Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Marker Therapeutics, Inc. | v450946_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Marker Therapeutics, Inc. | v450946_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Marker Therapeutics, Inc. | v450946_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Marker Therapeutics, Inc. | v450946_ex31-1.htm |

| EX-3.1 - EXHIBIT 3.1 - Marker Therapeutics, Inc. | v450946_ex3-1.htm |

UNITED STATES SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C. 20549

FORM 10-Q

x Quarterly Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended September 30, 2016

¨ Transition Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from _____ to _____.

Commission File Number: 000-27239

| TAPIMMUNE INC. |

| (Name of registrant in its charter) |

| NEVADA | 45-4497941 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

|

50 N. Laura Street, Suite 2500 Jacksonville, FL |

32202 | |

| (Address of principal executive offices) | (Zip Code) | |

| 904-516-5436 | ||

| (Issuer's telephone number) |

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, non-accelerated filer or a smaller reporting company. See definition of “accelerated filer”, “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| ¨ Large accelerated filer | ¨ Accelerated filer |

| ¨ Non-accelerated filer (Do not check | x Smaller reporting company |

| if smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

As of November 2, 2016, the Company had 8,379,101 shares of common stock issued and outstanding.

NOTE REGARDING REVERSE STOCK SPLIT

On September 13, 2016, we filed a Certificate of Change pursuant to NRS 78.209 with the Secretary of State of the State of Nevada to effect a reverse split of our common stock at a ratio of one for twelve, effective on September 16, 2016. All historical share and per share amounts reflected in this report have been adjusted to reflect the reverse stock split.

CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

September 30, 2016 | December 31, 2015 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash | $ | 9,586,773 | $ | 6,576,564 | ||||

| Prepaid expenses and deposits | 111,652 | 68,803 | ||||||

| Total Assets | $ | 9,698,425 | $ | 6,645,367 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued liabilities | $ | 1,678,079 | $ | 967,358 | ||||

| Research agreement obligations | 492,365 | 492,365 | ||||||

| Derivative liability – warrants | 29,000 | 26,493,000 | ||||||

| Promissory note | 5,000 | 30,000 | ||||||

| Promissory note, related party | - | 23,000 | ||||||

| Total Liabilities | 2,204,444 | 28,005,723 | ||||||

| Commitments and Contingencies | - | - | ||||||

| Stockholders’ Equity (Deficit) | ||||||||

| Convertible preferred stock, $0.001 par value — 5,000,000 shares authorized: | ||||||||

| Series A, $0.001 par value, 1,250,000 shares designated, -0- shares issued and outstanding | - | - | ||||||

| Series B, $0.001 par value, 1,500,000 shares designated, -0- shares issued and outstanding | - | - | ||||||

| Common stock, $0.001 par value, 41,666,667 shares authorized, 8,395,768 and 5,882,976 shares issued and outstanding at September 30, 2016 and December 31, 2015, respectively | 8,396 | 5,884 | ||||||

| Additional paid-in capital | 151,724,573 | 112,142,187 | ||||||

| Accumulated deficit | (144,238,988 | ) | (133,508,427 | ) | ||||

| Total Stockholders’ Equity (Deficit) | 7,493,981 | (21,360,356 | ) | |||||

| Total Liabilities and Stockholders’ Equity (Deficit) | $ | 9,698,425 | $ | 6,645,367 | ||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| - 1 - |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

Three Months Ended September 30, | Nine months ended September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Operating Expenses: | ||||||||||||||||

| Research and development | $ | 1,109,332 | $ | 968,759 | $ | 3,343,248 | $ | 2,324,432 | ||||||||

| General and administrative | 1,612,305 | 769,219 | 3,557,701 | 1,579,754 | ||||||||||||

| Loss from Operations | (2,721,637 | ) | (1,737,978 | ) | (6,900,949 | ) | (3,904,186 | ) | ||||||||

| Other Income (Expense) | ||||||||||||||||

| Changes in fair value of derivative liabilities | 684,000 | 30,266,000 | 5,925,000 | (28,485,585 | ) | |||||||||||

| Foreign exchange gain | - | - | - | 775 | ||||||||||||

| Grant income | - | - | 231,200 | - | ||||||||||||

| Loss on debt settlement agreements | (65,325 | ) | (24,697 | ) | (135,640 | ) | (24,697 | ) | ||||||||

| Other income | - | - | 1,828 | - | ||||||||||||

| Net Income (Loss) | $ | (2,102,962 | ) | $ | 28,503,325 | $ | (878,561 | ) | $ | (32,413,693 | ) | |||||

| Basic Net Income (Loss) per Share | $ | (0.29 | ) | $ | 7.04 | $ | (0.14 | ) | $ | (10.61 | ) | |||||

| Diluted Net Income (Loss) per Share | $ | (0.29 | ) | $ | 4.23 | $ | (0.54 | ) | $ | (10.61 | ) | |||||

| Weighted Average Number of Common Shares Outstanding, Basic | 7,281,000 | 4,048,750 | 6,370,000 | 3,054,297 | ||||||||||||

| Weighted Average Number of Common Shares Outstanding, diluted | 7,281,000 | 6,745,416 | 6,935,000 | 3,054,297 | ||||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| - 2 - |

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY (DEFICIT)

(UNAUDITED)

| Common Stock | Additional | |||||||||||||||||||

Number of shares | Amount | Paid In Capital | Accumulated Deficit | Total | ||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||

| Balance, December 31, 2015 | 5,882,976 | 5,884 | 112,142,187 | (133,508,427 | ) | (21,360,356 | ) | |||||||||||||

| Issuance of common stock in private placement | 653,166 | 653 | 3,134,543 | - | 3,135,196 | |||||||||||||||

| Finders’ fee and legal costs relating to private placements | - | - | (804,070 | ) | - | (804,070 | ) | |||||||||||||

| Fair value of shares issued as inducement on August 10, 2016 | 750,000 | 750 | 4,499,250 | (4,500,000 | ) | - | ||||||||||||||

| Fair value of series F and F-1 warrants issued as inducement in August 2016 | - | - | 5,352,000 | (5,352,000 | ) | - | ||||||||||||||

| Reclassification of fair value of derivative liabilities to equity on amendment of warrant agreements | - | - | 15,465,000 | - | 15,465,000 | |||||||||||||||

| Exercise of warrants | 1,000,000 | 1,000 | 5,999,000 | - | 6,000,000 | |||||||||||||||

| Finders’ fee on exercise of warrants | - | - | (516,651 | ) | - | (516,651 | ) | |||||||||||||

| Reclassification of fair value of derivative liabilities at exercise date | - | - | 5,074,000 | - | 5,074,000 | |||||||||||||||

| Shares issued in debt settlement agreements | 10,191 | 10 | 70,305 | - | 70,315 | |||||||||||||||

| Stock- based compensation | 99,435 | 99 | 1,309,009 | - | 1,309,108 | |||||||||||||||

| Net loss | - | - | - | (878,561 | ) | (878,561 | ) | |||||||||||||

| Balance, September 30, 2016 | 8,395,768 | 8,396 | 151,724,573 | (144,238,988 | ) | 7,493,981 | ||||||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| - 3 - |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

Nine months ended September 30, 2016 | Nine months ended September 30, 2015 | |||||||

| Cash flow from operating activities | ||||||||

| Net loss | $ | (878,561 | ) | $ | (32,413,693 | ) | ||

| Adjustments to reconcile net loss to net cash from operating activities: | ||||||||

| Changes in fair value of derivative liabilities | (5,925,000 | ) | 28,485,585 | |||||

| Loss on debt settlement agreements | 70,315 | 24,697 | ||||||

| Stock based compensation | 1,309,109 | 261,805 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses | (42,849 | ) | (55,782 | ) | ||||

| Accounts payable and accrued liabilities | 710,720 | 204,956 | ||||||

| Net cash used in operating activities | (4,756,266 | ) | (3,492,432 | ) | ||||

| Cash flow from financing activities | ||||||||

| Private placements | 3,135,196 | 2,464,000 | ||||||

| Finders’ fee and legal costs on private placements | (804,070 | ) | (137,986 | ) | ||||

| Repayment of promissory note | (25,000 | ) | - | |||||

| Repayment of promissory note – related party | (23,000 | ) | - | |||||

| Proceeds from exercise of warrants | 6,000,000 | 7,427,998 | ||||||

| Finders’ fee on exercise of warrants | (516,651 | ) | (316,508 | ) | ||||

| Net cash provided by financing activities | 7,766,475 | 9,437,504 | ||||||

| Net increase in cash | 3,010,209 | 5,945,072 | ||||||

| Cash, beginning of period | 6,576,564 | 141,944 | ||||||

| Cash, end of period | $ | 9,586,773 | $ | 6,087,016 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Cash paid for interest | $ | - | $ | - | ||||

| Cash paid for taxes | $ | - | $ | - | ||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| - 4 - |

