Attached files

| file | filename |

|---|---|

| EX-32.2 - BALLANTYNE STRONG, INC. | ex32-2.htm |

| EX-32.1 - BALLANTYNE STRONG, INC. | ex32-1.htm |

| EX-31.2 - BALLANTYNE STRONG, INC. | ex31-2.htm |

| EX-31.1 - BALLANTYNE STRONG, INC. | ex31-1.htm |

| EX-24 - BALLANTYNE STRONG, INC. | ex24.htm |

| EX-23.2 - BALLANTYNE STRONG, INC. | ex23-2.htm |

| EX-23.1 - BALLANTYNE STRONG, INC. | ex23-1.htm |

| EX-10.22 - BALLANTYNE STRONG, INC. | ex10-22.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2017 |

| OR |

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

| Commission File No. 1-13906 |

Ballantyne Strong, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 47-0587703 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

11422 Miracle Hills Drive, Suite 300 Omaha, Nebraska |

68154 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (402) 453-4444

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of exchange on which registered | |

| Common Stock, $0.01 par value | NYSE American |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports filed pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [X] | Non-accelerated filer [ ] (Do not check if a smaller reporting company) |

Smaller reporting company [ ]

Emerging growth company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes [ ] No [X]

The aggregate market value of the Company’s voting common stock held by non-affiliates, based upon the closing price of the stock on the NYSE American on June 30, 2017 was $63,729,857. The Company does not have any non-voting common equity. As of March 2, 2018, 14,422,090 shares of common stock of Ballantyne Strong, Inc., were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for its 2018 Annual Meeting of Stockholders are incorporated by reference in Part III, Items 10, 11, 12, 13 and 14.

TABLE OF CONTENTS

| 2 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In addition, forward-looking statements may be made in press releases, orally, at conferences, on the Company’s web site, or otherwise, by or on behalf of the Company. Statements that are not historical are forward-looking and reflect expectations for future Company performance. These statements often use words such as “anticipates,” “targets,” “expects,” “hopes,” “estimates,” “intends,” “plans,” “goal,” “believes,” “continue” and other similar expressions or future or conditional verbs such as “will,” “may,” “might,” “should,” “would” and “could.” These statements involve certain known and unknown risks, uncertainties and assumptions that are difficult to predict and are often beyond the Company’s control. For these statements, the Company claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

You should not place undue reliance on any forward-looking statement and should consider the following uncertainties and risks, as well as the risks and uncertainties more fully discussed elsewhere in this report, including under Item 1A. Risk Factors of this Annual Report on Form 10-K and in any of the Company’s subsequent Securities and Exchange Commission filings for further information about factors that could affect such forward-looking statements: the Company’s ability to expand its revenue streams, potential interruptions of supplier relationships or higher prices charged by suppliers, the Company’s ability to successfully compete and introduce enhancements and new features that achieve market acceptance and that keep pace with technological developments, the Company’s ability to successfully execute its capital allocation strategy, the Company’s ability to retain or replace its significant customers, the impact of a challenging global economic environment or a downturn in the markets, economic and political risks of selling products in foreign countries, risks of non-compliance with U.S. and foreign laws and regulations, cybersecurity risks and risks of damage and interruptions of information technology systems, the Company’s ability to retain key members of management and successfully integrate new executives, the Company’s ability to complete acquisitions, strategic investments, entry into new lines of business, divestitures, mergers or other transactions on acceptable terms or at all, the Company’s ability to assert its intellectual property rights, the impact of natural disasters and other catastrophic events, the adequacy of insurance and the impact of having a controlling stockholder.

Given the risks and uncertainties, readers should not place undue reliance on any forward-looking statements and should recognize that the statements are predictions of future results which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described herein, as well as others not now anticipated. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in the forward-looking statements. Except as required by law, the Company assumes no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

General Description of Business

Ballantyne Strong, Inc. (“Ballantyne” or the “Company”), a Delaware corporation, is a holding company with diverse business activities focused on serving the cinema, retail, financial, advertising and government markets. The Company and its wholly owned subsidiaries Strong Technical Services, Inc., Strong/MDI Screen Systems, Inc., Convergent Media Systems Corporation (“Convergent”) and Strong Digital Media, LLC design, integrate, and install technology solutions for a broad range of applications; develop and deliver out-of-home messaging, advertising and communications; manufacture projection screens; and provide managed services including monitoring of networked equipment to our customers. The Company’s wholly-owned subsidiary, StrongVest Global Advisors LLC, serves as advisor to an exchange-traded fund (“ETF”) issued by the StrongVest ETF Trust.

| 3 |

Ballantyne is a Delaware corporation which was founded in 1932 and became a designer and manufacturer of film projectors. For more than 85 years, we have expanded our product lines and services to meet the needs of the ever-changing and technologically-advancing theater exhibition industry. Most recently, we entered the digital media sector through an acquisition which enables us to serve the advertising, education and communication needs of retail, corporate, and government markets. Ballantyne went public in 1995; our shares are traded on the NYSE American market under the symbol “BTN.”

We conduct our operations through two primary business segments: Cinema and Digital Media. During the fourth quarter of 2017, we decided to reorganize our segments to move the operations of Strong Technical Services, Inc. from the Digital Media segment to the Cinema segment. All prior periods have been recast in our segment reporting to reflect the current segment organization.

Strategy

Our Board of Directors has implemented a strategy focused on making optimal capital allocation decisions across all of the Company’s businesses and investments. The Board intends to consider and make investments in the Company’s existing Cinema and Digital Media businesses when attractive opportunities arise. The Board also intends to consider and make investments in other industries that are expected to produce higher returns on invested capital. This may involve investments in public companies or the complete acquisitions of other businesses, which may be within or outside of the Company’s existing markets. We intend our investments in public companies to be made in circumstances where we believe that we will be able to exercise some degree of influence or control.

The Company now holds investments in several public companies. These investments include RELM Wireless Corporation (NYSE American: RWC), a manufacturer of two-way wireless radio communications equipment, 1347 Property Insurance Holdings, Inc. (Nasdaq: PIH), a provider of property and casualty insurance in the States of Louisiana, Texas and Florida, and Itasca Capital Ltd. (TSX Venture: ICL), a holding company that holds a significant position in Limbach Holdings, Inc. (Nasdaq: LMB), a leading commercial provider of HVAC construction and related services. As of December 31, 2017, the Company holds approximately 8.3% of the outstanding stock of RELM Wireless Corporation, approximately 17.4% of the outstanding stock of 1347 Property Insurance Holdings, Inc., and approximately 32.3% of the outstanding stock of Itasca Capital Ltd.

Fundamental Global Investors, LLC, the funds that it manages, its other affiliates, and the directors, officers and employees of the Company and their affiliates together currently hold approximately 41.2% of the Company’s outstanding stock. In some cases, funds managed by Fundamental Global Investors, LLC may acquire positions in the same public companies as the Company. Fundamental Global Investors’ funds currently hold positions in both RELM Wireless Corporation and 1347 Property Insurance Holdings, Inc.

