Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Black Creek Diversified Property Fund Inc. | q417form8-k.htm |

Exhibit 99.1

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

Statements included in this portfolio performance and review package that are not historical facts (including any statements concerning investment objectives, other plans and objectives of management for future operations or economic performance or assumptions or forecasts related thereto) are forward looking statements. These statements are only predictions. We caution that forward looking statements are not guarantees. Actual events or our investments and results of operations could differ materially from those expressed or implied in the forward looking statements. Forward looking statements are typically identified by the use of terms such as “may,” “will,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology.

The forward looking statements included herein are based upon our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward looking statements. Factors which could have a material adverse effect on our operations and future prospects include, but are not limited to: high unemployment and a slow economic recovery, which may have a negative effect on the following, among other things, the fundamentals of our business, including overall market demand and occupancy, tenant space utilization, and rental rates; the value of our real estate assets, which may limit our ability to dispose of assets at attractive prices or obtain or maintain debt financing secured by our properties or on an unsecured basis; general risks affecting the real estate industry (including, without limitation, the inability to enter into or renew leases, dependence on tenants’ financial condition, and competition from other developers, owners and operators of real estate); our ability to effectively raise and deploy proceeds from our equity offerings; risks associated with the availability and terms of debt and equity financing and refinancing and the use of debt to fund acquisitions and developments, including the risk associated with interest rates impacting the cost and/or availability of financing and refinancing; the business opportunities that may be presented to and pursued by us; changes in laws or regulations (including changes to laws governing the taxation of real estate investment trusts); changes in accounting principles, policies and guidelines applicable to real estate investment trusts; environmental, regulatory and/or safety requirements; and the availability and cost of comprehensive insurance, including coverage for terrorist acts and earthquakes. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward looking statements after the date of this supplemental package, whether as a result of new information, future events, changed circumstances or any other reason. You should review the risk factors contained in Part I, Item 1A of our 2017 Annual Report on Form 10-K, filed with the Securities and Exchange Commission on March 7, 2018, and in our subsequent quarterly reports.

Please see the section titled “Definitions” at the end of this report for definitions of terms used herein.

Page | 2

PERFORMANCE |

Black Creek Diversified Property Fund Inc. is a monthly NAV-based perpetual life REIT that primarily focuses on investing in and operating a diverse portfolio of real property. As used herein, “we,” “our,” and “us” refer to Black Creek Diversified Property Fund Inc. and its consolidated subsidiaries, except where the context otherwise requires.

Quarter Highlights

• | Total return of 0.60% for the quarter; 2.66% for the last 12 months. |

• | Repaid two senior mortgage notes for $79.7 million with a weighted average interest rate of 3.59%. |

• | Sold six properties aggregating approximately 1.0 million square feet for net proceeds of $230.1 million. |

• | Percentage leased of 87.0% as of December 31, 2017 (or 84.2% leased if weighted by the fair value of each segment). |

• | Paid a weighted-average distribution rate of $0.0897 per share. |

Shareholder Returns (before class specific expenses) | Key Statistics | ||||||||||||

Q4 2017 | Year-to-Date | 1-Year | 3-Year | Since Inception - Annualized(5) | As of December 31, 2017 | ||||||||

Fair Value(1) of Investments | $ 2,065.2 million | ||||||||||||

Number of Real Properties | 48 | ||||||||||||

Number of Real Property Markets | 19 | ||||||||||||

Total Square Feet | 7.6 million | ||||||||||||

Distribution returns(3)(4) | 1.21% | 4.80% | 4.80% | 4.98% | 5.12% | Number of Tenants | 471 | ||||||

Net change in NAV, per share(4) | (0.61)% | (2.14)% | (2.14)% | 1.12% | 2.10% | Percentage Leased | 87.0 | % | |||||

Total return(4)(5) | 0.60% | 2.66% | 2.66% | 6.10% | 7.22% | Debt to Fair Value of Investments | 49.1 | % | |||||

(1) | Unless otherwise indicated, the term "fair value" of our real estate investments as used herein refers to the fair value as determined pursuant to our valuation procedures. Refer to "Definitions" for further detail regarding our valuation procedures. |

(2) | Any market for which we do not show a corresponding percentage of our total fair value comprises 1% or less of the total fair value of our real property portfolio. |

(3) | Represents the compounded return realized from reinvested distributions before ongoing class specific expenses. We pay our dealer manager: (i) a distribution fee equal to 0.85% per annum of the aggregate NAV of our outstanding Class T and S shares; and (ii) a distribution fee equal to 0.25% per annum of the aggregate NAV of our outstanding Class D shares. |

(4) | Excludes the impact of upfront sales commissions and dealer manager fees paid with respect to certain Class T and S shares. We pay (i) upfront selling commissions of up to 3.0% and dealer manager fees of 0.5% of the transaction price of each Class T share and (ii) upfront selling commissions of up to 3.5% of the transaction price of each Class S share sold in our ongoing public primary offering. |

(5) | Total return represents the compound annual rate of return assuming reinvestment of all dividend distributions. Past performance is not a guarantee of future results. The fourth quarter of 2012 represents the first full quarter for which we have complete NAV return data. As such, we use September 30, 2012 as the “inception” date for purposes of calculating cumulative returns since inception. Investors in our fixed price offering prior to NAV inception are likely to have a lower total return. |

Page | 3

FINANCIAL HIGHLIGHTS |

As of or For the Three Months Ended | As of or For the Year Ended | |||||||||||||||||||||||||||

($ and shares in thousands, except per share data) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Selected Operating Data | ||||||||||||||||||||||||||||

Total revenues | $ | 44,670 | $ | 49,672 | $ | 50,265 | $ | 52,739 | $ | 53,956 | $ | 197,346 | $ | 216,170 | ||||||||||||||

Gain on sale of real property | 72,035 | 670 | 10,352 | — | 2,165 | 83,057 | 45,660 | |||||||||||||||||||||

Net income (loss) | 71,301 | (2,145 | ) | 8,415 | 1,827 | 3,357 | 79,398 | 55,048 | ||||||||||||||||||||

Net income (loss) per share | $ | 0.49 | $ | (0.01 | ) | $ | 0.05 | $ | 0.01 | $ | 0.02 | $ | 0.51 | $ | 0.31 | |||||||||||||

Weighted-average number of common shares outstanding - basic | 134,488 | 139,925 | 145,288 | 149,891 | 154,807 | 142,349 | 159,648 | |||||||||||||||||||||

Weighted-average number of common shares outstanding - diluted | 145,931 | 151,739 | 157,209 | 161,919 | 166,942 | 154,156 | 172,046 | |||||||||||||||||||||

Portfolio Statistics | ||||||||||||||||||||||||||||

Operating properties | 48 | 53 | 51 | 55 | 55 | 48 | 55 | |||||||||||||||||||||

Square feet | 7,560 | 8,569 | 8,315 | 8,971 | 8,971 | 7,560 | 8,971 | |||||||||||||||||||||

Percentage leased at end of period | 87.0 | % | 89.5 | % | 86.9 | % | 87.8 | % | 91.2 | % | 87.0 | % | 91.2 | % | ||||||||||||||

Non-GAAP Supplemental Financial Measures | ||||||||||||||||||||||||||||

Net operating income ("NOI") (1) | 29,484 | 31,962 | 33,475 | 35,065 | 36,523 | 129,986 | 149,640 | |||||||||||||||||||||

Funds from Operations ("FFO") per share (1) | $ | 0.09 | $ | 0.09 | $ | 0.11 | $ | 0.12 | $ | 0.13 | $ | 0.42 | $ | 0.53 | ||||||||||||||

Net Asset Value ("NAV") | ||||||||||||||||||||||||||||

NAV per share at the end of period | $ | 7.41 | $ | 7.45 | $ | 7.50 | $ | 7.52 | $ | 7.57 | $ | 7.41 | $ | 7.57 | ||||||||||||||

Weighted-average distributions per share | $ | 0.0897 | $ | 0.0892 | $ | 0.0891 | $ | 0.0891 | $ | 0.0892 | $ | 0.3571 | $ | 0.3571 | ||||||||||||||

Weighted-average closing dividend yield - annualized | 4.84 | % | 4.78 | % | 4.75 | % | 4.74 | % | 4.71 | % | 4.84 | % | 4.72 | % | ||||||||||||||

Weighted-average total return for the period | 0.60 | % | 0.70 | % | 0.87 | % | 0.55 | % | 2.45 | % | 2.66 | % | 6.31 | % | ||||||||||||||

Aggregate fund NAV at end of period | $ | 1,064,398 | $ | 1,129,437 | $ | 1,137,640 | $ | 1,184,021 | $ | 1,229,300 | $ | 1,064,398 | $ | 1,229,300 | ||||||||||||||

Consolidated Debt | ||||||||||||||||||||||||||||

Leverage | 49.1 | % | 50.5 | % | 49.1 | % | 47.7 | % | 45.9 | % | 49.1 | % | 45.9 | % | ||||||||||||||

Weighted-average stated interest rate of total borrowings | 3.6 | % | 3.4 | % | 3.3 | % | 3.2 | % | 3.4 | % | 3.6 | % | 3.4 | % | ||||||||||||||

Secured borrowings | $ | 401,894 | $ | 482,034 | $ | 383,852 | $ | 360,063 | $ | 343,470 | $ | 401,894 | $ | 343,470 | ||||||||||||||

Secured borrowings as % of total borrowings | 39 | % | 42 | % | 35 | % | 33 | % | 33 | % | 39 | % | 33 | % | ||||||||||||||

Unsecured borrowings | $ | 617,000 | $ | 677,000 | $ | 728,000 | $ | 735,000 | $ | 711,000 | $ | 617,000 | $ | 711,000 | ||||||||||||||

Unsecured borrowings as % of total borrowings | 61 | % | 58 | % | 65 | % | 67 | % | 67 | % | 61 | % | 67 | % | ||||||||||||||

Fixed rate borrowings (2) | $ | 473,794 | $ | 478,934 | $ | 479,352 | $ | 542,593 | $ | 653,093 | $ | 473,794 | $ | 653,093 | ||||||||||||||

Fixed rate borrowings as % of total borrowings | 47 | % | 41 | % | 43 | % | 50 | % | 62 | % | 47 | % | 62 | % | ||||||||||||||

