Attached files

| file | filename |

|---|---|

| 8-K - INLAND REAL ESTATE INCOME TRUST, INC. - 8-K - 4/26/16 - Inland Real Estate Income Trust, Inc. | ireit-8k.htm |

Exhibit 99.1

inland - investments.com 1 Inland Real Estate Income Trust, Inc. THIS IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY THE SECURITIES DEPICTED HEREIN. THE OFFERING IS MADE ONLY BY THE PROSPECTUS. Net Asset Value Presentation April 26, 2016 • 1:00 pm CT Audio is available via webcast – dial in number not required. i nland - investments.com

inland - investments.com 2 Disclaimer This material is neither an offer to sell nor the solicitation of an offer to buy any security, which can be made only by the pros pec tus, which has been filed or registered with appropriate state and federal regulatory agencies, and sold only by broker dealers authoriz ed to do so. No regulatory agency has passed on or endorsed the merits of this offering. Any representation to the contrary is u nla wful. Past performance is not a guarantee of future results. The companies depicted in the photographs in this presentation are tenants of Inland Real Estate income Trust (Inland Income Trust or Company) and may have proprietary interests in their trademarks and trade names and nothing herein shall be considered an endorsement, authorization or approval of Inland Income Trust or its subsidiaries. The Inland name and logo are registered trademarks being used under license. This material has been distributed by Inland Securities Corporation, dealer manager for Inland Income Trust. Inland Securities Corporation, member FINRA/SIPC. Publication Date: 4/26/2016

inland - investments.com 3 Risk Factors Some of the risks related to investing in commercial real estate include, but are not limited to: market risks such as local pro perty supply and demand conditions; tenants’ inability to pay rent; tenant turnover; inflation and other increases in operating cos ts; adverse changes in laws and regulations; relative illiquidity of real estate investments; changing market demographics; acts of God s uch as earthquakes, floods or other uninsured losses; interest rate fluctuations; and availability of financing. An investment in Inland Income Trust’s shares involves significant risks. If Inland Income Trust is unable to effectively man age these risks, it may not meet its investment objectives and investors may lose some or all of their investment. Some of the risks re lat ed to investing in Inland Income Trust include, but are not limited to: the board of directors, rather than the trading market, det erm ines the offering price of shares; there is limited liquidity because shares are not bought and sold on an exchange; repurchase progra ms may be modified or terminated; a typical time horizon for an exit strategy may be longer than five years; there is no guarantee t hat a liquidity event will occur; distributions cannot be guaranteed and have been and may continue to be paid from sources other t han cash flow from operations, including borrowings and net offering proceeds; and failure to continue to qualify as a REIT and thus b ein g required to pay federal, state and local taxes. Please consult Inland Income Trust’s most recent Annual Report on Form 10 - K for more information on the specific risks.

inland - investments.com 4 Valuation Disclosure Our estimated per share net asset value (NAV) represents a snapshot in time, will likely change, and does not necessarily rep res ent the amount a stockholder would receive now or in the future for his or her shares of the Company’s common stock. Stockholder s should not rely on the estimated per share NAV in making a decision to buy or sell shares of our common stock. The estimated per share NAV is based on a number of assumptions, estimates and data that are inherently imprecise and susceptible to uncertaint y a nd changes in circumstances, including changes to the value of individual assets as well as changes and developments in the real es tate and capital markets, changes in interest rates, and changes in the composition of the Company’s portfolio . Throughout the valuation process, the Company’s board of directors, business manager and senior members of management reviewed, confirmed and approved the processes and methodologies used by CBRE Capital Advisors, Inc. (CBRE Cap) and their consistency with real estate industry standards and best practices . CBRE Cap’s valuation materials were prepared on a confidential basis and were addressed solely to the Company to assist its board of directors in establishing the estimated per share NAV. CBRE Cap’s valuation materials were not addressed to the public and sh ould not be relied upon by any other person to establish an estimated value of the Company’s common stock. CBRE Cap’s valuation materials do not constitute a fairness opinion for a potential or contemplated transaction and should not be represented as s uch .

