Attached files

| file | filename |

|---|---|

| 8-K/A - INVESTORS REAL ESTATE TRUST 8-K A 6-29-2015 - CENTERSPACE | form8ka.htm |

Exhibit 99.2

Fourth Quarter Fiscal 2015

Supplemental Operating and Financial Data

for the Quarter Ended April 30, 2015

|

CONTACT:

Cindy Bradehoft

Director of Investor Relations

Direct Dial: 952-401-4835

E-Mail: cbradehoft@iret.com

|

1400 31st Avenue SW, Suite 60

Minot, ND 58701

Tel: 701.837.4738

Fax: 701.838.7785

www.iret.com

|

Supplemental Financial and Operating Data

April 30, 2015

|

Page

|

|

|

Company Background and Highlights

|

2

|

|

Property Cost by Segment and by State

|

5

|

|

Key Financial Data

|

|

|

Condensed Consolidated Balance Sheets

|

6

|

|

Condensed Consolidated Statements of Operations

|

7

|

|

Funds From Operations

|

8

|

|

Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (Adjusted EBITDA)

|

9

|

|

Capital Analysis

|

|

|

Long-Term Mortgage Debt Analysis

|

10

|

|

Long-Term Mortgage Debt Detail

|

11-13

|

|

Capital Analysis

|

14

|

|

Portfolio Analysis

|

|

|

Same-Store Properties Net Operating Income Summary

|

15

|

|

Net Operating Income Detail

|

16-19

|

|

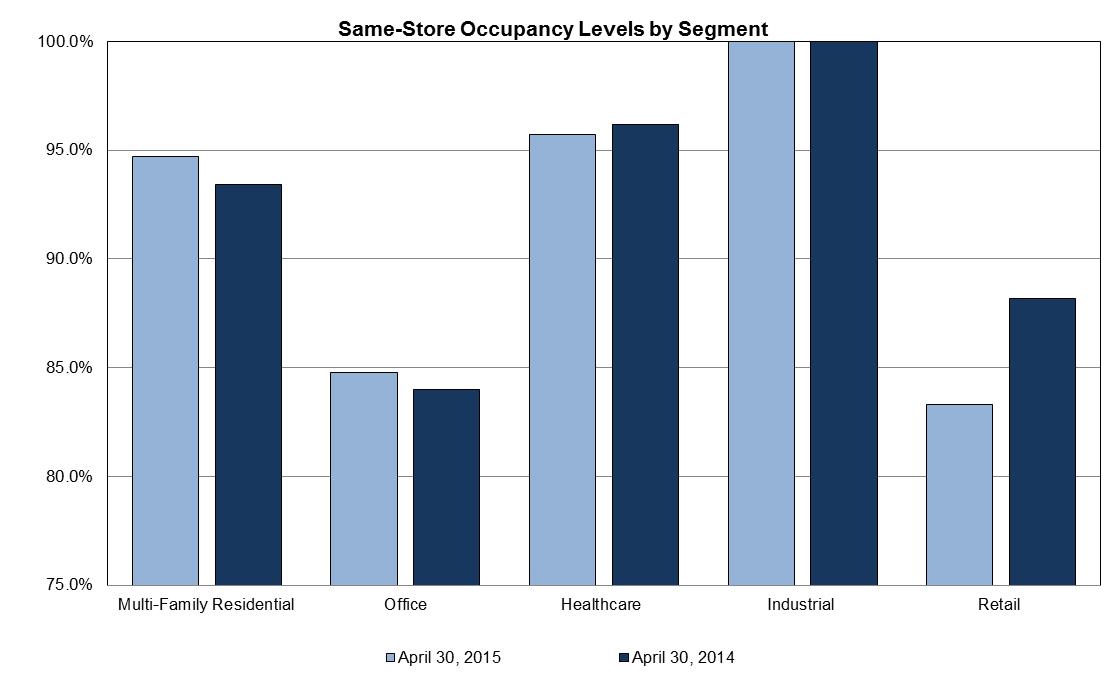

Same-Store Properties and All Properties Occupancy Levels by Segment

|

20

|

|

Tenant Analysis

|

|

|

Multi-Family Residential Summary

|

21

|

|

Commercial Leasing Summary

|

22-25

|

|

10 Largest Commercial Tenants - Based on Annualized Base Rent

|

26

|

|

Commercial Lease Expirations

|

27

|

|

Growth and Strategy

|

|

|

Acquisition Summary

|

28

|

|

Development Placed in Service Summary

|

29

|

|

Development in Progress Summary

|

30

|

|

Acquisitions and Development Liquidity Profile

|

31

|

|

Definitions

|

32

|

1

Company Background and Highlights

Fourth Quarter Fiscal 2015

Investors Real Estate Trust is a self-administered, equity real estate investment trust (REIT) investing in a portfolio of income-producing properties located primarily in the upper Midwest. IRET’s portfolio is diversified among multi-family residential; office; healthcare, including senior housing; industrial and retail segments.

During the fourth quarter of fiscal year 2015, the Company closed on its acquisition of a 119-unit multi-family residential property in Bismarck, North Dakota, for a purchase price of $15.0 million.

Also during the fourth quarter of fiscal year 2015, the Company sold nine office properties, one healthcare property, one retail property and one parcel of unimproved land for sales prices totaling $48.4 million.

The Company experienced improving trends in a majority of its apartment investments in fiscal year 2015. Same-store revenues for the portfolio outpaced same-store expenses and occupancy reached our target 95% at fiscal year end on same store-assets. Same-store revenues in the segment increased 3.4% over the prior fiscal year primarily driven by an increase in scheduled rent in all of our markets ranging from a 0.4% increase in Topeka, KS to 5.4% in Bismarck, ND. Demand was also strong for the 798 apartment units the Company placed in service during fiscal year 2015. However, the Company’s ability to maintain occupancy levels and raise rents remains dependent on continued healthy employment and wage growth. The Company has continued to observe considerable multi-family development activity in the Company’s markets, and as this new construction is completed and leased, the Company will experience increased competition for residents. However, based on information available to the Company, apartment developers in our markets are currently seeing increases in construction costs for potential new apartment developments, which may slow new developments in our markets. The U.S. economic outlook through 2017 is forecasted to be good according to U.S. Bureau of Labor Statistics and Moody’s Analytics. Businesses are adding jobs and for the first time in this phase of the economic cycle we are seeing meaningful wage growth. There is an attitudinal shift also occurring toward renting by professional millennials and to lesser, although growing degree, by baby boomers. These trends are beneficial to apartment owners.

The Company’s office segment, mostly concentrated in Minnesota, continued to be affected by a number of adverse macro conditions. Demand for office space is mixed, with space absorption in the Minneapolis market in particular concentrated in prime locations, and suburban office properties continuing to lag in terms of occupancy. Businesses appear to be maintaining their goal of increasing the density of their work spaces by placing more employees in less total square footage. The demand is strongest for modern office buildings which are in short supply due the lack of new construction of this class of building. The Company’s office buildings are mostly class B, which class has the greatest supply and only modest and selective demand. As a result, we have been unable to effectively compete for the limited number of tenant prospects in the market. The Company continues to expect a slow and uneven recovery in its office segment. Additionally, there is a movement by tenants to the urban cores to attract and retain the best workers. Most of IRET’s office portfolio is suburban.

The Company’s healthcare segment consists of medical office properties and senior housing facilities. The medical office sector remains stable with high occupancy and modest rent increases. The Company’s senior housing assets continue to benefit from the strengthening recovery in the housing market, as occupancy trends are closely aligned with the ability of seniors to sell their homes in anticipation of moving to a senior care facility.