TAPIMMUNE INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Nine months ended September 30, 2016 | Nine Months Ended September 30, 2015 | |||||||

| Supplemental schedule of non-cash investing and financing activities: | ||||||||

| Reclassification of accrued liability upon issuance of common shares relating to Dr. Glynn Wilson’s compensation | $ | 191,000 | $ | - | ||||

| Accounts payable settled in common stock | - | 24,000 | ||||||

| Fair value of issuance of series F and F-1 warrants as inducement in August 2016 | 5,352,000 | - | ||||||

| Fair value of shares issued as inducement on August 10, 2016 | 4,500,000 | - | ||||||

| Reclassification of fair value of derivative liabilities to equity on amendment of warrant agreements | 15,465,000 | - | ||||||

| Fair value of issuance of warrants in January and March 2015 financing | - | 9,313,000 | ||||||

| Issuance of additional warrants in May 28, 2015 transaction | - | 6,133,000 | ||||||

| Reclassification of Derivative Warrant Liabilities to Equity at Exercise Date | 5,074,000 | 11,745,000 | ||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| - 5 - |

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2016

(Unaudited)

| Note 1: | Nature of Operations |

TapImmune Inc. (the “Company”), a Nevada corporation incorporated in 1992, is a biotechnology company focusing on immunotherapy specializing in the development of innovative peptide and gene-based immunotherapeutics and vaccines for the treatment of oncology and infectious disease. Unlike other vaccine technologies that narrowly address the initiation of an immune response, TapImmune's approach broadly stimulates the cellular immune system by enhancing the function of killer T-cells and T-helper cells and by restoring antigen presentation in tumor cells allowing their recognition and killing by the immune system.

| NOTE 2: | Basis of Presentation |

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and pursuant to the instructions to Form 10-Q and Article 8 of Regulation S-X of the Securities and Exchange Commission (“SEC”) and on the same basis as the Company prepares its annual audited consolidated financial statements. In the opinion of management, the accompanying unaudited condensed consolidated financial statements reflect all adjustments, consisting of normal recurring adjustments, considered necessary for a fair presentation of such interim results.

The results for the statement of operations are not necessarily indicative of results to be expected for the year ending December 31, 2016 or for any future interim period. The condensed consolidated balance sheet at December 31, 2015 has been derived from audited financial statements; however, it does not include all of the information and notes required by U.S. GAAP for complete financial statements. The accompanying condensed consolidated financial statements should be read in conjunction with the consolidated financial statements for the year ended December 31, 2015, and notes thereto included in the Company’s annual report on Form 10-K.

| NOTE 3: | LIQUIDITY AND FINANCIAL CONDITION |

The Company’s activities since inception have consisted principally of acquiring product and technology rights, raising capital, and performing research and development. Successful completion of the Company’s development programs and, ultimately, the attainment of profitable operations are dependent on future events, including, among other things, its ability to access potential markets; secure financing, develop a customer base; attract, retain and motivate qualified personnel; and develop strategic alliances. From inception, the Company has been funded by a combination of equity and debt financings.

The Company expects to continue to incur substantial losses over the next several years during its development phase. To fully execute its business plan, the Company will need to complete certain research and development activities and clinical studies. Further, the Company’s product candidates will require regulatory approval prior to commercialization. These activities may span many years and require substantial expenditures to complete and may ultimately be unsuccessful. Any delays in completing these activities could adversely impact the Company. The Company plans to meet its capital requirements primarily through issuances of debt and equity securities and, in the longer term, revenue from product sales.

As of September 30, 2016, the Company had cash and cash equivalents of approximately $9,587,000. Historically, the Company had net losses and negative cash flows from operations. Management intends to continue its research efforts and to finance operations of the Company through debt and/or equity financings. Management plans to seek additional debt and/or equity financing through private or public offerings or through a business combination or strategic partnership. There can be no assurance that the Company will be successful in obtaining additional financing on favorable terms, or at all. These matters raise substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might result from the outcome of these uncertainties.

| - 6 - |

| Note 4: | SIGNIFICANT ACCOUNTING POLICIES |

There have been no material changes in the Company’s significant accounting policies to those previously disclosed in the Company’s annual report on Form 10-K, which was filed with the SEC on April 14, 2016 other than the one disclosed below relating to grant income:

Grant Income

The Company recognizes grant income in accordance with the terms stipulated under the grant awarded to the Company’s collaborators at the Mayo Foundation from the U. S. Department of Defense. In various situations, the Company receives certain payments from the U.S. Department of Defense for reimbursement of clinical supplies. These payments are non-refundable, and are not dependent on the Company’s ongoing future performance. The Company has adopted a policy of recognizing these payments as grant income when received.

Recent Accounting Pronouncement

Accounting Standards Update (“ASU”), No. 2016-09 - In March 2016, the Financial Accounting Standards Board (the “FASB”) issued ASU No. 2016-09, Compensation-Stock Compensation. The areas for simplification in this update involve several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. Some of the specific changes associated with the update include all excess tax benefits and tax deficiencies (including tax benefits of dividends on share-based payment awards) being recognized as income tax expense or benefit in the income statement. The tax effects of exercised or vested awards should be treated as discrete items in the reporting period in which they occur. An entity also should recognize excess tax benefits regardless of whether the benefit reduces taxes payable in the current period. An entity can make an entity-wide accounting policy election to either estimate the number of awards that are expected to vest (current GAAP) or account for forfeitures when they occur. ASU 2016-09 is effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years.

The Company has evaluated the impact of ASU No. 2016-09 and has determined that the adoption of the impact of forfeitures, net of income taxes, will not have a material impact on the Company’s future financial statements.

| Note 5: | net income (loss) per share |

Basic income (loss) per common share is computed by dividing net income by the weighted average number of common shares outstanding during the reporting period. Diluted income per common share is computed similar to basic income per common share except that it reflects the potential dilution that could occur if dilutive securities or other obligations to issue common stock were exercised or converted into common stock.

Income (loss) per-share amounts for all periods have been retroactively adjusted to reflect the Company’s 1-for-12 reverse stock split, which was effective September 16, 2016.

The following table sets forth the computation of income (loss) per share:

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Net income (loss) | $ | (2,102,962 | ) | $ | 28,503,325 | $ | (878,561 | ) | $ | (32,413,693 | ) | |||||

| Less: Non cash income from changes in fair value of derivative liabilities | - | - | (2,856,000 | ) | - | |||||||||||

| Net income (loss) - diluted | (2,102,962 | ) | 28,503,325 | (3,734,561 | ) | (32,413,693 | ) | |||||||||

| Weighted average shares outstanding - basic | 7,281,000 | 4,048,750 | 6,370,000 | 3,054,297 | ||||||||||||

| Common stock warrants | - | 2,663,333 | 565,000 | - | ||||||||||||

| Common stock options | - | 33,333 | - | - | ||||||||||||

| Weighted average shares outstanding - diluted | 7,281,000 | 6,745,416 | 6,935,000 | 3,054,297 | ||||||||||||

| Net income (loss) per share data: | ||||||||||||||||

| Basic | $ | (0.29 | ) | $ | 7.04 | $ | (0.14 | ) | $ | (10.61 | ) | |||||

| Diluted | $ | (0.29 | ) | $ | 4.23 | $ | (0.54 | ) | $ | (10.61 | ) | |||||

| - 7 - |

The following securities, rounded to the thousand, were not included in the diluted net loss per share calculation because their effect was anti-dilutive for the periods presented:

