Attached files

| file | filename |

|---|---|

| EX-31.1 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex311.htm |

| EX-32.1 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex321.htm |

| EX-32.2 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex322.htm |

| EX-31.2 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

þ Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended: September 30, 2015

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from _____________ to_____________

Commission File Number: 0-15905

BLUE DOLPHIN ENERGY COMPANY

(Exact name of registrant as specified in its charter)

|

Delaware

|

73-1268729

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

801 Travis Street, Suite 2100, Houston, Texas 77002

(Address of principal executive offices)

(713) 568-4725

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

þ

|

|

(Do not check if a smaller reporting company)

|

|||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

Number of shares of common stock, par value $0.01 per share outstanding as of November 16, 2015: 10,453,802

BLUE DOLPHIN ENERGY COMPANY & SUBSIDIARIES

FORM 10-Q REPORT INDEX

| 3 | ||

|

ITEM 1.

|

3

|

|

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

|

ITEM 2.

|

29

|

|

|

ITEM 3.

|

46

|

|

|

ITEM 4.

|

46

|

|

| 47 | ||

|

ITEM 1.

|

47

|

|

|

ITEM 1A.

|

47

|

|

|

ITEM 2.

|

47

|

|

|

ITEM 3.

|

47

|

|

|

ITEM 4.

|

47

|

|

|

ITEM 5.

|

47

|

|

|

ITEM 6.

|

48

|

|

| 49 | ||

2

Blue Dolphin Energy Company & Subsidiaries

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

ASSETS

|

||||||||

|

CURRENT ASSETS

|

||||||||

|

Cash and cash equivalents

|

$ | 1,518,359 | $ | 1,293,233 | ||||

|

Restricted cash

|

5,834,197 | 1,008,514 | ||||||

|

Accounts receivable

|

7,833,519 | 8,340,303 | ||||||

|

Prepaid expenses and other current assets

|

1,045,893 | 771,458 | ||||||

|

Deposits

|

420,176 | 68,498 | ||||||

|

Inventory

|

5,620,827 | 3,200,651 | ||||||

|

Deferred tax assets, current portion, net

|

2,892,459 | - | ||||||

|

Total current assets

|

25,165,430 | 14,682,657 | ||||||

|

Total property and equipment, net

|

46,054,365 | 37,371,075 | ||||||

|

Restricted cash, noncurrent

|

11,277,441 | - | ||||||

|

Surety bonds

|

1,667,000 | 1,642,000 | ||||||

|

Debt issue costs, net

|

1,296,480 | 479,737 | ||||||

|

Trade name

|

303,346 | 303,346 | ||||||

|

Deferred tax assets, net

|

387,824 | 5,928,342 | ||||||

|

Total long-term assets

|

60,986,456 | 45,724,500 | ||||||

|

TOTAL ASSETS

|

$ | 86,151,886 | $ | 60,407,157 | ||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

CURRENT LIABILITIES

|

||||||||

|

Accounts payable

|

$ | 16,459,787 | $ | 12,370,179 | ||||

|

Accounts payable, related party

|

- | 1,174,168 | ||||||

|

Asset retirement obligations, current portion

|

38,644 | 85,846 | ||||||

|

Accrued expenses and other current liabilities

|

2,005,206 | 2,783,704 | ||||||

|

Interest payable, current portion

|

57,140 | 56,039 | ||||||

|

Long-term debt, current portion

|

1,631,539 | 1,245,476 | ||||||

|

Deferred tax liabilities, net

|

- | 168,236 | ||||||

|

Total current liabilities

|

20,192,316 | 17,883,648 | ||||||

|

Long-term liabilities:

|

||||||||

|

Asset retirement obligations, net of current portion

|

1,928,371 | 1,780,924 | ||||||

|

Deferred revenues and expenses

|

561,864 | 691,525 | ||||||

|

Long-term debt, net of current portion

|

28,948,021 | 10,808,803 | ||||||

|

Long-term interest payable, net of current portion

|

1,430,371 | 1,274,789 | ||||||

|

Total long-term liabilities

|

32,868,627 | 14,556,041 | ||||||

|

TOTAL LIABILITIES

|

53,060,943 | 32,439,689 | ||||||

|

Commitments and contingencies (Note 21)

|

||||||||

|

STOCKHOLDERS' EQUITY

|

||||||||

|

Common stock ($0.01 par value, 20,000,000 shares authorized;10,603,802 and

|

||||||||

|

10,599,444 shares issued at September 30, 2015 and December 31, 2014, respectively)

|

106,038 | 105,995 | ||||||

|

Additional paid-in capital

|

36,738,737 | 36,718,781 | ||||||

|

Accumulated deficit

|

(2,953,832 | ) | (8,057,308 | ) | ||||

|

Treasury stock, 150,000 shares at cost

|

(800,000 | ) | (800,000 | ) | ||||

|

Total stockholders' equity

|

33,090,943 | 27,967,468 | ||||||

|

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY

|

$ | 86,151,886 | $ | 60,407,157 | ||||

See accompanying notes to consolidated financial statements.

3

| Three Months Ended September 30, |

Nine Months Ended September 30,

|

|||||||||||||||

|

2015

|

2014

|

2015

|

2014

|

|||||||||||||

|

REVENUE FROM OPERATIONS

|

||||||||||||||||

|

Refined petroleum product sales

|

$ | 54,924,070 | $ | 87,846,757 | $ | 174,830,292 | $ | 310,938,981 | ||||||||

|

Tank rental revenue

|

286,892 | 282,516 | 860,676 | 847,548 | ||||||||||||

|

Pipeline operations

|

45,925 | 56,900 | 119,882 | 178,793 | ||||||||||||

|

Total revenue from operations

|

55,256,887 | 88,186,173 | 175,810,850 | 311,965,322 | ||||||||||||

|

COST OF OPERATIONS

|

||||||||||||||||

|

Cost of refined products sold

|

48,415,627 | 82,781,856 | 151,604,774 | 289,819,720 | ||||||||||||

|

Refinery operating expenses

|

2,953,528 | 2,496,514 | 8,420,650 | 8,092,738 | ||||||||||||

|

Joint Marketing Agreement profit share

|

1,435,376 | 1,094,383 | 4,812,674 | 2,334,487 | ||||||||||||

|

Pipeline operating expenses

|

63,099 | 50,100 | 170,582 | 139,542 | ||||||||||||

|

Lease operating expenses

|

(1,143 | ) | 7,041 | 20,271 | 21,037 | |||||||||||

|

General and administrative expenses

|

312,365 | 253,437 | 1,058,267 | 1,049,981 | ||||||||||||

|

Depletion, depreciation and amortization

|

414,837 | 393,871 | 1,217,005 | 1,175,643 | ||||||||||||

|

Accretion expense

|

52,720 | 53,731 | 158,655 | 158,264 | ||||||||||||

|

Total cost of operations

|

53,646,409 | 87,130,933 | 167,462,878 | 302,791,412 | ||||||||||||

|

Income from operations

|

1,610,478 | 1,055,240 | 8,347,972 | 9,173,910 | ||||||||||||

|

OTHER INCOME (EXPENSE)

|

||||||||||||||||

|

Easement, interest and other income

|

724,349 | 1,813 | 856,816 | 253,745 | ||||||||||||

|

Interest expense

|

(382,191 | ) | (214,407 | ) | (1,322,562 | ) | (675,586 | ) | ||||||||

|

Loss on disposal of property and equipment

|

- | (4,400 | ) | - | (4,400 | ) | ||||||||||

|

Total other income (expense)

|

342,158 | (216,994 | ) | (465,746 | ) | (426,241 | ) | |||||||||

|

Income before income taxes

|

1,952,636 | 838,246 | 7,882,226 | 8,747,669 | ||||||||||||

|

Income tax expense

|

(688,403 | ) | (22,199 | ) | (2,778,750 | ) | (298,792 | ) | ||||||||

|

Net income

|

$ | 1,264,233 | $ | 816,047 | $ | 5,103,476 | $ | 8,448,877 | ||||||||

|

Income per common share

|

||||||||||||||||

|

Basic

|

$ | 0.12 | $ | 0.08 | $ | 0.49 | $ | 0.81 | ||||||||

|

Diluted

|

$ | 0.12 | $ | 0.08 | $ | 0.49 | $ | 0.81 | ||||||||

|

Weighted average number of common shares outstanding:

|

||||||||||||||||

|

Basic

|

10,453,802 | 10,446,218 | 10,451,168 | 10,439,684 | ||||||||||||

|

Diluted

|

10,453,802 | 10,446,218 | 10,451,168 | 10,439,684 | ||||||||||||

See accompanying notes to consolidated financial statements.