Both the industrial and retail property markets continue to improve. The Company’s industrial properties are located primarily in the Minneapolis market, and all of these Minneapolis properties are 83.4% leased. The demand for bulk warehouse and manufacturing space in the Company’s markets is healthy, with rents generally rising. The retail recovery is evident in regard to the Company’s Minneapolis-metro and grocery-anchored retail properties, which are performing well. Locations outside the Minneapolis-metro area experience less demand, although improving. There is little new construction in our markets, which bodes well going forward.

The Company is in process of selling substantially all of its commercial office and retail properties. In an update to its strategic plan previously announced, the Company is narrowing its property focus. Sale proceeds are intended to be used toward portfolio deleveraging and investments in multi-family residential and healthcare.

In the fourth quarter of fiscal year 2015, IRET paid its 176th consecutive quarterly distribution. The $0.1300 per share/unit distribution was payable on April 1, 2015. Subsequent to the end of the fourth quarter of fiscal year 2015, on June 2, 2015, the Company’s Board of Trustees declared a regular quarterly distribution of $0.1300 per share and unit on the Company’s common shares of beneficial interest and the limited partnership units of IRET Properties, payable July 1, 2015 to common shareholders and unitholders of record on June 15, 2015. Also on June 2, 2015, the Company’s Board of Trustees’ declared a distribution of $0.5156 per share on the Company’s Series A preferred shares of beneficial interest, payable June 30, 2015 to Series A preferred shareholders of record on June 15, 2015, and declared a distribution of $0.4968 per share on the Company’s Series B preferred shares of beneficial interest, payable June 30, 2015 to Series B preferred shareholders of record on June 15, 2015.

As of April 30, 2015, IRET owns a diversified portfolio of 249 properties consisting of 100 multi-family residential properties, 53 office properties, 66 healthcare properties (including senior housing), 7 industrial properties and 23 retail properties. IRET’s common shares are publicly traded on the New York Stock Exchange (NYSE: IRET).

2

Company Snapshot

(as of April 30, 2015)

|

Company Headquarters

|

Minot, North Dakota

|

|

Fiscal Year-End

|

April 30

|

|

Reportable Segments

|

Multi-Family Residential, Office, Healthcare, Industrial, Retail

|

|

Total Properties

|

249

|

|

Total Square Feet

|

|

|

(commercial properties)

|

9.6 million

|

|

Total Units

|

|

|

(multi-family residential properties)

|

11,844

|

|

Common Shares Outstanding (thousands)

|

124,456

|

|

Limited Partnership Units Outstanding (thousands)

|

14,000

|

|

Common Share Distribution - Quarter/Annualized

|

$0.13/$0.52

|

|

Dividend Yield

|

7.3%

|

|

Total Capitalization (see p.14 for detail)

|

$2.5 billion

|

Investor Information

(as of June 29, 2015)

Board of Trustees

|

Jeffrey L. Miller

|

Trustee and Chairman

|

|

John D. Stewart

|

Trustee, Vice Chairman, and Chair of Nominating and Governance Committee

|

|

Jeffrey K. Woodbury

|

Trustee, Chair of Audit Committee

|

|

Linda J. Hall

|

Trustee, Chair of Compensation Committee

|

|

Jeffrey P. Caira

|

Trustee

|

|

Terrance P. Maxwell

|

Trustee

|

|

Pamela J. Moret

|

Trustee

|

|

Stephen L. Stenehjem

|

Trustee

|

|

Timothy P. Mihalick

|

Trustee, President and Chief Executive Officer

|

Management

|

Timothy P. Mihalick

|

President and Chief Executive Officer; Trustee

|

|

Diane K. Bryantt

|

Executive Vice President and Chief Operating Officer

|

|

Ted E. Holmes

|

Executive Vice President and Chief Financial Officer

|

|

Michael A. Bosh

|

Executive Vice President, General Counsel and Assistant Secretary

|

|

Mark Reiling

|

Executive Vice President and Chief Investment Officer

|

|

Charles A. Greenberg

|

Senior Vice President, Commercial Asset Management

|

|

Andrew Martin

|

Senior Vice President, Residential Property Management

|

Corporate Headquarters:

1400 31st Avenue SW, Suite 60

Post Office Box 1988

Minot, North Dakota 58702-1988

Trading Symbol: IRET

Stock Exchange Listing: NYSE

Investor Relations Contact:

Cindy Bradehoft

cbradehoft@iret.com

3

Common Share Data (NYSE: IRET)

|

4th Quarter

Fiscal Year 2015

|

3rd Quarter

Fiscal Year 2015

|

2nd Quarter

Fiscal Year 2015

|

1st Quarter

Fiscal Year 2015

|

4th Quarter

Fiscal Year 2014

|

||||||||||||||||

|

High Closing Price

|

$

|

8.31

|

$

|

8.60

|

$

|

8.59

|

$

|

9.21

|

$

|

9.06

|

||||||||||

|

Low Closing Price

|

$

|

7.09

|

$

|

8.05

|

$

|

7.49

|

$

|

8.52

|

$

|

8.34

|

||||||||||

|

Average Closing Price

|

$

|

7.52

|

$

|

8.35

|

$

|

8.11

|

$

|

8.82

|

$

|

8.71

|

||||||||||

|

Closing Price at end of quarter

|

$

|

7.17

|

$

|

8.25

|

$

|

8.40

|

$

|

8.52

|

$

|

8.72

|

||||||||||

|

Common Share Distributions—annualized

|

$

|

0.520

|

$

|

0.520

|

$

|

0.520

|

$

|

0.520

|

$

|

0.520

|

||||||||||

|

Closing Dividend Yield - annualized

|

7.3

|

%

|

6.3

|

%

|

6.2

|

%

|

6.1

|

%

|

6.0

|

%

|

||||||||||

|

Closing common shares outstanding (thousands)

|

124,456

|

122,134

|

119,809

|

114,763

|

109,019

|

|||||||||||||||

|

Closing limited partnership units outstanding (thousands)

|

14,000

|

14,398

|

14,731

|

17,975

|

21,094

|

|||||||||||||||

|

Closing market value of outstanding common shares, plus imputed closing market value of outstanding limited partnership units (thousands)

|

$

|

992,729

|

$

|

1,126,389

|

$

|

1,130,136

|

$

|

1,130,928

|

$

|

1,134,585

|

||||||||||

Certain statements in these supplemental disclosures are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results to differ materially from projected results. Such risks, uncertainties and other factors include, but are not limited to: intentions and expectations regarding future distributions on our common shares and units, fluctuations in interest rates, the effect of government regulation, the availability of capital, changes in general and local economic and real estate market conditions, competition, our ability to attract and retain skilled personnel, and those risks and uncertainties detailed from time to time in our filings with the Securities and Exchange Commission, including our 2015 Form 10-K. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

Fourth Quarter Fiscal 2015 Acquisition

|

|

|

Legacy Heights (exterior)

Bismarck, ND

|

Legacy Heights (interior)