In addition to the Company’s operating businesses and investments in public companies, the Board expects to consider investments and transactions in other areas that it believes are likely to increase returns to shareholders, such as continued stock buybacks and monetizing physical or other assets held by the company.

The Board expects that over time the Company will be further transformed into a holding company with ownership of and investments in diverse businesses.

Operating Segments

Cinema

Overview

We provide a full range of products and services to the theater exhibition industry from the design and installation of new theater exhibition systems and related equipment to maintenance and monitoring of existing systems. The systems include a wide spectrum of premier audio-visual products and accessories such as: digital projectors, state of the art projection screens, servers and library management systems, menu boards, flat panel displays, and sound systems.

| 4 |

We market and sell directly to theater exhibitors, as well as through certain domestic and international Value Added Resellers (“VAR”). Over the course of our 85-year history, we have developed ongoing customer relationships with a large portion of the theater owners in the United States and a number of the major theater owners internationally. Our sales and marketing staff principally develop business by maintaining regular personal contact with our established customer relationships, including conducting site visits. In our sales and marketing efforts, we emphasize our value proposition of providing the broadest range of products and services delivered by one of the industry’s largest technical service teams, which provides a significant resource to our clients in managing the complexities of digital technology in the cinema exhibition industry. Our sales and marketing professionals have extensive experience with the Company’s product lines and have long-term relationships throughout the industry.

Products

Screens — We manufacture multiple standard and large format 2D and 3D screens for cinema and special venue applications through our ISO-certified manufacturing facility in Canada. There are certain digital 3D applications, such as the technology by RealD, that require unique “silver” screens that we manufacture. In addition, we purchased Peintures Elite, Inc. in 2013, the manufacturer of coatings that have been exclusive to our Company in the manufacture of our screens. This relatively small acquisition positioned us to retain the exclusive rights to this coating and to continue producing our unique screens. We are constantly innovating to set new standards within the screen industry, and in 2013 we developed the new Premium HGA screen that diffuses light more evenly over the entire screen surface, thereby reducing the formation of so-called “hot spots.”

Screen Support Systems — Our custom screen support structures are designed and built with quality and safety as a priority. They are easy to assemble, require no scaffolding and each one includes detailed and easy to understand installation instructions. Our mechanical design and engineering team supervises every step of the process, from design to manufacturing, at one location.

Projectors — Through distribution agreements with NEC and Barco, we distribute DLP Cinema projectors in the Americas. Both manufacturers of the projectors use the DLP cinema technology from Texas Instruments. NEC offers DLP Cinema projectors ranging from their NC900 projector for screens up to 31 feet wide to the NC3240S, which is a 4K projector designed for screens up to 105 feet wide. Barco offers DLP Cinema projectors ranging from their DP2K-10SX projector for screens up to 33 wide feet to the DP4K-32B cinema projector, which is an ultra-bright enhanced 4K cinema projector for screens up to 105 feet wide.

Servers — Through a formal distribution agreement with GDC Technology (USA), LLC, we distribute GDC’s line of digital cinema servers in North and South America. We also distribute their servers in certain other areas of the world under less formal arrangements. In addition, we distribute servers for other server manufacturers, including those manufactured by Dolby. Digital servers and the related integrated media block are used by our customers for the storage and delivery of digital movie content.

Audio Systems — We distribute a range of state of the art digital audio systems, including surround and 3D sound technologies from the following manufacturers: Dolby, Barco, USL, JBL and QSC. Our technicians are certified by each manufacturer to install, service and maintain these and other audio systems.

Additional Projection Products — We also distribute certain third-party accessories, which when coupled with the cinema projector, server and integrated media block, can fully outfit and automate a projection booth. The significant accessories include, but are not limited to, library management systems, automation products, pedestals, 3D accessories, lenses and lamps.

Technical Services

Network Operations Center — Our Network Operations Centers (“NOC”), staffed by software engineers and systems techs, operate 24/7/365 and provide technical support to our customers to meet Service Level Agreements (“SLA”). From each location in Alpharetta, GA and Omaha, NE, we are able to monitor our customers’ networked equipment remotely, often providing proactive solutions to systems issues before they cause system failures. Our remote services include systems monitoring and maintenance, software upgrades and system repairs. By utilizing NOC personnel to solve customer issues whenever possible, we eliminate travel time and expenses normally incurred by sending a technician onsite for repairs. Many issues that do not involve parts replacement or physical contact with the hardware can be handled remotely using our remote assistance technologies.

| 5 |

Onsite Service and Maintenance — We provide digital cinema equipment installations and after-sale maintenance services. Our onsite technicians work closely with our NOC staff to resolve systems issues that cannot be fixed remotely; they are certified to install and service a wide array of digital and audio equipment from a number of manufacturers. We offer cabling, wiring, installation and maintenance services for digital equipment on ad hoc, as-needed basis. We also offer long-term contractual service packages for maintenance and repairs to a wide range of installed digital equipment for customers. These long-term contractual service packages provide our Company with recurring revenue.

Markets

We sell our screen systems worldwide, with our primary markets being North America and Asia.

Our non-exclusive distribution agreements with NEC and Barco allow us to market digital projectors in North and South America, including the Caribbean. In China we have distribution rights to sell Barco. We do not have any territorial restrictions for any of our other products and services.

We provide Cinema technical services in the United States. We market and sell our services directly to theater owners and through dealers or VAR networks.

Competition

Screens and Screen Support Systems –While there are numerous screen manufacturing companies, the primary competitor in the worldwide cinema screen market is Harkness Screens. Competitive factors include product performance characteristics, quality, availability and price.

Digital Projection Equipment — The markets for our products in the Cinema segment have been highly competitive. The primary competitive factors are price, product quality, features and customer support. Competition in the digital cinema equipment market includes one other licensed original equipment manufacturer (OEM) of the Texas Instruments’ DLP cinema technology besides our partners NEC and Barco: Christie Digital Systems. We also compete with Sony, which uses its own 4K digital cinema technology.

Technical Services – The competition in the cinema service industry for installation, after-sale maintenance, and NOC services is primarily driven by the two largest cinema service companies: the Company and Christie Digital, although there are other smaller scale providers.

Revenues

The following table summarizes net revenues for the Cinema segment by similar classes of products and services for each of the last three fiscal years (in thousands):

| Years ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| Screen systems sales | $ | 18,915 | $ | 20,207 | $ | 18,833 | ||||||

| Digital equipment sales | 12,996 | 17,734 | 25,119 | |||||||||

| Field maintenance and monitoring services | 12,834 | 12,579 | 11,780 | |||||||||

| Installation services | 1,155 | 460 | 1,550 | |||||||||

| Other | 3,037 | 3,795 | 3,557 | |||||||||

| Total segment revenue | $ | 48,937 | $ | 54,775 | $ | 60,839 | ||||||

| 6 |

Digital Media

Overview

The Company delivers digital signage solutions and services across two primary markets: digital out-of-home and enterprise video. In 2018, we will also begin providing advertising services as described below. These markets are served through the capabilities that we developed from the acquisition of Convergent in 2013. While there is digital signage equipment sold within this segment, the primary focus of this segment is providing solutions and services to our customers.