4

Blue Dolphin Energy Company & Subsidiaries

|

Nine Months Ended September 30,

|

||||||||

|

2015

|

2014

|

|||||||

|

OPERATING ACTIVITIES

|

||||||||

|

Net income

|

$ | 5,103,476 | $ | 8,448,877 | ||||

|

Adjustments to reconcile net income to net cash

|

||||||||

|

provided by operating activities:

|

||||||||

|

Depletion, depreciation and amortization

|

1,217,005 | 1,175,643 | ||||||

|

Unrealized loss on derivatives

|

362,750 | 26,150 | ||||||

|

Deferred taxes

|

2,479,823 | - | ||||||

|

Amortization of debt issue costs

|

517,652 | 25,350 | ||||||

|

Accretion expense

|

158,655 | 158,264 | ||||||

|

Common stock issued for services

|

19,999 | 75,001 | ||||||

|

Loss on disposal of assets

|

- | 4,400 | ||||||

|

Changes in operating assets and liabilities

|

||||||||

|

Accounts receivable

|

506,784 | 2,058,624 | ||||||

|

Prepaid expenses and other current assets

|

(274,435 | ) | 152,655 | |||||

|

Deposits and other assets

|

(1,711,073 | ) | (490,838 | ) | ||||

|

Inventory

|

(2,420,176 | ) | (2,879,729 | ) | ||||

|

Accounts payable, accrued expenses and other liabilities

|

2,916,973 | (5,144 | ) | |||||

|

Accounts payable, related party

|

(1,174,168 | ) | (1,857,964 | ) | ||||

|

Net cash provided by operating activities

|

7,703,265 | 6,891,289 | ||||||

|

INVESTING ACTIVITIES

|

||||||||

|

Capital expenditures

|

(9,900,295 | ) | (1,145,720 | ) | ||||

|

Change in restricted cash for investing activities

|

(13,021,438 | ) | - | |||||

|

Net cash used in investing activities

|

(22,921,733 | ) | (1,145,720 | ) | ||||

|

FINANCING ACTIVITIES

|

||||||||

|

Proceeds from issuance of debt

|

25,000,000 | - | ||||||

|

Payments on long-term debt

|

(9,474,720 | ) | (6,103,131 | ) | ||||

|

Proceeds from notes payable

|

3,000,000 | 2,000,000 | ||||||

|

Payments on notes payable

|

- | (216,182 | ) | |||||

|

Change in restricted cash for financing activities

|

(3,081,686 | ) | (678,498 | ) | ||||

|

Net cash provided by (used in) financing activities

|

15,443,594 | (4,997,811 | ) | |||||

|

Net increase in cash and cash equivalents

|

225,126 | 747,758 | ||||||

|

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD

|

1,293,233 | 434,717 | ||||||

|

CASH AND CASH EQUIVALENTS AT END OF PERIOD

|

$ | 1,518,359 | $ | 1,182,475 | ||||

|

Supplemental Information:

|

||||||||

|

Non-cash operating activities

|

||||||||

|

Surety bond funded by seller of pipeline interest

|

$ | - | $ | 850,000 | ||||

|

Non-cash investing and financing activities:

|

||||||||

|

New asset retirement obligations

|

$ | - | $ | 300,980 | ||||

|

Financing of capital expenditures via capital lease

|

$ | - | $ | 536,635 | ||||

|

Interest paid

|

$ | 959,665 | $ | 1,211,773 | ||||

|

Income taxes paid

|

$ | 139,500 | $ | 231,552 | ||||

See accompanying notes to consolidated financial statements.

5

|

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) |

|

|

(1)

|

Organization

|

Nature of Operations

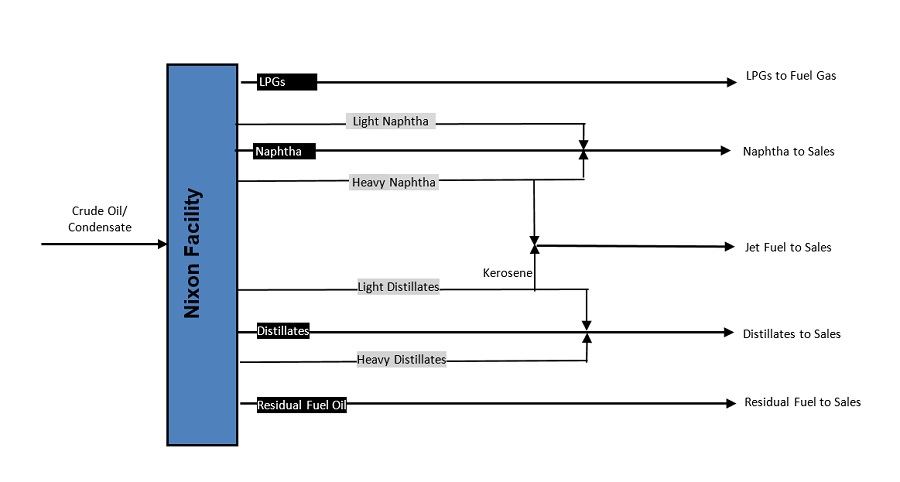

Blue Dolphin Energy Company (http://www.blue-dolphin-energy.com, referred to herein, with its predecessors and subsidiaries, as “Blue Dolphin,” “we,” “us” and “our”) is primarily an independent refiner and marketer of petroleum products. Our primary asset is a 15,000 bpd crude oil and condensate processing facility that is located in Nixon, Texas (the “Nixon Facility”). As part of our refinery business segment, we conduct petroleum storage and terminaling operations under third-party lease agreements at the Nixon Facility. We also own and operate pipeline assets and have leasehold interests in oil and gas properties. See “Note (4) Business Segment Information” of this report for further discussion of our business segments.

Structure and Management

We were formed as a Delaware corporation in 1986. We are currently controlled by Lazarus Energy Holdings, LLC (“LEH”), which owns approximately 81% of our common stock, par value $0.01 per share (the “Common Stock). LEH manages and operates all of our properties pursuant to an Operating Agreement (the “Operating Agreement”). Jonathan P. Carroll is Chairman of the Board of Directors (the “Board”), Chief Executive Officer and President of Blue Dolphin, as well as a majority owner of LEH. See “Note (10) Accounts Payable, Related Party,” “Note (13) Long-Term Debt,” and “Note (21) Commitments and Contingencies – Financing Agreements” of this report for additional disclosures related to the Operating Agreement, Jonathan P. Carroll, and LEH.

Our operations are conducted through the following operating subsidiaries:

|

·

|

Lazarus Energy, LLC, a Delaware limited liability company (“LE”);

|

|

·

|

Lazarus Refining & Marketing, LLC, a Delaware limited liability company (“LRM”);

|

|

·

|

Blue Dolphin Pipe Line Company, a Delaware corporation;

|

|

·

|

Blue Dolphin Petroleum Company, a Delaware corporation; and

|

|

·

|

Blue Dolphin Services Co., a Texas corporation.

|

See "Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Owned and Leased Assets” of this report for additional information regarding our operating subsidiaries.

|

(2)

|

Basis of Presentation

|

We have prepared our unaudited consolidated financial statements in accordance with U.S. generally accepted accounting principles (“GAAP”), as codified by the Financial Accounting Standards Board (the “FASB”) in its Accounting Standards Codification (“ASC”), and pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”). Our consolidated financial statements include Blue Dolphin and its subsidiaries. Significant intercompany transactions have been eliminated in the consolidation. In the opinion of management, such consolidated financial statements reflect all adjustments necessary to present fair consolidated statements of income, financial position and cash flows. We believe that the disclosures are adequate and the presented information is not misleading. This report has been prepared in accordance with the SEC’s Form 10-Q instructions and therefore, certain information and footnote disclosures normally included in our annual audited financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to the SEC’s rules and regulations.

|

(3)

|

Significant Accounting Policies

|

The summary of significant accounting policies of Blue Dolphin is presented to assist in understanding our consolidated financial statements. Our consolidated financial statements and accompanying notes are representations of management who is responsible for its integrity and objectivity. These accounting policies conform to GAAP and have been consistently applied in the preparation of our consolidated financial statements.

