Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - ERHC Energy Inc | ex32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - ERHC Energy Inc | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - ERHC Energy Inc | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - ERHC Energy Inc | ex31_1.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| ☒ |

Annual Report under Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the fiscal year ended September 30, 2016

OR

| ☐ |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the transition period ended: __________________

Commission file number: 000-17325

(Exact name of registrant as specified in its charter)

|

Colorado

|

88-0218499

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification No.)

|

|

5444 Westheimer Road, Suite 1440, Houston, Texas

|

77056

|

|

|

(Address of Principal Executive Office)

|

(Zip Code)

|

713-626-4700

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: common stock

Check if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Check if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Check if the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Check if there is no disclosure of delinquent filers in response to Item 405 of Regulation S-K contained in this form, and no disclosure will be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Check if the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer.

|

Large Accelerated Filer ☐

|

Accelerated Filer ☐

|

Non-Accelerated Filer ☒

|

Check if the registrant is a shell company. Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant on March 31, 2016 was $2,108,791.

On December 31, 2016, the registrant had shares of common stock issued and outstanding 952,399,512.

|

PART I

|

PAGE

|

|

|

Item 1.

|

4

|

|

|

Item 1A.

|

15

|

|

|

Item 1B.

|

19

|

|

|

Item 2.

|

19

|

|

|

Item 3.

|

20

|

|

|

Item 4.

|

21

|

|

|

PART II

|

||

|

Item 5.

|

21

|

|

|

Item 6.

|

22

|

|

|

Item 7.

|

23

|

|

|

Item 7A.

|

28

|

|

|

Item 8.

|

29

|

|

|

Item 9.

|

53

|

|

|

Item 9A.

|

53

|

|

|

Item 9B.

|

53

|

|

|

PART III

|

||

|

Item 10.

|

54

|

|

|

Item 11.

|

58

|

|

|

Item 12.

|

65

|

|

|

Item 13.

|

66

|

|

|

Item 14.

|

66

|

|

|

PART IV

|

||

|

Item 15.

|

67

|

|

|

68

|

Forward-Looking Statements

ERHC Energy Inc. (the “Company”) or its representatives may, from time to time, make or incorporate by reference certain written or oral statements which include, but are not limited to, information concerning the Company’s possible or assumed future business activities and results of operations and statements about the following subjects:

| · |

business strategy;

|

| · |

growth opportunities;

|

| · |

future development of concessions, exploitation of assets and other business operations;

|

| · |

future market conditions and the effect of such conditions on the Company’s future activities or results of operations;

|

| · |

future uses of and requirements for financial resources;

|

| · |

interest rate and foreign exchange risk;

|

| · |

future contractual obligations;

|

| · |

outcomes of legal proceedings;

|

| · |

future operations outside the United States;

|

| · |

competitive position;

|

| · |

expected financial position;

|

| · |

future cash flows;

|

| · |

future liquidity and sufficiency of capital resources;

|

| · |

future dividends;

|

| · |

financing plans;

|

| · |

tax planning;

|

| · |

budgets for capital and other expenditures;

|

| · |

plans and objectives of management;

|

| · |

compliance with applicable laws; and

|

| · |

adequacy of insurance or indemnification.

|

These types of statements constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and inherently are subject to a variety of assumptions, risks and uncertainties that could cause actual results, levels of activity, performance or achievements to differ materially from those expected, projected or expressed in forward-looking statements. These risks and uncertainties include, among others, the following:

| · |

general economic and business conditions;

|

| · |

worldwide demand for oil and natural gas;

|

| · |

changes in foreign and domestic oil and gas exploration, development and production activity;

|

| · |

oil and natural gas price fluctuations and related market expectations;

|

| · |

termination, renegotiation or modification of existing contracts;

|

| · |

the ability of the Organization of Petroleum Exporting Countries, commonly called OPEC, to set and maintain production levels and pricing, and the level of production in non-OPEC countries;

|

| · |

advances in exploration and development technology;

|

| · |

the political environment of oil-producing regions;

|

| · |

political instability in the Republic of Kenya, Republic of Chad, the Democratic Republic of Sao Tome and Principe and the Federal Republic of Nigeria;

|

| · |

casualty losses;

|

| · |

competition;

|

| · |

changes in foreign, political, social and economic conditions;

|

| · |

risks of international operations, compliance with foreign laws and taxation policies and expropriation or nationalization of equipment and assets;

|

| · |

risks of potential contractual liabilities;

|

| · |

foreign exchange and currency fluctuations and regulations, and the inability to repatriate income or capital;

|

| · |

risks of war, military operations, other armed hostilities, terrorist acts and embargoes;

|

| · |

regulatory initiatives and compliance with governmental regulations;

|

| · |

compliance with environmental laws and regulations;

|

| · |

compliance with tax laws and regulations;

|

| · |

customer preferences;

|

| · |

effects of litigation and governmental proceedings;

|

| · |

cost, availability and adequacy of insurance;

|

| · |

adequacy of the Company’s sources of liquidity;

|

| · |

labor conditions and the availability of qualified personnel; and

|

| · |

various other matters, many of which are beyond the Company’s control.

|

The risks and uncertainties included here are not exhaustive. Other sections of this report and the Company’s other filings with the U.S. Securities and Exchange Commission (“SEC”) include additional factors that could adversely affect the Company’s business, results of operations and financial performance. Given these risks and uncertainties, investors should not place undue reliance on our statements concerning future intent. Company’s statements included in this report speak only as of the date of this report. The Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any of our statements to reflect any change in its expectations with regard to the statement or any change in events, conditions or circumstances on which any forward-looking statement is based.

PART I

Overview

ERHC Energy Inc., a Colorado corporation, (“ERHC” or the “Company”) was incorporated in 1986. The Company is in the business of exploration for oil and gas in Africa. The Company’s business includes working interests in exploration acreage in the Republic of Kenya (“Kenya”), the Republic of Chad (“Chad”), the Joint Development Zone (“JDZ”) between the Democratic Republic of Săo Tomé and Príncipe (“STP”), the Federal Republic of Nigeria (“FRN” or “Nigeria”), and the exclusive economic zone of Săo Tomé and Príncipe (the “Exclusive Economic Zone” or “EEZ”).

ERHC’s strategy in Kenya and Chad is to partner with other oil and gas operators to perform exploration work and further develop assets held through Production Sharing Contracts (PSCs) with the governments of both countries. ERHC plans to raise funds by farming out some working interest in these blocks in exchange for cash payments or other valuable consideration.

The Company’s strategy in the JDZ and EEZ is to farm out its working interests to well established oil and gas operators for valuable consideration including upfront cash payments and being carried for ERHC’s share of the exploration costs. This has already been done successfully on Blocks 2, 3 and 4 of the JDZ where ERHC has benefited from partnerships with Addax Petroleum and Sinopec Corporation, which have operated some of the license areas on behalf of ERHC.

ERHC is now pursuing a similar approach for JDZ Blocks 5, 6 and 9 as well as for blocks in the EEZ.

Apart from its oil and gas exploration activities in Kenya, Chad, the JDZ and the EEZ, ERHC continues to pursue other oil and gas opportunities in Africa. These opportunities also include the possible acquisition of significant equity stakes in other oil and gas exploration and production companies and the resulting indirect interest in the underlying exploration and production assets of such other companies.

ERHC is currently acquiring oil and gas properties in Texas. These US acquisitions are being carried on by and in the name of NewStar Oil& Gas Company, Inc., a wholly owned subsidiary of ERHC (“NewStar”). NewStar is incorporated under the laws of the State of Texas. The focus of all acquisitions by Newstar will be producing or near-producing properties with significant upside potential.

