Pavia by the VAT authorities in Italy. Pursuant to the Italy Projects Agreement, we also issued a corporate guarantee to the Sellers, whereby the Company will secure the obligations of Bluesphere Pavia under the Italy Projects Agreement.

On December 14, 2015 (the “Closing Date”), pursuant to the Italy Projects Agreement, we completed the acquisitions of one hundred percent (100%) of the share capital of the “SPVs. On the Closing Date, the Company paid an amount of €1,952,858 (USD $2,143,181), which represented fifty percent (50%) of the Purchase Price adjusted for certain post-closing adjustments and closing costs. The remaining balance of the Purchase Price (balance less the adjusted closing payment) is promised by a note accruing interest at an annual rate of two percent (2%) to each Seller, with such principal and interest accrued due to each Seller on or before the third anniversary of the Closing Date, subject to adjustment to the variation of EBITDA, as described above. The portion of the Purchase Price and all closing costs, pre-closing receivables, fees and related expenses paid at closing were primarily financed by a loan of €2,900,000, obtained pursuant to the Helios Loan Agreement, of which €200,000 was repaid to Helios in March 2016.

The closing of the Italy Projects Agreement was subject to certain conditions precedent including, but not limited to, obtaining consent to the proposed sale and resulting change of control from its lender, Banca IMI, in connection with a certain €22,080,000 Financing Agreement, dated February 25, 2013, between the SPVs, Banca IMI and Intesa San Paolo S.p.A. (the “SPV Financing Agreement”), as well as from other counterparties to certain agreements to which the SPVs are a party. Amounts outstanding under the SPV Financing Agreement are secured by the assets of the SPVs. After the Closing Date, the SPV’s paid a waiver fee of approximately €109,000 to the SPVs’ lender, such amount representing 50% of the fees and expenses charged by the lenders in connection with obtaining these consents. In addition, under the Italy Projects Agreement, the Sellers granted us a special credit of €100,000 per SPV, half of which is allocable to each payment of the Purchase Price. Following the achievement of key milestones under the SPV Financing Agreement, on December 21, 2016, we agreed with the SPVs’ lender to certain revised terms under the SPV Financing Agreement for each SPV, specifically (a) each SPV received a new VAT line of credit equal to €300,000 per SPV, and an extension to each SPV’s existing VAT line of credit for one year, (b) our obligation to fund a debt service reserve account deposit totaling €1,100,000 was terminated, and (c) a minimum cash requirement of €200,000 per account was removed. In addition, on December 21, 2016, the SPVs’ lender also officially approved the Framework EBITDA Agreement. As of December 31, 2017, $15,250,000 was outstanding under the SPV Financing Agreement.

On July 21, 2017, the Company notified the Sellers of its estimated Deferred Payment, pursuant to Article 3.03 of the Italy Projects Agreement regulating the Deferred Payment adjustment mechanism. As of April 16, 2018, two of the three Sellers have accepted the Company’s estimate, and the third Seller, Volteo Energie S.p.A., is reviewing the Company’s estimate subject to an independent opinion of a third party appraiser. Volteo Energie S.p.A., which has a majority interest among the Sellers, is presently going through a bankruptcy procedure.

Termination of our Agreements with Austep to Operate, Maintain and Supervise the 2015 SPV Facilities

As discussed more fully below, the Company has terminated all four Plant EBITDA Agreements with Austep on July 18, 2017. Notwithstanding, these facilities are currently operating and the Company is in the process of replacing Austep with a new operator. The Company believes that the termination of the Plant EBITDA Agreements with Austep and the engagement of a new operator will result in the facilities being operated under terms that are more advantageous to the Company, which the Company believes will improve profitability. Therefore, the Company believes that there will ultimately be no material negative impact resulting from this change in operating partner.