| Nine Months Ended September 30, | ||||||||

| 2016 | 2015 | |||||||

| Common stock options | 432,000 | 39,000 | ||||||

| Common stock warrants - equity treatment | 5,054,000 | 211,000 | ||||||

| Common stock warrants - liability treatment | 6,000 | 4,750,000 | ||||||

| Potentially dilutive securities | 5,492,000 | 5,000,000 | ||||||

| Note 6: | DERIVATIVE LIABILITY - WARRANTs |

A summary of quantitative information with respect to valuation methodology and significant unobservable inputs used for the Company’s common stock purchase warrants that are categorized within Level 3 of the fair value hierarchy for the nine months ended 2016 and 2015 is as follows:

| Share Purchase Warrants | Weighted Average Inputs for the Period | |||||||

| Date of valuation | For the Nine Months Ending September 30, 2016 | For the Nine Months Ending September 30, 2015 | ||||||

| Exercise price | $ | 1.20 | $ | 7.56 | ||||

| Contractual term (years) | 1.3 | 4.5 | ||||||

| Volatility (annual) | 105 | % | 159 | % | ||||

| Risk-free rate | 1 | % | 1 | % | ||||

| Dividend yield (per share) | 0 | % | 0 | % | ||||

The foregoing assumptions are reviewed quarterly and are subject to change based primarily on management’s assessment of the probability of the events described occurring. Accordingly, changes to these assessments could materially affect the valuations.

Financial Assets and Liabilities Measured at Fair Value on a Recurring Basis

The fair value accounting standards define fair value as the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. As such, fair value is determined based upon assumptions that market participants would use in pricing an asset or liability. Fair value measurements are rated on a three-tier hierarchy as follows:

| · | Level 1 inputs: Quoted prices (unadjusted) for identical assets or liabilities in active markets; |

| · | Level 2 inputs: Inputs, other than quoted prices included in Level 1, that are observable either directly or indirectly; and |

| · | Level 3 inputs: Unobservable inputs for which there is little or no market data, which require the reporting entity to develop its own assumptions. |

| - 8 - |

Financial assets and liabilities measured at fair value on a recurring basis are summarized below and disclosed on the balance sheet under Derivative liability – warrants:

| As of September 30, 2016 | ||||||||||||||||||||

| Fair Value Measurements | ||||||||||||||||||||

| Fair Value | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||

| Derivative liability - warrants | $ | 29,000 | - | - | $ | 29,000 | $ | 29,000 | ||||||||||||

| Total | $ | 29,000 | - | - | $ | 29,000 | $ | 29,000 | ||||||||||||

| As of December 31, 2015 | ||||||||||||||||||||

| Fair Value Measurements | ||||||||||||||||||||

| Fair Value | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||

| Derivative liability - warrants | $ | 26,493,000 | - | - | $ | 26,493,000 | $ | 26,493,000 | ||||||||||||

| Total | $ | 26,493,000 | - | - | $ | 26,493,000 | $ | 26,493,000 | ||||||||||||

There were no transfers between Level 1, 2 or 3 during the nine months ended September 30, 2016.

The following table presents changes in Level 3 liabilities measured at fair value for the nine months ended September 30, 2016:

| Derivative liability – warrants | ||||

| Balance – December 31, 2015 | $ | 26,493,000 | ||

| Reclassification of derivative liabilities to equity at exercise date | (5,074,000 | ) | ||

| Reclassification of fair value of derivative liabilities to equity on amendment of warrant agreements | (15,465,000 | ) | ||

| Change in fair value of warrant liability | (5,925,000 | ) | ||

| Balance – September 30, 2016 | $ | 29,000 | ||

Warrant Amendment Transaction

On August 10, 2016, the Company and holders of an aggregate of 3,096,665 outstanding Series A Warrants, Series A-1 Warrants, Series C Warrants, Series C-1 Warrants, Series D Warrants, Series D-1 Warrants, Series E Warrants and Series E-1 Warrants entered into warrant amendment agreements (the “Amended Warrants”) in which they agreed to amend the terms of the outstanding series warrants to remove provisions that had previously precluded equity classification treatment on the Company’s balance sheets.

In consideration for such amendment and the exercise of the Series C Warrants and Series C-1 Warrants, the Company issued an aggregate of 750,000 additional shares of common stock to such warrant holders and new five-year warrants to purchase 1,000,000 shares of Company common stock at an exercise price of $7.20 per share. The value of the shares and fair value of the warrants was treated as dividend on the statement of stockholders’ equity of $4.5 million.

The fair value of the Amended Warrants was re-measured immediately prior to the date of amendment with changes in fair value recorded as a gain of $556,000 in the statement of operations and $15.5 million was reclassified to equity.

| - 9 - |

| Note 7: | STOCK-BASED COMPENSATION |

The following table summarizes the components of stock-based compensation expense in the condensed consolidated statements of operations for the three and nine months ended September 30, 2016 and 2015, respectively:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Research and development | $ | - | $ | - | $ | - | $ | - | ||||||||

| General and administrative | 573,137 | 13,244 | 1,309,109 | 261,805 | ||||||||||||

| Total stock-based compensation | $ | 573,137 | $ | 13,244 | $ | 1,309,109 | $ | 261,805 | ||||||||

Stock Options

A summary of the Company’s stock option activity is as follows:

| Stock Options | Weighted Average Exercise Price per Share | Weighted Average Remaining Contractual Life | Aggregate Intrinsic Value | |||||||||||||

| Outstanding as of December 31, 2015 | 298,679 | $ | 9.25 | 9.75 | $ | 177,000 | ||||||||||

| Granted | 135,000 | 6.00 | ||||||||||||||

| Exercised | - | - | ||||||||||||||

| Forfeited/Cancelled | (1,667 | ) | 228.00 | |||||||||||||

| Outstanding as of September 30, 2016 | 432,013 | $ | 7.25 | 9.25 | $ | 271,000 | ||||||||||

| Exercisable as of September 30, 2016 | 262,395 | $ | 8.00 | 9.00 | $ | 174,000 | ||||||||||

Total stock-based compensation cost related to unvested awards not yet recognized and the weighted average periods over which the awards are expected to be recognized as of September 30, 2016 are as follows:

| Unrecognized stock-based compensation cost: | $ | 1,081,000 | ||

| Expected weighted average period compensation costs to be recognized (years): | 1.75 |

| Note 8: | Promissory note |

At September 30, 2016, the Company had an outstanding promissory note in the amount of $5,000 as compared to two outstanding promissory notes totaling $30,000 at December 31, 2015. The promissory note outstanding at September 30, 2016 bears 10% annual interest.

During the nine months ended September 30, 2016, the Company paid a $25,000 promissory note and $6,524 of accrued interest in final settlement.

| Note 9: | Promissory note, related party |

At December 31, 2015, the Company had an outstanding promissory note in the amount of $23,000 owed to an officer of the Company. The promissory note bore no interest charges and had no fixed repayment terms. In September 2016, the note was paid in full.

| - 10 - |

| Note 10: | Capital Stock |

Reverse Stock Split

Effective September 16, 2016, the Company effected a one for twelve reverse stock-split of our issued and outstanding common stock and has retroactively adjusted our common shares outstanding, options and warrants amounts outstanding. The Company has presented its share data for and as of all periods presented on this basis. The par value was not adjusted as a result of the one for twelve reverse stock split. All prior period share transactions included in the Company’s stock transactions and balances have been retroactively restated.

2016 Common Stock Transactions

Private placements

On August 10, 2016 and August 25, 2016, the Company completed private placements of units with certain accredited investors. The units consisted of (i) one share of the Company’s common stock, par value $0.001 per share and (ii) one five-year warrant to purchase one share of Company common stock for $6.00. The Company issued and sold an aggregate of 653,166 units at a purchase price per unit of $4.80 for an aggregate of approximately $3.1 million. The Company incurred approximately $0.8 million in agency fees and legal costs.

In addition, the Company issued five-year warrants to the placement agent in the offering providing for the purchase of up to 65,317 shares of Company common stock for $4.80 per share.

Pursuant to the registration rights agreements entered into in connection with the private placements, the Company is required to file a registration statement with the Securities and Exchange Commission registering for resale (a) the common stock issued in the private placement offering; (b) the shares of common stock issuable upon the exercise of the five-year warrants; and (c) the shares of common stock issuable upon the exercise of the warrants issued to the placement agent. The Company is required to file the registration statement within 120 days of the August 10, 2016 closing or by December 8, 2016. The Company is also required to ensure that the registration statement is declared effective within 90 calendar days after filing with the Securities and Exchange Commission, or by March 8, 2017.