Solutions

Digital Signage – Our industry-first Digital Signage as a Service gives customers an end-to-end solution that includes hardware, software, content distribution, management, network monitoring and field services, all for a single monthly fee. Our “as-a-service” model lowers up-front customer capital costs, allows customers to scale more easily and allows them to ‘turn on’ or ‘turn-off’ features as needed. It also eliminates the risk of investing in quickly changing technologies, removes complexity and lessens resource burdens typically associated with traditional digital signage systems. We primarily market our solutions to large businesses in North America that do not have the resources, expertise or desire to create, manage and maintain their digital signage system internally. Customers typically require deployment across many locations and utilize digital signage to increase product sales, improve the consumer experience, enhance their brand or engage their audience.

Enterprise Video – We provide video communication services and solutions, including design, integration, monitoring, maintenance and installation for the government and corporate markets. These solutions provide enterprises with the infrastructure necessary to communicate, collaborate, train and educate employees.

Advertising – During the first quarter of 2018, we signed an agreement to provide advertising services on over 3,500 New York City taxicabs. The advertising will be on a combination of vinyl printed signs and digital signs. We have leased 300 digital signs, which we expect to install during the first half of 2018. The remainder of the taxicabs will initially feature print advertising. We expect to convert more taxicabs to digital signs over time.

Products and Services

Digital Signage as a Service (DSaaS) Platform – Our platform leverages internally developed and third-party software to automate the customer’s digital signage workflow, including from content creation, approval, storage and management, network deployment, monitoring, case management and incident resolution. Since it is cloud-based, it provides inherent scalability to enable customers to expand or contract their network. The DSaaS platform supports a wide range of applications – all of which are managed through a single user interface. New features and functionality are frequently added, both through the efforts of our in-house software development team and integration with an ever-growing ecosystem of third-party applications.

Content Creation – We provide creative services to digital signage clients that include media strategy, content design and production. Our creative services team develops custom content to support the branding and marketing initiatives of each client.

Content Management and Distribution – Content management is provided to ensure accurate playback at the right place and at the right time based on a number of factors such as geography, site characteristics, location within a site or consumer demographics. We utilize our DSaaS platform for the management and distribution of content. Content is prepared, scheduled and centrally distributed from our cloud infrastructure.

Network Operations Center – Our NOC in Alpharetta, GA provides similar services to our Digital Media customers as described under Cinema above.

Service and Maintenance — We provide digital signage installations and after-sale maintenance services. Our onsite technicians work closely with our NOC staff to resolve systems issues that cannot be fixed remotely; they are certified to install and service a wide array of digital and audio equipment from a number of manufacturers. We offer cabling, wiring, installation and maintenance services for digital menu boards and other digital equipment on ad hoc, as-needed basis. We also offer long-term contractual service packages for maintenance and repairs to digital signage equipment. These long-term contractual service packages provide our Company with recurring revenue.

| 7 |

Network Connectivity – We offer nationwide internet connectivity to fulfill content distribution and network management functions. We utilize third party providers for traditional terrestrial connectivity, as well as wireless service across North America.

Measurement and Analytics – We offer the tools and resources to measure the impact of digital signage solutions. We develop measurement criteria, establish benchmarks and identify control mechanisms to test the effectiveness of such solutions during proof of concept and full rollout scenarios.

Markets

Digital Out-of-Home – The Digital Out-of-Home (“DOOH”) advertising market is a subset of the overall OOH advertising market that includes in-store digital displays and interactive promotion kiosks. DOOH marketing campaigns consist of a network of digital displays that are centrally managed and target both mobile and captive customers outside the home. We are primarily focused on pursuing DOOH communication opportunities within the retail, banking, entertainment and corporate markets.

Enterprise Video Solutions – The Enterprise Video Solutions (“EVS”) market consists of customers seeking corporate video communications, employee training and system monitoring solutions. We are primarily focused on pursuing EVS opportunities within the government, banking, retail and corporate markets.

Competition

There are many players in the DOOH and EVS markets who have expertise in integration. Some of the key players include Diversified Media Group, Stratacache and Christie Digital.

Revenues

The following table summarizes net revenues for the Digital Media segment by similar classes of products and services for each of the last three fiscal years (in thousands):

| Years ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| Field maintenance and monitoring services | $ | 9,796 | $ | 9,023 | $ | 8,727 | ||||||

| Installation services | 8,598 | 7,275 | 5,876 | |||||||||

| Digital equipment sales | 4,932 | 5,613 | 2,512 | |||||||||

| Other | 1,158 | 85 | 318 | |||||||||

| Total segment revenue | $ | 24,484 | $ | 21,996 | $ | 17,433 | ||||||

Subsidiaries

As of December 31, 2017, we have the following wholly-owned operational subsidiaries:

| ● | Strong Technical Services, Inc. performs service work for all of our products. | |

| ● | Strong/MDI Screen Systems, Inc. manufactures cinema screens and related accessories. |

| ● | Convergent Media Systems Corporation performs all digital signage solutions and services. |

| ● | StrongVest Global Advisors, LLC serves as advisor to an exchange-traded fund (ETF). |

| 8 |

During the first quarter of 2018, we established a new subsidiary, Strong Digital Media, LLC, to provide advertising services within the Digital Media segment as described above.

Sale of Business

On May 17, 2017, the Company sold the operational assets of Strong Westrex, Inc. (“SWI”), a wholly-owned subsidiary of the Company, for total proceeds of $60 thousand. The Company recorded an insignificant gain on the sale of SWI.

Financial Instruments and Credit Risk Concentrations

The Company’s top ten customers accounted for approximately 53% of 2017 consolidated net revenues. Trade accounts receivable from these customers represented approximately 39% of net consolidated receivables at December 31, 2017. Sales to the following customers in fiscal 2017 exceeded 10% of our net revenues from continuing operations (dollars in thousands):

| Revenue | % | |||||||

| Regal Cinemas | $ | 7,978 | 10.9 | % | ||||

| Wells Fargo & Company | 7,797 | 10.7 | % | |||||

| American Multi-Cinema (AMC) | 7,593 | 10.4 | % | |||||

Manufacturing

We manufacture cinema screens through Strong/MDI, our screen subsidiary in Joliette, Quebec, Canada. These manufacturing operations consist of an 83,000 square-foot facility for the manufacture of cinema screen systems. These facilities include expanded PVC welding operations with programmable automations, as well as two 90-foot high screen coating towers with state of the art precision coating application software and painting systems. This world class ISO certified operation has the capability of manufacturing multiple standard screens simultaneously to large format 2D and 3D screens for cinema and special venue applications.

Quality Control

We believe that our quality control procedures and the quality standards for the products that we manufacture, distribute or service have contributed significantly to our reputation for high performance and reliability. The inspection of incoming materials and components as well as the testing of all of our products during various stages of the sales and service cycle are key elements of this program.

Trademarks

We own or otherwise have rights to various trademarks and trade names used in conjunction with the sale of our products. We believe our success will not be dependent upon trademark protection, but rather upon our scientific and engineering capabilities and research and production techniques. We consider the following trademarks to be of value to our business: Strong® and Convergent™.