CURRENT BUSINESS OPERATIONS

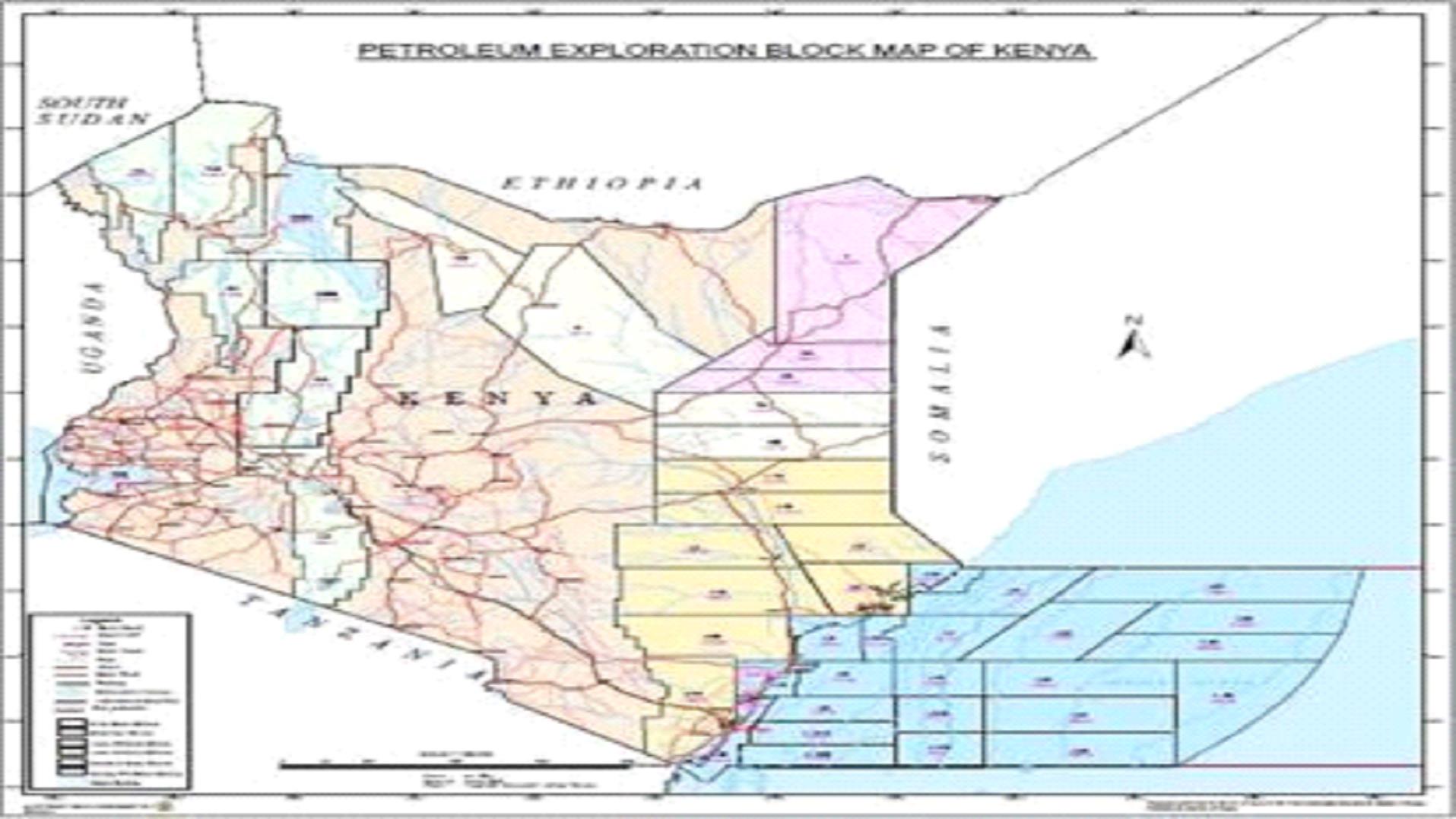

REPUBLIC OF KENYA

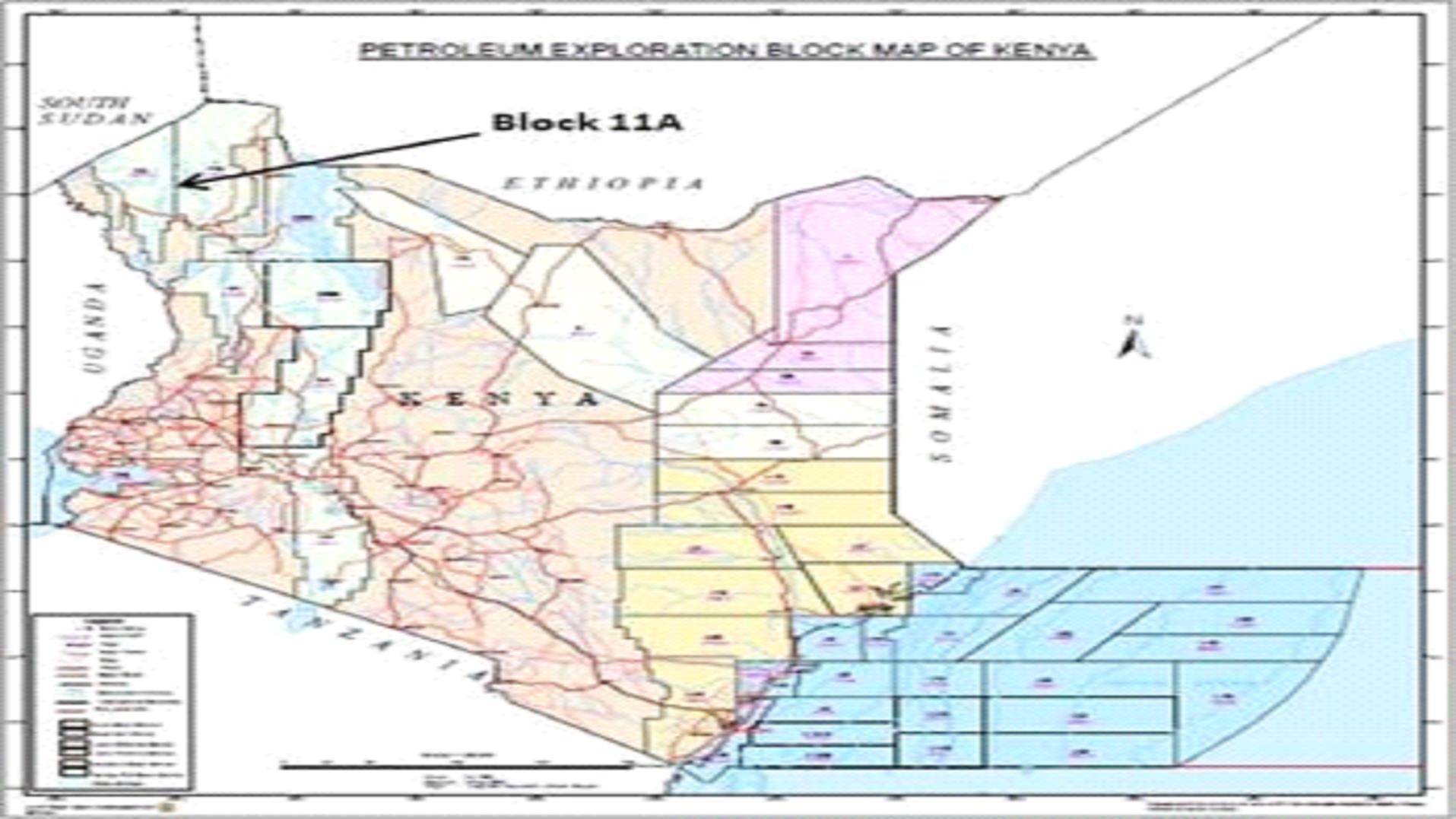

ERHC Kenya Acreage

In June 2012, after months of negotiations between ERHC and the Government of Kenya, the Government awarded Block 11A for oil and gas exploration and development in Kenya to the Company. On June 28, 2012, the Company announced that it had signed a Production Sharing Contract (PSC) on Block 11A with the Government of Kenya. A PSC is an agreement that governs the relationship between ERHC (and any future joint-venture partners) and the Government of Kenya in respect of exploration and production in the Block awarded to the Company. The PSC details, among other things, the work commitments (including acquisition of data, drilling of wells, social projects, etc.), the time frame for completion of the work commitments, production sharing between the parties and the Government, and how the costs of exploration, development and production will be recovered.

By virtue of the PSC, the Company initially acquired a 90% interest in Block 11A, which encompasses 11,950.06 square kilometers or 2.95 million square acres. The Government of Kenya has a 10% carried participating interest up to the declaration of commerciality and may thereafter acquire an additional 10% interest in the PSC in which case the total Government participation would rise to 20%.

Circle Oil Limited (www.circleoilandgas.com) (“Circle”) acted as finder in ERHC’s acquisition of the Block by facilitating ERHC’s entry into Kenya, including the introduction of Dr. Peter Thuo, ERHC’s Kenya-based geoscientist and technical adviser who provided liaison services in the pursuit of ERHC’s application. Circle’s involvement provided significant efficiencies, including substantial cost savings, in ERHC’s application process. By virtue of the terms of the business finder’s agreement reached between Circle and ERHC, Circle is entitled to receive a 5% payment on the value of the acquisition accruing to ERHC from the application. Circle has opted to receive this fee in the form of a carried 5% of ERHC’s total interest in Block 11A.

In October, 2013, ERHC entered into a farm-out agreement with CEPSA Kenya Limited, an affiliate of Compañía Española de Petróleos, S.A.U., an international oil and gas company ("CEPSA"). The farm-out agreement was approved by the Government of the Republic of Kenya during the quarter ended June 30, 2014. Under terms of the agreement, ERHC transferred majority of its interest in Kenya Block 11A as well as operatorship to CEPSA. The farm-out agreement includes a carry and other considerations.

Kenya Operations Update

| · |

As previously advised, the Tarach-1 well was always designed as an exploratory well. An exploratory well is drilled purely for information gathering (“exploration”) purposes in an area that is yet unproven with regard to petroleum resources. The site selection for an exploratory well is based on seismic data and other pre-drill geoscientific surveys.

|

| · |

Operator analysis of the results if the Tarach-1 well shows that it did not encounter any reservoirs. The operator has therefore classified Tarach-1 a dry well. The well has accordingly been plugged and abandoned

|

It is important to remind investors and other stakeholders, while the pre-drill geological and geophysical work might indicate prospectively and reasonable chances of success, there are no guarantees before drilling that there will be a discovery of hydrocarbons. If there is a discovery, there is no guarantee that it will be commercial or in such quantities as to justify a development project.

The Company continues to work with Deloitte Corporate Finance LLC (DCF) on a further farm-down of our interest in the Block to help raise funds for the company.

Key Provisions of the ERHC’s PSC on Block 11A

KENYA BLOCK 11A

|

LICENSE:

|

PSC with the Government of Kenya (effective September 2012)

|

|

PARTIES:

|

ERHC (35%); CEPSA (55%); Government of Kenya (10%)1

|

WORK PROGRAM:

Phase 1 (2 years – September 2012 to September 2014)

|

Minimum Work

|

Minimum Expenditure

|

Status

|

|

Acquire and interpret 1,000 square kilometers of gravity and magnetic data

|

$250,000

|

Completed: 14,943.8 line kilometers of FTG data acquired by January 2014 at an estimated total cost of $2,700,000.

|

|

Acquire and interpret 1,000 kilometers of 2D seismic data

|

$10,000,000

|

Completed: 1,086.6 line kilometers of 2D seismic data acquired by August 2014 at an estimated total cost of $28,300,000

|

Phase 2 (2 years – September 2014 to September 2016)

|

Minimum Work

|

Minimum Expenditure

|

Status

|

|

Acquire 750 square kilometers of 3D seismic data

|

$30,000,000

|

Decision taken not to acquire 3D seismic but to proceed to drilling based on FTG and 2D seismic

|

|

OR

|

OR

|

|

|

Drill one (1) well to a minimum depth of 3,000m

|

$30,000,000

|

Completed.

|

Phase 3 (2 years – September 2016 to September 2018)

|

Minimum Work

|

Minimum Expenditure

|

Status

|

|

Drill one (1) well to a minimum depth of 3,000m

|

$30,000,000

|

Not yet arisen

|

1 CEPSA is carrying ERHC’s proportionate share of exploration costs except for the first exploration well where ERHC is expected to contribute 25% of its proportionate (35%) share of costs of the well.