In accordance with the registration rights agreements, should the Company fail to meet the above criteria, the Company is subject to pay the investors liquidated damages. The liquidated damages shall be a cash sum payment calculated at a rate of ten percent (10%) per annum of the aggregate purchase price for the registrable securities or aggregate amount upon exercise of the placement agent warrants.

In accordance with applicable U.S. generally accepted accounting principles, a contingent obligation to make future payments must be recorded if the transfer of consideration under a registration payment arrangement is probable and can be reasonably estimated. The Company has determined that should it be required to pay liquidated damages to the investors of the private placements, the aggregate contingent liability it would be required to record would be approximately $29,000 per month for each month it fails or is estimated to fail to meet the above criteria.

At the August 10, 2016 and August 26,2016 private placement closings, and on September 30, 2016, the Company concluded that it is not probable that it will be required to remit any payments to the investors for failing to obtain an effective registration statement or failing to maintain its effectiveness.

Warrant Amendment Transaction

On August 10, 2016, the Company and holders of an aggregate of 3,096,665 outstanding Series A Warrants, Series A-1 Warrants, Series C Warrants, Series C-1 Warrants, Series D Warrants, Series D-1 Warrants, Series E Warrants and Series E-1 Warrants entered into warrant amendment agreements (the “Amended Warrants”) in which they agreed to amend the terms of the outstanding series warrants to remove provisions that had previously precluded equity classification treatment on the Company’s balance sheets.

In consideration for such amendment and the exercise of the Series C Warrants and Series C-1 Warrants, the Company issued an aggregate of 750,000 additional shares of common stock to such warrant holders and new five-year warrants to purchase 1,000,000 shares of Company common stock at an exercise price of $7.20 per share. The value of the shares and fair value of the warrants was treated as dividend on the statement of stockholders’ equity of $4.5 million.

| - 11 - |

Share Purchase Warrants

A summary of the Company’s share purchase warrants as of September 30, 2016 and changes during the period is presented below:

| Number of Warrants | Weighted Average Exercise Price | |||||||

| Balance, December 31, 2015 | 4,343,000 | $ | 8.67 | |||||

| Exercised | (1,000,000 | ) | 6.00 | |||||

| Issued | 1,718,000 | 6.65 | ||||||

| Expired | (2,000 | ) | 300 | |||||

| Balance, September 30, 2016 | 5,059,000 | $ | 8.51 | |||||

Consulting Arrangements

During the nine months ended September 30, 2016, the Company issued 60,000 common shares as part of consulting agreements. The fair value of the common stock of approximately $414,000 was recognized as stock-based compensation in general and administrative expense.

Debt Settlement

In May 2016, the Company issued 10,191 common shares as part of debt conversion agreements from 2014. The fair value of the common stock of approximately $70,000 was recognized as loss on debt settlement agreements in other income (expense).

In September 2016, the Company paid $27,000 for a promissory note from 2008 and related $38,000 of accrued interest. The $65,000 payment was recognized as loss on debt settlement agreements in other income (expense).

| Note 11: | grant income |

During the nine months ended September 30, 2016, the Company received approximately $231,000 of grant awarded to Mayo Foundation from the U.S. Department of Defense for the Phase II Clinical Trial of TPIV 200. The grant paid for the clinical supplies purchased by the Company.

| Note 12: | COMMITMENTs |

Employment Agreements

In November 2015, the Company entered into an employment agreement with Dr. Glynn Wilson, the Company’s Chief Executive Officer, President and Chairman of the Company. As part of the agreement, Dr. Wilson was awarded 19,018 fully vested common shares in March 2016. The fair value of the common stock of approximately $146,000 was recognized as stock-based compensation in general and administrative expense.

In July, 2016, the Company entered into an employment agreement with Dr. John Bonfiglio relating to his appointment as the Company’s President and Chief Operating Officer. As part of the agreement, Dr. Bonfiglio was awarded 20,833 common shares, which will vest upon the earlier of (i) the listing of the Company’s common stock on a national securities exchange in the United States or (ii) the first anniversary of the employment agreement, so long as Dr. Bonfiglio is employed with the Company. The fair value of the common stock of approximately $103,000 was recognized as stock-based compensation in general and administrative expense.

In August 2016, the Company appointed Michael Loiacono as the Company’s Chief Financial Officer, Chief Accounting Officer, Secretary and Treasurer. In connection with Mr. Loiacono’s appointment he entered into an employment agreement with the Company. The employment agreement provides that Mr. Loiacono’s base salary will be $200,000 per year and he is eligible for an annual performance bonus of up to 50% of his base salary. The term of the employment agreement is for two years and will be automatically extended for an additional 12 months unless terminated by Mr. Loiacono or the Company.

| - 12 - |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This quarterly report on Form 10-Q contains forward-looking statements within the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended, that involve risks and uncertainties. All statements other than statements relating to historical matters including statements to the effect that we “believe”, “expect”, “anticipate”, “plan”, “target”, “intend” and similar expressions should be considered forward-looking statements. Our actual results could differ materially from those discussed in the forward-looking statements as a result of a number of important factors, including factors discussed in this section and elsewhere in this quarterly report on Form 10-Q, and the risks discussed in our other filings with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis, judgment, belief or expectation only as the date hereof. We assume no obligation to update these forward-looking statements to reflect events or circumstance that arise after the date hereof.

As used in this quarterly report: (i) the terms “we”, “us”, “our”, “TapImmune” and the “Company” mean TapImmune Inc. and its wholly owned subsidiary, GeneMax Pharmaceuticals Inc. which wholly owns GeneMax Pharmaceuticals Canada Inc., unless the context otherwise requires; (ii) “SEC” refers to the Securities and Exchange Commission; (iii) “Securities Act” refers to the Securities Act of 1933, as amended; (iv) “Exchange Act” refers to the Securities Exchange Act of 1934, as amended; and (v) all dollar amounts refer to United States dollars unless otherwise indicated.

The following should be read in conjunction with our unaudited consolidated interim financial statements and related notes for the three and nine months ended September 30, 2016 included in this quarterly report, as well as our Annual Report on Form 10-K for the year ended December 31, 2015.

Company Overview

Our Cancer Vaccines

We are a clinical-stage immuno-oncology company specializing in the development of innovative peptide and gene-based immunotherapeutics and vaccines for the treatment of cancer & metastatic disease. We are also developing a proprietary technology to improve the ability of the cellular immune system to recognize and destroy diseased cells. This DNA expression technology named Polystart is in preclinical development.

To enhance shareholder value and taking into account development timelines, we plan to focus on advancing our clinical programs including our Folate Receptor Alpha program for breast and ovarian cancer and our HER2/neu peptide antigen program into Phase II clinical trials. In parallel, we plan to complete the preclinical development of our Polystart technology as an integral component of our prime-and-boost vaccine methodology.

The Immunotherapy Industry for Cancer

Immuno-oncology has become the most rapidly growing sector in the pharmaceutical and biotech industry. The approval and success of checkpoint inhibitors Yervoy and Opdivo (Bristol Myers Squibb) and Keytruda (Merck & Co.) together with the development of CAR T-cell therapies (Juno Therapeutics, Kite Pharma) has provided much momentum in this sector. In addition, new evidence points to the increasing use of combination immunotherapies for the treatment of cancer. This has provided greater opportunities for the successful development of T-cell vaccines in combination with other approaches.

Products and Technology in Development-Clinical

Phase I Human Clinical Trials – Folate Alpha Breast and Ovarian Cancer – Mayo Clinic

Folate Receptor Alpha is expressed in over 80% of triple negative breast cancers and in addition, over 90% of ovarian cancers, for which the only treatment options are surgery, radiation and chemotherapy, leaving a very important and urgent clinical need for a new therapeutic. Time to recurrence is relatively short for these types of cancer and survival prognosis is extremely poor after recurrence. In the United States alone, there are approximately 30,000 ovarian cancer patients and 40,000 triple negative breast cancer patients newly diagnosed every year.

| - 13 - |

TPIV 200 Folate Receptor Alpha

A 24 patient Phase I clinical trial has been completed. The vaccine is well tolerated and safe and 20 out of 21 evaluable patients showed positive immune responses providing a strong rationale rational for progressing to phase II trials. GMP manufacturing for Phase II trials is progressing well towards a commercial formulation and final analyses of clinical plans are near completion. On July 27, 2015, TapImmune exercised its option agreement with Mayo Clinic with the signing of a worldwide exclusive license agreement to commercialize a proprietary folate receptor alpha vaccine technology for all cancer indications. As part of this Agreement, the IND for the folate receptor alpha Phase I trial was transferred from Mayo to TapImmune for amendment for the Company’s Phase II Clinical Trials on our lead product.