Use of Estimates

We have made a number of estimates and assumptions related to the reporting of our consolidated assets and liabilities and to the disclosure of contingent assets and liabilities to prepare these consolidated financial statements in conformity with GAAP. While we believe our current estimates are reasonable and appropriate, actual results could differ from those estimated.

6

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Cash and Cash Equivalents

Cash and cash equivalents represent liquid investments with an original maturity of three months or less. Cash balances are maintained in depository and overnight investment accounts with financial institutions that, at times, may exceed insured deposit limits. We monitor the financial condition of the financial institutions and have experienced no losses associated with these accounts. Cash and cash equivalents totaled $1,518,359 and $1,293,233 at September 30, 2015 and December 31, 2014, respectively.

Restricted Cash

Restricted cash totaled $5,834,197 and $1,008,514 at September 30, 2015 and December 31, 2014, respectively. Restricted cash, noncurrent totaled $11,277,441 and $0 at September 30, 2015 and December 31, 2014, respectively. Restricted cash primarily represents: (i) a construction contingency account under which Sovereign Bank, a Texas state bank (“Sovereign”) will fund contingencies, (ii) a payment reserve account held by Sovereign as security for payments under a loan agreement, and (iii) a certificate of deposit held by Sovereign as security under a loan agreement. Restricted cash, noncurrent, represents a disbursement account under which Sovereign will make payments for construction related expenses to build new petroleum storage tanks. See “Note (13) Long-Term Debt” of this report for additional disclosures related to loan agreements with Sovereign.

Accounts Receivable, Allowance for Doubtful Accounts and Concentration of Credit Risk

Accounts receivable are customer obligations due under normal trade terms. The allowance for doubtful accounts represents our estimate of the amount of probable credit losses existing in our accounts receivable. We have a limited number of customers with individually large amounts due on any given date. Any unanticipated change in any one of these customers’ credit worthiness or other matters affecting the collectability of amounts due from such customers could have a material adverse effect on our results of operations in the period in which such changes or events occur. We regularly review all of our aged accounts receivable for collectability and establish an allowance for individual customer balances as necessary.

Concentration of Risk

Bank Accounts

Financial instruments that potentially subject us to concentrations of risk consist primarily of cash, trade receivables and payables. We maintain our cash balances at financial institutions located in Houston, Texas. In the United States, the Federal Deposit Insurance Corporation (the “FDIC”) insures certain financial products up to a maximum of $250,000 per depositor. We had cash balances in excess of the FDIC insurance limit per depositor in the amount of $18,017,488 and $1,113,977 at September 30, 2015 and December 31, 2014, respectively.

Significant Customers

Customers of our refined petroleum products include distributors, wholesalers, and refineries primarily in the lower portion of the Texas Triangle (the Houston - San Antonio - Dallas/Fort Worth area). We have bulk term contracts, including month-to-month, six months, and up to five year terms in place with most of our customers. Certain of our contracts require us to sell fixed quantities and/or minimum quantities of intermediate and finished petroleum products and many of these arrangements are subject to periodic renegotiation, which could result in us receiving higher or lower relative prices for our refined petroleum products. See “Note (15) Concentration of Risk” of this report for additional disclosures related to significant customers.

Inventory

The nature of our business requires us to maintain inventory, which primarily consists of refined petroleum products and chemicals. Inventory reflected for crude oil and condensate is nominal and represents line fill. Our overall inventory is valued at lower of cost or market with costs being determined by the average cost method. If the market value of our refined petroleum product inventories declines to an amount less than our average cost, we record a write-down of inventory and an associated adjustment to cost of refined products sold. See “Note (7) Inventory” of this report for additional disclosures related to our inventory.

7

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Derivatives

We are exposed to commodity prices and other market risks including gains and losses on certain financial assets as a result of our inventory risk management policy. Under our inventory risk management policy, Genesis Energy, LLC (“Genesis”) may, but is not required to, use commodity futures contracts to mitigate the change in value for certain of our refined petroleum product inventories subject to market price fluctuations. The physical inventory volumes are not exchanged and these contracts are net settled with cash.

Although these commodity futures contracts are not subject to hedge accounting treatment under FASB ASC guidance, we record the fair value of these Genesis hedges in our consolidated balance sheet each financial reporting period because of contractual arrangements with Genesis under which we are effectively exposed to the potential gains or losses. We recognize all commodity hedge positions as either current assets or current liabilities in our consolidated balance sheets and those instruments are measured at fair value. Changes in the fair value from financial reporting period to financial reporting period are recognized in our consolidated statements of income. Net gains or losses associated with these transactions are recognized within cost of refined products sold in our consolidated statements of income using mark-to-market accounting.

See “Note (19) Fair Value Measurement” and “Note (20) Inventory Risk Management” of this report for additional disclosures related to derivatives.

Property and Equipment

Refinery and Facilities

Additions to refinery and facilities are capitalized. Expenditures for repairs and maintenance are expensed as incurred and are included as operating expenses under the Operating Agreement. Management expects to continue making improvements to the Nixon Facility based on technological advances.

Refinery and facilities are carried at cost. Adjustment of the asset and the related accumulated depreciation accounts are made for refinery and facilities’ retirements and disposals, with the resulting gain or loss included in the consolidated statements of income. For financial reporting purposes, depreciation of refinery and facilities is computed using the straight-line method using an estimated useful life of 25 years beginning when the refinery and facilities are placed in service. We did not record any impairment of our refinery and facilities for the three and nine months ended September 30, 2015 and 2014.

Oil and Gas Properties

We account for our oil and gas properties using the full-cost method of accounting, whereby all costs associated with acquisition, exploration and development of oil and gas properties, including directly related internal costs, are capitalized on a cost center basis. Amortization of such costs and estimated future development costs are determined using the unit-of-production method. Our oil and gas properties had no production during the three and nine months ended September 30, 2015 and 2014. All leases associated with our oil and gas properties have expired.

Pipelines and Facilities

We record pipelines and facilities at cost less any adjustments for depreciation or impairment. Depreciation is computed using the straight-line method over estimated useful lives ranging from 10 to 22 years. In accordance with FASB ASC guidance on accounting for the impairment or disposal of long-lived assets, we periodically evaluate our long-lived assets for impairment. Additionally, we evaluate our long-lived assets when events or circumstances indicate that the carrying value of these assets may not be recoverable.

Construction in Progress

Construction in progress expenditures, which relate to construction ans refurbishment activities at the Nixon Facility, are capitalized as incurred. Depreciation begins once the asset is placed in service.

See “Note (8) Property, Plant and Equipment, Net” of this report for additional disclosures related to our refinery and facilities, oil and gas properties, pipelines and facilities, and construction in progress.

8

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Intangibles – Other

We have an acquisition-related intangible asset consisting of the Blue Dolphin trade name in the amount of $303,346. We have determined our trade name to have an indefinite useful life. We account for other intangible assets under FASB ASC guidance related to intangibles, goodwill and other. Under the guidance, we test intangible assets with indefinite lives annually for impairment. Management performed its regular annual impairment testing of trade name in the fourth quarter of 2014. Upon completion of that testing, we determined that no impairment was necessary as of December 31, 2014.

Debt Issue Costs

We have debt issue costs related to certain refinery and facilities debt. Debt issue costs are capitalized and amortized over the term of the related debt using the straight-line method, which approximates the effective interest method. When a loan is paid in full, any unamortized financing costs are removed from the related asset accounts and expensed as interest expense. See “Note (9) Debt Issue Costs” of this report for additional disclosures related to debt issue costs.