Floating rate borrowings | $ | 545,100 | $ | 680,100 | $ | 632,500 | $ | 552,470 | $ | 401,377 | $ | 545,100 | $ | 401,377 | ||||||||||||||

Floating rate borrowings as % of total borrowings | 53 | % | 59 | % | 57 | % | 50 | % | 38 | % | 53 | % | 38 | % | ||||||||||||||

Total borrowings | $ | 1,018,894 | $ | 1,159,034 | $ | 1,111,852 | $ | 1,095,063 | $ | 1,054,470 | $ | 1,018,894 | $ | 1,054,470 | ||||||||||||||

Net GAAP adjustments (3) | $ | (6,786 | ) | $ | (7,533 | ) | $ | (6,700 | ) | $ | (6,618 | ) | $ | (5,669 | ) | $ | (6,786 | ) | $ | (5,669 | ) | |||||||

Total borrowings (GAAP Basis) | $ | 1,012,108 | $ | 1,151,501 | $ | 1,105,152 | $ | 1,088,445 | $ | 1,048,801 | $ | 1,012,108 | $ | 1,048,801 | ||||||||||||||

(1) | NOI and FFO are non-GAAP measures. See "Results From Operations" for a reconciliation of NOI to GAAP net income (loss) and "Fund From Operations" for a reconciliation of GAAP net income (loss) to FFO. |

(2) | Fixed rate borrowings presented includes floating rate borrowings that are effectively fixed by a derivative instrument such as a swap through maturity or substantially through maturity. |

(3) | Include net deferred issuance costs and mark-to-market adjustments on assumed debt. These items are included in debt on our consolidated balance sheets in accordance with GAAP. |

Page | 4

NET ASSET VALUE |

The following table sets forth the components of NAV as of the end of each of the five quarters ending December 31, 2017. As used below, “Fund Interests” means our Class T shares, Class S, Class D shares, Class I shares, and Class E shares, along with the OP Units held by third parties, and “Aggregate Fund NAV” means the NAV of all of the Fund Interests.

As of | ||||||||||||||||||||

(in thousands, except per share data) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | |||||||||||||||

Office properties | $ | 1,148,200 | $ | 1,190,050 | $ | 1,187,550 | $ | 1,186,100 | $ | 1,187,600 | ||||||||||

Retail properties | 851,000 | 1,006,500 | 1,007,600 | 1,013,300 | 1,012,850 | |||||||||||||||

Industrial properties | 66,000 | 86,550 | 54,850 | 81,050 | 81,750 | |||||||||||||||

Total investments | 2,065,200 | 2,283,100 | 2,250,000 | 2,280,450 | 2,282,200 | |||||||||||||||

Cash and other assets, net of other liabilities | 17,772 | 5,916 | (508 | ) | 1,233 | 5,158 | ||||||||||||||

Debt obligations | (1,018,574 | ) | (1,159,579 | ) | (1,111,852 | ) | (1,095,063 | ) | (1,054,470 | ) | ||||||||||

Outside investors' interests | — | — | — | (2,599 | ) | (3,588 | ) | |||||||||||||

Aggregate Fund NAV | $ | 1,064,398 | $ | 1,129,437 | $ | 1,137,640 | $ | 1,184,021 | $ | 1,229,300 | ||||||||||

Total Fund Interests outstanding | 143,692 | 151,550 | 151,738 | 157,409 | 162,396 | |||||||||||||||

NAV Per Fund Interest | $ | 7.41 | $ | 7.45 | $ | 7.50 | $ | 7.52 | $ | 7.57 | ||||||||||

Page | 5

NET ASSET VALUE (continued) |

The following table sets forth the quarterly changes to the components of NAV for the Portfolio, for each of the most recent four quarters, as well as for the years ended December 31, 2017 and 2016:

Three Months Ended | Year Ended | |||||||||||||||||||||||

(in thousands, except per share data) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2017 | December 31, 2016 | ||||||||||||||||||

NAV as of beginning of period | $ | 1,129,437 | $ | 1,137,640 | $ | 1,184,021 | $ | 1,229,300 | $ | 1,229,300 | $ | 1,317,839 | ||||||||||||

Fund level changes to NAV | ||||||||||||||||||||||||

Realized/unrealized losses on net assets | (3,877 | ) | (6,035 | ) | (6,011 | ) | (9,067 | ) | (24,990 | ) | (4,283 | ) | ||||||||||||

Income accrual | 13,500 | 16,173 | 19,923 | 19,564 | 69,160 | 97,940 | ||||||||||||||||||

Advisory fee | (3,025 | ) | (3,283 | ) | (3,431 | ) | (3,468 | ) | (13,207 | ) | (14,704 | ) | ||||||||||||

Performance based fee | — | — | — | (1 | ) | (1 | ) | (94 | ) | |||||||||||||||

Class specific changes to NAV | ||||||||||||||||||||||||

Net dividend accrual | (13,085 | ) | (13,546 | ) | (14,020 | ) | (14,448 | ) | (55,099 | ) | (61,503 | ) | ||||||||||||

Distribution and Dealer Manager fee | (43 | ) | (107 | ) | (135 | ) | (131 | ) | (416 | ) | (450 | ) | ||||||||||||

NAV as of end of period before share/unit sale/redemption activity | $ | 1,122,907 | $ | 1,130,842 | $ | 1,180,347 | $ | 1,221,749 | $ | 1,204,747 | $ | 1,334,745 | ||||||||||||

Dollar/unit sale/redemption activity | ||||||||||||||||||||||||

Amount sold | 12,095 | 9,202 | 11,535 | 11,210 | 44,042 | 112,457 | ||||||||||||||||||

Amount redeemed | (70,604 | ) | (10,607 | ) | (54,242 | ) | (48,938 | ) | (184,391 | ) | (217,902 | ) | ||||||||||||

NAV as of end of period | $ | 1,064,398 | $ | 1,129,437 | $ | 1,137,640 | $ | 1,184,021 | $ | 1,064,398 | $ | 1,229,300 | ||||||||||||

Shares outstanding beginning of period | 151,550 | 151,738 | 157,409 | 162,396 | 162,396 | 176,490 | ||||||||||||||||||

Shares/units sold | 1,627 | 1,229 | 1,535 | 1,484 | 5,875 | 15,137 | ||||||||||||||||||

Shares/units redeemed | (9,485 | ) | (1,417 | ) | (7,206 | ) | (6,471 | ) | (24,579 | ) | (29,231 | ) | ||||||||||||

Shares/units outstanding as of end of period | 143,692 | 151,550 | 151,738 | 157,409 | 143,692 | 162,396 | ||||||||||||||||||

NAV per share/unit as of beginning of period | $ | 7.45 | $ | 7.50 | $ | 7.52 | $ | 7.57 | $ | 7.57 | $ | 7.47 | ||||||||||||

Change in NAV per share/unit | (0.04 | ) | (0.05 | ) | (0.02 | ) | (0.05 | ) | (0.16 | ) | 0.10 | |||||||||||||

NAV per share/unit as of end of period | $ | 7.41 | $ | 7.45 | $ | 7.50 | $ | 7.52 | $ | 7.41 | $ | 7.57 | ||||||||||||

Page | 6

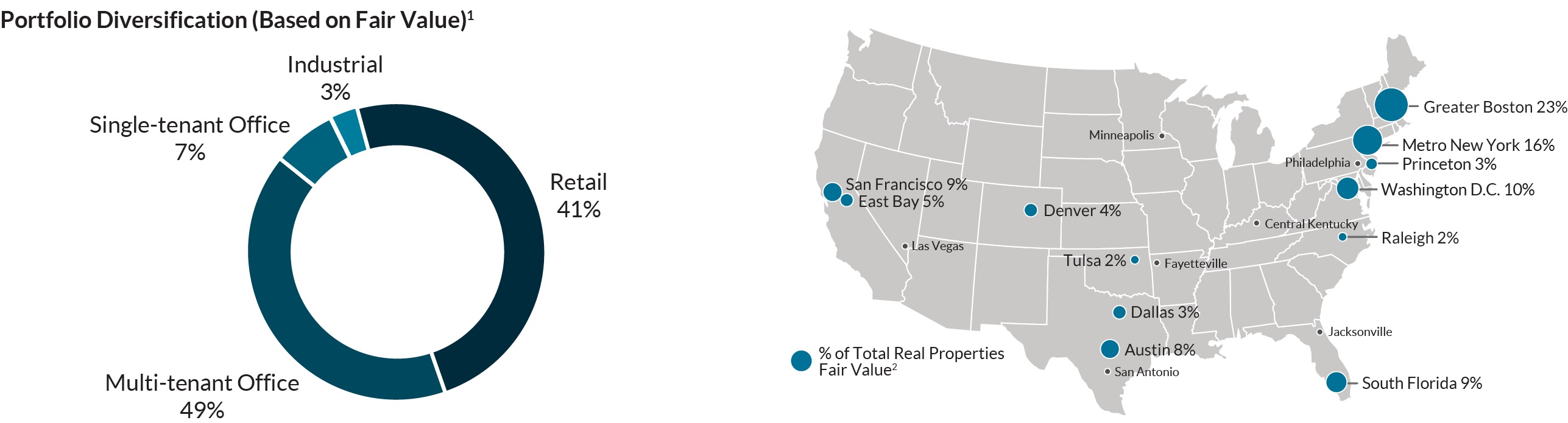

PORTFOLIO PROFILE |

As of December 31, 2017, our real property investments were geographically diversified across 19 markets throughout the United States. The following table presents information about the operating results and fair value of our real property portfolio as of or for the three months and year ended December 31, 2017.