On September 15, 2015, we announced that our collaborators at the Mayo Clinic had been awarded a grant of $13.3 million from the U.S. Department of Defense. This grant, commencing September 15, 2015, will cover the costs for a 280 patient Phase II Clinical Trial of Folate Receptor Alpha Vaccine in patients with Triple Negative Breast Cancer. TapImmune will work closely with Mayo Clinic on this clinical trial by providing clinical and manufacturing expertise as well as providing GMP vaccine formulations. These vaccine formulations are being developed for multiple Phase II clinical programs in triple negative breast and ovarian cancer in combination with other immunotherapeutics.

On December 9, 2015, we announced that we received Orphan Drug Designation from the U.S. Food & Drug Administration’s Office of Orphan Products Development (OOPD) for our cancer vaccine TPIV 200 in the treatment of ovarian cancer. The TPIV 200 ovarian cancer clinical program will now receive benefits including tax credits on clinical research and 7-year market exclusivity upon receiving marketing approval. TPIV 200 is a multi-epitope peptide vaccine that targets Folate Receptor Alpha which is overexpressed in multiple cancers.

On February 3, 2016 we announced that the U.S. Food & Drug Administration (FDA) has designated the investigation of multiple-epitope Folate Receptor Alpha Peptide Vaccine (TPIV 200) with GM-CSF adjuvant for maintenance therapy in subjects with platinum-sensitive advanced ovarian cancer who achieved stable disease or partial response following completion of standard of care chemotherapy, as a Fast Track Development Program. A Phase 2 study in this indication is being readied for initiation by the end of 2016.

We are currently enrolling a Company sponsored triple negative breast cancer study at 8 clinical sites nation-wide. The study will enroll 80 patients. It is open-label and designed to look at dosing regimens, immune responses and efficacy.

The Company also announced the start of an ovarian cancer study sponsored by Memorial Sloan Kettering Cancer Center in New York City in collaboration with Astra Zeneca Pharmaceuticals. This study is currently enrolling platinum resistant ovarian cancer patients and is designed to look at the effects of combination therapy with Astra Zeneca’s checkpoint inhibitor durvalamab. The study will enroll 40 patients and is open label. Although we have no business relationship with Astra Zeneca, we are paying for half of the clinical study plus providing our TPIV 200 for the study.

Phase I Human Clinical Trials – HER2/neu+ Breast Cancer – Mayo Clinic

Patient dosing has been completed. Final safety analysis on all the patients treated is complete and shown to be safe. In addition, 19 out of 20 evaluable patients showed robust T-cell immune responses to the antigens in the vaccine composition providing a solid case for advancement to Phase II in 2015. An additional secondary endpoint incorporated into this Phase I Trial will be a two year follow on recording time to disease recurrence in the participating breast cancer patients.

For Phase I(b)/II studies, we plan to add a Class I peptide, licensed from the Mayo Clinic (April 16, 2012), to the four Class II peptides. Management believes that the combination of Class I and Class II HER2/neu antigens, gives us the leading HER2/neu vaccine platform. As the folate receptor alpha vaccine is our lead product our plans are now initiating formulation studies to progress the HER2/neu vaccine towards a Phase II Clinical Trial in 2017.

Products and Technology-Preclinical

Polystart

We converted the previously filed U.S. Provisional Patent Application on Polystart into a full Patent Application, and in February 2016 we received a Notice of Allowance from the U.S. Patent and Trademark Office (USPTO) for a patent application entitled, “A chimeric nucleic acid molecule with non-AUG initiation sequences.” The term of this patent extends to March 17, 2034. Additional patent filings are in progress. We plan to develop PolyStart as both a stand-alone therapy and as a ‘boost strategy’ to be used synergistically with our peptide-based vaccines for breast and ovarian cancer.

| - 14 - |

Current State of the Company

We are a clinical-stage immunotherapy company specializing in the development of innovative peptide and gene-based immunotherapeutics and vaccines for the treatment of cancer. We now plan to conduct multiple Phase II clinical trials on our vaccines. The largest of these studies in triple-negative breast cancer is totally funded by a $13.3 million grant from the U.S. Department of Defense to our collaborators at the Mayo Clinic in Jacksonville, Florida. A Company-sponsored trial in triple negative breast cancer started during the second quarter of 2016 with recruitment at multiple sites and treatment of first patients. We believe that our development pipeline is strong and provides us the opportunity to continue to expand on collaborations with leading institutions and corporations.

We believe, the strength of our science and development approaches is becoming more widely appreciated, particularly as our clinical program has now generated positive interim data on both clinical programs in Breast and Ovarian Cancer.

We continue to be focused on our entry into Phase II Triple Negative Cancer Trials including application for Fast Track & Orphan Drug Status as well as planning for Phase II HER2/neu Breast Cancer Trials.

We expect to continue to prosecute our PolyStart patent filings and develop new constructs to facilitate collaborative efforts in our current clinical indications and those where others have already indicated interest in combination therapies.

We believe that these fundamental programs and corporate activities have positioned TapImmune to capitalize on the acceptance of immunotherapy as a leading therapeutic strategy in cancer and infectious disease.

TapImmune’s Pipeline

Clinical Program

We have a pipeline of potential immunotherapies under development. Phase I clinical programs on HER2/neu for breast and ovarian cancer have been completed and strong immune responses in over 90% of patients treated has provided the rationale and catalyst to advance these programs to Phase II clinical trials.

| - 15 - |

In addition to the exciting clinical developments, our peptide vaccine technology may be coupled with our recently developed in-house Polystart nucleic acid-based technology designed to make vaccines significantly more effective by producing four times the required peptides for the immune systems to recognize and act on. Our nucleic acid-based systems can also incorporate “TAP” which stands for Transporter associated with Antigen Presentation.

A key component to success is having a comprehensive patent strategy that continually updates and extends patent coverage for key products. It is highly unlikely that early patents will extend through ultimate product marketing, so extending patent life is an important strategy for ensuring product protection.

We have three active patent families that we are supporting:

1. Filed patents on PolyStart expression vector (owned by TapImmune and filed in 2014: this IP covers the use with TAP). The Company announced the allowance of this patent in February 2016.

2. Filed patents on HER2/neu Class II and Class I antigens: exclusive license from Mayo Foundation; and

3. Filed patents on Folate Receptor Alpha antigens: exclusive license from Mayo Foundation

While the pathway to successful product development takes time, we believe we have put in place significant for success. The strength of our product pipeline and access to leading scientists and institutions gives us a unique opportunity to make a major contribution to global health care.

With respect to the broader market, a major driver and positive influence on our activities has been the emergence and general acceptance of the potential of a new generation of immunotherapies that promise to change the standard of care for cancer. The immunotherapy sector has been greatly stimulated by the approval of Provenge® for prostate cancer and Yervoy™ for metastatic melanoma, progression of the areas of checkpoint inhibitors and adoptive T-cell therapy and multiple approaches reaching Phase II and Phase III status.

We believe that through our combination of technologies, we are well positioned to be a leading player in this emerging market. It is important to note that many of the late stage immunotherapies currently in development do not represent competition to our programs, but instead offer synergistic opportunities to partner our antigen based immunotherapeutics, and Polystart expression system. Thus, the use of naturally processed T-cell antigens discovered using samples derived from cancer patients plus our Polystart expression technology to improve antigen presentation to T-cells could not only produce an effective cancer vaccine in its own right but also to enhance the efficacy of other immunotherapy approaches such as CAR-T and PD1 inhibitors for example.