inland - investments.com 5 Valuation Disclosure Neither CBRE Cap nor any of its affiliates is responsible for the board of directors’ determination of the estimated per shar e N AV or the repurchase price for shares under the Company’s share repurchase program (SRP). CBRE Cap assumed that the financial forecasts and other information and data provided to or otherwise reviewed by or discussed with CBRE Cap were reasonably prepared in good faith on bases reflecting the best then currently available estimates and judgements of the Company, and relied upon the Company to advise CBRE Cap promptly if any information previously provided became inaccurate or was required to be updated during its review. CBRE Cap made numerous assumptions as of various points in time in its preparation of valuation materials. In the ordinary course of its business, CBRE Cap, its affiliates, directors and officers may trade or otherwise structure and ef fect transactions in the shares or assets of the Company for its own account or for the accounts of its customers and, accordingly , m ay at any time hold a long or short position, finance positions or otherwise structure and effect transactions in the Company’s sha res or assets. CBRE Cap is an affiliate of CBRE Group, Inc. ( CBRE ), a parent holding company of affiliated companies that are engaged in the ordinary course of business in many areas related to commercial real estate and related services. Through CBRE's affiliat es, CBRE may have in the past, and may from time to time in the future, perform one or more roles in a transaction related to the Company or its affiliates. CBRE Cap is not a legal, accounting or tax expert, and makes no representation or warranty as to the sufficiency or adequacy of its valuation materials with respect to such issues. Nothing contained therein should be construed as tax, accounting or legal ad vic e.

inland - investments.com 6 Forward - Looking Statements In addition to historical information, this webcast contains "forward - looking statements" made under the "safe harbor" provision s of the Private Securities Litigation Reform Act of 1995. The statements may be identified by terminology such as "may," “can,” "would, " “will,” "expect," "intend," "estimate," "anticipate," "plan," "seek," "appear," or "believe." Such statements reflect the current view of Inland Income Trust with respect to future events and are subject to certain risks, uncertainties and assumptions related to certain fa ctors including, without limitation, the uncertainties related to general economic conditions, unforeseen events affecting the real es tate industry or particular markets, and other factors detailed under Risk Factors in our most recent Form 10 - K on file with the Securities and Exchange Commission . Although Inland Income Trust believes that the expectations reflected in such forward - looking statements are reasonable, it can give no assurance that such expectations will prove to be correct. You should exercise caution when considering forward - looking statements and not place undue reliance on them. Based upon changing conditions, should any one or more of these risks or uncertainties materialize, or should any underlying assumptions prove incorrect, actual results may va ry materially from those described herein. Except as required by federal securities laws, Inland Income Trust undertakes no obliga tion to publicly update or revise any written or oral forward - looking statements, whether as a result of new information, future events, changed circumstances or any other reason after the date of this webcast.

inland - investments.com On Today’s Call 7 Mitchell Sabshon Chief Executive Officer JoAnn McGuinness President and Chief Operating Officer David Lichterman Vice President, Chief Accounting Officer & Treasurer