Bismarck, ND

|

4

Percentage of Total Property Cost by State

5

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands)

|

4/30/2015

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

||||||||||||||||

|

ASSETS

|

||||||||||||||||||||

|

Real estate investments

|

||||||||||||||||||||

|

Property owned

|

$

|

2,098,037

|

$

|

2,093,148

|

$

|

2,013,770

|

$

|

2,025,327

|

$

|

1,996,031

|

||||||||||

|

Less accumulated depreciation

|

(448,987

|

)

|

(439,153

|

)

|

(426,545

|

)

|

(435,317

|

)

|

(424,288

|

)

|

||||||||||

|

1,649,050

|

1,653,995

|

1,587,225

|

1,590,010

|

1,571,743

|

||||||||||||||||

|

Development in progress

|

153,994

|

114,005

|

146,390

|

131,862

|

104,609

|

|||||||||||||||

|

Unimproved land

|

25,827

|

27,675

|

24,947

|

24,772

|

22,864

|

|||||||||||||||

|

Total real estate investments

|

1,828,871

|

1,795,675

|

1,758,562

|

1,746,644

|

1,699,216

|

|||||||||||||||

|

Real estate held for sale

|

22,912

|

44,259

|

41,183

|

6,508

|

2,951

|

|||||||||||||||

|

Cash and cash equivalents

|

48,970

|

52,148

|

52,999

|

60,620

|

47,267

|

|||||||||||||||

|

Other investments

|

329

|

329

|

329

|

329

|

329

|

|||||||||||||||

|

Receivable arising from straight-lining of rents, net of allowance

|

26,211

|

27,169

|

27,425

|

27,286

|

27,096

|

|||||||||||||||

|

Accounts receivable, net of allowance

|

3,675

|

5,574

|

3,719

|

7,013

|

10,206

|

|||||||||||||||

|

Real estate deposits

|

2,489

|

7,494

|

4,924

|

3,741

|

145

|

|||||||||||||||

|

Prepaid and other assets

|

3,907

|

5,580

|

2,263

|

3,428

|

4,639

|

|||||||||||||||

|

Intangible assets, net of accumulated amortization

|

27,267

|

28,475

|

29,745

|

31,478

|

32,639

|

|||||||||||||||

|

Tax, insurance, and other escrow

|

11,249

|

11,277

|

16,338

|

20,451

|

20,880

|

|||||||||||||||

|

Property and equipment, net of accumulated depreciation

|

1,542

|

1,619

|

1,598

|

1,641

|

1,681

|

|||||||||||||||

|

Goodwill

|

1,911

|

1,940

|

1,940

|

1,951

|

1,100

|

|||||||||||||||

|

Deferred charges and leasing costs, net of accumulated amortization

|

18,504

|

19,803

|

20,445

|

20,677

|

21,072

|

|||||||||||||||

|

TOTAL ASSETS

|

$

|

1,997,837

|

$

|

2,001,342

|

$

|

1,961,470

|

$

|

1,931,767

|

$

|

1,869,221

|

||||||||||

|

LIABILITIES AND EQUITY

|

||||||||||||||||||||

|

LIABILITIES

|

||||||||||||||||||||

|

Accounts payable and accrued expenses

|

$

|

71,072

|

$

|

69,901

|

$

|

67,037

|

$

|

62,517

|

$

|

59,105

|

||||||||||

|

Revolving line of credit

|

60,500

|

50,500

|

40,500

|

35,500

|

22,500

|

|||||||||||||||

|

Mortgages payable

|

974,828

|

1,006,179

|

1,013,161

|

1,017,574

|

997,689

|

|||||||||||||||

|

Construction debt and other

|

144,115

|

132,210

|

107,731

|

83,666

|

63,178

|

|||||||||||||||

|

TOTAL LIABILITIES

|

1,250,515

|

1,258,790

|

1,228,429

|

1,199,257

|

1,142,472

|

|||||||||||||||

|

REDEEMABLE NONCONTROLLING INTERESTS – CONSOLIDATED REAL ESTATE ENTITIES

|

6,368

|

6,340

|

6,373

|

6,313

|

6,203

|

|||||||||||||||

|

EQUITY

|

||||||||||||||||||||

|

Investors Real Estate Trust shareholders’ equity

|

||||||||||||||||||||

|

Series A Preferred Shares of Beneficial Interest

|

27,317

|

27,317

|

27,317

|

27,317

|

27,317

|

|||||||||||||||

|

Series B Preferred Shares of Beneficial Interest

|

111,357

|

111,357

|

111,357

|

111,357

|

111,357

|

|||||||||||||||

|

Common Shares of Beneficial Interest

|

951,868

|

935,287

|

918,221

|

884,415

|

843,268

|

|||||||||||||||

|

Accumulated distributions in excess of net income

|

(438,432

|

)

|

(430,282

|

)

|

(420,036

|

)

|

(407,052

|

)

|

(389,758

|

)

|

||||||||||

|

Total Investors Real Estate Trust shareholders’ equity

|

652,110

|

643,679

|

636,859

|

616,037

|

592,184

|

|||||||||||||||

|

Noncontrolling interests – Operating Partnership

|

58,325

|

61,177

|

63,207

|

84,250

|

105,724

|

|||||||||||||||

|

Noncontrolling interests – consolidated real estate entities

|

30,519

|

31,356

|

26,602

|

25,910

|

22,638

|

|||||||||||||||

|

Total equity

|

740,954

|

736,212

|

726,668

|

726,197

|

720,546

|

|||||||||||||||

|

TOTAL LIABILITIES, REDEEMABLE NONCONTROLLING INTERESTS AND EQUITY

|

$

|

1,997,837

|

$

|

2,001,342

|

$

|

1,961,470

|

$

|

1,931,767

|

$

|

1,869,221

|

||||||||||

6

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands, except per share data)

|

Twelve Months Ended

|

Three Months Ended

|

|||||||||||||||||||||||||||

|

OPERATING RESULTS

|

4/30/2015

|

4/30/2014

|

4/30/2015

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

|||||||||||||||||||||

|

Real estate revenue

|

$

|

279,670

|

$

|

265,482

|

$

|

69,838

|

$

|

71,953

|

$

|

70,042

|

$

|

67,837

|

$

|

66,983

|

||||||||||||||

|

Real estate expenses

|

110,997

|

108,487

|

27,808

|

28,434

|

27,237

|

27,518

|

29,589

|

|||||||||||||||||||||

|

Gain on involuntary conversion

|

0

|

2,480

|

0

|

0

|

0

|

0

|

0

|

|||||||||||||||||||||

|

Net operating income

|

168,673

|

159,475

|

42,030

|

43,519

|

42,805

|

40,319

|

37,394

|

|||||||||||||||||||||

|

TRS senior housing revenue

|

3,520

|

1,627

|

921

|

963

|

843

|

793

|

823

|

|||||||||||||||||||||

|

TRS senior housing expenses

|

(2,997

|

)

|

(1,331

|

)

|

(754

|

)

|

(825

|

)

|

(725

|

)

|

(693

|

)

|

(660

|

)

|

||||||||||||||

|

Depreciation/amortization

|

(70,607

|

)

|

(70,918

|

)

|

(18,133

|

)

|

(17,750

|

)

|

(17,668

|

)

|

(17,056

|

)

|

(17,262

|

)

|

||||||||||||||

|

Administrative expenses

|

(11,824

|

)

|

(10,743

|

)

|

(2,516

|

)

|

(2,754

|

)

|

(2,890

|

)

|

(3,664

|

)

|

(2,801

|

)

|

||||||||||||||

|

Other expenses

|

(2,010

|

)

|

(2,132

|

)

|

(332

|

)

|

(488

|

)

|

(578

|

)

|

(612

|

)

|

(502

|

)

|

||||||||||||||

|

Impairment of real estate investments

|

(6,105

|

)

|

(42,566

|

)

|

0

|

(540

|

)

|

(3,245

|

)

|

(2,320

|

)

|

(37,768

|

)