Revenue Recognition

Refined Petroleum Products Revenue

We sell jet fuel in nearby markets, and our intermediate products, including liquefied petroleum gas, naphtha, heavy oil-based mud blendstock (“HOBM”), and atmospheric gas oil (“AGO”), to wholesalers and nearby refineries for further blending and processing. Revenue from refined petroleum products sales is recognized when title passes. Title passage occurs when refined petroleum products are sold or delivered in accordance with the terms of the respective sales agreements. Revenue is recognized when sales prices are fixed or determinable and collectability is reasonably assured.

Customers assume the risk of loss when title is transferred. Transportation, shipping, and handling costs incurred are included in cost of refined products sold. Excise and other taxes that are collected from customers and remitted to governmental authorities are not included in revenue.

Tank Rental Revenue

Tank rental fees are invoiced monthly in accordance with the terms of the related lease agreement and recognized in revenue as earned.

Easement Revenue

Land easement revenue is recognized monthly as earned and is included in other income.

Pipeline Transportation Revenue

Revenue from our pipeline operations is derived from fee-based contracts and is typically based on transportation fees per unit of volume transported multiplied by the volume delivered. Revenue is recognized when volumes have been physically delivered for the customer through the pipeline.

Deferred Revenue

On February 5, 2014, we entered into an Asset Sale Agreement (the “Purchase Agreement”) with WBI Energy Midstream, LLC, a Colorado limited liability company (“WBI”), whereby we reacquired WBI’s 1/6th interest in the Blue Dolphin Pipeline System, the Galveston Area Block 350 Pipeline, and the Omega Pipeline (the “Pipeline Assets”) effective October 31, 2013. Pursuant to the Purchase Agreement, WBI paid us $100,000 in cash, and a surety company $850,000 in cash as collateral for supplemental pipeline bonds for our benefit in exchange for the payment and discharge of any and all payables, claims, and obligations related to the Pipeline Assets. We recorded the amount received for our benefit for the supplemental pipeline bonds as deferred revenue. The deferred revenue is being recognized on a straight-line basis through December 31, 2018, the expected retirement date of the assets that the supplemental pipeline bonds secure.

9

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Income Taxes

We account for income taxes under FASB ASC guidance related to income taxes, which requires recognition of income taxes based on amounts payable with respect to the current year and the effects of deferred taxes for the expected future tax consequences of events that have been included in our financial statements or tax returns. Under this method, deferred tax assets and liabilities are determined based on the differences between the financial accounting and tax basis of assets and liabilities, as well as for operating losses and tax credit carryforwards using enacted tax rates in effect for the year in which the differences are expected to reverse.

As of each reporting date, management considers new evidence, both positive and negative, to determine the realizability of deferred tax assets. Management considers whether it is more likely than not that some portion or all of the deferred tax assets will be realized, which is dependent upon the generation of future taxable income prior to the expiration of any net operating loss (“NOL”) carryforwards. When management determines that it is more likely than not that a tax benefit will not be realized, a valuation allowance is recorded to reduce deferred tax assets.

The guidance also prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return, as well as guidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosures, and transition.

See “Note (17) Income Taxes” of this report for further information related to income taxes.

Impairment or Disposal of Long-Lived Assets

In accordance with FASB ASC guidance on accounting for the impairment or disposal of long-lived assets, we periodically evaluate our long-lived assets for impairment. Additionally, we evaluate our long-lived assets when events or circumstances indicate that the carrying value of these assets may not be recoverable. The carrying value is not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the asset or group of assets. If the carrying value exceeds the sum of the undiscounted cash flows, an impairment loss equal to the amount by which the carrying value exceeds the fair value of the asset or group of assets is recognized. Significant management judgment is required in the forecasting of future operating results that are used in the preparation of projected cash flows and, should different conditions prevail or judgments be made, material impairment charges could be necessary.

Asset Retirement Obligations

FASB ASC guidance related to asset retirement obligations (“AROs”) requires that a liability for the discounted fair value of an ARO be recorded in the period in which it is incurred and the corresponding cost capitalized by increasing the carrying amount of the related long-lived asset. The liability is accreted towards its future value each period, and the capitalized cost is depreciated over the useful life of the related asset. If the liability is settled for an amount other than the recorded amount, a gain or loss is recognized.

Management has concluded that there is no legal or contractual obligation to dismantle or remove the refinery and facilities. Further, management believes that these assets have indeterminate lives under FASB ASC guidance for estimating AROs because dates or ranges of dates upon which we would retire these assets cannot reasonably be estimated at this time. When a date or range of dates can reasonably be estimated for the retirement of these assets, we will estimate the cost of performing the retirement activities and record a liability for the fair value of that cost using present value techniques.

We recorded an ARO liability related to future asset retirement costs associated with dismantling, relocating, or disposing of our offshore platform, pipeline systems, and related onshore facilities, as well as for plugging and abandoning wells and restoring land and sea beds. We developed these cost estimates for each of our assets based upon regulatory requirements, structural makeup, water depth, reservoir characteristics, reservoir depth, equipment demand, current retirement procedures, and construction and engineering consultations. Because these costs typically extend many years into the future, estimating future costs are difficult and require management to make judgments that are subject to future revisions based upon numerous factors, including changing technology, political, and regulatory environments. We review our assumptions and estimates of future abandonment costs on an annual basis.

See “Note (12) Asset Retirement Obligations” of this report for additional information related to our AROs.

10

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Computation of Earnings Per Share

We apply the provisions of FASB ASC guidance for computing earnings per share (“EPS”). The guidance requires the presentation of basic EPS, which excludes dilution and is computed by dividing net income available to common stockholders by the weighted-average number of shares of common stock outstanding for the period. The guidance requires dual presentation of basic EPS and diluted EPS on the face of our consolidated statements of income and requires a reconciliation of the numerators and denominators of basic EPS and diluted EPS. Diluted EPS is computed by dividing net income available to common stockholders by the diluted weighted average number of common shares outstanding, which includes the potential dilution that could occur if securities or other contracts to issue shares of common stock were converted to common stock that then shared in the earnings of the entity.

The number of shares related to options, warrants, restricted stock, and similar instruments included in diluted EPS is based on the “Treasury Stock Method” prescribed in FASB ASC guidance for computation of EPS. This method assumes theoretical repurchase of shares using proceeds of the respective stock option or warrant exercised, and, for restricted stock, the amount of compensation cost attributed to future services that has not yet been recognized and the amount of any current and deferred tax benefit that would be credited to additional paid-in-capital upon the vesting of the restricted stock, at a price equal to the issuer’s average stock price during the related earnings period. Accordingly, the number of shares includable in the calculation of EPS in respect of the stock options, warrants, restricted stock, and similar instruments is dependent on this average stock price and will increase as the average stock price increases. See “Note (18) Earnings Per Share” for additional information related to EPS.

Stock-Based Compensation

In accordance with FASB ASC guidance for stock-based compensation, share-based payments to personnel, including grants of restricted stock units, are measured at fair value as of the date of grant and are expensed in our consolidated statements of income over the service period (generally the vesting period).

Treasury Stock

We account for treasury stock under the cost method. When treasury stock is re-issued, the net change in share price subsequent to acquisition of the treasury stock is recognized as a component of additional paid-in-capital in our consolidated balance sheets. See “Note (14) Treasury Stock” for additional disclosures related to treasury stock.

Reclassification

We have reclassified certain insignificant prior period amounts related to our tank rental revenue to conform to our 2015 presentation.