On July 17, 2015, we entered into a Framework EBITDA Guarantee Agreement (the “Framework EBITDA Agreement”) with Austep S.p.A. (“Austep”), an Italian corporation. Austep specializes in the design, construction, operation and servicing of anaerobic digestion plants. The Framework EBITDA Agreement provided a framework pursuant to which Austep performed technical analyses of operating anaerobic digestion plants in Italy that we identified as potential acquisition targets. If and when we acquired such anaerobic digestion plants in Italy, we and Austep had agreed to negotiate individual agreements pursuant to which Austep would operate, maintain and supervise each plant and guarantee agreed-upon levels of EBITDA to us for a specified period. On the Closing Date, all four SPVs entered into Plant EBITDA Agreements with Austep. In accordance with the Plant EBITDA Agreements, Austep operated, maintained and supervised each biogas plant owned by the SPVs until July 12, 2017. The Plant EBITDA Agreements provided that we would receive an annual aggregate EBITDA of €3,760,000 for the four SPVs, collectively, and that Austep would receive ninety percent (90%) of the revenue in excess of such levels.

11

On July 12, 2017, Austep personnel shut down the engines at all of the 2015 SPV Facilities, and exited all four sites. The Company immediately notified Banca IMI, the SPVs’ lender, and began coordinating with Banca IMA on its remedial action plan. The Company believes that Austep’s failure to perform under the Plant EBITDA Agreements was due to a liquidation/restructuring of Austep. From the Official Records, the Company learned that on June 20, 2017, Austep was put in voluntary liquidation by shareholders’ resolution pursuant the Italian Civil Code and on June 30, 2017, Austep filed a petition in the Bankruptcy Court of Milan (Milan Court) for a creditors’ settlement procedure pursuant to Italian Bankruptcy Law. On July 6, 2017, the Milan Court approved Austep’s petition for a creditors’ settlement procedure and declared that Austep shall, by November 3, 2017, submit (i) the final debt restructuring plan and (ii) a request for certification of the restructuring agreement’s debts. For more information concerning the foregoing, see the subsection entitled “Change in Operator in Italy and Transfer of North Carolina and Rhode Island Project Agreements” above.

On July 14, 2017, the Company notified Austep’s liquidator, in accordance with the Plant EBITDA Agreements, that because (i) Austep had neglected specified contractual obligations concerning maintenance of the 2015 SPV Facilities, which each SPV had notified Austep of on June 21, 2017, and (ii) Austep, without notice, abandoned the 2015 SPV facilities, the Company had taken over direct management and supervision of the 2015 SPV Facilities to ensure their proper operation, safety and security. The Company reserved all rights to claim any and all damages arising as a consequence of Austep’s conduct, including costs incurred by the Company in its intervention.

On July 18, 2017, the SPVs delivered to Austep a notice of termination of the Plant EBITDA Agreements due to several breaches of Austep’s obligations, representations and warranties thereunder including without limitation those outlined in the notice provided to Austep’s liquidator on July 14, 2017. The Company further notified Austep that, as a consequence of early termination, (i) it is obligated to pay a penalty of €85,000 to each SPV, and (ii) that Austep will be deemed liable to hold the SPVs harmless and indemnified for any direct and indirect losses (including loss of business), damages, costs of engaging replacement contractors and suppliers, costs relating to the supply of feedstock for years 2017 through 2018, insurance premium costs, costs incurred in connection with the financing facility agreement with Banca IMI, and any other expenses or other liabilities incurred or to be incurred by the SPVs as a consequence of or in connection with Austep’s breaches, actions and/or omissions under the Plant EBITDA Agreements. The notice was prepared in coordination with Banca IMI. The Company withheld its costs and damages arising from the loss in generation at the 2015 SPV Facilities, and the costs or remediating and implementing its short-term and long-term operational solutions, from any amounts payable to Austep under the terminated Plant EBITDA Agreements.