($ and square feet in thousands) | Office | Retail | Industrial | Total | ||||||||||||

As of December 31, 2017: | ||||||||||||||||

Number of properties | 15 | 30 | 3 | 48 | ||||||||||||

Rentable square feet | 3,274 | 3,215 | 1,071 | 7,560 | ||||||||||||

Percentage leased as of period end | 76.2 | % | 93.8 | % | 100.0 | % | 87.0 | % | ||||||||

Aggregate fair value | $ | 1,148,200 | $ | 851,000 | $ | 66,000 | $ | 2,065,200 | ||||||||

Fair value as % of total | 55.6 | % | 41.2 | % | 3.2 | % | 100.0 | % | ||||||||

For the three months ended December 31, 2017: | ||||||||||||||||

Revenue | $ | 24,142 | $ | 18,450 | $ | 1,904 | $ | 44,496 | ||||||||

NOI (1) | 13,533 | 14,405 | 1,546 | 29,484 | ||||||||||||

% of total NOI | 45.9 | % | 48.9 | % | 5.2 | % | 100.0 | % | ||||||||

NOI—cash basis (2) | $ | 10,998 | $ | 13,668 | $ | 1,504 | $ | 26,170 | ||||||||

For the year ended December 31, 2017: | ||||||||||||||||

Revenue | $ | 108,305 | $ | 81,871 | $ | 6,342 | $ | 196,518 | ||||||||

NOI (1) | 63,785 | 61,483 | 4,718 | 129,986 | ||||||||||||

% of total NOI | 49.1 | % | 47.3 | % | 3.6 | % | 100.0 | % | ||||||||

NOI—cash basis (2) | $ | 62,210 | $ | 58,285 | $ | 4,677 | $ | 125,172 | ||||||||

(1) | NOI is a non-GAAP measure. See "Results From Operations" for a reconciliation of NOI to GAAP net income. |

(2) | NOI—cash basis is a non-GAAP measure. See "Results From Operations" for a reconciliation of NOI—cash basis to GAAP net income. |

Page | 7

BALANCE SHEETS |

The following table presents our consolidated balance sheets as of the end of each of the five quarters ended December 31, 2017:

As of | ||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | |||||||||||||||

ASSETS | ||||||||||||||||||||

Net investments in real estate properties | $ | 1,540,270 | $ | 1,691,854 | $ | 1,662,518 | $ | 1,695,877 | $ | 1,711,411 | ||||||||||

Debt-related investments, net | 11,147 | 11,259 | 14,941 | 15,076 | 15,209 | |||||||||||||||

Cash and cash equivalents | 10,475 | 5,841 | 5,362 | 10,894 | 13,864 | |||||||||||||||

Restricted cash | 8,541 | 8,268 | 7,160 | 8,765 | 7,282 | |||||||||||||||

Other assets | 37,673 | 40,549 | 35,297 | 36,947 | 35,962 | |||||||||||||||

Total assets | $ | 1,608,106 | $ | 1,757,771 | $ | 1,725,278 | $ | 1,767,559 | $ | 1,783,728 | ||||||||||

LIABILITIES AND EQUITY | ||||||||||||||||||||

Liabilities | ||||||||||||||||||||

Debt, net | $ | 1,012,108 | $ | 1,151,501 | $ | 1,105,152 | $ | 1,088,445 | $ | 1,048,801 | ||||||||||

Intangible lease liabilities, net | 52,629 | 55,856 | 56,637 | 58,119 | 59,545 | |||||||||||||||

Other liabilities | 50,643 | 58,917 | 57,812 | 62,635 | 67,291 | |||||||||||||||

Total liabilities | 1,115,380 | 1,266,274 | 1,219,601 | 1,209,199 | 1,175,637 | |||||||||||||||

Equity | ||||||||||||||||||||

Stockholders' equity: | ||||||||||||||||||||

Common stock | 1,325 | 1,399 | 1,399 | 1,458 | 1,506 | |||||||||||||||

Additional paid-in capital | 1,224,061 | 1,282,495 | 1,280,621 | 1,324,200 | 1,361,638 | |||||||||||||||

Distributions in excess of earnings | (818,608 | ) | (872,249 | ) | (857,792 | ) | (851,636 | ) | (839,896 | ) | ||||||||||

Accumulated other comprehensive loss | (909 | ) | (4,618 | ) | (5,550 | ) | (4,926 | ) | (6,905 | ) | ||||||||||

Total stockholders' equity | 405,869 | 407,027 | 418,678 | 469,096 | 516,343 | |||||||||||||||

Noncontrolling interests | 86,857 | 84,470 | 86,999 | 89,264 | 91,748 | |||||||||||||||

Total equity | 492,726 | 491,497 | 505,677 | 558,360 | 608,091 | |||||||||||||||

Total liabilities and equity | $ | 1,608,106 | $ | 1,757,771 | $ | 1,725,278 | $ | 1,767,559 | $ | 1,783,728 | ||||||||||

Page | 8

STATEMENTS OF OPERATIONS |

The following table presents our consolidated statements of operations for each of the five quarters ended December 31, 2017, and for the years ended December 31, 2017 and 2016:

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands, except per share data) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Revenues: | ||||||||||||||||||||||||||||

Rental revenues | $ | 44,496 | $ | 49,478 | $ | 50,036 | $ | 52,508 | $ | 53,723 | $ | 196,518 | $ | 215,227 | ||||||||||||||

Debt-related income | 174 | 194 | 229 | 231 | 233 | 828 | 943 | |||||||||||||||||||||

Total revenues | 44,670 | 49,672 | 50,265 | 52,739 | 53,956 | 197,346 | 216,170 | |||||||||||||||||||||

Operating expenses: | ||||||||||||||||||||||||||||

Rental expenses | 15,012 | 17,516 | 16,561 | 17,443 | 17,200 | 66,532 | 65,587 | |||||||||||||||||||||

Real estate-related depreciation and amortization | 14,409 | 16,927 | 18,798 | 17,936 | 20,083 | 68,070 | 80,105 | |||||||||||||||||||||

General and administrative expenses | 2,201 | 2,760 | 2,024 | 2,250 | 2,257 | 9,235 | 9,450 | |||||||||||||||||||||

Advisory fees, related party | 3,070 | 3,274 | 3,451 | 3,490 | 3,740 | 13,285 | 14,857 | |||||||||||||||||||||

Acquisition expenses | — | — | — | — | 6 | — | 667 | |||||||||||||||||||||

Impairment of real estate property | — | — | 1,116 | — | — | 1,116 | 2,677 | |||||||||||||||||||||

Total operating expenses | 34,692 | 40,477 | 41,950 | 41,119 | 43,286 | 158,238 | 173,343 | |||||||||||||||||||||

Other income (expenses): | ||||||||||||||||||||||||||||

Interest expense | (11,112 | ) | (11,346 | ) | (10,163 | ) | (9,684 | ) | (9,388 | ) | (42,305 | ) | (40,782 | ) | ||||||||||||||

Gain on sale of real property | 72,035 | 670 | 10,352 | — | 2,165 | 83,057 | 45,660 | |||||||||||||||||||||

Other income (expense) | 400 | (664 | ) | (89 | ) | (109 | ) | (90 | ) | (462 | ) | 2,207 | ||||||||||||||||

Gain on extinguishment of debt | — | — | — | — | — | — | 5,136 | |||||||||||||||||||||

Total other income (expenses) | 61,323 | (11,340 | ) | 100 | (9,793 | ) | (7,313 | ) | 40,290 | 12,221 | ||||||||||||||||||

Net income (loss) | 71,301 | (2,145 | ) | 8,415 | 1,827 | 3,357 | 79,398 | 55,048 | ||||||||||||||||||||

Net (income) loss attributable to noncontrolling interests | (5,591 | ) | 185 | (1,610 | ) | (166 | ) | (245 | ) | (7,182 | ) | (5,072 | ) | |||||||||||||||

Net income (loss) attributable to common stockholders | $ | 65,710 | $ | (1,960 | ) | $ | 6,805 | $ | 1,661 | $ | 3,112 | $ | 72,216 | $ | 49,976 | |||||||||||||

Net income (loss) per common share—basic and diluted | $ | 0.49 | $ | (0.01 | ) | $ | 0.05 | $ | 0.01 | $ | 0.02 | $ | 0.51 | $ | 0.31 | |||||||||||||

Weighted-average number of common shares outstanding | ||||||||||||||||||||||||||||

Basic | 134,488 | 139,925 | 145,288 | 149,891 | 154,807 | 142,349 | 159,648 | |||||||||||||||||||||

Diluted | 145,931 | 151,739 | 157,209 | 161,919 | 166,942 | 154,156 | 172,046 | |||||||||||||||||||||

Weighted-average distributions declared per common share | $ | 0.0897 | $ | 0.0892 | $ | 0.0891 | $ | 0.0891 | $ | 0.0892 | $ | 0.3571 | $ | 0.3571 | ||||||||||||||

Page | 9

FUNDS FROM OPERATIONS |

FFO is a non-GAAP measure. The following tables present a reconciliation of GAAP net income (loss) attributable to common stockholders to FFO for each of the five quarters ended December 31, 2017, and for the years ended December 31, 2017 and 2016:

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands, except for per share data and percentages) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Reconciliation of net income (loss) to FFO: | ||||||||||||||||||||||||||||

Net income (loss) attributable to common stockholders | $ | 65,710 | $ | (1,960 | ) | $ | 6,805 | $ | 1,661 | $ | 3,112 | $ | 72,216 | $ | 49,976 | |||||||||||||

Add (deduct) NAREIT-defined adjustments: | ||||||||||||||||||||||||||||

Real estate-related depreciation and amortization | 14,409 | 16,927 | 18,798 | 17,936 | 20,083 | 68,070 | 80,105 | |||||||||||||||||||||

Impairment of real estate property | — | — | 1,116 | — | — | 1,116 | 2,677 | |||||||||||||||||||||

Gain on sale of real estate property | (72,035 | ) | (670 | ) | (10,352 | ) | — | (2,165 | ) | (83,057 | ) | (45,660 | ) | |||||||||||||||

Noncontrolling interests' share of adjustments | 4,519 | (1,266 | ) | 200 | (1,361 | ) | (1,331 | ) | 2,092 | (2,802 | ) | |||||||||||||||||

FFO attributable to common stockholders | 12,603 | 13,031 | 16,567 | 18,236 | 19,699 | 60,437 | 84,296 | |||||||||||||||||||||

FFO attributable to OP units | 1,072 | 1,100 | 1,360 | 1,463 | 1,544 | 4,995 | 6,546 | |||||||||||||||||||||

FFO | $ | 13,675 | $ | 14,131 | $ | 17,927 | $ | 19,699 | $ | 21,243 | $ | 65,432 | $ | 90,842 | ||||||||||||||

FFO per common share—basic and diluted | $ | 0.09 | $ | 0.09 | $ | 0.11 | $ | 0.12 | $ | 0.13 | $ | 0.42 | $ | 0.53 | ||||||||||||||

FFO payout ratio | 96 | % | 96 | % | 78 | % | 73 | % | 70 | % | 84 | % | 68 | % | ||||||||||||||