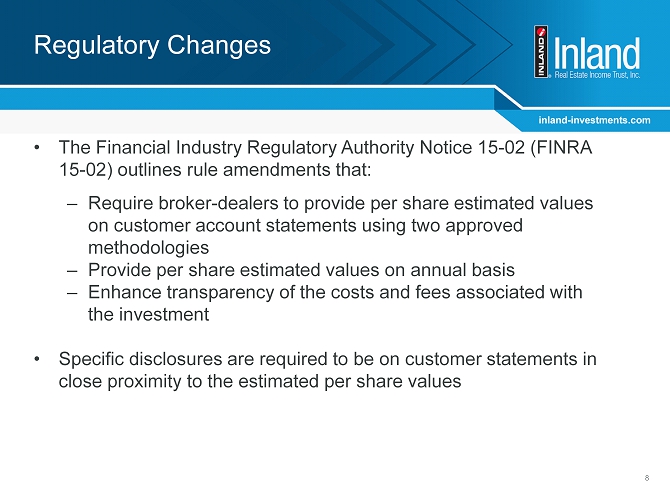

inland - investments.com Regulatory Changes 8 • The Financial Industry Regulatory Authority Notice 15 - 02 (FINRA 15 - 02) outlines rule amendments that: – Require broker - dealers to provide per share estimated values on customer account statements using two approved methodologies – Provide per share estimated values on annual basis – Enhance transparency of the costs and fees associated with the investment • Specific disclosures are required to be on customer statements in close proximity to the estimated per share values

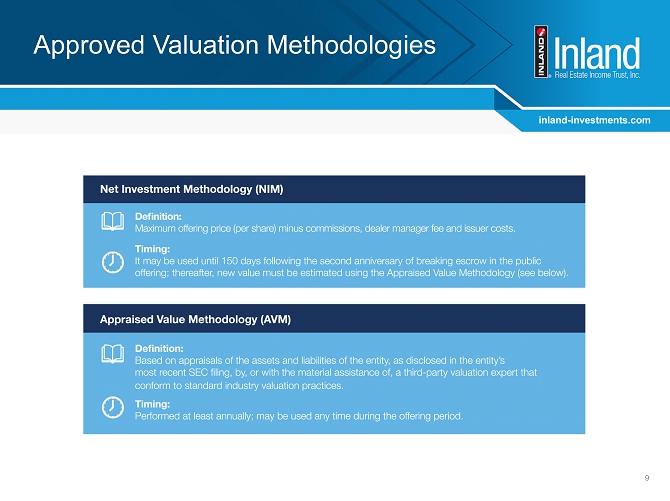

inland - investments.com Approved Valuation Methodologies 9

inland - investments.com Benefits to Investors 10

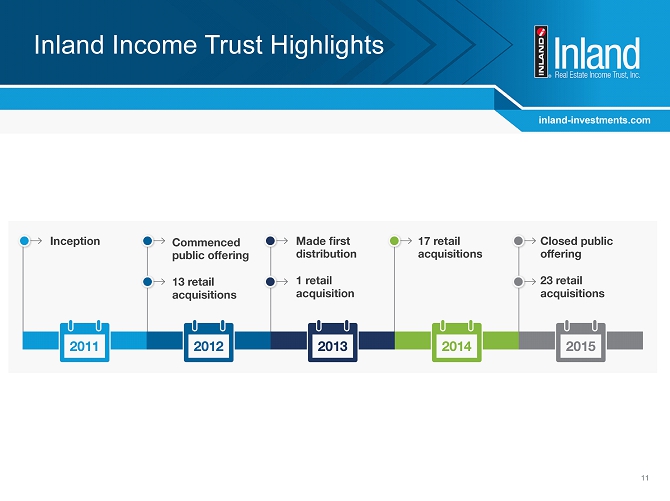

inland - investments.com 11 Inland Income Trust Highlights

inland - investments.com 12 Portfolio Snapshot No Assets 0 - 5% of ABR* 5.01 - 10% of ABR 10.01% or Greater of ABR * Annualized Base Rent as of December 31, 2015 As of December 31 , 2015 Total Number of Properties: 54 Total Square Feet: 6,025,330 Number of States: 22 Economic Occupancy: 97.2% Physical Occupancy : 96.2% Number of Tenants: 668

inland - investments.com 4 th Quarter 2015 Acquisitions 13 Property: Milford Marketplace Market: Milford, Connecticut Acquisition Date: October 1, 2015 Acquisition Price: $34.0 Million Leasable Area: 112,257 SF Tenants: Whole Foods, JoS. A. Bank, Ann Taylor’s Loft Property: Settlers Ridge Market: Pittsburgh, Pennsylvania Acquisition Date: October 1, 2015 Acquisition Price: $139.1 Million Leasable Area: 472,572 SF Tenants: Giant Eagle, Cinemark Theaters, REI Property: Marketplace at El Paseo Market: Fresno, California Acquisition Date: October 16, 2015 Acquisition Price: $70 Million Leasable Area: 224,683 SF Tenants: Marshalls, Burlington, Ross Dress for Less