Employees

We employed 335 persons at December 31, 2017. Of these employees, 162 positions were considered manufacturing or operational, 90 were service related and 83 were considered sales and administrative. We are not a party to any collective bargaining agreement.

| 9 |

Seasonality

Generally, our business exhibits a minimal level of seasonality.

Regulation

We are subject to complex laws, rules and regulations affecting our domestic and international operations relating to, for example, environmental, safety and health requirements; exports and imports; bribery and corruption; tax; data privacy; labor and employment; competition; and intellectual property ownership and infringement. Compliance with these laws, rules and regulations may be onerous and expensive, and if we fail to comply or if we become subject to enforcement activity, our ability to manufacture our products and operate our business could be restricted and we could be subject to fines, penalties or other legal liability. Furthermore, should these laws, rules and regulations be amended or expanded, or new ones enacted, we could incur materially greater compliance costs or restrictions on our ability to manufacture our products and operate our business.

Some of these complex laws, rules and regulations – for example, those related to environmental, safety and health requirements – may particularly affect us in the jurisdictions in which we manufacture products, especially if such laws and regulations: require the use of abatement equipment beyond what we currently employ; require the addition or elimination of a raw material or process to or from our current manufacturing processes; or impose costs, fees or reporting requirements on the direct or indirect use of energy, or of materials or gases used or emitted into the environment, in connection with the manufacture of our products. There can be no assurance that in all instances a substitute for a prohibited raw material or process would be available, or be available at reasonable cost.

Executive Officers of the Company

D. Kyle Cerminara, age 40, has been Executive Chairman since September of 2015 and Chief Executive Officer since November of 2015. Mr. Cerminara has served on the Board of Directors since February of 2015.

Ray F. Boegner, age 68, has been President of the Cinema business since November of 2015. Mr. Boegner joined us in 1985 and has acted in various sales roles for our Company, including as Senior Vice President from 1997 to 2015.

Stephen L. Schilling, age 53, has been President of the Digital Media business since November of 2015.

Lance V. Schulz, age 50, has been Senior Vice President, Chief Financial Officer and Treasurer since March of 2017.

Information Available on Ballantyne Website

We make available free of charge on our website (www.ballantynestrong.com), through a link to the Securities and Exchange Commission (“SEC”) website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. However, information posted on our website is not part of the Form 10-K. The Board of Directors has adopted the following governance documents, which are also posted on our website:

| ● | Code of Ethics | |

| ● | Audit Committee Charter | |

| ● | Nominating and Corporate Governance Committee Charter | |

| ● | Compensation Committee Charter |

| 10 |

These corporate governance documents are also available in print to any stockholder upon request by writing to:

| Corporate

Secretary Ballantyne Strong, Inc. 11422 Miracle Hills Drive, Suite 300 Omaha, NE 68154 |

Financial Information About Segments and Geographic Areas

The financial information about segments and geographic areas is included in Note 17 of our consolidated financial statements in this report.

Our business and financial performance are subject to various risks and uncertainties, some of which are beyond our control. We discuss in this section some of the risk factors that, if they actually occurred, could materially and adversely affect our business, financial condition and results of operations. In that event, the trading price of our common stock could decline and you may lose part or all of your investment. You should consider these risk factors in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K because these factors could cause our actual results and financial condition to differ materially from those projected in forward-looking statements. We undertake no obligation to revise or update any forward-looking statements contained herein to reflect subsequent events or circumstances or the occurrence of unanticipated events.

If we are unable to expand our revenue streams to compensate for the lower demand for our digital cinema products and installation services, our business, financial condition and results of operations could be materially adversely affected.

A significant portion of our revenue in recent years has been generated from the theater exhibition industry’s need for digital cinema equipment and services to support the industry’s transformation from film to digital equipment. This transition required us to commit substantial resources to the process of retrofitting existing theater complexes by removing the film equipment and replacing it with digital equipment, and we experienced significant financial gains from this work. With the completion of this digital conversion by North America theater exhibitors, we are no longer able to rely on that income as a major source of our earnings. If we are unable to expand our revenue streams with other products and services, our future growth would be significantly curtailed.

Interruptions of, or higher prices of, components from our suppliers may affect our results of operations and financial performance.

A portion of our revenues are dependent on the distribution of products supplied by various key suppliers. If we fail to maintain satisfactory relationships with our suppliers, or if our suppliers experience significant financial difficulties, we could experience difficulty in obtaining needed goods and services. Some suppliers could also decide to reduce inventories or raise prices to increase cash flow. The loss of any one or more of our suppliers could have an adverse effect on our business, and we may be unable to secure alternative manufacturing arrangements. Even if we are able to obtain alternative manufacturing arrangements, such arrangements may not be on terms similar to our current arrangements or we may be forced to accept less favorable terms in order to secure a supplier as quickly as possible so as to minimize the impact on our business operations. In addition, any required changes in our suppliers could cause delays in our operations and increase our production costs and new suppliers may not be able to meet our production demands as to volume, quality or timeliness.

| 11 |

The markets for our products and services are highly competitive and if market share is lost, we may be unable to lower our cost structure quickly enough to offset the loss of revenue.

Within the cinema market, the domestic and international markets for our product lines are highly competitive, evolving and subject to rapid technological and other changes. Our Digital Media business, in particular, is highly dependent on technology. We expect the intensity of competition in each of these areas to continue in the future for a number of reasons including:

| ● | Certain of the competitors for our digital equipment have longer operating histories and greater financial, technical, marketing and other resources than we do, which, among other things, may permit them to adopt aggressive pricing policies. As a result, we may suffer from pricing pressures that could adversely affect our ability to generate revenues and our results of operations. Some of our competitors also have greater name and brand recognition and a larger customer base than us. | |

| ● | Some of our competitors are manufacturing their own digital equipment while we employ a distribution business model through our distribution agreements with NEC, BARCO and certain other suppliers. As a result, we may suffer from pricing pressures that could adversely affect our ability to generate revenues. | |

| ● | Suppliers could decide to utilize their current sales force to supply their products directly to customers rather than utilizing channels. |

In addition, we face competition for consumer attention from other forms of entertainment. The other forms of entertainment may be more attractive to consumers than those utilizing our technologies, which could harm our business, prospects and operating results.

For these and other reasons, we must continue to enhance our technologies and our existing products and services and introduce new high quality technologies, products and services to meet the wide variety of competitive pressures that we face. If we are unable to compete successfully, our business, prospects and results of operations will be materially adversely impacted.

Our capital allocation strategy may not be successful, which could adversely impact our financial condition.