Weighted-average number of shares outstanding—basic | 134,488 | 139,925 | 145,288 | 149,891 | 154,807 | 142,349 | 159,648 | |||||||||||||||||||||

Weighted-average number of shares outstanding—diluted | 145,931 | 151,739 | 157,209 | 161,919 | 166,942 | 154,156 | 172,046 | |||||||||||||||||||||

Page | 10

FUNDS FROM OPERATIONS (continued) |

The following table presents certain other supplemental information for each of the five quarters ended December 31, 2017, and for the years ended December 31, 2017 and 2016:

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Capital expenditures summary: | ||||||||||||||||||||||||||||

Recurring capital expenditures (1) | $ | 10,149 | $ | 10,862 | $ | 5,952 | $ | 2,801 | $ | 8,039 | $ | 29,764 | $ | 26,696 | ||||||||||||||

Non-recurring capital expenditures | 1,411 | 1,104 | 586 | 469 | 1,078 | 3,570 | 3,508 | |||||||||||||||||||||

Total capital expenditures | $ | 11,560 | $ | 11,966 | $ | 6,538 | $ | 3,270 | $ | 9,117 | $ | 33,334 | $ | 30,204 | ||||||||||||||

Other non-cash adjustments: | ||||||||||||||||||||||||||||

Straight-line rent (increase) decrease to rental revenue | $ | (2,319 | ) | $ | 109 | $ | 238 | $ | 117 | $ | 522 | $ | (1,855 | ) | $ | 1,263 | ||||||||||||

Amortization of above- and below- market rent (increase) decrease to rental revenue | (1,020 | ) | (714 | ) | (710 | ) | (559 | ) | 143 | (3,003 | ) | (535 | ) | |||||||||||||||

Amortization of loan costs and hedges - increase to interest expense | 1,334 | 1,372 | 1,074 | 1,032 | 873 | 4,812 | 3,750 | |||||||||||||||||||||

Amortization of mark-to-market adjustments on borrowings - decrease to interest expense | (34 | ) | (34 | ) | (33 | ) | (33 | ) | (33 | ) | (134 | ) | (678 | ) | ||||||||||||||

Total other non-cash adjustments | $ | (2,039 | ) | $ | 733 | $ | 569 | $ | 557 | $ | 1,505 | $ | (180 | ) | $ | 3,800 | ||||||||||||

(1) | Recurring capital expenditures include lease incentives. Unlike other capital expenditures, we record lease incentives as other assets in our balance sheet and we classify payments for lease incentives as cash used in operating activities in our statement of cash flows. |

Page | 11

RESULTS FROM OPERATIONS |

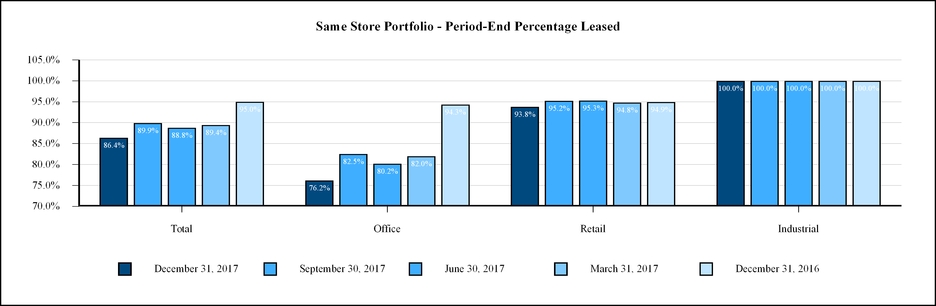

NOI and NOI—cash basis are non-GAAP measures. See page 13 for a reconciliation of GAAP net income (loss) attributable to common stockholders to NOI and NOI—cash basis. The following table presents revenue and NOI of our three operating segments for each of the five quarters ending December 31, 2017, and for the years ended December 31, 2017 and 2016. Our same store portfolio includes all operating properties owned for the entirety of all periods presented and totals 45 properties, comprising approximately 7.1 million square feet or 94.4% of our total portfolio when measured by square feet:

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Revenue: | ||||||||||||||||||||||||||||

Same store real property: | ||||||||||||||||||||||||||||

Office (1) | $ | 23,814 | $ | 26,007 | $ | 26,409 | $ | 28,289 | $ | 29,523 | $ | 104,519 | $ | 119,482 | ||||||||||||||

Retail | 16,638 | 16,300 | 16,603 | 16,967 | 17,006 | 66,508 | 65,891 | |||||||||||||||||||||

Industrial | 600 | 600 | 600 | 600 | 600 | 2,400 | 2,400 | |||||||||||||||||||||

Total same store real property revenue | 41,052 | 42,907 | 43,612 | 45,856 | 47,129 | 173,427 | 187,773 | |||||||||||||||||||||

2016/2017 Acquisitions/Dispositions | 3,444 | 6,571 | 6,424 | 6,652 | 6,594 | 23,091 | 27,454 | |||||||||||||||||||||

Total | $ | 44,496 | $ | 49,478 | $ | 50,036 | $ | 52,508 | $ | 53,723 | $ | 196,518 | $ | 215,227 | ||||||||||||||

NOI: | ||||||||||||||||||||||||||||

Same store real property: | ||||||||||||||||||||||||||||

Office | $ | 13,325 | $ | 14,862 | $ | 15,371 | $ | 17,466 | $ | 18,762 | $ | 61,024 | $ | 79,135 | ||||||||||||||

Retail | 12,859 | 11,988 | 13,019 | 12,736 | 12,761 | 50,602 | 49,702 | |||||||||||||||||||||

Industrial | 593 | 589 | 592 | 589 | 592 | 2,363 | 2,369 | |||||||||||||||||||||

Total same store real property NOI | 26,777 | 27,439 | 28,982 | 30,791 | 32,115 | 113,989 | 131,206 | |||||||||||||||||||||

2016/2017 Acquisitions/Dispositions | 2,707 | 4,523 | 4,493 | 4,274 | 4,408 | 15,997 | 18,434 | |||||||||||||||||||||

Total | $ | 29,484 | $ | 31,962 | $ | 33,475 | $ | 35,065 | $ | 36,523 | $ | 129,986 | $ | 149,640 | ||||||||||||||

NOI—cash basis: | ||||||||||||||||||||||||||||

Same store real property: | ||||||||||||||||||||||||||||

Office | $ | 10,785 | $ | 15,081 | $ | 15,728 | $ | 17,844 | $ | 20,306 | $ | 59,438 | $ | 83,279 | ||||||||||||||

Retail | 12,209 | 11,291 | 12,316 | 12,040 | 12,002 | 47,856 | 46,570 | |||||||||||||||||||||

Industrial | 606 | 597 | 591 | 588 | 591 | 2,382 | 2,329 | |||||||||||||||||||||

Total same store real property NOI—cash basis | 23,600 | 26,969 | 28,635 | 30,472 | 32,899 | 109,676 | 132,178 | |||||||||||||||||||||

2016/2017 Acquisitions/Dispositions | 2,570 | 4,396 | 4,374 | 4,156 | 4,296 | 15,496 | 18,213 | |||||||||||||||||||||

Total | $ | 26,170 | $ | 31,365 | $ | 33,009 | $ | 34,628 | $ | 37,195 | $ | 125,172 | $ | 150,391 | ||||||||||||||

(1) | In January 2017, our lease with Sybase Inc. ("Sybase"), our second largest tenant based on annualized base rent as of December 31, 2016, was terminated which had an adverse impact on our results from operations for three months and year ended December 31, 2017. Sybase had leased our entire 417,000 square foot office property in East Bay, CA ("Park Place") and, as of December 31, 2017, we have leased 17.5% of Park Place to a replacement tenant; however the lease does not commence until the first half of 2018. Please see the table below for revenue, NOI and NOI–cash basis for our same store office portfolio excluding Park Place for each of the five quarters ending December 31, 2017, and for the years ended December 31, 2017 and 2016. |

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Same store office portfolio excluding Sybase: | ||||||||||||||||||||||||||||

Revenue | $ | 23,808 | $ | 25,976 | $ | 26,534 | $ | 26,730 | $ | 26,196 | $ | 103,048 | $ | 105,563 | ||||||||||||||

NOI | 14,142 | 15,655 | 16,218 | 16,515 | 15,698 | 62,530 | 65,560 | |||||||||||||||||||||

NOI–cash basis | 11,602 | 15,873 | 16,577 | 16,513 | 15,894 | 60,565 | 64,931 | |||||||||||||||||||||

Page | 12

RESULTS FROM OPERATIONS (continued) |

The following table presents a reconciliation of GAAP net income (loss) attributable to common stockholders to NOI and NOI—cash basis of our three operating segments for each of the five quarters ending December 31, 2017, and for the years ended December 31, 2017 and 2016:

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Net income (loss) attributable to common stockholders | $ | 65,710 | $ | (1,960 | ) | $ | 6,805 | $ | 1,661 | $ | 3,112 | $ | 72,216 | $ | 49,976 | |||||||||||||

Debt-related income | (174 | ) | (194 | ) | (229 | ) | (231 | ) | (233 | ) | (828 | ) | (943 | ) | ||||||||||||||

Real estate-related depreciation and amortization expense | 14,409 | 16,927 | 18,798 | 17,936 | 20,083 | 68,070 | 80,105 | |||||||||||||||||||||

General and administrative expenses | 2,201 | 2,760 | 2,024 | 2,250 | 2,257 | 9,235 | 9,450 | |||||||||||||||||||||

Advisory fees, related party | 3,070 | 3,274 | 3,451 | 3,490 | 3,740 | 13,285 | 14,857 | |||||||||||||||||||||

Acquisition expenses | — | — | — | — | 6 | — | 667 | |||||||||||||||||||||

Impairment of real estate property | — | — | 1,116 | — | — | 1,116 | 2,677 | |||||||||||||||||||||

Interest expense | 11,112 | 11,346 | 10,163 | 9,684 | 9,388 | 42,305 | 40,782 | |||||||||||||||||||||

Gain on sale of real property | (72,035 | ) | (670 | ) | (10,352 | ) | — | (2,165 | ) | (83,057 | ) | (45,660 | ) | |||||||||||||||

Other (income) expense | (400 | ) | 664 | 89 | 109 | 90 | 462 | (2,207 | ) | |||||||||||||||||||