OTHER FINANCIAL OBLIGATIONS:

|

Ministry Training Fund

|

$175,000 per annum during the exploration period

|

|

$200,000 per annum (minimum) from adoption of first development plan

|

|

|

Social Projects:

|

$50,000 per annum (minimum)

|

|

Surface Rentals:

|

$5/km2 per annum (exploration phase 1); $10/km2 per annum (exploration phase 2); $15/km2 per annum (exploration phase 3)

|

|

$100/km2 per annum (development and production period)

|

|

Cost Recovery:

|

|

|

Cost Oil

|

Up to 60% of Cost Oil each fiscal year

|

Profit Oil

|

Incremental Production Tranches

|

Government Share

|

Contractor Share

|

|

0-30,000 barrels per day

|

50%

|

50%

|

|

Next 25,000 barrels per day

|

60%

|

40%

|

|

Next 25,000 barrels per day

|

65%

|

35%

|

|

Next 20,000 barrels per day

|

70%

|

30%

|

|

Above 100,000 barrels per day

|

78%

|

22%

|

REPUBLIC OF CHAD

ERHC’s Chad Acreage

On July 6, 2011, the Company announced that it had signed a Production Sharing Contract (PSC) on the three oil blocks with the Government of Chad. A PSC is an agreement that governs the relationship between ERHC (and any future joint-venture partners) and the Government of Chad in respect of exploration and production in the Blocks awarded to the Company. The initial period of exploration commenced on July 12, 2012 with the publication, in Chadian Government’s Gazette Principal, of the Exclusive Exploration Authorization, granted to ERHC by the Government of Chad.

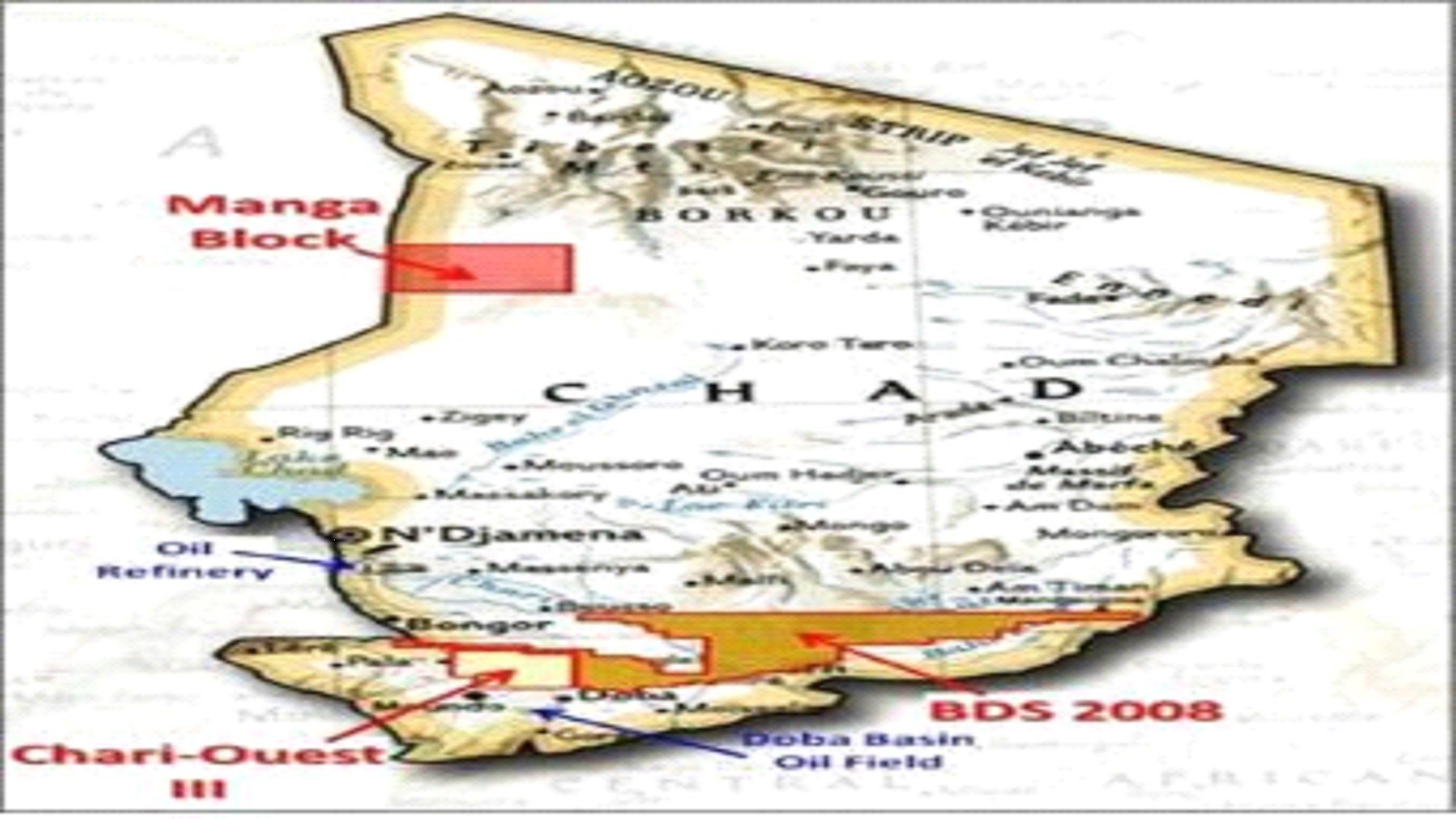

During the quarter ended June 30, 2014, the Company received the arrêté (decree) of the President of Chad giving presidential seal of approval to the Company’s request to obtain oil exploration Block BDS 2008 and its voluntary relinquishment of the Manga and Chari-Ouest III Blocks.

