Attached files

| file | filename |

|---|---|

| 10-K - FORM 10-K - CSB BANCORP INC /OH | d318212d10k.htm |

| EX-32.2 - EX-32.2 - CSB BANCORP INC /OH | d318212dex322.htm |

| EX-32.1 - EX-32.1 - CSB BANCORP INC /OH | d318212dex321.htm |

| EX-31.2 - EX-31.2 - CSB BANCORP INC /OH | d318212dex312.htm |

| EX-31.1 - EX-31.1 - CSB BANCORP INC /OH | d318212dex311.htm |

| EX-23.1 - EX-23.1 - CSB BANCORP INC /OH | d318212dex231.htm |

| EX-21 - EX-21 - CSB BANCORP INC /OH | d318212dex21.htm |

| EX-10.4 - EX-10.4 - CSB BANCORP INC /OH | d318212dex104.htm |

Exhibit 13

Hello

Relationships

you can bank on.

With The Commercial & Savings Bank you’re invited into a network of relationships

– among customers, employees, and shareholders – that contribute to the well-being and satisfaction of a community and its residents.

TABLE OF CONTENTS

2016 Financial Highlights 3

2016 Letter to Shareholders 4

Board of Directors 7

2016 Financial Review 8

Report on Management’s Assessment of Internal Control over Financial Reporting 23

Report of Independent

Registered

Public Accounting Firm 24

Consolidated Balance Sheets 25

Consolidated Statements of Income 26

Consolidated Statements of

Comprehensive Income 27

Consolidated Statements of

Changes in Shareholders’ Equity 27

Consolidated Statements of Cash Flows 28

Notes to Consolidated Financial Statements 30

Officers of The Commercial and Savings Bank 60

Shareholders and General Inquiries 61

Banking Center Information 62

2 2016 Report to Shareholders | CSB Bancorp, Inc.

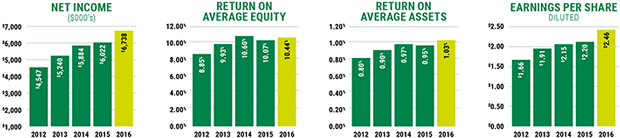

2016 FINANCIAL HIGHLIGHTS

| For the Year Ended December 31 | 2016 | 2015 | % CHANGE | |||||||||

|

|

||||||||||||

| (Dollars in thousands, except per share data) | ||||||||||||

| CONSOLIDATED RESULTS |

||||||||||||

| Net interest income |

$ 22,159 | $ 20,430 | 8% | |||||||||

| Net interest income – fully taxable-equivalent (FTE) basis |

22,531 | 20,758 | 9 | |||||||||

| Noninterest income |

4,296 | 4,424 | (3) | |||||||||

| Provision for loan losses |

493 | 389 | 27 | |||||||||

| Noninterest expense |

16,255 | 15,796 | 3 | |||||||||

| Net income |

6,738 | 6,022 | 12 | |||||||||

|

|

||||||||||||

| AT YEAR-END |

||||||||||||

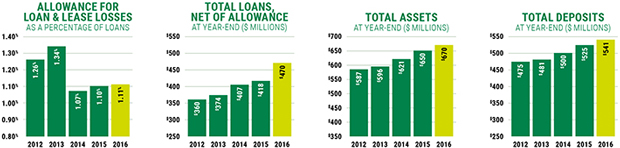

| Loans, net |

$ 470,158 | $ 418,209 | 12% | |||||||||

| Assets |

669,978 | 650,314 | 3 | |||||||||

| Deposits |

540,785 | 525,042 | 3 | |||||||||

| Shareholders’ equity |

65,415 | 61,266 | 7 | |||||||||

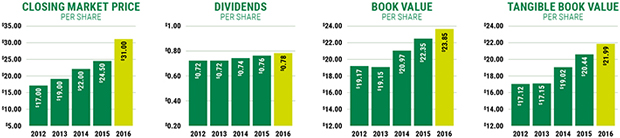

| Cash dividends declared per share |

0.78 | 0.76 | 3 | |||||||||

| Book value per share |

23.85 | 22.35 | 7 | |||||||||

| Tangible book value per share |

21.99 | 20.44 | 8 | |||||||||

| Market price per share |

31.00 | 24.50 | 27 | |||||||||

| Basic and diluted earnings per share |

2.46 | 2.20 | 12 | |||||||||

|

|

||||||||||||

| FINANCIAL PERFORMANCE |

||||||||||||

| Return on average assets |

1.03 | % | 0.95 | % | ||||||||

| Return on average equity |

10.44 | 10.07 | ||||||||||

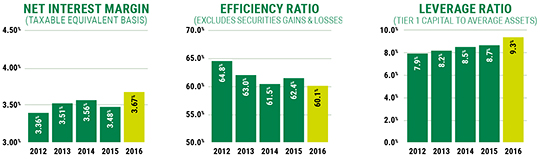

| Net interest margin, FTE |

3.67 | 3.48 | ||||||||||

| Efficiency ratio |

60.14 | 62.37 | ||||||||||

|

|

||||||||||||

| CAPITAL RATIOS |

||||||||||||

| Risk-based capital: |

||||||||||||

| Common equity Tier 1 |

12.58 | % | 12.49 | % | ||||||||

| Tier 1 |

12.58 | 12.49 | ||||||||||

| Total |

13.67 | 13.52 | ||||||||||

| Leverage |

9.30 | 8.74 | ||||||||||

2016 Report to Shareholders | CSB Bancorp, Inc.

3

LETTER TO SHAREHOLDERS

DEAR FELLOW SHAREHOLDER:

2016 was a good year for CSB as we continued to grow and build momentum. Our progress was marked by a fifth consecutive year of record earnings. Total return on CSB stock amounted to 30% including the reinvestment of dividends.

These financial results are encouraging, yet we firmly believe that continued progress and improvement is vital to maintaining our momentum. We strive for consistent improvement in performance and capabilities. While significant investments or changing macroeconomic conditions tend to impact results for a period of time, our vision of enduring greatness keeps us focused on delivering shareholder value in a sustainable manner and conducting business for the long haul.

The balance of this letter reviews some highlights of the past year and initiatives we are focusing on for the future.

TRENDS BY THE NUMBERS:

Return on assets climbed above 1% in 2016 and return on equity exceeded 10% for the third consecutive year. Additional metrics reflect our consistency in performance and improving trends.

UNDERLYING FUNDAMENTALS

In last year’s shareholder letter, we reported loan growth was elusive for much of 2015 and we had responded by increasing our team of lenders and streamlining loan approval processes. These efforts, along with a steadily improving economy, resulted in 12% loan growth during 2016 with increases in all major categories. We will continue to focus on loan growth in 2017.

Credit quality remained acceptable and relatively stable during 2016. Total delinquent and non-accrual balances again averaged well under 1%, and we posted a net recovery of 0.03% of total average balances. As we enter 2017, consumer and commercial credit categories are both performing acceptably. Credit risk is ever-present in banking and we manage it by disciplined underwriting and review, maintaining a diversified mix of loans, monitoring concentrations and correlated risks, and reserving for losses with consistent and appropriately conservative methodology.

Deposit balances increased 3% during 2016. Over the past eight years, our compound annual growth rate (CAGR) for deposits equates to 9.6%, while total deposits for FDIC-insured institutions in our four county area have exhibited a 2.8% CAGR. We focus on attracting core deposits, which we believe can best support steady growth and provide manageable cost of funds.

We believe we have considerable opportunity to gain additional market share. We hold 5% of FDIC-insured institution deposits in our four county market area, more than any other community bank and now sixth overall when including large regional and national banks. We also hold 12.5% of deposits in combined Holmes, Tuscarawas and Wayne counties, second only to a very large national bank with a 15% share. Stark County, where we have only one banking center and 0.1% of total deposits, also offers significant loan and deposit growth potential for our bank.

THE BANKING ENVIRONMENT AND OUR COMPANY’S POSTURE

Eight years of extremely low interest rates have created significant search for yield and volume in the banking industry, resulting in very strong competition for earning assets. We have maintained a relatively balanced interest rate risk posture throughout the period and will continue to avoid balance sheet strategies that create significant interest rate risk.

| 4 2016 Report to Shareholders | CSB Bancorp, Inc. |

| LETTER TO SHAREHOLDERS | ||

Merger and acquisition activity remains a somewhat steady presence in the banking industry. The increased revenue generation and efficiencies that can be gained through acquired volume are primary drivers of much of this activity, with regulatory burden and leadership succession also factors. Several transactions have occurred in our area over the past two years. We view these transactions and the resulting market disruption as providing further opportunity for our organic growth and we are leveraging efforts accordingly. In addition, we remain open to the possibility of growing our Company through compelling transaction opportunities.