Recent Developments and Company Highlights

Research Programs

Her2neu License Agreement

On June 7, 2016 we announced that we exercised our option agreement with Mayo Clinic and signed a worldwide license agreement to a proprietary HER2neu vaccine technology. The license gives us the right to develop and commercialize the technology in any cancer indication in which the Her2neu antigen is overexpressed.

Phase II Trials Started

On April 26, 2016 we announced plans to participate in a Phase 2 trial of our cancer vaccine, TPIV 200, a multi-epitope anti-folate receptor vaccine (FRα), in combination with durvalumab (MEDI4736), an anti-PD-L1 antibody, in patients with platinum-resistant ovarian cancer. The study started with the enrollment and treatment of patients in the second quarter of 2016 at Memorial Sloan Kettering Cancer Center in New York and is being led by Jason Konner, M.D. as Principal Investigator. On June 21, 2016, we announced the treatment of the first patient in a company-sponsored Phase II trial in triple negative breast cancer as part of a multi-center study.

Manufacturing

On April 7, 2016, we announced that we have successfully completed formulation development, scale-up, GMP (Good Manufacturing Practice) manufacturing, and the release of TPIV 200, our multi-epitope folate receptor peptide vaccine for breast and ovarian cancer. The manufactured product contains five peptide antigens freeze dried in a single vial, ready for injection after reconstitution and addition of granulocyte-macrophage colony-stimulating factor (GM-CSF). TPIV 200 doses are now available for the upcoming Phase II clinical trials in both triple negative breast cancer and ovarian cancer.

| - 16 - |

Recent Developments

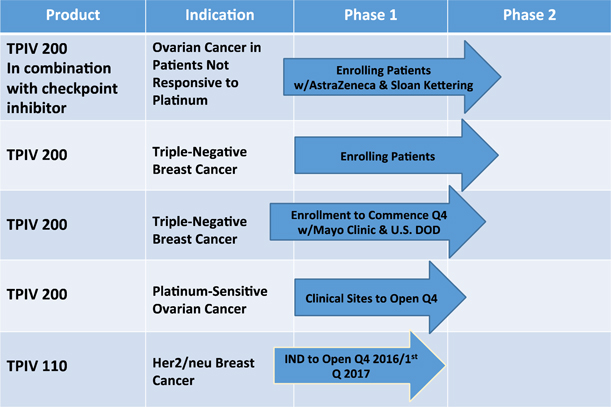

Enrolling Patients: Phase 2 TPIV 200 Trial in Triple Negative Breast Cancer

We have opened 8 clinical sites and begun treating patients in a Phase 2 trial of our Folate Receptor Alpha cancer vaccine, TPIV 200, in the treatment of triple negative breast cancer, one of the most difficult to treat cancers representing a clear unmet medical need. The open-label, 80 patient clinical trial is designed to evaluate dosing regimens, adjuvants, efficacy, and immune responses in women with triple negative breast cancer. Key data from the trial is expected to be included in a future New Drug Application submission to the FDA for marketing clearance. This trial is sponsored and conducted by TapImmune.

Enrolling Patients: Phase 2 Trial at Memorial Sloan Kettering of TPIV 200 in Ovarian Cancer

A Phase 2 study of TPIV 200 in ovarian cancer patients who are not responsive to platinum, a commonly used chemotherapy for ovarian cancer, sponsored by Memorial Sloan Kettering Cancer Center, and in collaboration with AstraZeneca and TapImmune, has begun enrollment for a 40 patient study. The open-label study is designed to evaluate a combination therapy which includes our TPIV 200 T-cell vaccine and AstraZeneca’s checkpoint inhibitor, durvalumab. Because they are unresponsive to platinum, these patients have no real options left. If the combination therapy proves effective, we believe it would address a critical unmet need. TPIV 200 has received Orphan Drug designation for use in the treatment of ovarian cancer.

Enrollment to Commence in Q4 2016: Phase 2 Mayo Clinic-U.S. DOD Trial of TPIV 200 in Triple Negative Breast Cancer We anticipate this Phase 2 study of TPIV 200 in the treatment of triple negative breast cancer, conducted by the Mayo Clinic and sponsored by the U.S. Department of Defense (DOD), will begin to enroll patients in the fourth quarter of this year. The anticipated 280 patient study will be led by Dr. Keith Knutson of the Mayo Clinic in Jacksonville, Florida. Dr. Knutson is the inventor of the technology and an advisor to TapImmune. While TapImmune is supplying doses of TPIV 200 for the trial, the remaining costs associated with conducting this study will be funded by a $13.3 million grant made by the DOD to the Mayo Clinic.

Clinical Sites to Open in Q4 2016: Phase 2 TPIV 200 Trial in Platinum-Sensitive Ovarian Cancer

By the end of 2016, we expect to have at least one clinical site open in a Phase 2 trial of TPIV 200 in 80 ovarian cancer patients who are responsive to platinum. We have received the FDA’s Fast Track designation to develop TPIV 200 as a maintenance therapy in combination with platinum, in platinum responsive ovarian cancer. This multi-center, double-blind efficacy study is sponsored and conducted by TapImmune.

Open IND with FDA for TPIV 110 in Q4 2016 or in Q1 2017: Phase 2 Protocol Now in Preparation

We have reformulated our second cancer vaccine product, TPIV 110, following very strong safety and immune responses from a Phase 1 Mayo Clinic study. TPIV 110 targets Her2/neu, which makes it applicable to breast, ovarian and colorectal cancer. The reformulated product adds a fifth antigen which should produce an even more robust immune response activating both CD4+ and CD8+ T-cells. We have requested a pre-Investigational New Drug (IND) meeting with the FDA and submitted questions to the FDA related to opening the IND. A response from the FDA is expected in September and we anticipate having an open IND by year-end pending comments from FDA. The protocol for a Phase 2 trial of TPIV 110 in the treatment of Her2/neu positive breast cancer patients has been designed and is now being reviewed by our Scientific Advisory Board and collaborators.

TPIV Products are Off-the-Shelf, Commercially Viable, with Excellent Potential Margins

We are continuously working on improving our product formulation and supply. We believe TPIV 200 and TPIV 110 are both very stable, off-the-shelf, lyophilized products that only require reconstitution at the clinical site before injection. We believe the investments we have made in the formulation work we have performed will result in a commercially viable product with excellent potential profit margins.

Robust Product Data & Independent Vetting Key to High-Value Collaborations

We believe the Phase 1 data produced for both TPIV 200 and TPIV 100 in collaboration with the Mayo Clinic are the driving force behind the high-value collaborations we have been able to maintain and establish with organizations including Mayo Clinic, AstraZeneca, Sloan Kettering, and the U.S. Department of Defense. As we move forward into advancing the Phase 2 studies, some of which are represent collaboration with prestigious third party organizations, we believe this represents further independent vetting of potential of our technology.

| - 17 - |

Company Highlights

Reverse Stock Split

On September 16, 2016, at the opening of trading, we effected a one-for-twelve reverse split of our common shares. The common shares began trading on a split-adjusted basis on September 16, 2016. The reverse stock split was effected in connection with the Company’s intent to apply to list the common stock on the NASDAQ Capital Market. On November 2, 2016, we received notification that we were approved for listing on The Nasdaq Capital Market. Our common stock is expected to begin trading on The Nasdaq Capital Market at the opening of trading on Tuesday, November 8, 2016 under the ticker symbol, TPIV.

Our historical financial results have been adjusted to reflect a reduction in the number of shares of our outstanding common stock from 62,890,763 shares to 5,240,897 shares at September 30, 2015 and from 70,550,763 shares to 5,879,230 shares at December 31, 2015. In addition, effective upon the reverse stock split, the number of authorized shares of our common stock was reduced from 500 million shares to 41,666,667 shares. All fractional shares resulting from the reverse stock split were rounded up to the nearest whole share. All share data herein has been retroactively adjusted for the reverse stock split. The par value was not adjusted as a result of the one for twelve reverse stock split.

August 2016 Private Placement Transaction

On August 10, 2016 and August 25, 2016, the Company completed private placements of units with certain accredited investors. The units consisted of (i) one share of the Company’s common stock, par value $0.001 per share and (ii) one five-year warrant to purchase one share of Company common stock for $6.00. The Company issued and sold an aggregate of 653,166 units at a purchase price per unit of $4.80 for an aggregate of approximately $3.1 million. The Company incurred approximately $0.8 million in agency fees and legal costs.