Chad Operations Update

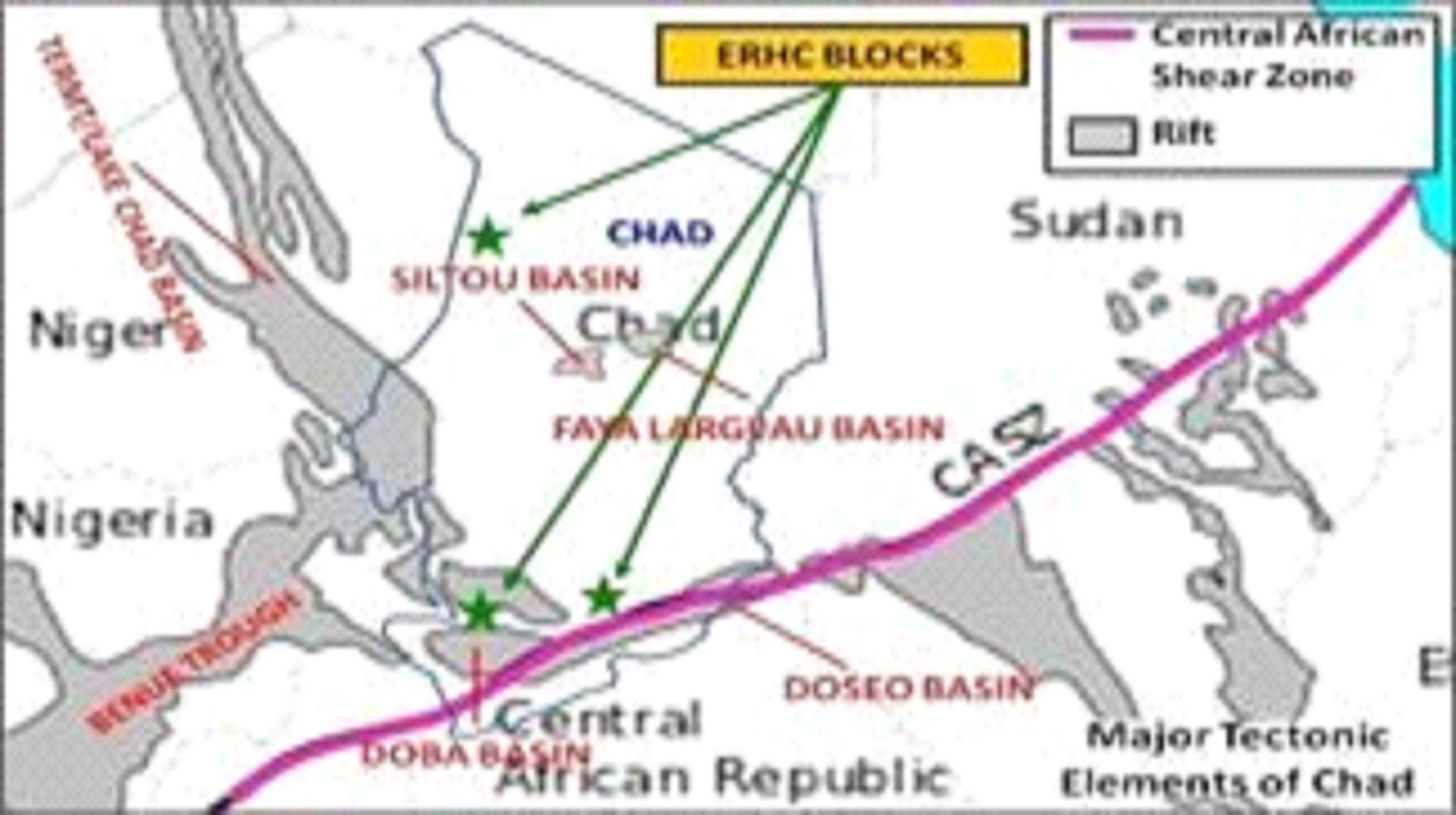

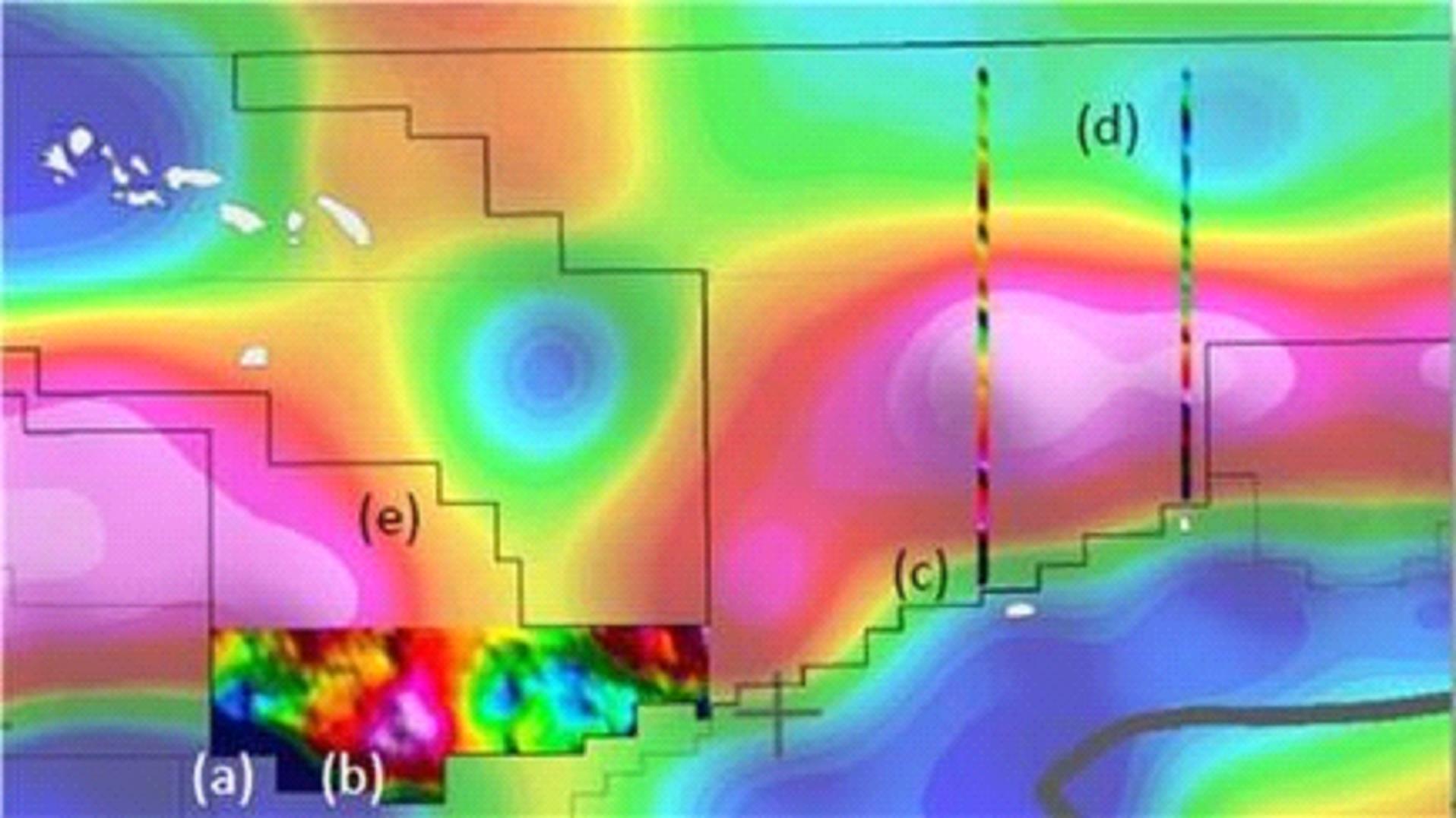

As of September 30, 2016, ERHC continues to talk with potential farm-in partners. The next stage of exploration is a seismic survey on ERHC’s two focus areas. ERHC is exploring, as one of its funding options, the possibility of a right-to-earn partnership in exchange for seismic services. Based on the result of an aero-magnetic and gravity survey that ERHC completed over the Block, total Petroleum Initially in Place (PIIP) for one of ERHC's two focus areas has been estimated at 278 million barrels (with a high case of 876 million barrels). ERHC holds a 100 percent interest in BDS 2008.

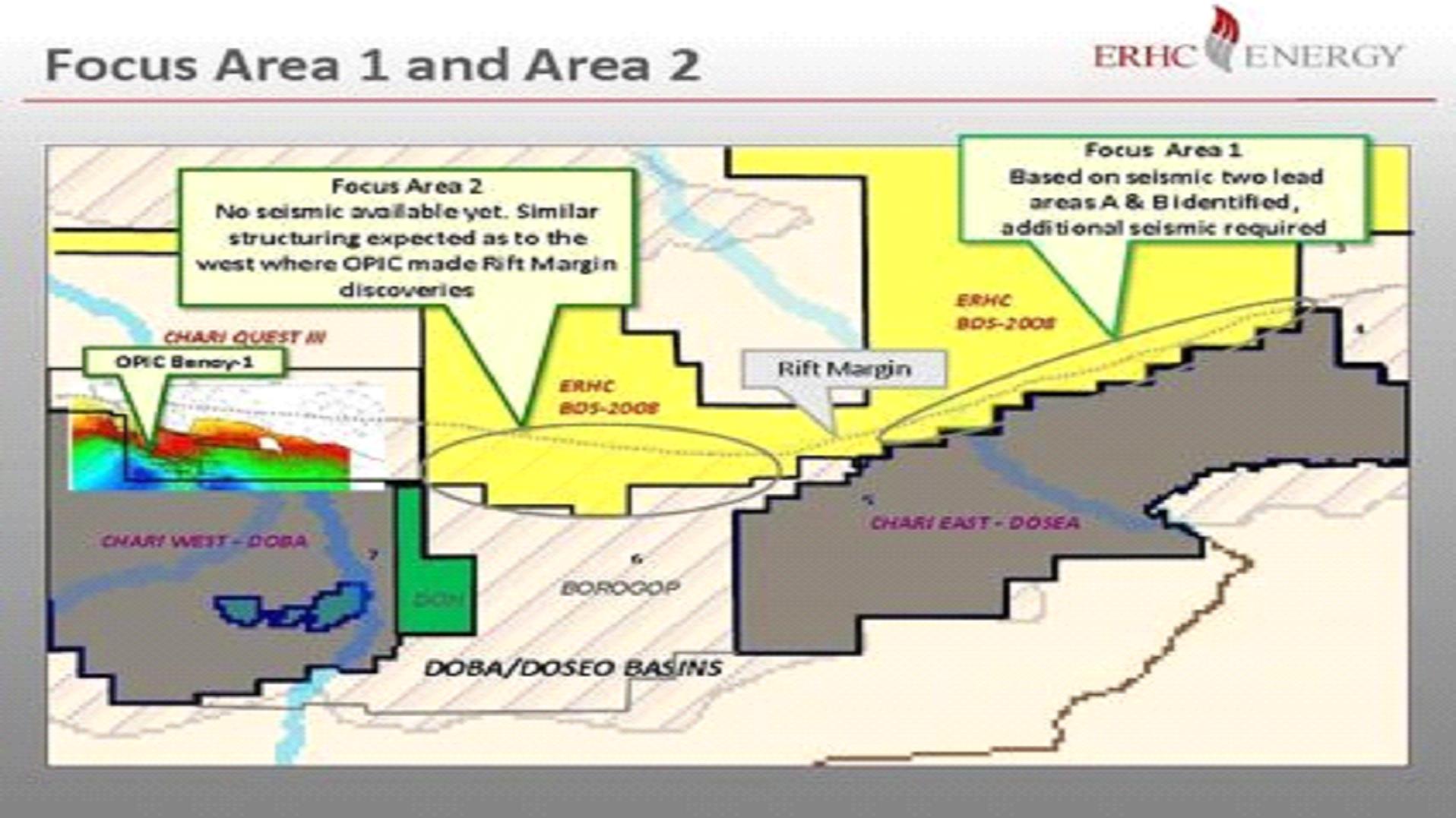

ERHC's exploration team is developing a Request for Proposals for a 2-D seismic acquisition program. The exploration team continues to work on securing regulatory approvals for the seismic program in ERHC's two focus areas. One is north of Esso's Tega and Maku discoveries in the Doseo basin and the other is east of and on trend with OPIC's Benoy-1 margin discovery in the Doba basin.

Focus Areas

ERHC's exploration focus is on Block BDS 2008 which measures 41,800 square kilometers or 10,329,000 acres. Within this block, two focus areas have been identified:

- North of Esso’s Tega and Maku discoveries in the Doseo basin; and

- East of and on trend with OPIC’s Benoy-1 margin discovery in the Doba basin.

Key Provisions of ERHC’s Production Sharing Contract (PSC) in Chad

CHAD BLOCK BDS 2008

|

LICENSE:

|

PSC with the Government of Chad signed June 20112

|

|

PARTIES:

|

ERHC (100%)

|

WORK PROGRAM:

Phase 1 (5 years – June 2012 to June 2017)3

|

Minimum Work

|

Minimum

Expenditure

|

Status

|

|

|

Unspecified: annual work program to be proposed yearly by contractor

|

$15,000,000 in total for the exploration phase

|

EIA completed;

|

|

|

Aero gravity and magnetic survey completed;

|

|||

|

·

|

4,720 line kilometers of high precision gravity and magnetic data acquired by November 2014;

|

||

|

·

|

Three leads identified;

|

||

|

Seismic in preparation;

|

|||

|

·

|

2D seismic on focus areas planned

|

||

2 PSC originally covered thee Blocks; ERHC voluntarily relinquished two Blocks in 2013, retaining only BDS 2008. Relinquishment and retention approved by Presidential Decree as provided for in PSC.

3 PSC provides for exploration period to run from date of grant of Exclusive Exploration Authorization (“EEA”). EEA granted to ERHC in June 2012.

Phase 2 (3 years)

|

Minimum Work

|

Minimum Expenditure

|

Status

|

|

Unspecified: annual work program to be proposed yearly by contractor

|

$1,000,000

|

ERHC proposes an exploration well in this period if Phase 1 G&G studies justify

|

|

OTHER FINANCIAL OBLIGATIONS:

|

|

|

Ministry Training Fund

|

$250,000 per annum during the exploration period

|

|

$500,000 per annum during the exploitation period

|

|

|

Social Projects:

|

None specified in the PSC

|

|

Surface Rentals

|

$1/km2 per annum (Exploration Phase 1); $5/ km2 per annum (Exploration Phase 2); $10// km2 per annum (Extension)

|

|

$100/ km2 per annum (Exploitation Phase 1); $150/ km2 per annum (Exploitation Phase 1)

|

|

|

COST RECOVERY AND PRODUCTION SHARING:

|

|

|

Royalty

|

14.25% for crude oil

|

|

5% for natural gas

|

|

|

Cost Oil

|

Up to 70% of net production after deduction of royalty

|

Profit Oil

|

R-Factor, as defined by the PSC 4

|

Less than or equal to 2.25

|

Between 2.25 and 3

|

Greater than 3

|

|

Contractor’s share of profit oil

|

60%

|

50%

|

40%

|

|

State’s share of profit oil

|

40%

|

50%

|

60%

|

4 R-factor is based on a formula defined in the PSC.

ERHC’s exploration team has commenced planning toward 2-D seismic acquisition. The information gathered through an airborne gravity/magnetic survey of the Block in Southern Chad proved to be a significant improvement on current data resolution. ERHC's sub-contractor, Bridgeporth Ltd., a specialist geosciences company, completed the survey during the fourth quarter of 2014, confirming the preliminary leads and revealing additional targets. The main conclusions of the study are as follows:

a) The Graben edge is clearly visible in the southwest corner of the Bridgeporth survey.

b) The data can be used to target seismic acquisition over possible rift associated structures.

c) It appears that the Graben edge will enter into the ERHC block northeast of the Bridgeporth survey.

d) Regional profile data acquired by Bridgeporth suggests that the gravity low to the north of BDS 2008 could indeed be a rifted section.

e) The saddle feature in the west central portion of the Block should be investigated.