THE TRUMP EFFECT?

A sense of increased optimism about the economy and business conditions emerged with the results of November’s national election. Financial institution stock prices jumped 21% nationally in the three months following the election (CSB stock rose 6%). Expectations for lower taxes, increased spending on infrastructure, less regulation, and rising interest rates seem to be fueling optimism for bank stocks. Time will tell to what degree these anticipated conditions materialize. Our strategy is built on attracting and retaining great talent, developing superb capabilities, and executing with prudent business practices. As such, on a relative basis, we will not be dependent upon changes in regulatory or fiscal policies in order to meet our objectives.

| BANKING CENTERS While most banking centers are experiencing a slow decline in transaction counts and branch visits per customer, our physical locations remain a key link to the customers and communities we serve. Location convenience continues to be one key determinant of in-branch activity. We prefer to be located along mainstream consumer traffic patterns and we prefer to own our locations wherever practical. During 2016, we purchased our existing Charm location, relocated the downtown Wooster banking center from West Liberty Street to East Liberty Street, and made plans to consolidate our two leased Orrville locations | ||||||||||||

| into one new banking center to be constructed on property we purchased in the 100 block of West High Street. We anticipate opening this new banking center in late 2017 or early 2018.

DIGITAL WORLD We are closely monitoring and investing in various forms of financial technology. Our objective is to offer safe, convenient, and customer-friendly digital platforms that provide solutions to real needs, thus enhancing the CSB experience. Over the past year and a half, a team of CSB specialists completely redesigned our website. Launched in January 2017, the new csb1.com provides significant functional upgrades for customers, shareholders, and prospective employees, and is built on a customizable platform that sets the stage for further enhancements. Other significant technology investments over the past several years include upgraded or new systems for core processing, digital content management, mortgage origination, consumer lending, loan processing, credit analysis, and corporate phone communications. These systems are solid and scalable to support continued growth. |

| |||||||||||

|

SENIOR MANAGEMENT OF THE COMMERCIAL & SAVINGS BANK

| ||||||||||||

| Pictured Left to Right:

|

||||||||||||

| BUD STEBBINS | PAULA MEILER | EDDIE STEINER | ||||||||||

| Senior Vice President | Senior Vice President | President | ||||||||||

| Senior Loan Officer

|

Chief Financial Officer | Chief Executive Officer | ||||||||||

| ANDREA MILEY | BRETT GALLION | |||||||||||

| Senior Vice President | Senior Vice President | |||||||||||

| Senior Risk Officer | Senior Operations Officer | |||||||||||

| Senior Information Officer | ||||||||||||

| 2016 Report to Shareholders | CSB Bancorp, Inc. 5 |

| LETTER TO SHAREHOLDERS |

|

EDDIE STEINER

ROBERT BAKER |

THE CSB BRAND As we continue to grow in newer markets, we are focusing more intently on brand awareness. We are promoting our presence within each market, increasing familiarity with CSB and its people, and adding value through customer education. These brand building efforts highlight our local experts, customized services, high-touch technology, principled growth and community involvement. We are utilizing a blend of traditional messaging (e.g. billboards) and digital content messaging (e.g. social media) in these brand building efforts.

OUR PEOPLE The dedicated team members throughout the Company are the very essence of CSB. Our culture, our commitment to excellence, our foundation of dealing uprightly in all respects, and ultimately our success are all attributable to the efforts of these talented individuals. CSB team members do great things every day; their efforts are what make CSB noticeably different. We are proud to be associated with this talented group of individuals.

CONCLUDING REMARKS CSB is a strong community bank and continually improving. Our systems, talented people, and development initiatives are positioning us well for growth. Our board is fully engaged and we have a culture of excellence and good governance. We believe we are delivering value for our shareholders and we are working diligently to forge an enduring and rewarding future for the CSB’s stakeholders. We are grateful for the continued support of shareholders, employees, and the communities CSB serves. We consider it an extraordinary privilege to be part of The CSB Way and are thankful to provide this report on behalf of the entire CSB team. | |

|

|

| |||||

| EDDIE STEINER President and Chief Executive Officer |

ROBERT “ROC” BAKER Chairman of the Board of Directors | |||||

6 2016 Report to Shareholders | CSB Bancorp, Inc.

BOARD OF DIRECTORS

| Pictured Left to Right: | ||||

| JOHN R. WALTMAN | ROBERT K. BAKER | JULIAN L. COBLENTZ | ||

| Attorney, Of Counsel, Critchfield, Critchfield & Johnson |

Co-Owner and Controller, Bakerwell, Inc. Chairman, CSB Bancorp, Inc. |

Vice President, Coblentz Distributing, Inc. Operations Manager, Walnut Creek Foods | ||

| JEFFERY A. ROBB, SR. | EDDIE L. STEINER | J. THOMAS LANG | ||

| CEO, Robb Companies, Inc. Robbco Marine/Ohio Yamaha |

President, Chief Executive Officer, CSB Bancorp, Inc. |

Veterinarian Dairy Farmer, Spring Hill Farms, Inc. | ||

| RONALD E. HOLTMAN | ||||

| Retired Attorney |

||||

2016 Report to Shareholders | CSB Bancorp, Inc.

7

2016 FINANCIAL REVIEW

INTRODUCTION

CSB Bancorp, Inc. (the “Company” or “CSB”) was incorporated under the laws of the State of Ohio in 1991 and is a registered financial holding company. The Company’s wholly-owned subsidiaries are The Commercial and Savings Bank (the “Bank”) and CSB Investment Services, LLC. The Bank is chartered under the laws of the State of Ohio and was organized in 1879. The Bank is a member of the Federal Reserve System, with deposits insured by the Federal Deposit Insurance Corporation, and its primary regulators are the Ohio Division of Financial Institutions and the Federal Reserve Board.

The Company, through the Bank, provides retail and commercial banking services to its customers including checking and savings accounts, time deposits, cash management, safe deposit facilities, personal loans, commercial loans, real estate mortgage loans, installment loans, IRAs, night depository facilities, and trust and brokerage services. Its customers are located primarily in Holmes, Tuscarawas, Wayne, Stark, and portions of surrounding counties in Ohio.

Economic activity in the Company’s market area has been increasing at a modest but rather steady pace for the past eight years. The expansion has been most prevalent in small to mid-sized manufacturing and across various professional and non-professional service sectors. Reported unemployment levels at December 2016 ranged from 3.4% to 5.2% in the four primary counties served by the Company. These levels are largely unchanged from December 2015. Many local employers report tight hiring conditions. Wage pressure has increased for entry level jobs in certain sectors such as banking and construction. The local housing market continues to improve. Unit sales and housing construction levels increased during 2016 with some observable price appreciation. Ohio’s shale gas industry reported an uptick in the number of permits issued and drilling rigs operating during 2016. The increased activity was supported by oil prices recovering from record lows in January 2016 as well as regional gas producers maintaining output near historic highs to fund cash and debt service requirements. The Company’s market is adjacent to areas of primary shale activity.

FORWARD-LOOKING STATEMENTS

Certain statements contained in Management’s Discussion and Analysis of Financial Condition and Results of Operations are not related to historical results, but are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve a number of risks and uncertainties. Any forward-looking statements made by the Company herein and in future reports and statements are not guarantees of future performance. Actual results may differ materially from those in forward-looking statements because of various risk factors as discussed in this annual report and the Company’s Annual Report on Form 10-K. The Company does not undertake, and specifically disclaims, any obligation to publicly release the result of any revisions to any forward-looking statements to reflect the occurrence of unanticipated events or circumstances after the date of such statements.