New Pronouncements Issued but Not Yet Effective

FASB issues an Accounting Standards Update (“ASU”) to communicate changes to the FASB ASC, including changes to non-authoritative SEC content. The following are recently issued, but not yet effective, accounting standards that may have an effect on our consolidated financial position, results of operations, or cash flows:

|

·

|

Revenue from Contracts with Customers (“ASU 2014-09”) – In May 2014, FASB issued ASU 2014-09, which outlines a new, single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes most current revenue recognition guidance, including industry-specific guidance. This new revenue recognition model provides a five-step analysis in determining when and how revenue is recognized. The new model will require revenue recognition to depict the transfer of promised goods or services to customers in an amount that reflects the consideration a company expects to receive in exchange for those goods or services.

|

In August 2015, FASB issued Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date, which defers the effective date of ASU 2014-09 for all entities by one year. The effective date for public business entities is annual reporting periods beginning after December 15, 2017. Public business entities would apply the new revenue standard to interim reporting periods after December 15, 2017. As such, for a public business entity with a calendar year-end, ASU 2014-09 would be effective on January 1, 2018, for both its interim and annual reporting periods. This represents a one-year deferral from the original effective date. The new effective date guidance allows early adoption for all entities as of the original effective date (December 15, 2016). We are evaluating the impact that adoption of this guidance will have on the determination or reporting of our financial results.

11

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

|

·

|

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern (“ASU 2014-15”) – In August 2014, FASB issued ASU 2014-15, which requires management to perform interim and annual assessments of an entity’s ability to continue as a going concern for a one year period subsequent to the date of the financial statements. An entity must provide certain disclosures if conditions or events raise substantial doubt about the entity’s ability to continue as a going concern. The guidance is effective for all entities for the first annual period ending after December 15, 2016 and interim periods thereafter, with early adoption permitted. We do not anticipate adoption of this guidance to have a material effect on our consolidated financial statements.

|

|

·

|

Inventory (Topic 330): Simplifying the Measurement of Inventory (“ASU 2015-11”) – In July 2015, FASB issued ASU 2015-11. Current guidance requires an entity to measure inventory at the lower of cost or market. Market could be replacement cost, net realizable value, or net realizable value less an approximately normal profit margin. Under ASU 2015-11, an entity should measure inventory at the lower of cost or net realizable value. Net realizable value is the estimated selling price in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. Amendments under ASU 2015-11 more closely align the measurement of inventory in GAAP with the measurement of inventory in International Financial Reporting Standards. For public business entities, ASU 2015-11 is effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. ASU 2015-11 should be applied prospectively with earlier application permitted as of the beginning of an interim or annual reporting period. We do not anticipate adoption of this guidance to have a material effect on our consolidated financial statements.

|

|

·

|

Interest – Imputation of Interest: Simplifying the Presentation of Debt Issuance Costs ("ASU 2015-03") – In April 2015, FASB issued ASU 2015-03, which requires debt issue costs related to a recognized debt liability to be presented in the balance sheet as a direct deduction from the carrying value of that debt liability, consistent with debt discounts. The recognition and measurement guidance for debt issue costs are not affected by ASU 2015-03. The amendments in this ASU are effective retrospectively for fiscal years, and interim periods within those years, beginning after December 15, 2015. Early adoption is permitted. We do not anticipate adoption of this guidance to have a material effect on our consolidated financial statements.

|

|

·

|

Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements (“ASU 2015-15”) – In August 2015, FASB issued ASU 2015-15, which amends ASU 2015-03 by clarifying the presentation and subsequent measurement of debt issuance costs associated with lines of credit. These costs may be presented as an asset and amortized ratably over the term of the line of credit arrangement, regardless of whether there are outstanding borrowings on the arrangement. The effective date will be the first quarter of fiscal year 2016 and will be applied retrospectively. We do not anticipate adoption of this guidance to have a material effect on our consolidated financial statements.

|

Other new pronouncements issued but not effective until after September 30, 2015 are not expected to have a material impact on our financial position, results of operations or liquidity.

Remainder of Page Intentionally Left Blank

12

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

|

(4)

|

Business Segment Information

|

We have two reportable business segments: (i) Refinery Operations and (ii) Pipeline Transportation. Business activities related to our Refinery Operations business segment are conducted at the Nixon Facility. Business activities related to our Pipeline Transportation business segment are primarily conducted in the Gulf of Mexico through our Pipeline Assets and leasehold interests in oil and gas properties.

Business segment information for the three months ended September 30, 2015 and 2014 (and at September 30, 2015 and 2014), was as follows:

|

Three Months Ended September 30, 2015

|

Three Months Ended September 30, 2014

|

|||||||||||||||||||||||||||||||

|

Segment

|

Segment

|

|||||||||||||||||||||||||||||||

|

Refinery

|

Pipeline

|

Corporate &

|

Refinery

|

Pipeline

|

Corporate &

|

|||||||||||||||||||||||||||

|

Operations

|

Transportation

|

Other

|

Total

|

Operations

|

Transportation

|

Other

|

Total

|

|||||||||||||||||||||||||

|

Revenue from operations

|

$ | 55,210,962 | $ | 45,925 | $ | - | $ | 55,256,887 | $ | 88,129,273 | $ | 56,900 | $ | - | $ | 88,186,173 | ||||||||||||||||

|

Less: cost of operations(1)

|

(51,444,705 | ) | (114,675 | ) | (236,816 | ) | (51,796,196 | ) | (85,261,533 | ) | (110,872 | ) | (274,674 | ) | (85,647,079 | ) | ||||||||||||||||

|

Other non-interest income(2)

|

- | 62,500 | 660,000 | 722,500 | - | - | - | - | ||||||||||||||||||||||||

|

Adjusted EBITDA

|

3,766,257 | (6,250 | ) | 423,184 | 4,183,191 | 2,867,740 | (53,972 | ) | (274,674 | ) | 2,539,094 | |||||||||||||||||||||

|

Less: JMA Profit Share(3)

|

(1,435,376 | ) | - | - | (1,435,376 | ) | (1,094,383 | ) | - | - | (1,094,383 | ) | ||||||||||||||||||||

|

EBITDA

|

$ | 2,330,881 | $ | (6,250 | ) | $ | 423,184 | $ | 1,773,357 | $ | (53,972 | ) | $ | (274,674 | ) | |||||||||||||||||

|

Depletion, depreciation and amortization

|

(414,837 | ) | (393,871 | ) | ||||||||||||||||||||||||||||

|

Interest expense, net

|

(380,342 | ) | (212,594 | ) | ||||||||||||||||||||||||||||

|

Income before income taxes

|

1,952,636 | 838,246 | ||||||||||||||||||||||||||||||

|

Income tax expense

|

(688,403 | ) | (22,199 | ) | ||||||||||||||||||||||||||||

|

Net income

|

$ | 1,264,233 | $ | 816,047 | ||||||||||||||||||||||||||||

|

Capital expenditures

|

$ | 3,640,801 | $ | - | $ | - | $ | 3,640,801 | $ | 815,849 | $ | - | $ | - | $ | 815,849 | ||||||||||||||||

|

Identifiable assets(4)

|

$ | 79,442,106 | $ | 3,303,803 | $ | 3,405,977 | $ | 86,151,886 | $ | 57,520,835 | $ | 2,998,619 | $ | 523,533 | $ | 61,042,987 | ||||||||||||||||

|

(1)

|

Operation cost within the Refinery Operations and Pipeline Transportation segments includes related general, administrative, and accretion expenses. Operation cost within Corporate and Other includes general and administrative expenses associated with corporate maintenance costs, such as accounting fees, director fees, and legal expense.

|

|

(2)

|

Other non-interest income reflects FLNG easement revenue and the Grynberg Settlement Agreement. See “Part 1, Item 1. Financial Statements - Note (21) Commitments and Contingencies – FLNG Master Easement Agreement and Grynberg Settlement Agreement” of this report for further discussion related to FLNG and Grynberg.

|

|

(3)

|

The Joint Marketing Agreement profit share (the “JMA Profit Share”) represents the GEL Profit Share plus the Performance Fee for the period pursuant to the Joint Marketing Agreement. See “Note (21) Commitments and Contingencies – Genesis Agreements” and “Part 1, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Relationship with Genesis” of this report for further discussion related to the Joint Marketing Agreement.

|

|

(4)

|

Identifiable assets contain related legal obligations of each business segment including cash, accounts receivable, and recorded net assets.