As the Company did with the JDZ and Kenya Block 11A, ERHC continues to explore a farm-out to spread risk. The Chad acreage is also within the scope of Deloitte Corporation Finance LLC (DCF)'s engagement and ERHC continues to work with DCF to find suitable farm-out or joint venture partners.

NIGERIA – SAO TOME AND PRINCIPE JOINT DEVELOPMENT ZONE (“JDZ”)

Background of the JDZ

In the spring of 2001, Sao Tome & Principe and Nigeria signed a treaty establishing a JDZ for the joint development of petroleum and other resources in the overlapping area of their respective maritime boundaries. The treaty also established an administrative body, the Joint Development Authority (“JDA”), to administer the treaty and all activities in the JDZ. Revenues derived from the JDZ will be shared 60:40 between the governments of Nigeria and Săo Tomé & Príncipe, respectively. The JDZ lies approximately 180 kilometers south of Nigeria, in the Gulf of Guinea, one of the most prolific hydrocarbon regions of the world. .

ERHC’s Rights in the JDZ

In April 2003, the Company and STP entered into an Option Agreement (the “2003 Option Agreement”) in which the Company relinquished significant prior legal rights and financial interests in the Joint Development Zone (“JDZ”) in exchange for preferential exploration rights in the JDZ. Following the exercise of ERHC’s rights as set forth in the 2003 Option Agreement, the JDA confirmed the award in 2004 of participating interests (“Original Participating Interest”) in each of JDZ Blocks 2, 3, 4, 5, 6 and 9 of the JDZ during the 2004/5 licensing round conducted by the JDA. ERHC also jointly bid with internationally recognized technical partners for additional participating interests in the JDZ during the 2004/5 licensing round. As a result of the joint bid, ERHC won additional participating interests (“Joint Bid Participating Interest”) in Blocks 2, 3 and 4. The following is a tabulation of ERHC’s participating interests in the JDZ.

|

JDZ Block

|

ERHC Original

Participating

Interest

|

ERHC Joint Bid

Participating

Interest

|

Participating

Interest(s) Assigned

|

Current ERHC Retained

Participating Interest

|

|||||||||||||

| 2 |

30.00%

|

|

35.00%

|

43.00%

|

|

22.00%

|

|||||||||||

| 3 |

20.00%

|

|

5.00%

|

|

15.00%

|

|

10.00%

|

||||||||||

| 4 |

25.00%

|

|

35.00%

|

|

40.50%

|

|

19.50%

|

|

|||||||||

| 5 |

15.00%

|

|

-

|

-

|

15.00% (in arbitration)

|

||||||||||||

| 6 |

15.00%

|

|

-

|

-

|

15.00% (in arbitration )

|

||||||||||||

| 9 |

20.00%

|

|

-

|

-

|

20.00%

|

|

|||||||||||

ERHC’s Participating Agreements in the JDZ

The following are the particulars of the Participating Agreements by which ERHC assigned some of its participating interests in JDZ Blocks 2, 3 and 4 to technical partners so that the technical partners would operate the Blocks and carry ERHC’s proportionate share of costs in the Blocks until production, if any, commenced from the Blocks:

|

Date of Participation Agreement

|

Party(ies) to the Participation Agreement

|

Participating

Interest(s)

Assigned

|

Participating

Interest Assigned

Price

|

||||||

|

JDZ Block 2 - Participation Agreement - ERHC Retained Interest of 22.00%

|

|||||||||

|

March 2, 2006

|

Sinopec International Petroleum Exploration Production Co. Nigeria Ltd - a subsidiary of Sinopec International Petroleum and Production Corporation

|

28.67

|

%

|

$

|

13,600,000

|

||||

|

Addax Energy Nigeria Limited - an Addax Petroleum Corporation subsidiary

|

14.33

|

%

|

$

|

6,800,000

|

|||||

|

JDZ Block 3 - Participation Agreement - ERHC Retained Interest of 10.00%

|

|||||||||

|

February 15, 2006

|

Addax Petroleum Resources Nigeria Limited - a subsidiary of Addax Petroleum Corporation

|

15.00

|

%

|

$

|

7,500,000

|

||||

|

JDZ Block 4 - Participation Agreement - ERHC Retained Interest of 19.50%

|

|||||||||

|

November 15, 2005

|

Addax Petroleum Nigeria (Offshore 2) Limited - a subsidiary of Addax Petroleum Corporation

|

40.50

|

%

|

$

|

18,000,000

|

||||

Under the terms of the Participation Agreements Sinopec and Addax agreed to pay all of ERHC’s future costs for petroleum operations (“the carried costs”) in respect of ERHC's retained interests in the blocks. Additionally, Sinopec and Addax are entitled to 100% of ERHC’s allocation of cost oil plus up to 50% of ERHC’s allocation of profit oil from the retained interests on individual blocks until Sinopec and Addax Sub recover 100% of ERHC’s carried costs.

On or about October 2, 2009, Sinopec International Petroleum Exploration and Production Corporation acquired all of the outstanding shares of Addax Petroleum Corporation

ERHC’s JDZ Acreage

ERHC has working interests in six of the nine Blocks in the JDZ, as follows:

| · |

JDZ Block 2: 22.0%

|

| · |

JDZ Block 3: 10.0%

|

| · |

JDZ Block 4: 19.5%

|

| · |

JDZ Block 5: 15.0% (in arbitration)

|

| · |

JDZ Block 6: 15.0% (in arbitration)

|

| · |

JDZ Block 9: 20.0%

|

The working interest percentages represent ERHC’s share of all the hydrocarbon production from the blocks and obligates ERHC to pay a corresponding percentage of the costs of drilling, production and operating the blocks. Through Exploration Phase 1 in blocks 2, 3 and 4, these costs have been carried by the operators. The operators can only recover their costs by carrying ERHC until production whereupon the operators will recover their costs from production revenues.

In 2009, Sinopec and Addax, ERHC's technical partners and operators in Blocks 2, 3 and 4 undertook an exploratory drilling campaign across the three blocks that was completed in January 2010.

Biogenic gas was discovered in each block and discussions continue between the Joint Development Authority and the parties, including ERHC, that hold interests in JDZ Blocks 2, 3 and 4, regarding drilling results. The meetings with the JDA are aimed at reaching a definitive agreement on how to proceed with the next stage of exploration in the Blocks following the expiration of Exploration Phase I in March 2012.

JDZ Operations Update

The JDZ partnership is currently assessing the data for possible new exploration play concepts in this area. As of September 30, 2016 The Nigeria - São Tomé and Príncipe Joint Development Authority (JDA) continues to engage with the remaining JDZ contracting parties, including ERHC, on the way forward for further exploration.

SAO TOME AND PRINCIPE EXCLUSIVE ECONOMIC ZONE (“EEZ”)

Overview of ERHC’s EEZ Blocks

The Săo Tomé and Príncipe EEZ is delineated over an expanse of waters offshore Săo Tomé and Príncipe that covers approximately 160,000 square kilometers. In terms of hydrocarbon exploration and exploitation, the EEZ is a frontier region that sits south of the Niger Delta and west of the Gabon salt basin, retaining similarities with each of those prolific hydrocarbon regions. The regional seismic database comprises approximately 12,000 kilometers of seismic data. Interpretation of that seismic data shows numerous structures in the EEZ that have similar characteristics to known hydrocarbon accumulations in the area.

ERHC’s Rights in the EEZ

Under a 2001 agreement with the Government of Săo Tomé and Príncipe (“STP”), ERHC was vested with the rights to participate in exploration and production activities in the EEZ. These rights included (a) the right to receive up to 100% of two blocks of ERHC’s choice and (b) the option to acquire up to a 15% paid working interest in each of two additional blocks of ERHC’s choice in the EEZ. In 2010, ERHC exercised its rights to receive up to 100% of two blocks of ERHC’s choice in the EEZ and was duly awarded Blocks 4 and 11 of the EEZ by the Government of STP.

EEZ Block 4 is 5,808 square kilometers, situated directly east of the island of Príncipe. The northeastern area near EEZ Block 4 contains a large graben structure, which is bound by the Kribi Fracture Zone.

EEZ Block 11 totals 8,941 square kilometers, situated directly east of the island of Săo Tomé and abuts the territorial waters of Gabon. The southern area of the EEZ, where EEZ Block 11 is situated, contains parts of the Ascension and Fang Fracture Zones.

ERHC will decide whether to take up the option to acquire up to a 15% paid working interest in each of two additional blocks of the EEZ when called upon to exercise the option by the Government of STP in accordance with the agreements which provide for the rights and option.

PSC for the EEZ Block 11

In July 2014, ERHC and the National Petroleum Agency of Săo Tomé and Príncipe (ANP-STP) announced the conclusion of final terms for the Production Sharing Contract for EEZ Block 11.

A PSC is an agreement that governs the relationship between the Company (and its joint venture partners) and the Government of Săo Tomé and Príncipe in respect of exploration and production in any Block awarded to the Company. The PSC spells out, among other things, the work commitments (including acquisition of data, drilling of wells, social projects, etc.), the time frames for accomplishing the work commitments, how production will be shared between the parties and the government, and how the costs of exploration, development and production will be recovered.

In October 2015, the Company reached an agreement with Kosmos Energy (NYSE: KOS), a leading independent oil and gas exploration and production company focused on frontier and emerging areas to transfer all ERHC's rights to Block 11 of the São Tomé and Principe Exclusive Economic Zone (EEZ) to Kosmos. The agreement has been approved by the National Petroleum Agency of Sao Tome & Principe ("ANP-STP") as required in the requisite Production Sharing Contract ("PSC") for EEZ Block 11.