8

2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

SELECTED FINANCIAL DATA

The following table sets forth certain selected consolidated financial information:

| (Dollars in thousands, except share data)

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||

|

|

||||||||||||||||||||

| Statements of income: |

||||||||||||||||||||

| Total interest income |

$ | 23,632 | $ | 21,997 | $ | 21,656 | $ | 21,138 | $ | 20,584 | ||||||||||

| Total interest expense |

1,473 | 1,567 | 1,729 | 2,255 | 2,978 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

22,159 | 20,430 | 19,927 | 18,883 | 17,606 | |||||||||||||||

| Provision for loan losses |

493 | 389 | 643 | 840 | 823 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for loan losses |

21,666 | 20,041 | 19,284 | 18,043 | 16,783 | |||||||||||||||

| Noninterest income |

4,296 | 4,424 | 4,250 | 4,318 | 4,204 | |||||||||||||||

| Noninterest expense |

16,255 | 15,796 | 15,082 | 14,848 | 14,450 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

9,707 | 8,669 | 8,452 | 7,513 | 6,537 | |||||||||||||||

| Income tax provision |

2,969 | 2,647 | 2,568 | 2,273 | 1,990 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 6,738 | $ | 6,022 | $ | 5,884 | $ | 5,240 | $ | 4,547 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Per share of common stock: |

||||||||||||||||||||

| Basic income per share |

$ | 2.46 | $ | 2.20 | $ | 2.15 | $ | 1.91 | $ | 1.66 | ||||||||||

| Diluted income per share |

2.46 | 2.20 | 2.15 | 1.91 | 1.66 | |||||||||||||||

| Dividends |

0.78 | 0.76 | 0.74 | 0.72 | 0.72 | |||||||||||||||

| Book value |

23.85 | 22.35 | 20.97 | 19.15 | 19.17 | |||||||||||||||

| Average basic common shares outstanding |

2,742,028 | 2,739,470 | 2,737,636 | 2,736,473 | 2,734,889 | |||||||||||||||

| Average diluted common shares outstanding |

2,742,028 | 2,742,108 | 2,739,078 | 2,738,477 | 2,735,141 | |||||||||||||||

| Year-end balances: |

||||||||||||||||||||

| Loans, net |

$ | 470,158 | $ | 418,209 | $ | 406,522 | $ | 374,040 | $ | 360,000 | ||||||||||

| Securities |

132,372 | 166,402 | 143,038 | 151,535 | 134,754 | |||||||||||||||

| Total assets |

669,978 | 650,314 | 620,981 | 596,465 | 586,900 | |||||||||||||||

| Deposits |

540,785 | 525,042 | 500,075 | 480,933 | 475,443 | |||||||||||||||

| Borrowings |

61,127 | 62,063 | 61,580 | 61,130 | 56,664 | |||||||||||||||

| Shareholders’ equity |

65,415 | 61,266 | 57,450 | 52,411 | 52,453 | |||||||||||||||

| Average balances: |

||||||||||||||||||||

| Loans, net |

$ | 443,862 | $ | 407,517 | $ | 400,876 | $ | 369,889 | $ | 338,441 | ||||||||||

| Securities |

147,649 | 151,181 | 145,065 | 138,976 | 132,567 | |||||||||||||||

| Total assets |

651,318 | 633,298 | 604,605 | 581,150 | 564,875 | |||||||||||||||

| Deposits |

519,941 | 505,913 | 479,330 | 468,395 | 453,526 | |||||||||||||||

| Borrowings |

64,528 | 65,515 | 67,657 | 57,882 | 57,735 | |||||||||||||||

| Shareholders’ equity |

64,524 | 59,799 | 55,529 | 52,787 | 51,384 | |||||||||||||||

| Select ratios: |

||||||||||||||||||||

| Net interest margin, tax equivalent basis |

3.67 | % | 3.48 | % | 3.56 | % | 3.51 | % | 3.36 | % | ||||||||||

| Return on average total assets |

1.03 | 0.95 | 0.97 | 0.90 | 0.80 | |||||||||||||||

| Return on average shareholders’ equity |

10.44 | 10.07 | 10.60 | 9.93 | 8.85 | |||||||||||||||

| Average shareholders’ equity as a percent of average total assets |

9.91 | 9.44 | 9.18 | 9.08 | 9.10 | |||||||||||||||

| Net loan charge-offs as a percent of average loans |

(0.03 | ) | 0.03 | 0.33 | 0.09 | 0.09 | ||||||||||||||

| Allowance for loan losses as a percent of loans at year-end |

1.11 | 1.10 | 1.07 | 1.34 | 1.26 | |||||||||||||||

| Shareholders’ equity as a percent of total year-end assets |

9.76 | 9.42 | 9.25 | 8.79 | 8.94 | |||||||||||||||

| Dividend payout ratio |

31.71 | 34.55 | 34.42 | 37.60 | 43.30 | |||||||||||||||

2016 Report to Shareholders | CSB Bancorp, Inc.

9

2016 FINANCIAL REVIEW

RESULTS OF OPERATIONS

Net Income

CSB’s 2016 net income was $6.7 million compared to $6.0 million for 2015, representing an increase of 12%. Basic and diluted earnings per share were $2.46, up 12% from the prior year. The return on average assets was 1.03% in 2016 compared to 0.95% in 2015 and return on average equity was 10.44% in 2016 compared to 10.07% in 2015.

Net income for 2015 was $6.0 million while basic and diluted earnings per share were $2.20 as compared to $5.9 million, or $2.15 per share, for the year ended December 31, 2014. Net income increased 2% during 2015 as compared to 2014 due primarily to a $503 thousand increase in total net interest income and $254 thousand decrease in the provision for loan losses. Partially offsetting the higher revenue were increases in noninterest expenses and federal income taxes. Return on average assets was 0.95% in 2015 compared to 0.97% in 2014 and return on average shareholders’ equity was 10.07% in 2015 as compared to 10.60% in 2014.

Net Interest Income

| (Dollars in thousands)

|

2016

|

2015

|

2014

|

|||||||||

|

|

||||||||||||

| Net interest income |

$ | 22,159 | $ | 20,430 | $ | 19,927 | ||||||

| Taxable equivalent1 |

372 | 328 | 285 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net interest income, fully taxable equivalent |

$ | 22,531 | $ | 20,758 | $ | 20,212 | ||||||

|

|

|

|

|

|

|

|||||||

| Net interest margin |

3.61 | % | 3.42 | % | 3.51 | % | ||||||

| Taxable equivalent adjustment1 |

0.06 | 0.06 | 0.05 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net interest margin-taxable equivalent |

3.67 | % | 3.48 | % | 3.56 | % | ||||||

|

|

|

|

|

|

|

|||||||

1Taxable equivalent adjustments have been computed assuming a 34% tax rate.

Net interest income is the largest source of the Company’s revenue and consists of the difference between interest income generated on earning assets and interest expense incurred on liabilities (deposits, short-term and long-term borrowings). Volumes, interest rates, composition of interest-earning assets, and interest-bearing liabilities affect net interest income.

Net interest income increased $1.7 million, or 8%, in 2016 compared to 2015 primarily due to a 9% increase in average loan balances and a decrease of 3 basis points in the average rate paid on interest-bearing liabilities. The net interest margin increased to 3.61% from 3.42% in 2015.

Net interest income increased $503 thousand, or 3%, in 2015 compared to 2014 partially due to a 5% increase in average earning assets with increased average loan, investment, and cash balances. Additionally, the net interest margin decreased to 3.42% from 3.51% in 2014. The margin decrease was primarily due to increased cash balances throughout nine months of the year with loan growth returning during the fourth quarter of 2015.

Interest income increased $1.6 million, or 7%, in 2016 compared to 2015 due to a $37 million increase in average loan balances. The increase in average loan volume throughout the year helped mitigate the low interest rate environment. In 2016, interest rates paid on deposits hit their lowest point with the first increases to deposit rates starting in December 2016.

Interest income increased $341 thousand, or 2%, in 2015 compared to 2014 due to the $6 million increase in average loan balances, partially offset by a 1 basis point lower yield. Rates decreased on loans and securities categories with reduced rates on new and repriced assets due to lending competition and a lower interest rate environment. The increase in average loan volume helped mitigate the low interest rate environment. In 2015, average cash and securities balances to average gross earning assets rose 2% to 31%. Securities yields continued to decline in 2015 with new and reinvestment cash flows being deployed at lower rates.

Interest expense decreased $94 thousand, or 6%, in 2016 as compared to 2015 due to decreases in time deposits and other borrowed funds and a continued shift in the liability mix towards less expensive, noninterest bearing demand deposits. Total average time deposits continued to decline as customers anticipate rising interest rates.

Interest expense decreased $162 thousand, or 9%, in 2015 as compared to 2014 due to decreases in the cost of all categories of interest-bearing liabilities and a continued shift in the liability mix towards less expensive, noninterest bearing demand deposits, and savings accounts. Total average time deposits continued to decline with an emphasis on growing customers with multiple banking relationships, as opposed to single service time deposit customers.