Gain on extinguishment of debt | — | — | — | — | — | — | (5,136 | ) | ||||||||||||||||||||

Net income (loss) attributable to noncontrolling interests | 5,591 | (185 | ) | 1,610 | 166 | 245 | 7,182 | 5,072 | ||||||||||||||||||||

NOI | $ | 29,484 | $ | 31,962 | $ | 33,475 | $ | 35,065 | $ | 36,523 | $ | 129,986 | $ | 149,640 | ||||||||||||||

Net amortization of above- and below-market lease assets and liabilities, and other non-cash adjustments to rental revenue | (995 | ) | (706 | ) | (704 | ) | (554 | ) | 150 | (2,959 | ) | (512 | ) | |||||||||||||||

Straight line rent | (2,319 | ) | 109 | 238 | 117 | 522 | (1,855 | ) | 1,263 | |||||||||||||||||||

NOI—cash basis | $ | 26,170 | $ | 31,365 | $ | 33,009 | $ | 34,628 | $ | 37,195 | $ | 125,172 | $ | 150,391 | ||||||||||||||

The following table presents details regarding our capital expenditures for each of the five quarters ending December 31, 2017, and for the years ended December 31, 2017 and 2016 (amounts in thousands):

Three Months Ended | Year Ended | |||||||||||||||||||||||||||

(in thousands) | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | December 31, 2017 | December 31, 2016 | |||||||||||||||||||||

Recurring capital expenditures: | ||||||||||||||||||||||||||||

Land and building improvements | $ | 4,046 | $ | 4,003 | $ | 3,276 | $ | 1,108 | $ | 5,740 | $ | 12,433 | $ | 10,712 | ||||||||||||||

Tenant improvements | 3,853 | 4,610 | 1,438 | 1,046 | 1,267 | 10,947 | 8,506 | |||||||||||||||||||||

Leasing costs (1) | 2,250 | 2,249 | 1,238 | 647 | 1,032 | 6,384 | 7,478 | |||||||||||||||||||||

Total recurring capital expenditures | $ | 10,149 | $ | 10,862 | $ | 5,952 | $ | 2,801 | $ | 8,039 | $ | 29,764 | $ | 26,696 | ||||||||||||||

Non-recurring capital expenditures: | ||||||||||||||||||||||||||||

Land and building improvements | $ | 274 | $ | 384 | $ | 266 | $ | 292 | $ | 782 | $ | 1,216 | $ | 2,013 | ||||||||||||||

Tenant improvements | 934 | 646 | 64 | 93 | 165 | 1,737 | 1,061 | |||||||||||||||||||||

Leasing costs | 203 | 74 | 256 | 84 | 131 | 617 | 434 | |||||||||||||||||||||

Total non-recurring capital expenditures | $ | 1,411 | $ | 1,104 | $ | 586 | $ | 469 | $ | 1,078 | $ | 3,570 | $ | 3,508 | ||||||||||||||

(1) | Recurring leasing costs include lease incentives. Unlike other capital expenditures, we record lease incentives as other assets in our balance sheet and we classify payments for lease incentives as cash used in operating activities in our statement of cash flows. |

Page | 13

FINANCE & CAPITAL |

The following table describes certain information about our capital structure. Amounts reported as financing capital represent the total principal outstanding under our total borrowings. Amounts reported as equity capital are presented based on the NAV as of December 31, 2017:

(in thousands) | As of December 31, 2017 | ||||||||

Unsecured line of credit | $ | 142,000 | |||||||

Unsecured term loans | 475,000 | ||||||||

Mortgage notes | 401,894 | ||||||||

Total Financing (1) | $ | 1,018,894 | |||||||

(in thousands, except per share data and percentages) | Shares / Units | Percentage of Aggregate Shares and Units Outstanding | NAV Per Share / Unit | Value | ||||||||||

Class T Common Stock | 2,062 | 1.4 | % | $ | 7.41 | $ | 15,276 | |||||||

Class S Common Stock | 64 | — | 7.41 | 474 | ||||||||||

Class D Common Stock | 2,510 | 1.7 | 7.41 | 18,589 | ||||||||||

Class I Common Stock (2) | 34,069 | 23.7 | 7.41 | 252,368 | ||||||||||

Class E Common Stock | 93,695 | 65.3 | 7.41 | 694,044 | ||||||||||

Class E OP Units | 11,292 | 7.9 | 7.41 | 83,647 | ||||||||||

Total/Weighted Average | 143,692 | 100.0 | % | $ | 7.41 | $ | 1,064,398 | |||||||

TOTAL CAPITALIZATION | $ | 2,083,292 | ||||||||||||

(1) | For a reconciliation of the total outstanding principal balance under our total borrowings to total borrowings on a GAAP basis see page 15. |

(2) | Amounts reported do not include approximately 66,000 restricted stock units granted to the Advisor that remain unvested as of December 31, 2017. |

Page | 14

FINANCE & CAPITAL (continued) |

The following table presents a summary of our borrowings as of December 31, 2017:

($ in thousands) | Weighted-Average Effective Interest Rate | Maturity Date | Outstanding Principal Balance | Fair Value of Real Properties Securing Borrowings | ||||||||

Line of credit (1) | 3.27% | January 2019 | $ | 142,000 | N/A | |||||||

Term loan (2) | 3.25% | January 2018 | 275,000 | N/A | ||||||||

Term loan (3) | 3.94% | February 2022 | 200,000 | N/A | ||||||||

Total unsecured borrowings | 3.48% | 617,000 | N/A | |||||||||

Fixed-rate mortgage notes (4) | 3.89% | September 2021 - December 2029 | 123,794 | $ | 238,450 | |||||||

Floating-rate mortgage notes (5) | 3.88% | January 2020 - August 2023 | 278,100 | 542,850 | ||||||||

Total mortgage notes | 3.88% | $ | 401,894 | $ | 781,300 | |||||||

Total principal amount / weighted-average (6) | 3.64% | $ | 1,018,894 | |||||||||

Less unamortized debt issuance costs | $ | (7,322 | ) | |||||||||

Add mark-to-market adjustment on assumed debt | 536 | |||||||||||

Total debt, net | $ | 1,012,108 | ||||||||||

(1) | The effective interest rate is calculated based on the London Interbank Offered Rate ("LIBOR"), plus a margin ranging from 1.40% to 2.30%, depending on our consolidated leverage ratio. There were no interest rate swap agreements relating to this line of credit as of December 31, 2017. As of December 31, 2017, the unused and available portions under the line of credit were approximately $258.0 million and $145.8 million, respectively. The line of credit is available for general business purposes including, but not limited to, refinancing of existing indebtedness and financing the acquisition of permitted investments, including commercial properties. |

(2) | The effective interest rate is calculated based on LIBOR, plus a margin ranging from 1.35% to 2.20%, depending on our consolidated leverage ratio. The weighted-average interest rate is the all-in interest rate, including the effects of interest swap agreements relating to approximately $150.0 million in borrowings under this term loan. In January 2018, we exercised a one-year extension option on this term loan. This term loan is available for general business purposes including, but not limited to, refinancing of existing indebtedness and financing the acquisition of permitted investments, including commercial properties. |

(3) | The effective interest rate is calculated based on LIBOR, plus a margin ranging from 1.65% to 2.55%, depending on our consolidated leverage ratio. The weighted-average interest rate is the all-in interest rate and is entirely fixed through interest swap agreements. This term loan is available for general business purposes including, but not limited to, refinancing of existing indebtedness and financing the acquisition of permitted investments, including commercial properties. |

(4) | Amount as of December 31, 2017 includes a $33.0 million floating-rate mortgage note that was subject to an interest rate spread of 1.60% over one-month LIBOR, which we have effectively fixed using an interest rate swap at 3.051% for the term of the borrowing. |

(5) | The effective interest rate is calculated based on LIBOR plus a margin. As of December 31, 2017, our floating rate mortgage notes were subject to a weighted-average interest rate spread of 2.31%. |

(6) | The weighted-average remaining term of our borrowings was approximately 2.6 years as of December 31, 2017. |

Page | 15

FINANCE & CAPITAL (continued) |

The following table presents a summary of our covenants and our actual results for each of the five quarters ended December 31, 2017, calculated in accordance with the terms of our credit facilities:

Portfolio-Level Covenants: | Covenant | December 31, 2017 | September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | |||||||||||

Leverage | < 60% | 52.5 | % | 53.9 | % | 52.3 | % | 50.8 | % | 47.5 | % | ||||||

Fixed Charge Coverage | > 1.50 | 2.3 | 2.4 | 3.0 | 3.3 | 3.3 | |||||||||||

Secured Indebtedness | < 55% | 20.7 | % | 22.4 | % | 18.1 | % | 16.7 | % | 15.5 | % | ||||||

Unencumbered Pool Covenants: | |||||||||||||||||

Leverage | < 60% | 48.5 | % | 52.7 | % | 51.2 | % | 50.7 | % | 45.5 | % | ||||||

Unsecured Interest Coverage | >2.0 | 3.1 | 3.2 | 4.2 | 5.2 | 6.8 | |||||||||||

Page | 16

FINANCE & CAPITAL (continued) |

The following table presents a detailed analysis of our borrowings outstanding as of December 31, 2017:

($ in thousands) | Principal Balance | Secured / Unsecured | Maturity Date | Extension Options | % of Total Borrowings | Fixed or Floating Interest Rate | Current Interest Rate | |||||||||||

Bank of America Term Loan (1) | $ | 150,000 | Unsecured | 1/31/2018 | (2) | 2 - 1 Year | 14.7 | % | Fixed | 3.31 | % | |||||||

Bank of America Term Loan | 125,000 | Unsecured | 1/31/2018 | (2) | 2 - 1 Year | 12.3 | Floating | 3.17 | ||||||||||

Line of Credit | 142,000 | Unsecured | 1/31/2019 | 1 - 1 Year | 13.8 | Floating | 3.27 | |||||||||||

3 Second Street (3) | 127,000 | Secured | 1/10/2020 | 2 - 1 Year | 12.5 | Floating | 3.82 | |||||||||||

655 Montgomery (4) | 98,600 | Secured | 9/7/2020 | 2 - 1 Year | 9.7 | Floating | 4.32 | |||||||||||

Shenandoah | 10,197 | Secured | 9/1/2021 | None | 1.0 | Fixed | 4.84 | |||||||||||