|

|||||||||||||||

|

Interest expense

|

(59,020

|

)

|

(59,142

|

)

|

(15,162

|

)

|

(14,595

|

)

|

(14,599

|

)

|

(14,664

|

)

|

(14,617

|

)

|

||||||||||||||

|

Interest and other income

|

2,961

|

2,391

|

904

|

670

|

696

|

691

|

922

|

|||||||||||||||||||||

|

Income (loss) before loss on sale of real estate and other investments and income from discontinued operations

|

22,591

|

(23,339

|

)

|

6,958

|

8,200

|

4,639

|

2,794

|

(34,471

|

)

|

|||||||||||||||||||

|

Income (loss) on sale of real estate and other investments

|

6,093

|

(51

|

)

|

6,904

|

951

|

1,231

|

(2,993

|

)

|

(51

|

)

|

||||||||||||||||||

|

Income (loss) from continuing operations

|

28,684

|

(23,390

|

)

|

13,862

|

9,151

|

5,870

|

(199

|

)

|

(34,522

|

)

|

||||||||||||||||||

|

Income from discontinued operations

|

0

|

6,450

|

0

|

0

|

0

|

0

|

0

|

|||||||||||||||||||||

|

Net income (loss)

|

$

|

28,684

|

$

|

(16,940

|

)

|

$

|

13,862

|

$

|

9,151

|

$

|

5,870

|

$

|

(199

|

)

|

$

|

(34,522

|

)

|

|||||||||||

|

Net loss (income) attributable to noncontrolling interest – Operating Partnership

|

(1,526

|

)

|

4,676

|

(908

|

)

|

(657

|

)

|

(363

|

)

|

402

|

6,082

|

|||||||||||||||||

|

Net income attributable to noncontrolling interests – consolidated real estate entities

|

(3,071

|

)

|

(910

|

)

|

(2,201

|

)

|

(123

|

)

|

(393

|

)

|

(354

|

)

|

(102

|

)

|

||||||||||||||

|

Net (loss) income attributable to Investors Real Estate Trust

|

24,087

|

(13,174

|

)

|

10,753

|

8,371

|

5,114

|

(151

|

)

|

(28,542

|

)

|

||||||||||||||||||

|

Dividends to preferred shareholders

|

(11,514

|

)

|

(11,514

|

)

|

(2,878

|

)

|

(2,879

|

)

|

(2,878

|

)

|

(2,879

|

)

|

(2,878

|

)

|

||||||||||||||

|

NET (LOSS) INCOME AVAILABLE TO COMMON SHAREHOLDERS

|

$

|

12,573

|

$

|

(24,688

|

)

|

$

|

7,875

|

$

|

5,492

|

$

|

2,236

|

$

|

(3,030

|

)

|

$

|

(31,420

|

)

|

|||||||||||

|

Per Share Data

|

||||||||||||||||||||||||||||

|

Earnings (loss) per common share from continuing operations – Investors Real Estate Trust – basic & diluted

|

$

|

.11

|

$

|

(.28

|

)

|

$

|

.07

|

$

|

.05

|

$

|

.02

|

$

|

(.03

|

)

|

$

|

(.29

|

)

|

|||||||||||

|

Earnings per common share from discontinued operations – Investors Real Estate Trust – basic & diluted

|

.11

|

.05

|

.00

|

.00

|

.00

|

.00

|

.00

|

|||||||||||||||||||||

|

Net income per common share – basic & diluted

|

$

|

.11

|

$

|

(.23

|

)

|

$

|

.07

|

$

|

.05

|

$

|

.02

|

$

|

(.03

|

)

|

$

|

(.29

|

)

|

|||||||||||

|

Percentage of Revenues

|

||||||||||||||||||||||||||||

|

Real estate expenses

|

39.7

|

%

|

40.9

|

%

|

39.8

|

%

|

39.5

|

%

|

38.9

|

%

|

40.6

|

%

|

44.2

|

%

|

||||||||||||||

|

Depreciation/amortization

|

25.2

|

%

|

26.7

|

%

|

26.0

|

%

|

24.7

|

%

|

25.2

|

%

|

25.1

|

%

|

25.8

|

%

|

||||||||||||||

|

Administrative expenses

|

4.2

|

%

|

4.0

|

%

|

3.6

|

%

|

3.8

|

%

|

4.1

|

%

|

5.4

|

%

|

4.2

|

%

|

||||||||||||||

|

Interest

|

21.1

|

%

|

22.3

|

%

|

21.7

|

%

|

20.3

|

%

|

20.8

|

%

|

21.6

|

%

|

21.8

|

%

|

||||||||||||||

|

Income from discontinued operations

|

0.0

|

%

|

2.4

|

%

|

0.0

|

%

|

0.0

|

%

|

0.0

|

%

|

0.0

|

%

|

0.0

|

%

|

||||||||||||||

|

Net (loss) income

|

10.3

|

%

|

(6.4

|

)%

|

19.8

|

%

|

12.7

|

%

|

8.4

|

%

|

(0.3

|

)%

|

(51.5

|

)%

|

||||||||||||||

|

Ratios

|

||||||||||||||||||||||||||||

|

Adjusted EBITDA(1)/Interest expense

|

2.63

|

x

|

2.36

|

x

|

2.41

|

x

|

2.53

|

x

|

2.48

|

x

|

2.29

|

x

|

2.26

|

x

|

||||||||||||||

|

Adjusted EBITDA(1)/Interest expense plus preferred distributions

|

2.20

|

x

|

1.97

|

x

|

2.05

|

x

|

2.14

|

x

|

2.10

|

x

|

1.94

|

x

|

1.90

|

x

|

||||||||||||||

| (1) | See Definitions on page 32. Adjusted EBITDA is a non-GAAP measure; see page 9 for a reconciliation of Adjusted EBITDA to net income. |

7

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands, except per share and unit data)

|

Twelve Months Ended

|

Three Months Ended

|

|||||||||||||||||||||||||||

|

4/30/2015

|

4/30/2014

|

4/30/2015

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

||||||||||||||||||||||

|

Funds From Operations(1)

|

||||||||||||||||||||||||||||

|

Net income (loss) attributable to Investors Real Estate Trust

|

$

|

24,087

|

$

|

(13,174

|

)

|

$

|

10,753

|

$

|

8,371

|

$

|

5,114

|

$

|

(151

|

)

|

$

|

(28,542

|

)

|

|||||||||||

|

Less dividends to preferred shareholders

|

(11,514

|

)

|

(11,514

|

)

|

(2,878

|

)

|

(2,879

|

)

|

(2,878

|

)

|

(2,879

|

)

|

(2,878

|

)

|

||||||||||||||

|

Net (loss) income available to common shareholders

|

12,573

|

(24,688

|

)

|

7,875

|

5,492

|

2,236

|

(3,030

|

)

|

(31,420

|

)

|

||||||||||||||||||

|

Adjustments:

|

||||||||||||||||||||||||||||

|

Noncontrolling interests – Operating Partnership

|

1,526

|

(4,676

|

)

|

908

|

657

|

363

|

(402

|

)

|

(6,082

|

)

|

||||||||||||||||||

|

Depreciation and amortization

|

70,450

|

71,830

|

18,083

|

17,706

|

17,624

|

17,037

|

17,239

|

|||||||||||||||||||||

|

Impairment of real estate investments

|

6,105

|

44,426

|

0

|

540

|

3,245

|

2,320

|

37,768

|

|||||||||||||||||||||

|

(Gain) loss on depreciable property sales attributable to Investors Real Estate Trust

|

$

|

(4,079

|

)