|

13

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Business segment information for the nine months ended September 30, 2015 and 2014 (and at September 30, 2015 and 2014), was as follows:

|

Nine Months Ended September 30, 2015

|

Nine Months Ended September 30, 2014

|

|||||||||||||||||||||||||||||||

|

Segment

|

Segment

|

|||||||||||||||||||||||||||||||

|

Refinery

|

Pipeline

|

Corporate &

|

Refinery

|

Pipeline

|

Corporate &

|

|||||||||||||||||||||||||||

|

Operations

|

Transportation

|

Other

|

Total

|

Operations

|

Transportation

|

Other

|

Total

|

|||||||||||||||||||||||||

|

Revenue from operations

|

$ | 175,690,968 | $ | 119,882 | $ | - | $ | 175,810,850 | $ | 311,786,529 | $ | 178,793 | $ | - | $ | 311,965,322 | ||||||||||||||||

|

Less: cost of operations(1)

|

(160,208,576 | ) | (296,291 | ) | (928,331 | ) | (161,433,198 | ) | (297,956,882 | ) | (355,645 | ) | (973,154 | ) | (299,285,681 | ) | ||||||||||||||||

|

Other non-interest income(2)

|

- | 187,500 | 660,000 | 847,500 | - | 208,333 | - | 208,333 | ||||||||||||||||||||||||

|

Adjusted EBITDA

|

15,482,392 | 11,091 | (268,331 | ) | 15,225,152 | 13,829,647 | 31,481 | (973,154 | ) | 12,887,974 | ||||||||||||||||||||||

|

Less: JMA Profit Share(3)

|

(4,812,674 | ) | - | - | (4,812,674 | ) | (2,334,487 | ) | - | - | (2,334,487 | ) | ||||||||||||||||||||

|

EBITDA

|

$ | 10,669,718 | $ | 11,091 | $ | (268,331 | ) | $ | 11,495,160 | $ | 31,481 | $ | (973,154 | ) | ||||||||||||||||||

|

Depletion, depreciation and amortization

|

(1,217,005 | ) | (1,175,643 | ) | ||||||||||||||||||||||||||||

|

Interest expense, net

|

(1,313,247 | ) | (630,175 | ) | ||||||||||||||||||||||||||||

|

Income before income taxes

|

7,882,226 | 8,747,669 | ||||||||||||||||||||||||||||||

|

Income tax expense

|

(2,778,750 | ) | (298,792 | ) | ||||||||||||||||||||||||||||

|

Net income

|

$ | 5,103,476 | $ | 8,448,877 | ||||||||||||||||||||||||||||

|

Capital expenditures

|

$ | 9,900,295 | $ | - | $ | - | $ | 9,900,295 | $ | 1,145,720 | $ | - | $ | - | $ | 1,145,720 | ||||||||||||||||

|

Identifiable assets(4)

|

$ | 79,442,106 | $ | 3,303,803 | $ | 3,405,977 | $ | 86,151,886 | $ | 57,520,835 | $ | 2,998,619 | $ | 523,533 | $ | 61,042,987 | ||||||||||||||||

|

(1)

|

Operation cost within the Refinery Operations and Pipeline Transportation segments includes related general, administrative, and accretion expenses. Operation cost within Corporate and Other includes general and administrative expenses associated with corporate maintenance costs, such as accounting fees, director fees, and legal expense.

|

|

(2)

|

Other non-interest income reflects FLNG easement revenue and the Grynberg Settlement Agreement. See “Part 1, Item 1. Financial Statements - Note (21) Commitments and Contingencies – FLNG Master Easement Agreement and Grynberg Settlement Agreement” of this report for further discussion related to FLNG and Grynberg.

|

|

(3)

|

The JMA Profit Share represents the GEL Profit Share plus the Performance Fee for the period pursuant to the Joint Marketing Agreement. See “Note (21) Commitments and Contingencies – Genesis Agreements” and “Part 1, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Relationship with Genesis” of this report for further discussion related to the Joint Marketing Agreement.

|

|

(4)

|

Identifiable assets contain related legal obligations of each business segment including cash, accounts receivable, and recorded net assets.

|

|

(5)

|

Prepaid Expenses and Other Current Assets

|

Prepaid expenses and other current assets consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Prepaid related party operating expenses

|

$ | 712,688 | $ | - | ||||

|

Prepaid insurance

|

196,305 | 156,558 | ||||||

|

Unrealized hedging gains

|

133,150 | 495,900 | ||||||

|

Prepaid listing fees

|

3,750 | 15,000 | ||||||

|

Prepaid professional fees

|

- | 104,000 | ||||||

| $ | 1,045,893 | $ | 771,458 | |||||

14

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

|

(6)

|

Deposits

|

Deposits consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Construction deposits

|

$ | 300,000 | $ | - | ||||

|

Equipment deposits

|

100,463 | 48,785 | ||||||

|

Utility deposits

|

10,250 | 10,250 | ||||||

|

Rent deposits

|

9,463 | 9,463 | ||||||

| $ | 420,176 | $ | 68,498 | |||||

|

(7)

|

Inventory

|

Inventory consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

HOBM

|

$ | 3,044,646 | $ | 124,176 | ||||

|

Jet fuel

|

1,557,847 | 2,631,546 | ||||||

|

AGO

|

403,875 | 224,007 | ||||||

|

Naphtha

|

362,049 | 194,688 | ||||||

|

Chemicals

|

216,208 | - | ||||||

|

Crude oil and condensate

|

19,041 | 19,041 | ||||||

|

Propane

|

12,817 | - | ||||||

|

LPG mix

|

4,344 | 7,193 | ||||||

| $ | 5,620,827 | $ | 3,200,651 | |||||

|

(8)

|

Property, Plant and Equipment, Net

|

Property, plant and equipment, net, consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Refinery and facilities

|

$ | 39,969,028 | $ | 36,462,451 | ||||

|

Pipelines and facilities

|

2,127,207 | 2,127,207 | ||||||

|

Onshore separation and handling facilities

|

325,435 | 325,435 | ||||||

|

Land

|

602,938 | 602,938 | ||||||

|

Other property and equipment

|

644,795 | 597,064 | ||||||

| 43,669,403 | 40,115,095 | |||||||

|

Less: Accumulated depletion, depreciation, and amortization

|

(5,803,580 | ) | (4,586,575 | ) | ||||

| 37,865,823 | 35,528,520 | |||||||

|

Construction in progress

|

8,188,542 | 1,842,555 | ||||||

| $ | 46,054,365 | $ | 37,371,075 | |||||

15

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

|

(9)

|

Debt Issue Costs

|

Debt issue costs, net of accumulated amortization, totaled $1,296,480 and $479,737 at September 30, 2015 and December 31, 2014, respectively. Debt issue costs at September 30, 2015 related to loan agreements with Sovereign. Debt issue costs at December 31, 2014 related to a loan agreement with American First National Bank.

Accumulated amortization totaled $22,781 and $211,244 at September 30, 2015 and December 31, 2014, respectively. Amortization expense, which is included in interest expense, was $17,086 and $8,450 for the three months ended September 30, 2015 and 2014, respectively. Amortization expense was $517,652 and $25,350 for the nine months ended September 30, 2015 and 2014, respectively. Amortization expense for the nine months ended September 30, 2015 included $456,287 related to writing off debt issue costs associated with the refinance of debt owed to American First National Bank.

See “Note (13) Long-Term Debt” of this report for additional disclosures related to the loan agreements with Sovereign and American First National Bank.

|

(10)

|

Accounts Payable, Related Party

|

LEH manages and operates all of our properties pursuant to the Operating Agreement. For services rendered, LEH receives reimbursements and fees as follows:

|

·

|

Reimbursements – For management and operation of all properties excluding the Nixon Facility, LEH is reimbursed at cost for all reasonable expenses incurred while performing the services. Unsettled reimbursements are reflected within either prepaid expenses or accounts payable, related party in our consolidated balance sheets. Amounts reimbursed to LEH are reflected in the appropriate asset or expense accounts in our consolidated statements of income. |

|

·

|

Fees – For management and operation of the Nixon Facility, LEH receives fees: (i) in the form of weekly payments from GEL TEX Marketing, LLC (“GEL”) not to exceed $750,000 per month, (ii) $0.25 for each barrel processed at the Nixon Facility up to a maximum quantity of 10,000 barrels per day determined on a monthly basis, and (iii) $2.50 for each barrel processed at the Nixon Facility in excess of 10,000 barrels per day determined on a monthly basis. In the normal course of business, we make estimates and assumptions related to amounts expensed for fees since actual amounts can vary depending upon production volumes. We then use the cumulative catch-up method to account for revisions in estimates, which may result in prepaid expenses or accounts payable, related party on our consolidated balance sheets. Amounts expensed as fees are reflected as refinery operating expenses in our consolidated statements of income. |

At September 30, 2015, we were in a prepaid position with respect to fees and reimbursements under the Operating Agreement. Prepaid related party operating expenses totaled $712,688 and $0 at September 30, 2015 and December 31, 2014, respectively. Accounts payable, related party totaled $0 and $1,174,168 at September 30, 2015 and December 31, 2014, respectively.