10 2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

The following table provides detailed analysis of changes in average balances, yield, and net interest income:

AVERAGE BALANCE SHEETS AND NET INTEREST MARGIN ANALYSIS

| 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands)

|

Average

|

Interest

|

Average

|

Average

|

Interest

|

Average

|

Average

|

Interest

|

Average

|

|||||||||||||||||||||||||||||||||||

| Interest-earning assets |

||||||||||||||||||||||||||||||||||||||||||||

| Federal funds sold |

$ | 732 | $ | 3 | 0.44% | $ | 982 | $ | 2 | 0.23% | $ | 546 | $ | 1 | 0.22% | |||||||||||||||||||||||||||||

| Interest-earning deposits |

16,946 | 107 | 0.63 | 32,395 | 94 | 0.29 | 16,356 | 42 | 0.26 | |||||||||||||||||||||||||||||||||||

| Securities: |

||||||||||||||||||||||||||||||||||||||||||||

| Taxable |

119,701 | 2,598 | 2.17 | 129,700 | 2,790 | 2.15 | 128,973 | 2,857 | 2.22 | |||||||||||||||||||||||||||||||||||

| Tax exempt |

27,948 | 646 | 2.31 | 21,481 | 563 | 2.61 | 16,092 | 466 | 2.89 | |||||||||||||||||||||||||||||||||||

| Loans3 |

448,941 | 20,278 | 4.52 | 412,147 | 18,548 | 4.50 | 405,973 | 18,290 | 4.51 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| Total interest-earning assets |

614,268 | 23,632 | 3.85% | 596,705 | 21,997 | 3.69% | 567,940 | 21,656 | 3.81% | |||||||||||||||||||||||||||||||||||

| Noninterest-earning assets |

||||||||||||||||||||||||||||||||||||||||||||

| Cash and due from banks |

13,914 | 13,661 | 13,663 | |||||||||||||||||||||||||||||||||||||||||

| Bank premises and equipment, net |

8,531 | 8,290 | 8,494 | |||||||||||||||||||||||||||||||||||||||||

| Other assets |

19,684 | 19,272 | 19,605 | |||||||||||||||||||||||||||||||||||||||||

| Allowance for loan losses |

(5,079 | ) | (4,630 | ) | (5,097 | ) | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Total assets |

$ | 651,318 | $ | 633,298 | $ | 604,605 | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Interest-bearing liabilities |

||||||||||||||||||||||||||||||||||||||||||||

| Demand deposits |

$ | 83,956 | 33 | 0.04% | $ | 77,689 | 27 | 0.03% | $ | 73,307 | 36 | 0.05% | ||||||||||||||||||||||||||||||||

| Savings deposits |

163,271 | 123 | 0.08 | 158,531 | 113 | 0.07 | 151,822 | 130 | 0.09 | |||||||||||||||||||||||||||||||||||

| Time deposits |

116,427 | 850 | 0.73 | 125,180 | 941 | 0.75 | 129,676 | 1,000 | 0.77 | |||||||||||||||||||||||||||||||||||

| Borrowed funds |

64,528 | 467 | 0.72 | 65,515 | 486 | 0.74 | 67,657 | 563 | 0.83 | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| Total interest-bearing liabilities |

428,182 | 1,473 | 0.34% | 426,915 | 1,567 | 0.37% | 422,462 | 1,729 | 0.41% | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| Noninterest-bearing liabilities and shareholders’ equity |

||||||||||||||||||||||||||||||||||||||||||||

| Demand deposits |

156,287 | 144,513 | 124,525 | |||||||||||||||||||||||||||||||||||||||||

| Other liabilities |

2,325 | 2,071 | 2,089 | |||||||||||||||||||||||||||||||||||||||||

| Shareholders’ equity |

64,524 | 59,799 | 55,529 | |||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Total liabilities and equity |

$ | 651,318 | $ | 633,298 | $ | 604,605 | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Net interest income |

$ | 22,159 | $ | 20,430 | $ | 19,927 | ||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Net interest margin |

3.61% | 3.42% | 3.51% | |||||||||||||||||||||||||||||||||||||||||

| Net interest spread |

3.51% | 3.32% | 3.40% | |||||||||||||||||||||||||||||||||||||||||

1Average balances have been computed on an average daily basis.

2Average rates have been computed based on the amortized cost of the corresponding asset or liability.

3Average loan balances include nonaccrual loans.

2016 Report to Shareholders | CSB Bancorp, Inc.

11

2016 FINANCIAL REVIEW

The following table compares the impact of changes in average rates and changes in average volumes on net interest income:

RATE/VOLUME ANALYSIS CHANGES IN INCOME AND EXPENSE1

| 2016 v. 2015 | 2015 v. 2014 | |||||||||||||||||||||||||||||||

| (Dollars in thousands)

|

Net Increase

|

Volume

|

Rate

|

Net Increase

|

Volume

|

Rate

| ||||||||||||||||||||||||||

| Increase (decrease) in interest income: |

||||||||||||||||||||||||||||||||

| Federal funds |

$ | 1 | $ | (1 | ) | $ | 2 | $ | 1 | $ | 1 | $ | – | |||||||||||||||||||

| Interest-earning deposits |

13 | (98 | ) | 111 | 52 | 46 | 6 | |||||||||||||||||||||||||

| Securities: |

||||||||||||||||||||||||||||||||

| Taxable |

(192 | ) | (217 | ) | 25 | (67 | ) | 16 | (83 | ) | ||||||||||||||||||||||

| Tax exempt |

83 | 149 | (66 | ) | 97 | 141 | (44 | ) | ||||||||||||||||||||||||

| Loans |

1,730 | 1,661 | 69 | 258 | 278 | (20 | ) | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total interest income change |

1,635 | 1,494 | 141 | 341 | 482 | (141 | ) | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Increase (decrease) in interest expense: |

||||||||||||||||||||||||||||||||

| Demand deposits |

6 | 2 | 4 | (9 | ) | 2 | (11 | ) | ||||||||||||||||||||||||

| Savings deposits |

10 | 4 | 6 | (17 | ) | 5 | (22 | ) | ||||||||||||||||||||||||

| Time deposits |

(91 | ) | (64 | ) | (27 | ) | (59 | ) | (34 | ) | (25 | ) | ||||||||||||||||||||

| Other borrowed funds |

(19 | ) | (7 | ) | (12 | ) | (77 | ) | (16 | ) | (61 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total interest expense change |

(94 | ) | (65 | ) | (29 | ) | (162 | ) | (43 | ) | (119 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net interest income change |

$ | 1,729 | $ | 1,559 | $ | 170 | $ | 503 | $ | 525 | $ | (22 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

1Changes attributable to both volume and rate, which cannot be segregated, have been allocated based on the absolute value of the change due to volume and the change due to rate.

Provision For Loan Losses

The provision for loan losses is determined by management as the amount required to bring the allowance for loan losses to a level considered appropriate to absorb probable future net charge-offs inherent in the loan portfolio as of period end. The provision for loan losses was $493 thousand in 2016, $389 thousand in 2015, and $643 thousand in 2014. Higher provision expense in 2016 and 2015 reflects an increasing volume in the loan portfolio. See “Financial Condition – Allowance for Loan Losses” for additional discussion and information relative to the provision for loan losses.

Noninterest Income

| YEAR ENDED DECEMBER 31 | |||||||||||||||||||||||||||||||||||

|

Change from 2015 |

Change from 2014 | ||||||||||||||||||||||||||||||||||

| (Dollars in thousands)

|

2016

|

Amount

|

%

|

2015

|

Amount

|

%

|

2014

| ||||||||||||||||||||||||||||

| Service charges on deposit accounts |

$ | 1,166 | $ | (37 | ) | (3.1 | )% | $ | 1,203 | $ | (66 | ) | (5.2 | )% | $ | 1,269 | |||||||||||||||||||

| Trust services |

861 | 1 | 0.0 | 860 | 49 | 6.0 | 811 | ||||||||||||||||||||||||||||

| Debit card interchange fees |

1,087 | 99 | 10.0 | 988 | 78 | 8.6 | 910 | ||||||||||||||||||||||||||||

| Gain on sale of loans, including MSR’s |

309 | (54 | ) | (14.9 | ) | 363 | 165 | 83.3 | 198 | ||||||||||||||||||||||||||

| Earnings on bank-owned life insurance |

276 | 6 | 2.2 | 270 | 6 | 2.3 | 264 | ||||||||||||||||||||||||||||

| Securities gains |

1 | (55 | ) | (98.2 | ) | 56 | (77 | ) | (57.9 | ) | 133 | ||||||||||||||||||||||||

| Other |

596 | (88 | ) | (12.9 | ) | 684 | 19 | 2.9 | 665 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

| Total noninterest income |

$ | 4,296 | $ | (128 | ) | (2.9 | )% | $ | 4,424 | $ | 174 | 4.1 | % | $ | 4,250 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

12

2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

Noninterest income decreased $128 thousand, or 3%, in 2016 compared to the same period in 2015. Gains on sales of mortgage loans including mortgage servicing rights (“MSRs”) decreased 15% due to decreasing sales of real estate mortgage loans into the secondary market and customers opting into variable rate mortgages that have been retained by the Bank. The Bank originated and sold $11 million in mortgage loans in 2016 as compared to the sale of $12 million of loans in 2015. Service charges on deposits, which are primarily customer overdraft fees, decreased 3% in 2016, with a 6% decrease in overdraft fees due to improving consumer deposit balances. Debit card interchange fees increased 10% in 2016 compared to 2015 due to increased volume.