On July 14, 2017, the Company entered into a month-to-month Biogas Plants’ Ordinary Management Proposal (the “Interim Agreement”) with Società Agricola Burnigaia Società Semplice d/b/a La Fenice, an Italian company experienced in the operation of biogas plants (“La Fenice”), pursuant to which it operated and supervised the 2015 SPV Facilities. The Interim Agreement with La Fenice terminated in accordance with its terms on September 30, 2017, at which time La Fenice stopped providing operational and supervisory services at the 2015 SPV Facilities.

Our New Agreements to Operate, Maintain and Supervise the 2015 SPV Facilities

On November 7, 2017, each of four SPVs entered into an Operating and Maintenance Contract for an Anaerobic Digestion Plant Using Biogas to Produce Electric Power (each, an “SPV Operating Agreement” and collectively, the “SPV Operating Agreements”) with a new operator, Biogaservizi S.r.l., an Italian company (“Biogaservizi”). Pursuant to the SPV Operating Agreements, Biogaservizi began providing full-service operation, maintenance, and supervision of the 2015 SPV Facilities, including the supply of feedstock, effective as of October 1, 2017. The SPV Operating Agreements are for a term of ten (10) years, and are renewable by the SPVs for one (1) year intervals. The SPV Operating Agreements may be terminated by the SPVs for reasons including, but not limited to, an insolvency or bankruptcy affecting Biogaservizi, revocation of specified state authorizations necessary to operate an SPV facility, and specified operator breaches, failures and delays. An SPV may request a suspension of an SPV Operating Agreement, but if such suspension exceeds thirty (30) days in any contract year and is not attributable to a breach of performance by Biogaservizi, then Biogaservizi shall be entitled to the reimbursement of reasonably incurred and documents costs and expenses resulting from such suspension. Biogaservizi may terminate an SPV Operating Agreement if the SPV fails to make payment of the Operator Fee (defined below) within sixty (60) days of such fee becoming due. In connection with each SPV Operating Agreement, Biogaservizi has until May 4, 2018 to present, to each SPV a first demand guarantee from a leading Italian or EU bank of four hundred thousand Euros (€400,000), to guarantee its obligations, required payments and potential damages under each SPV Operating Agreement (the “Guarantee”). Biogaservizi may reduce the Guarantee to an amount that is at least twenty-five percent (25%) of initial amount if it fully performs for two (2) years following the effective date. Biogaservizi will receive an annual fee for the operation of each 2015 SPV Facility of four hundred and five thousand Euros (€405,000), plus VAT, which is inclusive of all services to be provided (the “Operator Fee”). Biogaservizi guarantees specified performance levels at each 2015 SPV Facility and if it fails to meet such performance levels as measured in six (6) month reference periods, compensatory penalties will be deducted from the Operator Fee, as determined based on a specified formula. Compensatory penalties shall not exceed, on an annual basis, the Operator Fee.

The 2015 SPV Facilities are presently transmitting electricity to the grid, and we anticipate that during the first quarter of 2018, all 2015 SPV Facilities will be generating at full capacity.

The Helios Loan Agreement for the 2015 SPV Facilities

On August 18, 2015, we and two of our wholly-owned subsidiaries, Eastern Sphere Ltd. (“Eastern Sphere”), the parent of Bluesphere Pavia, and Bluesphere Pavia, entered into a Long Term Mezzanine Loan Agreement (the “Helios Loan Agreement”) with Helios Italy Bio-Gas 1 L.P. (“Helios”) to finance the Italy Projects Agreement. Under the Helios Loan Agreement, Helios made up to five million euros (€5,000,000) available to Bluesphere Pavia (the “Helios Loan”) to finance (a) ninety percent (90%) of the total required investment of the first four SPVs acquired, (b) seventy to eighty percent (70-80%) of the total required investment of up to three SPVs subsequently acquired, if applicable, (c) certain broker fees incurred in connection with the acquisitions, and (d) any taxes associated with registration of an equity pledge agreement (as described below). Each financing of an SPV acquisition will be subject to specified conditions precedent and will constitute a separate loan under the Helios Loan Agreement. Helios’s obligation to provide additional funds under the Helios Loan Agreement, in connection with subsequently acquired SPVs, terminated on June 30, 2016.