EEZ Operations Update

ERHC has concluded negotiation of the terms of a Production Sharing Contract with the National Petroleum Agency of São Tomé and Principe (ANP-STP) for Block 4. The Company is currently in discussions with potential farm in partners. ERHC holds a 100 percent interest in EEZ Block 4, and 15% right to paid working interest in each of two additional blocks of the EEZ.

INVESTMENT IN OANDO ENERGY RESOURCES (FORMERLY EXILE RESOURCES)

During the year ended September 30, 2011, ERHC invested $1,350,000 in Exile Resources Inc, a company listed on the Toronto Stock Exchange (Ventures Exchange) stock in open market purchases. ERHC’s intention was to gain an indirect interest in Exile’s underlying oil and gas exploration and production assets as well as the ability to participate in Exile’s decision making in respect of those assets. ERHC was particularly interested in Exile’s carried interest in the proven Akepo field in the Niger Delta.

In July 2011, Oando Petroleum and Exploration Company (“Oando Petroleum”) commenced a reverse takeover (“RTO”) of Exile Resources. In July 2012, Exile announced the completion of the RTO by Oando Petroleum and the change of name of the resultant company to Oando Energy Resources Inc, (“Oando Energy”). It also announced the listing of the company’s shares under the symbol “OER” on the Toronto Stock Exchange (TSX) and commencement of trading in the shares on the TSX from July 30, 2012.

During the year ended September 30, 2016, ERHC’s investment in the common stock of Oando Energy Resources, Inc. (“OER”), a Canadian oil and gas company that trades on the Toronto Stock Exchange (TSX) was purchased by the majority shareholder of OER, pursuant to a shareholder approved buyout.

CURRENT PLANS FOR OPERATIONS

ERHC’s principal assets are its interests in rights for exploration for hydrocarbons in Kenya, Chad, the JDZ and the EEZ. ERHC has no current sources of income from its operations. The Company plans to develop its business by the acquisition of other assets which may include revenue-producing assets in diverse geographical areas and the forging of strategic, new business partnerships and alliances. ERHC cannot currently predict the outcome of negotiations for acquisitions, or, if successful, their impact on the Company's operations.

PLANS FOR FUNDING EXISTING ASSETS AND POTENTIAL NEW ACQUISITIONS

ERHC's future plans will depend on the Company's ability to attract new funding. The Company is implementing a series of steps to fund the geophysical work, including magnetic/gravity and seismic surveys, prior to securing potential farm-out on Chad acreage. Said funding steps include but are not limited to the issuance of a series of convertible notes, which the Company has commenced, issuance of shares of common stock through registered direct offerings, which the Company plans to commence shortly and farm-outs to potential partners on its assets in Africa. The fund raising might include:

| · |

Farm-outs of part of the Company’s assets in Kenya, Chad and the Săo Tomé and Príncipe Exclusive Economic Zone

|

| · |

Issue shares of common stock through a registered direct offering

|

| · |

Other available financing options

|

The Company is continuing discussions with several international investment advisory and financial brokerage firms to act as financial advisors and intermediaries to ERHC. While ERHC has always used expert professional assistance to formulate and execute its capital raising initiatives, it is re-focusing on the retention of such advisors and intermediaries as a strategic imperative of the increased funding requirements that arise from the rollout of the new work programs in Chad and Kenya. The new firms retained will perform such financial advisory and investment banking services for the Company as are customary and appropriate in transactions of this type, including assisting the Company in analyzing, structuring, negotiating and effecting proposed capital raises. These initiatives may include any transaction or series of transactions in which one or more capital providers (existing or otherwise) commits debt capital to the Company, purchases equity of the Company (or securities of the Company convertible into equity), or alternatively funds the Company either directly or through farm-ins, farm-outs or other arrangements in which the capital provider earns an interest in oil and gas properties of the Company.

UPDATES AND INFORMATION

ERHC’s website at http://www.erhc.com contains information about the Company’s operations, assets, and initiatives and a FAQ page that is frequently updated to address the latest questions.

The Company provides free of charge on our website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable.

SEC’s Public Reference Room at 100 F Street NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers, including us, that file electronically with the SEC. The public can obtain any documents that we file with the SEC at h http://www.sec.gov after we electronically file such material with, or furnish it to, the SEC.

You should carefully consider the risks described below before making any investment decision related to the Company’s securities. The risks and uncertainties described below are not the only ones facing the Company. Additional risks and uncertainties not presently known or that the Company currently deems immaterial also may impair its business operations. If any of the following risks actually occur, the Company’s business could be affected.

The Company has no sources of revenue and a history of losses from operations

The Company’s business is in an early stage of development. The Company has not generated any operating revenue since its entry into the oil and gas industry and has historically incurred significant operating losses. The Company may continue to incur operating losses for the foreseeable future. As such, the Company is subject to significant risks and may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors that may adversely affect its business. The Company’s financial statements as of September 30, 2016 have been prepared on the assumption that the Company will continue as a going concern. The Company’s business requires significant financial resources. The ability of the Company to continue as a going concern is dependent on raising additional capital to fund its exploration projects and for other working capital requirements. There can be no assurance that the Company will be successful in its efforts to raise additional financing or if financing is available, that it will be on terms acceptable to the Company.

The Company has a limited operating history in the oil and gas industry

The Company’s operations have consisted solely of acquiring rights to working interests in Kenya, Chad, the JDZ and the EEZ and entering into production sharing contracts. The Company may not be the operator with respect to these contracts. The Company’s future financial results depend primarily on (1) the ability of the Company or its venture partners to provide or obtain sufficient financing to meet their financial commitments in the production sharing contracts, (2) the ability to discover commercial quantities of oil and gas, and (3) the market price for oil and gas. Management cannot predict if or when the production sharing contracts will result in future wells being drilled or if drilled, whether oil and/or gas will be discovered in commercial quantities.

Financing may be needed to fund the financial commitments of the production sharing contracts

The Company’s failure or the failure of the Company’s venture partners to provide or obtain the necessary financing may preclude the continuation of exploration activities which would adversely affect the value of its concessions in Kenya, Chad, the JDZ and the EEZ.

The Company may not discover commercially productive reserves in Kenya, Chad, the JDZ or the EEZ

The Company’s future success depends on its ability to economically discover oil and gas reserves in commercial quantities in Kenya, Chad, the JDZ, and/or the EEZ. There can be no assurance that the Company’s planned projects in Kenya, Chad, the JDZ or the EEZ will result in significant, if any, reserves or that the Company and its partners will have future success in drilling productive wells.

The Company’s non-operator status limits its control over oil and gas projects in Kenya, Chad, the JDZ and the EEZ

The Company will focus primarily on creating exploration opportunities and forming relationships with oil and gas companies to develop those opportunities in Kenya, Chad, the JDZ and the EEZ. As a result, the Company may have only a limited ability to exercise control over a significant portion of a project’s operations and the associated costs of those operations in Kenya, Chad, the JDZ or the EEZ. The success of a future project is dependent upon a number of factors that may be outside the Company’s control. These factors include:

| · |

the availability of future capital resources to the Company and the other participants for drilling additional wells;

|

| · |

the approval of the Company or other participants for determining well locations and drilling time-tables;

|

| · |

the economic conditions at the time of drilling, including the prevailing and anticipated price of oil and gas; and

|

| · |

the availability and cost of land based and/or deep water drilling rigs and the availability of operating personnel.

|

The Company’s reliance on its consortium partners and its limited ability to directly control future project costs could have a material adverse effect on its future rates of return.

The Company’s success depends on its ability to exploit its limited assets

The Company’s primary assets are rights to working interests in exploration acreage in Kenya, Chad, the JDZ and the EEZ under agreements with the Government of Kenya, Chad, the JDA and DRSTP. The Company’s operations have been limited to managing and sustaining its rights under these agreements. The Company’s viability depends on its ability to exploit these assets. However, there is no assurance that it will be successful.

The Company is subject to Government Regulation over which it has no control

In the event the Company begins direct exploration and exploitation of hydrocarbons, it will be required to make necessary expenditures to comply with applicable health and safety, environmental and other regulations.

The oil and gas industry is subject to various types of regulations throughout the world. Legislation affecting the oil and gas industry has been pervasive and is under constant review for amendment or expansion. Pursuant to such legislation, numerous government agencies have enacted extensive laws and regulations binding on the oil and gas industry and companies engaged in this industry, some of which carry substantial penalties for failure to comply. Such laws and regulations have a significant impact on oil and gas exploration, production and marketing and midstream activities. These laws and regulations increase the cost of doing business and, consequently, will affect results of operations.

In as much as new legislation affecting the oil and gas industry is commonplace and existing laws and regulations are frequently amended or reinterpreted, the Company is unable to predict the future cost or the impact of complying with such laws and regulations. However, the Company does not expect that any of these laws and regulations will affect its operations in a manner materially different from that in which they would affect other oil and gas companies of similar size and scope of operations.

Having interests outside the United States requires the Company to comply with United States laws and other laws in foreign jurisdictions related to pursuing, owing, and exploiting foreign investments, agreements and other relationships. The Company is subject to all such laws, including, but not limited to, the Foreign Corrupt Practices Act of 1977 (“FCPA”).

The Company’s competition includes oil and gas conglomerates that have significant advantages over it

The oil and gas industry is highly competitive. Many companies are engaged in exploring for crude oil and natural gas and acquiring crude oil and natural gas properties, resulting in significant competition for desirable exploratory and producing properties. The companies with which the Company competes are much larger and have greater financial resources and technical expertise than the Company.

Various factors beyond the Company’s control will affect prices of oil and gas

The availability of a ready market for the Company’s future crude oil and natural gas production if any depends on numerous factors beyond its control, including the cyclical nature of the price of crude oil and natural gas, the level of consumer demand, the extent of worldwide crude oil and natural gas production, the costs and availability of alternative fuels, the costs and proximity of transportation facilities, regulation by authorities and the costs of complying with applicable environmental and other regulations.

The Company’s business interests are located outside of the United States which subjects it to risks associated with international activities beyond its control.