Noninterest income increased $174 thousand, or 4%, in 2015 compared to the same period in 2014. Gains on sales of mortgage loans including MSRs increased 83% due to increasing unit sales of real estate and the extension of the low interest rate environment in 2015. The Bank originated and sold $12 million in mortgage loans in 2015 as compared to the sale of $6 million of loans in 2014. Service charges on deposits, which are primarily customer overdraft fees, decreased 5% in 2015, with a 6% decrease in overdraft fees due to increasing health of consumer deposit balances. Trust and brokerage services increased 6% as brokerage fees contained within trust services increased $54 thousand in 2015. The average market value of trust assets under management was $95 million in 2015 and 2014. During 2015, available-for-sale securities with gains of $56 thousand were sold.

Noninterest Expenses

| YEAR ENDED DECEMBER 31

| |||||||||||||||||||||||||||||||||||

| Change from 2015

|

Change from 2014

|

||||||||||||||||||||||||||||||||||

| (Dollars in thousands)

|

2016

|

Amount

|

%

|

2015

|

Amount

|

%

|

2014

| ||||||||||||||||||||||||||||

| Salaries and employee benefits |

$ | 9,354 | $ | 535 | 6.1 | % | $ | 8,819 | $ | 498 | 6.0 | % | $ | 8,321 | |||||||||||||||||||||

| Occupancy expense |

973 | (54 | ) | (5.3 | ) | 1,027 | 13 | 1.3 | 1,014 | ||||||||||||||||||||||||||

| Equipment expense |

679 | 16 | 2.4 | 663 | (52 | ) | (7.3 | ) | 715 | ||||||||||||||||||||||||||

| Professional and director fees |

832 | 2 | 0.2 | 830 | 105 | 14.5 | 725 | ||||||||||||||||||||||||||||

| Financial institutions tax |

427 | 27 | 6.8 | 400 | 39 | 10.8 | 361 | ||||||||||||||||||||||||||||

| Marketing and public relations |

415 | (4 | ) | (1.0 | ) | 419 | 41 | 10.8 | 378 | ||||||||||||||||||||||||||

| Software expense |

799 | (2 | ) | (0.2 | ) | 801 | 74 | 10.2 | 727 | ||||||||||||||||||||||||||

| Debit card expense |

445 | 32 | 7.7 | 413 | (8 | ) | (1.9 | ) | 421 | ||||||||||||||||||||||||||

| FDIC insurance |

282 | (75 | ) | (21.0 | ) | 357 | (1 | ) | (0.3 | ) | 358 | ||||||||||||||||||||||||

| Amortization of intangible assets |

121 | (4 | ) | (3.2 | ) | 125 | (5 | ) | (3.8 | ) | 130 | ||||||||||||||||||||||||

| Other |

1,928 | (14 | ) | (0.7 | ) | 1,942 | 10 | 0.5 | 1,932 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

| Total noninterest expenses |

$ | 16,255 | $ | 459 | 2.9 | % | $ | 15,796 | $ | 714 | 4.7 | % | $ | 15,082 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

Noninterest expense increased $459 thousand, or 3%, in 2016 compared to 2015. Salaries and employee benefits increased $535 thousand due to base compensation increasing $436 thousand as a result of additional full-time employees and annual adjustments. Increases in 2016 included medical and dental expense rising $45 thousand and employment taxes rising $38 thousand. The capitalization of employee costs of loan originations contributed to a decrease in salary expense of $109 thousand. Debit card expense increased $32 thousand in 2016, with increased costs due to the migration to EMV chip cards. Debit cards are being issued with embedded chips that protect cardholder data. An increase in the Ohio Financial institutions tax was recognized as capital increased. Equipment expense increased $16 thousand in 2016, as compared to 2015, with small equipment replacement. The FDIC insurance assessment decreased $75 thousand, or 21%, due to a rate reduction starting July 1, 2016. Occupancy expense decreased primarily with a reduction of branch facility costs, which included a branch relocation and the purchase of a branch office that had been previously leased.

Noninterest expense increased $714 thousand, or 5%, in 2015 compared to 2014. Salaries and employee benefits increased $498 thousand due to base compensation increasing $277 thousand as a result of additional full-time employees and annual adjustments. Medical and dental expense increased $76 thousand in 2015. Capitalization of employee costs of loan originations contributed to an increase in expense of $34 thousand. Software expense increased $74 thousand in 2015, primarily due to a loss of earned software maintenance credits of approximately $37 thousand in 2014 that were not available to the Company in 2015. Additionally, the Company installed new loan input software and credit review software in late 2014, which increased software maintenance by $28 thousand annually in 2015. Equipment expense decreased $52 thousand in 2015, as compared to 2014, with a reduction of expense due to the purchase of copiers at the conclusion of a lease, a reduction in automobile expense with a decrease in mileage and gasoline costs, and a reduction in small equipment purchased in 2015, as compared to 2014. Professional and director fees increased $105 thousand, a result of the increase in outside service fees, with $110 thousand incurred during the first quarter to contract a professional firm to assist the Company with the assessment of market opportunities and long-term strategic goals.

| 2016 Report to Shareholders | CSB Bancorp, Inc. 13 |

2016 FINANCIAL REVIEW

Income Taxes

The provision for income taxes amounted to $3.0 million in 2016, $2.6 million in 2015, and $2.6 million in 2014, resulting in an effective rate of 30.6% in 2016, 30.5% in 2015, and 30.4% in 2014. The slight increase in the effective tax rate during 2016 as compared to 2015 was due primarily to increased income.

FINANCIAL CONDITION

Total assets of the Company were $670 million at December 31, 2016, compared to $650 million at December 31, 2015, representing an increase of $20 million, or 3%. Net loans increased $52 million, or 12%, while investment securities decreased $34 million, or 20%, and interest-earning deposits with other banks increased $2 million. Deposits and short-term borrowings increased $16 million and $144 thousand respectively, while other borrowings from the Federal Home Loan Bank (“FHLB”) decreased by $1 million, or 8%.

Securities

Total investment securities decreased $34 million, or 20%, to $132 million at year-end 2016. CSB’s portfolio is primarily comprised of agency mortgage-backed securities, obligations of state and political subdivisions, other government agencies’ debt, and corporate bonds. Restricted securities consist primarily of FHLB stock.

The Company has no exposure to government-sponsored enterprise preferred stocks, collateralized debt obligations, or trust preferred securities. The Company’s municipal bond portfolio consists of both taxable and tax-exempt general obligation and revenue bonds. As of December 31, 2016, $26 million, or 87%, held an S&P or Moody’s investment grade rating and $4 million, or 13%, were non-rated. The municipal portfolio includes a broad spectrum of counties, towns, universities, and school districts with 89% of the portfolio originating in Ohio, and 11% in Pennsylvania. Gross unrealized security losses within the portfolio were 1% of total securities at December 31, 2016, reflecting interest rate fluctuations, not credit downgrades.

One of the primary functions of the securities portfolio is to provide a source of liquidity and it is structured such that maturities and cash flows track the Company’s liquidity needs and asset/liability management requirements.

Loans

Total loans increased $53 million, or 12%, during 2016 with increases in all loan categories. Volume increases were recognized as follows: residential real estate loans increased $19 million, or 15%, commercial loans increased $11 million, or 9%, and commercial real estate loans increased $11 million, or 7%. Aided by low interest rates, business expansion and consumer borrowing continued to increase throughout 2016.

Attractive interest rates in the secondary market continued to drive consumer demand for longer-term 1-4 family fixed rate residential mortgages during 2016. The Company sold $11 million of originated mortgages into the secondary market, as compared to $12 million in 2015. With the expansion of the mortgage loan originator team, the Company originated $36 million of portfolio mortgage loans, which were predominately variable rate in 2016 as compared to 2015 origination of $22 million for the Company’s portfolio. Demand for home equity loans improved in 2016, with balances increasing $5 million. Installment lending continued to improve with consumer loans increasing 44% on a year-over-year basis to $13 million at December 31, 2016. This growth is primarily from RV finance loans originated in northeast Ohio.