For the three months ended September 30, 2015 and 2014, refinery operating expenses totaled $2,953,528 (approximately $2.66 per barrel of throughput) and $2,496,514 (approximately $2.94 per barrel of throughput), respectively. For the nine months ended September 30, 2015 and 2014, refinery operating expenses totaled $8,420,650 (approximately $2.73 per barrel of throughput) and $8,092,738 (approximately $2.78 per barrel of throughput), respectively.

The Operating Agreement expires upon the earliest to occur of: (a) the date of the termination of the Joint Marketing Agreement pursuant to its terms, (b) August 12, 2018, or (c) upon written notice of either party to the Operating Agreement of a material breach of the Operating Agreement by the other party.

16

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

|

(11)

|

Accrued Expenses and Other Current Liabilities

|

Accrued expenses and other current liabilities consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Excise and income taxes payable

|

$ | 1,489,921 | $ | 1,228,411 | ||||

|

Other payable

|

175,634 | 149,962 | ||||||

|

Genesis JMA Profit Share payable

|

162,470 | 521,739 | ||||||

|

Property taxes

|

92,002 | - | ||||||

|

Board of director fees payable

|

85,179 | 345,000 | ||||||

|

Transportation and inspection

|

- | 190,000 | ||||||

|

Unearned revenue

|

- | 252,500 | ||||||

|

Insurance

|

- | 96,092 | ||||||

| $ | 2,005,206 | $ | 2,783,704 | |||||

|

(12)

|

Asset Retirement Obligations

|

Refinery and Facilities

Management has concluded that there is no legal or contractual obligation to dismantle or remove the refinery and facilities. Management believes that the refinery and facilities have indeterminate lives under FASB ASC guidance for estimating AROs because dates or ranges of dates upon which we would retire these assets cannot reasonably be estimated at this time. When a date or range of dates can reasonably be estimated for the retirement of these assets, we will estimate the cost of performing the retirement activities and record a liability for the fair value of that cost using present value techniques.

Pipelines and Facilities and Oil and Gas Properties

We have AROs associated with the dismantlement and abandonment in place of our pipelines and facilities, as well as the plugging and abandonment of our oil and gas properties. We recorded a discounted liability for the fair value of an ARO with a corresponding increase to the carrying value of the related long-lived asset at the time the asset was installed or placed in service. We amortize the amount added to property and equipment and recognize accretion expense in connection with the discounted liability over the remaining life of the asset.

Plugging and abandonment costs for oil and gas properties and pipelines are recorded as information becomes available from operators to substantiate actual and/or probable costs. Abandonment costs that exceed the asset’s ARO liability are recorded as abandonment expense during the period incurred. For the three and nine months ended September 30, 2015 and 2014, we did not incur any abandonment expense related to our oil and gas properties.

17

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

AROs on a roll-forward basis were as follows:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Asset retirement obligations, at the beginning of the period

|

$ | 1,866,770 | $ | 1,597,661 | ||||

|

New asset retirement obligations and adjustments

|

49 | 300,980 | ||||||

|

Liabilities settled

|

(58,459 | ) | (243,866 | ) | ||||

|

Accretion expense

|

158,655 | 211,995 | ||||||

| 1,967,015 | 1,866,770 | |||||||

|

Less: current portion of asset retirement obligations

|

(38,644 | ) | (85,846 | ) | ||||

|

Long-term asset retirement obligations, at the end of the period

|

$ | 1,928,371 | $ | 1,780,924 | ||||

The WBI transaction resulted in a $300,980 increase in our AROs related to the Pipeline Assets, which represents the fair value of the liability, and increased accretion expense throughout the remaining useful life of certain of the Pipeline Assets. For additional information related to the WBI Transaction, see “Note (3) Significant Accounting Policies – Revenue Recognition – Deferred Revenue” and “Note (21) Commitments and Contingencies – Supplemental Pipeline Bonds” of this report.

|

(13)

|

Long-Term Debt

|

Long-term debt consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Term Loan Due 2034

|

$ | 24,822,362 | $ | - | ||||

|

Term Loan Due 2016

|

3,000,000 | - | ||||||

|

Notre Dame Debt

|

1,300,000 | 1,300,000 | ||||||

|

Term Loan Due 2017

|

1,109,962 | 1,638,898 | ||||||

|

Capital Leases

|

347,236 | 466,401 | ||||||

|

Refinery Note

|

- | 8,648,980 | ||||||

| 30,579,560 | 12,054,279 | |||||||

|

Less: current portion of long-term debt

|

(1,631,539 | ) | (1,245,476 | ) | ||||

| $ | 28,948,021 | $ | 10,808,803 | |||||

Term Loan Due 2034

We entered into a Loan and Security Agreement with Sovereign on June 22, 2015, as administrative agent and lender pursuant to a term loan in the principal amount of $25.0 million (the “Term Loan Due 2034”). The Term Loan Due 2034 matures in June 2034, has a monthly payment of principal and interest of $185,289, and accrues interest at a rate based on the Wall Street Journal Prime Rate plus 2.75%. Pursuant to a construction rider in the Term Loan Due 2034, proceeds available for use were placed in a disbursement account whereby Sovereign makes payments for construction related expenses. Amounts held in the disbursement account are reflected as restricted cash and restricted cash, noncurrent in our consolidated balance sheets. The principal balance outstanding on the Term Loan Due 2034 was $24,822,362 and $0 at September 30, 2015 and December 31, 2014, respectively. Interest was accrued on the Term Loan Due 2034 in the amount of $33,102 and $0 at September 30, 2015 and December 31, 2014, respectively.

As a condition of the Term Loan Due 2034, Jonathan P. Carroll was required to guarantee repayment of funds borrowed and interest accrued under the loan. For his personal guarantee, we entered into a Guaranty Fee Agreement with Jonathan P. Carroll whereby he receives a contingent fee equal to 2.00% per annum, paid monthly, of the outstanding principal balance owed under the Term Loan Due 2034. For the three and nine months ended September 30, 2015 and 2014, guaranty fees related to the Term Loan Due 2034 totaled $142,002. There were no guaranty fees paid in 2014 related to the Term Loan Due 2034. Guaranty fees are recognized monthly as incurred and are included in other income as interest expense. LEH, LRM and Blue Dolphin also guaranteed the Term Loan Due 2034. See “Note (10) Accounts Payable, Related Party” of this report for additional disclosures related to LEH.

18

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

Proceeds of the Term Loan Due 2034 were used to refinance approximately $8.5 million of debt owed to American First National Bank under the Refinery Note. Remaining proceeds are being used primarily to construct new petroleum storage tanks. The Term Loan Due 2034 is secured by: (i) a first lien on all Nixon Facility business assets (excluding accounts receivable and inventory), (ii) assignment of all Nixon Facility contracts, permits, and licenses, (iii) absolute assignment of Nixon Facility rents and leases, including tank rental income, (iv) a $1.0 million payment reserve account held by Sovereign, and (v) a pledge of $5.0 million of a life insurance policy on Jonathan P. Carroll. The Term Loan Due 2034 contains representations and warranties, affirmative, restrictive, and financial covenants, as well as events of default which are customary for credit facilities of this type.