We intend to continue investing part of our cash balances in public companies. We intend our investments in public companies to be made in circumstances where we believe that we will be able to exercise some degree of influence or control. To date, our investments are highly concentrated in three public companies – 1347 Property Insurance Holdings, Inc. (Nasdaq: PIH), RELM Wireless Corporation (NYSE American: RWC) and Itasca Capital Ltd. (TSX Venture: ICL). In some cases, funds controlled by the Company’s affiliate Fundamental Global Investors, LLC have, and may in the future, acquire positions in the same public companies as the Company. These types of investments are riskier than holding our cash balances as bank deposits or, for example, such conservative investments as treasury bonds or money market funds. There can be no assurance that we will be able to maintain or enhance the value or the performance of the companies in which we have invested or may invest in the future, or that we will achieve returns or benefits from these investments. Under certain circumstances, significant declines in the fair values of these investments may require the recognition of other-than-temporary impairment losses. We may lose all or part of our investment relating to such companies if their value decreases as a result of their financial performance or for any other reason. If our interests differ from those of other investors in companies over which we do not have control, we may be unable to effect any change at those companies. We are not required to meet any diversification standards, and our investments may continue to remain concentrated. If our capital allocation strategy is not successful or we achieve less than expected returns from these investments, it could have a material adverse effect on us. The Board of Directors may also change our capital allocation strategy at any time, and such changes could further increase our exposure, which could adversely impact us.

If we are not able to develop and introduce enhancements and new features that achieve market acceptance or that keep pace with technological developments, our business could be harmed.

We operate in a dynamic environment characterized by rapidly changing technologies and industry and legal standards. Innovation is critical to our success. The introduction of new software solutions by our competitors, the market acceptance of solutions based on new or alternative technologies or the emergence of new industry standards could render our platform obsolete. Our ability to compete successfully, attract new customers and increase revenues from existing customers depends in part on our ability to enhance and improve our existing software platform and to identify new software partners, which would allow us to continually introduce or acquire new features that are in demand by the market that we serve. The success of any enhancement or new solution depends on several factors, including timely completion and integration, adequate quality testing, introduction and market acceptance. Any new platform or feature that we develop or acquire may not be introduced in a timely or cost-effective manner, may contain defects or may not achieve the broad market acceptance necessary to generate significant revenues. If we are unable to anticipate, or timely and successfully develop or acquire, new offerings or features, or enhance our existing platform to meet customer requirements, our business and operating results will be adversely affected. Additionally, for technologies that are acquired, we may not be able to successfully integrate or monetize the acquired technology at a rate that is consistent with the market’s expectations, which could have a material adverse impact on us.

| 12 |

If we are unable to maintain our brand and reputation, our business, results of operations and prospects could be materially harmed.

Our business, results of operations and prospects depend, in part, on maintaining and strengthening our brand and reputation for providing high quality products and services. Reputational value is based in large part on perceptions. Although reputations may take decades to build, any negative incidents can quickly erode trust and confidence, particularly if they result in adverse publicity, governmental investigations or litigation. If problems with our products cause operational disruption or other difficulties, or there are delays or other issues with the delivery of our products or services, our brand and reputation could be diminished. Damage to our reputation could also arise from actual or perceived legal violations, product safety issues, data security breaches, actual or perceived poor employee relations, actual or perceived poor service, actual or perceived poor privacy practices, operational or sustainability issues, actual or perceived ethical issues or other events within or outside of our control that generate negative publicity with respect to us. Any event that has the potential to negatively impact our reputation could lead to lost sales, loss of new opportunities and retention and recruiting difficulties. If we fail to promote and maintain our brand and reputation successfully, our business, results of operations and prospects could be materially harmed.

Our sales cycle can be long and unpredictable, particularly with respect to large enterprises, which could harm our business and operating results.

The timing of our sales is difficult to predict. Our sales efforts involve educating our customers, frequently at an executive level, about the use, potential return on investment, technical capabilities, security and other benefits of our solution. Customers often undertake a prolonged product-evaluation process, which frequently involves not only our solutions but also those of our competitors. As we continue to target our sales efforts at large enterprise customers, we will face greater costs, long sales cycles and less predictability in completing some of our sales. In this market segment, the customer’s decision to subscribe to our solution is often an enterprise-wide decision and may require us to provide even greater levels of education regarding the use and benefits of our solution and obtain support from multiple departments. In addition, prospective enterprise customers may require customized features and functions unique to their business process that may need acceptance testing related to those unique features. As a result of these factors, these sales opportunities may require us to devote greater sales support, operational support and professional services resources to individual customers, increasing costs and time required to complete sales and diverting our own sales and professional services resources to a smaller number of larger transactions. The long and unpredictable nature of our sales cycle could materially adversely impact our business and results of operations.

We are substantially dependent upon significant customers who could cease purchasing our products at any time.

The Company’s top ten customers accounted for approximately 53% of 2017 consolidated net revenues. Trade accounts receivable from these customers represented approximately 39% of net consolidated receivables at December 31, 2017. We had three customers that each individually accounted for over 10% of our consolidated net revenues in 2017. Most arrangements with these customers are made by purchase order and are terminable at will by either party. A significant decrease or interruption in business from the Company’s significant customers could have a material adverse effect on the Company’s business, financial condition and results of operations.

The Company has deferred tax assets that are subject to annual valuation testing, which assets may not be realized, thus negatively impacting us.

The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income. We consider the scheduled reversal of taxable temporary differences, projected future taxable income and tax planning strategies in making this assessment. A cumulative loss in a particular tax jurisdiction in recent years is a significant piece of evidence with respect to the realizability that is difficult to overcome. Based on the available objective evidence, including recent updates to the taxing jurisdictions generating income, we concluded that we should maintain our valuation allowance against our U.S. deferred tax assets as of December 31, 2017. We face risks that our recorded deferred tax assets may not be realized, thus negatively impacting us.

| 13 |

Our business is subject to the economic and political risks of selling products in foreign countries.

Sales outside the United States (mainly cinema) continue to be significant, accounting for approximately 21% of consolidated sales in fiscal 2017. We expect that international sales will continue to be important to our business for the foreseeable future. Foreign sales are subject to general political and economic risks, including the recent presidential and congressional elections in the United States, which have created uncertainty regarding international trade, unanticipated or unfavorable circumstances arising from host country laws or regulations, unfavorable changes in U.S. policies on international trade and investment, the imposition of governmental economic sanctions on countries in which we do business, quotas, capital controls or other trade barriers, whether adopted by individual governments or addressed by regional trade blocks, threats of war, terrorism or governmental instability, currency controls, fluctuating exchange rates with respect to sales not denominated in U.S. dollars, changes in import/export regulations, tariffs and freight rates, potential negative consequences from changes to taxation policies, restrictions on the transfer of funds into or out of a country and the disruption of operations from labor and political disturbances. Government policies on international trade and investment can affect the demand for our products, impact the competitive position of our products or prevent us from being able to sell or manufacture products in certain countries. The implementation of more restrictive trade policies, such as higher tariffs or new barriers to entry, in countries in which we sell large quantities of products and services could negatively impact our business, results of operations and financial condition. For example, a government’s adoption of “buy national” policies or retaliation by another government against such policies could have a negative impact on our results of operations. If we were unable to navigate the foreign regulatory environment, or if we were unable to enforce our contract rights in foreign countries, our business could be adversely impacted. Any of these events could reduce our sales, limit the prices at which we can sell our products, interrupt our supply chain or otherwise have an adverse effect on our operating performance.