Management anticipates the Company’s local service areas will continue to exhibit modest economic growth in line with the past three years. Commercial and commercial real estate loans comprise approximately 62% and 64% of the total loan portfolio at year-end 2016 and 2015, respectively. Residential real estate loans remained stable at approximately 30% of the total loan portfolio. Construction and land development loans rose to 5% of the total portfolio at December 31, 2016. The Company is well within the respective regulatory guidelines for investment in construction, development, and investment property loans that are not owner occupied.

Most of the Company’s lending activity is with customers primarily located within Holmes, Tuscarawas, Wayne, and Stark counties in Ohio. Credit concentrations, including commitments, as determined using North American Industry Classification Codes (NAICS), to the four largest industries compared to total loans at December 31, 2016, included $42 million, or 9%, of total loans to lessors of non-residential buildings or dwellings; $26 million, or 5%, of total loans to logging, sawmills, and timber tract operations; $20 million, or 4%, of total loans to lessors of residential real estate and $21 million, or 4%, of total loans to borrowers in the hotel, motel, and lodging business. These loans are generally secured by real property and equipment, with repayment expected from operational cash flow. Credit evaluation is based on a review of cash flow coverage of principal, interest payments, and the adequacy of the collateral received.

14 2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

Nonperforming Assets, Impaired Loans, and Loans Past Due 90 Days or More

Nonperforming assets consist of nonaccrual loans, loans past due 90 days and still accruing, and other real estate acquired through or in lieu of foreclosure. Other impaired loans include certain loans that are internally classified as substandard or doubtful. Loans are placed on nonaccrual status when they become past due 90 days or more, or when mortgage loans are past due as to principal and interest 120 days or more, unless they are both well secured and in the process of collection.

| NONPERFORMING ASSETS | DECEMBER 31 | |||||||

| (Dollars in thousands)

|

2016

|

2015

|

||||||

|

|

||||||||

| Nonaccrual loans

|

||||||||

| Commercial

|

$ | 425 | $ | 177 | ||||

| Commercial real estate

|

497 | 796 | ||||||

| Residential real estate

|

490 | 603 | ||||||

| Construction & land development

|

– | – | ||||||

| Consumer

|

37 | – | ||||||

| Loans past due 90 days or more and still accruing

|

||||||||

| Commercial

|

– | – | ||||||

| Commercial real estate

|

39 | – | ||||||

| Residential real estate

|

196 | 105 | ||||||

| Construction & land development |

– | – | ||||||

|

|

|

|

|

|||||

| Total nonperforming loans

|

1,684 | 1,681 | ||||||

| Other real estate owned |

– | – | ||||||

|

|

|

|

|

|||||

| Total nonperforming assets |

$ | 1,684 | $ | 1,681 | ||||

|

|

|

|

|

|||||

| Nonperforming assets as a percentage of loans plus other real estate |

0.35 | % | 0.40 | % | ||||

Allowance for Loan Losses

The allowance for loan losses is maintained at a level considered by management to be adequate to cover loan losses that are currently anticipated based on past loss experience, general economic conditions, changes in mix and size of the loan portfolio, information about specific borrower situations, and other factors and estimates which are subject to change over time. Management periodically reviews selected large loans, delinquent and other problem loans, and selected other loans. Collectability of these loans is evaluated by considering the current financial position and performance of the borrower, estimated market value of the collateral, the Company’s collateral position in relationship to other creditors, guarantees, and other potential sources of repayment. Management forms judgments, which are in part subjective, as to the probability of loss and the amount of loss on these loans as well as other loans taken together. The Company’s Allowance for Loan Losses Policy includes, among other items, provisions for classified loans, and a provision for the remainder of the portfolio based on historical data, including past charge-offs.

2016 Report to Shareholders | CSB Bancorp, Inc.

15

2016 FINANCIAL REVIEW

| ALLOWANCE FOR LOAN LOSSES | FOR THE YEAR ENDED | |||||||

| (Dollars in thousands)

|

2016

|

2015

|

||||||

|

|

||||||||

| Beginning balance of allowance for loan losses

|

$ | 4,662 | $ | 4,381 | ||||

| Provision for loan losses

|

493 | 389 | ||||||

| Charge-offs:

|

||||||||

| Commercial

|

260 | 94 | ||||||

| Commercial real estate

|

50 | 61 | ||||||

| Residential real estate & home equity

|

12 | 132 | ||||||

| Construction & land development

|

– | – | ||||||

| Consumer

|

59 | 46 | ||||||

| Deposit accounts

|

37 | 15 | ||||||

| Credit cards |

– | – | ||||||

|

|

|

|

|

|||||

| Total charge-offs

|

418 | 348 | ||||||

| Recoveries:

|

||||||||

| Commercial

|

202 | 193 | ||||||

| Commercial real estate

|

334 | 13 | ||||||

| Residential real estate & home equity

|

5 | 18 | ||||||

| Construction & land development

|

– | – | ||||||

| Consumer

|

1 | 10 | ||||||

| Deposit accounts

|

12 | 6 | ||||||

| Credit cards |

– | – | ||||||

|

|

|

|

|

|||||

| Total recoveries |

554 | 240 | ||||||

|

|

|

|

|

|||||

| Net (recoveries) charge-offs |

(136 | ) | 108 | |||||

|

|

|

|

|

|||||

| Ending balance of allowance for loan losses |

$ | 5,291 | $ | 4,662 | ||||

|

|

|

|

|

|||||

| Net charge-offs as a percentage of average total loans

|

(0.03 | )% | 0.03 | % | ||||

| Allowance for loan losses as a percentage of total loans

|

1.11 | 1.10 | ||||||

| Allowance for loan losses to total nonperforming loans |

3.18 | x | 2.77 | x | ||||

| Components of the allowance for loan losses:

|

||||||||

| General reserves

|

$ | 4,562 | $ | 4,273 | ||||

| Specific reserve allocations |

729 | 389 | ||||||

|

|

|

|

|

|||||

| Total allowance for loan losses |

$ | 5,291 | $ | 4,662 | ||||

|

|

|

|

|

|||||

The allowance for loan losses totaled $5.3 million, or 1.11%, of total loans at year-end 2016 as compared to $4.7 million, or 1.10%, of total loans at year-end 2015. The Bank had net recoveries of $136 thousand for 2016 as compared to net charge-offs of $108 thousand in 2015.

The Company maintains an internal watch list on which it places loans where management’s analysis of the borrower’s operating results and financial condition indicates the borrower’s cash flows are inadequate to meet its debt service requirements and loans where there exists an increased risk that such a shortfall may occur. Nonperforming loans, which consist of loans past due 90 days or more and nonaccrual loans, aggregated $1.7 million, or 0.35% of loans at year-end 2016 as compared to $1.7 million, or 0.4% of loans at year-end 2015. Impaired loans were $7.2 million at year-end 2016 as compared to $8.7 million at year-end 2015. Impaired loans as a percentage of total loans declined from 2015 to 2016 and reflect economic stabilization in the Company’s market area. Management has assigned loss allocations to absorb the estimated losses on these impaired loans. These allocations are included in the total allowance for loan losses balance.

Other Assets

Net premises and equipment increased $540 thousand to $9 million at year-end 2016 primarily because of the purchase of a branch facility that was previously leased in 2016. There was no other real estate owned at December 31, 2016 or 2015. At December 31, 2016, the Company recognized a net deferred tax asset of $603 thousand, as compared to a net deferred tax asset of $364 thousand at December 31, 2015.

16 2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

Deposits

The Company’s deposits are obtained primarily from individuals and businesses located in its market area. For deposits, the Company must compete with products offered by other financial institutions, as well as alternative investment options. Demand and savings deposits increased for the year ended 2016, due to focused retail and business banking strategies to obtain more account relationships as well as customers reflecting their preference for shorter maturities.

| December 31 | Change from 2015 | |||||||||||||||

| (Dollars in thousands)

|

2016

|

2015

|

Amount

|

%

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest-bearing demand

|

$ | 167,824 | $ | 151,549 | $ | 16,275 | 10.7 | % | ||||||||

| Interest-bearing demand

|

97,683 | 86,472 | 11,211 | 13.0 | ||||||||||||

| Traditional savings

|

95,275 | 93,523 | 1,752 | 1.9 | ||||||||||||

| Money market savings

|

67,894 | 74,232 | (6,338 | ) | (8.5 | ) | ||||||||||

| Time deposits in excess of $250,000

|

13,102 | 13,834 | (732 | ) | (5.3 | ) | ||||||||||

| Other time deposits |

99,007 | 105,432 | (6,425 | ) | (6.1 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

$ | 540,785 | $ | 525,042 | $ | 15,743 | 3.0 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

Other Funding Sources

The Company obtains additional funds through securities sold under repurchase agreements, overnight borrowings from the FHLB or other financial institutions, and advances from the FHLB. Short-term borrowings, consisting of securities sold under repurchase agreements, increased $144 thousand. Other borrowings, consisting of FHLB advances, decreased $1 million as the result of maturities and principal repayments.