At September 30, 2016, the Company’s major assets are located outside the United States. The Company’s primary assets are cash in various financial institutions and agreements with Kenya, Chad, the DRSTP and the JDA, which provide ERHC with rights to participate in exploration and production activities in Kenya, Chad, the EEZ and the JDZ. Production is subject to political risks which are inherent in all foreign operations. The Company’s ability to exploit its interests in this area pursuant to such agreements may be adversely impacted by this circumstance.

The future success of the Company’s international operations may also be adversely affected by risks associated with international activities, including economic and labor conditions, political instability, risk of war, expropriation, termination, renegotiation or modification of existing contracts, tax laws (including host-country import-export, excise and income taxes and United States taxes on foreign subsidiaries) and changes in the value of the U.S. dollar relative to the local currencies in which future oil and gas producing activities may be denominated. Changes in exchange rates may also adversely affect the Company’s future results of operations and financial position.

In addition, to the extent the Company engages in operations and activities outside the United States, it is subject to the Foreign Corrupt Practices Act (the “FCPA”) which, among other restrictions, prohibits U.S. companies and their intermediaries from making payments to foreign officials for the purpose of obtaining or keeping business or otherwise obtaining favorable treatment, and requires companies to maintain adequate record-keeping and internal accounting practices to accurately reflect their financial and other transactions with foreign officials. The FCPA applies to companies, individual directors, officers, employees and agents. The FCPA also applies to foreign companies and persons taking any action in furtherance of such payments while in the United States. Under the FCPA, U.S. companies may also be held liable for actions taken by strategic or local partners or representatives.

The FCPA imposes civil and criminal penalties for violations of its provisions. Civil penalties may include fines of up to $500,000 per violation, and equitable remedies such as disgorgement of profits causally connected to the violation (including prejudgment interest on such profits) and injunctive relief. Criminal penalties for violations of the payments provisions could range up to the greater of $2 million per violation or twice the gross pecuniary gain sought by making the payment, and/or incarceration for up to 5 years per violation. Moreover, if a director, officer or employee of a company is found to have willfully violated the FCPA books and records provisions, the maximum penalty would be imprisonment for 20 years per violation. Maximum fines of up to $25 million may also be imposed for willful violations of the books and records provisions by a company.

The Company’s business interests are located in Kenya, Chad and in the Gulf of Guinea offshore Africa and are subject to the volatility of foreign governments

The Company’s primary assets are located in Kenya, Chad and in the Gulf of Guinea, offshore Africa. The Governments of Kenya, Chad, Nigeria and the island nation of Sao Tome and Principe granted ERHC participation interests in various concessions in their lands and offshore waters. The Governments of Kenya, Chad, Nigeria and Sao Tome and Principe exist in a volatile political and economic environment and the Company is subject to all the risks associated with those governments. These risks include, but are not limited to:

| · |

Loss of future revenue and concessions as a result of hazards such as war, acts of terrorism, insurrection and other political risks;

|

| · |

Increases in taxes and governmental interests;

|

| · |

Unilateral renegotiation of contracts by government entities;

|

| · |

Difficulties in enforcing our rights against a governmental agency because of the doctrine of sovereign immunity and foreign sovereignty over international operations;

|

| · |

Changes in laws and policies governing operations of foreign-based companies, and

|

| · |

Currency restrictions and exchange rate fluctuations.

|

The Company’s foreign operations may also be adversely affected by laws and policies of the United States affecting foreign trade and taxation. Realization of any of these factors could materially and adversely affect our financial position, results of operations and cash flows.

The Company has filed suit to prevent tampering with its interest and any adverse ruling related to JDZ Blocks 5 and 6. This action could have a material adverse effect on ERHC’s business, prospects, operations, financial condition and cash flow.

The Company’s rights in JDZ Blocks 5 and 6 are currently the subject of legal proceedings at the London Court of International Arbitration and the Federal High Court in Abuja, Nigeria. The Company instituted both proceedings in November 2008 against the JDA and the Governments of Nigeria and Săo Tomé and Príncipe. The Company seeks legal clarification that its rights in the two Blocks remain intact.

The issue in contention is contractual. The Company was awarded a 15 percent working interest in each of the Blocks in a 2004/5 bid/licensing round conducted by the JDA following the Company’s exercise of preferential rights in the Blocks as guaranteed by contract and treaty. The JDA and the Government of STP contend that certain correspondence issued by a previous CEO/President of the Company in 2006 amount to a relinquishment of the Company’s rights in Blocks 5 and 6 under the Company’s contracts with STP which provide for the rights. The Company contends that no such relinquishment has occurred and has sought recourse to arbitration accordingly. It also filed the suit to prevent any tampering with its said rights in JDZ Blocks 5 and 6 pending the outcome of arbitration.

Proceedings on the suit and the arbitration are currently suspended while the Company pursues amicable settlement with the Governments of Nigeria and Săo Tomé & Príncipe.

The Company has limited sources of working capital

The Company is currently focused on consolidating and exploiting its interests in Kenya, Chad, JDZ Blocks 2, 3, 4, 5, 6 and 9 and has limited working capital.

As described in more detail in “Item 7 Future Capital Requirements” of this Form 10-K, the Company’s minimum working capital requirements in 2017 will be approximately $13,100,000.

If ERHC is unable to successfully raise capital to cover its planned operations or negotiate participation agreements with operating and other partners in, Chad and the EEZ, the Company’s cash resources could be strained and the Company’s future plans curtailed.

The Company’s results of operations are susceptible to general economic conditions

The Company’s revenues and results of operations will be subject to fluctuations based upon the general economic conditions both in the United States and internationally. A general economic downturn or a recession in the industry, will adversely impact the Company’s prospective future revenues, the value of its oil and natural gas exploration concession, as well as its ability to exploit its assets.

The Company’s stock price is highly volatile

The Company’s common stock is currently traded on the Over-the-Counter (OTC) Bulletin Board. The market price of the Company’s common stock has experienced fluctuations that are unrelated to its operating performance. The market price of the common stock has been highly volatile over the last several years. The Company can provide no assurance regarding its stock price.

The Company does not currently pay dividends on its common stock and does not anticipate doing so in the near future

The Company has paid no cash dividends on its common stock, and there is no assurance that the Company will achieve sufficient earnings to pay cash dividends on its common stock in the foreseeable future. The Company intends to retain any earnings to fund its future operations.

The Company’s stock is considered a “penny stock”

The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in “penny stocks.” Penny stocks generally are equity securities with a share price of less than $5.00. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document prepared by the SEC that provides information about penny stocks and the nature and level of risks in the penny stock market. These disclosure requirements may have the effect of reducing the level of trading activity in any secondary market for a stock that becomes subject to the penny stock rules. The Company’s common stock may be subject to the penny stock rules, and accordingly, investors in the common stock may find it difficult to sell their shares in the future, if at all.

None.

Republic of Kenya

The Company initially held a 90% interest in Block 11A, which encompasses 11,950.06 square kilometers or 2.95 million square acres. The Government of Kenya has a 10% carried participating interest up to the declaration of commerciality and may thereafter acquire an additional 10% interest in the PSC in which case the total Government participation would rise to 20%. Circle Limited, which acted as ERHC’s finder in the acquisition of ERHC’s interest in the Block is entitled to 5% of ERHC’s interest as agreed finder’s fee.

In October, 2013, the Company entered into a farm-out agreement with CEPSA Kenya Limited, an affiliate of Compañía Española de Petróleos, S.A.U., an international oil and gas company ("CEPSA"). Under the terms of this agreement, the Company assigned and transferred 55% of its participating interest in Kenya Block 11A to CEPSA.

In exchange for the transferred rights, CEPSA will carry the Company's proportionate share of obligations and financial costs under the terms and conditions outlined in the farm-out agreement. The agreement was approved in January 2014 by the Kenyan Government and from February 2014, CEPSA took over from ERHC as operator under the production sharing contract ("PSC") for Kenya Block 11A.

Republic of Chad

On July 6, 2011, the Company announced that it had signed a Production Sharing Contract (PSC) on the three oil blocks with the Government of Chad. The initial period of exploration commenced on July 12, 2012 with the publication, in Chadian Government’s Gazette Principal, of the Exclusive Exploration Authorization, granted to ERHC by the Government of Chad.

ERHC subsequently offered to novate the PSC by retaining only the BDS2008 Block and relinquishing the Manga and Chari Ouest III Blocks to the Chadian government for efficiency. The Chadian Ministry of Energy and Petroleum approved the novation of the PSC and ERHC received the Presidential decree of approval in March 2014. The BDS 2008 Block has an area of 16,360 square kilometers or 4,042,644 acres.

Joint Development Zone

|

ERHC has interests in six of the nine Blocks in the Joint Development Zone (JDZ), a 34,548 sq. km area approximately 200 km off the coast of Nigeria and Sao Tome and Principe that is adjacent to several large petroleum discovery areas. ERHC’s rights in the JDZ include:

|

|

| · |

JDZ Block 2: 22.0%

|

| · |

JDZ Block 3: 10.0%

|

| · |

JDZ Block 4: 19.5%

|

| · |

JDZ Block 5: 15.0% (in Arbitration)

|

| · |

JDZ Block 6: 15.0% (in Arbitration)

|

| · |

JDZ Block 9: 20.0%

|

Sao Tome and Principe Exclusive Economic Zone

ERHC holds the following working interests and rights in the EEZ:

| · |

EEZ Block 4: 100% working interest and no signature bonus

|

| · |

EEZ Block 11: 100% working interest and no signature bonus

|

| · |

The option to acquire up to a 15% paid working interest in additional two blocks of ERHC’s choice.

|

ERHC will be responsible for its proportionate share of exploration and exploitation costs in the EEZ blocks.

Corporate Office

The Company’s corporate office is located at 5444 Westheimer Road, Suite 1440, Houston, Texas 77056 pursuant to a lease that expires in July 2017.

JDZ Blocks 5 and 6

Arbitration and Lawsuit

The Company's rights in JDZ Blocks 5 and 6 are currently the subject of legal proceedings at the London Court of International Arbitration and the Federal High Court in Abuja, Nigeria. The Company instituted both proceedings in November 2008 against the JDA and the Governments of Nigeria and Săo Tomé and Príncipe. The Company seeks legal clarification that its rights in the two Blocks remain intact.