|

$

|

(6,948

|

)

|

(4,890

|

)

|

(951

|

)

|

(1,231

|

)

|

2,993

|

51

|

||||||||||||||

|

Funds from operations applicable to common shares and Units

|

86,575

|

79,944

|

$

|

21,976

|

$

|

23,444

|

$

|

22,237

|

$

|

18,918

|

$

|

17,556

|

||||||||||||||||

|

FFO per share and unit - basic and diluted

|

$

|

0.64

|

$

|

0.63

|

$

|

0.16

|

$

|

0.17

|

$

|

0.17

|

$

|

0.14

|

$

|

0.14

|

||||||||||||||

|

Adjusted funds from operations(1)

|

||||||||||||||||||||||||||||

|

Funds from operations applicable to common shares and Units

|

$

|

86,575

|

$

|

79,944

|

$

|

21,976

|

$

|

23,444

|

$

|

22,237

|

$

|

18,918

|

$

|

17,556

|

||||||||||||||

|

Adjustments:

|

||||||||||||||||||||||||||||

|

Tenant improvements at same-store(2) properties

|

(7,589

|

)

|

(9,937

|

)

|

(2,939

|

)

|

(1,984

|

)

|

(542

|

)

|

(2,169

|

)

|

(1,610

|

)

|

||||||||||||||

|

Leasing costs at same-store properties(2)

|

(2,290

|

)

|

(3,797

|

)

|

(684

|

)

|

(358

|

)

|

(699

|

)

|

(578

|

)

|

(1,038

|

)

|

||||||||||||||

|

Recurring capital expenditures(1)(2)

|

(6,135

|

)

|

(4,956

|

)

|

(1,342

|

)

|

(1,865

|

)

|

(1,567

|

)

|

(1,386

|

)

|

(1,118

|

)

|

||||||||||||||

|

Straight-line rents

|

12

|

(2,206

|

)

|

198

|

184

|

(103

|

)

|

(268

|

)

|

(70

|

)

|

|||||||||||||||||

|

Non-real estate depreciation

|

388

|

368

|

100

|

94

|

96

|

99

|

102

|

|||||||||||||||||||||

|

Default interest

|

528

|

0

|

528

|

0

|

0

|

0

|

0

|

|||||||||||||||||||||

|

Share based compensation expense(3)

|

2,215

|

1,162

|

280

|

260

|

601

|

1,073

|

272

|

|||||||||||||||||||||

|

Gain on involuntary conversion

|

0

|

(2,480

|

)

|

0

|

0

|

0

|

0

|

0

|

||||||||||||||||||||

|

Adjusted funds from operations applicable to common shares and Units

|

$

|

73,704

|

$

|

58,098

|

$

|

18,117

|

$

|

19,775

|

$

|

20,023

|

$

|

15,689

|

$

|

14,094

|

||||||||||||||

|

AFFO per share and unit - basic and diluted

|

$

|

0.55

|

$

|

0.46

|

$

|

0.13

|

$

|

0.15

|

$

|

0.15

|

$

|

0.12

|

$

|

0.11

|

||||||||||||||

|

Weighted average shares and units

|

134,598

|

127,028

|

137,412

|

135,315

|

133,295

|

131,332

|

129,244

|

|||||||||||||||||||||

| (1) | See Definitions on page 32. |

| (2) | Quarterly information is for properties in the same-store pool at that point in time; consequently, quarterly numbers may not total to year-to-date numbers. |

| (3) | Twelve months ended 4/30/14 revised to include share based compensation expense. Three months ended 7/31/14 and 4/30/14 revised to include trustee share-based compensation expense. |

8

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(unaudited)

(in thousands)

|

Twelve Months Ended

|

Three Months Ended

|

|||||||||||||||||||||||||||

|

4/30/2015

|

4/30/2014

|

4/30/2015

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

||||||||||||||||||||||

|

Adjusted EBITDA(1)

|

||||||||||||||||||||||||||||

|

Net income (loss) attributable to Investors Real Estate Trust

|

$

|

24,087

|

$

|

(13,174

|

)

|

$

|

10,753

|

$

|

8,371

|

$

|

5,114

|

$

|

(151

|

)

|

$

|

(28,542

|

)

|

|||||||||||

|

Adjustments:

|

||||||||||||||||||||||||||||

|

Noncontrolling interests – Operating Partnership

|

1,526

|

(4,676

|

)

|

908

|

657

|

363

|

(402

|

)

|

(6,082

|

)

|

||||||||||||||||||

|

Income (loss) before noncontrolling interests – Operating Partnership

|

25,613

|

(17,850

|

)

|

11,661

|

9,028

|

5,477

|

(553

|

)

|

(34,624

|

)

|

||||||||||||||||||

|

Add:

|

||||||||||||||||||||||||||||

|

Interest expense

|

59,020

|

59,563

|

15,162

|

14,595

|

14,599

|

14,664

|

14,617

|

|||||||||||||||||||||

|

Depreciation/amortization related to real estate investments

|

67,112

|

68,542

|

17,266

|

16,834

|

16,814

|

16,198

|

16,449

|

|||||||||||||||||||||

|

Amortization related to non-real estate investments

|

3,495

|

3,416

|

867

|

916

|

840

|

872

|

826

|

|||||||||||||||||||||

|

Amortization related to real estate revenues(2)

|

231

|

241

|

50

|

50

|

66

|

65

|

66

|

|||||||||||||||||||||

|

Impairment of real estate investments

|

6,105

|

44,426

|

0

|

540

|

3,245

|

2,320

|

37,768

|

|||||||||||||||||||||

|

Less:

|

||||||||||||||||||||||||||||

|

Interest income

|

(2,238

|

)

|

(1,908

|

)

|

(557

|

)

|

(561

|

)

|

(560

|

)

|

(560

|

)

|

(562

|

)

|

||||||||||||||

|

Gain on depreciable property sales attributable to Investors Real Estate Trust

|

(4,079

|

)

|

(6,948

|

)

|

(4,890

|

)

|

(951

|

)

|

(1,231

|

)

|

2,993

|

51

|

||||||||||||||||

|

Gain on involuntary conversion

|

0

|

(2,480

|

)

|

0

|

0

|

0

|

0

|

0

|

||||||||||||||||||||

|

Adjusted EBITDA

|

$

|

155,259

|

$

|

147,002

|

39,559

|

40,451

|

39,250

|

35,999

|

34,591

|

|||||||||||||||||||

| (1) | See Definitions on page 32. |

| (2) | Included in real estate revenue in the Statement of Operations. |

9

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands)