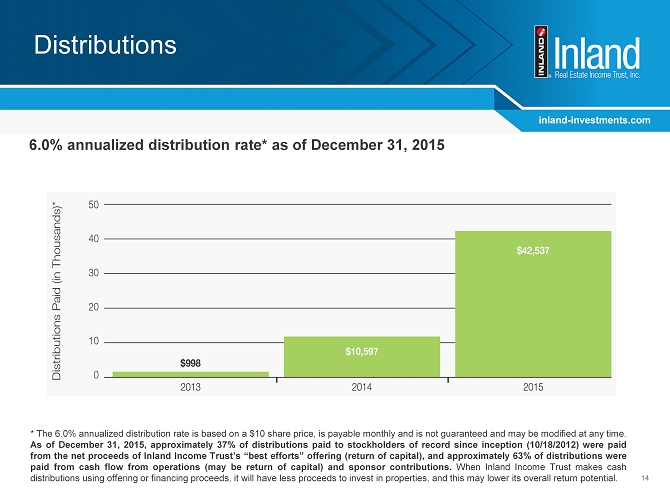

inland - investments.com Distributions * The 6 . 0 % annualized distribution rate is based on a $ 10 share price, is payable monthly and is not guaranteed and may be modified at any time . As of December 31 , 2015 , approximately 37 % of distributions paid to stockholders of record since inception ( 10 / 18 / 2012 ) were paid from the net proceeds of Inland Income Trust’s “best efforts” offering (return of capital), and approximately 63 % of distributions were paid from cash flow from operations (may be return of capital) and sponsor contributions . When Inland Income Trust makes cash distributions using offering or financing proceeds, it will have less proceeds to invest in properties, and this may lower its overall return potential . 6.0% annualized distribution rate* as of December 31, 2015 14

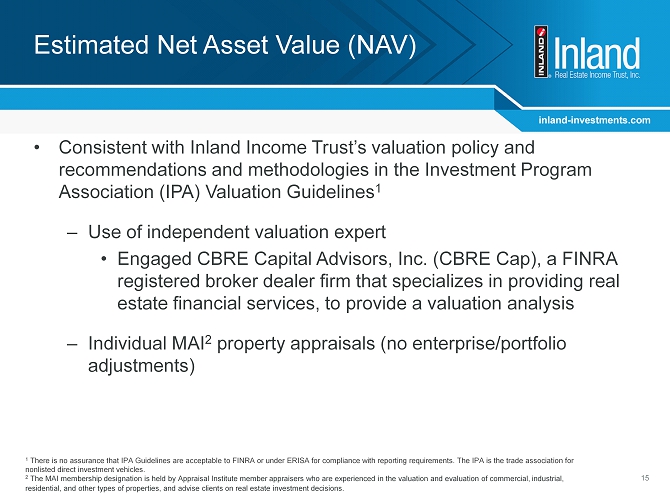

inland - investments.com Estimated Net Asset Value (NAV) 15 • Consistent with Inland Income Trust’s valuation policy and recommendations and methodologies in the Investment Program Association (IPA) Valuation Guidelines 1 – Use of independent valuation expert • Engaged CBRE Capital Advisors, I nc. (CBRE Cap), a FINRA registered broker dealer firm that specializes in providing real estate financial services , to provide a valuation analysis – Individual MAI 2 property appraisals (no enterprise/portfolio adjustments) 1 There is no assurance that IPA Guidelines are acceptable to FINRA or under ERISA for compliance with reporting requirements. The IPA is the trade association for nonlisted direct investment vehicles. 2 The MAI membership designation is held by Appraisal Institute member appraisers who are experienced in the valuation and evaluat ion of commercial, industrial, residential, and other types of properties, and advise clients on real estate investment decisions.