In addition, the Company issued five-year warrants to the placement agent in the offering providing for the purchase of up to 65,317 shares of Company common stock for $4.80 per share.

Pursuant to the registration rights agreements entered into in connection with the private placements, the Company is required to file a registration statement with the Securities and Exchange Commission registering for resale (a) the common stock issued in the private placement offering; (b) the shares of common stock issuable upon the exercise of the five-year warrants; and (c) the shares of common stock issuable upon the exercise of the warrants issued to the placement agent. The Company is required to file the registration statement within 120 days of the August 10, 2016 closing or by December 8, 2016. The Company is also required to ensure that the registration statement is declared effective within 90 calendar days after filing with the Securities and Exchange Commission, or by March 8, 2017.

In accordance with the registration rights agreements, should the Company fail to meet the above criteria, the Company is subject to pay the investors liquidated damages. The liquidated damages shall be a cash sum payment calculated at a rate of ten percent (10%) per annum of the aggregate purchase price for the registrable securities or aggregate amount upon exercise of the placement agent warrants.

In accordance with applicable U.S. generally accepted accounting principles, a contingent obligation to make future payments must be recorded if the transfer of consideration under a registration payment arrangement is probable and can be reasonably estimated. The Company has determined that should it be required to pay liquidated damages to the investors of the private placements, the aggregate contingent liability it would be required to record would be approximately $29,000 per month for each month it fails or is estimated to fail to meet the above criteria.

At the August 10, 2016 and August 26,2016 private placement closings, and on September 30, 2016, the Company concluded that it is not probable that it will be required to remit any payments to the investors for failing to obtain an effective registration statement or failing to maintain its effectiveness.

August 2016 Warrant Exercises

On August 11, 2016, holders of an aggregate of 583,333 outstanding Series C Warrants and 416,667 Series C-1 Warrants, each providing for the purchase of one share of our common stock for $6.00 per share, exercised their warrants for an aggregate exercise price of $6,000,000.

August 2016 Warrant Amendments

Simultaneous with the exercise of the warrants, we and holders of an aggregate of 3,096,665 outstanding Series A Warrants, Series A-1 Warrants, Series C Warrants, Series C-1 Warrants, Series D Warrants, Series D-1 Warrants, Series E Warrants and Series E-1 Warrants (the “Outstanding Series Warrants”) entered into Warrant Amendment Agreements (the “Amendment Agreement”), in which they agreed to amend the terms of the Outstanding Series Warrants to remove provisions from the Outstanding Series Warrants that had previously caused them to be classified as a derivative liability as opposed to equity on our balance sheet. In consideration for such amendment and the exercise of the Series C Warrants and Series C-1 Warrants, we issued an aggregate of 750,000 additional shares of common stock to such warrant holders and new five-year warrants to purchase 1 million shares of our common stock at an exercise price of $7.20 per share (the “Series F and F-1Warrants”).

| - 18 - |

The following table reflects the status of the outstanding warrants from the January 2015, March 2015, and August 2016 private placement financings (including placement agent warrants) following the Amendment Agreement and private placement:

| Series | Outstanding Warrants | Exercise Price | Expiration | |||||||

| A | 214,433 | $ | 1.20 | 01/13/2020 | ||||||

| C | 424,433 | $ | 6.00 | 01/13/2020 | ||||||

| D | 610,000 | $ | 9.00 | Between 07/16/2020 and 08/13/2020 and 08/19/2020 and 09/09/2020 | ||||||

| E | 616,100 | $ | 15.00 | Between 10/01/2020 and 11/12/2020 and 11/30/2020 and 12/09/2020 | ||||||

| A-1 | 418,750 | $ | 1.20 | 03/09/2020 | ||||||

| C-1 | 2,083 | $ | 6.00 | 01/13/2020 | ||||||

| D-1 | 416,667 | $ | 9.00 | Between 08/19/2020 and 09/09/2020 | ||||||

| E-1 | 418,750 | $ | 15.00 | 06/16/2020 | ||||||

| F | 583,333 | $ | 7.20 | 8/11/2021 | ||||||

| F-1 | 416,667 | $ | 7.20 | 8/11/2021 | ||||||

| PIPE Warrants | 653,166 | $ | 6.00 | 8/11/2021 | ||||||

| Broker Warrants | 65,317 | $ | 4.80 | 8/11/2021 | ||||||

Addition of Executive Officers

On July 18, 2016 we announced that Dr. John Bonfiglio, a consultant and a member of our Board of Directors, was appointed as our President and Chief Operating Officer and entered into an employment agreement with us. Concurrent with such appointment we amended the employment agreement of Dr. Wilson for Dr. Wilson to relinquish the office of President.

On August 25, 2016 we announced that Michael J. Loiacono, a consultant, was appointed as our Chief Financial Officer, Chief Accounting Officer, Secretary and Treasurer and entered into an employment agreement with us.

Critical Accounting Policies

The condensed consolidated financial statements are prepared in conformity with U.S. GAAP, which require the use of estimates, judgments and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of expenses in the periods presented. We believe that the accounting estimates employed are appropriate and resulting balances are reasonable; however, due to inherent uncertainties in making estimates, actual results could differ from the original estimates, requiring adjustments to these balances in future periods. The critical accounting estimates that affect the consolidated financial statements and the judgments and assumptions used are consistent with those described under Part II, Item 7 of our Annual Report on Form 10-K for the year ended December 31, 2015.

| - 19 - |

Results of Operations

In this discussion of the Company’s results of operations and financial condition, amounts, other than per-share amounts, have been rounded to the nearest thousand dollars.

Three Months Ended September 30, 2016 Compared to Three Months Ended September 30, 2015

We recorded a net loss of $2,103,000 or ($0.29) basic and diluted per share during the three months ended September 30, 2016 compared to a net income of $28,503,000 or $7.04 basic and $4.23 diluted per share during the three months ended September 30, 2015.

Operating costs increased to $2,722,000 during the three months ended September 30, 2016 compared to $1,738,000 in the prior period. Significant changes in operating expenses are outlined as follows:

| · | Research and development costs during the three months ended September 30, 2016 were $1,109,000 compared to $969,000 during the prior period. The increase was primarily due to the Company expensing the Mayo Foundation license fee payments in the current period and higher expenses relating to research. |

| · | General and administrative expenses increased to $1,612,000 during the three months ended September 30, 2016 from $769,000 during the prior period. This was due to generally increased expenses relating to consulting, general and administrative and professional fees during the three months ended September 30, 2016 due to increased activity in operations. |

| · | The changes in fair value of derivative liabilities for the three months ended September 30, 2016 was $684,000 as compared to $30,266,000 for the three months ended September 30, 2015. The variance is due to the revaluation of the Series A and A-1, Series C and C-1, Series D and D-1 and Series E and E-1 warrants issued by us in January and March 2015. We revalue the derivative liabilities at each balance sheet date to fair value. The fair value is determined using Black-Scholes valuation model using various assumptions. The most significant changes in the assumptions was the difference in the strike price used at September 30, 2016 of $6.69 compared to $7.40 at September 30, 2015, the exercise of warrants with derivative liabilities and the August 2016 amendments to certain of the warrants to remove the clause that caused the warrants to be classified as derivative liabilities. Due to these significant changes, the fair value of the derivative liabilities decreased by $684,000 with a corresponding gain in the condensed consolidated statement of operations. |

| · | During the three-month period ended September 30, 2016 the Company incurred $65,000 loss on debt settlement agreements relating to an outstanding agreement from a previous year. This compares to $25,000 loss on debt settlement agreements for the three months ended September 30, 2015. |

Nine months ended September 30, 2016 Compared to Nine months ended September 30, 2015

We recorded a net loss of $879,000 or ($0.14) basic and ($0.54) diluted per share during the nine months ended September 30, 2016 compared to a net loss of $32,414,000 or ($10.61) basic and diluted per share for the nine months ended September 30, 2015.