In addition, a portion of our foreign sales are denominated in foreign currencies and amounted to $4.7 million in 2017. To the extent that orders are denominated in foreign currencies, our reported sales and earnings are subject to foreign exchange fluctuations. In addition, there can be no assurance that our remaining international customers will continue to accept orders denominated in U.S. dollars. For those sales which are denominated in U.S. dollars, a weakening in the value of foreign currencies relative to the U.S. dollar could have a material adverse impact on us by increasing the effective price of our products in international markets. Certain areas of the world are also more cost conscious than the U.S. market and there are instances where our products are priced higher than local manufacturers. We are also exposed to foreign currency fluctuations between the Canadian and U.S. dollar due to our screen manufacturing facility in Canada where a majority of its sales are denominated in the U.S. dollar while its expenses are denominated in Canadian currency. We cannot predict the effects of exchange rate fluctuations upon our future operating results because of the number of currencies involved, the variability of currency exposures and the potential volatility of currency exchange rates.

Any of these factors could adversely affect our foreign activities and our business, financial condition and results of operations.

The risk of non-compliance with U.S. and foreign laws and regulations applicable to our international operations could have a significant impact on our results of operations, financial condition and strategic objectives.

Our global operations subject us to regulation by U.S. federal and state laws and multiple foreign laws, regulations and policies, which could result in conflicting legal requirements. These laws and regulations are complex, change frequently, have tended to become more stringent over time and increase our cost of doing business. These laws and regulations include import and export control, environmental, health and safety regulations, data privacy requirements, international labor laws and work councils and anti-corruption and bribery laws such as the U.S. Foreign Corrupt Practices Act, the U.N. Convention Against Bribery and local laws prohibiting corrupt payments to government officials. We are subject to the risk that we, our employees, our affiliated entities, contractors, agents or their respective officers, directors, employees and agents may take action determined to be in violation of any of these laws. An actual or alleged violation could result in substantial fines, sanctions, civil or criminal penalties, and debarment from government contracts, curtailment of operations in certain jurisdictions, competitive or reputational harm, litigation or regulatory action and other consequences that might adversely affect our results of operations, financial condition and strategic objectives.

| 14 |

A reversal of the U.S. economic recovery and a return to volatile or recessionary conditions in the United States or abroad could adversely affect our business or our access to capital markets in a material manner.

Worsening economic and market conditions, downside shocks, or a return to recessionary economic conditions could serve to reduce demand for our products and adversely affect our operating results. These economic conditions may also impact the financial condition of one or more of our key suppliers, which could affect our ability to secure product to meet our customers’ demand. In addition, a downturn in the cinema market could impact the valuation and collectability of certain long-term receivables held by us. We could also be adversely affected by such factors as changes in foreign currency rates and weak economic and political conditions in each of the countries in which we sell our products.

We rely extensively on our information technology systems and are vulnerable to damage and interruption.

We rely on our information technology systems and infrastructure to process transactions, summarize results and manage our business, including maintaining client and supplier information. Additionally, we utilize third parties, including cloud providers, to store, transfer and process data. Our information technology systems, as well as the systems of our customers, suppliers and other partners, are vulnerable to outages and an increasing risk of continually evolving deliberate intrusions to gain access to company sensitive information. Likewise, data security incidents and breaches by employees and others with or without permitted access to our systems pose a risk that sensitive data may be exposed to unauthorized persons or to the public. We may be unable to prevent outages or security breaches in our systems that could adversely affect our results of operations and cash flows, as well as our business reputation.

Any failure to maintain the security of information relating to our customers, employees and suppliers, whether as a result of cybersecurity attacks or otherwise, could expose us to litigation, government enforcement actions and costly response measures, and could disrupt our operations and harm our reputation.

In connection with the sales and marketing of our products and services, we may from time to time transmit confidential information. We also have access to, collect or maintain private or confidential information regarding our customers, employees, and suppliers, as well as our business. Cyberattacks are rapidly evolving and becoming increasingly sophisticated. It is possible that computer hackers and others might compromise our security measures, or security measures of those parties that we do business with now or in the future, and obtain the personal information of our customers, employees and suppliers or our business information. A security breach of any kind, including physical or electronic break-ins, computer viruses and attacks by hackers, employees or others, could expose us to risks of data loss, litigation, government enforcement actions and costly response measures, and could seriously disrupt our operations. Any resulting negative publicity could significantly harm our reputation, which could cause us to lose market share and have an adverse effect on our results of operations.

If we fail to retain key members of management, or successfully integrate new executives, our business may be materially harmed.

Our future success depends, in substantial part, on the efforts and abilities of our current management team. If certain of these individuals were to leave unexpectedly, we could experience substantial loss of institutional knowledge, face difficulty in hiring qualified successors and could experience a loss in productivity while any successor obtains the necessary training and experience. Our loss of services of any of our senior executives, or any failure to effectively integrate new management into our business processes, controls, systems and culture, could have a material adverse effect on us.

We have made changes to our management team in recent years. On November 24, 2015, the Board of Directors appointed D. Kyle Cerminara as our Chairman and Chief Executive Officer, effective immediately. Mr. Cerminara has been a member of the Board since February 2015 and has served as its Chairman since May 2015, assuming the role of Executive Chairman in September 2015. On November 2, 2015, Stephen L. Schilling joined us as President of the Digital Media business, and Ray F. Boegner was promoted to the newly created position of President of the Cinema business. On March 29, 2017, Lance V. Schulz was appointed as our Senior Vice President, Chief Financial Officer and Treasurer. These or other changes in key management could create uncertainty among our employees, suppliers and other business partners and are resulting in changes to the strategic direction of our business, any of which could have a material adverse effect on us.

| 15 |

Our previous and any potential future acquisitions, strategic investments, entry into new lines of business, divestitures, mergers or joint ventures may subject us to significant risks, any of which could harm our business.

Our long-term strategy may include identifying and acquiring, investing in or merging with suitable candidates on acceptable terms, entry into new lines of business and markets or divesting of certain business lines or activities. In particular, over time, we may acquire, make investments in or merge with providers of product offerings that complement our business or may terminate such activities. Mergers, acquisitions, divestitures and entries into new lines of business include a number of risks and present financial, managerial and operational challenges, including but not limited to:

| ● | diversion of management attention from running our existing business; | |

| ● | possible material weaknesses in internal control over financial reporting; | |

| ● | increased expenses including legal, administrative and compensation expenses related to newly hired or terminated employees; | |

| ● | increased costs to integrate, develop or, in the case of a divestiture, separate the technology, personnel, customer base and business practices of the acquired, new or divested business or assets; | |

| ● | potential exposure to material liabilities not discovered in the due diligence process; | |

| ● | potential adverse effects on reported operating results due to possible write-down of goodwill and other intangible assets associated with acquisitions; | |

| ● | potential damage to customer relationships or loss of synergies in the case of divestitures; and | |

| ● | unavailability of acquisition financing or inability to obtain such financing on reasonable terms. |

Any acquired business, technology, service or product or entry into a new line of business could significantly under-perform relative to our expectations, and may not achieve the benefits we expect. For example, our entry into the taxicab advertising line of business in 2018 poses many of the risks discussed above. For all these reasons, our pursuit of an acquisition, investment, new line of business, divestiture, merger or joint venture could cause our actual results to differ materially from those anticipated.