Wells Fargo Term Loan (5) | 200,000 | Unsecured | 2/27/2022 | None | 19.6 | Fixed | 3.94 | |||||||||||

Norwell | 3,756 | Secured | 10/1/2022 | None | 0.4 | Fixed | 6.76 | |||||||||||

Preston Sherry Plaza (6) | 33,000 | Secured | 3/1/2023 | None | 3.2 | Fixed | 3.05 | |||||||||||

1300 Connecticut (7) | 52,500 | Secured | 8/5/2023 | None | 5.2 | Floating | 3.22 | |||||||||||

270 Center | 70,000 | Secured | 12/1/2025 | None | 6.9 | Fixed | 3.80 | |||||||||||

New Bedford | 6,841 | Secured | 12/1/2029 | None | 0.7 | Fixed | 5.91 | |||||||||||

Total borrowings | $ | 1,018,894 | 100.0 | % | 3.64 | % | ||||||||||||

Add: mark-to-market adjustment on assumed debt | 536 | |||||||||||||||||

Less: net debt issuance costs | (7,322 | ) | ||||||||||||||||

Total Borrowings (GAAP basis) | $ | 1,012,108 | ||||||||||||||||

(1) | Borrowings under this term loan are effectively fixed by the use of interest rate swap agreements as of December 31, 2017. The stated interest rates disclosed above include the impact of these swaps. |

(2) | In January 2018, we exercised an option to extend this term loan for another year until January 31, 2019. |

(3) | The 3 Second Street term loan was subject to an interest rate spread of 2.25% over one-month LIBOR as of December 31, 2017. However, in conjunction with this borrowing, we entered into an interest rate protection agreement with a LIBOR strike rate of 3.00%. |

(4) | The 655 Montgomery term loan was subject to an interest rate spread of 2.75% over one-month LIBOR as of December 31, 2017. However, in conjunction with this borrowing, we entered into an interest rate protection agreement with a LIBOR strike rate of 3.00%. |

(5) | Borrowings under this term loan are effectively fixed by the use of fixed-for-floating rate swap instruments as of December 31, 2017. |

(6) | The Preston Sherry Plaza term loan was subject to an interest rate spread of 1.60% over one-month LIBOR. However, we have effectively fixed the interest rate of the borrowing using an interest rate swap at 3.051% for the term of the borrowing as of September 30, 2017. |

(7) | As of December 31, 2017, the 1300 Connecticut term loan was subject to an interest rate spread of 1.65% over one-month LIBOR. However, we entered into an interest rate swap which will effectively fix the interest rate of the borrowing at 2.852% from July 1, 2018 to July 1, 2021. |

Page | 17

REAL PROPERTIES |

The following table describes our operating property portfolio as of December 31, 2017:

($ and square feet in thousands) | Number of Properties | Investment in Real Estate Properties | % of Gross Investment Amount | Rentable Square Feet | % of Total Rentable Square Feet | % Leased (1) | Secured Indebtedness (2) | |||||||||||||||

Office Properties: | ||||||||||||||||||||||

Metro New York | 1 | $ | 232,848 | 11.6 | % | 594 | 7.8 | % | 66.9 | % | $ | 127,000 | ||||||||||

Austin | 3 | 157,049 | 7.7 | 585 | 7.7 | 93.6 | — | |||||||||||||||

East Bay | 1 | 152,963 | 7.5 | 417 | 5.5 | 17.5 | — | |||||||||||||||

San Francisco | 1 | 125,171 | 6.2 | 263 | 3.5 | 81.9 | 98,600 | |||||||||||||||

Denver | 1 | 83,867 | 4.1 | 262 | 3.5 | 78.9 | — | |||||||||||||||

South Florida | 2 | 81,769 | 4.0 | 363 | 4.8 | 80.5 | — | |||||||||||||||

Washington, DC | 1 | 71,292 | 3.5 | 126 | 1.7 | 99.1 | 52,500 | |||||||||||||||

Princeton | 1 | 51,375 | 2.5 | 167 | 2.2 | 100.0 | — | |||||||||||||||

Philadelphia | 1 | 47,311 | 2.3 | 174 | 2.3 | 90.9 | — | |||||||||||||||

Dallas | 1 | 38,872 | 1.9 | 155 | 2.1 | 93.4 | 33,000 | |||||||||||||||

Minneapolis/St Paul | 1 | 29,528 | 1.5 | 107 | 1.4 | 100.0 | — | |||||||||||||||

Fayetteville | 1 | 12,468 | 0.6 | 61 | 0.8 | 100.0 | — | |||||||||||||||

Total/Weighted Average Office: 12 markets with average annual rent of $30.38 per sq. ft. | 15 | 1,084,513 | 53.4 | 3,274 | 43.3 | 76.2 | 311,100 | |||||||||||||||

Retail Properties: | ||||||||||||||||||||||

Greater Boston | 22 | 510,458 | 25.2 | 2,074 | 27.4 | 94.2 | 10,597 | |||||||||||||||

South Florida | 2 | 106,769 | 5.3 | 206 | 2.7 | 94.7 | 10,197 | |||||||||||||||

Washington, DC | 1 | 62,867 | 3.1 | 233 | 3.1 | 100.0 | 70,000 | |||||||||||||||

Metro New York | 1 | 59,188 | 2.9 | 224 | 3.0 | 93.9 | — | |||||||||||||||

Raleigh | 1 | 45,839 | 2.3 | 143 | 1.9 | 100.0 | — | |||||||||||||||

Tulsa | 1 | 34,068 | 1.7 | 101 | 1.3 | 100.0 | — | |||||||||||||||

San Antonio | 1 | 32,572 | 1.6 | 161 | 2.1 | 88.7 | — | |||||||||||||||

Jacksonville | 1 | 20,237 | 1.0 | 73 | 1.0 | 48.0 | — | |||||||||||||||

Total/Weighted Average Retail: eight markets with average annual rent of $17.78 per sq. ft. | 30 | 871,998 | 43.1 | 3,215 | 42.5 | 93.8 | 90,794 | |||||||||||||||

Industrial Properties: | ||||||||||||||||||||||

Central Kentucky | 1 | 30,840 | 1.5 | 727 | 9.6 | 100.0 | — | |||||||||||||||

Las Vegas | 1 | 24,656 | 1.2 | 248 | 3.3 | 100.0 | — | |||||||||||||||

East Bay | 1 | 16,899 | 0.8 | 96 | 1.3 | 100.0 | — | |||||||||||||||

Total/Weighted Average Industrial: three markets with average annual rent of $4.48 per sq. ft. | 3 | 72,395 | 3.5 | 1,071 | 14.2 | 100.0 | — | |||||||||||||||

Total real estate portfolio | 48 | $ | 2,028,906 | 100.0 | % | 7,560 | 100.0 | % | 87.0 | % | $ | 401,894 | ||||||||||

(1) | Based on executed leases as of December 31, 2017. If weighted by the fair value of each segment, our portfolio was 84.2% leased as of December 31, 2017. |

(2) | Secured indebtedness represents the principal balance outstanding and does not include our mark-to-market adjustment on debt or net debt issuance costs. |

Page | 18

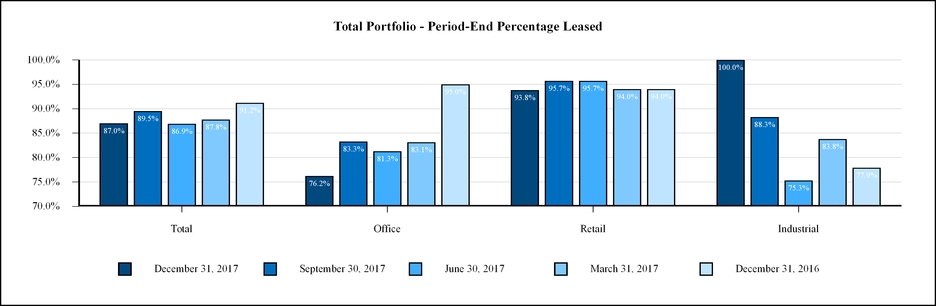

LEASING ACTIVITY |

The following graphs highlight our total portfolio and same store portfolio percentage leased at the end of each of the five quarters ended December 31, 2017, by segment and in total:

Page | 19

LEASING ACTIVITY (continued) |

As of December 31, 2017, the weighted average remaining term of our leases was approximately 5.2 years, based on annualized base rent, and 5.1 years, based on leased square footage. The following table presents our lease expirations, by segment and in total, as of December 31, 2017:

Total | Office | Retail | Industrial | |||||||||||||||||||||||||||||||||||||

($ and square feet in thousands) | Number of Leases Expiring | Annualized Base Rent | % of Total Annualized Base Rent | Square Feet | Number of Leases Expiring | Annualized Base Rent | Square Feet | Number of Leases Expiring | Annualized Base Rent | Square Feet | Number of Leases Expiring | Annualized Base Rent | Square Feet | |||||||||||||||||||||||||||

2018 (1) | 82 | $ | 6,365 | 4.7 | % | 267 | 44 | $ | 4,173 | 163 | 38 | $ | 2,192 | 104 | — | $ | — | — | ||||||||||||||||||||||

2019 | 95 | 22,557 | 16.8 | 923 | 48 | 14,221 | 447 | 47 | 8,336 | 476 | — | — | — | |||||||||||||||||||||||||||

2020 | 112 | 20,562 | 15.3 | 917 | 50 | 9,041 | 339 | 61 | 11,426 | 565 | 1 | 95 | 13 | |||||||||||||||||||||||||||

2021 | 62 | 15,251 | 11.4 | 1,201 | 29 | 7,231 | 206 | 31 | 4,938 | 232 | 2 | 3,082 | 763 | |||||||||||||||||||||||||||

2022 | 65 | 14,205 | 10.6 | 734 | 24 | 6,610 | 223 | 41 | 7,595 | 511 | — | — | — | |||||||||||||||||||||||||||

2023 | 53 | 20,937 | 15.6 | 832 | 21 | 15,081 | 497 | 32 | 5,856 | 335 | — | — | — | |||||||||||||||||||||||||||

2024 | 24 | 3,839 | 2.9 | 187 | 9 | 2,567 | 113 | 15 | 1,272 | 74 | — | — | — | |||||||||||||||||||||||||||

2025 | 22 | 4,529 | 3.4 | 183 | 10 | 2,809 | 98 | 11 | 1,557 | 66 | 1 | 163 | 19 | |||||||||||||||||||||||||||