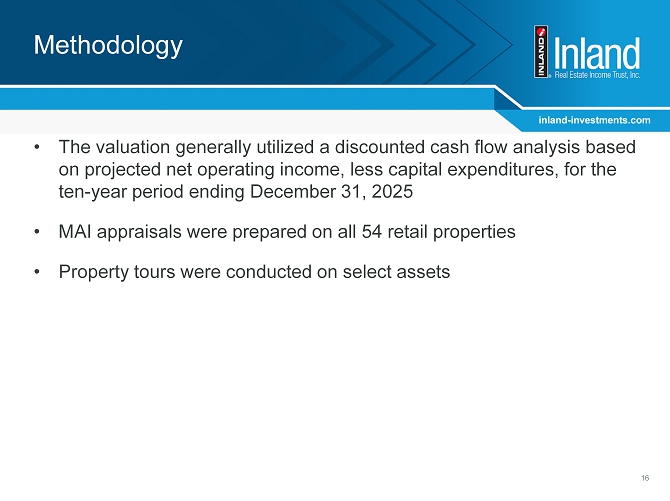

inland - investments.com Methodology 16 • The valuation generally utilized a discounted cash flow analysis based on projected net operating income, less capital expenditures, for the ten - year period ending December 31, 2025 • MAI appraisals were prepared on all 54 retail properties • Property tours were conducted on select assets

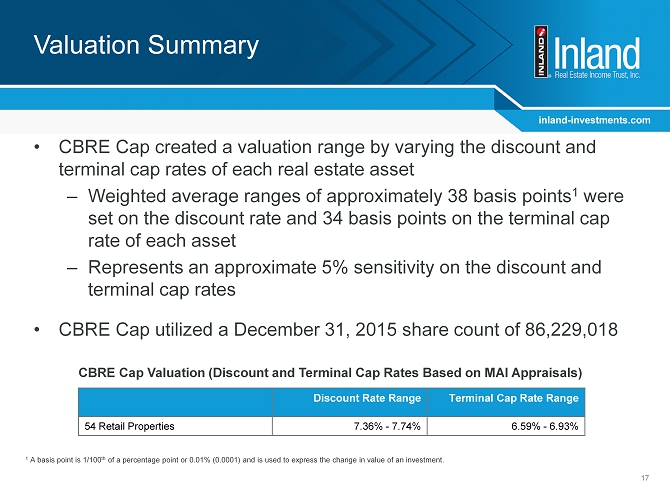

inland - investments.com Valuation Summary 17 • CBRE Cap created a valuation range by varying the discount and terminal cap rates of each real estate asset – Weighted average ranges of approximately 38 basis points 1 were set on the discount rate and 34 basis points on the terminal cap rate of each asset – Represents an approximate 5% sensitivity on the discount and terminal cap rates • CBRE Cap utilized a December 31, 2015 share count of 86,229,018 Discount Rate Range Terminal Cap Rate Range 54 Retail Properties 7.36% - 7.74% 6.59% - 6.93% CBRE Cap Valuation (Discount and Terminal Cap Rates Based on MAI Appraisals) 1 A basis point is 1/100 th of a percentage point or 0.01% (0.0001) and is used to express the change in value of an investment.