12

Subject to specified terms, representations and warranties, the Helios Loan Agreement provides that each loan thereunder will accrue interest at a rate of fourteen and one-half percent (14.5%) per annum, and that Helios is entitled to an annual operation fee of one and one-half percent (1.5%) per annum. Payments of principal, interest and the operation fee are due and payable quarterly. The final payment for each loan will become due no later than the earlier of (a) thirteen and one half years from the date such loan was made available to Bluesphere Pavia, and (b) the date that the license to produce electricity granted to the relevant SPV expires. Pursuant to the Helios Loan Agreement and an equity pledge agreement, Eastern Sphere pledged all its shares in Bluesphere Pavia to secure all loan amounts utilized under the Helios Loan Agreement.

In addition, the Helios Loan Agreement provides for no prepayment of the outstanding amount; however, subject to Helios’ right of first refusal and following 5 years from the date of closing, we may prepay upon meeting certain conditions, including that the net consideration of such prepayment will be the principal amount of the Helios Loan, less loan principal, interest and operation fees previously paid, multiplied by 2.12. The Helios Loan Agreement is subject to certain standard events of default subject to a 7-day cure period, including our failure to make two consecutive installment payments or pay the operations fee, events of insolvency or liquidation, and the declaration of an event of default under each the SPV Financing Agreement.

On December 2015, we borrowed €2,900,000 ($3,149,000) under the Helios Loan Agreement to finance the purchase of the SPVs, of which €200,000 was repaid to Helios in March 2016. No additional funds have since been borrowed. As of December 31, 2017, the outstanding balance under the Helios Loan was $2,804,736.

The Udine SPV Acquisition

Acquisition of our Udine SPV

On June 29, 2017, we entered into a Share Purchase Agreement (the “Udine SPA”) with Pronto Verde A.G. (“Pronto Verde”), relating to the purchase of one hundred percent (100%) of the share capital of Futuris Papia S.r.l., a limited liability company organized under the laws of Italy, which owns and operates a 995 Kw clean-tech plant for the production of electricity from vegetal oil located in Udine, Italy. In connection with the closing of the Udine SPA, Futuris Papia S.r.l. was converted into Futuris Papia S.p.A., a joint stock company organized under the laws of Italy (the “Udine SPV”).

On July 12, 2017, we entered into an Amendment Agreement to the Udine SPA with Pronto Verde and Bluesphere Italy S.r.l., an Italian limited liability company and our wholly-owned subsidiary (“Blue Sphere Italy”), whereby we assigned all of our rights, titles or interests arising out of the Udine SPA to Blue Sphere Italy. The parties also agreed to change the closing date to July 31, 2017. On July 31, 2017, the Company and Blue Sphere Italy entered into a Second and Third Amendment Agreement to the Udine SPA, pursuant to which (a) the closing date was extended to September 4, 2017 and (b) the Company agreed to pay to Pronto Verde an “Advance Payment” in an amount equal to €1,200,000 (USD $1,427,000).

On September 4, 2017, Blue Sphere Italy completed the acquisition of the Udine SPV. The Company paid an aggregate purchase price of €2,408,000 (approximately USD $2,864,051), subject to certain post-closing adjustments, consisting of an advance payment of €1,200,000 (approximately USD $1,427,268) paid on August 1, 2017, and €1,208,000 (approximately USD $1,436,783) paid by the Company at closing, using funds available pursuant to the Second Helios Loan Agreement (as defined below). The transaction included the following: (a) €1,217,000 (approximately USD $1,379,000) to repay the balance of a mortgage loan on the Udine SPV; (b) a commitment to supply feedstock fee and to operate the plant payable to Pronto Verde in the amount of €800,000 (approximately USD $906,000); (c) €100,000 (approximately USD $113,000) to be held in escrow; and (d) €132,000 (approximately USD $149,000) to a former shareholder of the Udine SPV.