2026 | 17 | 3,320 | 2.5 | 207 | 6 | 1,193 | 31 | 10 | 1,921 | 148 | 1 | 206 | 28 | |||||||||||||||||||||||||||

2027 | 18 | 6,463 | 4.8 | 528 | 3 | 1,277 | 70 | 14 | 3,935 | 210 | 1 | 1,251 | 248 | |||||||||||||||||||||||||||

Thereafter | 28 | 16,229 | 12.0 | 595 | 11 | 11,543 | 298 | 17 | 4,686 | 297 | — | — | — | |||||||||||||||||||||||||||

Total | 578 | $ | 134,257 | 100.0 | % | 6,574 | 255 | $ | 75,746 | 2,485 | 317 | $ | 53,714 | 3,018 | 6 | $ | 4,797 | 1,071 | ||||||||||||||||||||||

(1) | Includes three leases with combined annualized base rent of approximately $34,000 that are on a month-to-month basis. |

Page | 20

LEASING ACTIVITY (continued) |

The following table presents our top 10 tenants by annualized base rent and their related industry sector, as of December 31, 2017 (dollars and square feet in thousands):

($ and square feet in thousands) | Number of Locations (1) | Industry Sector (2) | Annualized Base Rent (3) | % of Total Annualized Base Rent (3) | Square Feet | % of Total Leased Square Feet | |||||||||||

Stop & Shop | 13 | Food and Beverage Stores | $ | 13,579 | 10.1 | % | 803 | 12.2 | % | ||||||||

Novo Nordisk | 1 | Chemical Manufacturing | 4,721 | 3.5 | 167 | 2.5 | |||||||||||

Mizuho Bank Ltd. | 1 | Credit Intermediation and Related Activities | 4,497 | 3.3 | 116 | 1.8 | |||||||||||

Seton Health Care | 1 | Hospitals | 4,339 | 3.2 | 156 | 2.4 | |||||||||||

Amazon.com | 2 | Non-Store Retailers | 3,618 | 2.7 | 975 | 14.8 | |||||||||||

I.A.M. National Pension Fund | 1 | Funds, Trusts and Other Financial Vehicles | 3,207 | 2.4 | 63 | 1.0 | |||||||||||

Shaw's Supermarket | 3 | Food and Beverage Stores | 3,037 | 2.3 | 181 | 2.8 | |||||||||||

TJX Companies | 6 | Clothing and Clothing Accessories Stores | 2,832 | 2.1 | 287 | 4.4 | |||||||||||

Citco Fund Services | 1 | Funds, Trusts and Other Financial Vehicles | 2,812 | 2.1 | 70 | 1.1 | |||||||||||

Trinet Group, Inc. | 1 | Professional, Scientific and Technical Services | 2,713 | 2.0 | 73 | 1.1 | |||||||||||

30 | $ | 45,355 | 33.7 | % | 2,891 | 44.1 | % | ||||||||||

(1) | Reflects the number of properties for which the tenant has at least one lease in-place. |

(2) | Industry sector based upon the North American Industry Classification System. |

(3) | Annualized base rent is calculated as monthly base rent including the impact of any contractual tenant concessions (cash basis) per the terms of the lease as of December 31, 2017, multiplied by 12. |

Page | 21

LEASING ACTIVITY (continued) |

The following series of tables details leasing activity during the four quarters ended December 31, 2017:

Quarter | Number of Leases Signed | Gross Leasable Area ("GLA") Signed | Weighted Average Rent Per Sq. Ft. | Weighted Average Growth / Straight Line Rent | Weighted Average Lease Term (mos) | Tenant Improvements & Incentives Per Sq. Ft. | Average Free Rent (mos) | |||||||||||||

Office Comparable (1) | ||||||||||||||||||||

Q4 2017 | 13 | 55,434 | $ | 39.09 | 39.5 | % | 56 | $ | 19.20 | 1.9 | ||||||||||

Q3 2017 | 14 | 129,151 | 23.02 | 22.8 | % | 103 | 28.09 | 4.1 | ||||||||||||

Q2 2017 (2) | 15 | 95,858 | 47.49 | 110.5 | % | 136 | 111.25 | 4.7 | ||||||||||||

Q1 2017 | 8 | 24,088 | 23.53 | 40.8 | % | 52 | 23.84 | 3.3 | ||||||||||||

Total - twelve months | 50 | 304,531 | $ | 37.09 | 66.0 | % | 108 | $ | 68.55 | 3.9 | ||||||||||

Retail Comparable (1) | ||||||||||||||||||||

Q4 2017 | 10 | 47,571 | $ | 22.97 | 24.2 | % | 76 | $ | 0.37 | 0.6 | ||||||||||

Q3 2017 | 17 | 112,791 | 30.81 | 19.3 | % | 72 | 9.32 | — | ||||||||||||

Q2 2017 | 15 | 72,487 | 25.91 | 12.7 | % | 133 | 29.96 | 0.1 | ||||||||||||

Q1 2017 | 16 | 92,674 | 19.13 | 13.5 | % | 96 | 0.85 | — | ||||||||||||

Total - twelve months | 58 | 325,523 | $ | 25.34 | 16.7 | % | 100 | $ | 13.10 | 0.1 | ||||||||||

Industrial Comparable (1) | ||||||||||||||||||||

Q4 2017 | — | — | $ | — | — | % | — | $ | — | — | ||||||||||

Q3 2017 | — | — | — | — | % | — | — | — | ||||||||||||

Q2 2017 | — | — | — | — | % | — | — | — | ||||||||||||

Q1 2017 | 2 | 156,896 | 3.06 | 13.6 | % | 30 | 0.35 | 1.7 | ||||||||||||

Total - twelve months | 2 | 156,896 | $ | 3.06 | 13.6 | % | 30 | $ | 0.35 | 1.7 | ||||||||||

Total Comparable Leasing (1) | ||||||||||||||||||||

Q4 2017 | 23 | 103,005 | $ | 33.88 | 28.7 | % | 60 | $ | 15.01 | 1.6 | ||||||||||

Q3 2017 | 31 | 241,942 | 26.64 | 18.5 | % | 91 | 20.90 | 2.5 | ||||||||||||

Q2 2017 | 30 | 168,345 | 41.30 | 54.8 | % | 135 | 89.17 | 3.4 | ||||||||||||

Q1 2017 | 26 | 273,658 | 10.30 | 16.9 | % | 54 | 2.59 | 1.3 | ||||||||||||

Total - twelve months | 110 | 786,950 | $ | 30.00 | 32.5 | % | 101 | $ | 48.01 | 2.6 | ||||||||||

Total Leasing | ||||||||||||||||||||

Q4 2017 | 37 | 218,358 | $ | 28.67 | 68 | $ | 16.78 | 2.2 | ||||||||||||

Q3 2017 | 53 | 442,748 | 28.67 | 102 | 53.54 | 3.7 | ||||||||||||||

Q2 2017 | 41 | 216,786 | 40.23 | 133 | 85.14 | 3.2 | ||||||||||||||

Q1 2017 | 38 | 358,544 | 10.15 | 54 | 54.82 | 1.4 | ||||||||||||||

Total - twelve months | 169 | 1,236,436 | $ | 29.11 | 102 | $ | 59.16 | 3.0 | ||||||||||||

(1) | Comparable leases comprise leases for which prior leases were in place for the same suite within 12 months of executing a new lease. Comparable leases must have terms of at least six months and the square footage of the suite occupied by the new tenant cannot deviate by more than 50% from the size of the old lease’s suite. |

(2) | In Q2 2017, we signed a 53,000 square foot lease with WeWork LLC ("WeWork") at an office property in San Francisco, CA. Excluding WeWork, our weighted average growth for comparable office leases for the three months ended June 30, 2017 and for the trailing twelve months ended December 31, 2017 was 29.5% and 30.3%, respectively. Excluding WeWork, our weighted average growth for total comparable leases for the three months ended June 30, 2017 and for the year ended December 31, 2017 was 14.6% and 18.6%, respectively. |

Page | 22

INVESTMENT ACTIVITY |

The following tables describe changes in our portfolio from December 31, 2015 through December 31, 2017:

Square Feet | ||||||||||||||

(square feet in thousands) | Number of Properties | Total | Office | Retail | Industrial | |||||||||

Properties owned as of | ||||||||||||||

December 31, 2015 | 60 | 10,133 | 4,461 | 3,763 | 1,909 | |||||||||

2016 Acquisitions | 1 | 82 | — | 82 | — | |||||||||

2016 Dispositions | (7) | (1,236 | ) | (1,058 | ) | (52 | ) | (126 | ) | |||||

Building remeasurement and other (1) | 1 | (8 | ) | (3 | ) | (4 | ) | (1 | ) | |||||

December 31, 2016 | 55 | 8,971 | 3,400 | 3,789 | 1,782 | |||||||||

2017 Acquisitions | 2 | 344 | — | — | 344 | |||||||||

2017 Dispositions | (10) | (1,797 | ) | (155 | ) | (587 | ) | (1,055 | ) | |||||

Building remeasurement and other (1) | 1 | 42 | 29 | 13 | — | |||||||||

December 31, 2017 | 48 | 7,560 | 3,274 | 3,215 | 1,071 | |||||||||

(1) | Building remeasurements reflect changes in gross leasable area due to renovations or expansions of existing properties. In the fourth quarter of 2016, we sold one building of a multi-building grocery-anchored retail property, and continue to own the remaining buildings. In the third quarter of 2017, we sold one building from a three-building industrial property. The remaining two buildings were disposed of during the fourth quarter of 2017. Additionally, in the fourth quarter of 2017, we sold a retail outparcel that was part of a multi-building office property, and continue to own the remaining buildings. |

($ and square feet in thousands) | Segment | Market | Acquisition Date | Number of Properties | Contract Purchase Price | Square Feet | |||||||||

2017 Acquisitions: | |||||||||||||||

Vasco Road | Industrial | East Bay | 7/21/2017 | 1 | $ | 16,248 | 96 | ||||||||

Northgate | Industrial | Las Vegas | 7/26/2017 | 1 | 24,500 | 248 | |||||||||

Total 2017 Acquisitions | 2 | $ | 40,748 | 344 | |||||||||||

2016 Acquisitions: | |||||||||||||||

Suniland | Retail | South Florida | 5/27/2016 | 1 | $ | 66,500 | 82 | ||||||||

Page | 23

INVESTMENT ACTIVITY (continued) |

($ and square feet in thousands) | Segment | Market | Disposition Date | Number of Properties | Contract Sales Price | Square Feet | |||||||||