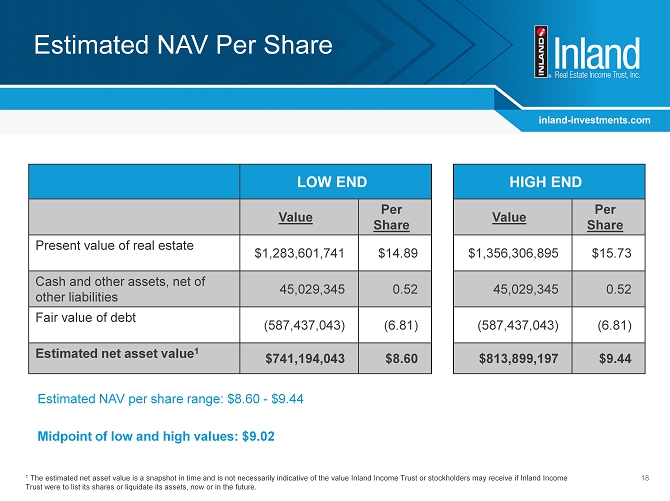

inland - investments.com Estimated NAV Per Share 18 LOW END HIGH END Value Per Share Value Per Share Present value of real estate $1,283,601,741 $14.89 $1,356,306,895 $15.73 Cash and other assets, net of other liabilities 45,029,345 0.52 45,029,345 0.52 Fair value of debt (587,437,043) (6.81) (587,437,043) (6.81) Estimated net asset value 1 $741,194,043 $8.60 $813,899,197 $9.44 1 The estimated net asset value is a snapshot in time and is not necessarily indicative of the value Inland Income Trust or sto ck holders may receive if Inland Income Trust were to list its shares or liquidate its assets, now or in the future. Estimated NAV per share range: $8.60 - $9.44 Midpoint of low and high values: $9.02

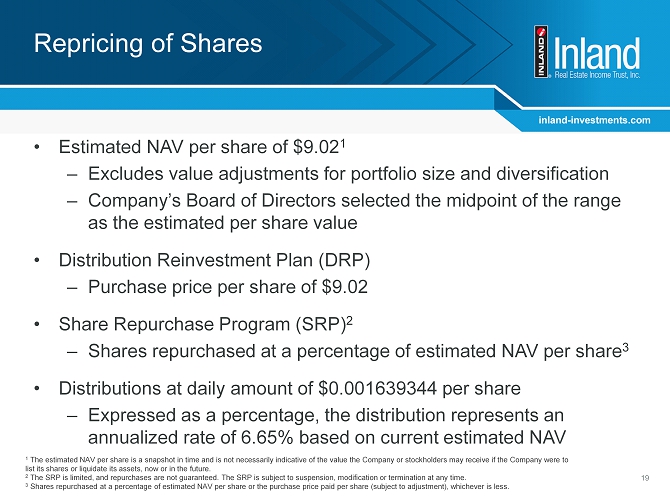

inland - investments.com Repricing of Shares 19 • Estimated NAV per share of $9.02 1 – Excludes value adjustments for portfolio size and diversification – Company’s Board of Directors selected the midpoint of the range as the estimated per share value • Distribution Reinvestment Plan (DRP) – Purchase price per share of $9.02 • Share Repurchase Program (SRP) 2 – Shares repurchased at a percentage of estimated NAV per share 3 • Distributions at daily amount of $0.001639344 per share – Expressed as a percentage, the distribution represents an annualized rate of 6.65% based on current estimated NAV 1 The estimated NAV per share is a snapshot in time and is not necessarily indicative of the value the Company or stockholders ma y receive if the Company were to list its shares or liquidate its assets, now or in the future. 2 The SRP is limited, and repurchases are not guaranteed. The SRP is subject to suspension, modification or termination at any ti me. 3 Shares repurchased at a percentage of estimated NAV per share or the purchase price paid per share (subject to adjustment), w hi chever is less.

inland - investments.com 20 Strategy for the Future 1 Statista . Consumers’ weekly grocery shopping trips in the United States from 2006 to 2015 1 Continued focus on multi - tenant, necessity - based shopping centers with the following key attributes:

inland - investments.com Questions?