The Helios Mezzanine Loan Facility

On August 30, 2017, the Company and Blue Sphere Italy entered into a Long Term Mezzanine Loan Agreement (the “Second Helios Loan Agreement”) with Helios 3 Italy Bio-Gas 2 L.P. (“Helios 3”), pursuant to which Helios 3 agreed to provide a mezzanine loan facility (the “Second Helios Loan”) of up to €1,600,000 (approximately USD $1,912,166) to finance (a) a portion of the total purchase price of the Udine SPV, (b) certain broker fees incurred in connection with the acquisition of the Udine SPV, and (c) taxes associated with registration of a pledge agreement. The Company’s liabilities and obligations under the Second Helios Loan Agreement are secured by a pledge of all of the Company’s shares of Blue Sphere Italy. In addition, any loan granted to Blue Sphere Italy by the Company shall rank subordinate to the Second Helios Loan.

13

The Second Helios Loan accrues interest at a rate of fourteen and one-half percent (14.5%) per annum, paid quarterly, beginning six (6) months following the closing of the Second Helios Loan. In addition, Helios 3 is entitled to an annual operation fee, paid quarterly. The final payment for the Second Helios Loan will become due no later than the earlier of (i) seven (7) years from the date the funds were made available to Blue Sphere Italy or (ii) the date of expiration of certain licenses granted to the Udine SPV. The Second Helios Loan may not be prepaid by the Company, but after payment by the Company of eight (8) quarterly payments, Helios 3 is entitled to demand repayment of the amount of the Second Helios Loan outstanding, provided that the amount shall not exceed the maximum distributable proceeds of the Udine SPV, by providing notice at least twenty-one (21) days prior to such demand. At such time the Company shall be entitled to refinance and prepay the entire amount outstanding under the Second Helios Loan, including the expected interest and operation fee due for the remaining period of the Second Helios Loan, less fifteen percent (15%) of the aggregate sum of such amounts. If the Company intends to refinance the Second Helios Loan, Helios shall have a right of first refusal to make a loan on the same terms.

In September 2017, we borrowed €1,408,000 ($1,682,500) under the Second Helios Loan Agreement to finance the purchase of the Udine SPV. No additional funds have since been borrowed. As of December 31, 2017, the balance of the Second Helios Loan was $1,686,432.

Operations of the Udine SPV

In accordance with a Guarantee Plant Operation Management Agreement, dated September 4, 2017 (the “GPOMA”), between Pronto Verde and the Udine SPV, Pronto Verde satisfied its guarantee to procure the services of CCEngineering S.r.l., a limited liability company duly incorporated and existing under the laws of Italy, to perform “all-inclusive” services for the operation and maintenance of the facilities, and ISG Sviluppo SA, a company duly incorporated and existing under the laws of Switzerland, to supply to the vegetal oil necessary for the regular functioning of the Udine SPV. The GPOMA became effective upon execution. On November 27, 2017, we notified the Seller that the Udine GPOMA was terminated because, in part, (a) the Seller did not successfully engage the designated supplier to supply vegetal oil, and Futuris Papia was forced to procure vegetal oil from another supplier at a higher cost; (b) the Seller and its operator did not diligently perform specified tasks under the Udine GPOMA, including a proper inspection and review of the facility and preparation of a takeover plan, and Futuris Papia was forced to procure such services from another operator at a higher cost than contemplated by the Udine GPOMA; and (c) due to a number of specified breaches by the Seller to perform under the Udine GPOMA. We reserved our right to recover the damages incurred as a consequence of documented material breaches made in connection with the Udine GPOMA.

Presently, Biogaservizi, the operator of our four other SPVs, is performing general operation and maintenance of the Udine SPV, and OMPI Mottaran S.r.l. is performing operation of the Udine SPV’s engine, subject to our supervision. We have agreed to operate in this capacity with the operators for a period of six (6) months, and then negotiate a longer term agreement for such services.