Failure to effectively utilize or successfully assert intellectual property rights could negatively impact us.

We own or otherwise have rights to various trademarks and trade names used in conjunction with the sale of our products, the most significant of which are Strong® and Convergent™. We rely on trademark laws to protect these intellectual property rights. We cannot assure that these intellectual property rights will be effectively utilized or, if necessary, successfully asserted. There is a risk that we will not be able to obtain and perfect our own intellectual property rights, or, where appropriate, license from others, intellectual property rights necessary to support new product introductions. Our intellectual property rights, and any additional rights we may obtain in the future, may be invalidated, circumvented or challenged in the future. Our failure to perfect or successfully assert intellectual property rights could harm our competitive position and could negatively impact us.

| 16 |

Natural disasters and other catastrophic events beyond our control could adversely affect our business operations and financial performance.

The occurrence of one or more natural disasters, such as fires, hurricanes, tornados, tsunamis, floods and earthquakes; geo-political events, such as civil unrest in a country in which our suppliers are located or terrorist or military activities disrupting transportation, communication or utility systems; or other highly disruptive events, such as nuclear accidents, pandemics, unusual weather conditions or cyberattacks, could adversely affect our operations and financial performance. Such events could result, among other things, in operational disruptions, physical damage to or destruction or disruption of one or more of our properties or properties used by third parties in connection with the supply of products or services to us, the lack of an adequate workforce in parts or all of our operations and communications and transportation disruptions. These factors could also cause consumer confidence and spending to decrease or result in increased volatility in the United States and global financial markets and economy. Such occurrences could have a material adverse effect on us and could also have indirect consequences such as increases in the costs of insurance if they result in significant loss of property or other insurable damage.

The insurance that we maintain may not fully cover all potential exposures.

We maintain property, business interruption and casualty insurance but such insurance may not cover all risks associated with the hazards of our business and is subject to limitations, including deductibles and maximum liabilities covered. We are potentially at risk if one or more of our insurance carriers fail. Additionally, severe disruptions in the domestic and global financial markets could adversely impact the ratings and survival of some insurers. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

Entities affiliated with Fundamental Global Investors, LLC, whose interests may differ from the interests of our other stockholders, have significant influence over the Company.

The interests of Fundamental Global Investors, LLC and its affiliates may differ from the interests of our other stockholders. Fundamental Global Investors, LLC and its affiliates hold approximately 28.7% of the Company’s outstanding shares of common stock as of December 31, 2017. Mr. Cerminara, the Chief Executive Officer, Co-Founder and Partner of Fundamental Global Investors, LLC, serves as our Chairman and Chief Executive Officer. In addition, Lewis M. Johnson, the President, Co-Founder and Partner of Fundamental Global Investors, LLC, serves as a member of our board of directors. As a result of its ownership position and Mr. Cerminara’s and Mr. Johnson’s positions with the Company, Fundamental Global Investors, LLC has the ability to exert significant influence over our policies and affairs, including the power to impact the election of our directors, appointment of our management and approval of any action requiring a shareholder vote, such as amendments to our certificate of incorporation, bylaws, significant stock issuances, mergers and asset sales. Fundamental Global Investors, LLC may have interests that differ from those of our other stockholders and may vote in a way with which our other stockholders disagree and which may be adverse to their interests. Fundamental Global Investors, LLC’s significant ownership may also have the effect of delaying, preventing or deterring a change of control of the Company, could deprive our stockholders of an opportunity to receive a premium for their common stock as part of a sale of the Company and might ultimately affect the market price of our common stock.

Our stock price is vulnerable to significant fluctuations.

The trading price of our common stock has been highly volatile in the past and could be subject to significant fluctuations in response to variations in quarterly operating results, general conditions in the industries in which we operate and other factors. In addition, the stock market is subject to price and volume fluctuations affecting the market price for the stock of many companies generally, which fluctuations often are unrelated to operating performance.

Item 1B. Unresolved Staff Comments

The Company has no unresolved staff comments to report pursuant to this item.

| 17 |

Our headquarters are located at 11422 Miracle Hills Drive, Omaha, Nebraska, where we lease office space. The premises are used for offices supporting both of our operating segments and operating the Omaha NOC. The lease expires in November 2021. In addition, our subsidiaries owned or leased the following facilities as of December 31, 2017:

| ● | Our Strong/MDI Screen Systems, Inc. subsidiary owns an 83,000 square-foot manufacturing plant in Joliette, Quebec, Canada. The facilities are used for offices, manufacturing, assembly and distribution of the cinema and other screens. We believe this facility is well maintained and adequate for future needs, and is used by our Cinema segment. | |

| ● | In addition, the Company leases office space in Mooresville, North Carolina, which is used by both of our operating segments. The lease expires in November of 2020. | |

| ● | Our Convergent Media Systems Corporation subsidiary owns a 43,000 square-foot office facility in Alpharetta, Georgia, which is subject to first and second lien deeds of trust as described in Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations, Liquidity and Capital Resources. The facility is used for offices and operating the Alpharetta NOC. Convergent also leases our distribution facility, which is in Lawrenceville, Georgia, where we lease approximately 40,000 square feet. The lease expires in April 2020. The premises are used for distribution of certain products. In addition, Convergent leases two office facilities in Toronto, Ontario, Canada. These leases expire in March 2018 and October 2019. The office lease expiring March 2018 is not being renewed, as we intend to consolidate our Toronto operations into the remaining location. We believe these facilities are adequate for future needs and are used by both of our operating segments. |

We do not anticipate any difficulty in retaining occupancy of any leased facilities, either by renewing leases prior to expiration or replacing them with equivalent leased facilities.

In the ordinary course of our business operations, we are involved, from time to time, in certain legal disputes. No such disputes, individually or in the aggregate, are expected to have a material effect on our business or financial condition.

Item 4. Mine Safety Disclosures

Not applicable.

| 18 |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is listed and traded on the NYSE American under the symbol “BTN.” The following table sets forth the high and low per share sale price for the common stock as reported by the NYSE American.

| High | Low | |||||||||

| 2017 | First Quarter | $ | 8.10 | $ | 5.70 | |||||

| Second Quarter | 7.35 | 5.60 | ||||||||

| Third Quarter | 7.00 | 5.50 | ||||||||

| Fourth Quarter | 6.55 | 4.05 | ||||||||

| 2016 | First Quarter | $ | 4.77 | $ | 4.00 | |||||

| Second Quarter | 5.99 | 4.21 | ||||||||

| Third Quarter | 7.01 | 5.09 | ||||||||

| Fourth Quarter | 8.00 | 6.10 | ||||||||

According to the records of our transfer agent, we had 113 stockholders of record of our common stock on March 2, 2018. Because brokers and other institutions hold many of our shares on behalf of stockholders, we are unable to estimate the total number of stockholders represented by these record holders. The last reported per share sale price for the common stock on March 2, 2018 was $5.25. We had 14,422,090 shares of common stock outstanding on March 2, 2018.