Debt Maturity Schedule

Annual Expirations

Total Mortgage Debt*

|

|

Future Maturities of Mortgage Debt

|

|||||||||||||||||||

|

Fiscal Year

|

Fixed Debt

|

Variable Debt

|

Total Debt

|

Weighted

Average(1)

|

% of

Total Debt

|

|||||||||||||||

|

2016

|

$

|

97,993

|

$

|

0

|

$

|

97,993

|

4.23

|

%

|

10.1

|

%

|

||||||||||

|

2017

|

167,804

|

15,000

|

182,804

|

5.85

|

%

|

18.7

|

%

|

|||||||||||||

|

2018

|

32,718

|

31,000

|

63,718

|

4.32

|

%

|

6.5

|

%

|

|||||||||||||

|

2019

|

80,828

|

5,345

|

86,173

|

5.80

|

%

|

8.8

|

%

|

|||||||||||||

|

2020

|

112,812

|

18,622

|

131,434

|

5.37

|

%

|

13.5

|

%

|

|||||||||||||

|

2021

|

128,720

|

0

|

128,720

|

5.30

|

%

|

13.2

|

%

|

|||||||||||||

|

2022

|

128,774

|

0

|

128,774

|

5.61

|

%

|

13.2

|

%

|

|||||||||||||

|

2023

|

37,164

|

0

|

37,164

|

4.25

|

%

|

3.8

|

%

|

|||||||||||||

|

2024

|

66,326

|

0

|

66,326

|

4.29

|

%

|

6.8

|

%

|

|||||||||||||

|

2025

|

19,845

|

0

|

19,845

|

4.04

|

%

|

2.1

|

%

|

|||||||||||||

|

Thereafter

|

31,877

|

0

|

31,877

|

4.41

|

%

|

3.3

|

%

|

|||||||||||||

|

Total maturities

|

$

|

904,861

|

$

|

69,967

|

$

|

974,828

|

5.16

|

%

|

100.0

|

%

|

||||||||||

| (1) | Weighted average interest rate of debt that matures in fiscal year. |

|

4/30/15

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

||||||||||||||||

|

Balances Outstanding

|

||||||||||||||||||||

|

Mortgage

|

||||||||||||||||||||

|

Fixed rate

|

$

|

904,861

|

$

|

927,724

|

$

|

949,002

|

$

|

972,142

|

$

|

977,224

|

||||||||||

|

Variable rate

|

69,967

|

78,455

|

64,159

|

45,432

|

20,465

|

|||||||||||||||

|

Mortgage total

|

$

|

974,828

|

$

|

1,006,179

|

$

|

1,013,161

|

$

|

1,017,574

|

$

|

997,689

|

||||||||||

|

Weighted Average Interest Rates Secured

|

5.16

|

%

|

5.17

|

%

|

5.26

|

%

|

5.32

|

%

|

5.37

|

%

|

||||||||||

10

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands)

|

Property

|

Maturity Date

|

Fiscal 2016

|

Fiscal 2017

|

Fiscal 2018

|

Fiscal 2019

|

Thereafter

|

Total(1)

|

||||||||||||||||||

|

Multi-Family Residential

|

|||||||||||||||||||||||||

|

Campus Center - St Cloud, MN(2)

|

6/1/2015

|

$

|

1,127

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

1,127

|

||||||||||||

|

Campus Knoll - St Cloud, MN(2)

|

6/1/2015

|

752

|

0

|

0

|

0

|

0

|

752

|

||||||||||||||||||

|

Landmark - Grand Forks, ND

|

8/24/2015

|

1,573

|

0

|

0

|

0

|

0

|

1,573

|

||||||||||||||||||

|

Regency Park Estates - St Cloud, MN

|

1/1/2016

|

6,680

|

0

|

0

|

0

|

0

|

6,680

|

||||||||||||||||||

|

Pebble Springs – Bismarck, ND

|

7/1/2016

|

0

|

757

|

0

|

0

|

0

|

757

|

||||||||||||||||||

|

Southview – Minot, ND

|

7/1/2016

|

0

|

1,035

|

0

|

0

|

0

|

1,035

|

||||||||||||||||||

|

Homestead Gardens I – Rapid City, SD

|

7/11/16

|

0

|

6,895

|

0

|

0

|

0

|

6,895

|

||||||||||||||||||

|

River Ridge – Bismarck, ND

|

6/30/17

|

0

|

0

|

13,200

|

0

|

0

|

13,200

|

||||||||||||||||||

|

Evergreen II – Isanti, MN

|

11/1/2017

|

0

|

0

|

2,066

|

0

|

0

|

2,066

|

||||||||||||||||||

|

Ponds – Sartell, MN

|

11/1/2017

|

0

|

0

|

3,852

|

0

|

0

|

3,852

|

||||||||||||||||||

|

Homestead Gardens II - Rapid City, SD

|

6/1/2018

|

0

|

0

|

0

|

3,433

|

0

|

3,433

|

||||||||||||||||||

|

IRET Corporate Plaza Apts - Minot, ND

|

8/1/2018

|

0

|

0

|

0

|

5,348

|

0

|

5,348

|

||||||||||||||||||

|

Greenfield - Omaha, NE

|

2/1/2019

|

0

|

0

|

0

|

3,552

|

0

|

3,552

|

||||||||||||||||||

|

Grand Gateway - St. Cloud, MN

|

3/1/2019

|

0

|

0

|

0

|

5,345

|

0

|

5,345

|

||||||||||||||||||

|

Brooklyn Heights - Minot, ND

|

4/1/2019

|

0

|

0

|

0

|

694

|

0

|

694

|

||||||||||||||||||

|

Colton Heights - Minot, ND

|

4/1/2019

|

0

|

0

|

0

|

391

|

0

|

391

|

||||||||||||||||||

|

Pines - Minot, ND

|

4/1/2019

|

0

|

0

|

0

|

111

|

0

|

111

|

||||||||||||||||||

|

Summit Park - Minot, ND

|

4/1/2019

|

0

|

0

|

0

|

963

|

0

|

963

|

||||||||||||||||||

|

Terrace Heights - Minot, ND

|

4/1/2019

|

0

|

0

|

0

|

160

|

0

|

160

|

||||||||||||||||||

|

Summary of Debt due after Fiscal 2019

|

0

|

0

|

0

|

0

|

366,018

|

366,018

|

|||||||||||||||||||

|

Sub-Total Multi-Family Residential

|

$

|

10,132

|

$

|

8,687

|

$

|

19,118

|

$

|

19,997

|

$

|

366,018

|

$

|

423,952

|

|||||||||||||

|

Office

|

|||||||||||||||||||||||||

|

US Bank Financial Center - Bloomington, MN

|

7/1/2015

|

12,766

|

0

|

0

|

0

|

0

|

12,766

|

||||||||||||||||||

|

Rapid City 900 Concourse Drive - Rapid City, SD

|

8/1/2015

|

181

|

0

|

0

|

0

|

0

|

181

|

||||||||||||||||||

|

Westgate I - Boise, ID

|

8/1/2015

|

1,115

|

0

|

0

|

0

|

0

|

1,115

|

||||||||||||||||||

|

Westgate II - Boise, ID

|

8/1/2015

|

2,729

|

0

|

0

|

0

|

0

|

2,729

|

||||||||||||||||||

|

Brook Valley I - LaVista, NE

|

1/1/2016

|

1,209

|

0

|

0

|

0

|

0

|

1,209

|

||||||||||||||||||

|

Spring Valley IV - Omaha, NE

|

1/1/2016

|

720

|

0

|

0

|

0

|

0

|

720

|

||||||||||||||||||

|

Spring Valley V - Omaha, NE

|

1/1/2016

|

792

|

0

|

0

|

0

|

0

|

792

|

||||||||||||||||||

|

Spring Valley X - Omaha, NE

|

1/1/2016

|

734

|

0

|

0

|

0

|

0

|

734

|

||||||||||||||||||

|

Spring Valley XI - Omaha, NE

|

1/1/2016

|

720

|

0

|

0

|

0

|

0

|

720

|

||||||||||||||||||

|

American Corporate Center – Mendota Heights, MN

|

9/1/2016

|

0

|

8,670

|

0

|

0

|

0

|

8,670

|

||||||||||||||||||

|

Mendota Office Center I – Mendota Heights, MN

|

9/1/2016

|

0

|

3,734

|

0

|

0

|

0

|

3,734

|

||||||||||||||||||

|

Mendota Office Center II - Mendota Heights, MN

|

9/1/2016

|

0

|

5,516

|

0

|

0

|

0

|

5,516

|

||||||||||||||||||

|

Mendota Office Center III - Mendota Heights, MN

|

9/1/2016

|

0

|

3,791

|

0

|

0

|

0

|

3,791

|

||||||||||||||||||

|

Mendota Office Center IV - Mendota Heights, MN

|

9/1/2016

|

0

|

4,507

|

0

|

0

|

0

|

4,507

|

||||||||||||||||||

|

Corporate Center West – Omaha, NE(3)