The issue in contention is contractual. The Company was awarded a 15 percent working interest in each of the Blocks in a 2004/5 bid/licensing round conducted by the JDA following the Company's exercise of preferential rights in the Blocks as guaranteed by contract and treaty. The JDA and the Government of STP contend that certain correspondence issued by a previous CEO/President of the Company in 2006 amount to a relinquishment of the Company's rights in Blocks 5 and 6 under the Company's contracts with STP which provide for the rights. The Company contends that no such relinquishment has occurred and has sought recourse to arbitration accordingly. It also filed the suit to prevent any tampering with its said rights in JDZ Blocks 5 and 6 pending the outcome of arbitration.

Suspension of Proceedings on the Arbitration and Lawsuit

Proceedings on the suit and the arbitration are currently suspended while the Company pursues amicable settlement with the Governments of Nigeria and Săo Tomé Príncipe.

Routine Claims

From time to time, ERHC may be subject to routine litigation, claims, or disputes in the ordinary course of business. ERHC intends to defend these matters vigorously; the Company cannot predict with certainty, however, the outcome or effect of any of the litigation or investigatory matters specifically described above or any other pending litigation or claims. There can be no assurance as to the ultimate outcome of these lawsuits and investigations.

None.

PART II

| Item 5. |

Market and Related Information

ERHC’s common stock is currently traded on the OTC Bulletin Board under the symbol “ERHE.” The market for the Company’s common stock is unpredictable and highly volatile. The following table sets forth the closing sales price per share of the common stock for the past three fiscal years. These prices reflect inter-dealer prices, without retail mark-ups, markdowns or commissions, and may not necessarily represent actual transactions.

Stock Price Highs & Lows

|

High

|

Low

|

|||||||

|

(Price per share)

|

||||||||

|

Fiscal Year 2016

|

||||||||

|

First Quarter

|

$

|

0.002

|

$

|

0.001

|

||||

|

Second Quarter

|

$ |

0.440

|

$ |

0.014

|

||||

|

Third Quarter

|

$ |

0.090

|

$ |

0.033

|

||||

|

Fourth Quarter

|

$ |

0.055

|

$ |

0.006

|

||||

|

Fiscal Year 2015

|

||||||||

|

First Quarter

|

$

|

0.053

|

$

|

0.070

|

||||

|

Second Quarter

|

$ |

0.023

|

$ |

0.001

|

||||

|

Third Quarter

|

$ |

0.003

|

$ |

0.001

|

||||

|

Fourth Quarter

|

$ |

0.004

|

$ |

0.001

|

||||

As of December 31, 2016, there were approximately 2,200 stockholders of record. The closing price of the common stock as reported on the OTC Bulletin Board on December 31, 2016 was $0.0002. The Company has not paid any dividends during the last three fiscal years and does not anticipate paying any cash dividends in the foreseeable future.

Securities Authorized for Issuance under Equity Compensation Plans

In November 2004, the Board of Directors adopted a 2004 Compensatory Stock Option Plan pursuant to which it reserved 20,000,000 shares for issuance. This plan was approved at a special meeting of the stockholders of the Company in February 2005. Under this plan, 14,681,756 shares have been authorized.

|

Number of securities to

be issued upon exercise

of outstanding options,

warrants and rights (a)

|

Weighted-average

exercise price of

outstanding options,

warrants and rights (b)

|

Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding

securities reflected in

column (a)) (c)

|

||||||||||

|

Equity compensation plans approved by security holders

|

4,150,000

|

0.20

|

5,318,244

|

|||||||||

|

Equity compensation plans not approved by security holders

|

-

|

-

|

-

|

|||||||||

Recent Sales of Securities Exempt from Registration

None.

Issuer Purchases of Equity Securities

The Company has not repurchased any of its Common Stock.

Not applicable.

Introduction

The following discussion and analysis presents management’s perspective of the Company’s business and, financial condition and its overall performance. This information is intended to provide investors with an understanding of our past performance, current financial condition and outlook for the future. You must read the following discussion of the results of the operations and financial condition of the Company in conjunction with its financial statements, including the notes thereto included in this Form 10-K filing. The Company’s historical results are not necessarily an indication of trends in operating results for any future period.

Reference is made to “Item 6. Selected Financial Data” and “Item 8. Financial Statements and Supplementary Data.”

The business of exploring for, developing, or acquiring oil and gas assets is capital intensive and the Company expects to continue to make significant capital expenditures over the next several years as part of its long-term growth strategy. The Company has no revenue from current operations and its existing cash and cash equivalents are finite. It is anticipated that external financing will be required in the future to fund the Company’s intended acquisition and exploration programs.

Possible sources of funding include private or public financings (including possible rights offering, registered direct offerings or private placements of the Company’s capital stock), strategic relationships or other arrangements. While ERHC has obtained funding for operations from private equity placements in the past, there is no assurance that the Company will be able to do so again in the near future at commercially reasonable terms or at all despite any progress in its business prospects. At the Company’s current stage of development, public or private debt funding may not be available on acceptable terms or at all. If ERHC enters into strategic relationships to raise additional funds, it might be required to relinquish certain rights to its assets and/or future revenue streams from any prospective resource plays.

Failure to raise capital or secure financing when needed could leave ERHC with insufficient resources in the future to sustain its exploration and development activities. Without additional capital resources, the Company may be forced to limit, defer or cease acquisitions or capital expenditures, sell assets, cede acreage or acquired interest, reduce operating expenses, or delay or reduce planned exploration and development programs, which in turn may adversely affect the Company’s financial condition and business prospects. Raising any additional funds through equity or debt financing, convertible debt financing, joint ventures with corporate partners or other sources may be dilutive to the Company’s existing shareholders and may affect the price of its common stock. Ultimately, there can be no assurance that ERHC will be successful in obtaining additional financing to fund its growth.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

This Annual Report on Form 10-K contains forward-looking statements. Forward-looking statements include statements concerning plans, objectives, goals, strategies, expectations, future events or performance and underlying assumptions and other statements which are other than statements of historical facts. Certain statements contained herein are forward-looking statements and, accordingly, involve risks and uncertainties which could cause actual results or outcomes to differ materially from those expressed in the forward-looking statements. Our expectations, beliefs and projections are expressed in good faith and are believed by us to have a reasonable basis, including without limitations, management's examination of historical operating trends, data contained in our records and other data available from third parties, but there can be no assurance that management's expectations, beliefs or projections will result or be achieved or accomplished. In addition to other factors and matters discussed elsewhere herein and the risks discussed in Item 1A. Risk Factors , the following are important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements: geopolitical instability where we operate; our ability to meet our capital needs; our ability to raise sufficient capital and/or enter into one or more strategic relationships with one or more industry partners to execute our business plan; our ability and success in finding, developing and acquiring oil and gas reserves; our ability to respond to changes in the oil exploration and production environment, competition, and the availability of personnel in the future to support our activities.

Overview

ERHC Energy Inc., a Colorado corporation, (“ERHC” or the “Company”) was incorporated in 1986. The Company’s business is the exploration and exploitation of oil and gas resources in Africa including its rights to working interests in exploration acreage in the Republic of Kenya (“Kenya”), in the Republic of Chad (“Chad”), in the Joint Development Zone (“JDZ”) between the Democratic Republic of Săo Tomé and Príncipe (“STP”) and the Federal Republic of Nigeria (“FRN or “Nigeria”) and in the exclusive economic zone of Săo Tomé (the “Exclusive Economic Zone” or “EEZ”).

A description of the Company’s current operations is contained in Item 1 of this Form 10-K and readers are encouraged to read that analysis in connection with Management’s Discussion and Analysis of Financial Condition and Plan of Operations.

In recent years ERHC has been focused on identifying opportunities in Africa that works to its strengths and leverage the experience gained through the Company's long term involvement in the JDZ and EEZ.

Critical Accounting Policies

The Company has identified the policies below as critical to its business operations and the understanding of its results of operations. The impact and any associated risks related to these policies on the Company’s business operations are discussed throughout this section where such policies affect the Company’s reported and expected financial results. Management’s preparation of this Annual Report on Form 10-K requires it to make estimates and assumptions that affect the reported amount of assets and liabilities, and the disclosure of contingent assets and liabilities. There is no assurance that actual results will not differ from those estimates and assumptions.

Concentration of Risks

The Company’s current focus is to exploit assets consisting of working interests in agreements with Kenya, Chad, the DRSTP and JDA concerning oil and gas exploration. The Company has developed internal capabilities and is also forming relationships with other oil and gas companies with the technical and financial capabilities to assist the Company in leveraging its interests in Kenya, Chad, the EEZ and the JDZ. The Company currently has no other operations.

Impairment of Long-lived Assets

ERHC evaluates the recoverability of long-lived assets when events and circumstances indicate that such assets might be impaired. ERHC determines impairment by comparing the undiscounted future cash flows estimated to be generated by these assets to their respective carrying amounts. Impairments are charged to operations in the period to which events and circumstances indicate that such assets might be impaired. ERHC has evaluated its investment in interests in Kenya, Chad, its DRSTP concession, and its JDA interests in light of its 2003 Option Agreement and there have been no events or circumstances that would indicate that such assets might be impaired.

Recent Accounting Pronouncements

In April 2015, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update ASU 2015-03 “Simplifying the Presentation of Debt Issuance Costs” (ASU 2015-03). ASU 2015-03 changes the presentation of debt issuance costs in financial statements. Upon adoption of ASU 2015-03, debt issuance costs will be reported in the balance sheet as a direct deduction from the related debt liability rather than as an asset. We adopted ASU 2015-03 retrospectively during the year ended September 30, 2016. As a result, $19,664 and $61,710 of debt issuance costs were recorded as a reduction of total debt at September 30, 2016 and September 30, 2015, respectively.

In March, 2016, the FASB issued ASU No. 2016-09, Compensation—Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. For public business entities, the amendments are effective for annual periods beginning after December 15, 2016, and interim periods within those annual periods. For all other entities, the amendments are effective for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018. Early adoption is permitted for any entity in any interim or annual period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period. An entity that elects early adoption must adopt all of the amendments in the same period.

In March, 2016, the FASB issued ASU No. 2016-06, Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments (a consensus of the Emerging Issues Task Force). For public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. For entities other than public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018. Early adoption is permitted, including adoption in an interim period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period.

In March, 2016, the FASB issued ASU No. 2016-07, Investments—Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting. Effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016. The amendments should be applied prospectively upon their effective date to increases in the level of ownership interest or degree of influence that result in the adoption of the equity method. Earlier application is permitted.