Term Loan Due 2016

We entered into a Loan and Security Agreement with Sovereign as lender on June 22, 2015, for a term note in the principal amount of $3,000,000 (the “Term Loan Due 2016”). The Term Loan Due 2016 was amended on November 10, 2015, pursuant to a Loan Modification Agreement (the "November Loan Modification Agreement"). Under the November Loan Modification Agreement, the due date was extended to November 2016. The Term Loan Due 2016 accrues interest at the greater of the Wall Street Journal Prime Rate plus 2.75% or 6.00%. The Term Loan Due 2016 requires payment of interest with full payment of the outstanding principal due at maturity. The principal balance outstanding on the Term Loan Due 2016 was $3,000,000 and $0 at September 30, 2015 and December 31, 2014, respectively. Interest was accrued on the Term Loan Due 2016 in the amount of $15,500 and $0 at September 30, 2015 and December 31, 2014, respectively.

As a condition of the Term Loan Due 2016, Jonathan P. Carroll was required to guarantee repayment of funds borrowed and interest accrued under the loan. For his personal guarantee, we entered into a Guaranty Fee Agreement with Jonathan P. Carroll whereby he receives a contingent fee equal to 2.00% per annum, paid monthly, of the outstanding principal balance owed under the Term Loan Due 2016. For the three and nine months ended September 30, 2015 and 2014, guaranty fees related to the Term Loan Due 2016 totaled $16,500. There were no guaranty fees paid in 2014 related to the Term Loan Due 2016. Guaranty fees are recognized monthly as incurred and are included in other income as interest expense. LE and Blue Dolphin also guaranteed the Term Loan Due 2016.

Proceeds of the Term Loan Due 2016 were used to purchase idle refinery equipment for the Nixon Facility. The Term Loan Due 2016 is secured by: (i) a first lien on the equipment that was purchased, (ii) a $1.5 million certificate of deposit at Sovereign, (iii) assignment of an easement agreement on land in Freeport, Texas (iv) a second lien on all LRM assets (excluding accounts receivable and inventory), and (v) a second lien and deed of trust on the Nixon Facility. The Term Loan Due 2016 contains representations and warranties, affirmative, restrictive, and financial covenants, as well as events of default which are customary for credit facilities of this type.

Notre Dame Debt

We entered into a loan with Notre Dame Investors, Inc. as evidenced by a Promissory Note in the original principal amount of $8.0 million, which is currently held by John Kissick (the “Notre Dame Debt”). The Notre Dame Debt matures in January 2017, and accrues interest at a rate of 16.00%. The principal balance outstanding on the Notre Dame Debt was $1,300,000 at September 30, 2015 and December 31, 2014. Interest was accrued on the Notre Dame Debt in the amount of $1,430,371 and $1,274,789 at September 30, 2015 and December 31, 2014, respectively.

The Notre Dame Debt is secured by a Deed of Trust, Security Agreement and Financing Statements (the “Subordinated Deed of Trust”), which encumbers the Nixon Facility and general assets of LE. There are no financial maintenance covenants associated with the Notre Dame Debt. Pursuant to a Subordination Agreement dated June 22, 2015, the holder of the Notre Dame Debt agreed to subordinate its interest and liens on the Nixon Facility and general assets of LE first in favor of Sovereign as holder of the Term Loan Due 2034 and second in favor of GEL. See “Note (21) Commitments and Contingencies” of this report for additional disclosures related to the Genesis Agreements.

Term Loan Due 2017

We entered into a Loan and Security Agreement with Sovereign on May 2, 2014, for a term loan facility in the principal amount of $2.0 million (the “Term Loan Due 2017”). The Term Loan Due 2017 was amended on March 25, 2015, pursuant to a Loan Modification Agreement (the “March Loan Modification Agreement”). Under the March Loan Modification Agreement, the interest rate was modified to be the greater of the U.S. Prime Rate plus 2.75% or 6.00% and the due date was extended to March 2017. Pursuant to the March Loan Modification Agreement, the monthly payment due under the Term Loan Due 2017 is $61,665 plus interest. The principal balance outstanding on the Term Loan Due 2017 was $1,109,962 and $1,638,898 at September 30, 2015 and December 31, 2014, respectively. Interest was accrued on the Term Loan Due 2017 in the amount of $5,550 and $8,470 at September 30, 2015 and December 31, 2014, respectively.

19

Blue Dolphin Energy Company & Subsidiaries

Notes to Consolidated Financial Statements (Unaudited) - Continued

As a condition of the Term Loan Due 2017, Jonathan P. Carroll was required to guarantee repayment of funds borrowed and interest accrued under the loan. For his personal guarantee, we entered into a Guaranty Fee Agreement with Jonathan P. Carroll whereby he receives a contingent fee equal to 2.00% per annum, paid monthly, of the outstanding principal balance owed under the Term Loan Due 2017. For the three and nine months ended September 30, 2015 and 2014, guaranty fees related to the Term Loan Due 2017 totaled $6,506. There were no guaranty fees paid in 2014 related to the Term Loan Due 2017. Guaranty fees are recognized monthly as incurred and are included in other income as interest expense.

The proceeds of the Term Loan Due 2017 were used primarily to finance costs associated with refurbishment of the Nixon Facility’s naphtha stabilizer and depropanizer units. The Term Loan Due 2017 is: (i) subject to a financial maintenance covenant pertaining to debt service coverage ratio and (ii) secured by the assignment of certain leases of LRM and assets of LEH. See “Note (10) Accounts Payable, Related Party” of this report for additional disclosures related to LEH.

Capital Leases

We entered into a 36 month “build-to-suit” capital lease on August 7, 2014, for the purchase of new boiler equipment for the Nixon Facility. The equipment was delivered in December 2014 and the cost was added to construction in progress. Once placed in service, the equipment will be reclassified to refinery and facilities and depreciation will begin. The capital lease requires a quarterly payment in the amount of $42,996. Capital lease obligations totaled $347,236 and $466,401 at September 30, 2015 and December 31, 2014, respectively. Interest was accrued on capital leases in the amount of $2,988 and $0 at September 30, 2015 and December 31, 2014, respectively.

The following is a summary of equipment held under long-term capital leases:

|

September 30,

|

December 31,

|

|||||||

|

2015

|

2014

|

|||||||

|

Boiler equipment

|

$ | 538,598 | $ | 538,598 | ||||

|

Less: accumulated depreciation

|

- | - | ||||||

| $ | 538,598 | $ | 538,598 | |||||

Refinery Note

We entered into a Loan Agreement with First International Bank on September 29, 2008, in the principal amount of $10.0 million (the “Refinery Note”). The Refinery Note was subsequently acquired by American First National Bank. The Refinery Note matured in October 2028 and accrued interest at a rate based on the U.S. Prime Rate plus 2.25%. The principal balance outstanding on the Refinery Note was $0 and $8,648,980 at September 30, 2015 and December 31, 2014, respectively. Interest was accrued on the Refinery Note in the amount of $0 and $47,569 at September 30, 2015 and December 31, 2014, respectively. All amounts due and outstanding under the Refinery Note were repaid in June 2015.

|

(14)

|

Treasury Stock

|

At September 30, 2015 and December 31, 2014, we had 150,000 shares of treasury stock.

|

(15)

|

Concentration of Risk

|

Key Supplier

Under the Crude Oil and Supply Throughput Services Agreement dated August 12, 2011 (the “Crude Supply Agreement”), GEL is our exclusive supplier of crude oil and condensate. We have the ability to purchase crude oil and condensate from other suppliers with the prior consent of GEL. The initial term was to expire on August 12, 2014. However, on October 30, 2013, we entered into a Letter Agreement Regarding Certain Advances and Related Agreements with GEL and Milam Services, Inc. (“Milam”)(the “October 2013 Letter Agreement”), effective October 24, 2013. In accordance with the terms of the October 2013 Letter Agreement, we agreed not to terminate the Crude Supply Agreement and GEL agreed to automatically renew the Crude Supply Agreement at the end of the initial term for successive one year periods until August 12, 2019, unless sooner terminated by GEL with 180 days prior written notice.

20

Blue Dolphin Energy Company & Subsidiaries