|

10/6/2016

|

0

|

17,315

|

0

|

0

|

0

|

17,315

|

||||||||||||||||||

|

Farnam Executive Center – Omaha, NE(3)

|

10/6/2016

|

0

|

12,160

|

0

|

0

|

0

|

12,160

|

||||||||||||||||||

|

Flagship – Eden Prairie, MN(3)

|

10/6/2016

|

0

|

21,565

|

0

|

0

|

0

|

21,565

|

||||||||||||||||||

|

Gateway Corporate Center – Woodbury, MN(3)

|

10/6/2016

|

0

|

8,700

|

0

|

0

|

0

|

8,700

|

||||||||||||||||||

11

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

LONG-TERM MORTGAGE DEBT* DETAIL AS OF APRIL 30, 2015 (continued)

(in thousands)

|

Property

|

Maturity Date

|

Fiscal 2016

|

Fiscal 2017

|

Fiscal 2018

|

Fiscal 2019

|

Thereafter

|

Total(1)

|

||||||||||||||||||

|

Office - continued

|

|||||||||||||||||||||||||

|

Miracle Hills One – Omaha, NE(3)

|

10/6/2016

|

$

|

0

|

$

|

8,895

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

8,895

|

||||||||||||

|

Pacific Hills – Omaha, NE(3)

|

10/6/2016

|

0

|

16,770

|

0

|

0

|

0

|

16,770

|

||||||||||||||||||

|

Riverport – Maryland Heights, MO(3)

|

10/6/2016

|

0

|

19,690

|

0

|

0

|

0

|

19,690

|

||||||||||||||||||

|

Timberlands – Leawood, KS(3)

|

10/6/2016

|

0

|

13,155

|

0

|

0

|

0

|

13,155

|

||||||||||||||||||

|

Woodlands Plaza IV – Maryland Heights, MO(3)

|

10/6/2016

|

0

|

4,360

|

0

|

0

|

0

|

4,360

|

||||||||||||||||||

|

TCA Building – Eagan, MN

|

2/3/2017

|

0

|

7,500

|

0

|

0

|

0

|

7,500

|

||||||||||||||||||

|

Interlachen Corporate Center – Eagan, MN

|

6/30/17

|

0

|

0

|

8,800

|

0

|

0

|

8,800

|

||||||||||||||||||

|

Plymouth 5095 Nathan Lane – Plymouth, MN

|

11/1/2017

|

0

|

0

|

1,147

|

0

|

0

|

1,147

|

||||||||||||||||||

|

Prairie Oak Business Center – Eden Prairie, MN

|

11/1/2017

|

0

|

0

|

3,120

|

0

|

0

|

3,120

|

||||||||||||||||||

|

Crosstown Centre – Eden Prairie, MN

|

12/1/2017

|

0

|

0

|

9,000

|

0

|

0

|

9,000

|

||||||||||||||||||

|

7800 West Brown Deer Road – Milwaukee, WI

|

4/1/2018

|

0

|

0

|

10,320

|

0

|

0

|

10,320

|

||||||||||||||||||

|

Intertech Building- Fenton, MO

|

5/1/2018

|

0

|

0

|

0

|

4,177

|

0

|

4,177

|

||||||||||||||||||

|

610 Business Center IV - Brooklyn Park, MN

|

7/1/2018

|

0

|

0

|

0

|

6,759

|

0

|

6,759

|

||||||||||||||||||

|

Plaza 16 - Minot, ND

|

8/1/2018

|

0

|

0

|

0

|

7,098

|

0

|

7,098

|

||||||||||||||||||

|

Wells Fargo Center - St Cloud, MN

|

8/1/2018

|

0

|

0

|

0

|

5,787

|

0

|

5,787

|

||||||||||||||||||

|

Ameritrade - Omaha, NE

|

4/1/2019

|

0

|

0

|

0

|

2,020

|

0

|

2,020

|

||||||||||||||||||

|

Summary of Debt due after Fiscal 2019

|

0

|

0

|

0

|

0

|

43,785

|

43,785

|

|||||||||||||||||||

|

Sub-Total Office

|

$

|

20,966

|

$

|

156,328

|

$

|

32,387

|

$

|

25,841

|

$

|

43,785

|

$

|

279,307

|

|||||||||||||

|

Healthcare

|

|||||||||||||||||||||||||

|

Edina 6363 France Medical - St Paul, MN

|

8/6/2015

|

9,567

|

0

|

0

|

0

|

0

|

9,567

|

||||||||||||||||||

|

Edina 6405 France Medical - Edina, MN

|

9/1/2015

|

8,145

|

0

|

0

|

0

|

0

|

8,145

|

||||||||||||||||||

|

Ritchie Medical Plaza - St Paul, MN(2)