Operating costs increased to $6,901,000 during the nine months ended September 30, 2016 compared to $3,904,000 in the prior period. Significant changes in operating expenses are outlined as follows:

| · | Research and development costs during the nine months ended September 30, 2016 were $3,343,000 compared to $2,324,000 during the prior period. This was due to the Company exercising its option to acquire Mayo Clinic technology as part of an agreement entered into in March 2014 and increased in-house research activity in the current period. |

| · | General and administrative expenses increased to $3,558,000 during the nine months ended September 30, 2016 from $1,580,000 during the prior period. This was due to generally increased expenses relating to consulting, general and administrative and professional fees during the nine months ended September 30, 2016 as the Company’s operating activities increased substantially. |

| · | The changes in fair value of derivative liabilities for the nine months ended September 30, 2016 was $5,925,000 as compared to ($28,486,000) for the nine months ended September 30, 2015. The variance in the current period is due to the revaluation of the Series A and A-1, Series C and C-1, Series D and D-1 and Series E and E-1 warrants issued by us in January and March 2015. We revalue the derivative liabilities at each balance sheet date to fair value. The most significant changes in the assumptions was the difference in the strike price used at September 30, 2016 of $6.69 compared to $7.40 at September 30, 2015, the exercise of warrants with derivative liabilities and the August 2016 amendments to certain of the warrants to remove the clause that caused the warrants to be classified as derivative liabilities. Due to these significant changes, the fair value of the derivative liabilities decreased by $5,925,000 with a corresponding gain in the condensed consolidated statement of operations. |

| - 20 - |

| · | During the nine months ended September 30, 2016, the Company received $231,000 of a grant awarded to Mayo Foundation from the U.S. Department of Defense for the Phase II Clinical Trial of TPIV 200. The grant paid for the clinical supplies purchased by the Company. |

| · | During the nine-month period ended September 30, 2016 the Company incurred $135,000 loss on debt settlement agreements relating to an outstanding debt agreement from previous years. This compares to $25,000 loss on debt settlement agreements for the nine months ended September 30, 2015. |

Liquidity and Capital Resources

We have not generated any revenues since inception, we have financed our operations primarily through public and private offerings of our stock and debt including warrants and the exercise thereof. The following table sets forth our cash and working capital as of September 30, 2016 and December 31, 2015:

September 30, 2016 | December 31, 2015 | |||||||

| Cash reserves | $ | 9,587,000 | $ | 6,577,000 | ||||

| Working capital (deficit) | $ | 7,494,000 | $ | (21,360,000 | ) | |||

Cash Flows

The following table summarizes our cash flows for the nine months ended September 30, 2016 and 2015:

| Nine Months Ended September 30, | ||||||||

| 2016 | 2015 | |||||||

| Net cash provided by (used in): | ||||||||

| Operating activities | $ | (4,756,000 | ) | $ | (3,492,000 | ) | ||

| Financing activities | 7,766,000 | 9,438,000 | ||||||

| Net increase in cash | $ | 3,010,000 | $ | 5,945,000 | ||||

Net Cash Used in Operating Activities

Net cash used in operating activities during the nine months ended September 30, 2016 was $4,756,000 compared to $3,492,000 during the prior period. We had no revenues during the current or prior periods. Operating expenditures, excluding non-cash interest and stock-based charges during the current period primarily consisted of consulting and management fees, office and general expenditures, and professional fees.

Net Cash Provided by Financing Activities

Net cash provided by financing activities during the nine months ended September 30, 2016 was $7,766,000 compared to net cash provided by financing activities of $9,438,000 during the prior period. The financing consisted of proceeds from private placements and warrant exercises in the current period as was in the prior period.

Financings

Our current available funding has come from financings that we conducted in January and March of 2015 and from the exercise of warrants issued in connection with our January and March, 2015 financings as well as our recent August 2016 private placement.

January 2015 Financing

In January, 2015, we entered into a Securities Purchase Agreement with certain investors for the sale of 610,000 units at a purchase price of $2.40 per unit, for a total purchase price of approximately $1,250,000, net of finders’ fee and offering expenses of approximately $214,000. Each unit consisting of (i) one share of the Company’s Common Stock, (ii) one Series A warrant to purchase one share of common stock, (iii) one Series B warrant to purchase one share of common stock (iv) one Series C warrant to purchase one share of common stock, (v) one Series D warrant to purchase one share of common stock, and (vi) one Series E warrant to purchase one share of common stock (the Series A, B, C, D and E warrants are hereby collectively referred to as the “January 2015 Warrants”). Series A warrants were exercisable at $18.00 per share, with a five-year term. Series B warrants were exercisable at $4.80 per share, with a six-month term. Series C warrants were exercisable at $12.00 per share, with a five-year term. Series D warrants were exercisable at $9.00 per share only if and to the extent that the Series B warrants are exercised, with a five-year term from the date that the Series B warrants are exercised. Series E warrants were exercisable at $15.00 per share, only if and to the extent that the Series C warrants are exercised, with a five-year term from the date that the Series C warrants are exercised. Pursuant to a placement agent agreement, we agreed to issue warrants to purchase 30,500 common shares with substantially the same terms as the January 2015 Warrants.

| - 21 - |

March 2015 Financing

In March, 2015, we entered into a Securities Purchase Agreement with certain accredited investors for the sale of 416,667 units at a purchase price of $2.40 per unit, for a total purchase price of approximately $950,000, net of finders’ fee and offering expenses of approximately $50,000. Each unit consisting of (i) one share of the Company’s Common Stock, (ii) one Series A-1 warrant to purchase one share of common stock, (iii) one Series B-1 warrant to purchase one share of common stock (iv) one Series C-1 warrant to purchase one share of common stock, (v) one Series D-1 warrant to purchase one share of common stock, and (vi) one Series E-1 warrant to purchase one share of common stock (the Series A-1, B-1, C-1, D-1 and E-1 warrants are hereby collectively referred to as the “March 2015 Warrants”). The March 2015 Warrants have substantially the same terms as the January 2015 Warrants. Pursuant to a placement agent agreement, we agreed to issue warrants to purchase 10,417 common shares with substantially the same terms as the March 2015 Warrants.

Restructuring of January and March 2015 Financings

In May 2015, we entered into a restructuring agreement with the investors of the January 2015 and March 2015 financings, where:

| · | The exercise price of the Series A and Series A-1 warrants was changed from $18.00 per share to $1.20 per share, |

| · | The exercise price of Series B and Series B-1 warrants was changed from $4.80 per share to $2.40 per share, |

| · | Each warrant of Series B and Series B-1 existing prior to the restructuring agreement was replaced with two warrants of such series, |

| · | The exercise price of the Series C and Series C-1 warrants was changed from $12.00 per share to $6.00 per share, and |

| · | Each warrant of Series C and Series C-1 existing prior to the restructuring agreement was replaced with two warrants of such series. |

As a result of the restructuring agreement, we issued an additional 1,026,667 Series B and B-1 warrants and 1,026,667 Series C and C-1 Warrants.

2016 Financing

August 2016 Private Placement Transaction

On August 10, 2016 and August 25, 2016, the Company completed private placements of units with certain accredited investors. The units consisted of (i) one share of the Company’s common stock, par value $0.001 per share and (ii) one five-year warrant to purchase one share of Company common stock for $6.00. The Company issued and sold an aggregate of 653,166 units at a purchase price per unit of $4.80 for an aggregate of approximately $3.1 million. The Company incurred approximately $0.8 million in agency fees and legal costs.

In addition, the Company issued five-year warrants to the placement agent in the offering providing for the purchase of up to 65,317 shares of Company common stock for $4.80 per share.

Pursuant to the registration rights agreements entered into in connection with the private placements, the Company is required to file a registration statement with the Securities and Exchange Commission registering for resale (a) the common stock issued in the private placement offering; (b) the shares of common stock issuable upon the exercise of the five-year warrants; and (c) the shares of common stock issuable upon the exercise of the warrants issued to the placement agent. The Company is required to file the registration statement within 120 days of the August 10, 2016 closing or by December 8, 2016. The Company is also required to ensure that the registration statement is declared effective within 90 calendar days after filing with the Securities and Exchange Commission, or by March 8, 2017.

In accordance with the registration rights agreements, should the Company fail to meet the above criteria, the Company is subject to pay the investors liquidated damages. The liquidated damages shall be a cash sum payment calculated at a rate of ten percent (10%) per annum of the aggregate purchase price for the registrable securities or aggregate amount upon exercise of the placement agent warrants.

| - 22 - |