CAPITAL RESOURCES

Total shareholders’ equity increased to $65.4 million at December 31, 2016, as compared to $61.3 million at December 31, 2015. This increase was primarily due to $6.7 million of net income which was partially offset by the payment of $2.1 million of cash dividends in 2016 and an increase in accumulated other comprehensive loss of $457 thousand. The Board of Directors approved a Stock Repurchase Program on July 7, 2005 that allowed the repurchase of up to 10% of the Company’s then-outstanding common shares. Repurchased shares are to be held as treasury stock and are available for general corporate purposes. At December 31, 2016, approximately 41 thousand shares could still be repurchased under the current authorized program. No shares were repurchased in 2016 or 2015.

Effective January 1, 2015, the Federal Reserve adopted final rules implementing Basel III and regulatory capital changes required by the Dodd-Frank Act. The rules apply to both the Company and the Bank. The rules established minimum risk-based and leverage capital requirements for all banking organizations.

The new rules include (a) a new common equity Tier 1 capital ratio of at least 4.5%, (b) a Tier 1 capital ratio of at least 6.0%, rather than the former 4.0%, (c) a minimum total capital ratio that remains at 8.0%, and (d) a minimum leverage ratio of 4%.

Under the guidelines, capital is compared to the relative risk related to the balance sheet. To derive the risk included in the balance sheet, one of several risk weights is applied to different balance sheet and off-balance sheet assets primarily based on the relative credit risk of the counterparty. The capital amounts and classifications are also subject to qualitative judgments by the regulators about components, risk weightings, and other factors.

The new rules also place restrictions on the payment of capital distributions, including dividends, and certain discretionary bonus payments to executive officers if the company does not hold a capital conservation buffer of greater than 2.5% composed of common equity Tier 1 capital above its minimum risk-based capital requirements, or if its eligible retained income is negative in that quarter and its capital conservation buffer ratio was less than 2.5% at the beginning of the quarter. The capital conservation buffer phases in starting on January 1, 2016, at .625%. The Company and Bank’s actual and required capital amounts are disclosed in Note 12 to the consolidated financial statements.

Dividends paid by the Bank to CSB are the primary source of funds available to the Company for payment of dividends to shareholders and for other working capital needs. The payment of dividends by the Bank to the Company is subject to restrictions by regulatory authorities, which generally limit dividends to current year net income and the prior two years net retained earnings, as defined by regulation. In addition, dividend payments generally cannot reduce regulatory capital levels below the minimum regulatory guidelines discussed above.

2016 Report to Shareholders | CSB Bancorp, Inc.

17

2016 FINANCIAL REVIEW

LIQUIDITY

|

December 31

|

Change | |||||||||||||||||

| (Dollars in millions)

|

2016

|

2015

|

from 2015 | |||||||||||||||

|

|

||||||||||||||||||

| Cash and cash equivalents

|

$ | 37 | $ | 38 | $ | (1 | ) | |||||||||||

| Unused lines of credit

|

66 | 52 | 14 | |||||||||||||||

| Unpledged securities at fair market value |

37 | 70 | (33 | ) | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| $ | 140 | $ | 160 | $ | (20 | ) | ||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Net deposits and short-term liabilities |

$ | 533 | $ | 516 | $ | 17 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Liquidity ratio

|

26.1 | % | 31.1 | % | ||||||||||||||

| Minimum board approved liquidity ratio |

20.0 | % | 20.0 | % | ||||||||||||||

Liquidity refers to the Company’s ability to generate sufficient cash to fund current loan demand, meet deposit withdrawals, pay operating expenses, and meet other obligations. Liquidity is monitored by CSB’s Asset Liability Committee. The Company was within all Board-approved limits at December 31, 2016 and 2015. Additional sources of liquidity include net income, loan repayments, the availability of borrowings, and adjustments of interest rates to attract deposit accounts.

As summarized in the Consolidated Statements of Cash Flows, the most significant investing activities for the Company in 2016 included net loan originations of $52 million, securities purchases of $37 million, offset by maturities and repayment of securities totaling $69 million. The Company’s financing activities included a $16 million increase in deposits, $2 million in cash dividends paid, and a $1 million net decrease in FHLB advances.

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The most significant market risk the Company is exposed to is interest rate risk. The business of the Company and the composition of its balance sheet consist of investments in interest-earning assets (primarily loans and securities), which are funded by interest-bearing liabilities (deposits and borrowings). These financial instruments have varying levels of sensitivity to changes in the market rates of interest, resulting in market risk. None of the Company’s financial instruments are held for trading purposes.

The Board of Directors establishes policies and operating limits with respect to interest rate risk. The Company manages interest rate risk regularly through its Asset Liability Committee. The Committee meets periodically to review various asset and liability management information including, but not limited to, the Company’s liquidity position, projected sources and uses of funds, interest rate risk position, and economic conditions.

Interest rate risk is monitored primarily through the use of an earnings simulation model. The model is highly dependent on various assumptions, which change regularly as the balance sheet and market interest rates change. The earnings simulation model projects changes in net interest income resulting from the effect of changes in interest rates. The analysis is performed quarterly over a twenty-four month horizon. The analysis includes two balance sheet models, one based on a static balance sheet and one on a dynamic balance sheet with projected growth in assets and liabilities. This analysis is performed by estimating the expected cash flows of the Company’s financial instruments using interest rates in effect at year-end 2016 and 2015. Interest rate risk policy limits are tested by measuring the anticipated change in net interest income over a two-year period. The tests assume a quarterly ramped 100, 200, 300, and 400 basis point increase and a 100 basis point decrease in 2016 in market interest rates as compared to a stable rate environment or base model. The following table reflects the change to interest income for the first twelve-month period of the twenty-four month horizon.

18

2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

Net Interest Income at Risk

| December 31, 2016 | ||||||||||||||||||||

| Change In

|

Net Interest Income

|

Dollar Change

|

Percentage

|

Board Policy Limits

|

||||||||||||||||

|

|

||||||||||||||||||||

| (Dollars in thousands) | + 400 | $ | 25,519 | $ | 1,889 | 8.0% | ± 25% | |||||||||||||

| + 300 | 25,063 | 1,433 | 6.1 | ± 15 | ||||||||||||||||

| + 200 | 24,577 | 947 | 4.0 | ± 10 | ||||||||||||||||

| + 100 | 24,092 | 462 | 2.0 | ± 5 | ||||||||||||||||

| 0 | 23,630 | – | – | |||||||||||||||||

| – 100 | 22,841 | (789 | ) | (3.3) | ± 5 | |||||||||||||||

| December 31, 2015

|

||||||||||||||||||||

|

|

||||||||||||||||||||

| + 400 | $ | 23,360 | $ | 1,624 | 7.5% | ± 25% | ||||||||||||||

| + 300 | 22,957 | 1,221 | 5.6 | ± 15 | ||||||||||||||||

| + 200 | 22,500 | 764 | 3.5 | ± 10 | ||||||||||||||||

| + 100 | 22,071 | 335 | 1.5 | ± 5 | ||||||||||||||||

| 0 | 21,736 | – | – | |||||||||||||||||

| – 100 | 21,172 | (564 | ) | (2.6) | ± 5 | |||||||||||||||

|

Management reviews Net Interest Income at Risk with the Board on a periodic basis. The Company was within all Board-approved limits at December 31, 2016 and 2015.

Economic Value of Equity at Risk

|

| |||||||||||||||||||

| December 31, 2016 | ||||||||||||||||||||

| Change In Interest Rates

|

Percentage Change

|

Board Policy Limits

|

||||||||||||||||||

|

|

||||||||||||||||||||

| + 400 | 18.1 | % | ± 35% | |||||||||||||||||

| + 300 | 14.9 | ± 30 | ||||||||||||||||||

| + 200 | 11.0 | ± 20 | ||||||||||||||||||

| + 100 | 6.1 | ± 15 | ||||||||||||||||||

| – 100 | (7.6 | ) | ± 15 | |||||||||||||||||

| December 31, 2015

|

||||||||||||||||||||

|

|

||||||||||||||||||||

| + 400 | 18.6 | % | ± 35% | |||||||||||||||||

| + 300 | 15.6 | ± 30 | ||||||||||||||||||

| + 200 | 11.8 | ± 20 | ||||||||||||||||||

| + 100 | 6.9 | ± 15 | ||||||||||||||||||

| – 100 | (9.8 | ) | ± 15 | |||||||||||||||||

2016 Report to Shareholders | CSB Bancorp, Inc.

19

2016 FINANCIAL REVIEW

The economic value of equity is calculated by subjecting the period-end balance sheet to changes in interest rates and measuring the impact of the changes on the values of the assets and liabilities. Hypothetical changes in interest rates are then applied to the financial instruments. Then the cash flows and fair values are again estimated using these hypothetical rates. For the net interest income estimates, the hypothetical rates are applied to the financial instruments based on the assumed cash flows.