2017 Dispositions: | |||||||||||||||

Hanover | Retail | Greater Boston | 5/31/2017 | 1 | $ | 4,500 | 51 | ||||||||

Riverport Industrial Portfolio (1) | Industrial | Louisville | 6/9/2017 | 3 | 26,800 | 609 | |||||||||

Shiloh Road - Building 620 (2) | Industrial | Dallas | 7/21/2017 | — | 7,661 | 128 | |||||||||

Jay Street | Office | Silicon Valley | 10/17/2017 | 1 | 44,900 | 143 | |||||||||

Centerton Square | Retail | Philadelphia | 10/25/2017 | 1 | 129,630 | 426 | |||||||||

Cohasset | Retail | Greater Boston | 12/7/2017 | 1 | 13,050 | 50 | |||||||||

Harwich | Retail | Greater Boston | 12/15/2017 | 1 | 17,000 | 59 | |||||||||

Venture Corporate Center Outparcel (3) | Retail | South Florida | 12/15/2017 | 1 | 5,972 | 13 | |||||||||

Shiloh Road - Buildings 600 and 640 (2) | Industrial | Dallas | 12/18/2017 | 1 | 19,575 | 318 | |||||||||

Total 2017 Dispositions | 10 | $ | 269,088 | 1,797 | |||||||||||

2016 Dispositions: | |||||||||||||||

Colshire Drive | Office | Washington, DC | 2/18/2016 | 1 | $ | 158,400 | 574 | ||||||||

40 Boulevard | Office | Chicago | 3/1/2016 | 1 | 9,850 | 107 | |||||||||

Washington Commons | Office | Chicago | 3/1/2016 | 1 | 18,000 | 199 | |||||||||

Rockland 360-372 Market | Retail | Greater Boston | 8/5/2016 | 1 | 3,625 | 39 | |||||||||

6900 Riverport | Industrial | Louisville | 9/2/2016 | 1 | 5,400 | 126 | |||||||||

Sunset Hills | Office | Washington, DC | 9/30/2016 | 1 | 18,600 | 178 | |||||||||

Holbrook CVS Parcel (4) | Retail | Greater Boston | 11/18/2016 | 1 | 6,200 | 13 | |||||||||

Total 2016 Dispositions | 7 | $ | 220,075 | 1,236 | |||||||||||

(1) | Riverport Industrial Portfolio included three properties. |

(2) | Shiloh Road - Building 620 was one building of a three-building industrial property ("Shiloh Road"). The remaining two buildings of the Shiloh Road industrial property were disposed of during the fourth quarter of 2017. |

(3) | The retail outparcel was part of a multi-building office property and we continue to own the remaining buildings. |

(4) | We sold CVS Holbrook, one building of a multi-building grocery-anchored retail property, and continue to own the remaining buildings. |

Page | 24

DEFINITIONS |

This section contains an explanation of certain non-GAAP financial measures we provide in other sections of this document, as well as the reasons why management believes these measures provide useful information to investors about the Company’s financial condition or results of operations. Additional detail can be found in the Portfolio’s most recent annual report on Form 10-K and quarterly report on Form 10-Q, as well as other documents filed with or furnished to the Securities and Exchange Commission from time to time.

2017 Annual Report on Form 10-K

We refer to our Annual Report on Form 10-K for the period ended December 31, 2017, filed with the Securities and Exchange Commission on March 7, 2018, as our “2017 Annual Report on Form 10-K.”

Annualized Base Rent

Annualized base rent represents the annualized monthly base rent of leases executed as of December 31, 2017.

Comparable leases

Comparable leases comprise leases for which prior leases were in place for the same suite within 12 months of executing a new lease. Comparable leases must have terms of at least six months and the square footage of the suite occupied by the new tenant cannot deviate by more than 50% from the size of the old lease’s suite.

Fair Value

As determined in accordance with our valuation procedures, filed as Exhibit 4.4 to our 2017 Annual Report on Form 10-K. For a description of key assumptions used in calculating the value of our real properties as of December 31, 2017, refer to “Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities" in Part II, Item 5 of our 2017 Annual Report on Form 10-K.

FFO

We believe that FFO, as defined by the National Association of Real Estate Investment Trusts (“NAREIT”), is a meaningful supplemental measure of our operating performance because historical cost accounting for real estate assets in accordance with U.S. Generally Accepted Accounting Principles (“GAAP”) implicitly assumes that the value of real estate assets diminishes predictably over time, as reflected through depreciation and amortization expense. However, since real estate values have historically risen or fallen with market and other conditions, many industry investors and analysts have considered presentation of operating results for real estate companies that use historical cost accounting to be insufficient. Thus, NAREIT created FFO as a supplemental measure of operating performance for real estate investment trusts that consists of net income (loss), calculated in accordance with GAAP, plus real estate-related depreciation and amortization and impairment of depreciable real estate, less gains (or losses) from dispositions of real estate held for investment purposes.

FFO is presented herein as a supplemental financial measure and has inherent limitations. We do not use FFO as, nor should it be considered to be, an alternative to net income (loss) computed under GAAP as an indicator of our operating performance, or as an alternative to cash from operating activities computed under GAAP, or as an indicator of liquidity or our ability to fund our short or long-term cash requirements, including distributions to stockholders. Management uses FFO, in addition to net income (loss) computed under GAAP and cash flows from operating activities computed under GAAP, to evaluate our consolidated operating performance and as a guide to making decisions about future investments. Our FFO calculation does not present, nor do we intend it to present, a complete picture of our financial condition and operating performance. We caution investors against using FFO to determine a price to earnings ratio or yield relative to our NAV. We believe that net income (loss) computed under GAAP remains the primary measure of performance and that FFO is only meaningful when used in conjunction with net income (loss) computed under GAAP. Further, we believe that our consolidated financial statements, prepared in accordance with GAAP, provide the most meaningful picture of our financial condition and operating performance.

Further, FFO is not comparable to the performance measure established by the Investment Program Association (the “IPA”), referred to as “modified funds from operations,” or “MFFO,” as MFFO makes further adjustments including certain mark-to-market items and adjustments for the effects of straight-line rent. As such, FFO may not be comparable to the MFFO of non-listed REITs that disclose MFFO in accordance with the IPA standard.

Page | 25

DEFINITIONS (continued) |

Gross Investment Amount

The allocated gross basis of real property and debt-related investments, after certain adjustments. Gross Investment Amount for real property (i) includes the effect of intangible lease liabilities, (ii) excludes accumulated depreciation and amortization, and (iii) includes the impact of impairments. Amounts reported for debt-related investments represent our net accounting basis of the debt investments, which includes (i) unpaid principal balances, (ii) unamortized discounts, premiums, and deferred charges, and (iii) allowances for loan loss.

Leverage

Leverage is calculated by dividing the total principal outstanding under our total borrowings by the fair value of our real property and debt investments.

NOI and NOI—Cash Basis

We also use NOI as a supplemental financial performance measure because NOI reflects the specific operating performance of our real properties and excludes certain items that are not considered to be controllable in connection with the management of each property, such as other-than-temporary impairment, losses related to provisions for losses on debt-related investments, gains or losses on derivatives, acquisition-related expenses, gains or losses on extinguishment of debt and financing commitments, interest income, depreciation and amortization, general and administrative expenses, advisory fees, interest expense and noncontrolling interests. However, NOI should not be viewed as an alternative measure of our operating financial performance as a whole, since it does exclude such items that could materially impact our results of operations. Further, our NOI may not be comparable to that of other real estate companies, as they may use different methodologies for calculating NOI. Therefore, we believe net income, as defined by GAAP, to be the most appropriate measure to evaluate our overall financial performance. “NOI - Cash Basis” is NOI after eliminating the effects of straight-lining of rent and the impact of above- and below-market lease amortization and other non-cash amortization adjustments to rental revenue.

Non-Recurring Capital Expenditures

We classify capital expenditures that significantly increase a property’s ability to generate additional revenues relative to our initial underwriting as non-recurring capital expenditures. Examples of such capital expenditures may include property expansions, renovations or other significant strategic upgrades. Conversely, we classify capital expenditures incurred to maintain a property’s ability to generate expected revenues as “recurring.” In addition, we also classify the following capital expenditures as non-recurring:

• | First Generation Leasing Costs: We classify capital expenditures incurred to lease spaces for which we have either (i) never had a tenant or (ii) we expected a vacancy of the leasable space within two years of acquisition as non-recurring capital expenditures. |

• | Value-Add Acquisitions: We define a Value-Add Acquisition as a property that we acquire with one or more of the following characteristics: (i) existing vacancy equal to or in excess of 20%, (ii) short-term lease roll-over, typically during the first two years of ownership, that results in vacancy in excess of 20% when combined with the existing vacancy at the time of acquisition or (iii) significant capital improvement requirements in excess of 20% of the purchase price within the first two years of ownership. We classify any capital expenditures in Value-Add Acquisitions as non-recurring until the property reaches the earlier of (i) stabilization, which we define as 90% leased or (ii) five years after the date we acquire the property. |

• | Other Acquisitions: For property acquisitions that do not meet the criteria to qualify as Value-Add Acquisitions, we classify all anticipated capital expenditures within the first year of ownership as non-recurring. |

Same Store Properties

In our analysis of NOI, particularly to make comparisons of NOI between periods meaningful, it is important to provide information for properties that were in-service and owned by us throughout each period presented. We refer to properties acquired or placed in-service prior to the beginning of the earliest period presented and owned by us through the end of the latest period presented as “Same Store Properties.” “Same Store Properties” therefore exclude properties placed in-service, acquired, repositioned, or in development or redevelopment after the beginning of the earliest period presented or disposed of prior to the end of the latest period presented. Accordingly, it takes at least one year and one quarter after a property is acquired or treated as “in-service” for that property to be included in “Same Store Properties.” For the purposes of this supplement, our “Same Store Properties” include properties classified as held for sale in our annual financial statements at the end of the most recently completed period.

Valuation Procedures

We refer to our Valuation Procedures filed as Exhibit 4.4 to our 2017 Annual Report on Form 10-K as our “Valuation Procedures.”

Page | 26