|

9/1/2015

|

5,980

|

0

|

0

|

0

|

0

|

5,980

|

||||||||||||||||||

|

Edgewood Vista – Fargo, ND

|

2/25/2016

|

11,846

|

0

|

0

|

0

|

0

|

11,846

|

||||||||||||||||||

|

Edgewood Vista – Fremont, NE

|

2/25/2016

|

550

|

0

|

0

|

0

|

0

|

550

|

||||||||||||||||||

|

Edgewood Vista – Hastings, NE

|

2/25/2016

|

567

|

0

|

0

|

0

|

0

|

567

|

||||||||||||||||||

|

Edgewood Vista – Hermantown I, MN

|

2/25/2016

|

15,197

|

0

|

0

|

0

|

0

|

15,197

|

||||||||||||||||||

|

Edgewood Vista – Kalispell, MT

|

2/25/2016

|

568

|

0

|

0

|

0

|

0

|

568

|

||||||||||||||||||

|

Edgewood Vista – Missoula, MT

|

2/25/2016

|

807

|

0

|

0

|

0

|

0

|

807

|

||||||||||||||||||

|

Edgewood Vista – Omaha, NE

|

2/25/2016

|

359

|

0

|

0

|

0

|

0

|

359

|

||||||||||||||||||

|

Edgewood Vista – Virginia, MN

|

2/25/2016

|

12,927

|

0

|

0

|

0

|

0

|

12,927

|

||||||||||||||||||

|

Airport Medical – Bloomington, MN

|

6/1/2016

|

0

|

431

|

0

|

0

|

0

|

431

|

||||||||||||||||||

|

Park Dental – Brooklyn Center, MN

|

6/1/2016

|

0

|

247

|

0

|

0

|

0

|

247

|

||||||||||||||||||

|

Sartell 2000 23rd St S – Sartell, MN

|

12/1/2016

|

0

|

1,593

|

0

|

0

|

0

|

1,593

|

||||||||||||||||||

|

Billings 2300 Grant Road – Billings, MT

|

12/31/2016

|

0

|

1,226

|

0

|

0

|

0

|

1,226

|

||||||||||||||||||

|

Missoula 3050 Great Northern Ave – Missoula, MT

|

12/31/2016

|

0

|

1,267

|

0

|

0

|

0

|

1,267

|

||||||||||||||||||

|

High Pointe Health Campus – Lake Elmo, MN

|

4/1/2017

|

0

|

7,500

|

0

|

0

|

0

|

7,500

|

||||||||||||||||||

|

Edgewood Vista – Billings, MT

|

4/10/2017

|

0

|

1,785

|

0

|

0

|

0

|

1,785

|

||||||||||||||||||

|

Edgewood Vista – East Grand Forks, MN

|

4/10/2017

|

0

|

2,718

|

0

|

0

|

0

|

2,718

|

||||||||||||||||||

|

Edgewood Vista – Sioux Falls, SD

|

4/10/2017

|

0

|

1,022

|

0

|

0

|

0

|

1,022

|

||||||||||||||||||

|

St Michael Clinic – St. Michael, MN

|

4/1/2018

|

0

|

0

|

1,795

|

0

|

0

|

1,795

|

||||||||||||||||||

|

Spring Creek - American Falls - American Falls, ID

|

9/1/2018

|

0

|

0

|

0

|

2,086

|

0

|

2,086

|

||||||||||||||||||

|

Spring Creek - Eagle - Eagle, ID

|

9/1/2018

|

0

|

0

|

0

|

1,919

|

0

|

1,919

|

||||||||||||||||||

|

Spring Creek - Meridian - Meridian, ID

|

9/1/2018

|

0

|

0

|

0

|

3,171

|

0

|

3,171

|

||||||||||||||||||

|

Spring Creek - Soda Springs - Soda Springs, ID

|

9/1/2018

|

0

|

0

|

0

|

751

|

0

|

751

|

||||||||||||||||||

12

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

LONG-TERM MORTGAGE DEBT* DETAIL AS OF APRIL 30, 2015 (continued)

(in thousands)

|

Property

|

Maturity Date

|

Fiscal 2016

|

Fiscal 2017

|

Fiscal 2018

|

Fiscal 2019

|

Thereafter

|

Total(1)

|

||||||||||||||||||

|

Healthcare - continued

|

|||||||||||||||||||||||||

|

Barry Pointe Office Park - Kansas City, MO

|

12/15/2018

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

1,369

|

$

|

0

|

$

|

1,369

|

||||||||||||

|

Health East St John & Woodwinds - Maplewood & Woodbury, MN

|

2/1/2019

|

0

|

0

|

0

|

7,366

|

0

|

7,366

|

||||||||||||||||||

|

Nebraska Orthopedic Hospital - Omaha, NE

|

4/1/2019

|

0

|

0

|

0

|

11,039

|

0

|

11,039

|

||||||||||||||||||

|

Summary of Debt due after Fiscal 2019

|

0

|

0

|

0

|

0

|

118,680

|

118,680

|

|||||||||||||||||||

|

Sub-Total Healthcare

|

$

|

66,513

|

$

|

17,789

|

$

|

1,795

|

$

|

27,701

|

$

|

118,680

|

$

|

232,478

|

|||||||||||||

|

Industrial

|

|||||||||||||||||||||||||

|

Stone Container - Fargo, ND

|

12/1/2015

|

172

|

0

|

0

|

0

|

0

|

172

|

||||||||||||||||||

|

Stone Container - Fargo, ND

|

12/1/2015

|

210

|

0

|

0

|

0

|

0

|

210

|

||||||||||||||||||

|

Urbandale 3900 106th Street – Urbandale, IA

|

7/5/2017

|

0

|

0

|

10,418

|

0

|

0

|

10,418

|

||||||||||||||||||

|

Summary of Debt due after Fiscal 2019

|

0

|

0

|

0

|

0

|

1,604

|

1,604

|

|||||||||||||||||||

|

Sub-Total Industrial

|

$

|

382

|

$

|

0

|

$

|

10,418

|

$

|

0

|

$

|

1,604

|

$

|

12,404

|

|||||||||||||

|

Retail

|

|||||||||||||||||||||||||

|

Chan West Village - Chanhassen, MN

|

0

|

0

|

0

|

12,307

|

0

|

12,307

|

|||||||||||||||||||

|

Jamestown Business Center – Jamestown, MN

|

0

|

0

|

0

|

327

|

0

|

327

|

|||||||||||||||||||

|

Summary of Debt due after Fiscal 2019

|

0

|

0

|

0

|

0

|

14,053

|

14,053

|

|||||||||||||||||||

|

Sub-Total Retail

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

12,634

|

$

|

14,053

|

$

|

26,687

|

|||||||||||||

|

Total

|

$

|

97,993

|

$

|

182,804

|

$

|

63,718

|

$

|

86,173

|

$

|

544,140

|

$

|

974,828

|

|||||||||||||

| * | Mortgage debt does not include the Company’s multi-bank line of credit or construction loans. The line of credit has a maturity date of September 1, 2017; as of April 30, 2015, the Company had borrowings of $60.5 million outstanding under this line. Construction loans and other debt totaled $144.1 million as of April 30, 2015. |

| (1) | Totals are principal balances as of April 30, 2015. |

| (2) | Loan was paid off subsequent to April 30, 2015. |

| (3) | Amount is part of a non-recourse $122.6 million CMBS loan, for which nine of the Company’s office properties serve as collateral and under which a special-purpose subsidiary of the Company is the borrower. This loan matures in October 2016. Because the loan amount significantly exceeds the Company’s current estimate of the fair value of this nine-property portfolio, the Company contacted the master servicer to initiate discussions on various alternatives with regard to the loan. During the first quarter of fiscal year 2015, the Company was notified that the loan has been transferred to the special servicer. On April 14, 2015 the Company received a letter from the special servicer advising that the loan was in default due to a nonpayment on April 6, 2015. The Company cannot predict the outcome of discussions with the special servicer regarding the loan. |

13

INVESTORS REAL ESTATE TRUST AND SUBSIDIARIES

(in thousands, except per share and unit amounts)

|

Three Months Ended

|

||||||||||||||||||||

|

4/30/2015

|

1/31/2015

|

10/31/2014

|

7/31/2014

|

4/30/2014

|

||||||||||||||||

|

Equity Capitalization

|

||||||||||||||||||||

|

Common shares outstanding

|

124,456

|

122,134

|

119,809

|

114,763

|

109,019

|

|||||||||||||||

|

Operating partnership (OP) units outstanding

|

14,000

|

14,398

|

14,731

|

17,975

|

21,094

|

|||||||||||||||

|

Total common shares and OP units outstanding

|

138,456

|

136,532

|

134,540

|

132,738

|

130,113

|

|||||||||||||||

|

Market price per common share (closing price at end of period)

|

$

|

7.17

|

$

|

8.25

|

$

|

8.40

|

$

|

8.52

|

$

|

8.72

|

||||||||||

|

Equity capitalization-common shares and OP units

|

$

|

1,142,262

|

$

|

1,126,389

|

$

|

1,130,136

|

$

|

1,130,928

|

$

|

1,134,585

|

||||||||||

|

Recorded book value of preferred shares

|

$

|

138,674

|

$

|

138,674

|

$

|

138,674

|

$

|

138,674

|

$

|

138,674

|

||||||||||

|

Total equity capitalization

|

$

|

1,280,936

|

$

|

1,265,063

|

$

|

1,268,810

|

$

|

1,269,602

|

$

|

1,273,259

|

||||||||||

|

Debt Capitalization

|

||||||||||||||||||||

|

Total debt

|

$

|

1,178,851

|

$

|

1,188,218

|

$

|

1,160,628

|

$

|

1,135,892

|

$

|

1,083,321

|

||||||||||

|

Total capitalization

|

$

|