Management periodically measures and reviews the Economic Value of Equity at Risk with the Board. At December 31, 2016, the market value of equity as a percent of base in a 400 basis point rising rate environment indicates an increase of 18.1% as compared to an increase of 18.6% as of December 31, 2015. The Company was within all Board-approved limits at December 31, 2016 and 2015.

SIGNIFICANT ASSUMPTIONS AND OTHER CONSIDERATIONS

The foregoing market risk analysis is based on numerous assumptions, including relative levels of market interest rates, loan prepayments, and reactions of depositors to changes in interest rates and this should not be relied upon as being indicative of actual results. Further, the analysis does not contemplate all actions the Company may undertake in response to changes in interest rates.

U.S. Treasury securities, obligations of U.S. Government corporations and agencies, obligations of states and political subdivisions will generally repay at their stated maturity or if callable prior to their final maturity date. Mortgage-backed security payments increase when interest rates are low and decrease when interest rates rise. Most of the Company’s loans permit the borrower to prepay the principal balance prior to maturity without penalty. The likelihood of prepayment depends on a number of factors: current interest rate and interest rate index (if any) on the loan, the financial ability of the borrower to refinance, the economic benefit to be obtained from refinancing, availability of refinancing at attractive terms, as well as economic, other factors in specific geographic areas which affect the sales and price levels of residential, and commercial property. In a changing interest rate environment, prepayments may increase or decrease on fixed and adjustable rate loans depending on the current relative levels and expectations of future short-term and long-term interest rates. Prepayments on adjustable rate loans generally increase when long-term interest rates fall or are at historically low levels relative to short-term interest rates, thus making fixed rate loans more desirable. While savings and checking deposits generally may be withdrawn upon the customer’s request without prior notice, a continuing relationship with customers resulting in future deposits and withdrawals is generally predictable, leading to a dependable and uninterrupted source of funds. Time deposits generally have early withdrawal penalties, which discourage customer withdrawal prior to maturity. Short-term borrowings have fixed maturities. Certain advances from the FHLB carry prepayment penalties and are expected to be repaid in accordance with their contractual terms.

FAIR VALUE MEASUREMENTS

The Company discloses the estimated fair value of its financial instruments at December 31, 2016 and 2015 in Note 15 to the consolidated financial statements.

OFF-BALANCE SHEET ARRANGEMENTS, CONTRACTUAL OBLIGATIONS, AND CONTINGENT LIABILITIES AND COMMITMENTS

The following table summarizes the Company’s loan commitments, including letters of credit, as of December 31, 2016:

| Amount of Commitment to Expire Per Period

|

||||||||||||||||||||

|

|

|

|||||||||||||||||||

| (Dollars in thousands)

Type of Commitment

|

Total

|

Less than 1 year

|

1 to 3 Years

|

3 to 5 Years

|

Over 5

|

|||||||||||||||

|

|

||||||||||||||||||||

|

Commercial lines of credit

|

$ | 105,215 | $ 90,474 | $ | – | $ | 1,107 | $ | 13,634 | |||||||||||

| Real estate lines of credit

|

45,787 | 1,814 | 4,017 | 6,524 | 33,432 | |||||||||||||||

| Consumer lines of credit

|

611 | 611 | – | – | – | |||||||||||||||

| Credit cards lines of credit

|

4,240 | 4,240 | – | – | – | |||||||||||||||

| Overdraft privilege

|

6,910 | 6,910 | – | – | – | |||||||||||||||

| Commercial real estate loan commitments

|

– | – | – | – | – | |||||||||||||||

| Letters of credit |

972 | 945 | – | 27 | – | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total commitments |

$ | 163,735 | $104,994 | $ | 4,017 | $ | 7,658 | $ | 47,066 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

All lines of credit represent either fee-paid or legally binding loan commitments for the loan categories noted. Letters of credit are also included in the amounts noted in the table since the Company requires that each letter of credit be supported by a loan agreement. The commercial and consumer lines represent both unsecured and secured obligations. The real estate lines are secured by mortgages on residential property. It is anticipated that a significant portion of these lines will expire without being drawn upon.

20

2016 Report to Shareholders | CSB Bancorp, Inc.

2016 FINANCIAL REVIEW

The following table summarizes the Company’s other contractual obligations, exclusive of interest, as of December 31, 2016:

| Payment Due by Period

|

||||||||||||||||||||

|

|

|

|||||||||||||||||||

| (Dollars in thousands)

Contractual Obligations

|

Total

|

Less than

|

1 to 3

|

3 to 5

|

Over 5

|

|||||||||||||||

|

|

||||||||||||||||||||

|

Total time deposits

|

$ | 112,109 | $ | 57,670 | $ | 42,839 | $ | 11,600 | $ | – | ||||||||||

| Short-term borrowings

|

48,742 | 48,742 | – | – | – | |||||||||||||||

| Other borrowings

|

12,385 | 10,730 | 923 | 477 | 255 | |||||||||||||||

| Operating leases |

305 | 152 | 153 | – | – | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total obligations |

$ | 173,541 | $ | 117,294 | $ | 43,915 | $ | 12,077 | $ | 255 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

The other borrowings noted in the preceding table represent borrowings from the FHLB. The notes require payment of interest on a monthly basis with principal due in monthly installments or at maturity, depending upon the issue. The obligations bear stated fixed interest rates and stipulate a prepayment penalty if the note’s interest rate exceeds the current market rate for similar borrowings at the time of repayment. As the notes mature, the Company evaluates the liquidity and interest rate circumstances, at that time, to determine whether to pay off or renew the note. The evaluation process typically includes: the strength of current and projected customer loan demand, the Company’s federal funds sold or purchased position, projected cash flows from maturing investment securities, the current and projected market interest rate environment, local and national economic conditions, and customer demand for the Company’s deposit product offerings.

CRITICAL ACCOUNTING POLICIES

The Company’s consolidated financial statements are prepared in accordance with U.S. generally accepted accounting principles and follow general practices within the commercial banking industry. Application of these principles requires management to make estimates, assumptions, and judgments that affect the amounts reported in the financial statements. These estimates, assumptions, and judgments are based upon the information available as of the date of the financial statements.

The most significant accounting policies followed by the Company are presented in the Summary of Significant Accounting Policies. These policies, along with the other disclosures presented in the Notes to Consolidated Financial Statements and the 2016 Financial Review, provide information about how significant assets and liabilities are valued in the financial statements and how those values are determined. Management has identified the other-than-temporary impairment of securities, allowance for loan losses, goodwill, and the fair value of financial instruments as the accounting areas that require the most subjective and complex estimates, assumptions and judgments and, as such, could be the most subject to revision as new information becomes available.

Securities are evaluated periodically to determine whether a decline in their value is other-than-temporary. Management utilizes criteria such as the magnitude and duration of the decline, in addition to the reasons underlying the decline, to determine whether the loss in value is other-than-temporary. The term “other-than-temporary” is not intended to indicate that the decline is permanent, but indicates that the prospect for a near-term recovery of value is not necessarily favorable, or that there is a lack of evidence to support a realizable value equal to or greater than the carrying value of the investment. Once a decline in value is determined to be other-than-temporary, the value of the security is reduced and a corresponding charge to earnings is recognized.

As previously noted in the section entitled Allowance for Loan Losses, management performs an analysis to assess the adequacy of its allowance for loan losses. This analysis encompasses a variety of factors including: the potential loss exposure for individually reviewed loans, the historical loss experience, the volume of nonperforming loans (i.e., loans in nonaccrual status or past due 90 days or more), the volume of loans past due, any significant changes in lending or loan review staff, an evaluation of current and future local and national economic conditions, any significant changes in the volume or mix of loans within each category, a review of the significant concentrations of credit, and any legal, competitive, or regulatory concerns.

The Company accounts for business combinations using the acquisition method of accounting. Goodwill and intangible assets with indefinite useful lives are not amortized. Intangible assets with finite useful lives, consisting of core deposit intangibles, are amortized using accelerated methods over their estimated weighted-average useful lives, approximating ten years. Additional information is presented in Note 5, Core Deposit Intangible Assets.