Stock Repurchases

On August 20, 2015, we announced that our Board of Directors adopted a stock repurchase program authorizing the repurchase of up to 700,000 shares of our outstanding common stock pursuant to a plan adopted under Rule 10b5-1 of the Securities Exchange Act of 1934 (as amended). The program has no expiration date. There were no repurchases during the fourth quarter of 2017. As of December 31, 2017, there were 636,931 shares that may yet be purchased under the stock repurchase program.

Dividend Policy

We intend to retain our earnings to assist in financing our business and making investments and do not anticipate paying cash dividends on our common stock in the foreseeable future. The declaration and payment of dividends by the Company are also subject to the discretion of the Board. Any determination by the Board as to the payment of dividends in the future will depend upon, among other things, business conditions, our financial condition and capital requirements, as well as any other factors deemed relevant by the Board. We have not paid cash dividends since we went public in 1995.

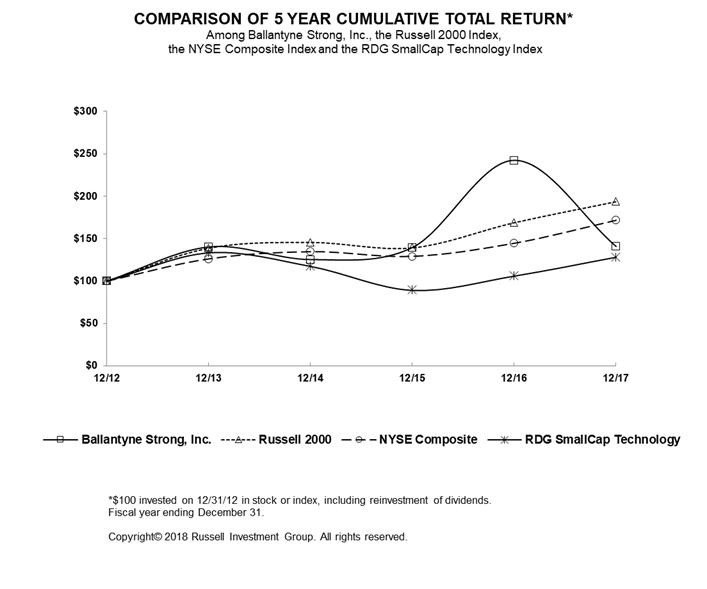

PERFORMANCE GRAPH

The following graph compares Ballantyne’s cumulative total stockholder return over the last five fiscal years with the cumulative total returns of the New York Stock Exchange Composite Index (“NYSE”), the Russell 2000 Index and the Research Data Group, Inc. (“RDG”) SmallCap Technology Index. The graph assumes $100 was invested on December 31, 2012, and assumes reinvestment of all dividends.

| 19 |

| 12/12 | 12/13 | 12/14 | 12/15 | 12/16 | 12/17 | |||||||||||||||||||

| Ballantyne Strong, Inc. | 100.00 | 140.30 | 125.45 | 139.70 | 242.42 | 140.91 | ||||||||||||||||||

| Russell 2000 | 100.00 | 138.82 | 145.62 | 139.19 | 168.85 | 193.58 | ||||||||||||||||||

| NYSE Composite | 100.00 | 126.28 | 134.81 | 129.29 | 144.73 | 171.83 | ||||||||||||||||||

| RDG SmallCap Technology | 100.00 | 133.48 | 117.53 | 89.29 | 106.10 | 128.29 |

Item 6. Selected Financial Data

The selected statement of operations data for the years ended December 31, 2017, 2016 and 2015, and the selected balance sheet data at December 31, 2017 and 2016, are derived from, and are qualified by reference to, the audited consolidated financial statements of the Company included elsewhere in this Annual Report on Form 10-K. The selected statement of operations data for the years ended December 31, 2014 and 2013, and the balance sheet data at December 31, 2015, 2014, and 2013, are derived from audited consolidated financial statements not included herein. The Company acquired Peintures Elite, Inc. on September 13, 2013 and Convergent Media Systems on October 1, 2013. In addition, the Company reclassified a portion of selected operations to discontinued operations in 2016. All prior periods have been restated to reflect the reclassification. See Note 2 to the Company’s consolidated financial statements.

| 20 |

| Year Ended December 31, | ||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Statement of operations data | ||||||||||||||||||||

| Net revenue | $ | 72,646 | $ | 76,254 | $ | 78,059 | $ | 83,165 | $ | 88,891 | ||||||||||

| Gross profit | $ | 18,934 | $ | 21,156 | $ | 16,712 | $ | 17,089 | $ | 15,434 | ||||||||||

| Net (loss) earnings from continuing operations | $ | (3,592 | ) | $ | 869 | $ | (16,724 | ) | $ | 142 | $ | 252 | ||||||||

| Net (loss) earnings per share from continuing operations | ||||||||||||||||||||

| Basic | $ | (0.25 | ) | $ | 0.06 | $ | (1.19 | ) | $ | 0.01 | $ | 0.02 | ||||||||

| Diluted | $ | (0.25 | ) | $ | 0.06 | $ | (1.19 | ) | $ | 0.01 | $ | 0.02 | ||||||||

| Balance sheet data | ||||||||||||||||||||

| Working capital | $ | 13,562 | $ | 19,433 | $ | 28,179 | $ | 40,228 | $ | 44,042 | ||||||||||

| Total assets | $ | 59,014 | $ | 62,439 | $ | 66,864 | $ | 82,060 | $ | 83,630 | ||||||||||

| Long-term debt, net of current portion | $ | 1,870 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Stockholders' equity | $ | 44,122 | $ | 45,154 | $ | 44,512 | $ | 60,847 | $ | 61,499 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with the consolidated financial statements and notes thereto appearing elsewhere in this report. Management’s discussion and analysis contains not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements that are not historical are forward-looking and reflect expectations for future Company performance. For these statements, the Company claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve a number of risks and uncertainties, including but not limited to those discussed in the “Risk Factors” section contained in Item 1A. Given the risks and uncertainties, readers should not place undue reliance on any forward-looking statement and should recognize that the statements are predictions of future results which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described herein, as well as others not now anticipated. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Except as required by law, the Company assumes no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

Overview

The Company is a holding company with diverse business activities focused on serving the cinema, retail, financial, advertising and government markets. It designs, integrates, and installs technology solutions for a broad range of applications; develops and delivers out-of-home messaging, advertising and communications; manufactures projection screens; and provides managed services, including monitoring of networked equipment, to our customers. We add value through our design, engineering, manufacturing excellence and customer service. We have two primary operating segments: Cinema and Digital Media. Our Cinema segment provides a full range of products and services to the theater exhibition industry, including digital projectors, state of the art projection screens, servers, library management systems, menu boards, flat panel displays, sound systems, maintenance services and network monitoring services. Our Digital Media segment delivers digital signage solutions and services across two primary markets: digital out-of-home and enterprise video.

| 21 |